step seminar reviewing financial statements & · pdf filestep seminar –reviewing...

TRANSCRIPT

STEP Seminar – Reviewing Financial Statements & introducing the new GAAP27th February 2017

By Will Morgan

1 CONFIDENTIAL

TUTOR & COMPANY BACKGROUND

• Team of Accountants & Project managers (23 staff)

• Provide outsourced accounting functions to licenced entities

• Provide client accounting support to trust and fund structures

• Offers project management and consultancy services to businesses in Guernsey, Jersey and Switzerland

• Assists companies with a variety of projects including operations, accounting and systems

• Also offer public and “in house” training courses

2 CONFIDENTIAL

CONTENTS

• Accounting Principles

• Accounting Standards – the new GAAP! (FRS 102)

• What do the new accouting standards mean?

• Techniques used to review financial statements

3 CONFIDENTIAL

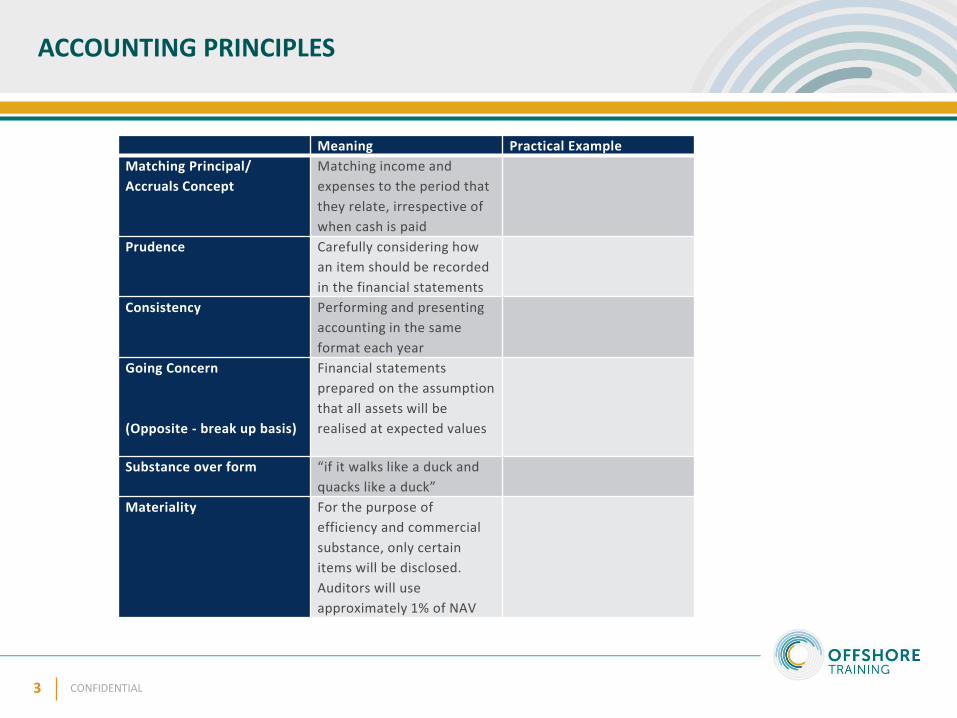

ACCOUNTING PRINCIPLES

Meaning Practical Example

Matching Principal/

Accruals Concept

Matching income and

expenses to the period that

they relate, irrespective of

when cash is paid

Prudence Carefully considering how

an item should be recorded

in the financial statements

Consistency Performing and presenting

accounting in the same

format each year

Going Concern

(Opposite - break up basis)

Financial statements

prepared on the assumption

that all assets will be

realised at expected values

Substance over form “if it walks like a duck and

quacks like a duck”

Materiality For the purpose of

efficiency and commercial

substance, only certain

items will be disclosed.

Auditors will use

approximately 1% of NAV

4 CONFIDENTIAL

OTHER CONSIDERATIONS

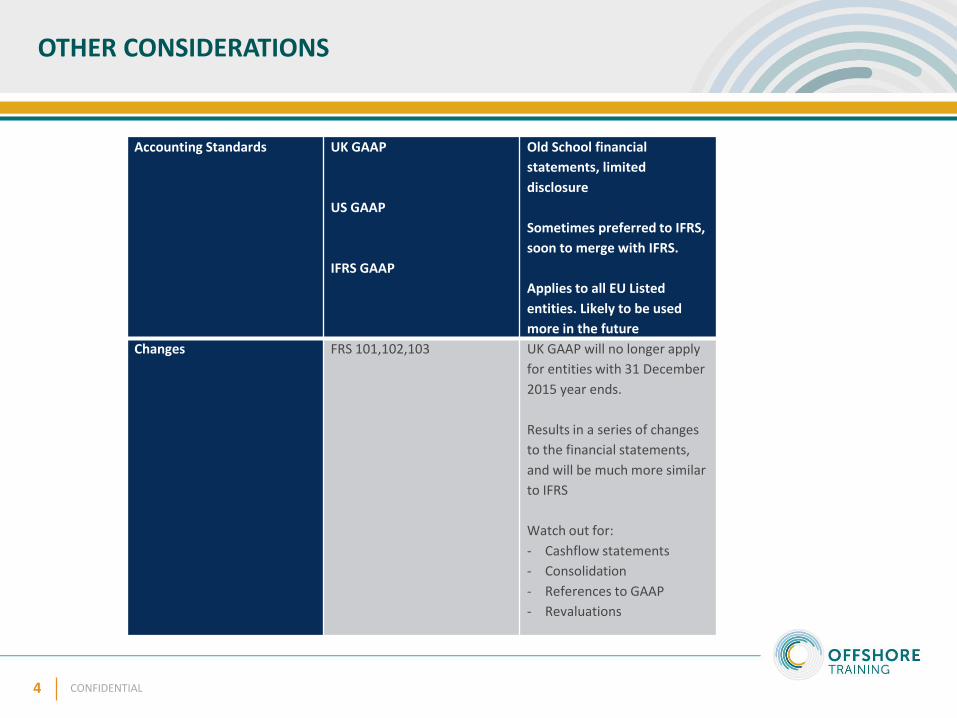

Accounting Standards UK GAAP

US GAAP

IFRS GAAP

Old School financial

statements, limited

disclosure

Sometimes preferred to IFRS,

soon to merge with IFRS.

Applies to all EU Listed

entities. Likely to be used

more in the future

Changes FRS 101,102,103 UK GAAP will no longer apply

for entities with 31 December

2015 year ends.

Results in a series of changes

to the financial statements,

and will be much more similar

to IFRS

Watch out for:

- Cashflow statements

- Consolidation

- References to GAAP

- Revaluations

5 CONFIDENTIAL

NEW GAAP – FRS 102

Regulated companies/ audited companies need to determine whether they:

1. Adopt full IFRS

2. Adopt the new Financial Reporting Standards FRS 101,102 & 103

3. Continue with the FRSSE (due to be abolished in 2 years)

FRS 102

This will replace the existing FRS/ UK GAAP model. The existing FRS 1 to X standards will be replaced by a new model that although is

similar, adopts a model that is more similar to IFRS. As previously mentioned, for many companies this was adopted for 31st December

2015 year ends and required the following highlights:

• Restating the prior year figures under the new regime

• Reconciliation between the primary statements for the change in standards

• Changes to reporting for:

• Revaluation of Assets/Investment Property

• Derivatives

• Holiday pay accruals

• Exceptional items no longer recorded on the face (FRS 3)

• Lease incentives

The document is 335 pages and includes 35 sections that relate the new framework being adopted.

Interestingly – all fair value disclosure items carry the “undue cost option” effectively giving an opportunity for companies to non-comply

on undue cost. It will be interesting to see how this is applied, and the impact that this has on the adoption.

6 CONFIDENTIAL

NEW GAAP – FRS 102

Property Investment Property

Valuation NBV = Cost less Depreciation Market Value

Ongoing Consider revaluation – Then ongoing (3/5 years) Assessment ongoing (3/ 5 years)

Revaluation

Impact

Continue to depreciate Revaluation Surplus

FRS 102

Impact

Revaluation Surplus Future changes in revaluation will be recorded in the profit

and loss account/ income statement

Continued Increased depreciation Revaluation as frequently as required

7 CONFIDENTIAL

NEW GAAP – FRS 102 – The Financial Statements

FRS 102 - Impact on the Financial Statements

The financial statements do not need to be presented differently following the adoption of the new standards. They do not insist that

the titles are changed, although one would expect that some parties will choose to adopt a more “IFRS” look to the financial statements:

Statement Of Comprehensive Income

Statement of Financial Position

Statement of Cashflow – Previously probably not required!

Statement of Change in Equity (SOCE)

Other Comprehensive Income (STRGL)

What does this mean for clients:

- Valuation becomes more material

- Accounting policy disclosure becomes more important (which GAAP?/ how are we valuing)

- The financial statements become comprehensive

- Some will understand, some will not care!

8 CONFIDENTIAL

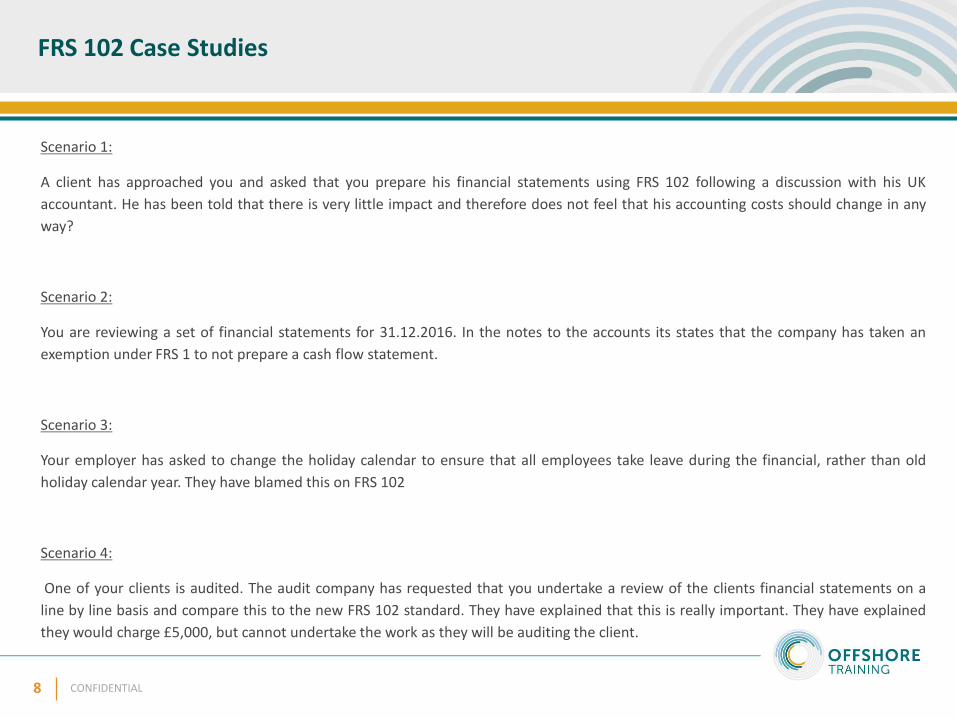

FRS 102 Case Studies

Scenario 1:

A client has approached you and asked that you prepare his financial statements using FRS 102 following a discussion with his UK

accountant. He has been told that there is very little impact and therefore does not feel that his accounting costs should change in any

way?

Scenario 2:

You are reviewing a set of financial statements for 31.12.2016. In the notes to the accounts its states that the company has taken an

exemption under FRS 1 to not prepare a cash flow statement.

Scenario 3:

Your employer has asked to change the holiday calendar to ensure that all employees take leave during the financial, rather than old

holiday calendar year. They have blamed this on FRS 102

Scenario 4:

One of your clients is audited. The audit company has requested that you undertake a review of the clients financial statements on a

line by line basis and compare this to the new FRS 102 standard. They have explained that this is really important. They have explained

they would charge £5,000, but cannot undertake the work as they will be auditing the client.

9 CONFIDENTIAL

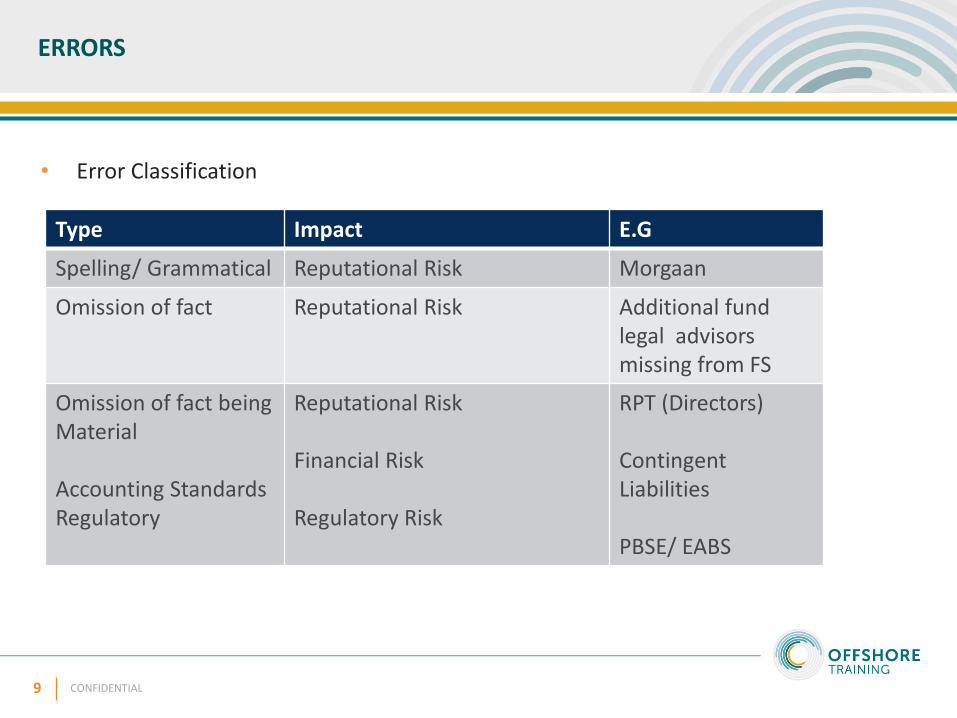

ERRORS

• Error Classification

Type Impact E.G

Spelling/ Grammatical Reputational Risk Morgaan

Omission of fact Reputational Risk Additional fund legal advisors missing from FS

Omission of fact beingMaterial

Accounting StandardsRegulatory

Reputational Risk

Financial Risk

Regulatory Risk

RPT (Directors)

ContingentLiabilities

PBSE/ EABS

10 CONFIDENTIAL

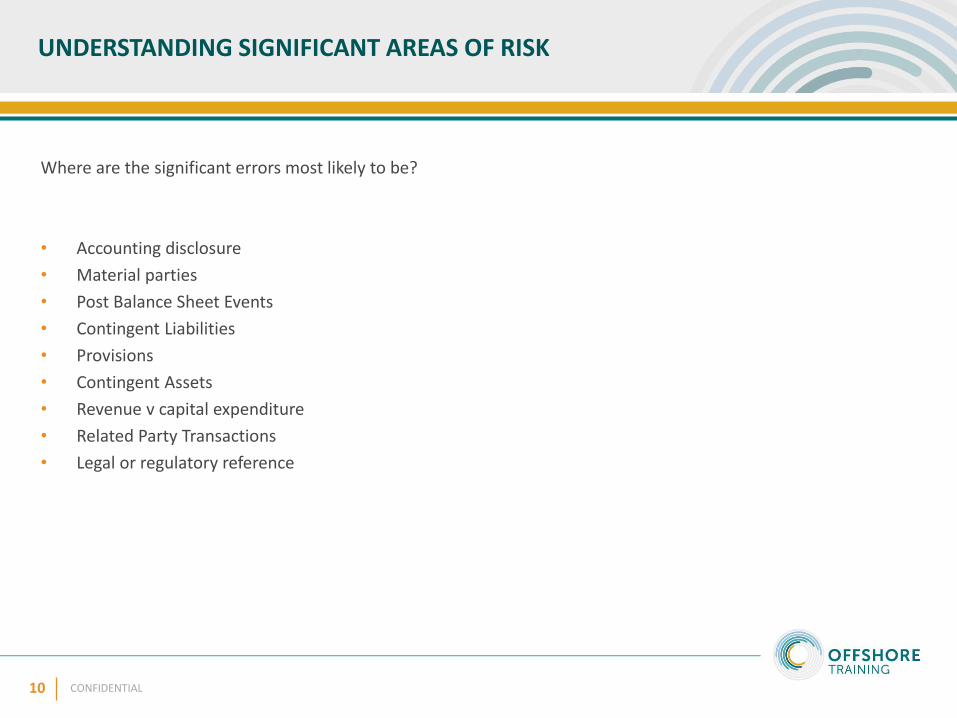

UNDERSTANDING SIGNIFICANT AREAS OF RISK

Where are the significant errors most likely to be?

• Accounting disclosure

• Material parties

• Post Balance Sheet Events

• Contingent Liabilities

• Provisions

• Contingent Assets

• Revenue v capital expenditure

• Related Party Transactions

• Legal or regulatory reference

11 CONFIDENTIAL

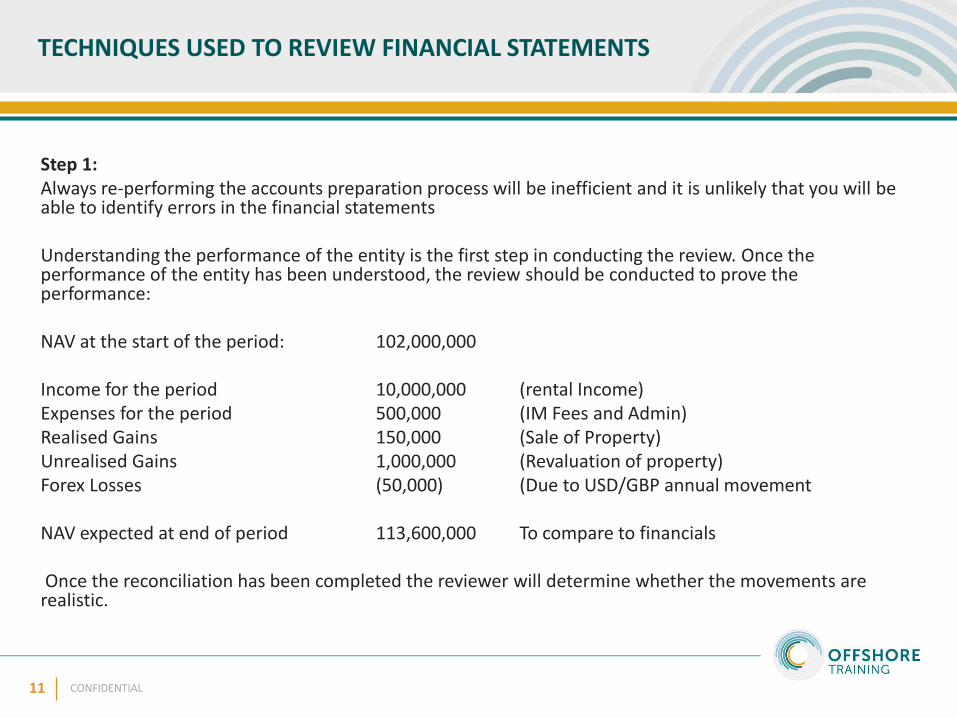

TECHNIQUES USED TO REVIEW FINANCIAL STATEMENTS

Step 1:Always re-performing the accounts preparation process will be inefficient and it is unlikely that you will be able to identify errors in the financial statements

Understanding the performance of the entity is the first step in conducting the review. Once the performance of the entity has been understood, the review should be conducted to prove the performance:

NAV at the start of the period: 102,000,000

Income for the period 10,000,000 (rental Income)Expenses for the period 500,000 (IM Fees and Admin)Realised Gains 150,000 (Sale of Property)Unrealised Gains 1,000,000 (Revaluation of property)Forex Losses (50,000) (Due to USD/GBP annual movement

NAV expected at end of period 113,600,000 To compare to financials

Once the reconciliation has been completed the reviewer will determine whether the movements are realistic.

12 CONFIDENTIAL

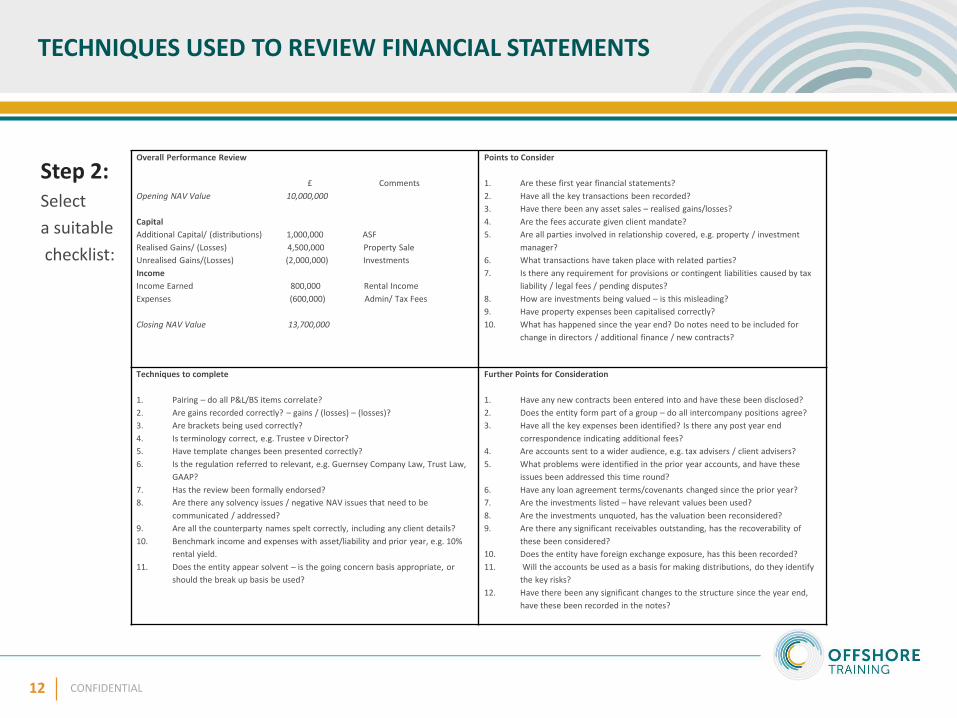

TECHNIQUES USED TO REVIEW FINANCIAL STATEMENTS

Step 2:Select

a suitable

checklist:

Overall Performance Review

£ Comments

Opening NAV Value 10,000,000

Capital

Additional Capital/ (distributions) 1,000,000 ASF

Realised Gains/ (Losses) 4,500,000 Property Sale

Unrealised Gains/(Losses) (2,000,000) Investments

Income

Income Earned 800,000 Rental Income

Expenses (600,000) Admin/ Tax Fees

Closing NAV Value 13,700,000

Points to Consider

1. Are these first year financial statements?

2. Have all the key transactions been recorded?

3. Have there been any asset sales – realised gains/losses?

4. Are the fees accurate given client mandate?

5. Are all parties involved in relationship covered, e.g. property / investment

manager?

6. What transactions have taken place with related parties?

7. Is there any requirement for provisions or contingent liabilities caused by tax

liability / legal fees / pending disputes?

8. How are investments being valued – is this misleading?

9. Have property expenses been capitalised correctly?

10. What has happened since the year end? Do notes need to be included for

change in directors / additional finance / new contracts?

Techniques to complete

1. Pairing – do all P&L/BS items correlate?

2. Are gains recorded correctly? – gains / (losses) – (losses)?

3. Are brackets being used correctly?

4. Is terminology correct, e.g. Trustee v Director?

5. Have template changes been presented correctly?

6. Is the regulation referred to relevant, e.g. Guernsey Company Law, Trust Law,

GAAP?

7. Has the review been formally endorsed?

8. Are there any solvency issues / negative NAV issues that need to be

communicated / addressed?

9. Are all the counterparty names spelt correctly, including any client details?

10. Benchmark income and expenses with asset/liability and prior year, e.g. 10%

rental yield.

11. Does the entity appear solvent – is the going concern basis appropriate, or

should the break up basis be used?

Further Points for Consideration

1. Have any new contracts been entered into and have these been disclosed?

2. Does the entity form part of a group – do all intercompany positions agree?

3. Have all the key expenses been identified? Is there any post year end

correspondence indicating additional fees?

4. Are accounts sent to a wider audience, e.g. tax advisers / client advisers?

5. What problems were identified in the prior year accounts, and have these

issues been addressed this time round?

6. Have any loan agreement terms/covenants changed since the prior year?

7. Are the investments listed – have relevant values been used?

8. Are the investments unquoted, has the valuation been reconsidered?

9. Are there any significant receivables outstanding, has the recoverability of

these been considered?

10. Does the entity have foreign exchange exposure, has this been recorded?

11. Will the accounts be used as a basis for making distributions, do they identify

the key risks?

12. Have there been any significant changes to the structure since the year end,

have these been recorded in the notes?

13 CONFIDENTIAL

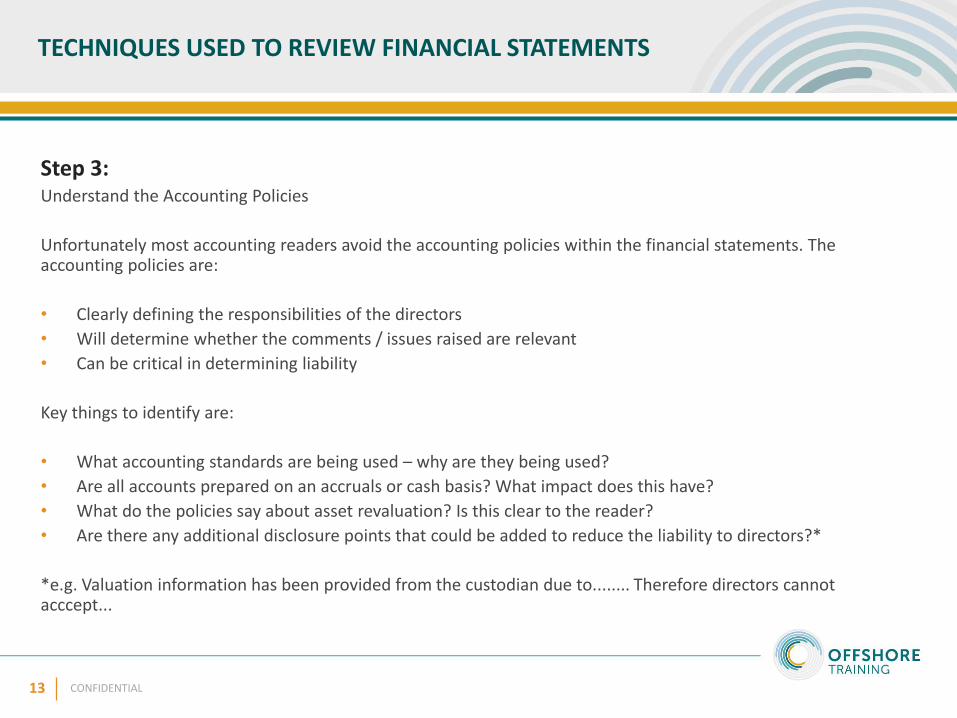

TECHNIQUES USED TO REVIEW FINANCIAL STATEMENTS

Step 3:Understand the Accounting Policies

Unfortunately most accounting readers avoid the accounting policies within the financial statements. The accounting policies are:

• Clearly defining the responsibilities of the directors

• Will determine whether the comments / issues raised are relevant

• Can be critical in determining liability

Key things to identify are:

• What accounting standards are being used – why are they being used?

• Are all accounts prepared on an accruals or cash basis? What impact does this have?

• What do the policies say about asset revaluation? Is this clear to the reader?

• Are there any additional disclosure points that could be added to reduce the liability to directors?*

*e.g. Valuation information has been provided from the custodian due to........ Therefore directors cannot acccept...

14 CONFIDENTIAL

Lessons Learned

Focus on a practical approach to reviewing financial statements:

1. Review the notes to the financial statements

2. Initially focus on the fundamentals rather than the detail

3. Complete a NAV Review of the entity

4. Consider a client summary – what would they be considering in their review

5. Consider the responsibilities of the Trust Officer

6. Focus on the detail

THANK YOUPLEASE VISIT WWW.OFFSHORE.GG TO VIEW OUR FULL RANGE OF COURSES

This course is the property of Offshore Consulting (Guernsey) Limited for the purposes of and in accordance with the Copyright (Bailiwick of Guernsey) Ordinance 2005.

All rights reserved. No part of this document may be reproduced, stored in a retrieval system of any kind or transmitted in any form or by any means, electronic, mechanical, photocopying,

recording or otherwise, without the prior written permission of Offshore Consulting (Guernsey) Limited.

Please note that this document is intended to provide training materials only. It is not intended to provide specific financial or legal advice and should not be relied upon as such.

© Offshore Consulting (Guernsey) Limited 2017