storage media overview projec2ng future trends from … tal… · storage media overview projec2ng...

TRANSCRIPT

R.Fontana,G.Decad–IBMSystemsSeptember19,2016

StorageMediaOverviewProjec2ngFutureTrends

from2008-2015HistoricPerspec2ves

©2016IBMCorporaAon

Outline

• ADefiniAon:StorageMediaisPBshipmentsforLTOTAPE,HDD,andNAND

• AComment:FuturePredicAonsareDifficultwhilePastPerformanceisVerifable

• Topics• StorageLandscapefor2008-2015

• Moore’sLaw–Underachievingimpliescomponentsaremorevaluable

• ExabytesandMillionsofSquareInchesandArealDensity

• LandscapeComparisons:2008-2015,2012-2015,2015

• MSIExamplesandSpecificTrends

• SummaryandtheFuture

©2016IBMCorpora2onPage2Fontana,Decad–LOC2016–StorageMedia

Storage Landscape for HDD, TAPE, NAND: 2008-2015

• ThestoragecomponentlandscapehasbeenmonitoredbytrackingannualrevenueandtechnologytrendsinLTOTAPEMEDIA,HDD,andNAND• Arealdensity,Revenue• $/GBandExabyteshipments

• 2015observaAons• NAND:SignificantEBgrowthbutminimalrevenuegrowth• HDD:MinimalEBgrowthwithrevenuedecrease• LTOTAPEMEDIA:EBgrowthwithlowerrevenue• $/GBforalltechnologiesreducedbybetween16%and22%• ArealDensityslowingforHDD

• Overview

©2016IBMCorpora2onPage3Fontana,Decad–LOC2016–StorageMedia

2015%CHANGE EXABYTES REVENUE $/GB AREALDENSITY

LTOTAPEMEDIA 9.6% -10.0% -18.4% 100%*

HDD 2.9% -15.3% -16.4% 11%

NANDFLASH 32.8% 3.1% -22.1% 25%

TOTAL 6.1% -6.3% NA NA*LT07introducedlate2015effec2velydoublingdensitybut2yearproductcycle

The Bit Cell Landscape

• BitCellObservaAons–“Thereisnotmuchroomattheboeom”forHDDandNAND

• NANDStrategy–MulAlayeror3Dcells(largercellareawithmulAplelayersofcells)

• HDDStrategy–SmallercellareausingthermalwriAngof“harder”magneAcmedia

• TAPEStrategy–Moore’sLawScaling–“ThereissAllroomattheboeom”

NAND-MLC1100Gbit/in²24nmx24nm

NAND-TLC1500Gbit/in²19nmx19nm

HDD1000Gbit/in²58nmx11nm

TAPE7Gbit/in²2000nmx47nm

©2016IBMCorpora2onPage4Fontana,Decad–LOC2016–StorageMedia

NAND–TLC3D1500Gbit/in²84nmx84nm20layers

Blu-RayBD-XL75Gbit/in²180nmx180nm3layers

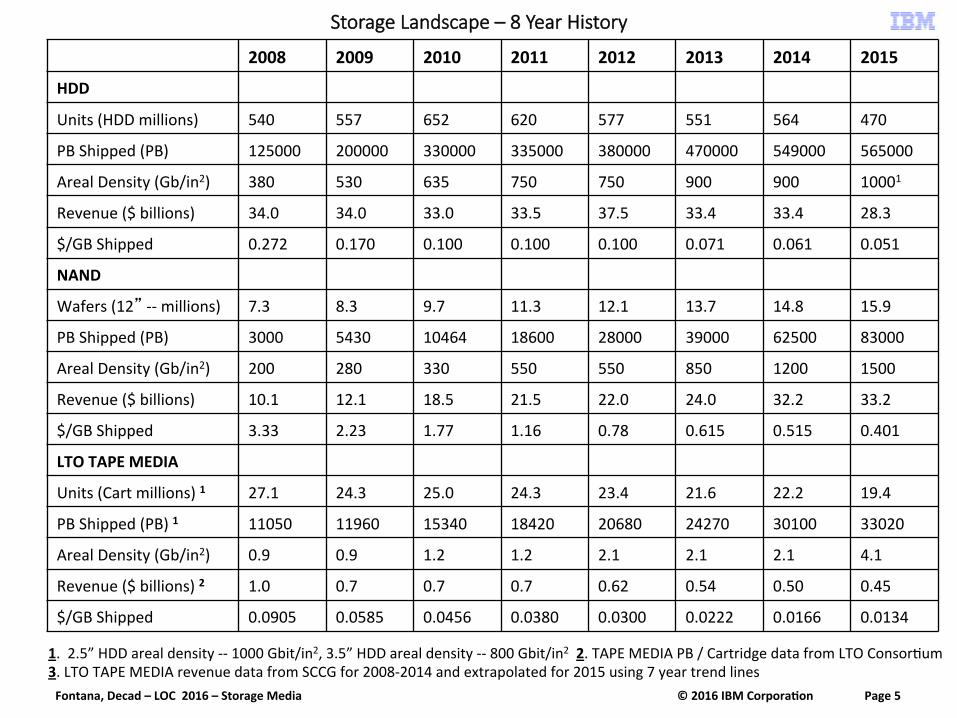

Storage Landscape – 8 Year History

1.2.5”HDDarealdensity--1000Gbit/in2,3.5”HDDarealdensity--800Gbit/in22.TAPEMEDIAPB/CartridgedatafromLTOConsorAum3.LTOTAPEMEDIArevenuedatafromSCCGfor2008-2014andextrapolatedfor2015using7yeartrendlines

2008 2009 2010 2011 2012 2013 2014 2015

HDD

Units(HDDmillions) 540 557 652 620 577 551 564 470

PBShipped(PB) 125000 200000 330000 335000 380000 470000 549000 565000

ArealDensity(Gb/in2) 380 530 635 750 750 900 900 10001

Revenue($billions) 34.0 34.0 33.0 33.5 37.5 33.4 33.4 28.3

$/GBShipped 0.272 0.170 0.100 0.100 0.100 0.071 0.061 0.051

NAND

Wafers(12”--millions) 7.3 8.3 9.7 11.3 12.1 13.7 14.8 15.9

PBShipped(PB) 3000 5430 10464 18600 28000 39000 62500 83000

ArealDensity(Gb/in2) 200 280 330 550 550 850 1200 1500

Revenue($billions) 10.1 12.1 18.5 21.5 22.0 24.0 32.2 33.2

$/GBShipped 3.33 2.23 1.77 1.16 0.78 0.615 0.515 0.401

LTOTAPEMEDIA

Units(Cartmillions)1 27.1 24.3 25.0 24.3 23.4 21.6 22.2 19.4

PBShipped(PB)1 11050 11960 15340 18420 20680 24270 30100 33020

ArealDensity(Gb/in2) 0.9 0.9 1.2 1.2 2.1 2.1 2.1 4.1

Revenue($billions)2 1.0 0.7 0.7 0.7 0.62 0.54 0.50 0.45

$/GBShipped 0.0905 0.0585 0.0456 0.0380 0.0300 0.0222 0.0166 0.0134

©2016IBMCorpora2onPage5Fontana,Decad–LOC2016–StorageMedia

Storage Media Environment -- EB

• 2015vs2012–NANDPBMarketShareIncrease,HDDPBMarketShareDecrease

HDD;380000 PB;89%

NAND,28000 PB,6%

LTOTAPE,21000 PB,5%

HDD NAND LTOTAPE

HDD;565000 PB;83%

NAND,83000 PB,12%

LTOTAPE,33000 PB,5%

HDD NAND LTOTAPE

2015PBShipments–681,000PB 2012PBShipments–429,000PB

©2016IBMCorpora2onPage6Fontana,Decad–LOC2016–StorageMedia

Storage Media – Exabytes, Areal Density, MSI DefiniQons

• Exabyte(EB)ShipmentsofStorageMediareliesonamanufacturingbase• NAND–300mmdiameterwaferstarts• HDD–Individualdriveshipmentswithheadsanddisksurfaces• LTOTAPE–Cartridgeshipmentswithmetersof½”tapewidth

• IncreasesinExabyteShipmentsofStorageMediacomesfromeitherincreasingthefactorycapacityofthemanufacturingbaseorbyincreasingtheefficiencyofstoringmorebitsperunitsurfaceareaofmanufacturedmedia• FactoryCapacityisMillionsofSquareInchesofmanufacturedmedia–MSI• BitsperUnitAreaisArealDensity–ADorGBpersquareinch

• EB=MSIxADandRevenue=EBx$/GBorRevenue=MSIxADx$/GB

• IncreaseinEBshipmentscomeswithcost:FactoriesforandMSIincreaseorR&DexpendituresforanADimprovement.

• Issue:ArealDensityandconsequently$/GBmetricshaveunderperformedinthelastthreeyears

©2016IBMCorpora2onPage7Fontana,Decad–LOC2016–StorageMedia

Storage Media – Moore’s Law RealiQes

• Moore’sLawPercepAon• $/GBdecreases30%peryearor50%everytwoyears• ADincreases40%peryearor100%everytwoyears• NET==Every2yearsthecomponentmanufacturerssell2Xmorestoragemediafor

0.5XlesscostperbitforarevenueneutralposiAon.Revenueincreasesonlyifmanufacturinginvestment(MSI)increasesorif│$/GB│reducAonsdecreases

• Moore’sLawReality• $/GBdecreased~20%/yrforthethreeyearperiod2013–2015• ArealDensity~40%/yrforNAND,26%/yrforLTOTAPE,10%/yrforHDDforthe

threeyearperiod2013-2105

• ConsequencesofMoore’sLaw($/GB)Underachieving(HDD–20%/yrvs30%/yr)• Storageismorevaluable;lesseasilyreplaced–62%increaseinreplacementcost

©2016IBMCorpora2onPage8Fontana,Decad–LOC2016–StorageMedia

4TBDrive 10PBSystem

2016Cost $160 $400K

2020Cost(20%/yr$/GBDecrease) $65 $162K

2020Cost(30%/yr$/GBDecrease) $40(Moore’sLaw) $100K(Moore’sLaw)

Storage Media Comparisons: 2008 – 2015, 2012 – 2015, and 2015

• Moore’sLawnotachieved:i.e.Densityincreasingat40%/YRand$/GBreducingat30%/YR

• Storageismorevaluable,lessreplaceable,andmustbereliableforlongerAmeperiods

©2016IBMCorpora2onPage9Fontana,Decad–LOC2016–StorageMedia

AnnualChange–last8years

AnnualChange--last3years

AnnualChange–lastyear

NAND$/GB -26% -20% -22%

HDD$/GB -21% -20% -16%

TAPE$/GB -24% -23% -19%

NANDEBShips +61% +43% +33%

HDDEBShips +24% +14% +3%

TAPEEBShips +17% +17% +10%

NANDRevenue +19% +15% +3%

HDDRevenue -3% -9% -15%

TAPERevenue -8% -9% -10%

NANDAD +33% +39% +25%

HDDAD +15% +10% +11%

TAPEAD +25% +26% +100%

Issue--RevenueDecrease

│$/GB│decrease≥

│EB│increase

Moore’sLaw–+40%/YR

Moore’sLaw–-30%/YR

Two Contrarian Trends from 2015 Data

• TotalannualmanufacturedExabytesshowsalineartrend(i.e.notexponenAal)withanannualincreaseoverthelast8yearsof77EB/YR(r2=0.98)

• TotalrevenueformanufacturedExabytesisstable,i.e.nogrowth,withdeclineinHDDrevenueabsorbedbyincreaseinNANDrevenue 0

10

20

30

40

50

60

70

2008 2009 2010 2011 2012 2013 2014 2015

Revenu

e($B)

Year

ComponentRevenue

HDD NAND LTOTAPEMEDIA

0100200300

400500600700800

2008 2009 2010 2011 2012 2013 2014 2015

Exabytes(EB)

Year

ManufacturedExabytes

HDD NAND TAPE

©2016IBMCorpora2onPage10Fontana,Decad–LOC2016–StorageMedia

Areal Density Roadmaps Not Being Updated

• TechnologyconsorAumsarelessrelevanttoindustrialdu-opoliesortri-opolies

• Arealdensityincreasesaremoredifficult,40%annualgrowthnolongerachievable

• Arealdensityroadmapsbeingarereplacedbycapacityroadmaps,i.e.whatclientsbuy

§ HDD: source ASTC 2013

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Normalized

Value

s(20

14re

ference)

Year

3DNANDROADMAP(ITRS)

NormalizedCapacity NormalizedLayerNumber NormalizedBits/Cell

128Gb

256Gb

512Gb

1024Gb

2Bits/Cell 4Bits/Cell3Bits/Cell24Layers

96Layers

48Layers

1.0

10.0

100.0

2010 2012 2014 2016 2018 2020 2022 2024

ArealDesnity(G

b/in

2 )

Year

TapeRoadmap-- ArealDensity

§ NAND: source ITRS 2013

§ TAPE: source NSIC 2013

2015NSICRoadmap

PresentEnterpriseProducts

©2016IBMCorpora2onPage11Fontana,Decad–LOC2016–StorageMedia

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

12"DiameterFlashNANDWaferStarts(millions)

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

LTOCartridgeUnits(millions)

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

HDDUnits(millions)

Revisi2ngMSI(millionsofsquareinches)forStorageComponents

• OnemeasureofstoragegrowthisMSIormillionsofsquareinchesofannuallymanufacturedstoragemedia.

• AnyincreaseinMSIcapabilityrequirescapitalinvestment

• AnincreaseinEBorPBmemoryshipmentsisaproductofincreasedMSIandADorarealdensity(i.e.thenumberofbitsthatamemorytechnologysupportsperunitarea)

• In2015LTOMedia,HDD,andNANDallincreasedEBmemoryshipmentsbutonlyNANDincreasedMSI• NANDMSI(waferstarts): +7%• HDDMSI(drivesshipped): -17%• LTOMSI(cartridgeshipped):-12%

• NANDinvestmentinMSIreflectsonNANDincreases(35%)inExabyteshipmentsofmemory

©2016IBMCorpora2onPage12Fontana,Decad–LOC2016–StorageMedia

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

12"DiameterFlashNANDWaferStarts(millions)

2015NANDMSIObserva2ons

• Landscape:16,000,000wafers,83,000PB,$33BRevenue• $0.401/GBor$2075/wafer• 5.187TB/wafer• 11.7GB/chip(44012mmx12mmchipsperwafer)• Stateofartchipis~3Xgreateror32GB(375chips13mmx13mmperwafer)or12.0TB/wafer

• Factories• $8Bstateofartfacilitycanproduce4000wafers/dayor1.4Mwafers/yrorupto16,000PB/yr• NANDwafercapacityincreasedatalinearrateof~1,000,000peryearimplyingannualnewfactory

investmentof~$6B/year• Withoutanyincreaseinarealdensity,adoublingofPBoutputforNANDwouldrequire6new

factoriesanda$48Binvestment.

• AnMSIExample• Usingbestofbreedchip(12TB/wafer)wouldrequire47Mwaferstoreplace565EBofHDDstorage• 47Mwafersrequires32$9Bfactoriesor$288BinCapital!!èarealdensityisabeeerstrategy!!!

©2016IBMCorpora2onPage13Fontana,Decad–LOC2016–StorageMedia

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

HDDUnits(millions)

2015HDDMSIObserva2ons

• 2015Landscape:• 470,000,000drives• 565,000PB• $28.3BRevenue• $0.051/GB• $60.2/drive• 1.2TB/HDD

• 3%morePB,and17%lower$/GBimplies~15%lessrevenue

• The20%increaseinTB/HDDnotresulAngsolelyfromarealdensityincreases• Arealdensityincreaseonly10%• Productmixshiyfrom2.5”HDDto3.5”HDD(moresurfaceareaandmoreMSI)• Moreplaeers/HDD(moresurfaceareaandmoreMSI)

• MSI(i.e.numberofplaeersandnumberofheads)mayhavedecreasedin2015

• 2014Landscape:• 564,000,000drives,• 549,000PB,• $33.4BRevenue• $0.061/GB• $59.2/drive• 1.0TB/HDD

©2016IBMCorpora2onPage14Fontana,Decad–LOC2016–StorageMedia

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

LTOCartridgeUnits(millions)

2015 LTO TAPE Media MSI ObservaQons

• Landscape:19,400,000cartridges,33,000PB,$0.45BMediaRevenue• $0.0134/GB• $23.20/cartridge• 1.7TB/cartridge(reflecAveofLTOproductmix)• Note:LTO5capacity1.5TB,LTO6capacity2.5TB,LTO7capacity6.0TB(4Q15introducAon)

• AnMSIExample• MediaCapacityis19.4Mcartridges• Maximumcartridgecapacityis6TB• LTOPBshipmentscouldincreasefrom33,000to116,000PBshipmentswithnonewcapitalinvestment

©2016IBMCorpora2onPage15Fontana,Decad–LOC2016–StorageMedia

0.01

0.1

1

10

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

$/GB

YEAR

HDD NAND LTOTAPEMEDIA

$/GB Trends: 2008-2015

$/GB201320141YEAR%Δ7YEARANNUAL%ΔLTOTAPEMEDIA0.0240.0196-18.3%-22.9%HDD0.0710.061-14.1%-22.1%NAND0.6150.49-20.3%-27.3%

• ObservaAons• $/GBreducAonisleastforHDD• RelaAveto8yearannualaverages,

2015$/GBreducAonsareless• $/GBdataforBlu-raydatadisc,

i.e.BD-RE,arenotavailableforlargequanAAessoopAcalcomponentcomparisonsarenotpossible.Note“upsidedown”$/GBpricingfordiskcapaciAes(quanAAesof~20)withnodecreasefor25GBBDbutdropin100GBBD.

100GBBD

50GBBD

25GBBD

$/GB 2014 20151YEAR%Δ

8YEARANNUAL

%Δ

LTOTAPEMEDIA 0.0166 0.0134 -19.3% -23.9%HDD 0.061 0.051 -16.4% -21.3%NAND 0.515 0.401 -22.1% -26.1%

©2016IBMCorpora2onPage16Fontana,Decad–LOC2016–StorageMedia

0.1

1

10

100

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Revenu

e($B)

Year

HDD NAND LTOTAPEMEDIA

Revenue Trends: 2008-2015

$/GB201320141YEAR%Δ7YEARANNUAL%ΔLTOTAPEMEDIA0.0240.0196-18.3%-22.9%HDD0.0710.061-14.1%-22.1%NAND0.6150.49-20.3%-27.3%

• ObservaAons• NANDrevenueexceedsHDDforfirstAme• SignificantHDDrevenuedecreaseleadsto

overalldropintotalcomponentrevenueforallstoragetechnologies

• SignificantNANDrevenuegrowthabovehistoricalaverages

• LTOTAPEcartridgerevenueconAnuesdeclineinthe8%to10%annualraterange

DVDRevenue

Revenue($B) 2014 20151YEAR%Δ

8YEARANNUAL

%Δ

LTOTAPEMEDIA 0.5 0.45 -10.0% -8.4%HDD 33.4 28.3 -15.3% -2.6%NAND 32.2 33.2 3.1% 18.5%

TOTALREVENUE 66.1 61.95 -6.3% 4.7%

©2016IBMCorpora2onPage17Fontana,Decad–LOC2016–StorageMedia

0.1

1

10

100

1000

10000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

AREA

LDEN

SITY(G

b/in

2 )

YEAR

HDD NAND LTOTAPEMEDIA

Maximum Areal Density Trends: 2008-2015

$/GB201320141YEAR%Δ7YEARANNUAL%ΔLTOTAPEMEDIA0.0240.0196-18.3%-22.9%HDD0.0710.061-14.1%-22.1%NAND0.6150.49-20.3%-27.3%

(1)(2)(3)

(1) LTO7introducedYE2015(2) HDDdensityincreaserepresentsshinglemagneAcrecording–

800Gb/in2for3.5”HDDand1000Gb/in2for2.5”HDD(3) NANDdensityincreaserepresentsTLC(3bit/cell)at16nm,5F2cell

• Comments• LTOarealdensitytrackingis

straigh{orward• HDDarealdensiAesarethemaximum

reportedin2.5”HDDs.Note,thatmaximumarealdensityreportedin3.5”HDDsininthe800Gbit/in2range.

• NANDarealdensitydifficulttodeterminesincetheclassic4F2celldesignisnotrigorouslyused.

BD-RE

AREALDENSITY(Gb/in²)

2014 20151YEAR%Δ

7YEARANNUAL

%Δ

LTOTAPEMEDIA 2.1 4.3 104.8% 25.0%HDD 900 1000 11.1% 14.8%NAND 1200 1500 25.0% 33.4%

©2016IBMCorpora2onPage18Fontana,Decad–LOC2016–StorageMedia

1

10

100

1000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

EBShipp

ed

YearHDD NAND LTOTAPEMEDIA

Exabyte Shipment Trends: 2008-2015

$/GB201320141YEAR%Δ7YEARANNUAL%ΔLTOTAPEMEDIA0.0240.0196-18.3%-22.9%HDD0.0710.061-14.1%-22.1%NAND0.6150.49-20.3%-27.3%

DVDEB

• ObservaAons• HDDEBshipmentincreasesignificantly

lessthanhistoricalaverage• LTOMediaEBshipmentincreaseisless

thanhistoricalaverage• SignificantNANDEBshipmentincrease

relaAvetoLTOTAPEandHDD.• NANDEBshipmentsexceedLTOEB

shipments(consumermarket,i.e.IPhone6)by>2X

• TotalEBshippedgrewonlyby6%!!!

EBSHIPPED 2014 20151YEAR%Δ

8YEARANNUAL

%Δ

LTOTAPEMEDIA 30.1 33.0 9.6% 16.9%HDD 549.0 565.0 2.9% 24.0%NAND 62.5 83.0 32.8% 60.7%TOTALEBSHIPPED 641.6 681.0 6.1% 25.6%

©2016IBMCorpora2onPage19Fontana,Decad–LOC2016–StorageMedia

Data CreaQon and Storage Manufacturing

$/GB201320141YEAR%Δ7YEARANNUAL%ΔLTOTAPEMEDIA0.0240.0196-18.3%-22.9%HDD0.0710.061-14.1%-22.1%NAND0.6150.49-20.3%-27.3%

• ObservaAons• Totalmanufacturedstoragein2015was

681EB,anincreaseof6%over2014manufacturedstorageEB

• Contrastthesevalueswith2013IDCclaimsthatcreatedusefuldatain2015wouldbe2180EB,anincreaseof40%over2014createdusefuldata,andthatusefuldatawouldconAnuetogrowat40%annually.

• Issue1:Shor{allbetweenphysicalstoragemanufacturedin2015vsusefuldatacreatedin2015is1500EB(2Xmorethanallstoragemanufacturedin2015).Someshor{allisabsorbedbyde-duplicaAonandbycompression.

• Issue2:Manufacturedstorageisgrowingbyatbest6%peryearvsperceiveddatagrownof40%year.

• Issue3:InviewofIssue1andIssue2,eithertheIDCforecastsarenotaccurateorstorageusersareselecAvelystoringdata

• Issue4:Manufacturedstorage(withtheexcepAonof2008-2010)isnotincreasinggeometrically

Δ

0

500

1000

1500

2000

2500

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Exabytes

Year

DataGrowth-- Exabytes

HDD NAND

LTOTAPEMEDIA ANNUALPHYSICALSTORAGE

USEFULDATA

←RECESSION→

←CLOUD→ExponenAalHDDGrowthTunnel,Recording

ThailandFloods

©2016IBMCorpora2onPage20Fontana,Decad–LOC2016–StorageMedia

Summary

• ChangingNANDenvironment–Oversupply• 2015:30%increaseinPBshipmentswith3%increaseinrevenue• 2014:60%increaseinPBshipmentswith30%increaseinrevenue

• ChangingHDDenvironment–MarketErosion• 2015:3%increaseinPBshipmentswith15%decreaseinrevenue• 2014:17%increaseinPBshipmentswith0%revenuechange

• ChangingLTOMediaenvironment–ConAnuingRevenueDrop~8%/YRto10%/YR

• NANDrevenueexceedsHDDrevenue;NANDarealdensityexceedsHDDarealdensity

• Manufacturingenvironment–Moore’sLaw“doubling”notachieved• RevenueformanufacturedPBofstoragedecreasedby6%• TotalmanufacturedPBonlyincreasedby6%in2015.AdirectconflictwiththepercepAon

thatusefuldataincreasesat40%annually.

• Technology• TAPE–NextgeneraAonsensorintroducAon--Moore’sLawScaling• HDD–HAMR,ShingleMagneAcRecording,MorePlaeers–NotMoore’sLawScaling• NAND–Planar3bit/celldesignsat<16nm,3DmulA-layercellsat~60nm–Not

SustainedMoore’sLawScaling(24layersto48layersto96layersto…)

©2016IBMCorpora2onPage21Fontana,Decad–LOC2016–StorageMedia

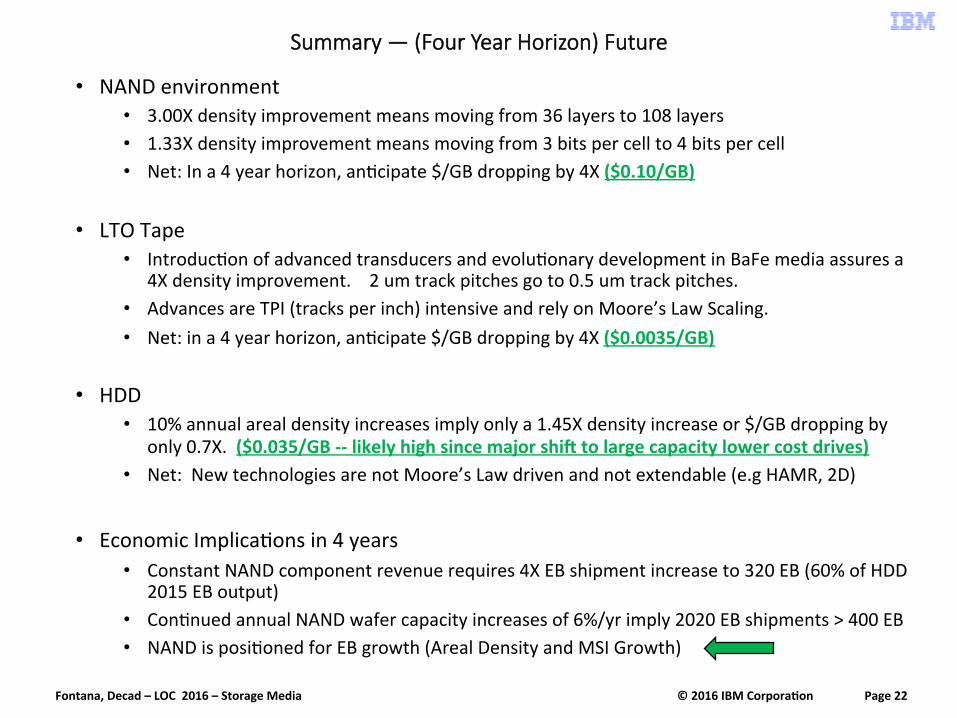

Summary — (Four Year Horizon) Future

• NANDenvironment• 3.00Xdensityimprovementmeansmovingfrom36layersto108layers• 1.33Xdensityimprovementmeansmovingfrom3bitspercellto4bitspercell• Net:Ina4yearhorizon,anAcipate$/GBdroppingby4X($0.10/GB)

• LTOTape• IntroducAonofadvancedtransducersandevoluAonarydevelopmentinBaFemediaassuresa

4Xdensityimprovement.2umtrackpitchesgoto0.5umtrackpitches.• AdvancesareTPI(tracksperinch)intensiveandrelyonMoore’sLawScaling.• Net:ina4yearhorizon,anAcipate$/GBdroppingby4X($0.0035/GB)

• HDD• 10%annualarealdensityincreasesimplyonlya1.45Xdensityincreaseor$/GBdroppingby

only0.7X.($0.035/GB--likelyhighsincemajorshimtolargecapacitylowercostdrives)• Net:NewtechnologiesarenotMoore’sLawdrivenandnotextendable(e.gHAMR,2D)

• EconomicImplicaAonsin4years• ConstantNANDcomponentrevenuerequires4XEBshipmentincreaseto320EB(60%ofHDD

2015EBoutput)• ConAnuedannualNANDwafercapacityincreasesof6%/yrimply2020EBshipments>400EB• NANDisposiAonedforEBgrowth(ArealDensityandMSIGrowth)

©2016IBMCorpora2onPage22Fontana,Decad–LOC2016–StorageMedia

Summary — Technology and the Market

• NANDenvironment

©2016IBMCorpora2onPage23Fontana,Decad–LOC2016–StorageMedia

Time

FigureofM

erit

(Reven

ue,V

olum

e,…)

MatureTechnology,StableMarket

NewTechnology,LowVolume,HighMargin

TechnologyCompaniesLead

Highgrowth,largeInvestment,mulApleplayers

ConsolidaAon,highvolumemanufacturing

Postconsumerdrivendesignpoints

HighVolume,LowerMargin,ConsumerCommodity

FlashEnterprise

HDDFlashConsumer

Tape