state and local income tax provisions ipt … and local income tax provisions . teresa dieguez . vp...

TRANSCRIPT

STATE AND LOCAL INCOME TAX PROVISIONS

Teresa Dieguez VP of Corporate Tax Wynn Resorts Limited Las Vegas, NV teresa.dieguez@wynnresor ts.com

Smitha Hahn Indirect Tax Senior Manager EY Detroit, MI [email protected] IP

T AN

NUA

L CO

NFE

REN

CE

IPT 2014 ANNUAL CONFERENCE

Teresa Dieguez is Vice President of Corporate Tax for Wynn Resorts Limited

Teresa has over twenty years of tax, finance, and accounting experience in both public accounting and private industry

Teresa’s positions as Director and Vice President of Tax have focused on strategy, opportunity, planning, implementation and risk management in multi-billion dollar companies with worldwide operations including Tetra Tech, Inc., and International Game Technology

Teresa has also served as Tax Partner and Tax Markets Leader for the Las Vegas Office of Ernst & Young

Teresa is an active member of the American Gaming Association’s Tax/Finance Task Force and a board member of the Women’s Networking Circle in Las Vegas

Teresa is a graduate of Arizona State University with a Master of Taxation and is a Certified Public Accountant in Arizona and Nevada. 2

TERESA DIEGUEZ

IPT 2014 ANNUAL CONFERENCE

Smitha Hahn is a senior manager with Ernst & Young LLP’s Indirect/State and Local Tax Pract ice and is based in Detroit . She has over 13 years of publ ic account ing exper ience and is current ly responsible for the management and implementat ion of state and local tax projects and services for her c l ients .

Smitha recent ly moved into the Nat ional Tax pract ice where she serves as the Indirect/State and Local Tax tax account ing leader for the f i rm. Smitha also previously served as the Michigan Tax Desk for the f i rm for f ive years .

Smitha serves a diverse cl ient base and has s ignif icant exper ience in the state income/franchise tax area, focusing on business-al igned restructur ings, merger and acquis i t ion structur ing, review and analys is of the state tax impl icat ions of proposed business reorganizat ions, analys is of state tax f i l ings for refunds and prospect ive favorable f i l ing posit ions, and representat ion of c l ients before administrat ive boards in state tax controvers ies. Smitha has managed state-focused bankruptcy projects at f ive For tune 500 companies, focusing on state attr ibute preservat ion. In addit ion, she has FAS 109 tax provis ion and FIN 48 calculat ion, review and remediat ion exper ience.

Smitha is a member of the American Inst i tute of Cer t i f ied Publ ic Accountants as wel l as the Michigan Associat ion of Cer t i f ied Publ ic Accountants and is a cer t i f ied publ ic accountant l icensed in the state of Michigan. She has served as a lecturer on state tax issues for seminars sponsored by the Tax Execut ives Inst i tute, Counci l on State Taxat ion, Michigan Associat ion of Cer t i f ied Publ ic Accountants , Insurance Account ing and Systems Associat ion and Straf ford Publ icat ions.

Smitha has a Bachelor of Ar ts in Economics from the Univers i ty of Michigan and a Master of Account ing from the Univers ity of Michigan Business School .

3

SMITHA HAHN

IPT 2014 ANNUAL CONFERENCE

►Current

►Deferred

►Valuation Allowance

►Uncertain Tax Positions

BASIC COMPONENTS OF THE TAX PROVISION

4

IPT 2014 ANNUAL CONFERENCE

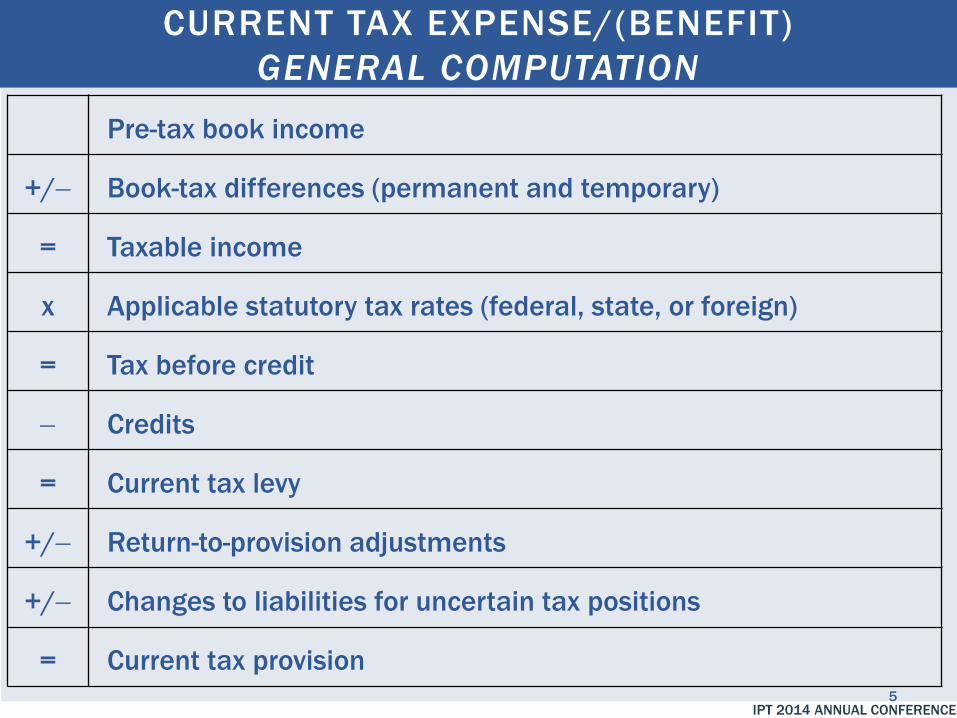

CURRENT TAX EXPENSE/(BENEFIT) GENERAL COMPUTATION

Pre-tax book income

+/− Book-tax differences (permanent and temporary)

= Taxable income

x Applicable statutory tax rates (federal, state, or foreign)

= Tax before credit

− Credits

= Current tax levy

+/− Return-to-provision adjustments

+/− Changes to liabilities for uncertain tax positions

= Current tax provision 5

IPT 2014 ANNUAL CONFERENCE

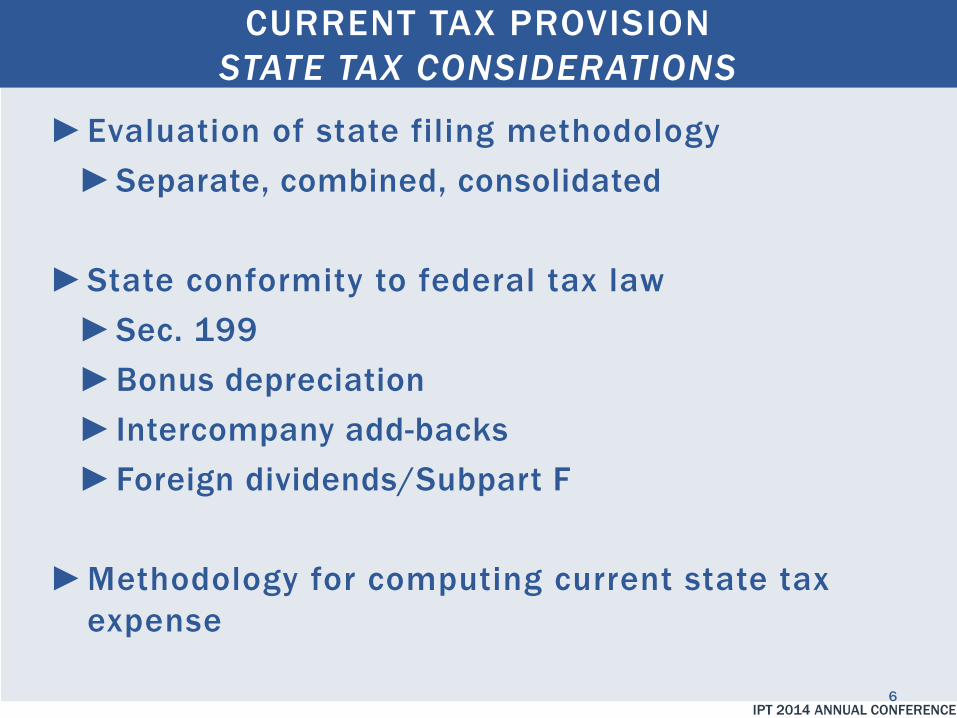

►Evaluation of state filing methodology ►Separate, combined, consolidated

►State conformity to federal tax law ►Sec. 199 ►Bonus depreciation ► Intercompany add-backs ►Foreign dividends/Subpart F

►Methodology for computing current state tax

expense

CURRENT TAX PROVISION STATE TAX CONSIDERATIONS

6

IPT 2014 ANNUAL CONFERENCE

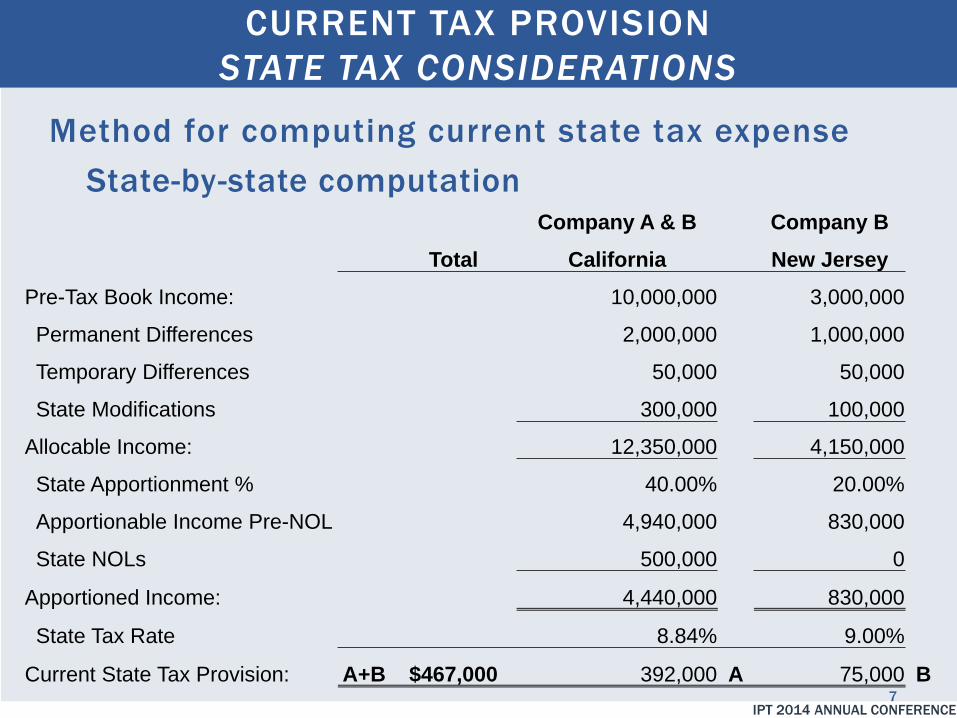

Method for computing current state tax expense State-by-state computation

CURRENT TAX PROVISION STATE TAX CONSIDERATIONS

Company A & B Company B

Total California New Jersey

Pre-Tax Book Income: 10,000,000 3,000,000

Permanent Differences 2,000,000 1,000,000

Temporary Differences 50,000 50,000

State Modifications 300,000 100,000

Allocable Income: 12,350,000 4,150,000

State Apportionment % 40.00% 20.00%

Apportionable Income Pre-NOL 4,940,000 830,000

State NOLs 500,000 0

Apportioned Income: 4,440,000 830,000

State Tax Rate 8.84% 9.00%

Current State Tax Provision: A+B $467,000 392,000 A 75,000 B 7

IPT 2014 ANNUAL CONFERENCE

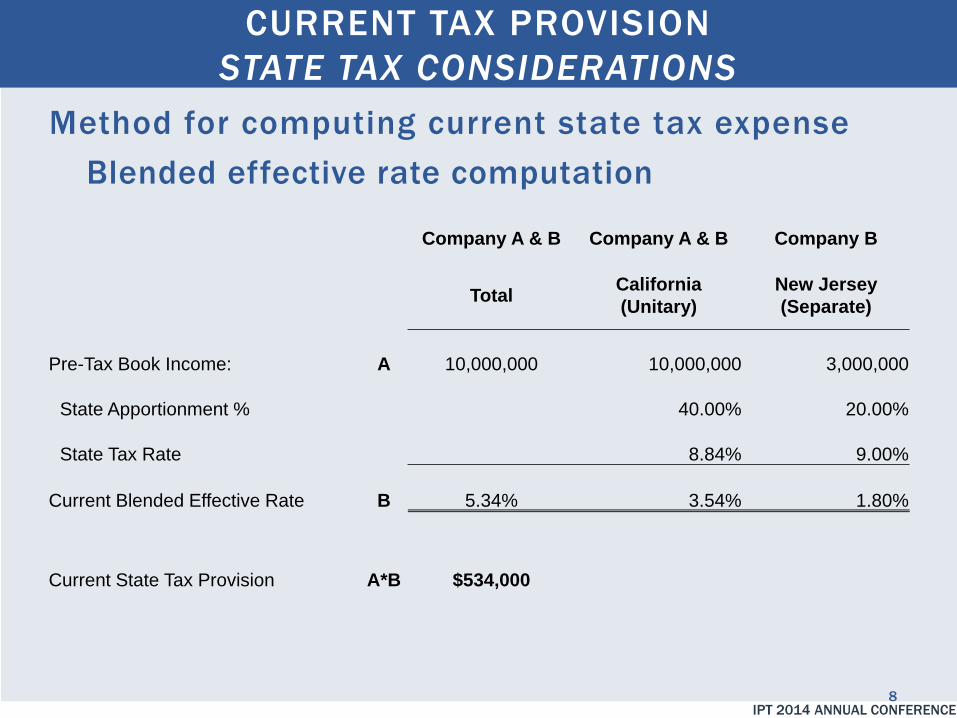

Method for computing current state tax expense Blended effective rate computation

CURRENT TAX PROVISION STATE TAX CONSIDERATIONS

Company A & B Company A & B Company B

Total California (Unitary)

New Jersey (Separate)

Pre-Tax Book Income: A 10,000,000 10,000,000 3,000,000

State Apportionment % 40.00% 20.00%

State Tax Rate 8.84% 9.00%

Current Blended Effective Rate B 5.34% 3.54% 1.80%

Current State Tax Provision A*B $534,000

8

IPT 2014 ANNUAL CONFERENCE

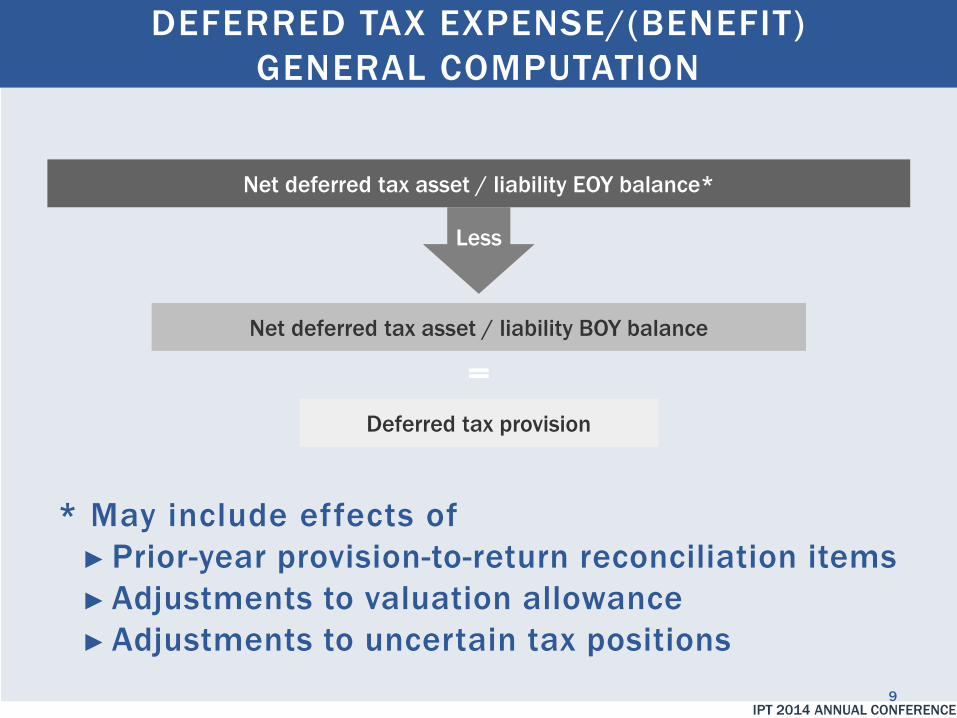

DEFERRED TAX EXPENSE/(BENEFIT) GENERAL COMPUTATION

* May include effects of ► Prior-year provision-to-return reconciliation items ► Adjustments to valuation allowance ► Adjustments to uncertain tax positions

Less

Deferred tax provision

Net deferred tax asset / liability EOY balance*

Net deferred tax asset / liability BOY balance

=

9

IPT 2014 ANNUAL CONFERENCE

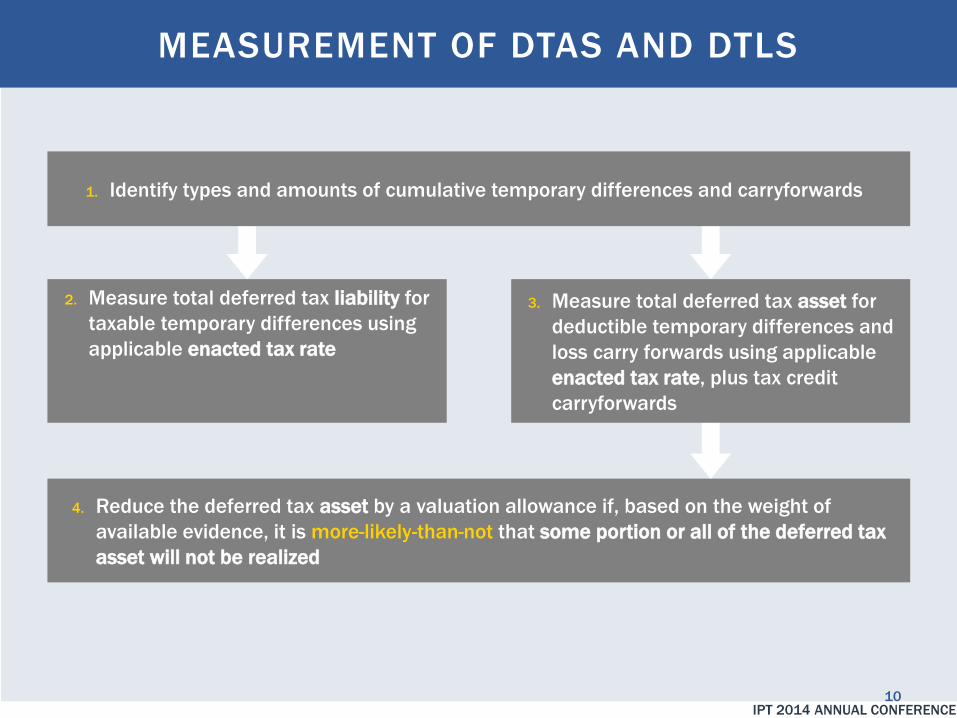

MEASUREMENT OF DTAS AND DTLS

4. Reduce the deferred tax asset by a valuation allowance if, based on the weight of available evidence, it is more-likely-than-not that some portion or all of the deferred tax asset will not be realized

2. Measure total deferred tax liability for taxable temporary differences using applicable enacted tax rate

3. Measure total deferred tax asset for deductible temporary differences and loss carry forwards using applicable enacted tax rate, plus tax credit carryforwards

1. Identify types and amounts of cumulative temporary differences and carryforwards

10

IPT 2014 ANNUAL CONFERENCE

►Understand differences from current tax

provision rate ►Deferreds should be booked at the rate the

deferred item is expected to turn ►Legislative changes are taken into account in

the period that they are enacted

►Future tax rate increases/decreases

►Future Business Changes

DEFERRED TAX PROVISION STATE TAX CONSIDERATIONS

11

IPT 2014 ANNUAL CONFERENCE

►Future changes in apportionment ►Weighting ►Sourcing

►Future tax reform

►State filing methodology ►Separate, combined, consolidated

► State conformity to federal tax law

► State NOLs and credits

DEFERRED TAX PROVISION STATE TAX CONSIDERATIONS (CONT.)

12

IPT 2014 ANNUAL CONFERENCE

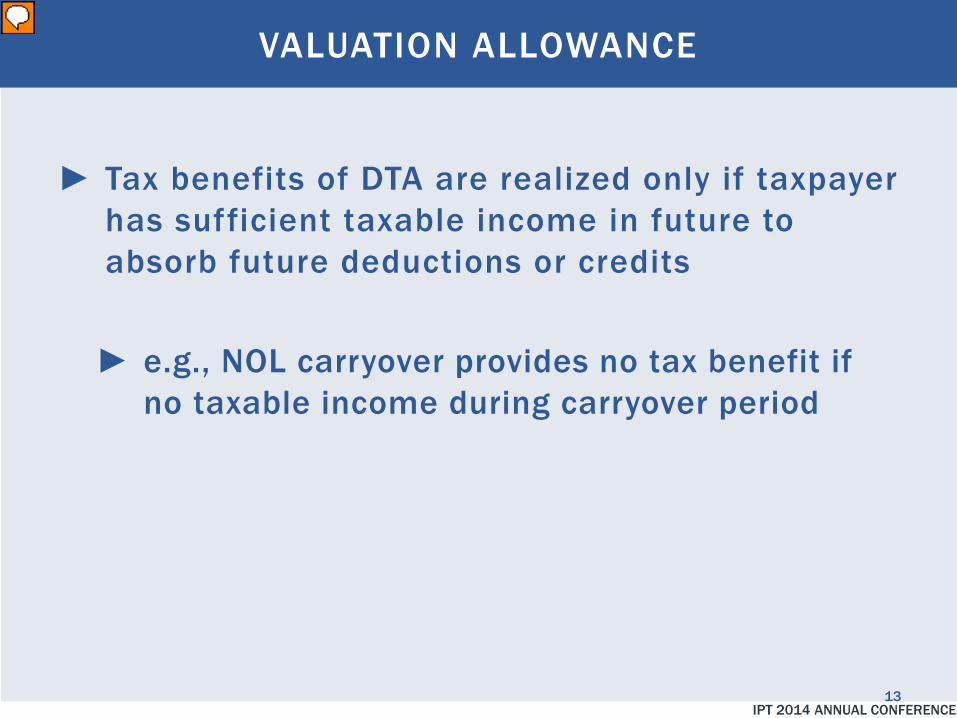

VALUATION ALLOWANCE

► Tax benefits of DTA are realized only if taxpayer has sufficient taxable income in future to absorb future deductions or credits ► e.g., NOL carryover provides no tax benefit if

no taxable income during carryover period

13

IPT 2014 ANNUAL CONFERENCE

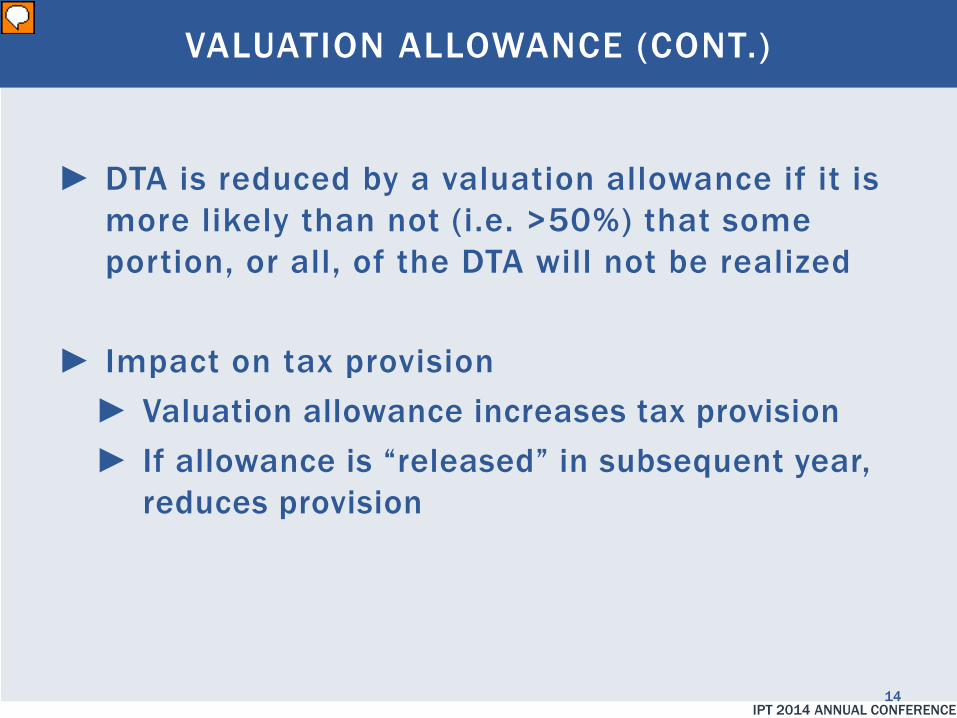

VALUATION ALLOWANCE (CONT.)

► DTA is reduced by a valuation allowance if it is more likely than not (i.e. >50%) that some portion, or all, of the DTA will not be realized

► Impact on tax provision ► Valuation allowance increases tax provision ► If allowance is “released” in subsequent year,

reduces provision

14

IPT 2014 ANNUAL CONFERENCE

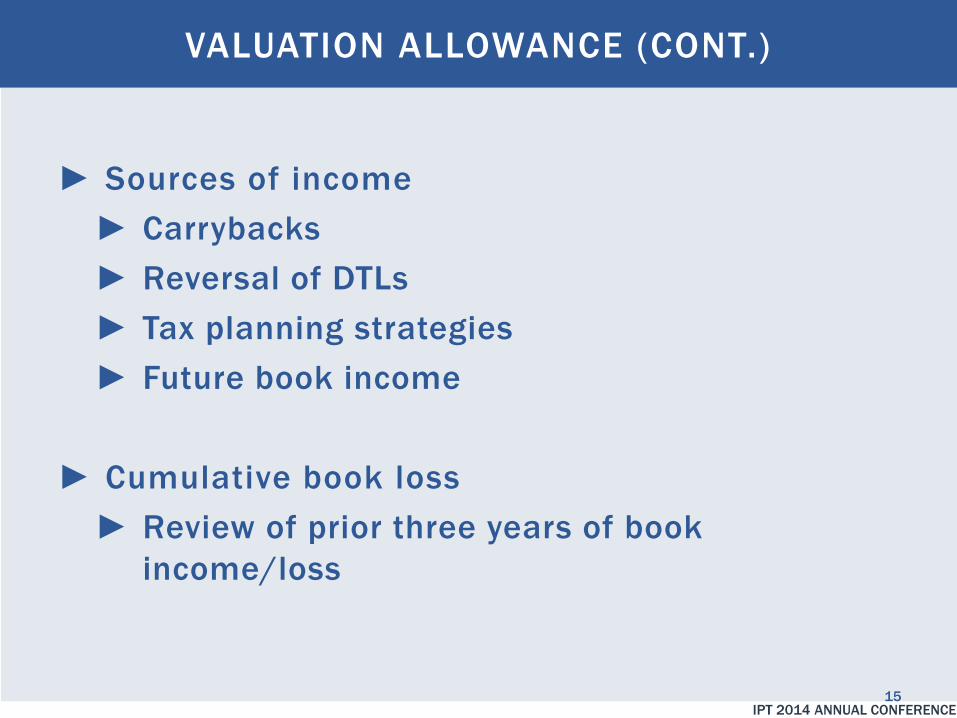

VALUATION ALLOWANCE (CONT.)

► Sources of income ► Carrybacks ► Reversal of DTLs ► Tax planning strategies ► Future book income

► Cumulative book loss ► Review of prior three years of book

income/loss

15

IPT 2014 ANNUAL CONFERENCE

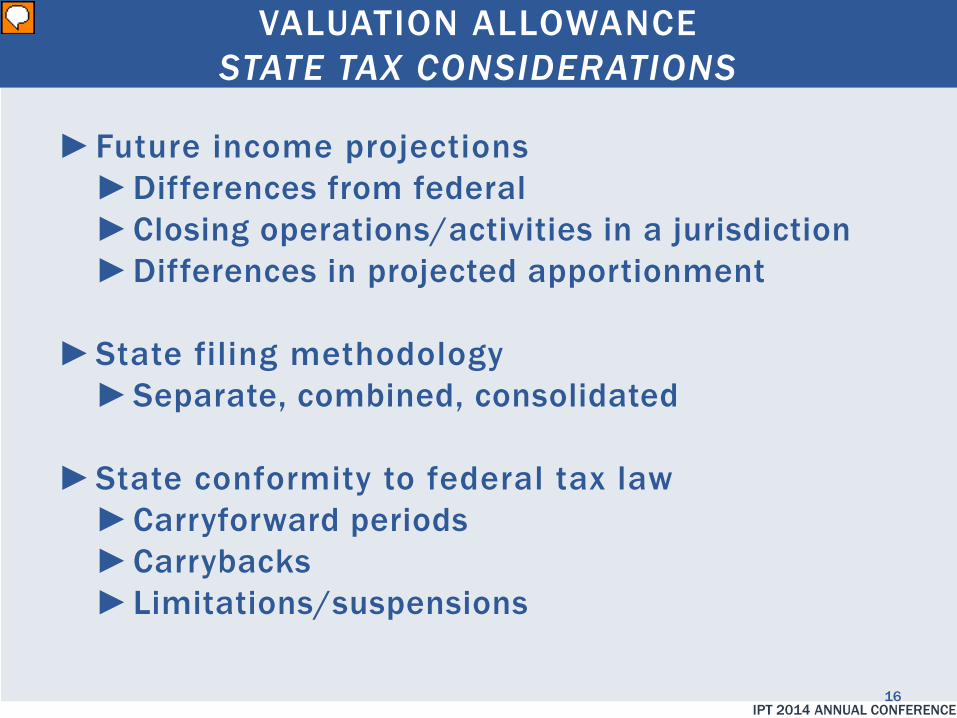

VALUATION ALLOWANCE STATE TAX CONSIDERATIONS

►Future income projections ►Differences from federal ►Closing operations/activities in a jurisdiction ►Differences in projected apportionment

►State filing methodology ►Separate, combined, consolidated

►State conformity to federal tax law ►Carryforward periods ►Carrybacks ►Limitations/suspensions

16

IPT 2014 ANNUAL CONFERENCE

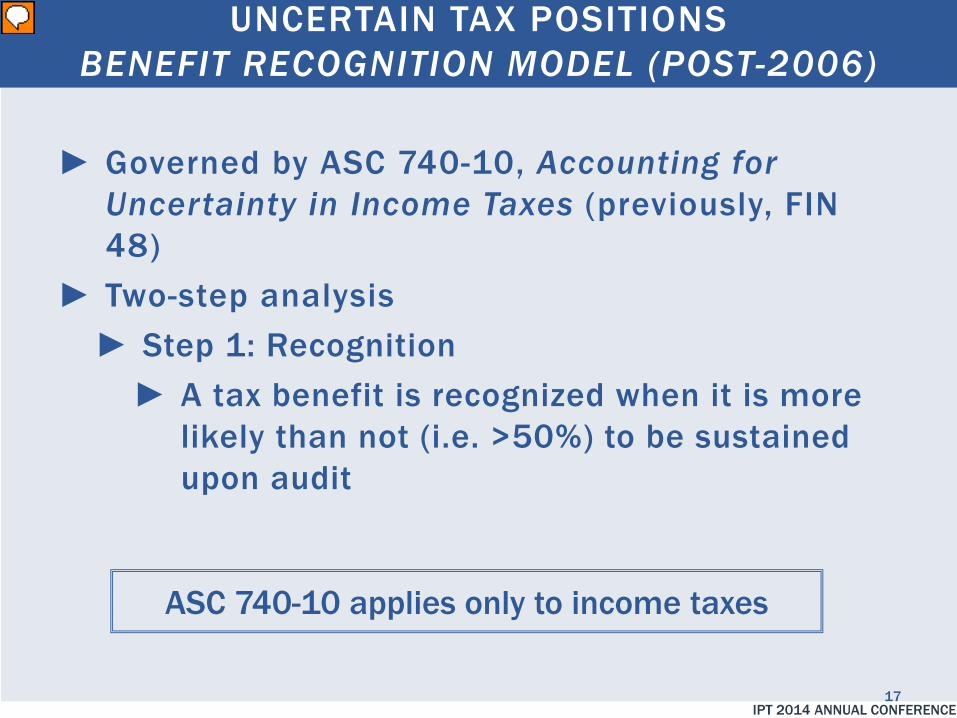

UNCERTAIN TAX POSITIONS BENEFIT RECOGNITION MODEL (POST-2006)

► Governed by ASC 740-10, Accounting for Uncertainty in Income Taxes (previously, FIN 48)

► Two-step analysis ► Step 1: Recognition ► A tax benefit is recognized when it is more

likely than not (i.e. >50%) to be sustained upon audit

ASC 740-10 applies only to income taxes

17

IPT 2014 ANNUAL CONFERENCE

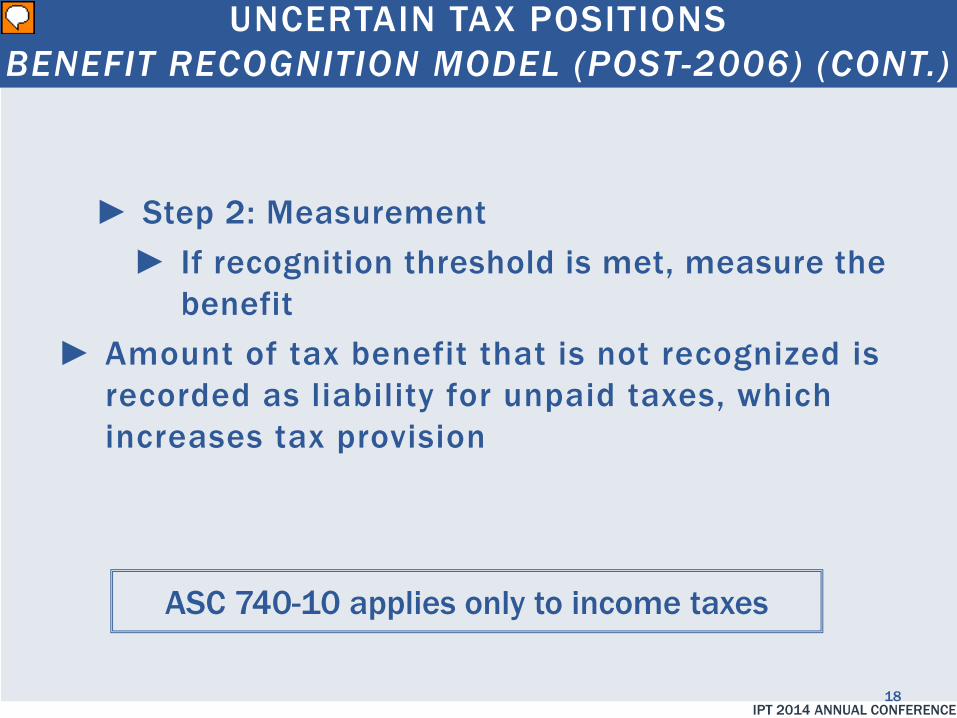

UNCERTAIN TAX POSITIONS BENEFIT RECOGNITION MODEL (POST-2006) (CONT.)

► Step 2: Measurement ► If recognition threshold is met, measure the

benefit ► Amount of tax benefit that is not recognized is

recorded as liability for unpaid taxes, which increases tax provision

ASC 740-10 applies only to income taxes

18

IPT 2014 ANNUAL CONFERENCE

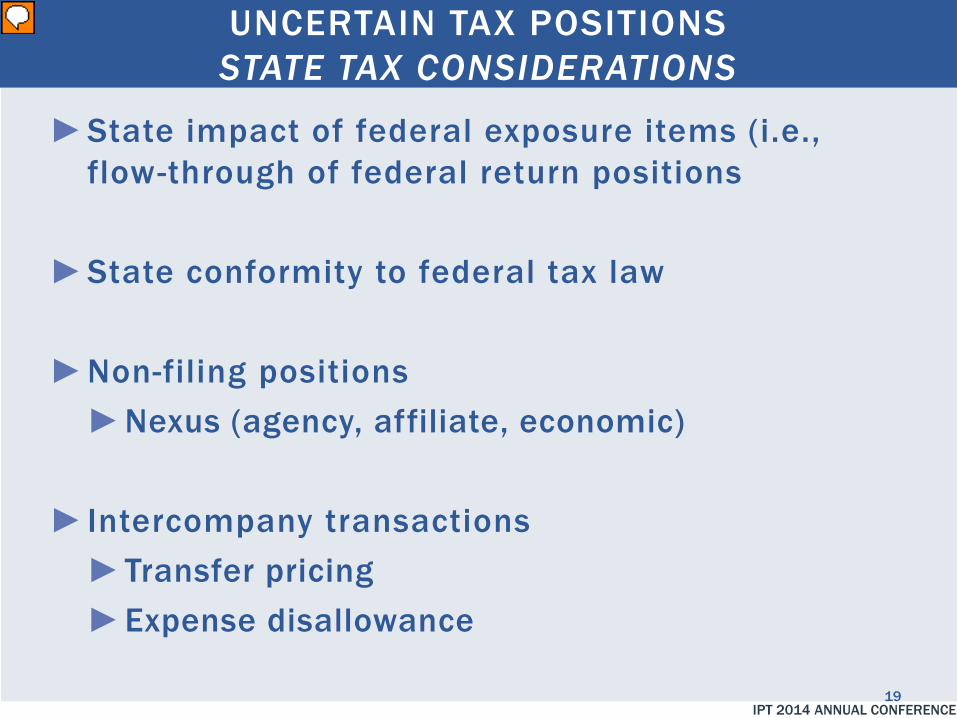

►State impact of federal exposure items (i.e., flow-through of federal return positions

►State conformity to federal tax law

►Non-filing positions ►Nexus (agency, affiliate, economic)

► Intercompany transactions ►Transfer pricing ►Expense disallowance

UNCERTAIN TAX POSITIONS STATE TAX CONSIDERATIONS

19

IPT 2014 ANNUAL CONFERENCE

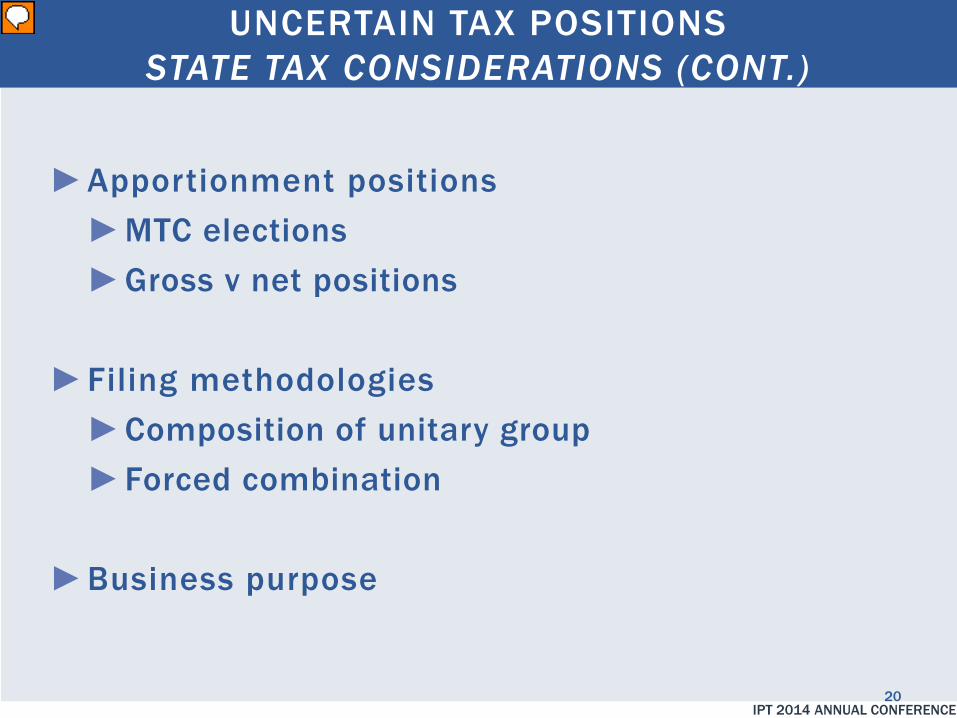

►Apportionment positions ►MTC elections ►Gross v net positions

►Filing methodologies ►Composition of unitary group ►Forced combination

►Business purpose

UNCERTAIN TAX POSITIONS STATE TAX CONSIDERATIONS (CONT.)

20

IPT 2014 ANNUAL CONFERENCE

►Economic substance

► Impact of voluntary compliance initiatives

► Jurisdictional interest and penalty provisions

►Documentation requirements ►Current year review of technical assessments of

prior UTPs

UNCERTAIN TAX POSITIONS STATE TAX CONSIDERATIONS (CONT.)

21

IPT

ANN

UAL

CON

FER

ENCE

THANK YOU FOR YOUR TIME

Teresa Dieguez VP of Corporate Tax Wynn Resorts Limited Las Vegas, NV teresa.dieguez@wynnresor ts.com

Smitha Hahn Indirect Tax Senior Manager EY Detroit, MI [email protected]