state of industry 20i7 report - nepra.org.pk of industry reports/state of industry... · 5.2...

TRANSCRIPT

STATE OF INDUSTRYREPORT 20

I7

NATIONAL ELECTRIC POWERREGULATORY AUTHORITY

i

CONTENTS

FOREWORD 011 EXECUTIVE SUMMARY 05

1.1 Installed Power Generation Capacity 051.2 Power Balances 05

1.2.1 NTDC System 051.2.2 K-Electric Limited System 06

1.3 Issues of Power Generation Additions 071.3.1 Capacity and Energy Mix 071.3.2 Impact of Capacity Additions 09

1.4 National Electricity Policy and Plan 111.5 Performance of Generation Sector 11

1.5.1 Public Sector (GENCOs and Hydel) 111.5.2 Private Sector (Independent Power Producers) 13

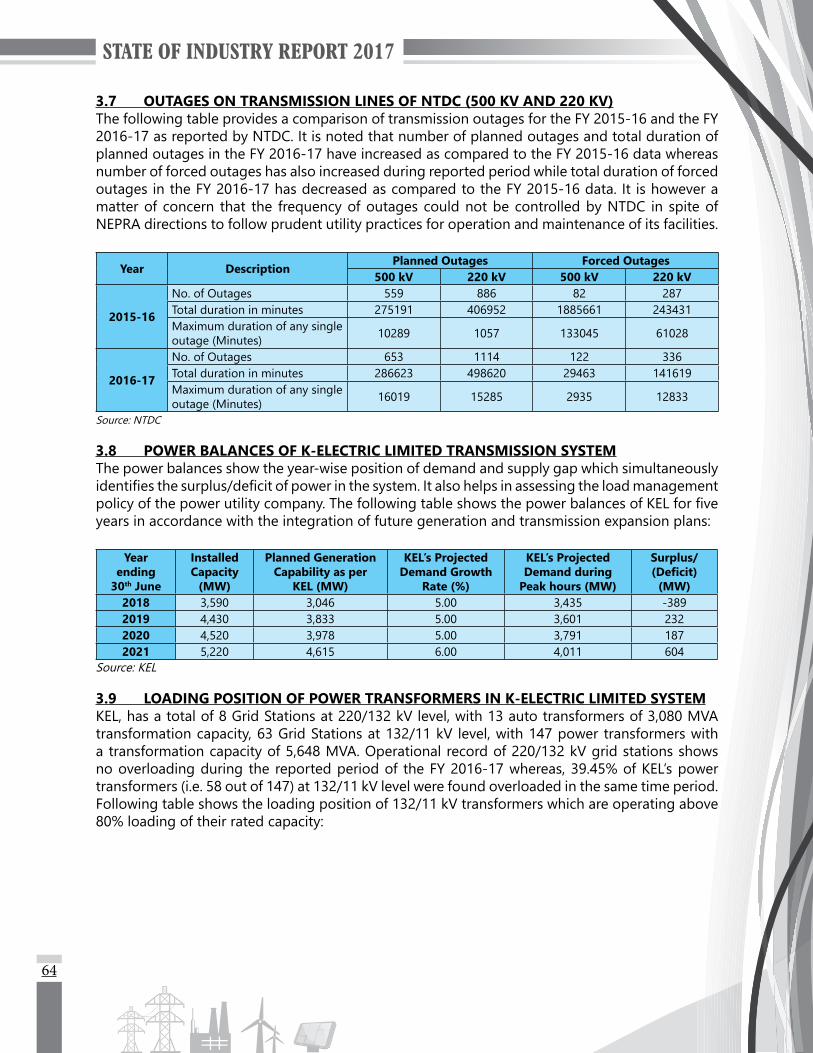

1.6 Transmission System 131.6.1 Outages on NTDC Transmission Lines (500 kV and 220 kV) 13

1.7 Overloading in DISCOs’ System 141.7.1 Loading Position of Power Transformers 141.7.2 Loading Position of 11 kV Feeders 141.7.3 Loading Position of Distribution Transformers 151.7.4 Province-wise Loading Positions 15

1.8 Transmission and Distribution Losses of DISCOs 161.9 Recovery Position of DISCOs 17

1.9.1 Recovery Position of Main Categories of Consumers 171.10 Performance of K-Electric Limited 18

1.10.1 Loading Position of Power Transformers, 11 kV Feeders and Distribution Transformers 19

1.10.2 Recovery Position of K-Electric Limited 191.11 The Regulation of Generation, Transmission and Distribution of Electric Power

(Amendment) Act, 2018 20

1.11.1 Major Amendments 201.11.2 Challenges 20

1.12 Energy, Environment and Sustainable Development 211.13 Comprehensive Reduction and Elimination of Polychlorinated Biphenyls 211.14 Rationalization of Generation Tariff Parameters 221.15 Review of Rate of Return 231.16 Industry – Academia Collaboration 231.17 Conclusions 231.18 Recommendations 24

2 PERFORMANCE OF GENERATION SECTOR 292.1 General 292.2 Installed Capacity and Electricity Generation 292.3 Hydropower 30

2.3.1 Power Purchase Agreements/Energy Purchase Agreements 302.3.2 Competitive Bidding of Hydropower Projects 30

ii

2.3.3 Performance Monitoring of Hydropower Projects 302.3.4 Implementations of Authority’s Direction 31

2.4 Overview of Public Sector GENCOs 312.4.1 Jamshoro Power Company Limited 312.4.2 Central Power Generation Company Limited 312.4.3 Northern Power Generation Company Limited 322.4.4 Lakhra Power Generation Company Limited 32

2.5 Independent Power Producers 322.6 Nuclear (CHASNUPP-I, II & III and KANUPP) 322.7 Renewables 33

2.7.1 Wind 332.7.2 Solar 332.7.3 Bagasse 332.7.4 Bagasse/Coal 33

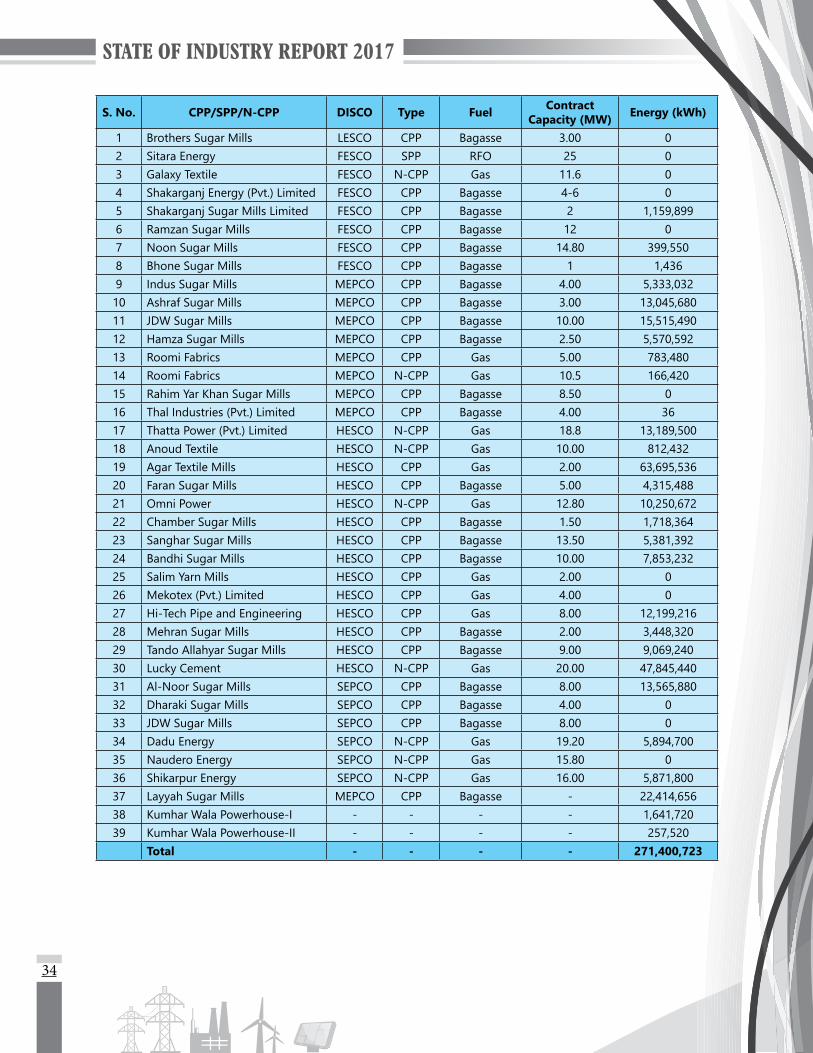

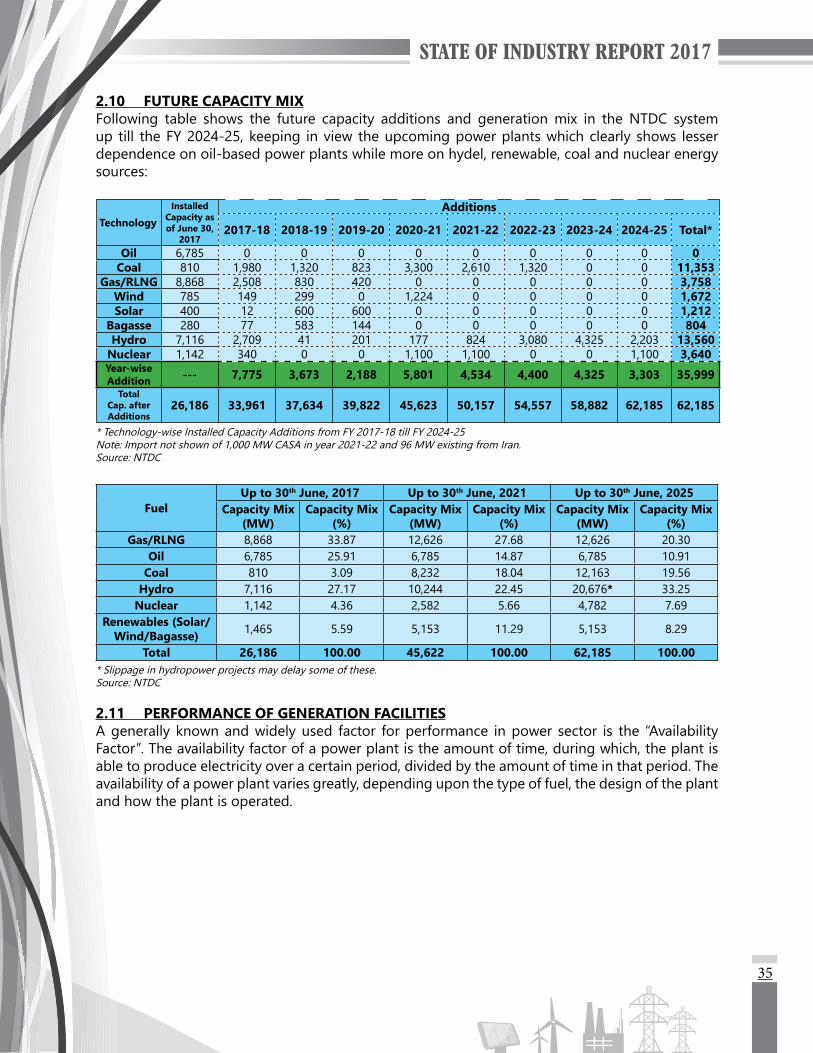

2.8 K-Electric Limited 332.9 Electricity Purchases from SPPs/CPPs/N-CPPs 332.10 Future Capacity Mix 352.11 Performance of Generation Facilities 35

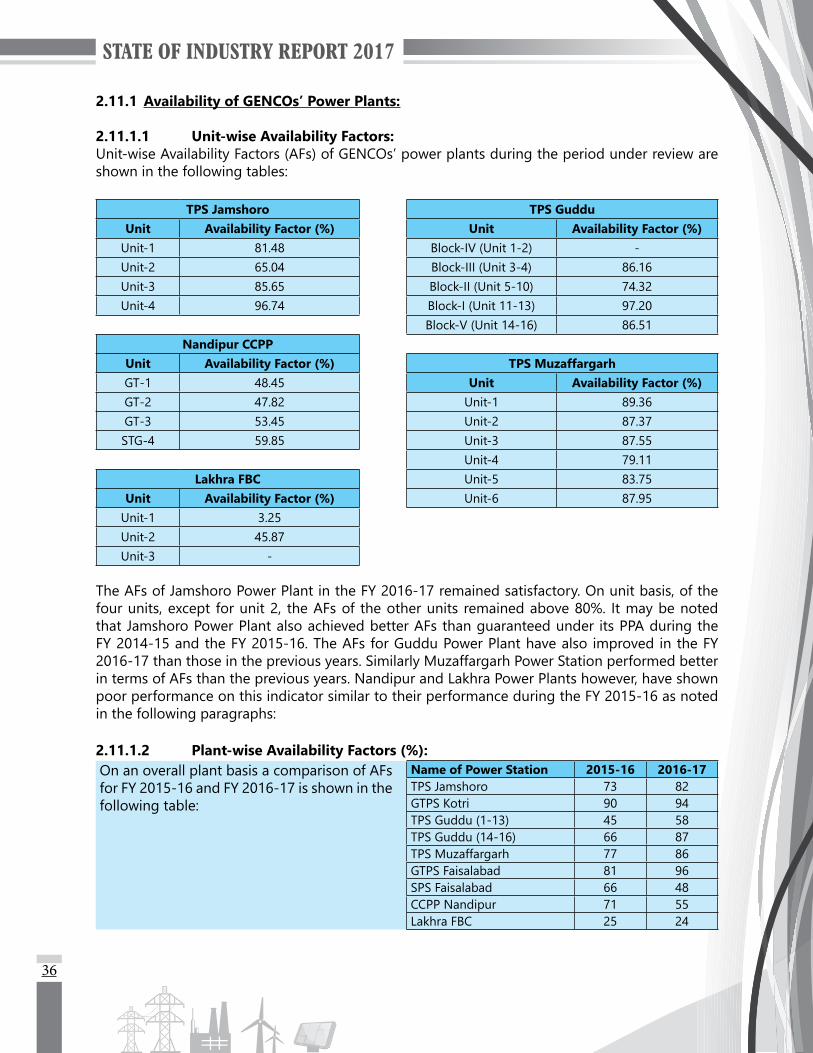

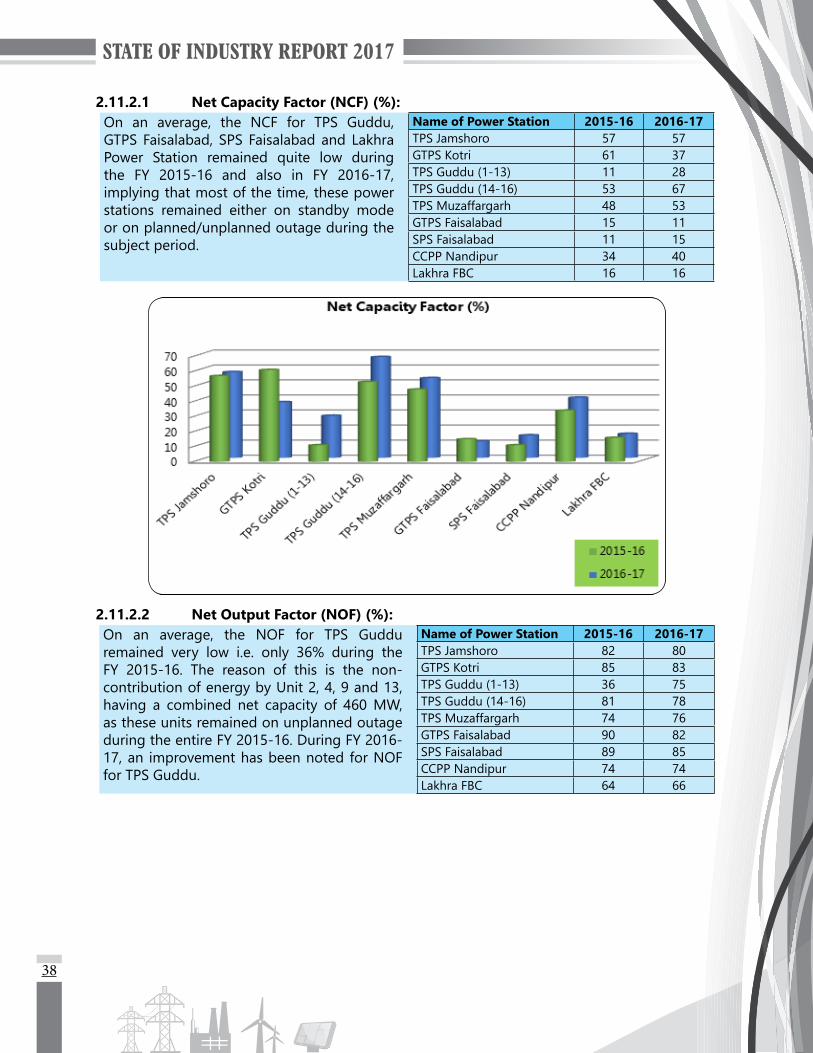

2.11.1 Availability of GENCOs’ Power Plants 352.11.2 Performance of Generation Facilities under NEPRA Performance Standards

(Generation) Rules, 200937

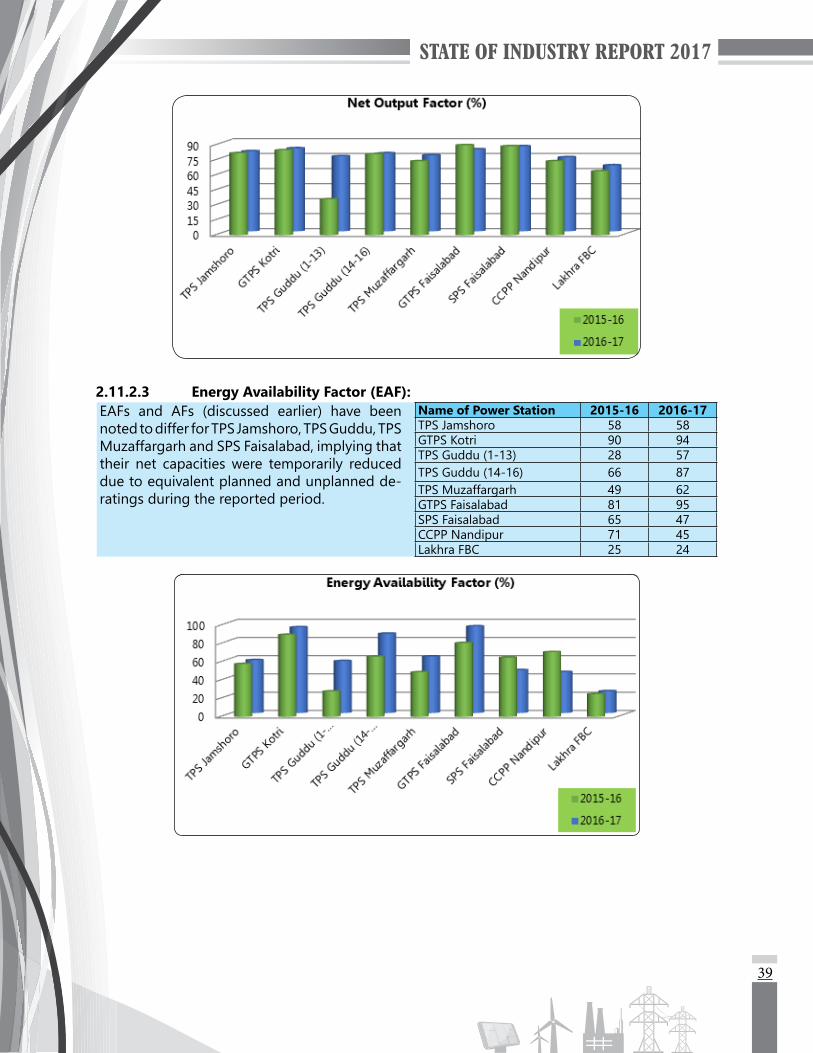

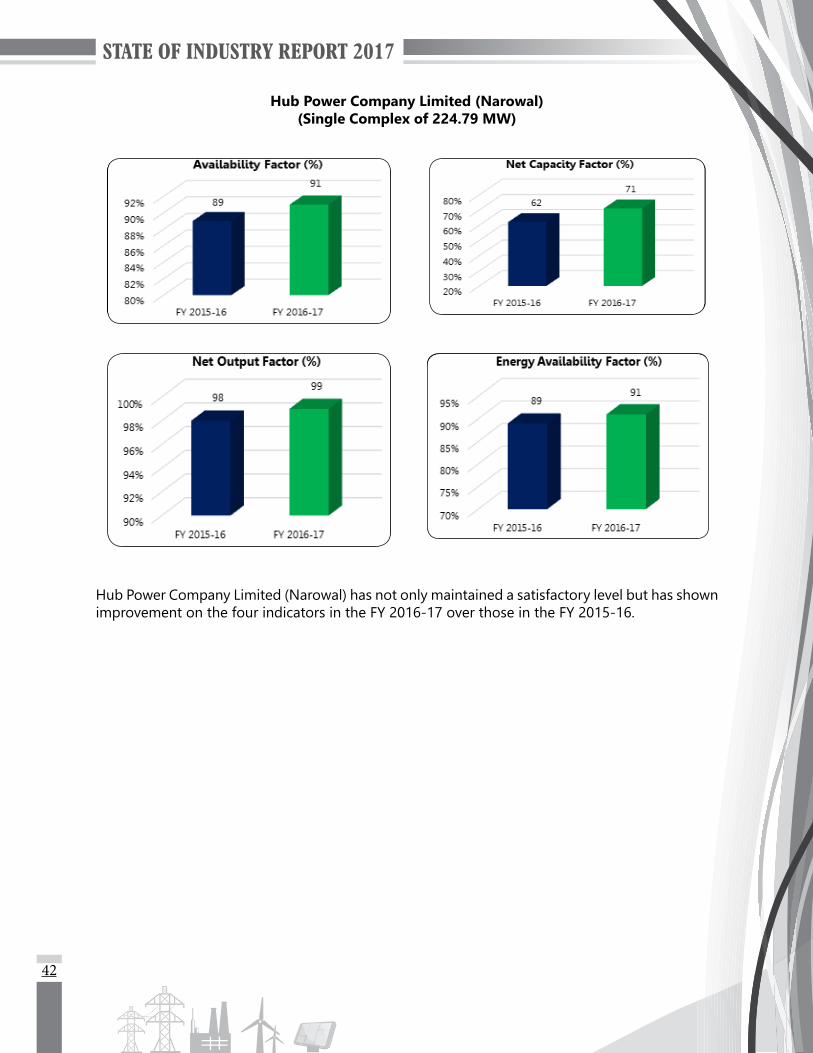

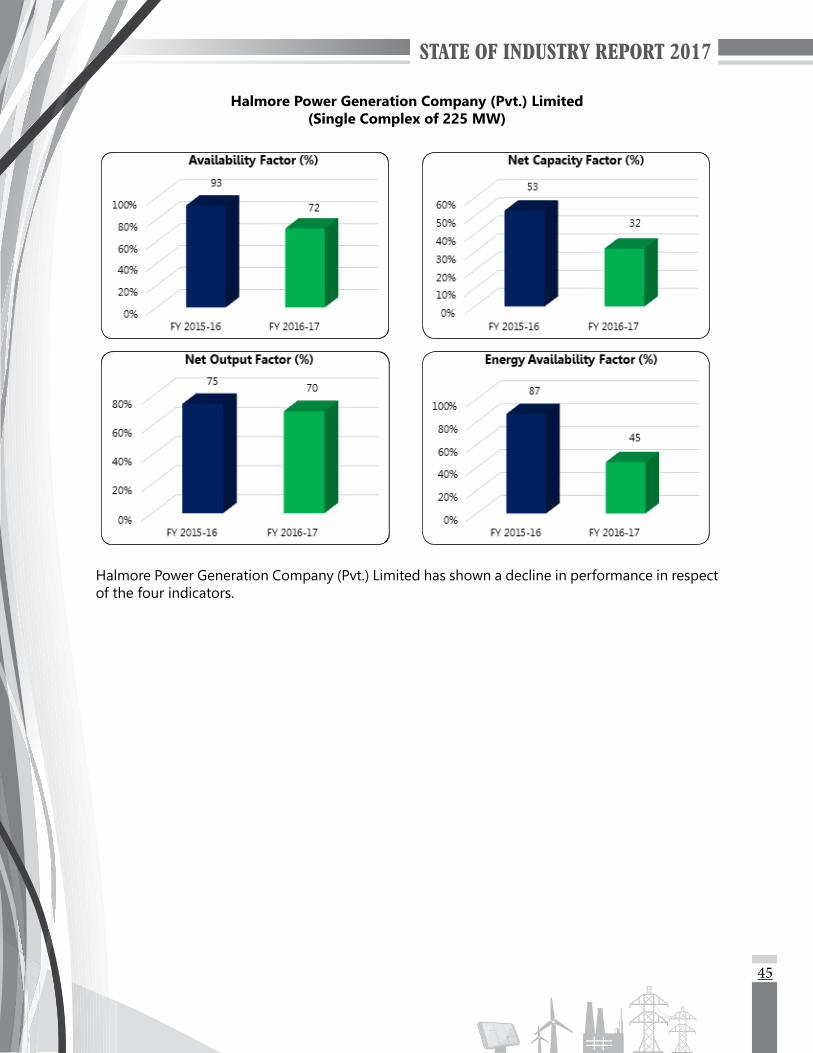

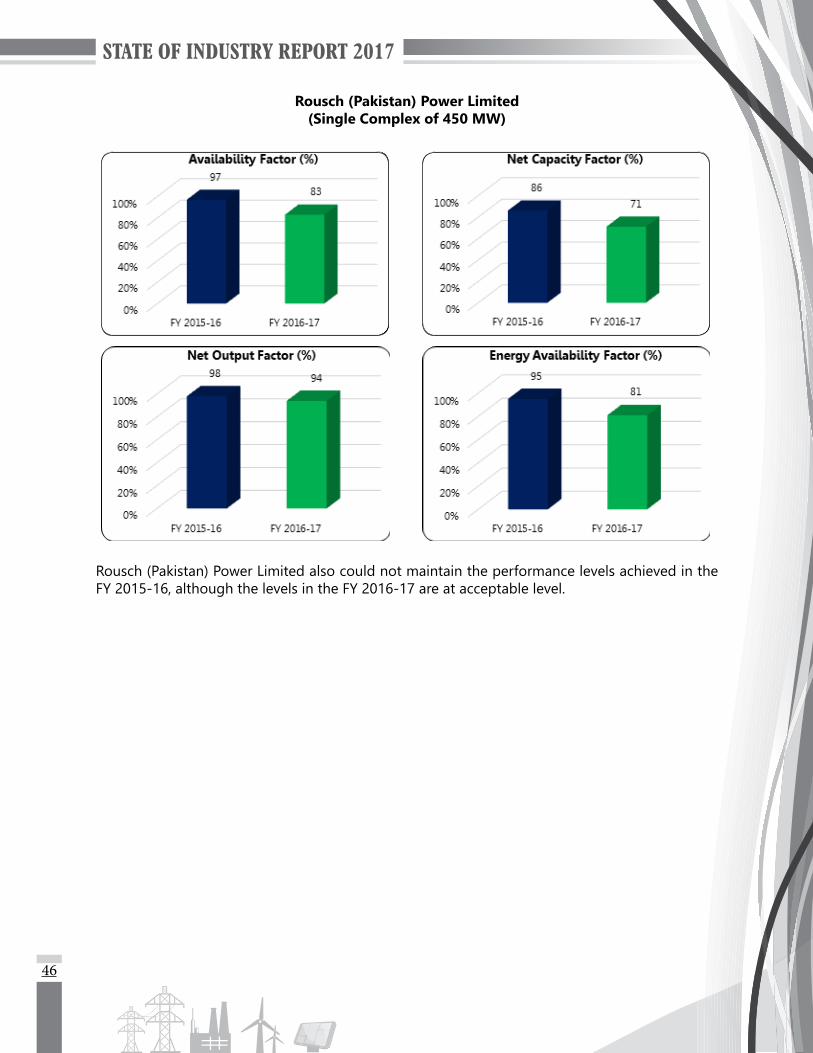

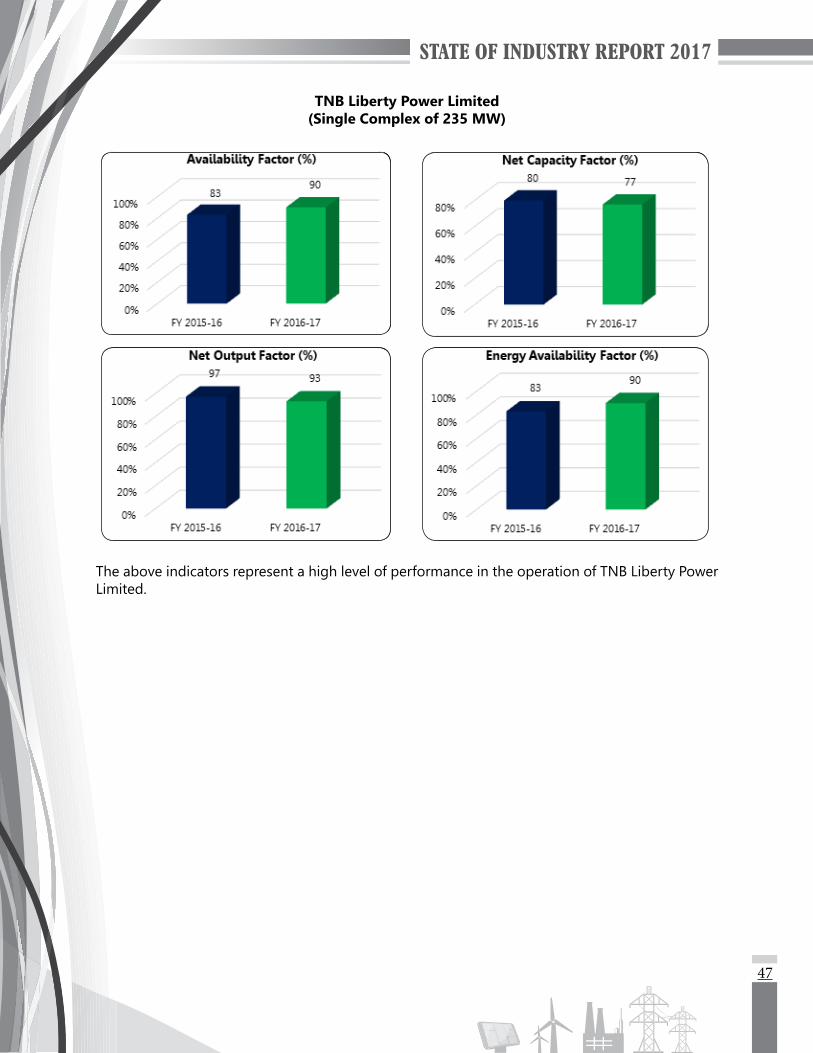

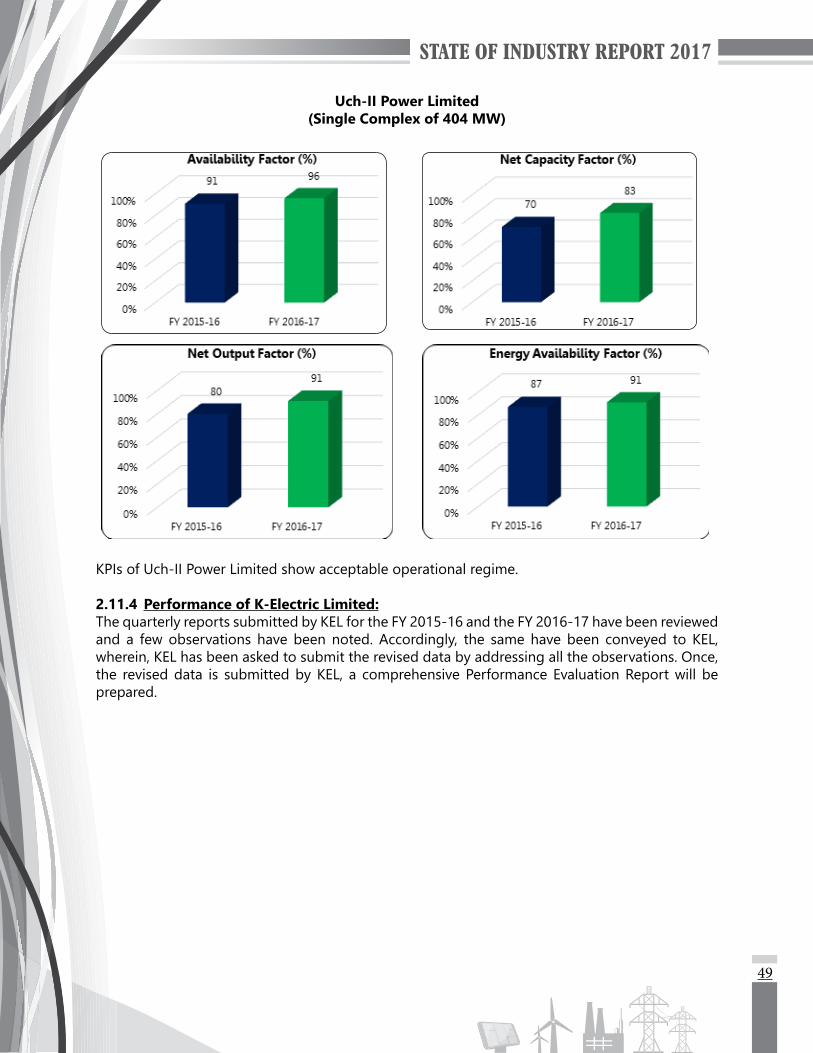

2.11.3 Performance of Independent Power Producers 392.11.4 Performance of K-Electric Limited 49

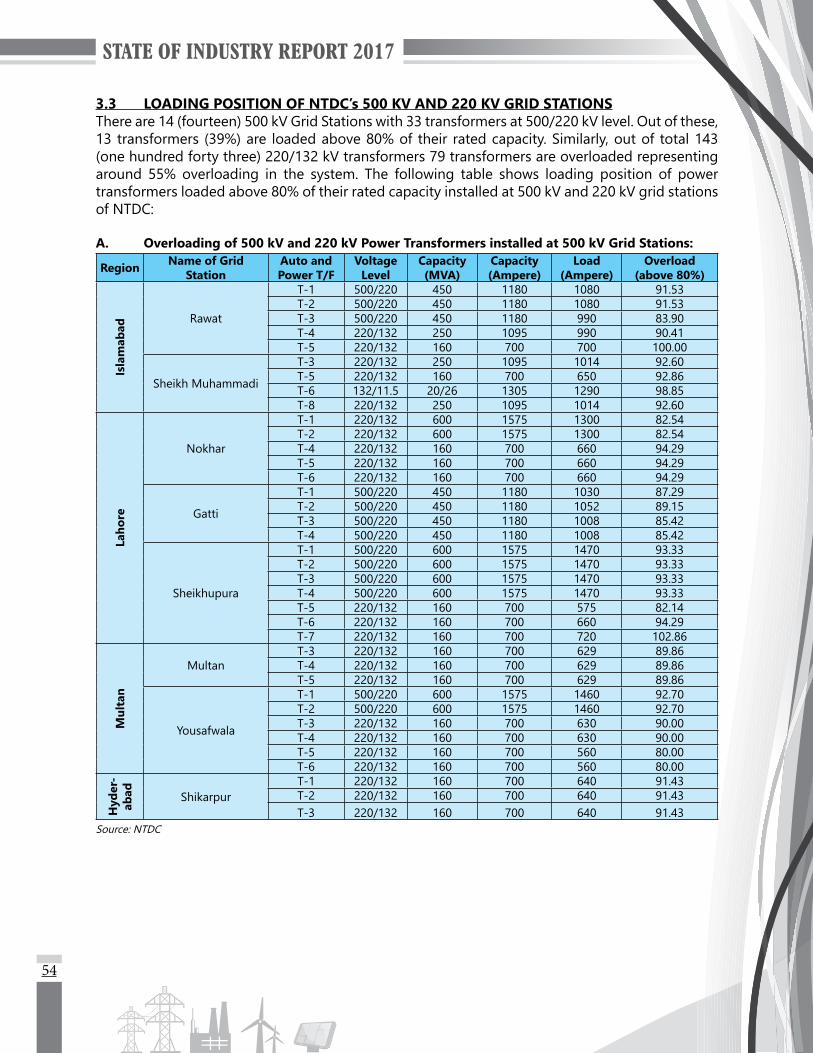

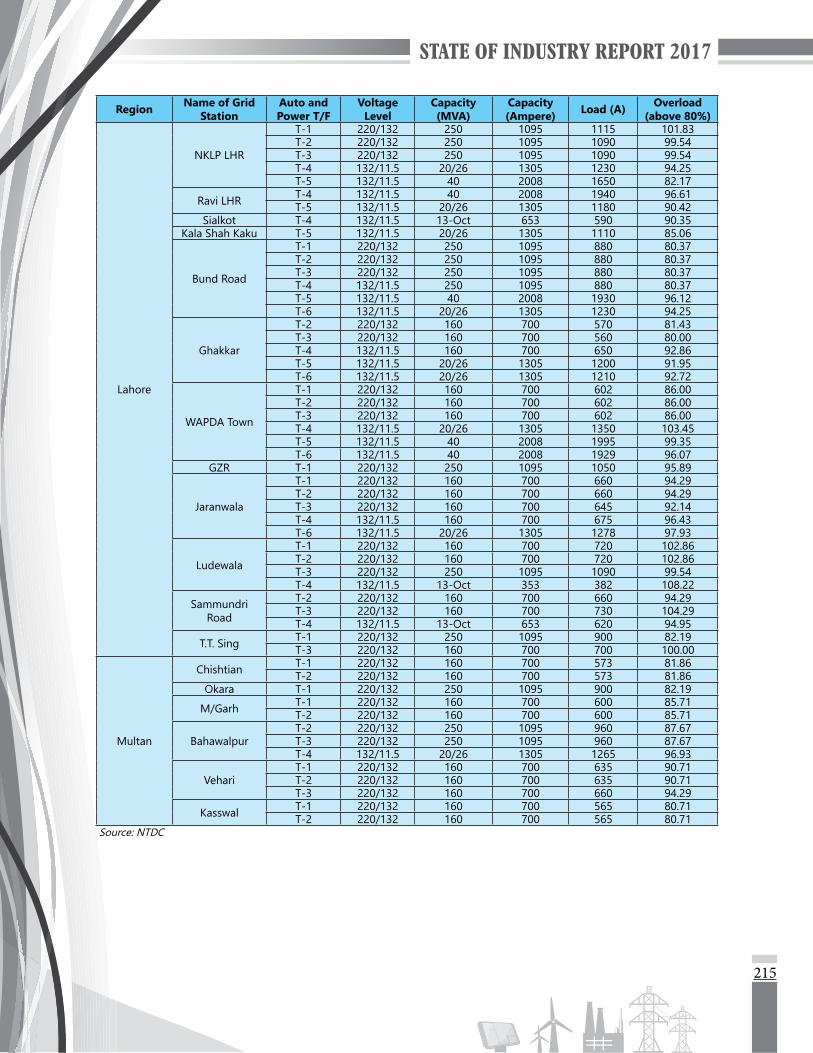

3 PERFORMANCE OF TRANSMISSION SECTOR 533.1 General 533.2 Power Balances of NTDC System 533.3 Loading Position of NTDC’s 500 kV and 220 kV Grid Stations 543.4 Constraints in NTDC System 57

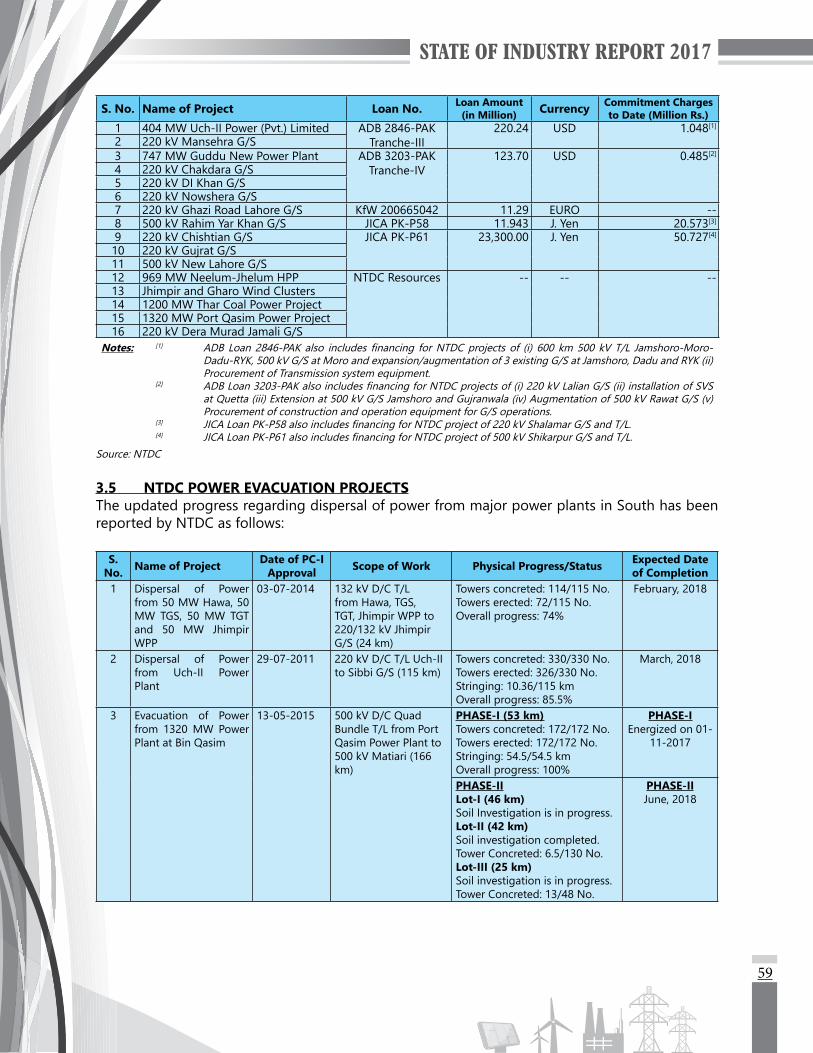

3.4.1 Current Status of Interconnection Arrangements 573.4.2 Project-wise Cost Over-run 573.4.3 Commitment Charges 58

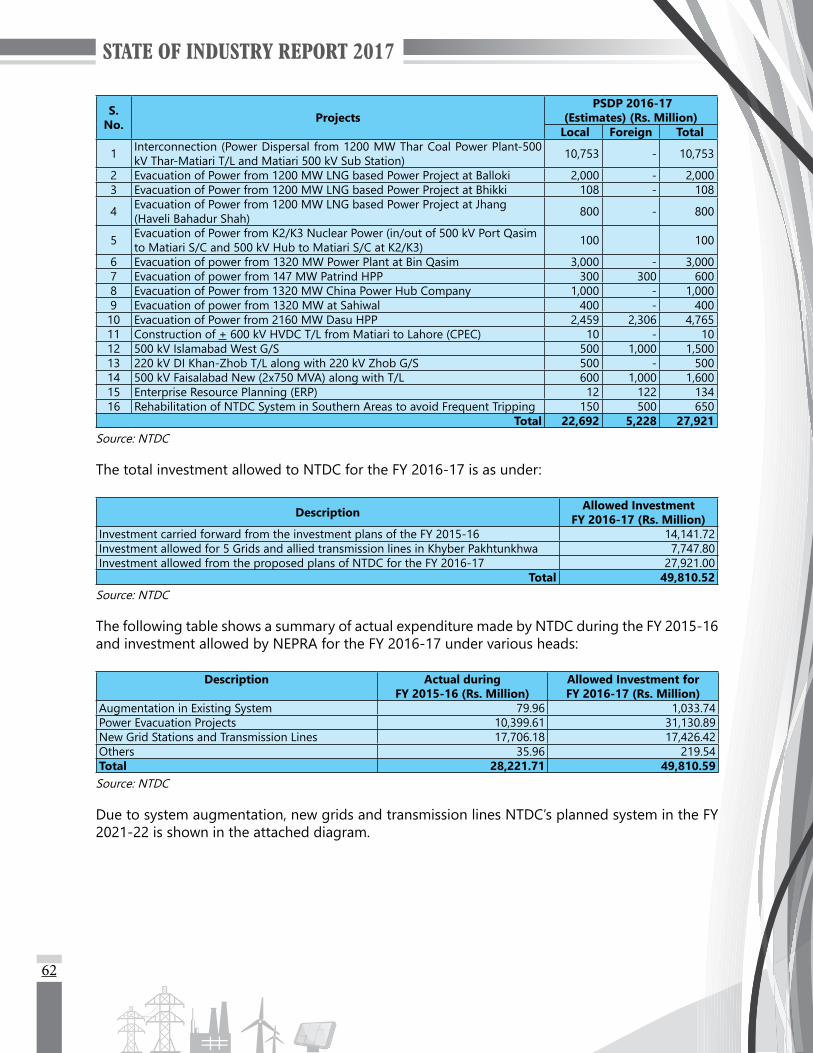

3.5 NTDC Power Evacuation Projects 593.6 Investment Plans of NTDC 603.7 Outages on Transmission Lines of NTDC (500 kV and 220 kV) 643.8 Power Balances of K-Electric Limited Transmission System 643.9 Loading Position of Power Transformers in K-Electric Limited System 643.10 K-Electric Limited Transmission Outage Statistics 663.11 NEPRA Performance Standards (Transmission) Rules, 2005 66

3.11.1 National Transmission and Despatch Company Limited 673.11.2 K-Electric Limited 67

4 PERFORMANCE OF DISTRIBUTION SECTOR 754.1 General 754.2 Circular Debt 754.3 T&D Losses 75

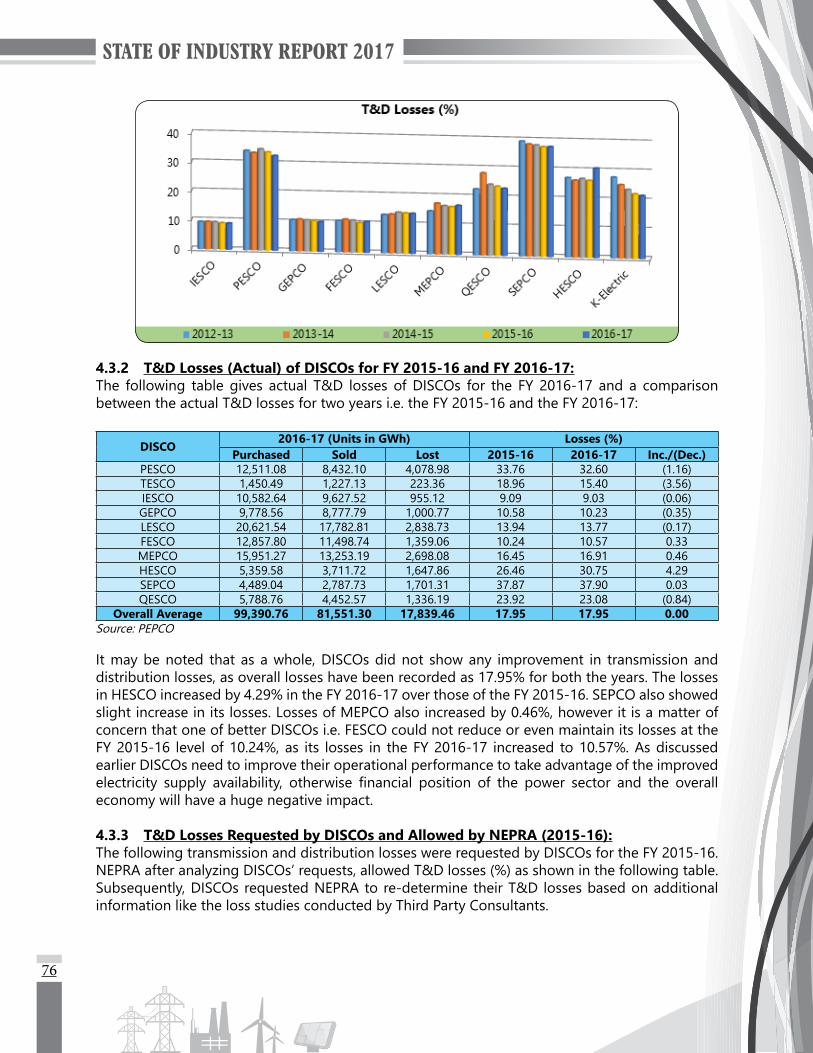

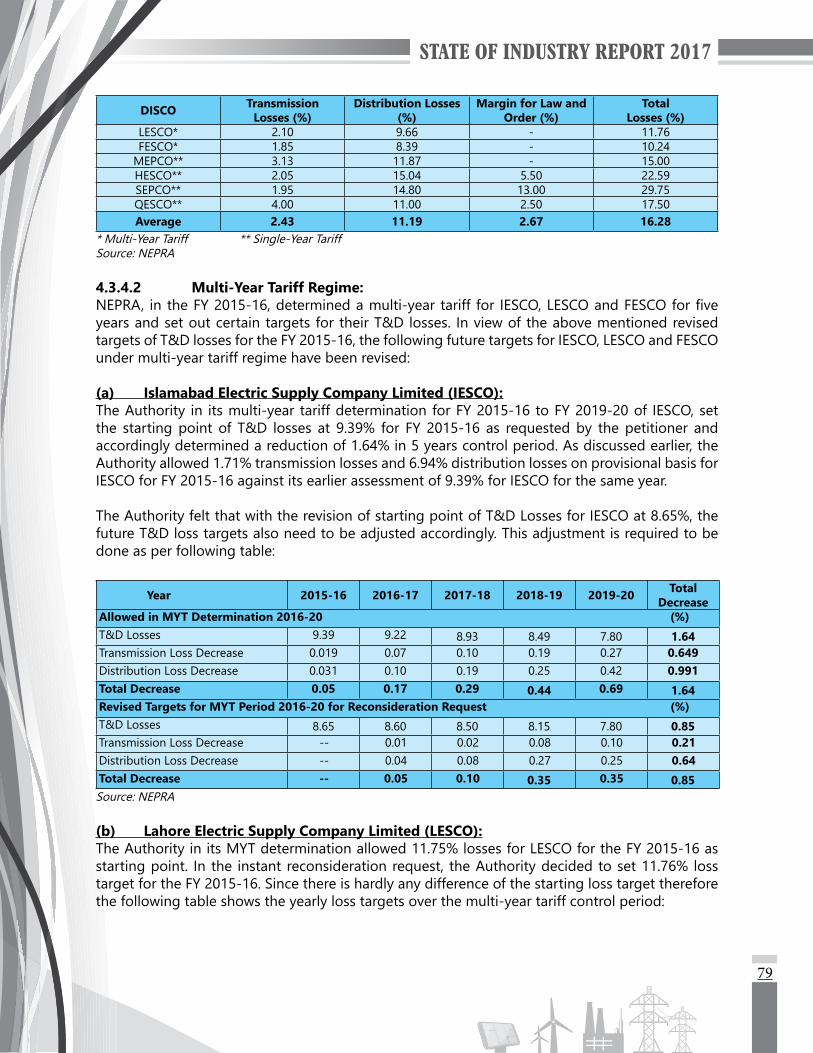

4.3.1 Transmission and Distribution Losses Overall Perspective 754.3.2 T&D Losses (Actual) of DISCOs for FY 2015-16 and FY 2016-17 764.3.3 T&D Losses Requested by DISCOs and Allowed by NEPRA (2015-16) 764.3.4 Re-Determination of T&D Loss Targets 77

4.4 Recovery Position of DISCOs 804.4.1 Recovery Position of Main Categories of Consumers 81

4.5 Receivables of DISCOs 81

iii

4.6 Overloading in DISCOs System 834.6.1 Loading Position of Power Transformers 834.6.2 Loading Position of 11 kV Feeders 834.6.3 Loading Position of Distribution Transformers 844.6.4 Province-wise Loading Positions 84

4.7 Fuel Price Adjustment of DISCOs 854.8 Status of Digitized Mapping of Distribution Network of DISCOs and K-Electric Limited 85

4.9 Loading Position of Power Transformers, 11 kV Feeders and Distribution Transformers in K-Electric Limited System 85

4.10 Recovery Position of K-Electric Limited 864.11 T&D Losses under Multi-Year Tariff Regime 864.12 Investment Details of Distribution Sector 864.13 Performance under NEPRA Standards 87

4.13.1 DISCOs’ Performance under NEPRA Standards 874.13.2 Performance of K-Electric Limited under NEPRA Standards 93

5 MONITORING OF THE SECTOR 975.1 General 975.2 Performance Evaluation Reports of GENCOs (2012, 2013 and 2014) 98

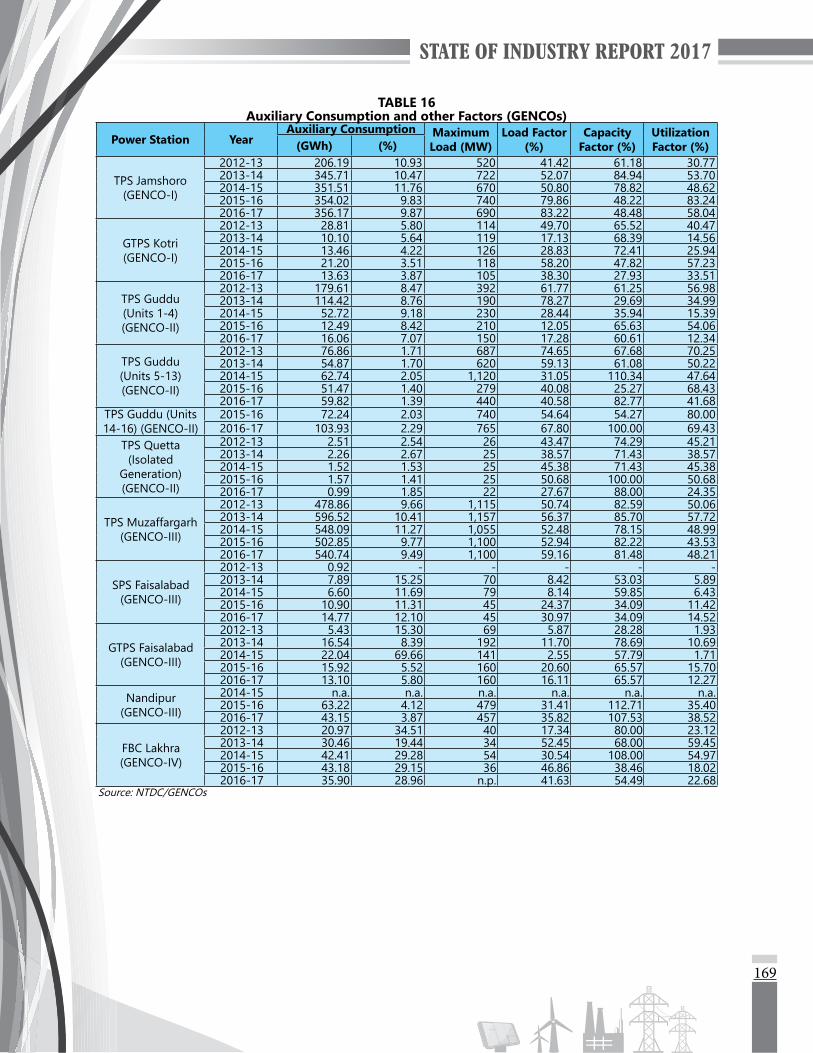

5.2.1 Auxiliary Consumption 985.2.2 Standby Mode 98

5.3 Performance Evaluation Report of GENCOs (2014-15 and 2015-16) 985.3.1 Auxiliary Consumption 985.3.2 Standby Mode 995.3.3 Planned and Unplanned Outages 99

5.4 Performance of K-Electric Limited 995.5 Monitoring of Transmission Sector 100

5.5.1 Performance Standards (Transmission) Rules, 2005 1005.5.2 Initiation of Legal Action against NTDC for Extending Completion Dates of

Projects 100

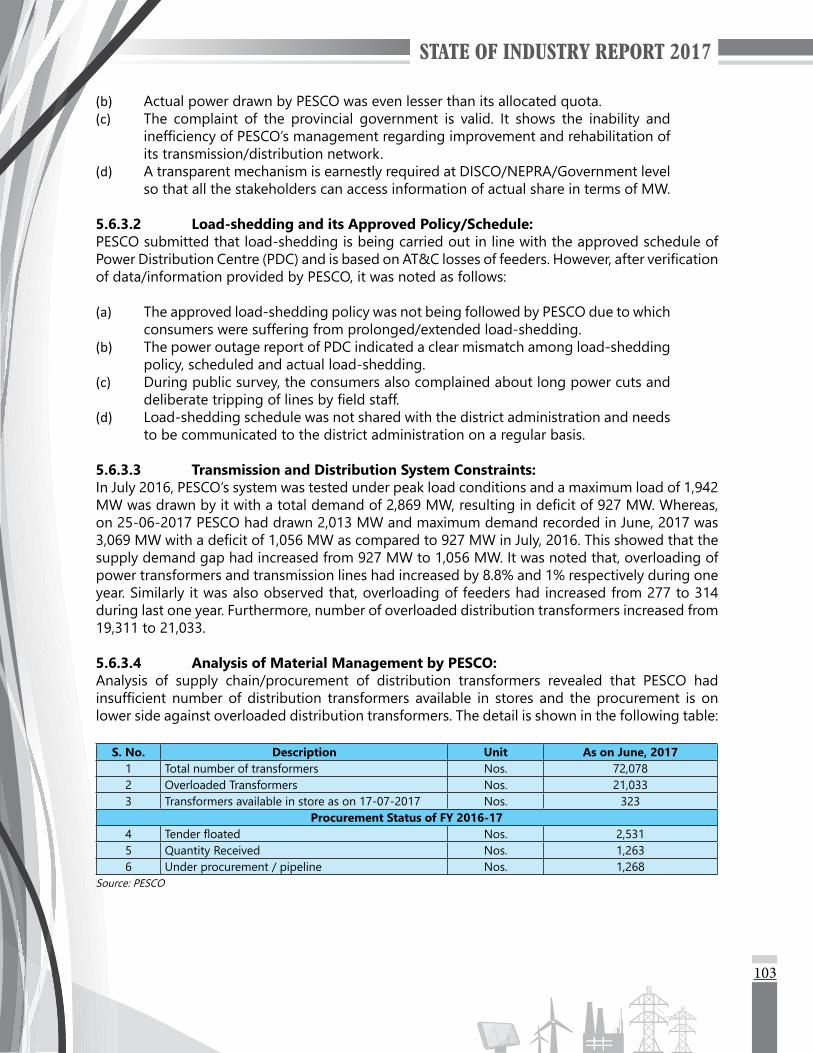

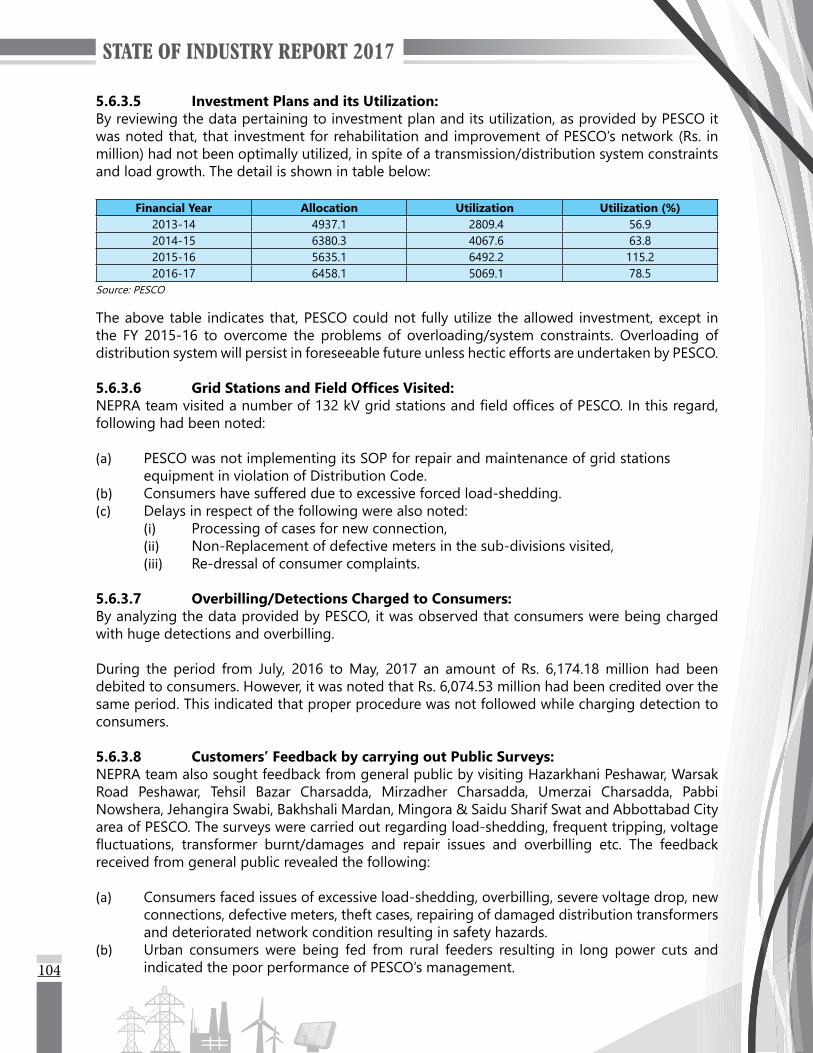

5.6 Monitoring of Distribution Sector 1005.6.1 Data Analysis and Reporting 1005.6.2 Monitoring of Performance Standards (Distribution) Rules, 2005 1015.6.3 Monitoring of PESCO 1025.6.4 Key Findings by Monitoring Teams about PESCO 1055.6.5 Monitoring of K-Electric Limited 106

5.7 Review of Reliability Standards of DISCOs and Linkage with Investments 1075.8 Initiation of Legal Proceedings against Distribution Licensees 107

5.8.1 Legal Proceeding against the Licensees for the Violations of the NEPRA Act, Rules and Regulations and the Applicable Documents 107

5.8.2 Inability of PESCO to Remove System Constraints of Transmission and Distribution Network 107

5.8.3 Un-Announced and Prolonged Hours of Load-Shedding by HESCO 1085.8.4 Un-Announced and Prolonged Hours of Load-Shedding by K-Electric Limited 108

6 INITIATIVES BY NEPRA 1116.1 Rationalization of Generation Tariff Parameters 1116.2 Review of Rate of Return 1116.3 Energy, Environment and Sustainable Development 1116.4 Comprehensive Reduction and Elimination of Polychlorinated Biphenyls 1126.5 Formats for Submission of Information for Generation Company 1136.6 Industry – Academia Collaboration 1136.7 Coal Pricing – Hiring of Consultant 1136.8 Wind Power Generation 114

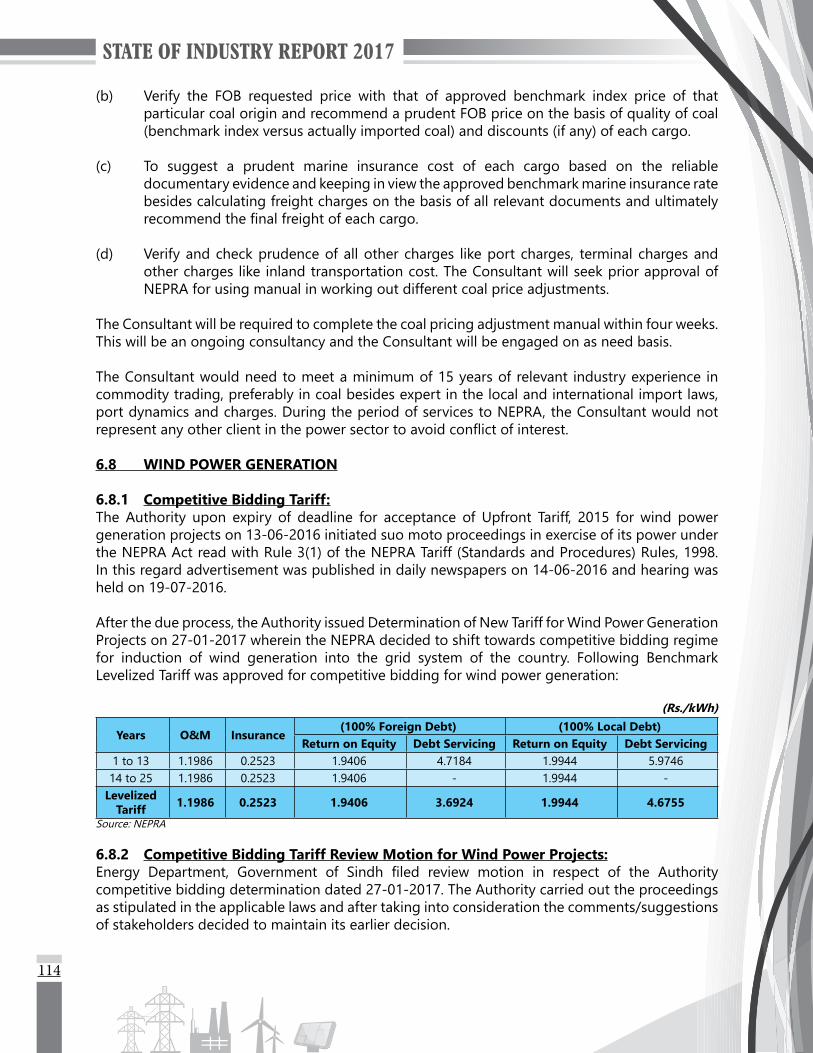

6.8.1 Competitive Bidding Tariff 114

iv

6.8.2 Competitive Bidding Tariff Review Motion for Wind Power Projects 1156.9 Solar PV Power Generation 115

6.9.1 Competitive Bidding Tariff 1156.9.2 Competitive Bidding Tariff Review Motion for Solar PV Power Projects 115

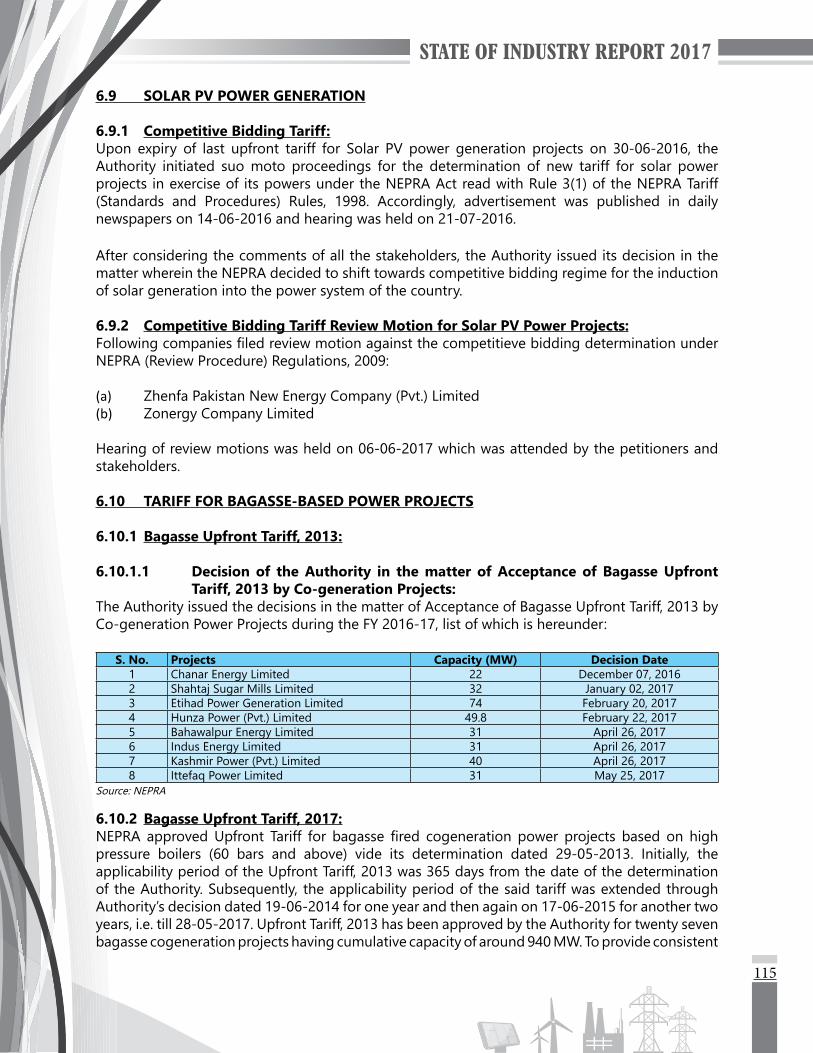

6.10 Tariff for Bagasse-Based Power Projects 1156.10.1 Bagasse Upfront Tariff, 2013 1156.10.2 Bagasse Upfront Tariff, 2017 116

7 INITIATIVES BY STAKEHOLDERS 117

7.1 The Regulation of Generation, Transmission and Distribution of Electric Power (Amendment) Act, 2018 119

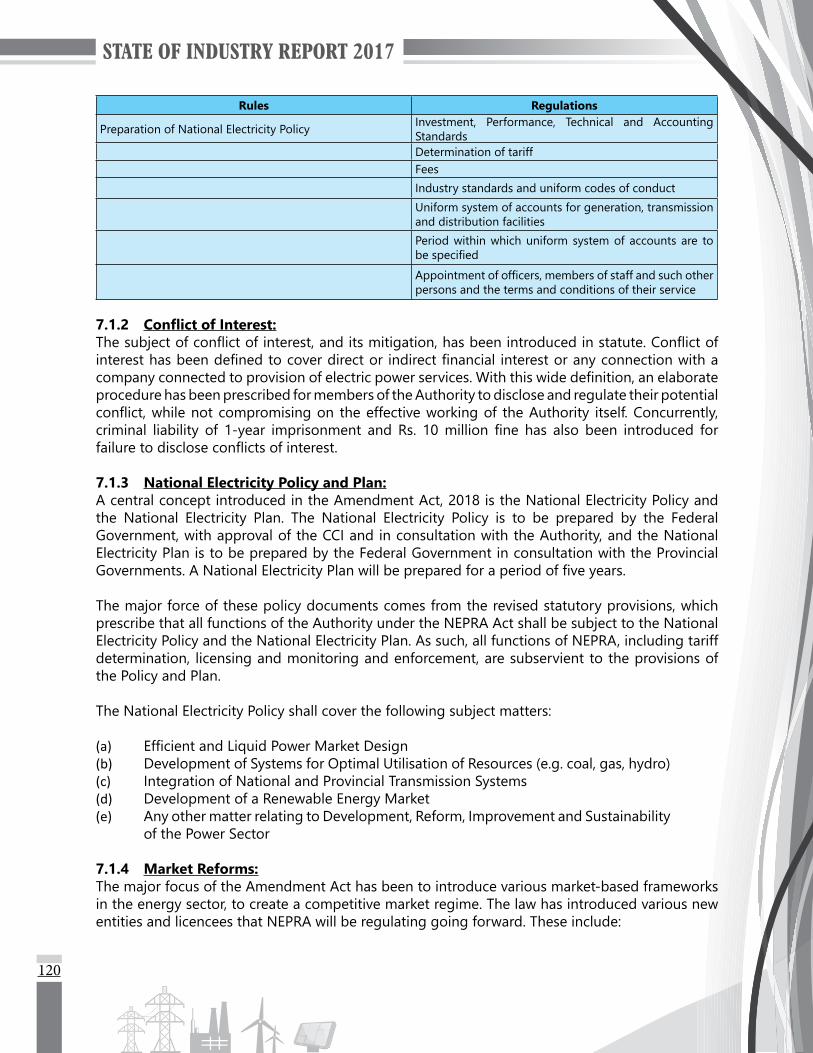

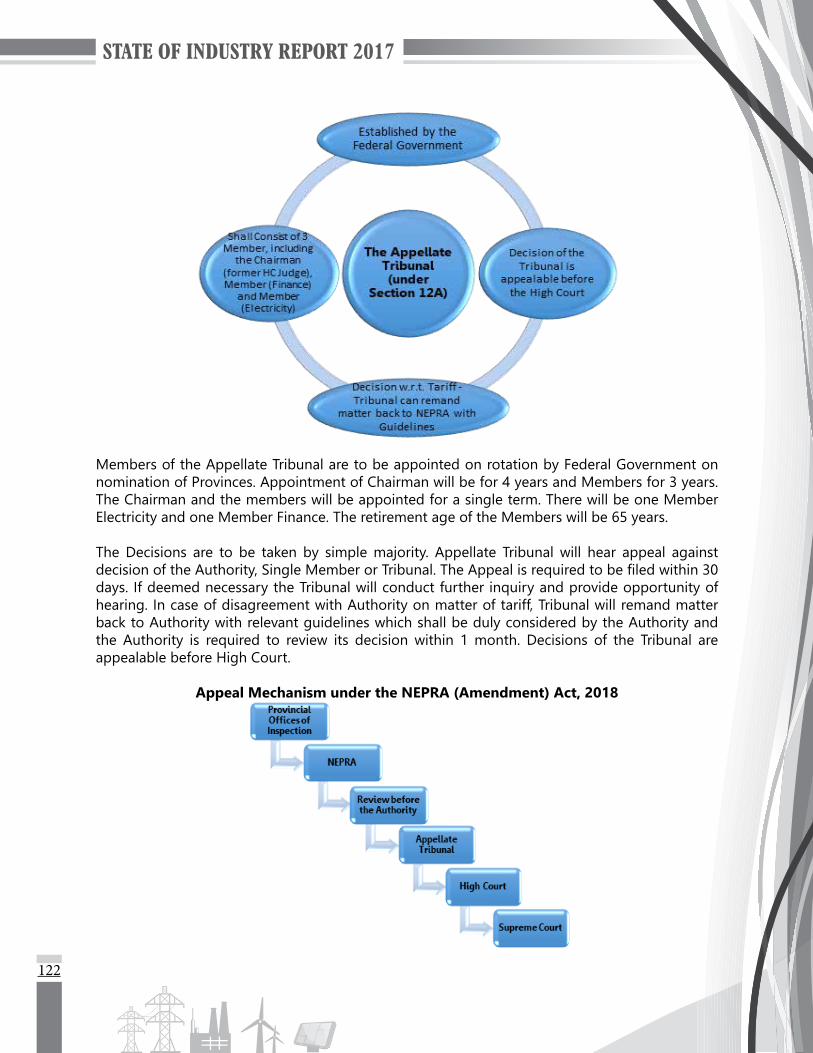

7.1.1 NEPRA Structural and Operational Reforms 1197.1.2 ConflictofInterest 1207.1.3 National Electricity Policy and Plan 1207.1.4 Market Reforms 1207.1.5 Tariff Determination 1217.1.6 Appellate Tribunal 1217.1.7 OfficesofComplaints 1237.1.8 Expansion of Regulatory Powers 123

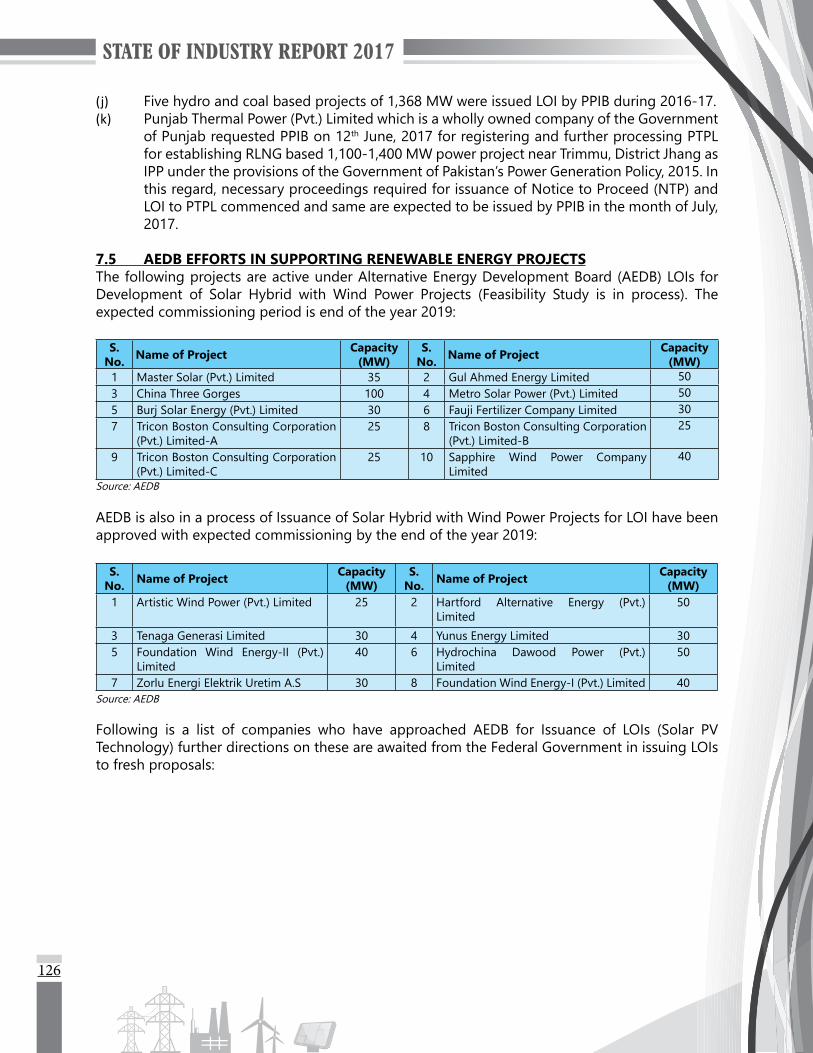

7.2 Progress on Grid Code Review Panel 1237.3 Progress on Distribution Code Review Panel 1237.4 PPIB Role, Planned Activities, Progress and Achievements 1247.5 AEDB efforts in Supporting Renewable Energy Projects 1267.6 PEDO efforts in Supporting Hydel and Renewable Energy Projects 1267.7 Functions of the PPDB Board 1308 MISCELLANEOUS 133

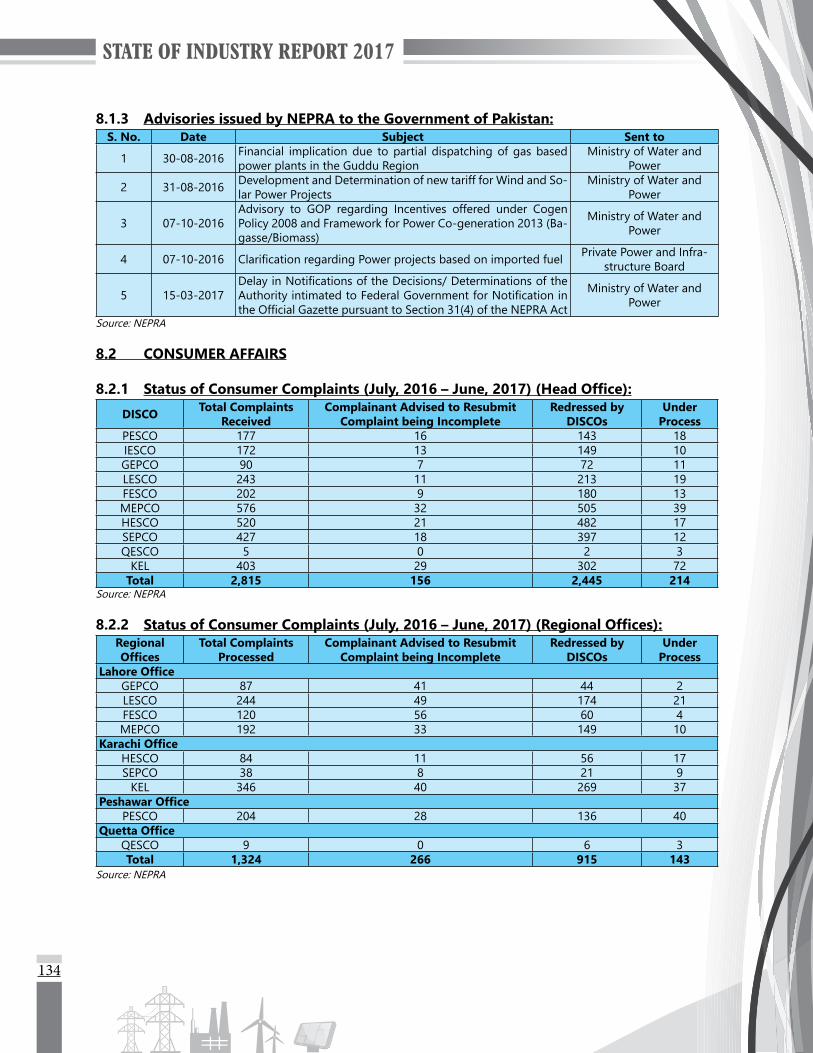

8.1 Summary of Activities during 2016-17 1338.1.1 Promulgation of New Rules/Regulations/Guidelines 1338.1.2 Amendments in NEPRA Rules/Regulations/Guidelines/Codes 1338.1.3 Advisories issued by NEPRA to the Government of Pakistan 134

8.2 Consumer Affairs 1348.2.1 StatusofConsumerComplaints(2016-17)(HeadOffice) 1348.2.2 StatusofConsumerComplaints(2016-17)(RegionalOffices) 1348.2.3 Major Activities/Developments 135

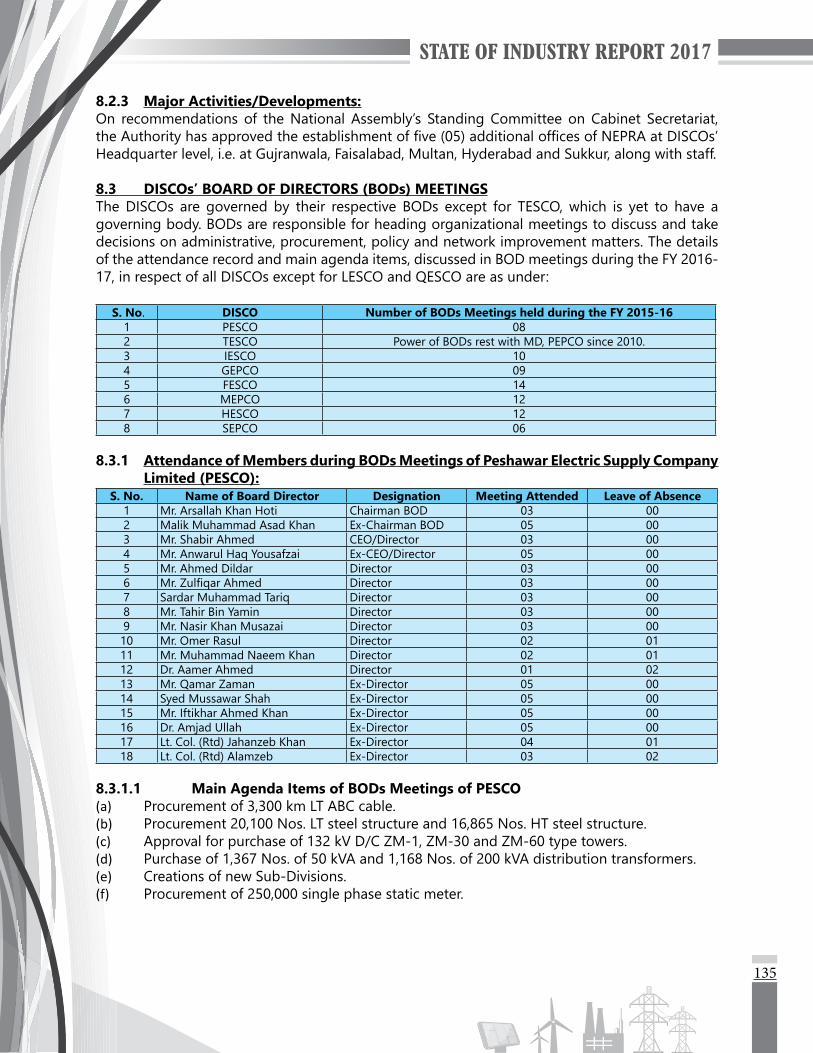

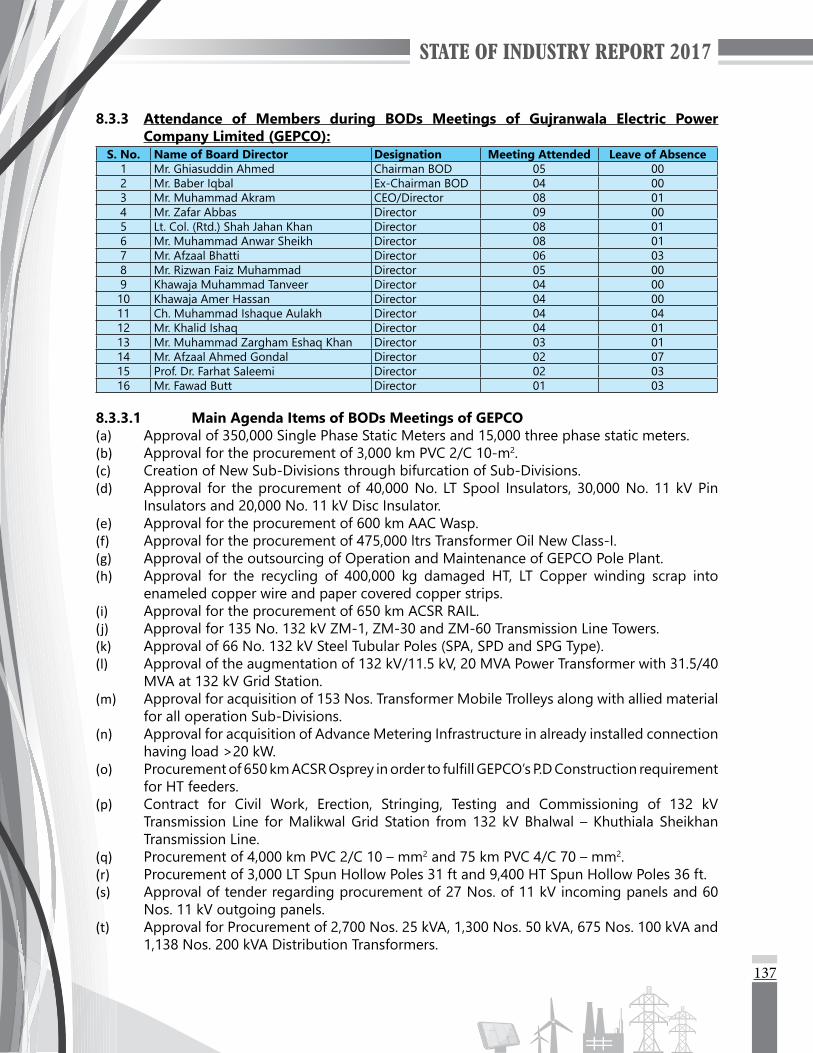

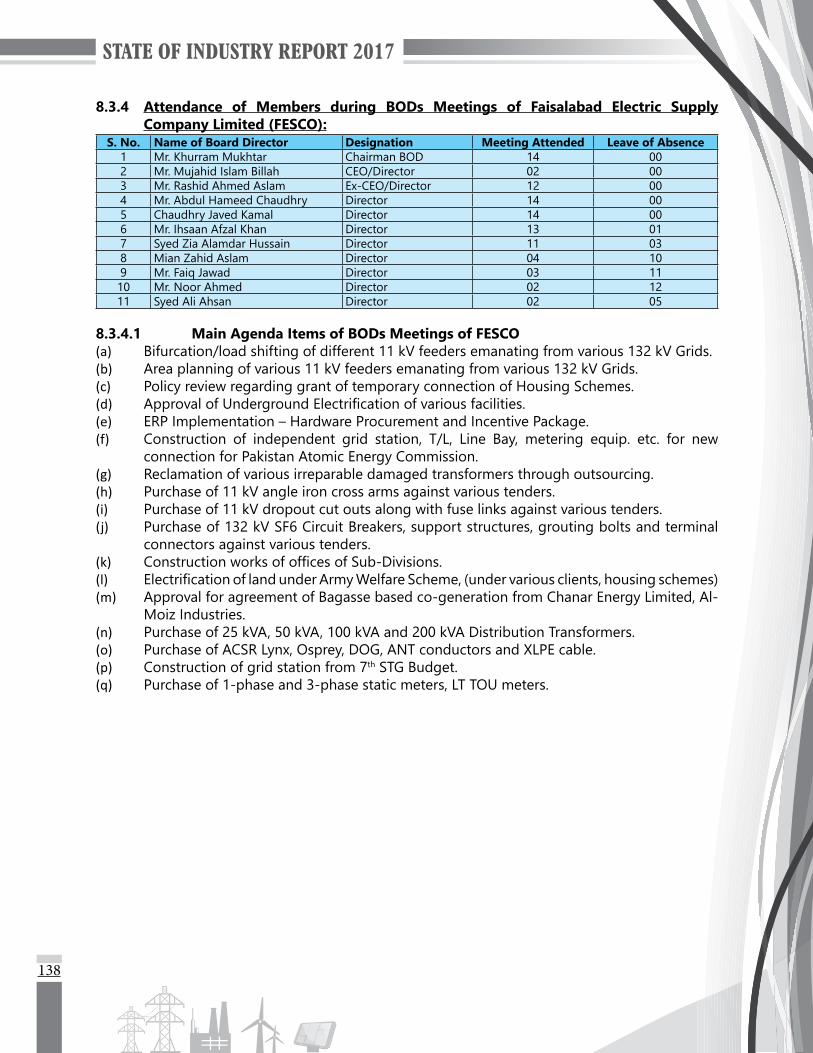

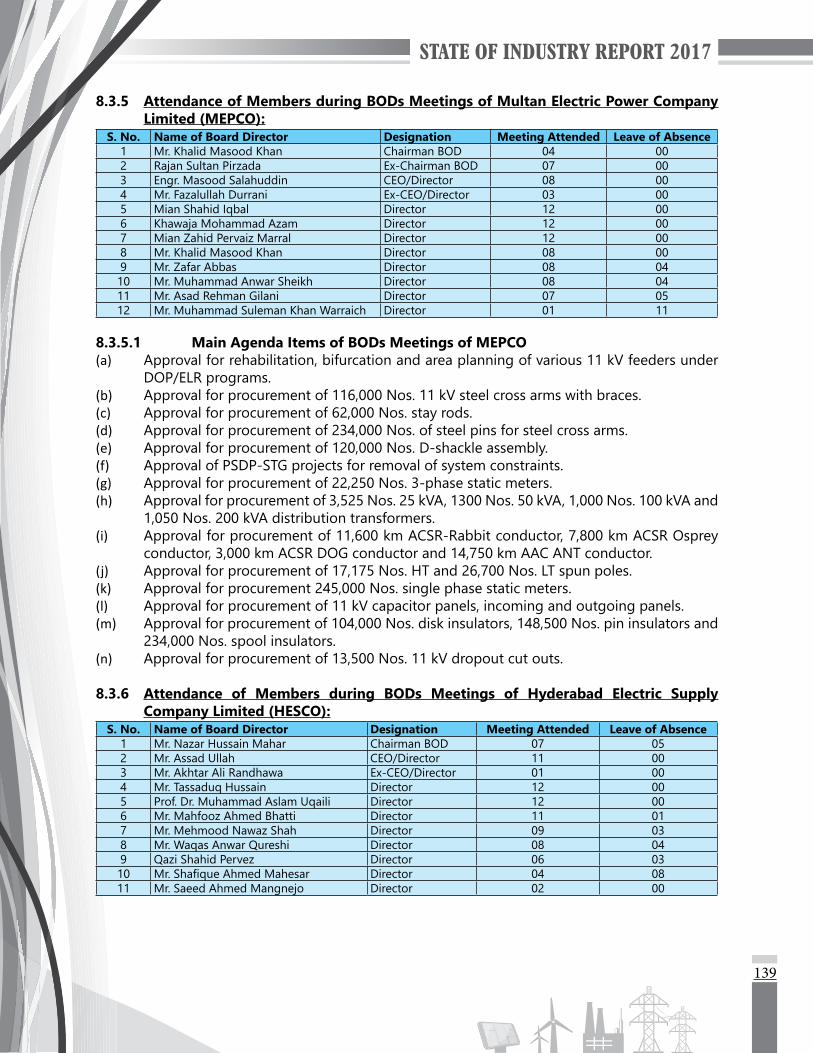

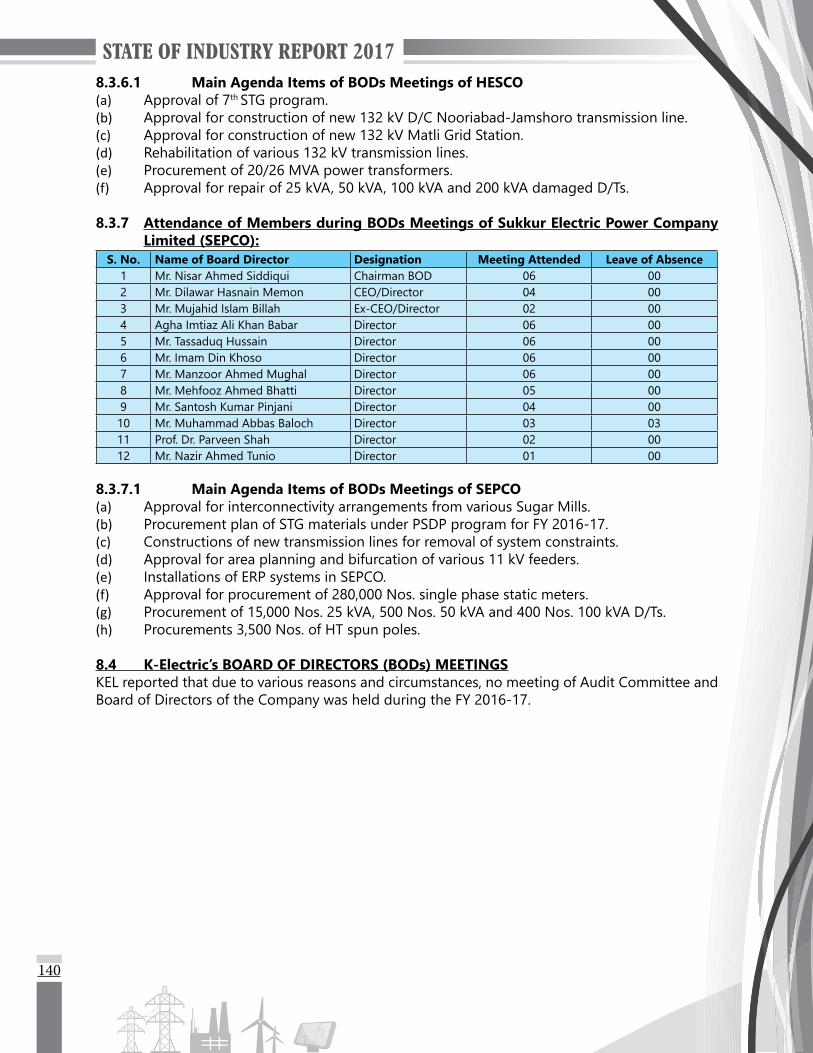

8.3 DISCOs’ Board of Directors Meetings 1358.3.1 Attendance of Members and Main Agenda Items of PESCO 1358.3.2 Attendance of Members and Main Agenda Items of IESCO 1368.3.3 Attendance of Members and Main Agenda Items of GEPCO 1378.3.4 Attendance of Members and Main Agenda Items of FESCO 1388.3.5 Attendance of Members and Main Agenda Items of MEPCO 1398.3.6 Attendance of Members and Main Agenda Items of HESCO 1398.3.7 Attendance of Members and Main Agenda Items of SEPCO 140

8.4 K-Electric’s Board of Director (BODs) MeetingSTATISTICAL DATA ABOUT ENERGY AND ELECTRICITY SECTOR

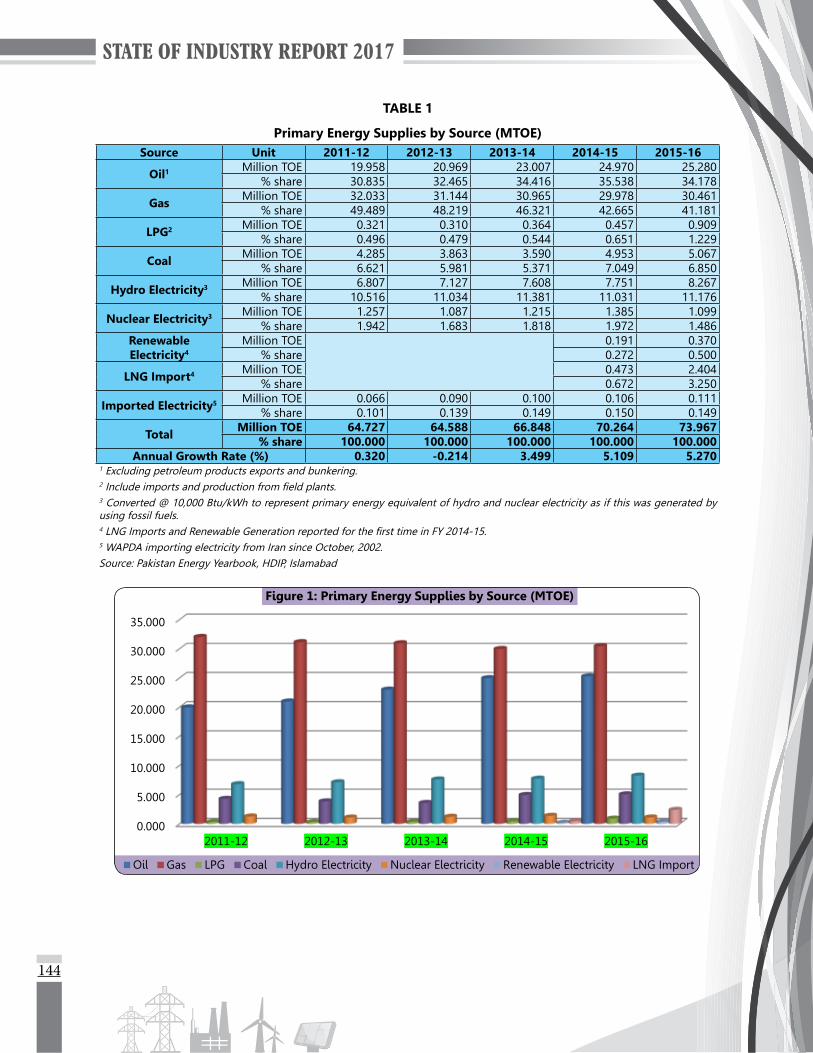

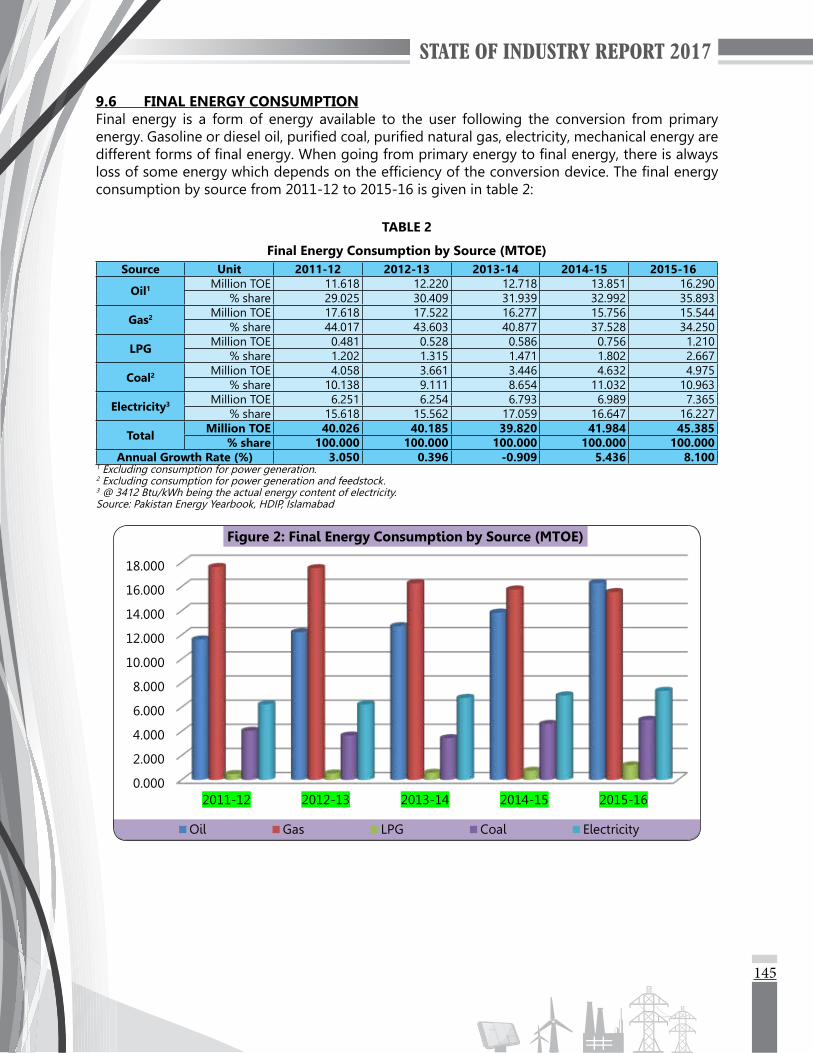

9 ENERGY SECTOR OVERVIEW 1439.1 General 1439.2 Oil Reserves 1439.3 Gas Reserves 1439.4 Coal Reserves 1439.5 Primary Energy Supplies 1439.6 Final Energy Consumption 1459.7 Fuel Consumption in Power Sector 14610 ELECTRICITY SECTOR OVERVIEW 149

10.1 Installed Capacity 149

v

10.2 Electricity Generation 15410.3 Cost of Generation, Fuel Cost and Fuel Consumption 16110.4 AuxiliaryConsumptionandOtherFactors,HeatRateandPlantEfficiency 16710.5 Load Pattern and Peak Load Hours 17810.6 Energy Sales and Consumer-Wise Electricity Consumption 17910.7 Pattern of Electricity Consumption 18210.8 Surplus/DeficitinDemandandSupplyduringPeakHours 18311 ELECTRICITY GENERATION 187

11.1 General 18711.2 Thermal Power Generation 18711.3 Thermal Power Generation and Fuel Consumption 18711.4 Hydel Power Generation 18811.5 Nuclear Power Generation 19011.6 Renewable Energy Generation (Wind, Solar and Bagasse) 19011.7 Investment Plan for Power Generation Projects 19111.8 Economic Load Despatch System 19711.9 Licenses Granted 19912 ELECTRICITY TRANSMISSION 211

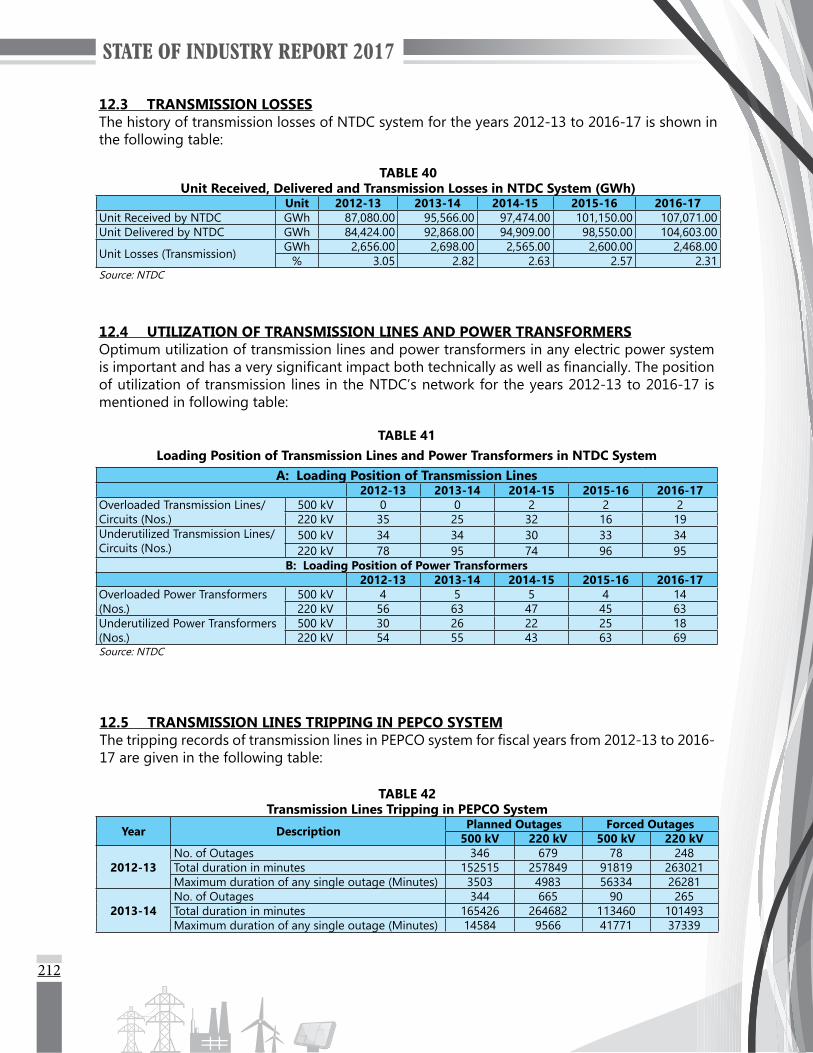

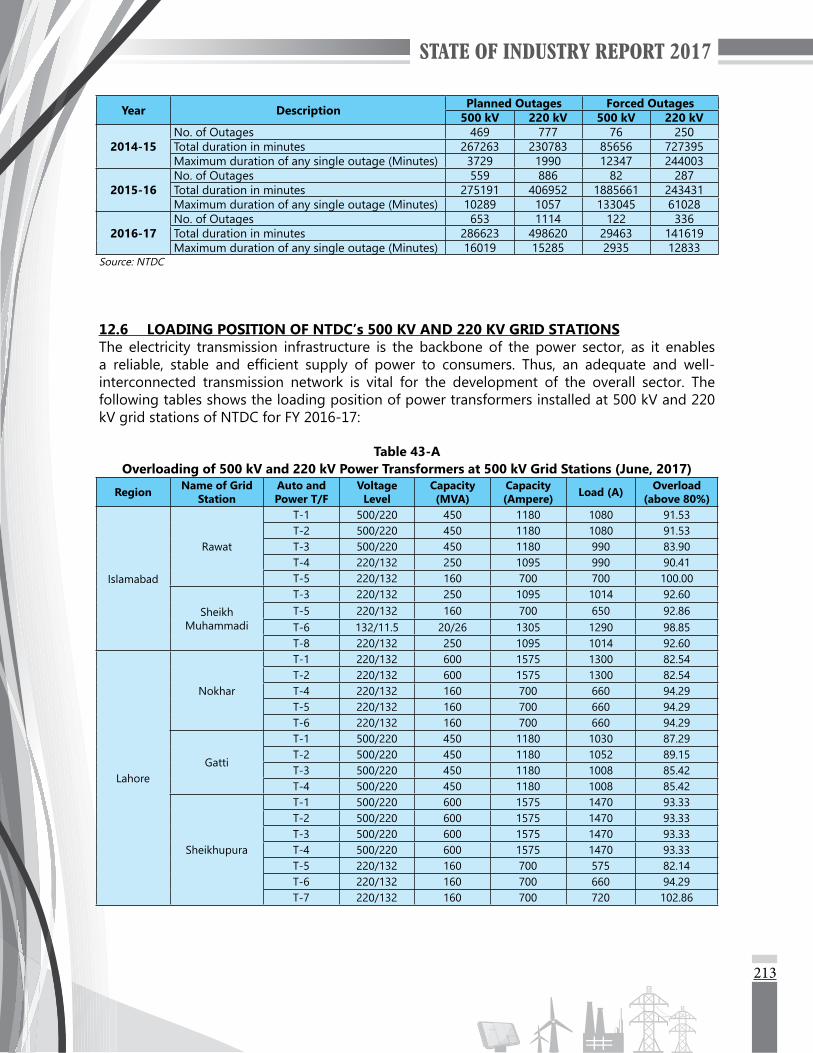

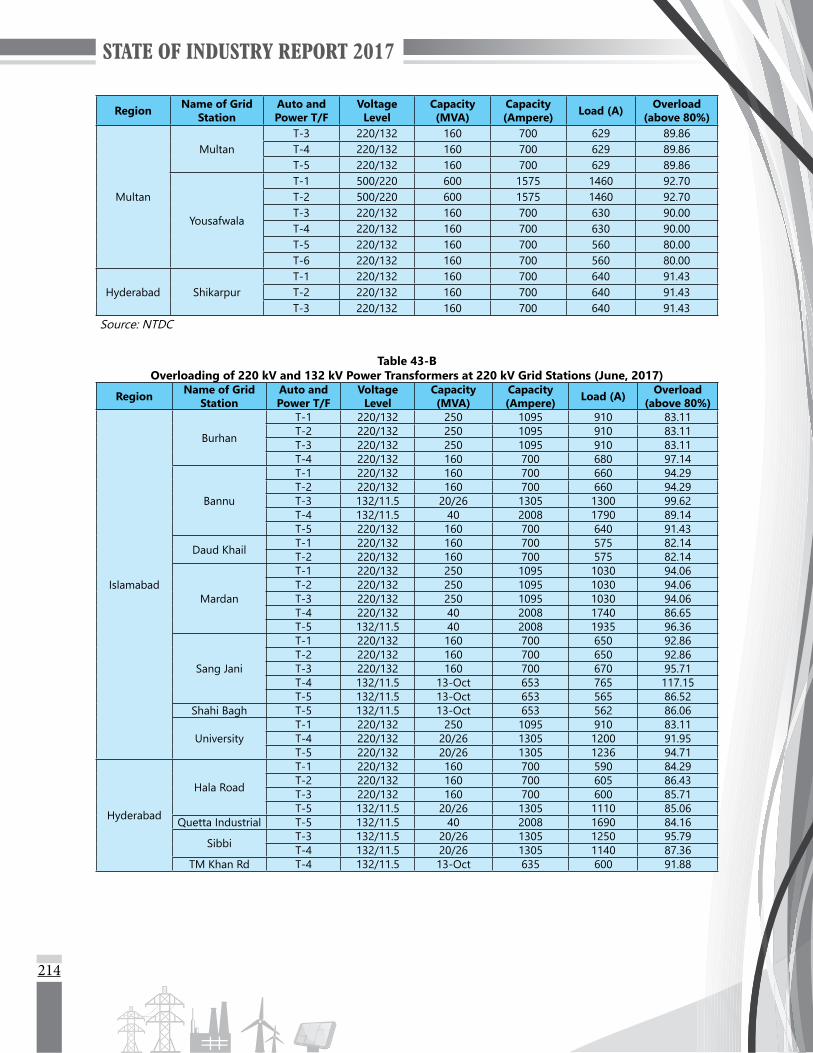

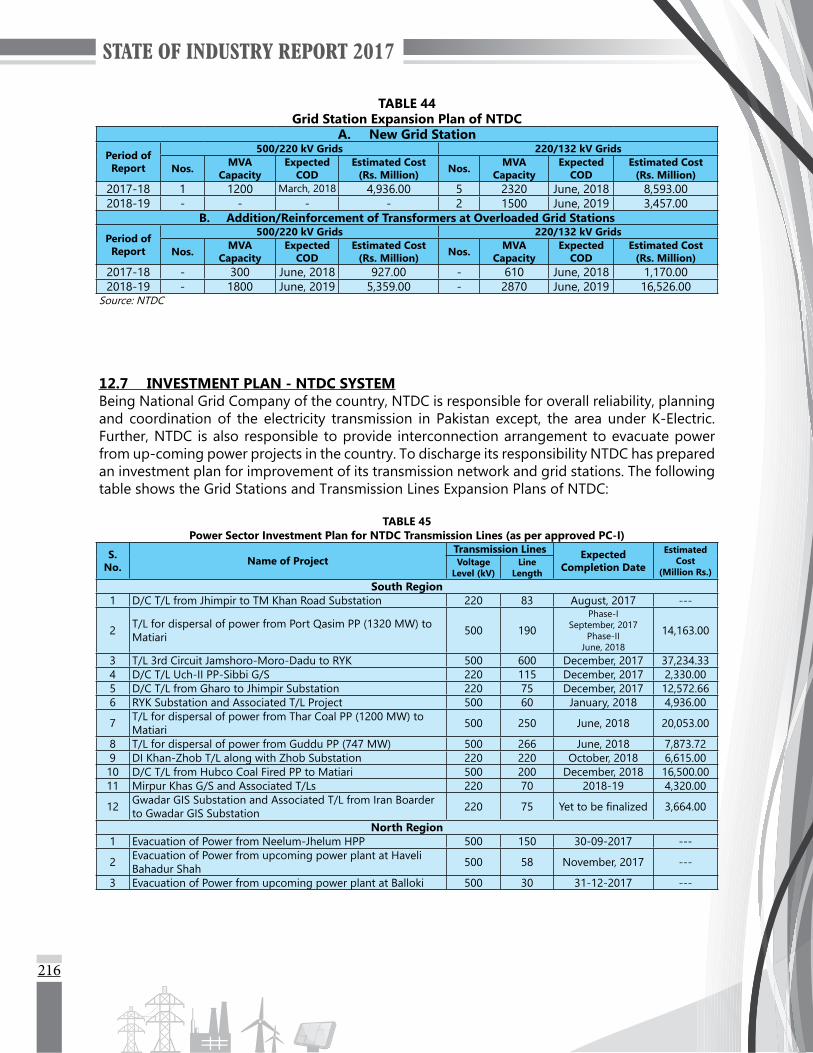

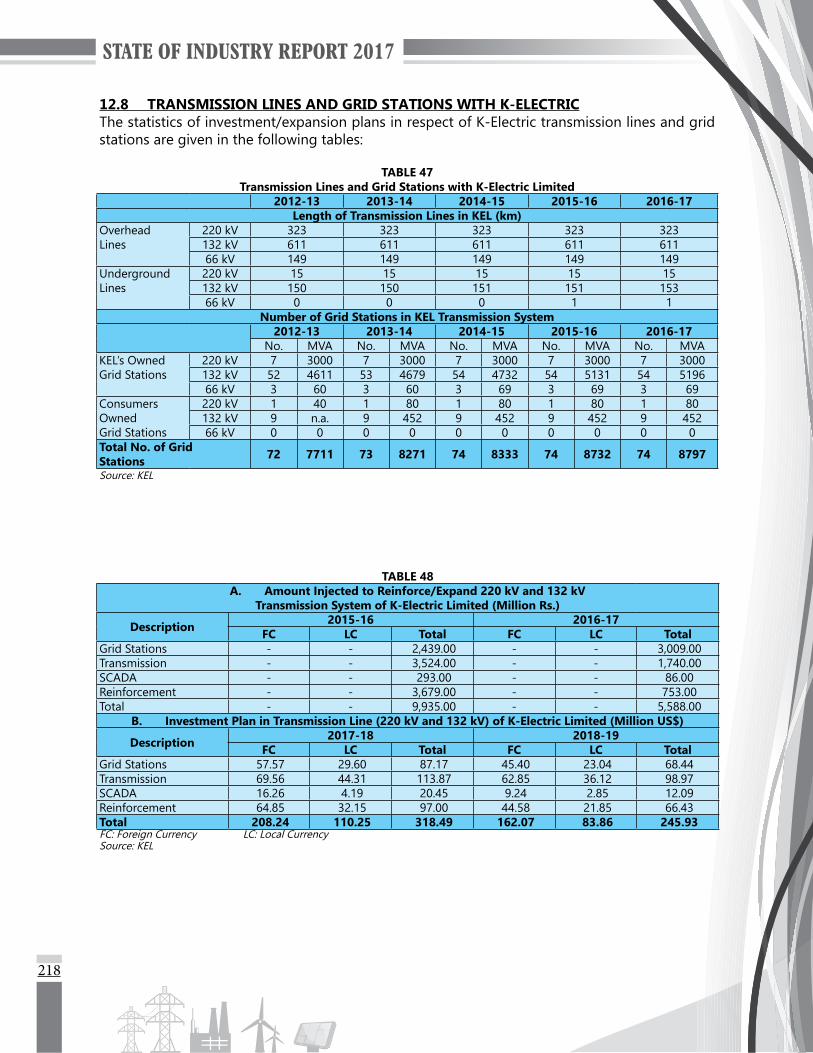

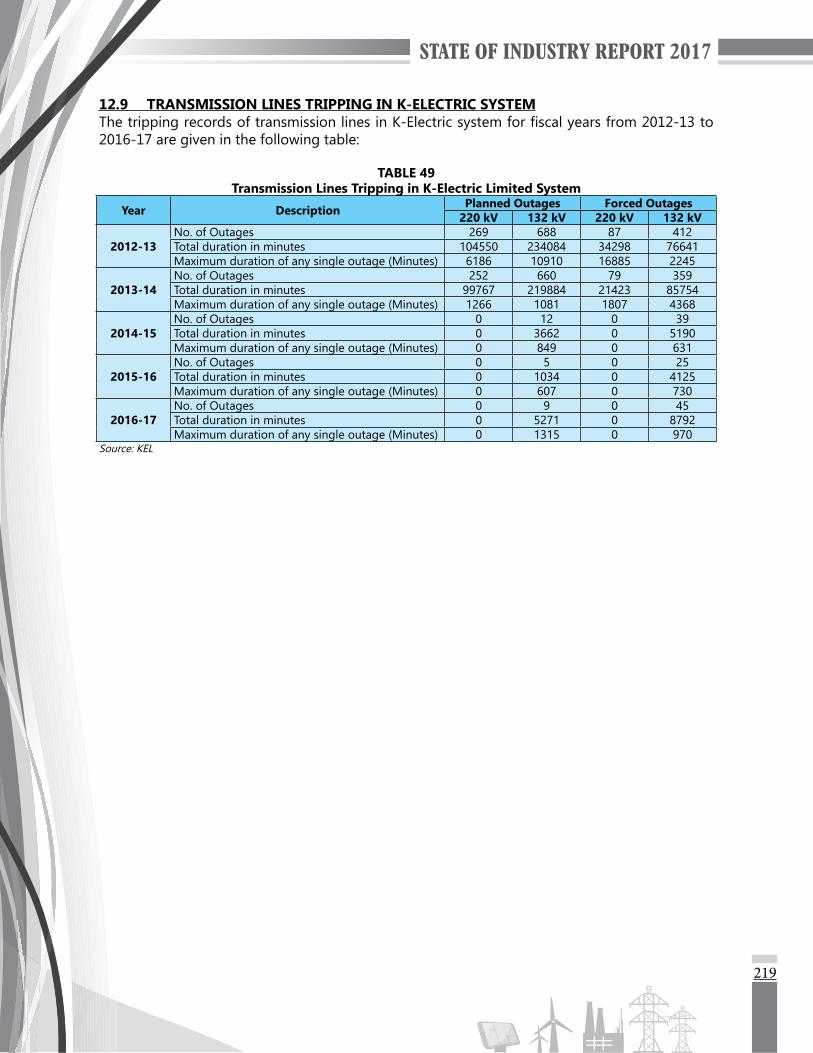

12.1 General 21112.2 Transmission Lines and Grid Stations with NTDC 21112.3 Transmission Losses 21212.4 Utilization of Transmission Lines and Power Transformers 21212.5 Transmission Lines Tripping in PEPCO System 21212.6 Loading Position of NTDC’s 500 kV and 220 kV Grid Stations 21312.7 Investment Plan - NTDC System 21612.8 Transmission Lines and Grid Stations with K-Electric 21812.9 Transmission Lines Tripping in K-Electric System 21913 ELECTRICITY DISTRIBUTION 223

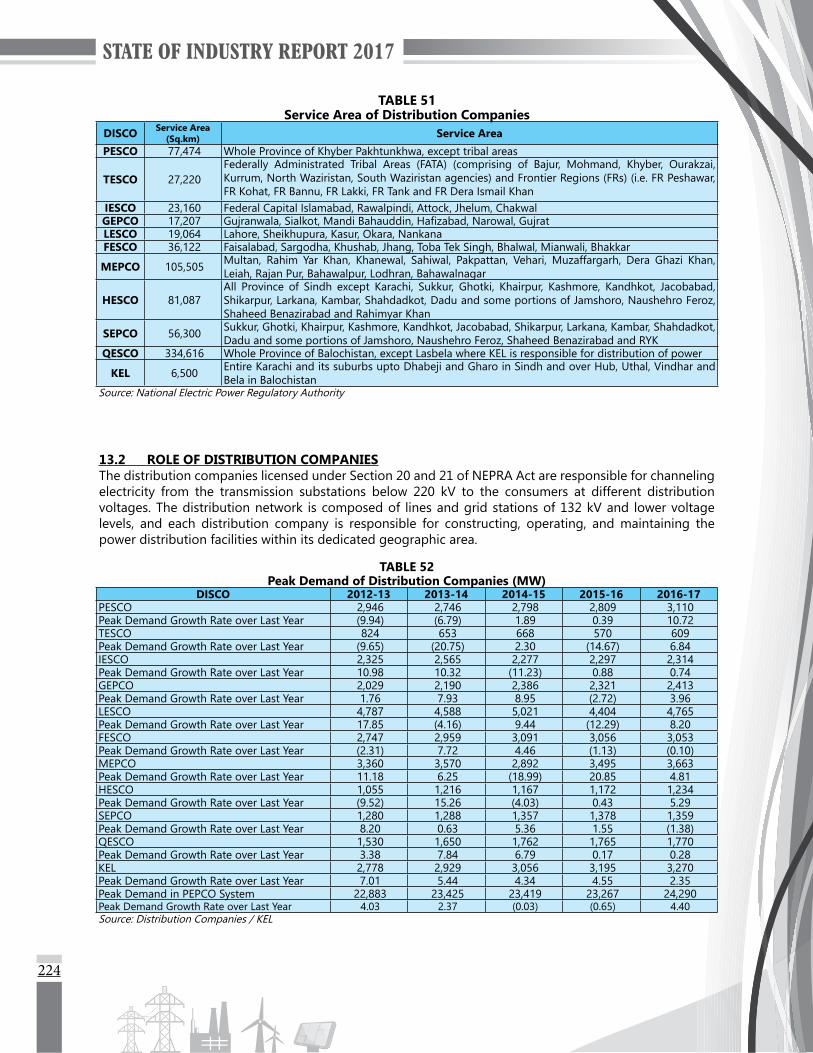

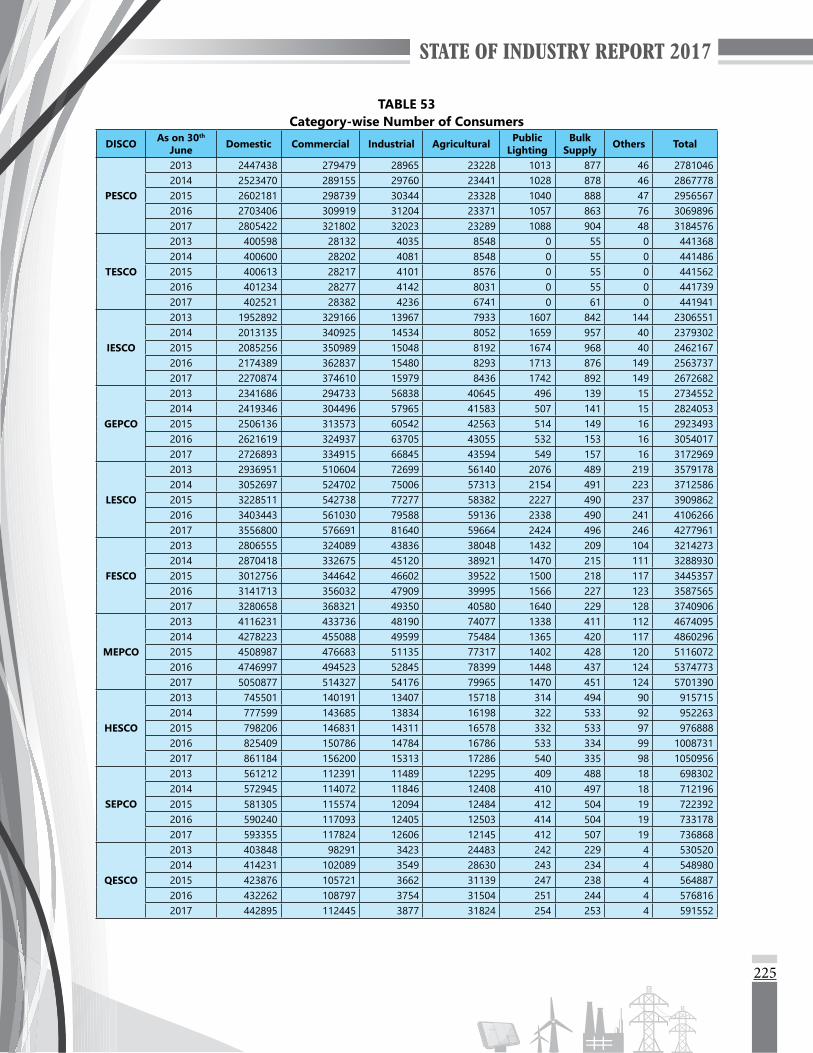

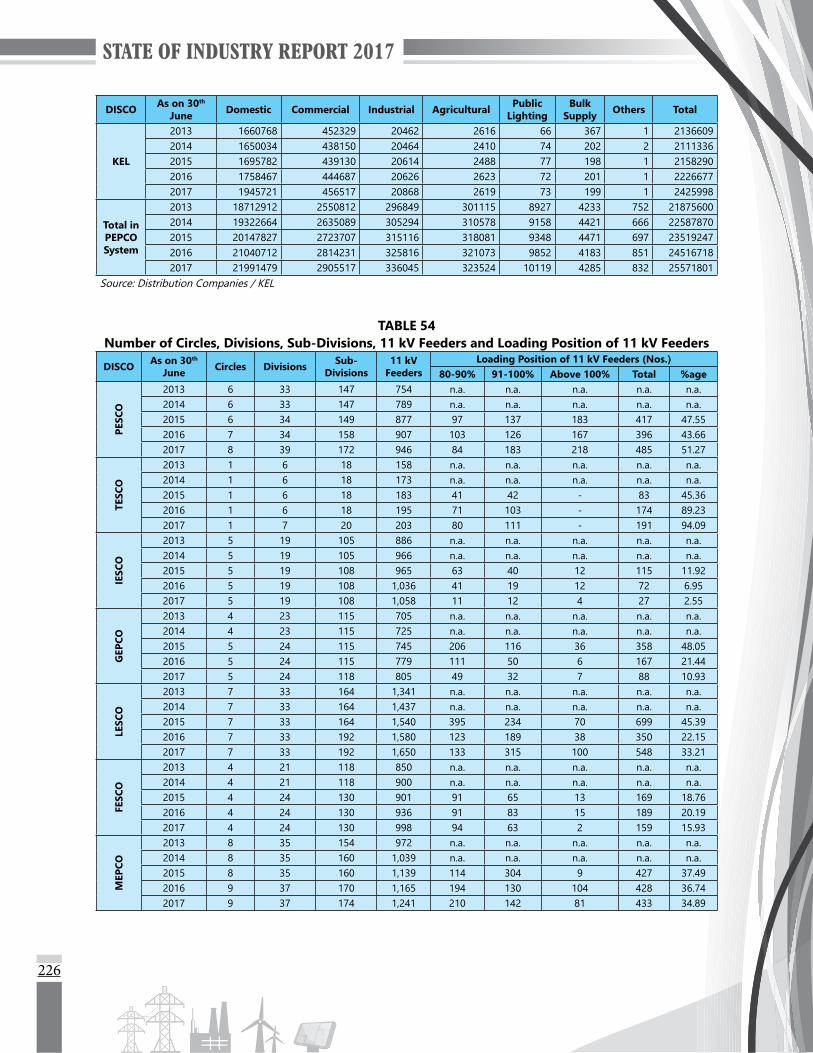

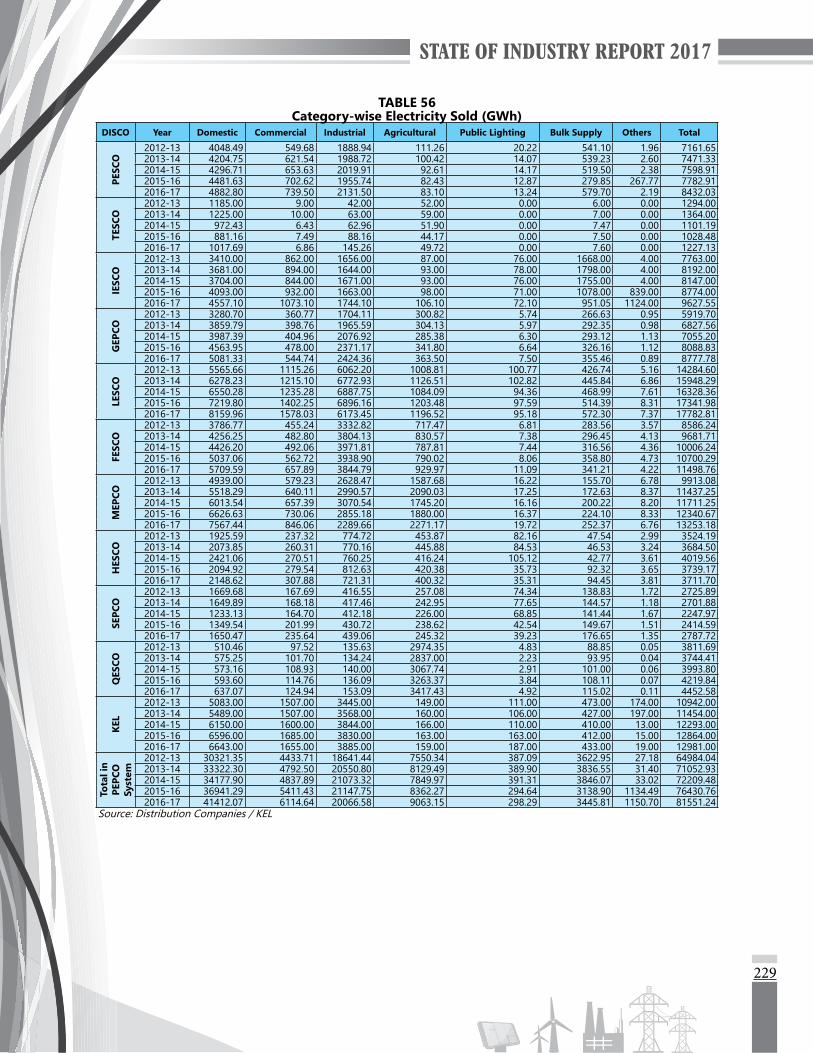

13.1 General 22313.2 Role of Distribution Companies 22413.3 Distribution System Performance 23514 ELECTRICITY TARIFF 251

14.1 General 25114.2 Tariff Setting 25114.3 Tariff Standards 251

List of Tables 281Acronyms and Abbreviations 284Source of Information 287

vi

1

FOREWORD

ThegenerationsectorofPakistanhaswitnessedamajortransformationoverthelastfiveyears(2013-2018), by moving towards a reliable supply system through large base-load power plants using indigenousand importedcoaland throughhighlyefficientgas-basedplants.Anumberof large hydropower plants have also achieved completion, whereas till date around 1,500 MW of solar and wind power plants, have also been inducted to encourage clean energy. Furnace Oil-based power generation plants which remained face of Pakistan power sector for over three decades, have been planned to be phased out over next few years and it is expected that the share of furnace oil-based energy will decline from around 30% to a negligible level in the overall mix in the coming years.

The challenges however, are immense, the addition of generation facilities have put added pressure for a strong transmission and distribution infrastructure to make the delivery of electricity to end-consumers possible. Over the years, the regulator has been stressing the need for strong and robust networks for a reliable power supply, however it is the concerted and urgent efforts of National Transmission and Despatch Company Limited (NTDC) and Distribution Companies (DISCOs) which can ensure sustainable reliable power supply to end-consumers.

Taking a holistic view of the transmission and distribution sectors, it is noted that (39%)1 transformers at 500/220 kV level were loaded above 80% of their rated capacity on June, 2017. At 220/132 kV level, (55%)2 transformers are overloaded. In distribution sector, at the end of June 2017, about 37% of high capacity transformers (power transformers) were over-loaded (above 80% of their capacity). Similarly 29% of the 11 kV feeders, used for bulk transmission of electricity at distribution level, were found over-loaded, whereas more than 12% of the distribution transformers are loaded above 80% of their capacity. It is also noted that on an overall basis, the overloading of equipment has slightly improved over the last year i.e. 2015-16 when the supply of electricity was constrained. With more supply available now, the system is expected to also meet the suppressed demand, which was not connected to the network earlier. Therefore a routine historical pace of improvement and refurbishment in network would not ensure provision of a reliable electricity supply to consumers.

The DISCOs on one hand, would have to strive to strengthen their network for providing reliable electricity supply, whereas on the other, they would be pressed to increase their energy sales, so that overall impact of increased capacity payments, due to additional generation capacity is neutralized, through increased energy sold, and the consumer-end tariff remains at affordable level.

Over the years the transmission and distribution losses could not be curtailed by the DISCOs and having taken divergent and contradictory positions about losses, almost all the DISCOs have now proposed new and higher loss levels than earlier requested. It is a matter of concern that DISCOs could not take such measures to bring improvement in this critical area. Ministry of Energy (Power Division) is also required to assign due priority to this major impediment in sustainability of the powersectorinPakistan.Itmaybenotedthatalleffortstobringefficiencyinthesectorwouldbedefeated if the DISCOs do not improve their Transmission and Distribution (T&D) loss position.

The Regulator has noted inconsistent positions of the Ministry of Energy (Power Division), especially 1 13 out of 33 2 79 out of 143

2

in respect of introduction of renewable energy based generation facilities including wind, solar and small hydropower plants. For fuel diversity and reducing dependence on imported fuels, the Ministry of Energy is required to be consistent for achieving overall objectives outlined in policies of the Federal Government.

Recently approved Amendment Act, 2018 has brought major changes in the existing regulatory regime. The distribution function has been separated into wire and sale businesses. In addition concepts of “trader” and “supplier” have been introduced which are entirely new for all the stakeholders. The Federal Government has also enhanced its role in policy and rule making for the regulator. The Amendment Act, 2018 provides for a major shift from the existing regime and it is observed that extensive discussions and consultations among stakeholders are required to identify gaps and resolve issues for making smooth transition to the new regime.

It is also noted that a number of entities with very specific roles have been defined in theAmendment Act. It appears that these entities are not well prepared to take over their assigned roles as human resource readiness, software and hardware availability and other skills essential for such roles are not available. It is urged to initiate dialogue at all levels to make regulatory regime through Amendment Act a success.

STATE OF INDUSTRY REPORT 2017

EXECUTIVE SUMMARY

5

EXECUTIVE SUMMARY

Over the past few years the policy makers in Pakistan have recognized it and made concerted effortsfordevelopmentinthepowersectoringeneralandgenerationsectorinparticular.Sufficientgeneration capacity has already been added in the system resulting in considerable improvement in load-shedding position all over the country. As per records, further generation capacity at different stages of implementation, will also be added over the next three years, (leading to a capacity surplus scenario in view of the available demand forecasts). Evacuation of power from thesefacilitieshasputextraburdenontransmissionanddistributionsectors.Infrastructuredeficitandabsenceofperformanceimprovementinthesesectorsmayhampertheeconomicbenefitsforeseen due to huge investment in the generation facilities.

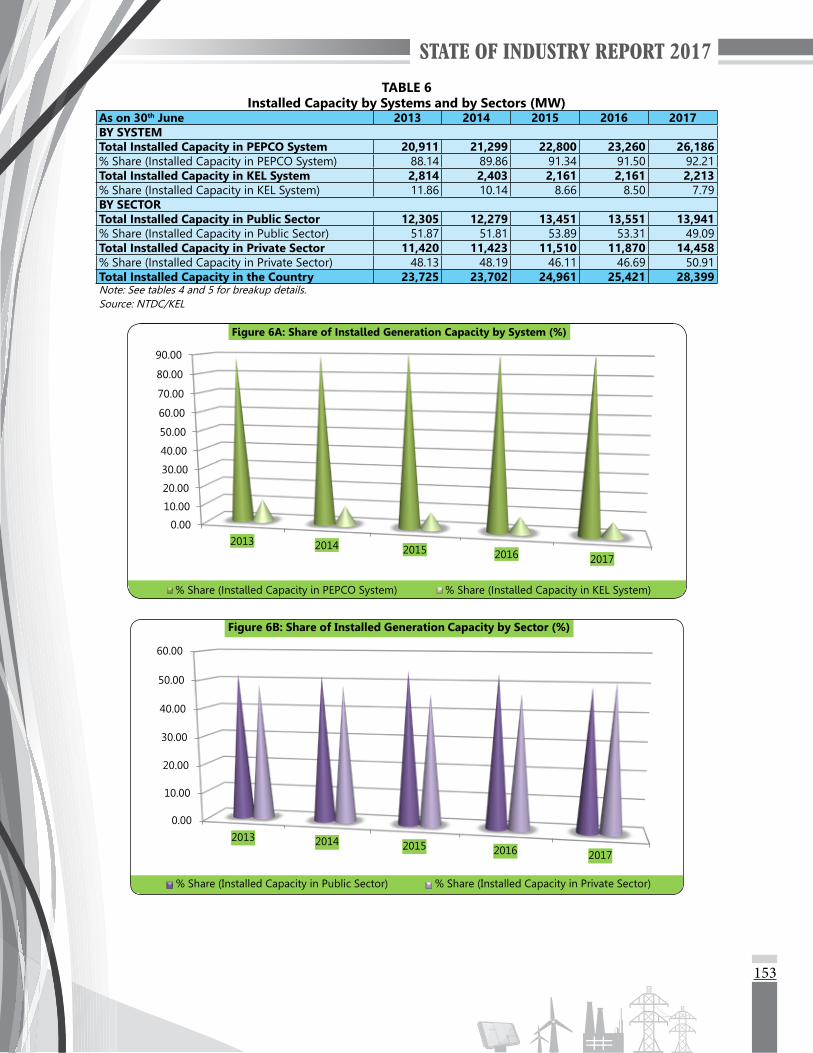

1.1 INSTALLED POWER GENERATION CAPACITYInstalled power generation capacity of Pakistan as of 30th June, 2017 stands at 28,399 MW of which 26,186 MW is connected with NTDC system whereas 2,213 MW is connected with K-Electric Limited (KEL) system. Since 2013 till date, more than 7,000 MW has been added to the generation facilities connected to NTDC system. Based on recent information by NTDC, and analysis by NEPRA, generation capacity additions in NTDC system over a period up to the FY 2024-25 are as shown inthefollowingtable.Itmaybenotedthatthefinalinstalledcapacityofmorethan62,000MWmay not be achieved as some of the power projects including hydro-based projects indicated to beinductedfrom2022to2025requireextensivetechnicalandfinancialprerequisitestocomplete.

NTDC System (MW)

TechnologyInstalled

Capacity as of June 30,

2017

ADDITIONS

2017-18 2018-19 2019-20 2020-21 2021-22 2022-23 2023-24 2024-25 Total*

Oil 6,785 0 0 0 0 0 0 0 0 0Coal 810 1,980 1,320 823 3,300 2,610 1,320 0 0 11,353

Gas/RLNG 8,868 2,508 830 420 0 0 0 0 0 3,758Wind 785 149 299 0 1,224 0 0 0 0 1,672Solar 400 12 600 600 0 0 0 0 0 1,212

Bagasse 280 77 583 144 0 0 0 0 0 804Hydro 7,116 2,709 41 201 177 824 3,080 4,325 2,203 13,560

Nuclear 1,142 340 0 0 1,100 1,100 0 0 1,100 3,640Year-wise Addition --- 7,775 3,673 2,188 5,801 4,534 4,400 4,325 3,303 35,999

Total Cap. after Additions

26,186 33,961 37,634 39,822 45,623 50,157 54,557 58,882 62,185 62,185

* Technology-wise Installed Capacity Additions from FY 2017-18 till FY 2024-25Note: Import not shown of 1,000 MW CASA in year 2021-22 and 96 MW existing from Iran.Source: NTDC

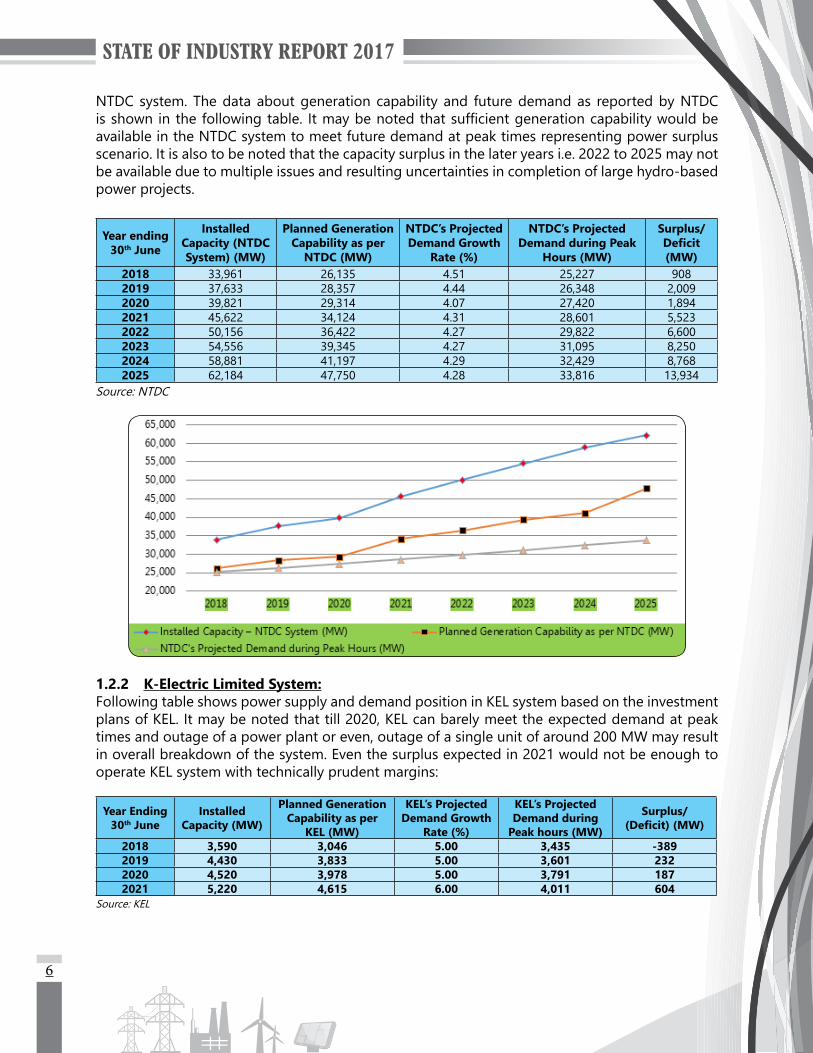

1.2 POWER BALANCES

1.2.1 NTDC System:The generation capability of generation facilities connected with NTDC system will be less than the installed capacity as shown in the above table due to various factors like auxiliary consumption, impact of site reference conditions and seasonality effects on the renewables and large hydropower plants. The generation capability is effectively the capacity for meeting the electricity demand in

01

6

NTDC system. The data about generation capability and future demand as reported by NTDC isshowninthefollowingtable. Itmaybenotedthatsufficientgenerationcapabilitywouldbeavailable in the NTDC system to meet future demand at peak times representing power surplus scenario. It is also to be noted that the capacity surplus in the later years i.e. 2022 to 2025 may not be available due to multiple issues and resulting uncertainties in completion of large hydro-based power projects.

Year ending 30th June

Installed Capacity (NTDC System) (MW)

Planned Generation Capability as per

NTDC (MW)

NTDC’s Projected Demand Growth

Rate (%)

NTDC’s Projected Demand during Peak

Hours (MW)

Surplus/Deficit (MW)

2018 33,961 26,135 4.51 25,227 9082019 37,633 28,357 4.44 26,348 2,0092020 39,821 29,314 4.07 27,420 1,8942021 45,622 34,124 4.31 28,601 5,5232022 50,156 36,422 4.27 29,822 6,6002023 54,556 39,345 4.27 31,095 8,2502024 58,881 41,197 4.29 32,429 8,7682025 62,184 47,750 4.28 33,816 13,934

Source: NTDC

1.2.2 K-Electric Limited System:Following table shows power supply and demand position in KEL system based on the investment plans of KEL. It may be noted that till 2020, KEL can barely meet the expected demand at peak times and outage of a power plant or even, outage of a single unit of around 200 MW may result in overall breakdown of the system. Even the surplus expected in 2021 would not be enough to operate KEL system with technically prudent margins:

Year Ending30th June

InstalledCapacity (MW)

Planned Generation Capability as per

KEL (MW)

KEL’s Projected Demand Growth

Rate (%)

KEL’s Projected Demand during

Peak hours (MW)

Surplus/ (Deficit) (MW)

2018 3,590 3,046 5.00 3,435 -3892019 4,430 3,833 5.00 3,601 2322020 4,520 3,978 5.00 3,791 1872021 5,220 4,615 6.00 4,011 604

Source: KEL

7

1.3 ISSUES OF POWER GENERATION ADDITIONS

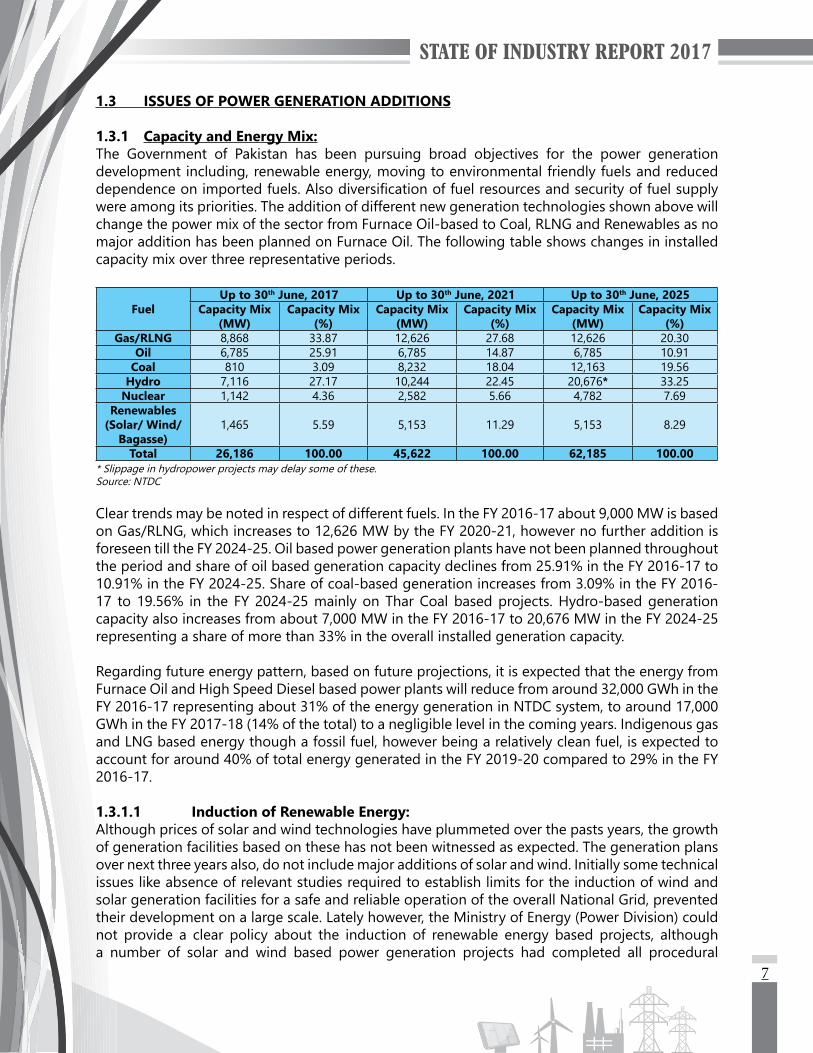

1.3.1 Capacity and Energy Mix:The Government of Pakistan has been pursuing broad objectives for the power generation development including, renewable energy, moving to environmental friendly fuels and reduced dependenceonimportedfuels.Alsodiversificationoffuelresourcesandsecurityoffuelsupplywere among its priorities. The addition of different new generation technologies shown above will change the power mix of the sector from Furnace Oil-based to Coal, RLNG and Renewables as no major addition has been planned on Furnace Oil. The following table shows changes in installed capacity mix over three representative periods.

FuelUp to 30th June, 2017 Up to 30th June, 2021 Up to 30th June, 2025

Capacity Mix (MW)

Capacity Mix (%)

Capacity Mix (MW)

Capacity Mix (%)

Capacity Mix (MW)

Capacity Mix (%)

Gas/RLNG 8,868 33.87 12,626 27.68 12,626 20.30Oil 6,785 25.91 6,785 14.87 6,785 10.91

Coal 810 3.09 8,232 18.04 12,163 19.56Hydro 7,116 27.17 10,244 22.45 20,676* 33.25

Nuclear 1,142 4.36 2,582 5.66 4,782 7.69Renewables

(Solar/ Wind/Bagasse)

1,465 5.59 5,153 11.29 5,153 8.29

Total 26,186 100.00 45,622 100.00 62,185 100.00* Slippage in hydropower projects may delay some of these.Source: NTDC

Clear trends may be noted in respect of different fuels. In the FY 2016-17 about 9,000 MW is based on Gas/RLNG, which increases to 12,626 MW by the FY 2020-21, however no further addition is foreseen till the FY 2024-25. Oil based power generation plants have not been planned throughout the period and share of oil based generation capacity declines from 25.91% in the FY 2016-17 to 10.91% in the FY 2024-25. Share of coal-based generation increases from 3.09% in the FY 2016-17 to 19.56% in the FY 2024-25 mainly on Thar Coal based projects. Hydro-based generation capacity also increases from about 7,000 MW in the FY 2016-17 to 20,676 MW in the FY 2024-25 representing a share of more than 33% in the overall installed generation capacity.

Regarding future energy pattern, based on future projections, it is expected that the energy from Furnace Oil and High Speed Diesel based power plants will reduce from around 32,000 GWh in the FY 2016-17 representing about 31% of the energy generation in NTDC system, to around 17,000 GWh in the FY 2017-18 (14% of the total) to a negligible level in the coming years. Indigenous gas and LNG based energy though a fossil fuel, however being a relatively clean fuel, is expected to account for around 40% of total energy generated in the FY 2019-20 compared to 29% in the FY 2016-17.

1.3.1.1 Induction of Renewable Energy:Although prices of solar and wind technologies have plummeted over the pasts years, the growth of generation facilities based on these has not been witnessed as expected. The generation plans over next three years also, do not include major additions of solar and wind. Initially some technical issues like absence of relevant studies required to establish limits for the induction of wind and solar generation facilities for a safe and reliable operation of the overall National Grid, prevented their development on a large scale. Lately however, the Ministry of Energy (Power Division) could not provide a clear policy about the induction of renewable energy based projects, although a number of solar and wind based power generation projects had completed all procedural

8

requirements for implementation.

Similarly small hydropower plants which also represent a renewable energy based source, could not be built as the Ministry of Energy (Power Division) did not provide a clear policy about their induction. Barring a number of issues like continuity of power supply throughout the year in case of small hydropower generation plants and intermittent nature of power supply in case of wind and solar, the advantages of these technologies make them the priority source of power generation in the long term scenario of any country in the world. These not only provide clean energy but help in fuel security while reducing dependence on imported fuels. Small hydropower plants may appear toberelativelyexpensivethansolarandwindatthisstage,howevertheireconomicandfinancialbenefitsarefargreateriftheirextremelylongoperationallifeisconsideredintheanalysis.

In order to encourage renewable energywhile also capturing the benefits of declining pricesof wind and solar, NEPRA announced a series of upfront tariff rounds, which allowed shorter processing times for the development of projects in addition to lower tariffs, consistent with the international trends. To have more attractive tariffs for the sector, lately, NEPRA has recommended to follow competitive bidding regime, which has been successfully used in different countries to have most competitive prices. In this respect, the role of Alternative Energy Development Board (AEDB) has become extremely important as being the relevant agency under the Ministry of Energy for the development of renewable energy projects. AEDB was required and it publically made a commitment to develop detailed documents including Request for Proposal (RFP) for facilitating competitive bidding for inducting renewable energy based projects. After a lapse of more than year and a half, however, AEDB has not been able to come up with these documents, thus creating anoveralluncertaintyinthesectorspecificallyforprospectiveinvestorsintherenewableenergy.The Ministry of Energy (Power Division) is therefore urged to take a clear and consistent policy about the induction of solar, wind and small hydropower projects. Accordingly, AEDB should initiate schedule for competitive bidding in solar and wind power projects at the earliest.

NEPRAhasnotifiedmultiple tariffsunder theNEPRAUp-frontTariff (ApprovalandProcedure)Regulations 2011, including upfront tariffs for Bagasse and Small Hydropower Generation Plants for providing an incentivized regime for clean power technologies. However, the CPPA-G as sole procurer of power on behalf of DISCOs, has in various cases refused to grant authorization for projects being implemented under tariffs and licences granted by the regulator. Moreover, the CPPA-G has continually acted in an ad-hoc and discriminatory manner towards various IPPs and other power projects. Ministry of Energy (Power Division) is therefore required to streamline internal functioning of CPPA-G on these matters.

1.3.1.2 Dynamics of Fuel:Fuel used for power generation plays a critical role as the availability of power generation facilities is directly linked to the fuel availability and its price in the international market. The exchange rate also impacts the overall price of fuel and ultimately the consumer-end tariff as fuel price is treated asapassthroughcomponentinfinaltariff.Inmediumterm,NationalPowerPolicy2013,focusedon reducing the basket price through cheaper fuels and addition of affordable and sustainable power generation to the grid. Reducing country’s reliance on imported oil has been another broad objective. For achieving these objectives, indigenous coal through Thar mining, imported coal, LNG based power plants, nuclear, solar and wind power are under implementation. It is expected that dependence on furnace oil will sharply come down. In order to reduce dependence on imported fuels, the Federal Government has decided to put a cap on the power generation plants based on imported coal. On similar lines, although LNG is a cleaner fuel, the Federal Government may look

9

into replacing it by construction of large and small hydropower projects through public-private partnership. A preliminary working shows that any slippage of 1 Rupee against US$ would add, roughly Rs. 4 billion annually, to the imported fuel bill for the planned generation facilities in near future.

1.3.2 Impact of Capacity Additions:From an overall perspective, addition of new power generation capacity to reduce and totally eliminate power shortages in the country makes economic sense, as the unserved energy impacts negatively to the economy of the country as a whole. At the same time however, one must be cognizantofdifferentissueswhichalsoneedtobeaddressedsimultaneously,tooptimizebenefitsof additional energy supply to the sector. It is noted that the Federal Government efforts to lower the overall consumer-end tariff may suffer if in addition to lowering fuel costs, the capacity cost is not kept at an affordable level.

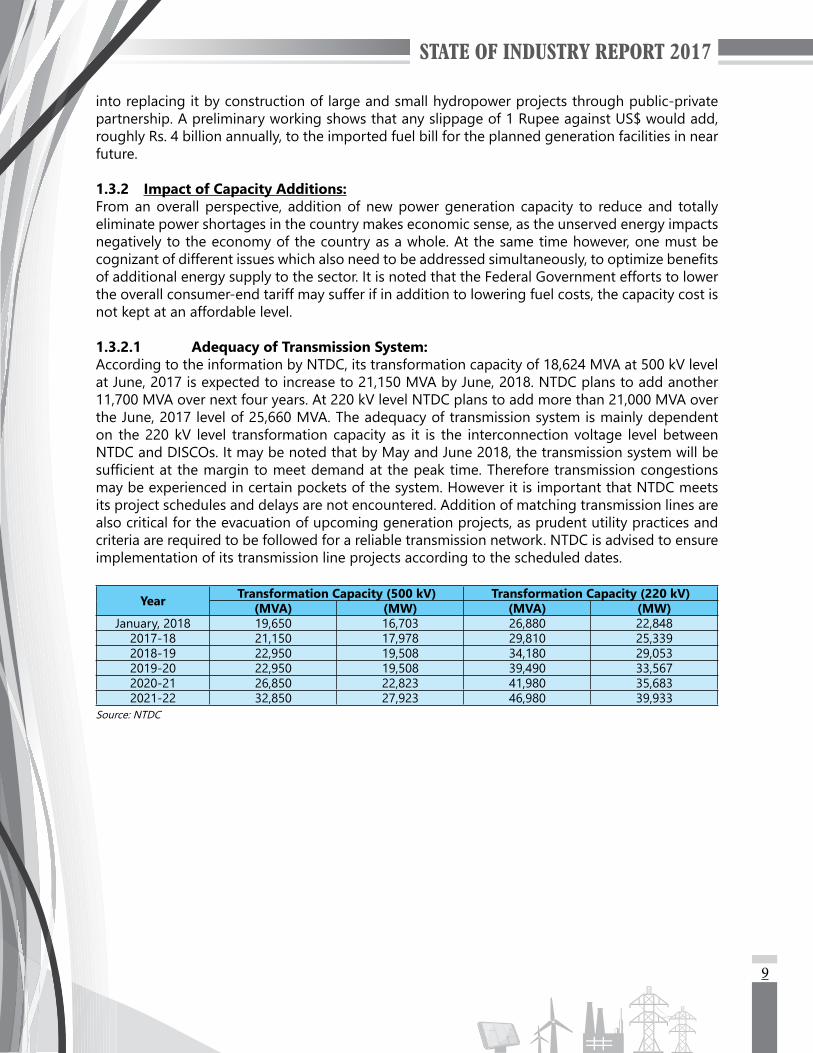

1.3.2.1 Adequacy of Transmission System:According to the information by NTDC, its transformation capacity of 18,624 MVA at 500 kV level at June, 2017 is expected to increase to 21,150 MVA by June, 2018. NTDC plans to add another 11,700 MVA over next four years. At 220 kV level NTDC plans to add more than 21,000 MVA over the June, 2017 level of 25,660 MVA. The adequacy of transmission system is mainly dependent on the 220 kV level transformation capacity as it is the interconnection voltage level between NTDC and DISCOs. It may be noted that by May and June 2018, the transmission system will be sufficientatthemargintomeetdemandatthepeaktime.Thereforetransmissioncongestionsmay be experienced in certain pockets of the system. However it is important that NTDC meets its project schedules and delays are not encountered. Addition of matching transmission lines are also critical for the evacuation of upcoming generation projects, as prudent utility practices and criteria are required to be followed for a reliable transmission network. NTDC is advised to ensure implementation of its transmission line projects according to the scheduled dates.

Year Transformation Capacity (500 kV) Transformation Capacity (220 kV)(MVA) (MW) (MVA) (MW)

January, 2018 19,650 16,703 26,880 22,8482017-18 21,150 17,978 29,810 25,3392018-19 22,950 19,508 34,180 29,0532019-20 22,950 19,508 39,490 33,5672020-21 26,850 22,823 41,980 35,6832021-22 32,850 27,923 46,980 39,933

Source: NTDC

10

The transformation capacity of NTDC system at 220 kV level is charted against the projected demand of NTDC system as shown here. The planned transformation capacity would be adequate over next four year forecast, to pass the demand of the system if the planned implementation schedules of different projects are met.

1.3.2.2 Capacity Payments:An analysis, only for the capacity payments corresponding to generation facilities in NTDC system, shows that such payments which were around Rs. 280 billion in the FY 2015-16 and reached more than Rs. 350 billion in the FY 2016-17, would be close to Rs. 490 billion in the FY 2017-18. A preliminary working in relation to the energy sold, after addition of new power generation plants, shows that capacity cost per unit of energy sold which was slightly higher than Rs. 3.4 in the FY 2015-16 would be around Rs. 4.1 in the FY 2016-17; an increase of Rs. 0.7/unit corresponding to a 6.2%growthinenergysoldintheFY2016-17overtheFY2015-16.ForthefirstsixmonthsoftheFY 2017-18, a growth in energy sold of more than 12.31% over the same period of the FY 2016-17 has been recorded. It is however noted that this growth rate would not be enough to keep the capacity cost component at the same level i.e. Rs. 4.1, as the expected cost components would be close to Rs. 5/unit. In order to keep the capacity cost component at the FY 2016-17 level, the energy sold would be required to increase by at least 30% from the FY 2017-18 to the FY 2018-19. Further analysis shows that in order to keep the capacity payment per unit of energy sold, at the level of the FY 2015-16, at least 57% increase in energy sold would be required in the FY 2018-19 over the FY 2017-18. It is understood that the suppressed demand would also be connected to the system as the electricity is made available, however, in all likelihood, an increase of more than 30% will not be achievable. Various factors including the presence of high loss feeders, in foreseeable future would not let the energy sold, to be increased beyond say 9% to 10% annually, over coming years. With such level of increases in energy sold, the capacity payment close to Rs. 5/unit of energy sold may be expected making the overall energy cost expensive, necessitating increased sustained efforts for cheaper fuels to keep overall tariff at affordable levels.

1.3.2.3 Need for Increasing Energy Sold:Since increasing the level of energy sold is the most critical parameter which can impact positively on the capacity cost per unit sold, therefore all possible means should be explored in this respect. It is noted that power is not supplied by DISCOs to consumers due to multiple reasons including constraints in the transmission and distribution systems, non-availability of generation due to fuel constraintsandotherunspecifiedfactors.InadditiontheMinistryofEnergy(PowerDivision)asa policy has decided not to supply electricity on high-loss feeders which add to the overall load being shed. It is therefore required to address these factors on war-footing for improvement in the system, so that, additional energy is made available through the same power generation capacity.

11

1.3.2.4 Need for Local Manufacturing for Power Sector Equipment:Pakistan as a country has become a consumer market, and it is also true for power sector machinery and equipment, all of which is invariably imported. Although recently there have been a number of very attractive low cost agreements for power equipment, specifically for RLNGbased projects, overall it has been noted to be a supplier’s choice. In order to lower the overall cost of power sector, it is imperative that plant and machinery in generation, transmission and distribution sectors is acquired at competitive prices, prevalent in the regional countries like India. Over the years, local manufacturing of power sector plant and machinery has remained as a low priority for the policy makers. It is however stressed that in order to have affordable consumer-end tariffs, local manufacturing of all major equipment used in power sector be undertaken. Steps in this respect be initiated forthwith.

1.4 NATIONAL ELECTRICITY POLICY AND PLANThe Federal Government has rightly decided to formulate an overall National Electricity Policy and National Electricity Plan for future development of electricity generation, transmission and distribution sectors. The National Electricity Policy would also provide road map for the market structure. The Authority considers that formulation of National Electricity Plans should be a regular activitybyrelevantagencies,astheplansshouldbeevolvingandreflecttechnologicalandfinancialchanges in the sector. The Authority also notes that National Electricity Plans should be adopted in letter and spirit as earlier such plans, though quite comprehensive, were never formed the basis of power sector development. Consequently roller coaster development of sector continued as occasional surpluses and long periods of electricity shortages were witnessed.

1.5 PERFORMANCE OF GENERATION SECTOR

1.5.1 Public Sector (GENCOs and Hydel):

1.5.1.1 Jamshoro Power Company Limited (GENCO-I):The energy generated by GENCO-I during the FY 2016-17 was 3,593 GWh, while, it was 3,828 GWhintheFY2015-16;adecreaseof235GWhor6.14%,overlastyear.NetefficiencyofGENCO-Iduring 2016-17 stood at 28.42% for TPS Jamshoro and 27.05% for GTPS Kotri. With a capacity utilization of 58.04% for TPS Jamshoro and 33.51% for GTPS Kotri due to forced outages and various maintenance issues, the overall performance of GENCO-I has not been satisfactory.

1.5.1.2 Central Power Generation Company Limited (GENCO-II):Total installed capacity of GENCO-II, up to 30th June, 2017 has been noted as 2,402 MW. No new generation plant was inducted during the year under review for GENCO-II. The energy generated by GENCO-II during the FY 2016-17 has been recorded at 8,079 GWh, while, it was 6,031 GWh during the FY 2015-16; an increase of 33.97%, compared with that of the last year. It is observed that various units of GENCO-II have remained off-bar for several years due to maintenance issues, forced outages, fuel constraints and rehabilitation activities etc. and are not being fully utilized. Withreducedannualefficiencyandreducedcapacityutilizationfactor,theoverallperformanceofGENCO-II has been unsatisfactory.

1.5.1.3 Northern Power Generation Company Limited (GENCO-III):Total installed capacity of GENCO-III, up to 30th June, 2017 has been noted as 2,293 MW. During the FY 2016-17, the installed capacity of GENCO-III remained same as compared with that of the year 2015-16. The energy generated by GENCO-III during the FY 2016-17 was 6,861 GWh, while

12

it was 6,273 GWh during the FY 2015-16 showing an increase of 588 GWh or 9.37%, compared withthelastyear.ItisobservedthattheoverallnetefficiencyofTPSMuzaffargarh,SPSFaisalabad,GTPS Faisalabad and Nandipur remained very low. Reportedly, due to various maintenance issues, forced outages and fuel constraints etc. resulting in annual capacity utilization of 48.21% for TPS Muzaffargarh, 14.52% for SPS Faisalabad, 12.27% for GTPS Faisalabad and 38.52% for Nandipur Power Plant, the overall performance of GENCO-III cannot be termed as satisfactory.

1.5.1.4 Lakhra Power Generation Company Limited (GENCO-IV):Total installed capacity of GENCO-IV, up to 30th June, 2017 has been noted as 150 MW. GENCO-IV had three units of 50 MW and during the FY 2016-17, generated 124 GWh as compared to 148 GWh produced during the FY 2015-16. It may be noted that, against the installed capacity of 150 MW, approximately, two third capacity of GENCO-IV is available for generation, which is also not being fully utilized due to forced outages etc. With utilization factor of 22.68% for the FY 2016-17, the overall performance of GENCO-IV has remained unsatisfactory.

AsawholeGENCOscontinuedtooperateatverylowefficienciesthantheirdesignvalues,mostlyon expensive furnace oil. It is also noted that these power plants are also not being operated according to prudent utility practices. GENCOs have low utilization factors and have also been operated in standby mode, where they incur costs without contributing energy to the National Grid, as they are ranked very low in the dispatch merit order. It is noted that during the FY 2016-17 about Rs. 39 billion has been paid to GENCOs on account of capacity payments, while around Rs. 156 billion were charged on account of energy payments. Ministry of Energy (Power Division) is thereforeurgedtophaseoutthesefacilitiesinviewoftheirinefficientanduneconomicroleinthesector. Due to their high operating costs, some of these plants may be totally closed down even if their capacity costs are continued to be paid, to minimize economic loss to the sector.

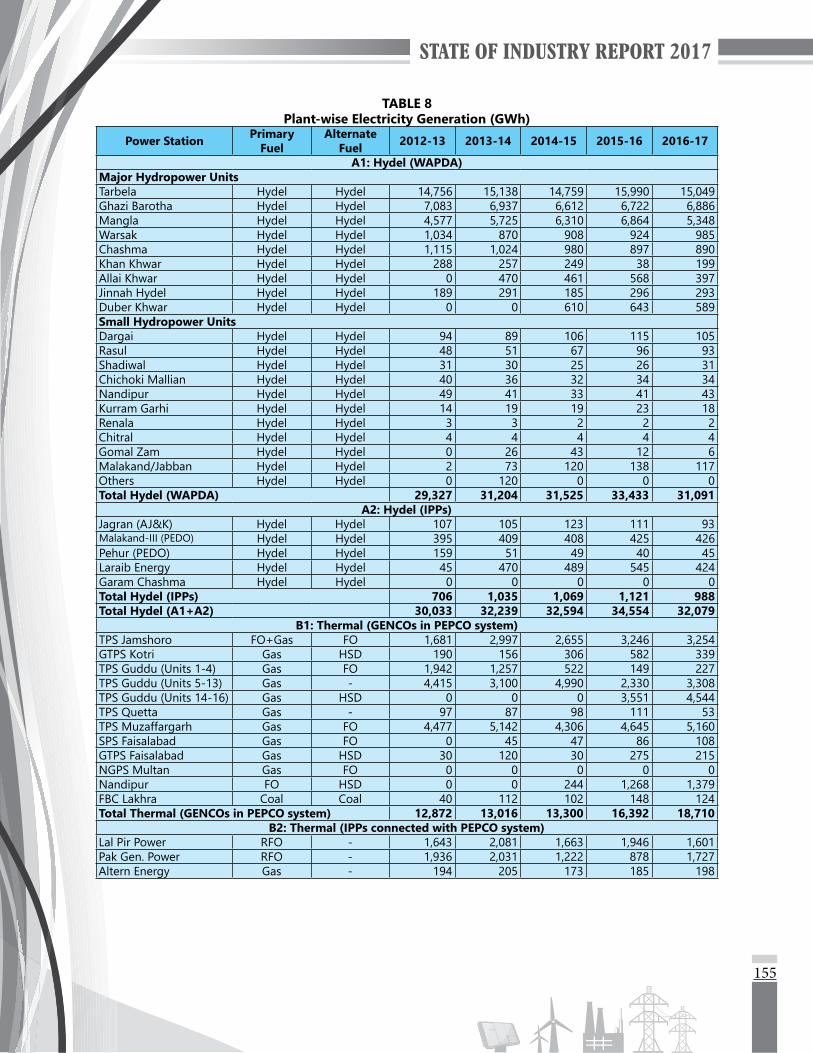

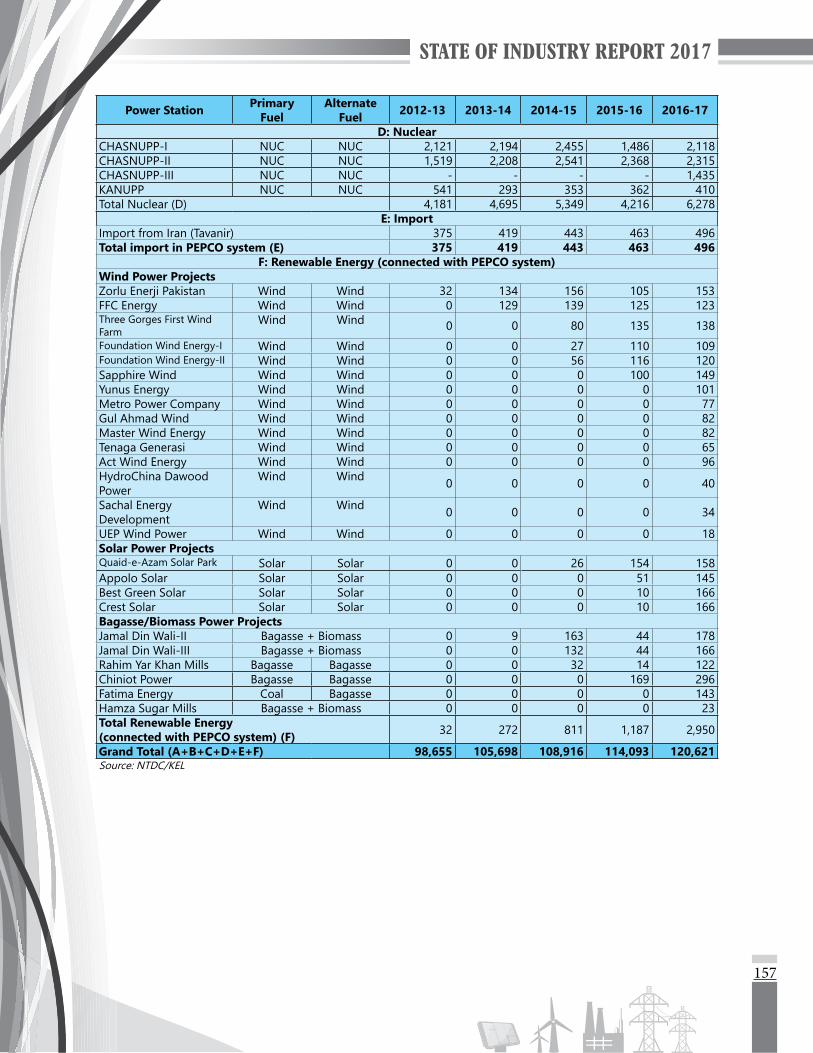

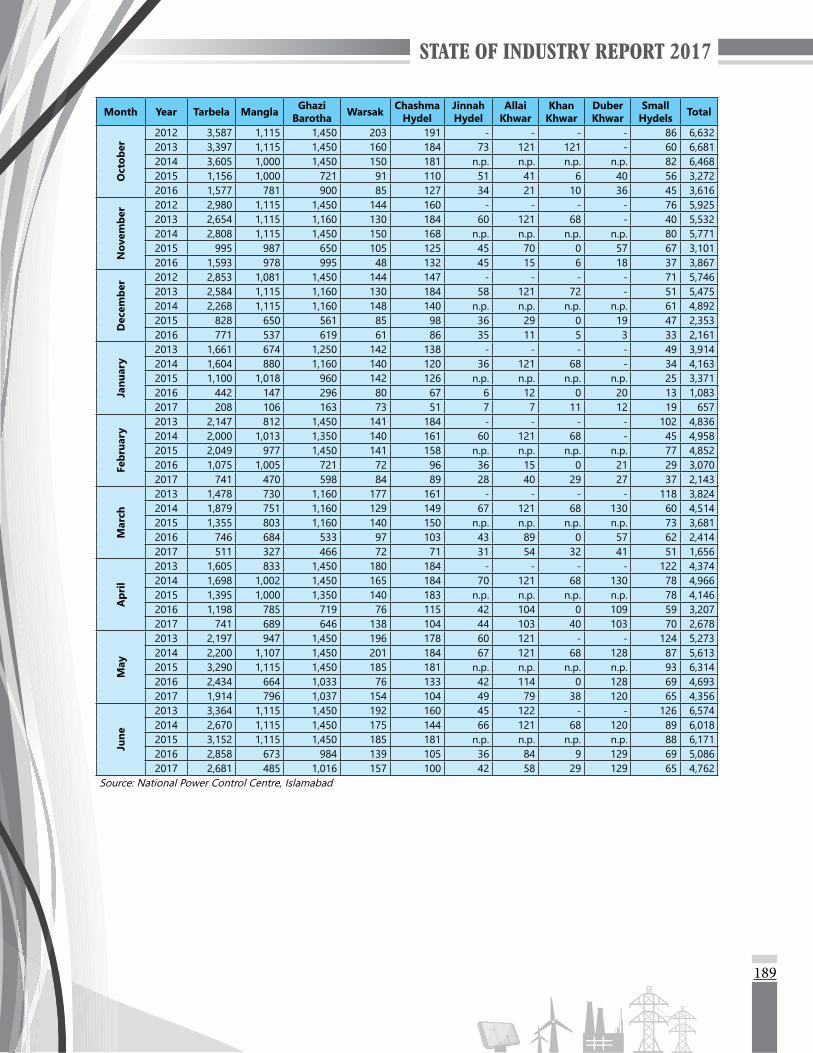

1.5.1.5 Hydropower:The installed capacity of WAPDA Hydropower remained at 6,902 MW in the years 2015, 2016 and 2017; however, the 31,091 GWh generated in the FY 2016-17, shows a decrease of 2,342 GWh from the last year. The decrease in energy production may be attributed to water availability and irrigation releases from large reservoir based power plants. Similarly, the Hydel IPPs also contributed 133 GWh less in the system during the FY 2016-17 with the same installed capacity as in the FY 2015-16. As for performance of major public sector hydropower plants including Tarbela,andMangla,thatiscomparablewithinternationalstandardsofefficiency,availabilityandauxiliary consumption levels. The hydropower energy production pattern over the year remained consistent with the historical trends.

1.5.1.5.1 Power Purchase Agreements/Energy Purchase Agreements:NEPRA has approved the PPAs of two large hydropower projects under Section 5 of “NEPRA Interim Power Procurement (Procedure and Standards) Regulations, 2005”. Details of these projects are given below:

S. No. Project Name Capacity (MW) Power Purchaser1 Karot Hydropower Project 720 CPPA-G2 Suki Kinari Hydropower Project 870 CPPA-G

1.5.1.5.2 Competitive Bidding of Hydropower Projects:NEPRA has approved the Request for Proposal (RFP) of Taunsa Hydropower Project and six other projectsidentifiedbyPEDOundertheCompetitiveBiddingTariff(ApprovalProcedure)Regulations

13

(CBTR), 2014. Subsequently, the bidding under CBTR-2014 for Taunsa Hydropower Project was successfullycompletedandtheAuthorityhasaccordinglynotifiedthelowestsuccessfulbidder.ThiswasthefirstpowergenerationprojectwhosetariffhasbeendeterminedthroughCompetitiveBidding in Pakistan’s power sector.

1.5.1.5.3 Performance Monitoring of Hydropower Projects:The monitoring of different hydropower projects was carried out in the year 2017 to check their performance according to the terms and conditions set in Licence, PPA, Tariff Determination and other relevant rules and regulations.

NEPRA has noted the unsatisfactory performance of Malakand-III (81 MW), Jinnah (96 MW) and Khan Khwar (72 MW) Hydropower Plants. The sponsors and the power purchaser have been directed to improve the operation and maintenance of these plants.

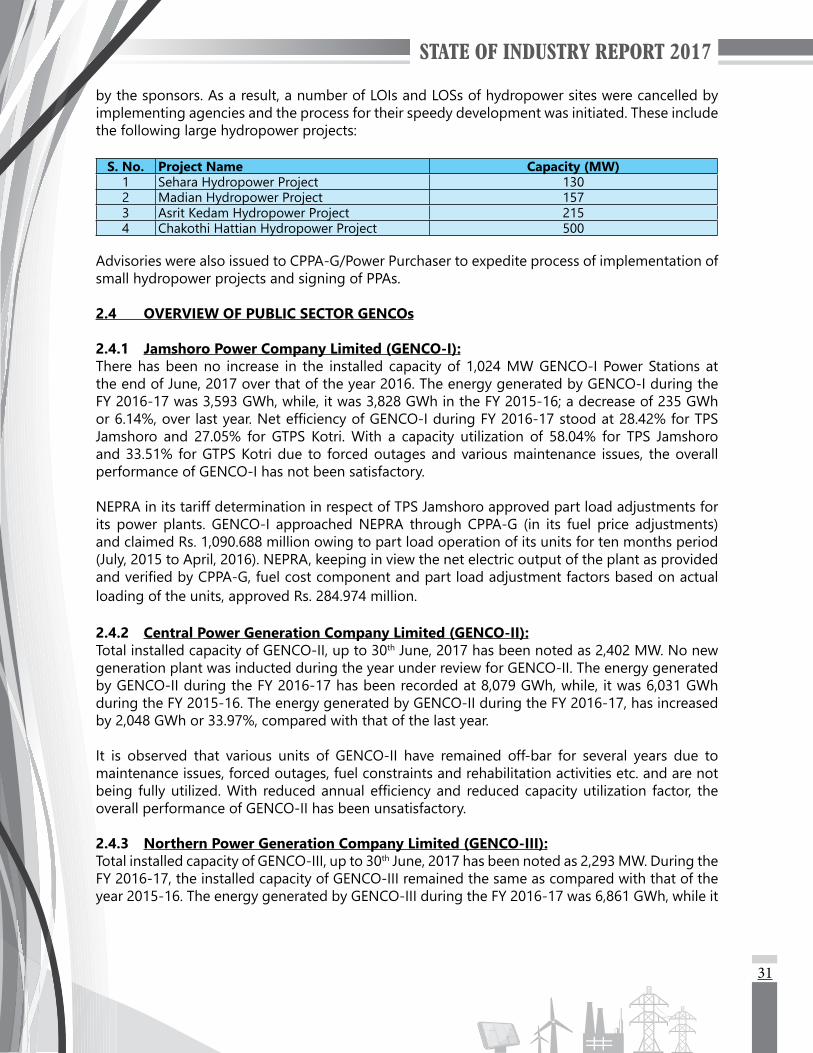

1.5.1.5.4 Implementations of Authority’s Directions:The Authority noted that a number of holders of LOIs for hydropower project sites were inordinately delaying the development of these sites. Accordingly, directions were issued to the relevant agencies to cancel all those LOI/LOS of projects which have been inordinately delayed by the sponsors. As a result, a number of LOIs and LOSs of hydropower sites were cancelled by implementing agencies and the process for their speedy development was initiated. These include the following large hydropower projects:

S. No. Project Name Capacity (MW)

1 Sehara Hydropower Project 1302 Madian Hydropower Project 1573 Asrit Kedam Hydropower Project 2154 Chakothi Hattian Hydropower Project 500

Advisories were also issued to CPPA-G/Power Purchaser to expedite process of implementation of small hydropower projects and signing of PPAs. 1.5.2 Private Sector (Independent Power Producers):Performance of thermal Independent Power Producers (IPPs) remained satisfactory during the FY 2016-17, with respect to the NEPRA Performance Standards (Generation) Rules, 2009. Further details may be found in subsequent chapters of the report.

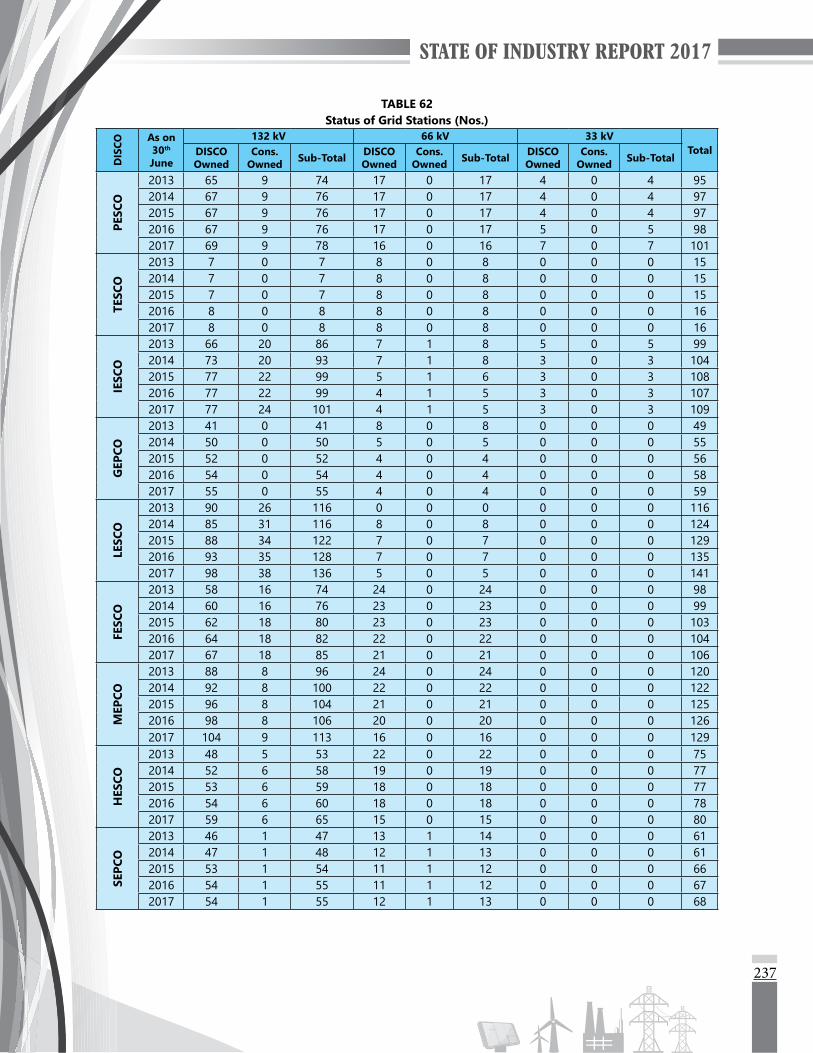

1.6 TRANSMISSION SYSTEMAs of 30th June 2017, NTDC is maintaining 14 (fourteen) 500 kV grid stations with a transformation capacityof18,624MVA.Thereare33(thirtythree)500/220kVtransformersand35(thirtyfive)220/132 kV transformers installed at these grid stations. At 220 kV level there are 38 grid stations with a transformation capacity of 25,660 MVA. There are 108 (one hundred eight) 220/132 kV transformers installed at 220 kV grid stations.

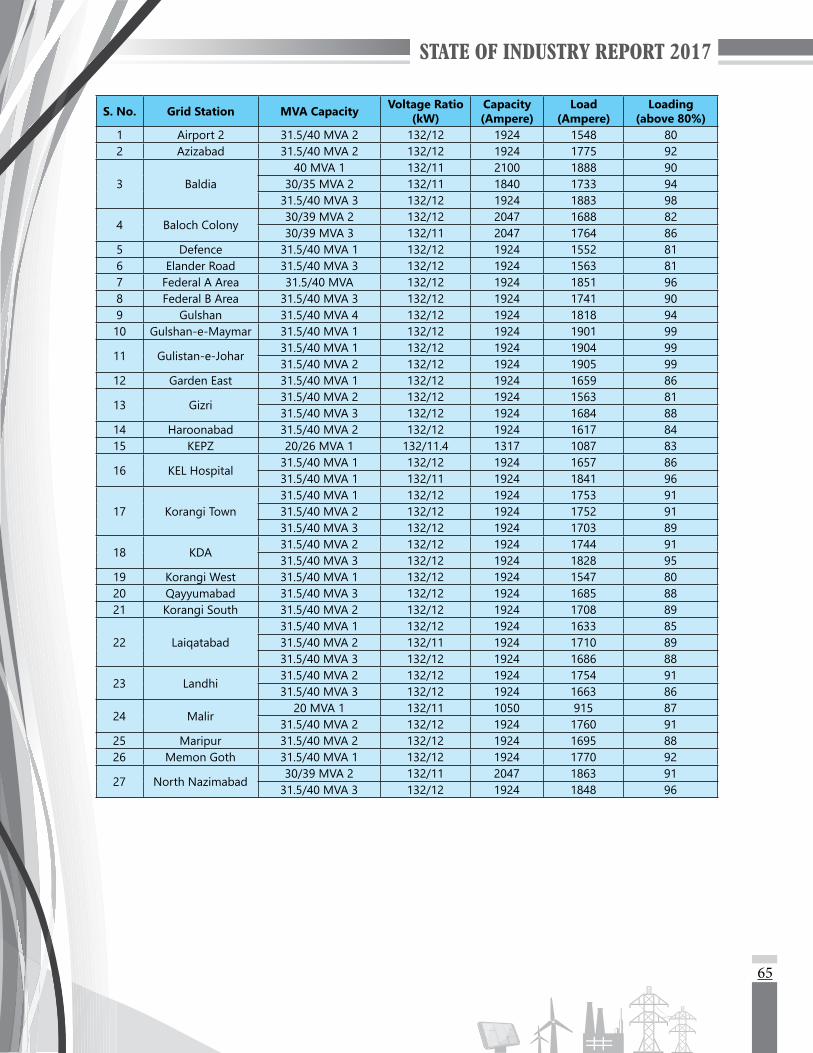

Out of 33 transformers at 500/220 kV level, 13 transformers (39%) are loaded above 80% of their rated capacity. Similarly, out of 143 (one hundred forty three) 220/132 kV transformers, 79 transformers are overloaded, representing around 55% overloading in the system.

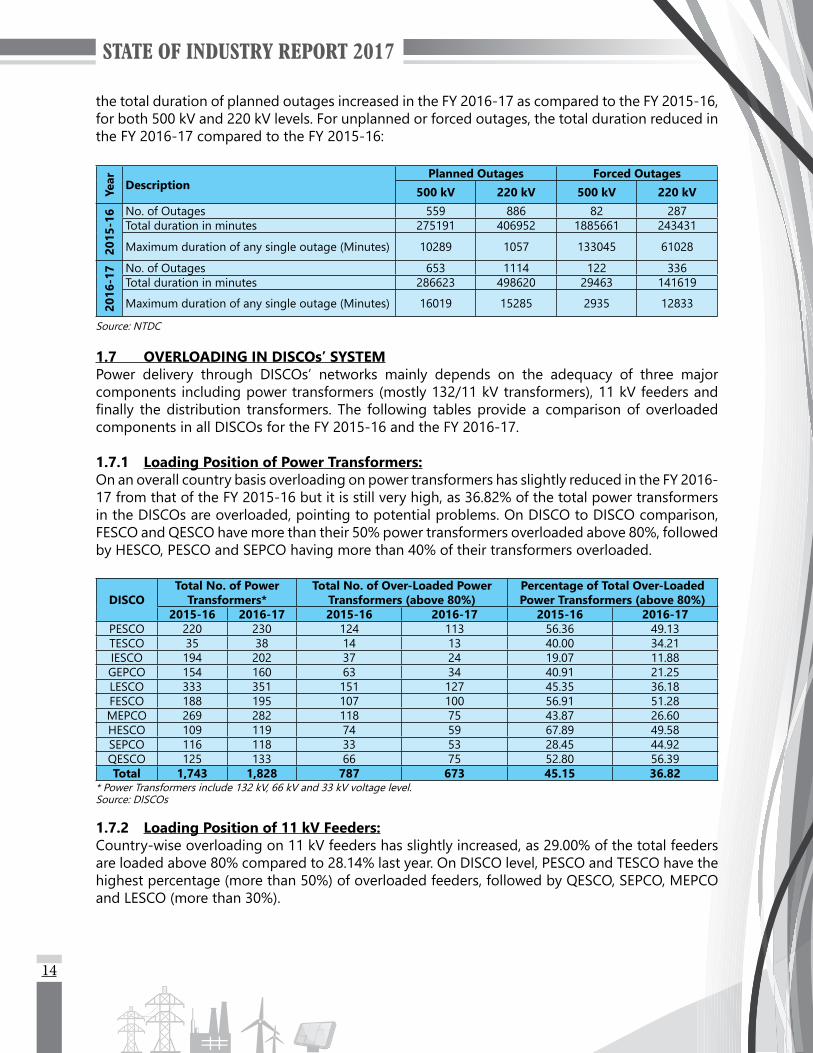

1.6.1 Outages on NTDC Transmission Lines (500 kV and 220 kV):As reported by NTDC the number of planned and unplanned outages in the FY 2016-17 have increased as compared to the FY 2015-16 at 500 kV and 220 kV levels. As for duration of outages

14

the total duration of planned outages increased in the FY 2016-17 as compared to the FY 2015-16, for both 500 kV and 220 kV levels. For unplanned or forced outages, the total duration reduced in the FY 2016-17 compared to the FY 2015-16:

Year Description

Planned Outages Forced Outages500 kV 220 kV 500 kV 220 kV

2015

-16 No. of Outages 559 886 82 287

Total duration in minutes 275191 406952 1885661 243431

Maximum duration of any single outage (Minutes) 10289 1057 133045 61028

2016

-17 No. of Outages 653 1114 122 336

Total duration in minutes 286623 498620 29463 141619

Maximum duration of any single outage (Minutes) 16019 15285 2935 12833

Source: NTDC

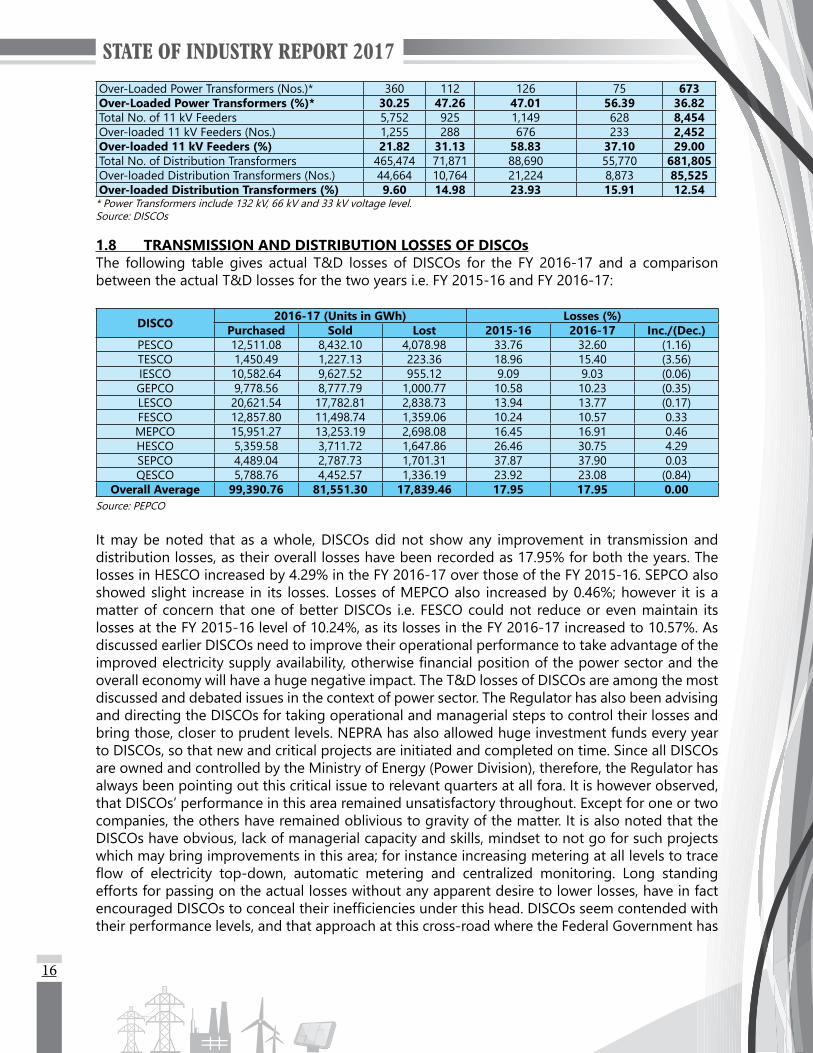

1.7 OVERLOADING IN DISCOs’ SYSTEMPower delivery through DISCOs’ networks mainly depends on the adequacy of three major components including power transformers (mostly 132/11 kV transformers), 11 kV feeders and finally thedistribution transformers. The following tablesprovidea comparisonofoverloadedcomponents in all DISCOs for the FY 2015-16 and the FY 2016-17.

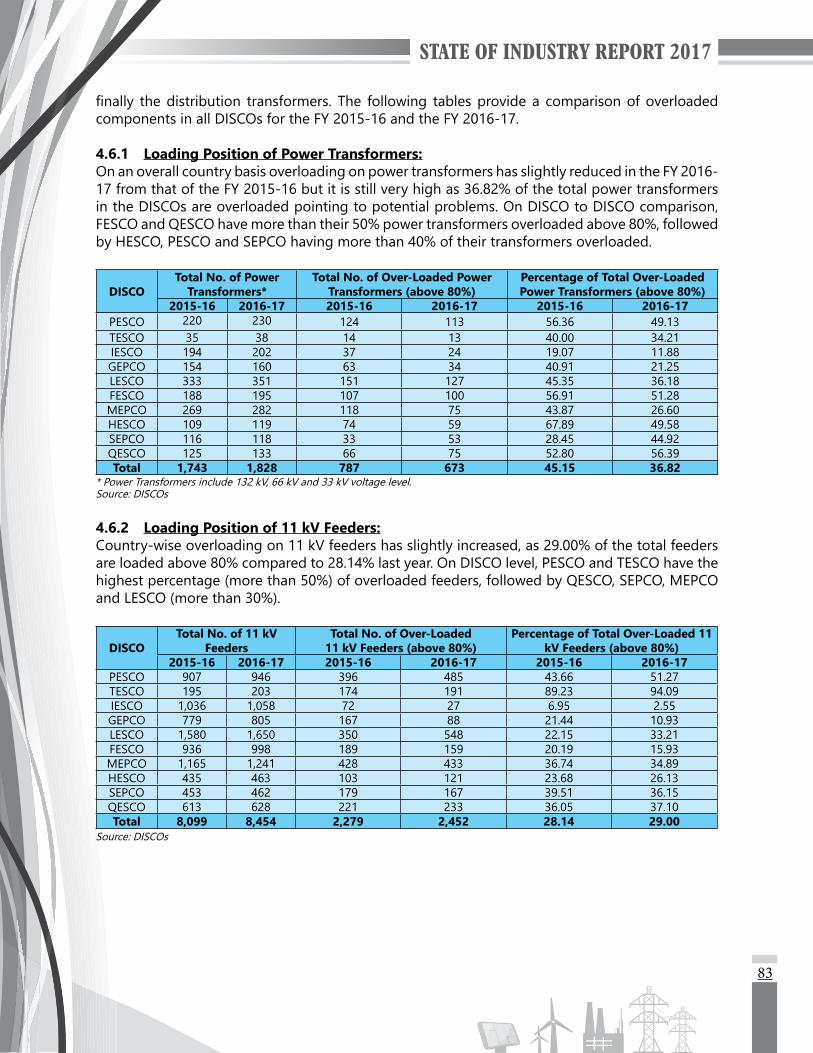

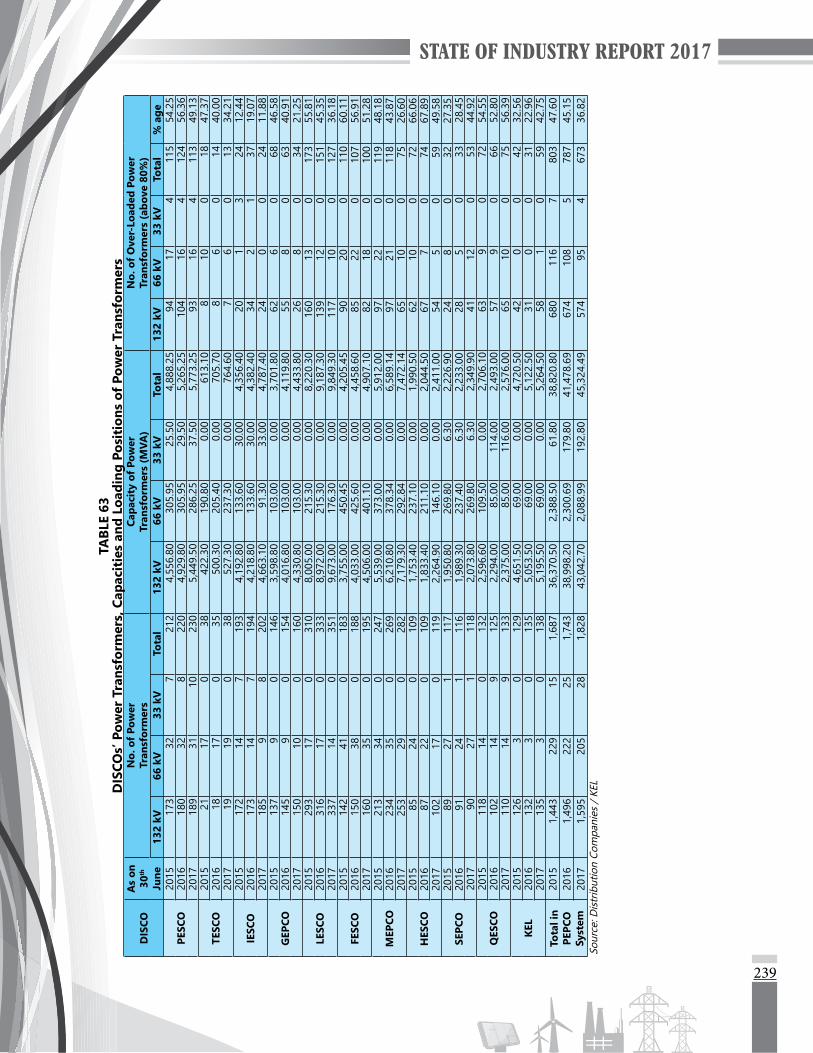

1.7.1 Loading Position of Power Transformers:On an overall country basis overloading on power transformers has slightly reduced in the FY 2016-17 from that of the FY 2015-16 but it is still very high, as 36.82% of the total power transformers in the DISCOs are overloaded, pointing to potential problems. On DISCO to DISCO comparison, FESCO and QESCO have more than their 50% power transformers overloaded above 80%, followed by HESCO, PESCO and SEPCO having more than 40% of their transformers overloaded.

DISCOTotal No. of Power

Transformers*Total No. of Over-Loaded Power

Transformers (above 80%)Percentage of Total Over-Loaded Power Transformers (above 80%)

2015-16 2016-17 2015-16 2016-17 2015-16 2016-17PESCO 220 230 124 113 56.36 49.13TESCO 35 38 14 13 40.00 34.21IESCO 194 202 37 24 19.07 11.88GEPCO 154 160 63 34 40.91 21.25LESCO 333 351 151 127 45.35 36.18FESCO 188 195 107 100 56.91 51.28MEPCO 269 282 118 75 43.87 26.60HESCO 109 119 74 59 67.89 49.58SEPCO 116 118 33 53 28.45 44.92QESCO 125 133 66 75 52.80 56.39Total 1,743 1,828 787 673 45.15 36.82

* Power Transformers include 132 kV, 66 kV and 33 kV voltage level.Source: DISCOs

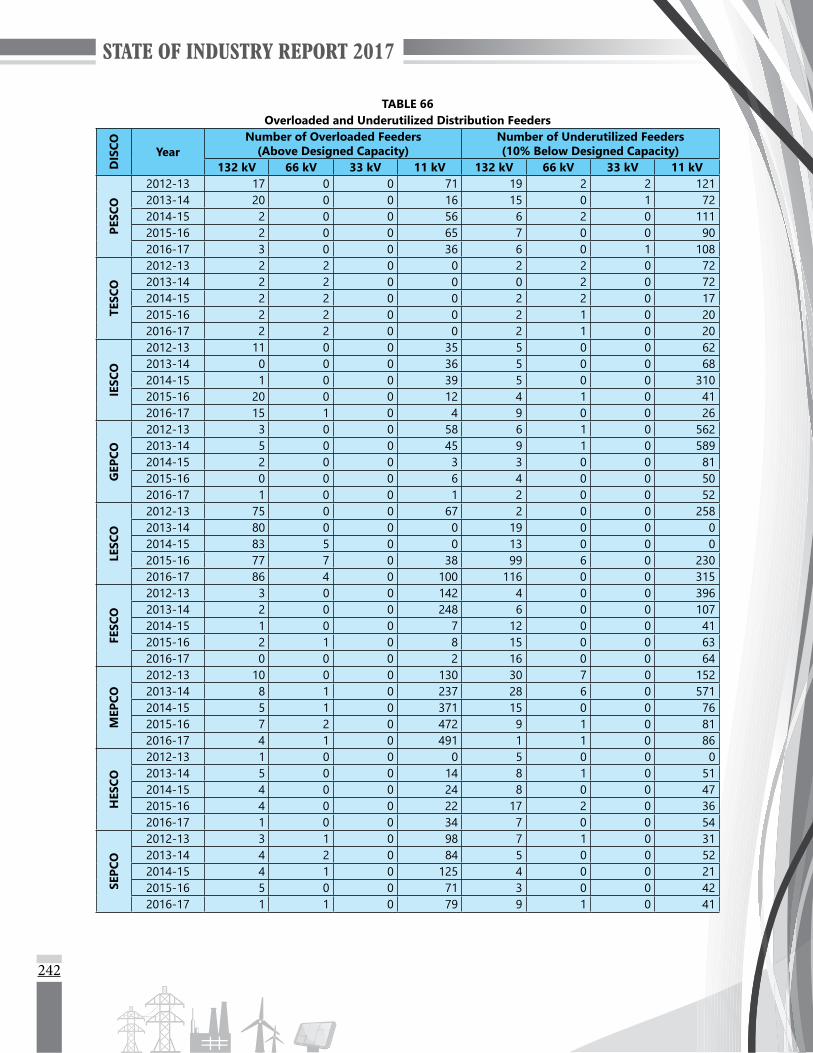

1.7.2 Loading Position of 11 kV Feeders:Country-wise overloading on 11 kV feeders has slightly increased, as 29.00% of the total feeders are loaded above 80% compared to 28.14% last year. On DISCO level, PESCO and TESCO have the highest percentage (more than 50%) of overloaded feeders, followed by QESCO, SEPCO, MEPCO and LESCO (more than 30%).

15

DISCOTotal No. of 11 kV

FeedersTotal No. of Over-Loaded

11 kV Feeders (above 80%)Percentage of Total Over-Loaded

11 kV Feeders (above 80%)2015-16 2016-17 2015-16 2016-17 2015-16 2016-17

PESCO 907 946 396 485 43.66 51.27TESCO 195 203 174 191 89.23 94.09IESCO 1,036 1,058 72 27 6.95 2.55GEPCO 779 805 167 88 21.44 10.93LESCO 1,580 1,650 350 548 22.15 33.21FESCO 936 998 189 159 20.19 15.93MEPCO 1,165 1,241 428 433 36.74 34.89HESCO 435 463 103 121 23.68 26.13SEPCO 453 462 179 167 39.51 36.15QESCO 613 628 221 233 36.05 37.10Total 8,099 8,454 2,279 2,452 28.14 29.00

Source: DISCOs

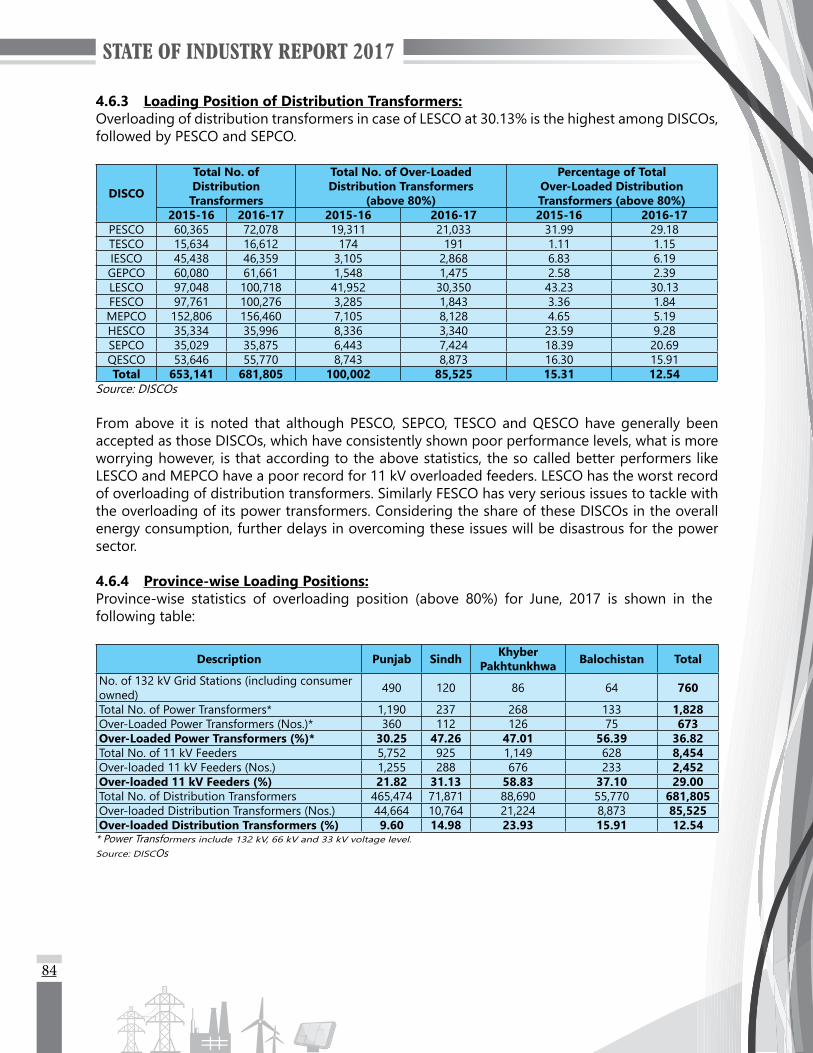

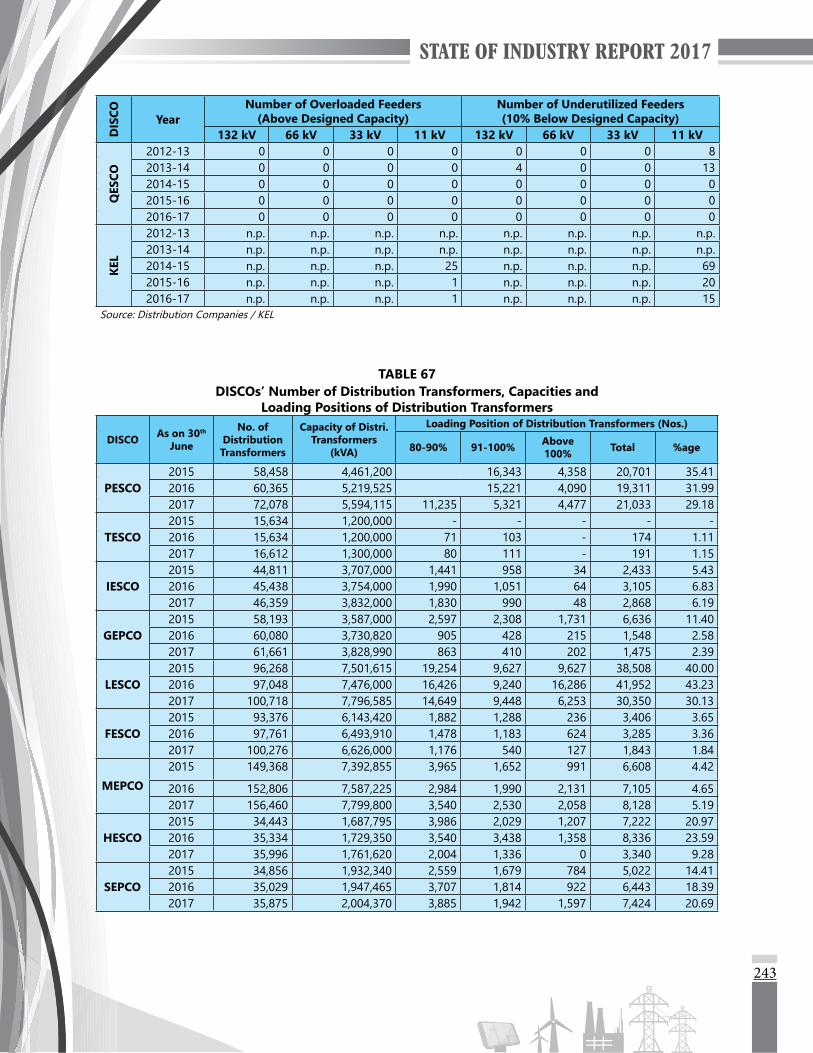

1.7.3 Loading Position of Distribution Transformers:Overloading of distribution transformers in case of LESCO at 30.13% is the highest among DISCOs, followed by PESCO and SEPCO.

DISCO

Total No. of Distribution Transformers

Total No. of Over-Loaded Distribution Transformers

(above 80%)

Percentage of TotalOver-Loaded Distribution Transformers (above 80%)

2015-16 2016-17 2015-16 2016-17 2015-16 2016-17PESCO 60,365 72,078 19,311 21,033 31.99 29.18TESCO 15,634 16,612 174 191 1.11 1.15IESCO 45,438 46,359 3,105 2,868 6.83 6.19GEPCO 60,080 61,661 1,548 1,475 2.58 2.39LESCO 97,048 100,718 41,952 30,350 43.23 30.13FESCO 97,761 100,276 3,285 1,843 3.36 1.84MEPCO 152,806 156,460 7,105 8,128 4.65 5.19HESCO 35,334 35,996 8,336 3,340 23.59 9.28SEPCO 35,029 35,875 6,443 7,424 18.39 20.69QESCO 53,646 55,770 8,743 8,873 16.30 15.91Total 653,141 681,805 100,002 85,525 15.31 12.54

Source: DISCOs

From above it is noted that although PESCO, SEPCO, TESCO and QESCO have generally been accepted as those DISCOs, which have consistently shown poor performance levels, what is more worrying however, is that according to the above statistics, the so called better performers like LESCO and MEPCO have a poor record for 11 kV overloaded feeders. LESCO has the worst record of overloading of distribution transformers. Similarly FESCO has very serious issues to tackle with the overloading of its power transformers. Considering the share of these DISCOs in the overall energy consumption, further delays in overcoming these issues will be disastrous for the power sector.

1.7.4 Province-wise Loading Positions:Province-wise statistics of overloading position (above 80%) for June, 2017 is shown in the following table:

Description Punjab Sindh Khyber Pakhtunkhwa Balochistan Total

No. of 132 kV Grid Stations (including consumer owned) 490 120 86 64 760

Total No. of Power Transformers* 1,190 237 268 133 1,828

16

Over-Loaded Power Transformers (Nos.)* 360 112 126 75 673Over-Loaded Power Transformers (%)* 30.25 47.26 47.01 56.39 36.82Total No. of 11 kV Feeders 5,752 925 1,149 628 8,454Over-loaded 11 kV Feeders (Nos.) 1,255 288 676 233 2,452Over-loaded 11 kV Feeders (%) 21.82 31.13 58.83 37.10 29.00Total No. of Distribution Transformers 465,474 71,871 88,690 55,770 681,805Over-loaded Distribution Transformers (Nos.) 44,664 10,764 21,224 8,873 85,525Over-loaded Distribution Transformers (%) 9.60 14.98 23.93 15.91 12.54

* Power Transformers include 132 kV, 66 kV and 33 kV voltage level.Source: DISCOs

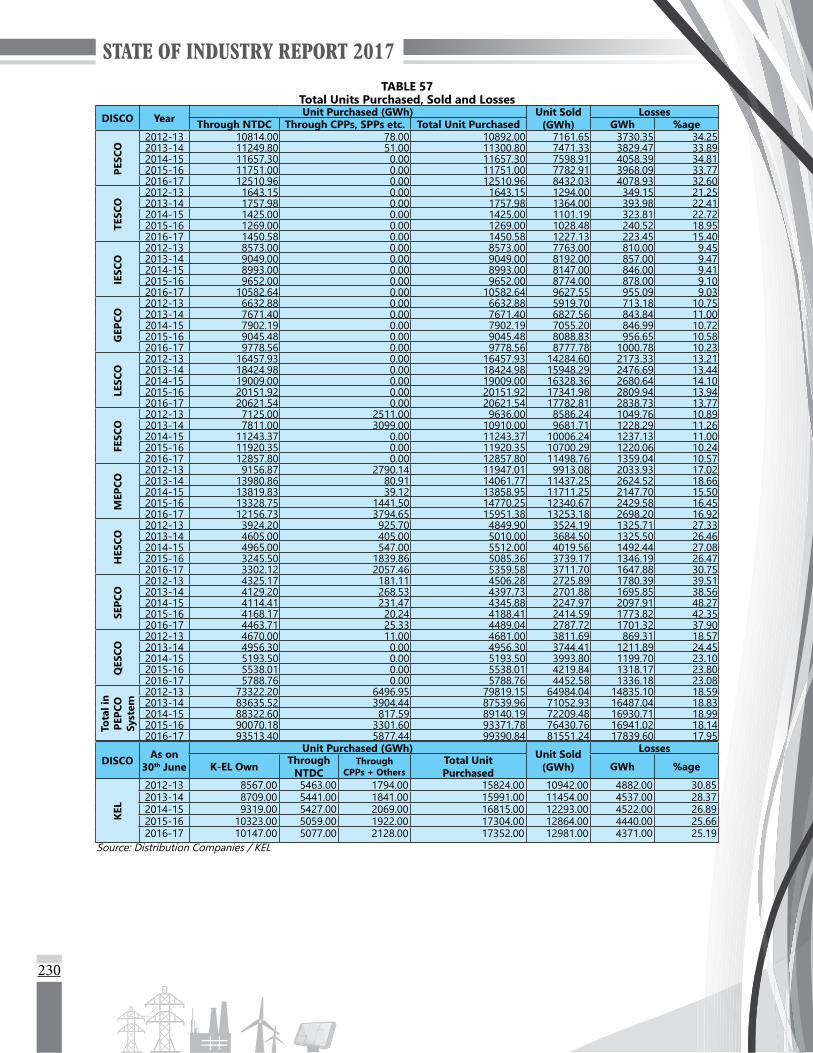

1.8 TRANSMISSION AND DISTRIBUTION LOSSES OF DISCOsThe following table gives actual T&D losses of DISCOs for the FY 2016-17 and a comparison between the actual T&D losses for the two years i.e. FY 2015-16 and FY 2016-17:

DISCO 2016-17 (Units in GWh) Losses (%)Purchased Sold Lost 2015-16 2016-17 Inc./(Dec.)

PESCO 12,511.08 8,432.10 4,078.98 33.76 32.60 (1.16)TESCO 1,450.49 1,227.13 223.36 18.96 15.40 (3.56)IESCO 10,582.64 9,627.52 955.12 9.09 9.03 (0.06)GEPCO 9,778.56 8,777.79 1,000.77 10.58 10.23 (0.35)LESCO 20,621.54 17,782.81 2,838.73 13.94 13.77 (0.17)FESCO 12,857.80 11,498.74 1,359.06 10.24 10.57 0.33MEPCO 15,951.27 13,253.19 2,698.08 16.45 16.91 0.46HESCO 5,359.58 3,711.72 1,647.86 26.46 30.75 4.29SEPCO 4,489.04 2,787.73 1,701.31 37.87 37.90 0.03QESCO 5,788.76 4,452.57 1,336.19 23.92 23.08 (0.84)

Overall Average 99,390.76 81,551.30 17,839.46 17.95 17.95 0.00Source: PEPCO

It may be noted that as a whole, DISCOs did not show any improvement in transmission and distribution losses, as their overall losses have been recorded as 17.95% for both the years. The losses in HESCO increased by 4.29% in the FY 2016-17 over those of the FY 2015-16. SEPCO also showed slight increase in its losses. Losses of MEPCO also increased by 0.46%; however it is a matter of concern that one of better DISCOs i.e. FESCO could not reduce or even maintain its losses at the FY 2015-16 level of 10.24%, as its losses in the FY 2016-17 increased to 10.57%. As discussed earlier DISCOs need to improve their operational performance to take advantage of the improvedelectricitysupplyavailability,otherwisefinancialpositionofthepowersectorandtheoverall economy will have a huge negative impact. The T&D losses of DISCOs are among the most discussed and debated issues in the context of power sector. The Regulator has also been advising and directing the DISCOs for taking operational and managerial steps to control their losses and bring those, closer to prudent levels. NEPRA has also allowed huge investment funds every year to DISCOs, so that new and critical projects are initiated and completed on time. Since all DISCOs are owned and controlled by the Ministry of Energy (Power Division), therefore, the Regulator has always been pointing out this critical issue to relevant quarters at all fora. It is however observed, that DISCOs’ performance in this area remained unsatisfactory throughout. Except for one or two companies, the others have remained oblivious to gravity of the matter. It is also noted that the DISCOs have obvious, lack of managerial capacity and skills, mindset to not go for such projects which may bring improvements in this area; for instance increasing metering at all levels to trace flow of electricity top-down, automatic metering and centralized monitoring. Long standingefforts for passing on the actual losses without any apparent desire to lower losses, have in fact encouragedDISCOstoconcealtheirinefficienciesunderthishead.DISCOsseemcontendedwiththeir performance levels, and that approach at this cross-road where the Federal Government has

17

inducted a large generation capacity to the system may drag the whole sector down if immediate steps to correct this position are not taken.

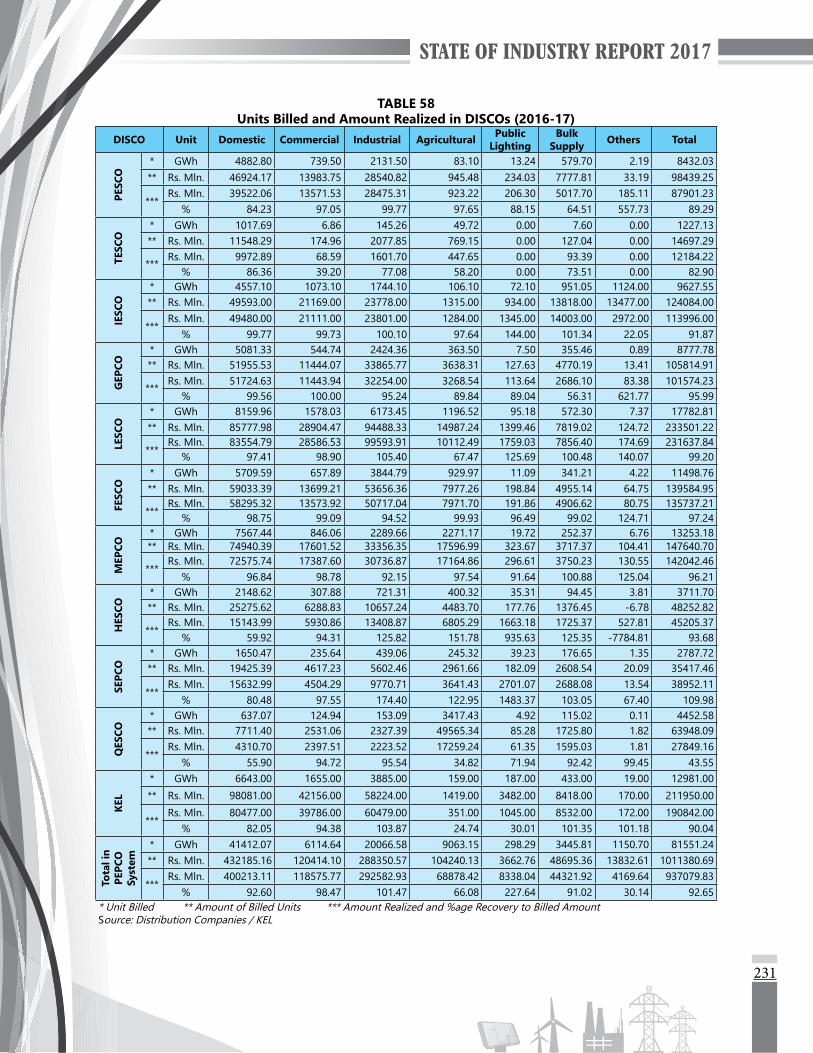

1.9 RECOVERY POSITION OF DISCOsThe following table shows a comparison of recovery ratios for all the DISCOs for the two years. It may be seen that apart from HESCO, PESCO and IESCO who improved upon their recovery position, none of the other DISCOs was able to improve its position over the previous year. LESCO managed to stay at the same level of good recovery ratio in the FY 2016-17, whereas FESCO, MEPCO and GEPCO could not match their performance of the last year as their recovery dropped by approximately 3% during the FY 2016-17. QESCO’s recovery position deteriorated drastically during the FY 2016-17 as only 43.55% of the amount billed was recovered. SEPCO though showed more than 100% recovery but in fact it is due to certain adjustment made with the Government of Sindhwhichhasinflatedthetruerecoveryfortheyear.

(%)

Year PESCO TESCO IESCO GEPCO LESCO FESCO MEPCO HESCO SEPCO QESCO OverallDISCO

2015-16 88.49 436.97* 91.14 99.41 99.20 100.06 99.99 72.09 55.18 71.62 94.482016-17 89.29 82.90 91.87 95.99 99.20 97.24 96.21 93.68 109.98 43.55 92.65

* Source payment received against billing of Private Domestic TESCO consumers for Rs. 18,955.61 million in 2015-16 from Federal Government.Source: DISCOs

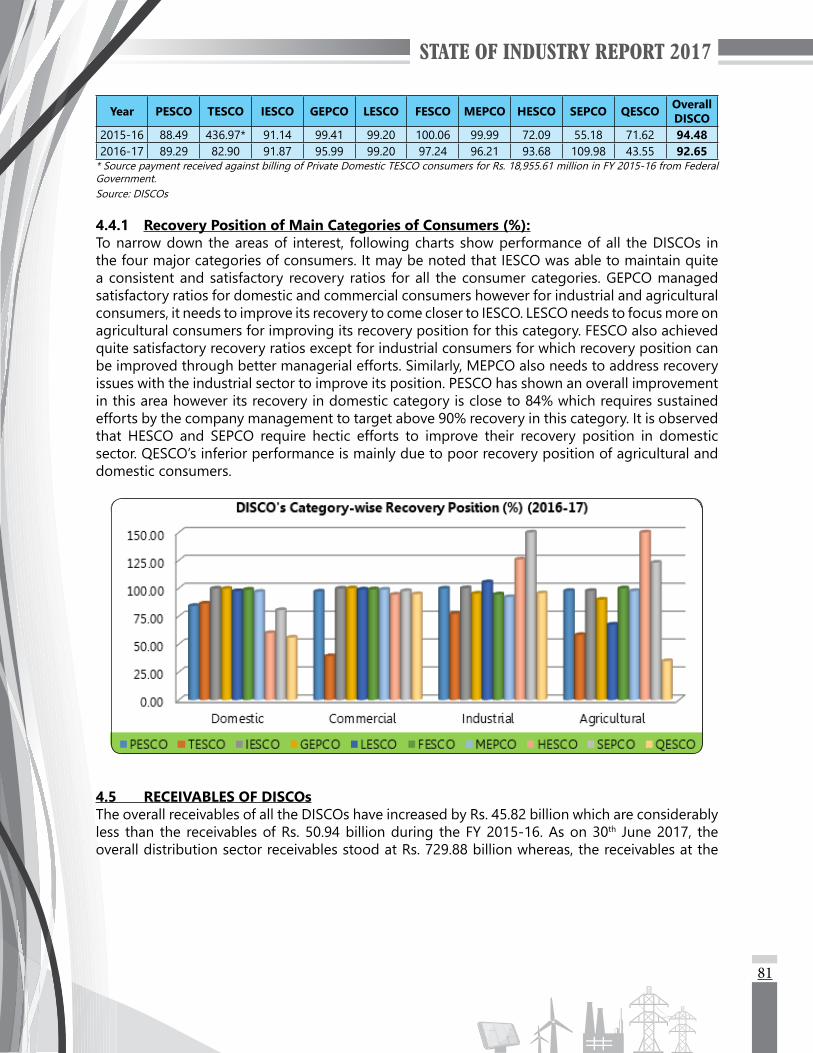

1.9.1 Recovery Position of Main Categories of Consumers (%):To narrow down the areas of interest, following charts show performance of all the DISCOs in the four major categories of consumers. It may be noted that IESCO was able to maintain quite a consistent and satisfactory recovery ratios for all the consumer categories. GEPCO managed satisfactory ratios for domestic and commercial consumers however for industrial and agricultural consumers, it needs to improve its recovery to come closer to IESCO. LESCO needs to focus more on agricultural consumers for improving its recovery position for this category. FESCO also achieved quite satisfactory recovery ratios except for industrial consumers for which recovery position can be improved through better managerial efforts. Similarly, MEPCO also needs to address recovery issues with the industrial sector to improve its position. PESCO has shown an overall improvement in this area, however its recovery in domestic category is close to 84% which requires sustained efforts by the company management to target above 90% recovery in this category. It is observed that HESCO and SEPCO require hectic efforts to improve their recovery position in domestic sector. QESCO’s inferior performance is mainly due to poor recovery position of agricultural and domestic consumers.

18

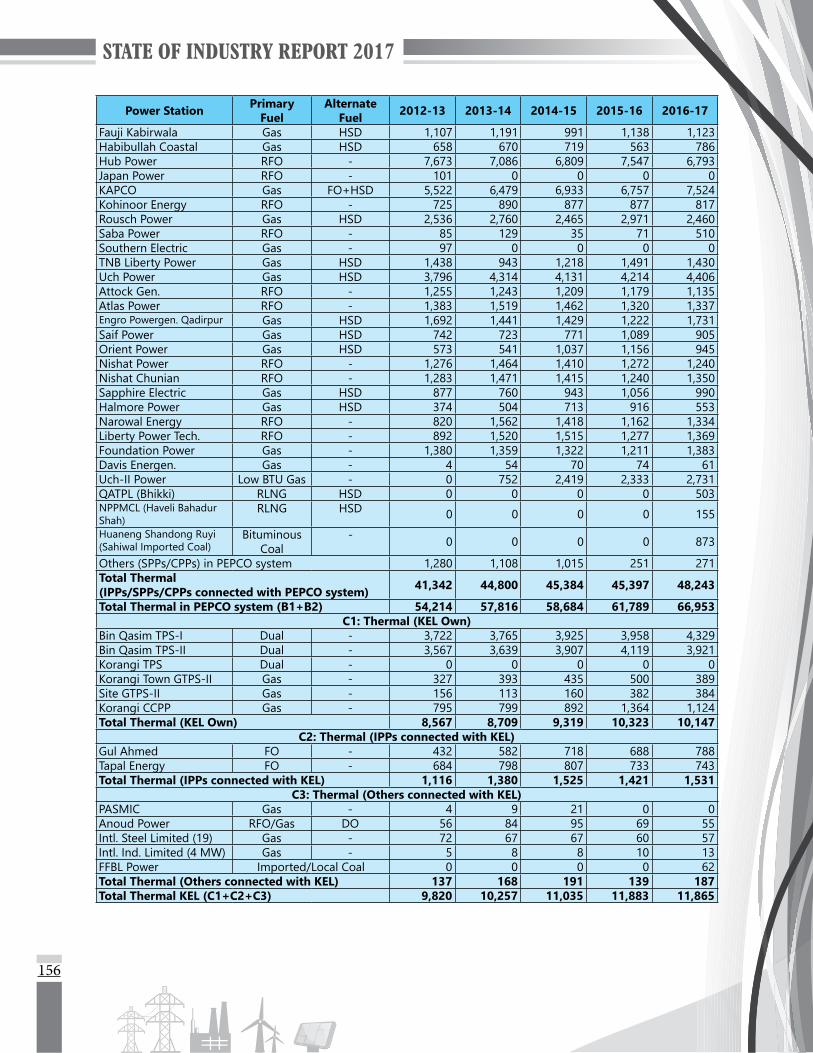

1.10 PERFORMANCE OF K-ELECTRIC LIMITEDBy March 2018, KEL had installed capacity of 2,261 MW through its own power plants whereas IPPs and CPPs add another 442 MW to KEL system. In addition to 137 MW KANUPP power plant, NTDC is also providing 650 MW to KEL system. Due to aging and deterioration in generation facilities, KEL’s present capacity is reported as 1,973 MW. Since KEL is responsible for maintaining integrated systems of generation, transmission and distribution, therefore it is required to look for other sources to meet the supply and demand gap. Inability of KEL to effectively increase its generation capacity has made it dependent on external power sources, including the import from NTDC system. During the FY 2016-17 also, in addition to purchasing power from IPPs, KEL imported around 650 MW of power from NTDC on regular basis. Although the agreement between NTDC and KEL for power purchase has already expired, the power is still being supplied to meet the requirement of KEL consumers.

The energy generated during the FY 2016-17 through KEL own power plants is noted as 10,147 GWhwhichshowsadecreaseof176GWhascomparedtothepreviousyearfigure i.e.10,323GWh; a decrease of 1.7%.

During the year KEL continued to underutilize its own generation power plants and it was also noted to ignore merit order operation of its power plants. The Authority initiated relevant proceedings under its law to address the matter.

KEL reportedly faced gas supply issues which added to problems of the utility, as the KEL power plants during the FY 2016-17 used 55,016 MMCFT of gas, which is lower by 11,867 MMCFT as compared to its gas consumption during the FY 2015-16.

ItmaybenotedthatKELwasabletoimprovetheaverageefficiencyofitsgenerationfleetfrom30.4%in2009topresentlevelsof37%in2017.ThedesignthermalefficiencyofsomeunitsofBQPS-I on oil and gas were 37.5% and 36% respectively. Owing to lack of proper O&M practices, thecurrentaverageefficiencyofBQPS-Iishoveringaround33.64%whichalthoughisbetterthanGENCOs’similarplants,havingefficienciesintherangeof24%to32%butwhencomparedtotheefficiencyof38.60%asallowedtoprivatepowerplantsunder1994PowerPolicy,theefficiencyand availability levels of KEL are not satisfactory.

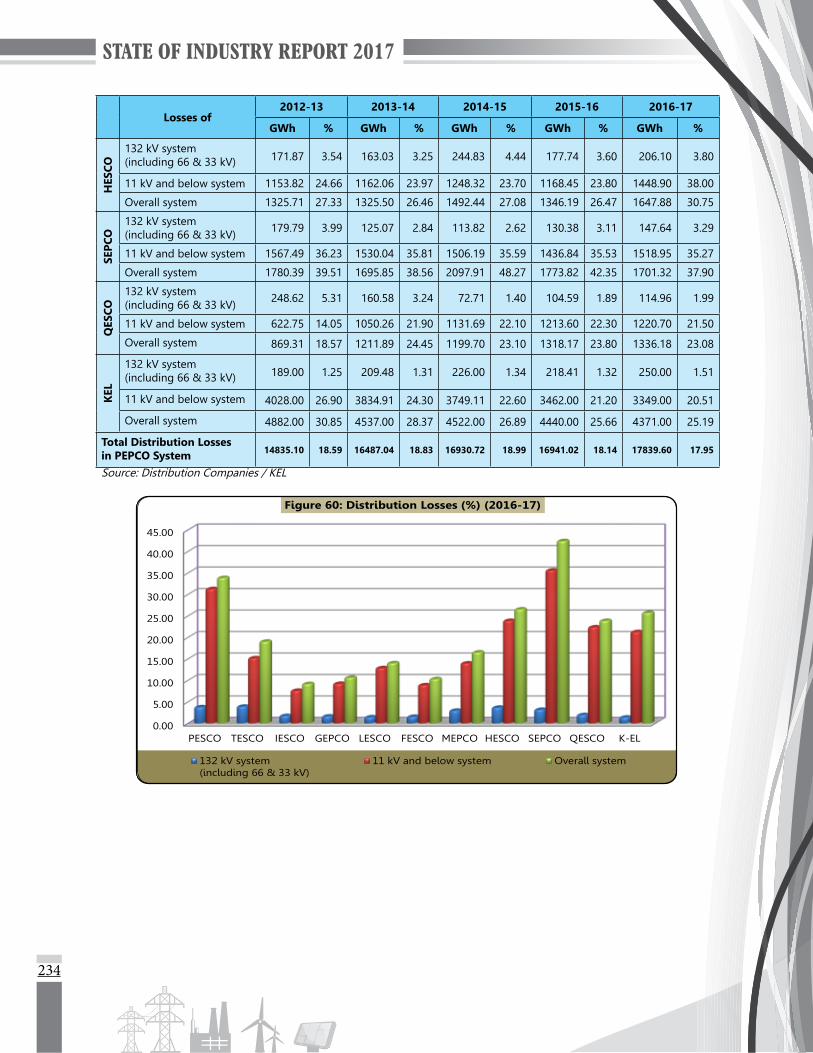

1.10.1 Loading Position of Power Transformers, 11 kV Feeders and Distribution Transformers:The following table provides overloading positions (above 80%) of overloaded components in KEL for the FY 2015-16 and the FY 2016-17:

Description 2015-16 2016-17Total No. of Over-Loaded Power Transformers (above 80%) 31 59Percentage of Total Over-Loaded Power Transformers (above 80%) 22.63 42.75Total No. of Over-Loaded 11 kV Feeders (above 80%) 104 91Percentage of Total Over-Loaded 11 kV Feeders (above 80%) 6.82 5.51Total No. of Over-Loaded Distribution Transformers (above 80%) 648 551Percentage of Total Over-Loaded Distribution Transformers (above 80%) 2.78 2.15

Source: KEL

It is noted that more than 40% power transformers of KEL are overloaded in the FY 2016-17, whereas in the FY 2015-16 approximately 22% transformers were noted to be operating above 80%

19

of their rated capacity. It may be concluded that KEL has not added enough power transformers in its network to maintain at least the same ratio of overloaded transformers as of last year, whereas it was required to maintain a system capable of providing a reliable supply at all times for consumers. KEL’s failure to add adequate number of power transformers was among the major reasons for frequent tripping and prolonged load shed hours during the FY 2016-17.

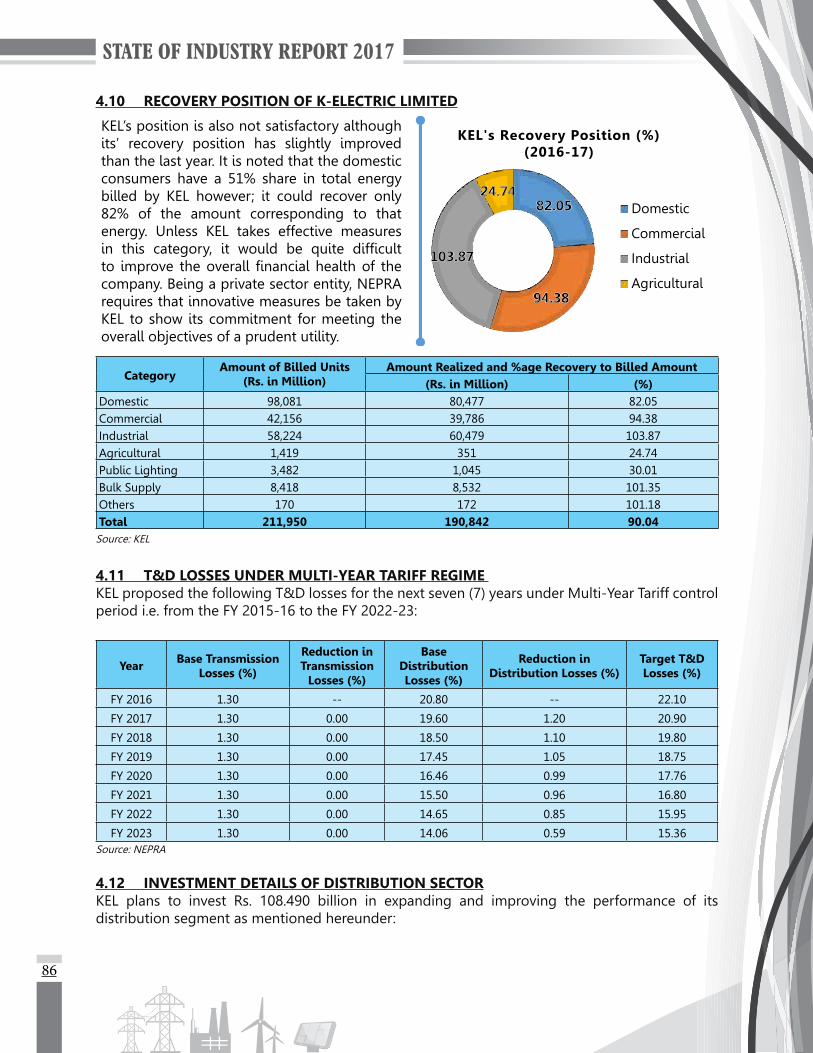

1.10.2 Recovery Position of K-Electric Limited:

KEL’s position is also not satisfactory although its’ recovery position has slightly improved than the last year. It is noted that the domestic consumers have a 51% share in total energy billed by KEL however; it could recover only 82% of the amount corresponding to that energy. Unless KEL takes effective measures in this category, it would be quite difficult to improve the overall financial health of the company. Being a private sector entity, NEPRA requires that innovative measures be taken by KEL to show its commitment for meeting the overall objectives of a prudent utility.

CategoryAmount of Billed Units

(Rs. in Million)Amount Realized and %age Recovery to Billed Amount

(Rs. in Million) (%)Domestic 98,081 80,477 82.05Commercial 42,156 39,786 94.38Industrial 58,224 60,479 103.87Agricultural 1,419 351 24.74Public Lighting 3,482 1,045 30.01Bulk Supply 8,418 8,532 101.35Others 170 172 101.18Total 211,950 190,842 90.04

Source: KEL1.11 THE REGULATION OF GENERATION, TRANSMISSION AND DISTRIBUTION OF

ELECTRIC POWER (AMENDMENT) ACT, 2018The Parliament has recently passed the Regulation of Generation, Transmission and Distribution of Electric Power (Amendment) Act, 2018 [Act No. XII of 2018]. The Amendment Act has restructured and evolved the energy sector in material respects and overhauled the role and responsibilities of NEPRA. The material changes to the law introduced vide the Amendment Act are as follows:

1.11.1 Major Amendments:The qualifying experience of the Chairman and members of the Authority have been reduced from 20 years to 12 years respectively, and the retirement ages of Members and the Chairman from 65 years to 60 years.

The concepts of the National Electricity Policy (formulated by the Federal Government and approved by the CCI) and National Electricity Plan (formulated by the Federal Government in consultation with Provincial Governments) have been introduced in the law. The Authority has to

20

exercise its mandate in accordance with both the Policy and Plan.

The law has further introduced frameworks for establishment and functioning of an Appellate Tribunal, under which all orders and determinations of the Authority shall be appealable.

The major focus of the Amendment Act has been to introduce various market-based frameworks in the energy sector, to create a competitive market regime. The law has introduced new entities, such as the Energy Supplier and Energy Trader, and revised the regulatory regime for existing entities, by introducing the new Market Operator and System Operator Licences. Traditional elements of the energy sector have also been reformed under this spirit, by the provision of a cessation mechanism for all Generation Licences and removal of exclusivity for Distribution Companies.

Flowing from the above, NEPRA’s role in the forthcoming energy sector has also been revised, with a major focus on the regulator’s enforcement powers. The Authority has been granted new enforcement powers of investigation, prohibition orders, issuance of directions and indemnity. In addition, the function of NEPRA as a regulation-making body has also been bolstered, with numerous subject matters falling within the purview of regulations to be exclusively prescribed by the Authority.

With a focus on betterment of end-consumer service, a new consumer complaints officeframeworkhasbeenintroducedinthelaw,underwhichofficesareenvisionedtobeestablishedata district level for overseeing complaints relating to overbilling, metering, theft etc. Concurrently, new penal provisions and offences have been introduced in statute, including the punishment of imprisonment.

1.11.2 Challenges: The abovediscussed reforms represent a significantdeparture from the traditional regulatoryframework under which NEPRA has been functioning for the preceding 20 years. As such, the Authority shall be facing innumerable challenges in effectuating the reforms introduced vide the Amendment Act.

Themost significant revision toNEPRA’s regulatorypurviewunder theAmendmentAct is theintroduction of the National Electricity Policy and Plan, and the Appellate Tribunal. Previously, all functions of the Authority were executed in an independent, impartial and unfettered manner. Now all functions are subject and subservient to both the Policy and Plan, and are directly appealable before the Appellate Tribunal. These frameworks curtail the autonomy of the regulator in material respects. As such, the regulator has to undertake the challenging task of reevaluating and realigning its regulatory functions in accordance with the new legal regime.

TheestablishmentoftheAppellateTribunalanddistrict-levelconsumercomplaintofficespresentfurther challenges for the Authority. The Appellate Tribunal is to be manned by 3 Members with diverse experiences and expertise, and provided in the law. However, it will be challenging for the Tribunal to adjudicate on complex matters that the Authority, with its 100 professionals holding immeasurable cumulative expertise in the sector, itself executes. Moreover, the Tribunal represents an additional layer in the dispensation of justice in an already exhaustive appellate framework. Inaddition,theestablishmentofmorethana100officesforcomplaintsineachdistrictposesamonumental logistical and human resource challenge for the Authority.

21

Various avant-garde concepts have been introduced in the amended law without necessary elaboration. For instance, noparameters for theNational Electricity Plan havebeen specified,the functions/role of the Electricity Trader Licensee have not been provided and the statutory provisions do not explicitly provide for treatment of consumer-end tariffs under the new law. There are also various inconsistencies found in the law, for instance the introduction of uniform tariffs(conflictswithprovisionsrelatingtocompetition)andsavingsunderprecedinglaw(conflictbetween provisions of existing saved licences and statutory provisions). These concerns lay significantchallengesbeforetheAuthorityintheexerciseofitsfunctionsgoingforward.

1.12 ENERGY, ENVIRONMENT AND SUSTAINABLE DEVELOPMENTCognizant of its responsibilities towards protection of environment of the country, in view of planned induction of large coal power plants, NEPRA organized a seminar about Energy, Environment and Sustainable Development. The seminar was attended by representatives from various organizations. The main aim and objectives of the said seminar were as follows:

(a) Awareness about environment among the stakeholders in Pakistan’s power sector; especially after the expected changes in the current energy mix.

(b) Adequacy of existing laws on environment protection and the role of relevant bodies.(c) NEPRA’s role. (d) Way forward.

During the seminar, representatives of Provincial Environmental Protection Agencies (EPAs), discussed about procedural aspects of their departments and showed keen commitment and needforcontinuousmonitoringofupcomingcoalfiredpowerplants.

NEPRA being the regulator of the power sector regularly interacts with relevant EPAs about compliance of their relevant acts. Moreover, NEPRA also obtains compliance reports from the project companies as required under generation licence.

1.13 COMPREHENSIVE REDUCTION AND ELIMINATION OF POLYCHLORINATED BIPHENYLS (PCBs)

Another project to protect environment is in shape of NEPRA’s support to Ministry of Climate Change (MOCC). The objective of MOCC project is to reduce risks for the human health and the environment by avoiding the release of Persistent Organic Pollutants (POPs) in the environment andpreventinghumanexposuretothese.POPscanbedefinedinanumberofwaysincludingthefollowing:

(a) Chemicals with high toxicity originated through anthropogenic activities.(b) Organic chemicals containing carbon and hydrogen are characterized by adverse

effects on life.(c) Bio-accumulation, persistence and long range transport pose a threat to humans

and the environment.(d) POPs are widely used as pesticides and/or industrial chemicals.

The project has been arranged in four components:

(a) Development and Implementation of a Regulatory Policy and Enforcement System to reduce POPs releases.

(b) Capacity building of local communities and public and private sector stakeholders

22

to reduce exposure to and releases of POPs.(c) Collection, Transport and Disposal of PCBs and POPs Pesticides.(d) Monitoring and Evaluation.

NEPRAhasbeencoordinatingwiththepowersectorentitiesandMOCC,essentiallyforidentificationof PCBs, present in power equipment.

1.14 RATIONALIZATION OF GENERATION TARIFF PARAMETERSAs part of its regulatory process, NEPRA has reviewed various tariff components for necessary changes needed therein. This aims to ensure that the power sector tariffs approved and awarded areconsistentand reflectiveofprevailingeconomicandfinancial circumstances that implicatepower generation tariffs approved by NEPRA. After a comprehensive review and discussion with various stakeholders, the Authority has decided to revise certain benchmarks and ceilings to be allowed for tariff components of generation projects. In this respect, the Authority would like to seek input of all stakeholders on these recommendationsbeforethesearefinalizedforapplicationintariffs.FollowingheadshavebeenidentifiedforreviewbytheAuthority:

(a) Banking Spread(b) Debt and Equity Ratios(c) IDC and ROEDC(d) Financing Fee(e) Insurance(f) Withholding Tax on dividends(g) Availability

The Authority in principle continues to move towards promoting the competitive mode in generationtariffs.However,forthespecificprojectstobeconsideredundercostplusregimeandfor certain parameters to be used in upfront tariffs, these benchmarks will be used accordingly.1.15 REVIEW OF RATE OF RETURNNEPRA has decided to review the returns offered in the power sector and prepared a concept paper for determination of the rates of return for the power companies which provided a basis for determining Internal Rate of Return (IRR) for various technologies, value chain of power sector i.e. generation, transmission and distribution and tariff regimes (cost plus, upfront). The basic objectiveisthattheIRRnowneedstobeeffectivelyreflectiveofspecificriskandreturnmatrixand its adjustment for a particular technology. The document was uploaded on NEPRA website for comments from the stakeholders.

1.16 INDUSTRY – ACADEMIA COLLABORATIONNational University of Sciences and Technology (NUST) is working closely with NEPRA on a research proposal namely “Modeling and Simulation of Pakistan’s Electric Power Sector to develop a Road Map for Transition from the Current Single Buyer Model to a Competitive Whole Sale Power Market”.

23

1.17 CONCLUSIONS1.17.1 It is concluded that with the current implementation and planned generation

additions,thecountrywouldhavegenerationcapacitysurpluspositionfornextfivetosixyears;ensuringsufficientmarginsforareliablepowersupply.

1.17.2 The question of dependence on dirty imported fuels has been partly addressed, as no new power plants have been planned on furnace oil and relatively clean fuel of RLNG has been introduced. Similarly, Federal Government has also put a cap on power generation plants using imported coal. However more than 12,000 MW RLNG/Gas based power plants will be expected to use imported RLNG by the FY 2020-21, therefore the power sector consumers will not get any reprieve from the international price uncertainties.

1.17.3 The prices of solar and wind based technology have fallen over past three years, and now their resulting tariffs are quite attractive in comparison with other technologies. Induction of clean energy based projects however, could not take place due to absence of clear policies of the Ministry of Energy (Power Division).

1.17.4 Similarly the induction of small hydropower plants could not take place due to different procedural issues. Due to their robust nature, these plants have useful operating life ofmore thanfiftyyears.Thereforeafter the initialyearsofdebt repayment, theseplants provide a very cheap energy without any dependence on fuel.

1.17.5 With the induction of new generation capacity in the system, it is imperative that every MW of it is optimally used. Transmission and distribution infrastructure must be capable of receiving all available electricity and delivering it to end-consumers. NEPRA notes that networks in NTDC and in most of the DISCOs are not adequate to transmit electricity under different system conditions.

1.17.6 With the addition of new generation facilities over a short span of time, the capacity payments are bound to increase. In order to minimize the impact of increased capacity component in the consumer-end tariff, multi-pronged strategies are needed to be followed.

1.17.7 KEL continued to under-utilize its generation facilities, whereas it failed to add sufficienttransformationcapacityinitsnetworkwhichresultedinanunreliablesystemoperation, frequent tripping of networks and prolonged load shed hours during the FY 2016-17.

1.17.8 The role of provincial bodies has become more important in overcoming power sector issues. The role of Provincial Government is critical in supporting transmission and distribution licensees in implementation of infrastructural projects. On the development of generation facilities however, NEPRA has observed that some of the provincial agencies lack management and procedural capacity and necessary skills fordevelopinggenerationresourcesefficiently.

24

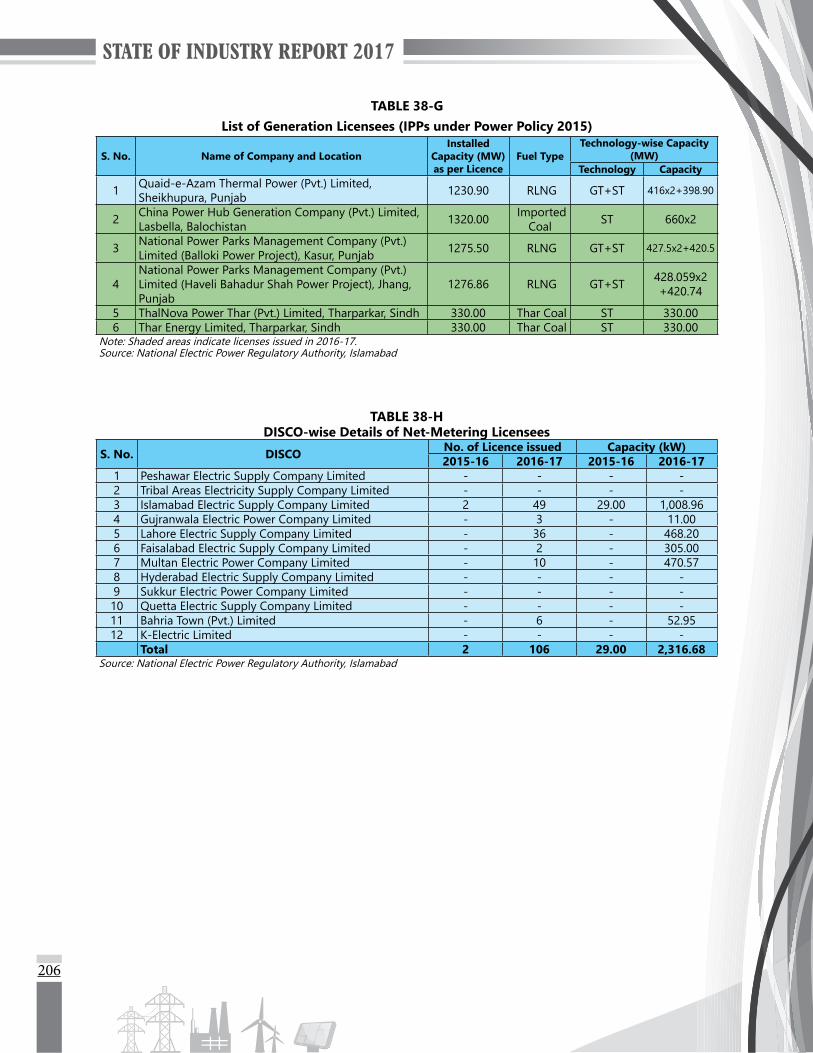

1.17.9 NEPRA has introduced Net-Metering regime since 2016. 108 consumers for 2,346 kW have been noted to participate in it upto June, 2017. Consumers and other stakeholders have been showing a lot of interest by proposing improvements in this regime.

1.17.10 Federal Government has recently approved Amendment Act, 2018 which provides for a complete shift in the existing regulatory regime. The distribution business has now been bifurcated into separate wire and sale businesses. At the same time concepts of “trader” and “supplier” have been introduced which in a way set the direction of a future market model. It is felt that by including framework for a future market in the Act, an inflexible approach has been adopted instead of conducting detaileddeliberation for recommending a solution.

1.18 RECOMMENDATIONS1.18.1 For continued reliability in the system, long term plans would be required to be

developed taking into consideration clear policies and supply and demand position.

1.18.2 In order to reduce dependence on imported fuel, new explorations and induction of indigenous gas should be encouraged.

1.18.3 Since solar and wind provide environmentally clean energy, without using fuel, therefore the Ministry of Energy (Power Division) is urged to resolve policy level ambiguities and technical issues for promotion of these technologies.

1.18.4 For long-term sustainability of the sector, small hydropower plants must be encouraged.

1.18.5 Ministry of Energy (Power Division) being owner of NTDC and DISCOs, is required to take extra ordinary steps for ensuring availability of strong transmission and distribution infrastructure to provide a reliable electricity supply.

1.18.6 Increase energy sold by reduction in T&D losses in DISCOs. DISCOs’ management mustfocusonspecifichighlossfeedersandsetcleartargetsforlossreduction.

1.18.7 DISCOsmustadoptallmeasures,whichhelp intrackingelectricityflowfromhighvoltage grids to end-consumers. Automatic metering systems, remote metering devices and centralized monitoring systems are to be installed immediately.

1.18.8 Recovery ratios in DISCOs need to be 100%. DISCOs having lower recovery ratios must take immediate measures to close the gap.

1.18.9 For improved management, large DISCOs may be considered for bifurcation.

25

1.18.10 KELmustaddefficientpowergenerationplantsinitssystemtoreducedependenceon external sources. Further, KEL needs to add power transformation capacity on urgent basis for a reliable power supply to consumers.

1.18.11 The provincial bodies responsible for power development, need capacity building and improved human resource skill level.

1.18.12 It is recommended to let Net-Metering regime continue so that burden on constrained networks of DISCOs may be reduced.

1.18.13 In order to reduce capital costs of major equipment in generation, transmission and distribution sectors, it is recommended to initiate and encourage local manufacturing.

1.18.14 After the approval of Amendment Act 2018, extensive consultations are required among stakeholders for the success of a new regulatory regime.

STATE OF INDUSTRY REPORT 2017

PERFORMANCE OF GENERATION SECTOR

29

PERFORMANCE OF GENERATION SECTOR

2.1 GENERALThe total installed generation capacity of Pakistan as on 30th June, 2017 stands at 28,399 MW, against 25,421 MW on 30th June, 2016, recording an increase of 2,978 MW or 11.71% over the last year. The power plants connected with NTDC and KEL’s system generated 120,621 GWh during the FY 2016-17 as compared to 114,093 GWh units produced during the FY 2015-16. During the FY 2016-17, the major additions to the system are thermal, nuclear and renewable based power projects.

2.2 INSTALLED CAPACITY AND ELECTRICITY GENERATIONThe following tables give additional details of source-wise installed capacity and electricity generation by different power plants connected with NTDC and KEL system along with a comparison of last two years:

Source-wise Installed Capacity by Type (MW)

As on 30th June 2016 2017Variation

Capacity %HYDELWAPDA Hydel 6,902 6,902 - -IPPs Hydel 214 214 - -THERMALGENCOs with PEPCO 5,897 5,897 - -KEL Own 1,874 1,874 - -

IPPs Connected with PEPCO 8,643 10,566 1,923 22.25Connected with KEL 252 252 - -

CPPs/SPPs connected with KEL 35 87 52 148.57NUCLEARCHASNUPP (I, II and III) 615 1,005 390* 63.41KANUPP 137 137 - -RENEWABLE ENERGY (WIND, SOLAR AND BAGASSE)RE Power Plants connected with PEPCO 852 1,465 613 71.94

Total Installed Capacity of the Country 25,421 28,399 2,978 11.71* Trued up the net capacities indicated earlier to Name Plate Capacities.Source: NTDC/KEL

Source-wise Electricity Generation by Type (GWh)

As on 30th June 2015-16 2016-17 VariationEnergy %

HYDELWAPDA Hydel 33,433 31,091 (2,342) (07.00)IPPs Hydel 1,121 988 (133) (11.86)THERMALGENCOs with PEPCO 16,392 18,710 2,318 14.14KEL Own 10,323 10,147 (176) (1.70)

IPPsConnected with PEPCO 45,146 47,972 2,826 6.26Connected with KEL 1,421 1,531 110 7.74

CPPs/SPPs connected with PEPCO 251 271 20 7.97CPPs/SPPs connected with KEL 139 187 48 34.53

As on 30th June 2015-16 2016-17Variation

Energy %NUCLEAR

02

30

CHASNUPP (I, II and III) 3,854 5,868 2,014 52.26KANUPP 362 410 48 13.26IMPORTImport from Iran 463 496 33 7.13RENEWABLE ENERGY (WIND, SOLAR AND BAGASSE)RE Power Plants connected with PEPCO 1,187 2,950 1,763 148.53Total Electricity Generation of the Country 114,093 120,621 6,528 5.72

Source: NTDC/KEL

2.3 HYDROPOWERIt may be noted that while the installed capacity of WAPDA Hydropower remained at 6,902 MW in the years 2015, 2016 and 2017, the 31,091 GWh generated in the FY 2016-17 shows a decrease of 2,342 GWh from the last year. Similarly, the Hydel IPPs also contributed 133 GWh less in the system during the FY 2016-17 with the same installed capacity as in the FY 2015-16. The hydropower energy production pattern over the year remained consistent with the historical trends. The availability and overall performance of major hydropower plants including Tarbela and Mangla has also remained satisfactory during the FY 2016-17.