structured products & financial engineering - imarticus.org study... · structured products...

TRANSCRIPT

Structured Products &

Financial Engineering The Practical Applications of

Financial Innovation

Day 1 Rajat Bhatia

Session 4: Real Life Complex Structured Deals

© RAJAT BHATIA 3

Agenda

In this session, you will learn about: • Practical Application of How to Use a Complex Cross-asset Barrier Option to Help a Client

Reduce their Cost of Hedging Jet Fuel, Interest rate

and Foreign Exchange Risks in an Integrated

Manner.

• Structured Products Proposed by a Leading

Investment Bank to a Major Airline in India will be

discussed.

• Practical Illustration of how a Major Global

Investment Bank Designed a New Bond Issue for a

Sovereign Issuer Along with the Use of Asset Swaps

to Identify Market Mis-pricings, thereby Creating

an Arbitrage.

• The Case of Republic of Italy’s US Dollar Bond Issue along with a Tender Offer to Buy-back Bonds

Issued in Other Currencies will be Discussed.

© RAJAT BHATIA 4

Decoding a Flight

Decoding Airline

Profitability

© RAJAT BHATIA 5

Jet Fuel is 34% of the Total Operating Cost of an Airline

The Airline industry spent more than

34% of its revenue

on Jet Fuel. Oliver Wyman research

It takes the fares of more

than 1/3rd of

passengers on a flight to pay for the gas

© RAJAT BHATIA 6

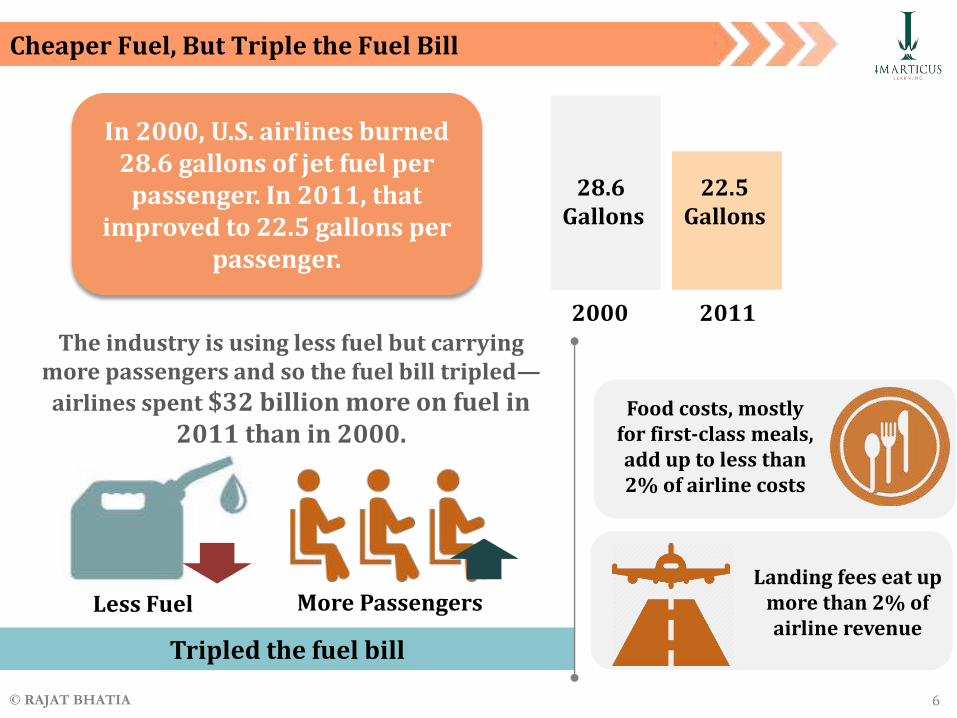

Tripled the fuel bill

Cheaper Fuel, But Triple the Fuel Bill

In 2000, U.S. airlines burned 28.6 gallons of jet fuel per

passenger. In 2011, that improved to 22.5 gallons per

passenger.

2000

28.6 Gallons

2011

22.5 Gallons

Less Fuel More Passengers

The industry is using less fuel but carrying more passengers and so the fuel bill tripled—airlines spent $32 billion more on fuel in

2011 than in 2000. Food costs, mostly

for first-class meals, add up to less than 2% of airline costs

Landing fees eat up more than 2% of airline revenue

© RAJAT BHATIA 7

According to Airlines for America®, rising Jet Fuel prices contributed to industry-wide annual losses of:

The sharp increase in the price of jet fuel in 2008 was the chief contributor to airline industry losses of about $4.3 billion in the first three quarters of 2008

Rising Jet Fuel Prices are a Key Contributor to Airline Losses

$3.6 billion in

2003

$9.1 billion in

2004

$5.7 billion in

2005

$9.5 billion in

2008

© RAJAT BHATIA 8

Singapore Airlines - Consolidated Income Statement

Fuel costs are the single largest Operating Expense accounting for nearly one-

third of all Operating Expenses of Singapore

Airlines

© RAJAT BHATIA 9

Singapore Airlines: Jet Fuel Price Risk

© RAJAT BHATIA 10

Impact of Jet Fuel Price on Airlines’ Profitability

An increase in price of one USD per barrel of jet fuel affects the annual fuel costs of

Singapore Airlines by $50 million.

$50 Million

Annual Fuel Costs

$1 per barrel

The Group manages this fuel price risk by using jet

fuel swap, option and collar, Brent swap and

crack swap contracts and hedging up to eight quarters forward.

© RAJAT BHATIA 11

Impact of Jet Fuel Price on Airlines’ Profitability

Singapore Airlines had hedged Jet Fuel at an average of $116 per barrel when spot market

rates had fallen to $85 per barrel in 2014.

Spot Market

Rate: $85

Hedged at an

average: $116

Singapore Airlines operating profit fell to S$146.3 million in October-December 2014 from S$151 million a year earlier.

October-December

2013

S$151 million

S$146.3 million

October-December

2014

The result was below an average forecast of S$169.4 million in a Reuters survey of five analysts.

© RAJAT BHATIA 12

Impact of Jet Fuel Price on Airlines’ Profitability

The group had hedged 65 percent of its jet fuel requirements at an average price of $116 per barrel,

leading to a hedging loss of $216 million.

Hedged

65% of its fuel

reqs.

Hedging Loss

$216 million

© RAJAT BHATIA 13

Impact of Jet Fuel Price on Airlines’ Profitability

Singapore Airlines had seen a drop of $105 million (-7.9%) in its Operating Profits from $1.317 Billion in 2005 to $1.213 Billion in 2006 mainly due to rise in higher

jet fuel price.

2005

$1.317 Billion

$1.213 Billion

2006

From this, one can see the profitability of the group lies mainly on its hedging strategy for Jet Fuel Oil Price Risk.

Dropped $105 million (-7.9%)

© RAJAT BHATIA 14

Bankruptcies from Rising Jet Fuel Oil Prices

This shows that management of jet fuel price risk is essential because it is: • Known to be highly volatile and

• Represents a third of Operating Costs

Long list of Airlines that have failed due to rising jet fuel prices

Oil prices going above US$ 100 per

barrel

Within three weeks

Four major airlines in America failed within three weeks of oil prices going

above US$ 100 per barrel • Aloha Airlines – stopped operations on 31

March 2008 • ATA – Filed for Chapter 11 on 2 April 2008 • Skybus - Halted operations on 5 April

2008 • Fronter Airlines – Filed for Chapter 11 on

11 April 2008 • Champion Air – Halted all flights on 31

May 2008

© RAJAT BHATIA 15

Singapore Airlines: Probability of Default

1-year probability of default (PD) for Singapore Airlines (SIA)

against the 1-year aggregate default probability of global airlines.

The near zero probability of default of Singapore Airlines is due to: • A low 3 month SIBOR (Singapore Interbank Offered Rate) rate of 0.37% • Large cash to total asset ratio • Effective jet fuel price risk management

© RAJAT BHATIA 16

Jet Fuel: A Major Risk Factor for All Airlines

• Hedged airlines are better positioned to take advantage of investment opportunities during periods of high jet fuel prices.

• Academic studies have shown that effective jet fuel price risk management increases the value of the firm.

Jet Fuel cost is a major risk factor for all Airlines as it accounts for a third of operating expenses

© RAJAT BHATIA 17

Singapore Airlines Jet Fuel Price Risk

Net fair value gain:

$82.2m

© RAJAT BHATIA 18

Singapore Airlines Foreign Currency Risk

65% of total revenue

69% of total operating

expenses

Foreign currency accounts for:

© RAJAT BHATIA 19

Singapore Airlines Foreign Currency Risk

The Group’s largest exposures are from: • USD • Euro • UK Sterling Pound • Swiss Franc • Australian Dollar • New Zealand Dollar

• Japanese Yen • Indian Rupee • Hong Kong Dollar • Chinese Yuan • Korean Won • Malaysian Ringgit

• Singapore Airlines generates a surplus in all of these currencies, with the exception of USD.

• The deficit in USD is attributable to capital expenditure, fuel costs and aircraft leasing costs – all conventionally denominated and payable in USD.

© RAJAT BHATIA 20

How SIA Manages its Currency Risk

Singapore Airlines manages its foreign

exchange exposure by matching, as far as

possible, receipts and payments in each

individual currency.

The Group also uses forward

foreign currency contracts to hedge

a portion of its future foreign

exchange exposure.

Such contracts provide for the group to sell currencies at

predetermined forward rates, with

settlement dates that range from one month

up to one year.

The Group uses forward

contracts purely as a

hedging tool.

© RAJAT BHATIA 21

Singapore Airlines Interest Rate Risk

Long-Term liabilities • Singapore Airlines leases are charged at LIBOR + 3.19% to 5.18% • SIA Cargo’s leases are charged at LIBOR + 2.88% to 4.74%

© RAJAT BHATIA 22

Singapore Airlines Interest Rate Risk

Non-equity Investments

382.4 million of interest-bearing investments with an

effective annual interest rate of 3.97%

© RAJAT BHATIA 23

The Flip Side of Cheap Oil : Costly Hedges

Some major U.S. airlines including Delta and Southwest are rushing to finance losing bets on oil and revamp fuel hedges as tumbling crude prices leave them with billions of dollars in losses.

© RAJAT BHATIA 24

The Flip Side of Cheap Oil: Costly Hedges

In theory, airlines are among the top

beneficiaries of a six-month slump that

halved crude prices to five-year lows..…. …..But the reality is

different.

© RAJAT BHATIA 25

The Flip Side of Cheap Oil : Costly Hedges

Now, carriers such as Delta and even Southwest Airlines, known for a successful hedging program that locked in cheap fuel prices before they rose a decade ago,

see the benefits of cheap fuel eaten away by hedging costs.

Delta had a $1.7 billion gain from lower fuel prices in

2015 but $1.2 billion in jet fuel hedge losses.

American Airlines, which has not entered any hedge

contracts since late 2013, saw a greater boost to its

bottom line.

vs

© RAJAT BHATIA 26

The Flip Side of Cheap Oil: Costly Hedges

Selling financial options that pay off when oil prices fall

Using the proceeds to buy protection against soaring

fuel costs

That is largely because they have used common but risky hedging strategies, among them a "costless collar":

SELL

BUY

With oil prices tumbling faster and further than anticipated, the collar hedges left airlines

with insurance against high costs they no longer need and on the hook for protection

they sold against a further slide.

© RAJAT BHATIA 27

Is the Costless Collar Really Without Costs?

Jet Fuel Collars looked great when Jet Fuel prices hovered around $100 per barrel for most of the past four years, allowing airlines to cap their fuel costs

without having to pay upfront for the options.

$100 per

barrel

"Costless collars are an effective strategy that works best when prices stay within a range…. …. but it becomes a very different animal when the market goes against that.

© RAJAT BHATIA 28

Is the Costless Collar Really Without Costs?

At Southwest, the world's biggest low-cost carrier, a 25 percent decline of Jet Fuel prices would force it to pay $615 million while Delta would pay $800 million to counterparties if oil fell 20 percent.

Would Pay

$615 million

25% drop in jet fuel

Would Pay

$800 million

20% drop in jet fuel

In reality, Brent has tumbled

more than 50%

© RAJAT BHATIA 29

Is the Costless Collar Really Without Costs?

Save about

80 cents

Save only 60

cents

These hedges weigh on the costs of their future fuel consumption, too.

For every $1 fall in oil prices:

Will reap the full

benefit of cheap fuel

© RAJAT BHATIA 30

Gambling Without a Clear Game Plan

Fuel hedging is a common, yet not always successful, way for airlines to mitigate volatile oil prices. But if well constructed, it need not be an unduly risky strategy.

© RAJAT BHATIA 31

Gambling Without a Clear Game Plan

Emirates Airline fuel risk management program – more accurately described as an oil hedging strategy.

Had saved

$1 billion over eight years

Emirates had to write down annual fuel hedging losses of

US$428 million 2008-2009

© RAJAT BHATIA 32

Gambling Without a Clear Game Plan

This mistake was repeated in airline boardrooms around the world.

In Dublin, shortly after admitting he had screwed up by not hedging when oil was cheap, Ryanair chief executive Michael O'Leary belatedly started locking in $120-

plus per barrel prices just as oil began its rapid descent back down to $40.

© RAJAT BHATIA 33

Gambling Without a Clear Game Plan

In China, the risk-averse government was so

furious about the hedging losses incurred

by its airlines that it banned them from

buying crude oil futures.

© RAJAT BHATIA 34

Gambling Without a Clear Game Plan

• Because airlines sell their tickets several months ahead of the date of travel, and because fuel accounts for more than one third of their expenses, there is a pressing need to insulate themselves from unknown future price movements.

• This is exacerbated by the added risk of buying fuel from refineries, whose jet fuel price may not move in tandem with the underlying price of crude oil.

Airlines sell their tickets several months ahead of the

date of travel

Fuel accounts for more than one third of their

expenses

Pressing need to insulate themselves from unknown

future price movements

1/3rd Of expenses

© RAJAT BHATIA 35

Gambling Without a Clear Game Plan

There was a fear that oil prices were going to go to $200 or $300 a barrel. The fear of being exposed to $200 a barrel was so great that a lot of people convinced themselves prices could

not decline.

Prices were rising so fast that many airlines started hedging without even really thinking about it. It became an emotional, rather than an analytical, decision.

$200 or $300 a barrel

© RAJAT BHATIA 36

Dual, (Hybrid, Outside or Rainbow) Barrier Options

In a Dual Barrier (also known as a Hybrid or Outside Barrier or Rainbow Barrier) Option, the Option Pay off is based on one asset (known as the Pay-off Asset) but the knock-in or knock-out is determined by movements of a different asset (known as the Barrier Asset)

Asset S1

(Pay off asset)

Knock-In or Knock-Out

Option Payoff

Asset S2 (Barrier Asset)

© RAJAT BHATIA 37

Hedging Jet Fuel Price Risk using Hybrid Barrier Options

1

3 2

An Airline

has exposure

to three

major

variables

Jet Fuel Prices (the most critical

determinant of Operating Profits)

Interest Rates Exchange Rates

© RAJAT BHATIA 38

Hedging Jet Fuel Price Risk using Hybrid Barrier Options

The Airline has some intrinsic hedges built into its business, which it can use to construct low cost option strategies without taking on undue risks:

• This is a less expensive hedge than an outright Jet Fuel price cap.

• Yet it offers protection when the Airline is impacted by BOTH higher fuel prices and higher interest rates.

• If Jet Fuel Prices rise but Interest Rates fall, their affect on profitability is offset by each other.

A Jet Fuel Option that knocks-out when interest rates fall

• Again this is a less expensive hedge than an outright Jet Fuel price cap.

• Yet it offers protection when the Airline is impacted by BOTH higher fuel prices and adverse Exchange Rates.

• If Jet Fuel Prices rise but Exchange Rates move adversely, their affect on profitability is offset by each other.

A Jet Fuel Option that knocks-out when Exchange rates move in a

favorable direction

© RAJAT BHATIA 39

Hybrid Barrier Option Strategies for Airlines

Higher Jet Fuel

Lower Interest Rates

Higher Jet Fuel

Favorable FX Rates

Higher Interest Rates

Favorable FX Rates

Buy a Jet Fuel Call which knocks-out when

interest rates fall

Buy a Jet Fuel Call which knocks-out when FX rates

are favorable

Buy an Interest Rate Cap which knocks-out when FX

rates are favorable

Higher Interest Rates

Lower Jet Fuel

Higher Jet Fuel

Adverse FX Rates

Higher Jet Fuel

Adverse Interest Rates

Buy am Interest Rate Cap which knocks-out

when Jet Fuel falls

Buy a Jet Fuel Call which knocks-in when FX rates

are adverse

Buy an Interest Rate Cap which knocks-in when

Interest rates are adverse

© RAJAT BHATIA 40

The Link between Crude Oil Price and US$ Exchange Rate

© RAJAT BHATIA 41

Correlation of Oil and the US Dollar Exchange Rate

Correlation of oil prices and the US Dollar nominal effective exchange rate computed over 6-month moving windows

© RAJAT BHATIA 42

Daily Return on Crude Oil Futures & Financial Investments

Correlations between daily returns on crude oil futures and financial investments

• Oil prices are negatively correlated to the US dollar exchange rate • Oil prices have tended to move in the opposite direction of US Treasury bonds • Oil prices and the S&P 500 have tended to move together • Oil prices are positively correlated with Inflation Expectations

1 U.S. Dollar Index (DXY), which is a weighted index of a basket of currencies, per U.S. dollar. As the dollar strengthens against other currencies, the value of the index rises. 2 U.S. bonds is based on the negative of the change in yield on 30-year U.S. government bonds because as yields rise, bond prices fall. 3 Inflation Expectations are based on daily changes in the 5 year Treasury - TIPS (Treasury Inflation Protected Securities) spread.

© RAJAT BHATIA 43

Rolling Correlation between Exchange Rates and Oil Prices

Rolling correlation between exchange rates and oil prices over time

12-month rolling average correlation between the log-difference of the effective US$ exchange rate and WTI crude oil prices using daily data

from 2 January 1986 to 19 October 2012

Source: European Central Bank working paper on oil Prices, exchange rates and asset Prices by Fratzscher,

Schneider and Van Robays

© RAJAT BHATIA 44

Correlation between US$ Exchange Rates and Oil Prices

Jan 2001 - Oct 2012 Correlation = -0.729

Jan 1986 - Dec 2000 Correlation = -0.226

US Dollar exchange rates

Oil Prices Oil Prices

US Dollar exchange rates

Source: European Central Bank working paper on oil Prices, exchange rates and asset Prices by Fratzscher,

Schneider and Van Robays

© RAJAT BHATIA 45

Relationship between Oil Prices & US$ Exchange Rates

Several hypotheses have been offered that tend to support an

inverse relationship between the exchange value of the dollar relative to other currencies

and crude oil prices.

© RAJAT BHATIA 46

Reasons for Inverse Relationship

Oil benchmarks are traditionally priced in U.S. dollars. A depreciation of the dollar decreases the effective price of oil

outside the United States. This decreased cost may increase consumers' demand for oil, adding upward pressure to prices.

Reason 1

Oil benchmarks are traditionally priced

in U.S. dollars.

Depreciation in Dollar

Decreases the effective price of oil

outside the US

Increased demand for Oil

Upward pressure to prices

© RAJAT BHATIA 47

Reasons for Inverse Relationship

U.S. dollar depreciation will decrease the effective profits of non-U.S. producers, when converted into foreign currencies.

Reason 2

• To counteract this, these countries may target higher dollar prices of oil to maintain real revenue, budget levels, and purchasing power in world markets.

• Dollar depreciation also reduces the returns on dollar-denominated assets, when measured in foreign currencies, which may increase the attractiveness of foreign investing in commodities like oil.

• Commodity investment may also become more attractive to U.S. investors as a hedge against inflation if dollar depreciation tends to increase expectations of greater inflation.

Depreciation in Dollar

GBP

Yen

Rupee

When Converted to Foreign Currencies

Decreased Effective Profit

© RAJAT BHATIA 48

Reasons for Inverse Relationship

A rise in oil prices also expands the U.S. trade imbalance, which can put additional downward pressures on the dollar, again yielding a

negative correlation albeit with causation going in the reverse direction.

Reason 3

Despite these many possible explanations, the actual correlation between oil prices and exchange rates has not been stable over time, and was close to zero for more than half

of the last decade.

Rise in Oil Prices

Expands US Trade Imbalance

Downward pressure on Dollar

Note: