strategic evaluation -...

TRANSCRIPT

STRATEGIC EVALUATION

CITIGROUP, INC.

MGMT-780: STRATEGIC MANAGEMENT

Professor Patrick Saparito

March 28, 2009

Forza 1

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

STRATEGIC EVALUATION: CITIGROUP INC.

Team Forza

Iman Jones

Anthony Kanoff

Colleen McDonough

Jason Nyzio

Brett Summerville

EMBA, Cohort XVI, Class of 2009

LeBow College of Business, Drexel University

Prof. Patrick Saparito, Ph.D.

MGMT-780, Strategic Management

March 27, 2009 [Class #8]

Forza 2

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Table of Contents

Abstract ..................................................................................................................................................................... 3

Strategic Evaluation: Citigroup Inc. ................................................................................................................ 4

Citigroup’s Environmental Threats & Opportunities .............................................................................. 7

Citigroup’s Strengths & Weaknesses ............................................................................................................. 8

Cost Leadership & Product Differentiation Strategies ......................................................................... 11

Citigroup’s Cost Leadership ........................................................................................................................... 11

Citigroup’s Product Differentiation ............................................................................................................. 13

Organizational Architecture ........................................................................................................................... 16

CEO Influence on Citigroup’s strategy ........................................................................................................ 18

Sanford “Sandy” I. Weill - CEO Citigroup 1998-2003 ........................................................................... 18

Charles Prince - CEO Citigroup 2003-2006 .............................................................................................. 20

Vikram S. Pandit - CEO Citigroup 2006-Present ..................................................................................... 23

Conclusion ............................................................................................................................................................. 26

Forza 3

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Abstract This paper will take an in-depth strategic examination and analysis of the international banking

firm, Citgroup, Inc. (Citi). The paper will provide an overview of Citi’s past and present

initiatives and how the initiatives guided the company to where it is today. Lastly, this paper will

dissect the company’s threats and weaknesses evident during the presently turbulent economic

environment and deepening global recession, as well as, offer possible remedies to mitigate risk

and capitalize on financial opportunities.

Forza 4

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Strategic Evaluation: Citigroup Inc. Citigroup Inc. (Citi) is the most diversified financial services company in the world.

Datamonitori states that Citi’s product portfolio includes retail banking, corporate banking,

investment banking and asset management. The firm has operations in 100 countries across

North America, Latin America, Asia, Europe, the Middle East and Africa. Citi is headquartered

in New York City and employs over 300,000 people. Citigroup Inc’s New York Stock Exchange

ticker is “C.” This paper will discuss Citi’s corporate profile and the unique strategic issues that

face the firm today.

Citigroup’s Strategy Citigroup does not clearly state its umbrella corporate strategy publicly. Jay Barneyii

states, “…a firm’s strategy is its theory of how to achieve high levels of performance in the

markets and industries within which it is operating.” A review of Citi’s evolution reveals a

pattern of Citi’s executed strategy to achieve high levels of performance in its target markets.

Citi appears to aspire to be all things to all parties in the financial market. Through a rapid

series of acquisitions, Citi expanded its portfolio of financial services to be the biggest and

broadest with the widest global reach. To develop its strategic competitive advantage, Citi has

organized itself into four major business segments: Consumer Banking, Global Cards,

Institutional Clients Group, and Global Wealth Management.iii Each business segment consists of

numerous financial services (Appendix A).

The current global banking industry crash and subsequent economic crisis has blown

apart Citi’s strategy to achieve competitive advantage. Using Barney’s test of a firm’s strategy;

Citi’s performance has been dismal. Over the past year, the firm’s stock has declined from its

52-week high on April 28, 2008, of $27.35 to a low of $0.97 per share on March, 5, 2009. The

stock has recovered from its “penny” status to $1.45 on March 10, 2009 and $2.81 by March

26, 2009. (Appendix B).iv Clearly Citi has not been alone in the plummet of its stock price. As a

point of comparison, however, the S&P500 index dropped 45.5%; whereas, Citi’s stock lost

93.3% of its value over the same time period (Appendix C).v Clearly, Citi’s previous strategy has

not enabled the firm to weather the recent financial storm without incurring serious damage.

As a result, the banking giant’s present strategy is simple—remain solvent by making the best of

whatever assistance the US government is willing to offer. As of the time of this writing,

Forza 5

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Citigroup has not failed; but the financial environment is changing by the minute—largely due to

decisions the government is making.

Perhaps in Citigroup’s case, it is appropriate to apply “Mintzberg’s Analysis of the

Relationship Between Intended and Realized Strategies.”vi Mintzberg helps visualize a firm’s

strategy which emerges over time or those that have been radically reshaped once they are

initially implemented. Citi’s strategy for competitive advantage has certainly been reshaped by

extraordinary events over the past year. Based on Mintzberg’s model, the relationship between

Citi’s intended and realized strategies is depicted in Figure 1.

Citi’s Relationship Between Intended and Realized Strategies

Figure 1

As mentioned, Citi’s near-term strategy is to remain solvent. The firm wants to recover

shareholder equity and regain investor confidence. The executive team wants to remain

employed through the recovery process. Stating opinion on a long-term strategy would be pure

speculation and completely unquantifiable given the firm’s grave situation and numerous

environmental factors that are completely out of it’s control. Citi is, however, executing the

following tactics in order to achieve its near-term objectives:

Forza 6

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Cooperate with the US Government

Government Economic Stimulus: Citi’s strategic plan includes an incredible amount

of reliance on positive results from the Obama administration’s efforts to stimulate the

economy. The administration’s plan was unveiled in the middle of February of this year.

Unfortunately, so far the much-anticipated plan has not helped struggling homeowners stave off

foreclosures and has failed to give US stocks a boost.vii During the week following the

announcement of the governmental plan, the financial sector finished little changed. The largest

banks, Citigroup and Bank of America, were two key losers, down 4.9 per cent to $2.91 and

6.7 per cent to $4.57, respectively.

Reorganize its Financial Structure

Raise Cash: Citi’s short term strategy is to sell off assets to raise cash in an attempt to

calm investors who are concerned the bank may become insolvent. Investors’ anxiety is

certainly valid. For example, Citi’s current Liabilities-to-Equity ratio of 15.26 (End of Q308 -

$1.924T Total Liabilities / $126.06B Equity) is relatively high (and therefore bad) in terms of the

proportion of profit produced relative to debt payment commitments. The company is not

solvent enough to service any additional debt without greatly increasing its equity or lowering

its liabilities.

Reduce Assets and Expenses: Citi’s spokesman Jon Diat said in an emailed statement

that the bank's capital base is "very strong" and its Tier-1 capital ratio is "among the highest in

the industry. "Diat added, "We continue to focus and make progress on reducing the assets on

our balance sheet, reducing expenses and streamlining our business for future profitable

growth." viii

Reorganize to Isolate High-Risk Business: Citi has separated its higher risk US

consumer finance and securities businesses from its global commercial banking operations in an

attempt to isolate its so-called “toxic” assets.ix People close to the situation said Citi would

place unwanted assets and businesses worth more than $600bn – a third of its balance sheet –

into a “non-core” unit to isolate them from healthier parts of the company.

Re-Open Credit Lines: Citi’s strategy is to reopen its credit lines but doing so hinges

on other banks doing the same. The interbank lending channels are virtually non-existent at this

Forza 7

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

time but signs are beginning to show that these channels are slowly working their way back.

The media has even accused banks of pocketing the government bailout money to cushion

balance sheets or snap up rivals, rather than re-opening credit lines to hard-pressed businesses

and consumers. Banks are under pressure to improve risk calculations and tighten lending

qualifications in order to build consumer confidence.

Change the Leadership Team

Board: Citi appointed a new Chairman, Mr. Parsons, on January 20, 2009. Parsons

announced that Citi’s 15-strong board could see two or three changes in coming months as

long-standing directors retire.

Management Team: Parsons plans to leave Citi’s management team intact. Although

there is a lack of shareholder confidence in retained Chief Executive, Vikram Pandit, Mr Parsons

reiterated board support for Mr [Vikram] Pandit who has come under fire from some investors

for his surprise decision to split Citi in two after pledging the company would not be broken

up. “To change management is the furthest thing from our mind,” Parsons said. “We believe

this management has its arms around the future.” x

Citigroup’s Environmental Threats & Opportunities

Citi’s past strategy to build competitive strategy was to position the firm with

economies of scale and a global presence. The strategy enabled Citi to combat the following

five primary environmental threats: 1) threat of entry, 2) rivalry, 3) buyers, 4) substitutes, and

5) suppliers. Citi’s strategy was to build a cost leadership position in order to mitigate

substantial threats in its industry (Appendix D).

Today, however, the success of its past expansion strategy could prove to be Citi’s

biggest liability. For example. As a result of the present financial crisis, investors appear to have

changed mindset and feel that big, diversified financial institutions, such as Citi, may not be as

attractive an investment as it was once thought.

The US Government does not appear to be willing to let Citi fail. The government’s

actions could present an opportunity for Citi to cleanse its balance sheet and gain market share.

The banking infrastructure is in disarray and ripe for massive failures and consolidations; which

will offer an opportunity to those banks still standing after the dust has settled.

Forza 8

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Citigroup’s Strengths & Weaknesses

Assessing Citi’s Strengths and Weaknesses in the present state of the financial markets

and the global economy is difficult. Just as previously considered threats could quickly become

opportunities for the firm, its past strengths could prove to be major weaknesses. Attributes

currently considered as strengths or weaknesses will most likely fail to stand the test of time,

however, the following aspects are noteworthy as possible contributing factors to Citi’s

survival.

Strengths

Although time will tell, Citi’s new chairman, Dick Parsons, could prove to provide

strength to the organization. Parsons has experience in managing through recessionary periods.

Parsons also has a relationship with President Obama. Parsons stated publically, “I lived through

the first crisis [when he ran Dime Bank, a small lender, between 1991 and 1995]. I remember

one of the keys to bottoming out of the crisis was the presence of the RTC… We now need

something along those lines.” xi

The second major strength possessed by Citi is the commitment the US

government appears to have to helping Citi survive the global financial crisis and

economic recession. “In a sign of how deeply the financial crisis has transformed America,

Republicans who embrace the sanctity of free markets are supporting some form of a U.S.

government takeover of increasingly insolvent banks. Alan Greenspan may have given

Republicans the political cover they need to consider nationalizing U.S. banks when the former

Federal Reserve chairman joined a growing list of experts who suggest nationalization is

inevitable.” xii

Weaknesses

Citi’s main weakness is due to its highly leveraged financial situation. The firm does not

have the flexibility to make new loans. Citi and other banks have argued that in the economic

conditions it is difficult to make loans to companies and individuals as most new lending would

be loss-making and end up burdening their balance sheets with further write-downs. “Today it

is cheaper to buy a loan in the secondary market than to make one,” Vikram Pandit, Citi’s chief

executive, recently told Wall Street analysts.xiii

Forza 9

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Citi is in survival mode and as a result does not have a clear mission or strategy. The

firm risks losing its identity while trying to correct course. “The creation of Citigroup as an all-

purpose financial supermarket and too-big-to-fail banking marvel was very much the

accomplishment of Clinton Democrats. They enacted the law in the late 1990s that authorized

this megabank monstrosity, with coaching from Treasury Secretary Robert Rubin, Fed chairman

Alan Greenspan and of course Sanford Weill, the creative genius who built Citigroup.” xiv

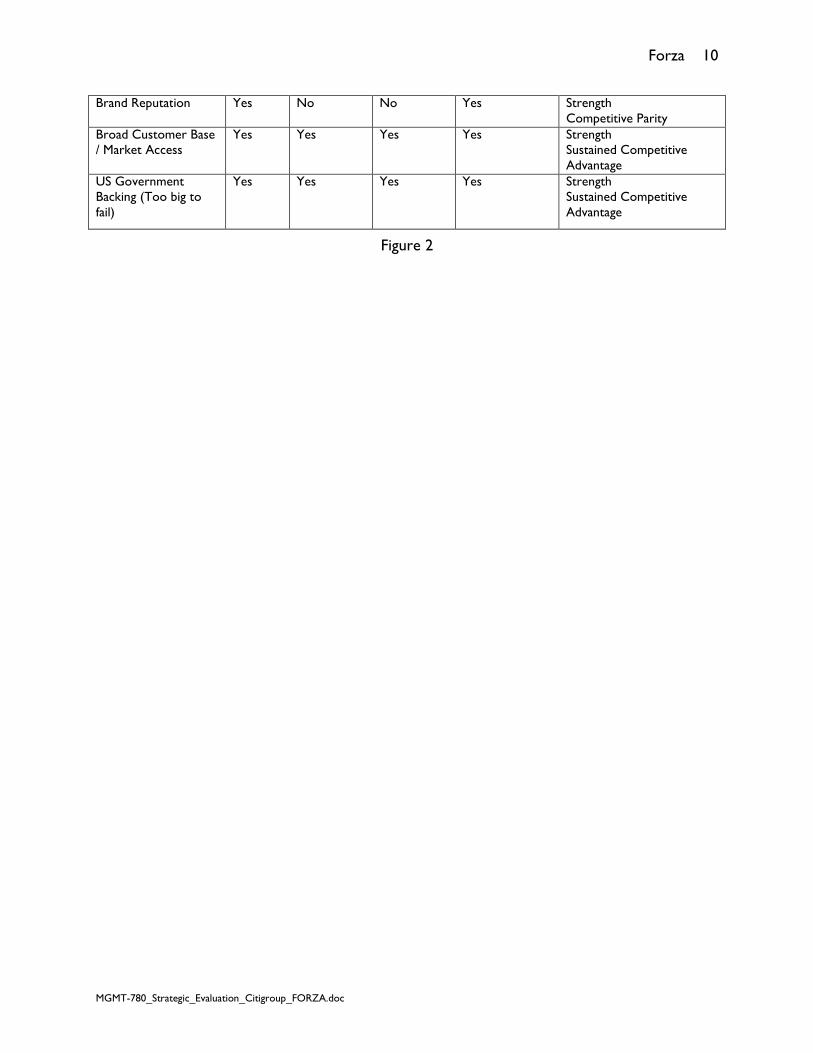

Resource-Based Analysis of Strengths and Weaknesses

As mentioned, Citi’s strategy has been to invest its resources in becoming the largest

financial services provider in the world. The following matrix shows how the firm’s resources

contribute to its present state of competitive advantage. The VRIO matrix (Figure 2) maps

Citi’s resources against the following questions: xv

1. Value: Does Citi’s resources and capabilities enable it to respond to

environmental threats or opportunities?

2. Rarity: Is a resource currently controlled by only a small number of competing

firms?

3. Imitability: Do firms without a resource face a cost disadvantage in obtaining

or developing it?

4. Organization: Are Citi’s other policies and procedures organized to support

the exploration of its valuable, rare, and costly-to-imitate resources?

Citi’s VRIO Frameworkxvi

Resource Valuable? Rare? Costly to Imitate?

Exploited by the Organization?

Strength or Weakness?

Global Presence Yes No Yes Yes Strength Competitive Parity

Broad Product Portfolio

Yes No Yes Yes Strength Competitive Parity

Large Capitalization Yes Yes (Today)

No (Prev.)

Yes (Today)

No (Prev.)

Yes Strength Sustained Competitive Advantage (Today) Competitive Parity (Prev.)

Diverse Employee Organization (Networked local market knowledge)

Yes Yes Yes No (Possibly Underexploited)

Strength Sustained Competitive Advantage

Forza 10

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Brand Reputation Yes No No Yes Strength Competitive Parity

Broad Customer Base / Market Access

Yes Yes Yes Yes Strength Sustained Competitive Advantage

US Government Backing (Too big to fail)

Yes Yes Yes Yes Strength Sustained Competitive Advantage

Figure 2

Forza 11

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Cost Leadership & Product Differentiation Strategies

Citigroup’s decade long cycle from boom to bust had its beginning with the 1998

merger between Travelers Group and Citicorp when Travelers’ CEO Sandy Weill took the

reigns of the combined companies. Weill had a long history of growing companies through

continuous mergers and acquisitions and did not slow down after reeling in Citibank. The

continual growth process became the overriding strategy at Citi. This “supermarket” approach

to differentiation and cost leadership strategies would prove to be ineffective.xvii

In 2002 as Citigroup focused more heavily on a differentiation strategy, Weill

reorganized the company’s approach from the u-structure, primarily used in cost leadership

organizations, to the m-structure (multi-divisional) common in companies dedicated on a

differentiated strategy. As a result of the reorganization, responsibility for strategic decision-

making was distributed over four international managers: three product managers and one

business manager.xviii

As the cracks began to show in late 2006-early 2007, the company started taking the

first steps towards a draw back from expansion. When Pandit took the helm in 2008 he

declared the intention of reviewing all Citigroup’s businesses with an eye towards separating

the strong performers from the under performers, strengthening the balance sheet for better

positioning if a downturn occurred and improving asset allocation through the elimination of

assets that were not pulling their weight and were not vital to strategy.

Citigroup’s Cost Leadership

In the process of becoming the world’s largest “financial supermarket” Citigroup

adopted a growth strategy to “push those businesses where Citigroup can achieve and sustain

dominance”.xix Citigroup became the first bank to provide commercial banking, investment

banking and insurance under one roof. They have maintained this mantra by acquiring an

average of three companies a year to continue their global reach within the financial sector.

Citigroup was allowed to begin acquisitions of investment banks through the repeal of the

Glass-Steagall Act by Congress in 1999. The repeal of this act lifted the restriction barring

traditional banks from affiliations with commercial and investment banks. In 2007, Citigroup

acquired or invested in nine banks across the globe. This rapid string of acquisitions enabled

Citigroup to pursue competitive advantage using “economies of scale” (Appendix E).

Forza 12

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

By December 2008 Citigroup was able to amass almost two trillion dollars in assets and

200 million customersxx. Citigroup has established a network of 22,000 fee-free ATM’s across

the United States including an additional 3,800 ATM’s in 46 countries through multiple

acquisitions. Having such a vast network allows Citigroup customers the flexibility they need as

they travel domestically and abroad without incurring additional ATM fees. They also maintain

lower costs for their customers for all their financial services while continually improving the

services they provide for retail and commercial customers. Since the banking industry is highly

competitive, they must continue to find new ways to retain existing clients while acquiring new

clients. In the past ten years, this has been primarily attempted through a multitude of mergers

and acquisitions.

The US banking industry is an oligopoly where the top four banks: Citigroup, Bank of

America, JP Morgan Chase, and Wells Fargo maintain a market share greater than 27%.xxi Each

of these banks holds more than a trillion dollars worth of assets whereas the number five bank,

HSBC North America Holdings, holds just over $400 billion.

In light of the current financial crisis, one of Citigroup’s key strategies is reducing costs

in order to remain solvent. This is a complete reversal of the growth strategy implemented in

the beginning of the decade. In 2008, Citigroup began a re-engineering project to reduce

headcount by approximately 20,600xxii and a Structural Expense Review “to create a more

streamlined organization, reduce expense growth, and provide investment funds for future

growth initiatives.”xxiii

It will be difficult for Citigroup to sustain a competitive advantage due to the current

upheaval in the banking system and the company’s lack of credibility in the marketplace.

Although the company’s development into a megabank has enabled it to offer relatively cheaper

products, the fact remains that it is not difficult to imitate Citigroup’s strategy, although

competitors will find it is costly to grow organically and/or through acquisitions. One could

argue that Citigroup does not have a cost leadership advantage to begin with so what is there

to sustain? Even if one could successfully argue that Citigroup maintains a cost leadership

position, it will be complex for the company to overcome the perception in the market that it

is nearly insolvent and therefore a risky firm with which to do business. This perception will be

the case until Citigroup, with the government’s assistance of course, strengthens its balance

Forza 13

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

sheet through cost and bad asset reduction and begins to sway public opinion back to the

positive. This could take several years of positive press and a return of confidence.

One area of Citigroup’s cost leadership strategy that may make it difficult and costly to

imitate is its technological software and vast network. Citigroup boasts of a proprietary

network that delivers the highest standards of technology and processesxxiv. Citigroup’s social

complexity and its history of over a century of industry leadership create a barrier to

competitors hoping to deploy similar technology and may enable Citigroup to sustain its

competitive advantage. However, the company’s history of acquisitions leads one to believe that

its technological software is a melting pot of several proprietary technologies without true

integration and ease of use.

Citigroup’s Product Differentiation

When we consider product differentiation in the banking industry, Citigroup has been

an innovator and leader. One hundred and fifteen years ago, Citigroup was the largest bank in

the U.S. and the first major U.S. bank to establish a department for foreign exchange trading. In

1904 the firm introduced traveler’s checks. In 1913 the bank was the first contributor to the

Federal Reserve Bank of New York and in 1921 it was the first major U.S. bank to offer

compound interest on savings accounts. These are just a few of the industry-changing products

and services Citigroup presciently developed in its early years that set the pattern for future

continued growth and game changing innovations.

Fast-forward to today and there are very few ways for banks to differentiate from the

competition. Citigroup is a diversified financial services company with businesses that provide a

wide range of services to consumer and corporate customers globally. As mentioned earlier,

Citigroup is organized and offers products and service in four major segments – Consumer

Banking, Global Cards, Institutional Clients Group, and Global Wealth Management (Appendix

A). Citigroup’s unique competitive advantage is to maintain a strong presence in emerging

markets. Currently, there are four main regions in which Citigroup operates: 1) North

America; 2) Latin America; 3) Asia; and 4) Europe, Middle East, Africa (EMEA). Again, the

complexity of its broad based, internationally focused organization serves to protect it from

competition by making it difficult to imitate.

Forza 14

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

2007 was an eventful year for Citigroup. As the subprime mortgage crisis began to

unfold, the firm continued to expandxxv and differentiate its product portfolio from its

competitors. In 2007 Citigroup acquired ten companies (Appendix F).

But by mid-2008, the U.S. financial crisis was taking its toll on Citigroup. Survival was

beginning to appear as the primary competitive advantage over other large banks. In a complete

about-face Citigroup executed divestitures and discontinued operations for seven of its

businessesxxvi (Appendix G).

Citigroup management believes that a realignment of the organization will position the

Company’s global businesses for future growth and opportunities. On January 16, 2009, Citi

officially announced a restructure to divide the company into two businesses effective the

second quarter of 2009:

Citicorp, a global bank for consumers and businesses, will have two primary underlying

businesses: Citigroup’s regional consumer banks which provide traditional banking services,

including branded cards as well as small and mid-market commercial banking; and the Global

Institutional Bank servicing private banking, corporate, institutional, and the public sector

clients.

Citi Holdings, will have three segments: brokerage and asset management, local

consumer finance and a special asset pool. Citi Holdings will continue to focus on risk

management and credit quality as it seeks to increase value in these businesses. It is Citigroup’s

opinion that the majority of the businesses in Citi Holdings are viable long-term companies with

strong market positions but that they will not add strength to the capabilities of Citigroup’s

core business model.

The perceived economic value of Citigroup, linked to its unique position among banks as

being too big to fail, was evidenced by the impact it had on the New York Stock Exchange on

March 10, 2009. After reporting a profit for the first two months of the year, shares soared 38

percent – which was enough information to help power Wall Street to its best day of 2009

with a gain of 7%. Of course, it will not be known until the first quarter report is released

whether this black will turn to red once further write-downs are taken. This bounce in public

confidence could quickly erode on news of a quarterly loss.

Forza 15

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Citigroup’s strategy of survival will work only if it is able to successfully sway public

opinion once the industry completes the shakeout. The fact that the government also considers

the company too big to fail is evidenced by the fact that the administration was willing to

acquire almost 40% of the company. Smaller, regional banks will be dependant on additional

government bailouts to be competitive with Citigroup’s capital structure.

Forza 16

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Organizational Architecture

The following summarizes the organizational tactics Citigroup executed in order to

successfully blend its cost leadership strategy with its product differentiation strategy since

approximately 2006.

2006 - 2008

Organizational Structure

• Pandit proposed to maintain the matrixed organization in spite of realizing

potential to create confusion

• Dump non-core operations-American community lending and leasing

• Focus on four lines of business-credit cards, wealth management, corporate

banking and investment banking

• Acquired British firm Egg Bank the world’s largest pure online bank

• Acquired Automated Trading Desk (ATD) an industry leader in electronic

market making and proprietary tradingxxvii

• Remain innovative to improve customer relationships-quick response, effective

communications, simplified transactions and faster innovation

• Reengineer expense management

Management Control Systems

• New executive hired to focus on cost cutting

• Create new Chief Risk Officer position

• Eliminate low-return, non-strategic assetsxxviii

• Continue to develop a broad product portfolio

• Extend retail consumer services: banking, lending, card services and investment

services

• Create new Chief Talent Officer

Forza 17

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

• Position business to capture global trends and to meet the anticipated

competition expected from current bank consolidations

Compensation Policies

• Specific changes in compensation have not been announced however; there is a

great deal of unhappiness about CEO compensation and calls for a return of

unearned bonuses for companies that received handouts.

• Compensation in cost leadership organizations are traditionally linked to a few

cost efficiency metrics.

• Create demanding performance management system to assure meritocracy is

the norm.

• Encourage respect, teamwork and create a supportive environment

Current

Organizational Structure

• Spin off Smith Barney. Possible divestitures: Consumer Finance-Primerica

Financial Services and CitiFinancial, private label credit cards and international

retail brokeragexxix

• Improve internal cooperation

Management Control Systems

• Reduce number of data centers world-wide

• Separate business, streamline organization

• Realign management into CitiCorp and CitiHolding

Compensation Policies

• While no specific statements about compensation could be found it is typical in a

matrixed organization to use a “balanced scorecard”

Forza 18

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

• In an effort to regain lost reputation and restore stability CitiGroup will

discontinue proprietary trading and segregate $600B of non-essential assets on

CitiBank’s balance sheet.xxx

CEO Influence on Citigroup’s strategy

Because Citigroup appears to have shifted from its supermarket approach to the

financial markets to a shear survival strategy, an examination of its leadership is appropriate.

The history, personality and drive posessed its leaders since 1998 uncovers some interesting

patterns that could explain the strategies the firm was driven to execute and its future

prospects under the leadership of present CEO, Vikram Pandit.

Sanford “Sandy” I. Weill - CEO Citigroup 1998-2003

Business/Education Biography

The Glass-Steagall Act was passed in the same year that Sandy Weill was born, 1933.

Sandy would spend a great deal of money and effort to overturn it five and a half decades later

in an effort to achieve his ultimate career goal of creating a financial supermarket.

Weill’s career started in 1955 with a job as a runner at Bear Stearns. Five years later he

would launch a brokerage business called Carter, Berlind, Potoma & Weill (later Carter,

Berlind, Weill & Levitt). Over the next 38 years Weill would orchestrate a long line of

acquisitions, and occasional sales, which would culminate, in 1998, with the merger between his

Travelers Insurance and John Reed’s Citicorp.xxxi The run-up to this merger was long and

impressive. (Appendix H)

This remarkable run sets Weill up for his fight to repeal the Glass-Steagall Act and

proceed with his plans for the world’s first financial supermarket. Having secured his objective,

the new company Citigroup was initially run with Weill and John Reed as co-CEOs. This

contentious relationship would last only two years until Reed resigned and Weill took the

controls.

There are disparate views, gleaned from peers, subordinates, analysts and the public

(Appendix J) that offer a glimpse into the psychological makeup of Sandy Weill. He appears to

be a complex man who is viewed simultaneously as driven, paranoid, passionate, insecure, hot-

tempered, demanding, ethical and straightforward. At the same time there are no indications

Forza 19

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

that Weill is arrogant, vindictive or pretentious. This combination of traits has driven him to

pursue an endless string of acquisitions that have fed his insatiable desire to keep moving

forward, never stop growing. During his tenure at Citigroup (1998-2002) Weill oversaw dozens

of acquisitions. The conventional wisdom says that they were all in pursuit of his ultimate goal-a

financial supermarket. Another view is voiced by Eric Dash in his April 3, 2008 Times article, “A

Stormy Decade for City Since Travelers Merger”, who believes that Weill’s obsession with

profits was more instrumental in his pursuit of the deal than any overarching belief in the

supermarket concept.xxxii Hindsight can be razor sharp.

Regardless of his motivations there is little disagreement that there was a lack of

efficient organizational structure for most of Weill’s tenure at Citi. Maintaining the u-shape

organization long after he could effectively manage the hugely complex organization contributed

to inefficient and incomplete integration of new units, failure to optimize synergies, increased

risk due to lack of oversight and problems keeping core people in the company. It is difficult to

see a corporate strategy here.

Much has been said about the amazing returns he delivered to investors. For a man that

has frequently called himself risk averse he seems to have ceded this conviction in favor of

creating his legacy; not realizing that the two were inextricable. There is no denying that this

was a boom period for Citi but, without the attention to core business or a clear strategy that

included complete and low risk integration, he failed to deliver on the second mandate of any

corporate manager; leave the business better than you found it and in a position to thrive well

into the future.

Citing a desire to avoid being a CEO who over stays his welcome, but promising to

remain as Chairman of the Board until 2006, in July 2003 Weill announced he would step down

at the end of the year. Weill handed over the reigns to Charles Prince whose legal background

was viewed as essential to weathering lawsuits and regulatory issues facing Citi at the time. xxxiii

Forza 20

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Charles Prince - CEO Citigroup 2003-2006

Business/Education Biography

Charles Prince was CEO of Citigroup from October 2003 to November 2007. Mr.

Prince is a disciple of his predecessor, Sandy Weill since his days at Commercial Credit. Mr.

Weill hired Mr. Prince in 1979 at Commercial Credit where he held multiple management

positions. Mr. Prince is a well educated man, receiving three degrees from the University of

Southern California and his Masters of Law degree from Georgetown University. He worked

his way up at Commercial Credit until he became Executive Vice President in 1995. When

Citigroup was formed by the mega merger between Travelers and Citicorp in 1998, Mr. Prince

was retained and held various executive positions such as:

o Chief Administrative Officer (2000 – 2001)

o Chief Operating Officer (2001 – 2002)

o Chairman and CEO, Global Corporate and Investment Bank (2002 –

2003)

Before being named CEO of the Investment Banking unit, Mr. Prince had no operational

experience during his time in the industry. Although he held numerous management positions

at Commercial Credit, Travelers and Citigroup, he primarily served as Mr. Weill’s top counsel.

Mr. Weill tapped Mr. Prince to succeed him as CEO because he was someone he trusted and

knew was capable, while Mr. Weill continued as the Chairman.

Psychological/Personality Assessment

After being appointed CEO in October 2003, the outsiders took notice of Mr. Prince’s

contrasting personality compared to Mr. Weill. Mr. Prince was not as well known in the media

as Mr. Weill because he preferred to “blend into the paneled woodwork of his spacious Park

Avenue office”.xxxiv Mr. Prince was more of a behind the scenes manager in the vein of the

“Wizard of Oz”. This was his modus operandi since he became an employee of Commercial

Credit. It was noted by journalists that “his name hardly appears in the society pages and he is

not a familiar face on magazine covers.”xxxv However, it has been noted that the one major

difference between the two men is that Mr. Prince is “far more collegial, people-oriented''.xxxvi

But at the same time, Mr. Prince believes in a “No Excuses” approach.

Forza 21

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Description of Leadership Style

Mr. Prince’s leadership style was very systematic and process driven. As a lawyer, he

was inclined to view all of the facts before making any pertinent decisions. Mr. Prince was

considered more cerebral than Mr. Weill and he chose to “set up a host of oversight

committees, hired lawyers for top positions, studied reports and polls, and centralized

operations and technology”.xxxvii

Mr. Prince was also very unitary in his decision making process. Numerous times

Chairman Weill, Robert Willumstad - Chief Operating Officer, and Marjorie Magner -

Chairman and CEO of Citigroup's Global Consumer Group were often ignored when giving

advice to Mr. Prince about key strategic decisions. He was very strong on his decisions and did

not tolerate unethical behavior or lack of accountability. When Japan ordered Citigroup to

shut down its private banking unit in 2004 due to a lack of internal controls, Mr. Prince ordered

an independent assessment of its operations and determined that the three executives in charge

of asset management, private banking, and international operations were to be held accountable

for the fraudulent transactions and forced to resign.

Mr. Prince was known as a good negotiator, especially when it came to government

regulations. He developed his negotiation skills under the tutelage of Sandy Weill. As CEO, Mr.

Prince’s management style was new to most and “unsettling”.xxxviii He was seen as a demanding

CEO and did not waver from the decisions he made. With little operational experience,

however, Prince “struggled with placing the right people in the right jobs.”xxxix

During the beginning of the current financial crisis, Mr. Prince realized he needed to

change his leadership style to become more open to his company and the media. Mr. Prince is

quoted as saying, "I'm not used to operating in the limelight, but the difficulty of the moment

demanded it. I had to get out front and say, ‘we're going in this direction, follow me’."xl Initially

he demanded that his team enforce policies, procedures and regulations, but then the industry

crisis forced him to begin thinking long-term for the viability of the company. Prince’s change of

leadership strategy may have come too late.

Within his first year as CEO, Mr. Prince was faced with the following major challenges:

• Class action settlement of $2.65b with WorldCom investors

Forza 22

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

• Federal Reserve fine of $70m for abuses in personal and mortgage loans to

low-income and high-risk borrowers

• British regulators investigation of a $13.5b bond trade

• Japan ordered Citigroup to close its private banking unit

• Federal Reserve’s one year ban on Citigroup making any major acquisitions

With these challenges near and abroad, Mr. Prince had major decisions to make in

terms of the growth-by-acquisition strategy that Citigroup had developed under Mr. Weill.

Upon receiving the CEO position in 2003, Mr. Prince initially wanted to continue growing the

company through acquisitions. In 2005, however, amid all of the scandals the company was

facing, Mr. Prince decided to implement the following changes in strategy for Citigroup:

• Invest heavily in the consumer businesses

• Capitalize on fast-growing international markets

• Build up the corporate investment bank

• Restore Citigroup’s reputation

Mr. Prince wanted to continue diversification for the company by focusing more on its

services than its products and slowing the growth by acquisitions. He wanted to increase

customer reward programs and build brand new branches and possibly acquire smaller banks

only if the deal was reasonable.

In the international market, Prince’s top priorities were to “invest more in retail banking

in emerging markets like Poland, Turkey, and India; at least double Citi's credit-card volume

worldwide, mostly in Southeast Asia and Latin America; and sell more investment products in

Europe.”xli Mr. Prince wanted to shift the growth from external to internal. He placed a self-

imposed acquisition ban after the Federal Reserve lifted the ban in 2006. He poured money into

“new standards for training, development, compensation, and annual reviews, all designed to

inspire and monitor good behavior”.xlii

With his new strategy, Mr. Prince divested the Legg Mason asset management unit,

forced out top executives, and brought in younger talent to create the new Citi team. His top

Forza 23

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

two executives, Robert Willumstad - Chief Operating Officer, and Marjorie Magner - Chairman

and CEO of Citigroup's Global Consumer Group, resigned to start their own private equity

fund due to the disagreement on the direction Mr. Prince wanted to take the company. He

combined Smith Barney and Citi retail branches to create cross-selling of its financial services

and products.

The financial crisis placed pressure on Mr. Prince to turn things around. Expenses were

growing faster than revenues. As a result, in 2007 Mr. Prince decided to change strategy again

and return to the growth-by-acquisition strategy in order to create gains in the revenue stream.

The new acquisitions included, ECount – prepaid card provider, Old Lane Partners – Hedge

Fund Management, and Automated Trading Desk (ATD) - electronic market making and

proprietary trading. In total, 10 acquisitions were completed in 2007; but, although Citigroup

posted strong earnings in the first two quarters of 2007, the bottom fell out when the market

collapsed mid-year.

Citi’s stock price, revenues and income experienced a rapid slide in 2007; and in

November of 2007, Mr. Prince resigned his positions as Chairman and CEO. In turn, the reigns

of the company transferred to Mr. Vikram Pandit.

Vikram S. Pandit - CEO Citigroup 2006-Present

Business/Education Biography

Vikrim Pandit, 51, born in India, educated in the U.S. in both engineering and finance, is

known as a quantitative thinker and largely devoid of experience in consumer banking. He has a

B.S. and M.S. in electrical engineering, an M.B.A, and received his Ph.D. in finance from

Columbia Business School in 1986.

Upon completion of his doctorate, Pandit entered academia and was an economics

professor at Columbia University and at Indiana University Bloomington before joining Morgan

Stanley in 1990. He was ahead of the learning curve and pushed Morgan Stanley executives to

establish a quantitative trading desk before it became commonplace on Wall Street. He also

helped establish a brokerage desk that catered to hedge funds and other high-volume traders,

known as a big prime brokerage. He served as the managing director and head of the U.S.

Equity Syndicate (1990-1994), served as the managing director and head of the Worldwide

Forza 24

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Institutional Equities Division (1994-2000), and served as the president and chief operating

officer of the Institutional Securities and Investment Banking Group, where he was responsible

for the overall management of the group and focused on the trading, sales and infrastructure

aspects of the business (2000-2005). xliii

In 2005, Pandit was fired from Morgan Stanley and started a hedge fund with other

Morgan Stanley expatriates named Old Lane Partners. Citigroup then purchased the poorly

performing fund in 2007 for $800 million. Pandit received approximately $165.2 million for the

deal. Many analysts believe that this large price was paid for a hedge fund with only $4.5 billion

under management to get Pandit under the Citigroup umbrella.

Pandit’s rise to the top job at Citigroup has been described as meteoric. Just a few

weeks into running the alternative investment unit, Pandit was recruited by Prince to figure out

ways to prevent billions of dollars in losses related to subprime mortgages and bad investments.

By mid-October 2007, Prince expanded his responsibilities to include oversight of the

investment bank. And after Prince abruptly resigned in November 2007 following the

announcement of $18 billion in write-downs, Pandit succeeded him as Citigroup’s chief

executive. On December 11, 2007, Pandit was officially named the new CEO of Citigroup,

replacing interim CEO Sir Winfried Bischoff, who remained CEO of Citigroup Europe.

Psychological/Personality Assessment

Pandit spends most of his free time with Swati, his wife of over 20 years, and their two

children. He points to his traditional Indian upbringing as a source of tranquility. "I cannot deny

that a piece of my Indian upbringing stayed with me," he says. "As I go about my life, there is a

clear sense of Karma, that the tide is going to come and go and the main thing you have to do is

influence where you are on the tide." xliv

Pandit has been characterized with a low-key demeanor. But Citigroup's stunning

decline has increased the scrutiny of Pandit's personality and management philosophy and raised

questions over whether his methodical, technocratic style is what the company needs to

survive. When asked to point out Pandit's most visible attributes, friends and foes point to his

sharp-mind and calm, professorial manner. xlv

Forza 25

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Description of Leadership Style

To his critics, Pandit's sharp mind and passion for intense analysis - often performed

personally with only spreadsheets - have hampered his maturity as a chief executive. "He is not

a leader of people, he is a quantitative trader who overanalyzes things and can take ages to

make tough decisions," says a former Morgan Stanley banker. xlvi

Some of Pandit’s current colleagues have the same opinion, saying that the charisma and

clarity of thought he displays in small congregations often disappears in front of large meetings

of employees or clients. Pandit has worked hard to dispel that impression. He gave a passionate

performance at a staff meeting after Citigroup had been beaten in the race to buy the regional

lender, Wachovia. Pandit admits that the turbulent events of the past few months have made

him reconsider his approach. "Analytics work when markets work analytically; but in these

markets you need to make decisions fast and I find myself turning to my instincts more and

more," he says.

Mr. Pandit has indicated to colleagues that he is frustrated and angered by the

destruction of shareholder value that is taking place under his leadership but remains

determined to carry out his mission of cleaning up Citigroup's balance sheet and reviving its

fortunes.

Pandit’s management style has clashed with several top executives at Citigroup--most

notably, Sallie Krawcheck. Forbes named her as number seven in its list of The World's 100 Most

Powerful Women of 2005. Prior to resigning at the end of 2008, Krawcheck was the CEO of

Citigroup’s wealth management business. From 2004 to 2007, she served as CFO and Head of

Strategy for Citigroup Inc. Prior to that, she was CEO of Citigroup's Smith Barney unit.

As the conflicts emerged with Pandit, Krawcheck felt that the fact that she was a woman

and not part of Pandit’s inner circle made her situation particularly difficult. She indicated that

most women at Citigroup are treated as “condiments” rather than “a main course.” xlvii

After a number of discussions about the best management structure for the wealth

management business, Krawcheck suggested to Vikram that she take an entirely client-facing

senior role as chairman of the business. A Citigroup spokeswoman added, “Vikram agreed that

such a role would be terrific given his view that Sallie has extraordinary client skills. Later, Sallie

Forza 26

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

changed her mind about this role and ultimately decided to leave the company. We were

disappointed that she made that decision.” xlviii

Citigroup's troubles just might call for a more visionary and charismatic leader than

Pandit’s analytical style can offer - but only time will tell. On September 29, 2008, Citigroup

had agreed to take over Wachovia's banking operations for $2.16 billion, or approximately $1 a

share, with the assistance of the Federal Deposit Insurance Corp. agreeing to take on potential

losses in Wachovia's loan portfolio. On Oct. 3, 2008, Wells Fargo agreed to purchase all of

Wachovia without FDIC assistance in a deal totaling $15.1 billion. In turn, Citigroup sued Wells

Fargo. Citigroup said the deal was "in clear breach" of an earlier agreement for Citigroup to

acquire Wachovia's banking. Wells Fargo officially acquired Wachovia on Dec. 31, 2008.

The 2008 takeover battle has created several lawsuits, including a Citigroup suit against

Wachovia; a Wells Fargo suit against Citigroup; and a Wachovia suit against Citigroup.

Citi’s trend in pursuing mergers and acquisitions ended in 2008 when it executed eight

divestitures. The divestitures included sale of Citi’s German Retail Banking Operations,

CitiStreet, and Diners Club International (Appendix G).

Conclusion Citigroup is managing over 300,000 employees; which is 80% more than its closest

competitor, Bank of America. Compounding the challenge of managing the enormous quantity

of workers, is the fact that they are spread throughout 109 countries and are tasked with

selling a wide range of products from credit cards to mortgages to investment banking.

Citigroup's executives admit that the employees do not share a common culture, typically care

less than they should about the global organization, and are often tied up in corporate politics.

The apparent challenges with this position are reflected in the inconsistent track records of

past CEOs. Current CEO, Vikrim Pandit indicated that the company is trying to refocus on its

uniqueness. The firm is slimming down, simplifying, getting more efficient, and going back to its

core purpose – to be a bank.

As the company streamlines its operations, it must attempt to accomplish the following

in the near term:

Forza 27

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

o Divest itself of toxic assets through use of the government’s TARP program at

best price (fire sale) to limit further write downs

o Rapidly increase loan-loss reserves to cover default risk on its debt of $38 billion

in commercial real estate which is estimated to fall 35-45% in price

o Rebuild credibility through encouraging publicity

� i.e. Citigroup profitable for the first two months of 2009

o Increase deposits while continuing to provide a global reach

� Bolster perception as a sound and safe institution

� U.S. deposits at the end of the 4th quarter were $289.8 billion

Citigroup is at a crossroads. Most of the world is watching to discover the company’s

ultimate fate. The full support of the U.S. Government is a very powerful ally for Citi to have in

its corner and will certainly aid in the company’s recovery. As part of TARP, the recent toxic-

asset cleansing plan will allow Citigroup to deleverage itself of assets that are in jeopardy of

defaulting. Also, Citigroup’s executive team would be wise to handle the current financial

industry and global economic crisis with a keen focus on stakeholder perception. Rebuilding

credibility through encouraging publicity, such as Pandit’s recent announcement that the

company was profitable in the first two months of 2009, will slowly change the stigma the

company currently carries with it.

Forza 28

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Appendix A

Citi is organized into the following four business segments:xlix

Consumer Banking Institutional Clients Group

Consumer Finance Sales and Trading/Capital Markets

• Real Estate Lending Investment Banking

• Student Loans Corporate and Commercial Banking

• Auto Loans Global Transaction Services

Retail • Treasury and Trade Solutions

• Retail Bank Branches • Securities and Fund Services

• Commercial Banking Alternative Investments

• Investment Services • Private Equity

• Retirement Services • Hedge Funds

• Personal Loans • Real Estate

• Sales Finance • Global Fixed Income Commercial Business • Infrastructure

• Commercial Banking

Global Wealth Management Global Cards

Ultra High Net Worth • Mastercard

• Private Bank • VISA

• Smith Barney Family Advisory • Diners Club High Net Worth • Private Label

• Smith Barney • Amex (U.S.)

• Retirement Services

• Banking Services

Emerging Affluent

• myFi

Institutional Clients Investments

Forza 29

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Appendix B

The following is Citi’s 1-year stock performance as of close of trading on March 10, 2009:l

Forza 30

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Appendix C

Citi’s key financial statistics, stated on March 10, 2009, were as follows:li

Forza 31

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Appendix D

With the banking industry being highly competitive, below is the five forces model for

environmental threats and Citigroup’s cost leadership position:

1. Threat of Entry

(Medium)

With the current financial situation it would be very difficult for any new bank to

position themselves as a cost leader.

Any new bank would need to spend large amounts of capital to procure the

economy of scales that Citigroup has established over the past 10 years.

2. Threat of Rivalry

(High)

With only four banks controlling a majority of the market share, Citigroup must

continually improve their services and attempt to lower costs in order to gain

market share. Innovation is key to stay ahead of rivals with like products and

services

3. Threat of

Substitutes

(High)

Thrifts, credit unions, government agencies, mortgage brokers and other

nonbank organizations are always a substitute for Citigroup customers.

However some of the smaller firms cannot provide the low costs that Citigroup

has maintained because of their specialization in specific areas of banking.

4. Threat of Buyers

(Low)

Citigroup’s clients are always looking for low fees and low interest rates for the

banks products and services. Their clients include: retail, commercial and

other banks.

5. Threat of Suppliers

(High)

This is currently high due to the financial crisis. Banks are not lending as

much to other bank, specifically Citigroup due to the low confidence level.

Their clients include: retail, commercial and other banks.

Forza 32

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Appendix E

The following table shows a timeline of the economies of scale Citi amassed through a rapid

series of acquisitions:

1999 • Mellon Bank's credit card business a portfolio of $1.9 billion in credit card receivables

• Associates First Capital $558 million loan portfolio • Santiago, a Chile-based Financiero Atlas, consumer finance company with 65

branches 2000 • Schroder., an investment banking business valued at $2.2 billion

2001 • AST StockPlan, a provider of stock benefit plan services

• American Bank from ABN Amro Bank

• Grupo Financiero Banamex-Accival.

2002 • Golden State Bancorp

• Cal Fed

2003 • Entered China's credit card market.

• 5% stake in the Chinese commercial bank Shanghai Pudong Development Bank (SPDB).

• $29 billion portfolio of private label and credit card receivables from Sears • Finance subsidiary of Washington Mutual, for $1.3 billion in cash

2004 • Majority stake in Nikko Cordial, a Japanese stockbroker. • Purchased KorAm Bank • Mortgage banking business of the Principal Financial Group

2005 • Legg Mason's broker-dealer business

2007 • 20% equity stake in Akbank, a bank in Turkey, • Grupo Financiero Uno (GFU), a consumer finance business in Central America. • Quilter, a wealth advisory firm from Morgan Stanley. • Egg Banking • Grupo Cuscatlan's banking, insurance, and other financial activities • Old Lane Partners, a global, multi-strategy hedge fund and a private equity fund • Strategic partnership with Quinenco • The BISYS Group • Automated Trading Desk (ATD)

Forza 33

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Appendix F

The following illustrates how, amidst the unfolding of the subprime mortgage crisis in 2007, Citi

continued to expand through acquisition in an effort to differentiate its product portfolio from

its competitors. Citi acquired the following ten companies in 2007:

Acquisitions in North America

• ABN AMRO Mortgage Group (AAMG) - is a subsidiary of LaSalle Bank Corporation

and ABN AMRO Bank N.V. AAMG - a national originator and servicer of prime

residential mortgage loans. Citigroup purchased in the order of $12 billion in assets,

which included $3 billion of mortgage servicing rights that resulted in the addition of

approximately 1.5 million customers.

• Old Lane Partners, L.P. - was the manager of a global, multi-strategy hedge fund and

a private equity fund with total assets under management and private equity

commitments of approximately $4.5 billion.

• BISYS Group, Inc. (BISYS) - was acquired for $1.47 billion in cash. Citigroup

completed the sale of the Retirement and Insurance Services Divisions of BISYS, making

the net cost of the transaction to Citigroup approximately $800 million. Citigroup

retained the Fund Services and Alternative Investment services businesses of BISYS,

which provides administrative services for hedge funds, mutual funds and private equity

funds.

• Automated Trading Desk (ATD) - a leader in electronic market making and

proprietary trading, was acquired for approximately $680 million ($102.6 million in cash

and approximately 11.17 million shares of Citigroup common stock).

Acquisitions in Latin America

• Grupo Financiero Uno (GFU) - the largest credit card issuer in Central America, was

acquired for $2.2 billion in assets.

• Grupo Cuscatlán - was acquired for $1.51 billion ($755 million in cash and 14.2

million shares of Citigroup common stock) from Corporacion UBC Internacional S.A.

Grupo.

Forza 34

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Acquisitions in Asia

• Bank of Overseas Chinese (BOOC) - located in Taiwan was acquired for

approximately $427 million.

Acquisitions in Europe, Middle East and Africa (EMEA)

• Egg Banking PLC (Egg) - an on-line U.K. financial services provider, was acquired

from Prudential PLC for approximately $1.39 billion.

• Quilter - a U.K. wealth advisory firm was acquired from Morgan Stanley.

• Akbank - the second largest privately owned bank by assets in Turkey, sold 20% equity

interest for approximately $3.1 billion to Citigroup.

Forza 35

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Appendix G

The following is a list of eight divestitures and discontinued operations that Citi executed in

2008:lii

• Upromise Cards Portfolio

• CitiStreet

• Divestiture of Diners Club International

• Citigroup Global Services Limited

• Citigroup Technology Services Limited

• Citi’s Nikko Citi Trust and Banking Corporation

• Citigroup’s German Retail Banking Operations

• CitiCapital

Forza 36

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Appendix H

Two Series of Major Mergers Spearheaded by Sandy Weill on his March to CitiGroup 1960-1985

First string: Weill acquires brokerage Hayden Stone which then acquires brokerage H. Heinz &

Co. and Shearson Hamill creating Shearson Hayden Stone. This company then acquires Loeb

Rhoades, the largest merger to date. Shearson Loeb Rhoades is sold to American Express and

in 1983 Weill becomes president only to resign two years later. This leaves Weill free to

embark on his next round of buys.

1986-1998

Second string: a controlling interest in consumer finance company Commercial Credit is bought

by Weill in 1986 laying the groundwork for the acquisition of Primerica which included Smith

Barney in 1988. In rapid succession a 27% stake in Travelers Insurance is added and Weill re-

acquires the Shearson portion of American Express. A year later he purchases the remainder of

Travelers and takes on the name. After shedding the health-insurance portion of Travelers he

picks up the property-casualty insurance segment of Aetna, the finance section of BankAmerica

and Salomon Brothers.liii

Forza 37

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

Appendix J

Quotes that offer an insight into Weill’s Psychological Makeup and Personality

Peter Cohen, American Express Brokerage (1985)

• "I never get as down as he does and I never get as high as he gets. His emotions drive

him."liv

Business Week, Anonymous Quote from Wall Street (1997)

• "The guy lives to do deals. That's what he does. It means no endgame"lv

Jeffrey Lane, Travelers, long time friend

• "When he gets close to a deal, he gets very, very nervous. His strength is his

insecurity."lvi

Peter Solomon, Shearson Lehman Brothers

• “You never bet against Sandy Weill. He always wanted to be king of the world.”lvii

Sandy himself

• "I don't know why I'm driven and I don't know whether I'm insecure or all these other

things I read about me. All I'm trying to do is the very best I can, working with a group

of terrific people. Paranoia is a psychological expression isn't it? I haven't spent a lot of

time on couches. Maybe I should."lviii

Quotes that offer an insight into Weill’s Leadership/Management Style

Jeffrey Lane, Travelers, long time friend

• Speaking of Weill’s paranoia: "It's a unique strength, especially now in business. If you

really think you have all the answers, they're clearly going to take you away in a box, so

he asks you, he asks himself, he asks everyone he can find. At the end of the story, all

the truths have been raised and that's a real strength."lix

Robert Rubin, CitiGroup, former Treasury Secretary

Forza 38

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

• “He has a view that if you stop building, if you stop being forward-looking, you'll

atrophy, and I think that's exactly right. You can't take the position that, 'Gee, we built a

great thing; now we're just going to run it in place.' You do that, you fall behind."lx

Charles Prince, CitiGroup

• "He wears his emotions completely on his sleeve, he can walk in in the morning and

take my head off about a work issue and then come back after lunch and be fine. He

doesn't hide things. You're never walking around thinking, 'What does he think?'"

Robert Willumstad, CitiGroup President 2000-2003

• "[Sandy] could care less that one part of the organization didn't perform and somebody

else's did, as far as he's concerned, if it didn't meet the expectations of the shareholders

then nobody succeeded."lxi

Richard X. Bove, Punk Ziegel Analyst

• “I cannot think of one positive thing that developed as a result of these two companies.

The miracle of Citigroup is that it still is in the position it is in, given the massive

mismanagement.”lxii

Quotes made by Sandy Weill himself

• "But I get maddest at those I respect the most because I know they could do better.”lxiii

• “You want to have that entrepreneurial kind of environment where people know

they're not going to get killed for every little thing they do wrong.”

• “If you make a mistake, though, surface it so we can fix it--don't try to bury it."

• "Succeeding is not being afraid to hire people who are smarter than you are and trying

to create a team effort, because a team will always do better than one single

superstar,"lxiv

• “…You know, we have very different management styles and they were getting different

directions from John and from me and you know, people began to leave and we couldn't

... we tried, we brought in a corporate shrink who was phenomenal by the name of Ram

Shriram…”lxv

Forza 39

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

References

i Datamonitor. (2008, August13). Citigroup Inc. company profile. Retrieved February 15, 2009, from www.datamonitor.com. ii Barney, J. (2002). Gaining and sustaining competitive advantage (3rd ed.). Upper Saddle River, NJ: Prentice Hall. iii Citigroup. (2009). Citi segments. Retrieved March 9, 2009, from http://www.citigroup.com/citi/business/index.htm iv Yahoo. (2009, March 10). Citigroup Inc. (C) basic chart. Retrieved March 10, 2009, from http://finance.yahoo.com v Yahoo. (2009, March 10). Citigroup Inc. (C) key statistics. Retrieved March 10, 2009, from http://finance.yahoo.com vi Barney, J. (2002). Gaining and sustaining competitive advantage (3rd ed.). Upper Saddle River, NJ: Prentice Hall. vii Gray, A. (2009, February 18). Mortgage plans fail to lift Wall Street. Financial Times. Retrieved February 19, 2009, from http://www.ft.com viii Retrieved February 19, 2009, from http://www.reuters.com/article/newsOne/idUSTRE51I4R720090220 ix Guerrera, F. (2009, January 13). Citigroup moves towards break-up. Financial Times. Retrieved January 14, 2009, from http://ft.com x Guerrera, F. (2009, January 21) Parsons takes over as Citi chairman. Financial Times. Retrieved January22, 2009, from http://ft.com xi Guerrera, F. (2009, January 21) Parsons takes over as Citi chairman. Financial Times. Retrieved January22, 2009, from http://ft.com xii Retrieved February 18, 2009, from http://www.financetech.com/feed/showArticle.jhtml?articleID=214501738&cid=RSSfeed_FTN_All xiii Larson, P.T., Tett, G., & Guerrera, F. (2009, January 30). Banker warns of risk of political interference. Financial Times. Retrieved January 30, 2009, from http://www.ft.com xiv Retrieved February 18, 2009, from http://www.thenation.com/blogs/notion/248817 xv Barney, J. (2002). Gaining and sustaining competitive advantage (3rd ed.). Upper Saddle River, NJ: Prentice Hall. xvi Barney, J. (2002). Gaining and sustaining competitive advantage (3rd ed.). Upper Saddle River, NJ: Prentice Hall. xvii Smith, Roy C. Painful Survival Strategies-but will Citigroup bite?. Forbes. January 15, 2000. xviii Buisness Editors. Citigroup Announces New Management Structure to Enhance Global Growth, Coordination and Accountability for Product Initiatives http://findarticles.com/p/articles/mi_m0EIN/is_2002_June_11/ai_87076966 . Business Wire copyright 2002; Gail, Cengage copyright 2008. June 11, 2002. xix Paul Beckett. (2000, February 29). New Citigroup Strategy Aims for No. 1 Spot With Citibank Unit, Using GE

Chief's Maxim. Wall Street Journal (Eastern Edition), p. C2 xx National Information Center, Top 50 Bank Holding Companies, http://www.ffiec.gov/nicpubweb/nicweb/Top50Form.aspx xxi IBISWorld Industry World Report, Commercial Banking in the US, Dec 2008, p. 37. xxii http://www.citigroup.com/citi/fin/sec.htm/Form10-K/2008 xxiii Ibid. xxiv Retrieved February 18, 2009, from http://www.transactionservices.citigroup.com/transactionservices/home/securities_svcs/intermediaries.jsp xxv http://www.citigroup.com/citi/fin/sec.htm/Form10-K/2008 xxvi Ibid xxvii Smith, Roy C. The Citi Never Sleeps-Only its Board, Risk Managers and Regulators. Information Arbitrage Website. January 12, 2009. http://www.informationarbitrage.com . xxviii Cit Group Press Release. Citi to Reorganize into Two Operating Units to Maximize Value of Core Franchise. January 16, 2009. xxix Enrich, David. Citi Board Backs CEO as Outlook Worsens. Wall Street Journal. January 12, 2009. xxx Ibid. xxxi Unknown. Sandy Weill, pragmatic dreamer: Travelers Group CEO Sanford Weill talks about his approach to dealmaking, governance, and life in and out of the spotlight. The Free Library by Farlex. http://www.thefreelibrary.com/Sandy+Weill,+pragmatic+dreamer:+Travelers+Group+CEO+Sanford+Weill...-a020899183 . Accessed 03/22/09 xxxii Ibid.

Forza 40

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

xxxiii Steve Geisi. Weill stepping down as Citigroup CEO Wall Street titan to retain chairman's post into 2006. Market Watch. July 16, 2003 http://www.marketwatch.com/News/Story/Story.aspx?guid=%7B7AE4E57C-D861-45F7-9FE8-E0F6D8E6AFEB%7D&siteid=mktw xxxiv Mara Der Hovanesian, Rewitring Chuck Prince, BusinessWeek, February 20, 2006 xxxv LANDON THOMAS Jr. and JENNIFER BAYOT, CHANGING THE GUARD: THE TITAN; A Hands-On Boss Will Try To Let an Old Friend Lead, New York Times, July 17, 2003 xxxvi Ibid xxxvii Monica Langley, Course Correction -- Behind Citigroup Departures: A Culture Shift by CEO Prince; His New Focus on Controls, More-Bureaucratic Style Spur Exits at Top Level; Adding Lawyers in High Places, Wall Street Journal, August 24, 2005 xxxviii Ibid xxxix Eric Dash and Landon Thomas Jr. Man in Citi’s Hot Seat, New York Times, October 7, 2007 xl Mara Der Hovanesian, Rewitring Chuck Prince, BusinessWeek, February 20, 2006 xli Mara Der Hovanesian, Chuck Prince’s Citi Planning, BusinessWeek, September 5, 2005 xlii Ibid xliii Source: Citigroup Company Web Site, 2007Biography xliv http://www.rediff.com///money/2008/nov/25bcrisis-man-in-the-news-vikram-pandit.htm xlv ibid xlvi Ibid xlviiThe New York Times: When Citi Lost Sallie by Geraldine Fabrikant, Published November 15, 2008, retrieved from: http://www.nytimes.com/2008/11/16/business/16sallie.html?em xlviii ibid xlix Citigroup. (2009). Citi segments. Retrieved March 9, 2009, from http://www.citigroup.com/citi/business/index.htm l Yahoo. (2009, March 10). Citigroup Inc. (C) basic chart. Retrieved March 10, 2009, from http://finance.yahoo.com li Yahoo. (2009, March 10). Citigroup Inc. (C) key statistics. Retrieved March 10, 2009, from http://finance.yahoo.com lii http://www.citigroup.com/citi/fin/sec.htm/Form10-K/2008 liii Unknown. Sandy Weill, pragmatic dreamer: Travelers Group CEO Sanford Weill talks about his approach to dealmaking, governance, and life in and out of the spotlight. The Free Library by Farlex. http://www.thefreelibrary.com/Sandy+Weill,+pragmatic+dreamer:+Travelers+Group+CEO+Sanford+Weill...-a020899183 . Accessed 03/22/09 liv Ibid. lv Gary Weiss. Gary’s Triumph. Business Week. October 6, 1997 lvi Unknown. Sandy Weill, pragmatic dreamer: Travelers Group CEO Sanford Weill talks about his approach to dealmaking, governance, and life in and out of the spotlight. The Free Library by Farlex. http://www.thefreelibrary.com/Sandy+Weill,+pragmatic+dreamer:+Travelers+Group+CEO+Sanford+Weill...-a020899183 . Accessed 03/22/09 lvii Gary Silverman. King of the world: MAN IN THE NEWS SANDY WEILL. Financial Times [London edition]. March 4, 2000. page 13 lviii Unknown. Sandy Weill, pragmatic dreamer: Travelers Group CEO Sanford Weill talks about his approach to dealmaking, governance, and life in and out of the spotlight. The Free Library by Farlex. http://www.thefreelibrary.com/Sandy+Weill,+pragmatic+dreamer:+Travelers+Group+CEO+Sanford+Weill...-a020899183 . Accessed 03/22/09 lix C.J. Prince . The dealmaker: Sandy Weill may shout more than other chiefs, but his moxie has won the loyalty of Citigroup's employees and shareholders, the respect of competitors and the title of Chief Executive of the Year - CEO of the Year. The Chief Executive, Bnet, July 2002. http://findarticles.com/p/articles/mi_m4070/is_2002_July/ai_89394652/pg_10?tag=content;col1 lx Ibid. lxi Ibid lxii Eric Dash. A Stormy Decade for Citi Since Travelers Merger. New York Times. April 3, 2008. http://www.nytimes.com/2008/04/03/business/03citi.html?_r=1&oref=slogin&ref=business&pagewanted=print lxiii C.J. Prince . The dealmaker: Sandy Weill may shout more than other chiefs, but his moxie has won the loyalty of Citigroup's employees and shareholders, the respect of competitors and the title of Chief Executive of the Year -

Forza 41

MGMT-780_Strategic_Evaluation_Citigroup_FORZA.doc

CEO of the Year. The Chief Executive, Bnet, July 2002. http://findarticles.com/p/articles/mi_m4070/is_2002_July/ai_89394652/pg_10?tag=content;col1 lxiv Ibid. lxv Unknown. Cornell universtiy Department of Applied Economics and Management. Video Clip Transcript. Weill06_mergerAnecdote3. Accessed 03/22/09. http://eclips.cornell.edu/clip.do?id=8780&tab=TabClipPage