strabag se investor presentation february 2019

TRANSCRIPT

STRABAG SEINVESTOR PRESENTATION

FEBRUARY 2019

This presentation is made by STRABAG SE (the "Company") solely for use at investor meetings and is furnished to you solely for your information.

This presentation speaks as of February 2019. The facts and information contained herein might be subject to revision in the future. Neither the delivery of this presentation nor any further discussions of the Company with any of the recipients shall, under any circumstances, create any implication that there has been no change in the affairs of the Company since such date. None of the Company or any of its parents or subsidiaries or any of such person's directors, officers, employees or advisors nor any other person (i) accepts any obligation to update any information contained herein or to adjust it to future events or developments or (ii) makes any representation or warranty, express or implied, as to, and no reliance should be placed on, the accuracy or completeness of the information contained in this presentation. None of the Company or any of its parents or subsidiaries or any of their directors, officers, employees and advisors nor any other person shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising, directly or indirectly, from any use of this presentation. The same applies to information contained in other material made available at the meeting.

This document is selective in nature and is intended to provide an introduction to, and overview of, the business of the Company. Where any information and statistics are quoted from any external source, such information or statistics should not be interpreted as having been adopted or endorsed by the Company as being accurate.

This presentation contains forward-looking statements relating to the business, financial performance and results of the Company and/or the industry in which the Company operates. These statements generally are

identified by words such as "believes“, "expects”, "predicts”, "intends”, "projects”, "plans”, "estimates”, "aims”, "foresees”, "anticipates”, "targets”, and similar expressions. The forward-looking statements, including but not limited to assumptions, opinions and views of the Company or information from third party sources, contained in this presentation are based on current plans, estimates, assumptions and projections and involve uncertainties and risks. Various factors could cause actual future results, performance or events to differ materially from those described in these statements. The Company does not represent or guarantee that the assumptions underlying such forward-looking statements are free from errors nor do they accept any responsibility for the future accuracy of the opinions expressed in this presentation. No obligation is assumed to update any forward-looking statements.

By accepting this presentation you acknowledge that you will be solely responsible for your own assessment of the market and of the market position of the Company and that you will conduct your own analysis and be solely responsible for forming your own view of the potential future performance of the Company's business.

DISCLAIMER

Investor Presentation February 20192

STRABAG AT A GLANCE THE CONSTRUCTION SECTOR WITHIN EVOLVING GLOBAL THEMES

FINANCIAL PERFORMANCE

APPENDIX

1 2 3

4 5

THE STRABAG STRATEGY & INVESTMENT PROPOSITION

Investor Presentation February 20193

STRABAG AT A GLANCE1

● Output volume 2018: € 16.3 billion● Net income 2017: € 292 million● 75,460 employees● >700 locations in more than 80 countries● Highly innovative: Central Technical Division with nearly 1,000

engineers, TPA (Quality & Innovation) with 880 people● Equity ratio: >30%● Investment grade rating by S&P: BBB, outlook stable● Strong brands: STRABAG & ZÜBLIN

FACTS & FIGURES MARKETS

OUTPUT VOLUME BY REGION (2018)

STRABAG AT A GLANCE

#2

SaudiArabia

OmanAbu Dhabi

Qatar

#1

#1#1#1

#1

#2

#3

Colombia

Chile

#1

Germany48%

Austria16%

CEE22%

Rest of Europe8%

Rest of world7%

Investor Presentation February 20195

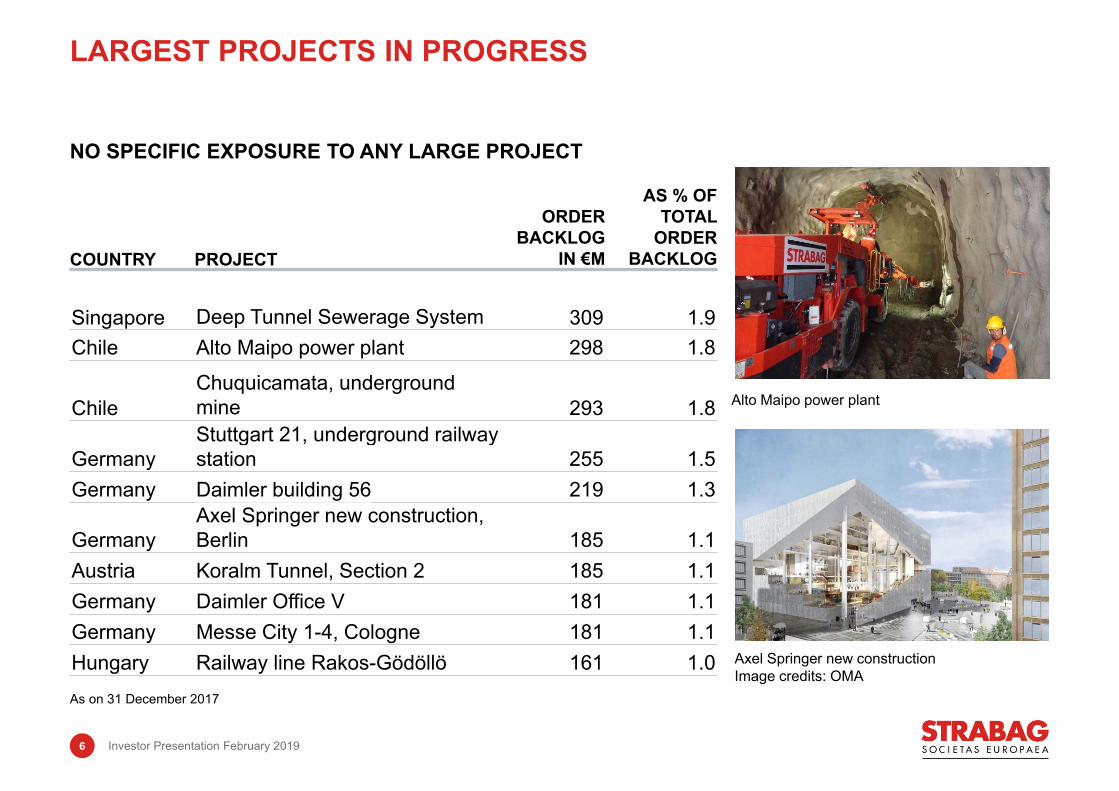

COUNTRY PROJECT

ORDER BACKLOG

IN €M

AS % OF TOTAL

ORDER BACKLOG

Singapore Deep Tunnel Sewerage System 309 1.9Chile Alto Maipo power plant 298 1.8

ChileChuquicamata, underground mine 293 1.8

GermanyStuttgart 21, underground railway station 255 1.5

Germany Daimler building 56 219 1.3

GermanyAxel Springer new construction, Berlin 185 1.1

Austria Koralm Tunnel, Section 2 185 1.1Germany Daimler Office V 181 1.1Germany Messe City 1-4, Cologne 181 1.1Hungary Railway line Rakos-Gödöllö 161 1.0

NO SPECIFIC EXPOSURE TO ANY LARGE PROJECT

As on 31 December 2017

LARGEST PROJECTS IN PROGRESS

Alto Maipo power plant

Axel Springer new constructionImage credits: OMA

6 Investor Presentation February 2019

Building of an arch bridge

Size: € 22 million (=60% share)

Project schedule: 2013–2017

Project scope: 475 m long arch bridge with a span of 260 m

TAMINA BRIDGE –SWITZERLAND

Financing, planning, building and operating

Size: € 330 million

Project schedule: 2014–2017

Project scope: 57 km motorway, 25-year operating period

PPP-MOTORWAY N17/N18 – IRELAND

Building of a twin-tube rail tunnel between Tulfes–Pfons

Size: € 380 million (=51% share)

Project schedule: 2014–2019

Project scope: 38 km twin-tube rail tunnel, exploratory and rescue tunnel

BRENNER BASE TUNNEL –AUSTRIA

Construction of new office and production buildings in Zug, Switzerland

Size: ~ € 100 million

Project schedule: 2016–2018

Project scope: General contractor, BIM 5D® applied

OFFICE & PRODUCTION BUILDINGS FOR SIEMENS

Picture: Thomas Böhm, Tiroler Tageszeitung

FLAGSHIP PROJECTS – EXAMPLES

Picture: Siemens Schweiz AG

Investor Presentation February 20197

FLAGSHIP PROJECTS – INTERNATIONAL

Size: € 197 million (=60% share)Project schedule: 2008–2020Project scope: Construction of an 8.9 km long two-lane road tunnel with integrated emergency tunnel beneath the roadway via the NATM tunnelling method

ROHTANG PASS HIGHWAY TUNNEL – INDIA

Size: € 165 millionProject schedule: 2016–2020Project scope: 12.9 km TBM tunnel, Ein Karem exit shaft (22 m deep), Soreq adit (1.4 km > NATM), complete tunnel with steel tube + Kesalon connecting route (320 m) + Ein Karem connecting route (10 m) > ca. 13.3 km steel hydraulics construction, commissioning

JV 5TH LINE WATER SUPPLY – JERUSALEM

Size: € 893 million(37.5% share)Project schedule: 2016–2022Project scope: 176 km national road (38 km 4-lane national road –71 km rehabilitation of 2-lane natinal road and operation and maintenance of 72 km national road), construction includes a 4.6 km tunnel and 67 bridges with a total length of 7.3 km

MAR1 – CONCESSION –COLOMBIA

Size: € 106 million (50% share)Project schedule: 2017–2020Project scope: Construction of a 1,132 m long bridge over the river Mtentu near the town of Flagstaff

AFRICA’S HIGHEST BRIDGE – SOUTH AFRICA

Investor Presentation February 20198

North + West South + EastInternational +

Special Divisions

Regions/Areas

Germany, Poland, Benelux, Scandinavia, Ground

Engineering

Austria, Switzerland, Hungary, Czech Republic, Slovakia,

Adriatic, Rest of Europe, Environmental Engineering,

Russia

International, Tunnelling, Services, Real Estate

Development, Infrastructure Development, Construction

Materials

Output volume (€m) 6,843 4,242 3,404

Order backlog (€m) 8,138 4,505 3,944

EBIT (€m) 199 205 62

EBIT margin (%) 3.1 5.0 2.4

Employees 23,366 17,916 25,618

4th, non-operating segment “Others”, output volume 1%, not shown

BUSINESS SEGMENT CONTRIBUTION 2017

29% of output volume

23% of output volume

47% of output volume

Investor Presentation February 20199

(€m) 2017 2016 %Output volume 14,621 13,491 8Revenue 13,509 12,400 9EBITDA 835 855 -2EBITDA adjusted 8271

EBIT 448 425 6EBIT adjusted 3971

Net income after minorities 279 278 0Cash flow from operating activities 1,345 264 409Cash flow from investing activities -333 -434 23Balance sheet total 11,054 10,378 7Group equity 3,398 3,265 4Equity ratio 30.7% 31.5%Net debt (+)/cash (-) -1,335 -449 -197Δ% was calculated with original, not rounded figures therefore, rounding differences may occur.

1 Adjusted for a non-operating profit in the amount of € 27.81 million.

KEY FINANCIALS

Investor Presentation February 201910

INTEGRATED MODEL TAKES ADVANTAGE OF ● local management skills● market knowledge● cost and efficiency synergies● risk diversification

COMPREHENSIVE COUNTRY NETWORK ENABLES STRABAG TO● make more use of technology and

machinery ● follow clients around the world

Only countries with a minimum annual output volume and a minimum order backlog of € 1 million are considered.

COMPREHENSIVE COUNTRY NETWORK

Investor Presentation February 201911

THE CONSTRUCTION SECTOR WITHIN EVOLVING GLOBAL THEMES

2

GERMANY: DAILY TRAFFIC LOAD 2030F

● By 2050 66% of the global population will live in cities (today: 54%) – an increase of the urban population by 2.5 billion.

Higher need for infrastructure● McKinsey: USD 57 trillion infrastructure investment

needed by 2030 to keep up with global economy, 4% annual growth rate for construction companies

● Significant need for rehabilitation and extension of the German transportation network within the next ten years – € 2.6 billion of additional investments p.a. necessary over 15 years according to Daehre Commission 2012

● Investments into German federal roads

2018e: € 13.9 billion / A-roads: € 7.2 billion

● “Bundesverkehrswegeplan 2030”: German investment plan with total sum of € 270 billion (focused on infrastructure in the Western part)

Sources: BMVI, Verkehrsverflechtungsprognose 2030 – Netzumlegungen, August 2015, Bundeshaushalt Einzelplan 12, Bundesverkehrswegeplan; Report of the Daehre Commission in December 2012; http://ec.europa.eu/cli; ma/policies/brief/eu/index_en.htm; „Voices on Infrastructure“, Global Infrastructure Initiative by McKinsey & Company

FIVE EUROPEAN TRENDS:(1) URBANISATION/DEMOGRAPHICS

Vehicles(thousands/day)

>9070-9050-7030-5020-3015-2010-15<10

Investor Presentation February 201913

0

45

Slovenia Germany Croatia Austria Hungary CzechRepublic

Slovakia Bulgaria Poland Romania

km m

otor

way

/ 1,

000

km2

1995 2006 2016Source: Eurostat

EXAMPLE:MOTORWAY DENSITY IN DIFFERENT MARKETS

Investor Presentation February 201914

● Investment of USD 48 trillion needed to just meet the world’s energy needs by 2035, according to McKinsey1

● EU: 2030 climate and energy framework sets 3 targets: At least 40% cuts in greenhouse gas emissions At least 27% share of renewable energy At least 27% improvement of energy efficiency

● Buildings account for the largest share of total EU final energy consumption (40%) and produce about 35% of all greenhouse gas emissions2

Clients increasingly ask for energy-efficient solutions, environmentally friendly products and a sustainable business conduct of suppliers.Own building materials network provides a high barrier to entry for other market participants, as the permits for building new mixing plants are not granted easily due to environmental concerns.

1 „Voices on Infrastructure: Rethinking engineering and construction“, Global Infrastructure Initiative by McKinsey & Company, October 20162 European Commission: http://ec.europa.eu/growth/sectors/construction_en (last accessed 24 August 2018)

FIVE EUROPEAN TRENDS:(2) ENERGY/SUSTAINABILITY

A2 Poland

Investor Presentation February 201915

● Historically low interest rates and highly volatile financial environment make real estate an attractive investment alternative for some investor groups

● Low financing costs facilitate investment into real estate

STRABAG Real Estate Development Tanzende Türme, Hamburg

FIVE EUROPEAN TRENDS:(3) FINANCIAL ENVIRONMENT

Investor Presentation February 201916

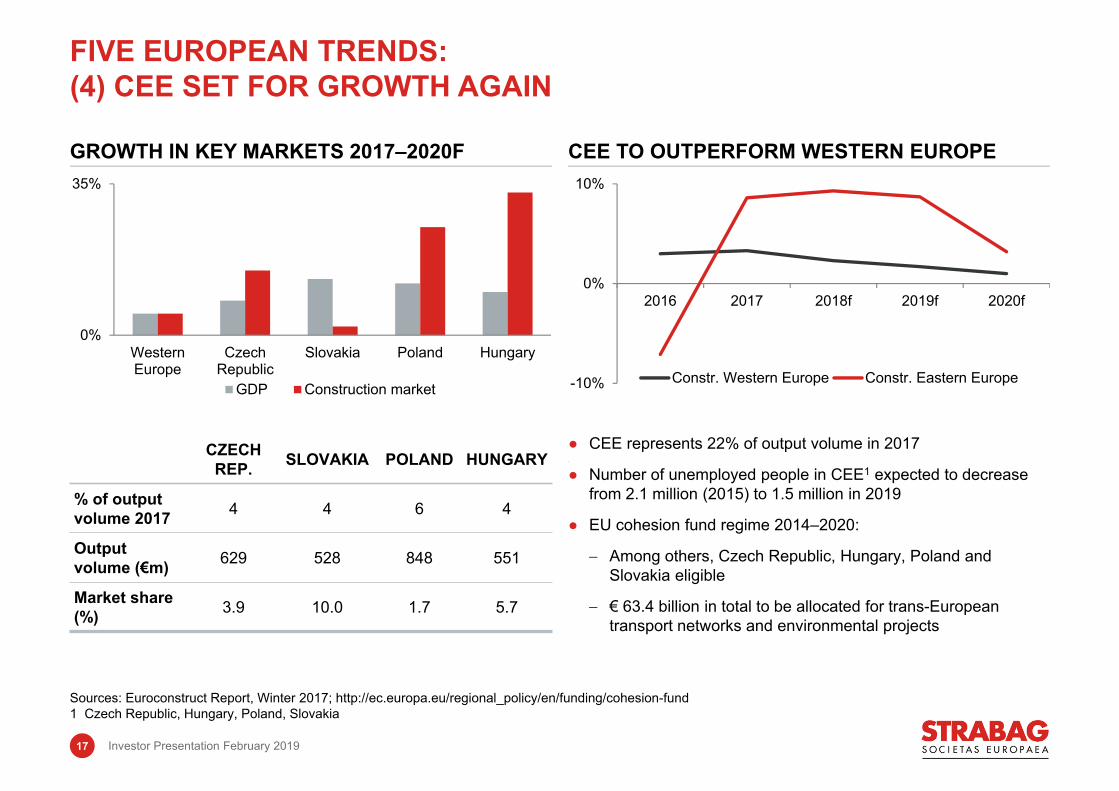

0%

35%

WesternEurope

CzechRepublic

Slovakia Poland Hungary

GDP Construction market

GROWTH IN KEY MARKETS 2017–2020F

CZECH REP. SLOVAKIA POLAND HUNGARY

% of output volume 2017 4 4 6 4

Output volume (€m) 629 528 848 551

Market share (%) 3.9 10.0 1.7 5.7

-10%

0%

10%

2016 2017 2018f 2019f 2020f

Constr. Western Europe Constr. Eastern Europe

CEE TO OUTPERFORM WESTERN EUROPE

● CEE represents 22% of output volume in 2017

● Number of unemployed people in CEE1 expected to decrease from 2.1 million (2015) to 1.5 million in 2019

● EU cohesion fund regime 2014–2020:

Among others, Czech Republic, Hungary, Poland and Slovakia eligible

€ 63.4 billion in total to be allocated for trans-European transport networks and environmental projects

Sources: Euroconstruct Report, Winter 2017; http://ec.europa.eu/regional_policy/en/funding/cohesion-fund 1 Czech Republic, Hungary, Poland, Slovakia

FIVE EUROPEAN TRENDS:(4) CEE SET FOR GROWTH AGAIN

Investor Presentation February 201917

CONSTRUCTION SECTOR LAGGING BEHIND REGARDING PRODUCTIVITY GAINS1

Less than 6% of construction companies use digital instruments for planning holistically.

<6%

Source: „Digitalisierung der Bauwirtschaft“, Roland Berger, 20161 Figures for Germany; period under consideration: 10 years

FIVE EUROPEAN TRENDS:(5) DIGITALISATION

Construction industry

4%Producing industry

27%Manufacturing industry

34%

of players in the construction sector agree that digitalisation will effect all their processes.

93%

Investor Presentation February 201918

-10%

0%

10%

2014 2015 2016 2017e 2018e

Residential Other building construction Civil

CONSTRUCTION SUBSEGMENTS GERMANY

-10%

0%

10%

2014 2015 2016 2017e 2018e

Germany Austria Eastern Europe

Public62%

Private38%

STRABAG CLIENT STRUCTURE

CONSTRUCTION OUTPUT BY COUNTRIES

● Public client:The price is mostly the dominant criterion.

● Private client:Often opts for the best offer, not necessarily the lowest.

Source: Euroconstruct

CONSTRUCTION SEGMENTS HAVE THEIR OWN BUSINESS MODELS AND CYCLES

Investor Presentation February 201919

SELECTION CRITERIA IN CONSTRUCTION

Financial strength

References

Technology& Innovation

Constructionmaterials supply

Experience andKnow-how of employees

Clients’ selection criteria

Price

Investor Presentation February 201920

THE STRABAG STRATEGY & INVESTMENT PROPOSITION

3

“STRABAG is a European-based technology group for construction services,

a leader in innovation and financial strength. We create added value for our

clients by integrating the most diverse services and assuming responsibility

for them: We bring together people, materials and machinery at the right place

and at the right time in order to realise even complex construction

projects – on schedule, of quality and at the best price.”

A EUROPEAN-BASED TECHNOLOGY GROUP FOR CONSTRUCTION SERVICES

STRABAG takes an agreed scope of responsibility and part of the risk, thereby relieving the client e.g. of the risk of delays and cost overruns.Professional and market experience as well as financial strength needed to create added valueHelps clients meet their goals (time, quality, lower costs)Technology/Innovation: Differentiation through superior technology and innovative solutions

Investor Presentation February 201922

SIX STRATEGIC FIELDS

Investor Presentation February 201923

(1) Margin Upside Strategic priority: Strengthening risk and opportunity management Strategic priority: Implementing efficiency-rising measures proposed by task force

(2) Flexible Business Model, Selective Diversity Strategic priority: Showing flexibility Strategic priority: Staying diversified Strategic priority: Offering top technology and sustainability

(3) Financial Strength Strategic priority: Maintaining financial strength

(4) Attractive Dividends on a reliable level

THE STRABAG INVESTMENT PROPOSITION

Investor Presentation February 201924

-3%

-3 %0%

-6%

8%

-8%

5%

2013 2014 2015 2016 2017 2018

5 %

2.1%2.3%

2.6%

3.2%

≥3.3%

0%

4%

2013 2014 2015 2016 2017 2018

3.3%

TARGET 2018 OF 3.3% EBIT MARGIN1

● Comprehensive risk management

TOP-LINE GROWTH NOT IN THE FOCUS

● Forecast for output volume 2018 should clearly exceed € 15.0 billion (+3%)

1 2016 adjusted for a non-operating profit in the amount of € 27.81 million; 2018 adjusted for a positive non-operating one-off due to the acquisition of the remaining 50 % interest in a German concession company in the amount of € 55.31 million

(1) MARGIN UPSIDE: TARGETS

8%

>3%

5%

Investor Presentation February 201925

● Four-eyes-principle

● Internal price committees (including a STRABAG SE board member when project volume ≥€ 70 m)

● Internal Audits

● Organisational structure with central divisions

● Management information system:

“We have developed a management information system that helps us to ensure that the same standards apply in all regions where STRABAG is active. This means: clear criteria for the assessment of new projects, a standardised process for the submission of bids and control systems serve as filters to avoid loss-bringing projects.”

Thomas Birtel, CEO

RISK MANAGEMENT INSTRUMENTS

● Joint Venture with the client

● Cost + fee

● Guaranteed maximum price

● Lump-sum

● Unit pricing

TYPES OF CONTRACTS

COMPOSITION OF THE ORDER BACKLOG

(1) MARGIN UPSIDE: RISK MANAGEMENT

14%Total of the ten largest projects in the order

backlog

12,443Construction sites

per year

Investor Presentation February 201926

(2) FLEXIBLE BUSINESS MODEL, SELECTIVE DIVERSITY: RESILIENCE IN A VOLATILE INDUSTRY

1 2016 adjusted for a non-operating profit in the amount of € 27.81 million.

OUTPUT VOLUME (€M) ORDER BACKLOG (€M)

EBITDA (€M) AND EBITDA MARGIN (%)1 EBIT (€M) AND EBIT MARGIN (%)1

13,573 13,566 14,290 13,491 14,621

0

20000

2013 2014 2015 2016 2017

13,470 14,40313,135

14,81616,592

0

20000

2013 2014 2015 2016 2017

397262 282 341

0

1000

2013 2014 2015 2016 2017

3.2%

2.1% 2.3%2.6%

3.3%

827

695 720816

0

1000

2013 2014 2015 2016 2017

6.9% 6.2%

5.6% 5.8%6.2%

835

448

20,000 20,000

1,000 1,000

Investor Presentation February 201927

Own40%

Sub-contractors

60%

SUBCONTR. BUILDING & CIVIL ENGINEERING

● Diversifying geographically

● Top market positions in stable home markets

● Offer services along the entire construction value chain

Own70%

Sub-contractors

30%

SUBC. TRANSPORTATION INFRASTRUCTURE

DIVERSIFIED PORTFOLIO BALANCES CYCLICAL/PROJECT-DRIVEN NATURE OF CONSTRUCTION

(2) FLEXIBLE BUSINESS MODEL, SELECTIVE DIVERSITY: SUBCONTRACTING AND PORTFOLIO MIX

Transportation Infrastructure

37%

Building Construction &

Civil Engineering 37%

Services 9%

International & Tunneling 9%

Construction Materials 6%

Project development & Concessions

2%

Own70%

Investor Presentation February 201928

● Asphalt mixing plants 2522

● Concrete mixing plants 1462

● Total quarries and gravel pits 1542

● Cement mixing plants 53

● Production of 3.9 million m³ of concrete, 15.8 million tons of asphalt and 1.2 million tons of cement in 2017

● Sales revenue of € 585 million in 2017

STRABAG FACILITIES1

● Hedge against price fluctuations, securing supply

● Existing quarries as effective entry barriers – lack of permits for new sites

● 30% in joint venture (at equity-consolidated since Q3/2011) with LafargeHolcim secures access to cement in Central and Eastern Europe

● Further optimisation of raw materials network and increased self-sufficiency except in asphalt

OWN COVERAGE OF MATERIAL NEEDS (%)

HIGHLIGHTS

1 December 20172 Includes active facilities from joint ventures and associates3 Thereof four in JV with LafargeHolcim (STRABAG share 30%) and one in another investment (STRABAG share 25.6%)

(2) FLEXIBLE BUSINESS MODEL, SELECTIVE DIVERSITY: OWN DENSE CONSTRUCTION MATERIALS NETWORK

0%

100%

Asphalt Concrete Cement Stone/Gravel2017 2016

18%

78%

26% 24%

78%

28% 28%17%

Investor Presentation February 201929

NUMBER OF STRABAG’S PPP1 PROJECTS SELECTED PPP PROJECTS

PPP STRATEGY SELECTED PPP PROJECTS

1 Public-Private Partnership/Build-Operate-Transfer

(2) FLEXIBLE BUSINESS MODEL, SELECTIVE DIVERSITY: STEADY INCOME THROUGH CONCESSION BUSINESS

Vocational schools, Germany Motorway A8, Germany

COUNTRY PROJECTTOTAL

COST (€M) % SHARECONCESSION

UNTIL STATUS

PL A2 Section II 1,543 10 2037 Operation

HU M5 Motorway 1,292 100 2031 Operation

HU M6 Motorway 966 50 2037 Operation

COL MAR1 893 37.5 2045 In progress

GER Schools,Mülheim 52 100 2045 Operation

GER Ministries, Potsdam 41 100 2035 Operation

● Focus on infrastructure and large public buildings● PPP/BOT1 in home markets, Eastern Europe and

increasingly in selected international markets (insufficient legal framework in some countries)

● Importance as public procurement method due to cost advantages

● High barriers to entry due to necessary PPP expertise and financial strength

36 37 34 35 38

0

50

2013 2014 2015 2016 2017

Investor Presentation February 201930

TARGET MARKETS

● Output 2017: € 1.1 billion

● ~ 10,000 employees (FTE)

● Broad range of customers: Airbus, Audi, Commerzbank, Deutsche Bahn, DFS, Hahn-Gruppe, ESPRIT, IMMOFINANZ, Jungheinrich, Nordex, ORSAY, RWE, Telefónica Deutschland, Vodafone, WealthCap, etc.

● Active in Germany, Austria, Hungary, Poland, Czech Republic, Slovakia

● #4 market position in German facility management (“Lünendonk” 2017 ranking)

● Long-term contract with client Deutsche Telekom AG will end June 2019

● Consolidated in the International + Special Divisions segment

KEY FACTS 2017

KEY ACCOUNTS

(2) FLEXIBLE BUSINESS MODEL, SELECTIVE DIVERSITY: PROPERTY & FACILITY SERVICES

Commerzbank Tower, Frankfurt, Germany

DFS Deutsche Flugsiche-rung HeadquartersFrankfurt, Germany

City Tower, Praha, Czech Republic

Investor Presentation February 201931

3D MODEL: DEFINING THE “TO BE BUILT” 4D – TIME: WHEN ARE WORKS EXECUTED?

5D – PROCESS: MATERIALS, ORDERS● Single data pool as an answer to specialisation

and growing number of companies involved● Risk management: Inconsistencies detected

earlier● Clients get a clearer picture of the impacts

resulting from alterations, renovations, additions● Budget and time overruns minimized

ADVANTAGES OF BIM 5D®

(2) OFFERING TECHNOLOGY AND SUSTAINABILITY: BIM 5D® COULD BE A REVOLUTION IN CONSTRUCTION

Investor Presentation February 201932

BIM 5D® ALSO APPLICABLE FOR TRANSPORTATION INFRASTRUCTURE PROJECTS

● 3D visualisation● Topographic mapping via drones and other

innovative hard- & software● Model-based quantity take-off during tender stage

and quantity on-site controlling in execution phase● Model-linked 4D time tables● Integrated logistics concepts and simulations● Model-based machine control on-site

Isometrics of a combined traffic & bridge construction model

(2) OFFERING TECHNOLOGY AND SUSTAINABILITY:INTELLIGENT PROCESS ENGINEERING

Investor Presentation February 201933

1.1 %

3.2 %

1.9 %1.5 %

0.6 %0.2 % 0.2 % 0.1 % 0.1 %

0%

4% % of total headcount

750 500 500450

150 125 105 100 900

2000 Number of employees ● Central Technical Division – organisation in charge of planning and execution of R&D projects

● Focus on building construction and civil engineering

● 24 locations

● TPA – organisation focused on optimising technical processes, workplace safety and quality

● Focus on transportation infrastructure

● STRABAG’s competence centre for quality management and construction R&D

● 130 locations

● Total R&D spending: ~ € 10-15 million p.a.

1 Analysis carried out by STRABAG R&D department in 2014

STRABAG AND PEERS: R&D/TECHNICAL DIVISION STAFF HEADCOUNT1

(2) OFFERING TECHNOLOGY AND SUSTAINABILITY: CASE STUDY – CENTRAL TECHNICAL DIVISION/TPA

Central Technical DivisionTPA

STRABAG Peers

STRABAG Peers

800

0

2,000

Investor Presentation February 201934

13.6% 13.8% 13.9% 14.9% 14.9%

8.6% 8.5% 8.7% 8.4% 9.0%

0%

16%

2013 2014 2015 2016 2017Women as % of management Women as % of staff

TARGET: GROW SHARE OF WOMEN IN TOTAL EMPLOYMENT AND MANAGEMENT EACH YEAR

(2) OFFERING TECHNOLOGY AND SUSTAINABILITY: EXAMPLE ON NON FINANCIAL TARGETS – WOMEN

Investor Presentation February 201935

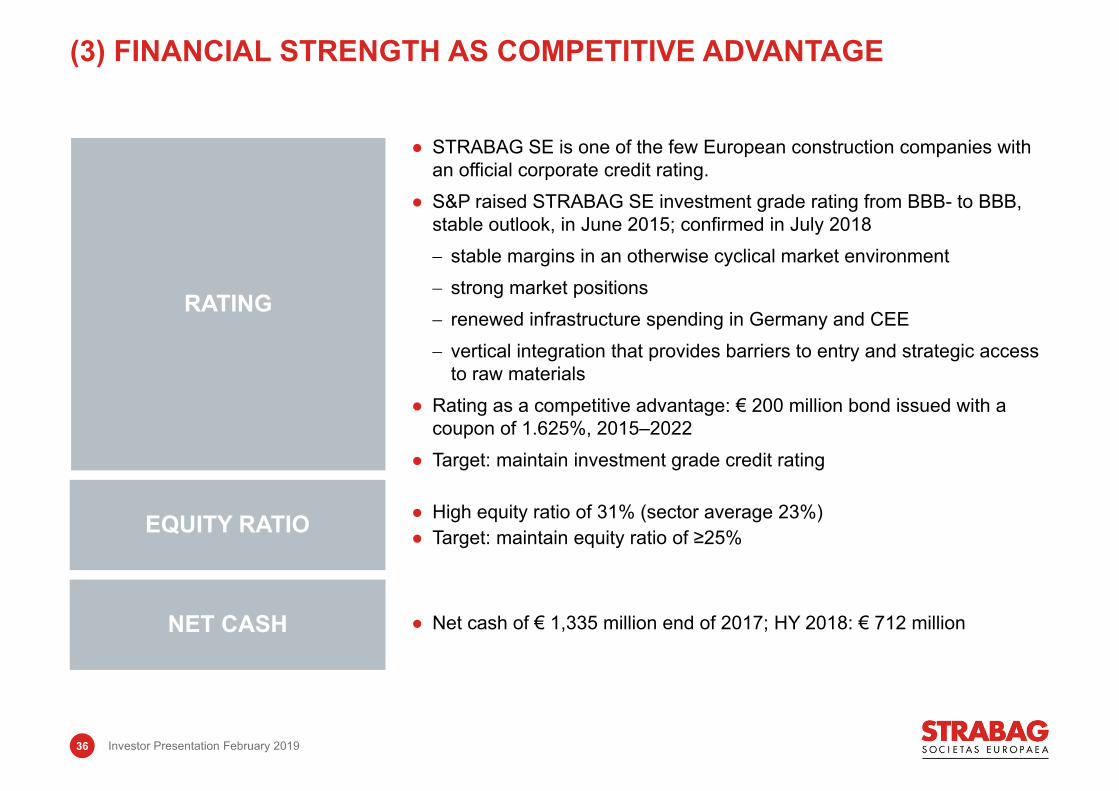

(3) FINANCIAL STRENGTH AS COMPETITIVE ADVANTAGE

RATING

● STRABAG SE is one of the few European construction companies with an official corporate credit rating.

● S&P raised STRABAG SE investment grade rating from BBB- to BBB, stable outlook, in June 2015; confirmed in July 2018 stable margins in an otherwise cyclical market environment strong market positions renewed infrastructure spending in Germany and CEE vertical integration that provides barriers to entry and strategic access

to raw materials● Rating as a competitive advantage: € 200 million bond issued with a

coupon of 1.625%, 2015–2022● Target: maintain investment grade credit rating

EQUITY RATIO

NET CASH

● High equity ratio of 31% (sector average 23%)● Target: maintain equity ratio of ≥25%

● Net cash of € 1,335 million end of 2017; HY 2018: € 712 million

Investor Presentation February 201936

DEBT REPAYMENT PROFILE (€M)

TERM INTEREST VOLUME ISIN

2012–2019 4.25% € 100 m AT0000A0V7D8

2013–2020 3.00% € 200 m AT0000A109Z8

2015–2022 1.625% € 200 m AT0000A1C741

● Cash and surety credit lines (31 December 2017): € 7.7 billion (thereof cash credit lines of € 0.4 billion)

● Bond issue: € 200 million, 1.625 %, 2015-2022

● € 2.0 billion syndicated surety loan (by 2023)

● € 400 million syndicated cash credit line (by 2023)

DIVERSIFIED MEANS OF FINANCING

CORPORATE BONDS

(3) FINANCIAL STRENGTH: DIVERSIFIED FINANCING

18.50

0

300

2019 2020 2021 2022

Bonds Bonded loan

100

200200

Investor Presentation February 201937

114 128156

278 2792.1%

0.9%

0.5 %

1.0%

0

350

2013 2014 2015 2016 2017

1.2%

2.2%

NET INCOME A.M. (€M) AND MARGIN (%)

2.72

1.11 1.251.52

2.71

0

3

2013 2014 2015 2016 2017

1.30

0.45 0.500.65

0.95

41% 40% 43%35%

48%

0%

100%

0

2

2013 2014 2015 2016 2017€

DIVIDEND (€) AND PAYOUT RATIO (%)

EARNINGS PER SHARE (€) DIVIDEND (€) AND PAYOUT RATIO (%)

(4) ATTRACTIVE DIVIDENDS:CONSISTENT PAYOUT RATIO

0%

0%

€

Investor Presentation February 201938

-14.8%

4.4%

-14.7%

3.4%

3.1%

2.4%-2.5%

-20%

50%

2013 2014 2015 2016 2017

Return from share price Return from dividends

3.6%

-14.7%

2.9%

2.4

42.7%

29.7%

1.1%%

(4) ATTRACTIVE DIVIDENDS: TOTAL SHAREHOLDER RETURN 2013–2017

Dividend policy: 30-50 % of net income after minorities distributed as a dividend

Ø dividend yield: 3.0%

Investor Presentation February 201939

Dividend yield based on average share price

FINANCIAL PERFORMANCE

4

Investor Presentation February 201941

9M/18: OUTPUT VOLUME ROSE BY 12 %

OUTPUT VOLUME (€M)

11,64610,383

14,621

0

20.000

9M/18 9M/17 2017

● Driven especially by German building construction & civil engineering business, Americas, Austria and Poland

12%

ORDER BACKLOG (€M)

18,16116,038 16,592

0

20.000

9M/18 9M/17 2017

13% ● Order backlog remains above € 18 billion

● Large orders from the group’s largest markets, e.g. Germany, Poland and Hungary

● Q2: triple-digit million-euro contract extension for Alto Maipo tunnelling project, Chile

20,000

20,000

Investor Presentation February 201942

571448

835

-100

1.000

9M/18 9M/17 2017

9M/18: EBITDA AND EBIT POSITIVELY IMPACTED BY ONE-OFF, UNDERLYING EARNINGS HIGHER AS WELL

EBITDA (€M)

● Positive non-operating one-off in the amount of € 55.31 million due to the acquisition of the remaining 50% interest in PANSUEVIA (“step-up”)

● EBITDA adjusted by one-off: € 516 million (+15%)

● Q3/18: EBITDA adjusted +6%

● Depreciation and amortisation decreased by 2%

● EBIT adjusted by one-off: € 244 million (+43%)

● Q3/18: EBIT adjusted +10%

27%

299

171

448

-100

500

9M/18 9M/17 2017

75%

1,000

EBIT (€M)

Investor Presentation February 201943

1.74

0.80

2.72

-1

3

9M/18 9M/17 2017

178

82

279

-100

300

9M/18 9M/17 2017

9M/18: NET INCOME AFTER MINORITIES MORE THAN DOUBLED

NET INCOME AFTER MINORITIES (€M)

● Net interest income at € -10 million after € -35 million in 9M/17, when negative internal exchange rate differences had burdened

● Earnings attributable to minority shareholders € 9 million (9M/17: € 5 million)

EARNINGS PER SHARE (€)

117%117%

Investor Presentation February 201944

(€m) 9M/18 2017Share capital 110 110Capital reserves 2,315 2,315Retained earnings 1,017 945Non-controlling interests 34 27Equity 3,477 3,398Provisions 1,139 1,161Financial liabilities 1,128 883Other liabilities 82 78Deferred taxes 105 24Non-current liabilities 2,456 2,145Provisions 672 747Financial liabilities 333 411Trade payables 3,684 3,402Other current liabilities 870 950Current liabilities 5,559 5,511Equity & Liabilities 11,492 11,054

(€m) 9M/18 2017Intangible assets 495 499Rights from concessionarrangements 622 0PP&E & investment property 2,080 1,942Equity-accounted investments 358 350Other investments 196 183Concession receivables 636 662Other receivables 238 271Deferred taxes 143 189Non-current assets 4,768 4,096Inventories 787 1,138Trade and other receivables 4,147 2,996Concession receivables 36 34Cash and cash equivalents 1,754 2,790Current assets 6,724 6,958

Assets 11,492 11,054

9M/18: HIGH EQUITY RATIO DESPITE BALANCE SHEET GROWTH

ASSETS1 EQUITY AND LIABILITIES1

1 Rounding differences might occur.

Investor Presentation February 201945

(€m) 9M/18 ∆% 9M/17Cash – beginning of period 2,790 40 1,998

Cash flow from earnings 413 31 316

∆ Working Capital -522 -30 -400

Cash flow from operating activities -109 -28 -85

Cash flow from investing activities -473 -95 -242

Cash flow from financing activities -437 -120 -199

Net change in cash -1,018 -94 -525

FX changes -18 n.m. 2

Change restricted cash -1 n.m. 1

Cash – end of period 1,753 19 1,474

9M/18: STRONGER WORKING CAPITAL INCREASE, HIGHER INVESTMENTS

Rounding differences might occur.

Investor Presentation February 201946

48% of group output volume

9M/18: NORTH + WEST: GOOD WEATHER AND GOOD BUSINESS IN GERMANY

KEY INDICATORS● Output volume increased by 15%

● EBIT higher by 71%; reflected good economic activity in the German TI segment

● Growth in orders 19%; large orders, among others:

Oldenburg–Wilhelmshaven rail upgrade line, Germany

Further sections of S7 and A1, Poland

Copenhagen’s Carlsberg quarter, Denmark

ODE building in Amsterdam, Netherlands

● Outlook:

Output volume 2018 expected to surpass last year’s record

German BC&CE should continue to contribute positively to output volume and earnings despite tense situation on subcontractor market

Excellent year for TI, but labour remains a limiting factor

Poland: capacity shortage led to double-digit percent price increases last year, but high order backlog enables greater project selection

COMMENTS

SHARE OF GROUP OUTPUT VOLUME

BC&CE: Building Construction & Civil EngineeringTI: Transportation Infrastructures

(€m) 9M/18 Δ% 9M/17

Output volume 5,556 15 4,814

Revenue 5,015 11 4,517

Order backlog 9,162 19 7,697

EBIT 44 71 25

EBIT margin % 0.9 0.6

Employees 23,969 4 23,146

Investor Presentation February 201947

(€m) 9M/18 Δ% 9M/17

Output volume 3,324 9 3,044

Revenue 3,189 15 2,769

Order backlog 4,903 16 4,238

EBIT 92 -34 139

EBIT margin % 2.9 5.0

Employees 18,434 4 17,644

9M/18: SOUTH + EAST: HIGH DEMAND FOR PERSONNEL AND SUBCONTRACTOR SERVICES WEIGHS ON MARGINS

KEY INDICATORS

● Output volume climbs by 9% thanks to Austria, Croatia and Hungary

● EBIT fell by 34%; tense markets for human resources and subcontractor services and unusually strong margins in 2017

● Order backlog +16%, mainly driven by TI projects in Hungary and BC projects in Austria

● Outlook:

Output volume expected to continue to grow with attractive margins in 2018

Situation in Austria remains positive

Falling margins in Czech Republic and Slovakia

Working off high order backlog in Hungary is a challenge

COMMENTS

SHARE OF GROUP OUTPUT VOLUME

TI: Transportation Infrastructures; BC: Building Construction

29% of group output volume

Investor Presentation February 201948

9M/18: INTERNATIONAL + SPECIAL DIVISIONS REPORTS ENORMOUS GROWTH IN EBIT

KEY INDICATORS● Output volume up by 11% due to the work on large projects

in the Americas

● Sale of real estate developments and the absence of burden from large international projects benefitted earnings

● Order backlog stable:

Contract extension for Alto Maipo project, Chile

1.7 km Boyneburg tunnel, Germany

13 km tunnel sector for Woodsmith Mine, UK

Backlog fell in Italy and Austria, among others

● Outlook:

Output volume 2018 should be comparable to 2017, improved earnings expected

Real estate development, property & facility services and existing public-private partnerships should continue to make very positive earnings contributions

International focus in southeast Africa and internationally financed projects

COMMENTS

SHARE OF GROUP OUTPUT VOLUME

(€m) 9M/18 Δ% 9M/17

Output volume 2,684 11 2,419

Revenue 2,462 20 2,051

Order backlog 4,093 0 4,099

EBIT 126 413 24

EBIT margin % 5.1 1.2

Employees 26,181 1 25,815

23% of group output volume

2,344

3,436

3,932 3,854

2,468

3,736 4,051 4,034

2,257

3,420

3,884 3,930

2,427

3,828 4,129 4,238

2,600

4,276

4,770

-16456 172 218

-15991 184 225

-145125 197 249

-143110 203

-,500

5,000

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17 Q3/17 Q4/17 Q1/18 Q2/18 Q3/18

Output volume EBIT

QUARTERLY DEVELOPMENT OF OUTPUT VOLUME AND EBIT (€M)

1 EBIT/revenue

HIGHLY SEASONAL BUSINESS

3.9%6.7%

-7.6%

EBIT

mar

gin1

-1.8% 4.9% 6.1%

-7.0%2.6% 4.9% 6.2%

-6.9%3.2%

5.5%

-5.9%

6.4%

500 -139279

-6.5%

7.2%5.4%

278

Investor Presentation February 201949

159

4.0%

Germany47%

Austria16%

CEE22%

Rest of Europe9%

Rest of world6%

OUTPUT VOLUME 2017 BY REGION

14,62113,491

0

20000

2017 2016

● Output volume rose by 8% to € 14.6 billion

● Especially strong increase in German transportation infrastructure and Austrian building construction

German share in group output volume continually rising

● Upward trend also in CEE core markets

OUTPUT VOLUME (€M)

OUTPUT VOLUME INCREASED IN NUMEROUS MARKETS

+8%20,000

Investor Presentation February 201950

Germany42%

Austria12%

CEE25%

Rest of Europe10%

Rest of world11%

ORDER BACKLOG 2017 BY REGION

16,59214,816

0

20000

2017 2016

ORDER BACKLOG (€M)

SEVERAL LARGE CONTRACTS LED TO RECORD ORDER BACKLOG

+12%20,000 ● Several large orders from diverse fields and

markets:

Transportation infrastructure in Hungary and Poland

Building construction and civil engineering in Germany

Tunnelling in Singapore

Investor Presentation February 201951

448 425

0

1000

2017 2016

EBIT (€M) AND EBIT MARGIN (%)

835 855

0

1000

2017 2016

● EBITDA 2016 clean of non-operating non-recurringitem: € 827 million, EBITDA margin 6.7%

● Earnings improvements in several markets, e.g. Germany

● Recognition of a receivable from a concessionproject

● EBIT clean of non-operating non-recurring item: € 397 million, EBIT margin 3.2%

● Extraordinary depreciation allowances significantlyreduced

● All three operative segments contrbuted toearnings improvement

EBITDA (€M) AND EBITDA MARGIN (%)

EBIT HIGHER DESPITE POSITIVE ONE-OFF IN 2016,EBIT MARGIN AT 3.3% – TARGET OF ≥3.0% SOLIDLY ACHIEVED

-2%

+6%

6.2% 6.9%

3.3% 3.4%

1,000

1,000

Investor Presentation February 201952

279 278

0

300

2017 2016

NET INCOME A. MINORITIES (€M) & MARGIN (%)

2.72 2.71

0

3

2017 2016

EARNINGS PER SHARE (€)

EARNINGS PER SHARE STABLE

0%0%

2.1% 2.2%

● Net interest income strongly worsened due to absence of positive foreign currency effects

● Effective tax rate at 30.6% slightly improved (2016: 33.0%)

● Earnings owed to minority shareholders increased from € 4 million to € 13 million, as in 2016 minority shareholders, which still existed at that time, helped to carry winter losses

● Squeeze-out at STRABAG AG, Germany, only completed on 29 December 2017

Investor Presentation February 201953

(€m) 2017 2016 Δ%Output volume 14,620.89 13,491.03 8Revenue 13,508.72 12,400.46 9

Changes in inventories/own work capitalised -48.09 55.55 n.m.

Other operating income 282.99 235.83 20

Construction materials, consumables and services used -8,839.87 -7,980.01 -11

Personnel cost -3,367.17 -3,210.91 -5Other operating expenses -842.79 -795.85 -6Share of profit or loss of associates 123.99 106.18 17Net income from investments 16.80 43.93 -62EBITDA 834.58 855.18 5EBITDA adjusted 827.371

Δ% was calculated with original, not rounded figures therefore, rounding differences might occur.

1 Adjusted for a non-operating profit in the amount of € 27.81 million.

GROUP INCOME STATEMENT 2017

Investor Presentation February 201954

(€m) 2017 2016 Δ%EBITDA 834.58 855.18 5Margin (%) 6.2 6.9Margin adjusted (%) 6.71

Depreciation and amortisation -386.22 -430.27 9EBIT 448.36 424.91 25EBIT adjusted 397.101

Margin (%) 3.3 3.4Margin adjusted (%) 3.21

Net interest income -27.15 -3.78 85Income tax expense -128.85 -139.13 -4Net income 292.36 282.00 55Attributable to minority interest 13.45 4.35 -83Attributable to equity holders of the parent 278.91 277.65 78Earnings per share (€) 2.72 2.71 78Δ% was calculated with original, not rounded figures therefore, rounding differences might occur.

1 Adjusted for a non-operating profit in the amount of € 27.81 million.

GROUP INCOME STATEMENT 2017 (CONT.)

Investor Presentation February 201955

0.45 0.50 0.65 0.95 1.30

41% 40% 43% 35% 48%

0%

100%

0

2

2013 2014 2015 2016 2017

● Dividend per share of € 1.30 proposed (+37%)

● Payout ratio of 48% at higher end of predetermined payout range of 30–50% of net income after minorities

● STRABAG has distributed a dividend within the predetermined payout range every year since the IPO in 2007

(PROPOSED) DIVIDEND (€) AND PAYOUT RATIO (%)

HIGHEST DIVIDEND SINCE IPO PROPOSED: € 1.30 PER SHARE

€

€

Investor Presentation February 201956

(€m) 2017 2016Share capital 110 110Capital reserves 2,315 2,315Retained earnings 945 761Non-controlling interests 27 79Equity 3,398 3,265Provisions 1,161 1,112Financial liabilities 883 1,224Trade payables & other liab. 78 63Deferred taxes 24 21Non-current liabilities 2,145 2,420Provisions 747 810Financial liabilities 411 203Trade payables 3,402 2,818Other current liabilities 950 862Current liabilities 5,511 4,693Equity & Liabilities 11,054 10,378

(€m) 2017 2016Intangible assets 499 496PP&E & investment property 1,942 1,936Associated companies 350 348Other financial assets 183 167Concession receivables 662 683Trade and other receivables 271 254Deferred taxes 189 246Non-current assets 4,096 4,130Inventories 1,138 1,183Trade and other receivables 2,996 3,031Concession receivables 34 31Cash and cash equivalents 2,790 2,003Current assets 6,958 6,248

Total assets 11,054 10,378

ASSETS LIABILITIES AND EQUITY

Rounding differences might occur.

HIGH EQUITY RATIO AND NET CASH POSITION

Investor Presentation February 201957

-74-249

-1,094

-449

-1,335-1500

0

1500

2013 2014 2015 2016 2017

NET DEBT (+)/NET CASH (-) (€M)

30.7% 30.6% 31.0% 31.5% 30.7%

0

0

2013 2014 2015 2016 2017

● Equity ratio remains at 31%; target: ≥25%

● Net cash position at untypically high level

Uncharacteristically high advance payments in the fourth quarter 2017

Normalisation expected over 2018

● S&P confirmed corporate credit rating of BBB (outlook: stable) in July 2017

NET CASH POSITION EXPANDED AND HIGH EQUITY RATIO MAINTAINED

40

EQUITY RATIO (%)1,500

-1,500

Investor Presentation February 201958

(€m) 2017 ∆% 2016

Cash – beginning of period 1,998 -27 2,727

Cash flow from earnings 634 -8 690

∆ Working Capital 711 n.m. -426

Cash flow from operating activities 1,345 409 264

Cash flow from investing activities -333 23 -434

Cash flow from financing activities -235 58 -564

Net change in cash 777 n.m. -734

FX changes 10 100 5

Change restricted cash 5 n.m. 0

Cash – end of period 2,790 40 1,998

Rounding differences might occur.

CASH AND CASH EQUIVALENTS OF € 2.8 BILLION

Investor Presentation February 201959

0

4000

Cash1.1.2017

CFO CFI CFF Currencytranslation

Restrictedcash

Cash31.12.2017

1,998

1,345

-333-235 10

2,790

5

CASH DEVELOPMENT (€M)

● Unusually strong working capital reduction

● Lower investments in property, plant and equipment

COMMENTS

CFO: Cash flow from operating activities CFF: Cash flow from financing activities CFI: Cash flow from investing activities (net CAPEX)

CASH AT € 2.8 BILLION

4,000

Investor Presentation February 201960

-19-209 -139

552

-107-263

-49

1,001

-418 -330-172

494

-64-206 -122

1,103

-1300

0

1300

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42014 2015 2016

WORKING CAPITAL PATTERN: CASH OUTFLOWS IN Q1–3; INFLOWS IN Q4 (€M)

COMMENTS

● Working capital outflows generally occur over the first nine months of the year due to business seasonality

● Unusually high improvement of working capital in Q4/2015 and Q4/2017 due to uncharacteristically high advance payments – reversal in 2018 expected

EXTRAORDINARILY HIGH CASH INFLOW IN Q4/2017

2017

1,300

-1,300

Investor Presentation February 201961

582

-426

711

-800

0

800

2015 2016 2017

Δ WORKING CAPITAL (€M)

1,240

264

1,345

320434

333

0

1500

2015 2016 2017

CFO VS. CFI (€M)

320434

333475 430 386

0

1000

2015 2016 2017

CFI VS. DEPRECIATION (€M)

FCF OF OVER € 1 BILLION IN 2017

1,500 1,000

● Exceptionally high FCF in 2015 and 2017

● Purchase of PP&E at € 458 million (2016: € 412 million), thereof ~ € 250 million maintenance CAPEX

● 2017 depreciation includes goodwill impairment of € 2 million (2016: € 5 million)

● Extraordinary depreciation allowances significantly reduced in 2017

Investor Presentation February 201962

47% of group output

volume

KEY INDICATORS

● Output volume 11% higher

● EBIT rose due to stronger project earnings

● Order backlog (+16%) driven again to new recordlevel by Germany and Poland

● Outlook:

Order backlog hints at higher output volume in 2018

Germany: Positive outlook for buildingconstruction and civil engineering as well as fortransportation infrastructure

Capacities increasingly scarce

Poland: especially positive in rail construction, higher activity in building construction and civilengineering

Scandinavia: Lasting upward trend

COMMENTS

SHARE OF GROUP OUTPUT VOLUME

NORTH + WEST BENEFITS FROM GERMANY

(€m) 2017 Δ% 2016

Output volume 6,843 11 6,175

Revenue 6,378 10 5,802

Order backlog 8,138 16 7,030

EBIT 199 17 170

EBIT margin % 3.1 2.9

Employees 23,366 5 22,233

Investor Presentation February 201963

29% of group output volume

(€m) 2017 Δ% 2016

Output volume 4,242 6 4,001

Revenue 4,073 5 3,889

Order backlog 4,505 29 3,483

EBIT 205 9 188

EBIT margin % 5.0 4.8

Employees 17,916 1 17,758

KEY INDICATORS

● Output volume increased by 6%, driven by Austria, Hungary and Slovakia

● EBIT 5% higher due to improvements in severalcountries

● Order backlog soared (+29%)

● Outlook:

Increase in output volume expected for 2018

Furher dynamic building construction in thegreater Vienna region and fierce competition in Austrian transportation infrastructure business

Subcontractor prices rising above all in Slovakia, Czech Republic and Hungary

COMMENTS

SHARE OF GROUP OUTPUT VOLUME

SOUTH + EAST: STRONG AT A HIGH LEVEL

Investor Presentation February 201964

23% of group output volume

● Output volume down especially due to Italy

● EBIT hardly changed in absolute terms – number of contrary effects related to large projects

● Order backlog coined by tunnelling project for Chilean copper mine

● Outlook:

Output volume 2017 should increase slightly

Property and facility services business as well as real estate development contribute positively to earnings

Very competitive market for tunnelling and concession projects

KEY INDICATORS

● Output volume rose by 8% due to large projects in Austria, Germany and Americas

● EBIT +28%: recognition of a receivable from a concession project, settlement agreement in Middle East, burden again stemming from projectAlto Maipo, Chile

● Order backlog down by 8%: reduction of Italianproject Pedemontana

● Outlook:

Output volume 2018 should increase slightly

Real estate development continues to contributepositively to earnings

Property and facility services business: Agreement with future service provider ofDeutsche Telekom regarding transition ofemployees concluded

COMMENTS

SHARE OF GROUP OUTPUT VOLUME

INTERNATIONAL + SPECIAL DIVISIONS: EARNINGS PLUS AFTER NUMBER OF CONTRARY EFFECTS

(€m) 2017 Δ% 2016

Output volume 3,404 8 3,155

Revenue 3,029 13 2,681

Order backlog 3,944 -8 4,295

EBIT 62 28 49

EBIT margin % 2.1 1.8

Employees 25,618 -2 26,027

Investor Presentation February 201965

APPENDIX5

1 CAGR over period 2013–2017

OUTPUT VOLUME BY COUNTRY

(€m) 2013 2014 2015 2016 2017 CAGR1 (%)Germany 5,789 6,080 6,256 6,270 6,960 5Austria 1,982 2,058 2,003 2,099 2,333 4Poland 787 817 941 774 848 2Czech Republic 645 620 765 631 629 -1Hungary 496 544 594 448 551 3Slovakia 340 427 716 461 528 12Americas 263 255 310 348 385 10Switzerland 386 359 343 378 320 -5Middle east 323 272 314 267 303 -2Benelux 400 324 302 309 294 -7Other European Countries 81 169 167 150 277 36Romania 322 181 241 254 183 -13Sweden 315 271 240 179 162 -15Denmark 152 197 219 234 159 1Russia 561 302 230 139 143 -29Croatia 133 121 68 78 120 -3Serbia 31 38 46 89 113 38Asia 103 87 92 131 99 -1Italy 168 179 188 82 67 -21Slovenia 67 68 98 65 53 -6Africa 165 158 120 78 48 -27Bulgaria 20 39 35 27 45 23Total 13,530 13,566 14,290 13,491 14,621 2

Investor Presentation February 201967

2016 (€M) CONSTRUCTION OUTPUT STRABAG OUTPUT MARKET SHARE (%)

Germany 310,809 6,270 2.0

Austria 34,948 2,097 6.0

Poland 44,936 774 1.7

Czech Republic 16,450 631 3.8

Hungary 7,480 448 6.0

Russia 113,567 139 0.1

Slovakia 4,615 461 10.0

Romania 46,970 254 0.5

Croatia 2,977 78 2.6

Slovenia 2,257 65 2.9

Serbia 2,145 89 4.1

Bulgaria 6,077 27 0.4

Switzerland 63,351 378 0.6

Benelux 114,993 309 0.3

Sweden 40,698 179 0.4

Italy 164,411 82 <0.1

Denmark 30,113 234 0.8

Sources: Euroconstruct Summer 2017, EECFA Country Reports Summer 2017, company data

STRABAG MARKET SHARE DATA

Investor Presentation February 201968

Sources: Companies’ Annual Reports; Deutsche Bauindustrie; Časopis Stavitel; OPTEN; Deloitte; 1 Habau and Rhomberg Gruppe listed with total revenue.

MARKET LEADING POSITIONS IN CENTRAL AND EASTERN EUROPEAN COUNTRIES

AUSTRIA

Output volume/Revenue 2016 (€m)

1. STRABAG 2,099

2. Porr 2,055

3. Swietelsky 1,278

4. Habau 1,1941

5. Rhomberg Gruppe 6901

GERMANY

Output volume/Revenue 2016 (€m)

1. STRABAG 6,270

2. Vinci 2,689

3. Goldbeck 1,664

4. Zech Group 1,335

5. Max Bögl 1,238

CZECH REPUBLIC

Output volume/Revenue 2016 (€m)

1. Metrostav 689

2. STRABAG 583

3. Skanska 407

4. Eurovia 354

5. Swietelsky 225

POLAND

Output volume/Revenue 2016 (€m)

1. Budimex 1,260

2. Skanska 857

3. STRABAG 774

4. Polimex-Mostostal 603

5. PBG 449

WESTERN EUROPE

EASTERN EUROPEHUNGARY

Output volume/Revenue 2016 (€m)

1. STRABAG 375

2. Market 295

3. KÉSZ 240

4. Swietelsky 200

5. Duna aszfalt 180

Investor Presentation February 201969

Sources: Companies’ Annual Reports; Trend Top v Stavebnictve 05/2017; ajpes.si; bonitete.si, www.fininfo.hr, Ministry of finance Romania

MARKET LEADING POSITION IN CENTRAL AND EASTERN EUROPEAN COUNTRIES (CONT.)

SLOVAKIA

Output volume/Revenue 2016 (€m)

1. STRABAG 470

2. Eurovia 112

3. Goldbeck 103

4. Vahostav 102

5. SAG 94

CROATIA

Output volume/Revenue 2016 (€m)

1. Kamgrad 107

2. STRABAG 78

3. Tehnika 76

4. GP Krk 70

5. ZM 60

SLOVENIA

Output volume/Revenue 2016 (€m)

1. Kolektor Koling + CPG 136

2. Pomgrad 95

3. CGP 92

4. STRABAG 59

5. Gorenjska 53

ROMANIA

Output volume/Revenue 2016 (€m)

1. STRABAG 254

2. Bog'Art 109

3. Porr 92

4. Hidroconstructia 88

5. Construcii Erbasu 83

Investor Presentation February 201970

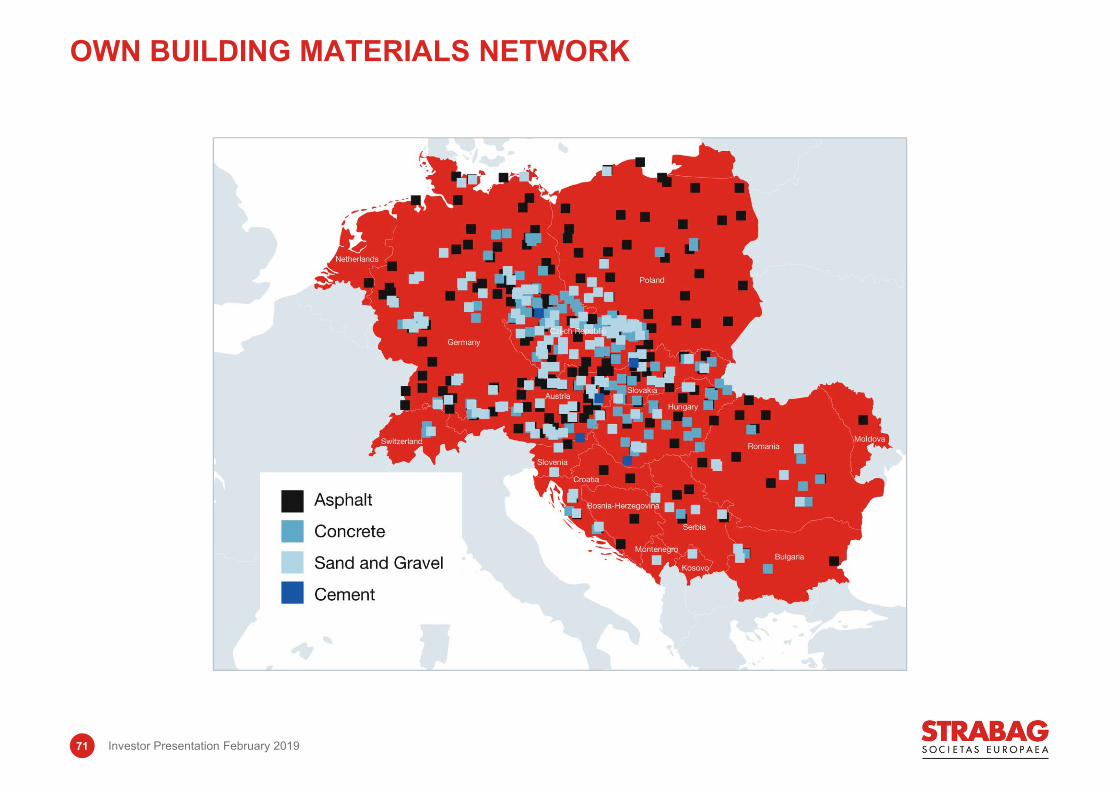

OWN BUILDING MATERIALS NETWORK

Investor Presentation February 201971

● The SPV1 is financed with equity (10%–30%) and bank debt (70%–90%)

● STRABAG – as a shareholder in the SPV –puts in equity

● Other SPV shareholders are e.g. governments, infrastructure funds and developers or other construction companies.

● The grantor pays a fee to the SPV which is used for construction, maintenance, repaying debt and paying dividends to equity partners.

● Availability and hard toll projects, forfeiting models ● Maintenance part of availability fee linked to

inflation● WACCs differ according to risk: 6%–13%● ROE targets: minimum 12%● Share of equity currently invested and committed:

€ 427 million (as at end of 2017)

TYPICAL FINANCING

410 378 370 400 427

0

700

2013 2014 2015 2016 2017

EQUITY INVESTED IN PPP (€M)

1 Special Purpose Vehicle

FINANCING PPP-PROJECTS

Investor Presentation February 201972

ILLUSTRATIVE PPP PROJECT STRUCTURE

SPC / Project Consortium / Company

Grantor

Construction Joint Venture(EPC – Contract)

Operations & Maintenance Company

STRABAG

[Public Entity]

Lenders

Insurance Providers

Project/Concession Contract

Funding Agreements

InsuranceContracts

Turnkey Design andConstruction

ContractOperations & Maintenance

Contract

ShareholdersAgreement

STRABAG

CJV Partner(s)

Partner(s)

IndependentEngineer

IndependentEngineer

Agreement

DEBT

EQU

ITY

A-Way

OJV Partner(s)

Investor Presentation February 201973

2008 Acquisition of Deutsche Telekom Immobilien und Services GmbH | Germany

2010 ● Acquisition of RIMEX Group | Germany● Acquisition of ECM Facility a.s. | Czech Republic

2012

2014

Acquisition of BWG (GSW Betreuungsgesellschaft f. Wohnungs- und Gewerbebau mbH) | GermanyAcquisition of DIW Instandhaltung | Germany

● Offsets seasonal and cyclicality factors (contracts of 3-5 years duration)

● One integrated provider for planning, construction and operation of properties

● Long-term relationship with customers, that does not end after the construction project has finished

● Growth opportunities through international market access and rising importance of lean real estate operations

EXTENDING THE VALUE CHAIN

● Real Estate Management Property Management Leasing and letting/area management

● Technical Facility Management

● Infrastructural Facility Management including technical cleaning and industrial services

● Extend business with new and existing customers

● Stable output volume of approx. € 1 billion (Deutsche Telekom accounts for approx. 60% of German revenues)

● Enter new market segments

● Set up real estate services 4.0: establish semi-automated order management by 2018, development of scalable products regarding BIM within existing buildings, sensor use cases and use of artificial intelligence.

TARGETS FOR 2018

BUSINESS SEGMENTS MILESTONES

PROPERTY & FACILITY SERVICES: STRATEGIC RATIONALE & TARGETS

Investor Presentation February 201974

Haselsteiner Family26.4%

UNIQA/Raiffeisen27.5%Rasperia Trading

25.9%

Free float13.5%

Treasury shares6.7%

SHAREHOLDER STRUCTURE SINCE 7/2016

● Core shareholders account for the majority >80% stake

● Shareholders’ syndicate extended in June 2017 by five years to end of 2022

● Flexibility: Strategic decisions can be taken and implemented very fast.

● Reduction of share capital in 2016: Withdrawal of 4 million own shares; share capital as at 22 July 2016: € 110,000,000

COMMENTS

STABLE SHAREHOLDER STRUCTURE

Investor Presentation February 201975

1 BMTI: equipment and vehicle management2 TPA: quality management, health/safety/environment and energy management, technical consultation, quality assurance, innovation management3 CML: prequalification, contract management and legal services

ORGANISATION – CENTRAL UNITS

ORGANISATIONAL STRUCTURE

Operative Segments

North + West

1 Board Member

4 DivisionsDivision Managers

37 SubdivisionsSubdivision Managers

South + East

1 Board Member

6 DivisionsDivision Managers

35 SubdivisionsSubdivision Managers

CEO

1 DivisionDivision Managers

3 SubdivisionsSubdivision Managers

International + Special Divisions

1 Board Member

8 DivisionsDivision Managers

25 SubdivisionsSubdivision Managers

BRVZAccounting, Financing, Taxes, IT, Human

Resources, Real Estate, Insurance, Project-Related Risk Management System (PRMS)/

Organisational Development, International BRVZ Coordination, Management Support

BMTI1 TPA2 CML3

Internal Auditing Corporate Communications

Zentrale Technik

Business Compliance

Central Divisions & Central Staff Divisions

CEO

CFO

As of 1 February 2018

Investor Presentation February 201976

Thomas Birtel, CEO (centre) ● Joined STRABAG in 1996● Management Board member since 2006● Born 1954 Education: Economics

Christian Harder, CFO (left) ● Joined STRABAG in 1994● Management Board member since 2013● Born 1968 Education: Business Administration

Alfred Watzl, Head of North + West Divisions segment (second right) ● Joined STRABAG in 1999● Management Board member since 2019● Born 1970 Education: Civil Engineering

Peter Krammer, Head of South + West segment (second left) ● Joined STRABAG in 1998● Management Board member since 2010● Born 1966 Education: Civil Engineering

Siegfried Wanker, Head of International + Special Devisions segment (right) ● Joined STRABAG in 1994● Management Board member since 2011● Born 1968 Education: Civil Engineering

LONG RECORD OF EXPERIENCE WITHIN STRABAG AND IN THE CONSTRUCTION SECTOR

THE MANAGEMENT BOARD

Over

100years combined experience at STRABAG

Investor Presentation February 201977

Company Date Title Target Price Rating

Commerzbank 12.2.2019Q4 output above but outlook sounds cautious € 42.0 Buy

Erste Group 15.2.2019Starke vorläufige Zahlen 2018 sowie ermutigender Ausblick 2019 € 42.9 Buy

RCB 13.2.2019Minor model update after confident FY 19 outlook € 38.5 Buy

Kepler Cheuvreux 23.1.2019 Reassuring presentation € 34.0 Hold

HSBC 14.1.2019 More light than shower € 35.0 Buy

LBBW 3.12.20182018 sollte für Strabag zu einem weiteren Rekordjahr werden € 38.0 Buy

Kepler Cheuvreux 30.11.2018 Solid 9M results € 34.0 Hold

Deutsche Bank 30.5.2018Solid start, FY output guidanceconservative € 40.0 Buy

MainFirst Bank 7.7.2017Transforming STRABAG – but to what extent? € 38.0 Neutral

STRABAG SHARE IS COVERED BY EIGHT INSTITUTIONS

Investor Presentation February 201978

0%

15%

2017 2018F 2019F

Construction total ResidentialNon-residential Public/CivilGDP growth

GROWTH IN CONSTRUCTION SEGMENTS● STRABAG is the German market leader with 2.0%

market share, 9.1% in road construction● Persistently good economic activity due to strong

increase in private consumption and public investment

● Germany should be able to keep the high level in public/civil it will have reached in 2018/19

● „Bundesverkehrswegeplan“: € 270 billion public investment into transportation infrastructure by 2030, thereof approx. 50% into A-roads

● Special need to catch up investment in bridges● A weakening is also not to be expected in building

construction by 2019● Strong need for living space, political goal:

400,000 residential units per year by 2020● Energy efficiency is one of the central goals of the

German government („Klimaschutzplan 2050“)

COMMENTS

Sources: Hauptverband der deutschen Bauindustrie May 2018; Euroconstruct June 2017

GERMANY: STRONG GROWTH IN HOME MARKET

Investor Presentation February 201979

0 90

DenmarkNetherlands

BelgiumIreland

SwedenSlovenia

AustriaBulgariaCroatia

SlovakiaCzech Republic

HungaryGermanyRomania

ItalyPoland

BUDGET EUROPEAN FUNDS1 2014–2020 (€BN)

● STRABAG – little to no direct exposure to UK

● But Brexit has a big indirect influence: UK payments to EU = payments of 20 smallest countries

● Given the reduced EU budgets as of 2021, funds for infrastructure projects could be retrieved to a greater extent in the nearer future

1 Source: European Commission; European structural and investment funds; only countries with STRABAG presence shown

BREXIT – IMPLICATIONS ON STRABAG

Investor Presentation February 201980

● Annual Report 2018 29 April 2019● Interim Report January–March 2019 29 May 2019● Annual General Meeting 2019 28 June 2019● Semi-Annual Report 2019 30 August 2019● Interim Report January–September 2019 28 November 2019

Diana Neumüller-Klein, CFAHead of Investor Relations & Corporate Communications+43 1 [email protected]

www.strabag.com

FINANCIAL CALENDAR AND IR CONTACT

Investor Presentation February 201981