initiating coverage karur vysya bank ltd. tiating coverage ... vysya bank - initiating... · p a g...

TRANSCRIPT

1 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

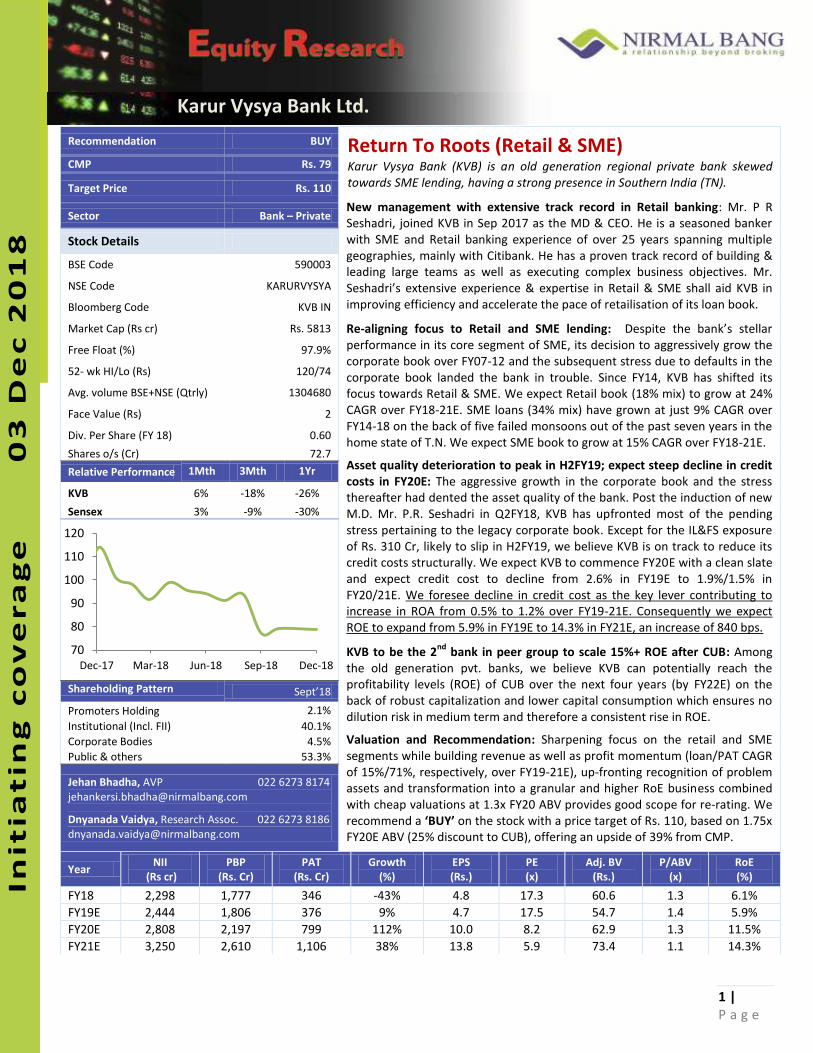

Recommendation BUY

Return To Roots (Retail & SME) Karur Vysya Bank (KVB) is an old generation regional private bank skewed

towards SME lending, having a strong presence in Southern India (TN).

New management with extensive track record in Retail banking: Mr. P R

Seshadri, joined KVB in Sep 2017 as the MD & CEO. He is a seasoned banker

with SME and Retail banking experience of over 25 years spanning multiple

geographies, mainly with Citibank. He has a proven track record of building &

leading large teams as well as executing complex business objectives. Mr.

Seshad i s e te si e e pe ie e & expertise in Retail & SME shall aid KVB in

improving efficiency and accelerate the pace of retailisation of its loan book.

Re-aligning focus to Retail and SME lending: Despite the a k s stella performance in its core segment of SME, its decision to aggressively grow the

corporate book over FY07-12 and the subsequent stress due to defaults in the

corporate book landed the bank in trouble. Since FY14, KVB has shifted its

focus towards Retail & SME. We expect Retail book (18% mix) to grow at 24%

CAGR over FY18-21E. SME loans (34% mix) have grown at just 9% CAGR over

FY14-18 on the back of five failed monsoons out of the past seven years in the

home state of T.N. We expect SME book to grow at 15% CAGR over FY18-21E.

Asset quality deterioration to peak in H2FY19; expect steep decline in credit

costs in FY20E: The aggressive growth in the corporate book and the stress

thereafter had dented the asset quality of the bank. Post the induction of new

M.D. Mr. P.R. Seshadri in Q2FY18, KVB has upfronted most of the pending

stress pertaining to the legacy corporate book. Except for the IL&FS exposure

of Rs. 310 Cr, likely to slip in H2FY19, we believe KVB is on track to reduce its

credit costs structurally. We expect KVB to commence FY20E with a clean slate

and expect credit cost to decline from 2.6% in FY19E to 1.9%/1.5% in

FY20/21E. We foresee decline in credit cost as the key lever contributing to

increase in ROA from 0.5% to 1.2% over FY19-21E. Consequently we expect

ROE to expand from 5.9% in FY19E to 14.3% in FY21E, an increase of 840 bps.

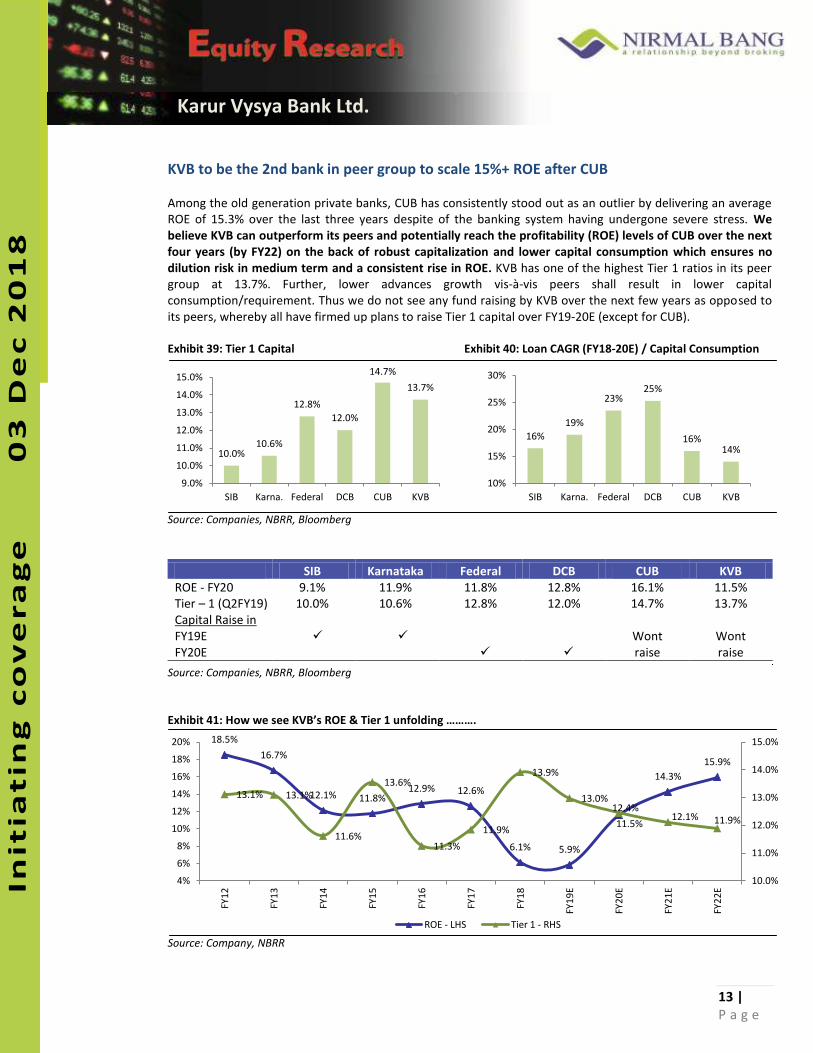

KVB to be the 2nd

bank in peer group to scale 15%+ ROE after CUB: Among

the old generation pvt. banks, we believe KVB can potentially reach the

profitability levels (ROE) of CUB over the next four years (by FY22E) on the

back of robust capitalization and lower capital consumption which ensures no

dilution risk in medium term and therefore a consistent rise in ROE.

Valuation and Recommendation: Sharpening focus on the retail and SME

segments while building revenue as well as profit momentum (loan/PAT CAGR

of 15%/71%, respectively, over FY19-21E), up-fronting recognition of problem

assets and transformation into a granular and higher RoE business combined

with cheap valuations at 1.3x FY20 ABV provides good scope for re-rating. We

recommend a BUY on the stock with a price target of Rs. 110, based on 1.75x

FY20E ABV (25% discount to CUB), offering an upside of 39% from CMP.

CMP Rs. 79

Target Price Rs. 110

Sector Bank – Private

Stock Details

BSE Code 590003

NSE Code KARURVYSYA

Bloomberg Code KVB IN

Market Cap (Rs cr) Rs. 5813

Free Float (%) 97.9%

52- wk HI/Lo (Rs) 120/74

Avg. volume BSE+NSE (Qtrly) 1304680

Face Value (Rs) 2

Div. Per Share (FY 18) 0.60

Shares o/s (Cr) 72.7

Relative Performance 1Mth 3Mth 1Yr

KVB 6% -18% -26%

Sensex 3% -9% -30%

Shareholding Pattern “ept 8

Promoters Holding 2.1%

Institutional (Incl. FII) 40.1%

Corporate Bodies 4.5%

Public & others 53.3%

Jehan Bhadha, AVP 022 6273 8174

Dnyanada Vaidya, Research Assoc. 022 6273 8186

Year NII

(Rs cr)

PBP

(Rs. Cr)

PAT

(Rs. Cr)

Growth

(%)

EPS

(Rs.)

PE

(x)

Adj. BV

(Rs.)

P/ABV

(x)

RoE

(%)

FY18 2,298 1,777 346 -43% 4.8 17.3 60.6 1.3 6.1%

FY19E 2,444 1,806 376 9% 4.7 17.5 54.7 1.4 5.9%

FY20E 2,808 2,197 799 112% 10.0 8.2 62.9 1.3 11.5%

FY21E 3,250 2,610 1,106 38% 13.8 5.9 73.4 1.1 14.3%

70

80

90

100

110

120

Dec-17 Mar-18 Jun-18 Sep-18 Dec-18

2 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

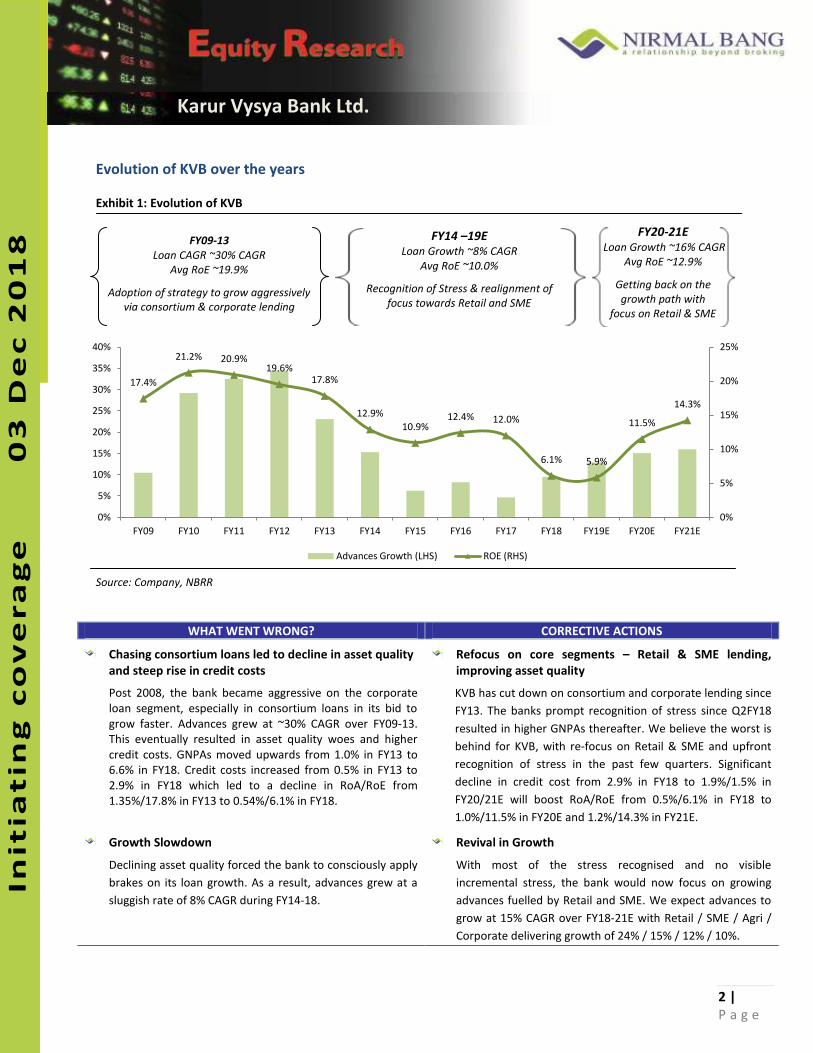

Evolution of KVB over the years

Exhibit 1: Evolution of KVB

Source: Company, NBRR

WHAT WENT WRONG? CORRECTIVE ACTIONS

Chasing consortium loans led to decline in asset quality

and steep rise in credit costs

Post 2008, the bank became aggressive on the corporate

loan segment, especially in consortium loans in its bid to

grow faster. Advances grew at ~30% CAGR over FY09-13.

This eventually resulted in asset quality woes and higher

credit costs. GNPAs moved upwards from 1.0% in FY13 to

6.6% in FY18. Credit costs increased from 0.5% in FY13 to

2.9% in FY18 which led to a decline in RoA/RoE from

1.35%/17.8% in FY13 to 0.54%/6.1% in FY18.

Refocus on core segments – Retail & SME lending,

improving asset quality

KVB has cut down on consortium and corporate lending since

FY13. The banks prompt recognition of stress since Q2FY18

resulted in higher GNPAs thereafter. We believe the worst is

behind for KVB, with re-focus on Retail & SME and upfront

recognition of stress in the past few quarters. Significant

decline in credit cost from 2.9% in FY18 to 1.9%/1.5% in

FY20/21E will boost RoA/RoE from 0.5%/6.1% in FY18 to

1.0%/11.5% in FY20E and 1.2%/14.3% in FY21E.

Growth Slowdown

Declining asset quality forced the bank to consciously apply

brakes on its loan growth. As a result, advances grew at a

sluggish rate of 8% CAGR during FY14-18.

Revival in Growth

With most of the stress recognised and no visible

incremental stress, the bank would now focus on growing

advances fuelled by Retail and SME. We expect advances to

grow at 15% CAGR over FY18-21E with Retail / SME / Agri /

Corporate delivering growth of 24% / 15% / 12% / 10%.

17.4%

21.2% 20.9% 19.6%

17.8%

12.9%

10.9% 12.4% 12.0%

6.1% 5.9%

11.5%

14.3%

0%

5%

10%

15%

20%

25%

0%

5%

10%

15%

20%

25%

30%

35%

40%

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Advances Growth (LHS) ROE (RHS)

FY09-13

Loan CAGR ~30% CAGR

Avg RoE ~19.9%

Adoption of strategy to grow aggressively

via consortium & corporate lending

FY14 –19E

Loan Growth ~8% CAGR

Avg RoE ~10.0%

Recognition of Stress & realignment of

focus towards Retail and SME

FY20-21E

Loan Growth ~16% CAGR

Avg RoE ~12.9%

Getting back on the

growth path with

focus on Retail & SME

3 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

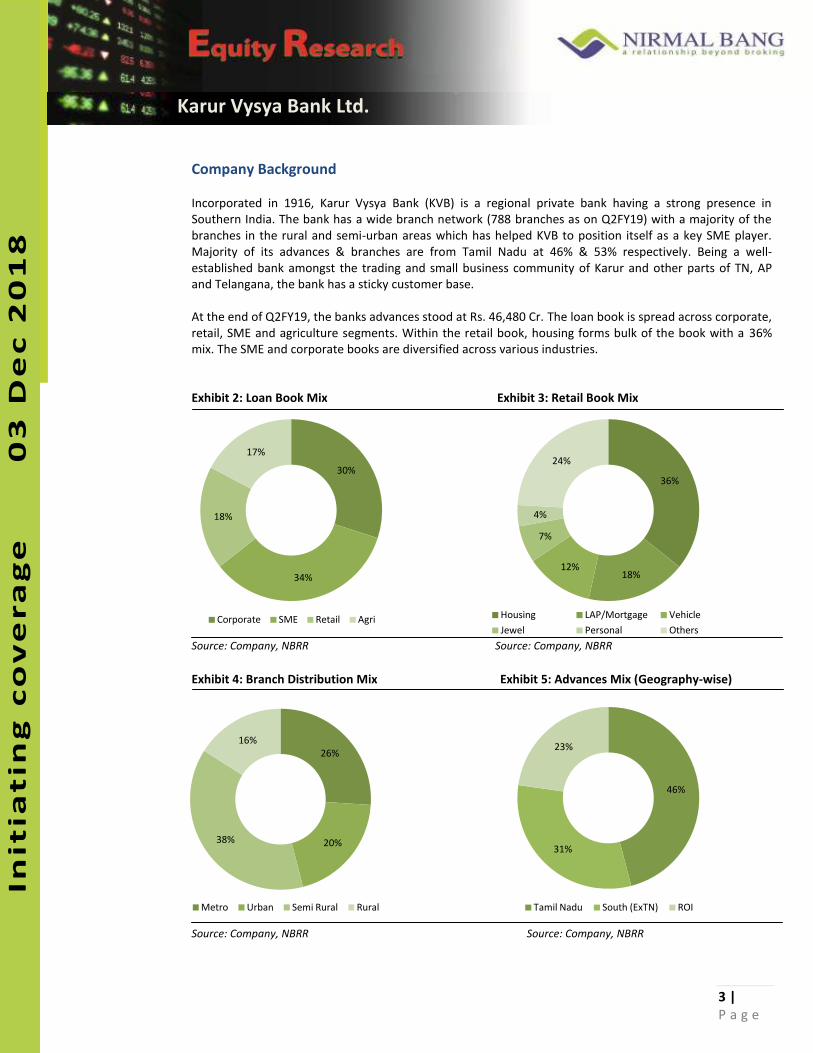

Company Background

Incorporated in 1916, Karur Vysya Bank (KVB) is a regional private bank having a strong presence in

Southern India. The bank has a wide branch network (788 branches as on Q2FY19) with a majority of the

branches in the rural and semi-urban areas which has helped KVB to position itself as a key SME player.

Majority of its advances & branches are from Tamil Nadu at 46% & 53% respectively. Being a well-

established bank amongst the trading and small business community of Karur and other parts of TN, AP

and Telangana, the bank has a sticky customer base.

At the end of Q2FY19, the banks advances stood at Rs. 46,480 Cr. The loan book is spread across corporate,

retail, SME and agriculture segments. Within the retail book, housing forms bulk of the book with a 36%

mix. The SME and corporate books are diversified across various industries.

Exhibit 2: Loan Book Mix Exhibit 3: Retail Book Mix

Source: Company, NBRR Source: Company, NBRR

Exhibit 4: Branch Distribution Mix Exhibit 5: Advances Mix (Geography-wise)

Source: Company, NBRR Source: Company, NBRR

30%

34%

18%

17%

Corporate SME Retail Agri

36%

18% 12%

7%

4%

24%

Housing LAP/Mortgage Vehicle

Jewel Personal Others

26%

20% 38%

16%

Metro Urban Semi Rural Rural

46%

31%

23%

Tamil Nadu South (ExTN) ROI

4 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

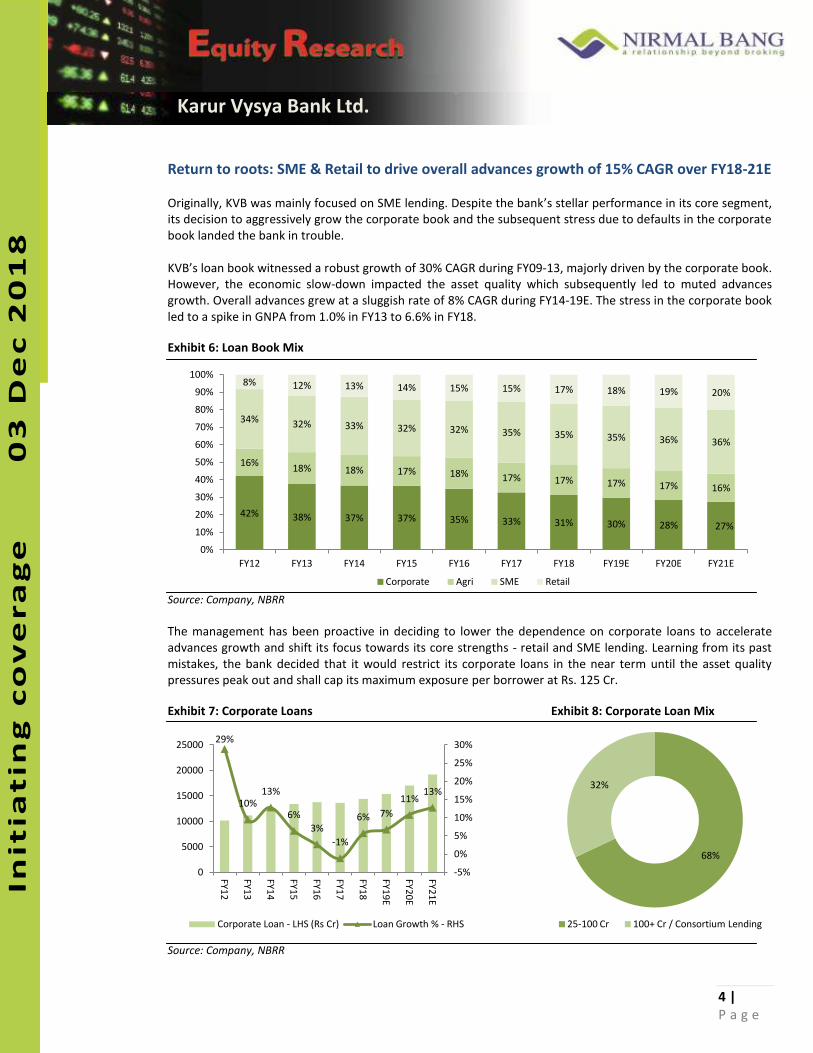

Return to roots: SME & Retail to drive overall advances growth of 15% CAGR over FY18-21E

Originally, KVB was mainly focused on SME lending. Despite the bank s stellar performance in its core segment,

its decision to aggressively grow the corporate book and the subsequent stress due to defaults in the corporate

book landed the bank in trouble.

KVB s loa ook it essed a o ust g o th of 30% CAGR during FY09-13, majorly driven by the corporate book.

However, the economic slow-down impacted the asset quality which subsequently led to muted advances

growth. Overall advances grew at a sluggish rate of 8% CAGR during FY14-19E. The stress in the corporate book

led to a spike in GNPA from 1.0% in FY13 to 6.6% in FY18.

Exhibit 6: Loan Book Mix

Source: Company, NBRR

The management has been proactive in deciding to lower the dependence on corporate loans to accelerate

advances growth and shift its focus towards its core strengths - retail and SME lending. Learning from its past

mistakes, the bank decided that it would restrict its corporate loans in the near term until the asset quality

pressures peak out and shall cap its maximum exposure per borrower at Rs. 125 Cr.

Exhibit 7: Corporate Loans Exhibit 8: Corporate Loan Mix

Source: Company, NBRR

42% 38% 37% 37% 35% 33% 31% 30% 28% 27%

16% 18% 18% 17% 18% 17% 17% 17% 17% 16%

34% 32% 33% 32% 32% 35% 35% 35% 36% 36%

8% 12% 13% 14% 15% 15% 17% 18% 19% 20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Corporate Agri SME Retail

29%

10% 13%

6%

3%

-1%

6% 7%

11% 13%

-5%

0%

5%

10%

15%

20%

25%

30%

0

5000

10000

15000

20000

25000

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

Corporate Loan - LHS (Rs Cr) Loan Growth % - RHS

68%

32%

25-100 Cr 100+ Cr / Consortium Lending

5 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

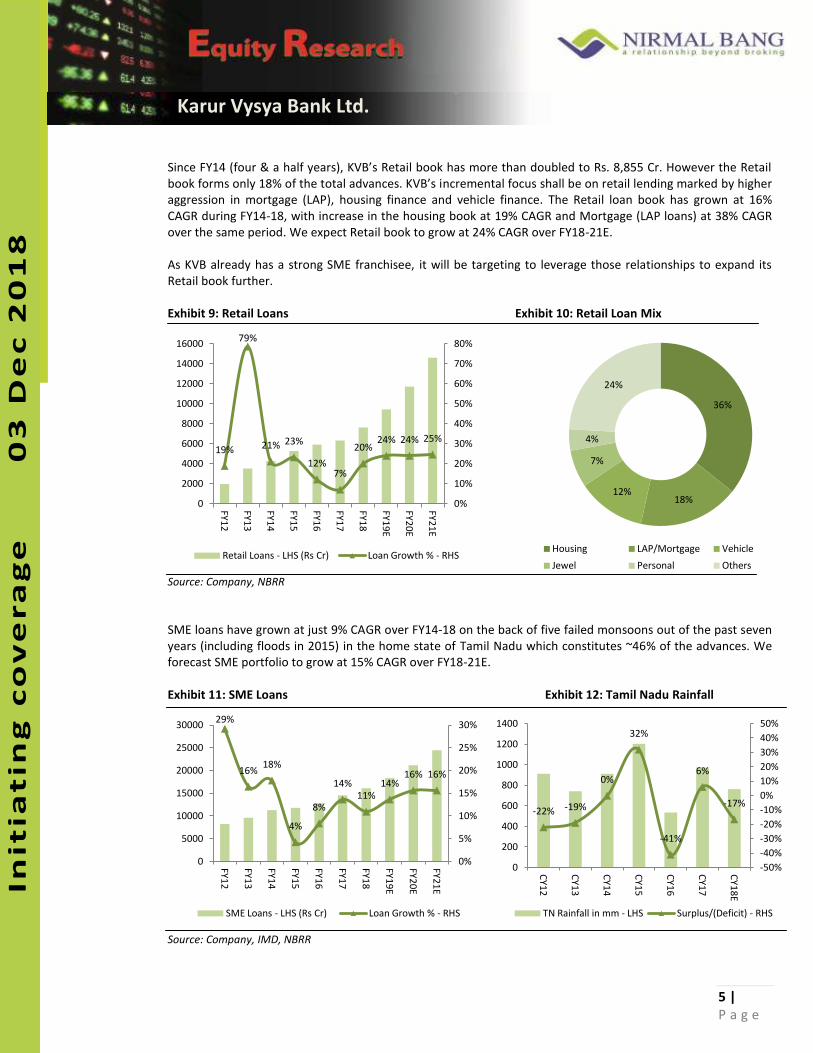

“i e FY fou & a half ea s , KVB s ‘etail ook has o e tha dou led to ‘s. 8,8 C . Ho e e the ‘etail ook fo s o l 8% of the total ad a es. KVB s incremental focus shall be on retail lending marked by higher

aggression in mortgage (LAP), housing finance and vehicle finance. The Retail loan book has grown at 16%

CAGR during FY14-18, with increase in the housing book at 19% CAGR and Mortgage (LAP loans) at 38% CAGR

over the same period. We expect Retail book to grow at 24% CAGR over FY18-21E.

As KVB already has a strong SME franchisee, it will be targeting to leverage those relationships to expand its

Retail book further.

Exhibit 9: Retail Loans Exhibit 10: Retail Loan Mix

Source: Company, NBRR

SME loans have grown at just 9% CAGR over FY14-18 on the back of five failed monsoons out of the past seven

years (including floods in 2015) in the home state of Tamil Nadu which constitutes ~46% of the advances. We

forecast SME portfolio to grow at 15% CAGR over FY18-21E.

Exhibit 11: SME Loans Exhibit 12: Tamil Nadu Rainfall

Source: Company, IMD, NBRR

19%

79%

21% 23%

12% 7%

20% 24% 24% 25%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

2000

4000

6000

8000

10000

12000

14000

16000

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

Retail Loans - LHS (Rs Cr) Loan Growth % - RHS

36%

18% 12%

7%

4%

24%

Housing LAP/Mortgage Vehicle

Jewel Personal Others

29%

16% 18%

4%

8%

14%

11%

14% 16% 16%

0%

5%

10%

15%

20%

25%

30%

0

5000

10000

15000

20000

25000

30000

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

SME Loans - LHS (Rs Cr) Loan Growth % - RHS

-22% -19%

0%

32%

-41%

6%

-17%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

200

400

600

800

1000

1200

1400

CY

12

CY

13

CY

14

CY

15

CY

16

CY

17

CY

18

E

TN Rainfall in mm - LHS Surplus/(Deficit) - RHS

6 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

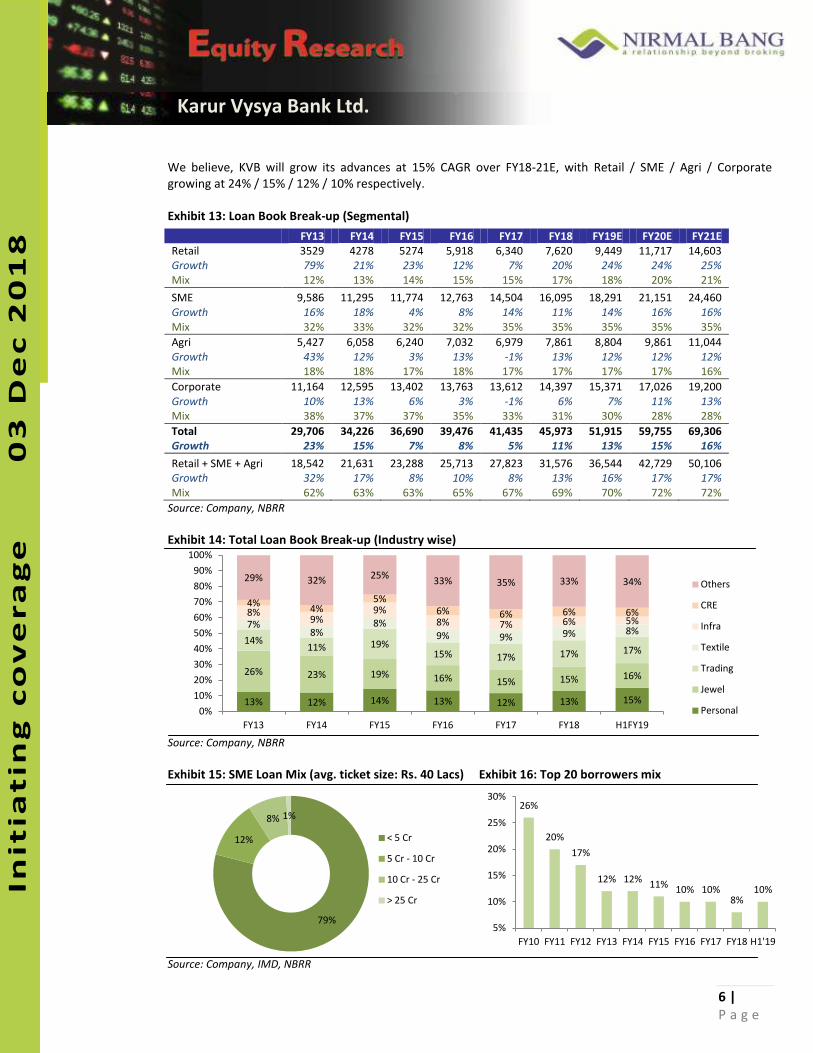

We believe, KVB will grow its advances at 15% CAGR over FY18-21E, with Retail / SME / Agri / Corporate

growing at 24% / 15% / 12% / 10% respectively.

Exhibit 13: Loan Book Break-up (Segmental)

FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Retail 3529 4278 5274 5,918 6,340 7,620 9,449 11,717 14,603

Growth 79% 21% 23% 12% 7% 20% 24% 24% 25%

Mix 12% 13% 14% 15% 15% 17% 18% 20% 21%

SME 9,586 11,295 11,774 12,763 14,504 16,095 18,291 21,151 24,460

Growth 16% 18% 4% 8% 14% 11% 14% 16% 16%

Mix 32% 33% 32% 32% 35% 35% 35% 35% 35%

Agri 5,427 6,058 6,240 7,032 6,979 7,861 8,804 9,861 11,044

Growth 43% 12% 3% 13% -1% 13% 12% 12% 12%

Mix 18% 18% 17% 18% 17% 17% 17% 17% 16%

Corporate 11,164 12,595 13,402 13,763 13,612 14,397 15,371 17,026 19,200

Growth 10% 13% 6% 3% -1% 6% 7% 11% 13%

Mix 38% 37% 37% 35% 33% 31% 30% 28% 28%

Total 29,706 34,226 36,690 39,476 41,435 45,973 51,915 59,755 69,306

Growth 23% 15% 7% 8% 5% 11% 13% 15% 16%

Retail + SME + Agri 18,542 21,631 23,288 25,713 27,823 31,576 36,544 42,729 50,106

Growth 32% 17% 8% 10% 8% 13% 16% 17% 17%

Mix 62% 63% 63% 65% 67% 69% 70% 72% 72%

Source: Company, NBRR

Exhibit 14: Total Loan Book Break-up (Industry wise)

Source: Company, NBRR

Exhibit 15: SME Loan Mix (avg. ticket size: Rs. 40 Lacs) Exhibit 16: Top 20 borrowers mix

Source: Company, IMD, NBRR

13% 12% 14% 13% 12% 13% 15%

26% 23% 19% 16% 15% 15% 16%

14% 11% 19%

15% 17% 17% 17%

7% 8%

8%

9% 9% 9% 8%

8% 9%

9%

8% 7% 6% 5%

4% 4%

5%

6% 6% 6% 6%

29% 32% 25%

33% 35% 33% 34%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY14 FY15 FY16 FY17 FY18 H1FY19

Others

CRE

Infra

Textile

Trading

Jewel

Personal

79%

12%

8% 1%

< 5 Cr

5 Cr - 10 Cr

10 Cr - 25 Cr

> 25 Cr

26%

20%

17%

12% 12% 11%

10% 10% 8%

10%

5%

10%

15%

20%

25%

30%

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 H1'19

7 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

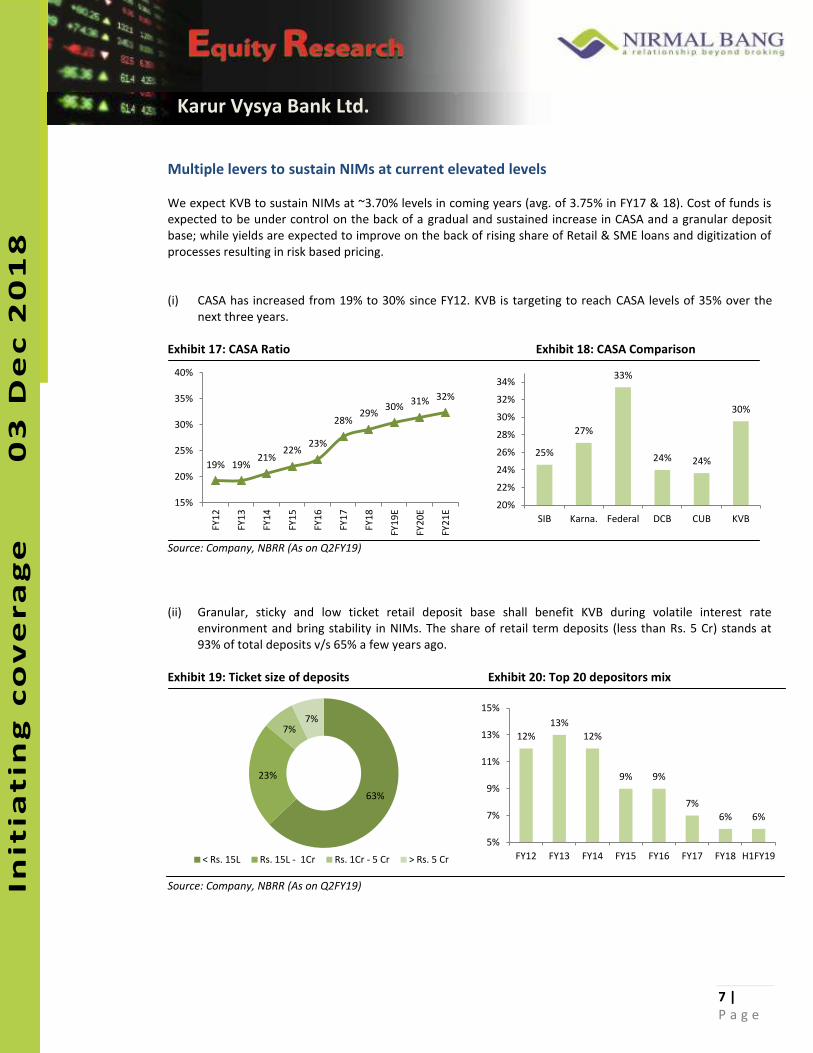

Multiple levers to sustain NIMs at current elevated levels

We expect KVB to sustain NIMs at ~3.70% levels in coming years (avg. of 3.75% in FY17 & 18). Cost of funds is

expected to be under control on the back of a gradual and sustained increase in CASA and a granular deposit

base; while yields are expected to improve on the back of rising share of Retail & SME loans and digitization of

processes resulting in risk based pricing.

(i) CASA has increased from 19% to 30% since FY12. KVB is targeting to reach CASA levels of 35% over the

next three years.

Exhibit 17: CASA Ratio Exhibit 18: CASA Comparison

Source: Company, NBRR (As on Q2FY19)

(ii) Granular, sticky and low ticket retail deposit base shall benefit KVB during volatile interest rate

environment and bring stability in NIMs. The share of retail term deposits (less than Rs. 5 Cr) stands at

93% of total deposits v/s 65% a few years ago.

Exhibit 19: Ticket size of deposits Exhibit 20: Top 20 depositors mix

Source: Company, NBRR (As on Q2FY19)

19% 19% 21%

22% 23%

28% 29%

30% 31% 32%

15%

20%

25%

30%

35%

40%

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

25%

27%

33%

24% 24%

30%

20%

22%

24%

26%

28%

30%

32%

34%

SIB Karna. Federal DCB CUB KVB

63%

23%

7% 7%

< Rs. 15L Rs. 15L - 1Cr Rs. 1Cr - 5 Cr > Rs. 5 Cr

12%

13%

12%

9% 9%

7%

6% 6%

5%

7%

9%

11%

13%

15%

FY12 FY13 FY14 FY15 FY16 FY17 FY18 H1FY19

8 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

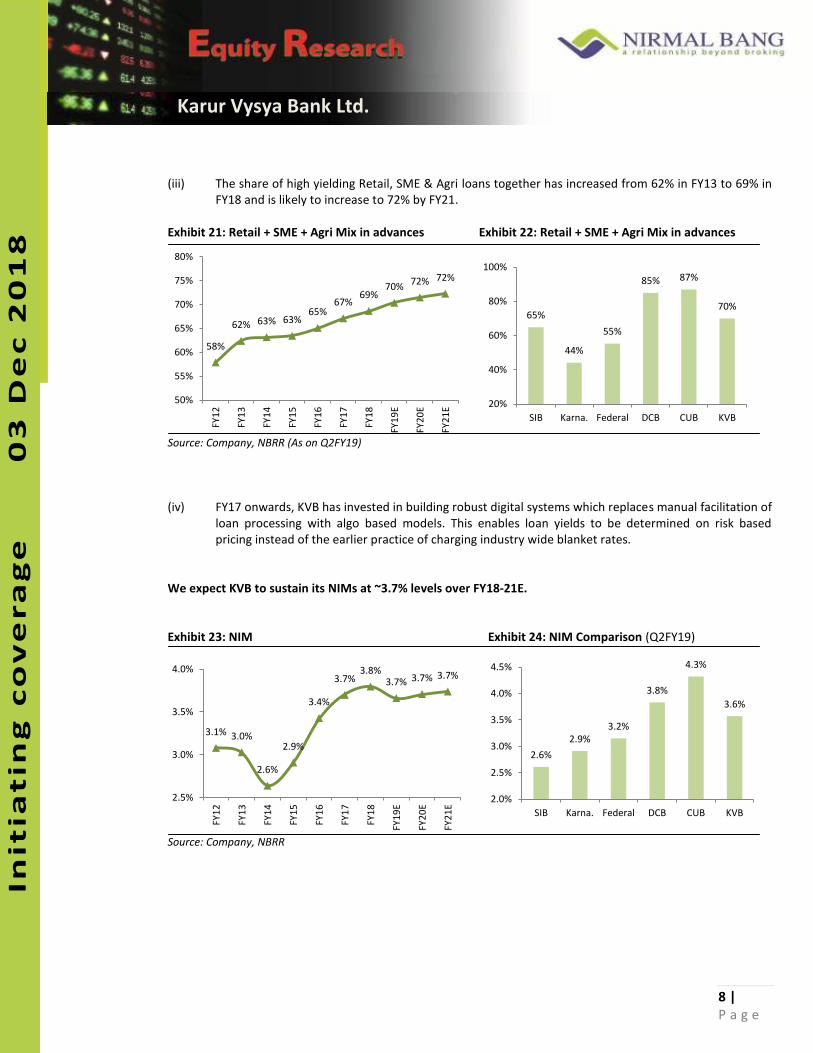

(iii) The share of high yielding Retail, SME & Agri loans together has increased from 62% in FY13 to 69% in

FY18 and is likely to increase to 72% by FY21.

Exhibit 21: Retail + SME + Agri Mix in advances Exhibit 22: Retail + SME + Agri Mix in advances

Source: Company, NBRR (As on Q2FY19)

(iv) FY17 onwards, KVB has invested in building robust digital systems which replaces manual facilitation of

loan processing with algo based models. This enables loan yields to be determined on risk based

pricing instead of the earlier practice of charging industry wide blanket rates.

We expect KVB to sustain its NIMs at ~3.7% levels over FY18-21E.

Exhibit 23: NIM Exhibit 24: NIM Comparison (Q2FY19)

Source: Company, NBRR

58%

62% 63% 63% 65%

67% 69%

70% 72% 72%

50%

55%

60%

65%

70%

75%

80%

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

65%

44%

55%

85% 87%

70%

20%

40%

60%

80%

100%

SIB Karna. Federal DCB CUB KVB

3.1% 3.0%

2.6%

2.9%

3.4%

3.7% 3.8%

3.7% 3.7% 3.7%

2.5%

3.0%

3.5%

4.0%

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

2.6%

2.9%

3.2%

3.8%

4.3%

3.6%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

SIB Karna. Federal DCB CUB KVB

9 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

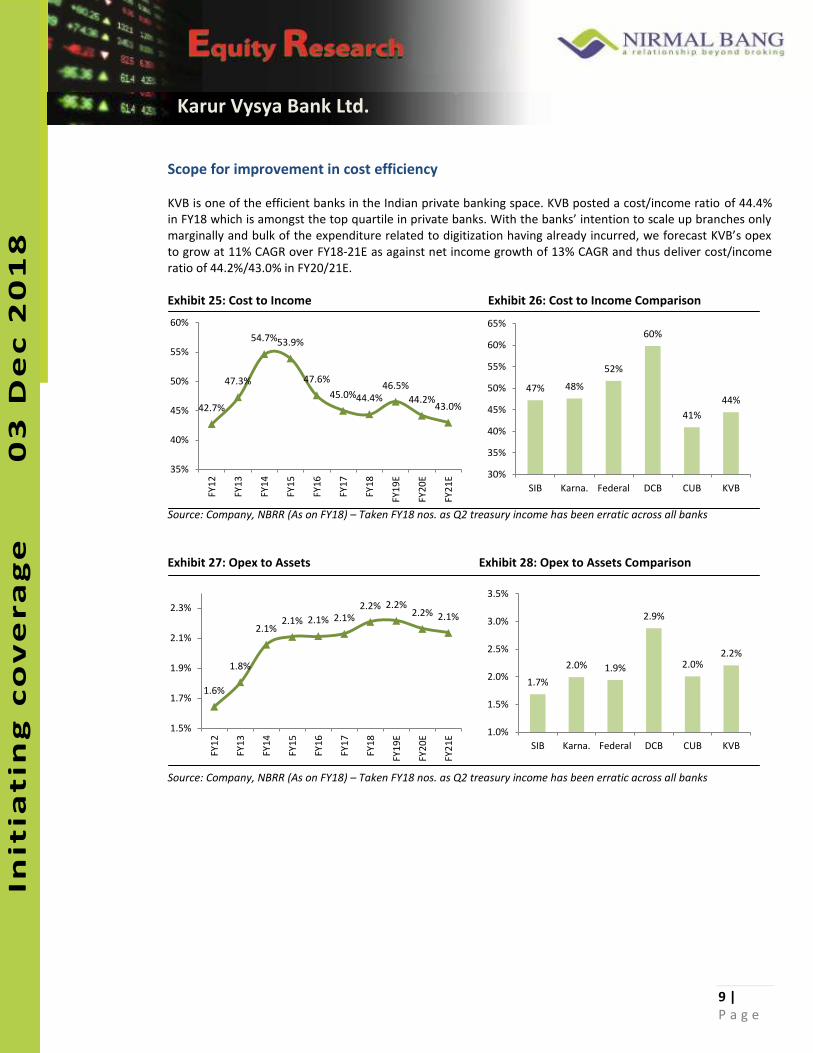

Scope for improvement in cost efficiency

KVB is one of the efficient banks in the Indian private banking space. KVB posted a cost/income ratio of 44.4%

i FY 8 hi h is a o gst the top ua tile i p i ate a ks. With the a ks i te tio to s ale up a hes o l a gi all a d ulk of the e pe ditu e elated to digitizatio ha i g al ead i u ed, e fo e ast KVB s ope

to grow at 11% CAGR over FY18-21E as against net income growth of 13% CAGR and thus deliver cost/income

ratio of 44.2%/43.0% in FY20/21E.

Exhibit 25: Cost to Income Exhibit 26: Cost to Income Comparison

Source: Company, NBRR (As on FY18) – Taken FY18 nos. as Q2 treasury income has been erratic across all banks

Exhibit 27: Opex to Assets Exhibit 28: Opex to Assets Comparison

Source: Company, NBRR (As on FY18) – Taken FY18 nos. as Q2 treasury income has been erratic across all banks

42.7%

47.3%

54.7% 53.9%

47.6%

45.0% 44.4%

46.5%

44.2% 43.0%

35%

40%

45%

50%

55%

60%

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

47% 48%

52%

60%

41%

44%

30%

35%

40%

45%

50%

55%

60%

65%

SIB Karna. Federal DCB CUB KVB

1.6%

1.8%

2.1% 2.1% 2.1% 2.1%

2.2% 2.2% 2.2% 2.1%

1.5%

1.7%

1.9%

2.1%

2.3%

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

1.7%

2.0% 1.9%

2.9%

2.0% 2.2%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

SIB Karna. Federal DCB CUB KVB

10 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

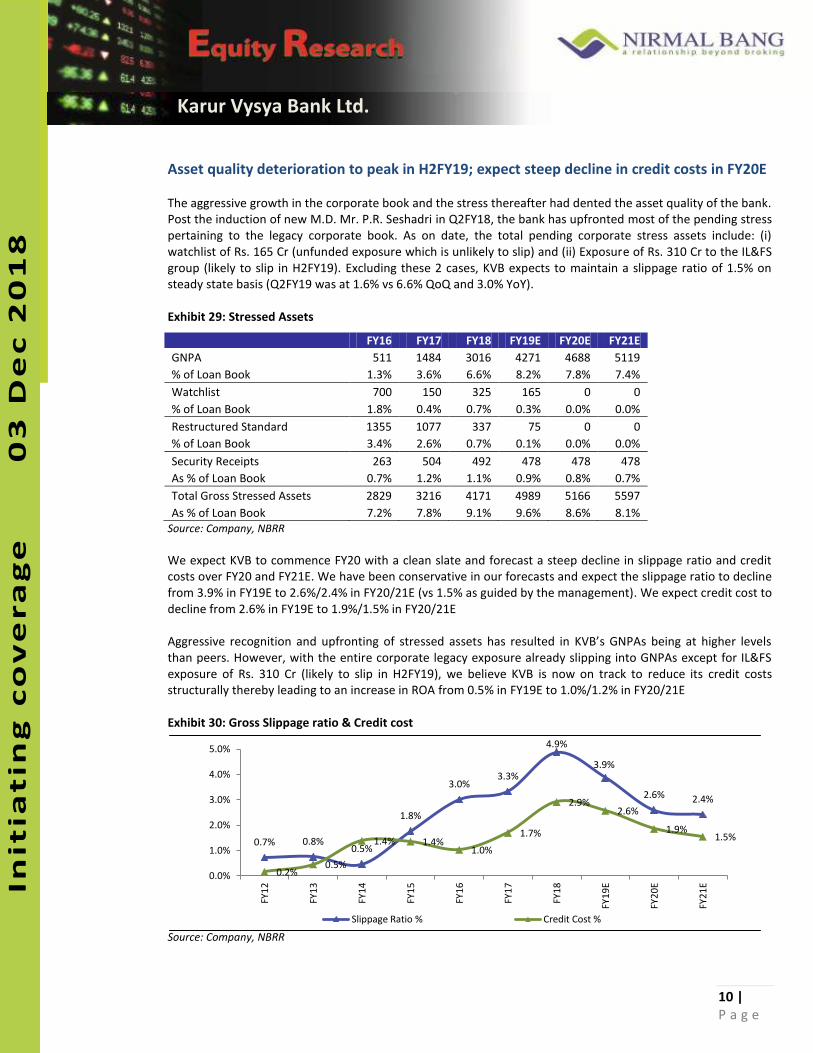

Asset quality deterioration to peak in H2FY19; expect steep decline in credit costs in FY20E

The aggressive growth in the corporate book and the stress thereafter had dented the asset quality of the bank.

Post the induction of new M.D. Mr. P.R. Seshadri in Q2FY18, the bank has upfronted most of the pending stress

pertaining to the legacy corporate book. As on date, the total pending corporate stress assets include: (i)

watchlist of Rs. 165 Cr (unfunded exposure which is unlikely to slip) and (ii) Exposure of Rs. 310 Cr to the IL&FS

group (likely to slip in H2FY19). Excluding these 2 cases, KVB expects to maintain a slippage ratio of 1.5% on

steady state basis (Q2FY19 was at 1.6% vs 6.6% QoQ and 3.0% YoY).

Exhibit 29: Stressed Assets

FY16 FY17 FY18 FY19E FY20E FY21E

GNPA 511 1484 3016 4271 4688 5119

% of Loan Book 1.3% 3.6% 6.6% 8.2% 7.8% 7.4%

Watchlist 700 150 325 165 0 0

% of Loan Book 1.8% 0.4% 0.7% 0.3% 0.0% 0.0%

Restructured Standard 1355 1077 337 75 0 0

% of Loan Book 3.4% 2.6% 0.7% 0.1% 0.0% 0.0%

Security Receipts 263 504 492 478 478 478

As % of Loan Book 0.7% 1.2% 1.1% 0.9% 0.8% 0.7%

Total Gross Stressed Assets 2829 3216 4171 4989 5166 5597

As % of Loan Book 7.2% 7.8% 9.1% 9.6% 8.6% 8.1%

Source: Company, NBRR

We expect KVB to commence FY20 with a clean slate and forecast a steep decline in slippage ratio and credit

costs over FY20 and FY21E. We have been conservative in our forecasts and expect the slippage ratio to decline

from 3.9% in FY19E to 2.6%/2.4% in FY20/21E (vs 1.5% as guided by the management). We expect credit cost to

decline from 2.6% in FY19E to 1.9%/1.5% in FY20/21E

Agg essi e e og itio a d upf o ti g of st essed assets has esulted i KVB s GNPAs ei g at highe le els than peers. However, with the entire corporate legacy exposure already slipping into GNPAs except for IL&FS

exposure of Rs. 310 Cr (likely to slip in H2FY19), we believe KVB is now on track to reduce its credit costs

structurally thereby leading to an increase in ROA from 0.5% in FY19E to 1.0%/1.2% in FY20/21E

Exhibit 30: Gross Slippage ratio & Credit cost

Source: Company, NBRR

0.7% 0.8% 0.5%

1.8%

3.0% 3.3%

4.9%

3.9%

2.6% 2.4%

0.2% 0.5%

1.4% 1.4% 1.0%

1.7%

2.9% 2.6%

1.9% 1.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

Slippage Ratio % Credit Cost %

11 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

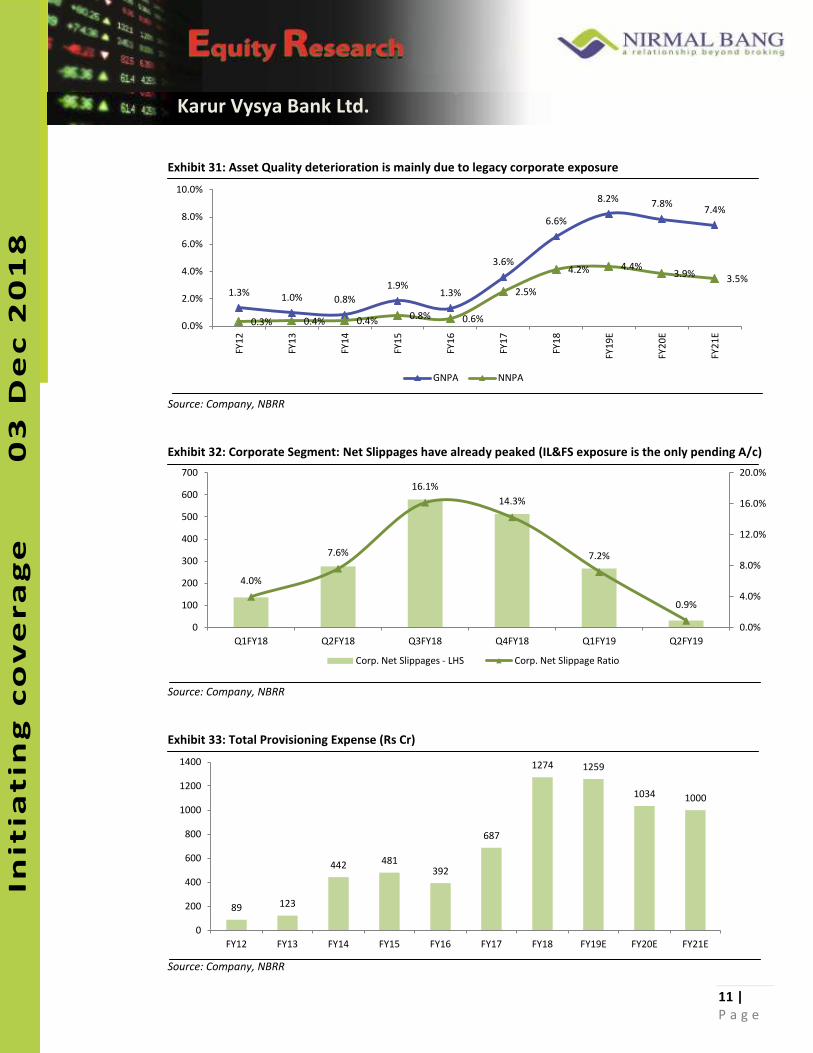

Exhibit 31: Asset Quality deterioration is mainly due to legacy corporate exposure

Source: Company, NBRR

Exhibit 32: Corporate Segment: Net Slippages have already peaked (IL&FS exposure is the only pending A/c)

Source: Company, NBRR

Exhibit 33: Total Provisioning Expense (Rs Cr)

Source: Company, NBRR

1.3% 1.0% 0.8%

1.9% 1.3%

3.6%

6.6%

8.2% 7.8%

7.4%

0.3% 0.4% 0.4% 0.8% 0.6%

2.5%

4.2% 4.4% 3.9%

3.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

GNPA NNPA

4.0%

7.6%

16.1%

14.3%

7.2%

0.9%

0.0%

4.0%

8.0%

12.0%

16.0%

20.0%

0

100

200

300

400

500

600

700

Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q2FY19

Corp. Net Slippages - LHS Corp. Net Slippage Ratio

89 123

442 481 392

687

1274 1259

1034 1000

0

200

400

600

800

1000

1200

1400

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

12 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

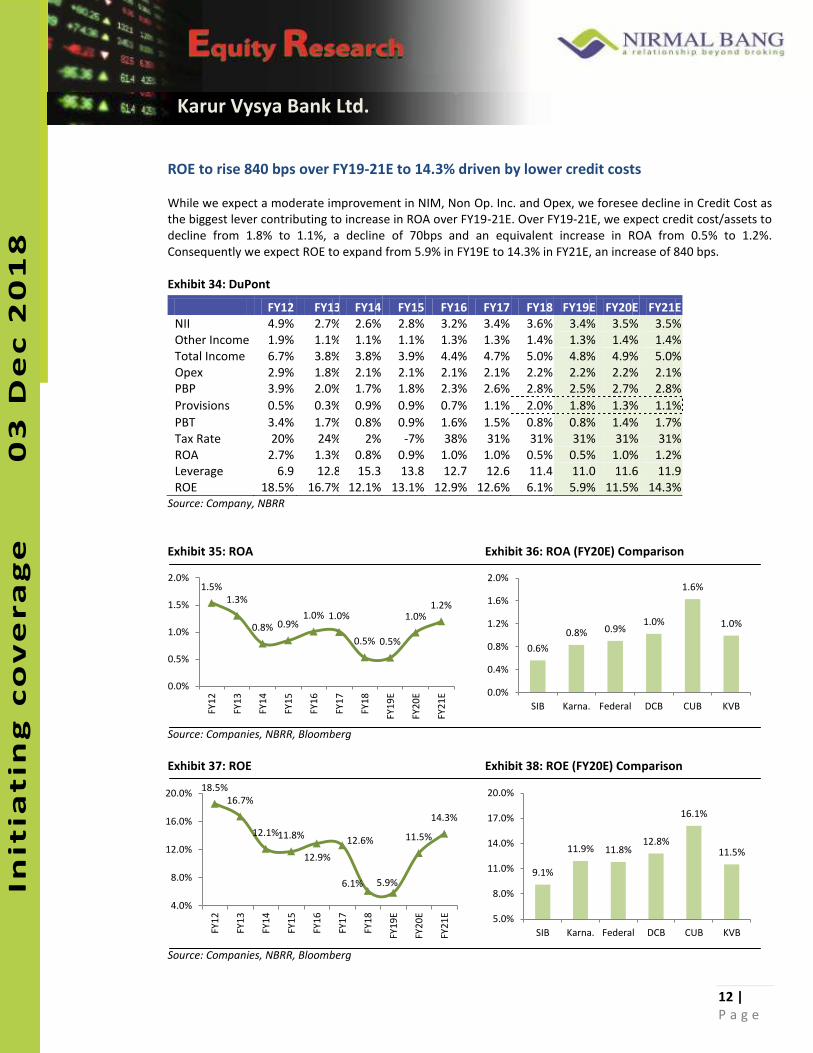

ROE to rise 840 bps over FY19-21E to 14.3% driven by lower credit costs

While we expect a moderate improvement in NIM, Non Op. Inc. and Opex, we foresee decline in Credit Cost as

the biggest lever contributing to increase in ROA over FY19-21E. Over FY19-21E, we expect credit cost/assets to

decline from 1.8% to 1.1%, a decline of 70bps and an equivalent increase in ROA from 0.5% to 1.2%.

Consequently we expect ROE to expand from 5.9% in FY19E to 14.3% in FY21E, an increase of 840 bps.

Exhibit 34: DuPont

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

NII 4.9% 2.7% 2.6% 2.8% 3.2% 3.4% 3.6% 3.4% 3.5% 3.5%

Other Income 1.9% 1.1% 1.1% 1.1% 1.3% 1.3% 1.4% 1.3% 1.4% 1.4%

Total Income 6.7% 3.8% 3.8% 3.9% 4.4% 4.7% 5.0% 4.8% 4.9% 5.0%

Opex 2.9% 1.8% 2.1% 2.1% 2.1% 2.1% 2.2% 2.2% 2.2% 2.1%

PBP 3.9% 2.0% 1.7% 1.8% 2.3% 2.6% 2.8% 2.5% 2.7% 2.8%

Provisions 0.5% 0.3% 0.9% 0.9% 0.7% 1.1% 2.0% 1.8% 1.3% 1.1%

PBT 3.4% 1.7% 0.8% 0.9% 1.6% 1.5% 0.8% 0.8% 1.4% 1.7%

Tax Rate 20% 24% 2% -7% 38% 31% 31% 31% 31% 31%

ROA 2.7% 1.3% 0.8% 0.9% 1.0% 1.0% 0.5% 0.5% 1.0% 1.2%

Leverage 6.9 12.8 15.3 13.8 12.7 12.6 11.4 11.0 11.6 11.9

ROE 18.5% 16.7% 12.1% 13.1% 12.9% 12.6% 6.1% 5.9% 11.5% 14.3%

Source: Company, NBRR

Exhibit 35: ROA Exhibit 36: ROA (FY20E) Comparison

Source: Companies, NBRR, Bloomberg

Exhibit 37: ROE Exhibit 38: ROE (FY20E) Comparison

Source: Companies, NBRR, Bloomberg

1.5%

1.3%

0.8% 0.9% 1.0% 1.0%

0.5% 0.5%

1.0% 1.2%

0.0%

0.5%

1.0%

1.5%

2.0%

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

0.6%

0.8% 0.9% 1.0%

1.6%

1.0%

0.0%

0.4%

0.8%

1.2%

1.6%

2.0%

SIB Karna. Federal DCB CUB KVB

18.5%

16.7%

12.1% 11.8%

12.9%

12.6%

6.1% 5.9%

11.5%

14.3%

4.0%

8.0%

12.0%

16.0%

20.0%

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

9.1%

11.9% 11.8% 12.8%

16.1%

11.5%

5.0%

8.0%

11.0%

14.0%

17.0%

20.0%

SIB Karna. Federal DCB CUB KVB

13 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

KVB to be the 2nd bank in peer group to scale 15%+ ROE after CUB

Among the old generation private banks, CUB has consistently stood out as an outlier by delivering an average

ROE of 15.3% over the last three years despite of the banking system having undergone severe stress. We

believe KVB can outperform its peers and potentially reach the profitability (ROE) levels of CUB over the next

four years (by FY22) on the back of robust capitalization and lower capital consumption which ensures no

dilution risk in medium term and a consistent rise in ROE. KVB has one of the highest Tier 1 ratios in its peer

group at 13.7%. Further, lower advances growth vis-à-vis peers shall result in lower capital

consumption/requirement. Thus we do not see any fund raising by KVB over the next few years as opposed to

its peers, whereby all have firmed up plans to raise Tier 1 capital over FY19-20E (except for CUB).

Exhibit 39: Tier 1 Capital Exhibit 40: Loan CAGR (FY18-20E) / Capital Consumption

Source: Companies, NBRR, Bloomberg

SIB Karnataka Federal DCB CUB KVB

ROE - FY20 9.1% 11.9% 11.8% 12.8% 16.1% 11.5%

Tier – 1 (Q2FY19) 10.0% 10.6% 12.8% 12.0% 14.7% 13.7%

Capital Raise in

FY19E

Wont Wont

FY20E

raise raise

Source: Companies, NBRR, Bloomberg

Exhibit 41: How we see KVB s ‘OE & Tier 1 unfolding ……….

Source: Company, NBRR

10.0% 10.6%

12.8%

12.0%

14.7%

13.7%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

SIB Karna. Federal DCB CUB KVB

16%

19%

23% 25%

16% 14%

10%

15%

20%

25%

30%

SIB Karna. Federal DCB CUB KVB

18.5%

16.7%

12.1% 11.8% 12.9% 12.6%

6.1% 5.9%

11.5%

14.3%

15.9%

13.1% 13.1%

11.6%

13.6%

11.3%

11.9%

13.9%

13.0% 12.4%

12.1% 11.9%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

4%

6%

8%

10%

12%

14%

16%

18%

20%

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

E

FY

20

E

FY

21

E

FY

22

E

ROE - LHS Tier 1 - RHS

14 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

New M.D. Mr. P.R.Seshadri has an extensive track record in Retail banking

Mr. P.R.Seshadri, joined KVB in Sep 2017 as the MD & CEO. He took up the job at KVB since he wanted to move

back to India for personal reasons (He was based in UK in his previous assignment). KVB has a history of long-

tenure CEOs, mostly serving 3 terms (9 years).

He is a seasoned banker with SME and Retail banking experience of over 25 years spanning multiple

geographies. He started his banking career with Citibank India in 1992 and was involved with Citibank India in

a ious apa ities till , hilst aki g sig ifi a t o t i utio s to Citi a k s usi ess i I dia. He has a

proven track record of building and leading large teams as well as executing complex business objectives.

Mr Seshadri was instrumental in successfully transforming Citi's consumer businesses by enhancing efficiency,

reducing costs and standardising products & services. We believe M . “eshad i s e te si e e pe ie e and

expertise in Retail and SME banking will aid KVB in improving efficiency and further accelerate the pace of

retailisation of its loan book.

Mr. Seshadri believes in the philosophy of maintaining and expanding NIMs/spreads even at the cost of lower

growth in advances.

Exhibit 42: Mr. P R Seshadri’s vast Retail experience

Organization Tenure Role

Citibank N.A. India

Branches Jan 98 – Nov 99

Head of Retail Collections - Responsible for maintaining the quality of

Citi's retail asset portfolio.

Citibank N.A. India

Branches Dec 99 – Mar 03

Marketing Director & Head of Structured Finance – Responsible for

launching a set of innovative products.

CitiFinancial Retail

Services, India Mar 01 – Apr 03

MD & CEO – Responsible for building out this legal vehicle into India's

largest sales finance provider.

Citifinancial

Consumer Finance,

India

Apr 03 – Sept 05

MD & CEO – Responsible to grow this entity to become the largest &

most profitable NBFC in India.

Citibank N.A.,

Singapore Oct 05 – Mar 10

Executive V.P & Regional Head Asset Products, Asia Pacific – Achieved

significant growth in the period prior to the Global Financial Crisis

Citibank N.A.,

Singapore Apr 10 – Oct 14

MD, Head Sales & Distribution, Asia Pacific –He Transformed the

branche network and architecture by adopting 'retail like' behaviour,

leading to a significantly smaller yet powerful distribution network.

Citi, Singapore Feb 15 – Jun 15 MD – Integrated Citi's consumer businesses and enhanced their

efficiency, reduced costs, standardized products and services.

BFC Bank, UK Oct 15 – Apr 17 CEO – Worked with the Group to establish a 'challenger' bank aimed at

making cross border payments easier, cheaper, seamless and accessible.

15 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

Key Risks & Concerns

Regional Dependence on Tamil Nadu

KVB faces concentration risk with over ~46% of the advances sourced from Tamil Nadu in FY18. The southern

region including Tamil Nadu comprises ~77% of the total loan book. Any major change in the state s poli ies o swing in regional environment can immediately affect our earnings estimates for the bank.

Continued lower growth and deterioration in asset quality in the SME segment could prolong the overall

recovery

The SME advances have grown at just 9% CAGR over FY14-18 on the back of five failed monsoons out of the

past seven years (including floods in 2015) in the home state of Tamil Nadu which constitutes ~46% of the

advances. Evolution of slippages in coming quarters would be a key determinant of the future profitability of

the bank.

Exhibit 43: SME: Net slippage ratio Exhibit 44: SME Loan Growth

Source: Company, NBRR

Macro headwind: Interest rates

The rise in interest rates over YTD CY18 has already had an adverse impact on the cost of borrowings and NIMs

of all the banks. A continuous increase in interest rates would result in a compression in NIMs for KVB.

Delayed recovery from NCLT cases

KVB has an exposure of Rs. 914 Cr to NCLT accounts and has already done 65.5% provisioning on them. KVB

expects over Rs. 600 Cr worth of loans to get resolved in the near future. Timely resolution of these cases

remains a key risk and challenge.

2.7%

1.0% 1.5% 1.6%

5.8%

2.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Q1 Q2 Q3 Q4

FY18 FY19

11.7%

13.1%

18.4%

11.0%

14.6%

10.0% 3.1%

3.2%

3.5% 3.3%

4.7%

5.3%

2.0%

3.0%

4.0%

5.0%

6.0%

9.0%

12.0%

15.0%

18.0%

21.0%

Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q2FY19

SME Loan Growth - LHS SME GNPA - RHS

16 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

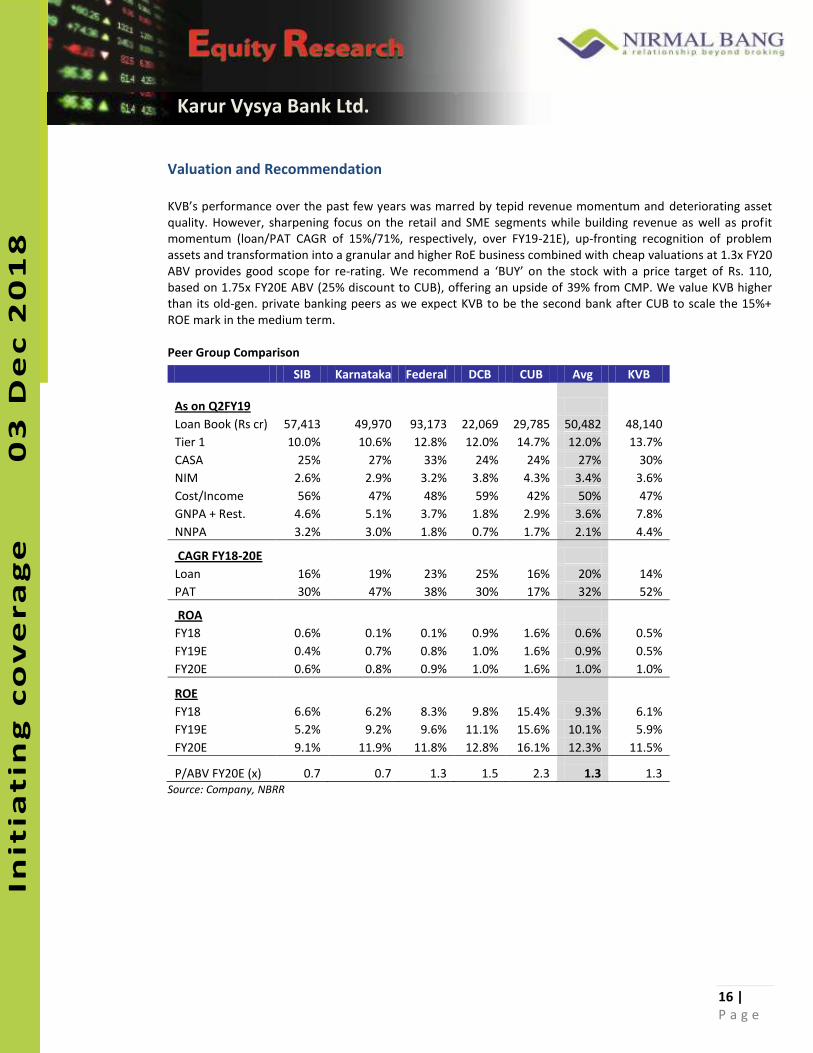

Valuation and Recommendation

KVB s performance over the past few years was marred by tepid revenue momentum and deteriorating asset

quality. However, sharpening focus on the retail and SME segments while building revenue as well as profit

momentum (loan/PAT CAGR of 15%/71%, respectively, over FY19-21E), up-fronting recognition of problem

assets and transformation into a granular and higher RoE business combined with cheap valuations at 1.3x FY20

ABV provides good scope for re- ati g. We e o e d a BUY on the stock with a price target of Rs. 110,

based on 1.75x FY20E ABV (25% discount to CUB), offering an upside of 39% from CMP. We value KVB higher

than its old-gen. private banking peers as we expect KVB to be the second bank after CUB to scale the 15%+

ROE mark in the medium term.

Peer Group Comparison

SIB Karnataka Federal DCB CUB Avg KVB

As on Q2FY19

Loan Book (Rs cr) 57,413 49,970 93,173 22,069 29,785 50,482 48,140

Tier 1 10.0% 10.6% 12.8% 12.0% 14.7% 12.0% 13.7%

CASA 25% 27% 33% 24% 24% 27% 30%

NIM 2.6% 2.9% 3.2% 3.8% 4.3% 3.4% 3.6%

Cost/Income 56% 47% 48% 59% 42% 50% 47%

GNPA + Rest. 4.6% 5.1% 3.7% 1.8% 2.9% 3.6% 7.8%

NNPA 3.2% 3.0% 1.8% 0.7% 1.7% 2.1% 4.4%

CAGR FY18-20E

Loan 16% 19% 23% 25% 16% 20% 14%

PAT 30% 47% 38% 30% 17% 32% 52%

ROA

FY18 0.6% 0.1% 0.1% 0.9% 1.6% 0.6% 0.5%

FY19E 0.4% 0.7% 0.8% 1.0% 1.6% 0.9% 0.5%

FY20E 0.6% 0.8% 0.9% 1.0% 1.6% 1.0% 1.0%

ROE

FY18 6.6% 6.2% 8.3% 9.8% 15.4% 9.3% 6.1%

FY19E 5.2% 9.2% 9.6% 11.1% 15.6% 10.1% 5.9%

FY20E 9.1% 11.9% 11.8% 12.8% 16.1% 12.3% 11.5%

P/ABV FY20E (x) 0.7 0.7 1.3 1.5 2.3 1.3 1.3

Source: Company, NBRR

17 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

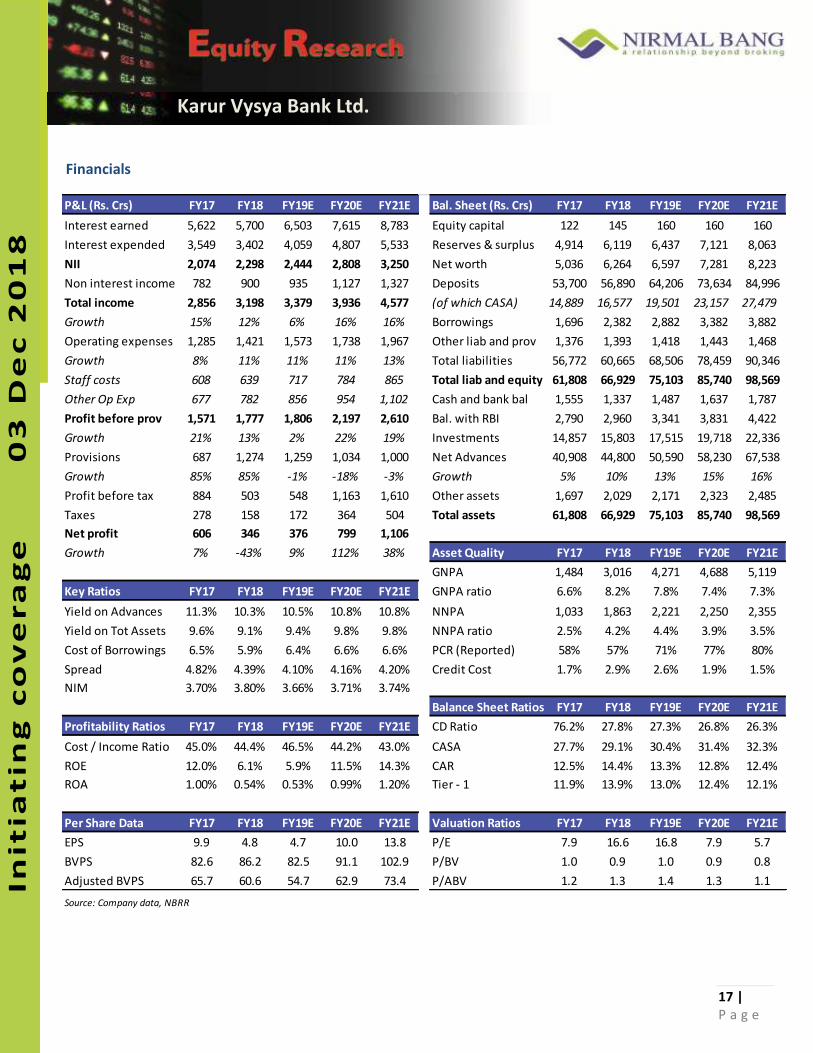

Financials

P&L (Rs. Crs) FY17 FY18 FY19E FY20E FY21E Bal. Sheet (Rs. Crs) FY17 FY18 FY19E FY20E FY21E

Interest earned 5,622 5,700 6,503 7,615 8,783 Equity capital 122 145 160 160 160

Interest expended 3,549 3,402 4,059 4,807 5,533 Reserves & surplus 4,914 6,119 6,437 7,121 8,063

NII 2,074 2,298 2,444 2,808 3,250 Net worth 5,036 6,264 6,597 7,281 8,223

Non interest income 782 900 935 1,127 1,327 Deposits 53,700 56,890 64,206 73,634 84,996

Total income 2,856 3,198 3,379 3,936 4,577 (of which CASA) 14,889 16,577 19,501 23,157 27,479

Growth 15% 12% 6% 16% 16% Borrowings 1,696 2,382 2,882 3,382 3,882

Operating expenses 1,285 1,421 1,573 1,738 1,967 Other liab and prov 1,376 1,393 1,418 1,443 1,468

Growth 8% 11% 11% 11% 13% Total liabilities 56,772 60,665 68,506 78,459 90,346

Staff costs 608 639 717 784 865 Total liab and equity 61,808 66,929 75,103 85,740 98,569

Other Op Exp 677 782 856 954 1,102 Cash and bank bal 1,555 1,337 1,487 1,637 1,787

Profit before prov 1,571 1,777 1,806 2,197 2,610 Bal. with RBI 2,790 2,960 3,341 3,831 4,422

Growth 21% 13% 2% 22% 19% Investments 14,857 15,803 17,515 19,718 22,336

Provisions 687 1,274 1,259 1,034 1,000 Net Advances 40,908 44,800 50,590 58,230 67,538

Growth 85% 85% -1% -18% -3% Growth 5% 10% 13% 15% 16%

Profit before tax 884 503 548 1,163 1,610 Other assets 1,697 2,029 2,171 2,323 2,485

Taxes 278 158 172 364 504 Total assets 61,808 66,929 75,103 85,740 98,569

Net profit 606 346 376 799 1,106

Growth 7% -43% 9% 112% 38% Asset Quality FY17 FY18 FY19E FY20E FY21E

GNPA 1,484 3,016 4,271 4,688 5,119

Key Ratios FY17 FY18 FY19E FY20E FY21E GNPA ratio 6.6% 8.2% 7.8% 7.4% 7.3%

Yield on Advances 11.3% 10.3% 10.5% 10.8% 10.8% NNPA 1,033 1,863 2,221 2,250 2,355

Yield on Tot Assets 9.6% 9.1% 9.4% 9.8% 9.8% NNPA ratio 2.5% 4.2% 4.4% 3.9% 3.5%

Cost of Borrowings 6.5% 5.9% 6.4% 6.6% 6.6% PCR (Reported) 58% 57% 71% 77% 80%

Spread 4.82% 4.39% 4.10% 4.16% 4.20% Credit Cost 1.7% 2.9% 2.6% 1.9% 1.5%

NIM 3.70% 3.80% 3.66% 3.71% 3.74%

Balance Sheet Ratios FY17 FY18 FY19E FY20E FY21E

Profitability Ratios FY17 FY18 FY19E FY20E FY21E CD Ratio 76.2% 27.8% 27.3% 26.8% 26.3%

Cost / Income Ratio 45.0% 44.4% 46.5% 44.2% 43.0% CASA 27.7% 29.1% 30.4% 31.4% 32.3%

ROE 12.0% 6.1% 5.9% 11.5% 14.3% CAR 12.5% 14.4% 13.3% 12.8% 12.4%

ROA 1.00% 0.54% 0.53% 0.99% 1.20% Tier - 1 11.9% 13.9% 13.0% 12.4% 12.1%

Per Share Data FY17 FY18 FY19E FY20E FY21E Valuation Ratios FY17 FY18 FY19E FY20E FY21E

EPS 9.9 4.8 4.7 10.0 13.8 P/E 7.9 16.6 16.8 7.9 5.7

BVPS 82.6 86.2 82.5 91.1 102.9 P/BV 1.0 0.9 1.0 0.9 0.8

Adjusted BVPS 65.7 60.6 54.7 62.9 73.4 P/ABV 1.2 1.3 1.4 1.3 1.1

Source: Company data, NBRR

18 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

Disclosure:

This Report is published by Nirmal Ba g “e u ities P i ate Li ited he ei afte efe ed to as NB“PL fo p i ate i ulatio . NB“PL is a registered Research Analyst under SEBI (Research Analyst) Regulations, 2014 having Registration no. INH000001766. NBSPL is

also a registered Stock Broker with National Stock Exchange of India Limited and BSE Limited in cash and derivatives segments. It is

also a registered Portfolio Manager having registration no as INP000002981.

NBSPL has other business divisions with independent research teams separated by Chinese walls, and therefore may, at times, have

different or contrary views on stocks and markets.

NBSPL or its associates have not been debarred / suspended by SEBI or any other regulatory authority for accessing / dealing in

securities Market. NBSPL, its associates or analyst or his relatives do not hold any financial interest in the subject company. NBSPL or

its associates or Analyst do not have any conflict or material conflict of interest at the time of publication of the research report with

the subject company. NBSPL or its associates or Analyst or his relatives hold / do not hold beneficial ownership of 1% or more in the

subject company at the end of the month immediately preceding the date of publication of this research report.

NBSPL or its associates / analyst has not received any compensation / managed or co-managed public offering of securities of the

company covered by Analyst during the past twelve months. NBSPL or its associates have not received any compensation or other

benefits from the company covered by Analyst or third party in connection with the research report. Analyst has not served as an

officer, director or employee of Subject Company and NBSPL / analyst has not been engaged in market making activity of the subject

company.

Analyst Certification: I/We, Jehan Bhadha and Dnyanada Vaidya, the research analysts and authors of this report, hereby certify that

the views expressed in this research report accurately reflects my/our personal views about the subject securities, issuers, products,

sectors or industries. It is also certified that no part of the compensation of the analyst(s) was, is, or will be directly or indirectly

related to the inclusion of specific recommendations or views in this research. The analyst(s) principally responsible for the

preparation of this research report and has taken reasonable care to achieve and maintain independence and objectivity in

making any recommendations.

19 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

Disclaimer:

This report is for the personal information of the authorized recipient and does not construe to be any investment, legal or

taxation advice to you. NBSPL is not soliciting any action based upon it. Nothing in this research shall be construed as a

solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any such transaction. In

preparing this research, we did not take into account the investment objectives, financial situation and particular needs of

the reader.

This research has been prepared for the general use of the clients of NBSPL and must not be copied, either in whole or in

part, or distributed or redistributed to any other person in any form. If you are not the intended recipient you must not use

or disclose the information in this research in any way. Though disseminated to all the customers simultaneously, not all

customers may receive this report at the same time. NBSPL will not treat recipients as customers by virtue of their receiving

this report. This report is not directed or intended for distribution to or use by any person or entity resident in a state,

country or any jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or

which would subject NBSPL & its group companies to registration or licensing requirements within such jurisdictions.

The report is based on the information obtained from sources believed to be reliable, but we do not make any representation

or warranty that it is accurate, complete or up-to-date and it should not be relied upon as such. We accept no obligation to

correct or update the information or opinions in it. NBSPL or any of its affiliates or employees shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in

this report. NBSPL or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any

kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability,

fitness for a particular purpose, and non-infringement. The recipients of this report should rely on their own investigations.

This information is subject to change without any prior notice. NBSPL reserves its absolute discretion and right to make or

refrain from making modifications and alterations to this statement from time to time. Nevertheless, NBSPL is committed to

providing independent and transparent recommendations to its clients, and would be happy to provide information in

response to specific client queries.

Before making an investment decision on the basis of this research, the reader needs to consider, with or without the

assistance of an adviser, whether the advice is appropriate in light of their particular investment needs, objectives and

financial circumstances. There are risks involved in securities trading. The price of securities can and does fluctuate, and an

individual security may even become valueless. International investors are reminded of the additional risks inherent in

international investments, such as currency fluctuations and international stock market or economic conditions, which may

adversely affect the value of the investment. Opinions expressed are subject to change without any notice. Neither the

company nor the director or the employees of NBSPL accept any liability whatsoever for any direct, indirect, consequential or

other loss arising from any use of this research and/or further communication in relation to this research. Here it may be

noted that neither NBSPL, nor its directors, employees, agents or representatives shall be liable for any damages whether

direct or indirect, incidental, special or consequential including lost revenue or lost profit that may arise from or in

connection with the use of the information contained in this report.

Copyright of this document vests exclusively with NBSPL. Our reports are also available on our website www.nirmalbang.com

20 |

P a g e

Init

iati

ng

Co

ve

rag

e

tia

tin

g C

ov

era

ge

Karur Vysya Bank Ltd.

In

itia

tin

g c

ov

era

ge

03

De

c 2

01

8

Nirmal Bang Research (Division of Nirmal Bang Securities Pvt. Ltd.)

B-2, 301/302, Marathon Innova,

Opp. Peninsula Corporate Park

Off. Ganpatrao Kadam Marg

Lower Parel (W), Mumbai-400013

Board No. : 91 22 6723 8000/8001

Fax. : 022 6723 8010