speaker(s)/confÉrencier(s) : marc tardif,...

TRANSCRIPT

SESSION/SÉANCE : 47 – CALM for thoughts

SPEAKER(S)/CONFÉRENCIER(S) :

Marc Tardif, Deloitte

AGENDA

• Changing economic environment

• Return on EN on Investment Return Assumptions

for NFI Assets

• CSOP Interpretations

• Default Rates and Risk Premiums

2

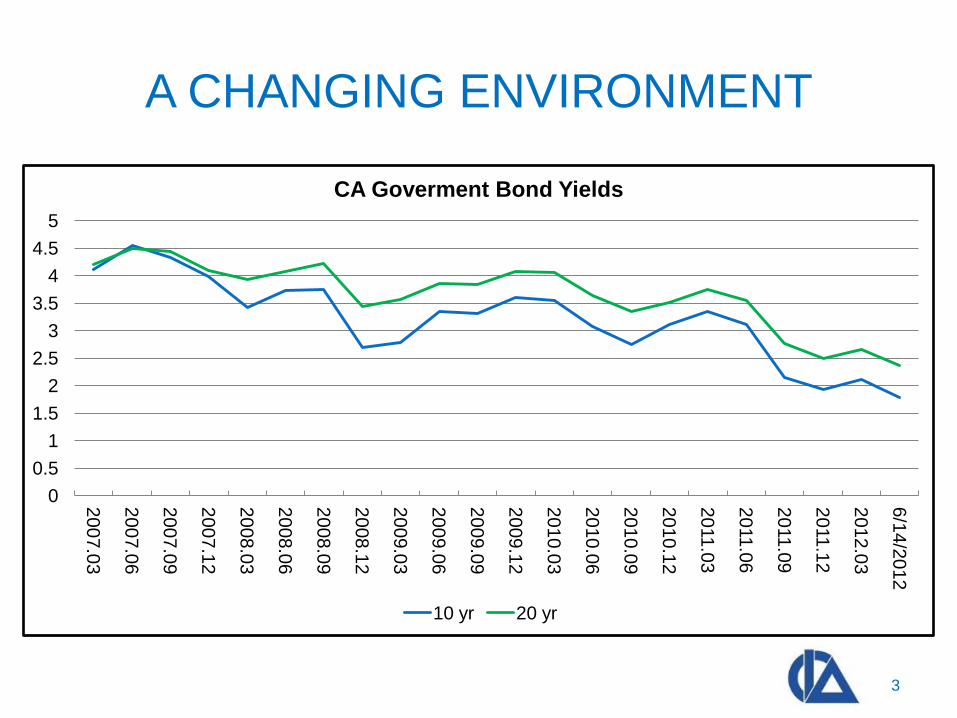

A CHANGING ENVIRONMENT

3

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

20

07

.03

20

07

.06

20

07

.09

20

07

.12

20

08

.03

20

08

.06

20

08

.09

2008.1

2

20

09

.03

20

09

.06

20

09

.09

20

09

.12

20

10

.03

2010.0

6

20

10

.09

20

10

.12

20

11

.03

20

11

.06

20

11

.09

2011.1

2

20

12

.03

6/1

4/2

01

2

CA Goverment Bond Yields

10 yr 20 yr

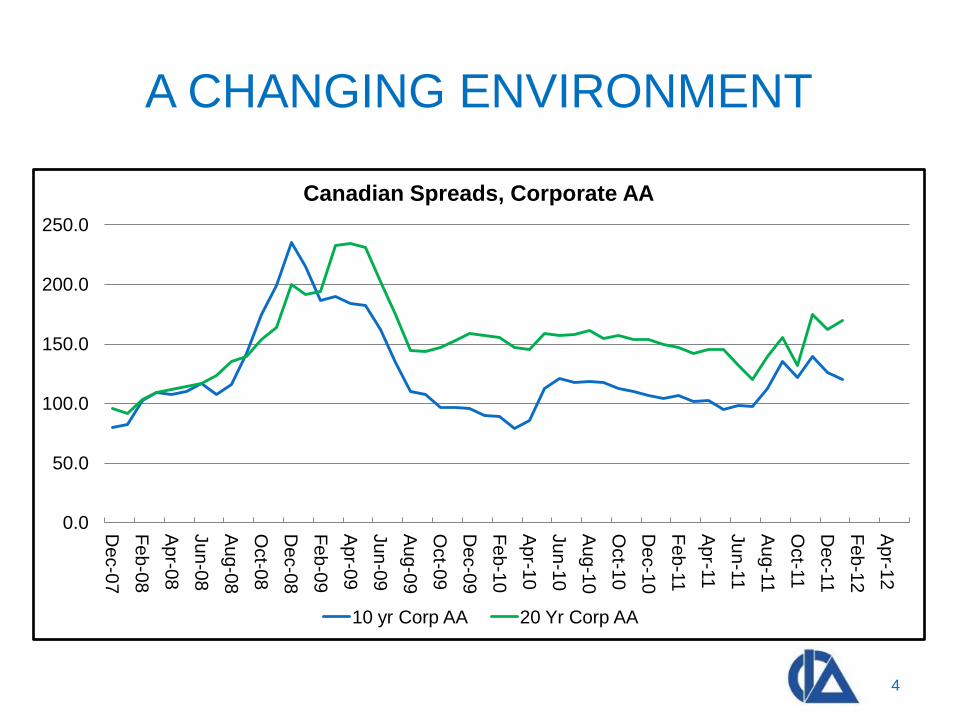

A CHANGING ENVIRONMENT

4

0.0

50.0

100.0

150.0

200.0

250.0

De

c-0

7

Fe

b-0

8

Apr-0

8

Ju

n-0

8

Aug-0

8

Oct-0

8

De

c-0

8

Fe

b-0

9

Apr-0

9

Ju

n-0

9

Aug-0

9

Oct-0

9

De

c-0

9

Fe

b-1

0

Apr-1

0

Ju

n-1

0

Aug-1

0

Oct-1

0

De

c-1

0

Fe

b-1

1

Apr-1

1

Ju

n-1

1

Aug-1

1

Oct-1

1

De

c-1

1

Fe

b-1

2

Apr-1

2

Canadian Spreads, Corporate AA

10 yr Corp AA 20 Yr Corp AA

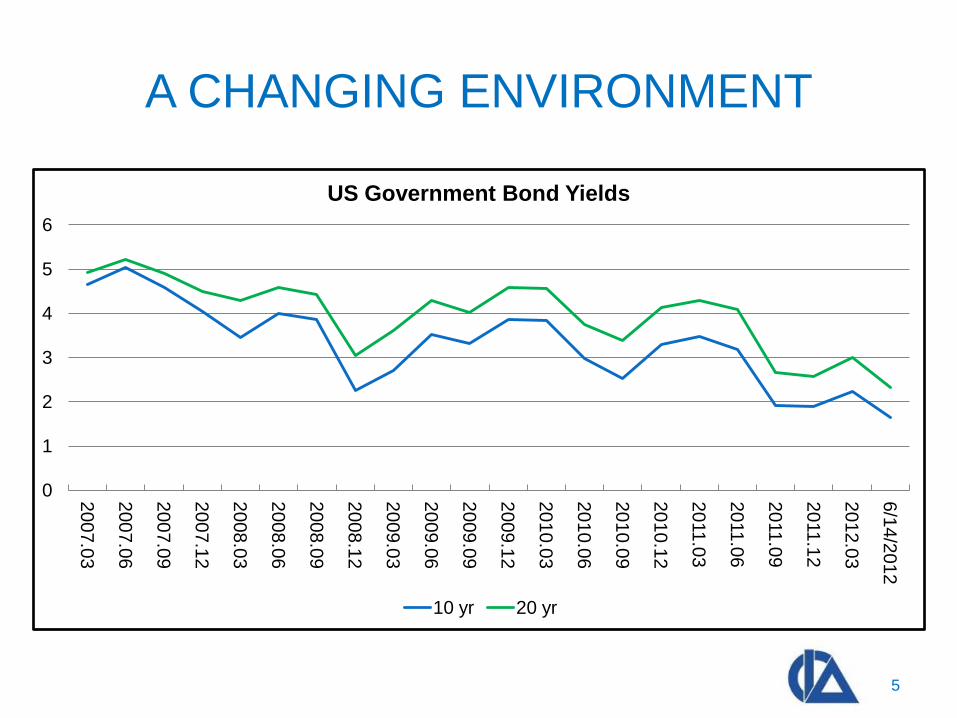

A CHANGING ENVIRONMENT

5

0

1

2

3

4

5

6

20

07

.03

20

07

.06

20

07

.09

20

07

.12

20

08

.03

20

08

.06

20

08

.09

20

08

.12

20

09

.03

20

09

.06

20

09

.09

20

09

.12

20

10

.03

20

10

.06

20

10

.09

20

10

.12

20

11

.03

20

11

.06

20

11

.09

20

11

.12

20

12

.03

6/1

4/2

01

2

US Government Bond Yields

10 yr 20 yr

A CHANGING ENVIRONMENT

6

0

1

2

3

4

5

6

20

07

.03

20

07

.06

20

07

.09

20

07

.12

20

08

.03

20

08

.06

20

08

.09

20

08

.12

20

09

.03

20

09

.06

20

09

.09

20

09

.12

20

10

.03

20

10

.06

20

10

.09

20

10

.12

20

11

.03

20

11

.06

20

11

.09

20

11

.12

20

12

.03

6/1

4/2

01

2

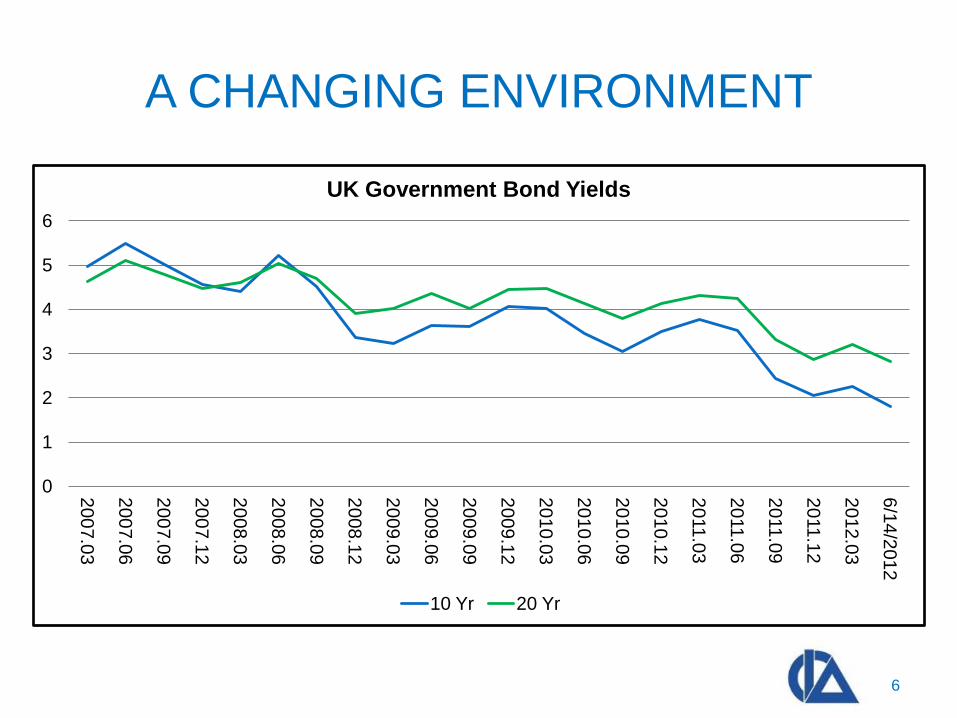

UK Government Bond Yields

10 Yr 20 Yr

A CHANGING ENVIRONMENT

7

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

30-S

ept-0

9

31

-De

c-0

9

31-M

ar-1

0

30-J

un

-10

30-S

ept-1

0

31

-De

c-1

0

31-M

ar-1

1

30-J

un

-11

30-S

ept-1

1

30-D

ec-1

1

30-M

ar-1

2

14-J

un

-12

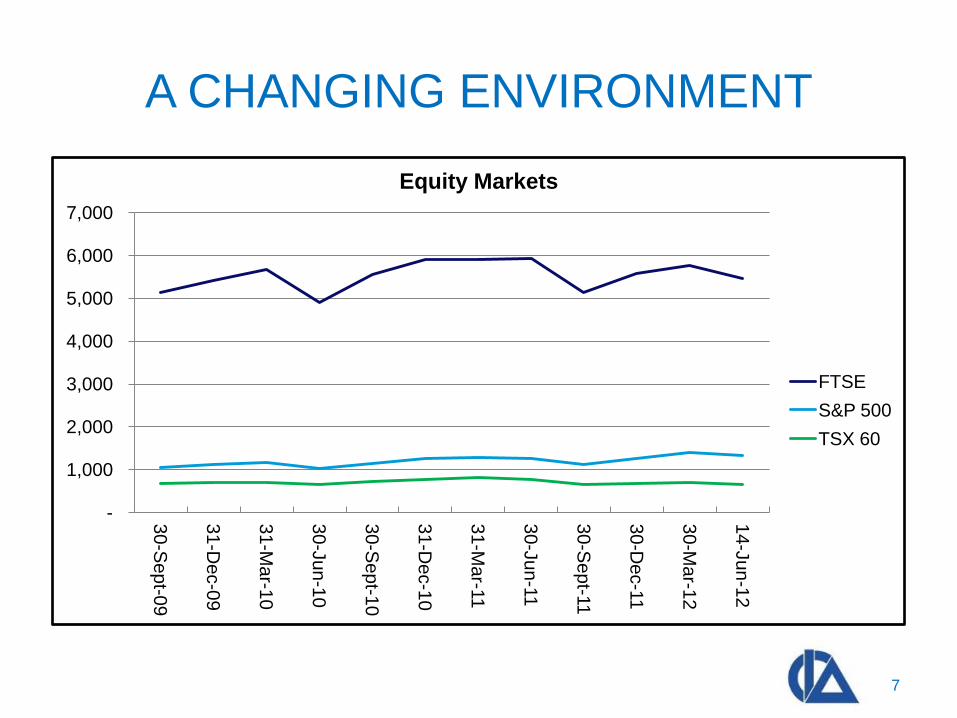

Equity Markets

FTSE

S&P 500

TSX 60

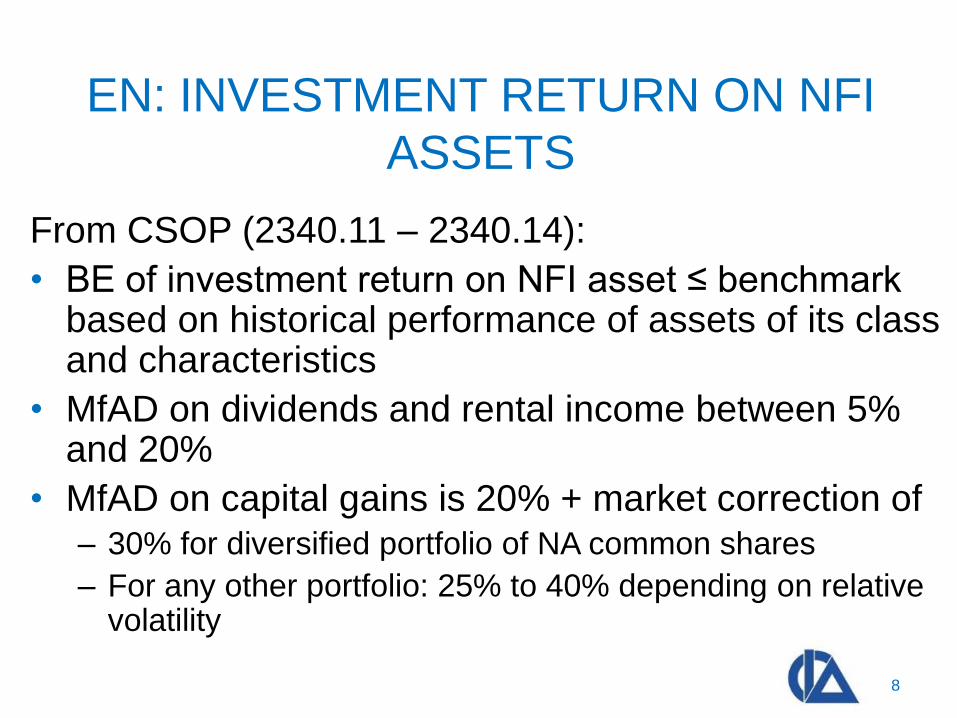

EN: INVESTMENT RETURN ON NFI

ASSETS

From CSOP (2340.11 – 2340.14):

• BE of investment return on NFI asset ≤ benchmark based on historical performance of assets of its class and characteristics

• MfAD on dividends and rental income between 5% and 20%

• MfAD on capital gains is 20% + market correction of – 30% for diversified portfolio of NA common shares

– For any other portfolio: 25% to 40% depending on relative volatility

8

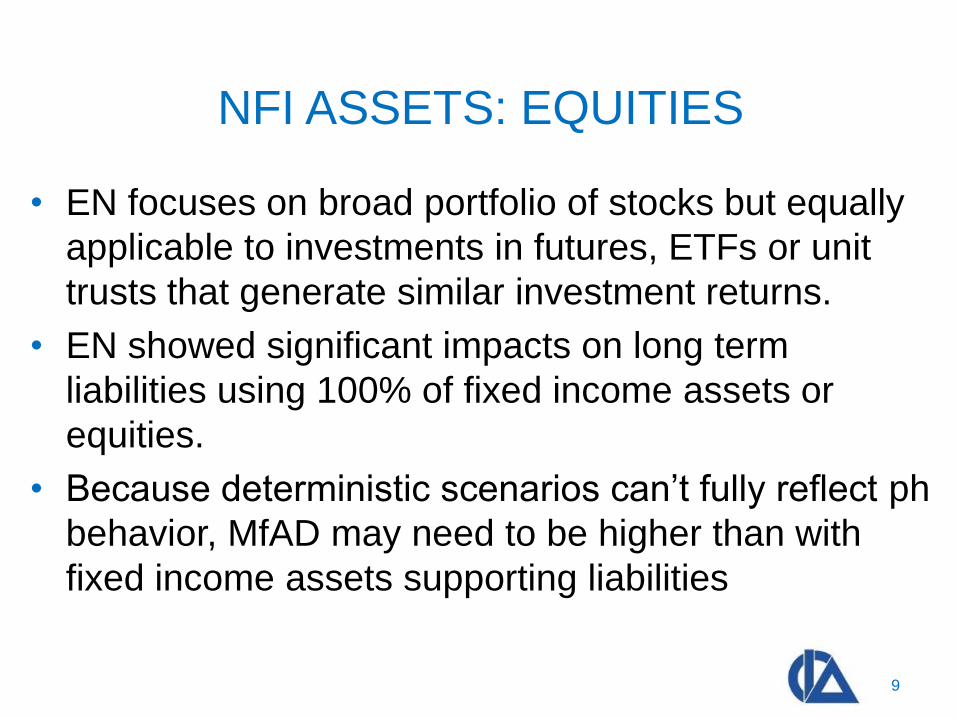

NFI ASSETS: EQUITIES

• EN focuses on broad portfolio of stocks but equally

applicable to investments in futures, ETFs or unit

trusts that generate similar investment returns.

• EN showed significant impacts on long term

liabilities using 100% of fixed income assets or

equities.

• Because deterministic scenarios can’t fully reflect ph

behavior, MfAD may need to be higher than with

fixed income assets supporting liabilities

9

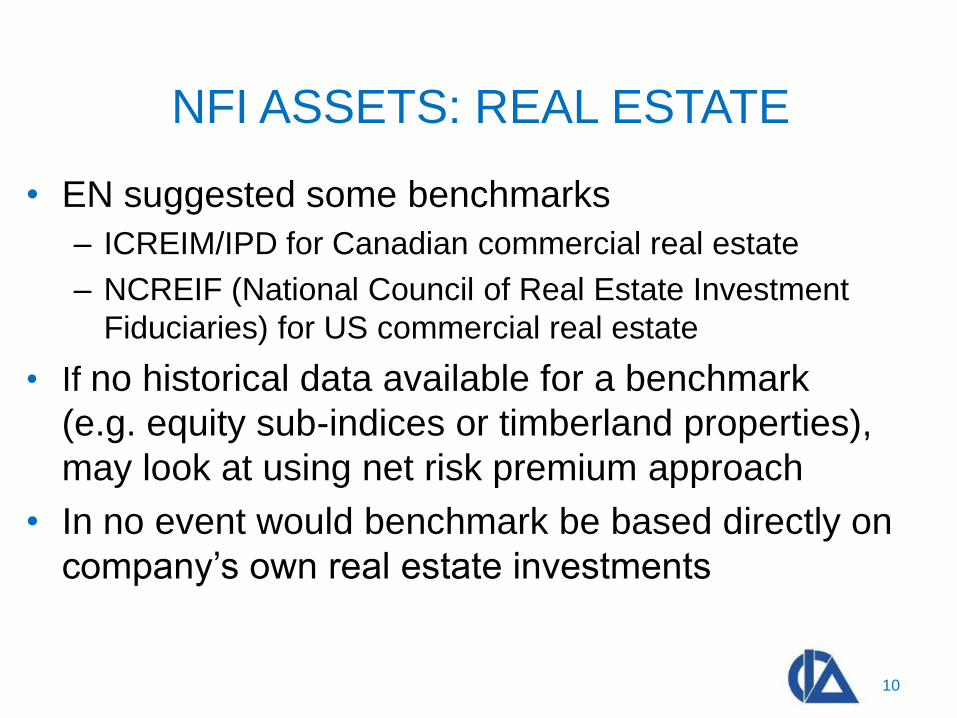

NFI ASSETS: REAL ESTATE

• EN suggested some benchmarks

– ICREIM/IPD for Canadian commercial real estate

– NCREIF (National Council of Real Estate Investment

Fiduciaries) for US commercial real estate

• If no historical data available for a benchmark

(e.g. equity sub-indices or timberland properties),

may look at using net risk premium approach

• In no event would benchmark be based directly on

company’s own real estate investments

10

NFI ASSETS: BENCHMARK SELECTION

• Need “a broad portfolio of assets available in the market or industry with similar performance, geography or sector”

• S&P/TSX Composite index is broad-based but financial, energy and material sectors represent almost 80% of the index’ capitalization

• Data over long historical periods is preferred although for real estate US data only since 1978 and Canadian data from 1985

• Need to be updated at least annually ideally at same month. Lag between calculation and valuation date not to exceed 12 months

11

NFI ASSETS: DIVIDEND AND RENTAL

INCOME

• Dividend yields are generally inversed related to

periods of economic growth and downturns

• Can assume that dividend or rental income not

impacted as significantly under market shift

• Taxable portion of dividend yield changed in 2011 as

income tax changes for income trusts became

effective

12

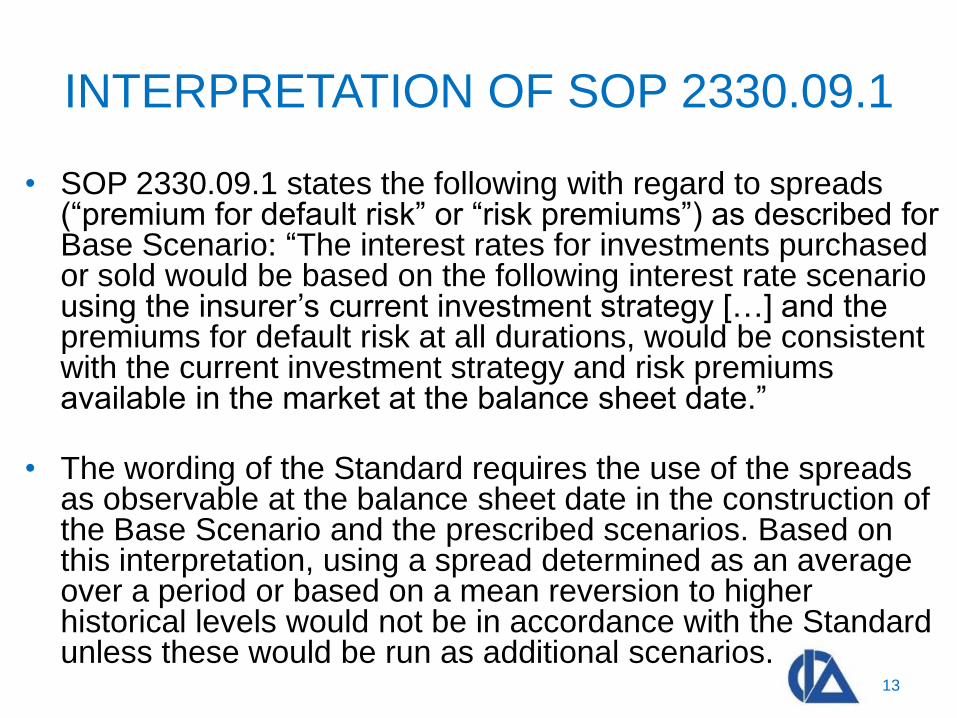

INTERPRETATION OF SOP 2330.09.1

• SOP 2330.09.1 states the following with regard to spreads

(“premium for default risk” or “risk premiums”) as described for Base Scenario: “The interest rates for investments purchased or sold would be based on the following interest rate scenario using the insurer’s current investment strategy […] and the premiums for default risk at all durations, would be consistent with the current investment strategy and risk premiums available in the market at the balance sheet date.”

• The wording of the Standard requires the use of the spreads as observable at the balance sheet date in the construction of the Base Scenario and the prescribed scenarios. Based on this interpretation, using a spread determined as an average over a period or based on a mean reversion to higher historical levels would not be in accordance with the Standard unless these would be run as additional scenarios.

13

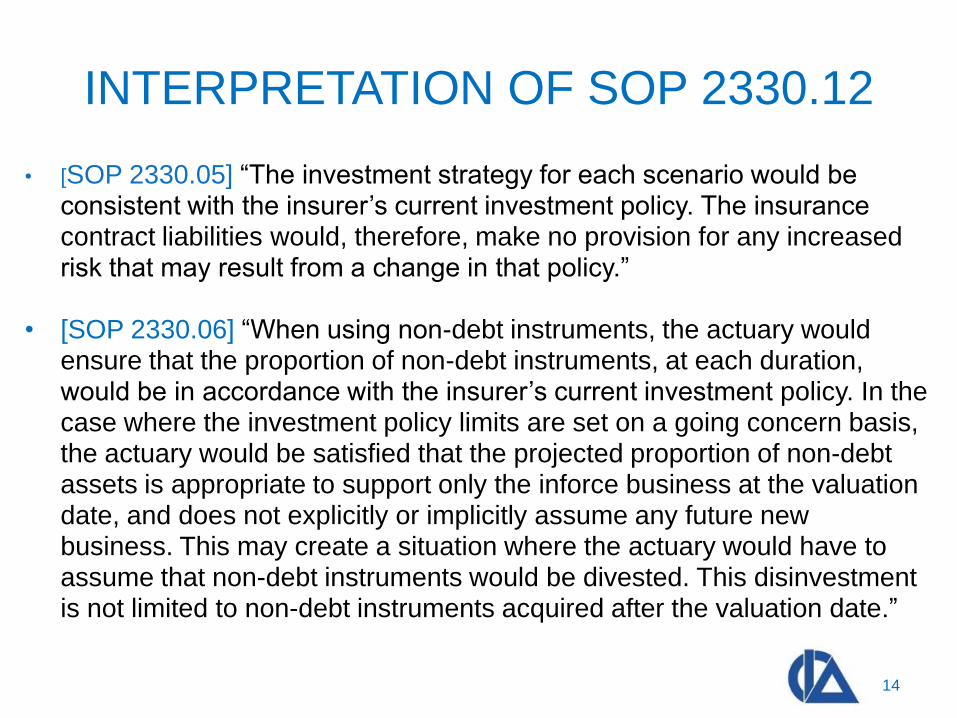

INTERPRETATION OF SOP 2330.12

• [SOP 2330.05] “The investment strategy for each scenario would be

consistent with the insurer’s current investment policy. The insurance contract liabilities would, therefore, make no provision for any increased risk that may result from a change in that policy.”

• [SOP 2330.06] “When using non-debt instruments, the actuary would

ensure that the proportion of non-debt instruments, at each duration, would be in accordance with the insurer’s current investment policy. In the case where the investment policy limits are set on a going concern basis, the actuary would be satisfied that the projected proportion of non-debt assets is appropriate to support only the inforce business at the valuation date, and does not explicitly or implicitly assume any future new business. This may create a situation where the actuary would have to assume that non-debt instruments would be divested. This disinvestment is not limited to non-debt instruments acquired after the valuation date.”

14

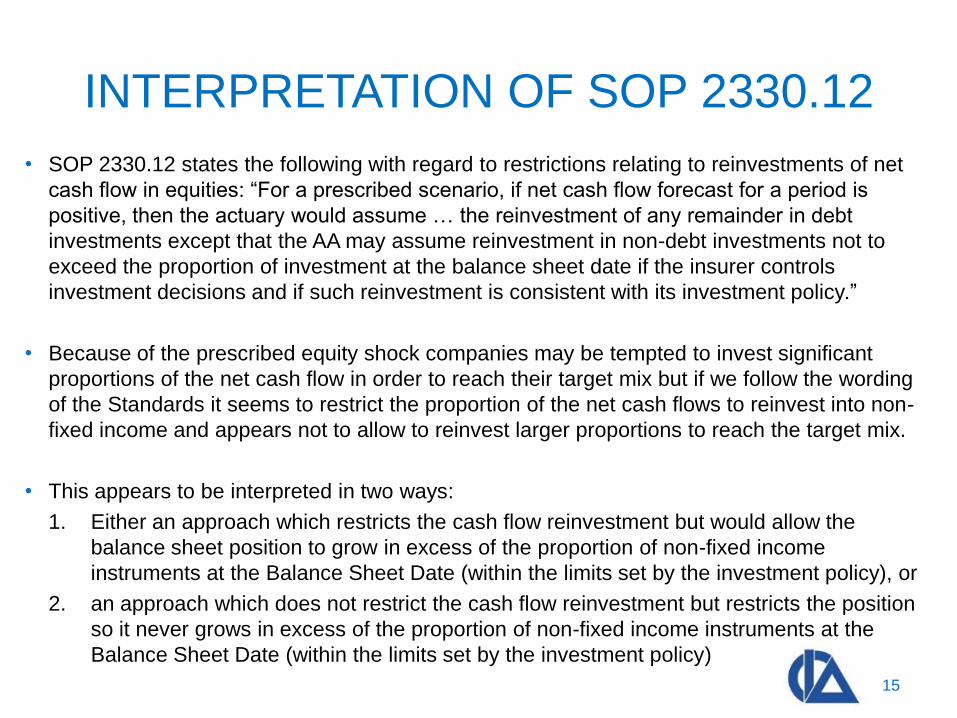

INTERPRETATION OF SOP 2330.12

• SOP 2330.12 states the following with regard to restrictions relating to reinvestments of net

cash flow in equities: “For a prescribed scenario, if net cash flow forecast for a period is

positive, then the actuary would assume … the reinvestment of any remainder in debt

investments except that the AA may assume reinvestment in non-debt investments not to

exceed the proportion of investment at the balance sheet date if the insurer controls

investment decisions and if such reinvestment is consistent with its investment policy.”

• Because of the prescribed equity shock companies may be tempted to invest significant

proportions of the net cash flow in order to reach their target mix but if we follow the wording

of the Standards it seems to restrict the proportion of the net cash flows to reinvest into non-

fixed income and appears not to allow to reinvest larger proportions to reach the target mix.

• This appears to be interpreted in two ways:

1. Either an approach which restricts the cash flow reinvestment but would allow the

balance sheet position to grow in excess of the proportion of non-fixed income

instruments at the Balance Sheet Date (within the limits set by the investment policy), or

2. an approach which does not restrict the cash flow reinvestment but restricts the position

so it never grows in excess of the proportion of non-fixed income instruments at the

Balance Sheet Date (within the limits set by the investment policy)

15

LINKAGE OF DEFAULT RATES AND RISK

PREMIUMS

• In the Standard there is room for interpretation regarding the

implementation of the assumption with regard to default

rates and the implementation of spreads. The default rate is

often on a LT basis whereby the spreads are those

observed at the balance sheet date.

16

REFERENCES

• Standards of Practice - Practice-Specific Standards

for Insurance [Part_2000_Jan_2012_E]

• Educational Note Supplement: Guidance for the

2011 Valuation of Insurance Contract Liabilities of

Life Insurers [211110]

• Educational Note: Approximations to Canadian Asset

Liability Method (CALM) [206133]

• Educational Note: Investment Return Assumptions

for Non-Fixed Income Assets for Life Insurers [211027]

17

AND NOW JEAN-YVES…

18