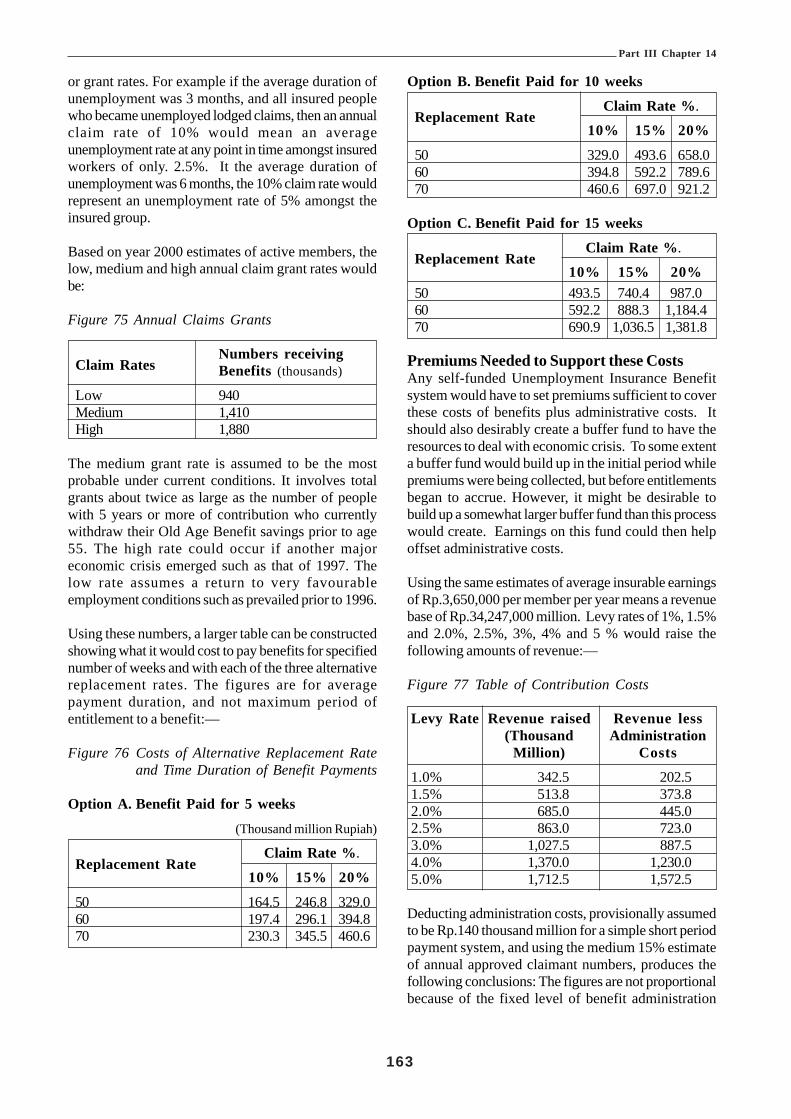

social security and coverage for all restructuring the ... · restructuring the social security...

TRANSCRIPT

ILO PROJECT INS/00/M04/NET

International Labour OfficeJakarta

SOCIAL SECURITY and COVERAGE FOR ALL

Restructuring the Social Security Scheme in Indonesia —Issues & Options

Version Date:- 20th December 2002

Copyright©International Labour Organization 2002

First published 2003

Publications of the International Labour Office enjoy copyright under Protocol 2 of the Universal Copyright Convention.Nevertheless, short excerpts from them may be reproduced without authorization, on condition that the source is indicated.For rights of reproduction or translation, application should be made to the Publications Bureau (Rights and Permissions),International Labour Office, CH-1211 Geneva 22, Switzerland. The International Labour Office welcomes such applications.

Libraries, institutions and other users registered in the United Kingdom with the Copyright Licensing Agency, 90 TottenhamCourt Road W1T 4LP [Fax: (+44)(0)20 7631 5500; email: [email protected]], in the United States with the Copyright ClearanceCenter, 222 Rosewood Drive, Danvers, MA 01923 [Fax: (+1)(978) 750 4470; email: [email protected]] or in other countrieswith associated Reproduction Rights Organization, may make photocopies in accordance with the licences issued to them forthis purpose.

ILOSocial Security and Coverage for All: Restructuring the Social Security Scheme in Indonesia - Issues & OptionsJakarta, International Labour Office, 2003

ISBN 92-2-113568-3

The designations employed in ILO publications, which are in conformity with United Nations practice, and the presentationof material there in do not imply the expression of any opinion whatsoever on the part of the International Labour Officeconcerning the legal status of any country, area or territory or of its authorities, or concerning the delimitation of its frontiers.

The responsibility for opinions expressed in signed articles, studies and other contributions rests solely with their authors,and publication does not constitute an endorsement by the International Labour Office of the opinions expressed in them.

Reference to names of firms and commercial products and processes does not imply their endorsement by the InternationalLabour Office, and any failure to mention a particular firm, commercial product or process is not a sign of disapproval.

ILO publications can be obtained through major booksellers or ILO local offices in many countries, or direct from ILOPublications, International Labour Office, CH-1211 Geneva 22, Switzerland or from the ILO Office in Jakarta, UN Building, 5thfloor, Jl. MH Thamrin 14, Jakarta 10340, Catalogues or lists of new publications are available free of charge from the aboveaddress, or by email: [email protected] ; [email protected].

Visit our website: www.ilo.org/publns ; www.un.or.id/ilo

Printed in Jakarta

iii

Table of ContentsANNEXES ............................................................................................................................................. viiLIST OF FIGURES AND TABLES ............................................................................................................. ixGLOSSARY ............................................................................................................................................ xiiiFOREWORD ........................................................................................................................................... xviiINTRODUCTION ....................................................................................................................................... xixDEFINITIONS ............................................................................................................................................ xxi

PART I SOCIAL SECURITY DEVELOPMENT BACKGROUND ...................................................1CHAPTER 1 THE ILO PROJECT — RESTRUCTURING THE SOCIAL SECURITY SYSTEM ......1

General Background..................................................................................................................... 1Immediate Objectives & Outputs ................................................................................................. 2

CHAPTER 2 OVERVIEW OF SOCIAL SECURITY IN INDONESIA ...................................................4General ........................................................................................................................................... 4Social Security Responsibilities ................................................................................................... 4Regional Autonomy ....................................................................................................................... 6Government and Private Employees Social Security Schemes ................................................. 6Labour Force and Social Security Membership ......................................................................... 8

PART II JAMSOSTEK ................................................................................................................................9Executive Summary........................................................................................................................ 9Rangkuman Eksekutif ................................................................................................................. 11

CHAPTER 3 JAMSOSTEK SOCIAL SECURITY PROGRAMMES ...................................................13Jamsostek Programs .................................................................................................................... 13Statistical Overview of Jamsostek Programs ............................................................................ 13Social Security Coverage of the General Population in Indonesia ....................................... 15

CHAPTER 4 STATUS OF JAMSOSTEK ................................................................................................16Implications of JAMSOSNAS for ‘Trust Fund’ Status of Institutions ..................................... 20

CHAPTER 5 JAMSOSTEK CORE BUSINESS......................................................................................22CHAPTER 6 JAMSOSTEK OPERATIONS & IT SYSTEMS ...............................................................23

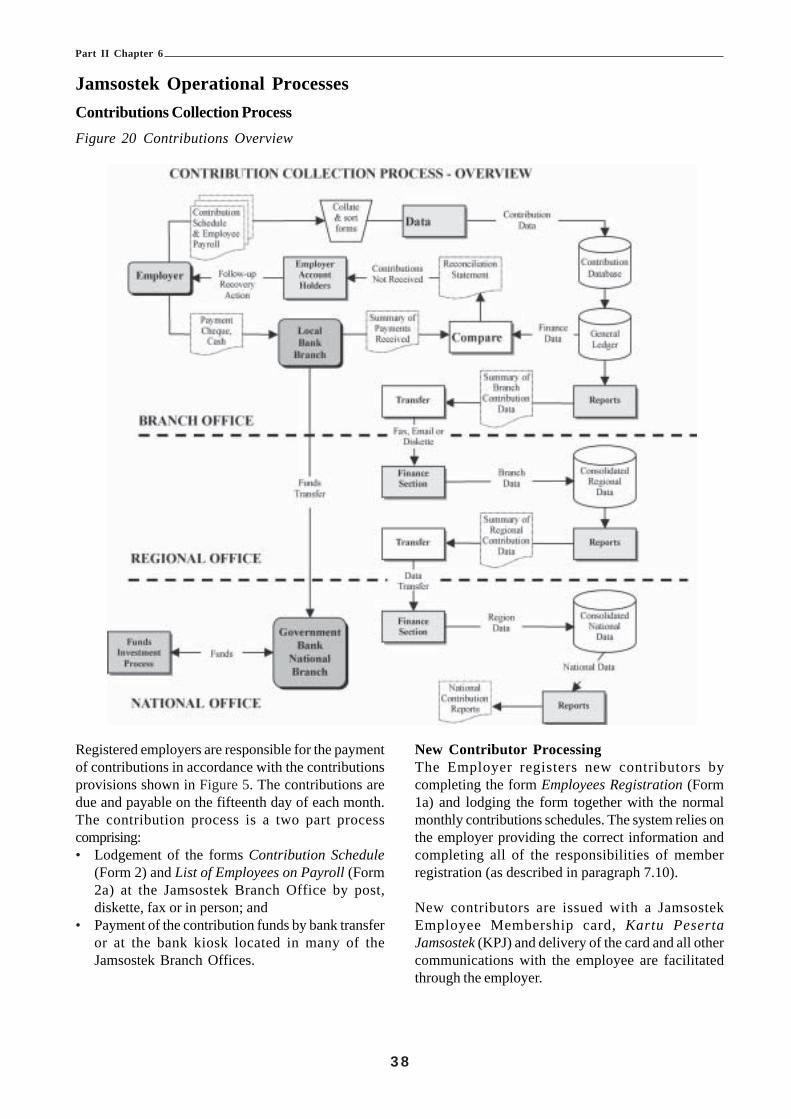

Executive Summary...................................................................................................................... 23Rangkuman Eksekutif ................................................................................................................. 26Introduction.................................................................................................................................. 30Jamsostek Organization .............................................................................................................. 30Jamsostek Operational Processes.............................................................................................. 30Information Systems in Jamsostek ............................................................................................. 46Observations and Discussion ..................................................................................................... 56Conclusion ................................................................................................................................... 77

CHAPTER 7 COMPLIANCE .................................................................................................................. 78CHAPTER 8 JAMSOSTEK CONTRIBUTIONS STRUCTURE ........................................................... 82CHAPTER 9 HUMAN RESOURCES .....................................................................................................83CHAPTER 10 JAMSOSTEK FINANCE AND INVESTMENTS ............................................................84

Executive Summary...................................................................................................................... 84Ramgkuman Eksekutif ................................................................................................................ 86Financial Analysis of Jamsostek ................................................................................................ 88Issues in the Investment of the Jamsostek Fund ....................................................................... 94

Table of Contents

iv

PART III BENEFIT PROGRAMME STUDIES .....................................................................................97CHAPTER 11 PENSION REFORM IN INDONESIA. ............................................................................97

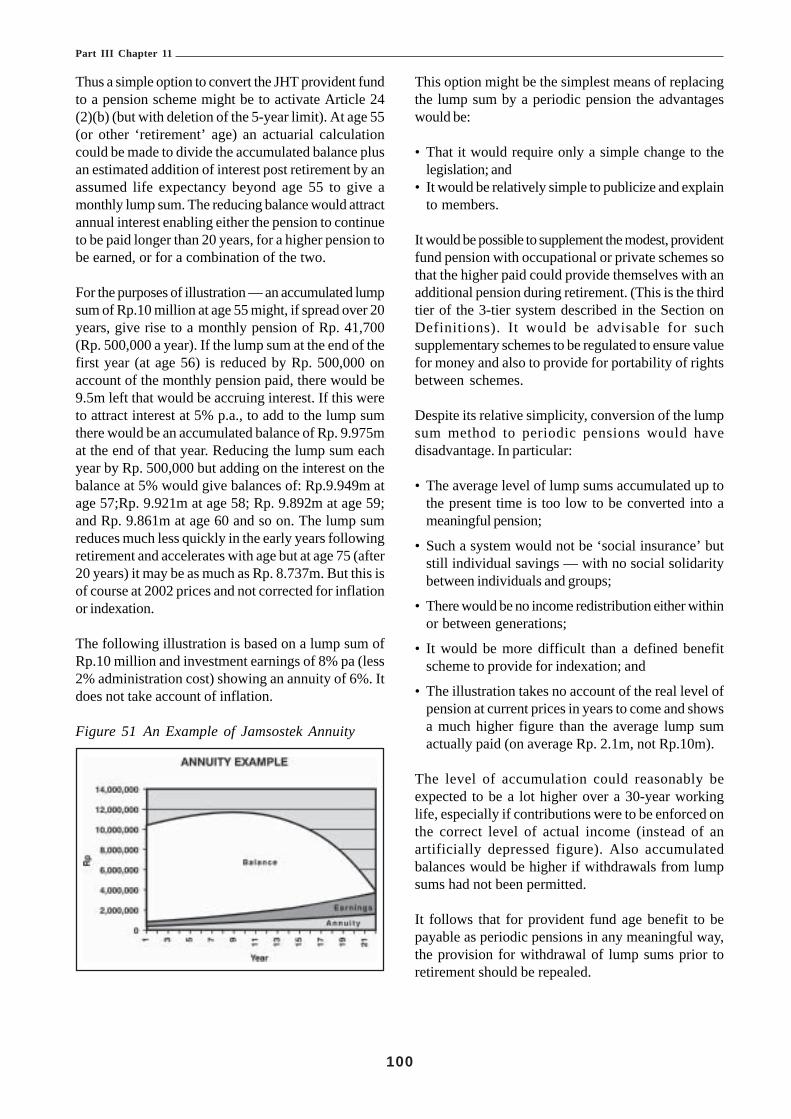

Executive Summary...................................................................................................................... 97Rangkuman Eksekutif ................................................................................................................. 98Jamsostek JHT Scheme and the Need for Change................................................................... 99A Notional Defined Contribution Scheme ............................................................................... 102A Mandatory Defined Contribution Scheme .......................................................................... 103A Mixed Pension System ........................................................................................................... 104A Defined Benefit Scheme ........................................................................................................ 105A Scheme for the Informal Sector ............................................................................................ 107A Scheme for the Self-Employed .............................................................................................. 109Pensions Administration ........................................................................................................... 109The Civil Service Pension Scheme Run by PT Taspen. .......................................................... 111Employer-Based and Financial Institution Pension Plans .................................................... 111Preparation for a New Pension Scheme ................................................................................. 112Conclusions................................................................................................................................ 113

CHAPTER 12 EMPLOYMENT INJURY AND DEATH BENEFITS ...................................................... 118Executive Summary.................................................................................................................... 118Rangkuman Eksekutif ............................................................................................................... 120Overview of the Legal Provisions and Their Implementation ............................................... 123Systems for Fixing Rates of Contribution ............................................................................... 125The Case for Accident Benefit .................................................................................................. 128JKK Scheme Benefits ................................................................................................................. 129Death Benefit Scheme ............................................................................................................... 131Implementation and Experience of the Schemes .................................................................... 131Recommended Benefit, Contribution and Administration Structure ..................................... 133Recommended Administrative Changes ................................................................................... 135Death Benefit Scheme ............................................................................................................... 136

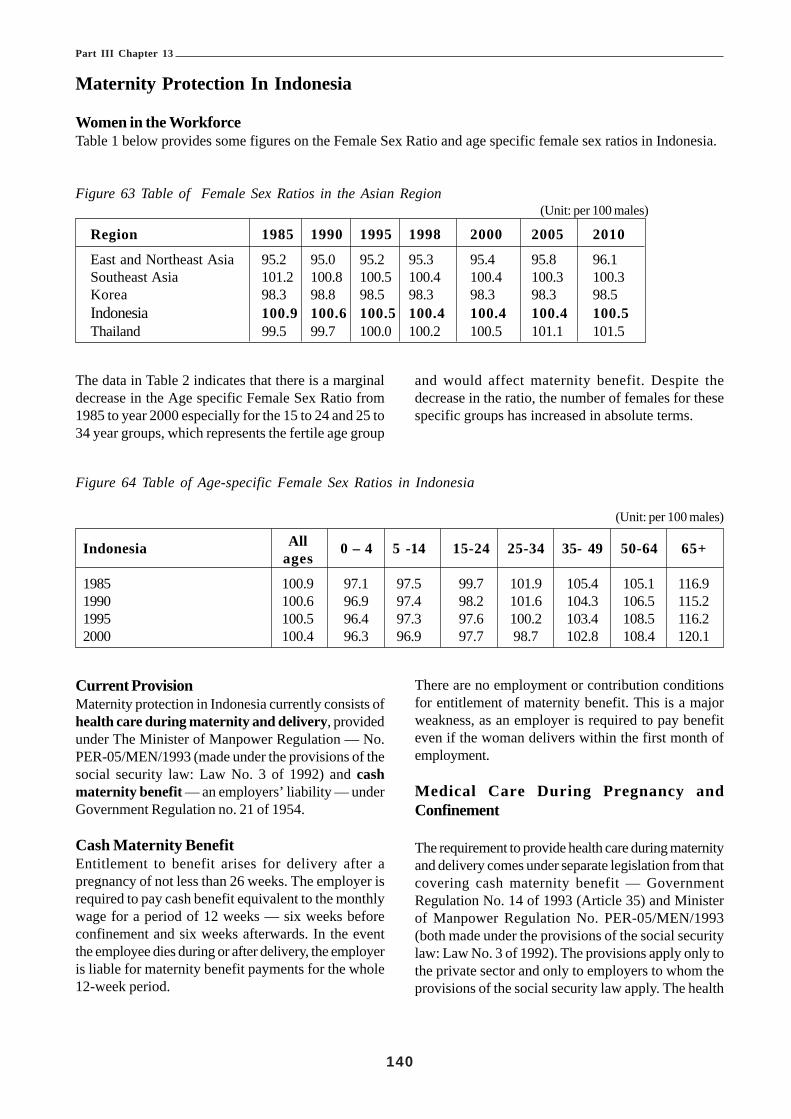

CHAPTER 13 MATERNITY PROTECTION ......................................................................................... 137Executive Summary.................................................................................................................... 137Rangkuman Eksekutif ............................................................................................................... 138Maternity Protection in Indonesia ........................................................................................... 140Analysis of the Programme ....................................................................................................... 141Recommendations ...................................................................................................................... 143Other Issues ............................................................................................................................... 145

CHAPTER 14 UNEMPLOYMENT BENEFIT INSURANCE............................................................... 146Executive Summary.................................................................................................................... 146Rangkuman Eksekutif ............................................................................................................... 147Employment and Unemployment In Indonesia ........................................................................ 148Unemployment ........................................................................................................................... 148Impact of the 1997 Crisis ......................................................................................................... 148Impact on Women....................................................................................................................... 149Redundancy Payments and Use of Retirement Savings ......................................................... 150Options for Unemployment Cover ........................................................................................... 151Unemployment Insurance with Private Companies ................................................................ 152Compulsory Savings Schemes .................................................................................................. 152Unemployment Insurance with a Central Fund ...................................................................... 152

Table of Contents

v

The Feasibility of Unemployment Benefit in Indonesia ......................................................... 153Attitudes of The Social Partners and Other Stakeholders .................................................... 155Possible Characteristics of Unemployment Insurance in Indonesia .................................... 156How an Unemployment Insurance Benefit might be Funded. ............................................... 158Replacing Severance Pay with Unemployment Benefit ......................................................... 159Use of Jamsostek Surpluses ..................................................................................................... 159Other Financing Options for Informal Sector Workers ........................................................ 160Jamsostek as a Potential Administrator of Unemployment Insurance ................................. 160Benefit Costs .............................................................................................................................. 162Implementation Strategy ........................................................................................................... 164Implementation and the Economy ............................................................................................ 165Conclusions................................................................................................................................ 165

CHAPTER 15 SOCIAL ASSISTANCE ................................................................................................... 167Executive Summary.................................................................................................................... 167Rangkuman Eksekutif ............................................................................................................... 169The 1997 Crisis and the Social Safety Net ............................................................................. 172The Size of the Social Safety Net Initiatives ........................................................................... 172Effectiveness of the Social Safety Net Programmes ............................................................... 173Summary on Social Safety Net Programmes ........................................................................... 176Other Anti Poverty Measures ................................................................................................... 176Social Safety Nets and Social Assistance................................................................................ 177Unmet Needs .............................................................................................................................. 177Scale of Funding Needed ......................................................................................................... 178Characteristics of Effective Social Assistance Systems ......................................................... 179Possible Strategies for Indonesia ............................................................................................ 180Administrative Improvements .................................................................................................... 182Feasible Types of Social Assistance ........................................................................................ 183Funding Sources ........................................................................................................................ 183Data for Targeting ..................................................................................................................... 184Summary ..................................................................................................................................... 184

CHAPTER 16 JAMSOSTEK HEALTH CARE PROGRAMME ........................................................... 186Executive Summary.................................................................................................................... 186Rangkuman Eksekutif ............................................................................................................... 188Current Health Care Policy and Delivery ............................................................................... 190Health Care Financing ............................................................................................................. 191Micro Financing Schemes ........................................................................................................ 194Access to Primary Care ............................................................................................................. 196Access to Hospital Services ...................................................................................................... 197Quality of Health Services........................................................................................................ 199Direction of Health Care Reform ............................................................................................. 201Analysis of the Organization of Health Care.......................................................................... 204The Alternative Scenarios for Reform ..................................................................................... 204JPK Jamsostek (Health Insurance Component of Jamsostek) .............................................. 206Summary of JPK Jamsostek Problems ..................................................................................... 213Possible Design of Health Insurance for Indonesia.............................................................. 214Health Benefits to be Covered and the Related Contributions ............................................. 217Recommendation for the Revision of Jpk Jamsostek ............................................................. 221

Table of Contents

vi

PART IV OTHER STUDIES .................................................................................................................... 224CHAPTER 17 EXTENSION OF COVERAGE TO EXCLUDED GROUPS ........................................ 224

Executive Summary.................................................................................................................... 224Rangkuman Eksekutif ............................................................................................................... 227General Overview of the Issues for Extension of Coverage ................................................. 230Introduction................................................................................................................................ 234The Incidence Of Poverty in Indonesia................................................................................... 235Social Security in Indonesia..................................................................................................... 243The Employment Sectors in Indonesia ..................................................................................... 245Findings And Options ............................................................................................................... 254

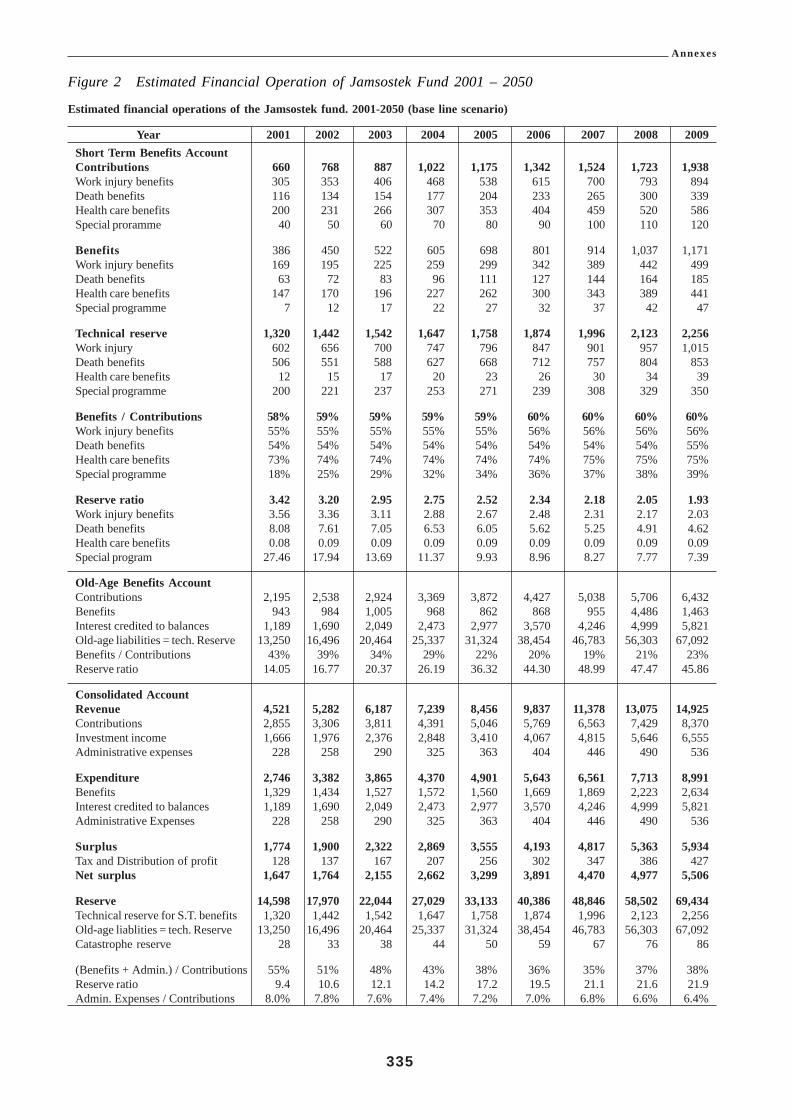

CHAPTER 18 THE SOCIAL BUDGET .................................................................................................. 276Executive Summary.................................................................................................................... 276Rangkuman Eksekutif ............................................................................................................... 277The Demographic and Socio-Economic Context .................................................................... 278Analysis of The Aggregate Social Insurance Expenditure – ................................................. 287Financial Projections of Social Insurance Schemes other than Jamsostek ........................ 289Functional Summary of Social Insurance Benefits ................................................................ 294Concluding Remarks ................................................................................................................. 295

CHAPTER 19 KLATEN REVISTED ....................................................................................................... 296Executive Summary.................................................................................................................... 296Rangkuman Eksekutif ............................................................................................................... 297Introduction................................................................................................................................ 298Essential Background ............................................................................................................... 298Health Sector Finance Project ................................................................................................. 299The Results of the HSF Project ................................................................................................ 300The Klaten Integrated Health Care Reform Field Trial ......................................................... 302The Two -Year IHCR project extension (Apr 1996 - Mar 1998) ........................................... 307Analysis and the Aftermath ....................................................................................................... 311Conclusions................................................................................................................................ 315Summary ..................................................................................................................................... 317

CHAPTER 20 CONCLUSION ................................................................................................................. 318BAB 20 Kesimpulan .................................................................................................................................. 320BIBLIOGRAPHY ...................................................................................................................................... 389

vii

ANNEXES

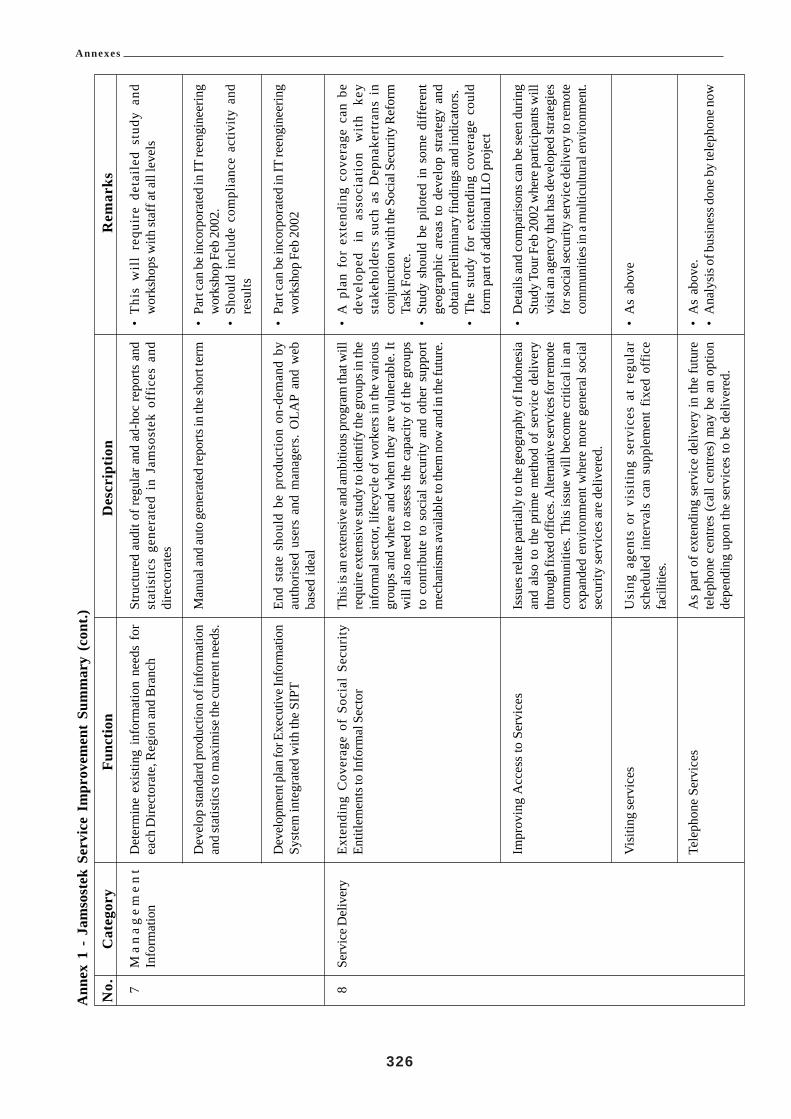

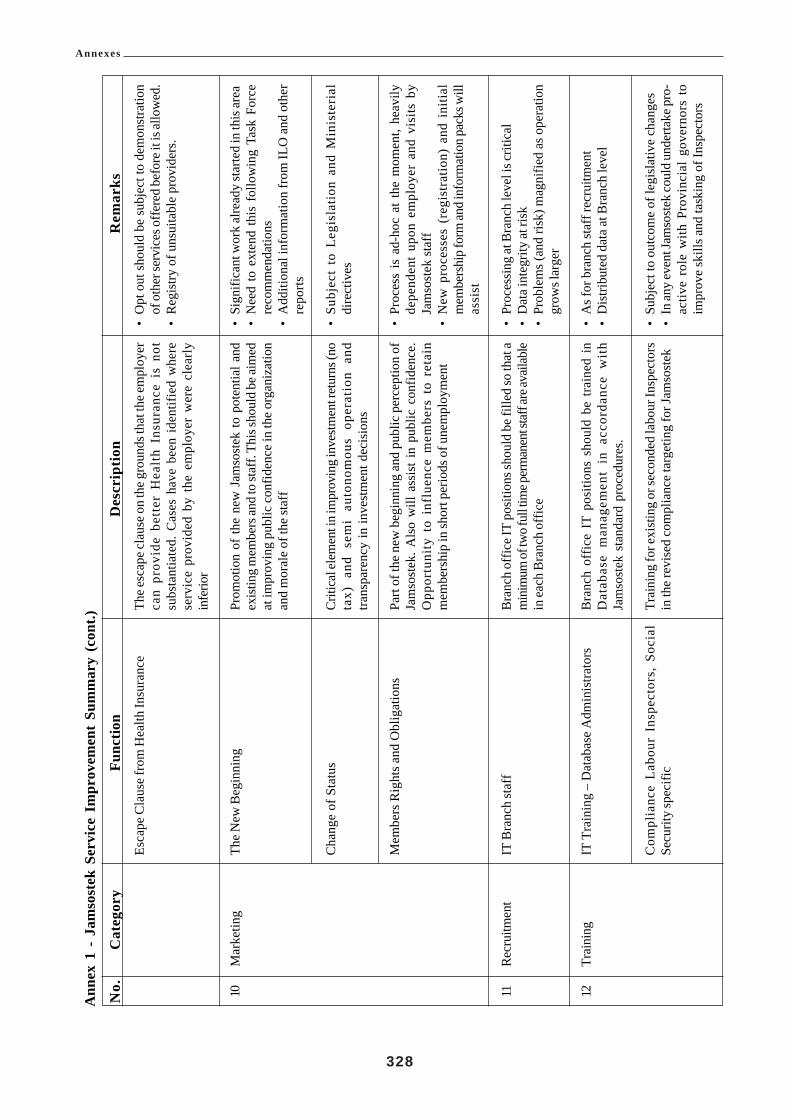

ANNEX 1 JAMSOSTEK SERVICE IMPROVEMENT SUMMARY .............................................................................. 322

ANNEX 2 TAXATION COLLECTION IN INDONESIA ............................................................................................... 331

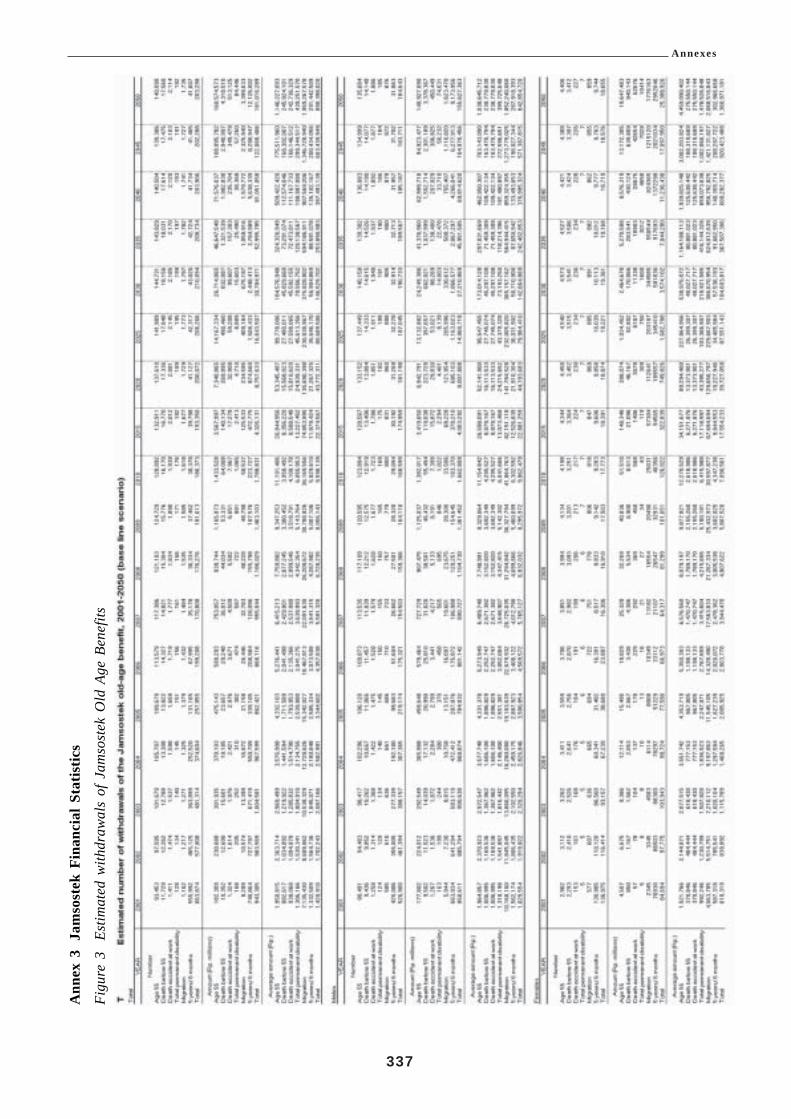

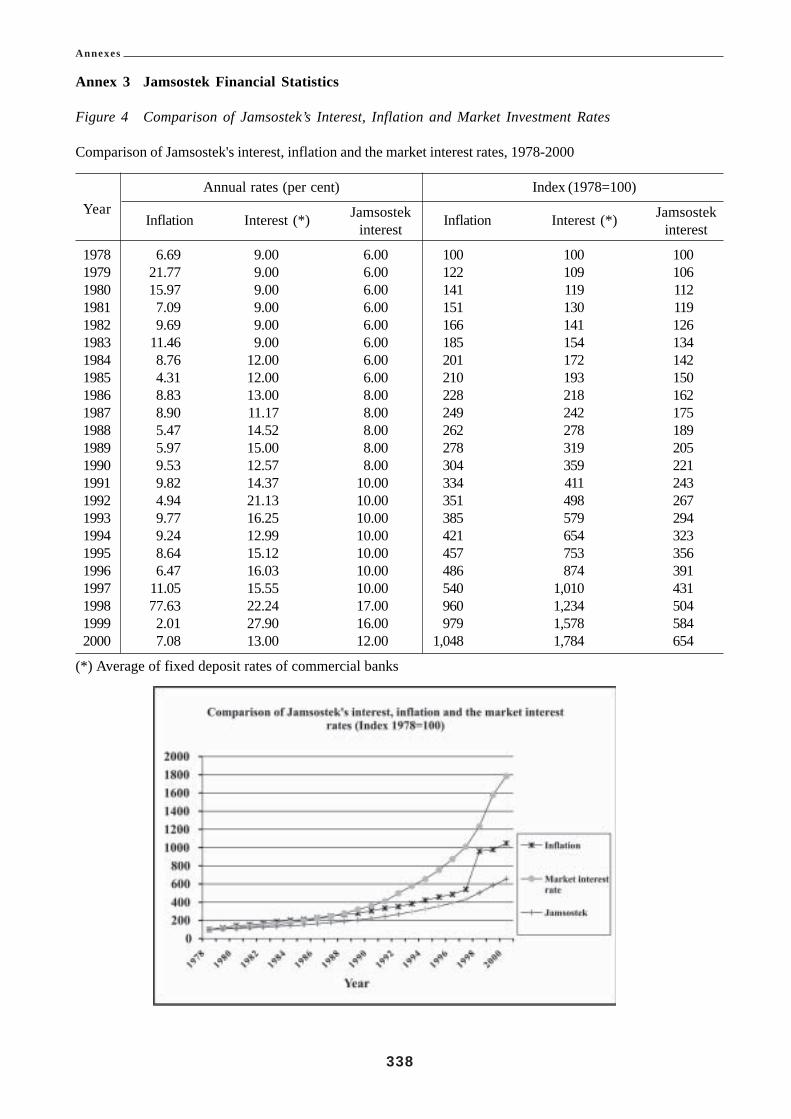

ANNEX 3 JAMSOSTEK FINANCIAL STATISTICS ................................................................................................... 333

ANNEX 4 JAMSOSTEK RETIREMENT PROGRAMME - OVERVIEW ....................................................................... 340

ANNEX 5 MONTHLY MINIMUM WAGES BY PROVINCE, YEAR 2000 .................................................................... 341

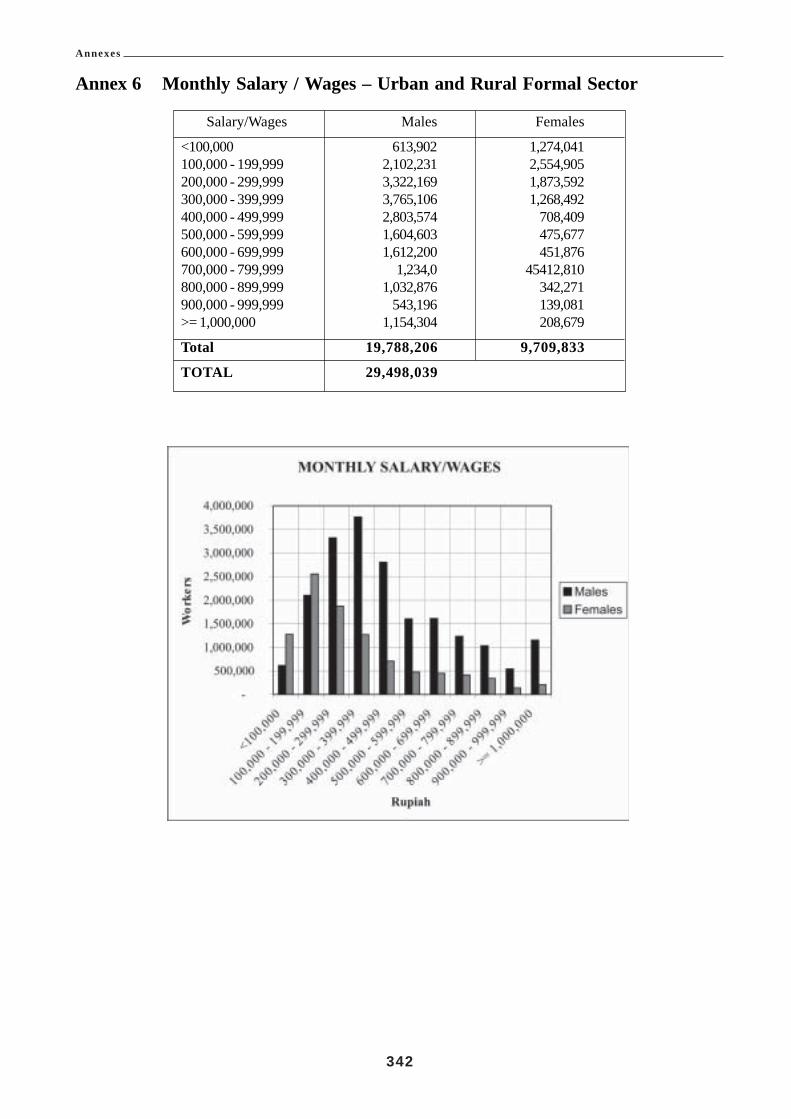

ANNEXE 6 MONTHLY SALARY / WAGES – URBAN AND RURAL FORMAL SECTOR ........................................... 342

ANNEX 7 FORMAL SECTOR – FEMALE SALARY EARNERS BY AGE ................................................................... 343

ANNEX 8 FORMAL SECTOR – MALE SALARY EARNERS BY AGE........................................................................ 344

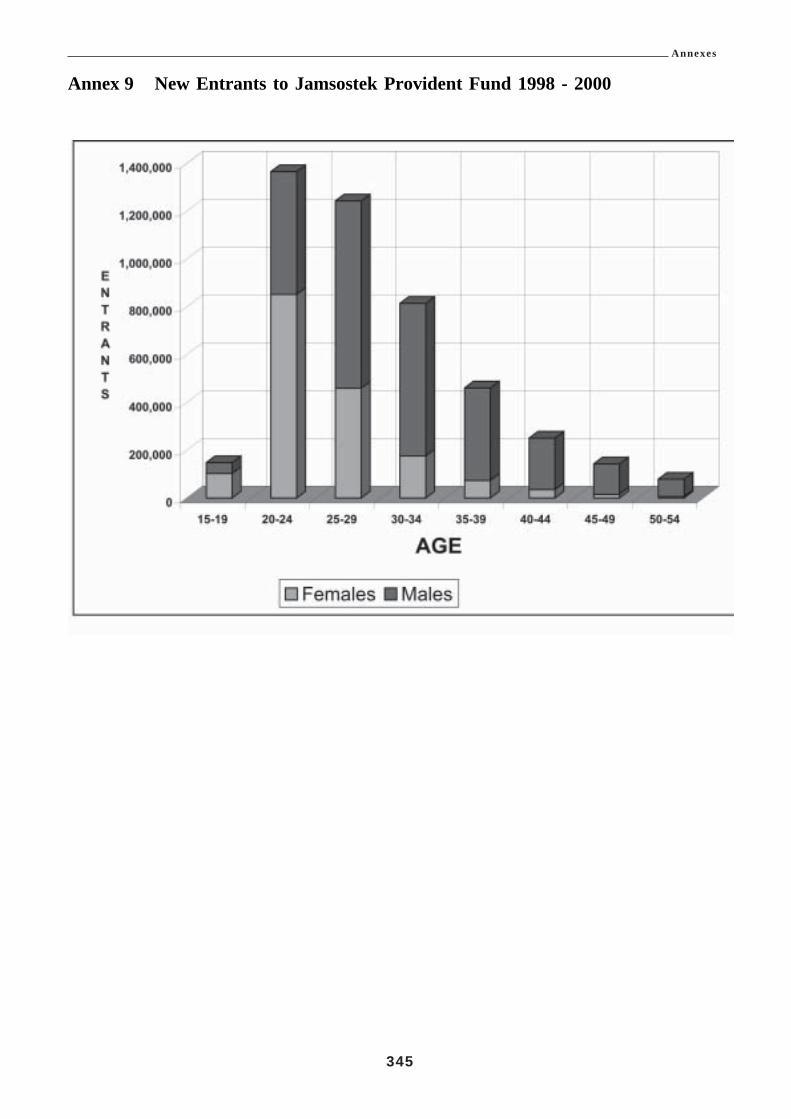

ANNEX 9 NEW ENTRANTS TO JAMSOSTEK PROVIDENT FUND 1998 - 2000 ....................................................... 345

ANNEX 10 OLD AGE DEPENDENCY RATIOS .............................................................................................................. 346

ANNEX 11 POPULATION PROJECTIONS 1998 –2040................................................................................................... 347

ANNEX 12 WORKFORCE COMPOSITION IN INDONESIA ......................................................................................... 348

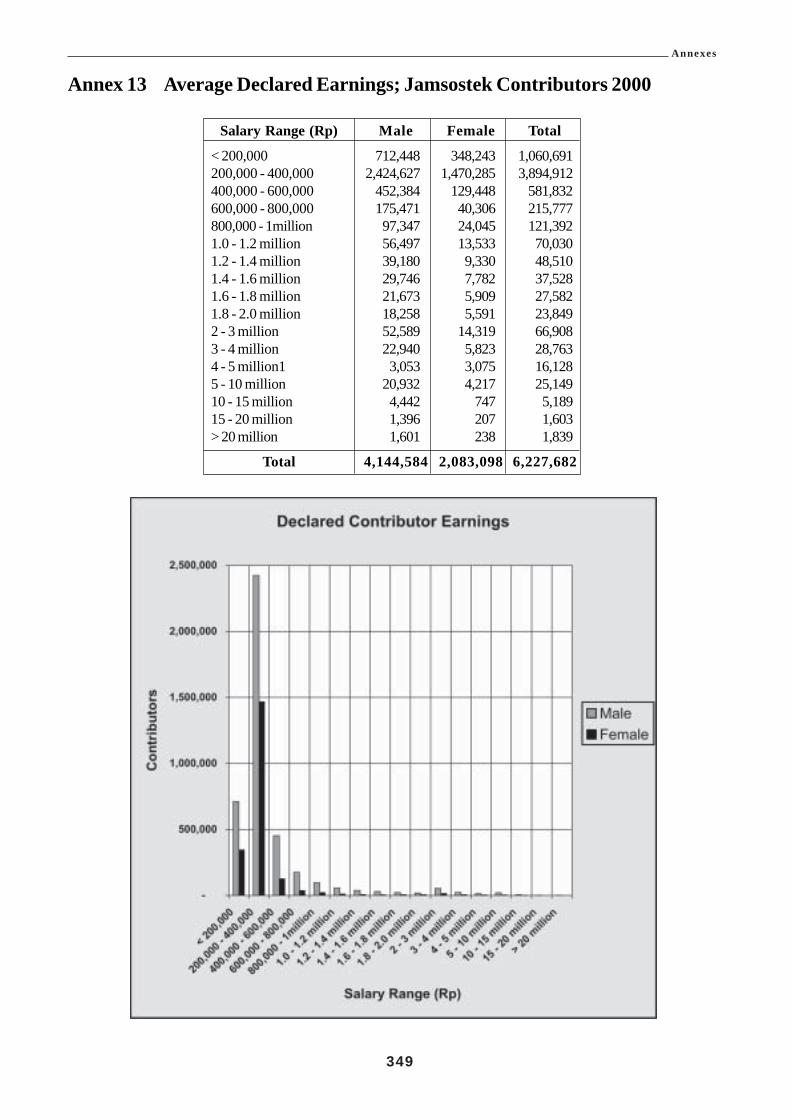

ANNEX 13 AVERAGE DECLARED EARNINGS; JAMSOSTEK CONTRIBUTORS 2000 .............................................. 349

ANNEX 14 WITHDRAWALS FROM JAMSOSTEK PROVIDENT FUND ..................................................................... 350

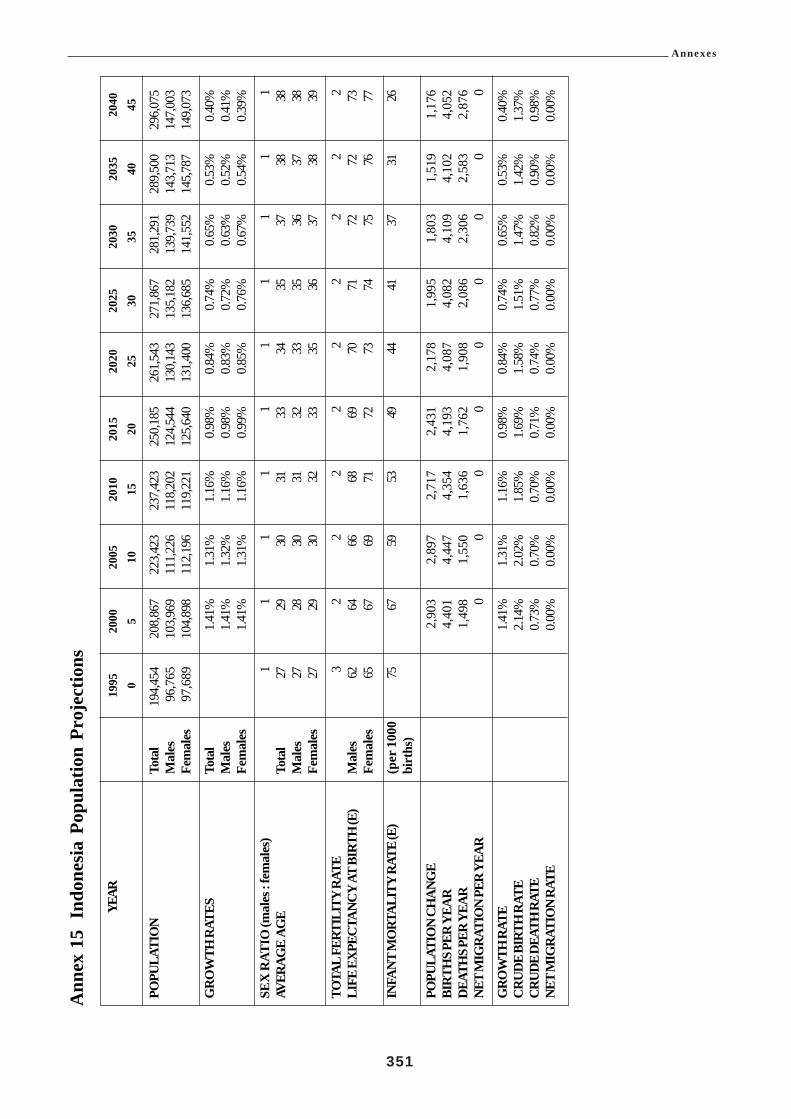

ANNEX 15 INDONESIA POPULATION PROJECTIONS................................................................................................ 351

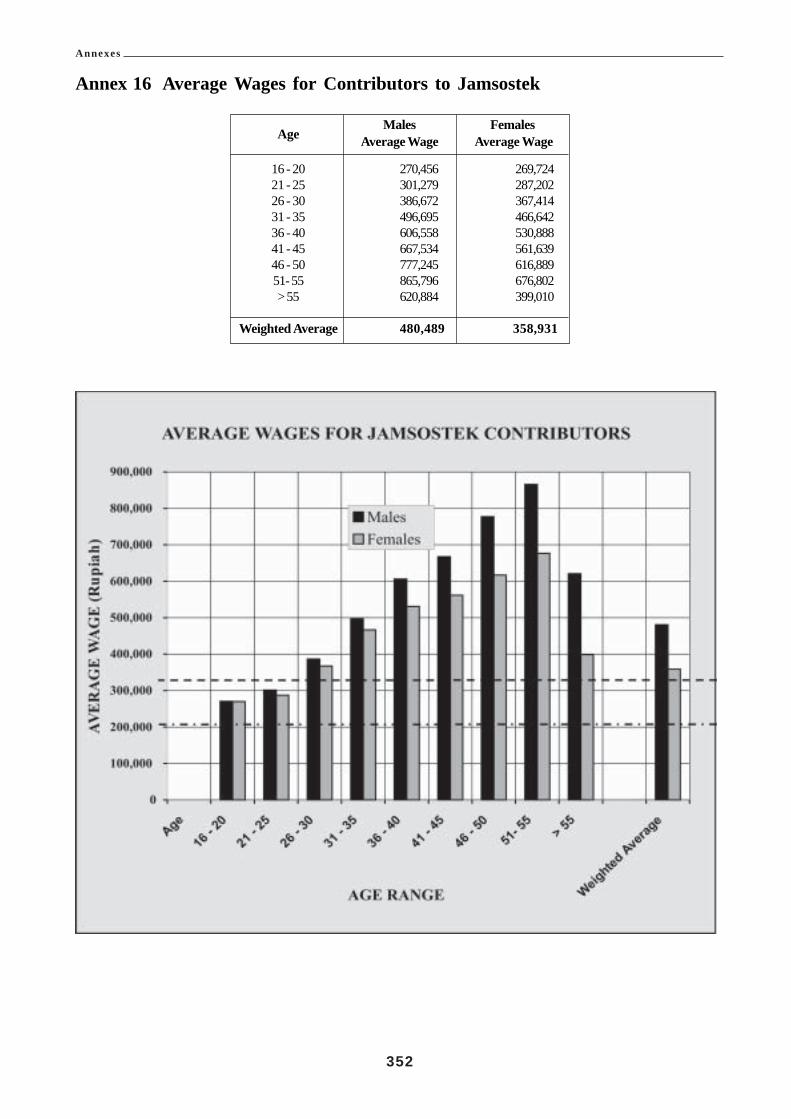

ANNEX 16 AVERAGE WAGES FOR CONTRIBUTORS TO JAMSOSTEK ................................................................... 352

ANNEX 17 LIFE EXPECTANCY ..................................................................................................................................... 353

ANNEX 18 GROUPS OF BUSINESSES ........................................................................................................................... 354

ANNEX 19 ANNUAL REPORT, MINISTRY OF MANPOWER AND TRANSMIGRATION 2001 .................................. 359

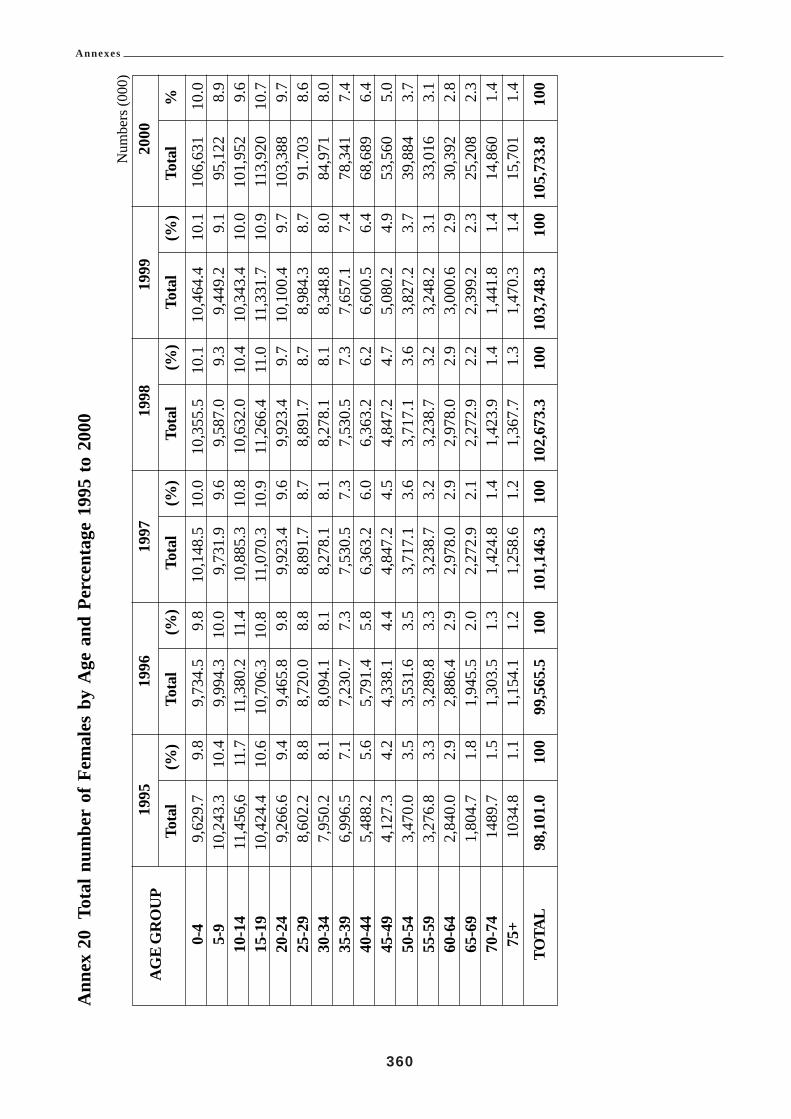

ANNEX 20 TOTAL NUMBER OF FEMALES BY AGE AND PERCENTAGE 1995 TO 2000 ........................................... 360

ANNEX 21 MARITAL STATUS OF URBAN RESIDENTS MALE & FEMALE ABOVE AGE 10 ................................... 361

ANNEX 22 UNEMPLOYMENT INSURANCE STATISTICS .......................................................................................... 362

ANNEX 23 A DRAFT SHORT PERIOD UNEMPLOYMENT BENEFIT SCHEME .......................................................... 370

ANNEX 24 ALTERNATIVE PROJECTIONS OF UNEMPLOYMENT INSURANCE OUTCOMES ................................. 371

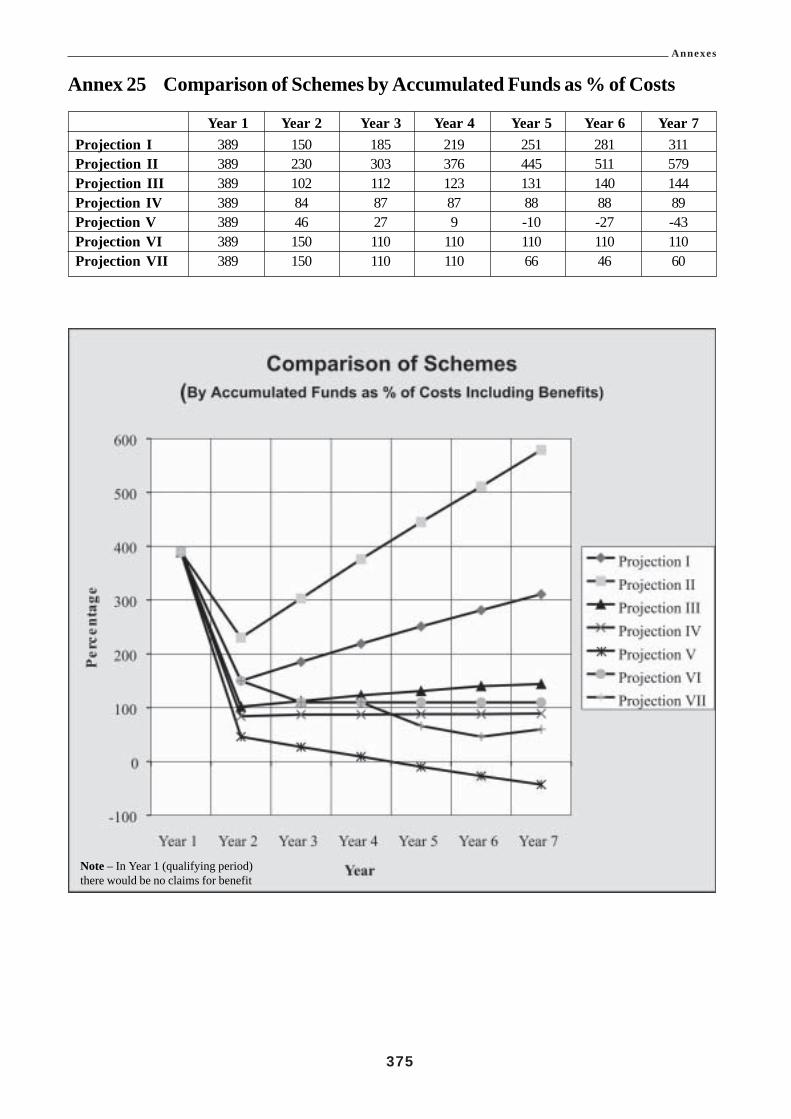

ANNEX 25 COMPARISON OF SCHEMES BY ACCUMULATED FUNDS AS % OF COSTS ........................................ 375

ANNEX 26 SOCIAL ASSISTANCE STATISTICS ........................................................................................................... 376

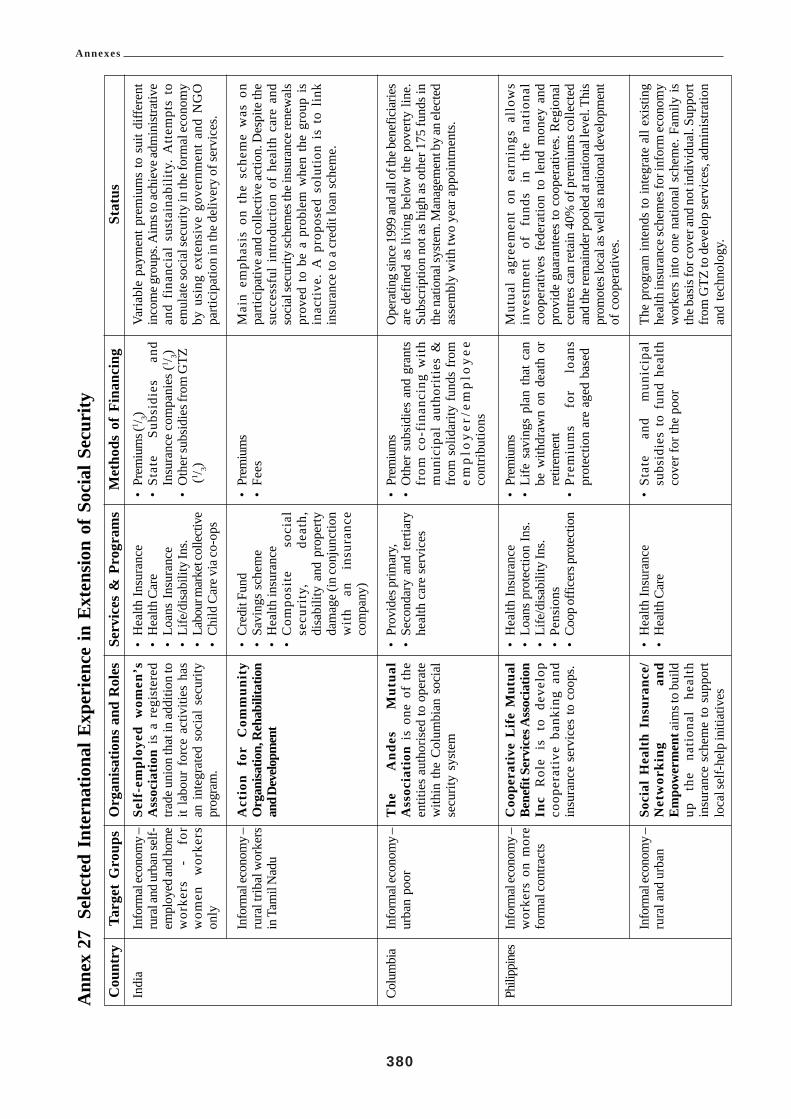

ANNEX 27 SELECTED INTERNATIONAL EXPERIENCE IN EXTENSION OF SOCIAL SECURITY ............................ 380

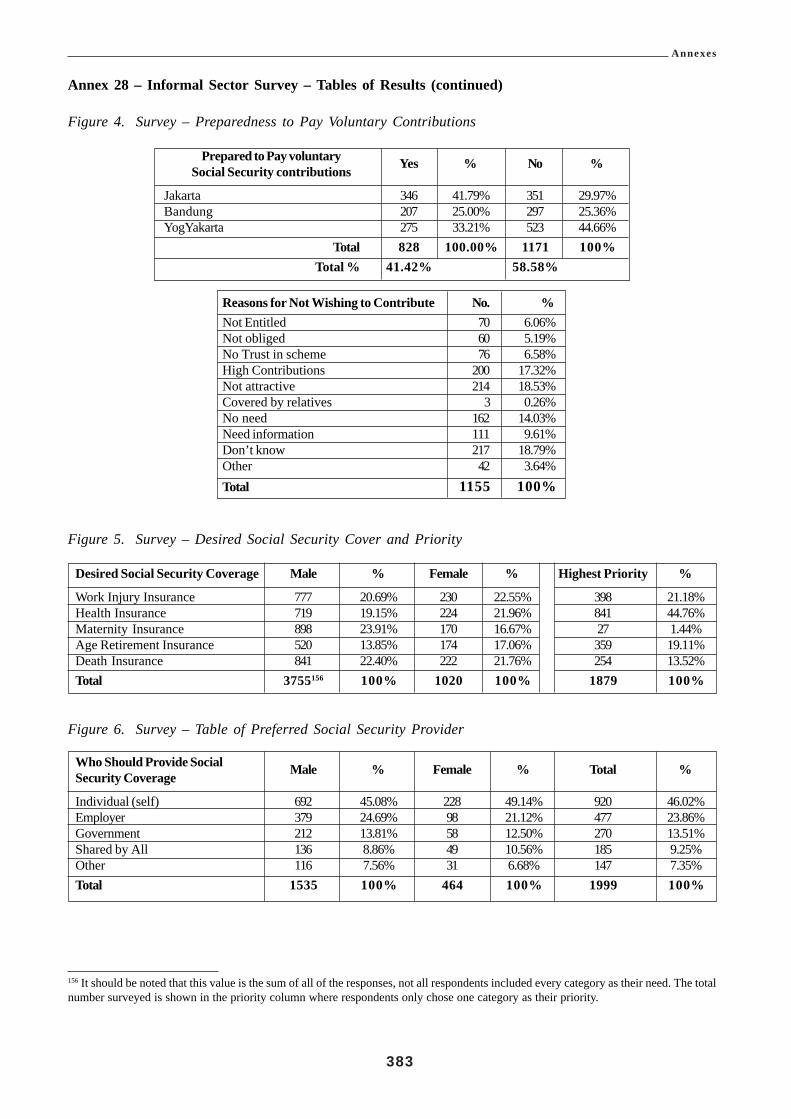

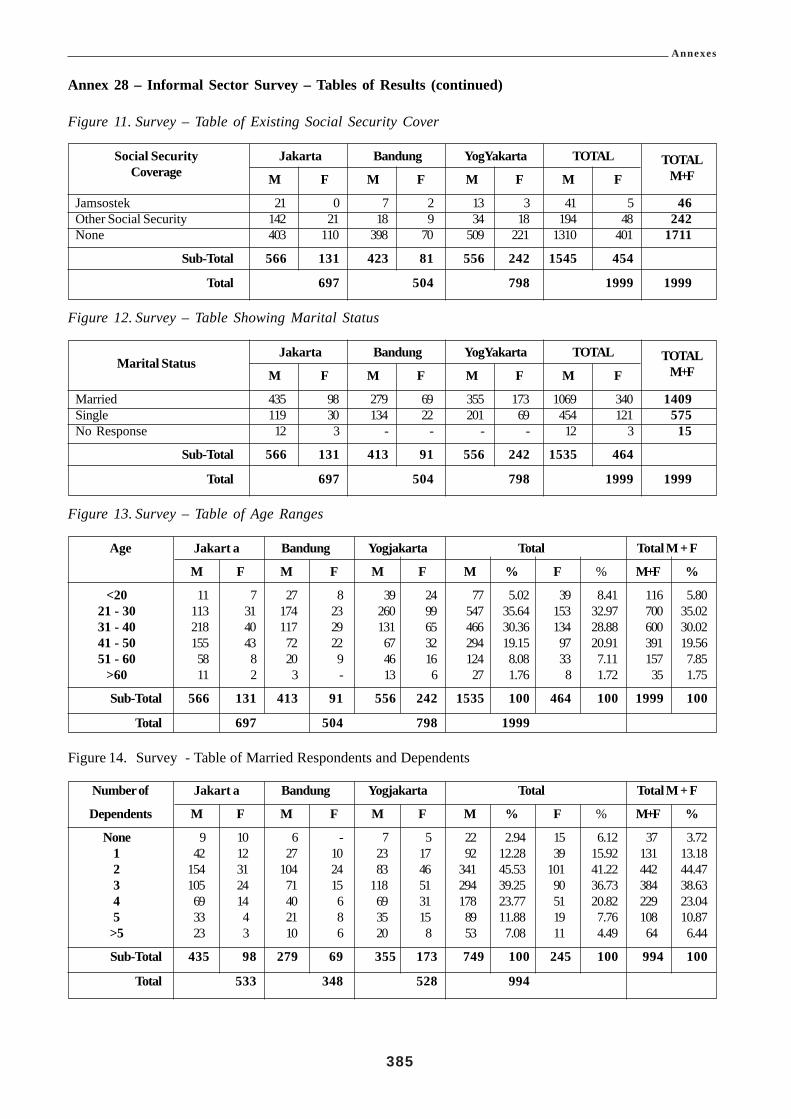

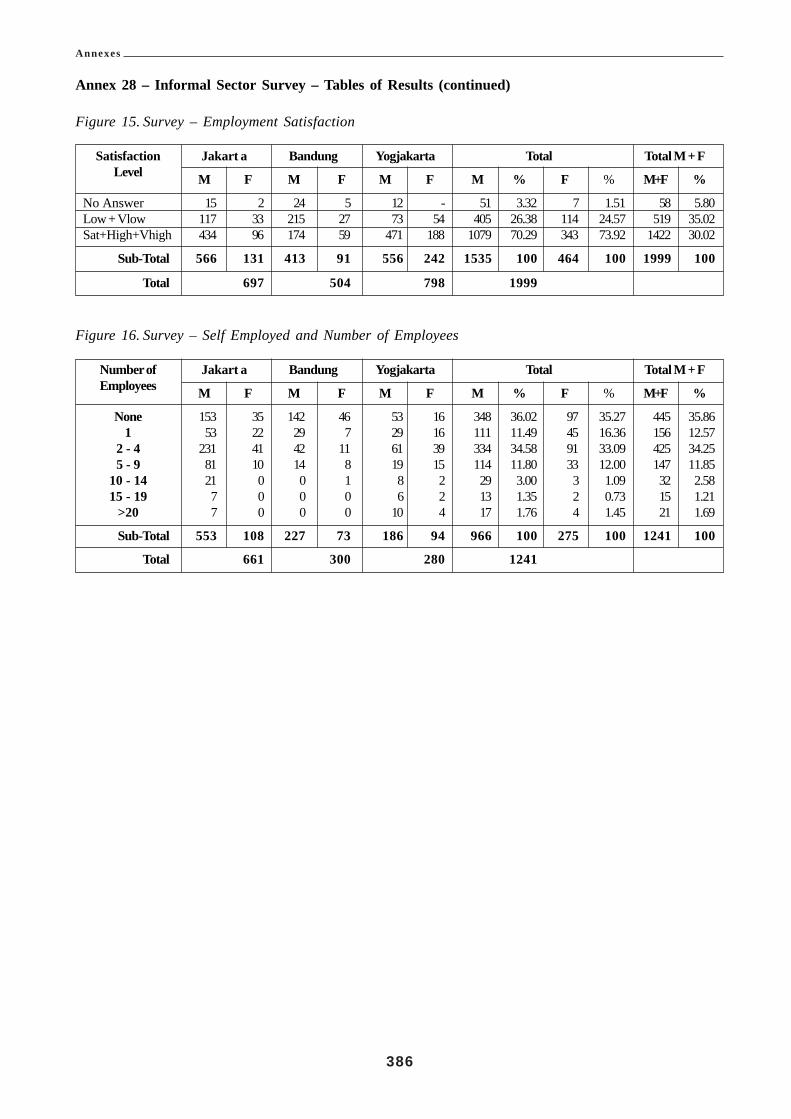

ANNEX 28 INFORMAL SECTOR SURVEY – TABLES OF RESULTS ............................................................................ 382

ANNEX 29 TRANSACTION COSTS BASED ON MAXIMUM CONTRIBUTIONS ...................................................... 387

Annexes

ix

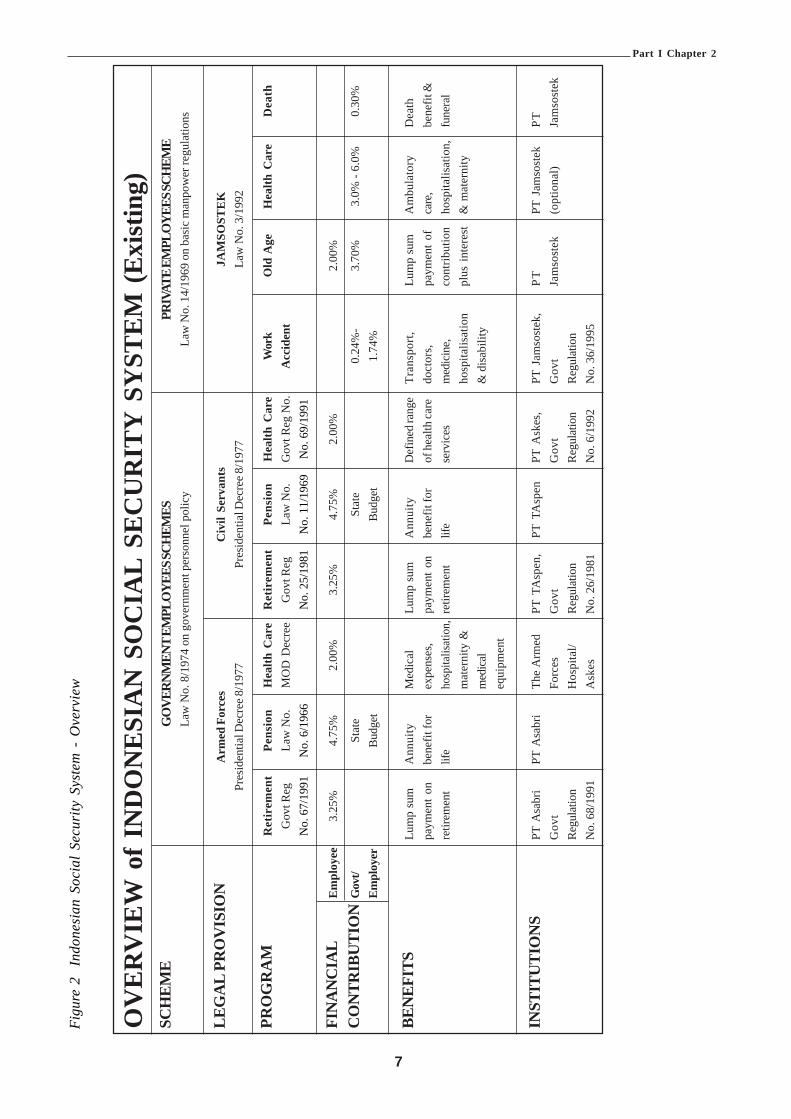

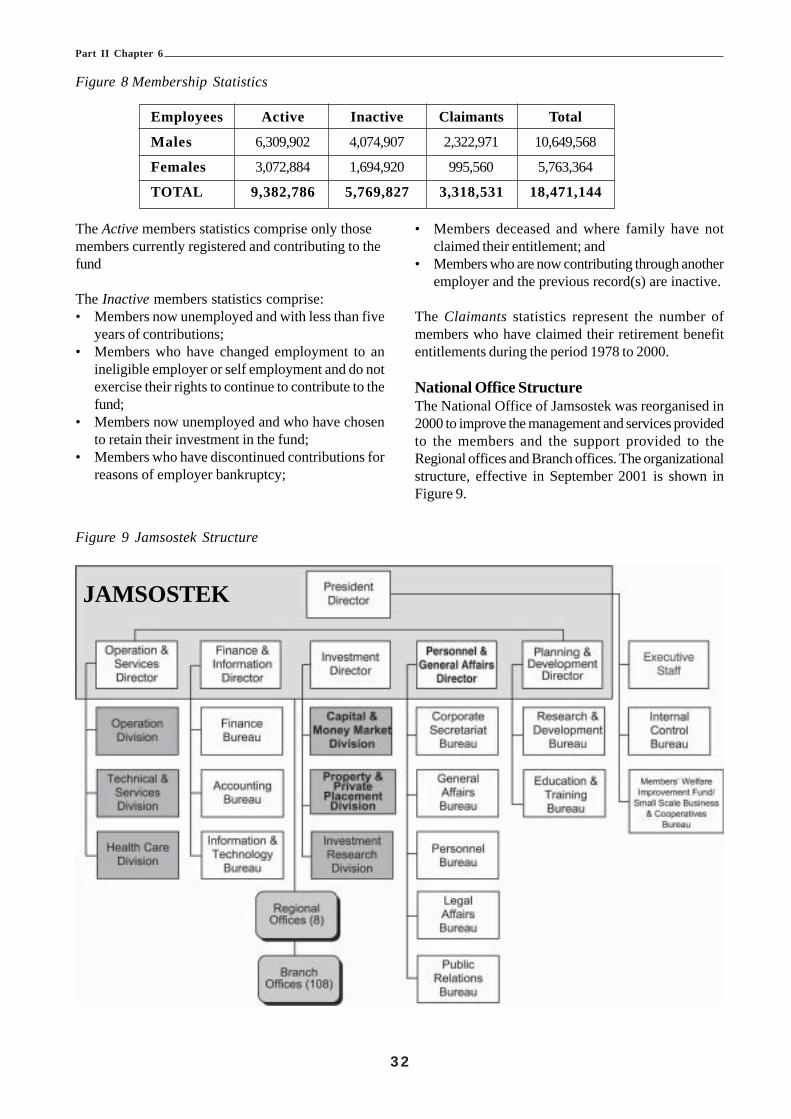

LIST OF FIGURES AND TABLESFigure 1 Social Security Responsibilities .......................................................................................................................... 5Figure 2 Indonesian Social Security System - Overview .................................................................................................. 7Figure 3 Table of Labour Force and Social Security Statistics .......................................................................................... 8Figure 4 Table of Membership Statistics .........................................................................................................................11Figure 5 Jamsostek Programs Overview ..........................................................................................................................12Figure 6 Possible Form of Jamsosnas Council .................................................................................................................19Figure 7 Labour Force Statistics ......................................................................................................................................25Figure 8 Membership Statistics .......................................................................................................................................26Figure 9 Jamsostek Structure ...........................................................................................................................................26Figure 10 President Director ..............................................................................................................................................27Figure 11 Operations and Services Directorate .................................................................................................................27Figure 12 Finance and Information Directorate .................................................................................................................27Figure 13 Investments Directorate ....................................................................................................................................27Figure 14 Personnel and General Affairs Directorate .........................................................................................................28Figure 15 Planning & Development Directorate ................................................................................................................28Figure 16 Regional Office Locations .................................................................................................................................28Figure 17 Service Delivery Network ..................................................................................................................................29Figure 18 Regional Office Structure ...................................................................................................................................30Figure 19 Branch Office Structure .....................................................................................................................................31Figure 20 Contributions Overview ....................................................................................................................................32Figure 21 Retirement Programs Claim Process ...................................................................................................................33Figure 22 Work Injury Program Claims Process .................................................................................................................34Figure 23 Health Care Registration ....................................................................................................................................36Figure 24 Health Care Treatment and Payment Process ....................................................................................................36Figure 25 Current Balance Sheet .......................................................................................................................................37Figure 26 Investment Management Process .....................................................................................................................39Figure 27 SIPT Context Diagram ........................................................................................................................................40Figure 28 Existing Communications Summary ...................................................................................................................41Figure 29 Proposed Communications Summary (first stage) .............................................................................................42Figure 30 Existing IT Organization ....................................................................................................................................43Figure 31 IT Organization (Proposed) ...............................................................................................................................44Figure 32 Regional Office IT Section .................................................................................................................................45Figure 33 Branch Office IT Organization ...........................................................................................................................46Figure 34 Software Inventory ............................................................................................................................................46Figure 35 SIPT Overview Diagram .....................................................................................................................................47Figure 36 Current Data Architecture .................................................................................................................................48Figure 37 Hardware - Server Summary ...............................................................................................................................49Figure 38 Jamsostek Employee Membership Card ............................................................................................................53Figure 39 National Index Sample Data ...............................................................................................................................57Figure 40 The National Index in a single site .....................................................................................................................58Figure 41 Inter Branch record updates ..............................................................................................................................58Figure 42 Interim National Index Option ............................................................................................................................60Figure 43 Overlap between Social Security Customers .....................................................................................................63Figure 44 Typical Social Security Customer Lifecycle .......................................................................................................63Figure 45 Business Re-engineering ...................................................................................................................................69Figure 46 Initial Business Reengineering Plan for Jamsostek ............................................................................................70Figure 47 Table of Jamsostek Contributions .....................................................................................................................76

List of Figures and Tables

x

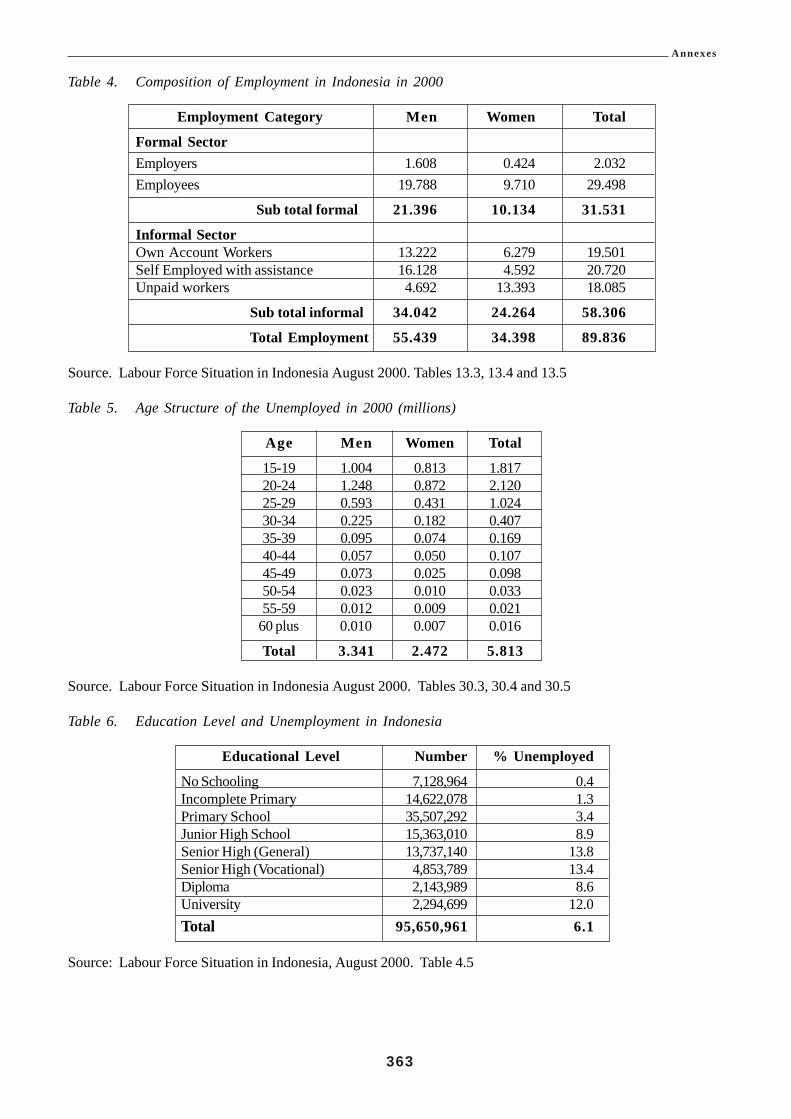

Figure 49 Table of Coverage of Jamsostek, 2000 ............................................................................................................... 81Figure 50 Table of Breakdown of Contribution Rates of Jamsostek ..................................................................................81Figure 51 An Example of Jamsostek Annuity ....................................................................................................................91Figure 52 Estimated Actuarial Annuity Factors at Age 55 for Selected Interest Rates & Guarantee Periods ...................92Figure 53 Social Security Priorities for Workers in the Informal Economy ........................................................................99Figure 54 Table of Estimated Benefits under the Defined-Benefit Option in 2001 Prices................................................. 107Figure 55 Table of Membership Statistics of Jamsostek .................................................................................................. 112Figure 56 Table of Labour Force, Employment and Jamsostek Membership ................................................................... 112Figure 57 Table of Schemes, Contributions and Benefits in Jamsostek ........................................................................... 116Figure 58 Table of Amount of Benefit Expenditure & Number of Cases ......................................................................... 118Figure 59 Table of Employment Injury Contributions and Benefit Data 1994- 2001 ......................................................... 120Figure 60 Table of Number of Cases of Withdrawal ........................................................................................................ 120Figure 61 Table of Income and Expenditure – Employment Injury for Construction Industry ........................................ 120Figure 62 Table of Death Benefits by Cases, Contributions and Benefits ....................................................................... 121Figure 63 Table of Female Sex Ratios in the Asian Region ............................................................................................. 126Figure 64 Table of Age-specific Female Sex Ratios in Indonesia ..................................................................................... 126Figure 65 Population 15 Years of Age and over by Age Group and Types of Activity ................................................... 128Figure 66 Table of Female Employees Wages: Salaries per Month by Region (August 2000) ........................................ 128Figure 67 Table of Maternal Deaths and Births in Hospitals in Indonesia year 2001 ...................................................... 128Figure 68 Table of Distribution of Patients By Gynaecological Problems in Hospitals during 1999 ................................ 129Figure 69 Table of Distribution of Patients receiving Gynaecology Treatment by Age (1999) ....................................... 129Figure 70 Table of Assumed Average Wage Calculations .............................................................................................. 131Figure 71 Table of Programme Calculations and cost Estimates ...................................................................................... 131Figure 72 Table of Jamsostek Programmes as % of Operating Costs .............................................................................. 146Figure 73 Average Weekly Cost per Benefit Paid ............................................................................................................ 147Figure 74 Cost per Beneficiary per Benefit Payment Paid ................................................................................................ 148Figure 75 Annual Claims Grants ...................................................................................................................................... 148Figure 76 Costs of alternative Replacement Rate and Time Duration of Benefit Payments ............................................. 148Figure 77 Table of Contribution Costs ............................................................................................................................ 149Figure 78 Table of Non-oil Subsidies ............................................................................................................................... 154Figure 79 Table of Five Leading Causes of Death from Series of Household Health Survey .......................................... 170Figure 80 Table of Health Care Financing in Selected Countries in Asia, 1997................................................................ 171Figure 81 Government Allocation of Health Services as Percent of Total Government Expenditures ............................. 172Figure 82 Visit Rates for Any Outpatient Care by Income Deciles, 1998 ......................................................................... 176Figure 83 Differences in Visit Rates for Primary Health Care Utilization by Income 1998 ................................................ 177Figure 84 Hospital Inpatient Days per 1000 People by Income Groups and Insurance Status, 1998. .............................. 178Figure 85 Average Financial Burden of Households (times household monthly expenditure) ........................................ 178Figure 87 Memberships Growth of Health Insurance Component of (JPK) Jamsostek, 1991-2000 .................................. 187Figure 88 Table of Utilization Rates per 1,000 Members of JPK Jamsostek 1992-2000 ..................................................... 193Figure 89 Possible Design of Social Health Insurance Scheme in Indonesia .................................................................. 195Figure 90 Agenda for Universal Coverage in the Proposed Compulsory Health Insurance Scheme .............................. 196Figure 91 Table of Estimates of the People below Poverty Line ...................................................................................... 214Figure 92 Table of the Official BPS Poverty Line (in Rupiah). ......................................................................................... 215Figure 93 Table of Estimates of the Incidence of Poverty, 1996-1999. ............................................................................. 215Figure 94 Numbers Below the Poverty Line 1984 - 1999 .................................................................................................. 216Figure 95 Table on the Proportion of Population below the BPS Poverty Line by Province ........................................... 216Figure 96 Table on the Incidence of Poverty by Main Sector of Occupation (%) ........................................................... 217Figure 97 Table of Poverty Profile by Education Level of Household Head (%) ............................................................. 217Figure 98 Enterprises by Employment Sector .................................................................................................................. 219Figure 99 Workers by Sector and Industry 2000 ............................................................................................................. 221

List of Figures and Tables

xi

Figure 100 Table of Comparison between Formal and Informal Economy ......................................................................... 223Figure 101 Industry Groupings in the Informal Economy ................................................................................................. 224Figure 102 Composition of Employment in Indonesia in 2000 ........................................................................................... 224Figure 103 Government Stakeholders in the Informal Economy ........................................................................................ 224Figure 104 Distribution of Formal Sector Enterprises ........................................................................................................ 229Figure 105 A Social Insurance Model based on Self-help Groups .................................................................................... 241Figure 106 A Possible Organization for a Social Security Pilot ......................................................................................... 243Figure 107 Table - Destination of Migrant Workers by Region ......................................................................................... 244Figure 108 Regional Office Locations ............................................................................................................................... 247Figure 109 Jamsostek Program Cost estimate 1997 ............................................................................................................ 248Figure 110 Summary of Estimated Transaction Costs in Jamsostek .................................................................................. 249Figure 111 Table of Main Demographic Indicators of Indonesia, 1970-2000 ..................................................................... 252Figure 112 Table of Key Assumptions of the Population Projection (intermediate scenario), 1995-2050 .......................... 253Figure 113 Table of Key Results of the Population Projection (intermediate scenario), 2000-2050 ................................... 254Figure 114 Table of Growth Rates of Real GDP, 1983-2000 ................................................................................................ 254Figure 115 GDP by Sector 1983 – 2000 .............................................................................................................................. 255Figure 116 Table of Growth Rates of the Labour Productivity, 1989-2000 ......................................................................... 255Figure 117 Table of Growth Rates of Employment, 1987-2000 ........................................................................................... 255Figure 118 Employment by Sector 1990 - 2000................................................................................................................... 256Figure 119 Labour Force Participation Rates by Sex, 1986 – 2000 ..................................................................................... 256Figure 120 Labour Force Participation Rates by Age Group 1986 – 2000 .......................................................................... 257Figure 121 Open Unemployment Rates by Age Group 1986 - 2000 ................................................................................... 257Figure 122 Table of Key Economic Assumptions, 2001-2030 ............................................................................................ 258Figure 123 Percentage of Workers in Formal Sector and Informal Economy 1986 – 2000 .................................................. 260Figure 124 The Social Budgeting Process ......................................................................................................................... 262Figure 125 Table of Taspen Financial Indicators ............................................................................................................... 263Figure 126 Askes Basic Indicators 1995, 1999 ................................................................................................................... 264Figure 127 Table of Social Insurance Expenditure and Revenue, 2000-2030...................................................................... 266Figure 128 Table of Social I nsurance Expenditure by Benefit, 2000-2030 ......................................................................... 267Figure 129 Old age and Short Term Benefits as % of GDP ................................................................................................ 268Figure 130 Short Term Benefits as % of GDP .................................................................................................................... 268Figure 131 Components of the Klaten IHR........................................................................................................................ 276Figure 132 Initial Budget Proposals for 1996-98 ................................................................................................................ 279Figure 133 Table of Project Finance 1988-99...................................................................................................................... 283Figure 134 Target Achievement by March 1999 ................................................................................................................ 284

List of Figures and Tables

xiii

GLOSSARYASABRI Social insurance system designed to provide

pension and endowment insurance benefitsto Indonesian Armed forces personnelAsuransi Sosial Angatan BersenjataRepublik Indonesia

ASKES PT Askes, (PT Asuransi KesehatanIndonesia), the State-owned, autonomous,for-profit insurance company administeringthe Public Service health insurance schemefor government civil servants, their familiesand for government civil service retirees. Italso provides health care service on behalf ofAsabri for members of the armed forces andtheir families.

ASTEK A state corporation (Perum) established in1990 and responsible for Employees SocialSecurity. Changed to JAMSOSTEK (Persero)in 1995.

BAPEL The carrier of JAMSOSTEK health insuranceprogramme also known as JPKM

BAPPENAS The National Development Planning agency

BBP Basic Benefit Package - essential healthservices in regulation Menkes #527

BPS Busan Pusat Statistik. The National StatisticsAgency in Indonesia

BUMD Badan Usaha Milik Daerah, - is a form ofcompany owned by local a government, eitherfully (100% shares) or partially. Unlike BUMN,these local companies are not sub-dividedinto several stages/forms. The objective ofBUMD is also profit.

BUMN (Badan Usaha Milik Negara) - is a legal statusof state-owned companies. The structure ofthis type of company is that of an ordinarypublic corporation in which there is a boardof directors and commissioners. Normally, theboards are drawn from civil servants orgovernment employees (including militarypersonnel). There are three tiers of BUMN:

Perjan (Perusahaan Jawatan) is the lowestlevel of companies, attached to certainministries for the purpose of technicaloversight. They are under the supervision ofthe Ministry of Finance for financial matters.In the health sector for instance, currently 13

central hospitals are being transformed intoPerjans. Under this status, the company isnot subject to the government accountingsystem. The mission of this type of companyis to provide services or goods to the public.In terms of financial goals, the company maypursue profits but must take intoconsideration its social objectives. Perjansmay receive subsidies from the government.

Perum (Perusahaan Umum) is the second stage ofprivatization. This type of company must befinancially independent and may not receivesubsidies from the government. A ministrystill holds the authority to oversee technicalaspects while the Ministry of Finance willoversee financial aspects. Any profitgenerated from the operation must be sharedwith the General Treasurer.

PT. Persero (Perseroan Terbatas) is the third stage ofprivatization of government institutions. Inthis form, all shares are owned by thegovernment but the company is managed asa fully private corporation with its goal tomaximize profit. The Indonesian socialsecurity system (comprised of: PT Jamsostek,PT Askes, PT Taspen and PT Asabri) ismanaged by Perseros but it is now consideredto be inappropriate for administration of socialsecurity.

Contract Doctor Postgraduate non-civil service doctor 2-3 year non-renewable contract

CV Perseroan Komanditer/ComanditairVenootschap is a type of proprietorship torun a business between individual(s) whois(are) willing to manage the business andtake full responsibility including privateassets of the other proprietor(s) not wishingto manage the business but willing only toassume limited responsibility in accordancewith their assets invested in the company.

DANA ALOKASI KHUSUS special allocationfunds.

DANA SEHAT Health fund a form of community healthcare financing or a micro financing schemethat was introduced by the Ministry of Healthand or a community initiative to share theburden of health care among the members ofthe community. Membership is voluntary,contribution level is based on consensus, andthe benefits are normally limited to healthservices in public health centre.

Glossary

xiv

DEPKES (Departemen Kesehatan) Department ofHealth.

DEPNAKERTRANS Depertamen Tenaga Kerja DanTransmigrasi. Department of Manpower andTransmigration

DINAS KERJA The provincial organization that hasassumed the responsibilities of localDepnakertrans functions under regionalautonomy. A Dinas is a district governmentorganization.

DINAS KESEHATAN District or Provincial HealthOffice.

DUKM Dana Upaya Kesehatan Masyarakat (healthfunds for the people)

FIRMA Firma is an establishment in the form of apartnership to run a business in a commonname with shared responsibility and profits.

FORMAL SECTOR The formal sector represents themore administratively visible part of theeconomy and society, namely the public andprivate corporate sector and comprisesenterprises and the professional self-employed that have been accorded LegalStatus and are regarded as legal entities

GOI Government of Indonesia

HMB A licensed JPKM company established inKlaten

HSF the Health Sector Finance Project

ICW Colonial Dutch law requiring remittance of allpublic revenues

IHCR Integrated Healthcare Reform

IJIN DIPARDA/SIUP Ijin Diparda is a specialpermit for establishments dealing in tourismin the form of Surat Ijin Usaha Pariwisata(SIUP) which is a business permit issued bythe tourist board in the local government.Included in this category are touristbusinesses operating under local governmentpermit other than a Diparda i.e. legal enterprisewithout a tourist permit.

INFORMAL ECONOMY The urban informal economycomprises those individuals and employersthat have not been accorded legal status andhave commenced their operations oftenwithout the sanction or knowledge of thelocal authorities (e.g. cottage workers)

JABOTABEK Jakarta – Bogor – Tangerang – Bekasi.The title given to the conglomeration ofJakarta and the surrounding cities.

JAMSOSTEK PT Jaminan Sosial Tenaga Kerja. The statecorporation (Persero) established in 1990 andresponsible for Employees (private sector)Social Security. Changed to JAMSOSTEKfrom ASTEK in 1995.

JASINDO Parastatal insurance company

JPKM Jaminan Pemeliharaan Kesehatan Masyarakat(or Jaring Pengaman Kesehatan Masyarakat)(JPKM) – translated as ‘Community HealthMaintenance Protection’ currentlyadministered as a Directorate of the Ministryof Health.

JPS Social Safety Net (General)

JPS-BK Social Safety Net (Health)

KARTU KELUAGA Family identity card issued bylocal administrations to the head of the family

KARTU SEHAT Health card issued to poor families toprovide them with free care in public healthcentre or public hospitals. It was introducedwhen the government launched a social safetynet program during the financial crisis in 1998.

KJKHM A secondary level dedicated servicecooperative established in Klaten

Klaten A district in South Central Java

KOPERASI Cooperative is an economic organisationbased on social spirit and comprised ofindividual and company members under amutual ownership system.

KTP KARTU TANDA Personal Identity cardissued by local administrations to allresidents.

LAN Local Area Network

LEGAL ENTITY An enterprise that has legal authority inthe form of Perum, PD, PT,/NV, CV, Firma,Koperasi, Yayasan, SIPD, Diparda, Villagecredit scheme, foreign company etc.

Ltd/Corporation Legal status of foreign enterprises thathave licences to operate in Indonesia

MOH Ministry of Health

Glossary

xv

PCD Post Contract Doctor

PD Perusahaan Daerah is a company of whichthe shares are owned by local governmentwith the assets separated from the localgovernment assets. A Perusahaan Daerah isrun for maximising profit to support localregional development.

PERATURAN PEMERINTAH G o v e r n m e n tRegulation.

PERJAN A Perjan is a non-profit oriented, governmentfunded departmental agency that provides aspecialized public service e.g. railways. Theother government public company types arePersero and Perum

PERSERO (PT) A Persero is a profit orientated, limitedliability, state company where thegovernment’s capital is based on shares,100% of which are owned by the government.The Ministry of Finance acts as a shareholderand the Ministry of State Owned Enterprisesis the authorized shareholder. The companyassets are separated from state owned assets.The other state company types are Perjan andPerum.

PERUM Perusahaan Umum Negara is a company notmerely aimed at making profit but also forproviding services to the public in the formof vital public utilities, by considering notonly its efficiency, effectiveness, economicaland its goods and services. The company’sentire capita is owned by the state and isdivorced from state owned assets. Thecompany can accept credit in the form ofgovernment bonds and can deal with othercompanies as part of its business. A typicalPerum is a non-profit oriented, public utilitycompany (e.g. electricity) that is not basedon shares divisions

Perum Husada Bhakti Previous name of Askes

Posyandu Health post

PT/NV. Perusahan Terbatas is a company owned byshareholders, with the shareholders assuminga limited liability no more than the nominalvalue of shares. Each shareholder has votingrights to participate in the running of thebusiness, depending on the number of sharesheld or by agreement among shareholders.PT is equivalent to Pty Ltd.

PTT Temporary contract healthcare employee ofthe government

Puskesmas Government health centre

RDU Rational Drug Use

RITSBLAAD/STAATSBLAAD Is an arrangement thatregulates the establishment of various villagecredits

GOVERNOR/BUPATI enterprises within Java andMadura.

SIPD (C class quarrying) is a local mining permit toconduct quarrying of rock, sand, clays, kaolinetc.

SWADANA Autonomous hospital

TASPEN Tabungan Asuransi Pegawai Negeri; Annuitypensions and endowment insurance benefitsscheme for government civil servants Pensiundan asuransi hari tua pagawai negeri sipil

USAID United States Agency for InternationalDevelopment

WAN Wide Area Network

YAYASAN A foundation that is a non-profit establish-ment mainly used for social service relatedpurposes with separately identified assets.

Glossary

xvii

FOREWORDSocial Security Reform is one of the great challenges facing Indonesia.The East Asian economic and financial crisis resulted in a significant increase in unemployment, underemploymentand poverty in Indonesia. It highlighted weaknesses in the social security system and increased the awareness ofthe need for change and improvement.The ILO has sought to assist in the process of change and improvement through the project “Restructuring ofthe Social Security System in Indonesia”, which was funded by the Government of the Netherlands.The ILO views the improvement of social security systems as part of an overall objective of providing decentwork for all men and women. The ILO believes that “decent work” is what workers throughout the world seek,namely work which is productive, which provides adequate income to meet their needs, in which their rights areprotected, and with adequate social protection.As part of the project, a series of research papers and reports were prepared by the Chief Technical Advisor andexpert consultants. The reports cover areas of crucial importance in improving the structure and operation of theSocial Security System in Indonesia and, in particular, the Employees’ Social Security Programme (Jamsostek).These include issues regarding:• Reform of pensions;• Options for improving benefits and arrangements in regard to work injuries;• Scope for provision of unemployment benefits and other social assistance to those unable to find work;• Ways in which the coverage of social security schemes might be extended to cover excluded groups (e.g.

migrant workers and those engaged in the informal economy); and• Administration of existing schemes – including the review of management operations and information technology;

and• Actuarial review of the current scheme and analysis of social security expenditure.The reports were presented to a meeting of stakeholders and experts held on 28-29 November 2002 in Jakarta.The consultation meeting brought together representatives of government, employers and workers together withmembers of the Presidential Task Force on Social Security Reform, managers of Jamsostek and other schemes,academics and NGOs. The main purpose of the consultation was to share the findings and get feedback fromparticipants in order to improve and finalize the reports and to consider how the reports might contribute to theSocial Security reform process in Indonesia, including the work of the Task Force. The proceedings included apresentation on the work of the National Task Force on Social Security Reform by its Chairman, ProfessorYaumil Achir.Following the consultations, the reports have been revised and collected together in this publication. The bookcontains a series of expert reports on major issues for consideration in the reform of social security in Indonesia.I believe that awareness about these issues, and discussion about realistic steps to be taken to improve bothaccess to social security and the type and level of benefits available, are essential to the development of aneffective plan of action to improve social security protection for workers in Indonesia. The ILO is highlightingsuch issues through its global campaign on Social Security and Coverage for All.Finally, I would like to thank and congratulate the persons involved in the project and in the preparation of thispublication. In particular I would like to thank Mr. Mike Smith, the Chief Technical Adviser of the project, and theconsultants who have prepared the reports. I would also like to thank the Department of Manpower andTransmigration for its support and collaboration throughout the project. In this regard I would like to acknowledgethe contribution of Mr. Syaufii Syamsuddin, National Project Director and Mr. Masri Hasyar, Director of SocialSecurity in the Department. The ILO is pleased to have been able to work with the Department on this importantexercise. The ILO is also most grateful for the support of the Dutch Government throughout the project.We trust that this book will be a valuable reference source for those concerned with the development of a bettersocial security system in Indonesia.

Alan BoultonDirectorILO Jakarta OfficeDecember 2002

Forward

xix

he International Labour Office has been involved in the development of social security in Indonesia formore than 20 years but during the last decade this has been limited to technical advice drawing attentionto the weaknesses in the national social security system. The financial crisis again exposed these

weaknesses and following a further analysis in early 1999 and an increased level of public criticism againstJamsostek (the social security institution administering social security for the private sector), the ILO providedresources for short-term technical assistance between September and December 1999. The need to restructurethe social security system and, in particular, to address the weaknesses of Jamsostek were analyzed by a NationalSteering Committee, established by the Ministry of Manpower in September 1999 to work with ILO specialists.This culminated in a National Workshop on the Restructuring of Social Security held in Jakarta on 16/17 November1999.

The report produced at the end of this technical assistance input (ILO/TAP/ Indonesia/R.20) set out recommendationsfor follow-up and the project: “Restructuring of the Social Security System” (INS/00/M04/NET) was implementedas a direct result of these recommendations. The objectives of the project were the establishment of a newinstitutional structure for the national social security scheme and the development of a national strategic plan forthe restructuring of the social security system.

The Director-General of the International Labour Office appointed Mr Michael Smith, an international expert onsocial security planning and administration as Chief Technical Adviser of the project. Also appointed were: MessrsJohn Angelini, Ole Nielsen, David Gent, Aniceto Orbeta, David Preston and Paguman Singh — respectivelyinternational experts on Information Technology; Actuarial Valuation; Pensions Policy; Labour Market Economy;Unemployment Insurance and Social Assistance Policy; and Occupational Injuries and Maternity Benefits Policy— to undertake detailed work on the studies. The Director General also appointed Mr Kenichi Hirose of the ILOSocial Security Finance, Actuarial and Statistical Services Branch and Mr Cristian Baeza of the ILO GlobalSTEP Programme to participate in the studies. Professor Sentanoe Kertonegoro, Dr Hasbullah Thabrany MD,Dr James R. Marzolf MD and Messrs Carunia Firdausy, Wendi Usino and Mrs Sofiati Mukadi were appointed asnational experts to the project. All the above national and international experts contributed in varying degrees tothe project reports and, therefore, to this publication. Mr Clive Bailey, Senior Social Security Specialist, of the ILOSocial Security Department, Geneva also contributed significantly — not only with material but also throughsupport to the project and to the cause of social security development in Indonesia over many years.

The Government Agency responsible for managing the project was the Department of Manpower andTransmigration (Depnakertrans) which appointed Mr Mohd. Syaufii Syamsuddin as National Project Director.From 1st August 2002 he was succeeded by Mr Masri Hasyar. Other cooperating agencies were the Departmentof Health and PT Jamsostek.

The purpose of this Publication is to present the series of studies undertaken during the project and others closelyassociated with it in a consolidated, readable form — hopefully with wider appeal than the formal project reportpresented to the government of Indonesia following the end of the project which ran from 1st April 2001 to 31st

December 2002 (with a break in project activities between 30th May and 1st August 2002). To this end, many ofthe Chapters in this Publication commence with their own Executive Summary.

This Publication was edited by Mike Smith, assisted by John Angelini.

INTRODUCTION

TIntroduction

xxi

n order to aid comprehension of the issues a listof definitions of social security terms used in thisPublication follows.

Social Security

The protection which society provides for its members,through a series of public measures against the distressthat otherwise would be caused by the stoppage orsubstantial reduction of earnings — resulting from:sickness, maternity, unemployment, invalidity, old age, ordeath. Social security also includes the provision of medicalcare and the provision of subsidies to families with children.

Social security is composed of:• Social Insurance;• Social Assistance;• Family Benefits;• Provident Funds; and• Provisions made by Employers such as:• Workmen’s Compensation Schemes; and• Other, complementary programmes.

Social Insurance

Social insurance is based on the principle of the pooling ofrisk. Thus everyone covered by a social insurance schememakes a contribution to a common fund. When a contributormeets the prescribed conditions for benefits ¾ his or herneeds (or at least part of them) are met from the insurancefund.

Social Insurance schemes may differ from one another buttheir principle elements are that:

• They are financed by contributions normally sharedbetween workers and employers, (often with some Stateparticipation);

• Require compulsory participation;• The contributions are paid into special funds out of

which benefits are paid.

In social insurance schemes:

• Surplus (reserve) funds are invested to earn furtherincome – returned to members through improvedbenefits;

• Benefits are guaranteed on the basis of the qualifyingconditions set out in the legislation, with regard to thepayment of contributions and without means testing(i.e. taking income and wealth into account);

• Contributions and benefit are often proportionate toearnings;

• Employment injury schemes are usually financed whollyby employers.

DEFINITIONSSocial Assistance

In social assistance schemes, benefits are provided as alegal right when the prescribed conditions are met. Generallyspeaking, means are taken into account when arriving atthe assessment of the benefit to be paid.

Social Protection

Social protection is a broader concept reflectinginternational economic and social change. It includes:• Social security; also• Private or non-statutory schemes.

Social protection also includes:

• Occupational or employer-based schemes;• Community based support systems; and• Micro-insurance schemes.

3-Tier Social Protection Systems

Many social protection systems consist of three tiers orlayers of protection:

! 1st Tier — a social safety net providing basic protectionsuch as primary health care and subsistence levelincome security (which would ordinarily be providedby the State, financed from taxes). 1st Tier PensionSchemes are, therefore, normally non-contributory. Tothe extent that the option of a 1st tier pension has beenconsidered under the present project, it will be mentionedin the Feasibility Study on Social Assistance.

! 2nd Tier — Social insurance schemes financed bycontributions from employers and workers – providingincome maintenance benefits during periods ofinterruption of employment and a broader range ofhealth care with some redistribution of income withinand between generations. The pension scheme optionsdiscussed in this report are 2nd Tier Pension Schemes(except where stated otherwise).

! 3rd Tier — Supplementary (voluntary) private provisionby individuals, employers or occupational schemes forpension savings and health insurance.

Defined Benefit Schemes

In defined benefit schemes the rules or the insurancecontract (in a public scheme, the provisions of thelegislation) clearly define the benefit rights of members (inline with a range of criteria: replacement rate, referenceearnings, duration, etc.) while leaving the contribution rateand the financial system to be set by actuarial assessment.

IDefinitions

xxii

Definitions

Members are thus guaranteed (and can predict) entitlementto a benefit representing a certain rate of replacement oftheir former earnings. Responsibility for the scheme’ssolvency is borne by those who finance it, usually employersand workers, who may be required to supplement theircontributions or to raise the book reserves which providefor the benefit payments. Sometimes governmentscontribute directly to the Fund or meet part of theadministration costs and, in the case of a public schemeestablished by law, government stands behind the promisesmade by the legislation and is the ultimate guarantor.

Defined Contribution Schemes

In defined contribution schemes, only the contribution ratesand bases of calculation are determined in advance. Thebenefit is a direct product of the contributions paid togetherwith the return on their investment. Consequently, thefinancial risk is borne by the employees. Benefit levels canvary significantly, depending on how the investmentsperform. There are no guarantees in this regard becausethe employer makes no commitment as to the value of thepensions. On the other hand the cost of the scheme iseasier to control.

Social Security Financing

(i) Pay-As-You-Go (PAYG)

Under PAYG systems of financing, no funds are set asidein advance (except for a small contingency reserve) andbenefits plus administrative costs are paid from currentcontributions. Each worker and employer pays a monthlycontribution into a common fund from which pensions arepaid to current pensioners who have contributed duringthe years when they were working. Thus currentcontributors pay for the benefits of current pensioners andincome is transferred vertically between generations. Risksare shared under a PAYG scheme. For example if an

unmarried worker dies say, one year after retirement, hispension dies with him. If his twin brother, also single, livesuntil he is 95 years old, he will have been paid a monthlypension for the whole of his life. In PAYG funding for short-term benefits (e.g. maternity benefit or unemploymentbenefit) financing is again by current contributionsrepresenting horizontal income transfer (i.e. within the samegeneration).

Given the pattern of rising annual expenditures in socialinsurance schemes, contribution rates (as a percentage ofinsured earnings) tend to be low in the early years of ascheme and increase annually for many years thereafter.

(ii) Advance Funding

With advance funding systems the annual contribution andinvestment income will exceed annual outgo on benefitsand administrative costs in the early years allowing reservesto be built up that are available for investment. The returnon investments is then used to supplement contributionincome when the annual disbursement eventually exceedsthe annual contributions. This build-up of reserves duringthe early years delays the need to increase contributionrates. But the contribution rate should not exceed thecapacities of workers, employers and the economy tosupport it; the reserves generated should not exceed thecapacity of the country to absorb the investments; andcontribution rates should remain relatively stable forextended periods of time ¾ with only gradual increases.

(iii) Funding from Taxation

Some social security schemes, particularly social assistanceand residence-based schemes, are funded through taxation.As there is no direct link between the sums paid by anindividual by way of tax and the amount of benefit that heor she may receive, funding from taxation is generally lesspopular than other forms of social security financing.

1

General Background

The development of social security in Indonesia canbe seen as having had the following majorcharacteristics:• A strong reliance on the extended family and

communities to provide an informal social safety netagainst loss of income, ill health or other misfortune;

• Limited reliance on employers through labourlegislation reinforced by collective agreements, todirectly provide benefits such as wages duringsickness and maternity and on termination ofemployment;

• Only limited social insurance for the private sectorwith reliance on the provident fund system to providea lump sum on retirement;

• An integrated package of conditions of service andsocial benefits for civil servants and members of thearmed forces.

Responsibility for the different elements of the systemis spread between different Ministries and publicorganisations. The Department of Manpower andTransmigration is responsible for the labour legislationand for the supervision of Jamsostek and theimplementation of its related legislation; the Ministryof Finance acting for the Ministry of State OwnedEnterprises is responsible for the oversight of all publiclimited liability companies (Perseros such asJamsostek, Askes and Taspen) as well as for thesupervision of insurance companies and pensionschemes; the Ministry of Health is responsible for theprovision of health care but health insurance schemesare implemented by PT Jamsostek and PT Askes. Theresponsibility for Social Welfare has been passedbetween the National Social Welfare Agency, theMinistry of Health & Social Welfare and the Ministryof People’s Welfare. This division of responsibilitytogether with the absence of a clear strategy or anycoordinating mechanism has resulted in a piecemealapproach to social security development and to someuncertainty and policy inconsistency. There have alsobeen differing views as regards the respective rolesand responsibilities of the public and private sector in

PART I SOCIAL SECURITY DEVELOPMENT BACKGROUND

CHAPTER 1 THE ILO PROJECT — RESTRUCTURING THE SOCIALSECURITY SYSTEM

the provision of social security. The general inabilityof existing social security institutions to provideeffective social protection in response to the needsexposed by the crisis reopened general concerns as tothe structural weaknesses and the management of thesystem and in particular of Jamsostek. This linkedwith reports of political interference and themismanagement of funds stimulated calls for the reformof Jamsostek from various quarters.

The need to restructure the social security system and,in particular, to address the weaknesses of Jamsostekwere analysed by a National Steering Committee,established by the Ministry of Manpower in September1999 to work with ILO specialists. This culminated ina National Workshop on the Restructuring of SocialSecurity held in Jakarta on 16/17 November 1999 whichresulted in the following conclusions:• There is a need to define the respective roles of the

State, the private sector, employers and individualsin providing social protection and a strategy forreform of the social security system should be devisedon this basis;

• Jamsostek should remain the core of the system butits legal status should be changed to reflect this sothat it should be constituted on trust fund principleswith a tripartite supervisory body comprised ofrepresentatives of the Government, employers andworkers;

• There is a need to improve the benefit programmeto include, for example, pensions for private sectorworkers, extended access to health insurance,maternity benefits and to consider the feasibility ofunemployment benefit;

• The scheme should extend coverage to at least allthose who work as employees and progressively alsoto the self-employed;

• The investment programme of the scheme must beboth more professional and more transparent;

• The service to insured persons and employers mustbe improved and linked to prescribed performanceindicators and targets;

• Strengthening of compliance and enforcement wasessential and combined with improved service and

Part I Chapter 1

2

public relations would, to an extent, address thecoverage problem;