stralem montreux

TRANSCRIPT

1 1

Stralem & Company, Inc. 645 Madison Avenue New York, NY 10022 (Tel) 212.888.8123 (Fax) 212.888.8152 www.stralem.com

STRALEM & COMPANY

LARGE-CAP EQUITY STRATEGY

Adam Abelson Vice President

Andrea Baumann Lustig

Vice President

May 2013

2

Investment Team: Stability and Experience

Private Boutique founded in 1967

$3.7 Bn. in Assets Under Management*

One Strategy-- Three Formats

History of outperformance with reduced risk

Principals Invested in the Strategy

Team Based Decision Making

Hirschel Abelson

President

50+ years Industry Experience

45 years at Stralem

Andrew Eras, CFA

Dir. Institutional Asset Mgmt.

29 years Industry Experience

11 years at Stralem

Edward Cooper, CFA

Senior Research Analyst

15 years Industry Experience

7 years at Stralem

Adam Abelson

Senior Portfolio Manager

Director of Research

21 years Industry Experience

15 years at Stralem

Andrea Baumann Lustig

Dir. Private Client Asset Mgmt.

President, Stralem Equity Fund

29 years Industry Experience

10 years at Stralem

Michael Alpert

Portfolio Manager

22 years Industry Experience

3 Years at Stralem

Philippe Labaune

Head of Trading and Operations

17 years Industry Experience

16 years at Stralem Irene Bergman

Financial Advisor

50+ years Industry Experience

40 years at Stralem

* AUM as of 3/31/13

ABOUT STRALEM

3

Large Cap Equity Strategy Snapshot

All data as of 3/31/13. Source: Stralem, The Bank of New York Mellon Corporation.

See the performance notes included in this presentation.

Product Inception: January 1967

Benchmark: S&P 500

Number of Holdings: 28-35 Positions

Long Only

Weighted Avg. Market Cap: $125.1 billion

S&P Quality Rank: A

Cash Allocation +/- 5%

US Large Cap Equity Strategy

Objective: Build long term capital by delivering excess returns with less risk

during both up and down markets

4

Performance – Rolling Periods

Stralem has consistently outperformed across all rolling time frames

Performance is stated gross of fees. See the performance notes included in this presentation.

All data is based on monthly performance and is from January 1992 to March 2013.

Source: Stralem & Co.

Monthly Percent of

Rolling Average Total Number Annualized Returns Periods Stralem

Return Period of Periods Stralem LCES S&P 500 Index Stralem Premium Outperformed

3 Years 220 12.95% 8.85% 4.10% 82%

5 Years 196 12.42% 7.87% 4.55% 93%

10 Years 136 11.31% 6.20% 5.10% 100%

15 Years 76 12.16% 7.36% 4.80% 100%

20 Years 16 11.93% 8.31% 3.61% 100%

5

Structural Framework

70% Up / 30% Down 50% Up / 50% Down

90% Up / 10% Down 70% Up / 30% Down

Bull Market: Momentum Driven Bear Market: Valuation Driven

Bull Market: Valuation Driven Bear Market: Momentum Driven

Structure portfolio to successfully navigate

each market environment

Focus is on delivering growth with capital

preservation

Increase weighting of Up Market stocks as

market declines to enhance portfolio

growth potential

Increase allocation of Down Market stocks

as momentum increases to reduce

portfolio volatility

6

Portfolio Structure

Up Market Stocks

Capture Upside and Participate When Markets Rise

New Industries

Market Innovators

Leaders in Current Cycles

Technological Shifts

Stronger Growth

New Products

More Mature Growers

Intense Focus on R&D

More Predictable Growth

Horizontal Growth

Dominant Companies

Thematic Investments

Increasing Market Share

Leading Global Brands

World Class Management

Down Market Stocks

Provide Protection and Capital Preservation When Markets Fall

Low Price to Cash Flow

High Sustainable Levels of Cash Flow

Fundamentally and Financially Secure

Purchased at a Discount to Market

High Yield Companies

Dividend Yield Above Market Average

Increasing Dividend Faster than inflation

Dividend Payment Secure – Low Payout Ratio

7

Stock Selection and Research

Stock selection process is fundamentally driven and quantitatively enhanced

S&P 500 Index stocks with Market

Cap > $4B

Dominant Companies

New Industries

New Products

Low Price/CF

High Yield

Extensive due diligence focused on investing

rather than trading securities

Security Research

Research Activities

• Industry research and theme identification

• Management Meetings/Corporate Events

• Extensive travel within US, Europe, Asia

• Discussions with private operators/suppliers

• Minimal sell-side research

Financial Analysis

• Financial Statement Analysis

• Revenue and Earnings Growth Projections

• RGV Calculations and Scenarios

Identify Critical Success Factors

• Sources of Growth

• Drivers of Profitability

• Innovation/De-innovation

• New Product Development

Fundamental Focus

• Financial Statement Transparency

• Identifiable and Strong EPS Growth

• High Earnings Purity

• Business Generating Strong Free Cash Flow

• Increasing Profit Margins

• Demonstrated Ability to Innovate

• Ability to Invest in R&D

• Strong Management - Stewards of Capital

Seek to identify high quality business models

with long term competitive advantages

Security Screening

Valuation Analysis

• Appropriate Relative Growth Value (RGV)

8

Quantitative Risk Management

Category RGV

New Industries 3.07

New Products 1.78

Dominant Companies 1.56

Up-Market Total 1.80

Price-to-Cash Flow 0.52

High Yielding 1.55

Total Down-Market 1.23

Portfolio Total 1.63

S&P 500 0.88

Portfolio Target Pricing Metrics:

Up-Market Stocks > 2x S&P500

Portfolio Total > 1.5x S&P500

Reinforces optimal sector and

category weightings

Signals need to re-balance when

metrics violated

Portfolio Construction: Risk Control Tool

2010 2011 2012ee 3yr Avg 2013 ee EPS Growth P/E RGV

Stock A $3.03 $3.69 $4.08 $3.60 $4.79 33.1% 14x 2.33

Stock B $3.63 $3.80 $3.48 $3.64 $3.83 5.3% 10x 0.53

Prevents overpaying for growth

Enforces Buy/Sell discipline

Stock Selection: Valuation Tool

Relative Growth Valuation Model (RGV)

Performance is stated gross of fees. Returns are from 1/97-3/13. See the performance notes included in this presentation.

Portfolio Structure: A Multi-Year Snapshot (12/96-12/12)

0%

25%

50%

75%

100%

125%

150%

175%

200%

225%

250%

275%

300%

325%

350%

375%

400%

425%

Portfolio Structure:

Year-End 1996

Up Market - 65%

Down Market - 35%

Portfolio Structure:

November 2000

Up Market - 60%

Down Market - 40%

Portfolio Structure:

August 2001

Up Market - 55%

Down Market - 45%

Portfolio Structure:

October 2001

Up Market - 50%

Down Market - 50%

65 CUMULATIVE QUARTERLY RETURNS

TOTAL RETURN LCES 435.0%

S&P 500 184.4%

Up-Market Re-allocation:

Sell New Industries

December 1999

Down Market Re-allocation:

Buy LP/CF Energy

April 2004

Down- Market Re-allocation:

Sell LP/CF Energy

April 2007

Portfolio Structure:

October 2008 - March 2009

Up Market - 65%

Down Market - 35%

9

10

Historical Performance

Consistent Long Term record of delivering excess returns with significantly lower volatility

All Annualized Returns in the bar chart are through 3/31/13 and are stated gross of fees.

See the performance notes included in this presentation.

10.7%

11.9%

6.3%6.7%

10.5%

8.9%

12.5% 12.7%

14.0%12.7%

5.8%5.0%

8.5%

4.3%

8.5%

14.8%

0%

10%

20%

1 Year 3 Years 5 Years 7 Years 10 Years 15 Years 20 Years 10 Year Standard Deviation

LCES S&P 500

Calendar Years Q1 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999

Stralem LCES 10.50 8.69 8.83 10.82 21.49 -27.41 13.59 10.68 13.51 17.42 23.30 -19.70 0.95 5.93 33.16

S&P 500 10.61 16.00 2.11 15.06 26.46 -37.00 5.49 15.79 4.91 10.88 28.68 -22.06 -11.93 -9.10 21.04

11

Economic Backdrop

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

1951 1961 1971 1981 1991 2001 2011

$ B

illio

ns

Years

Growth in US Debt and GDP (1952 - Q112)

Source: Bloomberg, Stralem & Co.

Nominal GDP

Total Debt

Total US Debt as a Percentage of GDP

100%

150%

200%

250%

300%

350%

400% 1933: 299%

2003: 301%

2009: 367%

Average:204%

Source: Fed Reserve, BEA, Historical Statistical Abstract of the US, Stralem & Co.

20%

60%

100%

140%

1951 1956 1961 1966 1971 1976 1981 1986 1991 1996 2001 2006 2011

Household Debt to Disposable Income

Source: Fed Flow of Funds Report (F.100 and L.1), Bloomberg, Stralem & Co.

Liability Driven Recession

GDP growth fueled by excessive leverage

Consumer and Government remain over levered

Liability holders lack control

Economic recovery will be slow and below trend

No quick fixes—remedies take time

Deleveraging process will occur for several years

Consumer Driven Economy Impacted

70% of US Economy

Unemployment remains high—U6 vs. U3

Wages remain stagnant

Risk Management

12

Excesses of prior Bull Market have yet to be fully resolved Leverage remains excessive

Sovereigns still fragile

Low and Middle market consumers remain constrained

Structural Headwinds Persist Deleveraging Global Economy

Stagnant Job Growth

High Unemployment/Flat Personal Income

Expanding Income Inequality

Austerity Programs

Macro Risks Continue Unwinding of Unprecedented Central Bank Liquidity

Managing a return to rising rate environment

Ongoing geopolitical risks

Bull Market within a Structural Bear Market Earnings Driven by Stock Buybacks and Cost cutting—

Peak Corporate Margins

Positioned for A Momentum-Driven Bear Market

Allocation to Down Market Stocks

High Quality Focus

Growth Opportunities

13

Expansion of the Global Middle Class

The “Urbanization” of Emerging Markets is driving

demand for Western goods and services

Aggregate GDP of BRICs quadrupled over last decade

from $3T to $12T

Continuation of the Industrial Revolution

Global secular trends remain firmly in place

Strong demand for power, energy, machinery, mining

Proliferation of Mobile Technology

Internet traffic growing 29% per year from 2011-2016

Consumer demand shifting to mobile

Globalization of Disease and Health Care Issues

Demographics driving health care demand

Cost pressure driving innovation

China, Brazil, India to Account for One-Third of Smartphones by

2016

Source: Goldman Sachs

14

Stralem Investment Focus…

Large and innovative companies built to survive and thrive during periods of economic volatility

Strong Balance Sheet and Cash Generation

Can finance suppliers and customers to support consistent and predictable growth

Ability to reinvest capital into business without accessing capital markets

Low cost of capital advantage creates investment opportunities

Revenue Diversification and Global Reach

Multiple revenue streams prevent a reliance on any single product or market

Take advantage of emerging market growth rates that far exceed developed markets

Continued investment in innovation

Reduced Risk Profile

Focus on mega-cap securities

Disciplined stock entry/exit points, not chasing momentum

Long term investment approach

Portfolio Positioning

15

Overweight Industrials Access to global infrastructure, energy and urbanization trends

High barriers to entry

Geographic and product diversity

Select Exposure to Technology Access to tech growth trends in mobility, cloud and enterprise

Avoidance of end market exposure (No Apple)

Targeted Exposure to Consumer Economic pressures on consumer spending

Decreased access to credit

Highly leveraged

Overweight High Yield Companies High yield in a low interest rate environment

Stable and recurring cash flow

Decrease portfolio volatility and provide downside protection

No Exposure To Financials

Lack of financial statement and earnings transparency

Fundamental headwinds

Leverage remains a concern

Current Portfolio

16 See the performance notes included in this presentation.

C at e g o ry C o mp any Targ e t % C at e g o ry C o mp any Targ e t %

N ew Indust r ies Cisco Systems Price t o C ash F low Chevron Corp

Google Exxon M obil

M icrosoft

Oracle

Qualcomm

Subt o t al: 12 .5% Subt o t al: 8 .0 %

N ew Product s Abbott Laboratories High Y ield AT&T

Abbvie Dominion Resources

Celgene M erck & Co

Thermo Fisher Scient if ic NextEra Energy

Pfizer

PPL Corporat ion

Subt o t al: 7.5% Southern Company

D ominant C ompanies Coca-Cola Subt o t al: 2 4 .0 %

Danaher

Dow Chemicals D own- M arket Subt o t al: 3 2 .0 %

Dupont

Eaton Corporat ion C ash 3 .8 %

Federal Express

General Electric

Internat ional Business M achines

M cDonald's

Phillip M orris Internat ional

Schlumberger

United Technologies

Visa

Subt o t al: 4 4 .2 %

U p- M arket Subt o t al: 6 4 .2 %

Appendix

UCITS IV Fund

18

4 Year Track Record

Launched Adviser share class August 2008; Institutional class added November 2008

Distribution and Capitalization shares

Registered in 9 countries

Assets of $125M*

Shareholders from Switzerland, Germany, UK, Luxembourg, Austria, Netherlands

Private Banks, Insurance Companies, Asset Managers, Other Institutions, Individuals

Fully tax transparent in Germany

Dollar denominated, no currency hedging

US Large Cap Equity Strategy portfolio; trading done by Stralem

KTL Luxembourg is Management Company

KBL acts as custodian; Citi is sub-custodian for all US securities

Audited by Deloitte

Website with all documentation www.stralemucits.com

*As of 5/13/2013.

UCITS IV Fund-Fees

19

TER capped at 1.53% by Investment Manager for Institutional Shares

TER capped at 2.19% by Investment Manager for Adviser Shares

Management Fee at 80bps (I shares) and 1.30% (A shares)

20

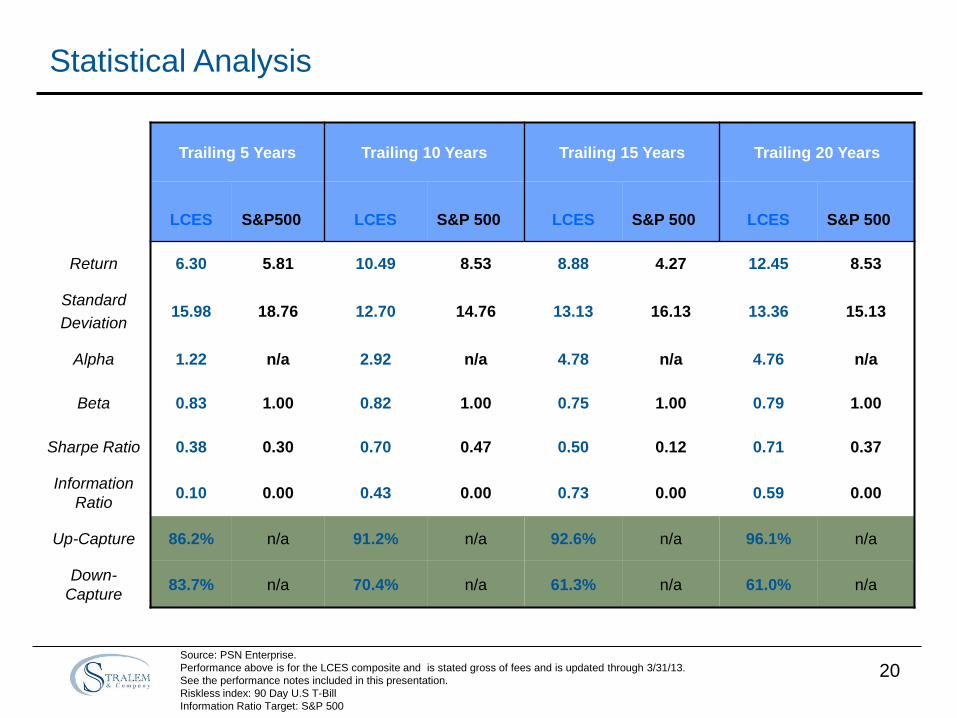

Statistical Analysis

Source: PSN Enterprise.

Performance above is for the LCES composite and is stated gross of fees and is updated through 3/31/13.

See the performance notes included in this presentation.

Riskless index: 90 Day U.S T-Bill

Information Ratio Target: S&P 500

Trailing 5 Years Trailing 10 Years Trailing 15 Years Trailing 20 Years

LCES

S&P500

LCES

S&P 500

LCES

S&P 500

LCES

S&P 500

Return 6.30 5.81 10.49 8.53 8.88 4.27 12.45 8.53

Standard

Deviation 15.98 18.76 12.70 14.76 13.13 16.13 13.36 15.13

Alpha 1.22 n/a 2.92 n/a 4.78 n/a 4.76 n/a

Beta 0.83 1.00 0.82 1.00 0.75 1.00 0.79 1.00

Sharpe Ratio 0.38 0.30 0.70 0.47 0.50 0.12 0.71 0.37

Information

Ratio 0.10 0.00 0.43 0.00 0.73 0.00 0.59 0.00

Up-Capture 86.2% n/a 91.2% n/a 92.6% n/a 96.1% n/a

Down-

Capture 83.7% n/a 70.4% n/a 61.3% n/a 61.0% n/a

Large Cap Equity Strategy Risk/Reward

Supplemental Information as of March 2013, 5 Year period. Risk Index: S&P 500. Risk-less Index: 90 Day U.S. T-Bill.

Source: PSN Enterprise

Performance is stated gross of fees. See the performance notes included in this presentation.

21

16 17 18 19 20 21 22 STANDARD DEVIATION

4

5

6

7

RA

TE

OF

RE

TU

RN

Standard & Poor's 500

More Return Less Risk

Less Return Less Risk

More Return More Risk

Less Return More Risk

Stralem & Co. LCES

Standard & Poor's 500

ROR Std Dev Pop Alpha Beta

6.30 17.83 1.11 0.83

5.81 21.09 0.00 1.00

22

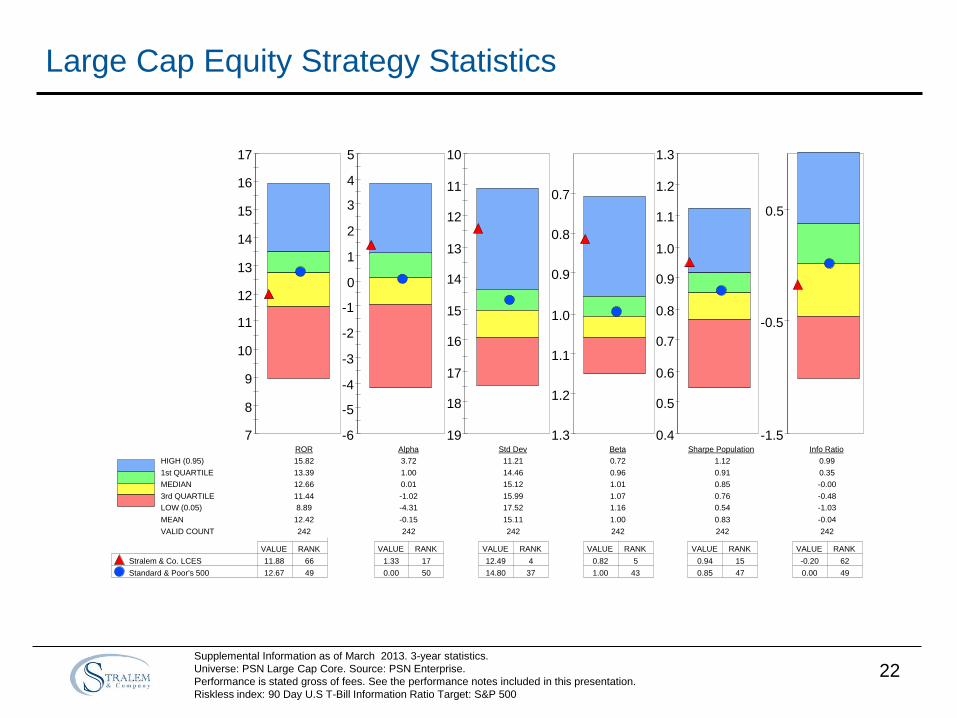

Large Cap Equity Strategy Statistics

Supplemental Information as of March 2013. 3-year statistics.

Universe: PSN Large Cap Core. Source: PSN Enterprise.

Performance is stated gross of fees. See the performance notes included in this presentation.

Riskless index: 90 Day U.S T-Bill Information Ratio Target: S&P 500

7

8

9

10

11

12

13

14

15

16

17

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5 10

11

12

13

14

15

16

17

18

19

0.7

0.8

0.9

1.0

1.1

1.2

1.3 0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

-1.5

-0.5

0.5

HIGH (0.95)

1st QUARTILE

MEDIAN

3rd QUARTILE

LOW (0.05)

MEAN

VALID COUNT

ROR

15.82

13.39

12.66

11.44

8.89

12.42

242

Alpha

3.72

1.00

0.01

-1.02

-4.31

-0.15

242

Std Dev

11.21

14.46

15.12

15.99

17.52

15.11

242

Beta

0.72

0.96

1.01

1.07

1.16

1.00

242

Sharpe Population

1.12

0.91

0.85

0.76

0.54

0.83

242

Info Ratio

0.99

0.35

-0.00

-0.48

-1.03

-0.04

242

VALUE RANK

Stralem & Co. LCES 11.88 66

Standard & Poor's 500 12.67 49

VALUE RANK

1.33 17

0.00 50

VALUE RANK

12.49 4

14.80 37

VALUE RANK

0.82 5

1.00 43

VALUE RANK

0.94 15

0.85 47

VALUE RANK

-0.20 62

0.00 49

23

Large Cap Equity Strategy Statistics

Supplemental Information as of March 2013. 5-year statistics.

Universe: PSN Large Cap Core. Source: PSN Enterprise.

Performance is stated gross of fees. See the performance notes included in this presentation.

Riskless index: 90 Day U.S T-Bill Information Ratio Target: S&P 500

3

4

5

6

7

8

9

10

11

-3

-2

-1

0

1

2

3

4

5

6 13

14

15

16

17

18

19

20

21

22

23

0.7

0.8

0.9

1.0

1.1

1.2

1.3 0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

-0.5

0.5

HIGH (0.95)

1st QUARTILE

MEDIAN

3rd QUARTILE

LOW (0.05)

MEAN

VALID COUNT

ROR

9.27

7.29

6.45

5.64

4.01

6.46

235

Alpha

4.02

1.62

0.80

-0.01

-1.53

0.84

235

Std Dev

14.67

17.86

18.64

19.42

21.12

18.50

235

Beta

0.75

0.93

0.98

1.01

1.10

0.97

235

Sharpe Population

0.55

0.38

0.34

0.29

0.19

0.34

235

Info Ratio

0.86

0.47

0.25

-0.05

-0.46

0.22

235

VALUE RANK

Stralem & Co. LCES 6.30 54

Standard & Poor's 500 5.81 69

VALUE RANK

1.22 35

0.00 74

VALUE RANK

15.98 6

18.76 55

VALUE RANK

0.83 7

1.00 63

VALUE RANK

0.38 27

0.30 71

VALUE RANK

0.10 60

0.00 69

24

Large Cap Equity Strategy Statistics

Supplemental Information as of March 2013. 10-year statistics.

Universe: PSN Large Cap Core. Source: PSN Enterprise.

Performance is stated gross of fees. See the performance notes included in this presentation.

Riskless index: 90 Day U.S T-Bill Information Ratio Target: S&P 500

7.5

8.5

9.5

10.5

11.5

-1.0

0.0

1.0

2.0

3.0

4.0 12.0

13.0

14.0

15.0

16.0

17.0

0.7

0.8

0.9

1.0

1.1

1.2

0.4

0.5

0.6

0.7

0.8

0.9

-0.5

0.5

HIGH (0.95)

1st QUARTILE

MEDIAN

3rd QUARTILE

LOW (0.05)

MEAN

VALID COUNT

ROR

11.67

10.04

9.36

8.79

7.60

9.46

169

Alpha

3.75

1.78

0.95

0.35

-0.52

1.10

169

Std Dev

12.21

14.24

14.74

15.21

16.51

14.70

169

Beta

0.79

0.95

0.98

1.01

1.07

0.97

169

Sharpe Population

0.74

0.58

0.53

0.48

0.41

0.53

169

Info Ratio

0.88

0.54

0.33

0.12

-0.29

0.32

169

VALUE RANK

Stralem & Co. LCES 10.49 14

Standard & Poor's 500 8.53 86

VALUE RANK

2.92 5

0.00 88

VALUE RANK

12.70 3

14.76 54

VALUE RANK

0.82 4

1.00 66

VALUE RANK

0.70 1

0.47 83

VALUE RANK

0.43 37

0.00 86

25

Investment Professionals

HIRSCHEL B. ABELSON, PRESIDENT & CHIEF INVESTMENT OFFICER: Mr. Abelson co-founded Stralem & Company Incorporated in 1966. He

became President in June of 1973. Mr. Abelson serves as Stralem’s Chief Investment Officer overseeing the firm’s investment strategy and is an officer

of Stralem Equity Fund. Prior to founding Stralem, Mr. Abelson was a partner in corporate finance as well as an economic Adviser at Ladenburg,

Thalmann which he joined in 1956. Mr. Abelson has managed and/or served on Boards of companies in the food service, housing, manufacturing,

computer products, specialty retailing, radio broadcasting and publishing industries. From 1987 – 2000, Mr. Abelson served on the trustee investment

committee of Cornell University. He is a member of the Board of Trustees at Pitzer College where he serves on the Investment Committee.

Education: BA, Cornell University, MBA, Cornell University

ADAM S. ABELSON, SENIOR PORTFOLIO MANAGER: Mr. Abelson leads the firm's research effort overseeing the implementation of the US Large-

Cap Equity Strategy. Mr. Abelson co-authors the firm's quarterly "West of the Hudson" letter, which is the product of the team's research trips around the

world. He serves as an officer of Stralem Equity Fund and a Director of Stralem Investment Fund (UCITS). MR. Abelson joined Stralem in 1998 after

managing business units within the emerging technologies, consumer products and hotel/gaming industries.

Education: BA, Pitzer College, Claremont Colleges

ANDREA BAUMANN LUSTIG, DIRECTOR, PRIVATE CLIENT ASSET MANAGEMENT; PRESIDENT, STRALEM EQUITY FUND: Ms. Lustig leads

the firm's marketing to private clients and wealth managers. She is President of Stralem Equity Fund (US) and a Director of Stralem Investment Fund

(UCITS). Prior to joining Stralem in 2003, Ms. Lustig was a Vice President with Bernstein Investment Research and Management where she spent five

years as a Financial Advisor working extensively with private clients. She joined Bernstein after eleven years at Booz, Allen & Hamilton, Inc., an

international management consulting firm, where she was a Principal in the Strategy Practice and the Director of Operations for Financial Services in the

US and Europe. Prior to Booz, Allen, Ms. Lustig was a Financial Analyst in Mergers & Acquisitions at Morgan Stanley & Co., Inc. and an Associate in

Investment Banking at Jefferies & Co. Ms. Lustig is also President of the Association for the Restoration of Jewish Works and Institutions in France

(www.arifusa.org). Ms. Lustig is a former Trustee of The Horace Mann School where she was President of the Parents Association. She is also Chair of

Annual Giving for the Princeton Class of 1980, a member of the Scholarship Committee for Le Rosey, a Steering Committee member of the Socrates

Society of the Aspen Institute, and a Board Member of the Madison Avenue Business Improvement District.

Education: BA, MPA Princeton University; MBA, Yale University. Fluent in French

ANDREW J. ERAS, CFA DIRECTOR, INSTITUTIONAL ASSET MANAGEMENT: Mr. Eras leads the firm's marketing to consultants and institutions.

Prior to joining Stralem in 2002, Mr. Eras was a Vice President with Bernstein Investment Research and Management where he spent three years as a

Pension Advisor in the Institutional Sales Group. Mr. Eras joined Bernstein after five years as Institutional Sales Manager at The Bank of Tokyo-

Mitsubishi. Prior to that, he spent five years as an internal wholesaler in the Capital Markets Group at Prudential Securities and five years as a Vice

President at Dreyfus Securities. Mr. Eras is a member of the CFA Institute and NYSSA and is a CFA Charterholder.

Education: BA, State University of New York (SUNY) at Albany

26

Investment Professionals

PHILIPPE T. LABAUNE, VICE PRESIDENT, DIRECTOR, TRADING & OPERATIONS: Mr. Labaune joined Stralem in 1997 where he directs all

trading operations for the firm. Mr. Labaune is also a Vice President of Stralem Equity Fund. Prior to joining Stralem, Mr. Labaune was a trader in

charge of ADR's at Société Générale Securities Corp.

Education: DEUG Catholic University of Lyon; BA, MBA, Pace University. Fluent in French

MICHAEL J. ALPERT, PORTFOLIO MANAGER: Mr. Alpert focuses on research for the firm's US Large Cap Equity Strategy. Prior to joining

Stralem in 2010, Mr. Alpert was a Managing Director at J&W Seligman & Co where he was the Portfolio Manager and Head of the Seligman Small

Company Growth Team. Mr. Alpert joined J&W Seligman in 1999 from business school as an Investment Analyst and became Portfolio Manager

in 2006. He had security selection responsibility in a variety of sectors including, Consumer, Technology, Industrials, Financials and Commercial

Services. Prior to business school, Mr. Alpert was a Manager for 7 years at Andersen Consulting where he did Technology and Strategic

Consulting in the Communications Industry Group.

Education: BA, University of Connecticut Honors Program, MBA Wharton School of the University of Pennsylvania

EDWARD N. COOPER, CFA, SENIOR RESEARCH ANALYST: Mr. Cooper is a senior member of the firm's research team. Prior to joining

Stralem 2006, Mr. Cooper spent ten years with Bloomberg L.P., a financial information provider, where he worked as an Equity Fundamental

Analyst., a Fixed Income Research Analyst, and a French Translator with the Localization Group. In his positions at Bloomberg, Mr. Cooper

specialized in security-level and portfolio-level analytics. He placed 1st out of a class of 40 in the 6-week intensive Bloomberg Analytics Desk

training program. Mr. Cooper is a member of the CFA Institute and NYSSA and is a CFA Charterholder. He also served in the U.S. Peace Corps in

Togo, West Africa.

Education: AB, Bowdoin College; MBA, Rutgers University. Fluent in French, Spanish and Mandarin Chinese.

IRENE BERGMAN, SENIOR VICE PRESIDENT: Ms. Bergman joined Stralem & Co. in 1973 where she has been a financial advisor and account

manager for domestic and foreign clients. Prior to Stralem, she was a senior investment professional in the International Department of Loeb,

Rhoades & Co. For ten years prior to Loeb, Rhoades, Ms. Bergman was Assistant Manager in the Foreign Department of Hallgarten & Co. where

she was active in merger arbitrages and authored a weekly market letter.

Education: Bismarck Lyceum – Berlin. Languages: Fluent in Dutch, German

27

Performance Notes

Stralem & Company (“Stralem”) is an independent, SEC registered investment adviser established in 1966. The Large Cap Equity Strategy ™ Composite (LCES) consists of fully discretionary large

capitalization equity accounts. The investment objective of the LCES is to deliver above market returns with less risk during both up and down markets. The investment philosophy of the Large Cap Equity

Strategy is predicated on the belief that there are four types of market environments, two types of bull markets and two types of bear markets each characterized by momentum and valuation factors. Market

environments affect portfolio structure so it is critical to identify and prepare for changing market environments. The Large Cap Equity Strategy adds value by purchasing a set of fundamentally solid

growth companies along with a set of companies that deliver strong cash flow and adjusting the balance between these two groups depending on where we are in the market cycle. Stralem defines the LCES

as a conservative growth strategy that also focuses on preserving capital during down markets.

For comparison purposes, the composite is measured against the S&P 500 and Russell 1000 Growth indices. The S&P 500 index is widely recognized as a leading indicator of the U.S. equity markets. The

Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher

forecasted growth values.

Stralem claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Stralem has been independently

verified for the periods January 1, 1992 through December 31, 2012. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a

firm-wide basis and (2) the firm’s policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. The Large Cap Equity Strategy Composite has been

examined for the periods January 1, 1992 through December 31, 2012. The verification and performance examination reports are available upon request.

The Large Cap Equity Strategy Composite was created July 1, 2002.

The Large Cap Equity Strategy Composite has been examined by an independent third party verifier (Ashland Partners & Company LLP). The firm maintains a complete list and description of composites,

which is available upon request. To receive a complete list and description of Stralem's composites contact Stralem at 212-888-8123.

Results are based on fully discretionary accounts under management, including those accounts no longer with the firm. Past performance is not indicative of future results. Policies for valuing portfolios,

calculating performance, and preparing compliant presentations are available upon request.

The U.S. Dollar is the currency used to express performance. Returns are presented both gross and net of management fees and include the reinvestment of all income. There are portfolios included in the

composite which have directed brokerage arrangements and are not charged trading commissions by their broker. These portfolios represent less than 2% of composite assets. Performance for these

accounts do not include transaction costs, and it has been determined that there is no material impact on composite performance. Returns are presented gross of custodial fees and withholding taxes but net

of all trading expenses. Gross returns will be reduced by investment advisory fees and other expenses that may be incurred in the management of the account. Actual investment advisory fees incurred by

clients may vary. Net of fee performance is calculated using the composite actual net performance during the period. Prior to 2006, net performance is calculated using the highest client's management fee

in the composite. From 2000 - 2005 the highest fee was 1.50%. Prior to 2000 the highest fee was 1.00%. A fee schedule is an integral part of a complete presentation and is described in Part II of the firm’s

ADV, which is available upon request. The annual composite dispersion presented is an asset-weighted standard deviation calculated for the accounts in the composite the entire year. The investment

management fee schedule is as follows: 0.80% on the first $5 million, 0.70% on the next $20 million, and 0.50% on the remainder. Actual investment advisory fees incurred by clients may vary. Clients

may have different fee arrangements than the above fee schedule with fees that are higher or lower depending on when the contract was entered into and the services provided. Accounts that require

additional resources for administration, management and servicing may be charged an advisory fee of up to 1.25% per annum. Upon request, Stralem will also provide its clients with a fulcrum fee

arrangement, which includes a lower, fixed advisory fee plus a performance based fee. Fulcrum fees arrangements may vary among clients.

Prior to 1997, carve-outs are included in this composite and performance reflects required total segment plus cash returns. All cash not directly related to fixed income is included in the equity carve-out.

100% of composite assets were comprised of carve-out segments prior to 1997. There are no carve-out segments in the composite subsequent to 1996.

These presentation materials are intended for use by the recipient named on the front cover hereof for the exclusive purpose of evaluating the investment advisory services of Stralem & Company

Incorporated in an one-on-one presentation. Any other use is strictly prohibited. These presentation materials and any attachments delivered separately herewith may contain privileged or confidential

information of Stralem & Company Incorporated. Accordingly, neither this booklet nor any portion hereof may be reproduced or redistributed without the prior written consent of Stralem & Company

Incorporated. Disclosure of the information presented in this booklet to anyone other than the recipient's employees, officers, directors, or financial or legal representatives is also prohibited without the

prior written consent of Stralem & Company Incorporated. Do not distribute this to clients unless you are using this information in a one-on-one presentation with the disclosures set forth above.

All rights reserved. Stralem & Company Incorporated. 2013