skyway aviation handling company plc (rc:813022)€¦ · aviation handling company limited acquired...

TRANSCRIPT

SKYWAY AVIATION HANDLING COMPANY PLC

(RC:813022)

31 DECEMBER 2018

CHARTERED ACCOUNTANTS

GBENGA BADEJO & CO.

FINANCIAL STATEMENTS

FOR THE YEAR ENDED

SKYWAY AVIATION HANDLING COMPANY PLC

TABLE OF CONTENTS PAGE

CORPORATE INFORMATION 2-3

FINANCIAL HIGHLIGHTS 4

REPORT OF THE DIRECTORS 5-8

STATEMENT OF DIRECTORS' RESPONSIBILITIES 9

REPORT OF THE INDEPENDENT AUDITORS 10-15

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME 16

STATEMENT OF FINANCIAL POSITION 17

STATEMENT OF CHANGES IN EQUITY 18

STATEMENT OF CASH FLOWS 19

NOTES TO THE FINANCIAL STATEMENTS 20-70

OTHER NATIONAL DISCLOSURES:

VALUE ADDED STATEMENT 71

FIVE YEAR FINANCIAL SUMMARY 72

1

SKYWAY AVIATION HANDLING COMPANY PLC

CORPORATE INFORMATION

BOARD OF DIRECTORS: Barrister (Dr.) Afolabi Taiwo Chairman

Mr. Agboarumi Basil Managing Director (Appointed w.e.f. Sept. 18, 2018)

Mrs. Afolabi Abosede Folashade Director (Resigned w.e.f. Sept. 18, 2018)

Mr. Ariyo Olutoye Director

Barrister Oladipo Kayode Filani Director

Mr. Babatunde Afolabi Director (Appointed w.e.f. Sept. 18, 2018)

Captain Shehu Iyal Director (Appointed w.e.f. Sept. 18, 2018)

Mr. Anogwi Anyawu Director (Appointed w.e.f. Sept. 18, 2018)

Mr. Olaniyi Adigun Director (Appointed w.e.f. Sept. 18, 2018)

Mrs. Boma Ukwunna Director (Appointed w.e.f. Sept. 18, 2018)

Barr. Chike Ogeah Director (Appointed w.e.f. Sept. 18, 2018)

Dr. Oluropo Owolabi Director (Appointed w.e.f. Sept. 18, 2018)

PRINCIPAL OFFICERS: Agboarumi Basil Managing Director/CEO

Adigun Olaniyi Director -Sales and Marketing

Ukwunna Boma Director - Cargo Services

Oriowo James AGM- Engineering and Maintenance

Olugbenga Okeowo AGM- Operations

Omolara Bello Head - Legal/ Company Secretary

Ibrahim Amuda Head - Internal Audit

Omotoso Rotimi Head - Finance

Elegbede Folorunso Head - Human Resources

Oseghale Christie Head -Safety and Quality Assurance

Okunlola Adebowale Head -Security

Ogungbemi Yinka Head - Administration

REGISTERED OFFICE/ 54 Warehouse Road, Apapa, Lagos

OPERATIONAL OFFICE ADDRESS: Skyway Aviation Handling Company Plc Complex,

Cargo Terminal,

Murtala Muhammed International Airport,

Ikeja,

Lagos.

COMPANY SECRETARY: Omolara Bello

Skyway Aviation Handling Company Plc Complex,

Cargo Terminal,

Murtala Muhammed International Airport,

Ikeja,

Lagos.

PRINCIPAL BANKERS: Ecobank Nigeria Limited

Guaranty Trust Bank Plc

Stanbic IBTC Bank Plc

First City Monument Bank Plc

Union Bank of Nigeria Plc

Skye Bank Plc (Now Polaris Bank Ltd)

United Bank for Africa Plc

First Bank Nigeria Limited

Zenith Bank Plc

Access Bank Plc

2

SKYWAY AVIATION HANDLING COMPANY PLC

CORPORATE INFORMATION (CONT'D)

INDEPENDENT AUDITORS Gbenga Badejo and Co.

(Chartered Accountants)

24 Ladipo Oluwole Street,

Off Adeniyi Jones Avenue, Ikeja, Lagos.

Tel.: 0809-622-7865.

SOLICITORS Kayode Filani and Co.

9 Odunuga Street,

Off Link Road,

Opebi,

Lagos.

Tel.: +2348033282855

Sceptre Law

2c Idowu Olaitan Street,

Gbagada Expressway,

Gbagada Phase II,

Lagos.

H.A. Olaniyan and Co.

2nd Floor Rear Block,

208 Ikorodu Road,

Palmgrove,

Lagos.

3

SKYWAY AVIATION HANDLING COMPANY PLC

FINANCIAL HIGHLIGHTS

FOR THE YEAR ENDED 31 DECEMBER 2018

2018 2017

₦'000 ₦'000 ₦'000 %

STATEMENT OF FINANCIAL POSITION ITEMS:

Total assets 23,086,459 14,542,492 8,543,967 58.75

Non current assets 19,335,032 11,650,946 7,684,086 65.95

Total liabilites 4,124,443 9,039,522 (4,915,079) (54.37)

Equity 18,962,016 5,502,970 13,459,045 244.58

Non -current laibilities 1,154,964 5,733,542 (4,578,578) (79.86)

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME ITEMS:

Revenue 6,136,412 4,981,278 1,155,134 23.19

(Loss)/Profit Before Income Tax (302,895) 125,901 (428,796) (340.58)

(Loss)/Profit for the year (665,649) 217,727 (883,375) (405.73)

Total other comprehensive (loss)/ income 9,088,895 - 9,088,895 100.00

RATIO:

Current Ratio 1.26:1 0.87:1

Net Profit (%) (11) 4 (15) (348.18)

Return on Capital Employed (%) (4) 4 (7) (188.73)

Gearing 9 28 (19) (68.83)

PER SHARE DATA

(Loss)/Earnings Per Share (Kobo) (49.18) 51.23 (100) (195.99)

Net Assets Per Share (Kobo) 1,401 1,295 106 8.19

Number of Issued Share Capital 1,353,580,000 425,000,000 928,580,000 218.49

Gearing ratio measures the proportion of a company's borrowed funds to its equity.

Earnings per share and net assets per share are based on profit after taxation, net assets and dividend proposed respectively and the

number of issued and fully paid ordinary shares at the end of each financial year.

Current ratio indicates a company's ability to pay its current liabilities from its current assets.

Return on capital employed (ROCE) ratio measures a company's profitability and the efficiency with which its capital is employed.

Increase/ (Decrease)

4

SKYWAY AVIATION HANDLING COMPANY PLC

REPORT OF THE DIRECTORS

FOR THE YEAR ENDED 31 DECEMBER 2018

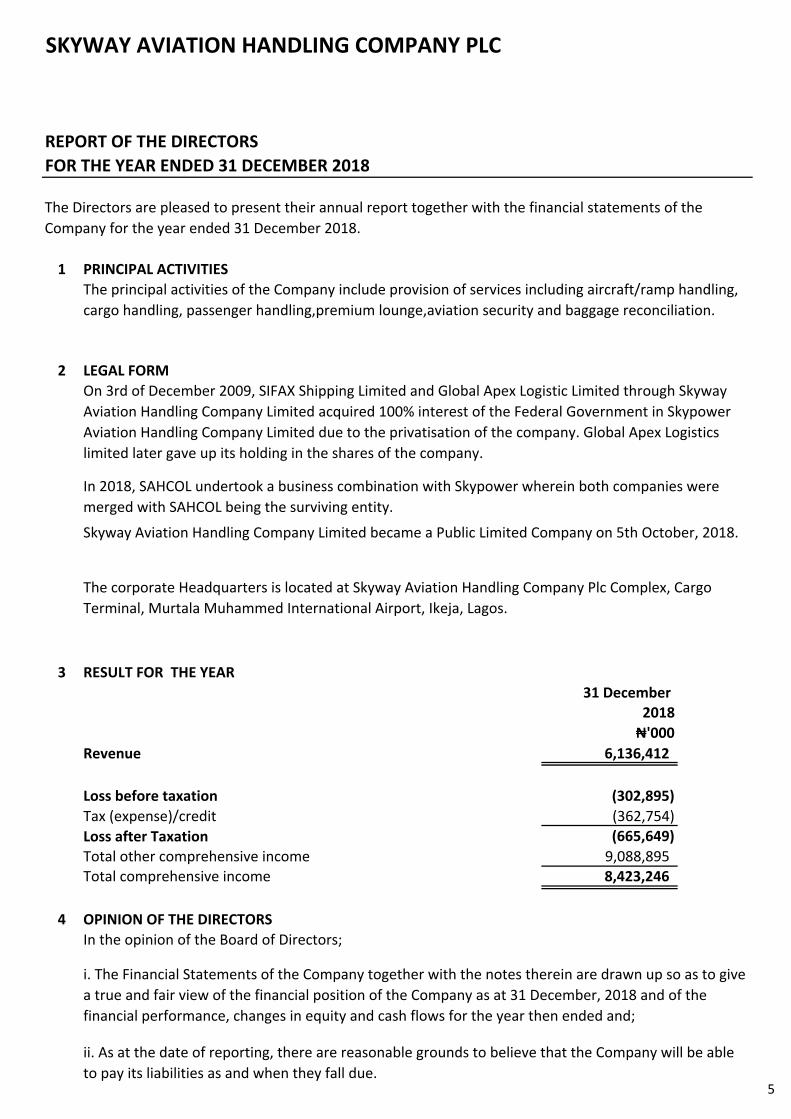

1 PRINCIPAL ACTIVITIES

2 LEGAL FORM

3 RESULT FOR THE YEAR

31 December

2018

₦'000

Revenue 6,136,412

Loss before taxation (302,895)

Tax (expense)/credit (362,754)

Loss after Taxation (665,649)

Total other comprehensive income 9,088,895

Total comprehensive income 8,423,246

4

The Directors are pleased to present their annual report together with the financial statements of the

Company for the year ended 31 December 2018.

The principal activities of the Company include provision of services including aircraft/ramp handling,

cargo handling, passenger handling,premium lounge,aviation security and baggage reconciliation.

On 3rd of December 2009, SIFAX Shipping Limited and Global Apex Logistic Limited through Skyway

Aviation Handling Company Limited acquired 100% interest of the Federal Government in Skypower

Aviation Handling Company Limited due to the privatisation of the company. Global Apex Logistics

limited later gave up its holding in the shares of the company.

The corporate Headquarters is located at Skyway Aviation Handling Company Plc Complex, Cargo

Terminal, Murtala Muhammed International Airport, Ikeja, Lagos.

OPINION OF THE DIRECTORS

In 2018, SAHCOL undertook a business combination with Skypower wherein both companies were

merged with SAHCOL being the surviving entity.

Skyway Aviation Handling Company Limited became a Public Limited Company on 5th October, 2018.

In the opinion of the Board of Directors;

i. The Financial Statements of the Company together with the notes therein are drawn up so as to give

a true and fair view of the financial position of the Company as at 31 December, 2018 and of the

financial performance, changes in equity and cash flows for the year then ended and;

ii. As at the date of reporting, there are reasonable grounds to believe that the Company will be able

to pay its liabilities as and when they fall due. 5

SKYWAY AVIATION HANDLING COMPANY PLC

REPORT OF THE DIRECTORS

FOR THE YEAR ENDED 31 DECEMBER 2018

5 DIRECTORS AND DIRECTORS' INTEREST

Direct Indirect Representing

Barr. Dr. Taiwo Afolabi 503,580,000 550,000,000 SIFAX Shipping Ltd

Barr. Chike Ogeah - - N/A

Dr. Oluropo Owolabi - - N/A

Bar. Oladipo Filani - - N/A

Mr. Olutoye Ariyo - - N/A

Mr. Babatunde Afolabi - - N/A

Captain Shehu Iyal - - N/A

Mr. Anogwi Anyawu - - N/A

Mr. Agboarumi Basil - - N/A

Mr. Olaniyi Adigun - - N/A

Mrs. Boma Ukwunna - - N/A

Direct Indirect Representing

Barr. Dr. Taiwo Afolabi - 275,000,000 Sifax Shipping Ltd

Barr. Chike Ogeah - - N/A

Dr. Oluropo Owolabi - - N/A

Bar. Oladipo Filani - - N/A

Mr. Olutoye Ariyo - - N/A

Mrs. Afolabi Folashade 150,000,000 - N/A

i. Mr. Babatunde Afolabi

ii. Captain Shehu Iyal

iii. Mr. Anogwi Anyawu

iv. Mr. Agboarumi Basil (Acted in acting capacity prior to full appointment)

v. Mr. Olaniyi Adigun

vi. Mrs. Boma Ukwunna

vii. Barr. Chike Ogeah

viii. Dr. Oluropo Owolabi

As at 31 December 2018

APPOINTMENT / RESIGNATION OF DIRECTORS

There were resignation and/or new appointment into the Board during the year. Mrs Afolabi Folashade

resigned from the Board on September 18, 2018 while the following Directors were newly appointed to the

Board on 18 September, 2018;

No of shares held (Unit)

As at 31 December 2017

The names of the Directors are detailed on page 2. The interests of the Directors in the Issued Share

Capital of the company are listed below in accordance with Section 275 and 342 of the Companies

and Allied Matters Act, CAP C20 LFN 2004:

No of shares held (Unit)

6

SKYWAY AVIATION HANDLING COMPANY PLC

REPORT OF THE DIRECTORS

FOR THE YEAR ENDED 31 DECEMBER 2018

6 DIVIDEND

The Board did not recommend any dividend for the reporting period.

7 EMPLOYMENT AND EMPLOYEES

(a) Employment of disabled persons:

(b) Health Safety and Welfare

(c) Employees Involvement and Training:

8 GIFTS AND DONATIONS

9 PROPERTY, PLANT AND EQUIPMENT

10 ACQUISITION OF OWN SHARES

The Company did not purchase any of its own shares during the year.

11 EVENTS AFTER REPORTING PERIOD

12 WHISTLE BLOWING POLICY

The Company is committed to fair and ethical business practices with transparency and integrity. Hence,

Skyway Aviation Handling Company Plc has a clear whistle blowing policy that ensures all employees

including prospective applicants, contractors agents, partners, bankers, other service providers, suppliers,

shareholders, host community and the general public are given a channel through which they can report all

matters they suspect of involving anything illegal, unethical, harmful and or improper. All matters reported

are accepted and treated with confidentiality of the identity of the whistle blower.

The Company has an employment policy which does not discriminate against the disabled persons.

The Company is fully committed to employees' well being and would continue to seek better ways of

guaranteeing their well being.

The Company attaches great importance to staff training and encourages employees to pursue self

development that will impact positively on the Company's service delivery. The Company is committed

to keeping employees as fully informed as possible regarding its focus, performance and progress.

No donation was made to any political organisation during the year. Charitable gifts of ₦15,800,000 were

given out in accordance with the Company's policy on social development and improvement of the

community, the environment and hygenic conditions of the less privileged.

Movements in property, plant and equipment during the year are shown in Note 12. In the opinion of the

Directors, the market value of the Company's property, plant and equipment are not less than the value

shown in the financial statements.

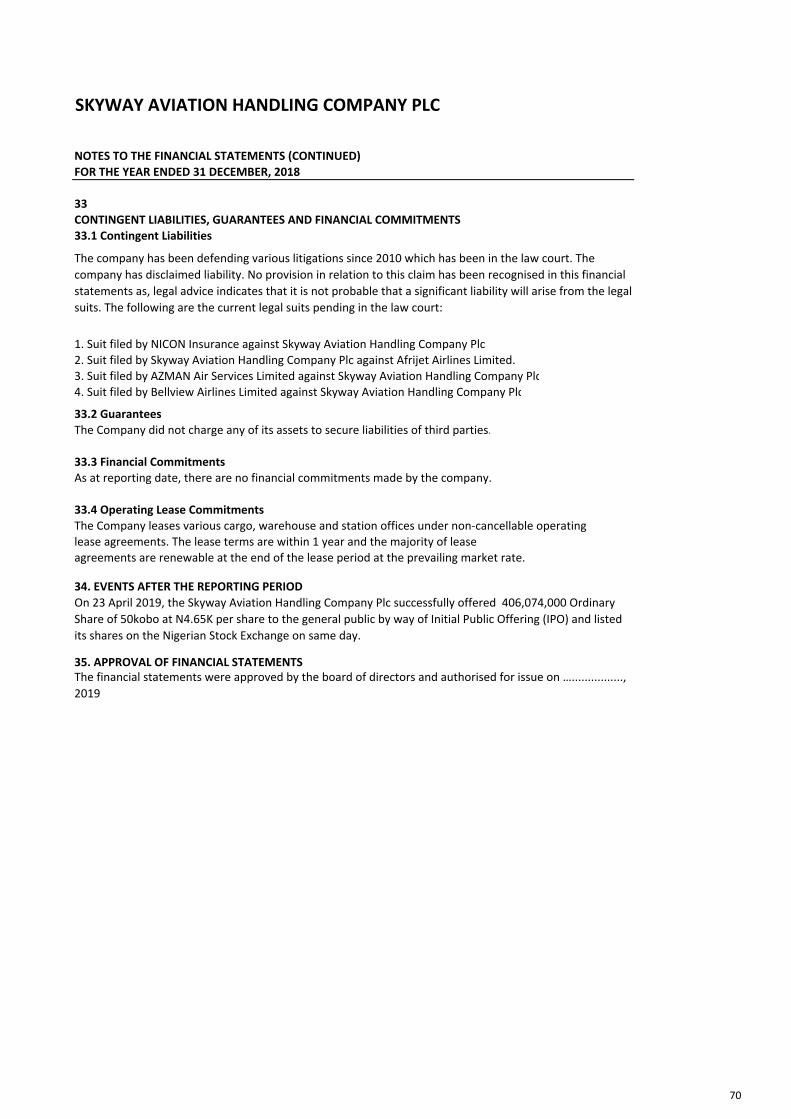

On 23 April 2019, the Skyway Aviation Handling Company Plc successfully offered 406,074,000 Ordinary

Share of 50kobo at N4.65K per share to the general public by way of Initial Public Offering (IPO) and listed its

shares on the Nigerian Stock Exchange on same day.

7

SKYWAY AVIATION HANDLING COMPANY PLC

REPORT OF THE DIRECTORS

FOR THE YEAR ENDED 31 DECEMBER 2018

13 COMPLAINTS MANAGEMENT POLICY

14 INSIDER INFORMATION POLICY

Skyway Aviation Handling Company Plc's Insider Information policy is to generally

ensure the board members, employees and its external stakeholders who have

knowledge of confidential and potentially price sensitive information are aware of

the prohibition imposed by law against using, disclosing (other than in the normal

course of the performance of their duties) or encouraging transactions in securities

on the basis of such insider information. In addition to obligations imposed by law,

Skyway Aviation Handling Company Plc wants board members, employees and

external stakeholders to respect the safeguarding of confidential information and

potentially price sensitive information.

Skyway Aviation Handling Company Plc is committed to providing high standards of

services for shareholders including a platform for efficient handling of shareholders'

complaints and enquiries, enabling shareholders to have shareholder related matters

acknowledged and addressed, providing sufficient resources to ensure the

shareholders' complaints and enquiries are dealt with adequately, and in an efficient

and timely manner and facilitating efficient and easy access to shareholders'

information.

The Company has therefore formulated a Complaint Management policy designed to

ensure the complaints and enquiries from the Company's shareholders are managed

in a fair, impartial, efficient and timely manner.

Furthermore, this policy has been prepared in recognition of the importance of

effective engagement in promoting shareholders / investors' confidence in the

company.

This policy sets out the broad framework by which Skyway Aviation Handling

Company Plc ("SAHCO PLC") and its Registrar will provide assistance regarding

shareholder issues and concerns. It also provides the opportunity for Skyway

Aviation Handling Company Plc's shareholders to provide feedback to the company

on matters that affect shareholders.

This policy only relates to the Company's shareholders and does not extend to its

customers, suppliers or other stakeholders.

The Company has a policy on insider information and prohibition of Insider dealings

as required by rules and regulations and the policy has been made publicly available

to all stakeholders.

8

SKYWAY AVIATION HANDLING COMPANY PLC

REPORT OF THE DIRECTORS

FOR THE YEAR ENDED 31 DECEMBER 2018

15 GOING CONCERN STATUS

16 APPROVAL OF FINANCIAL STATEMENTS

17 AUDITORS

BY ODER OF THE BOARD

Omolara Bello

Company Secretary

FRC NO. :

Dated this 25th June, 2019.

The Directors have made assessment of the Company's ability to continue as a

going concern and have no reason to believe that the Company will not remain a

going concern in the years ahead.

Resulting from the above, the directors have a reasonable expectation that the

company has adequate resources to continue operations for the foreseeable

future. Thus, directors continued the adoption of the going concern basis of

accounting in preparing the annual financial statements.

These financial statements for the year ended 31 December 2018 have been

approved for issue by the Directors on 25th June, 2019.

Messrs Gbenga Badejo and Co. (Chartered Accountants) have indicated their

willingness to continue in office as auditors of the Company in accordance with

the provisions of section 357 (2) of the Companies and Allied Act, CAP C20, LFN

2004. A resolution will be proposed authorising the Directors to fix their

remuneration.

9

SKYWAY AVIATION HANDLING COMPANY PLC

STATEMENT OF DIRECTORS' RESPONSIBILITIES

FOR THE YEAR ENDED 31 DECEMBER 2018

(a)

(b)

(c)

………………………………………….. …………………………………………..

Barr. (Dr.) Taiwo Afolabi Mr. Agboarumi Basil

Chairman Managing Director/CEO

FRC/2015/NBA/00000013106 FRC Number:

Date: 25th June, 2019 Date: 25th June, 2019

…………………………………………..

Mr. Rotimi Omotoso

Head - Finance

FRC/2016/ICAN/00000014593

Date:25th June, 2019

The Directors are of the opinion that the financial statements give a true and fair view of the state of

the financial affairs of the company and of its profit or loss. The directors further accept responsibility

for the maintenance of accounting records that may be relied upon in the preparation of financial

statement, as well as adequate systems of internal financial control. Nothing has come to the

attention of the directors to indicate that the company will not remain a going concern for at least

twelve months from the date of this statement.

The Companies and Allied Matters Act (section 334 and 335) , CAP C20 LFN, 2004 requires the

directors to prepare financial statements for each financial year that give a true and fair view of the

state of financial affairs of the Company at the end of the year and its profit or loss. The

responsibilities include ensuring that the company;

Keeps proper accounting records that disclose, with reasonable accuracy, the financial

position of the company and comply with the requirements of the Companies and Allied

Matters Act, CAP C20 LFN, 2004:

Establishes adequate internal controls to safeguard its assets and to prevent and detect fraud

and other irregularities; and

Prepares its financial statements using suitable accounting policies supported by reasonable

and prudent judgements and estimates, and are consistently applied.

The Directors accept responsibility for the financial statements, which have been prepared using

appropriate accounting policies supported by reasonable and prudent judgments and estimates, in

conformity with International Financial Reporting Standards as issued by the International Accounting

Standards Board, and the requirements of the Financial Reporting Council of Nigeria Act, No 6, 2011

and the Companies and Allied Matters Act, CAP C20 LFN, 2004.

10

REPORT OF THE INDEPENDENT AUDITORS

TO THE MEMBERS OF SKYWAY AVIATION HANDLING COMPANY PLC

BASIS FOR OUR OPINION

KEY AUDIT MATTERS

OPINION

We have audited the financial statements of Skyway Aviation Handling Company Plc (SAHCO PLC) herein referred

to as “the company”, which comprise of:

the company’s statement of financial position as at December 31, 2018;

the company’s statement of profit or loss and other comprehensive income for the year ended 31 December,

2018;

the company’s statement of changes in equity for the year ended 31 December, 2018;

the company’s statement of cash flows for the year ended 31 December, 2018;

the notes comprising a summary of the significant accounting policies and other explanatory information.

The accompanying Financial Statements give a true and fair view of the financial position of the company as at 31

December 2018 and its financial performance and cash flows for the year then ended in accordance with the

Companies and Allied Matters Act, CAP C20 LFN, 2004, the International Financial Reporting Standards (IFRSs)

except for Employee Benefits which is not in line with the provision of IAS 19 as issued by the International

Accounting Standards Board and in the manner required by Financial Reporting Council of Nigeria Act, No 6, 2011.

We conducted our audit in accordance with the International Standards on Auditing (ISAs) issued by the

International Auditing and Assurance Standards Board (IAASB) and Nigerian Standards on Auditing (NSAs) issued

by the Institute of Chartered Accountants of Nigeria (ICAN). Our responsibilities under those standards are further

described in the Auditors’ responsibilities for the audit of the Financial Statements section of our report. We are

independent of the company in accordance with the ICAN codes of ethics for professional accountants and we

have fulfilled our other ethical responsibilities in accordance with the code. We believe that the audit evidence we

have obtained is sufficient and appropriate to provide a basis for our opinion.

Key audit matters are those matters that in our professional judgments were of most significance in our audit of

the financial statements of the current period. These matters were addressed in the context of our audit of the

financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on

these matters.

11

REPORT OF THE INDEPENDENT AUDITORS (CONTD.)

TO THE MEMBERS OF SKYWAY AVIATION HANDLING COMPANY PLC

Key Audit Matter(s) How the matter was addressed in the Audit

Valuation of Employee Benefits Liabilities - See Note

20 to the Financial Statements.

Management has estimated the fair value of the

company’s End of Service Benefits to be N533.8million

as at 31st December 2018 with provision for the year

ended 31st December 2018 recorded in the profit or

Loss Account of N180.5 million. No Independent

external valuations were obtained to support

management’s estimates. The valuations by

management are dependent on certain key

assumptions that require significant management

judgement including discount rates and pay increase.

Our procedures in relation to the management's

valuation of Employee Benefits Liabilities include;

i. Evaluation of the key assumption and competence,

capabilities and objectivity of the management staff

involved in this estimation.

ii. Assessing the methodologies used by the

management to estimate the fair value.

iii. Checking on sample basis the accuracy and relevance

of the input data used by management to estimate

value in use.

iv. Our in-house expert review of the assumption of the

Management.

We found the key assumptions not adequate and

management had been notified to get an Independent

Valuers to estimate the fair value of the Employee

Benefits Liabilities.

Key Audit Matter(s) How the matter was addressed in the Audit

Goodwill - See Note 14 to the Financial Statements.

The company has recognised goodwill in the amount of

N 4.057billion as at 31 December, 2018.

The majority of the Goodwill had been allocated to

aircraft handling and cargo handling cash generating

units (CGUs).

Our audit procedure in this area includes

i. Evaluation of the appropriateness of the discount rate

applied, which includes comparing the weighted average

cost of capital with sector averages for the relevant

market in which the CGUs operate.

The annual impairment testing is considered to be a

key audit matter due to the complexity of the

accounting requirement and the significant judgement

required in determining the assumptions to be used to

estimate the recoverable amount. The recoverable

amount of the CGUs which is based on the higher of

the value in use or fair value less cost of sale has been

derived from discounted forecast cash flow model.

ii. Evaluating the appropriateness of the assumptions

applied to key inputs such as revenue, operating Costs,

inflation and long term growth rate which included

comparing these inputs with externally derived data as

well as our own assessment based on our knowledge of

the client and the industry.

iii. Performing our own sensitivity analysis, which

includes assessing the effect of possible reductions in

growth rates and forecast cash flows to evaluate the

impact on the currectly estimated recoverable amount.

We have determined the matters described below to be the key audit matters to be communicated in our report.

The key audit matters below relate to the audit of the financial statements.

12

REPORT OF THE INDEPENDENT AUDITORS (CONTD.)

TO THE MEMBERS OF SKYWAY AVIATION HANDLING COMPANY PLC

Goodwill - See Note 14 to the Financial Statements. How the matter was addressed in the Audit

This model uses several key assumptions including

estimates of future revenue, operating costs, terminal

value growth rate and the Weighted Average Cost of

Capital (WACC). The estimate is highly sensitive to

WACC and terminal growth rate

iv. Evaluating the adequacy of the financial statements

disclosures, including disclosure of key assumptions and

judgement.

Based on our review, We found the company's

impairment model, including assumptions and key

inputs used by the management to estimate recoverable

amount of the CGUs to be appropriate.

Receivable Loss Impairment: See Note 16 to the

Financial Statements.

How the matter was addressed in the Audit

The Company implemented IFRS 9 "Financial

Instruments" for the first time on 1 January 2018. IFRS

9 requires SAHCOL to recognize impairment using the

Expected Credit Loss (ECL) model. The ECL model is

dependent on significant judgement and estimates by

management in the measurement and determination

of impairment on Receivables and other financial

instruments. Our focus on this area was premised on

the significant judgement and subjectivity inherent or

applied by management in the estimation of the level

of impairment, and the size of this Receivables.

Our audit procedures to assess the Receivable loss

impairment included the following:

i. Updated our understanding of the controls put in

place by the management to identify impaired

receivables and provisions against those assets and

determined whether these controls have been

appropriately designed and implemented.

ii. We reviewed the appropriateness of the company's

determination of significant increase in credit risk and

ensured compliance with IFRS 9.

The ECL model is forward looking which incorporates

industry and prevailing economic events and requires

an application of historical financial data of the

Compay. All of these are combined to develop and

apply relevant models to the portfolio of the Company.

iii. We involved our internal credit specialists in the

review of the assessment of the overall compliance of

the model to the requirements of the IFRS 9.

Trade and other Receivables make up a significant

portion of the total assets of SAHCOL with the total risk

assets portfolio of N8.2 billion representing about 63%

of the Company's current assets. The total amount of

impairment on Receivables charged in the Statement of

Profit or Loss for the year is N215 million as stated in

note 16(a).

iv. We challenged the key data input and assumptions

for data input into the ECL model used by the Company.

v. We reviewed the transition adjustment though no

adjustment was recognized in the opening retained

earnings as at 1 January 2018.

The basis of the provisions is summarized in the

accounting policies in the financial statements (See

Note 4.13.2).

vi. On a sample basis, we reviewed recievables for

evidence of significant increase in credit risk with major

focus on receivables that were not reported as being

impaired.

13

REPORT OF THE INDEPENDENT AUDITORS (CONTD.)

TO THE MEMBERS OF SKYWAY AVIATION HANDLING COMPANY PLC

Receivable Loss Impairment: See Note 16 to the

Financial Statements.

How the matter was addressed in the Audit

SAHCOL's impairment model addresses the three

stages of credit classifications.

vii. We subjected the data used in the models to test as

well as assessing the model's methodology.

Because of the significance of these estimates,

judgments and the size of Trade Receivables, economic

conditions experienced in Nigeria during the year which

affected the performance of Receivables, the audit of

receivable's impairment is considered a key audit

matter.

Based on our review, we found that the company's

impairment methodology, including the model,

assumptions and key inputs used by management to

estimate the amount of receivable impairment losses

were comparable with historical performance, and

prevailing economic situations and that the estimated

receivable impairment loss determined was appropriate

in the circumstances.

Other information in the Annual Report

The directors are responsible for the other information. The other information comprises all the information in the

Skyway Aviation Handling Company Plc 2018 annual report other than the company financial statements and our

auditor’s report thereon (“the Other Information”).

Our opinion on the financial statements does not cover the other information and we do not express any form of

assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the Other Information and, in

doing so, consider whether the other Information is materially inconsistent with the financial statements or our

knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have

performed, we conclude that there is a material misstatement of this other Information; we are required to report

that fact. We have nothing to report in this regard.

Responsibilities of the directors and those charged with Governance for the Financial Statements

The directors are responsible for the preparation and fair presentation of the financial statements in accordance

with International Financial Reporting Standards and the requirement of the Companies and Allied Matters Act

CAP C20 LFN 2004, circulars and guidelines issued by the Financial Reporting Council Act 2011 and for such

internal control as the directors determine is necessary to enable the preparation of financial statements that are

free from material misstatement, whether due to fraud or error.

In preparing the financial statements, the directors are responsible for assessing the company’s ability to continue

as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of

accounting unless the directors either intends to liquidate the company or to cease operations, or have no realistic

alternative but to do so.

14

REPORT OF THE INDEPENDENT AUDITORS (CONTD.)

TO THE MEMBERS OF SKYWAY AVIATION HANDLING COMPANY PLC

iii. Evaluate the appropriateness of accounQng policies used and the reasonableness of accounQng esQmates and

related disclosures made by directors.

Auditors' Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free

from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our

opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in

accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from

fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to

influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional

skepticism throughout the audit. We also:

i. Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error;

design and perform audit procedures responsive to those risks; and, obtain audit evidence that is sufficient and

appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from

fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions,

misrepresentations, or the override of internal control.

ii. Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are

appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the

internal control.

iv. Conclude on the appropriateness of directors’s use of the going concern basis of accounQng and, based on the

audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast

significant doubt on the company’s ability to continue as a going concern. If we conclude that a material

uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the

financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on

the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may

cause the company to cease to continue as a going concern.

v. Evaluate the overall presentation, structure and content of the financial statements, including the disclosures,

and whether the financial statements represent the underlying transactions and events in a manner that achieves

fair presentation.

vi. We communicate with the Directors regarding, among other matters, the planned scope and timing of the audit

and significant audit findings, including any significant deficiencies in internal control that we identified during our

audit.

vii. We also provide the Directors with a statement that we have complied with relevant ethical requirements

regarding independence, and to communicate with them all relationships and other matters that may reasonably

be thought to bear on our independence, and where applicable, related safeguards.

15

REPORT OF THE INDEPENDENT AUDITORS (CONTD.)

TO THE MEMBERS OF SKYWAY AVIATION HANDLING COMPANY PLC

Report on other legal requirements

Adesuyi Oluwayomi Bamidele, FCA

FRC/2014/ICAN/000000007990,

Engagement Partner,

Gbenga Badejo & Co.,

(Chartered Accountants),

24, Ladipo Oluwole Street,

Off Adeniyi Jones Avenue,

Ikeja, Lagos.

Date: ............................2019.

i. We have obtained all the information and explanations which to the best of our knowledge and belief were

necessary for the purpose of our audit;

ii. In our opinion, proper books of account have been kept by the company; and

iii. The company's statement of financial position and statement of profit or loss and other comprehensive income

are in agreement with the books of account.

viii. From the matters communicated with the Directors, we determine those matters that were of most

significance in the audit of the financial statements of the current period and are therefore the key audit matters.

We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the

matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our

report because the adverse consequences of doing so would reasonably be expected to outweigh the public

interest benefits of such communication.

The Companies and Allied Matters Act,CAP C20 LFN, 2004 requires that in carring out our audit we consider and

report to you on the following matters. We confirm that:

16

25th June,

SKYWAY AVIATION HANDLING COMPANY PLC

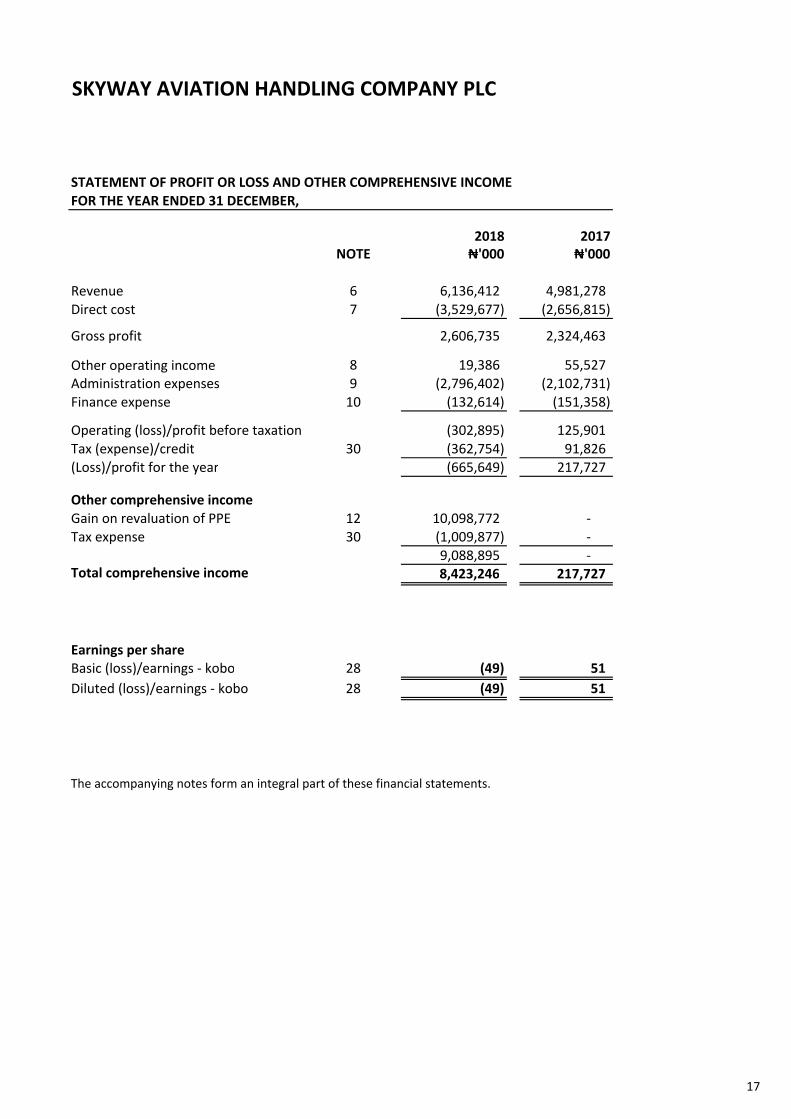

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

FOR THE YEAR ENDED 31 DECEMBER,

2018 2017

NOTE ₦'000 ₦'000

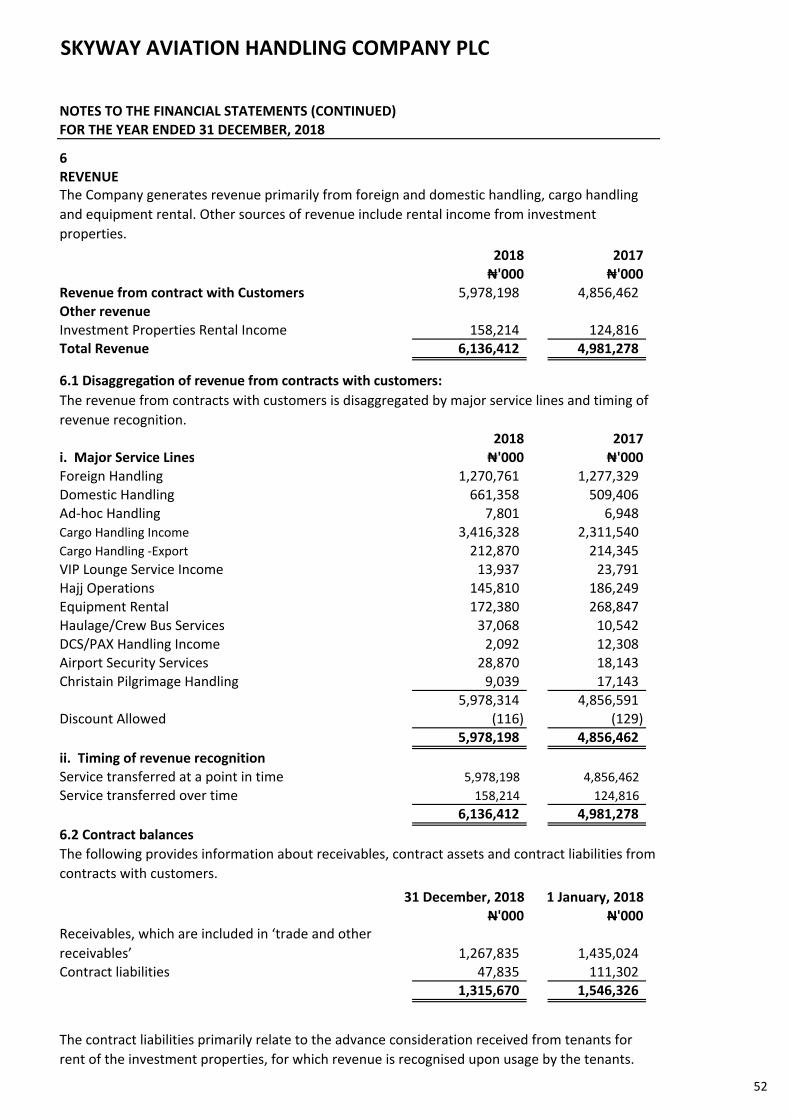

Revenue 6 6,136,412 4,981,278

Direct cost 7 (3,529,677) (2,656,815)

Gross profit 2,606,735 2,324,463

Other operating income 8 19,386 55,527

Administration expenses 9 (2,796,402) (2,102,731)

Finance expense 10 (132,614) (151,358)

Operating (loss)/profit before taxation (302,895) 125,901

Tax (expense)/credit 30 (362,754) 91,826

(Loss)/profit for the year (665,649) 217,727

Other comprehensive income

Gain on revaluation of PPE 12 10,098,772 -

Tax expense 30 (1,009,877) -

9,088,895 -

Total comprehensive income 8,423,246 217,727

Earnings per share

Basic (loss)/earnings - kobo 28 (49) 51

Diluted (loss)/earnings - kobo 28 (49) 51

The accompanying notes form an integral part of these financial statements.

17

SKYWAY AVIATION HANDLING COMPANY PLC

STATEMENT OF FINANCIAL POSITION

AS AT DECEMBER,

2018 2017

NON-CURRENT ASSETS NOTE ₦'000 ₦'000

Property, plant and equipment 12 14,975,961 6,340,457

Investment properties 13 301,683 309,502

Intangible assets 14 4,057,388 4,057,388

Deferred tax assets 31 - 943,599

19,335,032 11,650,946

CURRENT ASSETS

Inventories 15 179,211 120,868

Trade and other receivables 16 2,364,858 1,882,254

Cash and cash equivalent 17 1,207,357 888,424

3,751,427 2,891,546

TOTAL ASSETS 23,086,459 14,542,492

EQUITY

Share capital 24 676,790 425,000

Share premium 27 4,784,010 -

Retained earnings 25 4,412,321 5,077,970

Revaluation reserve 26 9,088,895 -

18,962,016 5,502,970

NON-CURRENT LIABILITIES

Deposit for shares 19 - 5,035,800

Long term borrowings 21 405,832 215,644

Deferred income 29 27,540 42,494

Deferred Tax Liability 31 187,716 -

Employee benefit liabilities 20 533,875 439,604

1,154,964 5,733,542

CURRENT LIABILITIES

Trade payable and other payables 18 2,388,698 2,499,157

Short term borrowings 21 205,777 283,043

Deferred income 29 20,295 68,809

Current income tax liabilities 30 354,709 454,971

2,969,479 3,305,980

TOTAL EQUITY AND LIABILITIES 23,086,459 14,542,492

……………………………………………. .……………………………

Barr. (Dr.) Taiwo Afolabi, MON Mr. Agboarumi Basil Mr. Rotimi Omotoso

Chairman Managing Director/CEO Head - Finance

FRC/2015/NBA/00000013106 FRC Number:…………………………. FRC/2016/ICAN/00000014593

The accompanying notes form an integral part of these financial statements.

The financial statements was approved by the Board of Directors on 25th June, 2019 and

signed on its behalf by:

…………………………….

18

SKYWAY AVIATION HANDLING COMPANY PLC

STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 31 DECEMBER, 2018

SHARE

CAPITAL

SHARE

PREMIUM

RETAINED

EARNINGS

REVALUATION

RESERVE

TOTAL

EQUITY

NOTE ₦'000 ₦'000 ₦'000 ₦'000 ₦'000

Balance at 1 January 2017 425,000 - 4,860,243 - 5,285,243

Profit for the year - - 217,727 - 217,727

Other comprehensive income for the year - - - - -

Total Comprehensive Income - - 217,727 - 217,727

Balance at 31 December 2017 425,000 - 5,077,970 - 5,502,970

Balance at 1 January 2018 425,000 - 5,077,970 - 5,502,970

Loss for the year - - (665,649) - (665,649)

Other comprehensive income for the year - - - 9,088,895 9,088,895

Total Comprehensive (Loss)/Income - (665,649) 9,088,895 8,423,246

Transactions with owners

recorded directly in equity

Issue of Shares 24 & 27 251,790 4,784,010 - - 5,035,800

Balance at 31 December 2018 676,790 4,784,010 4,412,321 9,088,895 18,962,017

The accompanying notes form an integral part of these financial statements.

19

SKYWAY AVIATION HANDLING COMPANY PLC

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 31 DECEMBER, 2018

2018 2017

NOTE ₦'000 ₦'000

Cash flows from operating activities:

(Loss)/Profit for the period (302,895) 125,901

Adjustments for net income to net cash provided by

operating activites

Finance Expenses 132,614 151,358

Allowance for impairment on Receivables 215,046 208,112

Provision for Employee benefit 20 180,550 99,913

Investment Property- Depreciation 13 11,934 11,803

Property Plant & Equipment-Depreciation 12 1,725,835 984,890

1,963,084 1,581,977

Changes in working capital

Increase in trade and other receivables (697,650) (120,722)

Decrease/(Increase) in inventories (58,343) 53,976

(Decrease)/ increase in trade and other payables (110,461) (59,045)

Increase in deferred income (63,467) 39,646

Cash generated from operations 1,033,163 1,495,833

Tax paid 30 (341,579) (259,448)

Payment made by the employer on the Employee

Benefit 20 (86,279) (51,100)

Finance expenses paid (132,614) (151,358)

Net cash inflow from operating activities 472,690 1,033,927

Cash flows from investing activities

Purchase of property, plant and equipment 12 (262,566) (143,852)

Investment Properties 13 (4,114) (6,128)

Proceed from Disposal of PPE - 1,657

Net cash outflow used in investing activities (266,680) (148,323)

Financing Activities:

Issued of Shares 5,035,800 -

Deposit for Shares (5,035,800) -

Loan Received 521,500 -

Repayment of borrowings 21 (408,578) (417,158)

Net cash inflow used in financing activities 112,922 (417,158)

Net increase/ (decrease) in cash and cash equivalents 318,933 468,446

Cash and cash equivalents at the beginning 888,424 419,978

Cash and cash equivalents at 31 December 17 1,207,357 888,424

20

SKYWAY AVIATION HANDLING COMPANY PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER, 2018

1

2

2.1 Accounting standards and interpretations issued and effectives

Impact of application of IFRS 15 Revenue from contracts with customers

Impact of Initial application of IFRS 9 Financial Instruments

Skyway Aviation Handling Company Limited became a Public Limited Company on 5th October, 2018.

The corporate Headquarters is located at Skyway Aviation Handling Company Plc Complex, Cargo Terminal, Murtala

Muhammed International Airport, Ikeja, Lagos State, Nigeria.

The application of these standards has not had any material impact on the company's financial statement as the revenue

recognition already meet the requirements of the standards.

General Information

Application of new and revised international financial reporting standards

IFRS 9 contains three principal classification categories for financial assets: measured at amortised cost, FVOCI and FVTPL. The

classification of financial assets under IFRS 9 is generally based on the business model in which a financial asset is managed and

its contractual cash flow characteristics. IFRS 9 eliminates the previous IAS 39 categories of held to maturity, loans and

receivables and available for sale. Under IFRS 9, derivatives embedded in contracts where the host is a financial asset in the

scope of the standard are never separated. Instead, the hybrid financial instrument as a whole is assessed for classification.

In the current year, the Company has applied IFRS 9 Financial Instruments (as revised in July 2014) and the related

consequential amendments to other IFRS standards that are effective for an annual period that begins on or after 1 January

2018. The transition provision of IFRS 9 allow an entity not to restate comparatives. The Company has elected not to restate

comparatives in respect of the classification and measurement of financial Instruments.

The principal activities of the Company include provision of services including aircraft/ramp handling, cargo handling,

passenger handling, premium lounge, aviation security and baggage reconciliation.

On 3rd of December 2009, SIFAX Shipping Limited and Global Apex Logistic Limited through Skyway Aviation Handling

Company Limited acquired 100% interest of the Federal Government in Skypower Aviation Handling Company Limited due to

the privatisation of the company. Global Apex Logistics limited later gave up its holding in the shares of the company.

In 2018, SAHCOL undertook a business combination with Skypower wherein both companies were consolidated with SAHCOL

as the surviving entity.

In the current year, the company has applied a number of amendments to IFRS standards and interpretations issued by the

International Accounting Standards Board (IASB) that are mandatorily effective for an accounting period that begins on or after

1 January 2018.

The company's policies for its revenue is disclosed in detail in Note 4.6. Apart from providing more extensive disclosures for

the company's revenue transactions, the application of IFRS 15 has not had a signficant impact on the finacial position and or

financial performance of the company.

This core principle is delivered in a five-step model framework: (i) Identify the contract(s) with a customer (ii)Identify the

performance obligations in the contract (iii)Determine the transaction price (iv)Allocate the transaction price to the

performance obligations in the contract (v)Recognise revenue when (or as) the entity satisfies a performance obligation.

The Company has applied these standards for the first time in the current year. IFRS 15 contains comprehensive guidance for

accounting for revenue and will replace existing requirements which are currently set out in a number of Standards and

Interpretations. The standard introduces significantly more disclosures about revenue recognition and it is possible that new

and/or modified internal processes will be needed in order to obtain the necessary information. The Standard requires

revenue recognised by an entity to depict the transfer of promised goods or services to customers in an amount that reflects

the consideration to which the entity expects to be entitled in exchange for those goods or services.

The followings revisions to accounting standards and pronouncements were issued and effective at the reporting date

21

SKYWAY AVIATION HANDLING COMPANY PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER, 2018

Impact of Initial application of IFRS 9 Financial Instruments (Continued)

iii. General hedge Accounting

The Company has applied IFRS 9 in accordance with the transition provisions set out in IFRS 9

i. Classfication and measurement of Financial Assets and Financial Liabilities.

Specifically:

debt instruments that are held within a business model whose objective is both to collect the contractual cash flows and to sell

the debt instruments, and that have contractual cash flows that are solely payments of principal and interest on the principal

amount outstanding, are measured subsequently at fair value through other comprehensive income (FVTOCI);

the Company may irrevocably elect to present subsequent changes in fair value of an equity investment that is neither held for

trading nor contingent consideration recognised by an acquirer in a business combination in other comprehensive income; and

the Company may irrevocably designate a debt investment that meets the amortised cost or FVTOCI criteria as measured at

FVTPL if doing so eliminates or significantly reduces an accounting mismatch.

The Directors of the Company reviewed and assessed the existing financial assets as at 1st January 2018 based on the facts and

circumstances that existed at that date and concluded that the initial application of IFRS 9 has had no material impact on the

financial assets as regards their classification and measurement.

All recognised financial assets that are within the scope of IFRS 9 are required to be measured subsequently at amortised cost

or fair value on the basis of the entity’s business model for managing the financial assets and the contractual cash flow

characteristics of the financial assets.

debt instruments that are held within a business model whose objective is to collect the contractual cash flows, and that have

contractual cash flows that are solely payments of principal and interest on the principal amount outstanding, are measured

subsequently at amortised cost;

debt instruments that are held within a business model whose objective is both to collect the contractual cash flows and to sell

the debt instruments, and that have contractual cash flows that are solely payments of principal and interest on the principal

amount outstanding, are measured subsequently at fair value through other comprehensive income (FVTOCI);

Details of these new requirements as well as their impact on the Company's Financial statements are described below.

The Company has assessed its existing financial assets and liabilities in terms of the requirements of IFRS 9. The company has

applied the requirements of IFRS 9 to instruments that continue to be recognised as at 1 January, 2018 and has not applied the

requirements to instruments that have already been derecognised as at 1 January, 2018.

IFRS 9 introduced new requirements for;

i. Classfication and measurement of Financial Assets and Financial Liabilities.

ii. Impairment of Financial Assets

In addition, the Company adopted amendments of IFRS 7 financial instruments: Disclosures that were applied to the

disclosures for 2018.

ii. Classification and measurement of financial liabilities

A significant change introduced by IFRS 9 in the classification and measurement of financial liabilities relates to the accounting

for changes in the fair value of a financial liability designated as at FVTPL attributable to changes in the credit risk of the issuer.

Specifically, IFRS 9 requires that the changes in the fair value of the financial liability that is attributable to changes in the credit

risk of that liability be presented in other comprehensive income, unless the recognition of the effects of changes in the

liability’s credit risk in other comprehensive income would create or enlarge an accounting mismatch in profit or loss. Changes

in fair value attributable to a financial liability’s credit risk are not subsequently reclassified to profit or loss, but are instead

transferred to retained earnings when the financial liability is derecognised.

Previously, under IAS 39, the entire amount of the change in the fair value of the financial liability designated as at FVTPL was

presented in profit or loss.

The Company does not hold financial liabilities designated as at FVTPL; therefore, the application of IFRS 9 has had no impact

on the classification and measurement of the Company’s financial liabilities.

22

SKYWAY AVIATION HANDLING COMPANY PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER, 2018

Impact of Initial application of IFRS 9 Financial Instruments (Continued)

IAS 39

31 December, 2017

Classification

Remeasureme

nt

Expected Credit

Loss/Write Back IFRS 9

1 January, 2018

Classification

₦'000 ₦'000 ₦'000 ₦'000

Financial Assets under IAS 39

Cash and cash equivalent AC 888,424 (888,424)

Trade receivables AC 1,435,024 (1,435,024)

Other receivables AC 201,013 (201,013)

Financial Assets under IFRS 9

Cash and cash equivalent 888,424 AC 888,424

Trade receivables 1,435,024 AC 1,435,024

Other receivables 201,013 AC 201,013

Financial liabilities under IAS 39

Borrowings AC 498,687 (498,687)

Trade payable AC 197,741 (197,741)

Other payables AC 1,266,759 (1,266,759)

Financial liabilities under IFRS 9

Borrowings 498,687 AC 498,687

Trade payable 197,741 AC 197,741

Other payables 1,266,759 AC 1,266,759

AC- Amortised Cost

i. debt investments measured subsequently at amortised cost or at FVTOCI;

ii. lease receivables;

iii. trade receivables and contract assets; and

iv. financial guarantee contracts to which the impairment requirements of IFRS 9 apply

In particular, IFRS 9 requires the Company to measure the loss allowance for a financial instrument at an amount equal to the

lifetime expected credit losses (ECL) if the credit risk on that financial instrument has increased significantly since initial

recognition, or if the financial instrument is a purchased or originated credit-impaired financial asset. However, if the credit

risk on a financial instrument has not increased significantly since initial recognition (except for a purchased or originated

credit-impaired financial asset), the Company is required to measure the loss allowance for that financial instrument at an

amount equal to twelve-months’ ECL. IFRS 9 also requires a simplified approach for measuring the loss allowance at an amount

equal to lifetime ECL for trade receivables, contract assets and lease receivables in certain circumstances.

The consequential amendments to IFRS 7 have also resulted in more extensive disclosures about the Company’s exposure to

credit risk in the financial statements (see note 5). The impact of IFRS 9 on opening balances was considered immaterial.

iii. Impairment of Financial Assets

In relation to the impairment of financial assets, IFRS 9 requires an expected credit loss model as opposed to an incurred credit

loss model under IAS 39. The expected credit loss model requires the Company to account for expected credit losses and

changes in those expected credit losses at each reporting date to reflect changes in credit risk since initial recognition of the

financial assets. In other words, it is no longer necessary for a credit event to have occurred before credit losses are

recognised.

Specifically, IFRS 9 requires the Company to recognise a loss allowance for expected credit losses on:

23

SKYWAY AVIATION HANDLING COMPANY PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER, 2018

Amendments to IAS 40 Transfers of Investment Property

IFRS 2 Share-based Payment Transactions

iv. General hedge accounting

The new general hedge accounting requirements retain the three types of hedge accounting. However, greater flexibility has

been introduced to the types of transactions eligible for hedge accounting, specifically broadening the types of instruments

that qualify for hedging instruments and the types of risk components of non-financial items that are eligible for hedge

accounting. In addition, the effectiveness test has been replaced with the principle of an “economic relationship”.

Retrospective assessment of hedge effectiveness is also no longer required. Enhanced disclosure requirements about the

Company’s risk management activities have also been introduced.

The Company does not apply hedge accounting; therefore, the application did not have any impact on the financial

statements.

i) the original liability is derecognised ;

c. A modification of a share-based payment that changes the transaction from cash-settled to equity-settled should be

accounted for as follows:

iii) any difference between the carrying amount of the liability at the modification date and the amount recognised in equity

should be recognised in profit or loss immediately.

The amendment to the standard has had no impact on the Company's financial statements. The Company does not operate

share based payment scheme.

ii) the equity-settled share-based payment is recognised at the modification date fair value of the equity instrument granted to

the extent that services have been rendered up to the modification date; and

The amendments clarify that a transfer to, or from, investment property necessitates an assessment of whether a property

meets, or has ceased to meet, the definition of investment property, supported by observable evidence that a change in use

has occurred. The amendments further clarify that situations other than the ones listed in IAS 40 may evidence a change in

use, and that a change in use is possible for properties under construction (i.e a change in use is not limited to completed

property.

The amendment to the standard has had no impact on the Company's financial statements.

a. In estimating the fair value of a cash-settled sharebased payment, the accounting for the effects of vesting and non-vesting

conditions should follow the same approach as for equity-settled sharebased payments.

b. Where tax law or regulation requires an entity to withhold a specified number of equity instruments equal to the monetary

value of the employee’s tax obligation to meet the employee’s tax liability which is then remitted to the tax authority, i.e. the

share-based payment arrangement has a ‘net settlement feature’, such an arrangement should be classified as equity-settled

in its entirety, provided that the share-based payment would have been classified as equity-settled had it not included the net

settlement feature.

The amendments clarify the following:

24

SKYWAY AVIATION HANDLING COMPANY PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2018

2.2

IFRS

Reference

Title and

Affected

Standard(s)

Nature of change Application

date

Impact on

initial

Application

IFRS 16 issued in

January 2016

Leases Annual reporting

periods

beginning on or

after 1 January

2019

The Company is

still reviewing the

impact the

standard may

have on the

preparation and

presentation of

the financial

statements when

the standard is

adopted in 2019.

i) the right-of-use asset is an

investment property and the lessee

fair values its investment property

under IAS 40; or

Standard, ammendments and interpretations to existing standard that are not yet effective and have not

been adopted early by the Company

At the date of authorisation of these financial statements, certain new standards, amendments and

interpretations to existing standards have been published by the IASB but are not yet effective, and have

not been adopted early by the Company.

The following new/amended accounting standards and interpretations have been issued, but are not

mandatory for financial year/period. They have not been adopted in preparing the financial statements for

the year ended 31 December 2018 and are expected not to affect the entity in the period of initial

application. In all cases, the entity intends to apply these standards from the application dates as indicated

in the table below.

IFRS 16 provides a single lessee

accounting model, requiring lessees

to recognise assets and liabilities for

all leases unless the lease term is 12

months or less or the underlying

asset has a low value. Lessors

continue to classify leases as

operating or finance. A contract is,

or contains, a lease if it conveys the

right to control the use of an

identified asset for a period of time

in exchange for consideration.

Control is conveyed where the

customer has both the right to direct

the identified asset’s use and to

obtain substantially all the economic

benefits from that use.

Accounting by lessees

Upon lease commencement a lessee

recognises a right-of-use asset and a

lease liability.

The right-of-use asset is initially

measured at the amount of the

lease liability plus any initial direct

25

SKYWAY AVIATION HANDLING COMPANY PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2018

IFRS

Reference

Title and

Affected

Standard(s)

Nature of change Application

date

Impact on

initial

Application

ii) the right-of-use asset relates to a

class of PPE to which the lessee

applies IAS 16’s revaluation model,

in which case all right-of-use assets

relating to that class of PPE can be

revalued.

Under the cost model a right-of-use

asset is measured at cost less

accumulated depreciation and

accumulated impairment. The lease

liability is initially measured at the

present value of the lease payments

payable over the lease term,

discounted at the rate implicit in the

lease if that can be readily

determined. If that rate cannot be

readily determined, the lessee shall

use their incremental borrowing

rate.

The lease liability is subsequently re-

measured to reflect changes in:

the lease term (using a revised

discount rate);

the assessment of a purchase option

(using a revised discount rate);

the amounts expected to be payable

under residual value guarantees

(using an unchanged discount rate);

or of future

lease payments resulting from a

change in an index or a rate used to

determine those payments (using an

unchanged discount rate).

The re-measurements are treated as

adjustments to the right-of-use

asset.

Accounting by lessor

Lessor shall continue to account for

leases in line with the provision in

IAS 17.

IFRS 16 issued in

January 2016

Leases

26

SKYWAY AVIATION HANDLING COMPANY PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2018

2

IFRS

Reference

Title and

Affected

Standard(s)

Nature of change Application

date

Impact on

initial

Application

The new Standard establishes the

principles for the recognition,

measurement, presentation and

disclosure of insurance contracts

and supersedes IFRS 4 Insurance

Contracts.

The Standard outlines a General

Model, which is modified for

insurance contracts with direct

participation features, described

as the Variable Fee Approach.

The General Model is simplified if

certain criteria are met by

measuring the liability for

remaining coverage using the

Premium Allocation Approach.

The General Model will use

current assumptions to estimate

the amount, timing and

uncertainty of future cash flows

and it will explicitly measure the

cost of that uncertainty, it takes

into account market interest

rates and the impact of

policyholders’ options and

guarantees.

The amendments to the

standards enable entities to

measure certain prepayable

financial assets with negative

compensation at amortised cost.

These assets, which include some

loan and debt securities, would

otherwise have to be measured

at fair value through profit or

loss.

Annual

reporting

periods

beginning on

or after 1

January 2019

To qualify for amortised cost

measurement, the negative

compensation must be

‘reasonable compensation for

early termination of the contract’

and the asset must be held

within a ‘held to collect’ business

model.

Amendments to

IFRS 9

Prepayment

Features with

Negative

Compensation

The directors of

the Company do

not anticipate

that the

application of

the amendments

in the future will

have an impact

on the financial

statements.

IFRS 17 was

issued in May

2017 as

replacement for

IFRS 4 Insurance

Contracts

Insurance

Contracts

Annual

reporting

periods

beginning on

or after 1

January 2021

The directors of

the Company do

not anticipate

that the

application of

the amendments

in the future will

have an impact

on the financial

statements.

27

SKYWAY AVIATION HANDLING COMPANY PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2018

IFRS

Reference

Title and

Affected

Standard(s)

Nature of change Application

date

Impact on

initial

Application

The amendments to IAS 19 clarify

the accounting for defined

benefit plan amendments,

curtailments and settlements.

They confirm that entities must :

i. calculate the current service

cost and net interest for the

remainder of the reporting

period after a plan amendment,

curtailment or settlement by

using the updated assumptions

from the date of the change

ii. any reduction in a surplus

should be recognised

immediately in profit or loss

either as part of past service cost,

or as a gain or loss on settlement.

In other words, a reduction in a

surplus must be recognised in

profit or loss even if that surplus

was not previously recognised

because of the impact of the

asset ceiling

iii. separately recognise any

changes in the asset ceiling

through other comprehensive

income.

Amendments to

IAS 19 Employee

Benefits Plan

Amendment,

Curtailment or

Settlement

Annual

reporting

periods

beginning on

or after 1

January 2019

The directors of

the Company do

not anticipate

that the

application of

the amendments

in the future will

have an impact

on the financial

statements.

IFRS 10 and IAS

28

Contribution of

Assets between

an Investor and

its Associate or

Joint venture

The amendments to IFRS 10 and

IAS 28 deal with situations where

there is a sale or contribution of

assets between an investor and

its associate or joint venture.

Specifically, the amendments

state that gains or losses

resulting from the loss of control

of a subsidiary that does not

contain a business in a

transaction with an associate or a

joint venture that is accounted

for using the equity method, are

recognised in the parent’s profit

or loss only to the extent of the

unrelated investors’ interests in

that associate or joint venture.

Similarly, gains and losses

resulting from the

remeasurement of investments

yet to be

determined

The amendment

to the standard

will not impact

on the

Company's

financial

statements

when it becomes

effective.

28

SKYWAY AVIATION HANDLING COMPANY PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2018

3. Critical accounting estimates and judgements

The Company makes certain estimates and assumptions regarding the future. Estimates and judgements are

continually evaluated based on historical experience as other factors, including expectations of future events

that are believed to be reasonable under the circumstances. In the future, actual experience may differ from

these estimates and assumptions. The estimates and assupmtions that have a significant risk of causing a

material adjustment to the carrying amounts of assets and liabilities within the next financial year are:

(a) Income and deferred taxation

The Company incurs significant amounts of income taxes payable, and also recognises significant changes to

deferred tax assets and deferred tax liabilities, all of which are based on management’s interpretations of

applicable laws and regulations. The quality of these estimates is highly dependent upon management’s ability

to properly apply at times a very complex sets of rules, to recognise changes in applicable rules and, in the case

of deferred tax assets, management’s ability to project future earnings from activities that may apply loss carry

forward positions against future income taxes.

(b) Impairment of property, plant and equipment

The Company assesses assets or groups of assets for impairment annually or whenever events or changes in

circumstances indicate that carrying amounts of those assets may not be recoverable. In assessing whether a

write-down of the carrying amount of a potentially impaired asset is required, the asset’s carrying amount is

compared to the recoverable amount. Frequently, the recoverable amount of an asset proves to be the

Company’s estimated value in use.

The estimated future cash flows applied are based on reasonable and supportable assumptions over the

remaining useful life of the cash flow generating assets.

(c) Legal proceedings

The Company reviews outstanding legal cases following developments in the legal proceedings and at each

reporting date, in order to assess the need for provisions and disclosures in its financial statements. Among the

factors considered in making decisions on provisions are the nature of litigation, claim or assessment, the legal

process and potential level of damages in the jurisdiction in which the litigation, claim or assessment has been

brought, the progress of the case (including the progress after the date of the financial statements but before

those statements are issued), the opinions or views of legal advisers, experience on similar cases and any

decision of the Company's management as to how it will respond to the litigation, claim or assessment.

(d) Trade Receivables

The Company assesses its trade receivables for probability of credit losses. Management considers several

factors including past credit record, current financial position and credibility of management, judgement is

exercised in determining the allowances made for credit losses.

(e) Employee Benefit Obligation (Defined Benefit Plan)

The cost of the defined benefit plans and the present value of retirement benefit obligations and long service

awards are determined using actuarial valuations. An actuarial valuation involves making various assumptions

that may differ from actual developments in the future. These include the determination of the discount rate,

future salary increases, mortality rates and changes in inflation rates. Due to the complexities involved in the

valuation and its long-term nature, these obligations are highly sensitive to changes in assumptions.

(f) Impairment of Goodwill

The Company assesses its goodwill for possible impairment if there are events or changes in circumstances that

indicate that carrying values of the cash generating unit (CGU) may not be recoverable, or atleast at every

reporting date.

The assessment for impairment entailed comparing the carrying value of the cash generating unit containing

the goodwill with its recoverable amount. The recoverable amount is based on an estimate of the value in use

of these assets. Value in use is determined on the basis of discounted estimated future net cash flows. During

the year, the Company recognised no impairment losses in respect of goodwill. See further details in Notes 15.

29

SKYWAY AVIATION HANDLING COMPANY PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2018

4 Significant accounting policies

The principal accounting policies applied in the preparation of these financial statements are set out below. These

policies have been consistently applied to all the years presented unless otherwise stated.

4.1 Statement of Compliance

The Company's financial statements for the year ended 31 December, 2018 have been prepared in conformity

with International Financial Reporting Standards as issued by the International Accounting Standards Board (IASB)

and interpretations issued by the International Financial Reporting Interpretations Committee (IFRIC) that are

effective at 31st December, 2018 and requirements of the companies and Allied Matters Act (CAMA) of Nigeria

and Financial Reporting Council (FRC) Act of Nigeria except for Employee Benefits which is not in line with the

provision of IAS 19.

Skyway Aviation Handling Company Plc has consistenly applied the same accounting policies and methods of

computation in its financial statements as in its 2017 financial statements except a change in policy during 2018

for the measurement of Property, Plant & Equipment.

The financial statements were authorised for issue by the Board of Directors on 25th June, 2019.

4.2 Basis of preparation

The financial statements have been prepared under the historical cost convention except for some financial assets

and liabilities measured at fair value and amortised cost; inventory at net realisable value; and the liabilitiy for

defined benefit obligations is recognised as the present value of the defined benefit obligation and related current

service cost.

4.3 Going concern

The directors assess the Company's future performance and financial position on a going concern basis and have

no reason to believe that the Company will not be a going concern in the year ahead. For this reason, the financial

statements have been prepared on a going concern basis.

4.5 Use of estimates and judgement

The preparation of financial statements in conformity with IFRS requires the use of certain critical accounting

estimates and judgments. It also requires management to exercise its judgement in the process of applying the

company’s accounting policies. The areas involving a higher degree of judgement or complexity, or areas where

assumptions and estimates are significant to the financial statements are disclosed in note 3.

The financial statements comprise the statement of financial position, the statement of profit or loss and other

comprehensive income, the statement of changes in equity, the statement of cash flows and the notes.

30

SKYWAY AVIATION HANDLING COMPANY PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2018

4.6 Revenue recognition

Revenue is measured based on the consideration specified in a contract with a customer. The

Company recognises revenue when it transfers control over a good or service to a customer.

Transfer of control is believed to be transferred to the customer at the point of delivery to the

customer.

4.6.1 Rendering of services - Cargo Income

The company is into Cargo handling in the aviation industry. Services rendered is recognised in

proportion to the stage of completion of the transaction at the reporting date. The proportion

recognised in the Statement of Profit or Loss and Other Comprehensive Income is assessed by

reference to services performed to date as a percentage of total services to be performed.

Revenue from cargo services is also recognised when control of the goods have passed to the

clearing agents or customers, usually on delivery of the goods. Delivery occurs when a

customer's truck has been loaded with the cargo goods specified in the invoice.

Revenue is recognised net of discount and rebates given on volume trade.

4.6.2 Aircraft Handling Income

The company also renders aircraft handling which include crew and passenger transportation,

passenger profiling, equipment rentals and ground handling services. Income from aircraft

handling are recognised in the profit or loss in proportion to stage of compeletion of the

transaction as the reporting date. However, when the services under a single arrangement are

rendered in different reporting periods, the consideration is allocated on a relative fair value

basis between the services.

4.6.3 Rental Income

Rentals from sub-leased property are recognised as rental income which is determined over the

term of lease.

4.7 Expenditure

Expenditures are recognised as they accrue during the course of the year. Analysis of expenses

recognised in the statement of profit or loss is presented in classification based on the function

of the expenses as this provides information that is reliable and more relevant than their

nature. The Company classifies its expenses as follows:

- Cost of sales;

- Administration expenses;

a) Cost of Goods Sold

These are the direct costs attributable to the service rendered by the company. These costs

includes directly attributable costs such as the concession fee, direct labour, cargo

shed/warehouse, Hajj and Christian Pilgrimage oparetion, as well as overheads, including

depreciation.

The cost of goods sold includes write-downs of inventories where necessary.

31

SKYWAY AVIATION HANDLING COMPANY PLC

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2018

b) Administrative expenses

Administrative expenses are recognised as they accrue during the course of the year. Analysis of

expenses recognised in the statement of profit or loss and other comprehensive income is