special business decisions and capital budgeting chapter 24 horngren ♦ harrison ♦ bamber ♦...

TRANSCRIPT

Special Business Decisions

and Capital Budgeting

Chapter 24

HORNGREN ♦ HARRISON ♦ BAMBER ♦ BEST ♦ FRASER ♦ WILLETT

24 - 2Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Objectives

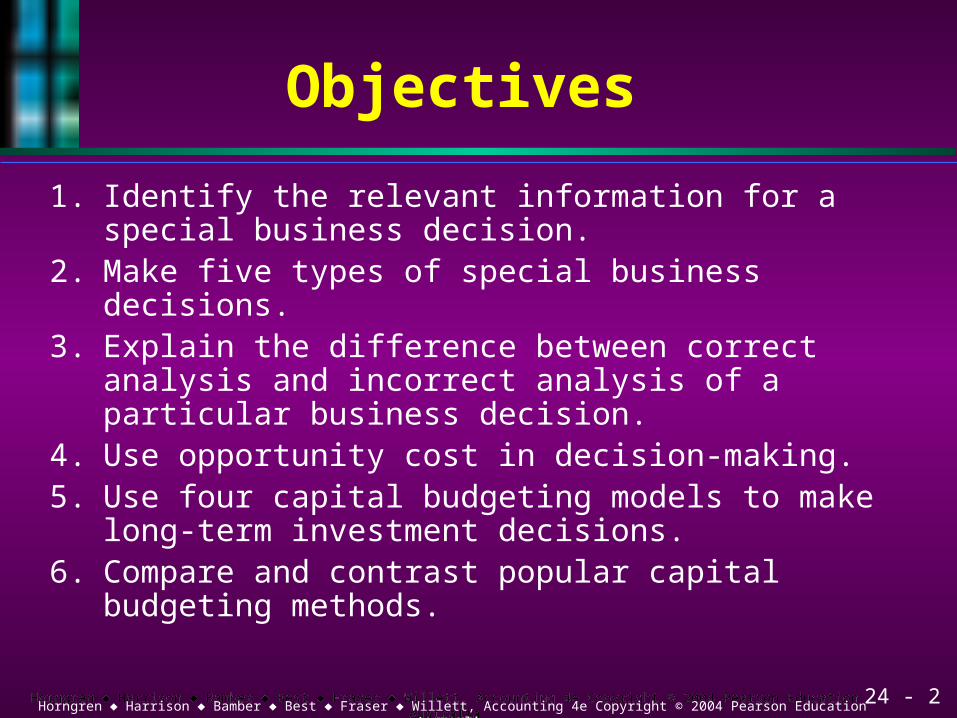

1. Identify the relevant information for a special business decision.

2. Make five types of special business decisions.3. Explain the difference between correct analysis

and incorrect analysis of a particular business decision.

4. Use opportunity cost in decision-making.5. Use four capital budgeting models to make long-

term investment decisions.6. Compare and contrast popular capital budgeting

methods.

24 - 3Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Identify the relevant informationfor a special business decision.

Objective 1

24 - 4Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

It is expected future data thatdiffers among alternatives.

It is expected future data thatdiffers among alternatives.

Only relevant data affect decisions.Only relevant data affect decisions.

Relevant Informationfor Decision Making

Relevant information has two distinguishing characteristics.

24 - 5Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Make five types of short-termspecial business decisions.

Objective 2

24 - 6Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Special Sales Order

ACDelco is a manufacturer of automobile parts located in Taree.

Ordinarily they sells oil filters for $3.20 each.

R. Pino and Co., from Fiji, has offered $35,000 for 20,000 oil filters, or $1.75 per filter.

24 - 7Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Special Sales Order

ACDelco’s manufacturing product cost is $2 per oil filter which includes variable manufacturing costs of $1.20 and fixed manufacturing overhead of $0.80.

Suppose that they made and sold 250,000 oil filters before considering the special order.

Should ACDelco accept the special order ?

24 - 8Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Special Sales Order

The $1.75 offered price will not cover the $2 manufacturing cost.

However, the $1.75 price exceeds variable manufacturing costs by $0.55 per unit.

Accepting the order will increase ACDelco’s contribution margin (and net profit).

20,000 units × $0.55 contribution margin per unit = $11,000

24 - 9Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Dropping Products,Departments, Territories

Assume that ACDelco already is operating at the 270,000 unit level (250,000 oil filters and 20,000 air cleaners).

Suppose that the company is considering dropping the air cleaner product line.

Revenues for the air cleaner product line are $35,000.

Should they drop the air cleaner line?

24 - 10Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Dropping Products,Departments, Territories

Variable manufacturing expenses are $1.20 per unit.

Total fixed expenses are $325,000. Total fixed expenses will continue even

if the product line is dropped.

24 - 11Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Product LineOil Filters Air Cleaners

TotalUnits 250,000 20,000 270,000Sales $800,000 $ 35,000 $835,000Variable expenses 375,000 24,000 399,000Contribution margin $425,000 $ 11,000 $436,000Fixed expenses 300,926 24,074

325,000Operating profit/(loss) $124,074 ($13,074) $111,000

Dropping Products,Departments, Territories

24 - 12Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Dropping Products,Departments, Territories

To measure product-line operating profit, ACDelco allocates fixed expenses in proportion to the number of units sold.

Total fixed expenses are $325,000 ÷ 270,000 units, or $1.20 fixed unit cost.

(more exactly $1.2037) Fixed expenses allocated to the air

cleaner product line are 20,000 units × $1.20 per unit, or $24,074.

24 - 13Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Oil Filters AloneUnits 250,000Sales $800,000Variable expenses 375,000Contribution margin 425,000Fixed expenses 325,000Net profit $100,000

Dropping Products,Departments, Territories

24 - 14Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Dropping Products,Departments, Territories

Suppose that the company employs a supervisor for $18,000.

This cost can be avoided if the company stops producing air cleaners.

Should the company stop producing air cleaners?

Yes! $11,000 – $18,000 = ($7,000)

24 - 15Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Product Mix

Companies must decide which products to emphasise if certain constraints prevent unlimited production or sales.

Assume that ACDelco produces oil filters and windscreen wipers.

The company has 4,000 machine hours available to produce these products.

24 - 16Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Product Mix

ACDelco can produce 5 oil filters in one hour or 8 windscreen wipers.

Product Oil Windscreen

Per Unit Filters WipersSales price $3.22 $13.50Variable expenses 1.50 12.00Contribution margin $1.72 $ 1.50Contribution margin ratio 53% 11%

24 - 17Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

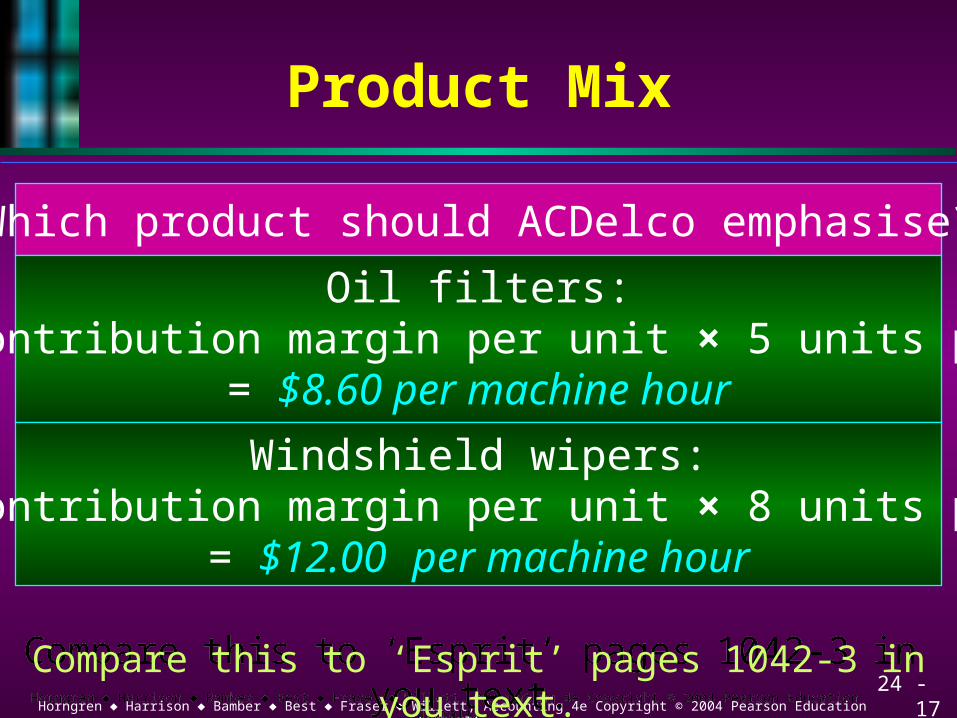

Product Mix

Which product should ACDelco emphasise?

Oil filters:$1.72 contribution margin per unit × 5 units per hour

= $8.60 per machine hour

Windshield wipers:$1.50 contribution margin per unit × 8 units per hour

= $12.00 per machine hour

Compare this to ‘Esprit’ pages 1042-3 in you text.Compare this to ‘Esprit’ pages 1042-3 in you text.

24 - 18Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Outsourcing (Make or Buy)

ACDelco is considering the production of a part it needs, or using a model produced by Fram Pty Ltd.

Fram offers to sell the part for $0.37. Should ACDelco manufacture the part

or buy it?

24 - 19Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Outsourcing (Make or Buy)

ACDelco has the following costs for250,000 units of Part no. 4:

Part no. 4 costs: TotalDirect materials $ 40,000Direct labour 20,000Variable overhead 15,000Fixed overhead 50,000Total $125,000

$125,000 ÷ 250,000 units = $0.50/unit

24 - 20Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Outsourcing (Make or Buy)

Assume that by purchasing the part, ACDelco can avoid all variable manufacturing costs and reduce fixed costs by $10,000 (fixed costs will decrease to $40,000).

ACDelco should continue to manufacture the part.

Why?

24 - 21Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Purchase cost (250,000 × $0.37) $ 92,500Fixed costs that will continue 40,000Total $132,500

The unit cost is then $0.53($132,500 ÷ 250,000).

$132,500 – $125,000 = $7,500, which is thedifference in favour of manufacturing the part.

Outsourcing (Make or Buy)

See Exhibit 24-8 page 1044 See Exhibit 24-8 page 1044

24 - 22Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

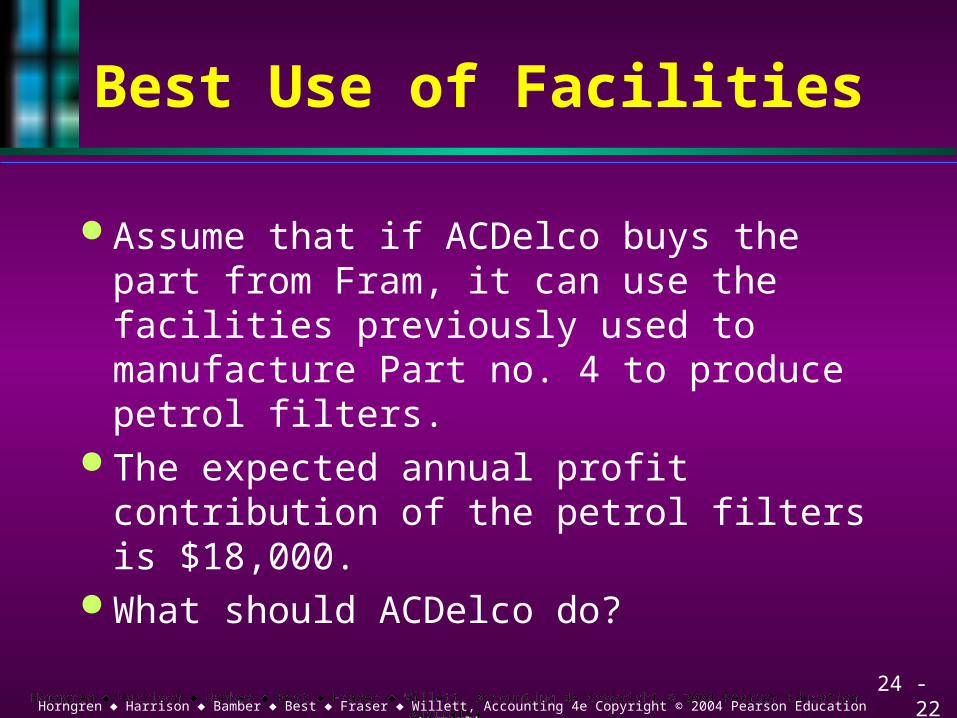

Best Use of Facilities

Assume that if ACDelco buys the part from Fram, it can use the facilities previously used to manufacture Part no. 4 to produce petrol filters.

The expected annual profit contribution of the petrol filters is $18,000.

What should ACDelco do?

24 - 23Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Expected cost of obtaining 250,000 parts:

Make part $125,000Buy part and leave facilities idle $132,500Buy part and use facilities for CD cases $114,500*

*Cost of buying part: $132,500 less$18,000 contribution from petrol filters.

Best Use of Facilities

24 - 24Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Sell As-Is Or Process Further

The sell as-is or process further is a decision whether to incur additional manufacturing costs and sell the inventory at a higher price, or sell the inventory as-is at a lower price.

Suppose that ACDelco spends $500,000 to produce 250,000 oil filters.

ACDelco can sell these filters for $3.20 per filter, for a total of $800,000.

24 - 25Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Sell As-Is Or Process Further

Alternatively, ACDelco can further process these filters into super filters at an additional cost of $25,000, which is $0.10 per unit ($25,000 ÷ 250,000).

Super filters will sell for $3.50 per filter for a total of $875,000.

Should they process the filters into super filters?

24 - 26Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

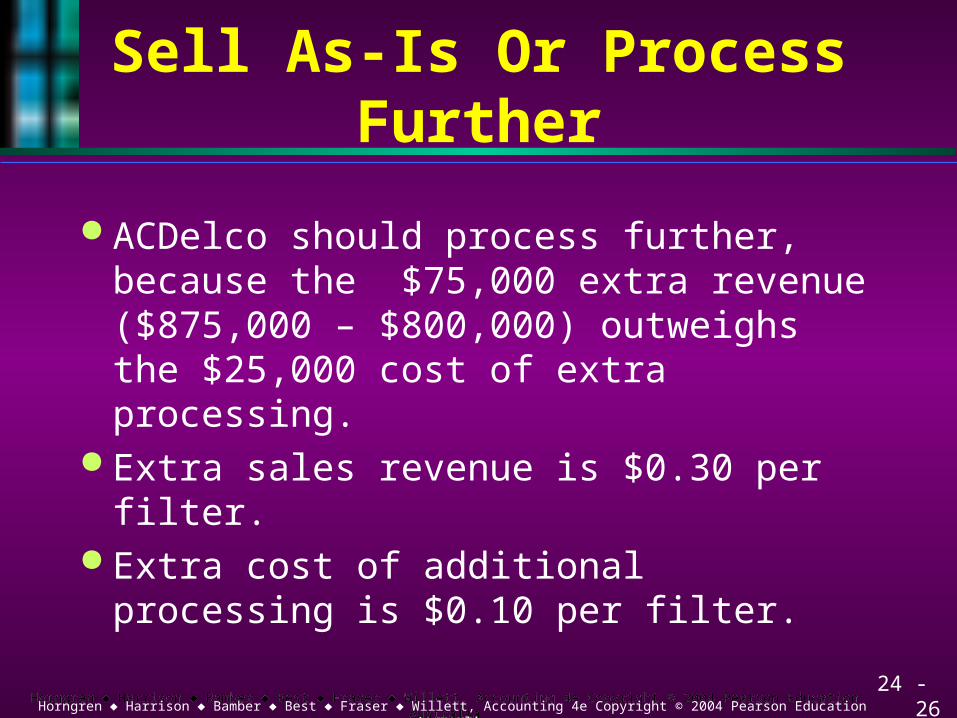

Sell As-Is Or Process Further

ACDelco should process further, because the $75,000 extra revenue ($875,000 – $800,000) outweighs the $25,000 cost of extra processing.

Extra sales revenue is $0.30 per filter. Extra cost of additional processing is

$0.10 per filter.

24 - 27Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Sell As-Is Or Process Further

Cost to produce 250,000 parts: $500,000

Sell these parts for $3.20 each: $800,000

Cost to process original parts further: $ 25,000

Sell these parts for $3.50 each: $875,000

Sales increase ($875,000 – $800,000) $ 75,000Less processing cost increase 25,000Net gain by processing further $ 50,000

24 - 28Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Explain the difference betweencorrect and incorrect

analysis of a particularbusiness decision.

Objective 3

24 - 29Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Correct Analysis

A correct analysis of a business decision focuses on differences in revenues and expenses.

The contribution margin approach, which is based on variable costing, often is more useful for decision analysis.

It highlights how expenses and revenue are affected by sales volume.

24 - 30Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Incorrect Analysis

The conventional approach to decision making, which is based on absorption costing, may mislead managers into treating a fixed cost as a variable cost.

Absorption costing treats fixed manufacturing overhead as part of the unit cost.

24 - 31Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Use opportunity costsin decision-making.

Objective 4

24 - 32Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Opportunity Cost...

– is the benefit that can be obtained from the next best course of action.

Opportunity cost is not an outlay cost, so it is not recorded in the accounting records.

Suppose that ACDelco is approached by a customer that needs 250,000 regular oil filters.

24 - 33Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Opportunity Cost

The customer is willing to pay more than $3.20 per filter.

ACDelco’s managers can use the $850,000 ($875,000 – $25,000) opportunity cost of not further processing the oil filters to determine the sales price that will provide an equivalent net profit.

$850,000 ÷ 250,000 units = $3.40

24 - 34Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Use four capital budgeting

models to make longer-term

investment decisions.

Objective 5

24 - 35Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

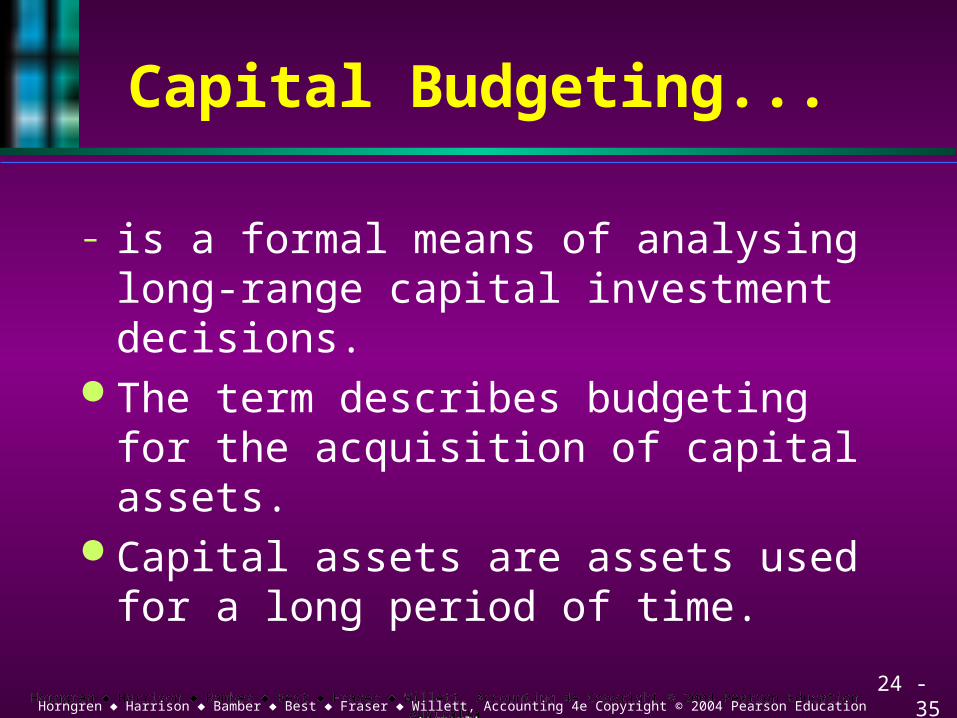

Capital Budgeting...

– is a formal means of analysing long-range capital investment decisions.

The term describes budgeting for the acquisition of capital assets.

Capital assets are assets used for a long period of time.

24 - 36Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Capital Budgeting

Capital budget models using net cash inflow from operations are:

– payback– accounting rate of return– net present value– internal rate of return

24 - 37Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

1 2 3

4 5 6 7 8 9 10

11 12 13 14 15 16 17

18 19 20 21 22 23 24

25 26 28 29 30 3127

Payback...

– is the length of time it takes to recover, in net cash inflows from operations, the dollars of capital outlays.

An increase in cash could result from an increase in revenues, a decrease in expenses, or a combination of the two.

24 - 38Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Payback Example

Assume that ACDelco is considering the purchase of a machine for $200,000, with an estimated useful life of 8 years, and zero predicted residual value.

Managers expect use of the machine to generate $40,000 of net cash inflows from operations per year.

24 - 39Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Payback Example

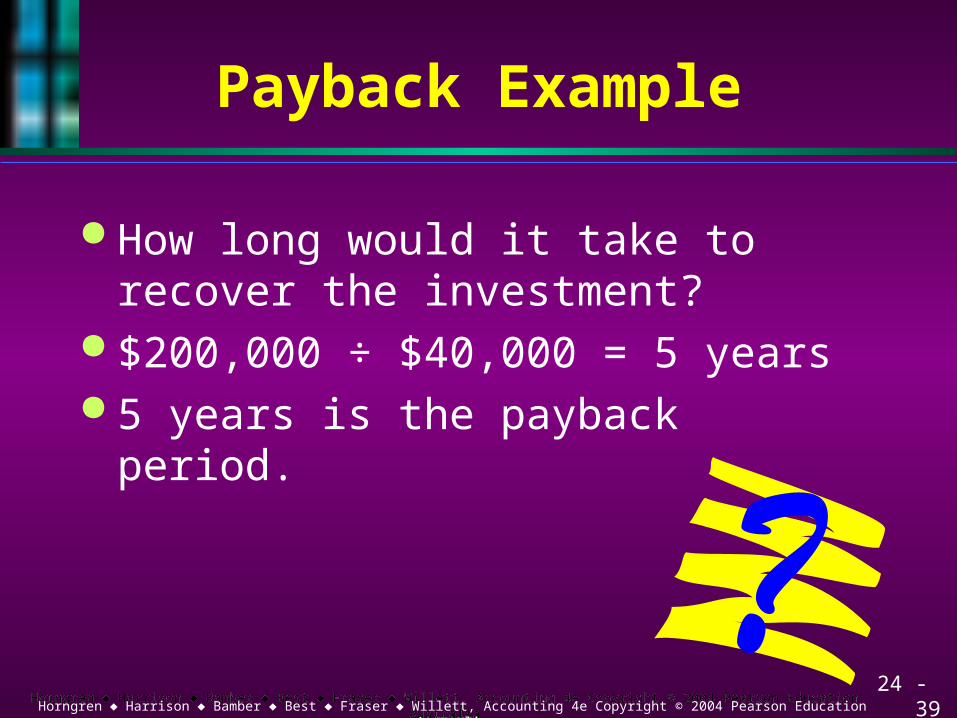

How long would it take to recover the investment?

$200,000 ÷ $40,000 = 5 years 5 years is the payback period.

24 - 40Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Payback Example

When cash flows are uneven, calculations must take a cumulative form.

Cash inflows must be accumulated until the amount invested is recovered.

Suppose that the machine will produce net cash inflows of $90,000 in Year 1, $70,000 in Year 2, and $30,000 in Years 3 through 8.

24 - 41Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Payback Example

What is the payback period? Years 1, 2, and 3 together bring in

$190,000. Recovery of the amount invested

occurs during Year 4. Recovery is 3 years + $10,000. 3 years + ($10,000 ÷ $30,000) = 3 years

and 4 months

24 - 42Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Accounting Rate of Return...

– measures profitability. It measures the average return over the

life of the asset. It is calculated by dividing average

annual net profit by the average amount of investment in the asset.

24 - 43Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Accounting Rate of Return Example

Assume that a machine costs $200,000, has no residual value, and has a useful life of 8 years.

How much is the straight-line depreciation per year?

$25,000 Management expects the machine to

generate annual net cash inflows of $40,000.

24 - 44Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Accounting Rate of Return Example

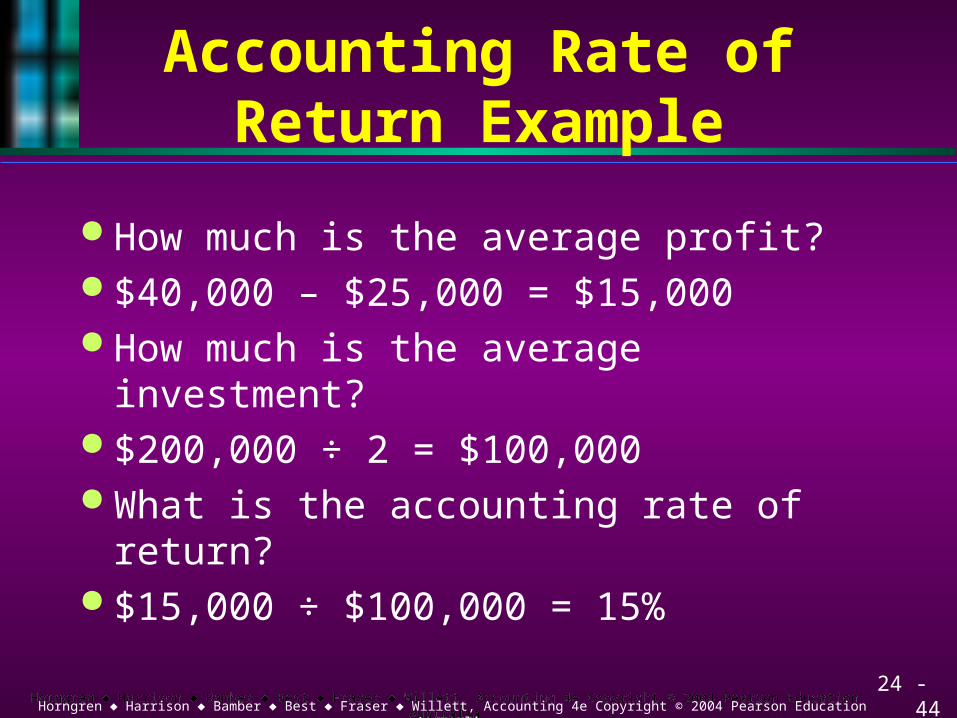

How much is the average profit? $40,000 – $25,000 = $15,000 How much is the average investment? $200,000 ÷ 2 = $100,000 What is the accounting rate of return? $15,000 ÷ $100,000 = 15%

24 - 45Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Discounted Cash-Flow Models

Discounted cash-flow models take into account the time value of money.

The time value of money means that a dollar invested today can earn revenue and become greater in the future.

These methods take those future values and discount them (deduct interest) back to the present.

24 - 46Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Discounted Cash-Flow Models

How much do I need to invest today at 16% to have $1 in one year?

86.2c So if you receive $1 in one years time

the present value is 86.2c See exhibit 24-15 p1054

24 - 47Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Net Present Value

The (NPV) method calculates the expected net monetary gain or loss from a project by discounting all expected cash flows to the present.

The amount of interest deducted is determined by the desired rate of return.

This rate of return is called the ‘discount rate’, ‘hurdle rate’, ‘required rate of return’, or ‘cost of capital’.

24 - 48Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Net Present Value Example

ACDelco is considering an investment of $450,000.

This proposed investment will yield yearly net cash inflows of $225,000, $230,000, and $210,000 over its three year life.

ACDelco expects a return of 16%. Should the investment be made?

24 - 49Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Net Present Value Example

Periods Amount PV Factor Present Value0 ($450,000) 1.000 ($450,000)1 225,000 0.862 193,9502 230,000 0.743 170,8903 210,000 0.641 134,610

Total PV of net cash inflows $499,450Net present value of project $ 49,450

24 - 50Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Internal Rate of Return...

– is another model using discounted cash flows.

The internal rate of return (IRR) is the rate of return that a company can expect to earn by investing in a project.

The higher the IRR, the more desirable the investment.

24 - 51Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Internal Rate of Return

The IRR is the rate of return at which the net present value equals zero.

Investment = Expected annual net cash inflow × PV annuity factor

Investment ÷ Expected annual net cash inflow = PV annuity factor

24 - 52Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Internal Rate of Return Example

Assume that ACDelco is considering investing $500,000 in a project that will yield net cash inflows of $152,725 per year over its 5-year life.

What is the IRR of this project? $500,000 ÷ $152,725 = 3.274 (PV

annuity factor – see exhibit 24-15 p 1054)

24 - 53Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Internal Rate of Return Example

The annuity table shows that 3.274 is in the 16% column for a 5-period row in this example.

Therefore, 16% is the internal rate of return of this project.

If the minimum desired rate of return is 16% or less, ACDelco should undertake this project.

24 - 54Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Compare and contrast popular

capital budgeting methods.

Objective 6

24 - 55Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Comparison of CapitalBudgeting Models

The discounted cash-flow models, net present value, and internal rate of return are conceptually superior to the payback and accounting rate of return models.

Strengths of the payback include: It is easy to calculate, highlights risks,

and is based on cash flows.

24 - 56Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

Comparison of CapitalBudgeting Models

Payback’s weaknesses are that it ignores cash flows beyond the payback, the time value of money (the pattern of cash flows), and profitability.

The strength of the accounting rate of return is that it is based on profitability.

Its weakness is that it ignores the time value of money.

24 - 57Horngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education AustraliaHorngren ♦ Harrison ♦ Bamber ♦ Best ♦ Fraser ♦ Willett, Accounting 4e Copyright © 2004 Pearson Education Australia

End of Chapter 24