sivs and the asset-backed commercial paper market · run on abcp and repo covitz, liang, suarez...

TRANSCRIPT

Short-term Funding and

Collapse of the Asset-Backed Commercial Paper Market

Nellie Liang

Jan. 23, 2014

* The views expressed here do not reflect those of the Federal Reserve System or its Board of Governors.

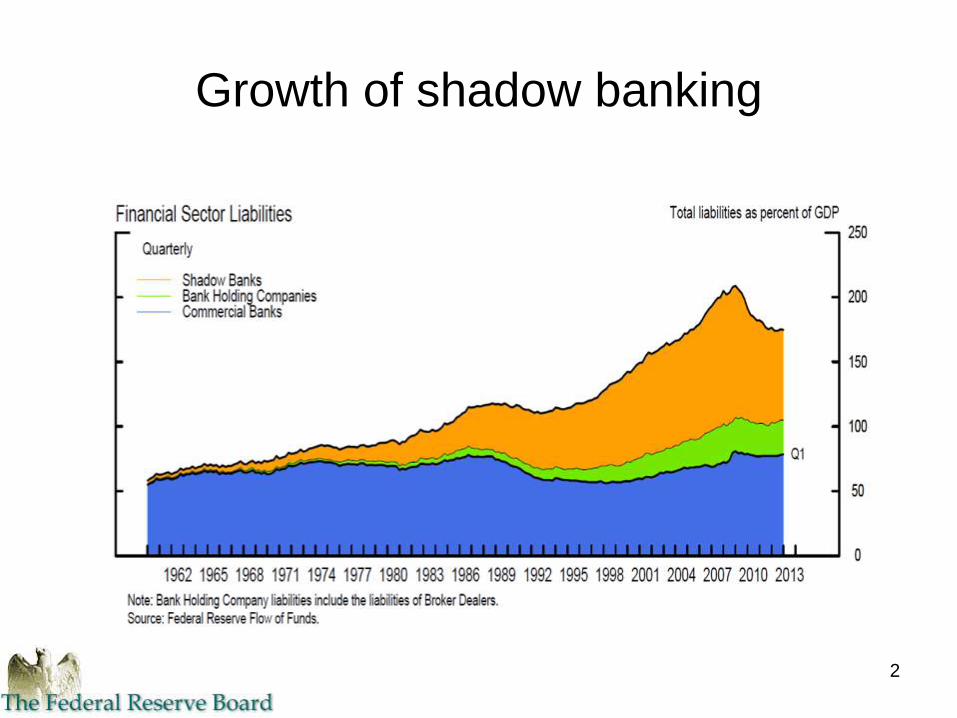

Growth of shadow banking

2

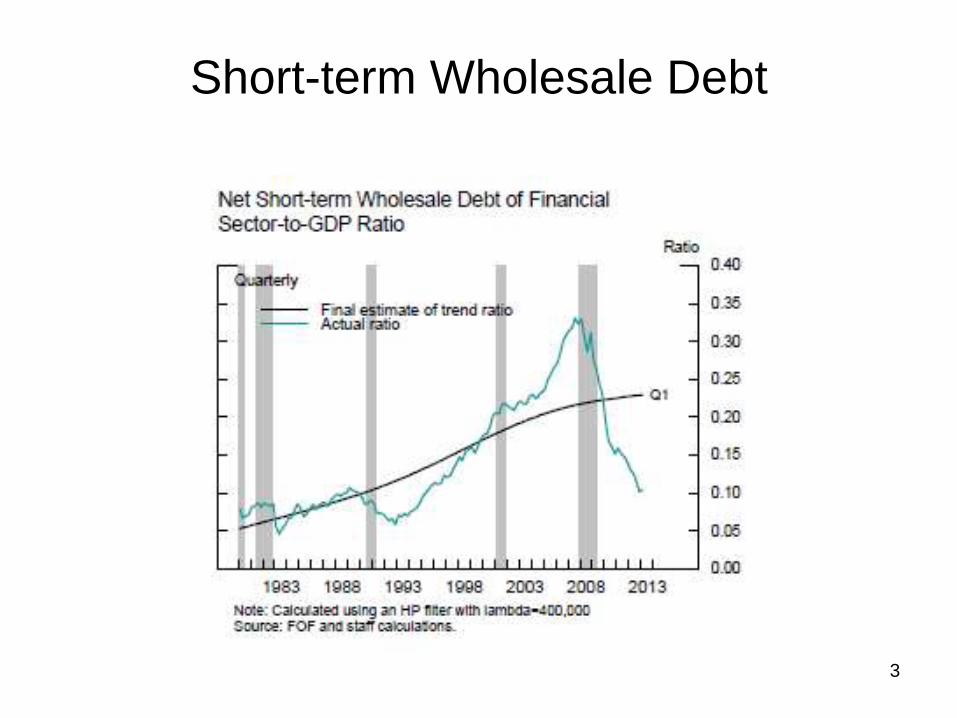

Short-term Wholesale Debt

3

Run on ABCP and Repo Covitz, Liang, Suarez (2013) Collapse of the Asset-Backed Commercial Paper Market

Gorton and Metrick (2012) Securitized Banking and the Run on Repo

4

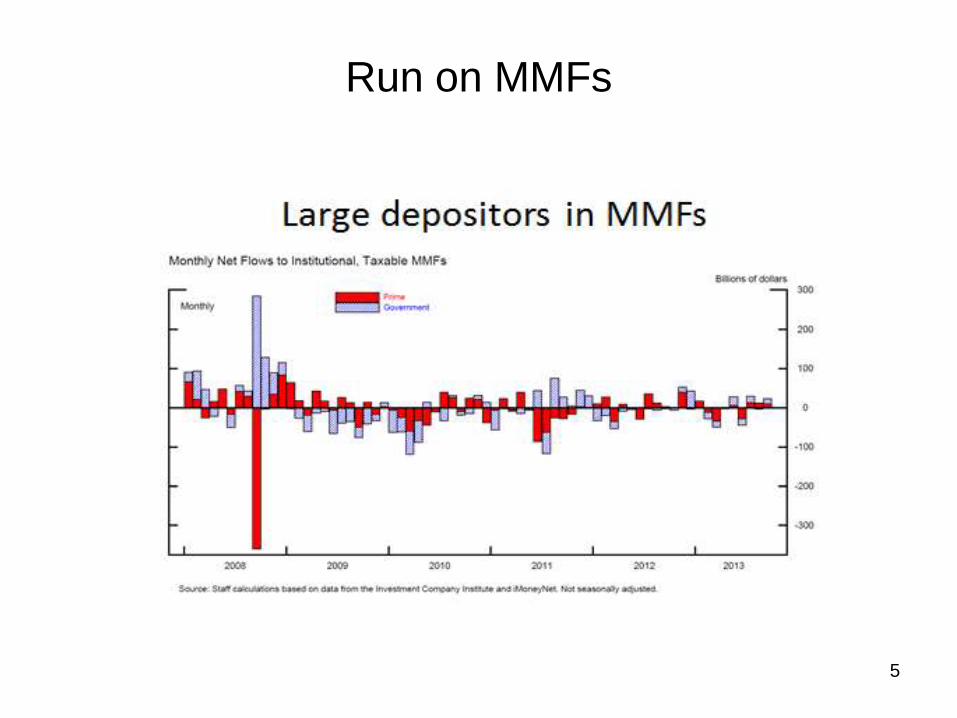

Run on MMFs

5

6

Overview of “Collapse of ABCP”

• ABCP programs are like banks

• ABCP programs differ by credit, liquidity, sponsor and other features

• Measuring “runs”

• Explaining runs

7

The ABCP Market in 2007: Outstandings

700

800

900

1000

1100

1200

1300

3-J

an

-07

17

-Jan

-07

31

-Jan

-07

14

-Feb

-07

28

-Feb

-07

14

-Mar-

07

28

-Mar-

07

11

-Ap

r-0

7

25

-Ap

r-0

7

9-M

ay

-07

23

-May

-07

6-J

un

-07

20

-Ju

n-0

7

4-J

ul-

07

18

-Ju

l-0

7

1-A

ug-0

7

15

-Au

g-0

7

29

-Au

g-0

7

12

-Sep

-07

26

-Sep

-07

10

-Oct-

07

24

-Oct-

07

7-N

ov

-07

21

-No

v-0

7

5-D

ec-0

7

19

-Dec-0

7

bil

lio

ns

of

doll

ars

Panel A. ABCP Outstandings

Weekly (Wednesday)

8

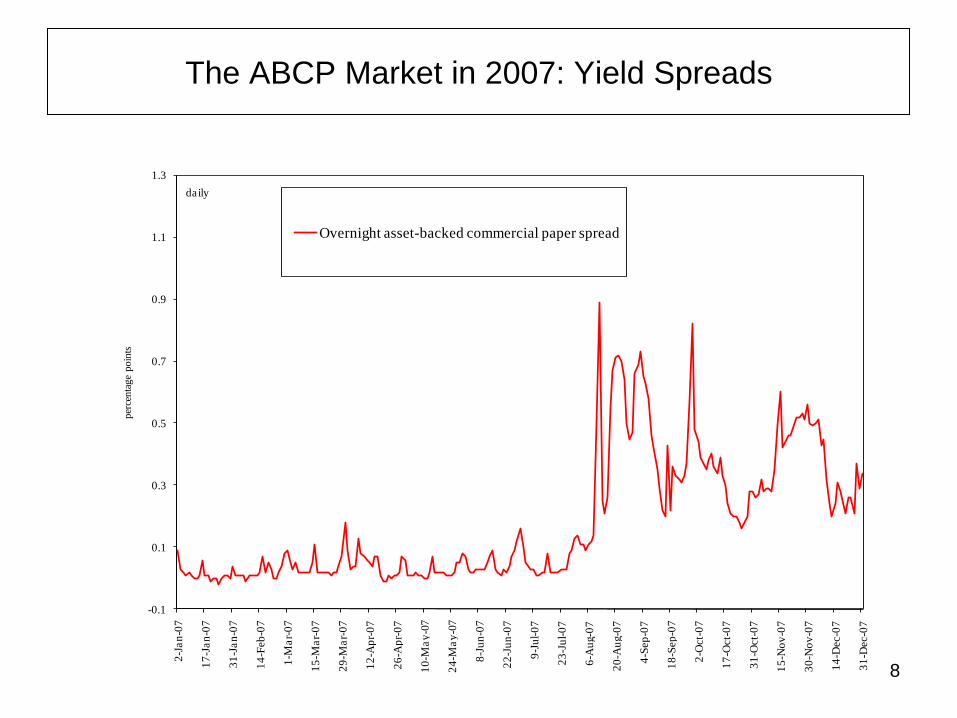

The ABCP Market in 2007: Yield Spreads

-0.1

0.1

0.3

0.5

0.7

0.9

1.1

1.32

-Ja

n-0

7

17

-Ja

n-0

7

31

-Ja

n-0

7

14

-Feb

-07

1-M

ar-

07

15

-Ma

r-0

7

29

-Ma

r-0

7

12

-Ap

r-0

7

26

-Ap

r-0

7

10

-Ma

y-0

7

24

-Ma

y-0

7

8-J

un

-07

22

-Ju

n-0

7

9-J

ul-

07

23

-Ju

l-0

7

6-A

ug-0

7

20

-Au

g-0

7

4-S

ep

-07

18

-Sep

-07

2-O

ct-

07

17

-Oct-

07

31

-Oct-

07

15

-No

v-0

7

30

-No

v-0

7

14

-Dec-0

7

31

-Dec-0

7

per

cen

tag

e p

oin

ts

Overnight asset-backed commercial paper spread

daily

9

The ABCP Market in 2007: Average Maturity

10

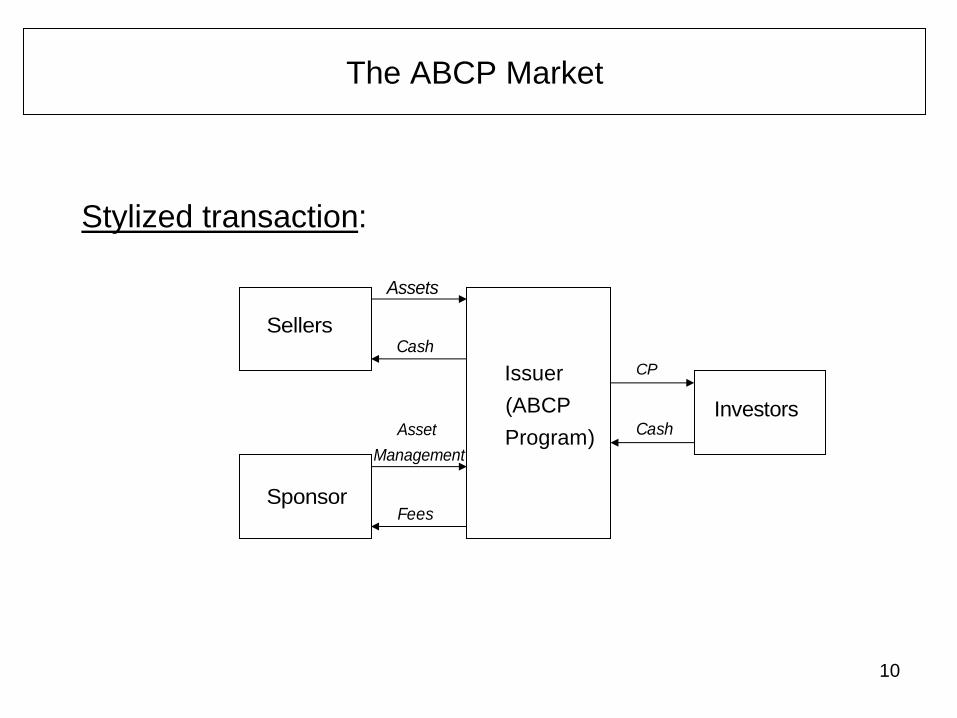

The ABCP Market

Stylized transaction:

Sellers

Issuer

(ABCP

Program)

Investors

Sponsor

Assets

Cash

Asset

Management

CP

Fees

Cash

11

ABCP programs are like banks

• Issues short-term debt to finance assets, such as

receivables, loans, and securities

o Substantial portion of liabilities is ‘overnight’

o Assets tend to have longer maturities

o Assets are relatively opaque, illiquid

• Liquidity support may attenuate rollover risk

12

What is known about ABCP programs

• “SIVs: An Oasis of Calm in the Subprime Maelstrom” Moody’s, July 2007

• SIVs invest in Aaa and Aa US RMBS and CDOs … exposures are limited owing to diversity of their portfolios … are not structured to forcibly liquidate assets … expects ratings to remain stable amid the current maelstrom

• “An ABCP Cheat Sheet,” JPMorgan, Aug. 16, 2007

In response to numerous questions .. . from investors both inside and outside of the short-term credit markets … ABCP is a complex investment that would take volumes to explain

completely … “

13

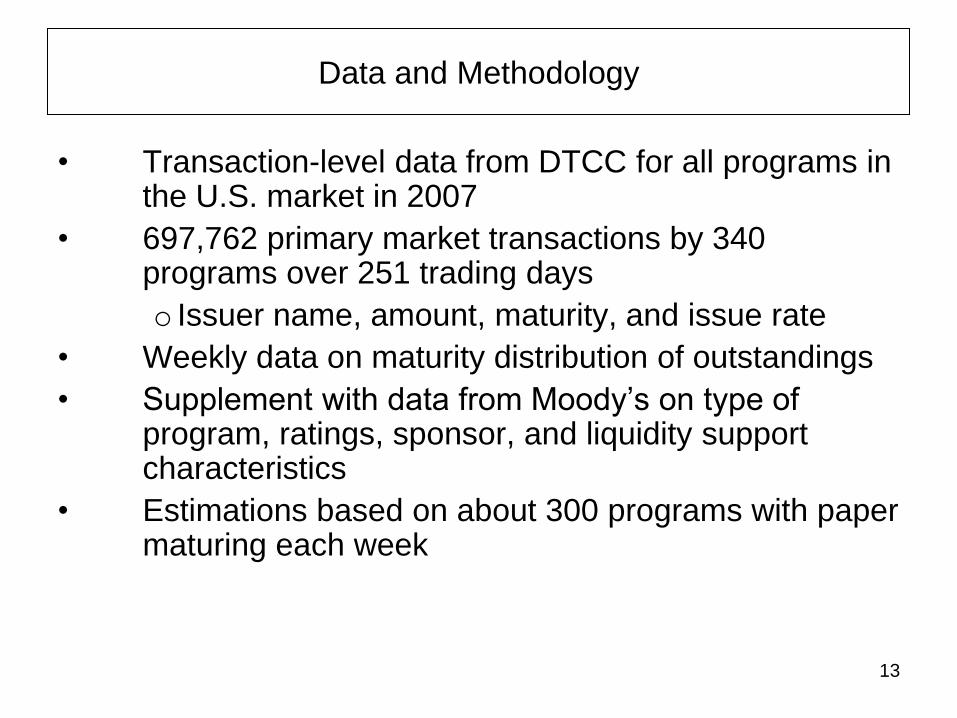

Data and Methodology

• Transaction-level data from DTCC for all programs in the U.S. market in 2007

• 697,762 primary market transactions by 340 programs over 251 trading days

o Issuer name, amount, maturity, and issue rate

• Weekly data on maturity distribution of outstandings

• Supplement with data from Moody’s on type of program, ratings, sponsor, and liquidity support characteristics

• Estimations based on about 300 programs with paper maturing each week

14

ABCP programs vary by assets and liquidity support

Program type Assets Liquidity

support

No. of

programs

Share

extendable (percent)

Multi seller Receivables, loans Full 98 19

Non-mortgage

single seller

Credit-card receivables, auto

loans

Implicit 40 62

Mortgage single

seller

Mortgages and MBS Implicit 11 67

Securities

arbitrage

Highly-rated long-term securities Full 35 9

SIVs Highly-rated long-term securities Little to

none 35 0

CDOs Highly-rated long-term securities Partial 36 25

Hybrid and

other

-- -- 84 20

15

ABCP programs also vary by type of sponsor and other

characteristics

Ratings

Credit support

Number of liquidity providers

CDS spread of main liquidity provider

Sponsors

– Domestic commercial banks

– Foreign commercial banks

– Nonbank sponsors – mortgage lenders, finance companies,

asset managers

16

Measuring Runs

• Define a run on an ABCP program as occurring if a program is unable to issue new paper to fund maturing obligations

, -1

Maturing1 if 0.1 and Issuance 0

Outstanding

Run 1 if Run 1 and Issuance 0

0 otherwise

itit

it

it i t it

17

Runs in ABCP Programs

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%3

-Ja

n

17

-Ja

n

31

-Ja

n

14

-Fe

b

28

-Fe

b

14

-Ma

r

28

-Ma

r

11

-Ap

r

25

-Ap

r

9-M

ay

23

-Ma

y

6-J

un

20

-Ju

n

4-J

ul

18

-Ju

l

1-A

ug

15

-Au

g

29

-Au

g

12

-Se

p

26

-Se

p

10

-Oct

24

-Oct

7-N

ov

21

-No

v

5-D

ec

19

-De

c

Fraction of ABCP programs experiencing "runs"

WeeklyWeekly

18

Runs are “Absorbing States” after August 2007

0%

10%

20%

30%

40%

50%

60%3

-Ja

n

17

-Ja

n

31

-Ja

n

14

-Fe

b

28

-Fe

b

14

-Ma

r

28

-Ma

r

11

-Ap

r

25

-Ap

r

9-M

ay

23

-Ma

y

6-J

un

20

-Ju

n

4-J

ul

18

-Ju

l

1-A

ug

15

-Au

g

29

-Au

g

12

-Se

p

26

-Se

p

10

-Oct

24

-Oct

7-N

ov

21

-No

v

5-D

ec

19

-De

c

Fraction of ABCP programs experiencing runs

Unconditional hazard of leaving the run state

WeeklyWeekly

19

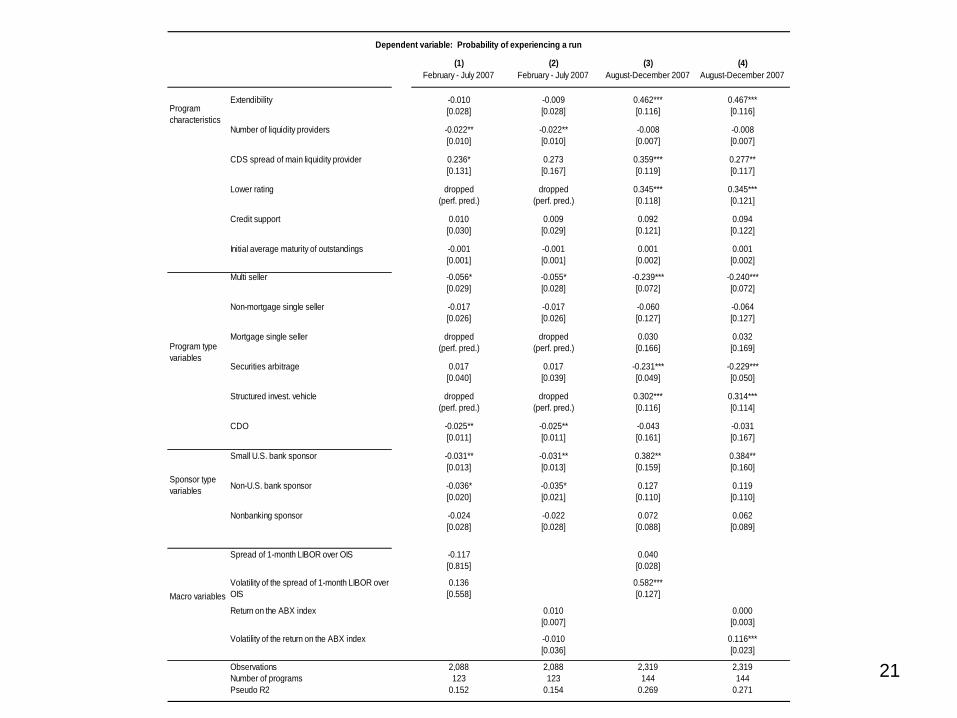

Explaining Runs

• Declines in programs in a run accounted for decline in outstandings

• Runs more likely at programs perceived to be weaker o Fewer liquidity providers

o Extendible

o Higher CDS for liquidity provider

o More likely to hold subprime mortgages

o More likely when markets are more volatile

• Similar factors explain higher spreads and shorter maturities for programs not in a run

Gorton (1988), National Banking Era crises

• Calomiris and Mason (2003), 1930s failures

• Demirgüç-Kunt and Detragiache (1998), cross country,1980-1994

Explain runs as function of credit and liquidity risks • Diamond and Dybvig – programs can be run in

equilibrium regardless of assets, given first-come first-serve

• Risks could be program-specific or market-wide • Investors are concerned about the ability of banks to simultaneously

meet commitments, or

• Investors update their views of overall asset quality

20

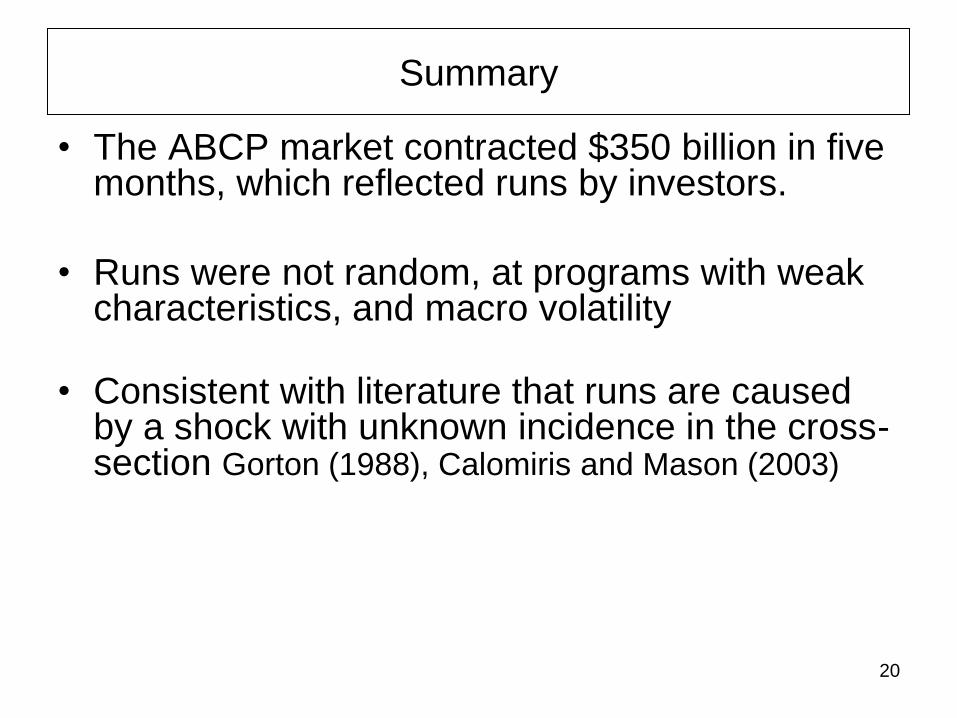

Summary

• The ABCP market contracted $350 billion in five months, which reflected runs by investors.

• Runs were not random, at programs with weak characteristics, and macro volatility

• Consistent with literature that runs are caused by a shock with unknown incidence in the cross-section Gorton (1988), Calomiris and Mason (2003)

21

(1) (2) (3) (4)

February - July 2007 February - July 2007 August-December 2007 August-December 2007

Extendibility -0.010 -0.009 0.462*** 0.467***

[0.028] [0.028] [0.116] [0.116]

Number of liquidity providers -0.022** -0.022** -0.008 -0.008

[0.010] [0.010] [0.007] [0.007]

CDS spread of main liquidity provider 0.236* 0.273 0.359*** 0.277**

[0.131] [0.167] [0.119] [0.117]

Lower rating dropped dropped 0.345*** 0.345***

(perf. pred.) (perf. pred.) [0.118] [0.121]

Credit support 0.010 0.009 0.092 0.094

[0.030] [0.029] [0.121] [0.122]

Initial average maturity of outstandings -0.001 -0.001 0.001 0.001

[0.001] [0.001] [0.002] [0.002]

Multi seller -0.056* -0.055* -0.239*** -0.240***

[0.029] [0.028] [0.072] [0.072]

Non-mortgage single seller -0.017 -0.017 -0.060 -0.064

[0.026] [0.026] [0.127] [0.127]

Mortgage single seller dropped dropped 0.030 0.032

(perf. pred.) (perf. pred.) [0.166] [0.169]

Securities arbitrage 0.017 0.017 -0.231*** -0.229***

[0.040] [0.039] [0.049] [0.050]

Structured invest. vehicle dropped dropped 0.302*** 0.314***

(perf. pred.) (perf. pred.) [0.116] [0.114]

CDO -0.025** -0.025** -0.043 -0.031

[0.011] [0.011] [0.161] [0.167]

Small U.S. bank sponsor -0.031** -0.031** 0.382** 0.384**

[0.013] [0.013] [0.159] [0.160]

Non-U.S. bank sponsor -0.036* -0.035* 0.127 0.119

[0.020] [0.021] [0.110] [0.110]

Nonbanking sponsor -0.024 -0.022 0.072 0.062

[0.028] [0.028] [0.088] [0.089]

Spread of 1-month LIBOR over OIS -0.117 0.040

[0.815] [0.028]

0.136 0.582***

[0.558] [0.127]

Return on the ABX index 0.010 0.000

[0.007] [0.003]

-0.010 0.116***

[0.036] [0.023]

Observations 2,088 2,088 2,319 2,319

Number of programs 123 123 144 144

Pseudo R2 0.152 0.154 0.269 0.271

Macro variables

Program type

variables

Sponsor type

variables

Program

characteristics

Volatility of the spread of 1-month LIBOR over

OIS

Volatility of the return on the ABX index

Dependent variable: Probability of experiencing a run

22

END

23

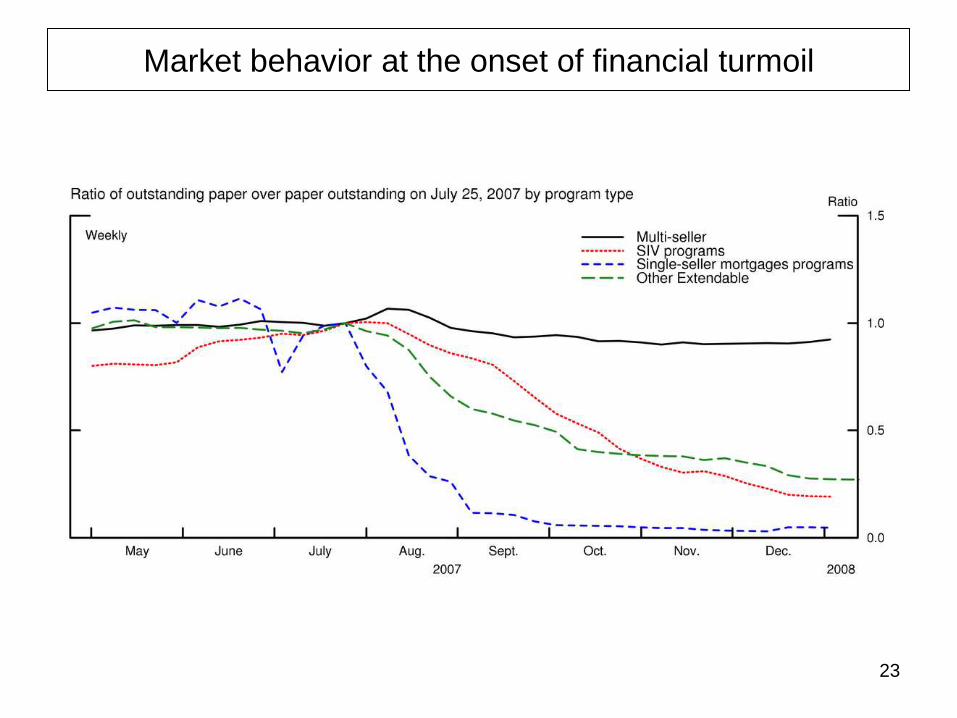

Market behavior at the onset of financial turmoil

24

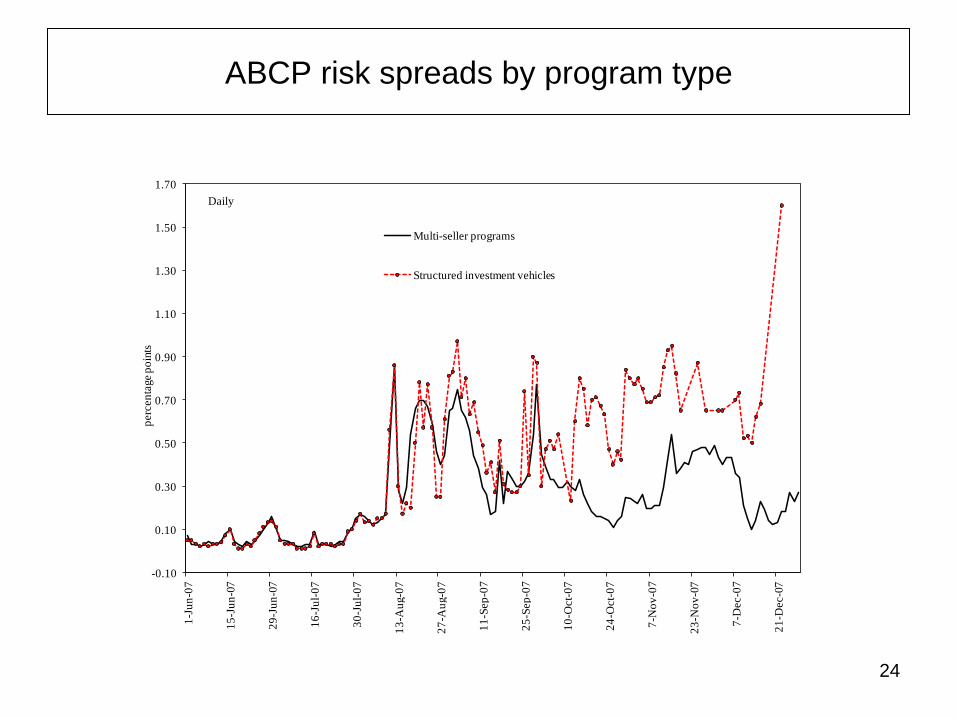

ABCP risk spreads by program type

-0.10

0.10

0.30

0.50

0.70

0.90

1.10

1.30

1.50

1.701

-Ju

n-0

7

15

-Ju

n-0

7

29

-Ju

n-0

7

16

-Ju

l-0

7

30

-Ju

l-0

7

13

-Au

g-0

7

27

-Au

g-0

7

11

-Sep

-07

25

-Sep

-07

10

-Oct-

07

24

-Oct-

07

7-N

ov

-07

23

-No

v-0

7

7-D

ec-0

7

21

-Dec-0

7

perc

en

tage

po

ints

Multi-seller programs

Structured investment vehicles

Daily

25

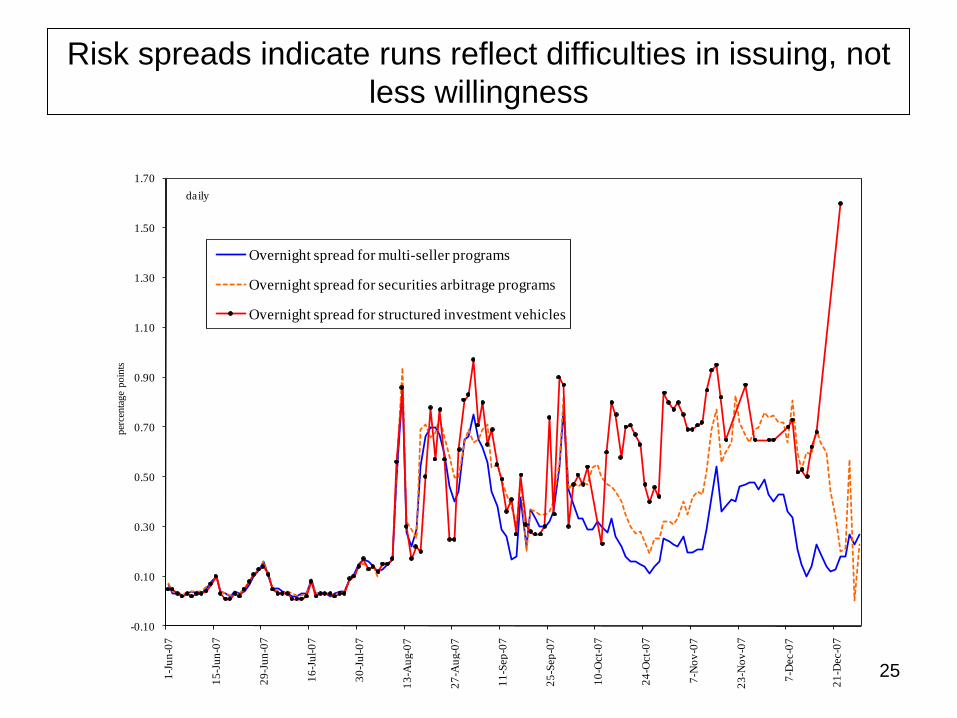

Risk spreads indicate runs reflect difficulties in issuing, not

less willingness

-0.10

0.10

0.30

0.50

0.70

0.90

1.10

1.30

1.50

1.701

-Ju

n-0

7

15

-Ju

n-0

7

29

-Ju

n-0

7

16

-Ju

l-0

7

30

-Ju

l-0

7

13

-Au

g-0

7

27

-Au

g-0

7

11

-Sep

-07

25

-Sep

-07

10

-Oct-

07

24

-Oct-

07

7-N

ov

-07

23

-No

v-0

7

7-D

ec-0

7

21

-Dec-0

7

per

centa

ge

poin

ts

Overnight spread for multi-seller programs

Overnight spread for securities arbitrage programs

Overnight spread for structured investment vehicles

daily

26

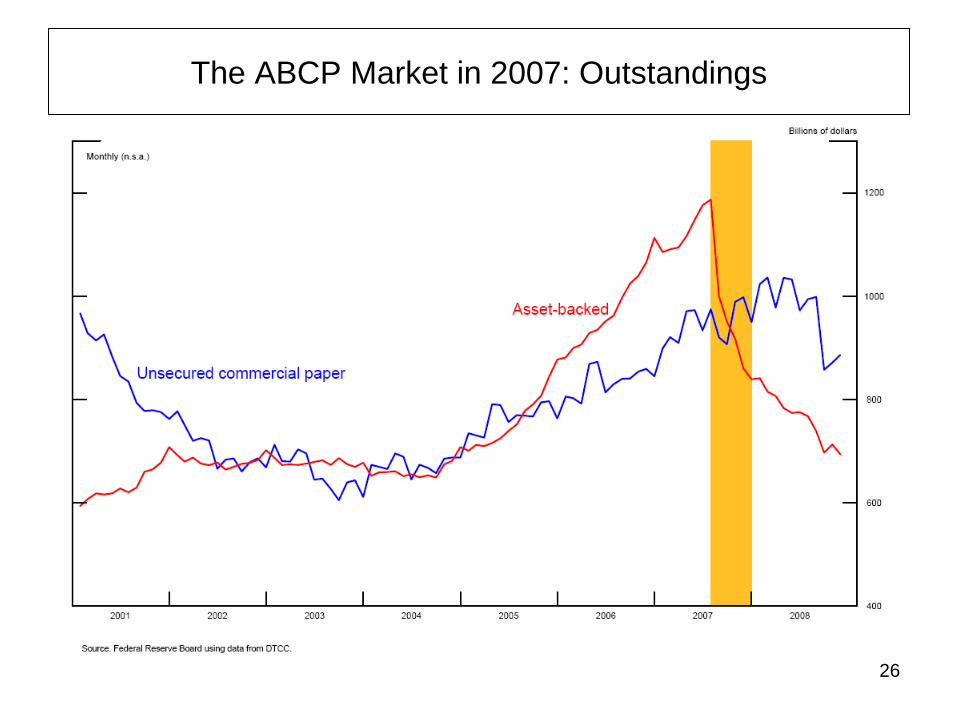

The ABCP Market in 2007: Outstandings