impact of federal reform on state corporate income tax ......key tcja provisions and the state tax...

TRANSCRIPT

Council On State Taxation

Impact of Federal Reform on State

Corporate Income Tax Base & the Best

and Worst of Sales Tax Administration—

Focus on New Mexico

Nikki Dobay

Senior Tax Counsel (COST)

2018 15th Annual NMTRI

Tax Policy Conference

1

Agenda

– Impact of Federal Tax Reform on the State

Corporate Income Tax Base

▪ Overview and Fiscal Impact of the Tax Cuts

and Jobs Act

▪ State Conformity and Non-Conformity Overview

▪ Key TCJA Provisions and the State Tax Impact

– The Best and Worst of Sales Tax

Administration

2

Overview and Fiscal Impact

of the Tax Cuts and Jobs Act

3

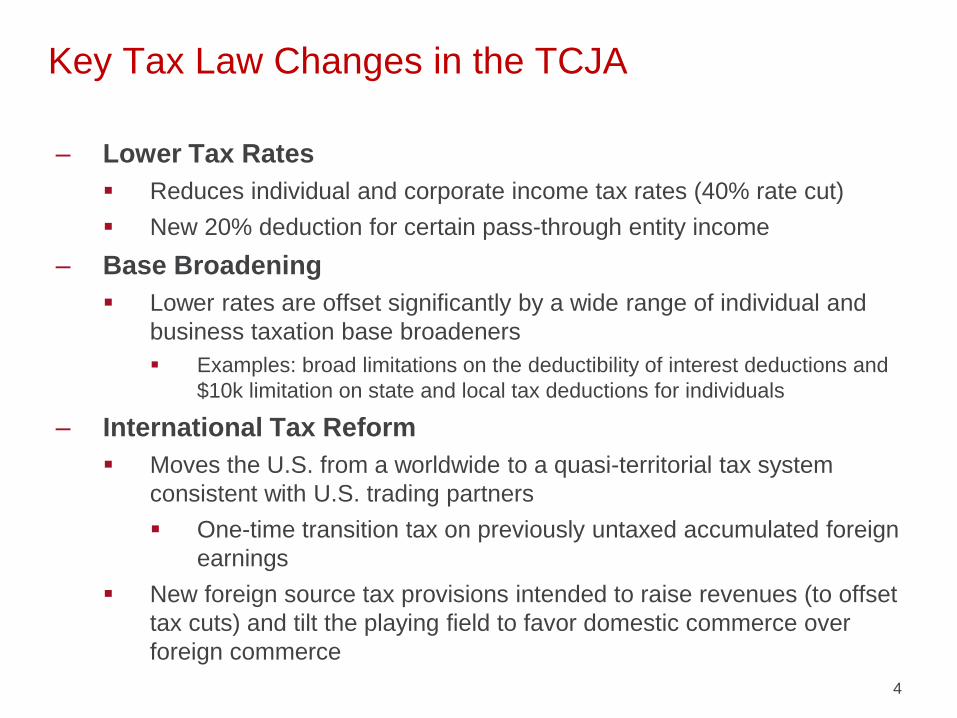

Key Tax Law Changes in the TCJA

– Lower Tax Rates

▪ Reduces individual and corporate income tax rates (40% rate cut)

▪ New 20% deduction for certain pass-through entity income

– Base Broadening

▪ Lower rates are offset significantly by a wide range of individual and

business taxation base broadeners

▪ Examples: broad limitations on the deductibility of interest deductions and

$10k limitation on state and local tax deductions for individuals

– International Tax Reform

▪ Moves the U.S. from a worldwide to a quasi-territorial tax system

consistent with U.S. trading partners

▪ One-time transition tax on previously untaxed accumulated foreign

earnings

▪ New foreign source tax provisions intended to raise revenues (to offset

tax cuts) and tilt the playing field to favor domestic commerce over

foreign commerce

4

Differential Federal and State Fiscal Impacts

of TCJA

– According to the Joint Committee on Taxation, at the federal

level, TCJA will result in about $6 trillion in tax cuts offset by

about $4.5 trillion in revenue raisers over the first 10 years

▪ Individual tax cuts over 10 years: $1.127 trillion (most sunset on

12/31/25)

▪ Corporate tax cuts over 10 years: $329.4 billion (10% decrease in

corporate tax base)

– Conversely, at the state level, TCJA will likely result in an

increase of approximately 12% in the corporate tax base

▪ Generally states do not conform to the federal provisions that

lower revenue (e.g., tax rate cuts), but do conform to many federal

provisions that increase revenue (e.g., base-broadening

measures)

5

Quantifying the impacts of TCJA on state corporate

taxes

– New EY/COST/STRI study provides

estimates of the impacts of TCJA on

state corporate tax bases.

– Study examines the impact of all

states updating their corporate tax

codes to the TCJA, but remaining

coupled to specific provisions as they

have in the past.

– The estimated percentage change in

the state corporate tax base from

TCJA is about 12 percent over the

first 10 years (2018-2027), with

significant variation among the

states.

6

7

State% increase in state corporate tax base State

% increase in state corporate tax base

Alabama 11% Nebraska 11%

Alaska* 12% Nevada n/aArizona 14% New Hampshire* 13%

Arkansas 12% New Jersey* 12%

California** 12% New Mexico* 11%

Colorado 12% New York* 12%

Connecticut* 12% North Carolina 12%

Delaware 10% North Dakota 10%

Florida 13% Ohio n/a

Georgia 12% Oklahoma 13%

Hawaii* 13% Oregon* 10%

Idaho 9% Pennsylvania* 14%

Illinois 9% Rhode Island* 11%

Indiana* 12% South Carolina 12%

Iowa 13% South Dakota n/a

Kansas 11% Tennessee* 12%

Kentucky* 12% Texas n/a

Louisiana 12% Utah* 12%

Maine 12% Vermont 14%

Maryland* 12% Virginia 13%

Massachusetts* 12% Washington n/a

Michigan 9% West Virginia 9%

Minnesota* 12% Wisconsin* 9%

Mississippi* 4% Wyoming n/a

Missouri 11% District of Columbia 12%

Montana* 9% Overall Change 12%

Estimated percentage change in state corporate tax base

from TCJA, by state (2018-2027)* State starts with

Form 1120 line

28. To the extent

IRC Section 250

deductions not

allowed, this

impact would be

higher by 4.5%.

** There may be a

California impact

relating to cash

repatriation for

waters’-edge filers

once the deemed

repatriated

earnings have

been actually

distributed as

dividends to U.S.

corporate

shareholders.

California has

estimated this

amount at

approximately

$350 million.

State Conformity and Non-

Conformity Overview

8

State income tax conformity to IRC

AK

HI

ME

VT

NH

MANYCT

PA

WV

NC

SC

GA

FL

ILOH

IN

MI

WI

KY

TN

ALMS

AR

LATX

OK

MOKS

IA

MN

ND

SD

NE

NMAZ

COUT

WY

MT

OR

ID

NV

CAVA

Key

Fixed

Rolling

Selective

No income tax

As of March 6, 2018

Note - CA & MA personal income tax law differs in its conformity to the IRC compared to CA & MA corporate tax law.

RI

NJ

DE

DC

Note - OH doesn’t have a corporate income tax. Personal income tax IRC adoption is Fixed

WA

9

Note – MI IRC conformity is January 2012 or if elected by Taxpayer Current Year (i.e. Rolling)

MD

Potential State Impact of Business Tax Reform Provisions

Federal States

Corporate tax rate reductions States have own rates

Special pass through entity deduction

Potentially impacts minority of states tied

to federal “taxable income” for PIT

purposes

Limitation of net interest deductions that

exceed 30% of adjusted taxable income

Mostly state conformity (uncertain

application to state filing groups)

Fully expensed investments2/3 of states opted out of bonus

depreciation

Broadened tax base including repeal of

Sec. 199 domestic production deduction

State conformity (although many states

already opted out of the domestic

production deduction)

Limit NOL deductionsMost states have their own NOL

provisions

Amortization of research and

experimental expendituresLikely state conformity

10

Potential State Impact of International Tax Reform Provisions

Federal States100 percent dividends-received deduction (DRD)

Most states have their own DRDs

Transition tax on “deemed” repatriated earnings

One-third of states tax some portion of Subpart F income and/or foreign dividends.

Tax on global intangible low-taxed income (GILTI) earned by foreign subsidiaries

Mostly state conformity (but constitutional limitations)

Deduction of 50 percent of GILTI income Mostly state conformity (but “special deduction” linkage issues)

Reduced tax on foreign-derived intangible income (FDII) of U.S. corporation

Mostly state conformity (but “special deduction” linkage issues)

Base erosion anti-avoidance tax (BEAT) Separate tax not in federal taxable income

Longer amortization schedule for foreign research and experimentation (15 years)

Likely state conformity (but constitutional issues)

11

Business Tax Provision% Change in

Federal Corporate Tax Base

State Conformity

One-time transition tax on unrepatriated foreign earnings

+ 9 %Modest conformity (but

typically of 25% or less)

Net interest expense limitation (30% of ATI) + 6.4% Mostly conformity

Global intangible low-taxed income (GILTI) + 5.5 % (gross

amount)Mostly Conformity

Modification of net operating loss deduction + 5.3% Mostly non-conformity

Base Erosion and Anti-Abuse Tax (BEAT) + 4.0% Non-conformity

Amortization of research and experimental expenditures

+ 2.9% Mostly Conformity

Repeal of domestic production activities deduction + 1.9% Mostly conformity

Foreign derived intangible income (FoDII) deduction - 1.7% Mostly conformity

Expensing provided under Section 168(k) bonus depreciation

- 1.8% Modest conformity

Global intangible low-taxed income (GILTI) deduction - 2.6% Mostly conformity

100% foreign DRD - 5.9% Mostly conformity

Top Increases and Decreases in Federal Corporate Tax Base

with TCJA and Potential State Conformity

12

Key TCJA Provisions and

the State Tax Impact

AK

HI

ME

RI

VT

NH

MANYCT

PANJ

DC

DE

WV

NC

SC

GA

FL

ILOH

IN

MIWI

KY

TN

ALMS

AR

LATX

OK

MOKS

IA

MN

ND

SD

NE

NMAZ

CO

UT

WY

MT

WA

OR

ID

NV

CAVA

MD

State Income Starting Point

Source: COST/STRI/EY study

Line 30

Line 28

Gross receipts tax or no corporate income tax

Other

This analysis assumes each state will update to the 2018 IRC consistent with the provisions the state conformed to prior to the enactment of the

TCJA. This map is intended for general information purposes only and should not be relied upon for tax advice.

14

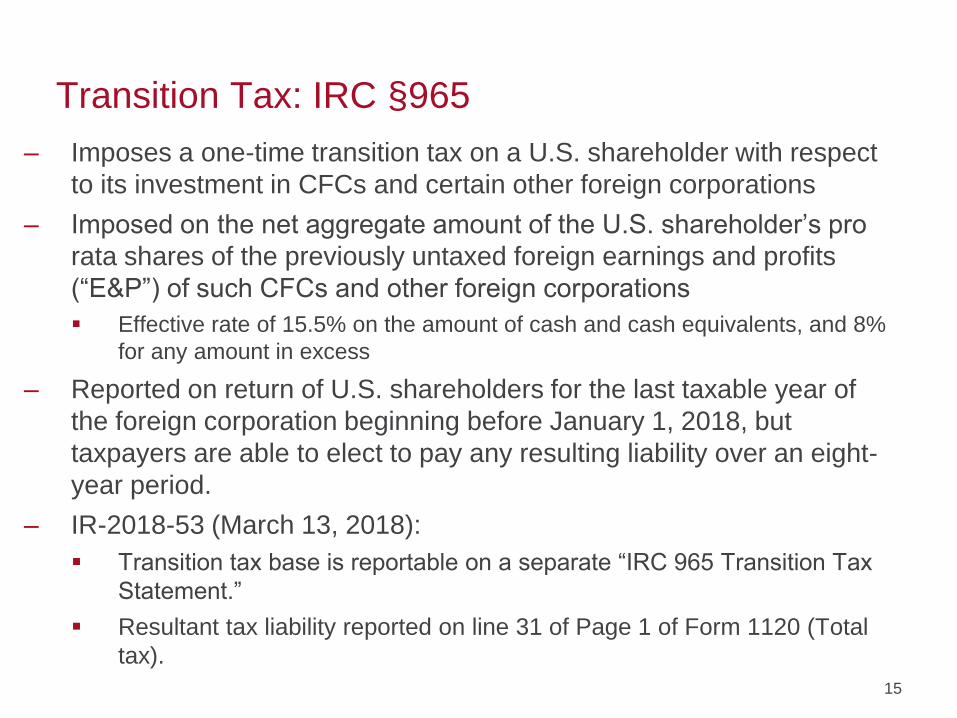

Transition Tax: IRC §965

– Imposes a one-time transition tax on a U.S. shareholder with respect

to its investment in CFCs and certain other foreign corporations

– Imposed on the net aggregate amount of the U.S. shareholder’s pro

rata shares of the previously untaxed foreign earnings and profits

(“E&P”) of such CFCs and other foreign corporations

▪ Effective rate of 15.5% on the amount of cash and cash equivalents, and 8%

for any amount in excess

– Reported on return of U.S. shareholders for the last taxable year of

the foreign corporation beginning before January 1, 2018, but

taxpayers are able to elect to pay any resulting liability over an eight-

year period.

– IR-2018-53 (March 13, 2018):

▪ Transition tax base is reportable on a separate “IRC 965 Transition Tax

Statement.”

▪ Resultant tax liability reported on line 31 of Page 1 of Form 1120 (Total

tax).

15

AK

HI

ME

RI

VT

NH

MANYCT

PANJ

DC

DE

WV

NC

SC

GA

FL

ILOH

IN

MIWI

KY

TN

ALMS

AR

LATX

OK

MOKS

IA

MN

ND

SD

NE

NMAZ

CO

UT

WY

MT

WA

OR

ID

NV

CAVA

MD

Potential State Taxation of Accumulated Foreign

Earnings

Source: COST/STRI/EY study

Assumes no impact

Assumes partial or full impact

California special treatment

This analysis assumes each state will update to the 2018 IRC consistent with the provisions the state conformed to prior to the enactment of the

TCJA. This map is intended for general information purposes only and should not be relied upon for tax advice.

16

Transition Tax: SALT Implications

– Impact is largely based on:

▪ States’ starting point for calculation of state taxable income: the

transition tax is reported and calculated on a separate IRC 965

Transition Tax Statement, with the liability going into line 31 and

line 32 of Form 1120.

▪ State treatment of subpart F income

▪ State adoption of IRC §965 (c) (effectively providing reduced

tax rates)

▪ Taxpayers’ state income tax filing method – worldwide

combined, water’s-edge, or separate

17

Transition Tax: SALT Implications

– Timing—States traditionally do not afford a similar

payment deferral mechanism as allowed for federal

income tax purposes

– Conforming states may run afoul of Kraft

– Factor representation - Is the inclusion of foreign

(deemed) dividends, but not including the corresponding

apportionment factors of the specified foreign

corporations unconstitutionally discriminatory?

18

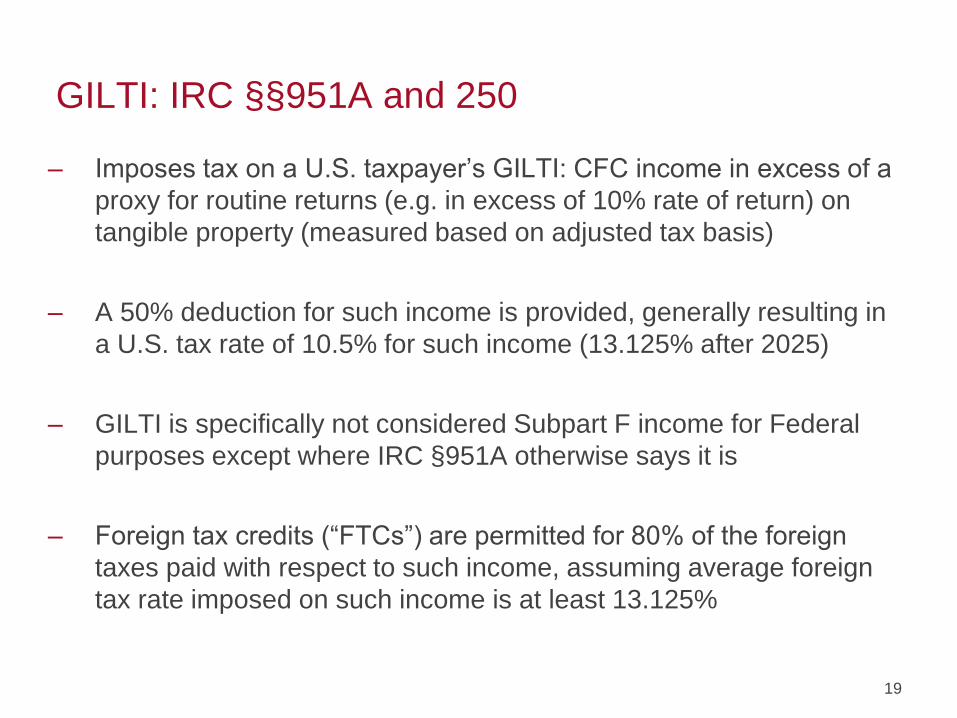

GILTI: IRC §§951A and 250

– Imposes tax on a U.S. taxpayer’s GILTI: CFC income in excess of a

proxy for routine returns (e.g. in excess of 10% rate of return) on

tangible property (measured based on adjusted tax basis)

– A 50% deduction for such income is provided, generally resulting in

a U.S. tax rate of 10.5% for such income (13.125% after 2025)

– GILTI is specifically not considered Subpart F income for Federal

purposes except where IRC §951A otherwise says it is

– Foreign tax credits (“FTCs”) are permitted for 80% of the foreign

taxes paid with respect to such income, assuming average foreign

tax rate imposed on such income is at least 13.125%

19

AK

HI

ME

RI

VT

NH

MANYCT

PANJ

DC

DE

WV

NC

SC

GA

FL

ILOH

IN

MIWI

KY

TN

ALMS

AR

LATX

OK

MOKS

IA

MN

ND

SD

NE

NMAZ

CO

UT

WY

MT

WA

OR

ID

NV

CAVA

MD

Potential Taxation of GILTI Income (Inclusion)

Source: COST/STRI/EY study

No exclusion of 951-964 income

Excludes 951-964 income

Gross receipts tax

States that have delinked from GILTI

This analysis assumes each state will update to the 2018 IRC consistent with the provisions the state conformed to prior to the enactment of the

TCJA. This map is intended for general information purposes only and should not be relied upon for tax advice.

20

GILTI: SALT Implications

– Potential base broadening

– Because IRC §951A is a new section, states will generally not have

a specific exclusion for GILTI

– If IRC §250 is considered a “special deduction,” the impact of the

corresponding deduction in IRC §250 is largely dependent on

states’ starting point for calculating state taxable income:

▪ Form 1120 line 28 – income before NOLs and special

deductions vs. line 30 – income after NOLs and special

deductions

– Splitting of IRC §951A and IRC §250 – providing for inclusion

without deduction

21

GILTI: SALT Implications

– Disconnect from federal treatment, as states generally

do not permit use of FTCs

– The impact of GILTI will be affected by a taxpayer’s

state income tax filing method

– Kraft issues

– Factor representation—Is the inclusion of foreign

(deemed) dividends, but not including the corresponding

apportionment factors of the CFCs unconstitutionally

discriminatory?22

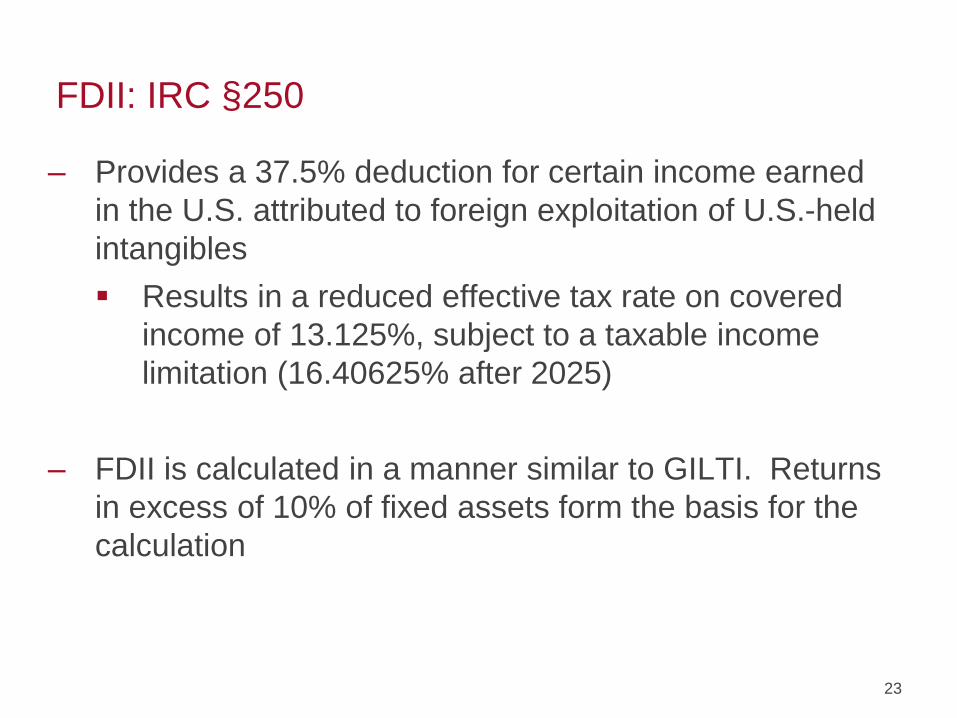

FDII: IRC §250

– Provides a 37.5% deduction for certain income earned

in the U.S. attributed to foreign exploitation of U.S.-held

intangibles

▪ Results in a reduced effective tax rate on covered

income of 13.125%, subject to a taxable income

limitation (16.40625% after 2025)

– FDII is calculated in a manner similar to GILTI. Returns

in excess of 10% of fixed assets form the basis for the

calculation

23

FDII: SALT Implications

– Deduction for FDII under IRC § 250 is likely a “special

deduction,” thus the impact (benefit) is largely

dependent on whether a state’s starting point for

calculation of state taxable income is Form 1120 line 28

or line 30

– The impact of FDII will be affected by a taxpayer’s state

income tax filing method

– Selective decoupling – FDII, as enacted, is to work with

GILTI

24

BEAT: IRC §59A

– Generally imposes a 10% minimum tax (5% in 2018) on a

taxpayer’s income determined without regard to tax deductions

arising from base erosion payments.

– Base erosion payments: generally amounts paid by a taxpayer to a

related foreign person that are deductible to the taxpayer (including

interest) or that create depreciable or amortizable asset basis.

– The BEAT applies to U.S. corporations (other than RICs, REITs, or

S corporations), which have average annual gross receipts of at

least $500 million for the preceding three tax years and which have

a base erosion percentage (generally, deductible payments to

foreign affiliates over total deductions) of 3% (2% for affiliated

groups that include a bank or securities dealer) or higher for the tax

year.

25

BEAT: SALT Implications

– The federal impact of the BEAT is the payment of

additional tax for those taxpayers subject to it

– Because the BEAT is a separate tax that does not go

into the calculation of federal taxable income, the BEAT

currently does not have an impact on state taxable

income

26

Interest Expense Limitation – IRC § 163(j)

• General Overview: Business interest expense cannot

exceed 30% of FTI exclusive of business interest income,

business interest expense, depreciation, amortization.

• State Tax Issues:

▪ How is the limitation computed for state purposes

when the state and federal filing methodologies differ?

▪ External vs. internal debt?

▪ Will state allow indefinite carryforward of disallowed

interest expense?

▪ How will the federal limits interact with state related

party interest expense disallowance statutes?

27

100% Bonus Depreciation – IRC §168(k)

• General Overview: Current bonus depreciation

percentage under IRC § 168(k) is increased from 50% to

100% for property acquired and placed in service after

September 27, 2017, and before December 31, 2022. The

100% expensing is phased down by 20 percentage points

per calendar year beginning in 2023.

• State Tax Issues:

• Will states conform?

• In state that historically decoupled from bonus, will

they decouple from the increase to 100%?

▪ Straight coupling to federal vs. MACRS vs. different

approaches

▪ Having to track different methods in different states28

COST Conformity Principles

– Manage conformity to achieve revenue neutrality and

avoid increasing the state’s business tax burden

– Do not selectively conform to revenue-increasing federal

tax reform changes only

▪ Example: GILTI but not IRC Section 250 deduction.

▪ Example: Interest deduction limitation but not 100%

expensing

– Do not conform to new foreign source income provisions

that would expand the state tax base beyond the water’s

edge

▪ Examples: GILTI; BEAT

– States should provide guidance to facilitate state income

tax compliance with complex new federal tax reform

provisions.29

State Conformity Changes: Base Narrowing

Legislation as of mid-April 2018

– Corporate Rate Cuts Following Federal Tax Reform

▪ FL (H.B. 7093); GA (H.B. 918); ID (H.B. 463)

– General Decoupling from TCJA Base Broadeners

▪ WI (A.B. 259) – decoupled from Interest Expense Limit, GILTI, FDII, R

& E amortization, Full Expensing, BEAT, Repatriation

– Decoupling from Interest Expense Limitation

▪ GA (H.B. 918); MS (no conformity due to preexisting law)

▪ Tenn. (in 2020)

– Decoupling from GILTI

▪ GA (S.B. 328);

▪ IL, MI, MT, WI (no conformity due to preexisting law)

– Allowing GILTI Deductions

▪ NY (DTF statement that IRC 250 deductions included; FDII decoupled

in budget)

– Transition Tax Installment Payments

▪ UT (S.B. 244)

Best and Worst of Sales Tax

Administration

Background on COST’s Scorecards

– Purpose of Scorecards is to grade the state tax administration on an

objective basis and to work with the states’ policy makers – both

executive and legislative – to improve state and local tax

administration for multijurisdictional businesses

– Other COST Scorecards:

▪ State Administrative Scorecard—increase in independent

tribunals & appeal period from 30 to 60 days

▪ Unclaimed Property Scorecard—increase in states exempting gift

cards and business-to-business transactions

▪ Property Tax Administration Scorecard

▪ International and improvement of some states appeal processes

32

The Sales Tax Scorecard Categories

– Exemption for Business-to-Business Transactions

– Fair Sales Tax Administration

– Centralized Sales Tax Administration

– Simplification & Transparency

– Reasonable Tax Payment Administration

– Fair Audit/Refund Procedures

– Other Issues Impacting Fair Tax Administration

– What the Scorecard Does Not Grade

▪ Tax Rate Differences

▪ Tax Base Breadth (other than Taxing Business Inputs)

33

38%

21%

12%

9%

6%

68%

Source: COST, STRI, Ernst & Young: “Total State and Local Business Taxes: State-by-State Estimates for Fiscal Year 2016”

Taxes on business property

Sales tax on business inputs

Excise, utility & Insurance taxes

Corporate income tax

Unemployment insurance tax

Individual income tax on business income

Business license, severance & other taxes

United States

Sales Taxes Make Up of

Overall Business State and Local Taxes

20%

42%

11%

4%

7%

2%

16%

New Mexico

34

AK

HI

ME

RI

VT

NH

MANYCT

PANJ

DC

DE

WV

NC

SC

GA

FL

ILOH

IN

MIWI

KY

TN

ALMS

AR

LATX

OK

MOKS

IA

MN

ND

SD

NE

NMAZ

CO

UT

WY

MT

WA

OR

ID

NV

CAVA

MD

N/A A B C D F

N/A 0-9 10-13 14-17 18-22 22+

35

States’ Overall Grades

Exemption for Business-to-Business Transactions

– COST/EY Study highlighting overall tax on business inputs – 2

points

– Manufacturing exemption – 3 points

▪ Manufacturing equipment exemption – 2 points

▪ Manufacturing inputs exemption – 1 point

– Pyramiding tax of service industries – 3 points

▪ Double tax on equipment to provide service and tax on

service when sold to consumer

– New Mexico’s Score – 8 (out of 8) points

36

AK

HI

ME

RI

VT

NH

MANYCT

PANJ

DC

DE

WV

NC

SC

GA

FL

ILOH

IN

MIWI

KY

TN

ALMS

AR

LATX

OK

MOKS

IA

MN

ND

SD

NE

NMAZ

CO

UT

WY

MT

WA

OR

ID

NV

CAVA

MD

N/A A B C D F

N/A 0-1 pts 2 pts 3-4 pts 5-6 pts 7-8 pts

37

Exemption for Business Inputs – States’ Grades

State and Local Sales Taxes Imposed on Business Inputs over Business Inputs Share of Total Sales

Tax Collected

47%

32%

37%

32%

46%

39%

37%

33%60%

42%

58%

48%

52%

41%

44%

58%

46%

42%

47%

39%

37% 32%

37%

41%

36% 35%

43%

40%

42%

40%

41%

37%

44%

42%

36% DC 42%

MD 42%

NJ 43%

42%

CT 39%

RI 36%

MA 48%

VT 51%

35%

40%

44%

HI 36%

38

25% - 35% 36% - 45% 46% + States With No Sales Tax

N/A

N/A

N/A

N/A

Breadth of States’ Manufacturing Equipment Exemptions

39

32% DCMDNJ

CTRIMAVT

HI

None or Restricted Exemption Direct or Primary Use Exemption Integrated Plant Exemption

States with No Sales TaxWA

OR

CA

NV

AZ

AK

ID

MT

WY

UT

ND

SD

NE

CO

NM

KS

OK

MN

IA

MO

AR

TX

WI

MI

IL IN

KY

TN

MS

LA

AL GA

FL

SC

NC

VAWV

OH

PA

NY

VTNH

ME

MACT

NJMD

Double Taxation of Select Service Providers: Wired/Wireless, Cable, Electric and Gas

No Double Tax

1 Service Industry Double Taxed 3 Service Industries Double Taxed2 Service Industries Double Taxed

40

States with No Sales Tax

32% DCMDNJ

CTRIMAVT

HI

WA

ORID

CA

NV

MT

WY

UT

AZ

CO

ND

SD

NE

KS

NM

TX

AK

MN

WI

MI

IA

MO

OK AR

LA

TN

MS

IL INOH

PA

NY

VT

ME

NH

WVVA

NC

SC

GAAL

FL

MDNJ

MACT

Fair Sales Tax Administration

– Exemption Certificate Procedure - 2 points

▪ Good faith on acceptance

▪ 120-day period on audit to perfect

▪ Allow MTC or SSUTA certificate

▪ Verification of exemption/account number

– Vendor Compensation – 2 points

▪ No vendor comp. or less than $12,000 per year (de minimis) - 2 points

▪ At least 0.5% for one-rate state or 0.75% for states with local rates – no

points

– Broad Direct Pay – 1 point

▪ Not overly restrictive – no thresholds over $1 million per year

– New Mexico’s Score – 5 (out of 5) points

41

Fair Sales Tax Administration – States’ Grades

42

Good Faith Requirement

43

Exemption Certificates

44

Vendor Compensation

45

Direct Pay

46

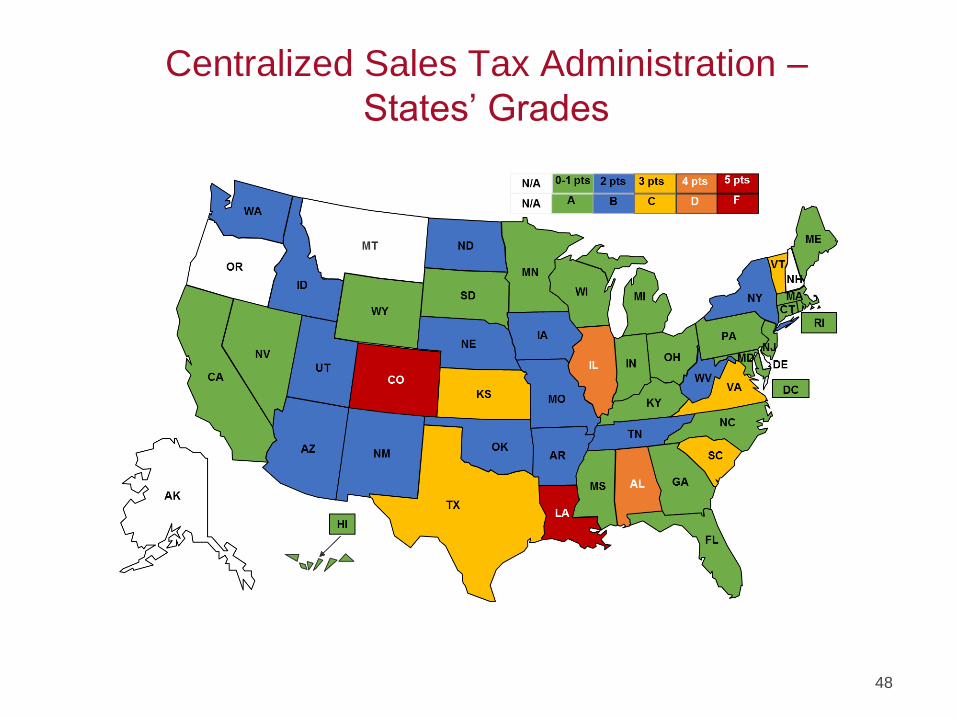

Centralized Sales Tax Administration

– Population of state as compared to number of local jurisdictions - 1

point

▪ Less than 20,000 – 1 point

– Central administration – 3 points

▪ Uniform tax base

▪ Centralized filing and auditing

▪ Centralized appeals

– Website has current & historical tax rates and boundaries – 1 point

– New Mexico’s Score – 2 (out of 4) points

47

Centralized Sales Tax Administration –

States’ Grades

48

States with Local Sales Tax Jurisdictions

49

Number of Taxing Jurisdictions

50

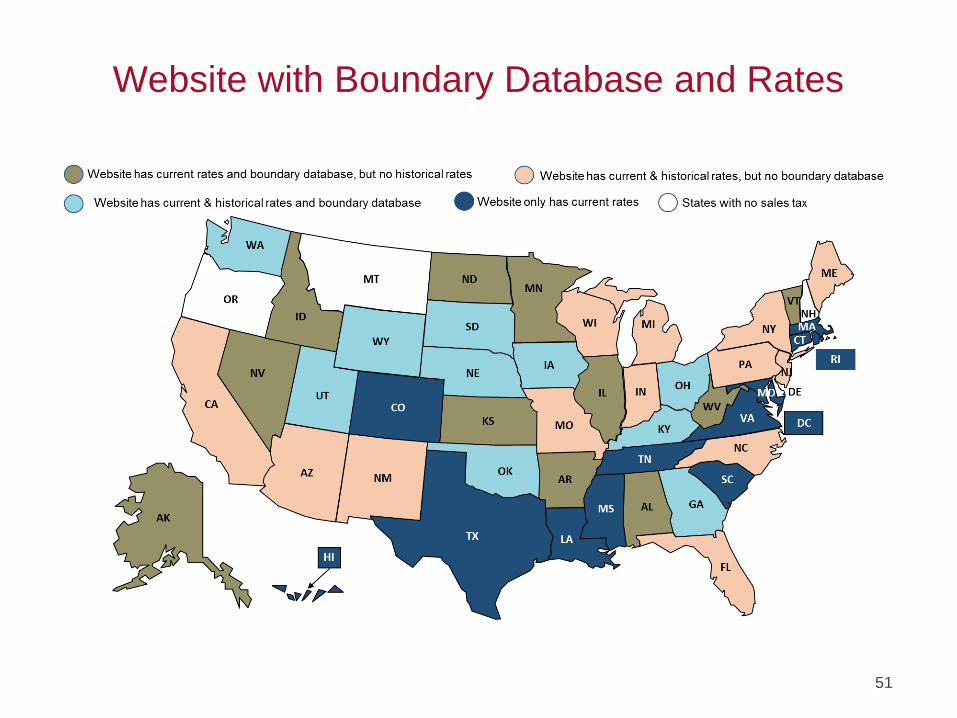

Website with Boundary Database and Rates

51

Simplification & Transparency

– SSUTA State - 2 points

– Tax on digital products and prewritten software – 2 points

▪ Is by legislation or administrative rule/policy position?

– Liability relief – 1 point

▪ Relief should broadly apply to most written

correspondence

– New Mexico’s Score – 4 (out of 5) points

52

Simplification & Transparency – States’ Grades

53

Streamlined Sales Tax States

54

Taxation of Digital Goods

55

Taxation of a Person Merely Accessing Pre-Written Software

AK

HI

ME

RI

VT

NH

MANYCT

PA

NJ

DC

DE

WV

NC

SC

GA

FL

ILOH

IN

MIWI

KY

TN

ALMS

AR

LATX

OK

MOKS

IA

MN

ND

SD

NE

NMAZ

CO

UT

WY

MT

WA

OR

ID

NV

CAVA

MD

No Tax Imposed Tax Imposed Without Statutory Authority

56

Tax Imposed by Statutory Authority

States With No Sales Tax

Tax Liability Relief for Sellers Relying on

Guidance

57

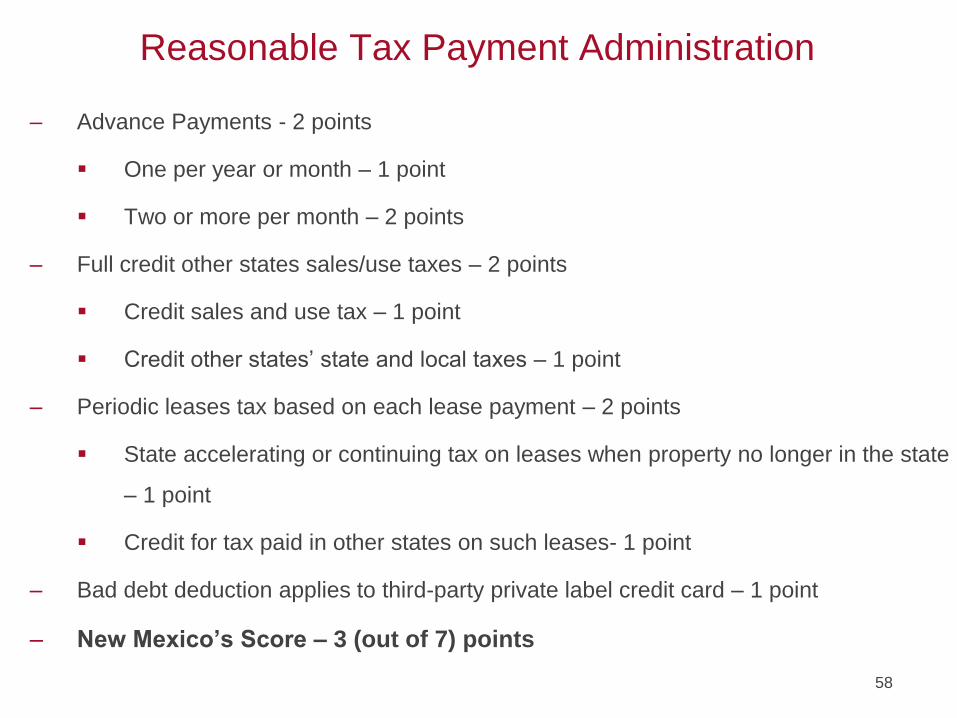

Reasonable Tax Payment Administration

– Advance Payments - 2 points

▪ One per year or month – 1 point

▪ Two or more per month – 2 points

– Full credit other states sales/use taxes – 2 points

▪ Credit sales and use tax – 1 point

▪ Credit other states’ state and local taxes – 1 point

– Periodic leases tax based on each lease payment – 2 points

▪ State accelerating or continuing tax on leases when property no longer in the state

– 1 point

▪ Credit for tax paid in other states on such leases- 1 point

– Bad debt deduction applies to third-party private label credit card – 1 point

– New Mexico’s Score – 3 (out of 7) points

58

Reasonable Tax Payment Procedure –

States’ Grades

59

Advance Payments

AK

HI

ME

RI

VT

NH

MANYCT

PA

NJ

DC

DE

WV

NC

SC

GA

FL

ILOH

IN

MIWI

KY

TN

ALMS

AR

LATX

OK

MOKS

IA

MN

ND

SD

NE

NMAZ

CO

UT

WY

MT

WA

OR

ID

NV

CAVA

MD

No Advance Payments 1 Advance Payment Per Month or Year

60

More Than 1 Advance Payment Per Month

States with no sales tax

Tax Credit Against Sales and Use Tax

61

Full Credit For Other States’

State & Local Sales and Use Taxes

62

Bad Debt Deduction

63

Fair Audit/Refund Procedures

– Purchasers ability to obtain refunds directly from the state

- 1 point

– False claims act & class action suits – 2 points

▪ Allow either – 1 point each

– Contingent fee or private auditing – 1 point

▪ Allow either – 1 point

– New Mexico’s Score – 1 (out of 4) points

64

Fair Refund/Audit Procedures –

States’ Grades

65

False Claims Act

66

AK

HI

ME

RI

VTNHMANY

CT

PANJ

MDDE

VAWV

NC

SC

GA

FL

ILOHIN

MIWI

KY

TN*

ALMS

AR

LATX

OK

MOKS

IA

MN ND

SD

NE

NMAZ

CO*UT

WY

MT

WA

OR

ID

NV

CA*

DC

Accelerated Lease Payments (ALPs)

No ALPs With Credit

ALPs and Continued Tax on Leases With Credit

67

No ALPs, No Credit

ALPs and Continued Tax on Leases With No Credit*CA, CO, TN: Continues tax on certain lease payments using origin location

Class Action Suits

68

Contingent Fee / Private Auditing

69

SSN and Other Issues

AK

HI

ME

RI

VTNH

MANYCT

PANJ

DC

DEWV

NC

SC

GA

FL

ILOH

IN

MIWI

KY

TN

ALMS

AR

LATX

OK

MOKS

IA

MN

ND

SD

NE

NMAZ

COUT

WY

MT

WA

OR

ID

NV

CAVA

MD

70

SSN and/or Home Addresses Other Issues