sono26 - 26 units luxury townhomes in northern liberties, philadelphia

TRANSCRIPT

- A PLANNED COMMUNITY -

This project management presentation has been prepared by National Realty & Investment Advisors, LLC (“NRIA”) on the basis ofinformation obtained from NRIA and other public sources. It is believed to be reliable as of the specified date. NRIA does not undertakeany duty or obligation to update the information. NRIA does not make or give any representation, warranty or guarantee, whether expressor implied, that the information contained in this presentation or otherwise supplied to the recipient, at any time by or on behalf of NRIA whether in writing or not, relating to the property project discussed herein is 100% complete or 100% accurate or that it has been or will be audited or independently verified. Reasonable care has been taken in compiling, preparing and furnishing the information. Thispresentation provides a project management guide only and it is not intended to be exhaustive and, in particular, does not containdisclosure of any of the risks associated with the opportunity which you will find in your NRIA project management disclosures. Thispresentation is not to be construed as investment, tax or legal advice in relation to the relevant subject matter. You must seek your own legal or other professional advice.

This presentation contains statements that are forward-looking statements. These forward-looking statements, which are subject to risks, uncertainties and assumptions, include projections of future financial performance, anticipated growth strategies and anticipatedtrends in the business. These statements are only predictions based on current expectations and projections about future events,subject to change due to actual results, market conditions, performance and achievements. Any estimate or forecast contained in thispresentation is not a promise or representation by NRIA as to future matters and nothing contained in the information should be relied upon as a representation as to be guaranteed. NRIA guarantees your satisfaction with your project only. See your 100% Money BackGuarantee for details.

Executive Summary

Property Description

Area Overview

Comparable Properties

The Market

Investment Requirement

1

2

3

4

5

6

TABLE OF CONTENTS

EXECUTIVESUMMARY1

Experience the excitement of SoNo26 – 26 groundbreaking luxury townhomes with garage & dedicated parking and common

park in Philadelphia’s Northern Liberties – a perpetually “up-and-coming” neighborhood that has permanently arrived. This former

manufacturing district fi rst started turning heads in the early ‘90s, when a progressive, artist-heavy fl ock, lured by cheap studio space,

began migrating north from Old City. Our high ceilings, large windows, and hardwood fl oors evoke the industrial loft - a melding of

traditional warmth and contemporary urban living. All units enjoy a breathtaking common space and gourmet kitchen, equipped

with high-end stainless steel appliances and granite countertops. Feel free to entertain, relax, or unwind- our open fl oor plans are

suited for any mood and any occasion. Enjoy the view from your private roof deck, and pamper yourself in the master suite with its

walk-in closets and a spa-like master bath. We invite you to leave your car in your private garage or dedicated parking space - with

direct access to bus and train routes, community gardens, and shopping centers, you will rarely need it. Welcome to Northern Liberties,

welcome to SoNo26.

SoNo26 embraces the commingling of like-minded residents and a quirky network of bars, restaurants and boutiques within

neighborhood limits (Girard Avenue and Callowhill Street north and south, the Delaware River and Sixth Street east and west).

Already a hotbed of enviro-friendly construction, Northern Liberties’ value was further boosted by the additions of Liberties Walk and

the Piazza at Schmidts, ambitious mixed-use complexes that reimagined overlooked industrial bones. Long established as a force,

Northern Liberties has become an economic and cultural infl uence on the neighborhoods around it.

SoNo26 – A Planned Community

EX

EC

UT

IVE

SU

MM

AR

Y

PROPERTYDESCRIPTION2

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Exterior Rendering

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Interior Rendering

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Media Room Rendering

PR

OP

ER

TY

DE

SC

RIP

TIO

N

First Floor Living Room Rendering

PR

OP

ER

TY

DE

SC

RIP

TIO

N

First Floor Dining Room Rendering

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Second Floor Rendering

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Third Floor Master Suite Rendering

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Roof Deck and Pilot House Suite Rendering

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Kitchen Rendering

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Living Room Rendering

PROPOSED SITE PLAN

TO BE DEMOLISHED

Proposed Site Plan

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Floor Plan – Type A (9 Units)

Floor Plan – Type B (13 Units)

PR

OP

ER

TY

DE

SC

RIP

TIO

N

3-STORY — 38’-0” HUNITS 1-9

FOOTPRINT: 833 SF (1ST FLOOR)

2ND FLOOR DECKPILOT HOUSE AND ROOF DECKPART FINISHED BASEMENT W/MEDIA ROOMPRIVATE DRIVE AND GARAGE

GFA: ±2,015 SF

TOTAL GROSS USEABLE AREA:± 2,389 SF (W/ BASEMENT)± 218 SF GARAGE± 153 SF 2ND FLOOR DECK± 560 SF ROOF DECK

± 3,779 TUA3 BR + 3.5 BATH

3-STORY — 38’-0” HUNITS 10-22

FOOTPRINT: 704 SF (1ST FLOOR)

REAR YARDPILOT HOUSE AND ROOF DECKPART FINISHED BASEMENT W/MEDIA ROOMPRIVATE DRIVE + PARKING SPACE

GFA: ±2,232 SF

TOTAL GROSS USEABLE AREA:± 2,936 SF (W/ BASEMENT)± 84 SF ROOF DECK

± 3,520 TUA3 BR + 3.5 BATHS

Floor Plan – Type C (3 Units)

Floor Plan – Type D (1 Unit)

PR

OP

ER

TY

DE

SC

RIP

TIO

N

3-STORY — 38’-0” HUNITs 23-25

FOOTPRINT: 750 SF (1ST FLOOR)

REAR YARDPILOT HOUSE AND ROOF DECKPART FINISHED BASEMENT W/MEDIA ROOMPRIVATE DRIVE + PARKING SPACE

GFA: ±2,370 SF

TOTAL GROSS USEABLE AREA:± 3,120 SF (W/ BASEMENT)± 630 SF ROOF DECK

± 3,750 TUA3 BR + 3.5 BATHS

3-STORY — 38’-0” HUNIT 26

FOOTPRINT: 720 SF (1ST FLOOR)

REAR YARDPILOT HOUSE AND ROOF DECK PART FINISHED BASEMENT W/MEDIA ROOMPRIVATE DRIVE + PARKING SPACE

GFA: ±2,280 SF

TOTAL GROSS USEABLE AREA:± 3,000 SF (W/ BASEMENT)± 600 SF ROOF DECK

± 3,600 TUA3 BR + 3.5 BATHS

Standard Building Specifi cations• Water tight 9’ high concrete walls in basement• Brick façade with metal, cement board, wood, or stucco siding• Off street parking (see site plan if appliacble)• Fiberglass roof deck and 100+ SF pilot house suite

(see site plan if applicable)• 3+ bedrooms • Minimum 2.5 bathrooms• Upper fl oor laundry room (if permits)• Finished basement/ media room (if no garage)• Energy effi cient dual zone hvac systems• Wood stairs with stained risers and treads• 10 year tax abatement pending

Foundation• Concrete foundations, cast-in-place basement walls and

basement slab• Footings and foundation walls built with reinforced bars

(REBAR)• Continuous vapor barrier under basement slab• Waterproof coating applied to foundation walls• Sump pump & pit in basement with French drain around

perimeter of basement

Exterior siding• Flashings and caulking as necessary to provide water-tight

system• Brick façade with metal, cement board, wood, or stucco siding• All exterior wall surfaces shall receive “home wrap”

HVAC• Dual zone HVAC• Duct-work and exterior venting for bathroom exhaust fans • Duct-work & exterior venting for dryer venting provided

Windows• Vinyl “geld-wyn” or equal

Drywall and paint• 5/8” gypsum wallboard on all locations• Double 5/8” drywall in garage• All drywall, trim, baseboard, casing to be painted with low VOC

paint. All white paint throughout

Electrical• 200 amp electrical service• Decora outlets and switches per code• Recessed lights throughout• Smoke detectors & carbon monoxide detectors hard-wired

per code• Recessed lights throughout - 6” in main house & bedrooms,

low voltage in bathrooms• Most closets lighted• Exhaust fans in each bathroom • Lighting package provided on roof & exterior

Insulation• Exterior walls on 2nd & 3rd fl oor - R19• Exterior walls on ground fl oor - R19• Roof insulation - R38

Building Specifi cations – Overall

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Plumbing• Kohler toilets, tubs, and bath fi xtures Grohe bath fi xtures

and faucets• Gas HVAC system, hot water heater, dryer and oven• Public water/sewer service• Drain, waste and vent piping• Sump pump• 75 gallon Bradford White gas hotwater heater• Garbage disposal on all kitchen sinks• Cast iron waste lines• Pex water system• French drain in basement

Roofi ng• Fiberglass roofi ng• Aluminum fl ashings, roof edging, gutters and downspouts as

required

Rough carpentry• 2 X 12 or TGI wood joists for fl oor framing and roof framing• Advantec sub-fl ooring shall be 3/4” tongue and groove• Zip wall system (or similar material) sheathing on exterior walls• Sub-fl ooring shall be glued to fl oor trusses with low VOC

adhesive• Demising partitions shall be 2” x 6” wood studs, 16” on center

with 5/8” zip wall system on the exterior surface and 5/8” dry-wall on the interior

• Front and rear exterior partition walls shall be 2” x 6” wood studs, 16” on center

• Interior partition walls shall be 2” x 4” wood studs, 16” on center

Finish carpentry• 5 1/4” Flatstock baseboards• 3 1/2” Flatstock door and window casing• Fully enclosed stairs, hardwood treads and risers• Modern style, brushed nickel lever handles and locksets

Building Specifi cations – Overall

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Building Specifi cations – Kitchen & Living Rooms

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Living Room• 4”-5” x 1/2” engineered fl ooring • 9’ 0”+ ceilings• Phone, cable and internet ready• 5 1/4” baseboard moulding• Recessed lights (6”)

KitchenGranite or manufactured quartz counters • Stainless steel appliances - Bosch appliance package• 3/4 HP garbage disposal• Recessed lights (6”)• Ultra Craft custom cabinetry with self close draws and

contemporary stainless hardware• 5 1/4” baseboard moulding• 9’ 0” + ceilings• 4”-5” X 1/2” engineered fl ooring • Tile backsplash

Powder Room• Tiled fl oors • Mirror over vanity• Ceiling exhaust fan

Dining Room• 4”-5” X 1/2” engineered fl ooring • 9’ 0”+ ceilings• 5 1/4” baseboard moulding• Recessed lights (6”)• Ceiling pendant light junction box

Building Specifi cations – Secondary Bedroom Levels

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Hallway• 4”-5” X 1/2” engineered fl ooring • 5 1/4” baseboard moulding• 8’ 0”+ ceilings• Recessed lights (6”)

Laundry/Mechanical Room• Full sized washer/dryer units - front or top loading• Tile fl ooring and baseboards (4” high)• Recessed lights (6”)• Custom cabinetry where applicable

Bedroom #1 - Front• 4”-5” X 1/2” engineered fl ooring 8’ + ceilings • Walk in closet with white laminate shelving and lighting• Phone, cable and internet ready• Recessed lights (6”)• Ceiling fan junction box

Full Bathroom Including: • Ultra Craft custom cabinetry with self close draws and

contemporary stainless hardware w/ marble or quartz tops• Tiled fl oors and baseboard (4” high)• 5’ drop in tub with tile to ceiling• Mirror over vanity (or medicine cabinet)• Ceiling exhaust fan (Panasonic or equal ultra quiet)• Recessed lighting

Bedroom #2- Rear• 4”-5” X 1/2” engineered fl ooring • 8’ + ceilings• Walk in closet with white laminate shelving and lighting• Phone, cable and internet ready• Recessed lights (6”)• Ceiling fan junction box

Full Bathroom Including: • Ultra craft custom cabinetry with self close draws and

contemporary stainless hardware w/ marble or quartz tops• Tiled fl oors and baseboard (4” high)• 5’ drop in tub with tile to ceiling or shower• Mirror over vanity (or medicine cabinet)• Ceiling exhaust fan (Panasonic or equal ultra quiet)• Recessed lighting

Linen Closet• White laminate shelving

Building Specifi cations – Master Bedroom Level

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Master Bathroom• Ultra craft custom cabinetry with self close draws and

contemporary stainless hardware w/ marble or quartz tops• 9’ + Ceilings• Ceiling exhaust fan • Custom tile shower with frameless glass enclosure• Overhead rain shower, ceiling & handheld shower heads• Mirrors over vanities (or medicine cabinet) • 6” Recessed lighting

Hallway• 4”-5” X 1/2” engineered fl ooring • 5 1/4” Baseboard moulding• 9’+ Ceilings• Recessed lights (6”)

Linen Closet• White laminate shelving

Master Bedroom• 4”-5” X 1/2” engineered fl ooring • 5 1/4” baseboard moulding• 9’+ ceilings• Up to 2 walk-in closets with built in shelving system-white

(if layout permits)• Phone, cable and internet ready• Recessed lights (6”)• Junction box for ceiling fan

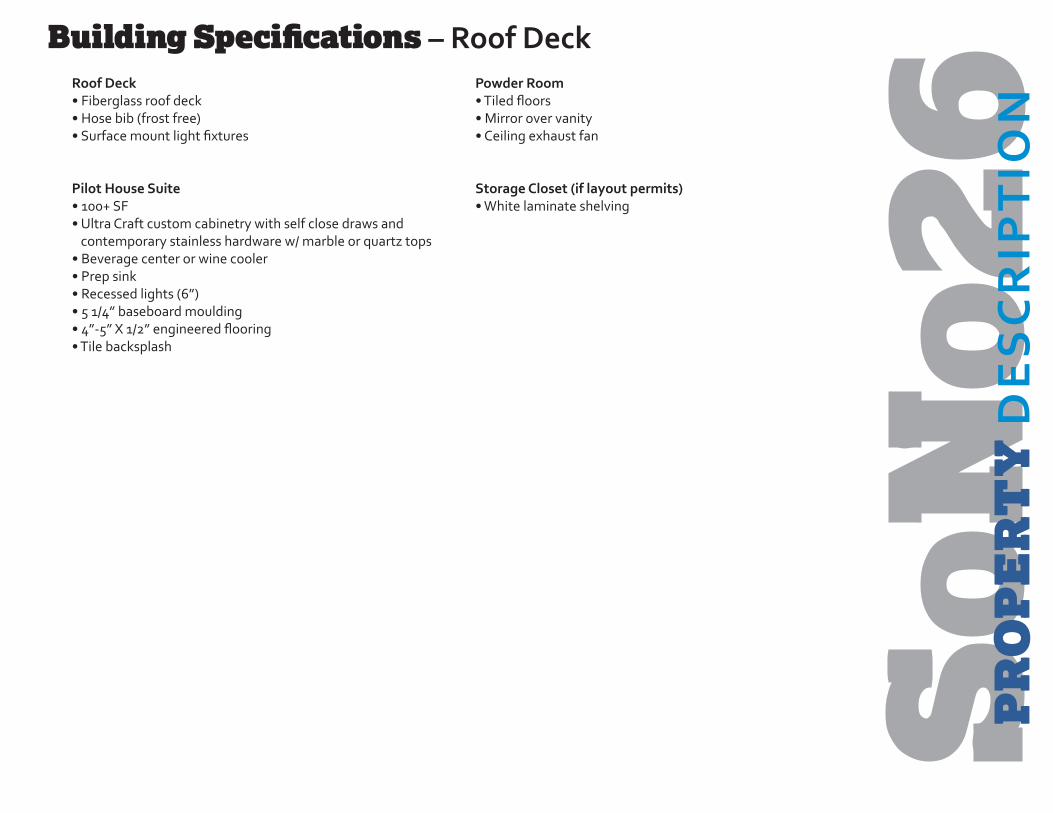

Building Specifi cations – Roof Deck

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Roof Deck• Fiberglass roof deck• Hose bib (frost free)• Surface mount light fi xtures

Pilot House Suite• 100+ SF• Ultra Craft custom cabinetry with self close draws and

contemporary stainless hardware w/ marble or quartz tops• Beverage center or wine cooler• Prep sink• Recessed lights (6”)• 5 1/4” baseboard moulding• 4”-5” X 1/2” engineered fl ooring• Tile backsplash

Powder Room• Tiled fl oors • Mirror over vanity• Ceiling exhaust fan

Storage Closet (if layout permits)• White laminate shelving

Building Specifi cations – Basement

PR

OP

ER

TY

DE

SC

RIP

TIO

N

Basement - Main Room/ Media Room• Fully carpeted or tiled• Phone, cable and internet ready• 5 1/4” baseboard moulding

Powder Room (if applicable)• Porcelain tile fl ooring and baseboards (4” high)• Mirror over sink• Ceiling exhaust fan (Panasonic or equal ultra quiet)• Single vanity with granite or quartz countertop

AREAOVERVIEW3

Philadelphia is the largest city in the Commonwealth of Pennsylvania and the fi fth largest metropolitan area in the United States with over eight million residents. As the second most powerful city on the East Coast after New York, Philadelphia serves as thebusiness capital of Pennsylvania and one of the most important economic and cultural hubs in the country. The City is ideally situated 100 miles from New York City and 140 miles from Washington, DC, strategically located in the epicenter of the wealthiest corridor in the United States.

Philadelphia:The 5th Largest Metropolitan Area in the United States

AR

EA

OV

ER

VIE

W

Northern Liberties, formerly known as a an industrial & manufacturing hub is a neighborhood of great current signifi gance inCentral Philadelphia. The neighborhood extends from Girard Avenue to Callowhill Street and from North 6th Street to the banks of the Delaware River. Northern Liberties was in existence long before the city of Philadelphia had even been established. Its name comes from “Northern Liberties Township,” which appeared in local legislature from the 1770s. By 1854, it was annexed to the district of Philadelphia, allowing Philadelphia to surpass Baltimore as the second largest city in the United States. Being located outside of the bustling city allowed Northern Liberties to thrive industrially. Many manufacturing mills, factories, and plants produced the tools and commodities needed within the city. By the 19th century, many Immigrants began to populate this area. Their heritage can still be seen today in the areas numerous and highly varied churches. In 1985, the area was declared as a historic district that is nowdedicated to preserving the Italianate, Greek Revival, and Federal style buildings that characterize the area. Today Northern Liberties is a beautiful community with close to 4,500 residents and known for its eclectic and “hip” collection of restaurants, shops, and art galleries.

Area Overview

AR

EA

OV

ER

VIE

W

Subject PropertySoNo26

Northern Liberties:Neighborhood Boundaries

AR

EA

OV

ER

VIE

W

AR

EA

OV

ER

VIE

W

Philadelphia:Diversifi ed EconomyPhiladelphia’s economy has undergone a dramatic transformation from its traditional manufacturing base to one driven by a variety of industries, with a special emphasis on the healthcare and higher education sectors. Philadelphia is home to 98 hospitals and more than 90 institutions of higher education, which employ more than 580,000 highly educated professionals across the region. ThePhiladelphia Metropolitan Area is also home to nine Fortune 500 companies, including AmerisourceBergen, Aramark, Campbell Soup Company, Comcast,Crown Holdings, E.I. du Pont de Nemours, and Lincoln National, among others. In 2013, these nine companiesgenerated in excess of $249 billion in annual revenues, representing nearly 67% of the Philadelphia Metropolitan Area’s grossmetropolitan product (GMP).

The city’s large and diversifi ed economy has helped generate a GMP of $364 billion, one of the highest in the United States. As of August 2014, the Philadelphia Metropolitan Area’s unemployment rate stood at 6.7%, lower than major U.S. cities such as Atlanta,Chicago, and Los Angeles. More recently, Philadelphia’s fast-growing biomedical and pharmaceutical industries have brought 14major pharmaceutical fi rms and nearly 100 biotech fi rms to the area. Eight of the world’s largest pharmaceutical companies arelocated within a 50-mile radius of Philadelphia, including Astra Zeneca, Bristol-Myers Squibb, GlaxoSmithKline, Janssen Biotech,Merck, and Novo Nordisk. Philadelphia is also one of the top 15 markets in the U.S. for venture capital investment with nearly $350 million of committed capital across 105 diff erent investments.

Within a 5-hour drive of 25% of the U.S. population• State-of-the-art international airport within a two-hour fl ight of half of the U.S. population

• Amtrak’s 30th Street Station serves nearly 4.2 million riders per year and off ers high-speed trains to New York,Washington, DC, and Boston

• SEPTA has the 6th largest rapid transit system by ridership in the country

• Home to 98 hospitals and over 90 institutions of higher education

• Headquarters of 9 Fortune 500 Companies with revenue of over $249 billion

• CHOP expected to add ~500 full-time doctors, researchers and other employees

• Penn Health gearing up for $1.5 billion hospital expansion, nearly doubling bed count

AR

EA

OV

ER

VIE

W

Philadelphia:Home to the Nation’s Leading Universities

Philadelphia’s educational leadership began in 1740 with the founding of one of the country’s fi rst universities, the Ivy League, world-class University of Pennsylvania. Over 250 years later,the region is home to leading universities specializing inbiotechnology, business, fi nance, medicine, and technology,which produce highly skilled graduates that continue tostimulate Philadelphia’s economy. Philadelphia is also home to fi ve nationally recognized schools of medicine, including Drexel University College of Medicine, Philadelphia College ofOsteopathic Medicine, Temple University School of Medicine,Jeff erson Medical College, and the Perelman School of Medicine at the University of Pennsylvania.

• Second highest number of four-year colleges in the countryafter New York, with more than 90 degree-granting institutions

• The second largest student population of any city on the East Coast, with approximately 368,000 students and more than 66,000 graduates each year

• Highly educated workforce with more than 75% of Center City residents holding at least a Bachelor’s degree

• Drexel University strategic plan to increase student population by 10,405 students by 2021 and full time employees by 4,119 during same period.

• 32,000 students downtown with an additional 54,000 acrossthe Schuylkill River in University City

AR

EA

OV

ER

VIE

W

Center City:Impressive Population GrowthCenter City has experienced the largest and most geographicallyconcentrated growth in Philadelphia. Since 2000, the CenterCity core population has grown by more than 24% driven by apersistent migration of young, urban professionals seeking to live in an amenity-rich, urban mixed-use environment. By comparison,the core Center City population growth since 2000 has exceededthat of major cities,including Boston (7.5%), San Francisco (6.2%), and New York (5.4%). Center City has one of the highest concentrations of residents with post-secondary education in the United States: in 2000, nearly 68% of Center City’s residents held at least a Bachelor’s Degree. By 2013, the fi gure had grown to more than 75%.This incredible population growth, particularly among educated residents, has contributed to a boom in multifamilydeliveries. Since 2000, approximately 2,100 multifamily units have been delivered in Center City.

As the third largest downtown population in the US (behind NYC and Chicago), Philadelphia is ranked as one of the most walkable/ bikeable cities in America. The Center City neighborhoodepitomizes this trend (scoring 98 for each) – refl ecting the newgeneration of renters favoring walkable, urban neighborhoods. Within Philadelphia, Rittenhouse Square boasts the highestpedestrian traffi c counts in the city ( approximately 23,000 people per day), and is especially pedestrian-oriented.

• Over 61% and 63% of residents in a one-mile radius of Walnut and Chestnut, respectively, take alternative means of transpor-tation to work, far exceeding the national average of 19%.

This trend is being further encouraged by the City of Philadelphia,which is revealing a new Bike Share program this fall. With aninitial rollout of 150 to 200 stations and over 2,000 bikes to be spread across the city over the next year, anticipated ridership is around 500,000 trips annually by 2015, with local use anticipated to surpass 2.5 million trips per year over the fi rst six years of opera-tions. The growing role of bicycles in Philadelphia will increase the dynamism and connectivity of the market, signifi cantly expanding the pedestrian count in Rittenhouse Square and Society Hill.

Center City: By the Numbers• 288,500 jobs, or 44% of Philadelphia’s total workforce,

with a total purchasing power of $13 billion

• Most diversifi ed workforce in the region with the offi cesector generating 31% of all jobs

• 305,000 daily commuters with SEPTA recording a 10.2%and 13.1% increase for subway and bus routes, respectively, into downtown over the last decade

• 409 cultural institutions as well as 14 colleges / universities and 5 hospitals

• 2nd nationally behind only Manhattan in the number of downtown art and cultural institutions

• More than 3,200 retail establishments, 11,300 hotel rooms, and 37.5 million square feet of Class A offi ce space

• 24.2% population growth from 2000 to 2013

• The adjacent University City is one of the nation’s preeminenteducation, health, and R&D nodes with UPenn, Drexel, and CHOP, creating a signifi cant opportunity for Philadelphia’s two largest employment centers to further integrate and drive growth for the region

AR

EA

OV

ER

VIE

W

The Comcast Innovation and Technology Center:A Key Center City Growth DriverComcast has broken ground on a $1.2 billion (or $800 PSF),1,121-foot skyscraper at 1800 Arch Street in late 2014. Designed by world-renowned architect Lord Norman Foster, Comcast’snew tower will become the tallest building in the city and willaccommodate the company’s rapid growth, as Comcast expects to add approximately 3,000 employees from around the country. The project is expected to create 6,300 temporary construction related jobs and an additional 14,400 jobs in Pennsylvania, and bring an abundance of talent to the region, making Philadelphia a central hub for broadcasting and technology.

SoNo26 is ideally positioned to benefi t from the delivery of the Comcast Center. Even though its one dozen blocks east, SoNo26 will be a unique residential alternative to capture Comcast-relatedresidential growth, while providing a contrasting historicalaesthetic to the ultra-modern and high-tech vertical offi ce campus.

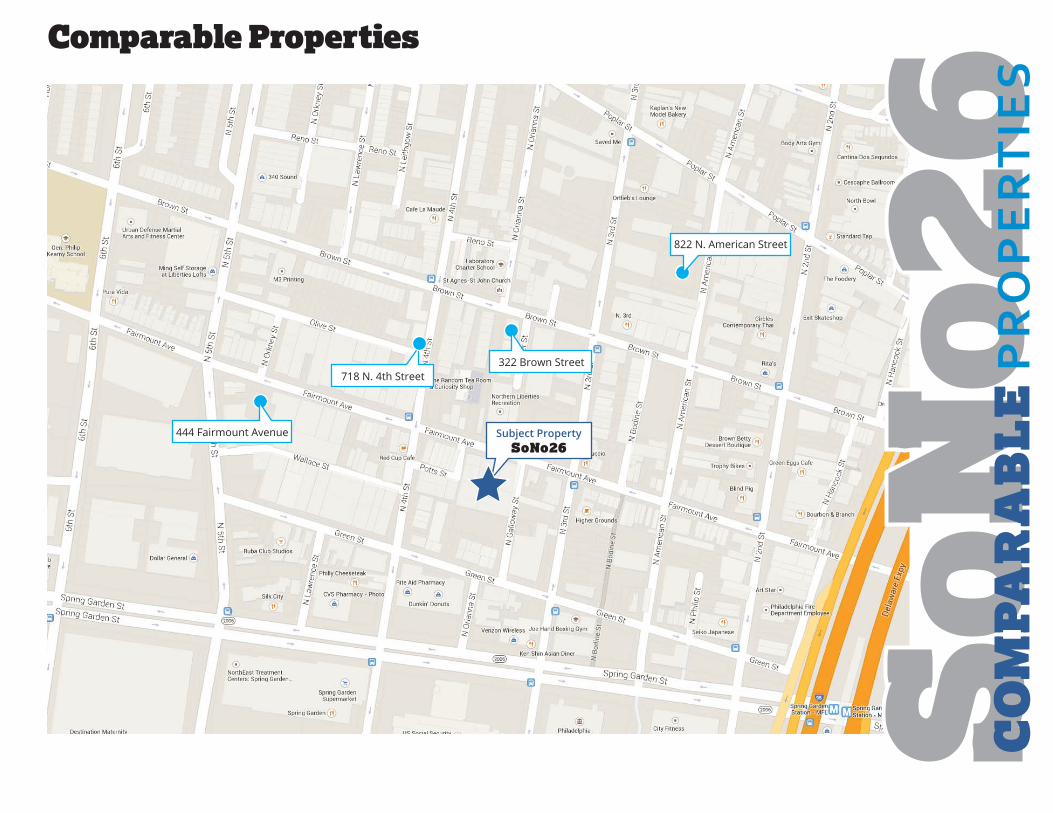

COMPARABLEPROPERTIES4

CO

MP

AR

AB

LE

PR

OP

ER

TIE

S

Comparable Properties

Subject PropertySoNo26

444 Fairmount Avenue

718 N. 4th Street322 Brown Street

822 N. American Street

Comparable Sale # 1

322 Brown Street, Unit A, Philadelphia, PA

Sale Date: 12/05/2014 Sale Price: $835,000

Comparable Sale # 2

718 N. 4th Street, Philadelphia, PA

Sale Date: 12/03/2014 Sale Price: $750,000

Comparable Properties

CO

MP

AR

AB

LE

PR

OP

ER

TIE

S

Comparable Sale # 3

310 Fairmount Avenue, Philadelphia, PA

Sale Date: 07/29/2014 Sale Price: $749,900

Comparable Sale # 4

822 N. American Street 3, Philadelphia, PA

Sale Date: 9/30/2015 Sale Price: $1,050,000

Comparable Properties

CO

MP

AR

AB

LE

PR

OP

ER

TIE

S

THEMARKET5

In recent weeks, we’ve been covering news of Philly’s fl ourishing housing boom and rising home values. Now, we might soon add offi ce properties to that increase: Finance & Commerce reports the city has hit a sweet spot in offi ce demand with sales doubling to $1.4 billion:

Real estate values approaching or surpassing peak levels in New York, Boston and Washington have buyers turning to Philadelphia for its higher yields, rising rents and falling vacancies. That’sbolstering offi ce deals in the fi fth-largest U.S. city at a time when Manhattan-like towers have opened with luxury condominiumsand cable operator Comcast Corp. is developing a skyscraperthat will be the area’s tallest.

The website adds that this boom in demand could be part of larger“Philadelphia renaissance” attributed to local university graduates “sticking around instead of leaving for jobs in other cities,” asBob Walters, CBRE Group’s executive managing director, put it.

A recent study by City Observatory backs this idea withfi ndings that show young college grads spur on economicand neighborhood revitalization.

As a result of all this, real estate investors’ growinginterest has prompted landlords to cash out:

About $400 million of offi ce buildings are for sale within afour-block radius in the Market Street West district ofdowntown that is being marketed by Jones Lang LaSalle,said Doug Rodio, a broker at the company.

Philly Hits Sweet Spot in Offi ce Space DemandBy Angelly Carrion | October 22, 2014 | http://www.phillymag.com

TH

E M

AR

KE

T

The city best known for Rocky, cheese steaks and sharp-elbowedsports fans is developing a new reputation as a nexus of oil and gas transportation, which bodes well for its economy.

With little fanfare, Philadelphia is undergoing a revolution powered by the U.S. energy renaissance. Renewed investment and activity in the region’s sprawling railway network and aging infrastructure is turning the City of Brotherly Love into a potential energy hub that some believe can rival Houston.

Energy experts cite two major factors working in Philly’s favor: it’sproximity to the booming Marcellus Shale, where 5,400 shale wells churned out nearly 2 trillion cubic feet of natural gas during the fi rst six months of the year; and the city’s bustling commercial railroad system, which has made it a transit point for oil being shipped from NorthDakota’s Bakken formation.

Along the Northeast corridor, “there are maybe six distribution pipeline proposals for natural gas,” said Vincent Devito, a law partner atBoston-based Bowditch & Dewey. “A lot is intended for exports andthe quickest and easiest way is through Philadelphia’s infrastructure.”

Devito, a former Department of Energy offi cial, said the city is already a draw for gas and energy related businesses “that like to be close to the pipeline for easy access,” he said. “Philly is in a fortunate spot because they are part of the Northeast corridor, there’s a lot of business and remarkable opportunities for business and economic development.”

Most recently, Philadelphia’s profi le in the energy sector got a large boost from Sunoco Logistics Partners, a pipeline investment vehicle that announced it would construct a $2.5 billion pipeline from the Marcellus into Philly. The new pipeline will complement an existing gas artery that may hike the region’s natural gas transport by fourfold.

With the U.S. experiencing an embarrassment of fossil fuel riches, Sunocoand other companies are channeling billions into pipeline investment across the country. As local rail companies like Monroe Energy negotiatefor increased access to Bakken crude, Philadelphia is one of severalregions that stands to benefi t from the infl ux of oil and gas.

“Philly has physical infrastructure, land and access to export markets, or you can transport [natural gas] to other markets in the U.S.,” said Adam Karpf, a portfolio manager at Atlantic Trust, which has $24 billion in assets under management.

The new Houston?

TH

E M

AR

KE

T

Oil, natural gas surge makes Philadelphiathe new energy hotspotTom DiChristopher | Javier E. David | November 16, 2014http://www.cnbc.com

Once it’s up and running, Sunoco Limited’s pipeline will funnel nearly 300,000 barrels per day of natural gas liquids (NGL) to Philadelphia’s Marcus Hook Industrial Complex.

The city is not what most would normally consider an energy hub.Traditionally, oil and gas production has taken place in locationsfurther south, like Houston and New Orleans.

However, the U.S. energy boom has upended many of those assumptions,transforming unlikely cities into hubs of fossil fuel production. Combined with a set of refi neries that are being retrofi tted for natgas purposes, Philadelphia could eventually rival energy powerhouses in Texas and Louisiana, some energy watchers say.

“Houston is not as close to the demand centers as Philadelphia is. The East Coast is an amazing engine of demand,” said Michael Krancer, chair of the energy industry practice at Blank Rome law fi rm.

The city’s 8.4 percent unemployment rate is well above the nationalaverage, and even above Pennsylvania’s. Many of the cities and states that are ground zero for shale production have seen jobless rates plummet. For that reason, energy watchers are reasonably optimistic that Philly can see some of the same magic other oil and gas producing regions have experienced through the shale boom.

Energy development in the region can help stem a brain drain ofeducated professionals out of the area, Krancer added.

“The potential is even greater than Houston,” he said. “The parts of the state that are benefi ting the most from this are the parts of the state that have been economically challenged for a generation or two.”

TH

E M

AR

KE

T

Oil, natural gas surge makes Philadelphiathe new energy hotspotTom DiChristopher | Javier E. David | November 16, 2014http://www.cnbc.com

One morning in August, Philadelphia’s deputy mayor for economicdevelopment, Alan Greenberger, was headed to the groundbreakingfor a new mixed-use complex near the city’s Art Museum. Theproject will include nearly 300 luxury apartments and a Whole Foods.On his way there, he stopped at the construction site for a luxuryapartment building on a busy central corridor, Chestnut Street.

Greenberger had come to take part in an announcement with theAssociated General Contractors of America, who had just rankedPhiladelphia metro region number three in the number of construction jobs added.

“I’ve been here now, this September, this will be my 40th year inPhiladelphia,” he told assembled architects and dignitaries. He saidhe’d been discussing this the day before with a local developer.“Neither of us can remember, in our lifetimes in this city, a construction boom of this magnitude.”

A whole lot of those workers are building housing.

Construction job numbers have been rising in about two-thirds ofU.S. metro areas tracked by the general contractors’ associationover the past year, and most of the top regions are located in southern states — with housing a major driver throughout the country. In 2012,Philadelphia’s Center City District (CCD), an economic development non-profi t, calculated that developers had completed 463 residential units in central Philadelphia. In 2014, the CCD estimated, that number could soar to 2,600. Most of it will be luxury and mid-market housing, with monthly rents above the city’s average.

Who’s Moving to Center City Philadelphia?The short version: Most of the people who will occupy these new homes and apartments will fall into two growing Philadelphia demographics. They’re the young and employed, and those nearing or over retirement age.

The urban aspirations of young professionals and empty nesters,“isn’t stuff we talk about generally, this is a very specifi c relationship,” Greenberger told me recently. Young people in particular, specifi cally those 25 to 34, he says, “want to be here because they can the live city life they want, can get to work, and it’s more aff ordablethan other cities.”

TH

E M

AR

KE

T

Is Philadelphia in a Housing Bubble?By Emma Jacobs | Next City | October 6, 2014

TH

E M

AR

KE

T

An upscale housing market driven by millennials may soundcounterintuitive. After all, headlines about the generation’s struggles abound. However, Steve Mullin says that in a metro region with sixmillion residents, it doesn’t take too many people changing theirbehavior to result in market shifts. That is to say, the suburbs don’t have to empty out for the city to require new housing. Mullin, president of Econsult Solutions, adds that “for 50 years, Philadelphia basically hadno new, quality housing.”

Normally, he says, people move into more expensive housing as theirincome improves, freeing up better housing to the next income level until structures in the worst condition get demolished, and he didn’t see that happening in Philadelphia, for years.

“What’s going on in Center City is causing it to expand outward,” says Victor Pinckney, vice president of the Homeowners Association ofPhiladelphia. He’s focused on rehabbing homes in Philadelphianeighborhoods north and northwest of Center City.

Banks are lending again, he says. “Two years ago, three, I tried to do a refi nance and it wasn’t going nowhere. A year and a half later they were trying to throw money at me. Nothing had changed on my end.”

Will the Market Break?Mullin thinks Philadelphians are natural pessimists about theirlong-suff ering economy. “It’s a very Philadelphia thing to say,‘how can we support two water ice stands?’”

Greenberger notes there’s some natural anxiety that comes with aconstruction boom.

“Boom cycles end,” he acknowledges, but “do they just sort of retreat back to some sort of manageable level or do they bust?” In this case, he thinks the strength of the city’s other sectors make it unlikely the fl oor would fall out of the housing market.

Brad Doremus of realty data tracking fi rm Reis says the metro’s vacancy rate fell from 4.4 percent at the close of 2011 to 3.3 percent as ofmid-2014, and the market seems ready to absorb new units throughthe end of the year.

“Past 2014, new construction is projected to outpace net absorptionon an annual basis for a few years,” he added, but, “this is not a bigworry — the market’s long-term average vacancy (since 1980) isaround 4.6 percent so it isn’t a surprise that it would begin slowlymoving up again.”

When the CCD presented its fi gures in March, President Paul Levyidentifi ed two potential market constraints: the Philadelphia school district’s funding crisis and the pace of job growth.

“To the extent that … people are unsure about schools in everyneighborhood, that’s going to limit people’s willingness to stayor buy homes within the city,” he says.

In an update two weeks ago, he told me, “Every indicator we have seen, as well as discussions with lenders and developers, suggests that the demand remains strong for the new units that are coming on line.”

Is Philadelphia in a Housing Bubble?By Emma Jacobs | Next City | October 6, 2014

House hunters in Philadelphia today might want to channel their innerRocky. It will take a good fi ght to fi nd the right property at the rightprice. Inventory in the city proper was down 10 percent in Septemberfrom a year ago, while the median price, $158,000, was up nearly thesame, according to the Berkshire Hathaway HomeServices Fox & RoachHomExpert Market Report.

The closer in to the city center, the higher that median price rises.

“I have sold more homes this year within the fi rst day or two or three that it goes on the market because there is such a shortage. If something shows nicely and is priced right, there will be multiple bids, and it will sell right away,” said Mike McCann, a real estate agent with Fox & Roach.

Closed sales are up just 2.4 percent from a year ago, and signed contractsare down 13 percent. Homes are also selling nearly 5 percent faster than a year ago. Demand is coming from what McCann calls “meds and eds” — growing demand from the city’s many hospitals and universities.

After falling in the last decade, Philadelphia’s population has rebounded since 2010, putting ever more pressure on housing. Comcast, owner of NBCUniversal, parent company of CNBC and CNBC.com, is building a second tower in the city, which is creating spinoff jobs in the downtown, especially for young millennials. Downsizing baby boomers are also adding to Philadelphia’s new residents.

“They want to be in town. This is the fi rst time we’ve had growth in the city. The downtown marketplace has been expanding dramatically. There are a lot of renovations of old neighborhoods that are being fi xed up and new construction. The market has expanded because of the shortage of inventory,” added McCann.

Helping the growth is a 10-year tax abatement for new construction. That is adding new product to parts of South Philadelphia andKensington. The center core is spreading farther, and retail andrestaurants are following suit. T

HE

MA

RK

ET

Why Philly homebuyers needto channel inner RockyBy Diana Olick | cnbc.com | October 15, 2015

TH

E M

AR

KE

T

Renters Struggle to Find Available UnitsBy Robert Greenberg | B2R Finance

As the country gains more renters, the demand for aff ordable rentals is outstripping supply.

Real estate investors who are able to provide aff ordable rental housing should have no problem fi nding tenants in many of the country’s major metropolitan areas, according to a joint research project about renting from New York University’s Furman Center and Capital One, whichindicated the need for aff ordable rentals is growing.

According to the study, the number of major U.S. cities with a majority renter population rose from fi ve to nine, from 2006 to 2013. Further, more than 50% of the population rents in these nine cities: Boston,Chicago, Dallas, Houston, Los Angeles, Miami, New York, San Franciscoand Washington, D.C., according to Furman. Miami had the highest share of renters as of 2013 — 65 percent — but Boston, L.A., and New York had 60 percent or more as well.

Even as rental stock rose in each of the 11 cities studied, it didn’t match the pace of growth in the rental population, with the exception ofAtlanta.

Nine of the 11 cities saw double-digit growth in renters, and fi vesaw growth exceeding 20 percent — Philadelphia, Miami, Boston,Washington, D.C., and San Francisco.

The center noted that rents rose faster than household incomes in fi ve of the cities. This issue was most noticeable in Los Angeles and New York. In Los Angeles, gross rent rose 11 percent while incomes fell 4 percent between 2006 and 2013. In New York, gross rent rose 12 percent and incomes had no growth. Conversely, incomes grew faster than rents in three cities: Boston, Chicago and Houston.

With the exception of Dallas and Houston, the average renter ineach metropolitan area could not aff ord the majority of recentlyavailable rental units in his or her city. Even in the most aff ordablecities, low-income renters could aff ord less than a tenth of theavailable rentals. Rent is considered to be ‘aff ordable” when itcomprises less than 30 percent of household income.

Since 2006, there has been an increase in the share of low- andmoderate-income renters who are severely rent-burdened — facingrent and utility costs equal to at least half of their income.

Lack of aff ordability coupled with growing demand were key themesof the study.

To be sure, real estate investors who are able to provide aff ordablerental housing in any of these 11 cities likely will see high demand for their properties.

For more than half a century, suburban growth surpassed growth in cities — in both population and job growth — but that is changing.

We’ve heard for several years now that the Millennial Generation prefers to live in city centers and close to their place of employment. Now we are beginning to hear about jobs moving back into city centers from suburban environments.

For the real estate investor, this trend could open up opportunities for a robust return on investment in housing located close to the urban core in cities around the nation.

The country’s largest metropolitan areas are recording faster job growth downtown — in the city core — than areas located further from the city center, according to research by the think tank City Observatory, which analyzed census data.

City Observatory looked at what occurred between 2007 to 2011 and compared urban cores to their peripheral areas. It defi nes a city center as the area within 3 miles of the center of each region’s central business district.

In city centers, jobs grew at a 0.5 percent annual rate, but in thesurrounding peripheral portion of metropolitan areas jobs declined 0.1 percent per year. City centers out-performed the surrounding areas for job growth in 21 of the 41 metropolitan areas examined.

As recently as 2002-2007, peripheral areas were growing much faster (1.2 percent annually) and aggregate job growth was stagnant in urban cores (0.1 percent).

The strength of city centers appears to be driven by a combination ofthe growing attractiveness of urban living, and the relatively stronger performance of urban-centered industries (business and professional services, software) relative to decentralized industries (construction, manufacturing) in this economic cycle.

Many companies have announced that they are moving to or expanding operations in city centers, in large measure to take advantage ofthe growing number of younger workers living in close-in urbanneighborhoods.

THE EFFECT ON HOUSING

City centers often play a unique role in the local housing market. They generally have the highest density of housing, and the proximity toservices and employment is valued by some high-income households and households without cars. Often the housing located right in the city core is in the form of high-rise condominiums and apartment buildings, which can be expensive.

More moderately priced single-family housing can often be foundclose-by, however. In some cities, older, depreciated housing in or close to the center is the most aff ordable for low- and moderate-income households. B2R Finance believes that these moderately priced homes very close to the city center could hold potential as acquisition targets for single-family rental investors.

This proximity to employment and other amenities can provideopportunities for lower and moderate-income citizens to enjoy the convenience of living near city centers. These homes, as rental property investments, also hold potential for rental growth and strong occupancy levels as the demand for urban housing grows in many metropolitan areas nationwide.

TH

E M

AR

KE

T

Housing Demand Rises in and Near CentralBusiness DistrictsBy Robert Greenberg | B2R Finance

Want double-digit returns and rents that soar more than 10 percent a year? It’s possible for the savvy real estate investor. A new report just released by RealtyTrac identifi es 20 markets with the potential to deliver returns of more than 15% and several over 20% during Q1 2015.

Plenty of good options still exist for single-family residential rentalinvestors in many U.S. counties, according to a recent report, analyzing U.S. single-family housing data. Investors can use the data to look at specifi c markets that have strong and growing populations ofMillennials, Gen-Xers, and Baby Boomers.

Single-family residential rental properties are expected to bring in an average return of 9.05 percent during the fi rst quarter of 2015, but 20 individual markets show the promise of returns of more than 15 percent.

Two counties in Georgia — Clayton and Bibb — show potential annual gross yields of 25.83 percent and 22.33 percent, respectively, the highest of 516 counties analyzed. Clayton County is located in the Atlanta metro area, while Bibb County is in the Macon, Ga. metro area.

Baltimore and Richmond off er potential annual gross yields of more than 20 percent and yields surpass 17 percent in the following counties: Wayne (Detroit metro area); Philadelphia; Pasco and Hernandocounties (Tampa, Fla., metro area); Oswego (Syracuse, N.Y.) andWyandotte (Kansas City metro area).

Baltimore County also holds the distinction as the county with the highest annual average cash fl ow — $13,770 — for a leveraged investor. Philadelphia County (in the Philadelphia metro area) and Clayton County (Atlanta metro area) round out the top three counties with the highest average annual cash fl ow for the leveraged investor of $12,048 and $11,352 respectively.

Although the rental returns forecast in some counties may beeye-popping, the risks may be high was well. An investor shouldcertainly weigh those risks carefully by conducting thorough duediligence. Most of the counties in the top 20 for the highest gross rental yields also had unemployment rates above the national average, which could translate into renters having trouble paying the rent. This could suggest that investors may see more evictions in these counties than in other, more economically stable markets and possible higher than normal vacancies as well.

The Best Places to Buy Single-Family Rentalsin Q1 2015By Robert Greenberg | B2R Finance

TH

E M

AR

KE

T

In a contributing article to Next City, Emma Jacobs reports that Phila-delphia could be in the midst of an unprecedented housing boom. The growth spurt is evident throughout the city, which was ranked in third place by the Associated General Contractors of America in a list of metro regions who saw a rise in construction jobs.

“Neither of us can remember, in our lifetimes in this city, a construction boom of this magnitude,” said deputy mayor of economic development Alan Greenberger during the announcement.

According to Jacobs, the Center City District estimated that in 2012,developers had constructed 463 residential units in the area. The CCD now predicts developers could build up to 2,600 residential units, most of which would be luxury and mid-market housing, this year. Victory Pinckney of the Homeowners Association of Philadelphia added that “what’s going on in Center City is causing it to expand outward.”

But how long could this housing bubble last? Here’s more from Next City:

[Steve] Mullin [of Econsult Solutions] thinks Philadelphians arenatural pessimists about their long-suff ering economy. “It’s avery Philadelphia thing to say, ‘how can we support two waterice stands?’”

“Boom cycles end,” he acknowledges, but “do they just sort ofretreat back to some sort of manageable level or do they bust?”In this case, he thinks the strength of the city’s other sectors makeit unlikely the fl oor would fall out of the housing market.

Jacobs writes that realty tracking fi rm Reis says “[e]very indicator we have seen, as well as discussions with lenders and developers, suggests that the demand remains strong for the new units that are coming on line.”

Photo credit: Flickr user Jeanette Runyon.

TH

E M

AR

KE

T

Philly Housing is Having a Growth SpurtBy Angelly Carrion | October 27, 2014 | http://www.phillymag.com

INVESTMENTREQUIREMENT6

FINANCED PURCHASE 25% DOWN & REFI 5/1 Arm @ 3.75%

Construction Overview Estimates:

Gross Living Interior: 2,080 SF 4th Story Entertainment Suite

No. of Bedrooms: 3 4th Story Roof Top Deck

No. of Bathrooms: 3.5 Bosch Appliances & Grohe Fixtures Package

Finished Basement: Yes w/Media Room or Basement w/Media Room

New HVAC CAC: Yes 3,274 Useable Square Footage

New Water Service: Yes 1 Car Garage or Dedicated Parking Space

New Gas Service: Yes Units 1-9 Garage & Units 10-26 Parking Space

New Electric Service: Yes

Financial Summary Estimates:

Land Purchase Price: $187,308

New Construction: $435,000

Closing & Initial Project Management: $23,500

Total Cost Amount: $645,808

After Built Value (ABV/ARV): $815,000

ASAP Built In Equity Profi t:ASAP Built In Equity Profi t: $169,192$169,192

Equity Overview312 Fairmount Avenue, Philadelphia, PA 19123UNITS 1-26

INV

ES

TM

EN

T R

EQ

UIR

EM

EN

T

Equity Overview312 Fairmount Avenue, Philadelphia, PA 19123UNITS 1-26

INV

ES

TM

EN

T R

EQ

UIR

EM

EN

T

CASH REQUIRED:

• $11,900 = Retainer…DUE NOW!

• $161,000 = (25% Deposit)…Parked at Land Closing

• 29,814 = Construction Loan Payments…Paid over Build

• TOTAL CASH-IN = $202,714

LOANS:

• $611,250 = Refi nance loan amount

• $484,808 = Construction loan amount

CASH-OUT at REFINANCE:

• $126,442 = CASH BACK TO YOU!

• Net cash to own this property is ONLY = $76,272

($202,714 - $126,442 = net cash to own)

RENT ECONOMIC BENEFITS:

• $1,824 per year estimated positive cash fl ow + $12,348 annual paydown of your mortgage = $14,172 annual economic benefi t from rents:

• $14,172/$76,272 (Cash Flow + Principal Pay Down/ Cash In) = 18.5%Return

Your Gross StartingEQUITY = $203,750

For Resale

Assumptions Annual Growth

Property Info

Purchase Price $187,308

Construction $435,000

Closing Costs $23,500

Total Purchase $645,808

Appraised Value $815,000 2.00%

Built-in Equity $169,192

Annual Taxes $1,020 0.00% Closing Costs $23,500

Annual Insurance $1,000 0.00%

Property Mngt Fee $50 Total Initial Investment $11,900

Loan Info (refi )

Mortgage Type Full Cash Out

Mortgage Term 30

Interest Rate 3.750% Loan to Value % Asap 120-180 Cash Out $0

Closing Cost as % 3.00% 75.00%

First Mort % $611,250

Second Mort % – Equity Remaining $203,750

Second Mort Int Rate 0.000% % Equity Remaining 25.00%

Other Info Amount Annual Growth

Rents $3,300.00 3.00%

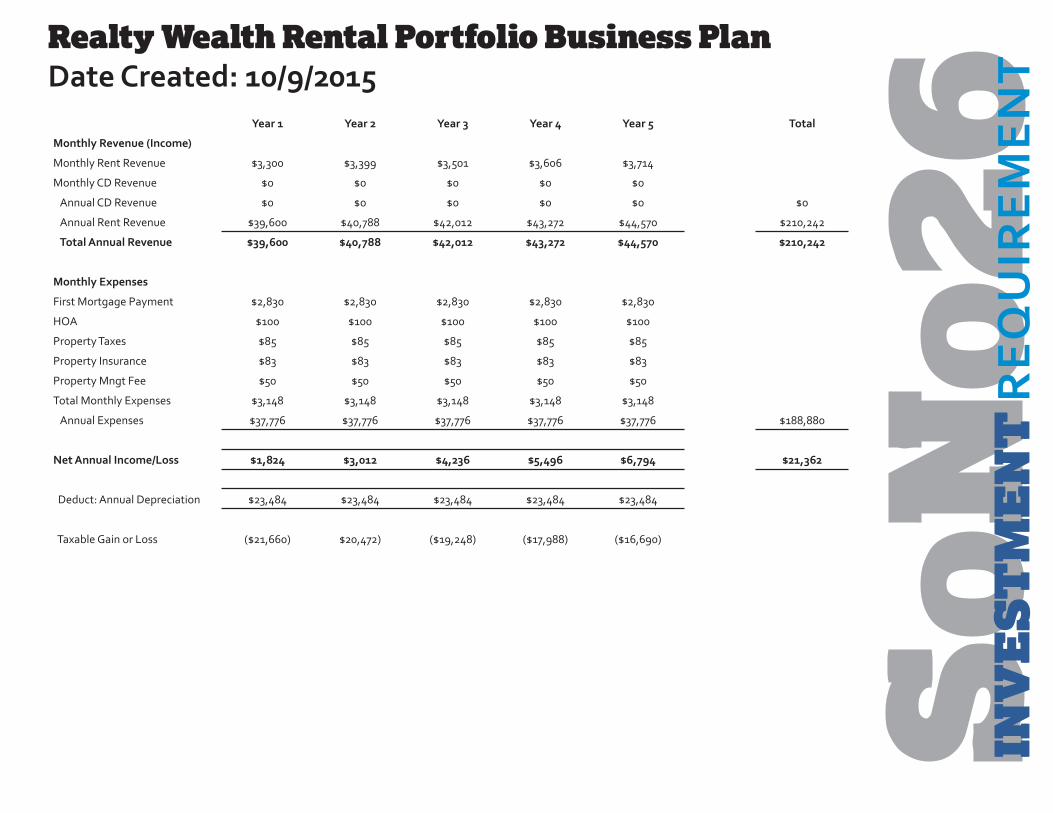

Realty Wealth Rental Portfolio Business PlanDate Created: 10/9/2015

INV

ES

TM

EN

T R

EQ

UIR

EM

EN

T

Year 1 Year 2 Year 3 Year 4 Year 5 Total

Monthly Revenue (Income)

Monthly Rent Revenue $3,300 $3,399 $3,501 $3,606 $3,714

Monthly CD Revenue $0 $0 $0 $0 $0

Annual CD Revenue $0 $0 $0 $0 $0 $0

Annual Rent Revenue $39,600 $40,788 $42,012 $43,272 $44,570 $210,242

Total Annual Revenue $39,600 $40,788 $42,012 $43,272 $44,570 $210,242

Monthly Expenses

First Mortgage Payment $2,830 $2,830 $2,830 $2,830 $2,830

HOA $100 $100 $100 $100 $100

Property Taxes $85 $85 $85 $85 $85

Property Insurance $83 $83 $83 $83 $83

Property Mngt Fee $50 $50 $50 $50 $50

Total Monthly Expenses $3,148 $3,148 $3,148 $3,148 $3,148

Annual Expenses $37,776 $37,776 $37,776 $37,776 $37,776 $188,880

Net Annual Income/Loss $1,824 $3,012 $4,236 $5,496 $6,794 $21,362

Deduct: Annual Depreciation $23,484 $23,484 $23,484 $23,484 $23,484

Taxable Gain or Loss ($21,660) $20,472) ($19,248) ($17,988) ($16,690)

Realty Wealth Rental Portfolio Business PlanDate Created: 10/9/2015

INV

ES

TM

EN

T R

EQ

UIR

EM

EN

T

Realty Wealth Rental Portfolio Business PlanDate Created: 10/9/2015

INV

ES

TM

EN

T R

EQ

UIR

EM

EN

T

Year 1 Year 2 Year 3 Year 4 Year 5 Total

Economic Impact

Net Annual Rent Income/Loss $1,824 $3,012 $4,236 $5,496 $6,794 $21,362

Year-end Property Value $831,300 $847,926 $864,885 $882,182 $899,826

Annual Increase to Prop Value $16,300 $16,626 $16,959 $17,298 $17,644 $84,826

less: Total Deferred Interest $0 $0 $0 $0 $0 $0

Tax Rate

add: Tax Benefi t 36% $7,798 $7,370 $6,929 $6,476 $6,008 $34,581

Equity Remaining $203,750

Net Economic Gain $344,518

5 Year Economic Benefi t5 Year Economic Benefi t $344,518$344,518

Return on initial $11,900 InvestmentReturn on initial $11,900 Investment 2,895%2,895%

Note: Actual results will vary based upon bank margin, realty appreciation, index interest rates, and actual investment rates. Past performance is not a guarantee of future results. See your disclosure documents reviewed and closing documents for loan details. See your tax and investment advisors for actual tax savings and investment review. This illustration does not include tax, investment, or legal advice. For concept illustration purposes only.