south africa morning sheet - absa cibcib.absa.co.za/clientoffering/documents/morning sheet... ·...

TRANSCRIPT

Research

Division

25 January 2018

Absa Research is produced by Absa Bank Limited acting through its Corporate and

Investment Bank division, which is a part of Barclays Africa Group Limited and also

affiliated with the Investment Bank of Barclays Bank PLC and its affiliates (referred to as

“Absa”).

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES STARTING AFTER PAGE 7

South Africa Morning Sheet

In an interview with Bloomberg in Davos yesterday, SARB Governor Kganyago

delivered a positive assessment of South Africa, noting that there has been a

resurgence of confidence due to the political changes since the ANC’s elective

conference in December

Headline CPI inflation edged higher in December on higher fuel prices; low point

still likely to come in February

We expect PPI inflation to increase slightly to 5.2% y/y in December from 5.1% in

November due to the effects of higher fuel prices

DA leadership intensifies approach towards Cape Town’s water crisis

Speaking in Davos yesterday to Bloomberg TV, SARB Governor Kganyago provided

an encouragingly positive assessment of South Africa’s progress both politically and,

by implication, economically since the ANC’s National Conference in December

chose Deputy President Ramaphosa as its new leader. Kganyago said that confidence

had surged with “renewed optimism” and evidence that South Africa’s institutions were

robust. In particular, he cited parliament’s return to its core purpose of holding the

executive and public officials to account, and said that “corruption and misrule will

soon be history”. We agree that developments appear to have been favourable since

Ramaphosa was narrowly elected, but think it could take a long time to root out alleged

corruption at all levels of government, even if the state capture at the top is addressed

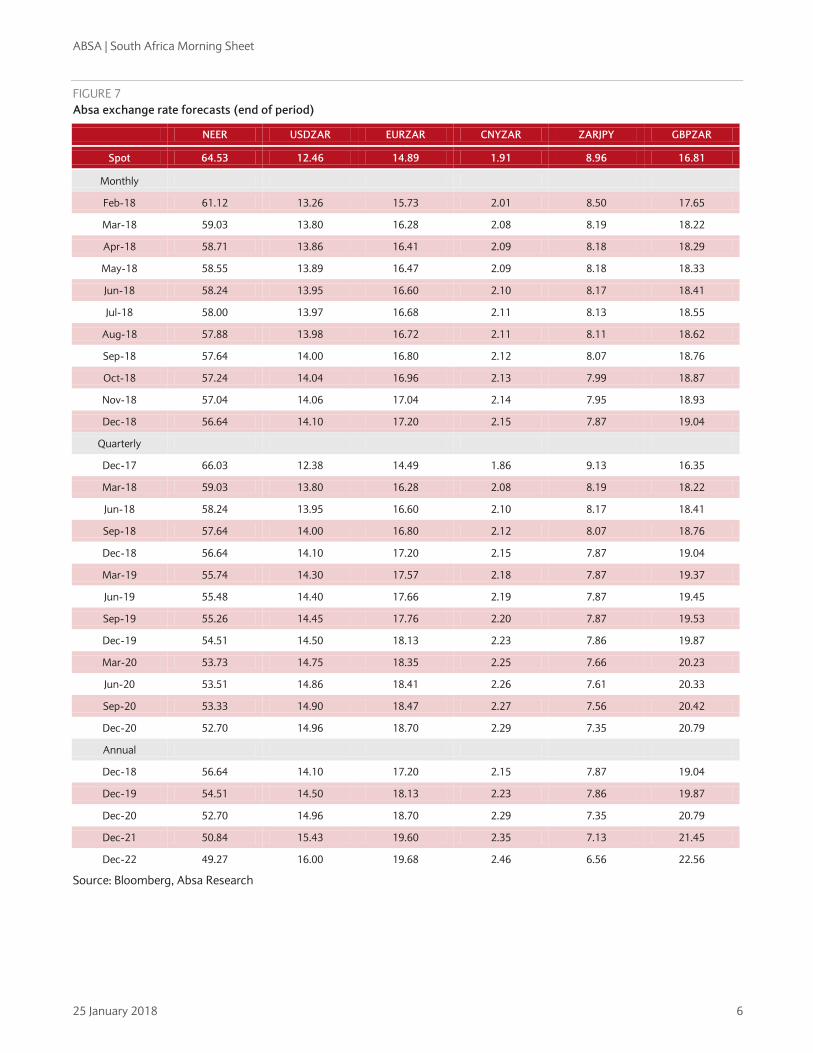

quickly. The Governor said that the rand’s strength currently reflected the end of long-

standing political uncertainty, and argued separately that a “cyclical recovery” was

underway now. However, we think that, despite current optimism, the still relatively

weak macro fundamentals will likely reassert and the exchange rate could weaken. We

also note that some of the performance of the exchange rate recently is due to the

weaker USD. Interestingly, Kganyago observed that while Zuma is still the president of

the country, Ramaphosa as deputy president and leader of the ANC is showing that he

is able to exercise some executive powers. Finally, Kganyago said that South Africa had

a good case to make for avoiding a downgrade when Moody’s completes its rating

review at end-February or early March, after putting the country on review for a

downgrade of its Baa3 Negative Outlook ratings on 24 November. However, we think

that Moody’s (whose current foreign currency rating is one notch above Fitch’s and two

notches above S&P’s) is more likely than not to downgrade South Africa unless the

Budget on 21 February is a masterful defeat of the huge fiscal slippage without further

constraining weak growth. In this regard, we think a hike in VAT is needed, but doubt

that even this new, more energized, ANC leadership would implement such a hike in a

pre-election year.

Peter Worthington

+27 21 927 6525

Absa, South Africa

Miyelani Maluleke

+27 11 895 5655

Absa, South Africa

www.absa.co.za

ABSA | South Africa Morning Sheet

25 January 2018 2

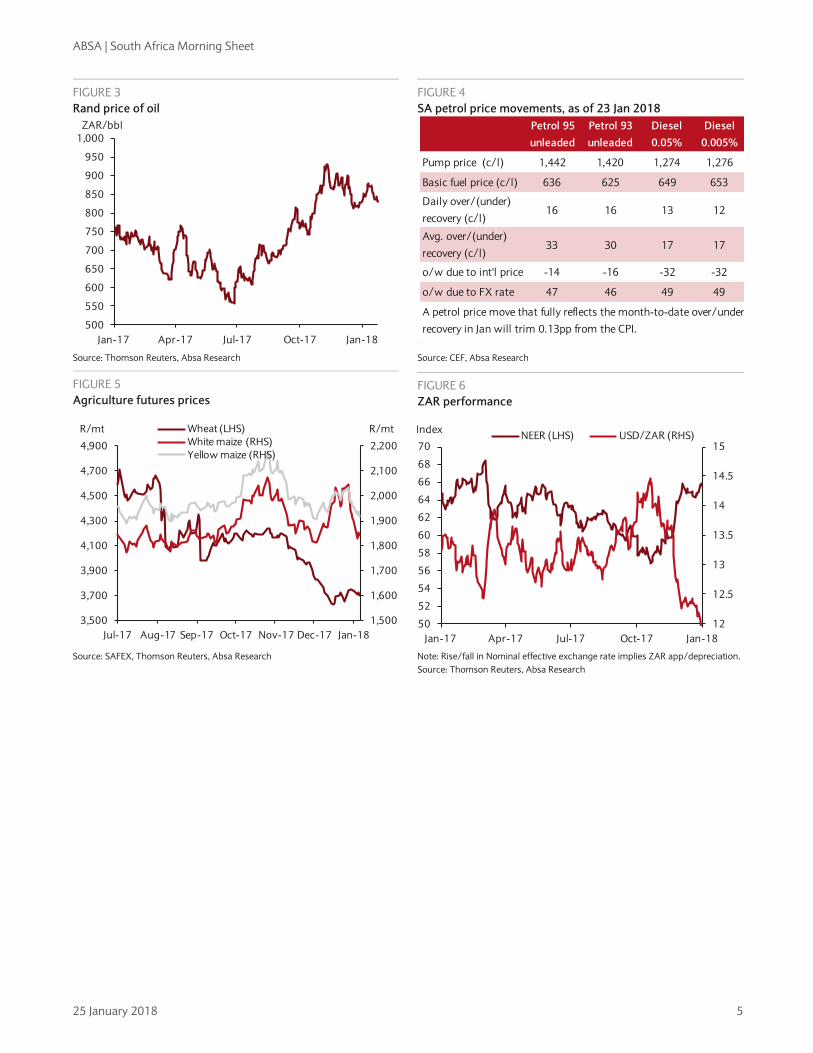

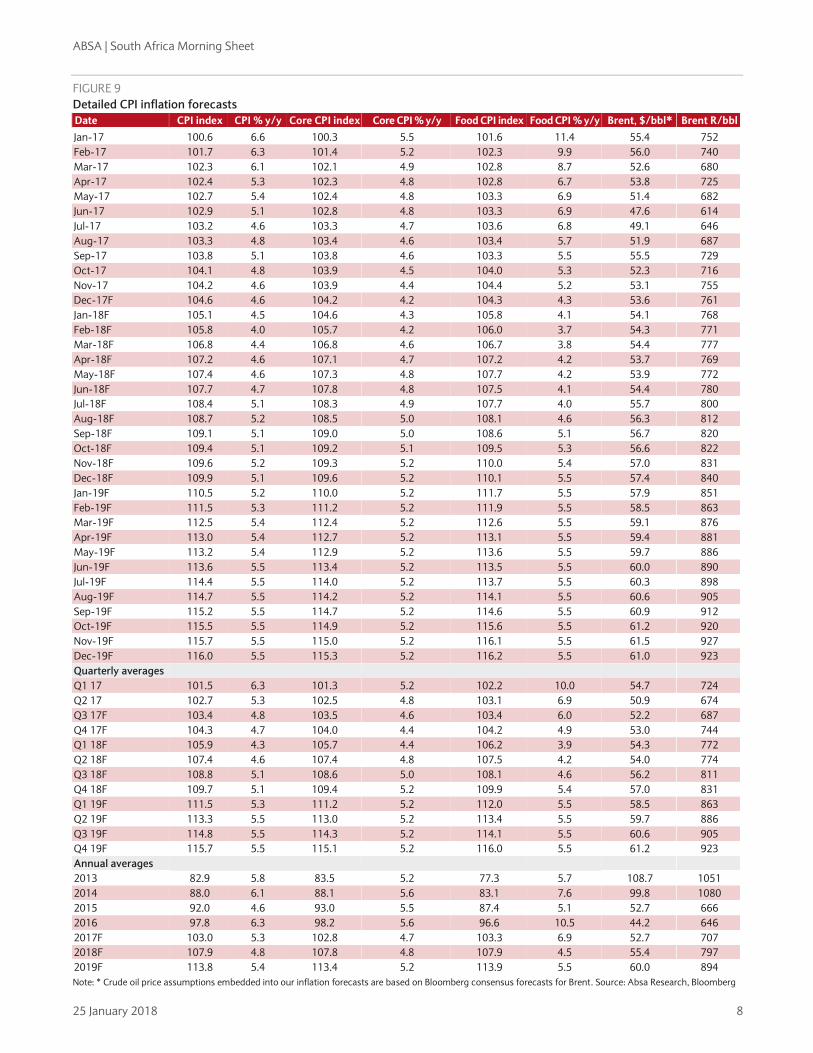

The December CPI data showed headline CPI inflation at 4.7% y/y, just 0.1pp higher

compared with November. This was in line with consensus but higher than our forecast of

an unchanged print. Core CPI inflation edged lower by 0.2pp to 4.2%, in line with our

forecast but slightly lower than consensus (4.3%). With food price inflation also easing in

December, the rise in headline CPI inflation owed primarily to the sharp increase in fuel

prices. The fuel price increase of 5.2% m/m in December, already earlier confirmed by the

Department of Energy, pushed y/y inflation on fuel to 14.2%, up from 7.9% in November.

Food price inflation eased less than we had expected, to 4.8% y/y in December from 5.2%

in November. Within the food basket, price pressures remained broadly contained with

meat price inflation slowing for the third straight month, to 14.0% y/y (Nov: 14.9%), but

there was some upside offset from ‘milk, eggs and cheese’ price inflation, which increased

to 4.8% y/y (Nov: 4.4%). Meanwhile, we see the decline in core CPI inflation as consistent

with persistent slack in economic activity and the effect of the stronger rand on tradable

goods. We expect headline CPI inflation to ease in the next two months, touching its low

point of 4.1% in February before beginning to rise gradually, averaging 5.2% in Q4 18.

Softer prints of around and below the mid-point of the SARB target range in the next two

releases could raise market expectations of a rate cut, but we remind investors that the

SARB MPC is more concerned with the CPI inflation outlook 12-18 months ahead. Both our

forecasts and the SARB’s show headline CPPI inflation averaging 5.5% in Q4 19 – close to

the upper end of the target range (see South Africa: Headline CPI edges higher on fuel

prices, 24 January 2018).

Stats SA is due to publish the December PPI data this morning at 11:30, adding more

evidence on inflation trends. We forecast headline PPI (i.e. PPI for final manufactured

goods) to have risen slightly to 5.2% y/y (consensus: 5.2%) from 5.1% in November. While

we look for food PPI inflation to have continued to ease on base effects and easing meat

price pressures, this is likely to be more than offset by the sharp 5.2% m/m increase in fuel

prices in December, particularly as fuel prices have a relatively higher weighing in PPI

relative to the CPI basket.

The leader of the Democratic Alliance, which governs the Western Cape and the City of

Cape Town, yesterday moved to take firmer control of the gathering water crisis, after

the estimates of Day Zero, when the city’s taps run dry, had been moved forward a week,

to 12 April. DA Cape Town executive mayor Patricia de Lille has been stripped of her

responsibility to manage the water crisis, with such powers being handed to Ian Neilson, the

Deputy Mayor, and Xanthea Limberg, the city counsellor in charge of the energy and

climate change portfolio. Also joining Maimane’s “drought crisis team” are Premier Helen

Zille, provincial DA leader Bonginkosi Madikizela and Anton Bredell, the provincial Minister

of Local Government, Environmental Affairs and Development Planning. Maimane warned

that intensified water-saving efforts were the only way to postpone and possibly avoid Day

Zero, with the current water supply augmentation efforts (mainly tapping into aquifers but

also three small scale desalination plants) only coming fully on stream by May and only

providing 120 million litres per day, compared with the current targeted consumption for

the city of 450 million litres/day, about 50 litres per person. Maimane also said that water

supply would be maintained in “essential service areas” without naming them, except for

hospitals. He also said, however, that Cape Town’s central business district might be spared

water shut-offs. Nonetheless, the CBD is only a tiny portion of Cape Town’s economic

activity, and thus the drought could pose a significant risk to growth. It is important to

remember, however, that Day Zero is predicated on the idea that there will be no more

water available when dam levels hit the 13.5% average. However, we think that this water

may still be utilized. Maimane said that he and Premier Zille would step up efforts to get the

necessary engagement from the national Department of Water and Sanitation, which has

legal and political responsibility for bulk water supply, and which they have accused of

dragging its feet during the gathering crisis.

ABSA | South Africa Morning Sheet

25 January 2018 3

ABSA | South Africa Morning Sheet

25 January 2018 4

FIGURE 1

Calendar

Time Country Event Period Consensus Absa Prior Prior-1

23-Jan 09:00 SA Leading Indicator index Nov -- 105.4 A 105.4 104.7

24-Jan 10:00 SA CPI, % y/y Dec 4.7 4.7 A 4.6 4.8

10:00 SA CPI, % m/m Dec 0.5 0.5 A 0.1 0.3

10:00 SA Core CPI, % y/y Dec 4.3 4.2 A 4.4 4.5

10:00 SA Core CPI, % m/m Dec 0.2 0.3 A 0.0 0.1

25-Jan 11:30 SA PPI, % y/y Dec 5.2 4.6 5.1 5.0

11:30 SA PPI, % m/m Dec 0.6 0.0 0.5 0.7

Source: Bloomberg, Absa Research

FIGURE 1

Review of last week’s key domestic data releases

Main indicators Period Survey Actual Prior Comments

Mining output, % m/m sa Nov -- -0.7 A 2.7 R Contraction mainly driven by PGMs and gold output.

Retail Sales constant, % m/m, sa Nov 0.8 4.0 A -0.1 Surge likely by the effect of ‘Black Friday’ sales.

SARB Repo rate, % Jan 6.75 6.75 A 6.75 MPC voted 5:1 to keep the repo rate on hold.

Source: Bloomberg, Absa Research

ABSA | South Africa Morning Sheet

25 January 2018 5

FIGURE 3

Rand price of oil

FIGURE 4

SA petrol price movements, as of 23 Jan 2018

Source: Thomson Reuters, Absa Research Source: CEF, Absa Research

FIGURE 5

Agriculture futures prices

FIGURE 6

ZAR performance

Source: SAFEX, Thomson Reuters, Absa Research Note: Rise/fall in Nominal effective exchange rate implies ZAR app/depreciation.

Source: Thomson Reuters, Absa Research

500

550

600

650

700

750

800

850

900

950

1,000

Jan-17 Apr-17 Jul-17 Oct-17 Jan-18

ZAR/bbl Petrol 95

unleaded

Petrol 93

unleaded

Diesel

0.05%

Diesel

0.005%

Pump price (c/l) 1,442 1,420 1,274 1,276

Basic fuel price (c/l) 636 625 649 653

Daily over/(under)

recovery (c/l)16 16 13 12

Avg. over/(under)

recovery (c/l)33 30 17 17

o/w due to int'l price -14 -16 -32 -32

o/w due to FX rate 47 46 49 49

A petrol price move that fully reflects the month-to-date over/under

recovery in Jan will trim 0.13pp from the CPI.

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

3,500

3,700

3,900

4,100

4,300

4,500

4,700

4,900

Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18

R/mtR/mt Wheat (LHS)

White maize (RHS)

Yellow maize (RHS)

12

12.5

13

13.5

14

14.5

15

50

52

54

56

58

60

62

64

66

68

70

Jan-17 Apr-17 Jul-17 Oct-17 Jan-18

IndexNEER (LHS) USD/ZAR (RHS)

ABSA | South Africa Morning Sheet

25 January 2018 6

FIGURE 7

Absa exchange rate forecasts (end of period)

NEER USDZAR EURZAR CNYZAR ZARJPY GBPZAR

Spot 64.53 12.46 14.89 1.91 8.96 16.81

Monthly

Feb-18 61.12 13.26 15.73 2.01 8.50 17.65

Mar-18 59.03 13.80 16.28 2.08 8.19 18.22

Apr-18 58.71 13.86 16.41 2.09 8.18 18.29

May-18 58.55 13.89 16.47 2.09 8.18 18.33

Jun-18 58.24 13.95 16.60 2.10 8.17 18.41

Jul-18 58.00 13.97 16.68 2.11 8.13 18.55

Aug-18 57.88 13.98 16.72 2.11 8.11 18.62

Sep-18 57.64 14.00 16.80 2.12 8.07 18.76

Oct-18 57.24 14.04 16.96 2.13 7.99 18.87

Nov-18 57.04 14.06 17.04 2.14 7.95 18.93

Dec-18 56.64 14.10 17.20 2.15 7.87 19.04

Quarterly

Dec-17 66.03 12.38 14.49 1.86 9.13 16.35

Mar-18 59.03 13.80 16.28 2.08 8.19 18.22

Jun-18 58.24 13.95 16.60 2.10 8.17 18.41

Sep-18 57.64 14.00 16.80 2.12 8.07 18.76

Dec-18 56.64 14.10 17.20 2.15 7.87 19.04

Mar-19 55.74 14.30 17.57 2.18 7.87 19.37

Jun-19 55.48 14.40 17.66 2.19 7.87 19.45

Sep-19 55.26 14.45 17.76 2.20 7.87 19.53

Dec-19 54.51 14.50 18.13 2.23 7.86 19.87

Mar-20 53.73 14.75 18.35 2.25 7.66 20.23

Jun-20 53.51 14.86 18.41 2.26 7.61 20.33

Sep-20 53.33 14.90 18.47 2.27 7.56 20.42

Dec-20 52.70 14.96 18.70 2.29 7.35 20.79

Annual

Dec-18 56.64 14.10 17.20 2.15 7.87 19.04

Dec-19 54.51 14.50 18.13 2.23 7.86 19.87

Dec-20 52.70 14.96 18.70 2.29 7.35 20.79

Dec-21 50.84 15.43 19.60 2.35 7.13 21.45

Dec-22 49.27 16.00 19.68 2.46 6.56 22.56

Source: Bloomberg, Absa Research

ABSA | South Africa Morning Sheet

25 January 2018 7

FIGURE 8

Absa exchange rate forecast (period average)

Period avg. USDZAR EURZAR CNYZAR ZARJPY GBPZAR

Spot 12.46 14.89 1.91 8.96 16.81

Monthly

Feb-18 12.86 15.31 1.96 8.73 17.23

Mar-18 13.53 16.01 2.05 8.34 17.93

Apr-18 13.83 16.35 2.08 8.19 18.25

May-18 13.87 16.44 2.09 8.18 18.31

Jun-18 13.92 16.53 2.10 8.18 18.37

Jul-18 13.96 16.64 2.11 8.15 18.48

Aug-18 13.97 16.70 2.11 8.12 18.58

Sep-18 13.99 16.76 2.12 8.09 18.69

Oct-18 14.02 16.88 2.13 8.03 18.82

Nov-18 14.05 17.00 2.14 7.97 18.90

Dec-18 14.08 17.12 2.15 7.91 18.98

Quarterly

Dec-17 13.20 15.66 2.00 8.53 17.58

Mar-18 13.09 15.39 1.97 8.66 17.28

Jun-18 13.87 16.44 2.09 8.18 18.31

Sep-18 13.97 16.70 2.11 8.12 18.58

Dec-18 14.05 17.00 2.14 7.97 18.90

Mar-19 14.20 17.39 2.17 7.87 19.20

Jun-19 14.35 17.62 2.19 7.87 19.41

Sep-19 14.43 17.71 2.20 7.87 19.49

Dec-19 14.48 17.94 2.22 7.86 19.70

Mar-20 14.63 18.24 2.24 7.76 20.05

Jun-20 14.80 18.38 2.26 7.63 20.28

Sep-20 14.88 18.44 2.26 7.58 20.37

Dec-20 14.93 18.58 2.28 7.46 20.60

Annual

Dec-18 13.24 16.03 2.03 8.45 17.88

Dec-19 14.30 17.66 2.19 7.87 19.45

Dec-20 14.73 18.41 2.26 7.61 20.33

Dec-21 15.19 19.15 2.32 7.24 21.12

Dec-22 15.72 19.64 2.41 6.85 22.01

Source: Bloomberg, Absa Research

ABSA | South Africa Morning Sheet

25 January 2018 8

FIGURE 9

Detailed CPI inflation forecasts

Date CPI index CPI % y/y Core CPI index Core CPI % y/y Food CPI index Food CPI % y/y Brent, $/bbl* Brent R/bbl

Jan-17 100.6 6.6 100.3 5.5 101.6 11.4 55.4 752

Feb-17 101.7 6.3 101.4 5.2 102.3 9.9 56.0 740

Mar-17 102.3 6.1 102.1 4.9 102.8 8.7 52.6 680

Apr-17 102.4 5.3 102.3 4.8 102.8 6.7 53.8 725

May-17 102.7 5.4 102.4 4.8 103.3 6.9 51.4 682

Jun-17 102.9 5.1 102.8 4.8 103.3 6.9 47.6 614

Jul-17 103.2 4.6 103.3 4.7 103.6 6.8 49.1 646

Aug-17 103.3 4.8 103.4 4.6 103.4 5.7 51.9 687

Sep-17 103.8 5.1 103.8 4.6 103.3 5.5 55.5 729

Oct-17 104.1 4.8 103.9 4.5 104.0 5.3 52.3 716

Nov-17 104.2 4.6 103.9 4.4 104.4 5.2 53.1 755

Dec-17F 104.6 4.6 104.2 4.2 104.3 4.3 53.6 761

Jan-18F 105.1 4.5 104.6 4.3 105.8 4.1 54.1 768

Feb-18F 105.8 4.0 105.7 4.2 106.0 3.7 54.3 771

Mar-18F 106.8 4.4 106.8 4.6 106.7 3.8 54.4 777

Apr-18F 107.2 4.6 107.1 4.7 107.2 4.2 53.7 769

May-18F 107.4 4.6 107.3 4.8 107.7 4.2 53.9 772

Jun-18F 107.7 4.7 107.8 4.8 107.5 4.1 54.4 780

Jul-18F 108.4 5.1 108.3 4.9 107.7 4.0 55.7 800

Aug-18F 108.7 5.2 108.5 5.0 108.1 4.6 56.3 812

Sep-18F 109.1 5.1 109.0 5.0 108.6 5.1 56.7 820

Oct-18F 109.4 5.1 109.2 5.1 109.5 5.3 56.6 822

Nov-18F 109.6 5.2 109.3 5.2 110.0 5.4 57.0 831

Dec-18F 109.9 5.1 109.6 5.2 110.1 5.5 57.4 840

Jan-19F 110.5 5.2 110.0 5.2 111.7 5.5 57.9 851

Feb-19F 111.5 5.3 111.2 5.2 111.9 5.5 58.5 863

Mar-19F 112.5 5.4 112.4 5.2 112.6 5.5 59.1 876

Apr-19F 113.0 5.4 112.7 5.2 113.1 5.5 59.4 881

May-19F 113.2 5.4 112.9 5.2 113.6 5.5 59.7 886

Jun-19F 113.6 5.5 113.4 5.2 113.5 5.5 60.0 890

Jul-19F 114.4 5.5 114.0 5.2 113.7 5.5 60.3 898

Aug-19F 114.7 5.5 114.2 5.2 114.1 5.5 60.6 905

Sep-19F 115.2 5.5 114.7 5.2 114.6 5.5 60.9 912

Oct-19F 115.5 5.5 114.9 5.2 115.6 5.5 61.2 920

Nov-19F 115.7 5.5 115.0 5.2 116.1 5.5 61.5 927

Dec-19F 116.0 5.5 115.3 5.2 116.2 5.5 61.0 923

Quarterly averages

Q1 17 101.5 6.3 101.3 5.2 102.2 10.0 54.7 724

Q2 17 102.7 5.3 102.5 4.8 103.1 6.9 50.9 674

Q3 17F 103.4 4.8 103.5 4.6 103.4 6.0 52.2 687

Q4 17F 104.3 4.7 104.0 4.4 104.2 4.9 53.0 744

Q1 18F 105.9 4.3 105.7 4.4 106.2 3.9 54.3 772

Q2 18F 107.4 4.6 107.4 4.8 107.5 4.2 54.0 774

Q3 18F 108.8 5.1 108.6 5.0 108.1 4.6 56.2 811

Q4 18F 109.7 5.1 109.4 5.2 109.9 5.4 57.0 831

Q1 19F 111.5 5.3 111.2 5.2 112.0 5.5 58.5 863

Q2 19F 113.3 5.5 113.0 5.2 113.4 5.5 59.7 886

Q3 19F 114.8 5.5 114.3 5.2 114.1 5.5 60.6 905

Q4 19F 115.7 5.5 115.1 5.2 116.0 5.5 61.2 923

Annual averages

2013 82.9 5.8 83.5 5.2 77.3 5.7 108.7 1051

2014 88.0 6.1 88.1 5.6 83.1 7.6 99.8 1080

2015 92.0 4.6 93.0 5.5 87.4 5.1 52.7 666

2016 97.8 6.3 98.2 5.6 96.6 10.5 44.2 646

2017F 103.0 5.3 102.8 4.7 103.3 6.9 52.7 707

2018F 107.9 4.8 107.8 4.8 107.9 4.5 55.4 797

2019F 113.8 5.4 113.4 5.2 113.9 5.5 60.0 894

Note: * Crude oil price assumptions embedded into our inflation forecasts are based on Bloomberg consensus forecasts for Brent. Source: Absa Research, Bloomberg

ABSA | South Africa Morning Sheet

25 January 2018 9

FIGURE 10

Main macroeconomic variables in South Africa

2017 2018 2019

2016 2017F 2018F 2019F 2020F 2021F Q3 Q4F Q1F Q2F Q3F Q4F Q1F Q2F Q3F Q4F

Output (% q/q saar)

Real GDP 2.0 1.5 1.1 1.0 1.2 1.2 1.7 2.1 2.5 2.6 0.3 0.9 1.4 1.7 1.9 1.9

Real GDP (%y/y) 1.0 1.4 1.8 1.4 1.2 1.1 1.3 1.6 1.9 2.2 0.3 0.9 1.4 1.7 1.9 1.9

Private consumption 2.6 0.8 0.8 0.8 0.9 1.1 1.2 2.5 2.7 3.2 0.8 1.3 1.3 1.7 2.0 1.9

Public consumption -0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 2.0 0.3 0.4 0.5 0.5 0.5

Investment 4.3 -0.1 0.9 1.5 1.8 2.1 2.5 3.3 3.4 4.5 -3.9 0.2 1.3 2.7 3.2 3.3

Exports -10.3 3.8 3.4 2.7 4.3 1.9 2.4 1.2 1.9 0.4 -0.1 0.8 2.2 2.1 1.7 1.8

Imports -13.7 3.2 2.2 2.4 3.8 2.4 1.4 2.2 1.9 1.5 -3.7 1.9 1.1 2.2 2.1 1.9

Prices (% y/y)

CPI inflation 4.8 4.7 4.3 4.6 5.1 5.1 5.3 5.5 5.5 5.5 6.3 5.3 4.8 5.5 5.5 5.7

Core CPI inflation 4.6 4.4 4.4 4.8 5.0 5.2 5.2 5.2 5.2 5.2 5.6 4.8 4.9 5.2 5.4 5.6

PPI inflation 4.3 4.9 4.9 5.0 5.2 5.0 4.6 5.3 5.2 5.2 7.1 4.8 5.0 5.1 5.4 5.1

External and government accounts (% of GDP)

Current account -2.3 -1.4 -2.1 -2.2 -2.2 -2.6 -2.8 -2.8 -2.8 -3.1 -3.3 -2.0 -2.3 -2.9 -3.3 -3.7

Consolidated fiscal balance* n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a -3.3 -4.3 -3.3 -3.2 -3.0 -2.9

Consolidated primary balance* n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a 0.0 -0.8 0.4 0.6 0.9 1.0

Government debt* n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a 50.7 54.2 56.4 57.5 58.5 59.4

Interest rates (% eop)

Repurchase rate 6.75 6.75 6.75 6.75 6.75 6.75 6.75 6.75 6.75 6.75 7.00 6.75 6.75 6.75 6.75 6.75

Prime rate 10.25 10.25 10.25 10.25 10.25 10.25 10.25 10.25 10.25 10.25 10.50 6.75 10.25 10.25 10.25 10.25

Note:*For fiscal year commencing 1 April.

Source: SARB, National Treasury, Stats SA, Thomson Reuters, Absa Research

Analyst Certification

We, Miyelani Maluleke and Peter Worthington, hereby certify (1) that the views expressed in this research report accurately reflect our personal views

about any or all of the subject securities or issuers referred to in this research report and (2) no part of our compensation was, is or will be directly or

indirectly related to the specific recommendations or views expressed in this research report.

Important Disclosures:

Absa Research is produced by Absa Bank Limited acting through its Corporate and Investment Bank division, which is a part of Barclays Africa Group

Limited and also affiliated with the Investment Bank of Barclays Bank PLC and its affiliates (referred to as “Absa”).

All authors contributing to this research report are Research Analysts unless otherwise indicated. The publication date at the top of the report reflects the

local time where the report was produced and may differ from the release date provided in GMT.

Availability of Disclosures:

For current important disclosures regarding any issuers which are the subject of this research report please refer to https://publicresearch.barclays.com

or alternatively send a written request to: Barclays Research Compliance, 745 Seventh Avenue, 13th Floor, New York, NY 10019 or call +1-212-526-1072.

Absa does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Absa may have a conflict

of interest that could affect the objectivity of this report. Absa regularly trades, generally deals as principal and generally provides liquidity (as market

maker or otherwise) in the debt securities that are the subject of this research report (and related derivatives thereof). Absa trading desks may have either

a long and / or short position in such securities, other financial instruments and / or derivatives, which may pose a conflict with the interests of investing

customers. Where permitted and subject to appropriate information barrier restrictions, Absa fixed income research analysts regularly interact with its

trading desk personnel regarding current market conditions and prices. Absa fixed income research analysts receive compensation based on various

factors including, but not limited to, the quality of their work, the overall performance of the firm (including the profitability of the Corporate and

Investment Banking division), the profitability and revenues of the Markets business and the potential interest of the firm's investing clients in research

with respect to the asset class covered by the analyst. To the extent that any historical pricing information was obtained from Absa trading desks, the firm

makes no representation that it is accurate or complete. All levels, prices and spreads are historical and do not represent current market levels, prices or

spreads, some or all of which may have changed since the publication of this document. The Absa Research Department within Absa Bank Limited

operates independently from the Barclays Research Department within the Investment Bank of Barclays Bank PLC and its affiliates (collectively

“Barclays”). Eligible clients may receive research reports from both research departments, which may reach different conclusions and may contain

different or conflicting ratings or research recommendations, whether as a result of differing time horizons, methodologies, or otherwise.

In order to access Barclays Statement regarding Research Dissemination Policies and Procedures, please refer to

https://publicresearch.barcap.com/static/S_ResearchDissemination.html. In order to access Barclays Research Conflict Management Policy Statement,

please refer to: https://publicresearch.barcap.com/static/S_ConflictManagement.html.

All pricing information is indicative only. Prices are sourced from Thomson Reuters as of the last available closing price at the time of production of the

research report, unless another time and source is indicated.

Explanation of other types of investment recommendations produced by Absa FICC Research:

Trade ideas contained herein that have been produced by the Credit teams within Absa Research are valid at current market conditions and may not be

otherwise relied upon.

Trade ideas contained herein that have been produced by other research teams within Absa FICC Research shall remain open until they are subsequently

amended or closed in a future research report.

Disclosure of previous investment recommendations produced by Absa and Barclays FICC Research:

Absa FICC Research may have published other investment recommendations in respect of the same securities/instruments recommended in this

research report during the preceding 12 months. To view previous investment recommendations published by Absa FICC Research and Barclays FICC

Research in the preceding 12 months please refer to https://live.barcap.com/go/research/ResearchInvestmentRecommendations.

Legal entities involved in producing Absa Research:

Absa Bank Limited (Absa, South Africa)

Disclaimer:

This publication has been produced by Absa Bank Limited acting through its Corporate and Investment Bank division, which is a part of Barclays Africa

Group Limited and affiliated with the Investment Bank of Barclays Bank PLC (referred to as “Absa”). It has been distributed by Absa or one or more

Barclays affiliated legal entities listed below. It is provided to our clients for information purposes only, and Absa makes no express or implied warranties,

and expressly disclaims all warranties of merchantability or fitness for a particular purpose or use with respect to any data included in this publication. To

the extent that this publication states on the front page that it is intended for institutional investors and is not subject to all of the independence and

disclosure standards applicable to debt research reports prepared for retail investors under U.S. FINRA Rule 2242, it is an “institutional debt research

report” and distribution to retail investors is strictly prohibited. Absa also distributes such institutional debt research reports to various issuers, regulatory

and academic organisations for informational purposes and not for the purpose of making investment decisions regarding any debt securities. Any such

recipients that do not want to continue receiving Absa institutional debt research reports should contact [email protected]. Absa will not treat

unauthorized recipients of this report as its clients and accepts no liability for use by them of the contents which may not be suitable for their personal use.

Prices shown are indicative and Absa is not offering to buy or sell or soliciting offers to buy or sell any financial instrument.

Without limiting any of the foregoing and to the extent permitted by law, in no event shall Absa, nor any affiliate, nor any of their respective officers,

directors, partners, or employees have any liability for (a) any special, punitive, indirect, or consequential damages; or (b) any lost profits, lost revenue, loss

of anticipated savings or loss of opportunity or other financial loss, even if notified of the possibility of such damages, arising from any use of this

publication or its contents.

Other than disclosures relating to Absa, the information contained in this publication has been obtained from sources that Absa Research believes to be

reliable, but Absa does not represent or warrant that it is accurate or complete. Absa is not responsible for, and makes no warranties whatsoever as to, the

information or opinions contained in any written, electronic, audio or video presentations of third parties that are accessible via a direct hyperlink in this

publication or via a hyperlink to a third-party web site (‘Third-Party Content’). Any such Third-Party Content has not been adopted or endorsed by Absa,

does not represent the views or opinions of Absa, and is not incorporated by reference into this publication. Third-Party Content is provided for

information purposes only and Absa has not independently verified its accuracy or completeness.

The views in this publication are those of the author(s) and are subject to change, and Absa has no obligation to update its opinions or the information in

this publication. If this publication contains recommendations, those recommendations reflect solely and exclusively those of the authoring analyst(s),

and such opinions were prepared independently of any other interests, including those of Absa and/or its affiliates. This publication does not constitute

personal investment advice or take into account the individual financial circumstances or objectives of the clients who receive it. The securities discussed

herein may not be suitable for all investors. Absa recommends that investors independently evaluate each issuer, security or instrument discussed herein

and consult any independent advisors they believe necessary. The value of and income from any investment may fluctuate from day to day as a result of

changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may

differ substantially from those reflected. Past performance is not necessarily indicative of future results.

This document is being distributed (1) only by or with the approval of an authorised person (Barclays Bank PLC) or (2) to, and is directed at (a) persons in

the United Kingdom having professional experience in matters relating to investments and who fall within the definition of "investment professionals" in

Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the "Order"); or (b) high net worth companies,

unincorporated associations and partnerships and trustees of high value trusts as described in Article 49(2) of the Order; or (c) other persons to whom it

may otherwise lawfully be communicated (all such persons being "Relevant Persons"). Any investment or investment activity to which this

communication relates is only available to and will only be engaged in with Relevant Persons. Any other persons who receive this communication should

not rely on or act upon it. Barclays Bank PLC is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and

the Prudential Regulation Authority and is a member of the London Stock Exchange.

The Investment Bank of Barclays Bank PLC undertakes U.S. securities business in the name of its wholly owned subsidiary Barclays Capital Inc., a FINRA

and SIPC member. Barclays Capital Inc., a U.S. registered broker/dealer, is distributing this material in the United States and, in connection therewith

accepts responsibility for its contents. Any U.S. person wishing to effect a transaction in any security discussed herein should do so only by contacting a

representative of Barclays Capital Inc. in the U.S. at 745 Seventh Avenue, New York, New York 10019.

Non-U.S. persons that are clients of Barclays should contact and execute transactions through a Barclays Bank PLC branch or affiliate in their home

jurisdiction unless local regulations permit otherwise.

Barclays Bank PLC, Paris Branch (registered in France under Paris RCS number 381 066 281) is regulated by the Autorité des marchés financiers and the

Autorité de contrôle prudentiel. Registered office 34/36 Avenue de Friedland 75008 Paris.

This material is distributed in Canada by Barclays Capital Canada Inc., a registered investment dealer, a Dealer Member of IIROC (www.iiroc.ca), and a

Member of the Canadian Investor Protection Fund (CIPF).

Subject to the conditions of this publication as set out above, Absa Bank Limited, acting through its Corporate and Investment Bank division, which is a

part of Barclays Africa Group Limited and affiliated with the Investment Bank of Barclays Bank PLC, an authorised financial services provider (Registration

No.: 1986/004794/06. Registered Credit Provider Reg No NCRCP7), is distributing this material in South Africa. Absa Bank Limited is regulated by the

South African Reserve Bank. This publication is not, nor is it intended to be, advice as defined and/or contemplated in the (South African) Financial

Advisory and Intermediary Services Act, 37 of 2002, or any other financial, investment, trading, tax, legal, accounting, retirement, actuarial or other

professional advice or service whatsoever. Any South African person or entity wishing to effect a transaction in any security discussed herein should do so

only by contacting a representative of Absa Bank Limited acting through its Corporate and Investment Bank division in South Africa, 7th Floor, Barclays

Towers West, 15 Troye Street, Johannesburg, 2001. Absa Bank Limited is an affiliate of the Barclays group.

All Absa research reports are distributed to institutional investors in Japan by Barclays Securities Japan Limited. Barclays Securities Japan Limited is a joint-

stock company incorporated in Japan with registered office of 6-10-1 Roppongi, Minato-ku, Tokyo 106-6131, Japan. It is a subsidiary of Barclays Bank PLC

and a registered financial instruments firm regulated by the Financial Services Agency of Japan. Registered Number: Kanto Zaimukyokucho (kinsho) No.

143.

Barclays Bank PLC, Hong Kong Branch is distributing this material in Hong Kong as an authorised institution regulated by the Hong Kong Monetary

Authority. Registered Office: 41/F, Cheung Kong Center, 2 Queen's Road Central, Hong Kong.

Absa equity research reports are distributed in India by Barclays Securities (India) Private Limited (BSIPL). BSIPL is a company incorporated under the

Companies Act, 1956 having CIN U67120MH2006PTC161063. BSIPL is registered and regulated by the Securities and Exchange Board of India (SEBI) as a

Research Analyst: INH000001519; Portfolio Manager INP000002585; Stock Broker/Trading and Clearing Member: National Stock Exchange of India

Limited (NSE) Capital Market INB231292732, NSE Futures & Options INF231292732, NSE Currency derivatives INE231450334, Bombay Stock Exchange

Limited (BSE) Capital Market INB011292738, BSE Futures & Options INF011292738; Depository Participant (DP) with the National Securities &

Depositories Limited (NSDL): DP ID: IN-DP-NSDL-299-2008; Investment Adviser: INA000000391. The registered office of BSIPL is at 208, Ceejay House,

Shivsagar Estate, Dr. A. Besant Road, Worli, Mumbai – 400 018, India. Telephone No: +91 2267196000. Fax number: +91 22 67196100. Any other reports

produced by Absa are distributed in India by Barclays Bank PLC, India Branch, an associate of BSIPL in India that is registered with Reserve Bank of India

(RBI) as a Banking Company under the provisions of The Banking Regulation Act, 1949 (Regn No BOM43) and registered with SEBI as Merchant Banker

(Regn No INM000002129) and also as Banker to the Issue (Regn No INBI00000950). Barclays Investments and Loans (India) Limited, registered with RBI

as Non Banking Financial Company (Regn No RBI CoR-07-00258), and Barclays Wealth Trustees (India) Private Limited, registered with Registrar of

Companies (CIN U93000MH2008PTC188438), are associates of BSIPL in India that are not authorised to distribute any reports produced by Absa.

Barclays Bank PLC Frankfurt Branch distributes this material in Germany under the supervision of Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin).

This material is distributed in Mexico by Barclays Bank Mexico, S.A.

Nothing herein should be considered investment advice as defined in the Israeli Regulation of Investment Advisory, Investment Marketing and Portfolio

Management Law, 1995 (“Advisory Law”). This document is being made to eligible clients (as defined under the Advisory Law) only. Barclays Israeli

branch previously held an investment marketing license with the Israel Securities Authority but it cancelled such license on 30/11/2014 as it solely

provides its services to eligible clients pursuant to available exemptions under the Advisory Law, therefore a license with the Israel Securities Authority is

not required. Accordingly, Barclays does not maintain an insurance coverage pursuant to the Advisory Law.

Barclays Bank PLC in the Dubai International Financial Centre (Registered No. 0060) is regulated by the Dubai Financial Services Authority (DFSA).

Principal place of business in the Dubai International Financial Centre: The Gate Village, Building 4, Level 4, PO Box 506504, Dubai, United Arab Emirates.

Barclays Bank PLC-DIFC Branch, may only undertake the financial services activities that fall within the scope of its existing DFSA licence. Related financial

products or services are only available to Professional Clients, as defined by the Dubai Financial Services Authority.

Barclays Bank PLC in the UAE is regulated by the Central Bank of the UAE and is licensed to conduct business activities as a branch of a commercial bank

incorporated outside the UAE in Dubai (Licence No.: 13/1844/2008, Registered Office: Building No. 6, Burj Dubai Business Hub, Sheikh Zayed Road, Dubai

City) and Abu Dhabi (Licence No.: 13/952/2008, Registered Office: Al Jazira Towers, Hamdan Street, PO Box 2734, Abu Dhabi).

Barclays Bank PLC in the Qatar Financial Centre (Registered No. 00018) is authorised by the Qatar Financial Centre Regulatory Authority (QFCRA).

Barclays Bank PLC-QFC Branch may only undertake the regulated activities that fall within the scope of its existing QFCRA licence. Principal place of

business in Qatar: Qatar Financial Centre, Office 1002, 10th Floor, QFC Tower, Diplomatic Area, West Bay, PO Box 15891, Doha, Qatar. Related financial

products or services are only available to Business Customers as defined by the Qatar Financial Centre Regulatory Authority.

This material is distributed in the UAE (including the Dubai International Financial Centre) and Qatar by Barclays Bank PLC.

This material is not intended for investors who are not Qualified Investors according to the laws of the Russian Federation as it might contain information

about or description of the features of financial instruments not admitted for public offering and/or circulation in the Russian Federation and thus not

eligible for non-Qualified Investors. If you are not a Qualified Investor according to the laws of the Russian Federation, please dispose of any copy of this

material in your possession.

This material is distributed in Singapore by the Singapore branch of Barclays Bank PLC, a bank licensed in Singapore by the Monetary Authority of

Singapore. For matters in connection with this report, recipients in Singapore may contact the Singapore branch of Barclays Bank PLC, whose registered

address is 10 Marina Boulevard, #23-01 Marina Bay Financial Centre Tower 2, Singapore 018983.

This material is distributed to persons in Australia by either Barclays Bank PLC, Barclays Capital Inc., Barclays Capital Securities Limited or Barclays Capital

Asia Limited. None of Barclays Bank PLC, nor any of the other referenced Barclays group entities, hold an Australian financial services licence and instead

they each rely on an exemption from the requirement to hold such a licence. This material is intended to only be distributed to “wholesale clients” as

defined by the Australian Corporations Act 2001.

IRS Circular 230 Prepared Materials Disclaimer: Absa does not provide tax advice and nothing contained herein should be construed to be tax advice.

Please be advised that any discussion of U.S. tax matters contained herein (including any attachments) (i) is not intended or written to be used, and

cannot be used, by you for the purpose of avoiding U.S. tax-related penalties; and (ii) was written to support the promotion or marketing of the

transactions or other matters addressed herein. Accordingly, you should seek advice based on your particular circumstances from an independent tax

advisor.

© Copyright Absa Bank Limited (2017). All rights reserved. No part of this publication may be reproduced or redistributed in any manner without the prior

written permission of Absa. Absa Bank Limited is duly registered in South Africa Registration No. 1986/004794/06 Registered office Barclays Towers

West, 15 Troye Street, Johannesburg, 2001. Additional information regarding this publication will be furnished upon request.