stealthgas inc. · interest rate swaps and foreign currency hedging arrangements, ... free cash...

TRANSCRIPT

StealthGas Inc. StealthGas Inc. 44thth Quarter 2010 ResultsQuarter 2010 Results

February 23February 23rdrd, , 20102010

CONSISTENCY & GREAT VALUECONSISTENCY & GREAT VALUE

Disclaimer

Forward-Looking Statements

This presentation contains forward-looking statements within the meaning of applicablefederal securities laws. Such statements are based upon current expectations thatinvolve risks and uncertainties. Any statements contained herein that are not statementsof historical fact may be deemed to be forward-looking statements. For example, wordssuch as “may,” “will,” “should,” “estimates,” “intends,” and similar expressions areintended to identify forward-looking statements. Actual results and the timing of certainevents may differ significantly from the results discussed or implied in the forward-looking statements. Among the factors that might cause or contribute to such adiscrepancy include, but are not limited to the risk factors described in the Company’sRegistration Statement filed with the Securities and Exchange Commission, particularlythose describing variations on charter rates and their effect on the Company’s revenues,net income and profitability as well as the value of the Company’s fleet.

1

Business Strategy Implementation

Consolidation and fleet renewal

Sold 5 LPG carriers in 2010

Acquiring 5 Newbuilding LPG Carriers (4 in 2011 and 1 in 2012)

Acquired Newbuilding Aframax Crude Oil Tanker in 2010

Moderate Leverage Fourth Quarter 2010 net debt to capitalization: 45.8%

Visible Revenue Stream –Consistency

61% of voyage days fixed for FY 2011

35% of voyage days fixed for FY 2012

During 2010 announced 20 new charter arrangements of duration 12months or more.

Modern Fleet Our fleet average age is 12.0 years

Sector average age is 18.5 years

Close Customer Relations High quality customer base – low counterparty risk

Cost-Efficient Operations

Consistent Breakeven

Net Income Breakeven of $6,188 per day in Q4 2010 (net of realized loss on interest rate swaps) compared to $6,311 in Q3 2010 and $5,963 in Q2

2010.

Common Stock

Re-Purchase

Instigated plan to buy-back up to $15 Million worth of Common Stock

As of December 31st 2010, repurchased 5.6 % of stocks outstanding.

Business Strategy

2

Fleet Development

Newbuilding program of 4 LPG carriers delivering in 2011 and 1 delivering in 2012

Newbuilding program has committed financing

Selective sale of older & smaller tonnage in 2010/11

3

Fleet Employment Profile

4

Fourth Quarter 2010 Financial Highlights

5

Fourth Quarter 2010

Q4 Net Income of $4.3 million, net revenues of $29.1 million, EBITDA of

$13.2 million

Q4 Net income of $2.4 million before net non cash gain of $1.3 million on

interest rate swaps and foreign currency hedging arrangements, $0.6

million gain on unrealized exchange difference

EPS of $0.21 per share (EPS $0.12 per share before non cash gain on

interest rate swaps and foreign currency hedging arrangements, gain on

unrealized exchange difference) on 21.1 million shares outstanding

Free cash balance of circa $30.0 million

Conservative leverage: net debt to capitalization of 45.8%

Fourth Quarter 2010 Income Statement

6

In US$ 000, except per share amounts Q4 2009 Q3 2010 Q4 2010

Net Revenues $28,381 $26,727 $29,056

Operating Income (20,843)(1)

4,540(2)

5,817

Net Income(3)

(27,151)(1)

990(2)

4,343

Net Income, net of interest rate swap, stock based compensation, impairment loss, unrealized exchange difference, contract termination fees and forfeiture of vessel deposit

2,270 942 2,440

EBITDA(3)

(17,645)(1)

9,703(2)

13,232

EPS(3)

(1.22)(1)

0.05(2)

0.21

EPS, net of interest rate swap, stock based compensation, impairment loss, unrealized exchange difference, contract termination fees and forfeiture of vessel deposit

0.10 0.04 0.12

Number of Shares, diluted 22,291,064 21,091,139 21,101,882

(1) Includes gain $ 1.1 million unrealized exchange difference on foreign currency deposit(2) Includes gain $ 0.6 million unrealized exchange difference on foreign currency deposit(3) Includes impairment loss $ 9.9 million and $10.75 million payment on termination of

vessel acquisition contract plus forfeiture of vessel deposit

Fourth Quarter 2010 Operating Highlights

7

Fleet Data Q4 2009 Q4 2010 FY 2009 FY 2010

Average number of vessels in fleet 42.8 38.0 42.0 38.6

Period end number of vessels in fleet 42 38 42 38

Total calendar days for fleet 3,934 3,496 15,335 14,075

Total voyage days for fleet 3,898 3,470 15,240 13,835

Fleet utilization 99.1% 99.3% 99.4% 98.3%

Total charter days for fleet 2,941 2,605 12,276 10,327

Total spot market days for fleet 957 865 2,964 3,508

Fleet operational utilization 86.8% 92.2% 90.2% 87.3%

Average Daily Results (in $) Q4 2009 Q4 2010 FY 2009 FY 2010

Time Charter Equivalent – TCE $7,324* $8,024* $7,712* $7,810*

Vessel Operating Expenses 3,473* 3,643* 3,464* 3,571*

Management Fees 355 379 341 368

General & Administrative Expenses 198 235 232 215

Total Vessel Operating Expenses 3,671* 3,878* 3,696* 3,786*

Fleet Data & Daily Results

* Assuming no vessels on Bareboat Charter

Daily Breakeven

8

Q4 2010 & FY 2010 Daily Cash Flow and Net Income Breakeven Composition

($ per vessel per day) Q4 2010 fleet calendar days: 3,496

FY 2010 fleet calendar days: 14,075

Q4 2010 Q4 2010

Cash Flow Net Income

FY 2010 FY 2010

Cash Flow Net Income

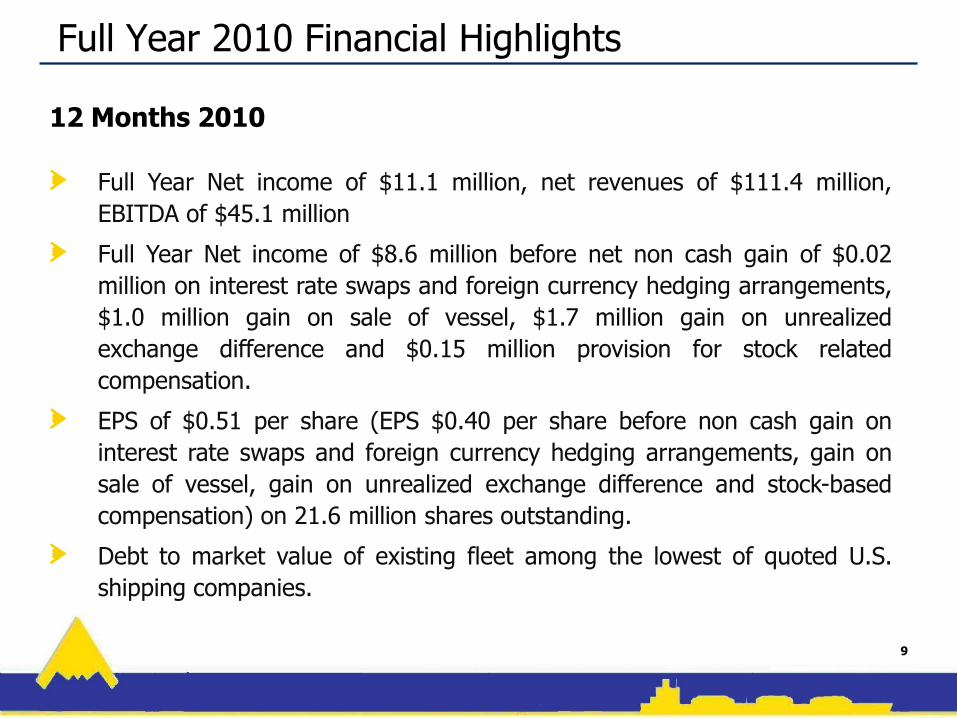

Full Year 2010 Financial Highlights

9

12 Months 2010

Full Year Net income of $11.1 million, net revenues of $111.4 million,

EBITDA of $45.1 million

Full Year Net income of $8.6 million before net non cash gain of $0.02

million on interest rate swaps and foreign currency hedging arrangements,

$1.0 million gain on sale of vessel, $1.7 million gain on unrealized

exchange difference and $0.15 million provision for stock related

compensation.

EPS of $0.51 per share (EPS $0.40 per share before non cash gain on

interest rate swaps and foreign currency hedging arrangements, gain on

sale of vessel, gain on unrealized exchange difference and stock-based

compensation) on 21.6 million shares outstanding.

Debt to market value of existing fleet among the lowest of quoted U.S.

shipping companies.

Full Year 2010 Income Statement

10

In US$ 000, except per share amounts12 Months

200912 Months

2010

Net Revenues $113,046 $111,410

Operating Income 1,287 23,024

Net Income (13,312) 11,093

Net Income, net of interest rate swap, loss/(gain) on sale of vessel, unrealized exchange difference and stock based compensation

15,876 8,580

EBITDA 22,132 45,075

EPS (0.60) 0.51

EPS, net of interest rate swap, loss/(gain) on sale of vessel, unrealized exchange difference and stock based compensation

0.71 0.40

Number of Shares, basic 22,219,442 21,553,659

Financial Estimator 2011

11

Contracted Revenues $77 million

Non contracted Voyage days 5,370

Drydock Expenses $5.1 million (11 vessels)

Interest & Swaps (cash portion) $14.2 million

Operating, G&A, Management Fees, Commissions at similar levels to 2010

D&A $29.0 million

Remaining Payments for Newbuildings $65.0 million (2011) $21million (2012)

LPGC Freight Rates

12

Average earnings in the spot market excluding waiting time / 1 yr TC rates

Source: Inge Steensland AS

100

200

300

400

500

600

700

800

2003 2004 2005 2006 2007 2008 2009 2010 2011

USD

10

00

's p

er m

on

th

15000 SR TCE

8000 ETH TCE

6500 SR TCE

3500 SR 1yr TC

3500 PR 1yr TC east

INGE STEENSLAND AS

Small LPG tanker rates are less volatile than crude tanker and drybulk rates

Data source: Clarkson Research Services 2009

Rates: 1-year TC measured weekly

Dry Bulk: average of Cape, Panamax, Handymax, and

Handysize rates

Crude Tanker: average of VLCC, Suezmax, and Aframax rates

But, small LPG rates remain relatively stable

1-Year TC Rate Volatility Since 2000

13

1-Year TC Rate Volatility Since 2000

Charter Market Rate Indicator (12 Month TCs)

Q4 2010 Average Current Q1 2011 Forecast

3,200 CBM S/R 256,000 270,000 270,000

3,500 CBM P/R 232,000 248,000 255,000

5,000 CBM P/R 265,000 295,000 310,000

6,000 CBM S/R 450,000 450,000 450,000

15,000 CBM S/R 514,000 525,000 540,000

35,000 CBM 591,000 620,000 650,000

60,000 CBM 650,000 650,000 650,000

78,000 CBM 711,000 725,000 725,000

Source: Lorentzen & Stemoco

14

3000-7999 cbm Fleet Development Vs. TC Rates/Earnings*

•TC equivalent spot earnings are assessed average earnings in the spot market excluding waiting time

•Fleet growth excl. Chinese fleet

Source: Inge Steensland AS 15

-5%

0%

5%

10%

15%

-

100

200

300

400

500

600

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Flee

t gro

wth

in %

(bar

s)

TC e

quiv

. spo

t ear

ning

sTC

rate

s in

USD

100

0's p

er m

onth

(lin

es)

Overall 3000-7999 fleet growth S/R 3000-7999 fleet growth SR 6500 cbm TCE

SR 3500 cbm 1yr TC PR 3500 cbm 1yr TC East

INGE STEENSLAND AS

Despite a “stop” in new ordering, lots of ships will be delivered But not in the LPG space

Source: DnB NOR Markets – Shipping Sector Outlook 2010* Includes all LPG Carriers size categories

16

Orderbooks in Percent of Existing Fleet

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

Tank Drybulk Product Chemical LPG LNG Container Reefer PCC

sep.09 jan.10

*

Shipping Sector “Value” Comparison

* Source: for LT/Cap and NAV Cantor & Fitzgerald & Co., as of February 14th , 2011

Company Name SymbolLT

Debt/CAP NAV P/NAVLatest Price

StealthGas Inc. “GASS” 48.0% $13.00 0.51x 6.59

Diana Shipping Inc. * “DSX” 23.0% $13.75 1.01x 12.56

DryShips Inc. * “DRYS” 47.0% $7.35 0.62x 4.88

Nordic American Tanker Shipping Ltd. * “NAT” 5.0% $14.6 1.70x 24.63

Double Hull Tankers * “DHT” 58.0% $4.76 1.01x 4.85

Crude Carriers * “CRU” 32.0% $19.00 0.81x 15.43

17

Contacts

Company Contact:

Konstantinos Sistovaris Visit our Website at:Chief Financial Officer www.stealthgas.comStealthGas Inc.011-30-210-6250-001E-mail: [email protected]

Weekly LPG Market Report

updated every Monday

Comprehensive Investor

Relations Information

18