south shore hospital, inc

TRANSCRIPT

South Shore Hospital, Inc. Financial Statements as of and for the Years Ended September 30, 2011 and 2010, Supplemental Schedules for the Year Ended September 30, 2011, and Independent Auditors’ Report

SOUTH SHORE HOSPITAL, INC.

TABLE OF CONTENTS

Page

INDEPENDENT AUDITORS’ REPORT 1

FINANCIAL STATEMENTS AS OF AND FOR THE YEARS ENDED SEPTEMBER 30, 2011 and 2010: Balance Sheets 2 Statements of Operations and Changes in Net Assets 3–4 Statements of Cash Flows 5–6 Notes to Financial Statements 7–24

SUPPLEMENTAL SCHEDULES FOR THE YEAR ENDED SEPTEMBER 30, 2011: 25 Independent Auditors’ Report on Supplemental Schedules 26 Net Revenue and Gains Available for Debt Service 27 Revenue Available to Meet Expenses and Expenses 28 Note to Supplemental Schedules 29

INDEPENDENT AUDITORS’ REPORT

To the Board of Directors of South Shore Hospital, Inc. South Weymouth, Massachusetts

We have audited the accompanying balance sheets of South Shore Hospital, Inc. (the “Hospital”) (a subsidiary of South Shore Health and Educational Corporation), as of September 30, 2011 and 2010, and the related statements of operations and changes in net assets and cash flows for the years then ended. These financial statements are the responsibility of the Hospital’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Hospital’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements present fairly, in all material respects, the financial position of the Hospital as of September 30, 2011 and 2010, and the results of its operations and changes in net assets and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

December 21, 2011

- 2 -

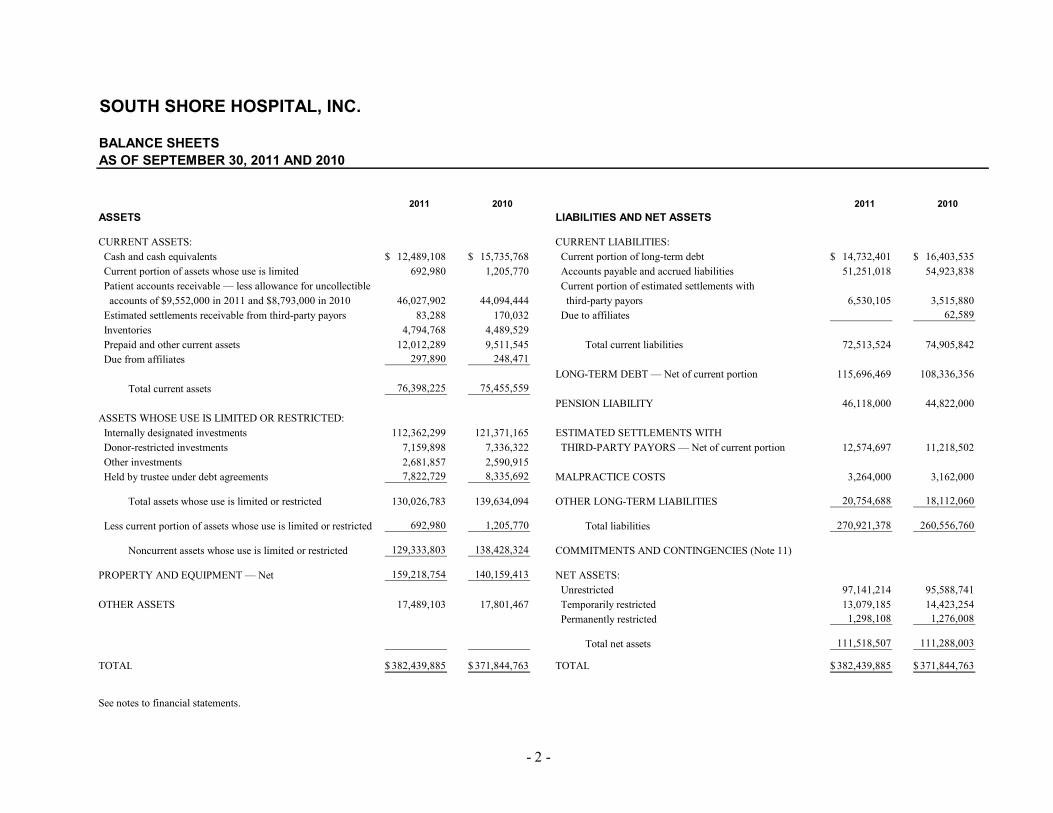

SOUTH SHORE HOSPITAL, INC.

BALANCE SHEETSAS OF SEPTEMBER 30, 2011 AND 2010

2011 2010 2011 2010ASSETS LIABILITIES AND NET ASSETS

CURRENT ASSETS: CURRENT LIABILITIES: Cash and cash equivalents 12,489,108$ 15,735,768$ Current portion of long-term debt 14,732,401$ 16,403,535$ Current portion of assets whose use is limited 692,980 1,205,770 Accounts payable and accrued liabilities 51,251,018 54,923,838 Patient accounts receivable — less allowance for uncollectible Current portion of estimated settlements with accounts of $9,552,000 in 2011 and $8,793,000 in 2010 46,027,902 44,094,444 third-party payors 6,530,105 3,515,880 Estimated settlements receivable from third-party payors 83,288 170,032 Due to affiliates 62,589 Inventories 4,794,768 4,489,529 Prepaid and other current assets 12,012,289 9,511,545 Total current liabilities 72,513,524 74,905,842 Due from affiliates 297,890 248,471

LONG-TERM DEBT — Net of current portion 115,696,469 108,336,356 Total current assets 76,398,225 75,455,559

PENSION LIABILITY 46,118,000 44,822,000 ASSETS WHOSE USE IS LIMITED OR RESTRICTED: Internally designated investments 112,362,299 121,371,165 ESTIMATED SETTLEMENTS WITH Donor-restricted investments 7,159,898 7,336,322 THIRD-PARTY PAYORS — Net of current portion 12,574,697 11,218,502 Other investments 2,681,857 2,590,915 Held by trustee under debt agreements 7,822,729 8,335,692 MALPRACTICE COSTS 3,264,000 3,162,000

Total assets whose use is limited or restricted 130,026,783 139,634,094 OTHER LONG-TERM LIABILITIES 20,754,688 18,112,060

Less current portion of assets whose use is limited or restricted 692,980 1,205,770 Total liabilities 270,921,378 260,556,760

Noncurrent assets whose use is limited or restricted 129,333,803 138,428,324 COMMITMENTS AND CONTINGENCIES (Note 11)

PROPERTY AND EQUIPMENT — Net 159,218,754 140,159,413 NET ASSETS: Unrestricted 97,141,214 95,588,741

OTHER ASSETS 17,489,103 17,801,467 Temporarily restricted 13,079,185 14,423,254 Permanently restricted 1,298,108 1,276,008

Total net assets 111,518,507 111,288,003

TOTAL 382,439,885$ 371,844,763$ TOTAL 382,439,885$ 371,844,763$

See notes to financial statements.

- 3 -

SOUTH SHORE HOSPITAL, INC.

STATEMENTS OF OPERATIONS AND CHANGES IN NET ASSETSFOR THE YEARS ENDED SEPTEMBER 30, 2011 AND 2010

2011 2010

UNRESTRICTED REVENUE, GAINS, AND OTHER SUPPORT: Net patient service revenue 417,327,525$ 404,721,625$ Other revenue 17,036,254 14,107,510 Net assets released from restrictions used for operations 1,619,061 1,976,656

Total unrestricted revenue, gains, and other support 435,982,840 420,805,791

EXPENSES: Salaries, wages, and employee benefits 257,549,066 243,594,850 Physician services 25,928,645 24,563,794 Supplies and other 106,709,297 107,117,860 Uncompensated care 11,906,762 12,636,759 Depreciation and amortization 18,400,901 17,279,101 Interest 6,055,232 6,009,821

Total expenses 426,549,903 411,202,185

OPERATING INCOME 9,432,937 9,603,606

NONOPERATING GAINS AND LOSSES: Investment income 1,649,823 1,883,453 Gain on sales of investments — net 3,026,867 4,633,049 Impairment of investments (700,153) (414,030) Loss on interest rate swap agreement (1,978,256) (4,422,696) Unrestricted gifts and bequests 304,704 397,426 Fundraising costs (2,674,321) (2,056,662)

Nonoperating (losses) gains — net (371,336) 20,540

EXCESS OF REVENUE OVER EXPENSES 9,061,601 9,624,146

(Continued)

- 4 -

SOUTH SHORE HOSPITAL, INC.

STATEMENTS OF OPERATIONS AND CHANGES IN NET ASSETSFOR THE YEARS ENDED SEPTEMBER 30, 2011 AND 2010

2011 2010

UNRESTRICTED NET ASSETS: Excess of revenue over expenses 9,061,601$ 9,624,146$ Change in net unrealized (losses) gains on investments (3,890,645) 3,467,240 Pension-related adjustments (8,718,996) 2,531,136 Gain on interest rate swap agreement 67,341 67,341 Consolidation of Friends of South Shore Hospital 12,774 Net assets released from restrictions used for purchase of property and equipment 5,033,172 1,644,184

Increase in unrestricted net assets 1,552,473 17,346,821

TEMPORARILY RESTRICTED NET ASSETS: Contributions 5,299,083 5,169,885 Investment income 31,713 30,286 Consolidation of Friends of South Shore Hospital 169,125 Change in net unrealized (losses) gains on investments (22,632) 88,065 Net assets released from restrictions (6,652,233) (3,620,840)

(Decrease) increase in temporarily restricted net assets (1,344,069) 1,836,521

PERMANENTLY RESTRICTED NET ASSETS — Contributions 22,100 12,600

INCREASE IN NET ASSETS 230,504 19,195,942

NET ASSETS — Beginning of year 111,288,003 92,092,061

NET ASSETS — End of year 111,518,507$ 111,288,003$

See notes to financial statements. (Concluded)

- 5 -

SOUTH SHORE HOSPITAL, INC.

STATEMENTS OF CASH FLOWSFOR THE YEARS ENDED SEPTEMBER 30, 2011 AND 2010

2011 2010

CASH FLOWS FROM OPERATING ACTIVITIES: Increase in net assets 230,501$ 19,195,942$ Adjustments to reconcile increase in net assets to net cash provided by operating activities: Depreciation and amortization 18,400,900 17,132,406 Unrealized and realized gains (losses) on investments, other than trading 944,536 (8,270,825) Impairment of investments 700,153 414,030 Loss on interest rate swap agreement 1,917,899 4,355,356 Provision for bad debts 8,777,960 9,498,529 Pension-related adjustments 8,718,996 (2,531,136) Amortization of original issue discounts and deferred financing costs 164,049 170,362 Restricted contributions and restricted investment income received (5,330,263) (3,898,375) (Decrease) increase in cash resulting from a change in: Patient accounts receivable — net (10,527,841) (12,952,888) Inventories (305,239) (195,826) Prepaid expenses and other current assets (2,684,321) (4,058,619) Trading securities (90,942) (366,648) Other assets 188,321 (2,411,061) Accounts payable and accrued liabilities (8,152,580) 7,534,244 Due to affiliates (112,008) 15,595 Pension liability (7,422,996) (8,046,864) Estimated settlements with third-party payors — net 4,457,164 2,539,414 Other long-term liabilities 588,908 579,512

Net cash provided by operating activities 10,463,197 18,703,148

CASH FLOWS FROM INVESTING ACTIVITIES: Purchase of property and equipment (21,935,025) (25,183,311) Purchase of investments (10,845,956) (36,329,159) Proceeds from sale of investments 18,899,520 35,456,636

Net cash used in investing activities (13,881,461) (26,055,834)

(Continued)

- 6 -

SOUTH SHORE HOSPITAL, INC.

STATEMENTS OF CASH FLOWSFOR THE YEARS ENDED SEPTEMBER 30, 2011 AND 2010

2011 2010

CASH FLOWS FROM FINANCING ACTIVITIES: Proceeds from restricted contributions and restricted investment income 5,330,263$ 3,898,375$ Increase in deferred bond issue costs (25,750) Payments on long-term debt (5,132,909) (4,834,354)

Net cash provided by (used in) financing activities 171,604 (935,979)

DECREASE IN CASH AND CASH EQUIVALENTS (3,246,660) (8,288,666)

CASH AND CASH EQUIVALENTS — Beginning of year 15,735,768 24,024,434

CASH AND CASH EQUIVALENTS — End of year 12,489,108$ 15,735,768$

SUPPLEMENTAL DISCLOSURES OF CASH FLOW INFORMATION: Cash paid for interest 5,598,203$ 5,737,186$ Equipment acquired through capital leases 10,800,648$ 196,980$

See notes to financial statements. (Concluded)

- 7 -

SOUTH SHORE HOSPITAL, INC.

NOTES TO FINANCIAL STATEMENTS AS OF AND FOR THE YEARS ENDED SEPTEMBER 30, 2011 AND 2010

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

General — South Shore Hospital, Inc. (the “Hospital”), is a subsidiary of South Shore Health and Educational Corporation (the “Corporation”), both of which are not-for-profit corporations. The Corporation is the sole member of the Hospital. The Hospital is an acute care hospital that provides inpatient, outpatient, home care, and emergency care services.

Basis of Presentation — The accompanying financial statements have been presented in conformity with accounting principles generally accepted in the United States of America (GAAP) consistent with the Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) 954, Health Care Entities, and other pronouncements applicable to health care organizations.

Use of Estimates — The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (GAAP) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements. Estimates also affect the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates. The primary estimates relate to collectibility of patient receivables, the valuation of investments in common collective trusts, estimated settlements with third-party payors, postretirement benefits, and self- insurance program reserves.

Revenue Recognition — Net patient service revenue is reported at the estimated net realizable amounts from patients, third-party payors, and others for services rendered. Under the terms of various agreements, regulations, and statutes, certain elements of third-party reimbursement are subject to negotiation, audit, and/or final determination by the third-party payors. As a result, there is at least a reasonable possibility that recorded estimates will change by a material amount in the near term. Variances between preliminary estimates of net patient service revenue and final third-party settlements are included in the statements of operations and changes in net assets in the year in which the settlement or change in estimate occurs. A portion of the estimated settlements with third-party payors has been classified as noncurrent because such amounts, by their nature or by virtue of regulation or legislation, will not be assessed within one year.

Third-Party Payment Agreements — The Hospital has entered into payment agreements with Medicare, BlueCross BlueShield of Massachusetts (“Blue Cross”), Medicaid, and various commercial insurance carriers, health maintenance organizations (HMOs), and preferred provider organizations. The basis for payment under these agreements varies and includes prospectively determined rates per discharge and per visit, discounts from established charges, cost (subject to limits), fee screens, and prospectively determined daily rates.

Uncompensated Care — Uncompensated care in the statements of operations and changes in net assets includes the provision for bad debts and the Hospital’s payments to the statewide Health Safety Net Fund (HSN) (see Note 2), net of recoveries from HSN for reimbursable bad debts.

- 8 -

Costs of Borrowing — Deferred financing costs and original issue discounts are amortized over the period that the related obligation is outstanding. Amortization of such costs during the period of construction of capital assets is capitalized as a component of the cost of acquiring such assets.

Statements of Operations and Changes in Net Assets — For purposes of display, transactions deemed by management to be ongoing, major, or central to the provision of health care services are reported as revenue and expenses. Peripheral or incidental transactions are reported as nonoperating gains and losses.

Excess of Revenue over Expenses — The statements of operations and changes in net assets include excess of revenue over expenses. Changes in unrestricted net assets, which are excluded from excess of revenue over expenses, consistent with industry practice, include permanent transfers of assets to and from affiliates for other than goods and services, changes in unrealized appreciation (depreciation) on investments (other than those classified as trading securities and those on which other-than-temporary losses are recognized), contributions of long-lived assets (including assets acquired using contributions which, by donor restriction, were to be used for the purposes of acquiring such assets), and pension-related adjustments.

Functional Expenses — Substantially all expenses reported in the accompanying statements of operations and changes in net assets are related to the delivery of health care services.

Temporarily and Permanently Restricted Net Assets — Temporarily restricted net assets are those whose use by the Hospital has been limited by donors to a specific time period or purpose. Permanently restricted net assets have been restricted by donors to be maintained by the Hospital in perpetuity.

The Hospital has interpreted state law as requiring realized and unrealized gains of permanently restricted net assets to be retained in a temporarily restricted net asset classification until appropriated by the Board of Directors (the “Board”) and expended. State law allows the Board to appropriate as much of the net appreciation of permanently restricted net assets as is prudent, considering the Hospital’s long- and short-term needs, present and anticipated financial requirements, expected total return on its investments, price-level trends, and general economic conditions. For the years ended September 30, 2011 and 2010, the Board did not appropriate any funds due to market conditions.

Gifts and Bequests — Unconditional promises to give cash and other assets to the Hospital are reported at fair value at the date the promise is received. Conditional promises to give and indications of intentions to give are reported at fair value at the date the gift is received. Gifts are reported as either temporarily or permanently restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is, when a stipulated time restriction ends or a purpose restriction is accomplished, temporarily restricted net assets are reclassified as unrestricted net assets and reported in the statements of operations and changes in net assets as net assets released from restrictions.

Unconditional promises to give that are expected to be collected within one year are recorded at net realizable value. Unconditional promises to give that are expected to be collected in future years are recorded at the present value of their estimated future cash flows. The discount on those amounts is computed using risk-free interest rates applicable to the years in which the promises to give are to be received. Amortization of the discount is included in contribution revenue. Conditional promises to give are not included as support until the conditions are substantially met.

- 9 -

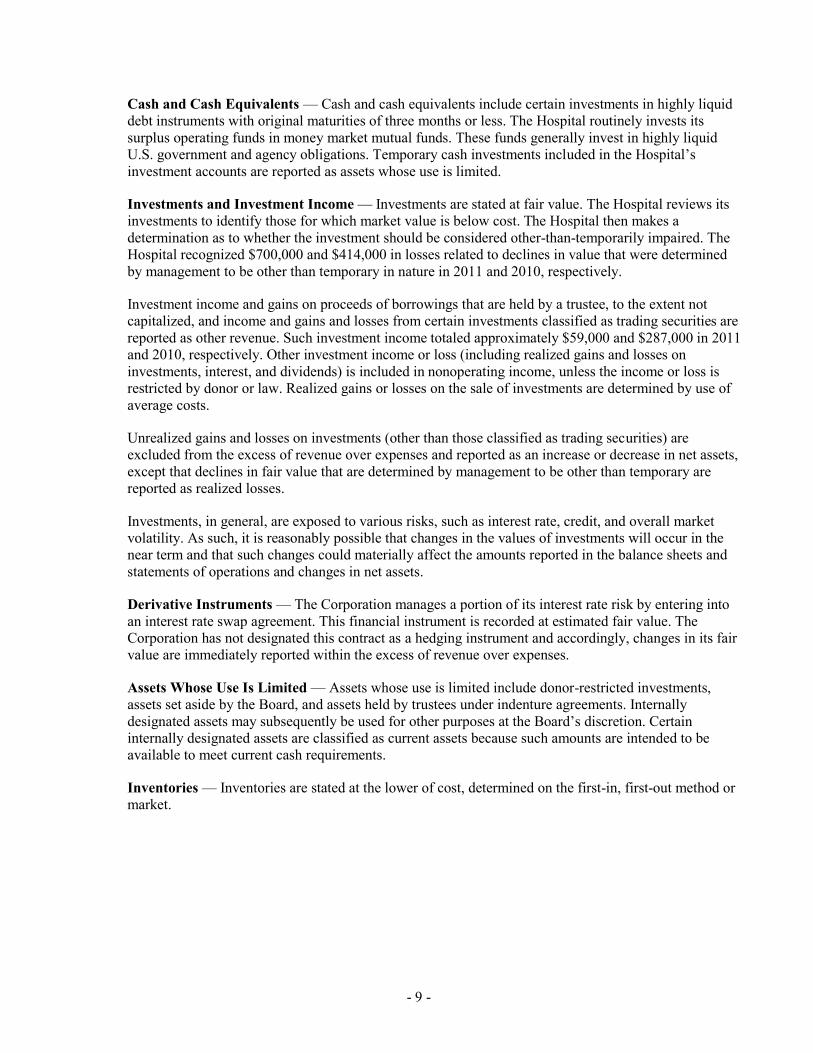

Cash and Cash Equivalents — Cash and cash equivalents include certain investments in highly liquid debt instruments with original maturities of three months or less. The Hospital routinely invests its surplus operating funds in money market mutual funds. These funds generally invest in highly liquid U.S. government and agency obligations. Temporary cash investments included in the Hospital’s investment accounts are reported as assets whose use is limited.

Investments and Investment Income — Investments are stated at fair value. The Hospital reviews its investments to identify those for which market value is below cost. The Hospital then makes a determination as to whether the investment should be considered other-than-temporarily impaired. The Hospital recognized $700,000 and $414,000 in losses related to declines in value that were determined by management to be other than temporary in nature in 2011 and 2010, respectively.

Investment income and gains on proceeds of borrowings that are held by a trustee, to the extent not capitalized, and income and gains and losses from certain investments classified as trading securities are reported as other revenue. Such investment income totaled approximately $59,000 and $287,000 in 2011 and 2010, respectively. Other investment income or loss (including realized gains and losses on investments, interest, and dividends) is included in nonoperating income, unless the income or loss is restricted by donor or law. Realized gains or losses on the sale of investments are determined by use of average costs.

Unrealized gains and losses on investments (other than those classified as trading securities) are excluded from the excess of revenue over expenses and reported as an increase or decrease in net assets, except that declines in fair value that are determined by management to be other than temporary are reported as realized losses.

Investments, in general, are exposed to various risks, such as interest rate, credit, and overall market volatility. As such, it is reasonably possible that changes in the values of investments will occur in the near term and that such changes could materially affect the amounts reported in the balance sheets and statements of operations and changes in net assets.

Derivative Instruments — The Corporation manages a portion of its interest rate risk by entering into an interest rate swap agreement. This financial instrument is recorded at estimated fair value. The Corporation has not designated this contract as a hedging instrument and accordingly, changes in its fair value are immediately reported within the excess of revenue over expenses.

Assets Whose Use Is Limited — Assets whose use is limited include donor-restricted investments, assets set aside by the Board, and assets held by trustees under indenture agreements. Internally designated assets may subsequently be used for other purposes at the Board’s discretion. Certain internally designated assets are classified as current assets because such amounts are intended to be available to meet current cash requirements.

Inventories — Inventories are stated at the lower of cost, determined on the first-in, first-out method or market.

- 10 -

Other Assets — Other assets as of September 30, 2011 and 2010, consist of the following:

2011 2010

Insurance policies 8,912,107$ 7,978,342$ Pledges receivable, net of current portion 4,264,606 5,452,927 Unamortized bond issue costs 2,504,918 2,621,974 Investments in joint venture 1,608,846 1,569,614 Swap termination 144,926 151,910 Security deposits 53,700 26,700

Total other assets 17,489,103$ 17,801,467$

Insurance Policies — The Hospital accounts for its interest in life insurance policies at the lower of the policies cash value or the discounted value of expected cash flows.

Property and Equipment — Property and equipment are stated at cost, less accumulated depreciation. Gifts of long-lived assets, such as land, buildings, or equipment, are reported as unrestricted support and excluded from the excess of revenue over expenses, unless explicit donor stipulations specify how the donated assets must be used. Gifts of long-lived assets with explicit restrictions that specify how the assets are to be used and gifts of cash or other assets that must be used to acquire long-lived assets are reported as restricted support. Absent explicit donor stipulations about how long those assets must be maintained and expirations of donor restrictions are reported when the donated or acquired long-lived assets are placed in service. Liabilities for the purchase of property and equipment aggregating approximately $1,967,000 and $917,000 remained in accounts payable and accrued liabilities as of September 30, 2011 and 2010, respectively.

Depreciation is computed using the straight-line method over the estimated useful lives of depreciable assets. Equipment under capitalized leases is amortized using the straight-line method over the shorter period of the lease term or the estimated useful life of the equipment. Such amortization is included with depreciation expense.

Other Liabilities — Other liabilities as of September 30, 2011 and 2010, consist of the following:

2011 2010

Workers’ compensation liability 3,018,169$ 2,474,992$ Asset retirement obligation liability 251,129 238,036 Executive and physician benefits payable 2,794,967 2,612,541 Interest rate swap contract 14,690,423 12,786,491

20,754,688$ 18,112,060$

Capitalized Interest — Interest costs incurred on borrowed funds during the period of construction of capital assets, net of investment income earned on borrowed funds held by trustees, are capitalized as a component of the cost of acquiring capital assets. In 2011, $234,000 was capitalized and $80,000 was capitalized in 2010.

Impairment of Long-Lived Assets — Long-lived assets to be held and used are reviewed for impairment whenever circumstances indicate that the carrying amount of an asset may not be recoverable. Long-lived assets to be disposed of are reported at the lower of carrying amount or fair value, less cost to sell.

- 11 -

Estimated Malpractice and Workers’ Compensation Liabilities — The liabilities for estimated medical malpractice and workers’ compensation claims include an estimate of the ultimate cost for claims incurred but not reported.

Income Tax Status — The Hospital has previously been determined by the Internal Revenue Service to be an organization described in Internal Revenue Code (IRC) Section 501(c)(3) and, therefore, exempt from federal income taxes on related income under IRC Section 501(a). Accordingly, no provision for income taxes has been made in the accompanying financial statements.

The Hospital follows the provisions of FASB Accounting Standards Codification (ASC) No. 740, Income Taxes, relating to accounting for uncertainty in income taxes. ASC 740 clarifies the accounting for uncertainty in income taxes recognized in an entity’s financial statements. It prescribes an uncertainty threshold and measurement attributes for financial statement disclosure of tax positions taken or expected to be taken on a tax return.

Accounting for Postretirement Benefit Plans — The Hospital recognizes the overfunded or underfunded status of its defined benefit plan as an asset or liability in its balance sheets. Changes in the funded status of the plan are reported as a change in unrestricted net assets presented below the excess of revenues over expenses in the statements of operations and changes in net assets in the year in which the changes occur.

Recently Issued Accounting Pronouncements — In July 2011, the FASB issued Accounting Standards Update (ASU) 2011-07, Health Care Entities (Topic 954), Presentation and Disclosure of Patient Service Revenue, Provision for Bad Debts, and the Allowance for Doubtful Accounts for Certain Health Care Entities. The adoption of ASU 2011-07 will require the Hospital to change the presentation of its statements of operations by reclassifying the provision for bad debts associated with patient service revenue from an operating expense to a deduction from patient service revenue (net of contractual allowances and discounts). Additionally, the ASU will require the Hospital to provide enhanced disclosures about its sources of patient service revenue, policies for recognizing revenue and assessing bad debts, as well as qualitative and quantitative information about changes in the allowance for doubtful accounts. The provisions of ASU 2011-07 are effective for the Hospital beginning October 1, 2012. The adoption of ASU 2011-07 is not expected to have any impact on the Hospital’s financial condition, overall results of operations, or cash flows.

In August 2010, the FASB issued Accounting Standards Update (ASU) No. 2010-24, Health Care Entities (Topic 954), Presentation of Insurance Claims and Related Insurance Recoveries, which clarifies that a health care entity should not net insurance recoveries against a related claim liability. Additionally, the amount of the claim liability should be determined without consideration of insurance recoveries. The adoption of ASU 2010-24 is effective for the Hospital beginning October 1, 2011. Management has not yet determined the effect that the adoption of ASU 2010-24 will have on the Hospital’s financial statements.

In August 2010, the FASB issued ASU 2010-23, Health Care Entities (Topic 954), Measuring Charity Care for Disclosure, which requires that cost be used as a measurement for charity care disclosure purposes and that cost be identified as the direct and indirect costs of providing the charity care. It also requires disclosure of the method used to identify or determine such costs. The provisions of ASU 2010-23 were effective for the Hospital beginning October 1, 2011. The adoption of ASU 2010-23 did not have a material impact on the Hospital’s financial statements.

Subsequent Events — Subsequent events have been evaluated through December 21, 2011, the date of issuance of these financial statements.

- 12 -

2. CHARITY CARE

The Hospital provides care without charge or at amounts less than its established rates to patients who meet certain criteria under its charity care policy. Because the Hospital does not pursue collection of amounts determined to qualify as charity care, they are not reported as revenue, except to the extent reimbursed by HSN. The Hospital also supports the delivery of health care services to the indigent through payments to HSN, which is operated by the Commonwealth of Massachusetts. The estimated cost of unreimbursed charity care provided by the Hospital and net payments to HSN for charity care provided by other institutions aggregated approximately $6,519,000 and $5,851,000 in 2011 and 2010, respectively.

3. TRANSACTIONS WITH THE CORPORATION AND ITS SUBSIDIARIES

The Hospital rented space to related entities in both 2011 and 2010. In addition, the Hospital purchased supplies for and provided services to related entities in both 2011 and 2010. The amounts related to these transactions totaled $5,900,000 in 2011 and $5,000,000 in 2010.

The Hospital entered into a 20-year lease with South Shore Property, Inc. (SSP), a controlled affiliate of the Corporation, for space in the Ambulatory Cancer Center (ACC). The lease, which has an annual base rental of approximately $1,500,000, took effect October 5, 2009, the date the building opened.

The Hospital entered into a 20-year ground lease with SSP to lease the property on which the ACC is located to SSP. The lease, which has an annual base rental of approximately $231,000, took effect October 5, 2009, the date the ACC opened.

4. CONTRIBUTIONS RECEIVABLE

Contributions receivable as of September 30, 2011 and 2010, consisted of the following:

2011 2010

Amounts due in: Less than one year 3,473,870$ 3,231,733$ Over one year 5,249,809 6,341,833

Unconditional promises to give before unamortized discount and allowance for uncollectibles 8,723,679 9,573,566

Less unamortized discount (202,349) (266,305)

Subtotal 8,521,330 9,307,261

Less allowance for uncollectible amounts (1,303,936) (944,320)

Net 7,217,394$ 8,362,941$

Contributions receivable are reported in the balance sheets in other current assets and other assets and do not include conditional promises to give.

- 13 -

5. ASSETS WHOSE USE IS LIMITED

Assets whose use is limited as of September 30, 2011 and 2010, consisted of the following:

2011 2010

Cash and money market investments 17,003,346$ 16,075,683$ Equities 290,358 Mutual fund investments 47,939,487 52,405,142 Common collective trusts 64,793,592 71,153,268

Total assets whose use is limited 130,026,783$ 139,634,093$ Investment income and gains (losses) from investments for the years ended September 30, 2011 and 2010, consisted of the following:

2011 2010

Investment income: Other revenue 58,893$ 287,318$ Nonoperating gains and losses 1,649,823 1,883,453 Temporarily restricted net assets 31,713 30,286 Gain on sales of investments — net 3,026,867 4,633,049 Impairment of investments (700,153) (414,030) Change in net unrealized losses and gains on investments: Unrestricted net assets (3,890,645) 3,467,240 Temporarily restricted net assets (22,632) 88,065

153,866$ 9,975,381$

6. PROPERTY AND EQUIPMENT

Property and equipment as of September 30, 2011 and 2010, consisted of the following:

2011 2010

Land 5,013,567$ 5,013,567$ Land improvements 2,581,807 2,776,357 Buildings 163,889,327 162,175,827 Fixed equipment 55,866,652 57,711,676 Major movable equipment 98,820,137 103,395,665 Buildings and equipment under capitalized leases 18,943,643 8,241,997 Construction in progress 12,022,481 3,532,648 Leasehold improvements 11,822,210 2,219,415

Total 368,959,824 345,067,152

Less accumulated depreciation (including $7,446,000 and $6,735,000 of accumulated amortization of equipment under capital leases in 2011 and 2010, respectively) (209,741,070) (204,907,739)

Property and equipment — net 159,218,754$ 140,159,413$

- 14 -

In May 2010, the Hospital entered into a 20-year lease with Perry South Shore Development LLC for 66% of a building in Hingham, Massachusetts. The building opened for business in early October 2011. The Hospital’s obligation to make monthly lease payments of approximately $110,000 commenced in August, 2011. The building is operating as an outpatient surgery unit, performing diagnostic imaging services, and subleasing a portion of the space to physicians.

The Hospital entered into a $34,010,000 construction contract to expand the number of beds on its main campus; the Hospital expects to finance a portion of the construction cost. At September 30, 2011, $4,057,000 related to this project was included in property, plant and equipment, of which $918,000 was in accrued liabilities.

7. LONG-TERM DEBT

Long-term debt as of September 30, 2011 and 2010, consisted of the following:

2011 2010

South Shore Hospital Issue, Series G 88,535,000$ 90,850,000$ South Shore Hospital Issue, Series F 20,000,000 20,020,000 South Shore Hospital Issue, Series D 10,710,000 12,815,000 Capital lease obligations 11,286,397 1,178,658

Total 130,531,397 124,863,658

Less original issue discount (net of $1,614,875 and $1,593,635 of accumulated amortization in 2011 and 2010, respectively) (102,527) (123,767)

Total 130,428,870 124,739,891

Less current portion 14,732,401 16,403,535

Long-term debt 115,696,469$ 108,336,356$

The Hospital is obligated under various revenue bonds issued by the Massachusetts Health and Educational Facilities Authority (HEFA). The terms of the related loan and trust agreements place limits on the incurrence of additional borrowings and contain various covenants and financial ratio requirements. Additionally, the Hospital has granted a lien on its revenue and gross receipts from all sources (other than gifts, grants, or bequests which, by their terms, may not be legally available for debt service) as collateral for the borrowings. The Hospital is also required to maintain certain funds, which are held by trustees. Such funds are included with assets whose use is limited. The revenue bonds require periodic interest payments and principal payments to these funds held in trust, which are proportionate to the annual interest and principal payments or sinking fund installments.

On February 28, 2008, the Hospital issued through HEFA $94,585,000 of tax-exempt variable rate revenue bonds (“Series G”), the proceeds of which were used to refund its Series E bonds in the amount of $10,905,000; refund $34,170,000 of Series F bonds; fund new capital expenditures, including the construction of a new parking garage; and pay issuance costs. The interest rate on the Series G bonds is set weekly. Series G bondholders have the option to put the bonds back to the Hospital. Such bonds would be subject to remarketing efforts by the Hospital’s remarketing agent. To the extent that such remarketing efforts were unsuccessful, the nonmarketable bonds would be purchased from the proceeds

- 15 -

of a standby bond purchase agreement with an investment banking firm that expires on February 28, 2013. The term of the repayment for such nonmarketable bonds is five years from the date of the standby bond purchase agreement disbursement or the expiration date. The Series G bonds have been classified in accordance with the repayment provisions contained in the standby bond purchase agreement in the accompanying balance sheets and in accordance with the scheduled maturities contained in the bond agreement in the table of annual principal payments of long-term debt.

The Hospital’s revenue bonds bear interest and mature as follows:

FinalIssue Interest Rate Maturity

Series G Variable 2032Series F 5.125%–5.75% 2029Series E 5.50% 2020Series D 6.50% 2022

The variable interest rate on Series G on September 30, 2011, was 0.24% (0.30% on September 30, 2010) and the average variable interest rate for the year ended September 30, 2011, was 0.29% (0.29% for the year ended September 30, 2010).

Funds held by trustees under debt agreements as of September 30, 2011 and 2010, were composed of the following:

2011 2010

Debt service funds 692,980$ 1,205,770$ Debt service reserve funds 7,129,949 7,129,922

7,822,929$ 8,335,692$

Effective October 1, 2010, HEFA merged into the Massachusetts Development Finance Agency.

Interest Rate Swap Agreement — In October 2008, the Hospital entered into a fixed-pay London InterBank Offered Rate (LIBOR) swap agreement with an original notional amount of $94,065,000 with an investment bank to hedge possible future interest rate increases on the Series G bonds. The Hospital’s fixed interest rate on the fixed-pay LIBOR swap was 3.325%. The Hospital in return received 67% of LIBOR (.239% and 0.256% as of September 30, 2011 and 2010, respectively) from the investment bank. The Hospital has elected not to apply hedge accounting to the swap. The loss on the swap of approximately $1,978,000 and $4,423,000 for the years ended September 30, 2011 and 2010, respectively, is included in nonoperating gains (losses) in the accompanying statement of operations and changes in net assets. The fair value of the interest rate swap agreement of approximately $14,690,000 and $12,786,000 as of September 30, 2011 and 2010, respectively, is included in other long-term liabilities in the accompanying balance sheets.

The Hospital and the counterparty in the interest rate swap agreements are exposed to credit risk in the event of nonperformance or early termination of the agreements. Depending upon the market price and the counterparty’s credit rating at the calculation date, the counterparty is required to either collateralize or insure any aggregate exposure in excess of $100,000.

- 16 -

Line of Credit — The Hospital has a committed revolving line-of-credit agreement with a bank under which the Hospital is permitted to borrow up to $20,000,000 through March 31, 2012. Borrowings under the agreement bear interest at one of various rates, which are determined at the time of the borrowing, based upon the Hospital’s election, and are unsecured. The Hospital did not borrow and had no outstanding amounts under the line of credit during 2011 or 2010.

Payments on Debt — Annual principal payments on long-term debt and total payments on capital lease obligations as of September 30, 2011, were as follows:

CapitalYears Ending Long-Term LeaseSeptember 30 Debt Obligations

2012 4,670,000$ 1,831,918$ 2013 4,850,000 1,537,104 2014 5,040,000 1,383,768 2015 5,245,000 1,356,171 2016 5,520,000 1,356,171 Thereafter 93,920,000 20,161,748

Total 119,245,000$ 27,626,880

Less amounts representing interest 16,340,483

Total 11,286,397$

If all of the Series G bonds were put back to the Hospital and not remarketed, the required repayments of long-term debt, after giving effect to the terms of the related standby bond purchase agreement, would be: 2012, $14,130,250; 2013, $18,602,000; 2014, $18,652,000; 2015, $20,412,000; 2016, $20,592,000; and thereafter, $26,856,750.

8. OPERATING LEASES

The Hospital leases certain of its facilities and equipment under noncancelable operating leases expiring through 2029. The leases generally provide for renewal options and require that the Hospital pay its share of operating expenses. Future minimum annual lease payments under noncancelable operating leases, excluding leases with related parties, as of September 30, 2011, were as follows:

Years EndingSeptember 30

2012 2,845,567$ 2013 2,039,863 2014 1,928,195 2015 1,794,172 2016 1,539,415 Thereafter 8,976,027

Total 19,123,239$

- 17 -

Rent expense, excluding rent paid to related parties (see Note 3), for the years ended September 30, 2011 and 2010, was approximately $5,919,000 and $6,818,000, respectively, and is recorded in supplies and other in the accompanying statements of operations and changes in net assets. Future minimum annual sublease receipts under noncancelable subleases will be: 2012, $215,000; 2013, $97,000; 2014, $97,000; 2015, $97,000; 2016, $97,000; and thereafter, $496,000.

9. TEMPORARILY AND PERMANENTLY RESTRICTED NET ASSETS

Temporarily restricted net assets were available as of September 30, 2011 and 2010, for the following purposes or periods:

2011 2010

Health care services: Purchase of equipment 4,106,900$ 2,594,827$ Indigent care 110,844 117,866 Other health care services 1,644,047 3,347,620 For periods after September 30 (generally for capital) 7,217,394 8,362,941

Total 13,079,185$ 14,423,254$

Capital appreciation of permanently restricted net assets, included above, amounted to approximately $194,000 and $217,000 as of September 30, 2011 and 2010, respectively.

Permanently restricted net assets as of September 30, 2011 and 2010, were restricted to:

2011 2010

Investments to be held in perpetuity, the income from which is expendable for the following purposes: Purchase of equipment 100,000$ 100,000$ Indigent care 635,884 628,784 Other health care services (restricted) 140,977 125,977 Other health care services (unrestricted) 421,247 421,247

Total 1,298,108$ 1,276,008$

Net assets were released from donor restrictions by incurring expenses and purchasing equipment, satisfying the restricted purposes for the years ended September 30, 2011 and 2010, as follows:

2011 2010

Health care services: Purchase of equipment 5,033,172$ 1,644,184$ Other health care services 1,619,061 1,976,656

Total 6,652,233$ 3,620,840$

- 18 -

10. EMPLOYEE BENEFIT PLANS

The Hospital has a defined benefit pension plan (the “Plan”) covering substantially all employees not covered under the Home and Community Services Division Plan (“Home Division Plan”) discussed below. The Plan’s benefit formula is based on a participant’s service and highest five-year final-average level of compensation. The Hospital’s funding policy is to make contributions to the Plan at least equal to the minimum required under the law.

On December 21, 2005, the Board voted to freeze participation and future service credits under the Plan, effective January 1, 2007. The Board also voted on December 21, 2005, to freeze participation in the Home Division Plan, effective January 1, 2007. Benefits under the frozen plans have been supplemented by a defined contribution plan consisting of Hospital funded core and matching contribution features through a 403(b) plan. Pension expense related to the new defined contribution plan was $11,019,000 and $10,373,000 for the years ended September 30, 2011 and 2010, respectively.

The Hospital uses a September 30 measurement date for measuring the assets and obligations of the Plan.

Benefit Obligations 2011 2010

Change in benefit obligation: Benefit obligation — beginning of year 145,993,000$ 141,814,000$ Service cost and assumed expenses 450,000 300,000 Interest cost 7,966,000 7,824,000 Actuarial loss 5,274,000 548,000 Benefits paid (4,129,000) (3,774,000) Actual administrative expenses paid (695,000) (719,000)

Benefit obligation — end of year 154,859,000$ 145,993,000$

The accumulated benefit obligation at the end of 2011 and 2010 was $145,328,000 and $136,240,000, respectively. A 5.29% and 5.52% discount rate was used to determine the benefit obligations as of September 30, 2011 and 2010, respectively.

Plan Assets 2011 2010

Change in Plan assets: Fair value of Plan assets — beginning of year 101,171,000$ 86,414,000$ Actual return on Plan assets 3,394,000 10,250,000 Employer contribution 9,000,000 9,000,000 Benefits and other expenses paid (4,824,000) (4,493,000)

Fair value of Plan assets — end of year 108,741,000$ 101,171,000$

- 19 -

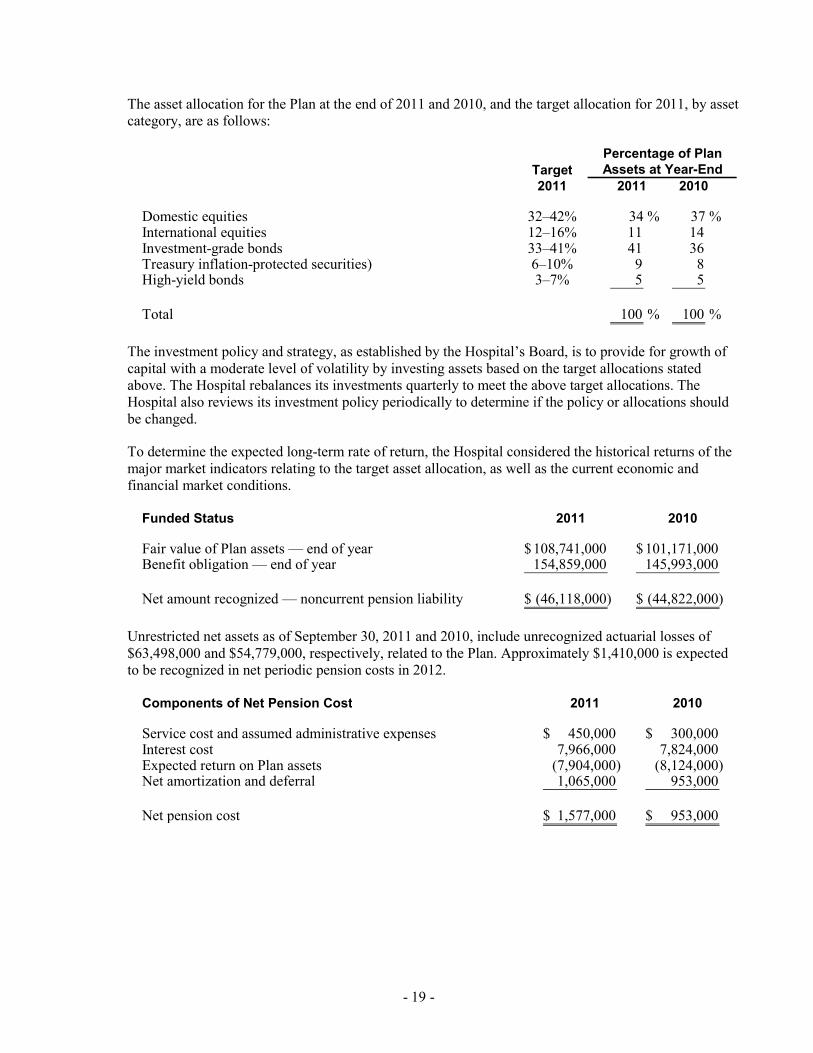

The asset allocation for the Plan at the end of 2011 and 2010, and the target allocation for 2011, by asset category, are as follows:

Target2011 2011 2010

Domestic equities 32–42% 34 % 37 %International equities 12–16% 11 14 Investment-grade bonds 33–41% 41 36 Treasury inflation-protected securities) 6–10% 9 8 High-yield bonds 3–7% 5 5

Total 100 % 100 %

Percentage of PlanAssets at Year-End

The investment policy and strategy, as established by the Hospital’s Board, is to provide for growth of capital with a moderate level of volatility by investing assets based on the target allocations stated above. The Hospital rebalances its investments quarterly to meet the above target allocations. The Hospital also reviews its investment policy periodically to determine if the policy or allocations should be changed.

To determine the expected long-term rate of return, the Hospital considered the historical returns of the major market indicators relating to the target asset allocation, as well as the current economic and financial market conditions.

Funded Status 2011 2010

Fair value of Plan assets — end of year 108,741,000$ 101,171,000$ Benefit obligation — end of year 154,859,000 145,993,000

Net amount recognized — noncurrent pension liability (46,118,000)$ (44,822,000)$

Unrestricted net assets as of September 30, 2011 and 2010, include unrecognized actuarial losses of $63,498,000 and $54,779,000, respectively, related to the Plan. Approximately $1,410,000 is expected to be recognized in net periodic pension costs in 2012.

Components of Net Pension Cost 2011 2010

Service cost and assumed administrative expenses 450,000$ 300,000$ Interest cost 7,966,000 7,824,000 Expected return on Plan assets (7,904,000) (8,124,000) Net amortization and deferral 1,065,000 953,000

Net pension cost 1,577,000$ 953,000$

- 20 -

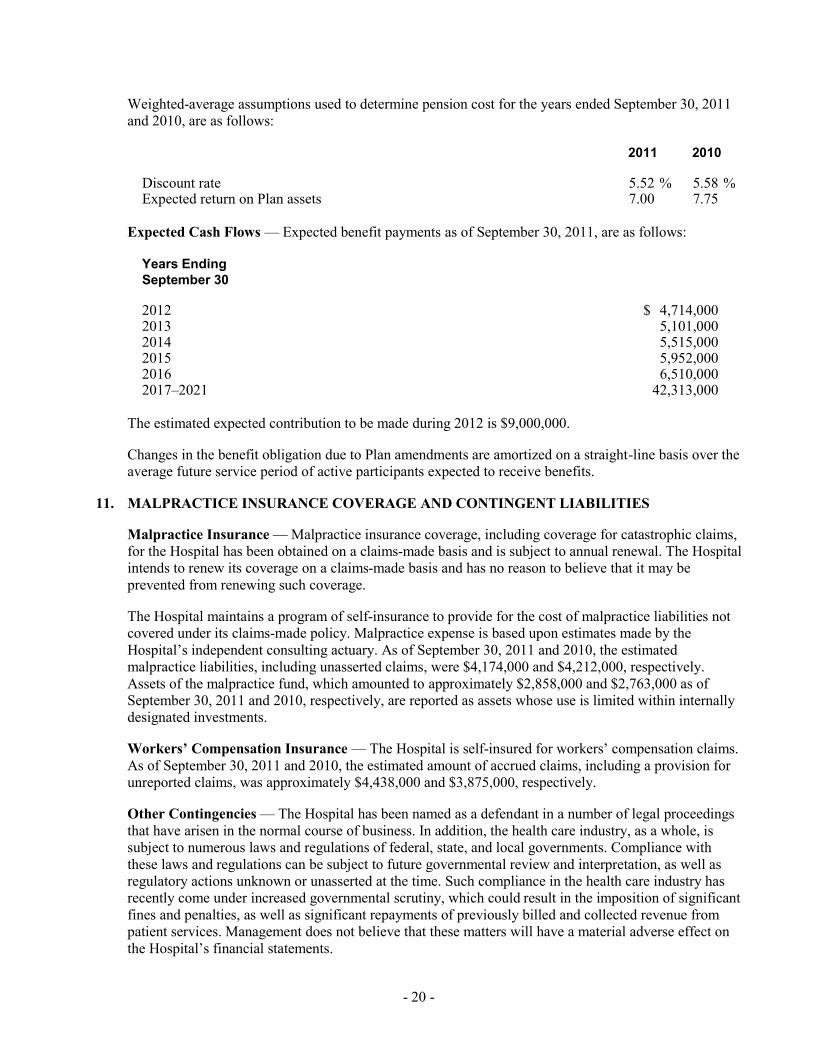

Weighted-average assumptions used to determine pension cost for the years ended September 30, 2011 and 2010, are as follows:

2011 2010

Discount rate 5.52 % 5.58 % Expected return on Plan assets 7.00 7.75

Expected Cash Flows — Expected benefit payments as of September 30, 2011, are as follows:

Years EndingSeptember 30

2012 4,714,000$ 2013 5,101,000 2014 5,515,000 2015 5,952,000 2016 6,510,000 2017–2021 42,313,000

The estimated expected contribution to be made during 2012 is $9,000,000.

Changes in the benefit obligation due to Plan amendments are amortized on a straight-line basis over the average future service period of active participants expected to receive benefits.

11. MALPRACTICE INSURANCE COVERAGE AND CONTINGENT LIABILITIES

Malpractice Insurance — Malpractice insurance coverage, including coverage for catastrophic claims, for the Hospital has been obtained on a claims-made basis and is subject to annual renewal. The Hospital intends to renew its coverage on a claims-made basis and has no reason to believe that it may be prevented from renewing such coverage.

The Hospital maintains a program of self-insurance to provide for the cost of malpractice liabilities not covered under its claims-made policy. Malpractice expense is based upon estimates made by the Hospital’s independent consulting actuary. As of September 30, 2011 and 2010, the estimated malpractice liabilities, including unasserted claims, were $4,174,000 and $4,212,000, respectively. Assets of the malpractice fund, which amounted to approximately $2,858,000 and $2,763,000 as of September 30, 2011 and 2010, respectively, are reported as assets whose use is limited within internally designated investments.

Workers’ Compensation Insurance — The Hospital is self-insured for workers’ compensation claims. As of September 30, 2011 and 2010, the estimated amount of accrued claims, including a provision for unreported claims, was approximately $4,438,000 and $3,875,000, respectively.

Other Contingencies — The Hospital has been named as a defendant in a number of legal proceedings that have arisen in the normal course of business. In addition, the health care industry, as a whole, is subject to numerous laws and regulations of federal, state, and local governments. Compliance with these laws and regulations can be subject to future governmental review and interpretation, as well as regulatory actions unknown or unasserted at the time. Such compliance in the health care industry has recently come under increased governmental scrutiny, which could result in the imposition of significant fines and penalties, as well as significant repayments of previously billed and collected revenue from patient services. Management does not believe that these matters will have a material adverse effect on the Hospital’s financial statements.

- 21 -

12. FAIR VALUE OF FINANCIAL INSTRUMENTS

Fair Value Measurements — GAAP establishes a fair value hierarchy that distinguishes between market participant assumptions based on market data obtained from sources independent of the reporting entity (observable inputs that are classified within Levels 1 and 2 of the hierarchy) and the reporting entity’s own assumption about market participant assumptions (unobservable inputs classified within Level 3 of the hierarchy).

The following table presents information as of September 30, 2011, about the Hospital’s financial assets that are measured at fair value on a recurring basis (in thousands):

QuotedPrices Other

in Active ObservableMarkets Inputs(Level 1) (Level 2) Fair Value

Cash and money market investments 17,003$ - $ - $ 17,003$ Equities 290 290 Mutual fund investments 7,317 7,317 International stock fund 16,316 16,316 Bond index fund 24,307 24,307 Common collective trusts: Equity 46,537 46,537 Fixed income 18,257 18,257

Total 65,233$ 64,794$ - $ 130,027$

UnobservableInputs

(Level 3)

The following table presents information as of September 30, 2010, about the Hospital’s financial assets that are measured at fair value on a recurring basis (in thousands):

QuotedPrices Other

in Active ObservableMarkets Inputs(Level 1) (Level 2) Fair Value

Cash and money market investments 16,076$ - $ - $ 16,076$ Mutual fund investments 8,165 8,165 International stock fund 21,180 21,180 Bond index fund 23,060 23,060 Common collective trusts: Equity 52,927 52,927 Fixed income 18,226 18,226

Total 68,481$ 71,153$ - $ 139,634$

UnobservableInputs

(Level 3)

- 22 -

The following table presents information as of September 30, 2011, about the Hospital’s pension plan assets that are measured at fair value on a recurring basis (in thousands):

QuotedPrices Other

in Active ObservableMarkets Inputs(Level 1) (Level 2) Fair Value

Cash and money market investments 561$ - $ - $ 561$ Mutual fund investments 2,766 2,766 International stock fund 6,280 6,280 Bond index fund 44,413 44,413 Common collective trusts: Equity 39,608 39,608 Fixed income 15,113 15,113

Total 54,020$ 54,721$ - $ 108,741$

UnobservableInputs

(Level 3)

The following table presents information as of September 30, 2010, about the Hospital’s pension plan assets that are measured at fair value on a recurring basis (in thousands):

QuotedPrices Other

in Active ObservableMarkets Inputs(Level 1) (Level 2) Fair Value

Cash and money market investments 494$ - $ - $ 494$ Mutual fund investments 3,317 3,317 International stock fund 14,174 14,174 Bond index fund 35,863 35,863 Common collective trusts: Equity 33,938 33,938 Fixed income 13,385 13,385

Total 53,848$ 47,323$ - $ 101,171$

UnobservableInputs

(Level 3)

The Hospital uses the following fair value hierarchy to present its fair value disclosures:

Level 1 — Quoted (unadjusted) prices for identical assets or liabilities in active markets. Active markets are those in which transactions for the asset or liability occur with sufficient frequency and volume to provide pricing information on an ongoing basis.

Level 2 — Other observable inputs, either directly or indirectly, including:

• Quoted prices for similar assets in active markets

• Quoted prices for identical or similar assets in nonactive markets (few transactions, limited information, noncurrent prices, high variability over time, etc.)

- 23 -

• Inputs other than quoted prices that are observable for the asset (interest rates, yield curves, volatilities, default rates, etc.)

• Inputs that are derived principally from or corroborated by other observable market data

Level 3 — Unobservable inputs that cannot be corroborated by observable market data.

The following is a description of the valuation methodologies used for assets and liabilities measured at fair value:

Cash and Money Market Investments — The carrying value of cash investments approximates fair value, as maturities are less than three months and/or include money market funds that are based on quoted prices and actively traded.

Mutual Fund Investments — The fair values of mutual fund investments, including index funds and international equity funds, are based on quoted market prices.

Common Collective Trusts — The estimated fair values of common collective trusts are determined based upon information provided by the fund managers. Such information is generally based on the pro rata interest in the net assets of the trusts which approximates the fair value of the underlying investments. The Hospital’s interest may be redeemed at net asset value on a daily basis with no redemption restrictions.

Pledges Receivable — The current yields for 1- to 10-year U.S. Treasury notes are used to discount contributions receivable. The Hospital considers these yields to be a Level 2 input in the context of the fair value hierarchy. Pledges received during 2011 were discounted at rates ranging from .96% to 2.33% (1.17% to 2.64% in 2010). Pledges received in 2011, which have been recorded at fair value, totaled approximately $5,197,000 ($7,436,000 in 2010).

Interest Rate Swap — The Hospital uses inputs other than quoted prices that are observable to value the interest rate swap. The Hospital considers these inputs to be Level 2 inputs in the context of the fair value hierarchy. The fair value of the interest rate swap liability was $14,690,000 and $12,786,000 as of September 30, 2011 and 2010, respectively. These values represent the estimated amounts the Hospital would receive or pay to terminate agreements, taking into consideration current interest rates and the current creditworthiness of the counterparty.

The following methods and assumptions were used by the Hospital in estimating the fair value of the Hospital’s financial instruments that are not measured at fair value on a recurring basis for disclosures in the financial statements:

Accounts Receivable, Other Current and Noncurrent Assets, Accounts Payable and Accrued Liabilities, and the Accrual for Estimated Settlements with Third-Party Payors — The carrying amounts of these items are reasonable estimates of their fair value.

Long-Term Debt — The fair value of the Hospital’s debt is estimated based upon quoted market prices for the same or similar issues. The fair value was approximately $132,556,000 and $126,140,000 as of September 30, 2011 and 2010, respectively.

- 24 -

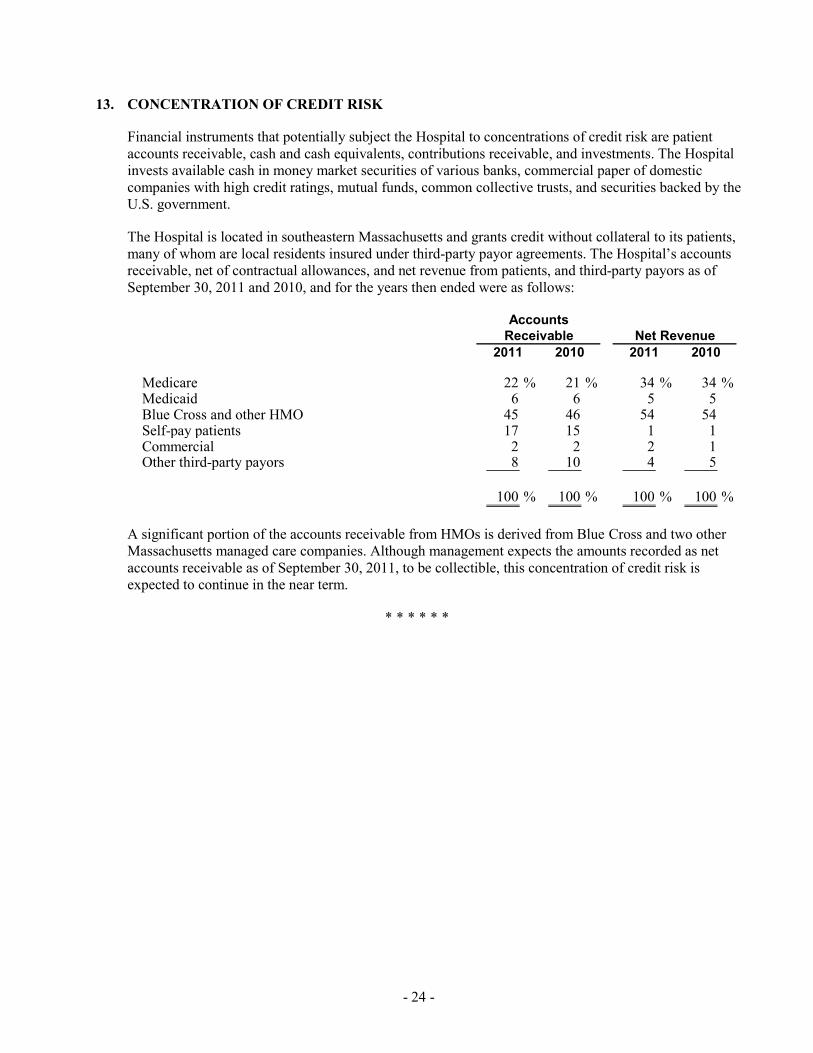

13. CONCENTRATION OF CREDIT RISK

Financial instruments that potentially subject the Hospital to concentrations of credit risk are patient accounts receivable, cash and cash equivalents, contributions receivable, and investments. The Hospital invests available cash in money market securities of various banks, commercial paper of domestic companies with high credit ratings, mutual funds, common collective trusts, and securities backed by the U.S. government.

The Hospital is located in southeastern Massachusetts and grants credit without collateral to its patients, many of whom are local residents insured under third-party payor agreements. The Hospital’s accounts receivable, net of contractual allowances, and net revenue from patients, and third-party payors as of September 30, 2011 and 2010, and for the years then ended were as follows:

2011 2010 2011 2010

Medicare 22 % 21 % 34 % 34 % Medicaid 6 6 5 5 Blue Cross and other HMO 45 46 54 54 Self-pay patients 17 15 1 1 Commercial 2 2 2 1 Other third-party payors 8 10 4 5

100 % 100 % 100 % 100 %

AccountsReceivable Net Revenue

A significant portion of the accounts receivable from HMOs is derived from Blue Cross and two other Massachusetts managed care companies. Although management expects the amounts recorded as net accounts receivable as of September 30, 2011, to be collectible, this concentration of credit risk is expected to continue in the near term.

* * * * * *

- 25 -

SUPPLEMENTAL SCHEDULES

INDEPENDENT AUDITORS’ REPORT ON SUPPLEMENTAL SCHEDULES

To the Board of Directors of South Shore Hospital, Inc. South Weymouth, Massachusetts

Our audit was conducted for the purpose of forming an opinion on the basic financial statements taken as a whole. The supplemental schedules of net revenue and gains available for debt service and revenue available to meet expenses and expenses, each for the year ended September 30, 2011, on pages 26 and 27, are presented for the purpose of additional analysis and are not a required part of the basic financial statements. The supplemental schedules are the responsibility of the management of South Shore Hospital, Inc. Such supplemental schedules have been subjected to the auditing procedures applied in our audit of the basic 2011 financial statements and, in our opinion, are fairly stated in all material respects when considered in relation to the basic financial statements taken as a whole.

December 21, 2011

- 27 -

SOUTH SHORE HOSPITAL, INC.

SUPPLEMENTAL SCHEDULE OF NET REVENUE AND GAINS AVAILABLE FOR DEBT SERVICEFOR THE YEAR ENDED SEPTEMBER 30, 2011

NET REVENUE AND GAINS AVAILABLE FOR DEBT SERVICE: Excess of revenue over expenses 9,061,601$ Add: Depreciation and amortization expense 18,400,901 Interest on long-term indebtedness 6,055,232 Impairment of investments 700,153 Loss on interest rate swaps 1,978,256

TOTAL 36,196,143$

TOTAL PRINCIPAL AND INTEREST REQUIREMENTS: Principal 5,132,909$ Interest 5,598,203

TOTAL 10,731,112$

RATIO OF NET REVENUE AND GAINS AVAILABLE FOR DEBT SERVICE TO TOTAL PRINCIPAL AND INTEREST REQUIREMENTS 3.37

See note to supplemental schedules.

- 28 -

SOUTH SHORE HOSPITAL, INC.

SUPPLEMENTAL SCHEDULE OF REVENUE AVAILABLE TO MEET EXPENSESAND EXPENSESFOR THE YEAR ENDED SEPTEMBER 30, 2011

REVENUE AVAILABLE TO MEET EXPENSES: Total unrestricted revenue, gains, and other support 435,982,840$ Nonoperating gains — net (371,336)

TOTAL 435,611,504$

EXPENSES: Total expenses 426,549,903$ Less: depreciation and amortization (18,400,901) Add: amortization of long-term indebtedness 5,132,909

TOTAL 413,281,911$

See note to supplemental schedules.

- 29 -

SOUTH SHORE HOSPITAL, INC.

NOTE TO SUPPLEMENTAL SCHEDULES FOR THE YEAR ENDED SEPTEMBER 30, 2011

BASIS OF ACCOUNTING

The accompanying supplemental schedules have been prepared in accordance with Section 1004 of the Series F Loan and Trust Agreement with Massachusetts Health and Educational Facilities Authority and are derived from the financial statements of South Shore Hospital, Inc., for the year ended September 30, 2011.

* * * * * *