solid assets ‒ solid earnings - bmo global asset...

TRANSCRIPT

For professional investors only

Solid assets ‒ solid earnings

Marcus Phayre-Mudge

Head of Property Equities

Guy Glover

Manager, F&C UK Property Fund

Marcus Phayre-Mudge

Head of Property Equities, lead manager of

the TR Property Trust and F&C Global Real

Estate Securities Fund

Guy GloverManager, F&C UK Property

Fund

Introduction

2

Paul Myles

Director, Sales & Client

Relationships

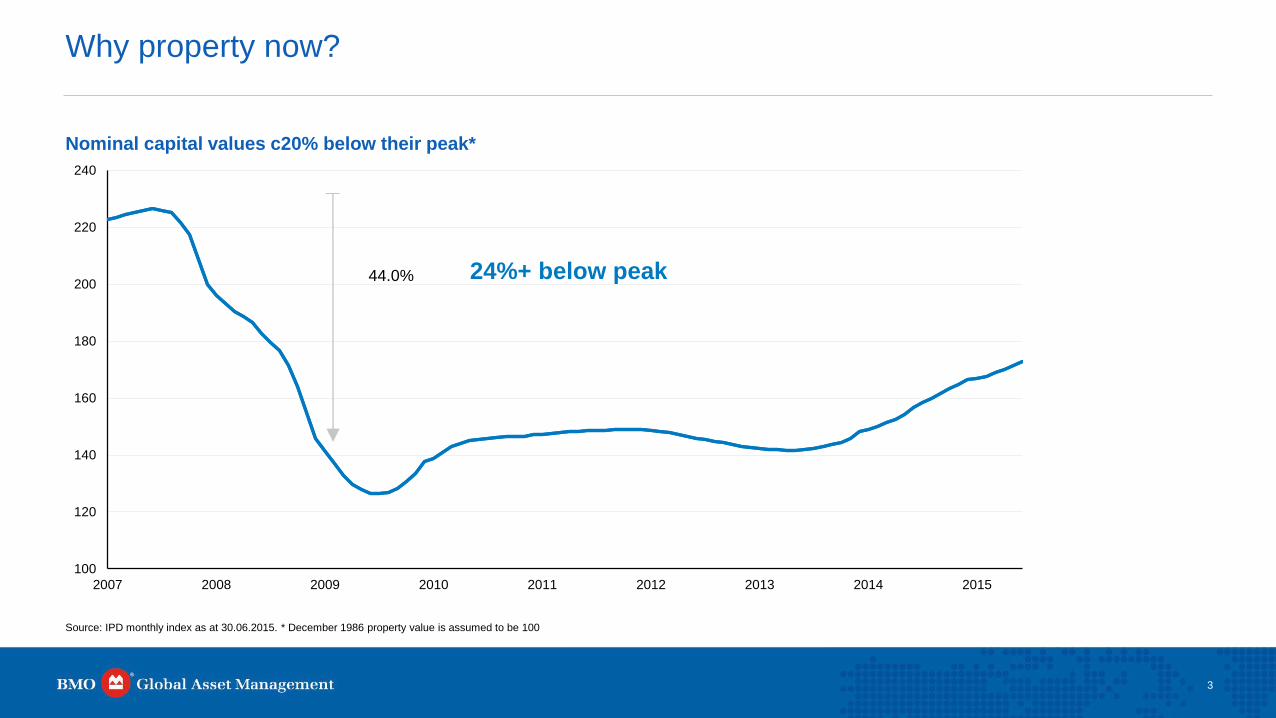

100

120

140

160

180

200

220

240

2007 2008 2009 2010 2011 2012 2013 2014 2015

Nominal capital values c20% below their peak*

Why property now?

3

44.0% 24%+ below peak

Source: IPD monthly index as at 30.06.2015. * December 1986 property value is assumed to be 100

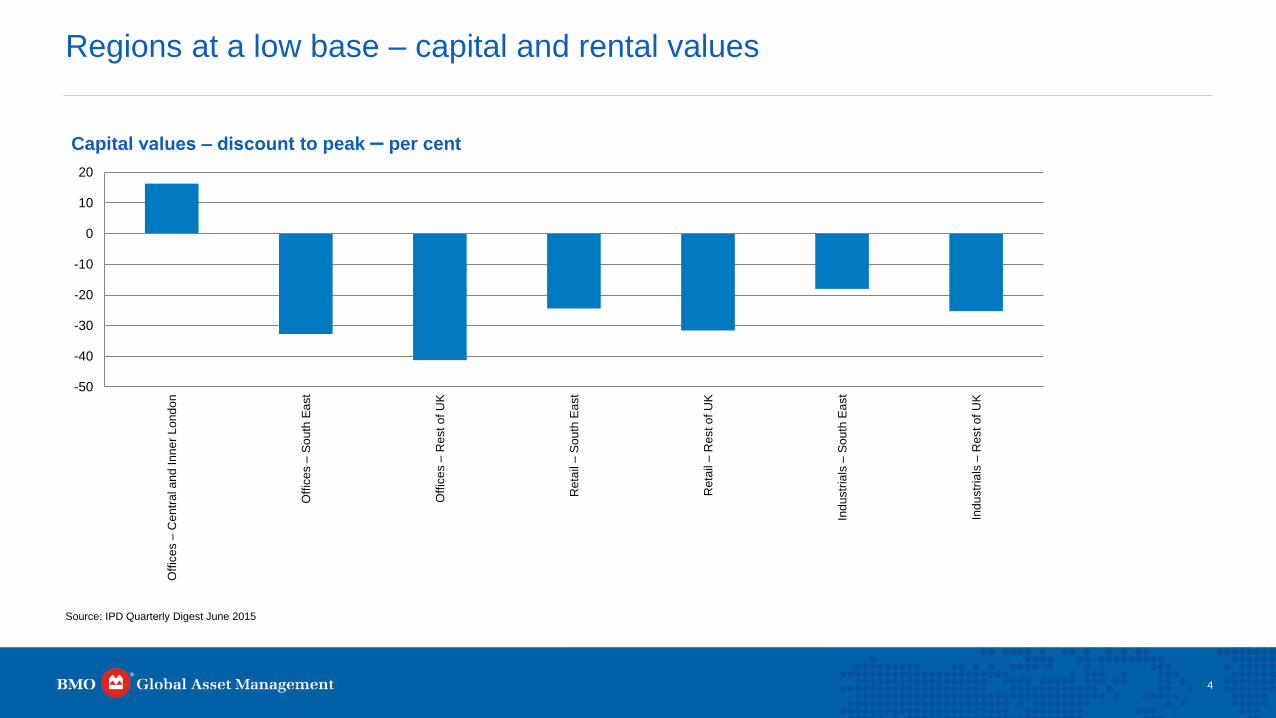

Regions at a low base – capital and rental values

4

-50

-40

-30

-20

-10

0

10

20O

ffic

es –

Cen

tra

l a

nd

In

ne

r L

on

do

n

Off

ice

s –

So

uth

Ea

st

Off

ice

s –

Rest o

f U

K

Reta

il –

So

uth

Ea

st

Reta

il –

Rest o

f U

K

Ind

ustr

ials

–S

ou

th E

ast

Ind

ustr

ials

–R

est o

f U

K

Capital values ‒ discount to peak ‒ per cent

Source: IPD Quarterly Digest June 2015

5.9

0.5

2.0

3.9

3.7

0

1

2

3

4

5

6

7

8

9

10

Jan 00 Jul 01 Jan 03 Jul 04 Jan 06 Jul 07 Jan 09 Jul 10 Jan 12 Jul 13 Jan 15

%

IPD UK Monthly Index Income Return UK base rates 10 year gilts IBOXX £ Corporate Bond Index FTSE 100 Income Return

Why property now?

5

Source: IPD monthly index, Datastream as at 30.06.2015. FTSE International Limited (“FTSE”) © FTSE 2015.

Income return January 2000 – May 2015 (%)

Property vs. gilt yield

6

Source: Thomson Datastream, IPD, Capital Economics

Bps – basis points

All-Property Initial Yields Less 10-Year Gilt Yields (Bps) (1993-2019) (Latest = May 15)

EPRA dividend yields vs. corporate bond yields

BBB yield vs. EPRA dividend yield

0

1

2

3

4

5

6

Aug 12 Dec 12 Apr 13 Aug 13 Dec 13 Apr 14 Aug 14 Dec 14 Apr 15

%

Source : Investment Property Databank (IPD), Bloomberg. Data as at 31.07.2015

FTSE EPRA/NAREIT Developed Europe Index Div Yield

FTSE Euro Corporate BBB average Yield

2014 (A) 2015 (E)

Earnings Yield* 4.2% 4.7%

Dividend Yield* 3.1% 3.7%

*Source: Internal Model. Data as at 31.08.2015. FTSE International Limited (“FTSE”) © FTSE 2015

(A) = Actual; (E) = Estimate

Estimates and forecasts are provided for illustrative purposes only. They are not a guarantee of future performance and should not be relied upon for any investment decision.

Estimates are based on assumptions and subject to change without notice.

7

Listed real estate delivering competitive returns

8

Source: Novelinvestor as at 31.12.2014. http://novelinvestor.com/investing/15-year-look-asset-class-sector-country-returns/

UK direct property market outlook

9

Comparative forecasts - total returns - end 2014-19 per cent per annum

Sources: BMO Real Estate Partners, Property Market Analysis (PMA), Real Estate Strategies (RES), IPF and Capital Economics (Cap Econ) as at 07.07.2015

*All industrials

Note: Estimates and forecasts are provided for illustrative purposes only. They are not a guarantee of future performance and should not be relied upon for any investment decision.

Estimates are based on assumptions and subject to change without notice.

BMO REP PMA Cap Econ RES IPF

Standard retail 8.0 6.9 8.5 8.4 7.0

Shopping centres 6.3 5.4 7.8 6.7 7.1

Retail warehouses 6.6 5.4 9.9 5.2 7.2

City offices 8.9 6.2 8.5 7.8 6.7

West End offices 9.8 5.3 8.4 8.1 6.6

South Eastern offices 9.9 6.5 11.9 7.3

Rest of UK offices 7.4 6.5 11.3 5.1

Standard industrials 7.4 7.4* 9.7* 7.5 8.2*

Distribution 7.8 6.4 7.5

All property 7.8 5.9 9.4 7.1 7.5

Offices - June 2013 Offices – March 2015

UK Property annual rental growth - offices

10

Key: Green >2%, Orange 0 to +2%, Red <0%

Source: BMO Real Estate Partners, IPD

Land securities – NAV (net asset value) and share price

11

Source: BMO Global Asset Management, Datastream, Exane BNP Paribas, as at 28.08.2015

Estimates and forecasts are provided for illustrative purposes only. They are not a guarantee of future performance and should not be relied upon for any investment decision.

Estimates are based on assumptions and subject to change without notice.

0

500

1000

1500

2000

2500

Mar 91 Mar 93 Mar 95 Mar 97 Mar 99 Mar 01 Mar 03 Mar 05 Mar 07 Mar 09 Mar 11 Mar 13 Mar 15 Mar 17

Pence

NAV Estimated NAV Share price

Central London – development profile

12

0

2

4

6

8

10

12

14

16

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

Completed U/C Let/Under Offer U/C Available Proposed Let/ Under Offer Proposed Available

10 year average take up

12.5m sq. ft.

Central London vacancy rate – 3.7%

Source: CBRE 31.12.2014

U/C – Under Construction

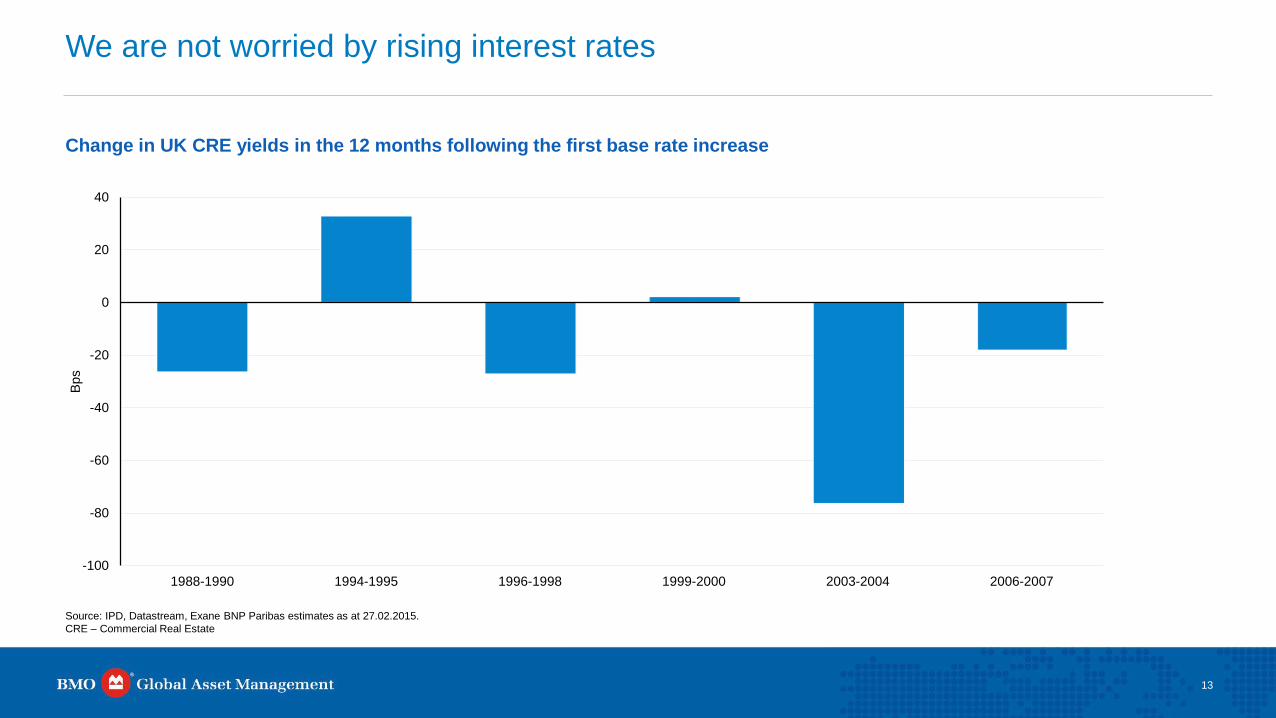

Change in UK CRE yields in the 12 months following the first base rate increase

We are not worried by rising interest rates

13

-100

-80

-60

-40

-20

0

20

40

1988-1990 1994-1995 1996-1998 1999-2000 2003-2004 2006-2007

Bps

Source: IPD, Datastream, Exane BNP Paribas estimates as at 27.02.2015.

CRE – Commercial Real Estate

Macro has dominated the sector in the past year

14

Relatively well insulated from emerging market risk

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Basic

Resou

rce

s

Foo

d &

Be

ve

rage

s

Pers

onal &

Hou

se

hold

Goo

ds

Ch

em

ica

ls

Techn

olo

gy

Industr

ial G

oo

ds &

Se

rvic

es

Oil

& G

as

Banks

Auto

s &

Part

s

Telc

om

s

Fin

ancia

l S

erv

ices

Co

nsum

er

& M

ate

rials

Re

tail

He

althcare

Insu

rance

Me

dia

Tra

vel &

Leis

ure

Utilit

ies

Re

al E

sta

te

Source: Datastream, Exane BNP Paribas estimates, September 2015

15

0

500

1000

1500

2000

2500

Dec 98 Dec 00 Dec 02 Dec 04 Dec 06 Dec 08 Dec 10 Dec 12 Dec 14

FT

SE

EP

RA

/NA

RE

IT D

evelo

ped I

ndex

US REIT performance during past Fed rate hikes

Past Fed rate

hike periods

Source: Bloomberg. Data as at 31.08.2015.

16

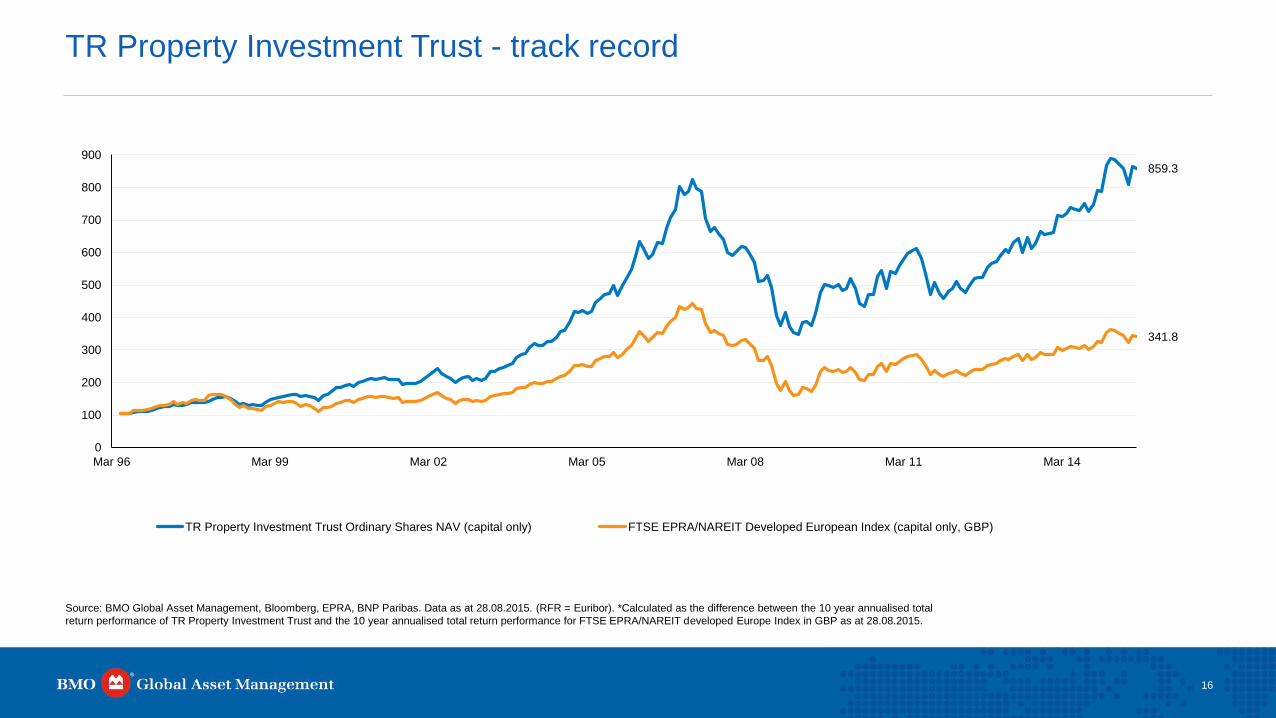

TR Property Investment Trust - track record

Source: BMO Global Asset Management, Bloomberg, EPRA, BNP Paribas. Data as at 28.08.2015. (RFR = Euribor). *Calculated as the difference between the 10 year annualised total

return performance of TR Property Investment Trust and the 10 year annualised total return performance for FTSE EPRA/NAREIT developed Europe Index in GBP as at 28.08.2015.

859.3

341.8

0

100

200

300

400

500

600

700

800

900

Mar 96 Mar 99 Mar 02 Mar 05 Mar 08 Mar 11 Mar 14

TR Property Investment Trust Ordinary Shares NAV (capital only) FTSE EPRA/NAREIT Developed European Index (capital only, GBP)

• Since inception, the fund has

produced a +101% total return.

+34% of alpha (net of all fees)

outperforming its benchmark in 19

out of 21 quarters

• Annual outperformance of 3.8%.

Information ratio of 2x

Alpha (excess return vs. benchmark) since launch*

17

F&C Real Estate Securities Fund:Outperformed in 19 out of 21 quarters since launch

Source: BMO Global Asset Management. Data as at 28.08.2015

*NAV of F&C Real Estate Securities fund (B GBP Acc) net of all fees vs. FTSE EPRA/NAREIT Developed Europe Capped Index TR (Net of Withholding Tax) GBP.

-2%

3%

8%

13%

18%

23%

28%

33%

38%

Apr 10 Aug 10 Dec 10 Apr 11 Aug 11 Dec 11 Apr 12 Aug 12 Dec 12 Apr 13 Aug 13 Dec 13 Apr 14 Aug 14 Dec 14 Apr 15 Aug 15

BMO REP – IPD monitored performance

18

BMO REP IPD-managed funds, if aggregated into a hypothetical single ‘house’ fund, has

outperformed the benchmark on a 1, 3, 5 and 10 year basis

Source: IPD as at 30 June 2015. ¹ BMO Real Estate Partners IPD monitored products

1 Year 3 Years 5 Years 10 Years

BMO REP house returns¹ 16.6% 12.9% 10.8% 7.4%

Percentile rank 39th 32nd 24th 19th

Benchmark (IPD Quarterly Universe) 15.7% 12.2% 10.2% 6.0%

Sector analysis Geographic analysis

F&C UK Property Fund geographic and sector analysis

19

Standard Retail13.0%

Retail Warehouse

28.5%

Offices36.1%

Industrial18.9%

Leisure3.6% Rest London

13.3%

South East34.0%

South West11.0%

Eastern3.8%

East Midlands1.8%

West Midlands12.2%

York / Humber9.7%

North West4.3%

Scotland10.0%

Source: BMO Real Estate Partners. Data as at 30.06.2015

Factors affecting the forecasts

20

• Domestic

‒ Timing and extent of interest rate normalisation

‒ Concerns about impact of EU referendum vote (BREXIT)

‒ Banks (and others), are lending again - £45bn in 2014

‒ What happens when the assets sold off in loan packages are marketed?

• External factors

‒ Subdued Eurozone GDP growth, ECB quantitative easing an unknown.

The Eurozone debt crisis is not over

‒ Oil price falls, possible deflation

‒ Geo-political considerations, Russia, emerging markets, China, Middle

East, Ukraine

‒ US – timing of interest rate rises

PMA predicts that a “BREXIT” scenario

would reduce UK all property total

returns by 3 percentage points per

annum in five years to 2019

– Central London offices especially

vulnerable to correction

Sources: De Montfort Survey May 2015, Property Market Analysis June 2015 (PMA). GDP- Gross domestic product,

ECB- European Central Bank

BREXIT = British exit from the EU

Central London offices – further to run?

21

Sugar Building, EC4

“Overseas demand for prime assets in Central London remains exceptionally

strong with aggressive bidding pushing up prices. As more landlords are

attracted to the market by price rises, the additional stock should stimulate

further increases in transaction levels.” CBRE

95 Wigmore Street, W1

Conclusion

22

• UK commercial property has seen 3 years of double digit returns. Will it continue to

perform in 2015 and beyond and where will this performance come from?

‒ 2015/16 forecasts are positive

‒ Regional yield shift plus increasing rental growth

‒ Income

• Is it still a good relative buy compared to other asset classes?

‒ Aims of investor

‒ Fair value

‒ Underpinned by fundamentals

Past performance should not be seen as an indication of future performance. The value of investments and income derived from them can go down as well as up

as a result of market or currency movements and investors may not get back the original amount invested.

Disclaimer

Copyright © 2015, S&P Capital IQ (and its affiliates, as applicable). This may contain information obtained from third parties, including ratings from credit ratings

agencies such as Standard & Poor’s. Reproduction and distribution of third party content in any form is prohibited except with the prior written permission of the

related third party. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and

are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. THIRD

PARTY CONTENT PROVIDERS GIVE NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF

MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. THIRD PARTY CONTENT PROVIDERS SHALL NOT BE LIABLE FOR ANY

DIRECT, INDIRECT, INCIDENTAL, EXEMPLARY, COMPENSATORY, PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES, COSTS, EXPENSES, LEGAL

FEES, OR LOSSES (INCLUDING LOST INCOME OR PROFITS AND OPPORTUNITY COSTS OR LOSSES CAUSED BY NEGLIGENCE) IN CONNECTION

WITH ANY USE OF THEIR CONTENT, INCLUDING RATINGS. Credit ratings are statements of opinions and are not statements of fact or recommendations to

purchase, hold or sell securities. They do not address the suitability of securities or the suitability of securities for investment purposes, and should not be relied on

as investment advice.

FTSE International Limited (“FTSE”) © FTSE 2015. “FTSE®” is a trade mark of the London Stock Exchange Group companies and is used by FTSE International

Limited under licence. All rights in the FTSE indices and/or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for

any errors or omissions in the FTSE indices and/or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express

written consent.

24

Contact Us

BMO Global Asset Management (EMEA) - Head Office

Exchange House

Primrose Street

London EC2A 2NY

Tel: +44 (0) 20 7628 8000

bmogam.com

© 2015 BMO Global Asset Management. All rights reserved. BMO Global Asset Management is a trading name

of F&C Management Limited, which is authorised and regulated by the Financial Conduct Authority.

Extensive worldwide investment capabilities

• Total focus on clients

• Comprehensive range of products and solutions

• Defined expertise – including a suite of specialist

investment boutiques

• Scale and stability – our parent company is the

Bank of Montreal, one of Canada’s largest banks