sun tv: initiating coverage

TRANSCRIPT

Initiating Coverage | MediaInitiating Coverage | MediaInitiating Coverage | MediaInitiating Coverage | MediaInitiating Coverage | Media

Please refer to important disclosures at the end of this report

Sun TV Networks (STNL) is a leader in 3 out of the 4 lucrative southern TV marketsthrough its bouquet of 20 channels across genres. We have modeled in 23.5%,24.9% and 25.3% CAGR in top-line, core EBIT (post amortisation) and earningsrespectively, for STNL, over FY2010-12E. We also estimate STNL's cash balance toswell to a whopping Rs10bn (~Rs33 per share) in FY2012E. At Rs402, the stock istrading at 19.4x FY2012E Earnings. WWWWWe initiate coverage on the stock with a Buye initiate coverage on the stock with a Buye initiate coverage on the stock with a Buye initiate coverage on the stock with a Buye initiate coverage on the stock with a Buyrecommendation and Trecommendation and Trecommendation and Trecommendation and Trecommendation and Target Parget Parget Parget Parget Price of Rs497 based on 24x P/E FY2012E EPSrice of Rs497 based on 24x P/E FY2012E EPSrice of Rs497 based on 24x P/E FY2012E EPSrice of Rs497 based on 24x P/E FY2012E EPSrice of Rs497 based on 24x P/E FY2012E EPS.....

STNL Ad Revenues to outpace Regional Ad growth, we peg 19% CASTNL Ad Revenues to outpace Regional Ad growth, we peg 19% CASTNL Ad Revenues to outpace Regional Ad growth, we peg 19% CASTNL Ad Revenues to outpace Regional Ad growth, we peg 19% CASTNL Ad Revenues to outpace Regional Ad growth, we peg 19% CAGR:GR:GR:GR:GR: DuringFY2010-12E, we expect STNL's standalone Ad revenues to register 19.3% CAGR,ahead of the 13.9% CAGR estimated in Regional advertising during the period,driven by:1) absorption of rate hikes (ad rates hiked 5-33% across channels),2) increased traction in niche Kids/Comedy channels, and 3) strong managementfocus on utilising inventory during off-peak hours and new weekend programming.

Multiple levers led by DTH to aid 37% CAMultiple levers led by DTH to aid 37% CAMultiple levers led by DTH to aid 37% CAMultiple levers led by DTH to aid 37% CAMultiple levers led by DTH to aid 37% CAGR in Subscription Revenues: GR in Subscription Revenues: GR in Subscription Revenues: GR in Subscription Revenues: GR in Subscription Revenues: DuringFY2010-12E, we expect STNL to register a robust 37% CAGR in overall Subscriptionrevenues aided by: 1) strong 58% CAGR in DTH revenues on the back of 28%CAGR in DTH subscribers and rise in ARPUs to Rs40, and 2) 20% CAGR in Analoguerevenues aided by restructuring of distribution business and Malayalam channels(Surya TV, Kiran TV) turning pay, effective from April 1, 2010.

Radio losses to reduce, Radio losses to reduce, Radio losses to reduce, Radio losses to reduce, Radio losses to reduce, Endhiran Endhiran Endhiran Endhiran Endhiran the wild card in FY2011Ethe wild card in FY2011Ethe wild card in FY2011Ethe wild card in FY2011Ethe wild card in FY2011E: : : : : Beyond broadcasting,we believe reduction in operating losses aided by revenue traction and costcurtailment in Radio subsidiaries, Kal and SAFM (we have modeled in near breakevenin FY2012E at operating level) and contribution from big budget movie, Endhiran(slated for release in 2HFY2011E, we have factored in Rs175cr revenue from moviedistribution/production in FY2011E and 20-25% EBIT Margins from Endhiran) willbe the key factors to watch out for.

June 22, 2010

Sun TV NetworkSun TV NetworkSun TV NetworkSun TV NetworkSun TV Network BUYBUYBUYBUYBUY

Sunny days ahead CMP Rs402Target Price Rs497

Stock Info

Shareholding Pattern (%)

Sector Media

Market Cap (Rs cr) 15,852

Beta 0.6

52 Week High / Low 453/210

Avg. Daily Volume 111,434

Face Value (Rs) 5

BSE Sensex 17,750

Nifty 5,317

Reuters Code SUNTV.BO

Bloomberg Code SUNTV@IN

Promoters 77.0

MF / Banks / Indian FIIs 4.9

FII / NRIs / OCBs 8.1

Indian Public / Others 10.0

Abs. (%) 3m 1yr 3yr

Sensex 1.9 23.9 22.7

Sun TV (3.0) 68.9 (1.3)

Investment Period 12 Months

Chitrangda KChitrangda KChitrangda KChitrangda KChitrangda Kapurapurapurapurapur+91 22 4040 3800 Ext: 323

Email: [email protected]: Company, Angel Research

Key Financials (Consolidated)Y/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr) FY2009FY2009FY2009FY2009FY2009 FY2010EFY2010EFY2010EFY2010EFY2010E FY2011EFY2011EFY2011EFY2011EFY2011E FY2012EFY2012EFY2012EFY2012EFY2012E

Net SalesNet SalesNet SalesNet SalesNet Sales 1,039 1,039 1,039 1,039 1,039 1,453 1,453 1,453 1,453 1,453 1,978 1,978 1,978 1,978 1,978 2,217 2,217 2,217 2,217 2,217

% chg 19.5 39.8 36.2 12.0

Net PNet PNet PNet PNet Profitrofitrofitrofitrofit 368 368 368 368 368 520 520 520 520 520 712 712 712 712 712 816 816 816 816 816

% chg 12.7 41.2 36.9 14.6

OPM (%) 70.9 75.1 75.7 76.1

EPS (Rs)EPS (Rs)EPS (Rs)EPS (Rs)EPS (Rs) 9.3 9.3 9.3 9.3 9.3 13.2 13.2 13.2 13.2 13.2 18.1 18.1 18.1 18.1 18.1 20.7 20.7 20.7 20.7 20.7

P/E (x) 43.0 30.5 22.3 19.4

P/BV (x) 9.3 8.4 6.7 5.4

RoE (%) 21.6 28.0 33.0 30.6

RoCE (%) 30.2 39.8 46.8 43.7

EV/Sales (x) 12.0 8.6 6.3 5.6

EV/EBITDA (x) 16.9 11.4 8.3 7.4

Anand ShahAnand ShahAnand ShahAnand ShahAnand Shah+91 22 4040 3800 Ext: 334

Email: [email protected]

June 22, 2010 2

Sun TV Network | Initiating Coverage

Source: Company, Angel Research, Bloomberg; Note: *Refer Exhibit: 20

Exhibit 1: Our estimates are ahead of consensusY/E MarchY/E MarchY/E MarchY/E MarchY/E March FY2011E FY2011E FY2011E FY2011E FY2011E FY2012EFY2012EFY2012EFY2012EFY2012E CommentsCommentsCommentsCommentsComments

TTTTTopopopopop-line (Rs cr)-line (Rs cr)-line (Rs cr)-line (Rs cr)-line (Rs cr)

Angel estimates 1,978 2,217 Consensus still not factoring in higher

Consensus 1,780 2,045 DTH ARPUs and contribution from Endhiran

Diff (%) 11.1 8.4

Net PNet PNet PNet PNet Profit (Rs cr)rofit (Rs cr)rofit (Rs cr)rofit (Rs cr)rofit (Rs cr)

Angel estimates 712 816 Higher MD's pay and SG&A/amortisation

Consensus 670 797 due to Endhiran reflects our proximity to

Diff (%) 5.8 5.0 consensus Earnings despite higher Top-line estimates*

Initiate Coverage with Buy and Target Price of Rs497

We estimate 25% Earnings CAGR over FY2010-12E

We have modeled in 23.5%, 24.9% and 25.3% CAGR in top-line, core EBIT (post

amortisation) and earnings respectively, for STNL over FY2010-12E. Moreover, we

expect STNL's cash balance to increase to a whopping Rs10bn (~Rs33 per share) in

FY2012E driven by strong rise in free cash flow (almost tripling over FY2010-12E) on

the back of strong earnings growth. As a result, we expect STNL's RoE to sustain at

28-31% levels and RoIC to rise to 47% (36% in FY2010) in FY2012E.

TP based on 24x P/E FY2012E EPS, 5% discount to 3-yr Average

We initiate coverage on STNL with a Buy recommendation and Target Price of Rs497,

equating to an upside of 24% from current levels. Our Target Price is based on

24x P/E FY2012E EPS of Rs20.7, 5% discount to its 3-year historical average P/E of

25.4x to account for risks associated with 1) high ARPUs in DTH subscription model,

and 2) release/success of Endhiran (big budget production).

We believe that premium valuations for STNL are justified given its: 1) strong earnings

CAGR of 25% over FY2010-12E, 2) leadership position in 3 out of 4 lucrative southern

markets, which account for ~73% of the regional TV ad market, 3) strong group

strength including political clout and presence across media value chains (distribution

via Kal cables and DTH via Sun Direct), 4) unique low-cost business model (Broadcast

fee and low SG&A), which enables it to register significantly higher operating margins,

and 5) significant reduction in losses in Radio subsidiaries (we have factored in near

break-even at operating level in FY2012E).

Source: Company, Angel Research

Exhibit 2: Key Triggers - Absorption of rate hikes, Spike in DTH revenues and Endhiran

Absorption of rate hikes (9-33% hike in ad rates in Tamil channels and 5-16% in other channels effective Jan 2010)

Significant increase in DTH ARPUs to Rs40/month in FY2011E (Rs26/month) due to 5 niche and Malayalam channels turning pay

Endhiran (budget of Rs100cr+) slated to release in 2HFY2011in three languages, viz. Tamil, Telugu and Hindi

Reduction in Radio operating losses (EBITDA) from Rs20cr in FY2010 to near break-even in FY2012E

June 22, 2010 3

Sun TV Network | Initiating Coverage

Source: Company, Angel Research; Note: Blue-line denotes 3yr avg P/E

Exhibit 3: STNL trading below its 3yr avg P/E of 25x Exhibit 4: STNL’s 3yr avg Prem over Sensex at 44%

Source: Company, Angel Research; Note: Blue-line denotes 3yr avg Premium

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

Apr

-06

Jun

-06

Aug

-06

Oct

-06

Dec

-06

Feb-0

7

Apr

-07

Jun

-07

Aug

-07

Oct

-07

Dec

-07

Feb-0

8

Apr

-08

Jun

-08

Aug

-08

Oct

-08

Dec

-08

Feb-0

9

Apr

-09

Jun

-09

Aug

-09

Oct

-09

Dec

-09

Feb-1

0

Apr

-10

0%

50%

100%

150%

200%

250%

Apr-

06

Jun

-06

Aug

-06

Oct

-06

Dec-

06

Feb-0

7

Apr-

07

Jun

-07

Aug

-07

Oct

-07

Dec-

07

Feb-0

8

Apr-

08

Jun

-08

Aug

-08

Oct

-08

Dec-

08

Feb-0

9

Apr-

09

Jun

-09

Aug

-09

Oct

-09

Dec-

09

Feb-1

0

Apr-

10

-25%

-5%

15%

35%

55%

75%

95%A

pr-

06

Jun-0

6

Aug-0

6

Oct

-06

Dec-

06

Feb

-07

Apr-

07

Jun-0

7

Aug-0

7

Oct

-07

Dec-

07

Feb

-08

Apr-

08

Jun-0

8

Aug-0

8

Oct

-08

Dec-

08

Feb

-09

Apr-

09

Jun-0

9

Aug-0

9

Oct

-09

Dec-

09

Feb

-10

Apr-

10

Source: Company, Angel Research

Exhibit 5: STNL & ZEEL trading at similar 1yr Fwd P/E Exhibit 6: STNL trades at 3yr avg Prem of 9% to ZEEL

Source: Company, Angel Research; Note: Blue-line denotes 3yr avg Premium

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

Apr-

06

Jun

-06

Aug

-06

Oct

-06

Dec

-06

Feb-0

7

Apr-

07

Jun

-07

Aug

-07

Oct

-07

Dec

-07

Feb-0

8

Apr-

08

Jun

-08

Aug

-08

Oct

-08

Dec

-08

Feb-0

9

Apr-

09

Jun

-09

Aug

-09

Oct

-09

Dec

-09

Feb-1

0

Apr-

10

BSE Sensex Sun TV Zee Ent

Exhibit 7: Relative Valuation - Sun TV has the highest EPS CAGR and strong RoEs v/s peers

(Rs cr)(Rs cr)(Rs cr)(Rs cr)(Rs cr) FY10-12EFY10-12EFY10-12EFY10-12EFY10-12E FY10-12EFY10-12EFY10-12EFY10-12EFY10-12E FY11EFY11EFY11EFY11EFY11E FY12EFY12EFY12EFY12EFY12E FY11EFY11EFY11EFY11EFY11E FY12EFY12EFY12EFY12EFY12E FY11EFY11EFY11EFY11EFY11E FY12EFY12EFY12EFY12EFY12E FY11EFY11EFY11EFY11EFY11E FY12EFY12EFY12EFY12EFY12E

IndiaIndiaIndiaIndiaIndia

BroadcastingBroadcastingBroadcastingBroadcastingBroadcasting

Sun TV 15,877 25.3 0.8 22.3 19.5 33.0 30.6 8.3 7.4 6.3 5.6

Zee Ent # 14,322 21.8 0.9 23.1 19.5 14.5 15.4 NA NA 5.1 4.4

PPPPPrintrintrintrintrint

HT Media 3,597 22.2 0.8 20.2 16.8 15.1 15.7 12.3 10.2 2.3 2.0

Jagran Prakashan 3,766 16.2 1.0 19.1 15.9 31.0 34.3 11.3 9.5 3.4 2.9

Deccan Chronicle 3,035 11.3 0.8 10.6 9.3 18.9 19.1 5.7 4.9 2.7 2.3

MCapMCapMCapMCapMCap EPS CAEPS CAEPS CAEPS CAEPS CAGRGRGRGRGR PEG (x)PEG (x)PEG (x)PEG (x)PEG (x) P/E (x)P/E (x)P/E (x)P/E (x)P/E (x) RoE (%) RoE (%) RoE (%) RoE (%) RoE (%) EV/EBITDEV/EBITDEV/EBITDEV/EBITDEV/EBITDA (x)A (x)A (x)A (x)A (x) EV/Sales (x)EV/Sales (x)EV/Sales (x)EV/Sales (x)EV/Sales (x)

Source: Company, Angel research; Note: # Zee Entertainment figures are consensus estimates from Bloomberg

June 22, 2010 4

Sun TV Network | Initiating Coverage

Investment Arguments

TV Ad to grow 15.6% CAGR, Regional Ad to grow faster

During FY2010, the Media & Entertainment (M&E) industry grew at a mere 1.5% yoy

to Rs590bn impacted by the economic slowdown and shrinking corporate budgets.

However, amidst weak macro economic conditions, the TV industry registered a modest

growth of 6.9% yoy to Rs260bn. Going ahead, the M&E industry is expected to rebound

and register 13.2% CAGR over FY2010-15E, while the Television sector is expected to

outpace the M&E industry growth, registering a CAGR of 15.2% over the mentioned

period.

Television advertising, which accounts for 40% of the total advertisement market, is

expected to post a CAGR of 15.6% over FY2010-15E to Rs182bn, aided by:

1) increasing number of channels (have nearly quadrupled to over 460 since FY2004),

2) rising viewership fragmentation, and 3) robust growth in niche genres like sports

(due to strong properties like IPL) and regional (emerging as a strong cost-effective

medium).

Television sector is expected to outpace the

M&E growth, registering a CAGR of 15.2%

over FY2010-15E

(Rs cr)(Rs cr)(Rs cr)(Rs cr)(Rs cr) FY2007FY2007FY2007FY2007FY2007 FY2008FY2008FY2008FY2008FY2008 FY2009FY2009FY2009FY2009FY2009 FY2010FY2010FY2010FY2010FY2010 FY2011EFY2011EFY2011EFY2011EFY2011E FY2012EFY2012EFY2012EFY2012EFY2012E FY2013EFY2013EFY2013EFY2013EFY2013E FY2014EFY2014EFY2014EFY2014EFY2014E FY2015EFY2015EFY2015EFY2015EFY2015E #####FY10-15EFY10-15EFY10-15EFY10-15EFY10-15E

TTTTTotal M&E Sizeotal M&E Sizeotal M&E Sizeotal M&E Sizeotal M&E Size 44,160 44,160 44,160 44,160 44,160 51,630 51,630 51,630 51,630 51,630 57,840 57,840 57,840 57,840 57,840 58,700 58,700 58,700 58,700 58,700 65,230 65,230 65,230 65,230 65,230 74,180 74,180 74,180 74,180 74,180 83,610 83,610 83,610 83,610 83,610 95,640 95,640 95,640 95,640 95,640 109,200 109,200 109,200 109,200 109,200 13.213.213.213.213.2

Growth (% yoy) 14.8 16.9 12.0 1.5 11.1 13.7 12.7 14.4 14.2

TTTTTotal Total Total Total Total Television Marketelevision Marketelevision Marketelevision Marketelevision Market 18,250 18,250 18,250 18,250 18,250 21,130 21,130 21,130 21,130 21,130 24,050 24,050 24,050 24,050 24,050 25,700 25,700 25,700 25,700 25,700 28,900 28,900 28,900 28,900 28,900 33,700 33,700 33,700 33,700 33,700 38,200 38,200 38,200 38,200 38,200 44,800 44,800 44,800 44,800 44,800 52,100 52,100 52,100 52,100 52,100 15.215.215.215.215.2

Growth (% yoy) 11.8 15.8 13.8 6.9 12.5 16.6 13.4 17.3 16.3

TTTTTotal Advertising Marketotal Advertising Marketotal Advertising Marketotal Advertising Marketotal Advertising Market 16,570 16,570 16,570 16,570 16,570 19,640 19,640 19,640 19,640 19,640 22,120 22,120 22,120 22,120 22,120 22,030 22,030 22,030 22,030 22,030 24,690 24,690 24,690 24,690 24,690 28,130 28,130 28,130 28,130 28,130 32,270 32,270 32,270 32,270 32,270 37,070 37,070 37,070 37,070 37,070 42,690 42,690 42,690 42,690 42,690 14.114.114.114.114.1

(% of Total M&E) 37.5 38.0 38.2 37.5 37.9 37.9 38.6 38.8 39.1

(% of GDP) 0.46 0.50 0.53 0.49 0.51 0.53 0.56 0.59 0.62

TTTTTelevision Ad Marketelevision Ad Marketelevision Ad Marketelevision Ad Marketelevision Ad Market 6,100 6,100 6,100 6,100 6,100 7,110 7,110 7,110 7,110 7,110 8,250 8,250 8,250 8,250 8,250 8,800 8,800 8,800 8,800 8,800 9,860 9,860 9,860 9,860 9,860 11,330 11,330 11,330 11,330 11,330 13,260 13,260 13,260 13,260 13,260 15,520 15,520 15,520 15,520 15,520 18,150 18,150 18,150 18,150 18,150 15.615.615.615.615.6

(% of Total Ad Market) 36.8 36.2 37.3 39.9 39.9 40.3 41.1 41.9 42.5

(% of Total Television Market) 33.4 33.6 34.3 34.2 34.1 33.6 34.7 34.6 34.8

Growth (% yoy) 17.5 16.6 16.0 6.7 12.0 14.9 17.0 17.0 16.9

Hindi GEC*Hindi GEC*Hindi GEC*Hindi GEC*Hindi GEC* 2,501 2,501 2,501 2,501 2,501 2,588 2,588 2,588 2,588 2,588 2,863 2,863 2,863 2,863 2,863 2,860 2,860 2,860 2,860 2,860 3,066 3,066 3,066 3,066 3,066 3,456 3,456 3,456 3,456 3,456 3,978 3,978 3,978 3,978 3,978 4,625 4,625 4,625 4,625 4,625 5,372 5,372 5,372 5,372 5,372 13.413.413.413.413.4

(% of Televsion Ad Market) 41.0 36.4 34.7 32.5 31.1 30.5 30.0 29.8 29.6

Growth (% yoy) - 3.5 10.6 (0.1) 7.2 12.7 15.1 16.3 16.2

Regional TV Ad MarketRegional TV Ad MarketRegional TV Ad MarketRegional TV Ad MarketRegional TV Ad Market 1,281 1,281 1,281 1,281 1,281 1,742 1,742 1,742 1,742 1,742 2,186 2,186 2,186 2,186 2,186 2,464 2,464 2,464 2,464 2,464 2,771 2,771 2,771 2,771 2,771 3,195 3,195 3,195 3,195 3,195 3,766 3,766 3,766 3,766 3,766 4,439 4,439 4,439 4,439 4,439 5,245 5,245 5,245 5,245 5,245 16.316.316.316.316.3

(% of Televsion Ad Market) 21.0 24.5 26.5 28.0 28.1 28.2 28.4 28.6 28.9

Growth (% yoy) - 36.0 25.5 12.7 12.4 15.3 17.9 17.9 18.2

Exhibit 8: Regional advertising to grow at faster pace v/s Hindi GECs and overall TV Advertising

Source: FICCI-KPMG report 2010, Angel research, # denotes: CAGR, * Hindi GEC Market includes Doordarshan

In Television, we believe the Regional Ad market is all set to outpace the larger Hindi

GEC market and record 16.3% CAGR during FY2010-15E on the back of favourable

demographics and significant changes in the dynamics of the Television industry

(increasing fragmentation and consolidation in the Hindi GEC space). Moreover,

Regional Media has witnessed increased levels of activity owing to significantly untapped

markets of Tier-II and III towns, which are emerging as the new focus areas of marketers

owing to low penetration levels, steady growth in consumer spending and high

long-term growth potential.

Favourable demographics and significant

changes in dynamics of Television industry

coupled with strong cost effective

proposition is expected to help the Regional

Ad market to grow at a faster clip

June 22, 2010 5

Sun TV Network | Initiating Coverage

STNL Ad Revenues to outpace Regional Ad growth, we peg 19% CAGR

The southern regional markets of Tamil Nadu, Andhra Pradesh, Karnataka and Kerala

account for ~73% of the total regional advertisement revenue. STNL with its dominant

market share across lucrative southern markets, through its bouquet of 20 channels

across genres like GECs, Music, News and Movies including flagship channels -

Sun TV (Tamil Nadu, market share 68%), Gemini TV (Andhra Pradesh, market share

36%), Udaya TV (Karnataka, market share of 40%) and Surya TV (Kerala, market

share of 33%) - is well placed to ride the regional wave.

South accounts for ~73% of the total

Regional Ad-market, where Sun is a leader

in three out of the four southern markets

Exhibit 9: STNL's Ad Revenue to grow at faster 19% CAGR vis-à-vis Regional Ad growth at 14% CAGR(Rs cr)(Rs cr)(Rs cr)(Rs cr)(Rs cr) FY2007FY2007FY2007FY2007FY2007 FY2008FY2008FY2008FY2008FY2008 FY2009FY2009FY2009FY2009FY2009 FY2010FY2010FY2010FY2010FY2010 FY2011EFY2011EFY2011EFY2011EFY2011E FY2012EFY2012EFY2012EFY2012EFY2012E #####FY10-12EFY10-12EFY10-12EFY10-12EFY10-12E

Regional TV Ad MarketRegional TV Ad MarketRegional TV Ad MarketRegional TV Ad MarketRegional TV Ad Market 1,281 1,281 1,281 1,281 1,281 1,742 1,742 1,742 1,742 1,742 2,186 2,186 2,186 2,186 2,186 2,464 2,464 2,464 2,464 2,464 2,771 2,771 2,771 2,771 2,771 3,195 3,195 3,195 3,195 3,195 13.9 13.9 13.9 13.9 13.9

Growth (% yoy) - 36.0 25.5 12.7 12.4 15.3

Tamil Ad Market 380 517 647 732 826 959 14.4

Telegu Ad market 301 406 509 572 643 741 13.9

Kannada Ad Market 147 199 250 281 319 367 14.4

Malyalam Ad Market 97 141 181 205 227 259 12.5

Southern Ad MarketSouthern Ad MarketSouthern Ad MarketSouthern Ad MarketSouthern Ad Market 926 926 926 926 926 1,263 1,263 1,263 1,263 1,263 1,588 1,588 1,588 1,588 1,588 1,789 1,789 1,789 1,789 1,789 2,014 2,014 2,014 2,014 2,014 2,326 2,326 2,326 2,326 2,326 14.0 14.0 14.0 14.0 14.0

Bengali Ad Market 158 223 280 323 363 422 14.3

Marathi Ad Market 143 188 236 271 310 358 14.9

STNL's Ad Revenue (Standalone)STNL's Ad Revenue (Standalone)STNL's Ad Revenue (Standalone)STNL's Ad Revenue (Standalone)STNL's Ad Revenue (Standalone) 363 363 363 363 363 467 467 467 467 467 573 573 573 573 573 788 788 788 788 788 945 945 945 945 945 1,122 1,122 1,122 1,122 1,122 19.3 19.3 19.3 19.3 19.3

(% of Southern TV Ad Market) 39.3 37.6 38.2 47.3 50.4 51.9

Growth (% yoy) - (4.2) 1.4 23.9 6.6 3.0

STNL's Ad Revenue (Incl Radio)STNL's Ad Revenue (Incl Radio)STNL's Ad Revenue (Incl Radio)STNL's Ad Revenue (Incl Radio)STNL's Ad Revenue (Incl Radio) 364 364 364 364 364 475 475 475 475 475 606 606 606 606 606 846 846 846 846 846 1,015 1,015 1,015 1,015 1,015 1,208 1,208 1,208 1,208 1,208 19.519.519.519.519.5

Growth (% yoy) - 30.6 27.4 39.6 20.1 18.9

Source: Company, Angel Research; Note: # denotes CAGR

During FY2010-12E, we peg STNL's standalone Ad revenues (excluding Radio) to

grow at 19.3% CAGR (management has guided for 17-18% yoy growth in advertising

in FY2011E), ahead of 13.9% CAGR in Regional advertising during the period, driven

by: 1) absorption of rate hikes (9-33% hike in ad rates in Tamil channels and 5-16%

in other channels effective January 2010), 2) increased traction from niche kids/comedy

channels (Adhitya TV, Khushi TV, Navvulu TV, Chintu TV and Ushe TV) launched in

1QFY2010, 3) strong focus of management on utilising inventory during off-peak

hours and new weekend programming, and 4) uptick in the economy (higher ad

spends from the FMCG sector in specific, which contributes ~80% of STNL's

advertisement revenues). While the ad-rate hike absorption will be a primary driver

for high advertisement revenues, we expect the ad-revenue growth to peak out in

1QFY2011 (with the culmination of the base effect) and dip into mid-teens by 3Q and

4QFY2011.

We highlight that during the last several quarters, STNL has posted high growth rates

(in the range of 35-45%) in advertising revenue, partially aided by low base, showing

strong resilience to: 1) increasing competition in its Telugu, Kannada and Malayalam

markets, and 2) shift in advertising flow towards sports properties like IPL - Season 3.

We have modeled in a 19.3% CAGR in

STNL's standalone Ad revenues driven by

rate hikes, improved inventory utilisation

and traction in new channels

We expect ad-revenue growth to peak out

in 1QFY2011with culmination of base effect

STNL has shown strong resilience to

intensifying competition and shift in

advertisement flow towards sports; however,

a change in the same carries downside risks

to our estimates

June 22, 2010 6

Sun TV Network | Initiating Coverage

Exhibit 10: High Per Capita Income and Urban Population make South a lucrative marketPPPPPer Capitaer Capitaer Capitaer Capitaer Capita GrowthGrowthGrowthGrowthGrowth TTTTTotal Potal Potal Potal Potal Popopopopop Urban P Urban P Urban P Urban P Urban Popopopopop % of Urban% of Urban% of Urban% of Urban% of Urban

IncomeIncomeIncomeIncomeIncome (%)(%)(%)(%)(%) (1,000s)(1,000s)(1,000s)(1,000s)(1,000s) (1,000s)(1,000s)(1,000s)(1,000s)(1,000s) PPPPPopopopopop

(current price - Rs)(current price - Rs)(current price - Rs)(current price - Rs)(current price - Rs)

TN 38,573 10.6 62,406 27,459 44

Andhra Pradesh 34,063 16.3 76,210 19,053 25

Karnataka 35,555 16.6 52,851 18,498 35

Kerela 41,814 14.2 31,841 11,463 36

All IndiaAll IndiaAll IndiaAll IndiaAll India 33,283 33,283 33,283 33,283 33,283 1,028,737 1,028,737 1,028,737 1,028,737 1,028,737 285,989 285,989 285,989 285,989 285,989 28 28 28 28 28

Source: Economic Survey 2007-08, Angel Research

Source: TAM, Angel Research

Exhibit 13: Battling out to stay a strong No1 Exhibit 14: Playing 2nd fiddle to leader Asianet

Source: TAM, Angel Research

Mark

etShare

(%)

43.7 44.1

37.6 38.4 39.1

42.8

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

4QFY2009 1QFY2010 2QFY2010 3QFY2010 4QFY2010 1QFY2011

Kannada GEC

Udaya TV ETV Kannada Zee Kannada

Kasturi Suvarna DD9 Chandana (Kannada)

Mark

etShare

(%)

35.0 34.632.2 33.3 32.7 32.3

-

10.0

20.0

30.0

40.0

50.0

60.0

4QFY2009 1QFY2010 2QFY2010 3QFY2010 4QFY2010 1QFY2011

Malyalam GEC

Asianet Surya TV Kairali Amrita TV DD4 Malayalam

Source: TAM, Angel ResearchSource: TAM, Angel Research

Exhibit 11: Sun's Bastion with ~70% share Exhibit 12: Successfully fending off competition

66.7 68.1 68.5 69.0 67.469.8

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

4QFY2009 1QFY2010 2QFY2010 3QFY2010 4QFY2010 1QFY2011

Tamil GEC

Sun TV Kalaignar TV Vijay TV Jaya TV

Raj TV Zee Tamizh Others

Mark

etSh

are

(%)

Mark

etSh

are

(%)

40.3

36.5 36.434.5

36.7

40.1

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

4QFY2009 1QFY2010 2QFY2010 3QFY2010 4QFY2010 1QFY2011

Telegu GEC

Gemini TV Eanadu TV Zee Telugu Maa Telugu

DD8 Telugu Sitara TV Vanitha TV

June 22, 2010 7

Sun TV Network | Initiating Coverage

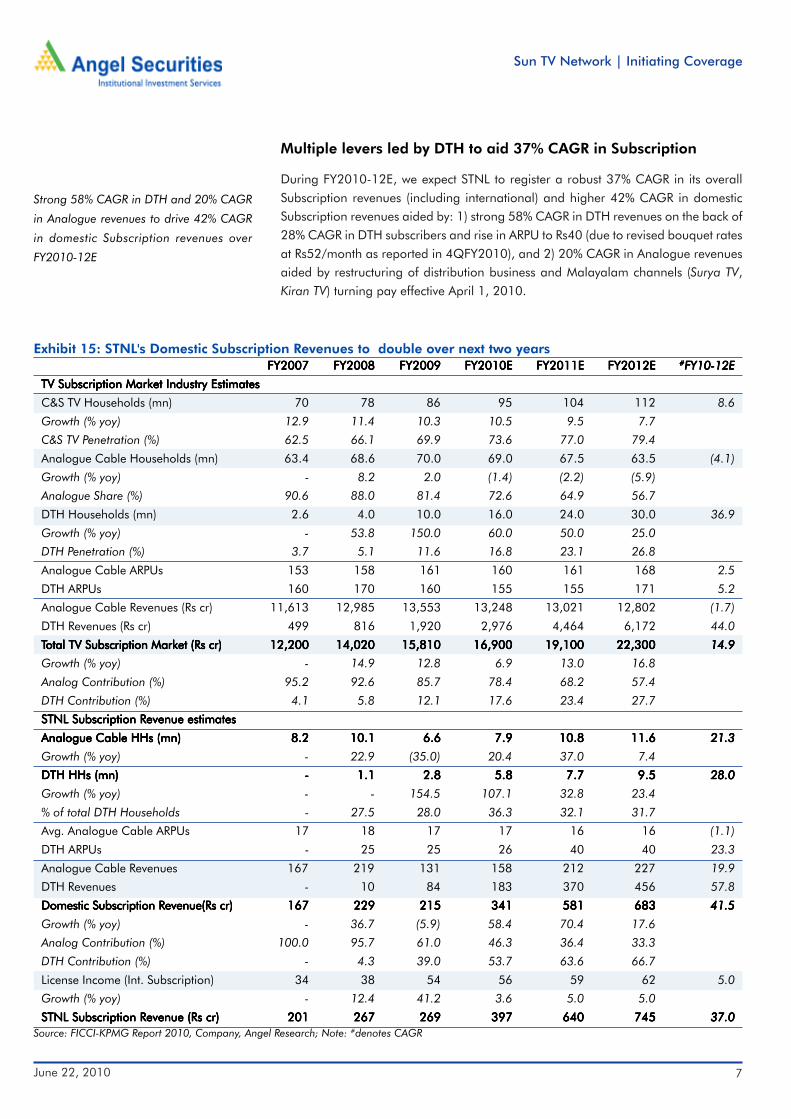

Multiple levers led by DTH to aid 37% CAGR in Subscription

During FY2010-12E, we expect STNL to register a robust 37% CAGR in its overallSubscription revenues (including international) and higher 42% CAGR in domesticSubscription revenues aided by: 1) strong 58% CAGR in DTH revenues on the back of28% CAGR in DTH subscribers and rise in ARPU to Rs40 (due to revised bouquet ratesat Rs52/month as reported in 4QFY2010), and 2) 20% CAGR in Analogue revenuesaided by restructuring of distribution business and Malayalam channels (Surya TV,Kiran TV) turning pay effective April 1, 2010.

Strong 58% CAGR in DTH and 20% CAGR

in Analogue revenues to drive 42% CAGR

in domestic Subscription revenues over

FY2010-12E

Exhibit 15: STNL's Domestic Subscription Revenues to double over next two yearsFY2007FY2007FY2007FY2007FY2007 FY2008FY2008FY2008FY2008FY2008 FY2009FY2009FY2009FY2009FY2009 FY2010EFY2010EFY2010EFY2010EFY2010E FY2011EFY2011EFY2011EFY2011EFY2011E FY2012EFY2012EFY2012EFY2012EFY2012E #####FY10-12EFY10-12EFY10-12EFY10-12EFY10-12E

TV Subscription Market Industry EstimatesTV Subscription Market Industry EstimatesTV Subscription Market Industry EstimatesTV Subscription Market Industry EstimatesTV Subscription Market Industry Estimates

C&S TV Households (mn) 70 78 86 95 104 112 8.6

Growth (% yoy) 12.9 11.4 10.3 10.5 9.5 7.7

C&S TV Penetration (%) 62.5 66.1 69.9 73.6 77.0 79.4

Analogue Cable Households (mn) 63.4 68.6 70.0 69.0 67.5 63.5 (4.1)

Growth (% yoy) - 8.2 2.0 (1.4) (2.2) (5.9)

Analogue Share (%) 90.6 88.0 81.4 72.6 64.9 56.7

DTH Households (mn) 2.6 4.0 10.0 16.0 24.0 30.0 36.9

Growth (% yoy) - 53.8 150.0 60.0 50.0 25.0

DTH Penetration (%) 3.7 5.1 11.6 16.8 23.1 26.8

Analogue Cable ARPUs 153 158 161 160 161 168 2.5

DTH ARPUs 160 170 160 155 155 171 5.2

Analogue Cable Revenues (Rs cr) 11,613 12,985 13,553 13,248 13,021 12,802 (1.7)

DTH Revenues (Rs cr) 499 816 1,920 2,976 4,464 6,172 44.0

TTTTTotal TVotal TVotal TVotal TVotal TV Subscription Market (Rs cr)Subscription Market (Rs cr)Subscription Market (Rs cr)Subscription Market (Rs cr)Subscription Market (Rs cr) 12,20012,20012,20012,20012,200 14,02014,02014,02014,02014,020 15,81015,81015,81015,81015,810 16,90016,90016,90016,90016,900 19,10019,10019,10019,10019,100 22,30022,30022,30022,30022,300 14.914.914.914.914.9

Growth (% yoy) - 14.9 12.8 6.9 13.0 16.8

Analog Contribution (%) 95.2 92.6 85.7 78.4 68.2 57.4

DTH Contribution (%) 4.1 5.8 12.1 17.6 23.4 27.7

STNL Subscription Revenue estimatesSTNL Subscription Revenue estimatesSTNL Subscription Revenue estimatesSTNL Subscription Revenue estimatesSTNL Subscription Revenue estimates

Analogue Cable HHs (mn)Analogue Cable HHs (mn)Analogue Cable HHs (mn)Analogue Cable HHs (mn)Analogue Cable HHs (mn) 8.2 8.2 8.2 8.2 8.2 10.1 10.1 10.1 10.1 10.1 6.6 6.6 6.6 6.6 6.6 7.9 7.9 7.9 7.9 7.9 10.8 10.8 10.8 10.8 10.8 11.6 11.6 11.6 11.6 11.6 21.321.321.321.321.3

Growth (% yoy) - 22.9 (35.0) 20.4 37.0 7.4

DTH HHs (mn)DTH HHs (mn)DTH HHs (mn)DTH HHs (mn)DTH HHs (mn) - - - - - 1.1 1.1 1.1 1.1 1.1 2.8 2.8 2.8 2.8 2.8 5.8 5.8 5.8 5.8 5.8 7.7 7.7 7.7 7.7 7.7 9.5 9.5 9.5 9.5 9.5 28.028.028.028.028.0

Growth (% yoy) - - 154.5 107.1 32.8 23.4

% of total DTH Households - 27.5 28.0 36.3 32.1 31.7

Avg. Analogue Cable ARPUs 17 18 17 17 16 16 (1.1)

DTH ARPUs - 25 25 26 40 40 23.3

Analogue Cable Revenues 167 219 131 158 212 227 19.9

DTH Revenues - 10 84 183 370 456 57.8

Domestic Subscription Revenue(Rs cr)Domestic Subscription Revenue(Rs cr)Domestic Subscription Revenue(Rs cr)Domestic Subscription Revenue(Rs cr)Domestic Subscription Revenue(Rs cr) 167167167167167 229229229229229 215215215215215 341341341341341 581581581581581 683683683683683 41.541.541.541.541.5

Growth (% yoy) - 36.7 (5.9) 58.4 70.4 17.6

Analog Contribution (%) 100.0 95.7 61.0 46.3 36.4 33.3

DTH Contribution (%) - 4.3 39.0 53.7 63.6 66.7

License Income (Int. Subscription) 34 38 54 56 59 62 5.0

Growth (% yoy) - 12.4 41.2 3.6 5.0 5.0

STNL Subscription Revenue (Rs cr)STNL Subscription Revenue (Rs cr)STNL Subscription Revenue (Rs cr)STNL Subscription Revenue (Rs cr)STNL Subscription Revenue (Rs cr) 201201201201201 267267267267267 269269269269269 397397397397397 640640640640640 745745745745745 37.037.037.037.037.0Source: FICCI-KPMG Report 2010, Company, Angel Research; Note: #denotes CAGR

June 22, 2010 8

Sun TV Network | Initiating Coverage

Higher ARPUs and Subscribers to aid 58% CAGR in DTH revenues

During 4QFY2010, the company reported a subscriber base of 6mn and a sharp

uptick in DTH realizations to Rs35-36/month (Rs26-27/month) on account of 5 new

niche channels turning pay adding to the company's ARPUs (new channel bouquet

available at Rs52/month). Hence, we have modeled in 58% CAGR in DTH Subscription

revenues over FY2010-12E, driven by - 1) yoy growth of 33% and 23% for

FY2011-12E in the Subscriber base to 7.7mn and 9.5mn respectively, 2) significant

52% yoy increase in ARPU to Rs40/month (Rs26/month) in FY2011E.

However, we note that ~60% of the DTH revenues for STNL come from its sister

concern Sun Direct, which has accepted the revised bouquet driving this sharp up-tick

in DTH revenues. Nonetheless, STNL continues to offer its original bouquet. However,

the stickiness of other operators to the same and non-confirmation of 4QFY2010

ARPU trend carries downside risks to our estimates.

Malayalam channels and distribution re-jig to boost Analogue revenues

Post the significant dip in Analogue subscription revenues in FY2009 due to power

cuts in Tamil Nadu, launch of new distributors (Arasu, Royal Cable) and Sun Direct

(cable operators boycotted the launch of DTH by cutting declaration levels), STNL has

renewed its focus and restructured its Distribution business with two separate teams,

the first focusing on South Indian operations and International business, and the second

focusing on expanding the company's bouquet to the North, West and Eastern markets

in India.

Moreover, on February 2010, STNL announced that its Malayalam channels Surya TV

and Kiran TV would become pay channels from April 1, 2010. According to

management, the non-CAS cable rates for the said channels, as a bouquet, would be

Rs20.3/month and CAS cable rates would be Rs5.4/channel/month. We highlight

that this move has come post its key competitor, Asianet, turning pay. We estimate that

the Malayalam market has ~4mn C&S households and have modeled in an initial

addition of 1.5mn subscribers in FY2011E with an ARPU of Rs15/month for STNL.

Hence, we expect incremental addition of Rs20-25cr to STNL's Subscription revenues

in FY2011E on account of the Malayalam channels turning pay.

We expect the Analogue subscription revenues to register 20% CAGR over

FY2010-12E, with 34% yoy growth in FY2011E itself on a low base (inclusion of

Malayalam subscription revenues)

Management upbeat on International subscription, we defer

In contrast to management guidance of sharp improvement in International subscription

revenue (program license fees), we have conservatively modeled in 5% CAGR over

FY2010-12E, owing to: 1) lack of traction in the same since several quarters, 2) changed

regulations for Pay TV in the South-East Asian countries of Malaysia and Singapore,

and 3) currency fluctuation risks. However, the distribution re-jig done by the company

(STNL has floated a wholly-owned subsidiary, Sun TV Network Europe in the UK to

distribute and broadcast its channel in UK and Europe) poses an upside risk to our

estimates.

4QFY2010 registered a sharp revision in

DTH ARPUs to Rs36/month aided by

addition of 5 niche channels and a new

bouquet priced at Rs52/month

Non-confirmation of 4QFY2010 ARPU trend

carries downside risks to our estimates

Re-jig of Distribution and renewed focus on

domestic Subscription augurs well for STNL's

Analogue Subscription revenues

We expect incremental addition of

Rs20-25cr to STNL's Subscription revenues

in FY2011E on account of Malayalam

channels turning pay

In contrast to management guidance, we

have conservatively modeled in 5% yoy

growth in Sun's International subscription

revenues in our FY2011-12E estimates

June 22, 2010 9

Sun TV Network | Initiating Coverage

Sun Pictures - Betting big on Endhiran

Sun entered the Movie business in September 2008 through subsidiary, Sun Pictures,

and has so far distributed 12-15 films, most of which have been successful and earning

an estimated 15-20% Return on Capital Employed. Going ahead, we have modeled

in an outlay of Rs70-80cr for FY2011-12E for distribution of 10-12 movies annually.

STNL recently entered into movie production with its high budget movie, Endhiran

(estimated budget for the movie is Rs100cr+), starring the southern superstar Rajnikant

and Bollywood's Aishwarya Rai. The movie is expected to be released in 2HFY2011in

three languages, viz. Tamil, Telugu and Hindi. Given the star cast and cutting edge

production techniques used in this movie, we expect it to register returns of 20-25% at

the EBIT level. Management has indicated that this is a one-off venture, and the company

would be focusing only on the distribution business in the future.

For FY2011E, we estimate STNL revenues from movie distribution (including release

of Endhiran) to increase 150% yoy to Rs175cr (Rs70cr) and then taper down to Rs110cr

in FY2012E, as effects of revenue traction from Endhiran wanes.

Radio - to reach near break-even at operating level by FY2012E

Sun operates 44 radio stations in total and has two subsidiaries Kal Radio (Kal) and

South Asia FM (SAFM) with stake of 97.8% and 59.2% respectively. STNL has entered

into a strategic tie-up to broadcast its own radio channels under the Red FM brand

(holds 48.9% stake in Red FM), operating at 93.5MHz. Consequently, S FM or Suryan

FM was re-branded into Red FM across 38 cities (except for the ones in Tamil Nadu) in

India.

Endhiran slated for release in 2HFY2011E

is expected to register returns of 20-25% at

EBIT level. We estimate a 150% yoy growth

in Movie revenue for FY2011E to Rs175cr,

tapering down to Rs110cr in FY2012E

Exhibit 16: Consolidated Radio losses to moderate to Rs37cr in FY2012EY/E MarchY/E MarchY/E MarchY/E MarchY/E March FY2008FY2008FY2008FY2008FY2008 FY2009FY2009FY2009FY2009FY2009 FY2010FY2010FY2010FY2010FY2010 FY2011EFY2011EFY2011EFY2011EFY2011E FY2012EFY2012EFY2012EFY2012EFY2012E

Net SalesNet SalesNet SalesNet SalesNet Sales 99999 3333333333 5858585858 7070707070 8686868686

Growth (% yoy) - 273.8 74.4 21.9 21.9

Other Income 6 2 2 3 3

Total Income 14 35 59 73 89

Operating ExpenditureOperating ExpenditureOperating ExpenditureOperating ExpenditureOperating Expenditure 3333333333 6868686868 7777777777 8080808080 8787878787

(% of sales) 377.6 205.9 134.0 113.6 100.9

Operating POperating POperating POperating POperating Profitrofitrofitrofitrofit (25)(25)(25)(25)(25) (35)(35)(35)(35)(35) (20)(20)(20)(20)(20) (10)(10)(10)(10)(10) (1)(1)(1)(1)(1)

OPM % (277.6) (105.9) (34.0) (13.6) (0.9)

Depn. & Amortn. 11 36 36 37 39

(% of sales) 122.5 107.1 61.4 52.5 45.0

PBIT (35) (71) (55) (47) (39)

PBIT % (400.1) (213.1) (95.4) (66.1) (45.8)

Interest 24.9 28.2 12.8 1.0 1.0

PPPPPAAAAATTTTT (55)(55)(55)(55)(55) (97)(97)(97)(97)(97) (66)(66)(66)(66)(66) (45)(45)(45)(45)(45) (37)(37)(37)(37)(37)

Source: Company, Angel Research

June 22, 2010 10

Sun TV Network | Initiating Coverage

Source: Company, Angel Research

Exhibit 17: Kal Radio - Strong Operating Profitability Exhibit 18: SAFM - To remain a drag operationally

Source: Company, Angel Research

6.6

22.0

35.9

43.0

51.6

(7.9)(6.2)

8.2

14.0

19.9

(20.0)

(10.0)

-

10.0

20.0

30.0

40.0

50.0

60.0

FY08 FY09 FY10 FY11E FY12E

Revenue EBITDA

(Rs

cr)

(Rs

cr) 2.3

11.1

22.0

27.5

34.3

(16.7)

(28.9) (27.9)(23.6)

(20.6)

(40.0)

(30.0)

(20.0)

(10.0)

-

10.0

20.0

30.0

40.0

FY08 FY09 FY10 FY11E FY12E

Revenue EBITDA

On a consolidated basis, we expect the company's Radio subsidiaries (Kal and SAFM)

to report top-line CAGR of 22% over FY2010-12E to Rs86cr (Rs58cr) driven by:

1) Red FM, the uniform brand identity of the company's radio channels, will act as an

effective tool for marketing the stations with agencies and customers, and 2) Red FM

has announced an increase in its ad rates by 12-15% effective June 2010.

In terms of Earnings, we expect the Radio business to register significant reduction in

operating losses (EBITDA level) from Rs20cr in FY2010 to near break-even in FY2012E

aided by sharp cost curtailment measures. Moreover, at the PAT level, we expect the

Radio business to reduce its losses to Rs37cr in FY2012E (aided by significant reduction

in interest costs as Loans & Advances to Radio subsidiaries have been reversed), down

from Rs66cr in FY2010, dragging down the consolidated EPS by ~4%.

We peg 22% CAGR in top-line aided by

re-branding of radio stations to Red FM and

Ad-rate hike of 12-15% effective June 2010

At operating level, we expect Radio business

to reach near break-even in FY2012E but

drag consolidated EPS down by ~4%

Kal Radio - Profitable at Operating level, to break-even at PAT in FY12E

During FY2010, Kal Radio (18 radio stations under operation primarily in South India)

clocked 63% yoy growth in top-line to Rs36cr (Rs22cr) aided by addition of new stations

and better inventory utilisation, and achieved operating profit of Rs8.2cr (loss of Rs6.2cr)

as operational cost remained flat. Going forward, we have modeled in 20% CAGR in

top-line (aided largely by rate hikes as incremental gain from new stations getting

added is factored in the base) and expect it to report a turnover of Rs43cr and Rs52cr

in FY2011E and FY2012E, respectively. Operating profit is expected to log in 55%

CAGR over FY2010-12E as we have factored in only a marginal 7-8% yoy increase in

operating expenditure.

SAFM - Operational losses to sustain in near term

In FY2010, SAFM (23 radio stations under operation primarily in Tier-III cities) doubled

its top-line to Rs22cr (Rs11cr) aided by addition of new stations and better inventory

utilisation. However, SAFM registered operating loss of Rs28cr (loss of Rs29cr) due to

25% rise in operational costs. Going forward, we expect SAFM to post revenue CAGR

of 25% over FY2010-12E. However, we do not expect the subsidiary to achieve EBITDA

breakeven by FY2012E, in contrast to management guidance of EBITDA breakeven

by FY2011E, and have modeled in a loss of Rs21cr for FY2012E.

Kal Radio to drive growth at operational

level, while SAFM is unlikely to achieve

EBITDA breakeven by FY2012E

June 22, 2010 11

Sun TV Network | Initiating Coverage

Financial Outlook

Steady Advt., sharp spike in DTH to aid 24% CAGR in top-line

During FY2010-12E, we expect STNL to report a strong consolidated 23.5% CAGR in

revenues driven largely by: 1) 19.5% CAGR in Advertising revenues, 2) 37% CAGR in

Subscription revenues largely led by 58% CAGR in DTH revenues, and 3) sharp spike

in Movie revenues driven by the release of the big budget Endhiran (slated for release

in 2HFY2011E), though mainly captured in FY2011E and tapering off in FY2012E.

(Rs cr)(Rs cr)(Rs cr)(Rs cr)(Rs cr) FY08FY08FY08FY08FY08 FY09FY09FY09FY09FY09 FY10FY10FY10FY10FY10 FY11EFY11EFY11EFY11EFY11E FY12EFY12EFY12EFY12EFY12E #####FY10-12EFY10-12EFY10-12EFY10-12EFY10-12E KKKKKey Growth Driversey Growth Driversey Growth Driversey Growth Driversey Growth Drivers

Advertising RevenueAdvertising RevenueAdvertising RevenueAdvertising RevenueAdvertising Revenue 475 475 475 475 475 606 606 606 606 606 846 846 846 846 846 1,015 1,015 1,015 1,015 1,015 1,208 1,208 1,208 1,208 1,208 19.5 19.5 19.5 19.5 19.5

Growth (% yoy) 30.6 27.4 39.6 20.1 18.9

Broadcasting 467 573 788 945 1,122 19.3 Rate hike absorption, Incremental gains from niche channels

Growth (% yoy) 28.5 22.7 37.6 20.0 18.7 and better inventory utilisation

Radio 9 33 58 70 86 21.9 Higher inventory off-take and recent rate hikes in Red FM

Growth (% yoy) 790.0 272.6 74.4 21.9 21.9 (12-15%)

Broadcast FBroadcast FBroadcast FBroadcast FBroadcast Feeeeeeeeee 126 126 126 126 126 130 130 130 130 130 135 135 135 135 135 142 142 142 142 142 148 148 148 148 148 4.6 4.6 4.6 4.6 4.6 Modeling in conservative growth based on hike in slot rates,

Growth (% yoy) 15.7 3.8 3.4 5.0 4.2 await 1QFY11 results before upgrading

SubscriptionSubscriptionSubscriptionSubscriptionSubscription 268 268 268 268 268 269 269 269 269 269 397 397 397 397 397 640 640 640 640 640 745 745 745 745 745 37.0 37.0 37.0 37.0 37.0

Growth (% yoy) 32.8 0.6 47.4 61.4 16.4

Analogue 219 131 158 212 227 20.1 Distribution re-jig (4QFY10 exhibits traction) and Malayalam

Growth (% yoy) 31.1 (40.2) 20.2 34.5 7.4 channels turning pay (to add Rs20-25cr)

DTH 10 84 183 370 456 57.8 Subscriber addition and revised ARPU (Rs40/month)

Growth (% yoy) - 748.5 117.9 101.9 23.4

Program Licence 38 54 56 59 62 5.0 Renewed focus, distribution tie-ups in UK - modeled a 5%

Growth (% yoy) 12.4 41.2 3.6 5.0 5.0 CAGR significantly lower than Mgmt guidance

MoviesMoviesMoviesMoviesMovies - - - - - 28 28 28 28 28 70 70 70 70 70 175 175 175 175 175 110 110 110 110 110 25.4 25.4 25.4 25.4 25.4 Endhiran release to spike revenues in FY11E, partialy

Growth (% yoy) - - 148.0 150.0 (37.1) spill-over in FY12E

Other SalesOther SalesOther SalesOther SalesOther Sales 1 1 1 1 1 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 3.33.33.33.33.3 Largely Income from content trading and Aircraft charter

Growth (% yoy) - - 0.9 3.2 3.4 services - to remain flat

Net SalesNet SalesNet SalesNet SalesNet Sales 870 870 870 870 870 1,039 1,039 1,039 1,039 1,039 1,453 1,453 1,453 1,453 1,453 1,978 1,978 1,978 1,978 1,978 2,217 2,217 2,217 2,217 2,217 23.523.523.523.523.5

Growth (% yoy) - 19.5 39.8 36.2 12.0

Exhibit 19: Consolidated Top-line Model - 36% yoy in FY2011E and 24% CAGR over FY2010-12E

Source: Company, Angel Research; Note: #denotes CAGR

June 22, 2010 12

Sun TV Network | Initiating Coverage

(Rs cr)(Rs cr)(Rs cr)(Rs cr)(Rs cr) FY08FY08FY08FY08FY08 FY09FY09FY09FY09FY09 FY10FY10FY10FY10FY10 FY11EFY11EFY11EFY11EFY11E FY12EFY12EFY12EFY12EFY12E #####FY10-12EFY10-12EFY10-12EFY10-12EFY10-12E KKKKKey Growth Driversey Growth Driversey Growth Driversey Growth Driversey Growth Drivers

Cost of RevenuesCost of RevenuesCost of RevenuesCost of RevenuesCost of Revenues 77 77 77 77 77 111 111 111 111 111 119 119 119 119 119 138 138 138 138 138 153 153 153 153 153 13.3 13.3 13.3 13.3 13.3 Drop as % of sales as incremental revenue from Ad rate hike

% of Sales 8.8 10.7 8.2 7.0 6.9 and DTH, Model absolute growth of ~13%

Staff CostStaff CostStaff CostStaff CostStaff Cost 96 96 96 96 96 116 116 116 116 116 134 134 134 134 134 201 201 201 201 201 231 231 231 231 231 31.4 31.4 31.4 31.4 31.4 Spike in FY11 as we model higher Pay to MD in FY11-12E

% of Sales 11.0 11.1 9.2 10.1 10.4 and Staff costs for new team set-ups

MD's Pay 65 74 74 125 141 38.1 In FY10, MD's Pay remained at FY09 levels, We model FY11

% of Sales 7.5 7.1 5.1 6.3 6.4 Pay at usual 10% of PBT

Other Staff Costs 26 28 42 56 68 27.9 Modeled in 28% CAGR rise in Staff costs due to new team

% of Sales 3.0 2.7 2.9 2.9 3.1 set-ups in distribution and new channels

Radio Staff Costs 5 13 18 19 21 9.4 To rise moderately at 9% CAGR as all stations are now

% of Radio Sales 51.0 40.7 31.0 27.5 25.0 operational and strong cost focus

SG&A ExpensesSG&A ExpensesSG&A ExpensesSG&A ExpensesSG&A Expenses 41 41 41 41 41 54 54 54 54 54 75 75 75 75 75 107 107 107 107 107 106 106 106 106 106 19.119.119.119.119.1 Modeling in 19% CAGR to support new launches, FY11 to

% of Sales 4.7 5.2 5.2 5.4 4.8 see spike due to Endhiran release

Other ExpensesOther ExpensesOther ExpensesOther ExpensesOther Expenses 59 59 59 59 59 22 22 22 22 22 34 34 34 34 34 35 35 35 35 35 40 40 40 40 40 8.48.48.48.48.4 To register significant moderation due to lower losses in Radio

% of Sales 6.8 2.1 2.3 1.8 1.8

EBITDEBITDEBITDEBITDEBITDAAAAA 597 597 597 597 597 737 737 737 737 737 1,091 1,091 1,091 1,091 1,091 1,497 1,497 1,497 1,497 1,497 1,686 1,686 1,686 1,686 1,686 24.3 24.3 24.3 24.3 24.3

EBITDA Margin (%) 68.7 70.9 75.1 75.7 76.1

AmortisationAmortisationAmortisationAmortisationAmortisation 86 86 86 86 86 153 153 153 153 153 233 233 233 233 233 326 326 326 326 326 347 347 347 347 347 22.122.122.122.122.1 Spike in FY11E due to release of Endhiran, to moderate in

% of Intangible Assets 15.9 20.8 23.6 26.7 24.3 FY12E

Core EBITCore EBITCore EBITCore EBITCore EBIT 511 511 511 511 511 583 583 583 583 583 858 858 858 858 858 1,171 1,171 1,171 1,171 1,171 1,339 1,339 1,339 1,339 1,339 24.9 24.9 24.9 24.9 24.9 Core EBIT Margins to expand 130bp due to lower losses in

Core EBIT Margin (%) 58.8 56.1 59.1 59.2 60.4 Radio and higher operating leverage

Reported PReported PReported PReported PReported PAAAAAT (After MI)T (After MI)T (After MI)T (After MI)T (After MI) 327 327 327 327 327 368 368 368 368 368 520 520 520 520 520 712 712 712 712 712 816 816 816 816 816 25.3 25.3 25.3 25.3 25.3

PAT Margin (%) 37.6 35.4 35.8 36.0 36.8

Exhibit 20:Cost and Earnings Breakup - Expect Margins to remain stable in FY11E before expansion in FY12E

Source: Company, Angel Research; Note: #denotes CAGR

Margins to sustain, we peg consolidated Earnings CAGR at 25%

During FY2010-12E, we expect EBITDA Margins to hover between 75-76% levels

aided by significant reduction in Radio losses (to achieve near break-even in FY2012E

at operational level) and higher operating leverage (as majority of incremental

top-line growth will be driven by ad rate hike and higher subscription revenues).

However, higher SG&A expenses (Endhiran release in FY2011E) and spike in MD's

pay (low base) to the usual 10% of PBT is likely to restrict Margin expansion.

In terms of core EBIT margins (including amortisation costs for films and distribution

rights), we expect STNL to sustain margins at ~59% in FY2011E, before expanding by

130bp yoy in FY2012E due to higher amortisation charges on the back of release of

Endhiran in FY2011E.

On a consolidated basis, we expect STNL's earnings to register 25.3% CAGR over

FY2010-12E driven largely by strong top-line growth and stable Margins.

June 22, 2010 13

Sun TV Network | Initiating Coverage

Source: Company, Angel Research

Exhibit 21: FCF to triple boosting cash balance Exhibit 22: RoE to sustain, RoIC to rise to 47%

Source: Company, Angel Research

(Rs

cr)

(38)

110

202

463

721

430365

435

581

1,036

(200)

-

200

400

600

800

1,000

1,200

FY08 FY09 FY10 FY11E FY12E

Free Cash Flow Cash Balance

2422

28

33

31

36

27

36

4547

-

5

10

15

20

25

30

35

40

45

50

FY08 FY09 FY10 FY11E FY12E

RoE RoIC

(%)

Debt-free Balance Sheet, Cash to swell to ~Rs10bn in FY2012E

STNL has a strong zero debt balance sheet and cash balance of ~Rs435cr as on

FY2010. Moreover, despite modeling heavy capex (including movie acquisition costs)

in the range of Rs420-440cr for FY2011-12E (in line with management guidance), we

expect STNL's cash balance to swell to a whopping Rs10bn or ~Rs33/share in FY2012E

accounting for almost 34% of capital employed. We attribute the jump in cash balance

to strong rise in free cash flow (almost tripling over FY2010-12E) on strong earnings

growth. As result, we expect STNL's RoE to sustain at 28-31% levels and RoIC to rise to

47% (36% in FY2010).

June 22, 2010 14

Sun TV Network | Initiating Coverage

Key Concerns

Delay/difficulty in absorption of rate hikes: Delay/difficulty in absorption of rate hikes: Delay/difficulty in absorption of rate hikes: Delay/difficulty in absorption of rate hikes: Delay/difficulty in absorption of rate hikes: We have modeled in a steady 19.3%

CAGR in STNL's standalone advertising revenues over FY2010-12E aided by absorption

of rate hikes (9-33% hike in ad rates in Tamil channels and 5-16% in other channels

effective Jan 2010). Any delay/difficulty to pass the same to advertisers on account of

competitive pressures, slowdown in GDP or other unforeseen factors would entail

downside risks to our estimates.

FFFFFall in DTH ARPUs beyond Rs35-40/month:all in DTH ARPUs beyond Rs35-40/month:all in DTH ARPUs beyond Rs35-40/month:all in DTH ARPUs beyond Rs35-40/month:all in DTH ARPUs beyond Rs35-40/month: During 4QFY2010, the company

reported a subscriber base of 6mn and a sharp uptick in DTH realisations to

Rs35-36/month (Rs26-27/month) on account of 5 new niche channels turning pay

(new channel bouquet available at Rs52/month). Hence, we have modeled in 58%

CAGR in DTH Subscription revenues over FY2010-12E, driven by - 1) growth of 33%

and 23% for FY2011-12E in the Subscriber base to 7.7mn and 9.5mn respectively,

2) significant 52% yoy increase in ARPU to Rs40/month (Rs26/month) in FY2011E.

Hence, non-confirmation of 4QFY2010 ARPU trend carries significant downside risks

to our estimates.

Delay/failure of big budget Delay/failure of big budget Delay/failure of big budget Delay/failure of big budget Delay/failure of big budget EndhiranEndhiranEndhiranEndhiranEndhiran::::: STNL is slated to release its first big budget

movie, Endhiran (estimated budget of Rs100cr+), starring the southern superstar

Rajnikant and Bollywood's Aishwarya Rai. For FY2011E, we estimate revenues from

movie distribution (including release of Endhiran) to increase 150% yoy to Rs175cr

(Rs70cr) with Endhiran expected to register 20-25% returns at the EBIT level. Any

delays in the release of movie or the movie tanking at the box office would dent our

revenue and earnings estimates.

June 22, 2010 15

Sun TV Network | Initiating Coverage

Exhibit 24: Sun TV Business Model - Spans Broadcasting, Radio and Movies

59.2%

Subsidiary

97.8%

SubsidiaryDivision of

STNL

Sun TV Network20 television channels across 4 southern states & 3 FM radio stations

South Asia FM Kal RadioSun Pictures

23 licenses focusedon northern, eastern

& western region

Production/distribution of movies insouthern region

18 licenses focusedon Southern cities

49% beneficialinterest

Strategic Alliancewith RED FM

3 radio stations in Mumbai,Delhi and Kolkatta

Source: Company, Angel Research

Exhibit 23: STNL operates 20 channels in 4 Southern marketsChannelsChannelsChannelsChannelsChannels TTTTTamilamilamilamilamil TTTTTelegueleguelegueleguelegu KKKKKannadaannadaannadaannadaannada MalyalamMalyalamMalyalamMalyalamMalyalam

GEC Sun TV Gemini TV Udaya TV Surya TV

News Sun News Gemini News Udaya Varthegalu

Movies K TV Teja TV Udaya Movies Kiran TV

Music Sun Music Gemini Music Udaya TV 2

Kids Chutti TV Khushi TV Chintu TV

Comedy Adithya TV Navvulu TV Ushe TVSource: Company, Angel Research

Company Background

Headquartered in Chennai, STNL was incorporated in December 1985 and listed in

April 2006. STNL, promoted by Kalanithi Maran, belongs to the Sun Network Group,

which is straddled across the media value chain, viz. Broadcasting, Radio, Films, Cable

distribution, DTH and Print Media. STNL is India's leading media conglomerate with

20 TV channels with a significant presence in the south (leader in three of the four

southern states - operates in Tamil Nadu, Andhra Pradesh and Karnataka).

Beyond television broadcasting, the company has a strong presence in radio

broadcasting (has a total of 44 FM licences) via its two subsidiaries - Kal FM (98%

stake) and SAFM (59% stake) and strategic tie-up with Red FM. Moreover, STNL entered

the movie business in September 2008 through its subsidiary, Sun Pictures and has so

far distributed 12-15 films. The company is also slated to release its first in-house

production, Endhiran during 2HFY2011.

June 22, 2010 16

Sun TV Network | Initiating Coverage

Unique low-cost business model keeps cost off STNL's books

STNL operates on "Sponsored Revenue model", wherein it leases out its time slots to

third party content producers for a fixed fee (termed as broadcast fee in P&L). In

return, the content producers have the right to about 4mins of advertising inventory

per half an hour, while STNL gets 2mins of this half an hour slot. Since the content

aired on STNL channels are not owned by STNL, the cost of content and the risks of

recouping the cost lie with the producer.

Moreover, the company also produces a large amount of content aired in the

non-prime time slots in-house, which furthers lowers its production costs. The company's

in-house production team sources around 75% of its daily content requirement

in-house, out of which 40-45% is movie based, 8-10% is news and the rest is accounted

by game, talk and variety shows. Further, the company has exclusive contracts with

artistes and anchors as part of its talent retention strategy.

STNL leads movie broadcasting via its largest movie library

STNL has a strong movie library comprising more than 8,500 titles, with rights across

all the four major South Indian languages. Apart from having an extensive movie

library, STNL purchases around 90% of all movie releases in these languages. The

company employs various strategies such as airing free trailers of movies prior to

release, through its wide range of channels. Consequently, the producer contracts

satellite rights to STNL at lower rates, resulting in lower acquisition costs for the company.

Usually, Sun pays Rs1-1.5cr for acquiring satellite rights and recovers the same in the

first two runs of the movie. In the southern market, screening of movies on satellite

channels is allowed only after 1-3 years of the theatrical release. Movies and

movie-related content attracts significant viewership in down south. As a result, STNL

earns around 25% of its advertising revenues from movies aired on dedicated channels

in each market.

Foray into niche channels like Kids and Comedy genre

Apart from the various GEC channels, STNL also broadcasts dedicated movie channels,

kids and infotainment channels and comedy channels (refer Exhibit 23). Foray into

these niche categories and entertaining selective TV viewers was a bold move.

Nonetheless, the move has paid well for the company - Chutti TV, the Tamil children

entertainment channel has ~5% market share and contributes ~3% to Sun's revenues.

For its kid's channels, Sun has exclusive tie ups with the content providers (tied up with

Disney India in December 2009 and DQ Entertainment in June 2010), wherein Sun

buys exclusive rights to cartoons and then dubs them in four languages. Operating

costs involved are confined to dubbing costs. This scale and low-cost model ensures

that these niche channels do not cause any significant margin dilution. STNL's comedy

channels also work on a similar low-cost model wherein clips from the movies in Sun's

library are telecast, keeping production costs minimal.

June 22, 2010 17

Sun TV Network | Initiating Coverage

Profit & Loss Statement (Consolidated) Rs croreY/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr) FY2008FY2008FY2008FY2008FY2008 FY2009FY2009FY2009FY2009FY2009 FY2010EFY2010EFY2010EFY2010EFY2010E FY2011EFY2011EFY2011EFY2011EFY2011E FY2012EFY2012EFY2012EFY2012EFY2012E

Gross sales 870 1,039 1,453 1,978 2,217

Less: Excise duty - - - - -

Net Sales 870 1,039 1,453 1,978 2,217

TTTTTotal operating incomeotal operating incomeotal operating incomeotal operating incomeotal operating income 870 870 870 870 870 1,039 1,039 1,039 1,039 1,039 1,453 1,453 1,453 1,453 1,453 1,978 1,978 1,978 1,978 1,978 2,217 2,217 2,217 2,217 2,217

% chg 28.3 19.5 39.8 36.2 12.0

TTTTTotal Expenditureotal Expenditureotal Expenditureotal Expenditureotal Expenditure 272 272 272 272 272 303 303 303 303 303 362 362 362 362 362 481 481 481 481 481 530 530 530 530 530

(Increase)/ Decrease in stock in trade - - 4 - -

Cost of Production 77 111 119 138 153

Staff Costs 96 116 134 201 231

Power & Fuel 7 14 19 23 25

Other Expenses 93 62 86 120 121

EBITDEBITDEBITDEBITDEBITDAAAAA 598 598 598 598 598 737 737 737 737 737 1,091 1,091 1,091 1,091 1,091 1,497 1,497 1,497 1,497 1,497 1,686 1,686 1,686 1,686 1,686

% chg 27.5 23.3 48.1 37.2 12.6

(% of Net Sales) 68.7 70.9 75.1 75.7 76.1

Depreciation & Amortisation 124 220 321 432 467

EBITEBITEBITEBITEBIT 474 474 474 474 474 516 516 516 516 516 770 770 770 770 770 1,065 1,065 1,065 1,065 1,065 1,219 1,219 1,219 1,219 1,219

% chg 34.4 9.0 49.1 38.3 14.5

(% of Net Sales) 54.4 49.7 53.0 53.8 55.0

Interest & other Charges 16 14 5 4 4

Other Income 56 67 35 30 33

(% of PBT) 10.8 11.7 4.4 2.7 2.7

Share in profit of Associates - - - - -

Recurring PBTRecurring PBTRecurring PBTRecurring PBTRecurring PBT 513 513 513 513 513 569 569 569 569 569 800 800 800 800 800 1,090 1,090 1,090 1,090 1,090 1,248 1,248 1,248 1,248 1,248

% chg 32.6 10.9 40.5 36.3 14.5

Prior Period & Extr. Exp./(Inc.) - - - - -

PBT (Reported)PBT (Reported)PBT (Reported)PBT (Reported)PBT (Reported) 513 513 513 513 513 569 569 569 569 569 800 800 800 800 800 1,090 1,090 1,090 1,090 1,090 1,248 1,248 1,248 1,248 1,248

Tax 201 229 299 392 444

(% of PBT) 39.2 40.3 37.4 35.9 35.5

PPPPPAAAAAT (Reported)T (Reported)T (Reported)T (Reported)T (Reported) 312 312 312 312 312 340 340 340 340 340 501 501 501 501 501 699 699 699 699 699 805 805 805 805 805

Add: Share of earnings of associate 1.1 0.2 0.8 1.0 1.2

Less: Minority interest (MI) (14) (28) (18) (12) (10)

PPPPPAAAAAT after MI (Reported)T after MI (Reported)T after MI (Reported)T after MI (Reported)T after MI (Reported) 327 327 327 327 327 368 368 368 368 368 520 520 520 520 520 712 712 712 712 712 816 816 816 816 816

ADJADJADJADJADJ. P. P. P. P. PAAAAATTTTT 327 327 327 327 327 368 368 368 368 368 520 520 520 520 520 712 712 712 712 712 816 816 816 816 816

% chg 32.8 12.7 41.2 36.9 14.6

(% of Net Sales) 37.6 35.4 35.8 36.0 36.8

Basic EPS (Rs)Basic EPS (Rs)Basic EPS (Rs)Basic EPS (Rs)Basic EPS (Rs) 8.3 8.3 8.3 8.3 8.3 9.3 9.3 9.3 9.3 9.3 13.2 13.2 13.2 13.2 13.2 18.1 18.1 18.1 18.1 18.1 20.7 20.7 20.7 20.7 20.7

FFFFFully Diluted EPS (Rs)ully Diluted EPS (Rs)ully Diluted EPS (Rs)ully Diluted EPS (Rs)ully Diluted EPS (Rs) 8.3 8.3 8.3 8.3 8.3 9.3 9.3 9.3 9.3 9.3 13.2 13.2 13.2 13.2 13.2 18.1 18.1 18.1 18.1 18.1 20.7 20.7 20.7 20.7 20.7

% chg 32.8 12.7 41.2 36.9 14.6

June 22, 2010 18

Sun TV Network | Initiating Coverage

Balance Sheet (Consolidated) Rs croreY/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr) FY2008FY2008FY2008FY2008FY2008 FY2009FY2009FY2009FY2009FY2009 FY2010EFY2010EFY2010EFY2010EFY2010E FY2011EFY2011EFY2011EFY2011EFY2011E FY2012EFY2012EFY2012EFY2012EFY2012E

Equity Share Capital 197 197 197 197 197

Preference Capital - - 88 88 88

Reserves& Surplus 1,252 1,505 1,679 2,160 2,711

Shareholders FShareholders FShareholders FShareholders FShareholders Fundsundsundsundsunds 1,449 1,449 1,449 1,449 1,449 1,702 1,702 1,702 1,702 1,702 1,964 1,964 1,964 1,964 1,964 2,445 2,445 2,445 2,445 2,445 2,996 2,996 2,996 2,996 2,996

Minority Interest 60 38 37 37 37

Total Loans 69 72 0 0 0

Deferred Tax Liability 1 26 34 34 34

TTTTTotal Liabilitiesotal Liabilitiesotal Liabilitiesotal Liabilitiesotal Liabilities 1,580 1,580 1,580 1,580 1,580 1,838 1,838 1,838 1,838 1,838 2,035 2,035 2,035 2,035 2,035 2,516 2,516 2,516 2,516 2,516 3,067 3,067 3,067 3,067 3,067

APPLICAAPPLICAAPPLICAAPPLICAAPPLICATION OF FUNDSTION OF FUNDSTION OF FUNDSTION OF FUNDSTION OF FUNDS

Gross Block 1,019 1,491 1,889 2,383 2,788

Less: Acc. Depreciation 474 677 998 1,430 1,897

Net BlockNet BlockNet BlockNet BlockNet Block 545 545 545 545 545 815 815 815 815 815 892 892 892 892 892 954 954 954 954 954 891 891 891 891 891

Capital Work-in-Progress 222 157 315 262 279

Goodwill - - - - -

InvestmentsInvestmentsInvestmentsInvestmentsInvestments 180 180 180 180 180 181 181 181 181 181 228 228 228 228 228 278 278 278 278 278 378 378 378 378 378

Non Current AssetsNon Current AssetsNon Current AssetsNon Current AssetsNon Current Assets 8 8 8 8 8 23 23 23 23 23 30 30 30 30 30 45 45 45 45 45 55 55 55 55 55

Current Assets 880 896 1,031 1,353 1,895

Cash 430 365 435 581 1,036

Loans & Advances 192 286 267 336 377

Other 258 245 330 435 482

Current liabilities 256 234 461 376 431

Net Current AssetsNet Current AssetsNet Current AssetsNet Current AssetsNet Current Assets 624 624 624 624 624 662 662 662 662 662 570 570 570 570 570 977 977 977 977 977 1,463 1,463 1,463 1,463 1,463

Mis. Exp. not written off 0 0 0 0 0

TTTTTotal Assetsotal Assetsotal Assetsotal Assetsotal Assets 1,580 1,580 1,580 1,580 1,580 1,838 1,838 1,838 1,838 1,838 2,035 2,035 2,035 2,035 2,035 2,516 2,516 2,516 2,516 2,516 3,067 3,067 3,067 3,067 3,067

June 22, 2010 19

Sun TV Network | Initiating Coverage

Cash Flow Statement (Consolidated) Rs croreY/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr) FY2008FY2008FY2008FY2008FY2008 FY2009FY2009FY2009FY2009FY2009 FY2010EFY2010EFY2010EFY2010EFY2010E FY2011EFY2011EFY2011EFY2011EFY2011E FY2012EFY2012EFY2012EFY2012EFY2012E

Profit before tax 513 569 800 1,090 1,248

Depreciation 124 220 321 432 467

Change in Working Capital (93) 41 (54) (109) (41)

Interest / Dividend (Net) (32) (26) (31) (24) (28)

Direct taxes paid 213 202 299 392 444

Others 54 1 21 (93) (61)

Cash Flow from OperationsCash Flow from OperationsCash Flow from OperationsCash Flow from OperationsCash Flow from Operations 354 354 354 354 354 604 604 604 604 604 757 757 757 757 757 905 905 905 905 905 1,142 1,142 1,142 1,142 1,142

(Inc.)/ Dec. in Fixed Assets (392) (494) (556) (441) (422)

(Inc.)/ Dec. in Investments (180) (0) (47) (50) (100)

Cash Flow from InvestingCash Flow from InvestingCash Flow from InvestingCash Flow from InvestingCash Flow from Investing (572) (572) (572) (572) (572) (494) (494) (494) (494) (494) (603) (603) (603) (603) (603) (491) (491) (491) (491) (491) (522) (522) (522) (522) (522)

Issue of Equity 76 6 67 12 10

Inc./(Dec.) in loans (49) (4) (73) (4) (3)

Dividend Paid (Incl. Tax) (46) (184) (105) (296) (197)

Interest / Dividend (Net) 17 8 26 20 24

Cash Flow from FCash Flow from FCash Flow from FCash Flow from FCash Flow from Financinginancinginancinginancinginancing (1) (1) (1) (1) (1) (174) (174) (174) (174) (174) (85) (85) (85) (85) (85) (267) (267) (267) (267) (267) (166) (166) (166) (166) (166)

Inc./(Dec.) in Cash (220) (64) 70 146 454

Opening Cash balancesOpening Cash balancesOpening Cash balancesOpening Cash balancesOpening Cash balances 649 649 649 649 649 430 430 430 430 430 365 365 365 365 365 435 435 435 435 435 581 581 581 581 581

Closing Cash balancesClosing Cash balancesClosing Cash balancesClosing Cash balancesClosing Cash balances 430 430 430 430 430 365 365 365 365 365 435 435 435 435 435 581 581 581 581 581 1,036 1,036 1,036 1,036 1,036

June 22, 2010 20

Sun TV Network | Initiating Coverage

Key RatiosY/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr)Y/E March (Rs cr) FY2008FY2008FY2008FY2008FY2008 FY2009FY2009FY2009FY2009FY2009 FY2010EFY2010EFY2010EFY2010EFY2010E FY2011EFY2011EFY2011EFY2011EFY2011E FY2012EFY2012EFY2012EFY2012EFY2012E

VVVVValuation Ratio (x)aluation Ratio (x)aluation Ratio (x)aluation Ratio (x)aluation Ratio (x)

P/E (on FDEPS) 48.5 43.0 30.5 22.3 19.4

P/CEPS 45.3 38.9 26.9 19.7 17.1

P/BV 10.9 9.3 8.4 6.7 5.4

Dividend yield (%) 0.6 0.6 1.9 1.2 1.4

EV/Sales 14.3 12.0 8.6 6.3 5.6

EV/EBITDA 20.8 16.9 11.4 8.3 7.4

EV / Total Assets 7.9 6.8 6.1 4.9 4.1

PPPPPer Share Data (Rs)er Share Data (Rs)er Share Data (Rs)er Share Data (Rs)er Share Data (Rs)

EPS (Basic) 8.3 9.3 13.2 18.1 20.7

EPS (fully diluted) 8.3 9.3 13.2 18.1 20.7

Cash EPS 8.9 10.3 14.9 20.4 23.5

DPS 2.5 2.5 7.5 5.0 5.8

Book Value 36.8 43.2 47.6 59.8 73.8

Dupont AnalysisDupont AnalysisDupont AnalysisDupont AnalysisDupont Analysis

EBIT margin 54.4 49.7 53.0 53.8 55.0

Tax retention ratio 0.6 0.6 0.6 0.6 0.6

Asset turnover (x) 1.1 0.9 1.1 1.3 1.3

RoIC (Post-tax) 36.0 27.3 36.2 45.1 47.5

Cost of Debt (Post Tax) 0.1 0.1 0.1 18.2 18.5

Leverage (x) 0.8 0.4 0.2 0.0 0.0

Operating RoE 63.7 33.3 33.7 32.0 30.4

Returns (%)Returns (%)Returns (%)Returns (%)Returns (%)

RoCE (Pre-tax) 33.1 30.2 39.8 46.8 43.7

Angel RoIC (Pre-tax) 59.2 45.7 57.8 70.3 73.6

RoE 23.6 21.6 28.0 33.0 30.6

TTTTTurnover ratios (x)urnover ratios (x)urnover ratios (x)urnover ratios (x)urnover ratios (x)

Asset Turnover (Gross Block) 0.9 0.7 0.8 0.8 0.8

Inventory / Sales (days) 0 0 0 0 0

Receivables (days) 108 86 83 80 79

Payables (days) 15 17 12 12 11

Working capital cycle (ex-cash) (days) 81 104 34 73 70

Solvency ratios (x)Solvency ratios (x)Solvency ratios (x)Solvency ratios (x)Solvency ratios (x)

Net debt to equity 0.4 0.4 0.0 0.0 0.0

Net debt to EBITDA 0.1 0.1 0.0 0.0 0.0

Interest Coverage (EBIT / Interest) 29.8 37.4 155.9 266.2 304.7

Sun TV Network

Disclaimer

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investmentdecision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should makesuch investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companiesreferred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits andrisks of such an investment.

Angel Securities Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investmentdecisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document arethose of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and tradingvolume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sourcesbelieved to be true, and is for general guidance only. Angel Securities Limited has not independently verified all the information containedwithin this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contentsor data contained within this document. While Angel Securities Limited endeavours to update on a reasonable basis the informationdiscussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributedor passed on, directly or indirectly.

Angel Securities Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or otheradvisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Securities Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or inconnection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)Reduce (-5% to -15%) Sell (< -15%)

Ratings (Returns) :

Disclosure of Interest StatementDisclosure of Interest StatementDisclosure of Interest StatementDisclosure of Interest StatementDisclosure of Interest Statement Sun TV NetworksSun TV NetworksSun TV NetworksSun TV NetworksSun TV Networks

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Sun TV Netwrok

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE: INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

Research Team

Fundamental:

Sarabjit Kour Nangra VP-Research, Pharmaceutical [email protected]

Vaibhav Agrawal VP-Research, Banking [email protected]

Vaishali Jajoo Automobile [email protected]

Shailesh Kanani Infrastructure, Real Estate [email protected]

Anand Shah FMCG , Media [email protected]

Deepak Pareek Oil & Gas [email protected]

Puneet Bambha Capital Goods, Engineering [email protected]

Sushant Dalmia Pharmaceutical [email protected]

Rupesh Sankhe Cement, Power [email protected]

Param Desai Real Estate, Logistics, Shipping [email protected]

Sageraj Bariya Fertiliser, Mid-cap [email protected]

Viraj Nadkarni Retail, Hotels, Mid-cap [email protected]

Paresh Jain Metals & Mining [email protected]

Amit Rane Banking [email protected]

Rahul Jain IT, Telecom [email protected]

Jai Sharda Mid-cap [email protected]

Sharan Lillaney Mid-cap [email protected]

Amit Vora Research Associate (Oil & Gas) [email protected]

V Srinivasan Research Associate (Cement, Power) [email protected]

Aniruddha Mate Research Associate (Infra, Real Estate) [email protected]

Mihir Salot Research Associate (Logistics, Shipping) [email protected]

Chitrangda Kapur Research Associate (FMCG, Media) [email protected]

Vibha Salvi Research Associate (IT, Telecom) [email protected]

Pooja Jain Research Associate (Metals & Mining) [email protected]

Technicals:

Shardul Kulkarni Sr. Technical Analyst [email protected]

Mileen Vasudeo Technical Analyst [email protected]

Derivatives:

Siddarth Bhamre Head - Derivatives [email protected]

Jaya Agarwal Derivative Analyst [email protected]

Institutional Sales Team:

Mayuresh Joshi VP - Institutional Sales [email protected]

Abhimanyu Sofat AVP - Institutional Sales [email protected]

Nitesh Jalan Sr. Manager [email protected]

Pranav Modi Sr. Manager [email protected]

Sandeep Jangir Sr. Manager [email protected]

Ganesh Iyer Sr. Manager [email protected]

Jay Harsora Sr. Dealer [email protected]

Meenakshi Chavan Dealer [email protected]

Gaurang Tisani Dealer [email protected]

Production Team:

Bharathi Shetty Research Editor [email protected]

Bharat Patil Production [email protected]

Dilip Patel Production [email protected]