statement of advice - smsf advisers network · this document (called a statement of advice or...

TRANSCRIPT

SMSF ADVISERS NETWORK PTY LTD

ABN 64 155 907 681 An Australian Financial Services Licensee

Licence Number: 430062 29-33 Palmerston Crescent, South Melbourne Vic 3205

Ph: 1800 906 456 Fax: 1300 306 351

© SMSF Advisers Network Pty Ltd

Wholly owned subsidiary of the

National Tax & Accountants’ Association

STATEMENT OF ADVICE

Prepared for

Client A Client B

Client C Client D

By Adviser Name

Adviser Number: xxxxxxxxx

Dated: xx/xx/20xx

Version 1.0

Adviser Office Address: Street Address

Suburb State P’Code

Phone: (XX) XXXX XXXX

Mobile: XXXX XXX XXX

Email: [email protected]

What this document is about

CLIENT NAME, you have asked for my advice in relation to your superannuation situation.

This document (called a Statement of Advice or ‘SOA’) explains my advice.

At the front of the SOA I highlight the key points of my advice, but please make sure you read each section of the SOA.

Please note that the advice given is based on the objectives you have stated and that of your current situation. Where the information you have given is incomplete or incorrect this may have an effect on whether my advice is appropriate or not. Because of this it is important you check the information contained in relation to your current situation and not just the recommendations provided.

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 2 of 30

Important information regarding this advice

What is the ‘scope’ of this advice

As an authorised representative of SMSF Advisers Network Pty Ltd I am authorised to provide advice only in relation to your superannuation needs.

This scope is further restricted to being able to advise only on whether the establishment of a Self Managed Superannuation Fund is appropriate given your goals and circumstances.

A further restriction to this advice is as to whether you should make use of a Limited Recourse Borrowing Arrangement (LRBA) as part of your superannuation structure.

This scope is further restricted to being able to solely advise on the amount of contributions to be made to your superannuation fund, given your current circumstances.

This scope is further restricted to being able to solely advise on how you could restructure your superannuation balance for a more effective estate distribution.

This scope is further restricted to providing advice about the establishment of an income stream from your current superannuation arrangements.

This scope is further limited in this instance to solely advise on whether or not you should wind-up your Self Managed Superannuation Fund (SMSF), given your current circumstances.

What impact does this ‘scope’ have on my situation

This advice is related only to your superannuation fund structure; it does not provide advice on any other area of your personal financial needs.

Further, it does not provide you with recommendations for any specific investment or insurance product to meet the requirements of the fund members and their member accounts.

Can these areas be addressed if I request?

I am only allowed to provide advice in relation to my authorisation given by my licensee (SMSF Advisers Network Pty Ltd). As I am not authorised to discuss such areas I cannot give advice in relation to these.

Should you wish to receive advice on such areas I will be happy to provide a referral for this purpose. By providing such a referral it should not be taken as a recommendation made by this practice of any financial product that the referrer should recommend. Any recommendation made by such a group is solely the recommendation of that party and is independent of any advice you have received from myself as an authorised representative of SMSF Advisers Network Pty Ltd.

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 3 of 30

Section 1: Important information about you

This section has information about you that I used in preparing my advice, such as:

Your goals and objectives;

Your personal and financial information; and

Your risk profile and financial knowledge.

Please tell me if you think this information is wrong or incomplete because it will affect my advice

Your goals and objectives

You have approached me requesting advice regarding:

Whether or not a Self Managed Superannuation Fund would be appropriate for your retirement savings needs;

If appropriate, how a Self Managed Superannuation Fund would be best structured;

If appropriate, how a Self Managed Superannuation Fund would operate (i.e., what is required for the members to do and what (if any) tasks might be outsourced to professionals); and

If appropriate, whether the SMSF should use borrowing as part of its structure to help achieve retirement goals.

What amount of contribution should be made to your superannuation fund?

How your superannuation fund balance might be restructured to provide a tax-free benefit payment to beneficiaries?

Whether or not you should commence a pension to be paid from your Superannuation Fund

whether or not you should commence a pension to be paid from your Superannuation Fund while you continue to work before full retirement

Whether or not your investment strategy should be adjusted in any way to support the payment of pension benefits from your fund.

Whether or not you should wind up your SMSF.

Other – personalize as required for your client

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 4 of 30

Your current situation

Personal Details

Full Name

Date of Birth

Health Status Excellent / Good / Poor

Smoking Status Smoker / Non-Smoker

Occupation

Employer

Gross Annual Income

Intended Retirement Age

Desired retirement income (today’s dollars) $

Health Insurance Provider

Total Life Insurance Held $

Total TPD Cover Held $

Salary Continuance Held $ per month

Total Debt Owed $

Dependants (Ages) ( )

( )

( )

( )

Will In Place Yes / No Updated: / /

Power of Attorney Yes / No General Financial Medical

Superannuation Assets

Total Superannuation Assets $

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 5 of 30

Personal Details

Full Name

Date of Birth

Health Status Excellent / Good / Poor

Smoking Status Smoker / Non-Smoker

Occupation

Employer

Gross Annual Income

Intended Retirement Age

Desired retirement income (today’s dollars) $

Health Insurance Provider

Total Life Insurance Held $

Total TPD Cover Held $

Salary Continuance Held $ per month

Total Debt Owed $

Dependants (Ages) ( )

( )

( )

( )

Will In Place Yes / No Updated: / /

Power of Attorney Yes / No General Financial Medical

Superannuation Assets

Total Superannuation Assets $

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 6 of 30

Personal Details

Full Name

Date of Birth

Health Status Excellent / Good / Poor

Smoking Status Smoker / Non-Smoker

Occupation

Employer

Gross Annual Income

Intended Retirement Age

Desired retirement income (today’s dollars) $

Health Insurance Provider

Total Life Insurance Held $

Total TPD Cover Held $

Salary Continuance Held $ per month

Total Debt Owed $

Dependants (Ages) ( )

( )

( )

( )

Will In Place Yes / No Updated: / /

Power of Attorney Yes / No General Financial Medical

Superannuation Assets

Total Superannuation Assets $

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 7 of 30

Personal Details

Full Name

Date of Birth

Health Status Excellent / Good / Poor

Smoking Status Smoker / Non-Smoker

Occupation

Employer

Gross Annual Income

Intended Retirement Age

Desired retirement income (today’s dollars) $

Health Insurance Provider

Total Life Insurance Held $

Total TPD Cover Held $

Salary Continuance Held $ per month

Total Debt Owed $

Dependants (Ages) ( )

( )

( )

( )

Will In Place Yes / No Updated: / /

Power of Attorney Yes / No General Financial Medical

Superannuation Assets

Total Superannuation Assets $

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 8 of 30

Current superannuation balances

Member Balance ($)

Member 1 Name

Member 2 Name

Member 3 Name

Member 4 Name

Total Fund Balance

Estimate sources of contribution

Source of funds Amount ($)

Estimated company profit at 30 June

Surplus income over expenses

Expected bonus remuneration

Surplus liquid assets

Sale of assets

Total funds available for contribution

Current superannuation balances

Member Total Balance ($) Taxable

Component Tax-Free

Component

Member 1 Name

Member 2 Name

Member 3 Name

Member 4 Name

Total Fund Balance

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 9 of 30

Your risk profile

Investing involves risk. Risk is the chance that an investment will not give you the returns you have hoped for or that you will lose money. Almost all investments have risk, but some have more than others.

Generally, investments that are expected to pay higher returns involve more risk. While these investments are likely to product higher returns over time than more conservative investments, over short periods they can fall in value and lose money.

From our discussions I believe you should invest the assets of your fund in line with what we would classify as a XXXXXXXXX investor. The major characteristics of this investor type are:

For more detail on the investment attitudes supporting this recommendation please refer to the fund investment strategy found in the appendices to this document. If there is any aspect of the analysis and recommendation that you do not feel meets your situation please let me know so that adjustments can be made where necessary.

OR

Making a contribution to superannuation does not require an assessment of your personal investor risk profile and makes no impact on the investment strategy for your superannuation fund.

OR

Restructuring your superannuation components does not require an assessment of your personal investor risk profile and makes no impact on the investment strategy for your superannuation fund.

OR

Investing involves risk. Risk is the chance that an investment will not give you the returns you have hoped for or that you will lose money. Almost all investments have risk, but some have more than others.

Generally, investments that are expected to pay higher returns involve more risk. While these investments are likely to produce higher returns over time than more conservative investments, over short periods they can fall in value and lose money.

As you move into the pension phase of your superannuation fund you need to bear in mind:

liquidity will be required to ensure pension payments can be met on a regular basis;

sufficient diversification is in place to reduce the risk of market volatility to the fund; and

growth is still targeted to ensure that the effect of inflation on investment balances and therefore pension payments is negated.

From our discussions I believe you should invest the assets of your fund in line with what we would classify as a XXXXXXXXX investor. The major characteristics of this investor type are:

INSERT RISK PROFILE DETAILS

If there is any aspect of the analysis and recommendation that you do not feel meets your situation please let me know so that adjustments can be made where necessary.

OR

The decision as to whether or not you should wind up your SMSF is based on factors other than your attitude to investment risk .

Because the sole issue for consideration with this advice is whether or not to wind up your SMSF we have not provided an analysis of your risk profile here.

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 10 of 30

Section 2: My advice to you

This section tells you:

What my advice is and why it is appropriate for you;

Any disadvantages of my advice;

The consequences of replacing one financial product with another; and

The areas my advice does not deal with.

Please read this section carefully and ask me if you have any questions.

What is my advice?

Based on your desire to control your own superannuation investments and my assessment of your abilities to understand and take responsibility for the running of such a structure I recommend that you commence the FUND NAME Superannuation Fund with the following members:

Member Balance ($)

Member 1 Name

Member 2 Name

Member 3 Name

Member 4 Name

Total Fund Balance

The trustee structure for this fund should be a corporate trustee that we will establish as CORPORATE TRUSTEE NAME Pty Ltd

OR

The trustee structure for this fund should be the individual members of the fund as the trustees.

You should establish an investment strategy to reflect that the assets of the fund will be invested in a manner that is in line with the risk profile selected for the fund. Please note that in establishing an investment strategy you also need to consider your requirements for personal insurance and if cover should be included in your fund.

Member balances of personal or other superannuation funds held should be rolled over into the FUND NAME Superannuation fund and invested according to the fund investment strategy.

OR

Establish binding death benefit nominations for payments to beneficiaries

Implement a limited recourse borrowing arrangement to allow the fund to borrow for investment purposes. Based on the situation of your super fund I recommend the following situation:

Name of Bare Trust

Anticipated value of property to be purchased $

Total deposit from superannuation fund $

Expected costs to be paid from superannuation fund $

Loan required $

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 11 of 30

Loan to Value ratio /

Estimated Loan repayments p.a. $

Expected rental income p.a. $

Expected total net contributions to fund p.a. $

Expected other investment income to fund p.a. $

Expected surplus income p.a. $

These figures above are based on what I believe to be the optimum situation for your superannuation fund.

Please be aware that in seeking finance for this structure, lenders will have their own requirements in relation to loan-to-value ratios, minimum loan amounts, etc.

Should your preferred lender recommend a significant change to the areas in the table above (i.e., an increase of greater than 5%) you should contact me immediately so we can review the revised figures before you proceed with seeking finance.

Based on your current situation, I recommend the following amount and type of contribution be made to superannuation for the following members:

Superannuation Fund Member Contribution ($) Contribution type

Member 1 Name Non-Concessional /

Concessional

Member 2 Name Non-Concessional /

Concessional

Member 3 Name Non-Concessional /

Concessional

Member 4 Name Non-Concessional /

Concessional

Based on your current situation, I recommend members withdraw the amounts shown in the table below, then immediately recontribute them to their superannuation balance:

Member Withdrawal/Recontribution ($)

Member 1 Name

Member 2 Name

Member 3 Name

Member 4 Name

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 12 of 30

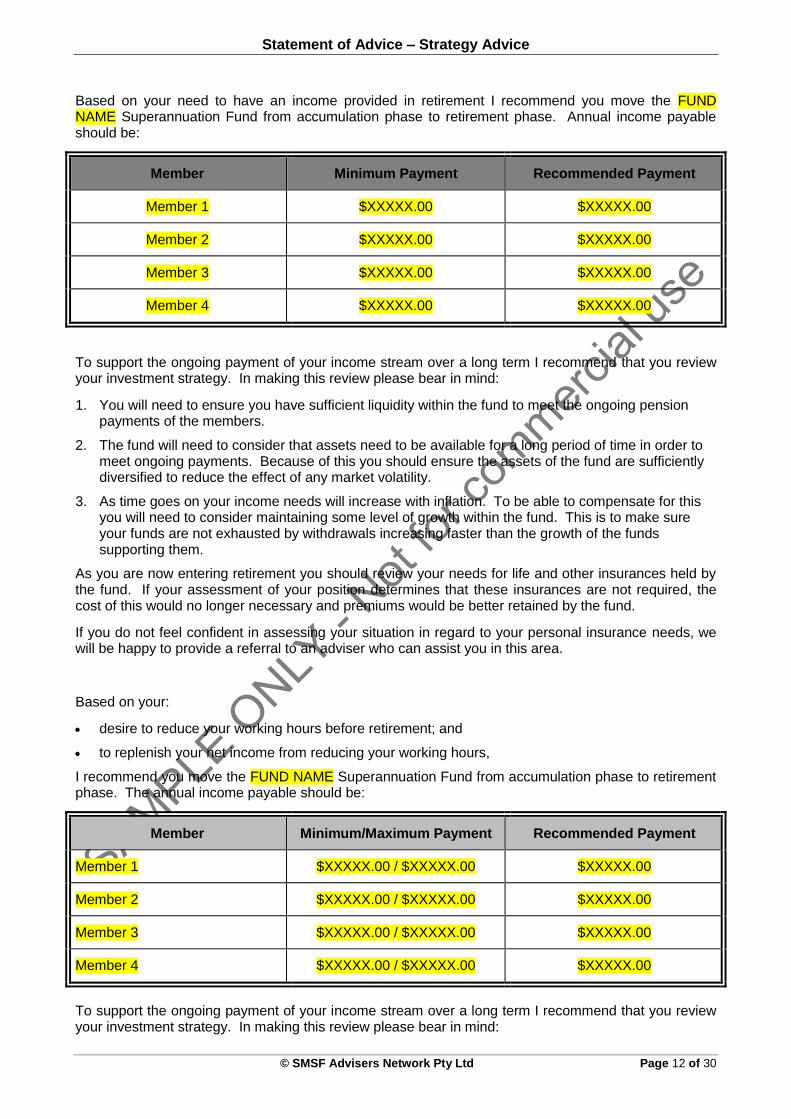

Based on your need to have an income provided in retirement I recommend you move the FUND NAME Superannuation Fund from accumulation phase to retirement phase. Annual income payable should be:

Member Minimum Payment Recommended Payment

Member 1 $XXXXX.00 $XXXXX.00

Member 2 $XXXXX.00 $XXXXX.00

Member 3 $XXXXX.00 $XXXXX.00

Member 4 $XXXXX.00 $XXXXX.00

To support the ongoing payment of your income stream over a long term I recommend that you review your investment strategy. In making this review please bear in mind:

1. You will need to ensure you have sufficient liquidity within the fund to meet the ongoing pension payments of the members.

2. The fund will need to consider that assets need to be available for a long period of time in order to meet ongoing payments. Because of this you should ensure the assets of the fund are sufficiently diversified to reduce the effect of any market volatility.

3. As time goes on your income needs will increase with inflation. To be able to compensate for this you will need to consider maintaining some level of growth within the fund. This is to make sure your funds are not exhausted by withdrawals increasing faster than the growth of the funds supporting them.

As you are now entering retirement you should review your needs for life and other insurances held by the fund. If your assessment of your position determines that these insurances are not required, the cost of this would no longer necessary and premiums would be better retained by the fund.

If you do not feel confident in assessing your situation in regard to your personal insurance needs, we will be happy to provide a referral to an adviser who can assist you in this area.

Based on your:

desire to reduce your working hours before retirement; and

to replenish your net income from reducing your working hours,

I recommend you move the FUND NAME Superannuation Fund from accumulation phase to retirement phase. The annual income payable should be:

Member Minimum/Maximum Payment Recommended Payment

Member 1 $XXXXX.00 / $XXXXX.00 $XXXXX.00

Member 2 $XXXXX.00 / $XXXXX.00 $XXXXX.00

Member 3 $XXXXX.00 / $XXXXX.00 $XXXXX.00

Member 4 $XXXXX.00 / $XXXXX.00 $XXXXX.00

To support the ongoing payment of your income stream over a long term I recommend that you review your investment strategy. In making this review please bear in mind:

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 13 of 30

4. Commencing a payment of this type requires the balance supporting the payment to be “non-commutable” (i.e., can’t be cashed). Because of this, the funds cannot be used for any short term liquidity needs.

5. You will need to ensure you have sufficient liquidity within the fund to meet the ongoing pension payments of the members.

6. The fund will need to consider that assets need to be intact for a long period of time in order to meet ongoing payments. Because of this you should ensure the assets of the fund are sufficiently diversified to reduce the effect of any market volatility.

7. As time goes on your income needs will increase with inflation. To be able to compensate for this you will need to maintain some level of growth within the fund to make sure your funds are not exhausted by withdrawals increasing faster than the growth of funds supporting them.

As you are now entering retirement, it is likely that your debt has reduced significantly and that any dependants are no longer financially dependent on you. Because of this you should review your needs for life and other insurances held by the fund. If they are not required, the cost of this is no longer necessary and premiums are better retained by the fund.

Please note: when you eventually retire fully this pension type can be converted to an Account Based Pension; a type that has no maximum amount for withdrawal and does allow lump sums to be accessed as required.

Based on your current situation, I recommend that you proceed with winding up the FUND NAME Superannuation Fund

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 14 of 30

What is a Self Managed Superannuation Fund?

A Self Managed Superannuation Fund (SMSF) is a superannuation trust structure, established for the purpose of providing retirement benefits to its members.

This type of superannuation fund can only have up to four members, each of which must be a trustee of the fund, or if using a Corporate Trustee, must be directors of that company.

The benefits of an SMSF are that it provides a high degree of flexibility in the way that it is run, subject to rules that govern this structure.

It should be noted that an SMSF should not simply be considered as another source of funds for investment. The “Sole Purpose Test” that override all SMSFs is there to ensure that the fund is maintained for the purpose of providing benefits to members at retirement – that it is not there to provide benefits or advantages before then.

To support the Sole Purpose Test, other regulations govern what can or can’t be done with the SMSF, including:

Restrictions on “related party transactions”, where only certain assets can be purchased from a “related party”;

Dealing at “arms length”, to make sure that assets are dealt with at market rates, ratehr than providing an advantage to members before retirement; and

Purchasing “collectibles” in the SMSF, where those who wish to purchase certain “collectible” assets must meet certain requirements for display, storage and insurance.

IMPORTANT – DISCLOSURE OF RISKS: MOVING TO AN SMSF

When moving from a commercial superannuation fund (what is referred to as a “public offer fund” or a workplace “corporate” fund, there are certain items that should be considered when making your decision to manage your own superannuation fund.

These considerations should be taken into account alongside the benefit of managing your own superannuation arrangements, and have been outlined for you in the appendix to this Statement of Advice.

You should take the time to all these points should be considered with any change to your current superannuation arrangements, I believe that an SMSF would suit your personal needs and provide benefits for the provision of your retirement income funding arrangement.

What is a Limited Recourse Borrowing Arrangement?

The use of a Limited Recourse Borrowing Arrangement (LRBA) by an SMSF is a popular method of funding the purchase of a range of assets including property and bundles of identical shares.

Under such an arrangement, SMSF trustees are allowed to purchase a “single acquirable asset” with a loan that does not have any recourse to the assets of the SMSF. To be able to meet this requirement (limited recourse), the asset must be held in a trust linked to but separate from the SMSF.

IMPORTANT RISK CONSIDERATION

You should note that entering into a gearing strategy (i.e. borrowing money to invest) is regarded as a high-risk strategy. This is because while the investment may grow, it may also lose value depending upon the particular market the investment is in.

While the investment may vary in value, a loan will remain constant, reduced only by repayments. Because of this, the risk involved with a gearing strategy is that it is possible at some stage that the value of the investment may be less than the outstanding loan.

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 15 of 30

This risk should be considered before entering into any gearing strategy. With a Limited Recourse Borrowing Arrangement, while the assets of the SMSF are protected against any claim to repay a loan, to make a loss of the investment would also see the loss of any loan repayments that have been made over time.

A more detailed description of an LRBA is provided as in the appendices to this plan.

The advantages and risks specific to your paricular situation are outlined in the next sections.

What is a “Withdrawal and Recontribution strategy”?

Currently your superannuation balances have the majority of their funds in what is known as a “taxable component”.

By withdrawing money from your superannuation fund “taxable component” (and not paying any tax on it) then recontributing it back to the fund, you change that amount from being “taxable” to “tax free” in the superannuation fund.

As you have met a “condition of release” you are able to access your superannuation benefits, and can access $XXX,XXX without incurring any tax penalty. This is the amount that you should withdraw from your fund and then re-contribute it straight back into the fund.

This will provide you with a “tax-free component’”, equal to the amount you have withdrawn and recontributed.

Why is my advice appropriate for you?

Advice area: Explanatory information:

To commence a Self Managed Super Fund (SMSF)

This will allow you to be ‘hands on’ with your investments, to make the most of your retirement savings for the future. The structure will also allow you to consider your superannuation benefits as a whole rather than as two isolated policies. It also provides a way of controlling the costs of your superannuation savings. You benefit also from the ability to transfer your direct business real property holdings into your fund.

Establish a Corporate Trustee

A Corporate Trustee provides both a layer of protection for investments, as well as a better ability to isolate the fund investments from investments in your personal name.

Utilise individual member trustee structure

Having members as individual trustees reduces a layer of complexity as there is no requirement to insert another corporate entity into the management of your superannuation fund.

Establish an investment strategy and invest balances accordingly

As we have noted, the establishment of an investment strategy is a requirement for an SMSF. You need to formulate this and document the strategy to be reviewed on a regular basis to ensure it meets your retirement needs

Review your need for personal insurance

Part of formulating your investment strategy is to consider your personal insurance needs. Where the fund you are transferring from has insurance benefits in place, you should calculate whether this amount of cover is required and, if so, how this would be replaced.

Establish binding death benefit nominations

The binding nature of the nomination ensures that your fellow trustees will have to direct the benefit amount of your personal account within the SMSF in the manner you have stated, rather than use their discretion for how any payment of your benefit is to be made.

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 16 of 30

Implement a Limited Recourse Borrowing arrangement

This type of arrangement allows you to accelerate your investment strategy with the use of borrowed funds to purchase an investment larger than the balance of the fund would allow. The fund should also benefit from the deductibility of interest payable for the loan entered into.

Appoint ACCOUNTANCY PRACTICE NAME to provide administration and accountancy services

To ensure the operation of your fund is performed in line with the requirements of legislation we recommend you outsource the administration, taxation and audit of your fund to an accountancy practice that has experience in providing this level of support. They will provide a service to establish the fund and then take care of the operational issues on a regular basis to ensure your compliance with the legislation that governs this area.

Effective means of retirement funding

You have stated that planning for your retirement by contributing funds to superannuation is a wealth creation strategy you wish to pursue. Superannuation benefits are an effective means of providing for future income in retirement, and by making contributions to a superannuation fund you increase the amount that will be available to create income at that time.

Effective use of company profit

Your company is in a position where it will record a profit this financial year, and as you do not require these funds at this time you are prepared to reduce this taxable profit by making superannuation contributions.

You do not expect that you will require use of these profits in the near future to meet any business or personal liquid cash/emergency fund needs.

Effective use of surplus funds

You have current surplus from estimated company profit / personal income over personal expenses / receiving bonus remuneration / liquid asset levels above your foreseeable requirements / the sale of assets that you are prepared to commit to a long term savings program.

Calculated within your contribution limits

The amounts recommended have been calculated to keep your contributions in this financial year at a total amount that is less than your “contributions cap” (the amount you can contribute to superannuation without incurring excess contributions tax)

Create a “tax free” distribution for non-dependent beneficiaries

The taxable component of a superannuation fund is taxed in the event of a death claim when paid to “non-dependants” (this includes adult children). By creating a “tax free component” in your super fund you increase the opportunity to allow beneficiaries to receive their inheritance in full, rather than be reduced by tax.

Provide a non-taxable part of your superannuation pension

Having a “tax-free” component when receiving a pension from your superannuation fund when less than age 60 provides a part of your income that is not taxable. This will provide you a greater net income payable.

Move your SMSF to pension phase

By taking this action your fund will now provide you with income from the benefits accumulated over time.

Further, in pension phase an SMSF pays no tax within the fund itself, so enhancing any returns by the superannuation tax rate.

Finally, as you are able to accept pension income you will also be able to access lump sums from the SMSF as you have met a condition of release by being retired.

Commence pension payments

Payments from a superannuation plan have taxation benefits attached – particularly for those over age 60 with the income being tax-free.

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 17 of 30

Review your investment strategy to support pension phase

Your investment strategy should be reviewed regularly. However, by reviewing it at this stage you will ensure you have the liquidity in the fund to meet pension payments where this was not necessary during the accumulation phase.

Ensuring a high level of diversification will help reduce the risk of any single investment failing and diminishing your account balance, as well as any subsequent income payments in the future.

Adjust any life or other insurance held by the SMSF

By reducing or cancelling personal insurances that are no longer necessary you are reducing the overall cost to the fund. This in turn allows those costs to be used to provide ongoing investment balance to support your income.

Move your SMSF to TTR pension phase

By taking this action your fund will now provide you with income from the benefits accumulated over time to supplement the reduction in income taken as you wind down towards full retirement.

Further, in pension phase an SMSF pays no tax within the fund itself so enhances any returns by the superannuation tax rate.

Commence pension payments

Payments from a superannuation plan have taxation benefits attached – particularly for those over age 60 with the income being tax-free.

Review your investment strategy to support pension phase

Your investment strategy should be reviewed regularly, however by reviewing it at this stage you will ensure you have the liquidity in the fund to meet pension payments where this was not necessary during the accumulation phase.

Ensuring a high level of diversification will also help reduce the risk of any single investment failing and diminishing your account balance and subsequent income payments in the future.

Adjust any life or other insurance held by the SMSF

By reducing or cancelling personal insurances that are no longer necessary you are reducing the overall cost to the fund. This in turn allows those costs to be used to provide ongoing investment balance to support your income.

Balance too low Your SMSF balance has reduced to a point where the ongoing fees for administration are no longer viable

Not confident meeting trustee responsibilities

You find the workload of being a trustee responsible for the ongoing running of the SMSF to be too great a burden, and are not confident you are able to meet the requirements in this area.

Lack confidence to administer

You have found the workload of being a trustee responsible for the ongoing running of the SMSF to be quite complex, and are not confident you are able to meet the requirements in this area.

Health issues You have suffered health issues, and believe that in order to concentrate on maintaining your good health you believe you need to reduce any potential for work pressure or other stress.

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 18 of 30

Does my advice have any disadvantages?

Advice area: Explanatory information:

To commence a Self Managed Super Fund (SMSF)

As trustees of an SMSF you now take responsibility for ensuring the fund is run according to the requirements of the legislation governing superannuation funds.

Establish a Corporate Trustee

A Corporate Trustee can bring an extra layer of complexity to the management of the superannuation fund as it is another entity that has to be dealt with in the terms of the constitution governing the entity, as well as additional reporting and taxation requirements to the SMSF.

Utilise individual member trustee structure

Care must be taken with the use of individual trustees that assets of the SMSF are not confused with the assets of the trustees in their personal names. Also, should at any time an SMSF be faced with having a single trustee, an adjustment to the fund will be required as an SMSF must have at least two individual trustees to operate.

Establish an investment strategy and invest balances accordingly

This document is a legal requirement and must be updated regularly to ensure that any investment of the fund is covered by the investment strategy. If investments are held that are not covered by this strategy the SMSF could be deemed to be non-compliant and incur penalties.

Review your need for personal insurance

Personal insurances in your superannuation fund may not provide a full range of features because of a conflict with the “sole purpose test”. Also, insurance premiums are a cost to the superannuation fund that can deplete member accounts.

Establish binding death benefit nominations

These must be reviewed on a regular basis to ensure that they reflect the wishes of the member as to who they want to receive payment of any death benefit. Nominations should also be confined to dependants as defined by the Australian Taxation Office (ATO) or benefits may be taxed upon passing to a non-dependant beneficiary.

Implement a Limited Recourse Borrowing arrangement

Using this strategy provides a higher level of risk (potential loss) and while there is limited recourse, any payments made on the loan will be forfeited where they could have been retained in the SMSF account balances. This strategy also provides another layer of complexity for the administration and operation of the fund, and must be carefully considered to ensure the fund does not breach compliance and incur taxation penalties.

Appoint ACCOUNTANCY PRACTICE NAME to provide administration and accountancy services

Although trustees may outsource elements of the running operation of the SMSF they still remain responsible for the performance of those duties by the service provider. Trustees will be asked to sign off on minutes of meetings and other documents so you should always be sure to read through any documentation provided to you and ask questions should you be concerned about any element presented or provided by them.

Contributions made to superannuation are preserved

Once a contribution is made to a superannuation fund it is subject to superannuation preservation rules. This means that you cannot access the funds until you reach a “condition of release” – the most common being that you have retired after reaching your “preservation age”

Impact on personal cash flow

By making a contribution to superannuation you are reducing the amount of income available to you to for other purposes such as short- and medium-

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 19 of 30

term goals or current lifestyle expenditure.

Limit on making future after-tax (non-concessional) contributions MUST INCLUDE THIS IF THE BRING FORWARD RULE HAS BEEN APPLIED

In making this recommendation we have applied what is known as the “bring forward” rule. This is where up to three years’ after tax contribution can be made in a single year. By using the three-year limit in a single payment, no further after-tax contribution can be made for that three-year period or tax penalties will apply. If you consider making after-tax contributions during the next three years, it is vital that you seek advice in relation to this.

Cashing current investments can incur fees

To be able to put this strategy into place you will be required to cash in some of your superannuation investment portfolio. This could incur fees and changes (including Capital Gains Tax). Further, depending upon the market value at the time a loss on the investments may be made if they were worth less at the time they were purchased than when you redeem them.

Move your SMSF to pension phase

Care must be taken to maintain your investment balance to support ongoing income. Being in pension phase will no longer allow contributions to be made to the fund that would prop-up the payment of future benefits.

Commence pension payments

Taking more income than is required or accessing lump sums can reduce the ongoing ability of the fund to continue to pay income at the level required to maintain your lifestyle.

Review your investment strategy to support pension phase

The review may give rise to decisions that must be made about relinquishing assets so they are more liquid to meet ongoing needs. Care must be taken also not to be too conservative in your approach so that you diminish the opportunity to have funds to achieve returns needed to support long term income payments.

Adjust any life or other insurance held by the SMSF

Reduction or cancellation of insurance benefits can reduce the ability of an estate to be created in the event of the death of the insured person.

Move your SMSF to TTR pension phase

Care must be taken to maintain your investment balance to support ongoing income. Being in pension phase will no longer allow contributions to be made to the fund that would prop-up the payment of future benefits.

Commence pension payments

Taking income at an earlier age increases the time over which funds will be accessed. This can reduce the ongoing viability of the fund to continue to pay income at the level required to maintain your lifestyle.

Review your investment strategy to support pension phase

The review may give rise to making a decision about relinquishing assets so they are more liquid to meet ongoing needs. Care must be taken also not to be too conservative in your approach so that you diminish the opportunity to have funds to achieve returns needed to support long-term income payments.

Adjust any life or other insurance held by the SMSF

Reduction or cancellation of insurance benefits can reduce the ability of an estate to be created in the event of the death of the insured person.

There will be fees involved

In winding up the fund, there will be fees payable to cover the costs of administering this process if you engage someone to do this for you.

If you are moving your funds to a commercial superannuation plan, please

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 20 of 30

be sure that you have an understanding of the fees payable in the new fund.

Change to Centrelink assessment of your entitlements (account based pension)

As your account based pension was started prior to 1 January 2015, Centrelink will assess your new fund in a different way – this may have the effect of reducing your Centrelink income entitlements. You should contact Centrelink to determine what effect this will have for you.

Change to Centrelink assessment of your entitlements (non-super)

Moving your assets from the superannuation environment will cause a change in the way that Centrelink assess your entitlements. You should contact Centrelink to determine what effect this will have for you.

Non-superannuation assets are subject to personal tax

If it is your intention to take your assets out of the superannuation environment, please be aware that investments outside superannuation will be subject to Capital Gains Tax on any future growth, as well as having the income taxed at your marginal rate (no tax is paid from the income you receive from the SMSF).

Non-superannuation assets can be caught by your estate

If it is your intention to totally remove your benefits from the superannuation system, any benefit nominations you had in place will cease to exist. You should be aware that by no longer being part of the superannuation environment you risk the assets from your estate being challenged, even when you have a will in place.

Withdrawal amount will be subject to tax

If it is your intention to totally remove your benefits from the superannuation system, we calculate that there will be a tax penalty applied to the withdrawal. We calculate that amount as $XXXXX – the way this has been calculated is demonstrated in the appendices to this document.

What other alternatives were considered?

Advice area: Explanatory information:

Retain your current superannuation arrangements

Your current superannuation plans don’t allow you the flexibility you have stated that you want from your superannuation fund. It also allows little control over the fees and charges that are levied, nor will it allow the opportunity to include your Business Real Property as part of your investment strategy.

You have also determined that you would like to pursue a strategy to borrow for investment within the superannuation environment – your current fund will not allow this strategy to take place.

Move your current superannuation benefits to a different commercially available superannuation fund

While there are many fund options available in the market place that provide flexibility with investment choice, these can be high in fees for greater superannuation balances. By having your own SMSF you can access investments directly without management fees being charged, as well as controlling the administration costs with a flat fee being charged for this activity.

As you wish to pursue a borrowing strategy in your superannuation, we are not aware of commercially available superannuation plans that will allow this to be part of the fund investment strategy.

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 21 of 30

Borrow for investment outside of superannuation

Entering into a gearing strategy outside the superannuation environment has definite advantages for the ability to reduce taxable income for higher income earners. However, funds may be limited in terms of being able to provide a deposit on any borrowings that could help reduce any loan taken and allow earlier repayment of the loan in full. Further, upon repayment of the loan and entering into retirement, the benefits of tax concessions available to superannuation funds in pension phase are attractive – the LRBA strategy will see any property inside superannuation at that time without having to transfer the property and incur charges (Capital Gains Tax, stamp duty).

Reduce profit by the pre-payment of other expenses

You have informed me that at this time there are no other business expenses you need to incur that would require you to use these funds for such a purpose other than making contributions to superannuation.

Retain funds for short term goals / immediate lifestyle expenses

You have informed me that in your current situation you do not require funds for short term purposes including emergency cash holdings or other lifestyle needs.

Retain your current superannuation components

By taking no action you would not affect your superannuation benefits as they stand, however by acting on the recommendation you are providing your estate with greater flexibility for distribution to those who are not identified as “dependants”.

Maintain your investments in the accumulation phase

Benefits held in the accumulation phase of superannuation are subject to tax on income and capital gains. Also, withdrawals are not automatic and on a regular basis. Moving to pension phase will see the fund pay no tax on the income or capital gains from the assets supporting the pension. Also, withdrawals can be established on a regular basis without the need to apply for an amount to be withdrawn each time.

Maintain your investments in the accumulation phase

As you are intending to continue to work, you have not met a “condition of release” for a superannuation fund to allow you to access funds, other than by the Transition to Retirement income stream recommended here. If your income is reduced by working less hours, to maintain your superannuation in its current form will not allow you access to funds to help reduce any income shortfall.

Retain your current arrangements (low balance)

While you have enjoyed the benefits of running your own superannuation fund, the costs of its ongoing administration, when considered as a percentage of the overall assets it is very high. Commercial arrangements exist that will provide the ongoing administration at a much lower percentage/cost, and will also remove you from the responsibility of having to act as trustee.

Retain your current arrangements (no time)

While you have enjoyed the benefits of running your own superannuation fund, it is a requirement for members to be active in the running of their fund. This does take time and attention, and as you believe you cannot devote sufficient time to this it would be better to be a member of a superannuation fund that does not require your time to meet trustee responsibilities.

Retain your current arrangements (too complex)

While you have enjoyed the benefits of running your own superannuation fund, it is a requirement for members to be active in the running of their fund. The legislation surrounding superannuation is complex and constantly changing, and while we are happy to assist you in the operation of your fund, trustees of superannuation funds must ultimately be

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 22 of 30

responsible. If you do not have the confidence that you can meet these requirements it is prudent to no longer be part of this type of arrangement.

Retain your current arrangements (health)

While you have enjoyed the benefits of running your own superannuation fund, it is a requirement for members to be active in the running of their fund. With the concerns you have expressed for your health and the need to limit any stress or worry, it would be prudent for you to remove yourself from the trustee responsibilities and be part of a superannuation fund that does not require your input in this area.

Consequences of replacing one financial product with another

A full analysis of the comparison of costs of current superannuation plans compared to the costs associated with the recommended SMSF is provided in the appendices to this SOA. However, the main points for consideration of this aspect are:

Member Fees and charges Lost Benefits Other

Considerations

Member Name

Member Name

Member Name

Member Name

OR

This recommendation does not involve the replacement of any financial product.

OR

These recommendations do not recommend the replacement of any financial product. They are simply for the adjustment of your Superannuation Fund to move it from accumulation to pension phase. Costs and charges will remain the same as you are continuing to use the same services for administration and audit.

OR

This recommendation is only concerned with whether or not your superannuation benefits should remain in the current SMSF arrangements. It does not give any representation about an alternative fund.

INCLUDE IF GOING TO NEW SUPER FUND - If it is your intention to roll your SMSF member accounts into another superannuation fund, we suggest that you consider the costs of an alternative. These costs include:

Entry fees

Administration fees

Product/Investment management fees

Ongoing advice fees

Other management fees (these can vary with the product provider)

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 23 of 30

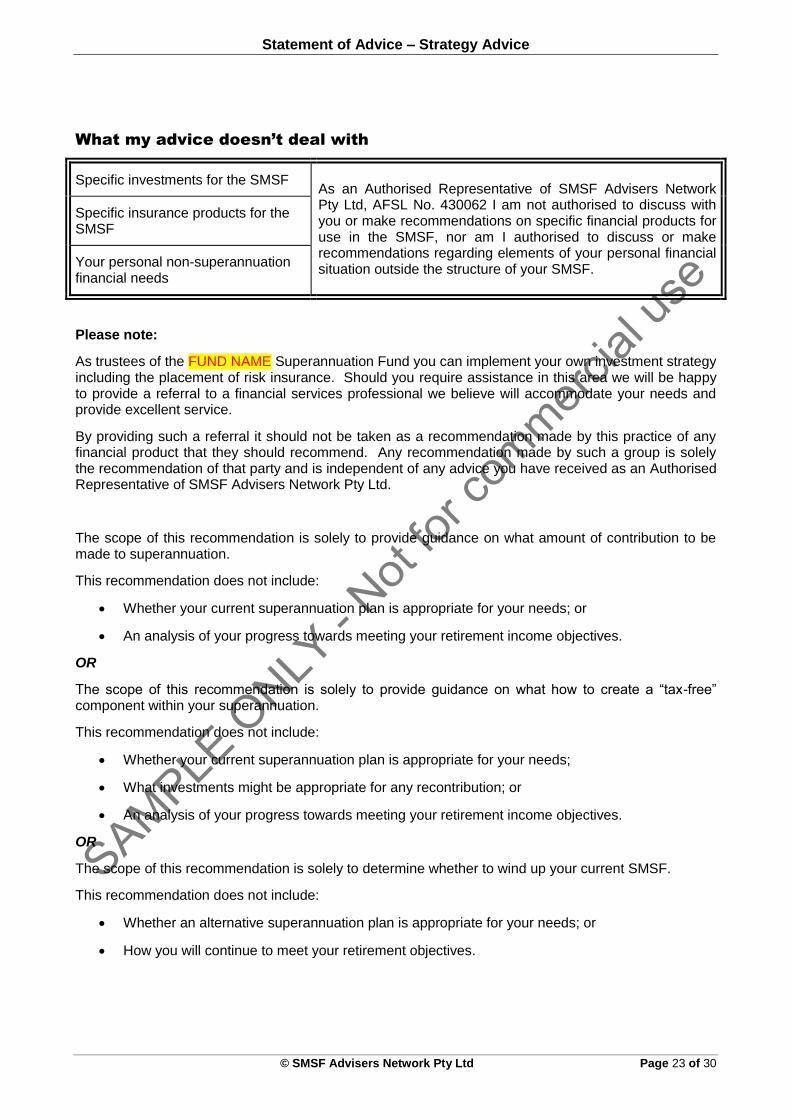

What my advice doesn’t deal with

Specific investments for the SMSF As an Authorised Representative of SMSF Advisers Network Pty Ltd, AFSL No. 430062 I am not authorised to discuss with you or make recommendations on specific financial products for use in the SMSF, nor am I authorised to discuss or make recommendations regarding elements of your personal financial situation outside the structure of your SMSF.

Specific insurance products for the SMSF

Your personal non-superannuation financial needs

Please note:

As trustees of the FUND NAME Superannuation Fund you can implement your own investment strategy including the placement of risk insurance. Should you require assistance in this area we will be happy to provide a referral to a financial services professional we believe will accommodate your needs and provide excellent service.

By providing such a referral it should not be taken as a recommendation made by this practice of any financial product that they should recommend. Any recommendation made by such a group is solely the recommendation of that party and is independent of any advice you have received as an Authorised Representative of SMSF Advisers Network Pty Ltd.

The scope of this recommendation is solely to provide guidance on what amount of contribution to be made to superannuation.

This recommendation does not include:

Whether your current superannuation plan is appropriate for your needs; or

An analysis of your progress towards meeting your retirement income objectives.

OR

The scope of this recommendation is solely to provide guidance on what how to create a “tax-free” component within your superannuation.

This recommendation does not include:

Whether your current superannuation plan is appropriate for your needs;

What investments might be appropriate for any recontribution; or

An analysis of your progress towards meeting your retirement income objectives.

OR

The scope of this recommendation is solely to determine whether to wind up your current SMSF.

This recommendation does not include:

Whether an alternative superannuation plan is appropriate for your needs; or

How you will continue to meet your retirement objectives.

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 24 of 30

Section 3: What else you need to know

This section:

Tells you about any fees that I will receive;

Explains what product fees you will pay; and

Answers other questions you might have about my advice.

Please also make sure you have read the Financial Services Guide (FSG) I have provided and be sure to ask me any questions you might have in relation to any of this.

What are my fees?

My fee for the preparation of this advice is $XXXX.XX (including GST).

Please note that as I am not authorised by my licensee (SMSF Advisers Network Pty Ltd) to recommend specific financial products to you I cannot receive commissions or other forms of payment or soft dollar benefits from product providers.

Please also be aware that my licence fee for SMSF Advisers Network Pty Ltd is paid on a fixed fee basis – there is not a set amount of any income received from fees received that they retain.

What product fees will I pay?

The cost of establishment of these arrangements will be charged by ACCOUNTANCY PRACTICE NAME. This cost will be $XXXX.XX (including GST). Please be aware that this accounting practice is a business that is associated with the provision of this advice. As a result, I will benefit from the payment of fees to that business in addition to the fees charged for this advice.

If you implement your own investment strategy, you should check to see what any product costs may be incurred – these can include brokerage, stamp duty, etc.

Should you receive recommendations from another financial services professional for what they deem to be suitable products for your needs, any costs for those products should be disclosed by that professional. Such costs are not part of the advice given in this recommendation and we hold no responsibility for those costs should you choose to implement the advice given by a separate party.

What steps do I take next?

Step required Who responsible Due by

Sign the Authority to Proceed at the rear of this document

Engage ACCOUNTANCY PRACTICE NAME to administer the implementation of the recommended structures

Arrange for transfer of the recommended contribution amount to your fund

Arrange for the amount recommended to be withdrawn from your superannuation fund and re-

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 25 of 30

contributed immediately

Engage ACCOUNTANCY PRACTICE NAME to administer the process to transfer your superannuation benefit from the accumulation phase to pension phase.

Instigate payment of the amount of regular income recommended

Engage ACCOUNTANCY PRACTICE NAME to administer the wind up of the SMSF

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 26 of 30

Other questions you might have

Am I restricted to an approved product list?

As noted previously in this section, I am not authorised by SMSF Advisers Network to recommend any specific financial product other than a Self Managed Superannuation Fund structure.

Is SMSF Advisers Network Pty Ltd associated with any recommended products?

The SMSF Advisers Network Pty Ltd is an entity owned by the National Tax & Accountants’ Association (NTAA). This group specialise in providing services to accounting groups for education and has now implemented this AFSL to support its members. The NTAA has no arm that provides financial products and therefore does not provide products to be included on an approved product list.

Does my advice have a time limit?

Yes, my advice should be revisited if it is not implemented within 28 days of the date on the cover of this SOA.

Is your information protected?

Yes. Your information is stored and not given to any party outside the SMSF Advisers Network unless the law says that we must.

Disclaimer

No warranty as to correctness is given and no liability is accepted for any error, or omission, or any loss, which may arise from relying on this data. Every effort has been made to assure the highest reasonable degree of accuracy in your financial plan. However, due to the dynamic nature of our economic and tax environments, no guarantees or assurances can be given regarding the profitability or tax benefits of any investment.

This plan is only as accurate as the information on which it was based. If the data originally supplied to us is incorrect or incomplete, the plan will reflect these inaccuracies, and these errors will project into the future at a magnified rate. Certain assumptions made by us, or you, may also limit the accuracy of the data.

Where tax benefits are illustrated, they are based on the best information currently available.

Various proposals are made from time to time to change the tax laws, and it seems probable that many of our current tax laws will undergo changes during the years illustrated in this financial plan. Some of these proposals, if enacted, might have a serious adverse effect on the tax consequences of some of the investment strategies proposed. On the other hand, some proposals may significantly enhance your position if enacted.

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 27 of 30

Authority to Proceed

I/We, CLIENT NAMES, having read the Statement of Advice (SOA) dated DATE and prepared by ADVISER NAME acknowledge:

The information provided in this document is accurate and reflects my/our current circumstances;

I/We understand and agree that the risk profile recommended meets my/our concerns and requirements;

That the recommendations given in this Statement of Advice meet our needs and objectives as stated in this document;

That the recommendations given are based on legislation current at the time of making these recommendations;

That because legislation is subject to change, these recommendations should be reviewed if not implemented within 28 days from the date on the cover of this SOA;

I/We understand that the recommendations made in this Statement of Advice are for our use only and should not be passed on as recommendations suitable to other parties;

That the recommendations made in this Statement of Advice, unless implemented in full as described, may not meet the desired outcomes stated as the goals and objectives described; and

That where a referral has been given to another party to seek recommendation for investment and personal insurances, any recommendation made by that party is not the recommendation of ADVISER NAME.

The recommendation in this SOA is for:

Establishment of FUND NAME Superannuation Fund

The trustee is to be CORPORATE TRUSTEE NAME / the individual members as trustees

Establishment of a Limited Recourse Borrowing Arrangement as part of your SMSF structure

The recommendation in this SOA is for contributions of the following amounts to be paid to your superannuation fund:

Member Contribution ($) Contribution type

Member 1 Name Non- / Concessional

Member 2 Name Non- / Concessional

Member 3 Name Non- / Concessional

Member 4 Name Non- / Concessional

The recommendation in this SOA is for withdrawal and recontribution of the following amounts for your superannuation fund:

Member Withdrawal/Recontribution ($)

Member 1 Name

Member 2 Name

Member 3 Name

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 28 of 30

Member 4 Name

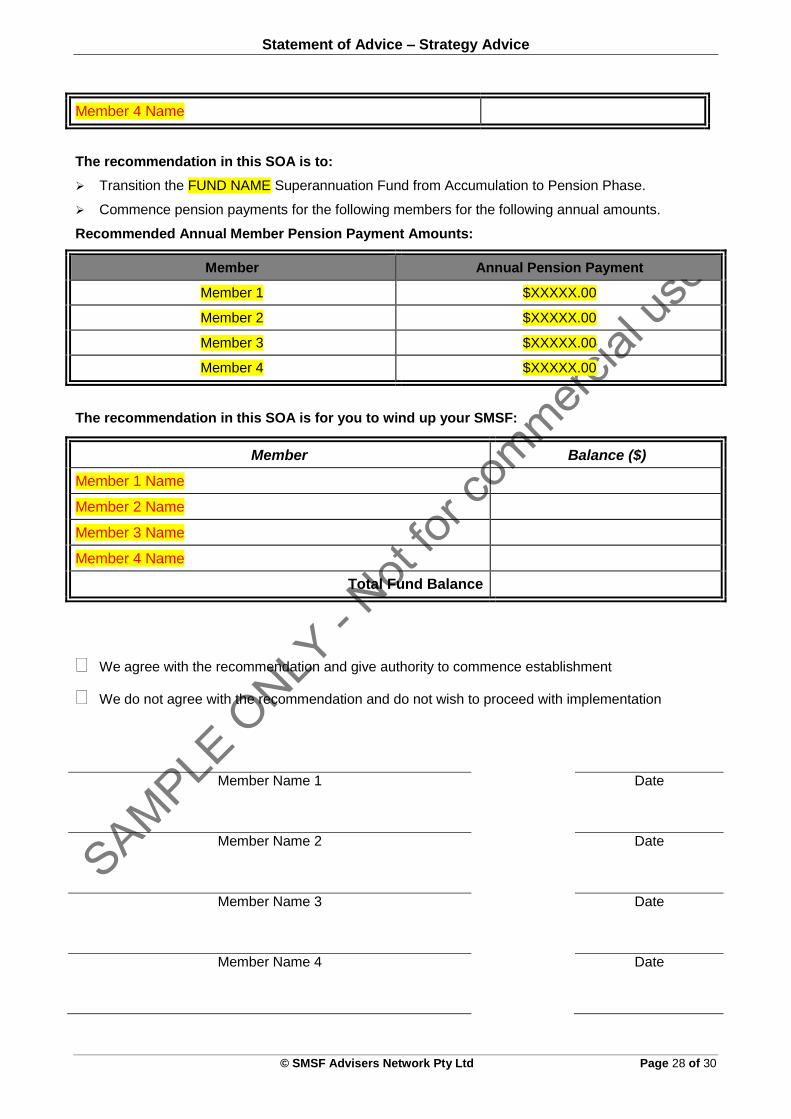

The recommendation in this SOA is to:

Transition the FUND NAME Superannuation Fund from Accumulation to Pension Phase.

Commence pension payments for the following members for the following annual amounts.

Recommended Annual Member Pension Payment Amounts:

Member Annual Pension Payment

Member 1 $XXXXX.00

Member 2 $XXXXX.00

Member 3 $XXXXX.00

Member 4 $XXXXX.00

The recommendation in this SOA is for you to wind up your SMSF:

Member Balance ($)

Member 1 Name

Member 2 Name

Member 3 Name

Member 4 Name

Total Fund Balance

We agree with the recommendation and give authority to commence establishment

We do not agree with the recommendation and do not wish to proceed with implementation

Member Name 1 Date

Member Name 2 Date

Member Name 3 Date

Member Name 4 Date

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 29 of 30

Adviser Name Date

Statement of Advice – Strategy Advice

© SMSF Advisers Network Pty Ltd Page 30 of 30

APPENDIX – DISCLOSURE OF RISKS: MOVING TO SMSF

When moving from a commercial superannuation fund (what is referred to as a “public offer fund” or a workplace “corporate” fund, there are certain items that should be considered when making your decision to manage your own superannuation fund.

These considerations should be taken alongside the benefit of managing your own superannuation arrangements. These points are:

Conduct and disclosure obligations – in giving you this advice I am doing so as an authorised representative of an Australian Financial Services Licensee. After providing you with my Financial Services Guide, I have made this recommendation that I believe to be in your best interests, based on an assessment of your current position and financial objectives.

Lack of statutory compensation – in moving from a public offer type fund, your superannuation arrangements will no longer be regulated by the government boy, the Australian Prudential Regulation Authority (APRA). By removing yourself from the APRA framework you no longer have available their compensation benefits for any theft or fraud on the fund. In addition, there will not be any compensation available under superannuation laws if the SMSF suffers any loss from theft or fraud in any of the fund’s underlying assets.

Insurance – Consideration should be given to any insurance benefits that may have been available with your previous plan. By moving from this fund this valuable cover may be lost, so a member should assess whether they need to replace this cover and if replacement cover should be included as part of the SMSF

PLEASE NOTE: I am not authorised to provide advice in relation to insurance needs or product. As an important part of your personal planning I recommend that you seek advice about this. Please let me know if you would like a referral to an insurance professional to assist your assessment of this area.

Lack of access to complaints mechanisms – members of commercially available superannuation plans have access to complaints mechanisms, such as the Superannuation Complaints Tribunal. Members of an SMSF do not have access to such schemes. However complaints about any advice given can be made to the licensee responsible for the advice, and if necessary the Credit and Investments Ombudsman (the compliant scheme that the SMSF Advisers Network is a member of).

Management obligations – an SMSF is not a “set and forget” operation. Becoming a trustee of an SMSF requires attention and ongoing management to ensure that the fund operates according to the requirements of superannuation regulations. While we are there to assist and guide you, ultimately the members as trustees are responsible for the SMSFs operations. This will require the members to ensure they have the time and skills required to meet these obligations.

Development of an investment strategy – superannuation law requires trustees to develop an investment strategy to meet the SMSF members retirement needs. This should be updated on a regular basis and must reflect the investments held by the SMSF. This document should also record consideration of a member’s personal insurance needs, and whether the fund should include personal insurance cover arrangements.

While all these points should be considered with any change to your current superannuation arrangements, I believe that an SMSF would suit your personal needs and provide benefits for the provision of your retirement income funding arrangement.