second quarter 2013 earnings release - union pacific · second quarter 2013 earnings release july...

TRANSCRIPT

1

Second Quarter 2013 Earnings Release July 18, 2013 Jack Koraleski, CEO

2

2011 2012 2013

$1.59

$2.10

$2.37 All-Time

Qtrly Record

Second Quarter 2013 Record Results

+13%

Earnings Per Share Second Quarter Positives

• Best-Ever Quarter – Operating Revenue – Operating Income – Operating Ratio – Earnings

• Franchise Diversity

Challenges • Grain Volumes • International Intermodal

Volumes

3

Second Quarter 2013 Marketing & Sales Review July 18, 2013 Eric Butler, Executive VP – Marketing & Sales

4

Creating Customer Value

• Industry Leading Franchise • Strategic Investments

• Excellent Service

• Innovative Products

• Strong Relationships

5

Chemicals

Automotive

Agricultural

Second Quarter 2013 Recap Volume Growth

Freight Revenue Mix

Intermodal

TOTAL

Flat

+4%

-3%

-10%

Flat

-1%

+10%

Coal

Industrial Products

Agricultural 15% Autos 11%

Chemicals 17%

Coal 19%

Industrial 19%

Intermodal 19%

Volume ARC Freight Revenue

Freight Revenue Performance (Year-Over-Year Change)

-1%

+5% +5%

6

Agricultural Products Revenue $784M (-8%) Volume 209K (-10%) ARC $3,750 (+2%)

Quarterly Drivers • Limited Corn Supply in UP

Territory • Local Feeding of DDGS • Foreign Bans on U.S. Beef and

Pork

Volume Mix

*Volume in thousands of carloads and excludes equipment shipments

77.1 76.5

Grain Products*

2012 2013

-1%

59.8 57.8

Food & Refrigerated* -3%

2012 2013

Grain Products

36%

Grain 36%

Food/ Refrigerated

28%

78.1 60.6

Grain*

2012 2013

-22%

7

Intermodal Revenue $993M (-1%) Volume 822K (-3%) ARC $1,210 (+2%)

Quarterly Drivers

• Soft Import Volumes Impact International

• Highway Conversions Drive Domestic Growth

International 52%

Domestic 48%

Volume Mix 466.3

429.6

International*

2012 2013

380.1

391.8

Domestic*

2012 2013

*Volume in thousands of units

-8%

+3%

8

Automotive Revenue $534M (+12%) Volume 197K (+4%) ARC $2,715 (+8%)

Finished Vehicles

58%

Volume Mix

110.7 113.4

Finished Vehicles*

2012 2013

+2%

78.8 83.0

Auto Parts*

2012 2013

+5%

*Volume in thousands of carloads

Quarterly Drivers • Vehicle Sales Continue to Gain

Momentum • Strong Demand for Light Trucks • Variable Production at Key

Assembly Plants

Auto Parts 42%

9

Petroleum Products & LP Gas**

Chemicals Revenue $890M (+12%) Volume 287K (+10%) ARC $3,098 (+2%)

Volume Mix*

47.5 50.8

Fertilizer** +7%

2012 2013

33.7

46.9

Crude Oil** +39%

**Volume in thousands of carloads and excludes equipment shipments

Plastics 20%

Industrial Chemicals

22%

Petroleum & LP Gas

14% Fertilizer 18% Soda Ash

10%

Crude Oil 16%

* Beginning in 2013, Fertilizer includes Phos Rock and Sulfur; Soda Ash includes Sodium Products; Crude Oil separated from Petroleum & LPG

Quarterly Drivers • Continued Crude Oil Growth • Strength in Petroleum

Products & LP Gas • International Potash Demand

2012 2013 2012 2013

35.4 38.8 +10%

2012 2013

10

Coal Revenue $975M (+12%) Volume 414K (Flat) ARC $2,353 (+12%)

36.1 36.5

Southern Powder River Basin*

2012 2013

*Tons in millions

7.1 6.3

Colorado/Utah*

2012 2013

+1%

-11%

Southern Powder River Basin

74%

Other 13%

Volume Impact (Weekly Carloadings)

1Q 4Q

River Bas74%

27,000

31,000

35,000

39,000

43,000

47,000

2011

2012

2Q 3Q

Quarterly Drivers • Reduced Coal Stockpiles and

Higher Natural Gas Prices • Utility Outages • 2013 Contract Loss

2013

11

Industrial Products Revenue $977M (+7%) Volume 317K (Flat) ARC $3,079 (+6%)

Quarterly Drivers • Shale Drilling – Frac Sand • Housing Growth • Declines in Scrap Steel, Rock,

and Military Shipments

Volume Mix

*Volume in thousands of carloads

27.0 29.9

Lumber*

2012 2013

+11%

53.3 62.9

Non-Metallic Minerals*

2012 2013

+18%

2012 2013

12.2 10.1

Ferrous Scrap* -17%

Paper 9%

Gov’t/Waste 8%

Metals 19%

Minerals/ Consumer

23%

Construction 31%

Lumber 10%

12

Second Half 2013 Outlook Agricultural Products – Diminished 2012 Crops + 2013 Crop Projections Automotive + Auto Sales Growth Chemicals + Crude Oil + Most Other Markets Remain Solid Coal – Contract Loss + Dependent on Weather Industrial Products + Shale Drilling - Frac Sand + Housing & Construction Intermodal + Domestic Growth and Improved

International Peak

13

Second Quarter 2013 Operations Review July 18, 2013

Lance Fritz, Executive VP - Operations

14

Dedicated Focus on Safety Second Quarter YTD Employee

(Reportable Personal Injury Incidents Per 200,000 Employee-Hours)

Rail Equipment (Reportable Derailment Incidents

Per Million Train Miles)

Public (Crossing Accidents Per Million Train Miles)

2008 2009 2010 2011 1H '12 1H '13

1.59 1.45 1.37

1.15 1.02 1.07

Good

2008 2009 2010 2011 1H '12 1H '13

3.68

3.17 2.98

3.28 3.11 3.07

-1%

Good

2008 2009 2010 2011 1H '12 1H '13

2.37

2.11

2.32

2.11 2.29 2.23

Good -3%

All-Time Annual Record

All-Time Annual Record

• Decrease in Severe Injuries

• Infrastructure Investments & Improved Defect Detection

• Continuing Focus on High Risk Crossings and Driver Behavior

+5%

15

2010 2011 2012 2013

92 89 90 88

93 95 95 96

Network Performance Second Quarter • Weather & Track

Renewal Program Impact • Continued Traffic Shifts • Agility & Resiliency

Demonstrated with Resources & Service Plan • Strategic Investments

Adding Capacity • Positioned for Growth

2010 2011 2012 2013

26.4 26.1 26.6 25.7

Velocity (as Reported to the AAR)

Service Delivery* and IS&P Industry Spot & Pull % Good

* Includes early deliveries

**

** Best-ever quarterly record

-3% Good

16

Network Productivity Second Quarter

2010 2011 2012 2013

1,055

714 553

399

Slow Order Miles Good

2nd Qtr Record

-28%

• Process Improvement – UP Way – Employee Engagement – Lean Principles

• Capital Effectiveness – Upgrades – Capacity

-3%

Flat

+1%

+2%

+2% Manifest

34 33 32

1,320 1,350 1,430

2011 2012 2013

The UP Way Fort Worth Terminal Performance

Jan – Jun Each Year

Throughput

Terminal Dwell

YOY Var

+6%

-3%

Cars / Day

Avg Hrs

Train Size Performance (vs 2Q 2012)

Auto*

Coal

Intermodal

Grain

Good

Good

* Best-ever quarterly record

17

Capital Investments Replacement, Growth & Productivity, and PTC

2013 Capital Investments ($ in Millions)

Service, Growth & Productivity

$975

PTC $450

Infrastructure Replacement

$2,175

YTD Track Replacement (% of Projects)

38%

11%

51% Complete

In Progress

Remaining

YTD Capacity Cutovers

• Sunset: 15 of 30 miles

• Southern Region Capacity - Siding additions - Terminal enhancements - Double track expansions - Signal upgrades

18

Full Year 2013

• Drive Safety, Service & Efficiency

• Remain Agile in Response to Traffic Shifts & Weather

• Productivity / Volume Leverage

• Capital Effectiveness

• Enhance Value Proposition

19

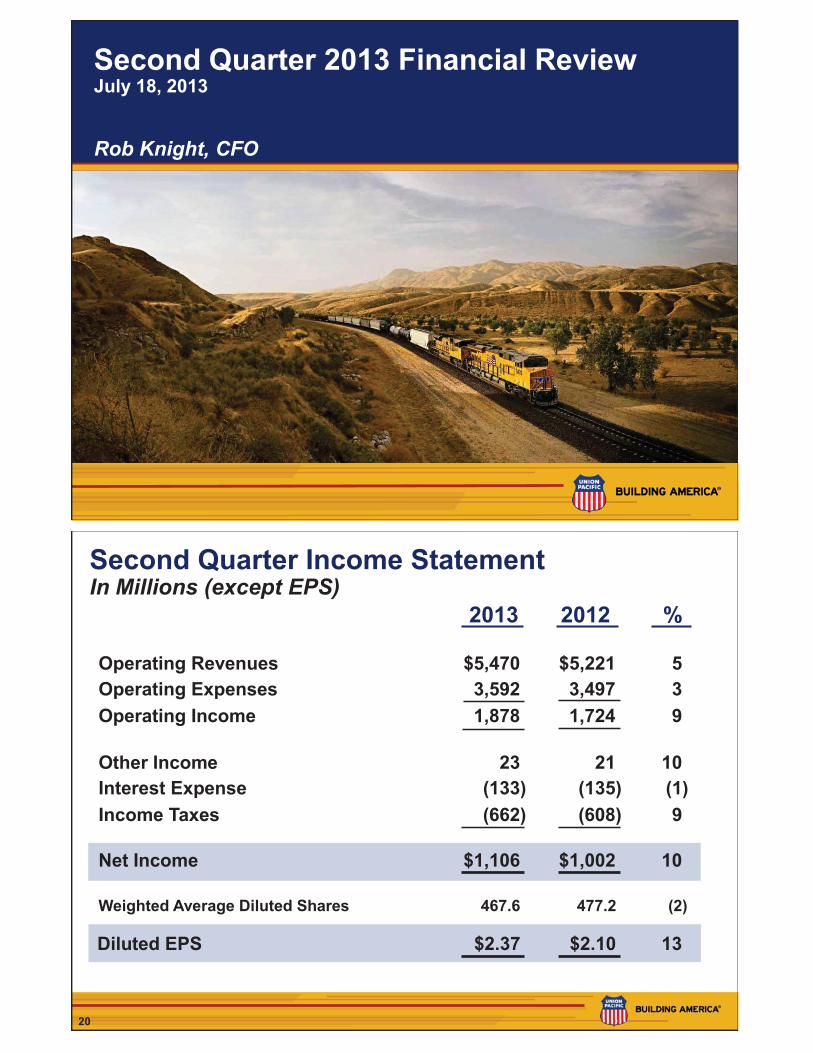

Second Quarter 2013 Financial Review July 18, 2013

Rob Knight, CFO

20

Second Quarter Income Statement In Millions (except EPS)

Operating Revenues $5,470 $5,221 5 Operating Expenses 3,592 3,497 3 Operating Income 1,878 1,724 9 Other Income 23 21 10 Interest Expense (133) (135) (1) Income Taxes (662) (608) 9 Net Income $1,106 $1,002 10 Weighted Average Diluted Shares 467.6 477.2 (2)

Diluted EPS $2.37 $2.10 13

2013 2012 %

21

Freight Revenue Second Quarter (In Millions)

2012

Volume Core Price

Fuel Surcharge

2013

-0.5%

+4% $5,153

$4,913

+5%

-0.5%

Mix

+2%

22

$1,151 $1,185

Compensation & Benefits Expense Second Quarter 2013 $1,185M, +3%

2012

Compensation & Benefits (in Millions)

2013

45,797 46,787

2012

Workforce Levels (Quarterly Average)

2013

+2%

• Inflation Costs • Shift in Traffic Mix • Lower Volume

• Increased Workforce – Shift in Traffic Mix – Capital (including PTC)

+3%

23

Fuel Expense Second Quarter 2013 $863M, -2%

• Lower Average Diesel Fuel Price

• GTMs Flat compared to 2012

• 2% Consumption Rate Increase

$3.21 $3.10

Average Fuel Price (Per Gallon Consumed)

2012 2013

-3%

234,483 235,396

2012

Gross-Ton-Miles (in Millions)

2013

Flat

24

$542 $585

Second Quarter 2013 Expense Review In Millions

2012

Purchased Services & Materials

2013

• Increased Locomotive & Freight Car Repair Costs

• Joint Facility Maint. expenses • New Logistics Management

Fees

+8%

$433 $438 • Higher Depreciable Asset Base from Recent Capital Spending Levels

• New Equipment Rate Study 2012

Depreciation

2013

+1%

25

Second Quarter 2013 Expense Review (cont) In Millions

• Container Costs - New Contract Arrangement

• Higher Freight Car Rental Expense

• Lower Freight Car and Locomotive Lease Expenses

$299 $302

2012

Equipment & Other Rents

2013

+1%

• Higher Personal Injury Expense • Higher Property Tax Expense • Increased Costs for Freight &

Property Damage

$190 $219

2012

Other

2013

+15%

26

Operating Ratio Performance

2010 2011 2012 2013

69.4

71.3

67.0 65.7

Second Quarter (Percent)

-1.3 pts

Best-Ever Quarter

Best-Ever Quarter

• Solid Core Pricing

• Network Efficiencies

• Lower Volume Levels

Reiterate Full Year Sub-65 Operating Ratio

Goal by 2017

27

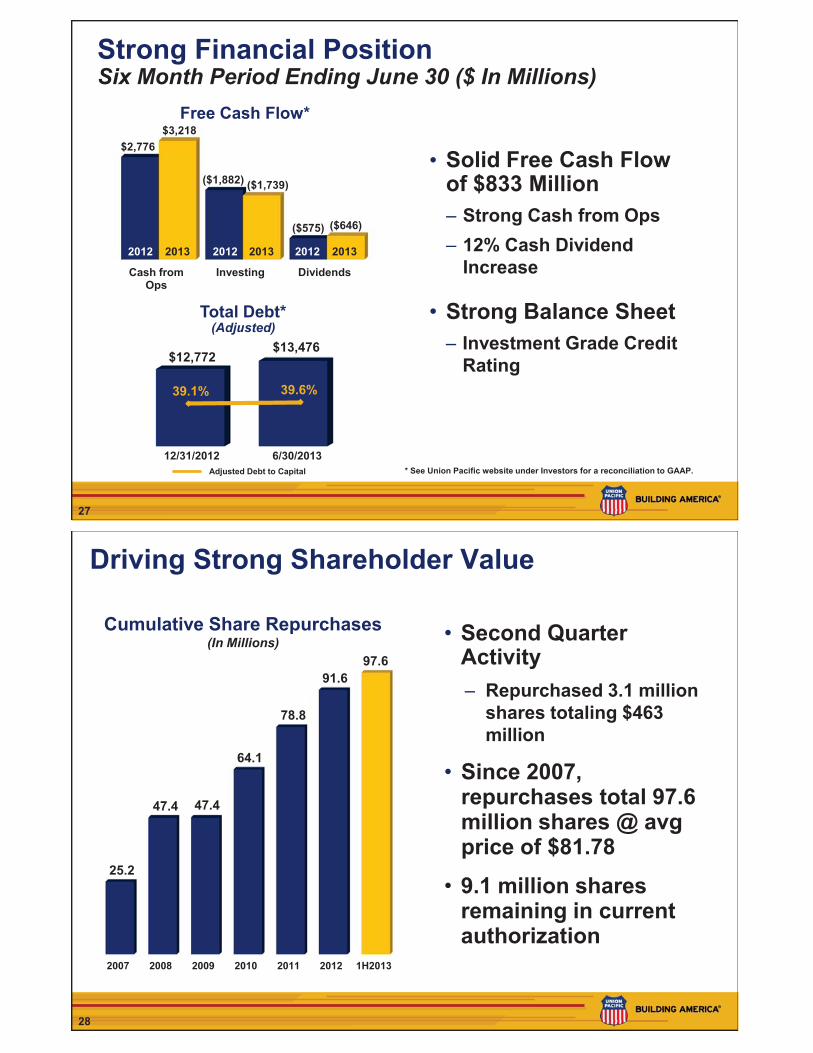

Cash from Ops

Investing Dividends

$2,776

($1,882)

($575)

$3,218

($1,739)

($646)

Strong Financial Position Six Month Period Ending June 30 ($ In Millions)

• Solid Free Cash Flow of $833 Million ‒ Strong Cash from Ops ‒ 12% Cash Dividend

Increase

• Strong Balance Sheet ‒ Investment Grade Credit

Rating

Free Cash Flow*

Total Debt* (Adjusted)

39.1% 39.6%

* See Union Pacific website under Investors for a reconciliation to GAAP. Adjusted Debt to Capital

12/31/2012 6/30/2013

$12,772 $13,476

2013 2012 2013 2012 2013 2012

28

Driving Strong Shareholder Value

Cumulative Share Repurchases (In Millions)

• Second Quarter Activity – Repurchased 3.1 million

shares totaling $463 million

• Since 2007, repurchases total 97.6 million shares @ avg price of $81.78

• 9.1 million shares remaining in current authorization

2007 2008 2009 2010 2011 2012 1H2013

25.2

47.4 47.4

64.1

78.8

91.6 97.6

29

2013 Outlook Assuming an Improving Economy

Second Half • Positive Volume Growth Full Year • Positive Volume Growth • Continued Real Core

Pricing Gains • Record Earnings • Growing Returns • Increased Shareholder

Value

30

Second Quarter 2013 Earnings Release July 18, 2013 Jack Koraleski, CEO

31

Positioned for Success

• Economic Uncertainty

• Reinvestible Pricing

• Growth Opportunities

• Growing Customer Value & Shareholder Returns

• Well Positioned for the Future

32

Cautionary Information This press release and related materials contain statements about the Corporation’s future that are not

statements of historical fact, including specifically the statements regarding the Corporation’s expectations with respect to general economic conditions, future economic improvement, and business growth and its ability to capitalize on any future economic improvement; obtain reinvestible pricing; develop new business; provide safe, efficient and reliable service; and generate value for our customers and shareholders. These statements are, or will be, forward-looking statements as defined by the Securities Act of 1933 and the Securities Exchange Act of 1934. Forward-looking statements also generally include, without limitation, information or statements regarding: projections, predictions, expectations, estimates or forecasts as to the Corporation’s and its subsidiaries’ business, financial, and operational results, and future economic performance; and management’s beliefs, expectations, goals, and objectives and other similar expressions concerning matters that are not historical facts.

Forward-looking statements should not be read as a guarantee of future performance or results, and will not necessarily be accurate indications of the times that, or by which, such performance or results will be achieved. Forward-looking information, including expectations regarding operational and financial improvements and the Corporation’s future performance or results are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in the statement. Important factors, including risk factors, could affect the Corporation’s and its subsidiaries’ future results and could cause those results or other outcomes to differ materially from those expressed or implied in the forward-looking statements. Information regarding risk factors and other cautionary information are available in the Corporation’s Annual Report on Form 10-K for 2012, which was filed with the SEC on February 8, 2013. The Corporation updates information regarding risk factors if circumstances require such updates in its periodic reports on Form 10-Q and its subsequent Annual Reports on Form 10-K (or such other reports that may be filed with the SEC).

Forward-looking statements speak only as of, and are based only upon information available on, the date the statements were made. The Corporation assumes no obligation to update forward-looking information to reflect actual results, changes in assumptions or changes in other factors affecting forward-looking information. If the Corporation does update one or more forward-looking statements, no inference should be drawn that the Corporation will make additional updates with respect thereto or with respect to other forward-looking statements. References to our website are provided for convenience and, therefore, information on or available through the website is not, and should not be deemed to be, incorporated by reference herein.

33

Second Quarter 2013 Earnings Release July 18, 2013 Question & Answer Session