sure passive income

TRANSCRIPT

Return to Top 10 List

Sure Passive Income

Rising Passive Income From Buy & Hold Forever Securities

December 2020 Edition

By Ben Reynolds, Bob Ciura, Josh Arnold, and Eli Inkrot

Edited by Brad Beams

Published on December 20th, 2020

2

Table of Contents

Opening Thoughts - Warren Buffett On Long-Term Investing - ............................................ 3

Sure Passive Income Top 10 - December 2020 ........................................................................... 4

Analysis of Top 10 Securities ....................................................................................................... 5

Archer-Daniels-Midland Co. (ADM) ......................................................................................... 5

General Dynamics Corp. (GD) ................................................................................................... 9

3M Co. (MMM) ........................................................................................................................ 13

Hormel Foods Corp. (HRL) ...................................................................................................... 17

Amgen Inc. (AMGN) ................................................................................................................ 21

The Home Depot Inc. (HD) ...................................................................................................... 25

The Travelers Companies Inc. (TRV) ...................................................................................... 29

Comcast Corp. (CMCSA) ......................................................................................................... 33

American Tower Corp. (AMT) ................................................................................................. 37

A. O. Smith Corp. (AOS) ......................................................................................................... 41

Closing Thoughts - Not All Sectors Are Equal - ...................................................................... 45

Buying & Ranking Criteria ....................................................................................................... 46

Portfolio Building Guide ............................................................................................................ 47

Examples ................................................................................................................................... 47

Past Recommendations & Performance ................................................................................... 48

List of Securities by Dividend Risk Score ................................................................................. 49

3

Opening Thoughts - Warren Buffett On Long-Term Investing -

Warren Buffett has put together one of the greatest long-term investment records in history. He is also an advocate of long-term investing. Several of Buffett’s quotes on long-term investing are analyzed below.

“I never attempt to make money on the stock market. I buy on the assumption that they could

close the market the next day and not reopen it for five years.”

&

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten

minutes.”

Long-term investing means investing in the business via the stock market, not investing in a stock and hoping the price goes up in the short run.

“Time is the friend of the wonderful company, the enemy of the mediocre.”

&

“When we own portions of outstanding businesses with outstanding managements, our favorite

holding period is forever.”

&

“Our approach is very much profiting from lack of change rather than from change. With

Wrigley chewing gum, it’s the lack of change that appeals to me.”

Not all companies are suitable for long-term buy and hold investing. Quality businesses that have

stood the test of time and are likely to continue growing far into the future are the type of

businesses worth holding for the long run. Being in a slow changing industry is helpful as well

because the competitive backdrop in which the business operates is more stable.

“You only have to do a very few things right in your life so long as you don’t do too many things

wrong.”

&

“It is not necessary to do extraordinary things to get extraordinary results.”

&

“There seems to be some perverse human characteristic that likes to make easy things difficult.”

People in general – and especially highly intelligent people – tend to overcomplicate things. Long-

term investing isn’t particularly complicated. This leads to a temptation to ‘not leave a good thing

alone’ and seek to buy and sell more frequently than is necessary or desirable.

Once you invest in a great business that’s likely to pay rising dividends over the long run, there’s

not much else to be done. Please keep reading The December 2020 edition of The Sure Passive

Income Newsletter to see our Top 10 recommendations now for rising passive income over the long

run.

4

Sure Passive Income Top 10 - December 2020

Name & Ticker Div. Risk

Score

Stock Price

# Years Div.

Increases

10- Yr. Avg. Div.

Yld.

Div. Yield

Exp. Growth

Exp. Growth + Div. Yield

Archer-Daniels-Mid. (ADM) A $49 45 2.6% 2.9% 6.0% 8.9%

General Dynamics (GD) A $152 28 2.3% 2.9% 6.0% 8.9%

3M (MMM) A $176 62 2.6% 3.3% 5.0% 8.3%

Hormel Foods (HRL) A $48 55 1.7% 2.0% 6.0% 8.0%

Amgen (AMGN) B $231 10 2.2% 3.1% 9.0% 12.1%

Home Depot (HD) B $273 11 2.1% 2.2% 9.0% 11.2%

Travelers (TRV) B $138 15 2.4% 2.4% 8.0% 10.4%

Comcast (CMCSA) B $51 12 1.7% 1.8% 7.0% 8.8%

American Tower (AMT) B $223 10 1.7% 2.1% 6.0% 8.1%

A. O. Smith (AOS) B $55 27 1.3% 1.9% 6.0% 7.9%

Notes: Data for the table above is from a spreadsheet during the past week of our Sure Analysis Research

Database and general data over the same week. ‘Div.’ stands for ‘Dividend.’ ‘# Years Div. Increases’

shows the consecutive years of dividend growth. ‘Exp. Growth’ means expected annualized growth rate

over the next five years. Data in the table above might be slightly different than individual company

analysis pages due to writing the company reports throughout the past week.

Disclosures: Ben Reynolds is long AMGN, & TRV from this month’s Top 10.

National Fuel Gas (NFG), Coca-Cola (KO), and J.M. Smucker (SJM) were replaced by Archer-

Daniels-Midland (ADM), 3M (MMM), and A. O. Smith (AOS). As a reminder, securities that fall out

of the Top 10 are holds, not sells.

An equally weighted portfolio of the Top 10 has the following dividend yield and expected gowth rate

characteristics:

Sure Passive Income Top 10 S&P 500

Dividend Yield: 2.4% 1.6%

Growth Rate: 6.8% 5.5%

Note: Data for this newsletter is from 12/15/20 through 12/18/20.

Return to Top 10 List

5

Analysis of Top 10 Securities Archer-Daniels-Midland Co. (ADM)

Overview & Current Events

Archer-Daniels-Midland, founded in 1902, is the largest publicly traded farmland product company in

the United States. ADM is a global leader in human and animal nutrition and the world’s premier

agricultural origination and processing company. Archer-Daniels-Midland's businesses include the

processing of cereal grains and oilseeds, and agricultural storage and transportation. Last year the $28

billion market cap company generated $65 billion in sales and $1.4 billion in net profit.

Archer-Daniels-Midland reported its Q3 earnings results on October 29th, 2020. The company

generated revenue of $15.1 billion, representing a 9.5% decline compared to Q3 2019. However,

adjusted earnings-per-share equaled $0.89 compared to $0.77 in the prior year quarter. For the first

nine months of 2020, Archer-Daniels-Midland has generated revenue of $46.4 billion, down 4.0%

compared to the first nine months of 2019. Meanwhile, earnings-per-share have grown from $1.83 for

the first nine months of 2019 to $2.38 per share in the first nine months of 2020.

During Q3 2020 the Nutrition segment delivered its fifth consecutive quarter of 20%+ year-over-year

profit growth. The Nutrition businesses include flavors, specialty ingredients, and health & wellness.

Meanwhile the Ag Services and Oilseeds segment saw 4.6% profit growth.

Safety

Archer-Daniels-Midland’s business is resilient since the demand for food products is not cyclical. The

company is one of the most significant players in its industry and has competitive advantages due to its

scale and geographical reach.

To this point, Archer-Daniels-Midland’s recession performance is noteworthy. During the last

downturn, the company posted earnings-per-share of $2.84, $3.06, $3.06 and $3.13 through the 2008 to

2011 stretch. Moreover, the dividend kept increasing during this time as well. Indeed, Archer-Daniels-

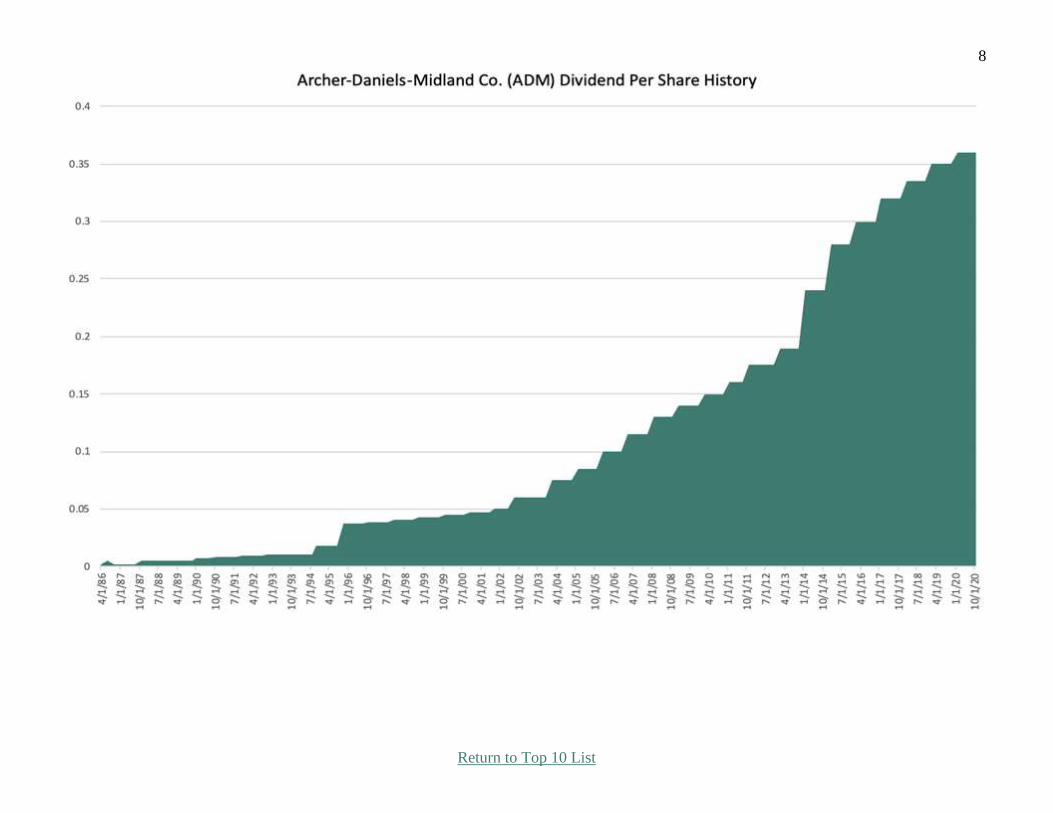

Midland’s dividend record is enviable. The company has paid a dividend for 356 consecutive quarters,

a record of 89 years of uninterrupted payments, to go along with increasing its payout for 45 straight

years. The current payout ratio is roughly 45%, with a 2.9% starting dividend yield.

Growth Prospects

On the one hand, Archer-Daniels-Midland is very resistant to recessions, as people have to eat even

during an economic downturn. On the other hand, a strong economy is not a significant tailwind for

the company as the amount of food sold does not rise quickly during good times.

In the 2010 through 2019 stretch, revenue increased by less than 1% per year, while earnings-per-share

have actually declined. Still, the company can find growth avenues such as the Ziegler Group

acquisition, the nutrition flavor research and customer center opening, and share repurchases. Archer-

Daniels-Midland has reduced its share count by 2.8% per year dating back to 2010. We are forecasting

6% yearly growth over the intermediate term. While this is not a robust forecast, we are impressed by

the company’s recession resilience, solid balance sheet, geographic diversification and dividend

history.

Key Statistics, Ratios, & Metrics Years of Dividend Increases: 45 5-Year Growth Estimate: 6.0%

Dividend Yield: 2.9% Most Recent Dividend Increase: 2.9%

Dividend Risk Score: A Stock Price: $49

Return to Top 10 List

6

Income Statement Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Revenue 61682 80676 89038 89804 81201 67702 62346 60828 64341 64656

Gross Profit 3843 4300 3668 3889 4768 3966 3618 3518 4181 4147

Gross Margin 6.2% 5.3% 4.1% 4.3% 5.9% 5.9% 5.8% 5.8% 6.5% 6.4%

SG&A Exp. 1398 1611 1626 1759 1933 1985 1981 1978 2165 2493

D&A Exp. 912 877 848 909 894 882 900 924 941 993

Operating Profit 2445 2689 2042 2130 2835 1981 1637 1540 2016 1654

Op. Margin 4.0% 3.3% 2.3% 2.4% 3.5% 2.9% 2.6% 2.5% 3.1% 2.6%

Net Profit 1930 2036 1223 1342 2248 1849 1279 1595 1810 1379

Net Margin 3.1% 2.5% 1.4% 1.5% 2.8% 2.7% 2.1% 2.6% 2.8% 2.1%

Free Cash Flow 1077 -3587 1418 4313 4049 580 -7390 -7015 -5626 -6280

Income Tax 666 997 523 670 877 438 534 7 245 209

Balance Sheet Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Total Assets 31808 42352 41771 43752 43997 40157 39769 39963 40833 43997

Cash & Equivalents 1046 615 1291 3121 1099 910 619 804 1997 852

Acc. Receivable N/A 4808 3439 4522 4236 2886 2426 2424 2683 3281

Inventories 7871 12055 12192 11441 9374 8243 8831 9173 8813 9170

Goodwill & Int. 523 602 603 561 3392 3688 3703 3918 4041 5476

Total Liabilities 17177 23514 23602 23558 24367 22242 22588 21641 21837 24772

Accounts Payable 5538 2581 2474 4513 4326 3474 3606 3894 3545 3746

Long-Term Debt 7548 10319 10320 6870 5660 5877 6931 7493 8388 8881

Total Equity 14609 18808 17969 20156 19575 17899 17173 18313 18981 19208

D/E Ratio 0.52 0.55 0.57 0.34 0.29 0.33 0.40 0.41 0.44 0.46

Profitability & Per Share Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Return on Assets 6.1% 5.5% N/A 3.0% 5.1% 4.4% 3.2% 4.0% 4.5% 3.3%

Return on Equity 13.7% 12.2% 6.7% 6.9% 11.3% 9.9% 7.3% 9.0% 9.7% 7.2%

ROIC 8.8% 7.9% N/A 4.8% 8.6% 7.5% 5.3% 6.4% 6.8% 5.0%

Shares Out. 644.0 654.0 666.0 663.0 656.0 621.0 591.0 572.0 567.0 565.0

Revenue/Share 95.78 123.36 133.69 135.45 123.78 109.02 105.49 106.34 113.48 113.48

FCF/Share 1.67 -5.48 2.13 6.51 6.17 0.93 -12.50 -12.26 -9.92 -11.12

Note: All figures in millions of U.S. Dollars unless per share or indicated otherwise.

Return to Top 10 List

7

Return to Top 10 List

8

Return to Top 10 List

9

General Dynamics Corp. (GD)

Overview & Current Events

General Dynamics is an aerospace & defense company that operates five business segments:

Aerospace (23% of sales), Combat Systems (17%), Marine Systems (23%), Information Technology

(23%), and Mission Systems (13%). The company makes the M1 Abrams tank, Stryker vehicle,

Virginia-class submarine, Columbia-class submarine, and Gulfstream business jets. General Dynamics

had revenue of nearly $40 billion last year.

The company reported third-quarter results on October 28th. Total revenue declined 3.4% year-over-

year, while diluted earnings-per-share declined 7.6%. Declines resulted from weakness in Aerospace,

Information Technology, and Mission Systems. Net debt is declining and is now 3.2% lower than last

quarter at $11.9 billion. The total backlog now stands at $81.5 billion, up 21% from the same quarter

last year. Revenue increased 3.5% for Combat Systems and 7.6% for Marine Systems. Information

Technology revenue declined 2% while Mission Systems was flat for the quarter.

Safety

General Dynamics is an entrenched military contractor. It has ground and marine platforms that serve

as the backbone for the U.S. Army, U.S. Navy, and militaries around the world. This leads to a

competitive advantage as these platforms have decades-long life cycles.

These characteristics lead to a reasonable degree of recession resistance. For example, from 2008-2010

during the Great Recession, General Dynamics increased its earnings-per-share by 11%. General

Dynamics also has a secure payout ratio at just 40% of expected fiscal 2020 adjusted earnings-per-

share.

Growth Prospects

We expect 6% annual earnings-per-share growth over the next five years. This earnings-per-share

growth will be achieved through a combination of rising revenue as well as share repurchases. General

Dynamics’ growth is due to increasing U.S. defense spending and international sales. The business jet

market is being negatively impacted due to COVID-19 and travel restrictions, but defense remains a

much bigger portion of General Dynamics’ revenue and earnings. General Dynamics has established

naval and ground platforms that support maintenance and modernization contracts, as well as future

prime contract wins.

General Dynamics has increased its dividend for 28 consecutive years, which makes it a Dividend

Aristocrat. Continued dividend growth is very likely due to the company’s durable competitive

advantages and market leadership. We expect 8% compound annual dividend growth over the next

five years.

Key Statistics, Ratios, & Metrics Years of Dividend Increases: 28 5-Year Growth Estimate: 6.0%

Dividend Yield: 2.9% Most Recent Dividend Increase: 7.8%

Dividend Risk Score: A Stock Price: $152

Return to Top 10 List

10

Income Statement Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Revenue 32466 32677 30992 30930 30852 31781 30561 30973 36193 39350 Gross Profit 5909 5856 4980 5728 5873 6232 5665 6242 6715 7059

Gross Margin 18.2% 17.9% 16.1% 18.5% 19.0% 19.6% 18.5% 20.2% 18.6% 17.9% SG&A Exp. 1964 2030 2221 2039 1984 1937 1921 2006 2258 2411 D&A Exp. 569 592 590 525 496 481 453 441 763 829

Operating Profit 3945 3826 2759 3689 3889 4295 3744 4236 4457 4648 Op. Margin 12.2% 11.7% 8.9% 11.9% 12.6% 13.5% 12.3% 13.7% 12.3% 11.8% Net Profit 2624 2526 -332 2357 2533 3036 2572 2912 3345 3484

Net Margin 8.1% 7.7% -1.1% 7.6% 8.2% 9.6% 8.4% 9.4% 9.2% 8.9% Free Cash Flow 2616 2780 2170 2675 3307 2038 1771 3448 2458 1994

Income Tax 1162 1166 854 1125 1129 1183 977 1165 727 718

Balance Sheet Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Total Assets 32545 34883 34309 35494 35337 31997 33172 35046 45408 48841 Cash & Equivalents 2613 2649 3296 5301 4388 2785 2334 2983 963 902

Acc. Receivable 3848 4429 4204 4370 4050 3446 3399 3617 3759 3544 Inventories 2158 7478 7740 7670 7812 7723 5118 5303 5977 6306

Goodwill & Int. 14641 15389 13431 12976 12643 12206 12123 12616 22179 21992 Total Liabilities 19229 21651 22919 20993 23508 21259 22871 23611 33676 35264

Accounts Payable 2736 2895 2469 2216 2057 1964 2538 3207 3179 3162 Long-Term Debt 3203 3907 3908 3909 3893 3399 3888 3982 12417 11930

Total Equity 13316 13232 11390 14501 11829 10738 10301 11435 11732 13577 D/E Ratio 0.24 0.30 0.34 0.27 0.33 0.32 0.38 0.35 1.06 0.88

Profitability & Per Share Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Return on Assets 8.2% 7.5% -1.0% 6.8% 7.2% 9.0% 7.9% 8.5% 8.3% 7.4% Return on Equity 20.4% 19.0% -2.7% 18.2% 19.2% 26.9% 24.4% 26.8% 28.9% 27.5%

ROIC 16.0% 15.0% -2.0% 14.0% 14.8% 20.3% 18.2% 19.7% 16.9% 14.0% Shares Out. 372 356 354 353 332 311 302 297 289 290

Revenue/Share 84.28 88.91 87.71 87.50 90.39 97.29 98.46 101.67 120.98 135.3 FCF/Share 6.79 7.56 6.14 7.57 9.69 6.24 5.71 11.32 8.22 6.86

Note: All figures in millions of U.S. Dollars unless per share or indicated otherwise.

Return to Top 10 List

11

Return to Top 10 List

12

Note: General Dynamics has paid large special dividends in the past, two of which are truncated in this image for better readability of the

normal quartlerly dividend.

13

Return to Top 10 List

3M Co. (MMM)

Overview & Current Events

The 3M Company is an industrial conglomerate that sells more than 60,000 products that are used in a

variety of settings, including offices, schools, residences, and hospitals. The company produces

products that are consumable, and are therefore purchased on a recurring basis, creating relatively

stable revenue over time. 3M has nearly 100,000 employees globally and produces about $32 billion in

annual revenue. The company is organized into four operating segments: Safety & Industrial,

Healthcare, Transportation & Electrics, and Consumer. 3M’s market capitalization is $101 billion.

3M reported third quarter earnings on October 27th, with results coming in better than expectations.

Revenue was up 5.1% year-over-year to $8.4 billion, although local-currency organic growth was just

0.9%, with the balance made up from acquisitions. North America saw organic sales climb by 3.4%,

although this strength was offset by weakness in other geographic areas. Safety & Industrial sales grew

nearly 7% in Q3, Transportation & Electric revenue was down by 7%, Healthcare rose 8%, and

Consumer sales rose more than 5%.

Adjusted free cash flow, which is critical for 3M considering how much capital it returns to

shareholders via share repurchases and dividends, rose 13% year-over-year to $2.2 billion. For the first

three quarters of the year, adjusted free cash flow was up 19% to $4.6 billion. 3M used some of that to

retire $1.3 billion in debt in the third quarter, in addition to paying its dividend. Adjusted earnings-per-

share fell 6% year-over-year to $2.43 in Q3. We now expect full-year adjusted earnings-per-share of

$8.35, which would be 3M’s weakest performance since 2016.

Safety

3M’s greatest competitive advantage is in its constant pursuit of innovation. 3M’s catalog is full of

products it developed in-house over the years, and it has been willing and able to acquire businesses

that fit its long-term plans for stability and growth. Decades of executing this strategy have left 3M in

a strong competitive position, offering tens of thousands of products people all over the world use

every day. The company also boasts a portfolio of more than 100,000 unique patents, and that list is

growing constantly.

3M isn’t necessarily safe from recessions given its wide and deep product portfolio, but it did cope

with the Great Recession well, seeing a swift rebound in earnings once it ended. The COVID recession

has harmed earnings, but we see 3M as rebounding rather quickly from 2021 forward.

3M has a 62-year streak of dividend increases, putting it in extremely rare company with the rest of the

Dividend Kings. Given that the projected payout ratio for this year is 70% during a year when earnings

are being depressed by a negative shock from COVID, we see 3M’s dividend safety as outstanding.

We do not see a scenario where 3M would be forced to cut its dividend.

Growth Prospects

3M has a decades-long history of producing higher dividends for shareholders. It is able to do this

through a deep and wide product catalog that offers diversification for a variety of customers.

Although growth can be choppy, we see the payout rising for many years to come.

Key Statistics, Ratios, & Metrics Years of Dividend Increases: 62 5-Year Growth Estimate: 5.0%

Dividend Yield: 3.3% Most Recent Dividend Increase: 2.0%

Dividend Risk Score: A Stock Price: $176

Return to Top 10 List

14

Income Statement Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Revenue 26662 29611 29904 30871 31821 30274 30109 31657 32765 32136

Gross Profit 12831 13918 14219 14765 15374 14891 14991 15602 16083 15000

Gross Margin 48.1% 47.0% 47.5% 47.8% 48.3% 49.2% 49.8% 49.3% 49.1% 46.7%

SG&A Exp. 5479 6170 6102 6384 6469 6229 6311 6626 7602 7029

Operating Profit 1120 1236 1288 1371 1408 1435 1474 1544 1488 1593

Op. Margin 22.2% 20.9% 21.7% 21.6% 22.4% 22.8% 23.0% 22.4% 20.3% 18.9%

Net Profit 4085 4283 4444 4659 4956 4833 5050 4858 5349 4570

Net Margin 15.3% 14.5% 14.9% 15.1% 15.6% 16.0% 16.8% 15.3% 16.3% 14.2%

Free Cash Flow 4083 3905 3816 4152 5133 4959 5242 4867 4862 5371

Income Tax 1592 1674 1840 1841 2028 1982 1995 2679 1637 1130

Balance Sheet Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Total Assets 30156 31616 33876 33550 31209 32883 32906 37987 36500 44659

Cash & Equivalents 3377 2219 2883 2581 1897 1798 2398 3053 2853 2353

Acc. Receivable 3615 3867 4061 4253 4238 4154 4392 4911 5020 4791

Inventories 3155 3416 3837 3864 3706 3518 3385 4034 4366 4134

Goodwill & Int. 8640 8963 9310 9033 8485 11850 11486 13449 12708 19823

Total Liabilities 14139 15754 15836 15602 18067 21415 22563 26365 26652 34533

Accounts Payable 1662 2159 2278 2346 2340 2260 1798 1945 2266 2228

Long-Term Debt 5452 5166 6001 6009 6811 10797 11650 13949 14622 20313

Total Equity 15663 15420 17575 17502 13109 11429 10298 11563 9796 10063

D/E Ratio 0.35 0.34 0.34 0.34 0.52 0.94 1.13 1.21 1.49 2.02

Profitability & Per Share Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Return on Assets 14.2% 13.9% 13.6% 13.8% 15.3% 15.1% 15.4% 13.7% 14.4% 11.3%

Return on Equity 28.7% 27.6% 26.9% 26.6% 32.4% 39.4% 46.5% 44.4% 50.1% 46.0%

ROIC 20.2% 20.2% 19.7% 19.4% 22.6% 22.9% 22.8% 20.4% 21.4% 16.6%

Shares Out. 712 695 687 663 635 609 597 595 585 582

Revenue/Share 36.75 41.18 42.52 44.51 48.07 47.51 48.66 51.67 54.43 54.92

FCF/Share 5.63 5.43 5.43 5.99 7.75 7.78 8.47 7.94 8.08 9.18

Note: All figures in millions of U.S. Dollars unless per share or indicated otherwise.

15

Return to Top 10 List

Return to Top 10 List

16

17

Return to Top 10 List

Hormel Foods Corp. (HRL)

Overview & Current Events

Hormel Foods was founded all the way back in 1891. Since that time, it has grown into a juggernaut in

the food products industry, with ~$10 billion in annual revenue. It has broadened its product line over

the years with multiple acquisitions. Today, Hormel sells its products in 80 countries. Some of its core

brands include Skippy, SPAM, Applegate, Justin’s, Jennie-O, and more than 30 others.

Hormel reported fourth-quarter and full-year earnings on November 24th, 2020 with results coming in

weaker than expected on both the top and bottom lines. For the fourth fiscal quarter, total revenue

declined 3% to $2.4 billion. Organic volume fell 3% and organic sales dropped 4%, with the additional

decline from weak pricing and an unfavorable mix. By operating segment, Grocery Products revenue

fell 1%, Refrigerated Foods fell 5%, and Jennie-O Turkey Store declined 6%. Helping to offset these

declines was the International & Other segment, which grew sales by 8% for the quarter. Retail sales

in the U.S. increased 7% as more consumers stayed at home, but foodservice revenue declined 23% for

the quarter due to widespread restaurant closures amid the coronavirus pandemic.

Safety

Hormel’s main competitive advantage is its strong brands. It has approximately 40 products that are

either #1 or #2 in their category. Hormel has brands that are proven, and that leadership position is

difficult for competitors to supplant. In addition, Hormel has a global network of distributors that few

food companies can rival.

Hormel’s earnings-per-share actually grew during the Great Recession while most of the world was in

rather dire straits, a testament to the stock’s defensive nature. With an expected dividend payout ratio

of approximately 55% for fiscal 2021, we view the dividend as highly secure.

Growth Prospects

Hormel has an impressive history of generating long-term growth. The company’s recession-resilience

and growth has allowed it to increase its dividend for 55 consecutive years. Hormel is on the exclusive

list of Dividend Kings. It has also paid 369 consecutive quarterly dividends.

We expect 6% annual earnings-per-share growth for Hormel over the next five years. Organic growth

through price increases, as well as external growth through acquisitions, are the main drivers of future

sales growth. Share buybacks will incrementally boost earnings-per-share growth as well.

We expect Hormel to increase its dividend by 5% per year over the next five years. This would be in-

line with the company’s recent dividend increases, including its most recent 5.4% raise on November

23rd.

Key Statistics, Ratios, & Metrics Years of Dividend Increases: 55 5-Year Growth Estimate: 6.0%

Dividend Yield: 2.0% Most Recent Dividend Increase: 5.4%

Dividend Risk Score: A Stock Price: $48

18

Return to Top 10 List

Income Statement Metrics Year 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Revenue 7895 8231 8752 9316 9264 9523 9168 9546 9497 9,608

Gross Profit 1334 1332 1413 1565 1809 2158 1997 1979 1885 1,826

Gross Margin 16.9% 16.2% 16.1% 16.8% 19.5% 22.7% 21.8% 20.7% 19.8% 19.0%

SG&A Exp. 619 606 627 651 744 872 759 841 728 761

D&A Exp. 124 119 125 130 133 132 131 162 165 206

Operating Profit 716 726 785 914 1065 1286 1237 1138 1157 1,065

Operating Margin 9.1% 8.8% 9.0% 9.8% 11.5% 13.5% 13.5% 11.9% 12.2% 11.1%

Net Profit 474 500 526 603 686 890 847 1012 979 908

Net Margin 6.0% 6.1% 6.0% 6.5% 7.4% 9.3% 9.2% 10.6% 10.3% 9.5%

Free Cash Flow 394 385 531 588 848 784 813 852 629 761

Income Tax 240 253 268 316 370 427 432 169 231 206

Balance Sheet Metrics Year 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Total Assets 4244 4564 4916 5456 6140 6370 6976 8142 8109 9,908

Cash & Equivalents 463 682 434 334 347 415 444 459 673 1,714

Accounts Receivable 461 507 552 610 606 591 618 600 574 702

Inventories 886 951 968 1055 993 986 921 964 1042 1,073

Goodwill & Int. Ass. 763 754 1313 1781 2527 2738 3147 3921 3516 3,689

Total Liabilities 1585 1739 1599 1844 2138 1919 2036 2537 2183 3,478

Accounts Payable 390 386 387 484 495 482 553 619 590 645

Long-Term Debt 250 250 250 250 435 250 250 625 250 1,304

Shareholder’s Equity 2657 2819 3311 3606 3998 4448 4936 5601 5921 6,426

D/E Ratio 0.09 0.09 0.08 0.07 0.11 0.06 0.05 0.11 0.04 0.20

Profitability & Per Share Metrics Year 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Return on Assets 11.4% 11.4% 11.1% 11.6% 11.8% 14.2% 12.7% 13.4% 12.0% 10.1%

Return on Equity 18.8% 18.3% 17.2% 17.4% 18.0% 21.1% 18.0% 19.2% 17.0% 14.7%

ROIC 16.7% 16.7% 15.8% 16.2% 16.5% 19.5% 17.1% 17.7% 15.8% 13.1%

Shares Out. 532 528 526 527 527 528 528 529 544 548

Revenue/Share 14.52 15.30 16.19 17.24 17.12 17.56 17.00 17.55 17.42 17.58

FCF/Share 0.72 0.72 0.98 1.09 1.57 1.45 1.51 1.57 1.15 1.39

Note: All figures in millions of U.S. Dollars unless per share or indicated otherwise.

19

Return to Top 10 List

20

Return to Top 10 List

21

Return to Top 10 List

Amgen Inc. (AMGN)

Overview & Current Events

Amgen is the largest independent biotech company in the world. Amgen discovers, develops,

manufactures, and sells medicines that treat serious illnesses. The company focuses on six therapeutic

areas: cardiovascular disease, oncology, bone health, neuroscience, nephrology, and inflammation.

Amgen announced earnings results for the third quarter on 10/28/20. Revenue increased 12% to $6.4

billion, while adjusted earnings-per-share (EPS) increased 19.4% to $4.37. Revenue and EPS both beat

consensus estimates. The company had volume growth of 18%, which was partially offset by lower

net selling prices. Sales for Enbrel, which treats rheumatoid arthritis and remains Amgen’s top

grossing product, were down 3%. Enbrel lost market share in the quarter and was also impacted by

lower growth in the rheumatology sector as a whole due to COVID-19. Offsetting this decline was the

bone health drug, Prolia, which grew sales by 11%, due mostly to volume gains.

The company also revised its guidance for the year, narrowing its revenue forecast but raising its

earnings forecast. Amgen expects revenue of $25.1 billion to $25.5 billion, from $25 billion to $25.6

billion previously. Adjusted EPS is now expected in a range of $15.80 to $16.15 for 2020, up from

$15.10 to $15.75 previously.

Safety

Amgen’s competitive advantages include its strong pharmaceutical assets as well as its robust pipeline.

Amgen spent 18.1% of its 2019 sales on research and development. As a result, it has a well-stocked

pipeline to fuel its future growth.

The company has also demonstrated resilience during recessions, as people will seek treatment for their

health issues regardless of economic conditions. The company has a reasonably low payout ratio of

40% expected for 2020, which will allow it to continue to raise its dividend going forward, even in a

prolonged recession.

Growth Prospects

We expect 9% annual earnings-per-share growth over the next five years for Amgen. This earnings-

per-share growth will be achieved through a combination of rising revenue as well as share

repurchases.

While Amgen is struggling with falling sales for legacy products such as Neulasta and Enbrel, new

products are generating growth for Amgen. For example, Repatha, which is used to control

cholesterol, grew sales by 22% in large part from a 60% increase in volume. Separately, Otezla, which

is used to treat inflammatory diseases, generated 11% year-over-year sales growth. Lastly, share

buybacks will boost earnings-per-share growth. Amgen repurchased 3 million shares at an average

share price of $251 during the third quarter (~0.5% of shares outstanding), and it still has $4.2 billion

remaining on its share repurchase authorization.

Key Statistics, Ratios, & Metrics Years of Dividend Increases: 10 5-Year Growth Estimate: 9.0%

Dividend Yield: 3.1% Most Recent Dividend Increase: 10.0%

Dividend Risk Score: B Stock Price: $231

22

Return to Top 10 List

Income Statement Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Revenue 15,053 15,582 17,265 18,676 20,063 21,662 22,991 22,849 23,747 23,362

Gross Profit 12,833 12,874 14,066 15,330 15,641 17,435 18,829 18,780 19,646 19,006

Gross Margin 85.3% 82.6% 81.5% 82.1% 78.0% 80.5% 81.9% 82.2% 82.7% 81.4%

SG&A Exp. 3,983 4,499 4,814 5,184 4,699 4,846 5,062 4,870 5,332 5,150

D&A Exp. 1,017 1,060 1,088 1,286 2,092 2,108 2,105 1,955 1,946 2,206

Operating Profit 5,545 4,312 5,577 5,867 6,191 8,470 9,794 9,973 10,263 9,674

Op. Margin 36.8% 27.7% 32.3% 31.4% 30.9% 39.1% 42.6% 43.6% 43.2% 41.4%

Net Profit 4,627 3,683 4,345 5,081 5,158 6,939 7,722 1,979 8,394 7,842

Net Margin 30.7% 23.6% 25.2% 27.2% 25.7% 32.0% 33.6% 8.7% 35.3% 33.6%

Free Cash Flow 5,207 4,552 5,168 5,598 7,949 9,137 9,616 10,513 10,558 9,150

Income Tax 690 467 664 184 427 1,039 1,441 7,618 1,151 1,296

Balance Sheet Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Total Assets 43,486 48,871 54,298 66,125 69,009 71,449 77,626 79,954 66,416 59,707

Cash & Equivalents 3,287 6,946 3,257 3,805 3,731 4,144 3,241 3,800 6,945 6,037

Acc. Receivable 2,335 2,896 2,518 2,697 2,546 2,995 3,165 3,237 3,580 4,057

Inventories 2,022 2,484 2,744 3,019 2,647 2,435 2,745 2,834 2,940 3,584

Goodwill & Int. 13,564 14,334 16,630 28,230 27,481 26,428 25,030 23,370 22,142 34,116

Total Liabilities 19,542 29,842 35,238 44,029 43,231 43,366 47,751 54,713 53,916 50,034

Accounts Payable 716 642 905 787 995 965 917 1,352 1,207 1,371

Long-Term Debt 13,362 21,428 26,529 32,128 30,715 31,429 34,596 35,342 33,929 29,903

Total Equity 23,944 19,029 19,060 22,096 25,778 28,083 29,875 25,241 12,500 9,673

D/E Ratio 0.56 1.13 1.39 1.45 1.19 1.12 1.16 1.40 2.71 3.09

Profitability & Per Share Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Return on Assets 11.1% 8.0% 8.4% 8.4% 7.6% 9.9% 10.4% 2.5% 11.5% 12.4%

Return on Equity 19.9% 17.1% 22.8% 24.7% 21.5% 25.8% 26.6% 7.2% 44.5% 70.7%

ROIC 13.1% 9.5% 10.1% 10.2% 9.3% 12.0% 12.5% 3.2% 15.7% 18.2%

Shares Out. 932 796 756 755 760 754 738 720 640 598

Revenue/Share 15.60 17.09 21.94 24.41 26.06 28.28 30.49 31.09 35.71 38.36

FCF/Share 5.40 4.99 6.57 7.32 10.32 11.93 12.75 14.30 15.88 15.02

Note: All figures in millions of U.S. Dollars unless per share or indicated otherwise.

23

Return to Top 10 List

24

Return to Top 10 List

Return to Top 10 List

25

The Home Depot Inc. (HD)

Overview & Current Events

Home Depot was founded in 1978, and since that time has grown into the leading home improvement

retailer with almost 2,300 stores in the U.S., Canada, and Mexico. In all, Home Depot generates

annual revenue of approximately $110 billion.

Home Depot reported excellent third-quarter financial results on November 17th. Revenue of $33.5

billion increased 23% year-over-year. Sales per retail square foot increased by 23% to $553, from

$449 in the same quarter last year. Comparable sales increased 24%, including 25% growth in the U.S.

Net earnings of $3.4 billion for the quarter were up 24%, and on a per-share basis earnings rose 26% to

$3.18 per share. In addition to revenue growth, share repurchases boosted earnings-per-share (EPS)

growth as the company reduced its diluted share count by 2.0% year-over-year. Liquidity remains very

healthy as the company ended the third quarter with cash and cash equivalents equal to $15 billion.

Safety

Home Depot’s most compelling competitive advantage is its leadership position in the home

improvement industry. Not only is demand for home improvement products growing at a high rate in

the U.S., but the industry is highly concentrated with just two major operators (Home Depot and

Lowe’s) taking the bulk of market share.

Home Depot has also proven to be resilient to recessions, including the coronavirus pandemic, which

has arguably helped Home Depot as consumers spend much more time at home. Home Depot has a

projected 2020 dividend payout ratio just above 53%, which indicates a safe dividend.

Growth Prospects

Home Depot’s earnings growth has been strong in the past decade as it has successfully capitalized on

the housing and construction boom that ensued following the Great Recession of 2008-2010. E-

commerce is another growth catalyst for Home Depot, as the company has invested heavily to expand

its digital footprint. Home Depot stated that sales leveraging its digital platforms increased

approximately 80% last quarter. We see five-year annual earnings growth of 9.0%, consisting of

comparable sales in the mid-single-digits, a low single-digit tailwind from buybacks, and a steady,

boost from operating margin expansion.

Home Depot has paid 135 consecutive quarterly dividends. The company’s streak of meaningful

dividend growth should continue, as we see the payout rising at the rate of EPS growth in the next five

years. The company has room to continue raising the dividend in the years to come. Further, as Home

Depot matures it may allow for a higher payout ratio for the dividend, which would further boost its

dividend growth prospects.

Key Statistics, Ratios, & Metrics Years of Dividend Increases: 11 5-Year Growth Estimate: 9.0%

Dividend Yield: 2.2% Most Recent Dividend Increase: 10.3%

Dividend Risk Score: B Stock Price: $273

26

Return to Top 10 List

Income Statement Metrics Year 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Revenue ($B) 68.00 70.40 74.75 78.81 83.18 88.52 94.60 100.90 108.20 110.2

Gross Profit 23304 24262 25842 26915 28389 30265 32313 34356 37160 37572

Gross Margin 34.3% 34.5% 34.6% 34.2% 34.1% 34.2% 34.2% 34.0% 34.3% 34.1%

SG&A Exp. 15849 16028 16508 16122 16280 16801 17132 17864 19513 19740

D&A Exp. 1718 1682 1684 1757 1786 1863 1973 2062 2152 2296

Operating Profit 5839 6661 7766 9166 10469 11774 13427 14681 15777 15843

Op. Margin 8.6% 9.5% 10.4% 11.6% 12.6% 13.3% 14.2% 14.5% 14.6% 14.4%

Net Profit 3338 3883 4535 5385 6345 7009 7957 8630 11121 11242

Net Margin 4.9% 5.5% 6.1% 6.8% 7.6% 7.9% 8.4% 8.6% 10.3% 10.2%

Free Cash Flow 3489 5430 5663 6239 6800 7870 8162 10134 10596 11045

Income Tax 1935 2185 2686 3082 3631 4012 4534 5068 3435 3473

Balance Sheet Metrics Year 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Total Assets 40125 40518 41084 40518 39946 41973 42966 44529 44003 51236

Cash & Equivalents 545 1987 2494 1929 1723 2216 2538 3595 1778 2133

Acc. Receivable 1245 1395 1398 1484 1890 1570 1604 1936 1738

Inventories 10625 10325 10710 11057 11079 11809 12549 12748 13925 14531

Goodwill & Int. 1187 1120 1170 1289 1353 2102 2093 2275 2252 2254

Total Liabilities 21236 22620 23307 27996 30624 35657 38633 43075 45881 54352

Accounts Payable 4717 4856 5376 5797 5807 6565 7000 7244 7755 7787

Long-Term Debt 9749 10788 10796 14724 17197 21216 23601 27028 29202 31483

Total Equity 18889 17898 17777 12522 9322 6316 4333 1454 N/A -3116

D/E Ratio 0.52 0.60 0.61 1.18 1.84 3.36 5.45 18.59 N/A -10.10

Profitability & Per Share Metrics Year 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Return on Assets 8.2% 9.6% 11.1% 13.2% 15.8% 17.1% 18.7% 19.7% 25.1% N/A

Return on Equity 17.4% 21.1% 25.4% 35.5% 58.1% 89.6% 149% 298% N/A 23.6%

ROIC 11.6% 13.5% 15.8% 19.3% 23.6% 25.9% 28.7% 30.6% N/A N/A

Shares Out. 1,623 1,537 1,484 1,380 1,307 1,252 1,203 1,158 1,121 1,088

Revenue/Share 41.01 44.84 49.47 54.96 61.79 68.99 76.66 85.22 94.67 100.5

FCF/Share 2.10 3.46 3.75 4.35 5.05 6.13 6.61 8.56 9.27 10.07

Note: All figures in millions of U.S. Dollars unless per share or indicated otherwise.

27

Return to Top 10 List

28

Return to Top 10 List

29

Return to Top 10 List

The Travelers Companies Inc. (TRV)

Overview & Current Events

The Travelers Companies was founded in 1864 in Connecticut by two businessmen. It began with life

insurance and accident insurance and has expanded into all different kinds of property and casualty

insurance, becoming a leader in the space. Travelers offers protection products for consumers, auto

insurance, home insurance, and various types of commercial products. Today, the company produces

around $29 billion in annual revenue and the stock trades with a market capitalization of $35 billion.

Travelers released its third-quarter earnings report on October 20th, and results were slightly better than

expected on the top and bottom lines. Core earnings-per-share came to $3.12 in Q3, five cents above

expectations. Travelers saw a favorable development on its prior year reserves, higher underlying

underwriting gains, and higher net investment income. The company once again suffered from

relatively high catastrophe losses, but it wasn’t enough to offset the good news elsewhere. Travelers

saw relative strength in auto insurance as miles driven continues to be quite low due to COVID-19

restrictions, and renewal rates were up more than 8% year-over-year as strong pricing continues.

Net written premiums were up from $7.57 billion to $7.77 billion year-over-year, while the combined

ratio fell from 94.1% to 91.5%; combined ratios are expenses including claims divided by premium

revenue, so the lower, the better. This helped core return on equity more than double year-over-year,

ending the third quarter at 13.5%.

Adjusted book value was $94.89 per share at the end of the period versus $90.09 in the same quarter

last year. We estimate $8.70 in earnings-per-share for 2020 following Q3 results.

Safety

Travelers’ primary competitive advantages are its scale and its brand, both of which have been built

steadily in the past century and a half. Travelers has a globally recognizable brand that stands for

stability, and its scale affords it the ability to diversify in different types of products, not only

diversifying risk away via differing revenue streams, but also allowing for cross-selling to customers,

maximizing customer value.

Travelers isn’t necessarily susceptible to economic slowdowns, as its policies are tied to specific

events, like catastrophes, rather than economic weakness. This gives Travelers a diversifying attribute

for an investor’s portfolio.

Travelers’ dividend ranks highly for safety as the payout ratio is just 39% on this year’s earnings. We

see Travelers as having the capacity to raise the payout for years to come.

Growth Prospects

We expect Travelers to grow at 8% annually in the coming years, primarily from higher underwritten

premium growth, better margins, and its well-funded buyback program. We note that unforeseen

catastrophe losses could temporarily derail our bullish expectations.

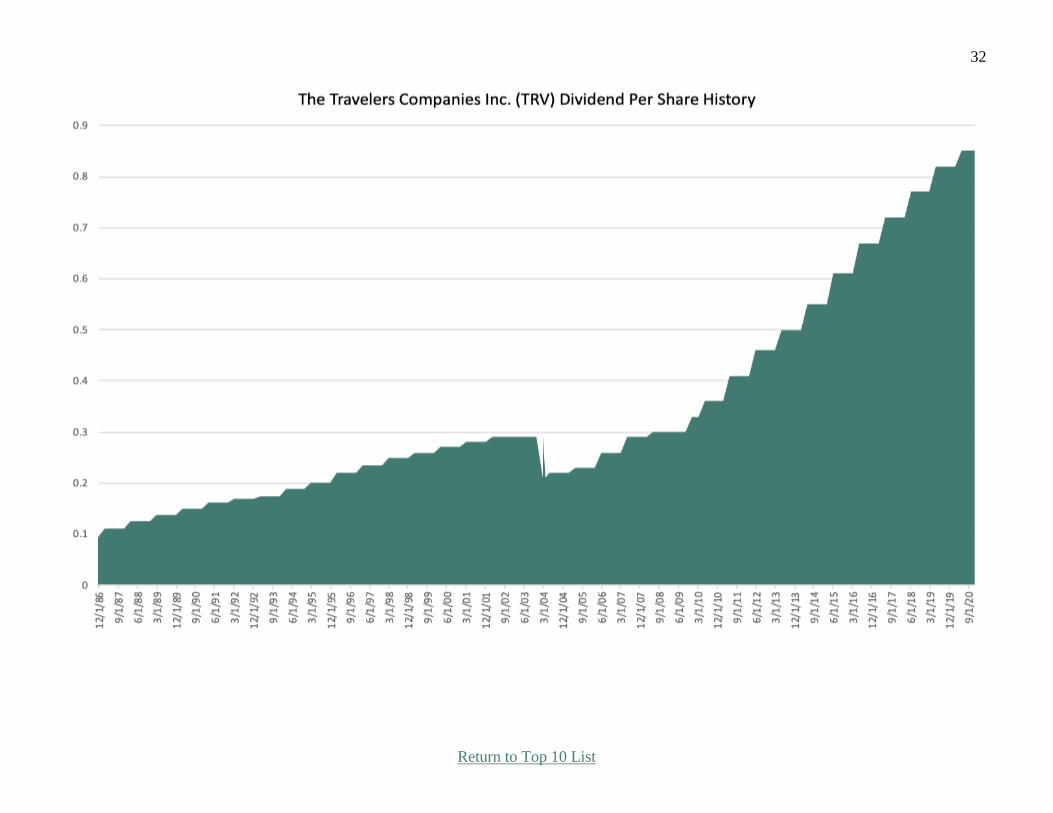

Key Statistics, Ratios, & Metrics Years of Dividend Increases: 15 5-Year Growth Estimate: 8.0%

Dividend Yield: 2.4% Most Recent Dividend Increase: 3.7%

Dividend Risk Score: B Stock Price: $138

30

Return to Top 10 List

Income Statement Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Revenue 25112 25446 25740 26191 27174 26815 27625 28902 30282 31581

SG&A Exp. 3406 3556 3610 3757 3964 4094 4154 4170 4297 4365

D&A Exp. 812 802 827 867 864 818 826 813 803 763

Net Profit 3216 1426 2473 3673 3692 3439 3014 2056 2523 2622

Net Margin 12.8% 5.6% 9.6% 14.0% 13.6% 12.8% 10.9% 7.1% 8.3% 8.3%

Free Cash Flow 3054 2169 3230 3816 3693 3434 4469 4148 4380 5205

Income Tax 1090 -74 693 1272 1397 1301 1039 674 438 516

Balance Sheet Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Total Assets ($B) 105.66 104.58 104.94 103.81 103.08 100.18 100.25 103.48 104.23 110.1

Cash & Equivalents 200 214 330 294 374 380 307 344 373 494

Acc. Receivable 5497 22071 21390 20166 19920 19721 19618 20228 20661 20763

Goodwill & Int. 3867 3798 3746 3985 3915 3852 3848 4293 4282 4291

Total Liabilities 80181 80098 79533 79016 78242 76586 77024 79752 81339 84179

Accounts Payable 407 5575 5152 4626 4698 4670 4882 5049 5074 4982

Long-Term Debt 6611 6605 6350 6346 6349 6344 6437 6571 6564 6558

Total Equity 25407 24477 25405 24796 24836 23598 23221 23731 22894 25943

D/E Ratio 0.26 0.27 0.25 0.26 0.26 0.27 0.28 0.28 0.29 0.25

Profitability & Per Share Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Return on Assets 3.0% 1.4% 2.4% 3.5% 3.6% 3.4% 3.0% 2.0% 2.4% 2.4%

Return on Equity 12.2% 5.7% 9.9% 14.6% 14.9% 14.2% 12.9% 8.8% 10.8% 10.7%

ROIC 9.7% 4.5% 7.9% 11.7% 11.8% 11.3% 10.1% 6.9% 8.4% 8.5%

Shares Out. 435 393 377 354 322 296 280 271 264 259

Revenue/Share 52.05 60.51 66.03 69.97 79.34 85.43 94.93 103.74 112.24 120.40

FCF/Share 6.33 5.16 8.29 10.20 10.78 10.94 15.36 14.89 16.23 19.84

Note: All figures in millions of U.S. Dollars unless per share or indicated otherwise.

31

Return to Top 10 List

32

Return to Top 10 List

33

Return to Top 10 List

Comcast Corp. (CMCSA)

Overview & Current Events

Comcast Corporation is a media, communications, and entertainment conglomerate. Its operating

segments include Cable Communications, NBCUniversal, Theme Parks, Broadcast TV, and Sky.

Collectively, through these segments, Comcast offers high-speed Internet, video, voice, wireless, cable

networks, filmed TV, and other services. Comcast was founded in 1963, has $109 billion in annual

revenue, and trades for a market capitalization of $233 billion.

Comcast reported its third-quarter earnings results on 10/29/20. For the quarter, the company’s

revenues declined 4.8% to $25.5 billion, adjusted EBITDA declined 11.3% to $7.6 billion, and

adjusted earnings-per-share (EPS) declined 17.7%. However, free cash flow rose 10.5% to nearly $2.3

billion. Comcast experienced record net additions of 556,000 Cable Communications customers in the

quarter, and also added 633,000 High-Speed Internet customers and 187,000 wireless lines.

NBCUniversal revenue fell 19%.

Safety

Comcast is one of the largest companies in the telecommunications and entertainment industry. The

whole cable industry is impacted by the cord-cutting trend, as some customers are ditching traditional

pay-TV entirely in favor of streaming services. Fortunately, consumers still need Internet service for

streaming, and Comcast has so far been able to withstand this trend through growth from its other

businesses.

We expect COVID-19 to be a temporary drag on Comcast. Another factor improving Comcast’s safety

is its balance sheet, as the company focused on deleveraging following the Sky takeover. Comcast’s

consolidated net-debt-to-adjusted-EBITDA ratio fell from 2.9x to 2.8x from Q3 2019.

Growth Prospects

We expect 7% annual earnings-per-share growth over the next five years. The company has a long

history of growth. From 2010 to 2019, its EPS grew yearly, by an average of 19% per year. We expect

a recovery as soon as the COVID-19 pandemic ends. Over the next five years, as the economy

normalizes, we see several drivers for the company’s earnings growth. Revenue growth will be driven

primarily by a higher customer count and rate increases. Although video revenue is struggling with

cord-cutting, higher revenues in the high-speed internet business have more than offset this headwind.

Comcast has had 12 consecutive annual dividend increases. The per share dividend has grown from

$0.19 in 2010 to $0.84 in 2019. The current payout ratio using expected fiscal 2020 adjusted earnings

is just 37%. The company’s dividend is well-covered by both earnings and cash flows and has room to

grow faster than earnings-per-share through payout ratio increases moving forward.

Key Statistics, Ratios, & Metrics Years of Dividend Increases: 12 5-Year Growth Estimate: 7.0%

Dividend Yield: 1.8% Most Recent Dividend Increase: 9.5%

Dividend Risk Score: B Stock Price: $51

34

Return to Top 10 List

Income Statement Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Revenue 37937 55842 62570 64657 68775 74510 80736 85029 94507 108942 Gross Profit 29,400 39,246 42,641 44,987 47,863 51,960 56,388 59,674 64,815 74,502

Gross Margin 77.5% 70.3% 68.1% 69.6% 69.6% 69.7% 69.8% 70.2% 68.6% 68.4% SG&A Exp. 14,804 20,889 22,664 23,553 24,940 27,282 30,131 31,968 5,130 40,424 D&A Exp. 6,803 14,423 7,798 7,871 8,019 8,680 9,426 9,688 10,676 12,953

Operating Profit 7,980 10,721 12,179 13,563 14,904 15,998 16,831 18,018 19,009 21,125 Operating Margin 21.0% 19.2% 19.5% 21.0% 21.7% 21.5% 20.8% 21.2% 20.1% 19.4%

Net Profit 3,635 4,160 6,203 6,816 8,380 8,163 8,678 22,735 11,731 13,057 Net Margin 9.6% 7.4% 9.9% 10.5% 12.2% 11.0% 10.7% 26.7% 12.4% 12.0%

Free Cash Flow 5,682 8,084 8,217 6,555 8,403 9,616 9,004 10,106 12,588 13,269 Income Tax 2,436 3,050 3,744 3,980 3,873 4,959 5,298 -7,569 3,380 3,673

Balance Sheet Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Total Assets (B) 119 158 165 159 159 167 119 158 165 159 Cash & Equivalents 5,984 1,620 10,951 1,718 3,910 2,295 5,984 1,620 10,951 1,718

Accounts Receivable 1,855 4,652 5,521 6,376 6,321 6,896 1,855 4,652 5,521 6,376 Good. & Int. Ass. (B) 78 110 109 109 109 115 78 110 109 109 Total Liabilities (B) 74 110 115 108 106 113 74 110 115 108 Accounts Payable --- 5,705 6,206 5,528 5,638 6,215 --- 5,705 6,206 5,528 Long-Term Debt 31415 39309 40,458 47,847 48,081 52,621 31,415 39,309 40,458 47,847

Shareholder’s Equity 44354 47274 49356 50694 52711 52269 44354 47274 49356 50694 D/E Ratio 0.71 0.83 0.82 0.94 0.91 1.01 0.71 0.83 0.82 0.94

Profitability & Per Share Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Return on Assets 3.1% 3.0% 3.8% 4.2% 5.3% 5.0% 3.1% 3.0% 3.8% 4.2% Return on Equity 8.3% 9.1% 12.8% 13.6% 16.2% 15.6% 8.3% 9.1% 12.8% 13.6%

ROIC 4.9% 5.1% 7.0% 7.2% 8.4% 7.9% 4.9% 5.1% 7.0% 7.2% Shares Out. 5.55 5.41 5.26 5.19 5.06 4.88 4.75 4.64 4.60 4.62

Revenue/Share 6.73 10.05 11.51 12.13 13.13 14.80 6.73 10.05 11.51 12.13 FCF/Share 1.01 1.46 1.51 1.23 1.60 1.91 1.01 1.46 1.51 1.23

Note: All figures in millions of U.S. Dollars unless per share or indicated otherwise.

35

Return to Top 10 List

36

Return to Top 10 List

37

Return to Top 10 List

American Tower Corp. (AMT)

Overview & Current Events

American Tower, founded in 1995, is one of the world’s largest global Real Estate Investment Trusts

(REITs). The company specializes in owning, operating and developing multitenant communications

real estate, with a portfolio of approximately 181,000 communications sites in the United States and

internationally. Last year the $98 billion company generated $3.5 billion in Adjusted Funds From

Operations (AFFO) attributable to stockholders.

On October 29th, 2020 American Tower reported Q3 2020 results for the period ending September 30th,

2020. For the quarter total revenue increased 3.0% to $2.013 billion. Net income declined 8.4% to

$463 million. Consolidated AFFO increased 14.7% to $1.022 billion or $2.29 per share, as results

continue to prove resilient amid the pandemic.

On November 5th, 2020 American Tower announced an agreement to acquire InSite Wireless Group,

which manages approximately 3,000 communication sites (including more than 1,400 towers in the

U.S.) for $3.5 billion. This deal is expected to contribute $150 million in revenue.

Safety

American Tower enjoys a competitive advantage in its leadership in the U.S market. Not only is the

company entrenched in the space but switching costs for the company’s customers (once equipment is

installed) are quite high. Meanwhile, American Tower enjoys economies of scale as it grows larger,

with the cost to add additional tenants to a tower being effectively negligible. Further, unlike its U.S.

counterparts, American Tower is geographically diversified around the globe. This can increase risk

somewhat – for instance with currency translation and working in different operating environments –

but it insulates the firm from relying on a single country.

As of the most recent report, American Tower had long-term obligations of $24 billion, with net-debt-

to-adjusted-EBITDA of 4.5x. This leverage is moderately elevated but is offset by the company’s

long-term leases. The dividend also warrants special mention. Despite the yield not being particularly

impressive, especially for a REIT, American Tower has raised its payout every quarter dating back to

2012. The current quarterly payout is $1.21, a 19.8% increase compared to last year.

Growth Prospects

American Tower has put together an exceptional record in the last decade, growing AFFO by nearly

16% per year dating back to 2011. Moreover, many of the growth drivers of the past remain today.

The company is rooted as a leader in the U.S. market and also has been significantly expanding into

international markets. The continued increase in data usage, especially as it relates to international

countries “catching up,” will be a trend for some time. Moreover, with long-term leases in place,

American Tower has good visibility into the future.

There are a variety of risks that could formulate in the years to come including carrier consolidation,

5G disrupting the company’s macro tower business and growing off such a large base. Weighing the

positives and negatives, we are somewhat cautious with our assumption of 6% annual growth.

Key Statistics, Ratios, & Metrics Years of Dividend Increases: 10 5-Year Growth Estimate: 6.0%

Dividend Yield: 2.1% Most Recent Dividend Increase: 19.8%

Dividend Risk Score: B Stock Price: $223

38

Return to Top 10 List

Income Statement Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Revenue 1985 2444 2876 3361 4100 4772 5786 6664 7440 7580

Gross Profit 1511 1823 2153 2502 3006 3463 3995 4607 5262 5364

Gross Margin 76.1% 74.6% 74.9% 74.4% 73.3% 72.6% 69.1% 69.1% 70.7% 70.8%

SG&A Exp. 230 289 327 416 447 498 543 637 733 730

D&A Exp. 461 556 644 800 1004 1285 1526 1716 2111 1778

Operating Profit 784 920 1120 1214 1487 1613 1853 1998 1905 2688

Operating Margin 39.5% 37.7% 38.9% 36.1% 36.3% 33.8% 32.0% 30.0% 25.6% 35.5%

Net Profit 373 396 637 551 825 685 956 1239 1236 1888

Net Margin 18.8% 16.2% 22.2% 16.4% 20.1% 14.4% 16.5% 18.6% 16.6% 24.9%

Free Cash Flow 674 643 846 875 1160 1438 2019 2122 2835 2761.3

Income Tax 182 125 107 60 63 158 156 31 -110 -0.2

Balance Sheet Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Total Assets 10368 12242 14089 20284 21264 26904 30879 33214 33010 42802

Cash & Equivalents 884 330 369 294 313 321 787 802 1209 1501

Accounts Receivable 81 101 144 151 199 227 308 514 459 462

Goodwill & Int. Ass. 4476 5171 6049 10425 10856 13930 16345 17422 16676 18497

Total Liabilities 6863 8832 10405 16694 17210 20191 23903 26386 27111 37311

Accounts Payable 293 216 90 173 90 97 119 143 131 148

Long-Term Debt 5587 7236 8753 14478 14540 17119 18534 20205 21160 24055

Shareholder’s Equity 3501 3287 3573 3534 3954 6652 6764 6242 5336 5055

D/E Ratio 1.60 2.20 2.45 4.10 3.68 2.57 2.74 3.24 3.97 4.76

Profitability & Per Share Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Return on Assets 3.9% 3.5% 4.8% 3.2% 4.0% 2.8% 3.3% 3.9% 3.7% 5.0%

Return on Equity 10.9% 11.7% 18.6% 15.5% 22.0% 12.9% 14.3% 19.1% 21.4% 36.3%

ROIC 4.5% 4.0% 5.5% 3.6% 4.5% 3.2% 3.9% 4.7% 4.6% 6.7%

Shares Out. 399 394 395 395 397 424 427 429 441 446

Revenue/Share 4.91 6.11 7.20 8.42 10.25 11.28 13.48 15.44 16.80 17.01

FCF/Share 1.67 1.61 2.12 2.19 2.90 3.40 4.70 4.92 6.40 6.20

Note: All figures in millions of U.S. Dollars unless per share or indicated otherwise.

39

Return to Top 10 List

40

Return to Top 10 List

41

Return to Top 10 List

A. O. Smith Corp. (AOS)

Overview & Current Events

A. O. Smith is a manufacturer that specializes in water heaters, boilers, and water treatment products

for commercial and residential customers. The company accrues about two-thirds of its sales from

North America, with most of the balance coming from China. A. O. Smith is a Dividend Aristocrat,

having raised its payout for 27 consecutive years. It was founded in 1874, produces $2.8 billion in

annual revenue, and trades with a market capitalization of $9.0 billion.

A. O. Smith reported third-quarter earnings on October 29th, with the company showing some

resilience in the face of COVID-related headwinds. Total revenue was up 4.4% year-over-year, with

North America leading the way with a 6% increase. Outside of the US, sales were flat, although China

did post a 4% growth rate, which was offset by weakness everywhere else.

Earnings-per-share were $0.66 during the quarter, up from $0.53 in the year-ago period. A. O. Smith

once again showed it can generate operating leverage as revenue rises.

A. O. Smith guided for earnings-per-share of $1.95 to $1.98 for the full year, which, if achieved, would

represent a 10% decline from last year. However, we see reduced demand for the company’s products

as a temporary condition from COVID-related shutdowns, and therefore believe we’ll see a meaningful

rebound in 2021 and beyond. We see long-term earnings power at $2.30 per share for this reason.

Safety

A. O. Smith’s competitive advantage is its specialized knowledge in a niche market. Water heaters and

treatment products are a relatively small market, but A. O. Smith has developed a brand advantage over

time that resonates with customers. It is leveraged to new construction and remodeling of both

residences and commercial properties, so the COVID-related shutdowns we’ve seen have reduced the

market opportunity for A. O. Smith and its competitors temporarily. We see A. O. Smith’s position

within that market as remaining intact when growth, particularly in China, does return.

A. O. Smith isn’t necessarily safe during a recession given its leverage to construction and housing

markets. When these industries face downturns, the demand for new water heaters and treatment

products declines. However, A. O. Smith has managed to raise its payout during very difficult

economic times, including three recessions, so while it has some exposure to economic conditions, it

has been able to weather the storm in the past, and we believe it will again in the future.

A. O. Smith’s dividend safety is quite strong given that its payout ratio for this year is just over half of

projected earnings, even in a down year. Under normalized conditions, we see the payout at less than

half of earnings, which gives A. O. Smith the flexibility to continue to raise the payout even when

earnings decline, as projected for 2020.

Growth Prospects

We see A. O. Smith as producing 6% annual earnings-per-share growth, although if another

recessionary period strikes, that growth may be uneven. We see China as a primary growth driver for

the company as it continues to build its brand in that enormous and growing market.

Key Statistics, Ratios, & Metrics Years of Dividend Increases: 27 5-Year Growth Estimate: 6.0%

Dividend Yield: 1.9% Most Recent Dividend Increase: 8.3%

Dividend Risk Score: B Stock Price: $55

42

Return to Top 10 List

Income Statement Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Revenue 1,489 1,711 1,939 2,154 2,356 2,537 2,686 2,997 3,188 2,993

Gross Profit 446 513 652 774 859 1,010 1,114 1,232 1,306 1,181

Gross Margin 29.9% 30.0% 33.6% 35.9% 36.5% 39.8% 41.5% 41.1% 41.0% 39.5%

SG&A Exp. 329 373 451 525 572 611 663 723 754 716

D&A Exp. 41 47 55 60 60 63 65 70 72 78

Operating Profit 117 140 202 249 287 399 452 510 552 465

Operating Margin 7.9% 8.2% 10.4% 11.6% 12.2% 15.7% 16.8% 17.0% 17.3% 15.5%

Net Profit 112 306 159 170 208 283 327 297 444 370

Net Margin 7.5% 17.9% 8.2% 7.9% 8.8% 11.2% 12.2% 9.9% 13.9% 12.4%

Free Cash Flow 71 5 74 182 178 279 366 232 364 392

Income Tax 17 50 71 67 79 120 136 224 114 102

Balance Sheet Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Total Assets 2,112 2,349 2,279 2,392 2,515 2,629 2,891 3,197 3,072 3,058

Cash & Equivalents 119 463 267 381 319 324 330 347 260 374

Accounts Receivable 368 425 459 475 501 519 593 647 590

Inventories 147 168 163 193 208 223 251 297 305 303

Goodwill & Int. Ass. 430 787 774 758 737 712 800 825 806 884

Total Liabilities 1,231 1,263 1,085 1,063 1,134 1,187 1,376 1,553 1,355 1,391

Accounts Payable 263 303 329 387 394 425 529 535 544 510

Long-Term Debt 261 462 244 192 224 249 324 410 221 284

Shareholder’s Equity 881 1,086 1,194 1,329 1,381 1,442 1,515 1,645 1,717 1,667

D/E Ratio 0.30 0.43 0.20 0.14 0.16 0.17 0.21 0.25 0.13 0.17

Profitability & Per Share Metrics Year 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Return on Assets 5.5% 13.7% 6.9% 7.3% 8.5% 11.0% 11.8% 9.7% 14.2% 12.1%

Return on Equity 13.5% 31.1% 13.9% 13.5% 15.3% 20.0% 22.1% 18.8% 26.4% 21.9%

ROIC 10.2% 22.7% 10.6% 11.5% 13.3% 17.2% 18.5% 15.2% 22.2% 19.0%

Shares Out. 183 184 185 182 179 176 173 172 171 164

Revenue/Share 8.07 9.18 10.41 11.61 12.95 14.17 15.19 17.16 18.51 17.95

FCF/Share 0.39 0.03 0.40 0.98 0.98 1.56 2.07 1.33 2.11 2.35

Note: All figures in millions of U.S. Dollars unless per share or indicated otherwise.

43

Return to Top 10 List

44

Return to Top 10 List

45

Disclaimer

Nothing presented herein is, or is intended to constitute, specific investment advice. Nothing in this newsletter should be construed as a recommendation to follow any investment strategy or allocation. Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements

or forecasts. No reliance should be placed on any such statements or forecasts when making any investment decision. While Sure Dividend has used reasonable efforts

to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made. There is a risk of loss from an investment in

securities. Past performance is not a guarantee of future performance.

Closing Thoughts - Not All Sectors Are Equal -

There are currently only 30 securities that have increased their per share dividend payments for 50 or more consecutive years. Collectively, these 30 securities are called the ‘Dividend Kings.’ They represent the ultimate in historical long-term dividend growth.

The sector breakdown for The Dividend Kings is decidedly not equal.

Source: Data from Sure Dividend

The consumer defensive and industrials sectors dominate the Dividend Kings list. Together, these two sectors account for more than half of the Dividend Kings.

This month’s Top 10 is similar to the Dividend Kings constituent breakdown in that 5 of the Top 10 are either industrials (GD, MMM, AOS) or consumer defensive (ADM, HRL) securities.

The consumer defensive sector clearly changes slower than most other sectors. Snacks, beverages, and disposable paper products haven’t changed all that much in decades. And they are very likely not to change significantly for decades to come.

The Dividend Kings in the industrial sector tend to be diversified manufacturers. They are companies that continuously improve and innovate. This corporate know-how and longevity, which results in more money to spend on research and development, create a durable advantage.

Thanks,

Ben Reynolds

The next Sure Passive Income Newsletter publishes on Sunday, January 17th, 2021

46

Buying & Ranking Criteria The method we use to come up with the Top 10 list for The Sure Passive Income Newsletter is as follows: Note: Ranking data is from the preceding Wednesday’s Sure Analysis data update.

1. Filter our Sure Analysis Research Database universe of securities for: - Dividend yield greater than or equal to the S&P 500’s - A & B Dividend Risk Scores - Dividend yield greater than or equal to the security’s 10-year historical dividend yield - U.S. securities only (no international securities)

2. Rank securities by 5-year forward dividend growth rate and 5-year historical price standard deviation

3. Sort securities by their average ranking between standard deviation and expected growth rate

4. No more than three companies per sector

5. Veto any securities from the Top 10 as necessary after qualitative analysis

6. The Top 10 is the 10 highest ranked securities from steps 1 through 5

7. “A” Dividend Risk Score securities rank ahead of “B” Dividend Risk Score securities within the Top 10. Within each Dividend Risk Score category, the Top 10 order will be sorted by dividend yield + expected 5-year growth rate (the higher the better).

To receive an “A” Dividend Risk Score, a security must be in the top 20% for dividend safety. To receive a “B” Dividend Risk Score, a security must be in the top 40% for dividend safety. The formula for the Dividend Risk Score is below: Dividend Risk Score (Raw) = Payout Ratio x 100 – # Years of Rising Dividends + 50 if deemed risky during a recession We view securities with “A” and “B” Dividend Risk Scores as generally having secure dividends that are very unlikely to be reduced in the near future. Note that the Dividend Risk Score factors in dividend history also. The combination of quality (low price standard deviation and our Dividend Risk Score), with ‘fair or better price’ dividend yield (yield greater than the S&P 500 and the security’s 10-year historical average), and growth (5-year expected growth rate) creates a compelling system to find buy and hold forever securities for rising passive income.

47

Portfolio Building Guide

The process of building a buy and hold rising passive income portfolio is outlined on this page.

Each month invest in the top-ranked security in which you own the smallest dollar amount out of

the Top 10. If you already have 25% or more of your equity portfolio in a specific sector, avoid

purchasing additional securities from that sector until a purchase would not push your allocation in the

sector above 25%.

Over time, you will build a diversified portfolio of high-quality securities likely to pay you rising

income over time.

Alternatively, the Top 10 list is also useful as an idea generation tool for those with a different portfolio

allocation plan.

Examples Portfolio 1 Portfolio 2

Ticker Name Amount Ticker Name Amount

ADM Archer-Daniels-Midland $ 1,002 ADM Archer-Daniels-Midland $ 4,374

GD General Dynamics $ - GD General Dynamics $ 4,878

MMM 3M $ - MMM 3M $ 4,353

HRL Hormel $ - HRL Hormel $ 7,428

AMGN Amgen $ - AMGN Amgen $ 3,309

HD Home Depot $ - HD Home Depot $ 8,099

TRV Travelers $ - TRV Travelers $ 5,629

CMCSA Comcast $ - CMCSA Comcast $ 2,176

AMT American Tower $ - AMT American Tower $ 1,079

AOS A. O. Smith $ - AOS A. O. Smith $ 4,864

- If you had portfolio 1, you would buy GD, the top-ranked security you own least.

- If you had portfolio 2, you would buy AMT, the top-ranked security you own least.

If you have an existing portfolio or a large lump sum to invest, you may wish to switch over to the Sure

Passive Income strategy over a 30-month period. Each month take 1/30 of your initial portfolio value

and buy the top-ranked security you own the least out of the Top 10, subject to the 25% sector

allocation rule discussed earlier. A portfolio with 30 securities purchased with equal dollar amounts

will have a high level of firm-specific diversification.

There’s no upper limit to the number of securities that can be held in a buy and hold portfolio because

securities need not be monitored as closely after purchasing. As a result, investors still in the

accumulation phase can further diversify by adding a greater number of securities over time.

If you are not ready to use the dividend income from your portfolio, set your securities to reinvest

dividends so that your portfolio automatically reinvests its dividend proceeds. This will have the effect

of compounding your portfolio’s dividend income stream faster, as you benefit from having more

shares in the companies and will likely be getting rising dividends from each share as well.

This simple investing process will build a diversified portfolio very likely to generate rising passive

income over time.

48

Past Recommendations & Performance

Every past recommendation in The Sure Passive Income Newsletter is shown below, along with the

date it would’ve been first purchased1, and total returns since the initial recommendation.

Name Ticker First Purchase Date Total Return

Honeywell HON 10/19/2020 23.9%

Colgate-Palmolive CL 10/19/2020 8.0%

Coca-Cola KO 10/19/2020 7.3%

Medtronic MDT 10/19/2020 6.3%

Atmos Energy ATO 10/19/2020 6.2%

Johnson & Johnson JNJ 10/19/2020 6.1%

Republic Services RSG 10/19/2020 5.4%

Mondelez MDLZ 10/19/2020 1.5%

NextEra Energy NEE 10/19/2020 0.6%

Lockheed Martin LMT 10/19/2020 -7.2%

Comcast CMCSA 11/16/2020 3.4%

National Fuel Gas NFG 11/16/2020 3.0%

Travelers TRV 11/16/2020 2.4%

General Dynamics GD 11/16/2020 -0.2%

Home Depot HD 11/16/2020 -1.3%

Amgen AMGN 11/16/2020 -2.9%

J.M. Smucker SJM 11/16/2020 -4.3%

American Tower AMT 11/16/2020 -7.9%

Hormel Foods HRL 11/16/2020 -9.0%

Archer Daniels Midland ADM 12/21/2020 N/A

A.O. Smith AOS 12/21/2020 N/A

3M MMM 12/21/2020 N/A

Note: Performance data is through the morning of December 18th, 2020.

1 This is the closing price from the first trading day after The Sure Passive Income Newsletter publishes.

49

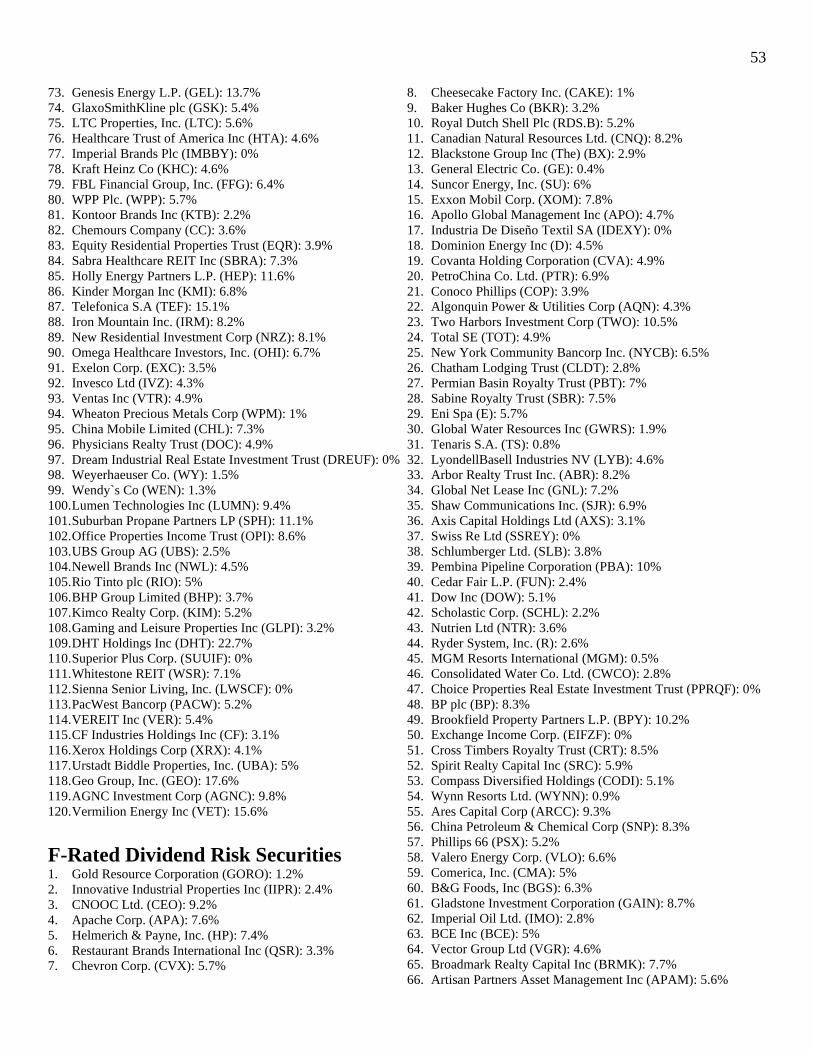

List of Securities by Dividend Risk Score

Each of the securities in the Sure Analysis Research Database are grouped according to Dividend

Risk Score and sorted (from highest to lowest) by expected 5-year growth rate. Dividend or

distribution yield is included next to each security’s ticker symbol. The Dividend Risk Score uses

payout ratio, dividend history, and recession resiliency to measure a company’s dividend safety.

You can learn more about how the score is calculated in the Sure Analysis Glossary. See our

‘Buying and Ranking Criteria’ for more information.

A-Rated Dividend Risk Securities 1. Tencent Holdings Ltd. (TCEHY): 0%

2. Ecolab, Inc. (ECL): 0.8%

3. Stryker Corp. (SYK): 1%

4. H.B. Fuller Company (FUL): 0.9%

5. CSX Corp. (CSX): 1.1%

6. Visa Inc (V): 0.6%

7. Northrop Grumman Corp. (NOC): 1.9%

8. Thermo Fisher Scientific Inc. (TMO): 0.2%

9. L3Harris Technologies Inc (LHX): 1.8%

10. Becton, Dickinson And Co. (BDX): 1.3%

11. Dollar General Corp. (DG): 0.7%

12. Parker-Hannifin Corp. (PH): 1.3%

13. Nike, Inc. (NKE): 0.7%

14. Jack Henry & Associates, Inc. (JKHY): 1.1%

15. Donaldson Co. Inc. (DCI): 1.5%

16. Costco Wholesale Corp (COST): 3.4%

17. Franklin Electric Co., Inc. (FELE): 0.9%

18. Apple Inc (AAPL): 0.6%

19. Albemarle Corp. (ALB): 1.1%

20. West Pharmaceutical Services, Inc. (WST): 0.2%

21. Roper Technologies Inc (ROP): 0.5%

22. McCormick & Co., Inc. (MKC): 1.3%

23. Oracle Corp. (ORCL): 1.5%

24. S&P Global Inc (SPGI): 0.8%

25. Tennant Co. (TNC): 1.3%

26. Ameriprise Financial Inc (AMP): 2.1%

27. SEI Investments Co. (SEIC): 1.2%

28. Moody`s Corp. (MCO): 0.8%

29. Applied Materials Inc. (AMAT): 1%

30. Dover Corp. (DOV): 1.6%

31. Stanley Black & Decker Inc (SWK): 1.6%

32. PPG Industries, Inc. (PPG): 1.4%

33. Microsoft Corporation (MSFT): 1%

34. Medtronic Plc (MDT): 1.9%

35. Computer Services, Inc. (CSVI): 0%

36. Cintas Corporation (CTAS): 1%

37. SJW Group (SJW): 1.8%

38. W.W. Grainger Inc. (GWW): 1.5%

39. Ping AN Insurance (Group) Co. of China, Ltd. (PNGAY): 0%

40. Enterprise Bancorp, Inc. (EBTC): 1.9%

41. Lowe`s Cos., Inc. (LOW): 1.4%

42. Silgan Holdings Inc. (SLGN): 1.3%

43. Atmos Energy Corp. (ATO): 2.3%

44. Carlisle Companies Inc. (CSL): 1.3%

45. Church & Dwight Co., Inc. (CHD): 1.1%

46. Sherwin-Williams Co. (SHW): 0.7%

47. Abbott Laboratories (ABT): 1.3%

48. Canadian National Railway Co. (CNI): 1.2%

49. Otis Worldwide Corp (OTIS): 0.9%

50. MSA Safety Inc (MSA): 1.1%

51. Brown-Forman Corp. (BF.B): 0.9%

52. Pentair plc (PNR): 1.4%

53. Polaris Inc (PII): 2.6%

54. Mckesson Corporation (MCK): 1%

55. General Dynamics Corp. (GD): 2.8%

56. Archer-Daniels-Midland Co. (ADM): 2.9%

57. Fresenius Medical Care AG & Co. KGaA (FMS): 1.7%

58. Assurant Inc (AIZ): 1.9%

59. Johnson & Johnson (JNJ): 2.6%

60. Hormel Foods Corp. (HRL): 2%

61. Advance Auto Parts Inc (AAP): 0.5%

62. Brown & Brown, Inc. (BRO): 0.5%

63. Eaton Vance Corp. (EV): 8.6%

64. Nordson Corp. (NDSN): 0.8%

65. Textron Inc. (TXT): 0.2%

66. Carrier Global Corp (CARR): 0.4%

67. Brookfield Asset Management Inc. (BAM): 1%

68. Eagle Financial Services, Inc. (EFSI): 0%

69. Walgreens Boots Alliance Inc (WBA): 4.4%

70. Perrigo Company plc (PRGO): 1.8%

71. Farmers & Merchants Bancorp (FMCB): 0%

72. Amerisource Bergen Corp. (ABC): 1.7%

73. Genuine Parts Co. (GPC): 3.2%

74. 3M Co. (MMM): 3.3%

75. Target Corp (TGT): 1.6%

76. Brady Corp. (BRC): 1.8%

77. Sonoco Products Co. (SON): 2.8%

78. ABM Industries Inc. (ABM): 1.8%

79. RenaissanceRe Holdings Ltd (RNR): 0.8%

80. Chubb Limited (CB): 2%

81. T. Rowe Price Group Inc. (TROW): 2.4%

82. Colgate-Palmolive Co. (CL): 2%

83. Walmart Inc (WMT): 1.5%

84. Emerson Electric Co. (EMR): 2.4%

85. Stepan Co. (SCL): 0.7%

86. Expeditors International of Washington, Inc. (EXPD): 1.2%

87. RPM International, Inc. (RPM): 1.7%

88. California Water Service Group (CWT): 1.6%

89. Clorox Co. (CLX): 2.1%

90. Tractor Supply Co. (TSCO): 1.1%

50

91. Black Hills Corporation (BKH): 3.5%

92. Community Trust Bancorp, Inc. (CTBI): 4%

93. PSB Holdings Inc (WI) (PSBQ): 0%

94. Franklin Resources, Inc. (BEN): 4.3%

95. Kimberly-Clark Corp. (KMB): 3.1%

96. Gorman-Rupp Co. (GRC): 1.7%

97. Lancaster Colony Corp. (LANC): 1.6%

98. AptarGroup Inc. (ATR): 1.1%

99. Kroger Co. (KR): 2.2%

100. Matthews International Corp. (MATW): 2.9%

101. AbbVie Inc (ABBV): 4.5%

102. Northeast Indiana Bancorp Inc. (NIDB): 0%

103. Cardinal Health, Inc. (CAH): 3.5%

104. Aflac Inc. (AFL): 2.5%

105. McGrath RentCorp (MGRC): 2.5%

106. Tootsie Roll Industries, Inc. (TR): 1.2%

107. RLI Corp. (RLI): 1.9%

108. MGE Energy, Inc. (MGEE): 2%

109. UGI Corp. (UGI): 3.6%

110. American States Water Co. (AWR): 1.6%

111. Nucor Corp. (NUE): 2.8%

112. Unum Group (UNM): 4.9%

113. National Fuel Gas Co. (NFG): 4%

114. Chesapeake Financial Shares Inc (CPKF): 0%

115. Arrow Financial Corp. (AROW): 3.2%

116. Procter & Gamble Co. (PG): 2.3%

117. Middlesex Water Co. (MSEX): 1.4%

118. First Financial Corp. - Indiana (THFF): 2.6%

119. Tompkins Financial Corp (TMP): 2.9%

120. United Bankshares, Inc. (UBSI): 4.4%

B-Rated Dividend Risk Securities 1. America Móvil S.A.B.DE C.V. (AMX): 0%

2. Ritchie Bros Auctioneers Inc (RBA): 1.5%

3. ResMed Inc. (RMD): 0.7%

4. Toro Co. (TTC): 1.1%

5. Lockheed Martin Corp. (LMT): 2.7%

6. CyrusOne Inc (CONE): 2.9%

7. UnitedHealth Group Inc (UNH): 1.4%

8. Keurig Dr Pepper Inc (KDP): 3.4%

9. Skyworks Solutions, Inc. (SWKS): 1.6%

10. Home Depot, Inc. (HD): 2.2%

11. AMGEN Inc. (AMGN): 2.7%

12. Blackrock Inc. (BLK): 2.1%

13. Intercontinental Exchange Inc (ICE): 1.1%

14. Intuit Inc (INTU): 0.6%

15. Domino’s Pizza Inc (DPZ): 0.8%

16. Xylem Inc (XYL): 1%

17. Honeywell International Inc (HON): 1.7%

18. Morningstar Inc (MORN): 0.6%

19. Republic Services, Inc. (RSG): 1.7%

20. Sap SE (SAP): 1.4%

21. Cummins Inc. (CMI): 2.3%

22. Travelers Companies Inc. (TRV): 2.4%

23. Booz Allen Hamilton Holding Corp (BAH): 1.4%

24. Automatic Data Processing Inc. (ADP): 2.1%