asset-backed securities primer

DESCRIPTION

Asset-Backed Securities PrimerTRANSCRIPT

A U G U S T 5 , 2 0 0 8

I N V E S T I N G I N A S S E T B A C K E D S E C U R I T I E S

ABS Research

Chris Flanagan AC

Head, Global Structured Finance Research (1-212) [email protected]

Edward Reardon (1-212) [email protected]

Amy Sze, CFA(1-212) [email protected]

Brynja Sigurdardottir(1-212) [email protected]

AgendaAgenda

Page

Home Equity ABS

Student Loan ABS (FFELP)

Automobile ABS

Credit Card

Introduction to ABS

1

1

11

35

53

86

IN

VE

ST

IN

GI

NA

SS

ET

BA

CK

ED

SE

CU

RI

TI

ES

404

536

732

901

1072

1281

1543

1694

1828

1955

24802472

2130

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

96 98 00 02 04 06 1Q08

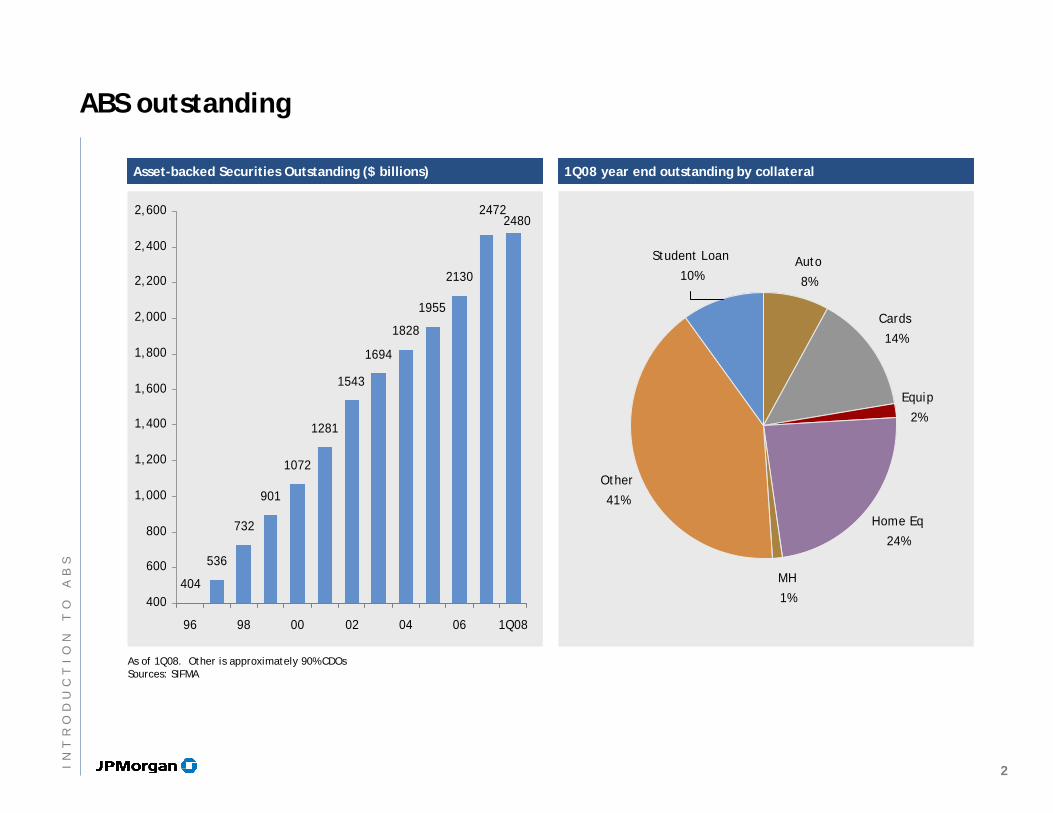

As of 1Q08. Other is approximately 90% CDOsSources: SIFMA

Asset-backed Securities Outstanding ($ billions)Asset-backed Securities Outstanding ($ billions) 1Q08 year end outstanding by collateral1Q08 year end outstanding by collateral

Cards

14%

Equip

2%

Home Eq

24%

Student Loan

10%

Other

41%

MH

1%

Auto

8%

ABS outstanding

2IN

TR

OD

UC

TI

ON

TO

AB

S

Supply ($ Billions)Supply ($ Billions)

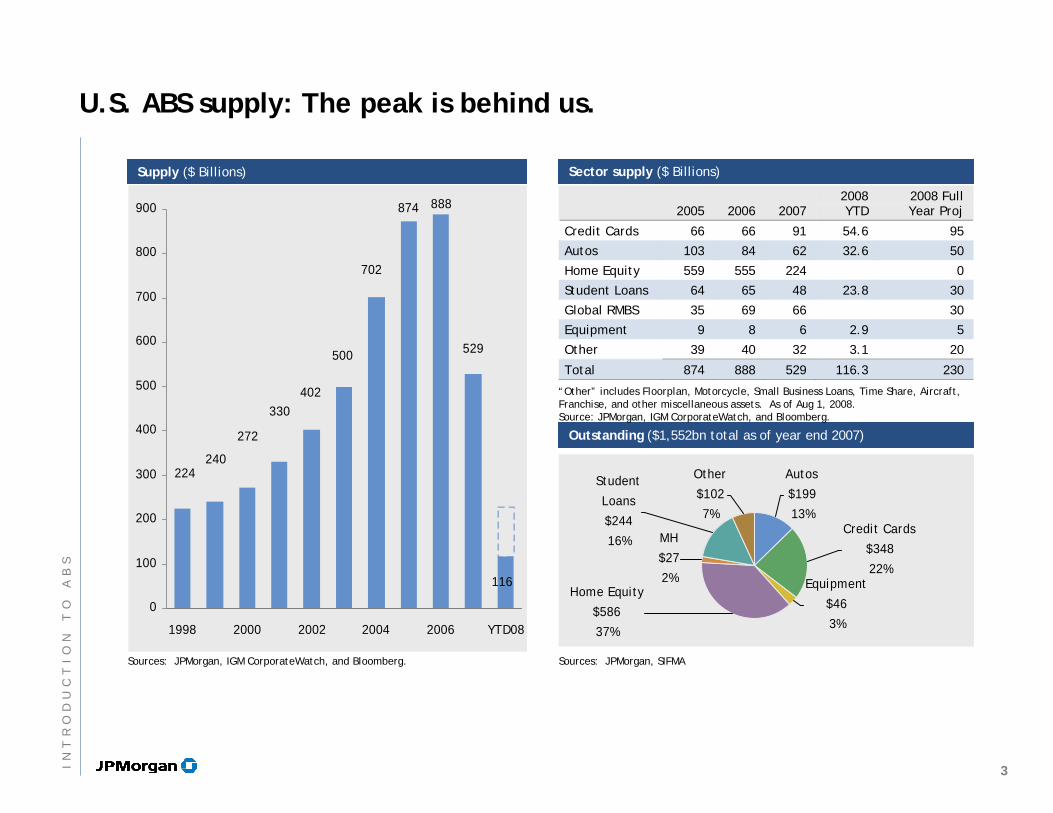

U.S. ABS supply: The peak is behind us.

Sources: JPMorgan, IGM CorporateWatch, and Bloomberg.

Sector supply ($ Billions)Sector supply ($ Billions)

Outstanding ($1,552bn total as of year end 2007)Outstanding ($1,552bn total as of year end 2007)

Other

$102

7%

Student

Loans

$244

16%

Home Equity

$586

37%

Equipment

$46

3%

MH

$27

2%

Autos

$199

13%Credit Cards

$348

22%

Sources: JPMorgan, SIFMA

224240

272

330402

500

702

874 888

529

116

0

100

200

300

400

500

600

700

800

900

1998 2000 2002 2004 2006 YTD08

2005 2006 2007 2008 YTD

2008 Full Year Proj

Credit Cards 66 66 91 54.6 95

Autos 103 84 62 32.6 50

Home Equity 559 555 224 0

Student Loans 64 65 48 23.8 30

Global RMBS 35 69 66 30

Equipment 9 8 6 2.9 5

Other 39 40 32 3.1 20

Total 874 888 529 116.3 230

“Other” includes Floorplan, Motorcycle, Small Business Loans, Time Share, Aircraft, Franchise, and other miscellaneous assets. As of Aug 1, 2008. Source: JPMorgan, IGM CorporateWatch, and Bloomberg.

3IN

TR

OD

UC

TI

ON

TO

AB

S

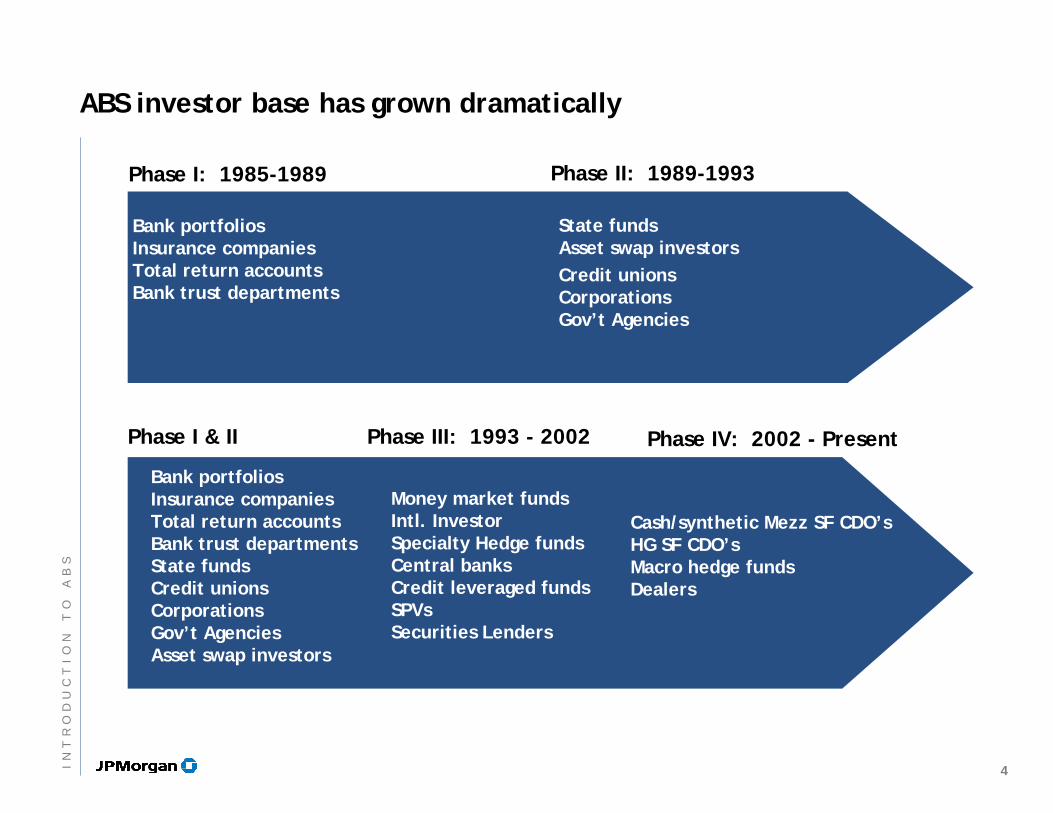

ABS investor base has grown dramatically

Bank portfoliosInsurance companiesTotal return accountsBank trust departments

Phase I: 1985-1989 Phase II: 1989-1993

Phase III: 1993 - 2002

State fundsAsset swap investorsCredit unionsCorporationsGov’t Agencies

Bank portfoliosInsurance companiesTotal return accountsBank trust departmentsState fundsCredit unionsCorporationsGov’t AgenciesAsset swap investors

Money market fundsIntl. InvestorSpecialty Hedge fundsCentral banksCredit leveraged fundsSPVsSecurities Lenders

Cash/synthetic Mezz SF CDO’sHG SF CDO’sMacro hedge fundsDealers

Phase IV: 2002 - PresentPhase I & II

4IN

TR

OD

UC

TI

ON

TO

AB

S

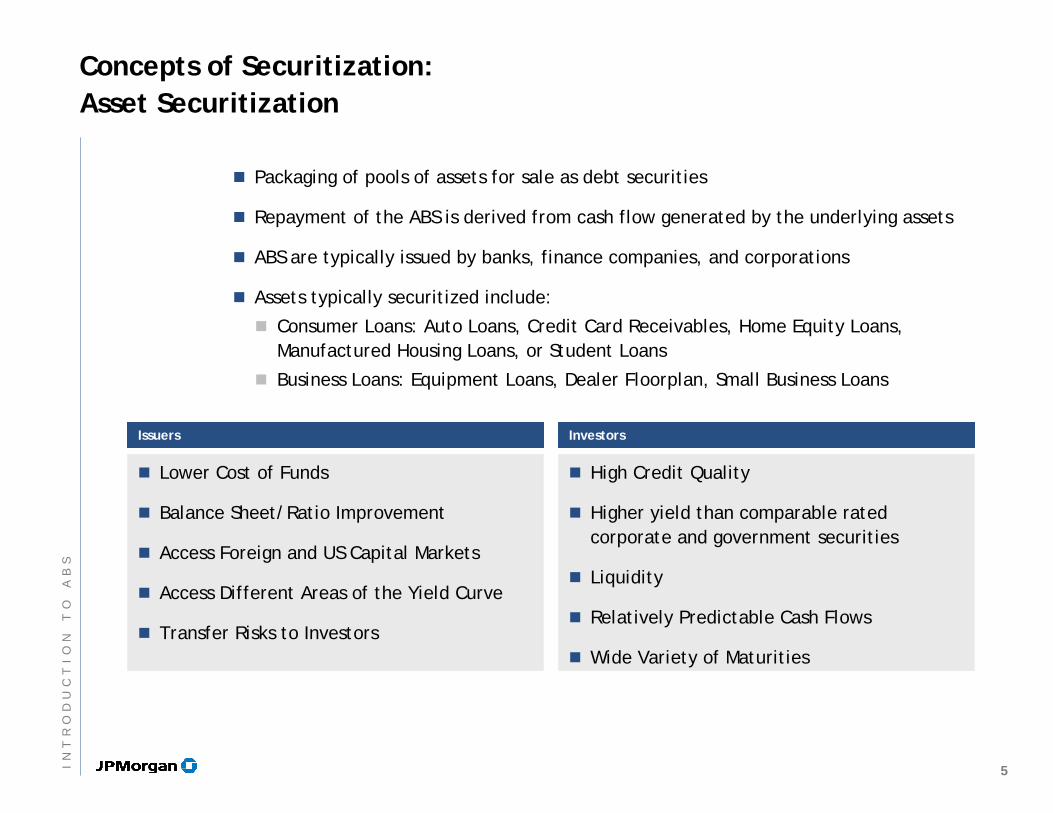

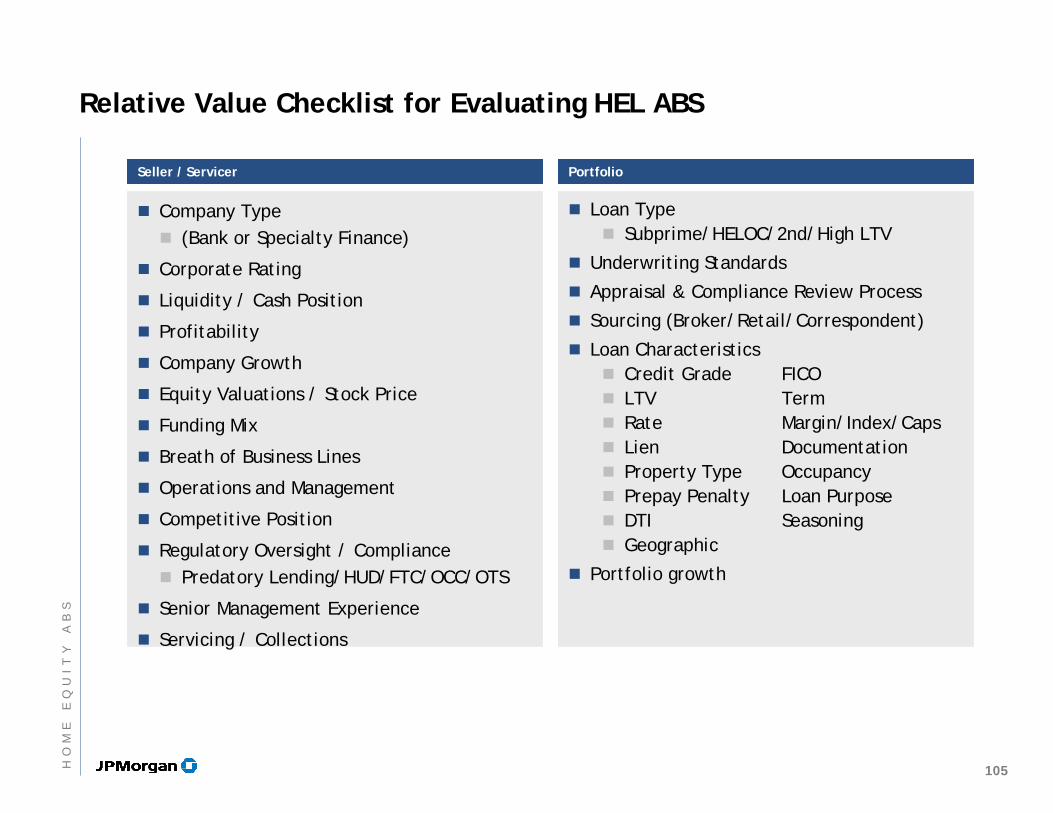

Concepts of Securitization:Asset Securitization

Packaging of pools of assets for sale as debt securities

Repayment of the ABS is derived from cash flow generated by the underlying assets

ABS are typically issued by banks, finance companies, and corporations

Assets typically securitized include:

Consumer Loans: Auto Loans, Credit Card Receivables, Home Equity Loans, Manufactured Housing Loans, or Student Loans

Business Loans: Equipment Loans, Dealer Floorplan, Small Business Loans

IssuersIssuers InvestorsInvestors

Lower Cost of Funds

Balance Sheet/Ratio Improvement

Access Foreign and US Capital Markets

Access Different Areas of the Yield Curve

Transfer Risks to Investors

High Credit Quality

Higher yield than comparable rated corporate and government securities

Liquidity

Relatively Predictable Cash Flows

Wide Variety of Maturities

5IN

TR

OD

UC

TI

ON

TO

AB

S

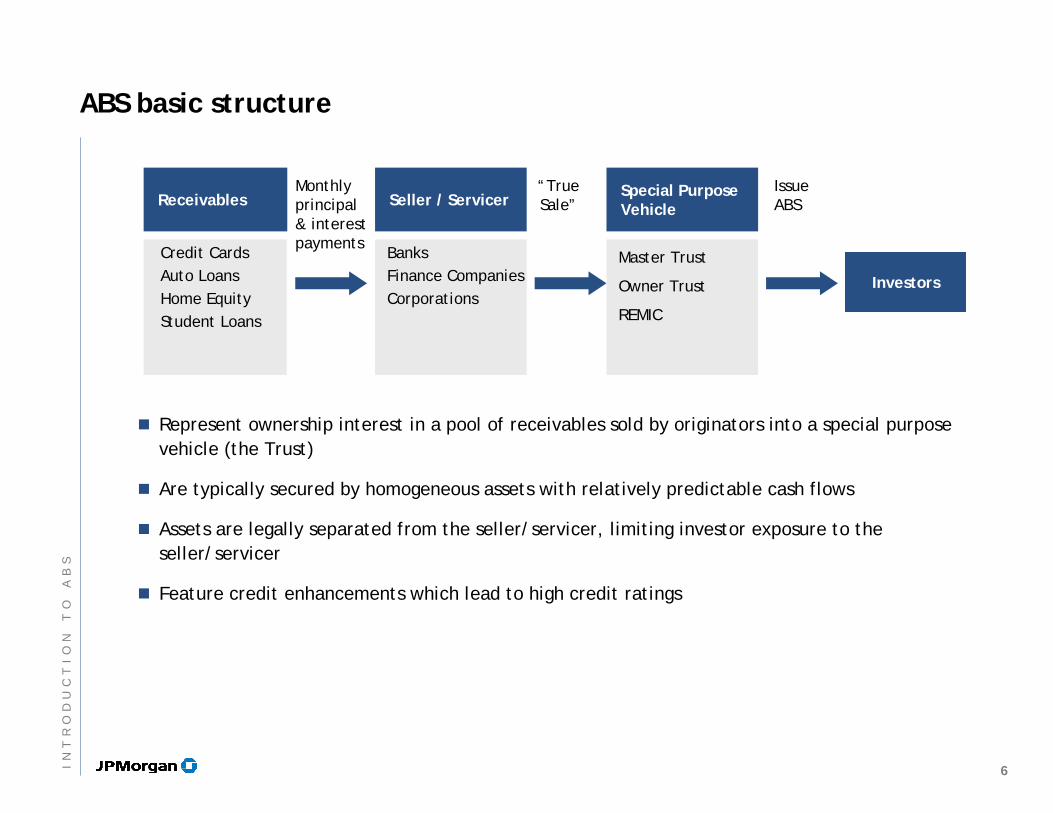

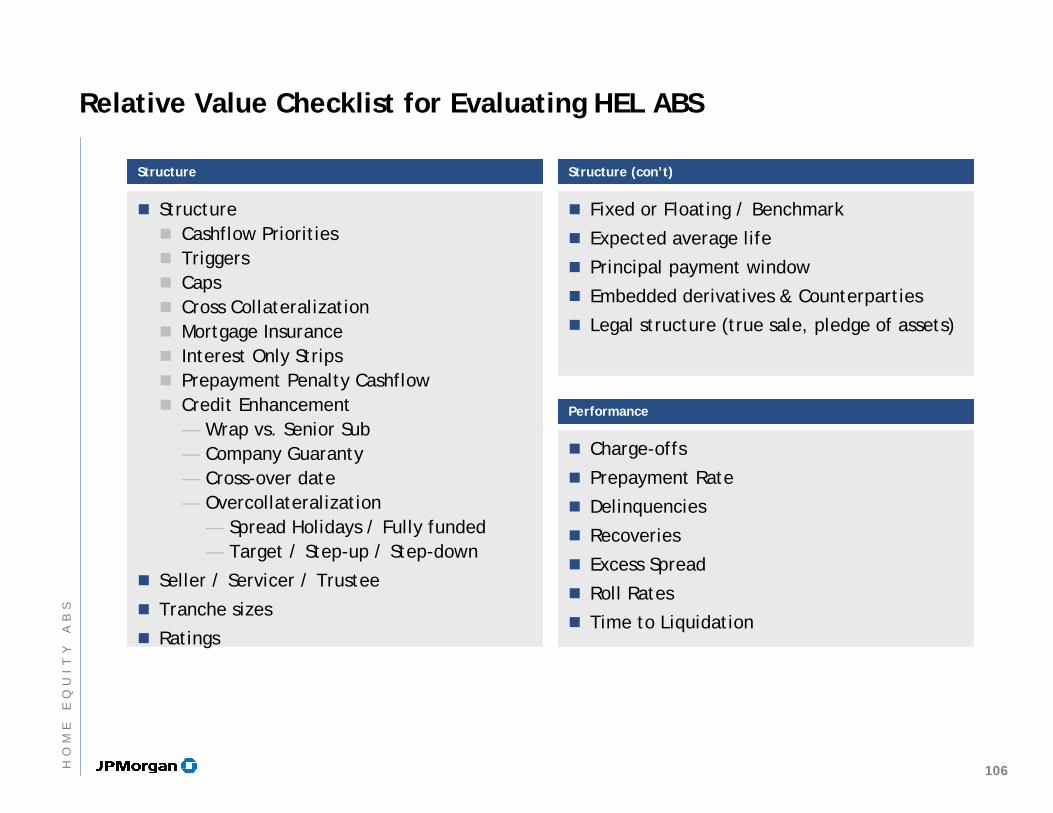

ABS basic structure

Represent ownership interest in a pool of receivables sold by originators into a special purpose vehicle (the Trust)

Are typically secured by homogeneous assets with relatively predictable cash flows

Assets are legally separated from the seller/servicer, limiting investor exposure to the seller/servicer

Feature credit enhancements which lead to high credit ratings

Monthlyprincipal & interest payments

“True Sale”

Issue ABS

Investors

Receivables

Credit CardsAuto LoansHome EquityStudent Loans

Seller / Servicer

BanksFinance CompaniesCorporations

Special Purpose Vehicle

Master Trust

Owner Trust

REMIC

6IN

TR

OD

UC

TI

ON

TO

AB

S

How do ABS issued get AAA Ratings?

AAA Rating

Trust StructureTrust Structure

Bankruptcy Remote Vehicle

Insulates Investor from Issuer

Payout Events /Performance Triggers

Payout Events /Performance Triggers

Protects investors from adverse credit developments

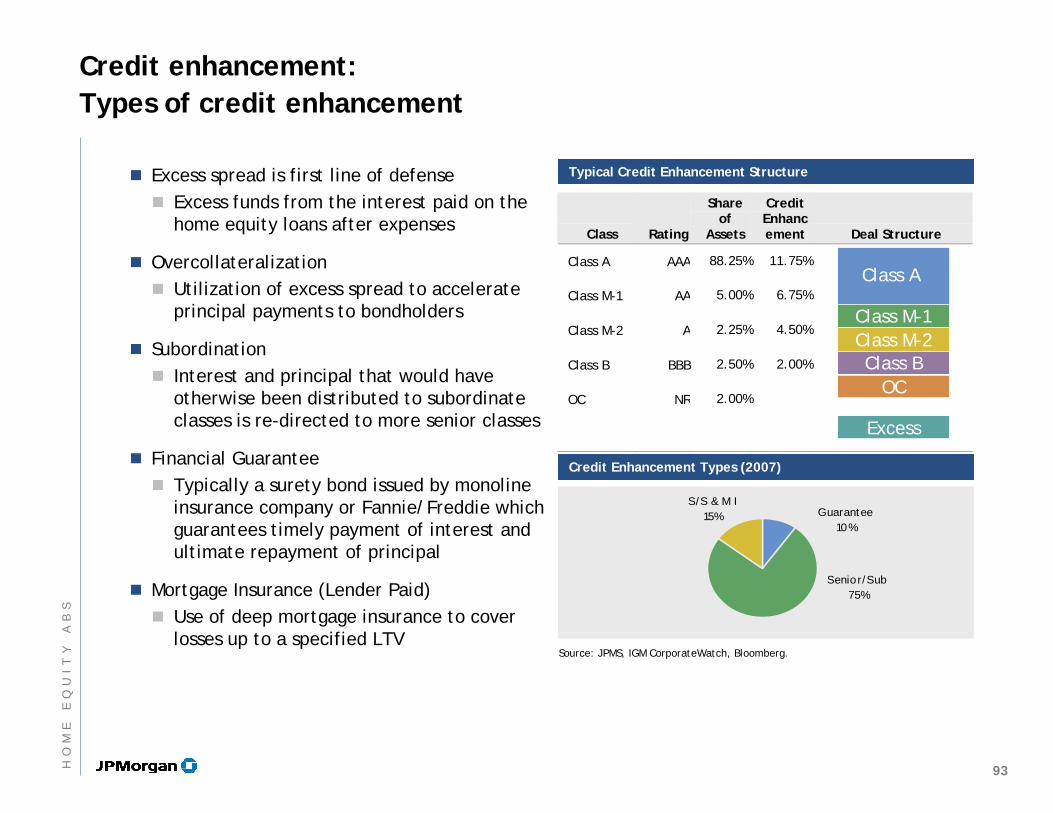

Credit EnhancementCredit Enhancement

Internal

Excess Spread

Subordination

Reserve Fund

Spread Account

Overcollateralization

External

AAA-rated Monoline Insurer

7IN

TR

OD

UC

TI

ON

TO

AB

S

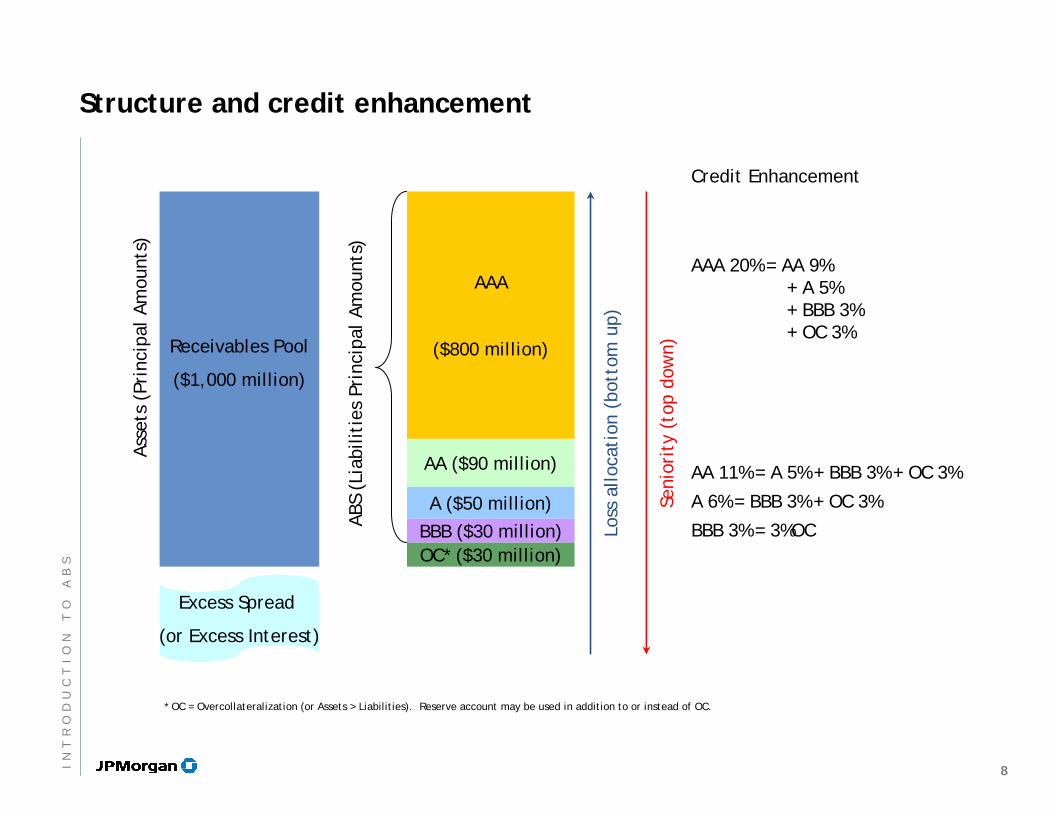

Structure and credit enhancement

Receivables Pool

($1,000 million)

AAA

($800 million)

AA ($90 million)

A ($50 million)BBB ($30 million)OC* ($30 million)

Asse

ts (

Prin

cipa

l Am

ount

s)

ABS

(Lia

bilit

ies

Prin

cipa

l Am

ount

s)

Excess Spread

(or Excess Interest)Lo

ss a

lloca

tion

(bo

ttom

up)

Credit Enhancement

AAA 20% = AA 9% + A 5% + BBB 3% + OC 3%

AA 11% = A 5% + BBB 3% + OC 3%

A 6% = BBB 3% + OC 3%

BBB 3% = 3%OC

* OC = Overcollateralization (or Assets > Liabilities). Reserve account may be used in addition to or instead of OC.

Seni

orit

y (t

op d

own)

8IN

TR

OD

UC

TI

ON

TO

AB

S

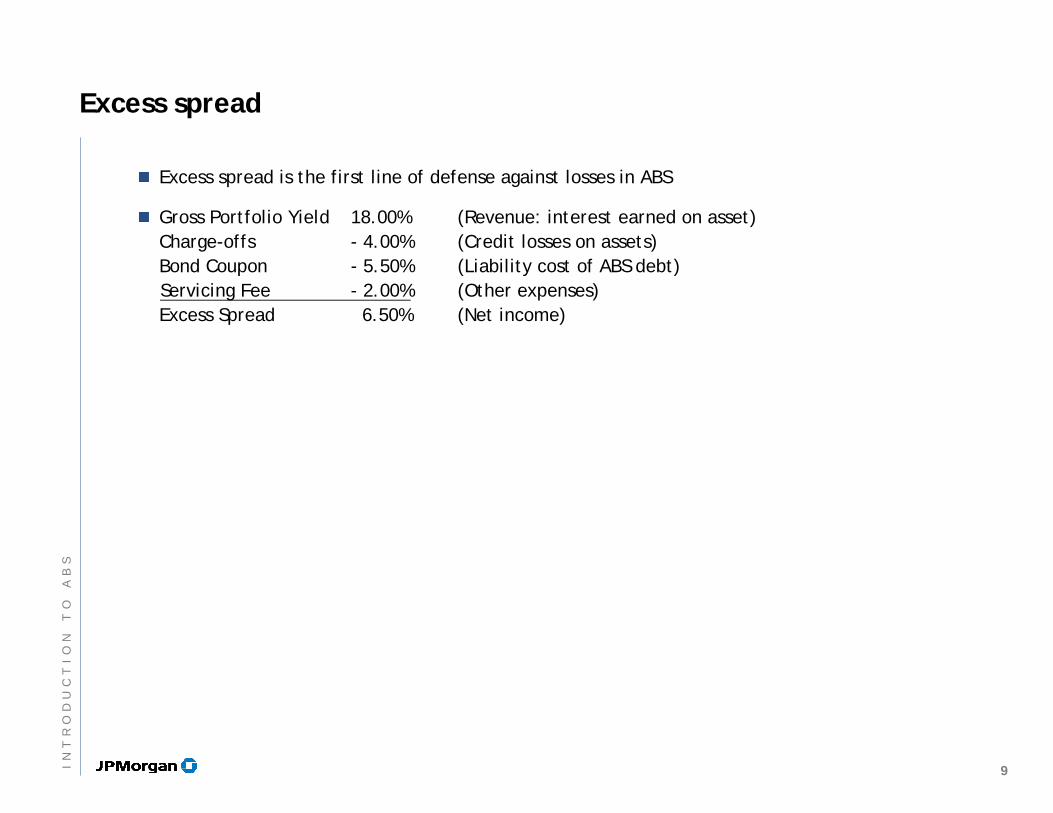

Excess spread

Excess spread is the first line of defense against losses in ABS

Gross Portfolio Yield 18.00% (Revenue: interest earned on asset)Charge-offs - 4.00% (Credit losses on assets)Bond Coupon - 5.50% (Liability cost of ABS debt)Servicing Fee - 2.00% (Other expenses)Excess Spread 6.50% (Net income)

9IN

TR

OD

UC

TI

ON

TO

AB

S

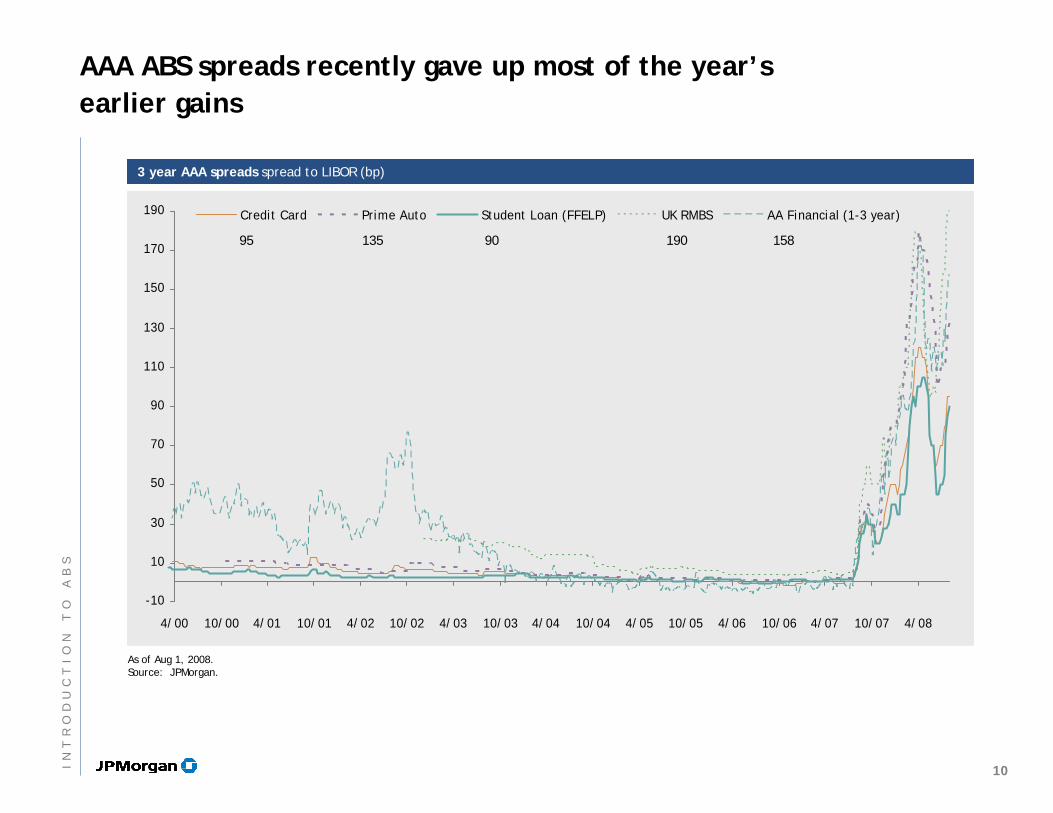

AAA ABS spreads recently gave up most of the year’s earlier gains

As of Aug 1, 2008.Source: JPMorgan.

3 year AAA spreads spread to LIBOR (bp)3 year AAA spreads spread to LIBOR (bp)

-10

10

30

50

70

90

110

130

150

170

190

4/00 10/00 4/01 10/01 4/02 10/02 4/03 10/03 4/04 10/04 4/05 10/05 4/06 10/06 4/07 10/07 4/08

Credit Card Prime Auto Student Loan (FFELP) UK RMBS AA Financial (1-3 year)

95 135 90 190 158

10IN

TR

OD

UC

TI

ON

TO

AB

S

AgendaAgenda

Page

Home Equity ABS

Student Loan ABS (FFELP)

Automobile ABS

Credit Card

Introduction to ABS

11

1

11

35

53

86

IN

VE

ST

IN

GI

NA

SS

ET

BA

CK

ED

SE

CU

RI

TI

ES

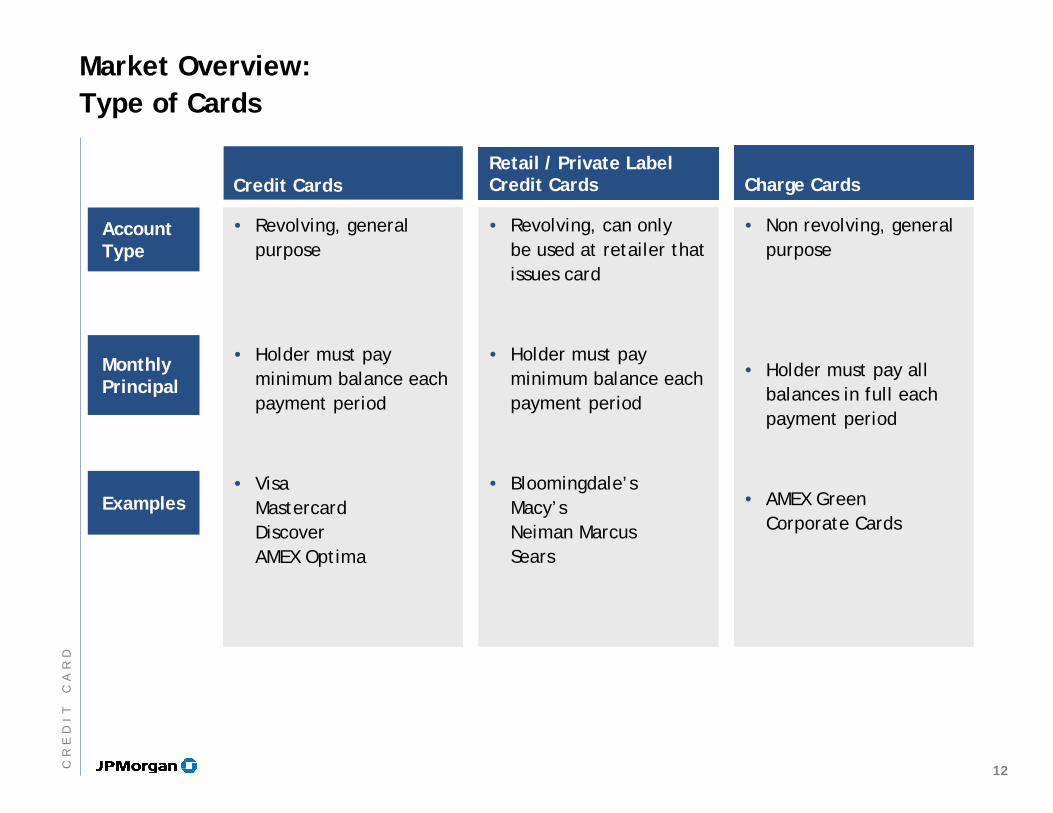

Credit CardsCredit CardsRetail / Private LabelCredit CardsRetail / Private LabelCredit Cards Charge CardsCharge Cards

Market Overview:Type of Cards

Revolving, general purpose

Holder must pay minimum balance each payment period

VisaMastercardDiscoverAMEX Optima

Revolving, can onlybe used at retailer that issues card

Holder must pay minimum balance each payment period

Bloomingdale’sMacy’sNeiman MarcusSears

Non revolving, general purpose

Holder must pay all balances in full each payment period

AMEX GreenCorporate Cards

AccountType

MonthlyPrincipal

Examples

12CR

ED

IT

CA

RD

Market Overview:Types of Credit Cards

Affinity cards

Cards marketed to a specific group to promote loyalty(e.g. college, sports team, professional organization)

“Teaser” rate cards

Have a low introductory APR. After the introductory period, the APR increases to a market rate

Co-branded cards

Visa / MasterCard jointly marketed with a retailer that often provide rewards at that retailer (e.g. Nordstrom VISA card)

Secured cards

Cards with credit limits backed by a cash security deposit

13CR

ED

IT

CA

RD

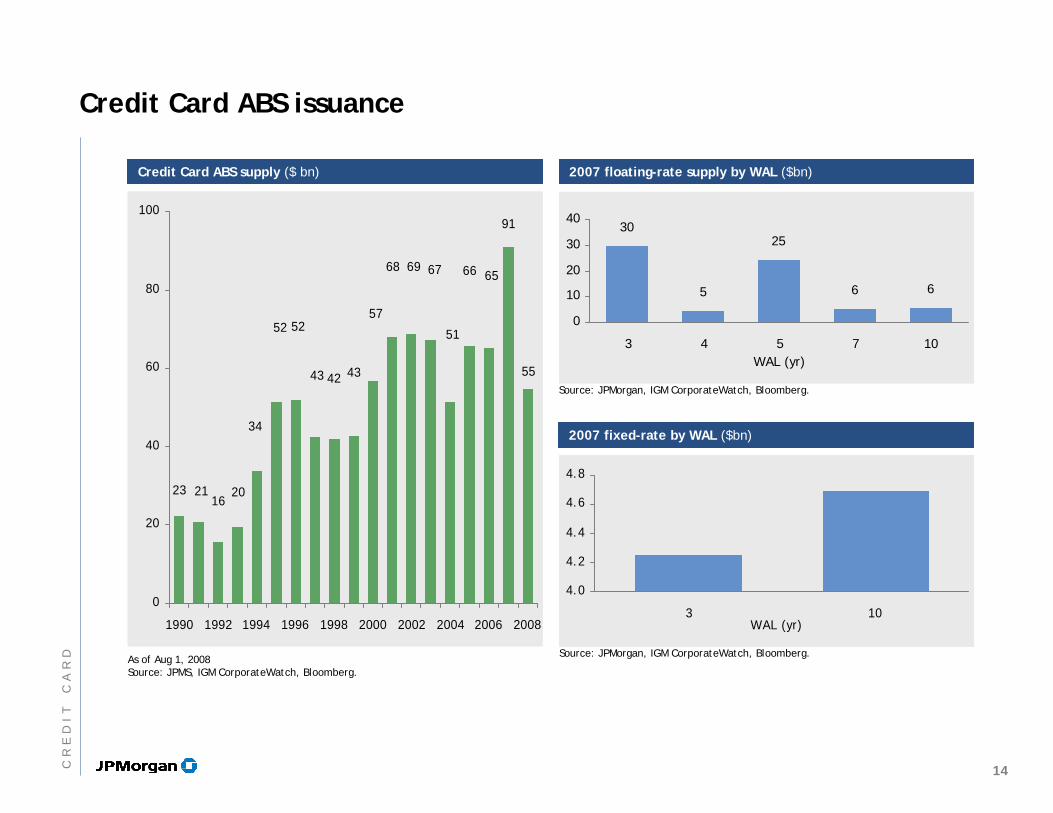

Credit Card ABS issuance

Credit Card ABS supply ($ bn)Credit Card ABS supply ($ bn)

55

91

6566

51

676968

57

434243

5252

34

2016

2123

0

20

40

60

80

100

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

As of Aug 1, 2008Source: JPMS, IGM CorporateWatch, Bloomberg.

Source: JPMorgan, IGM CorporateWatch, Bloomberg.

Source: JPMorgan, IGM CorporateWatch, Bloomberg.

2007 floating-rate supply by WAL ($bn)2007 floating-rate supply by WAL ($bn)

2007 fixed-rate by WAL ($bn)2007 fixed-rate by WAL ($bn)

30

5

25

6 6

0

10

20

30

40

3 4 5 7 10WAL (yr)

4.0

4.2

4.4

4.6

4.8

3 10WAL (yr)

14CR

ED

IT

CA

RD

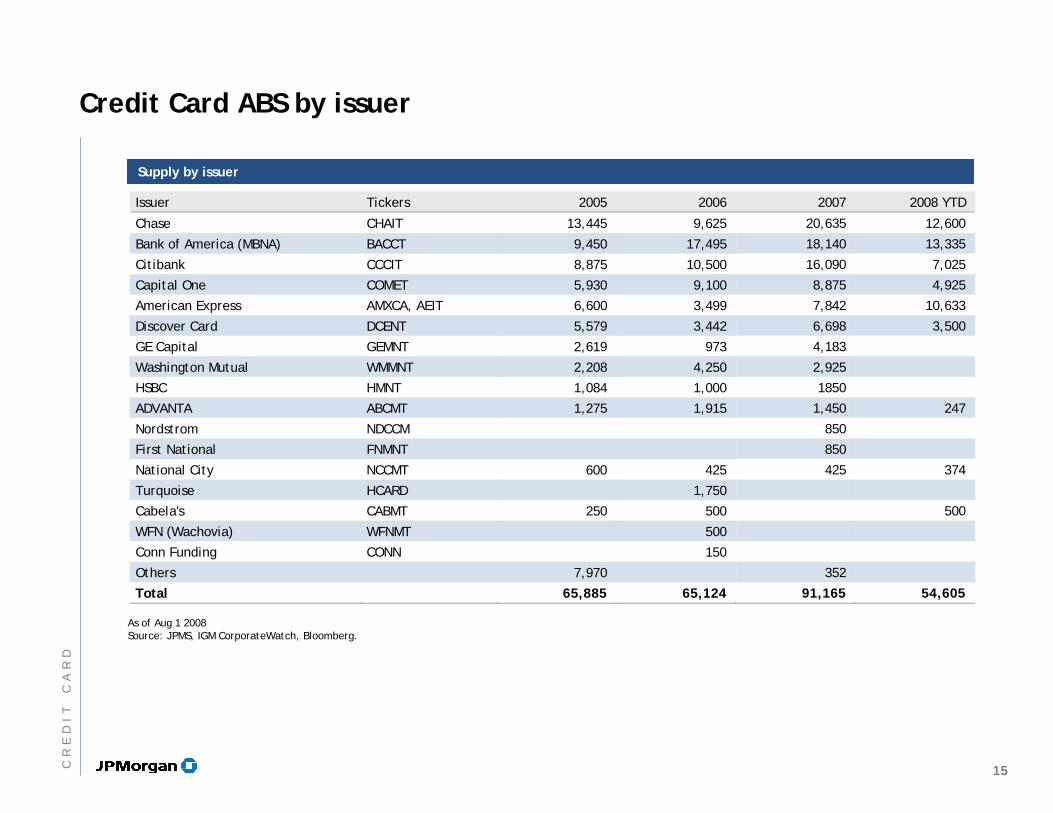

Credit Card ABS by issuer

Supply by issuerSupply by issuer

As of Aug 1 2008Source: JPMS, IGM CorporateWatch, Bloomberg.

Issuer Tickers 2005 2006 2007 2008 YTD

Chase CHAIT 13,445 9,625 20,635 12,600

Bank of America (MBNA) BACCT 9,450 17,495 18,140 13,335

Citibank CCCIT 8,875 10,500 16,090 7,025

Capital One COMET 5,930 9,100 8,875 4,925

American Express AMXCA, AEIT 6,600 3,499 7,842 10,633

Discover Card DCENT 5,579 3,442 6,698 3,500

GE Capital GEMNT 2,619 973 4,183

Washington Mutual WMMNT 2,208 4,250 2,925

HSBC HMNT 1,084 1,000 1850

ADVANTA ABCMT 1,275 1,915 1,450 247

Nordstrom NDCCM 850

First National FNMNT 850

National City NCCMT 600 425 425 374

Turquoise HCARD 1,750

Cabela's CABMT 250 500 500

WFN (Wachovia) WFNMT 500

Conn Funding CONN 150

Others 7,970 352

Total 65,885 65,124 91,165 54,605

15CR

ED

IT

CA

RD

Structure:Structural Features of Credit Card ABS

Trust Structures

Master note trust: “delinked”

Master trust

Cashflow Mechanics

Revolving period

Soft bullet

Controlled amortization (CAM)

Credit Enhancement

As unsecured revolving debt obligations, credit card receivables offer limited recovery in the event of a cardholder default.

Credit enhancement protects investors from resulting losses

Typical Credit Card ABS Deal Characteristics

Pricing Benchmarks Swaps, LIBOR

Coupon Type Fixed or Floating

Typical New Issue Size $1.0 billion

16CR

ED

IT

CA

RD

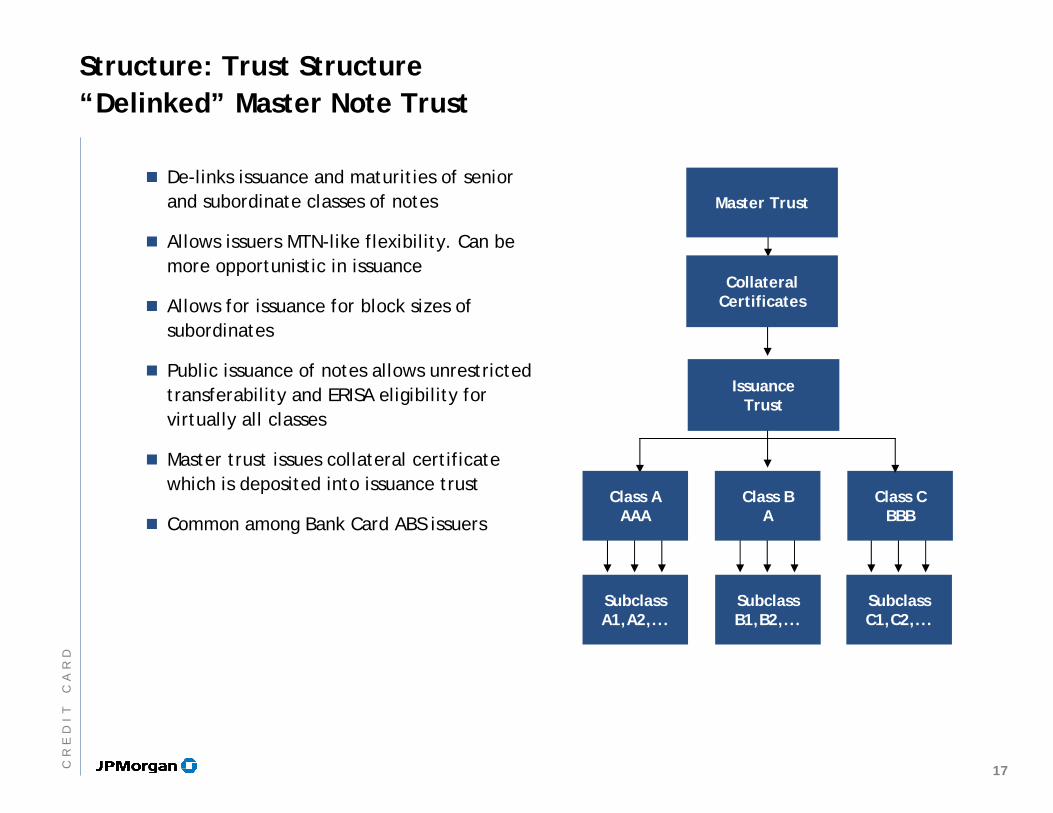

Structure: Trust Structure“Delinked” Master Note Trust

De-links issuance and maturities of senior and subordinate classes of notes

Allows issuers MTN-like flexibility. Can be more opportunistic in issuance

Allows for issuance for block sizes of subordinates

Public issuance of notes allows unrestricted transferability and ERISA eligibility for virtually all classes

Master trust issues collateral certificate which is deposited into issuance trust

Common among Bank Card ABS issuers

SubclassC1,C2,...

SubclassA1,A2,...

SubclassB1,B2,...

Class BA

Class AAAA

Class CBBB

Master Trust

CollateralCertificates

IssuanceTrust

17CR

ED

IT

CA

RD

Structure: Cashflow MechanicsRevolving Period

The interest-only period, during which time bondholders receive interest payments but no principal payments

Revolving period typically lasts from 1–10 years, depending on the life of the transaction

It is followed by the controlled amortization or accumulation period

Monthly principal collections are used to purchase new receivables

Revolving period can be terminated early if certain early amortization events occur

18CR

ED

IT

CA

RD

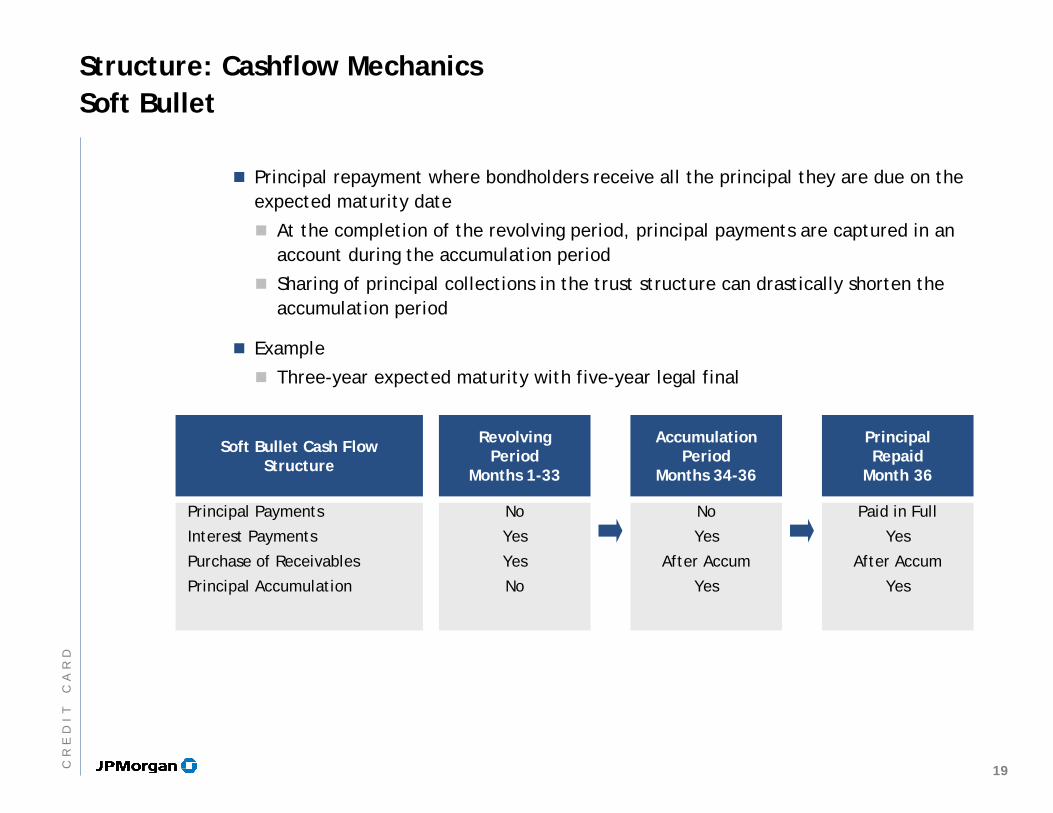

Structure: Cashflow Mechanics Soft Bullet

Principal repayment where bondholders receive all the principal they are due on the expected maturity date

At the completion of the revolving period, principal payments are captured in an account during the accumulation period

Sharing of principal collections in the trust structure can drastically shorten the accumulation period

Example

Three-year expected maturity with five-year legal final

Revolving Period

Months 1-33

No

Yes

Yes

No

Accumulation Period

Months 34-36

No

Yes

After Accum

Yes

PrincipalRepaid

Month 36

Paid in Full

Yes

After Accum

Yes

Soft Bullet Cash Flow Structure

Principal Payments

Interest Payments

Purchase of Receivables

Principal Accumulation

19CR

ED

IT

CA

RD

0

20

40

60

80

100

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36

Interest paid to investor Principal paid to investor

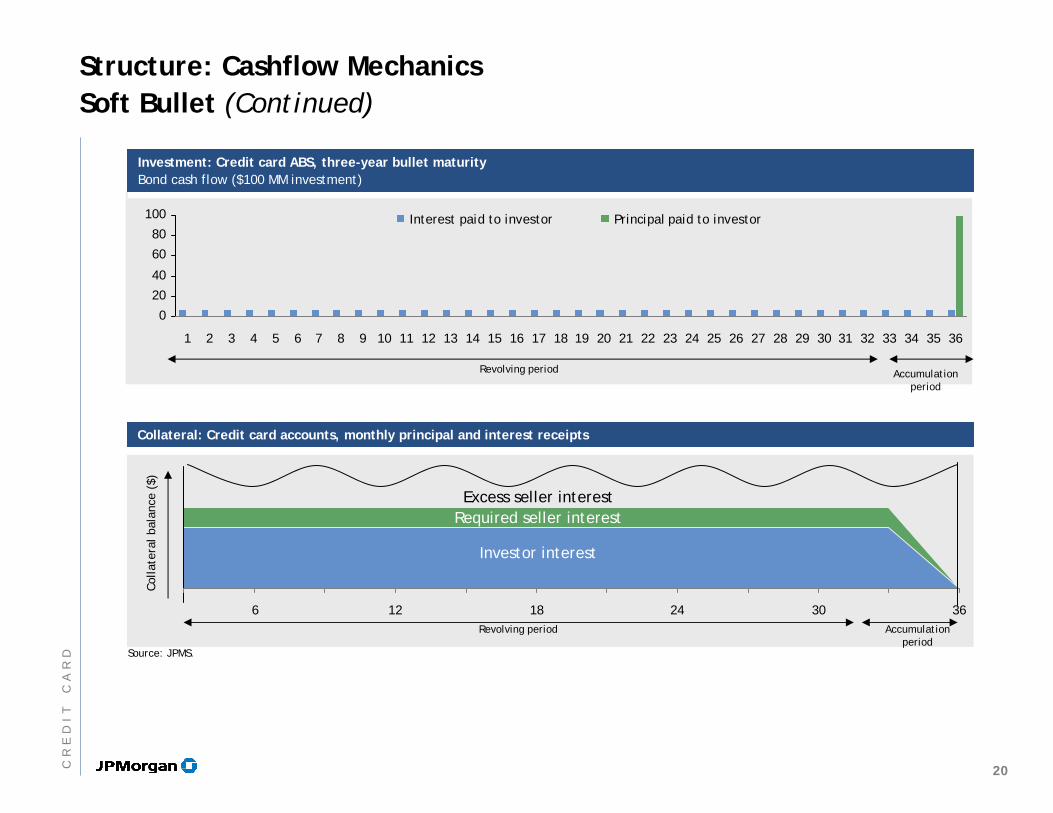

Investment: Credit card ABS, three-year bullet maturityBond cash flow ($100 MM investment)

Investment: Credit card ABS, three-year bullet maturityBond cash flow ($100 MM investment)

Collateral: Credit card accounts, monthly principal and interest receiptsCollateral: Credit card accounts, monthly principal and interest receipts

Source: JPMS.

6 12 18 24 30 36

Structure: Cashflow Mechanics Soft Bullet (Continued)

Revolving period Accumulation period

Excess seller interestRequired seller interest

Investor interest

Revolving period Accumulation period

Colla

tera

l bal

ance

($)

20CR

ED

IT

CA

RD

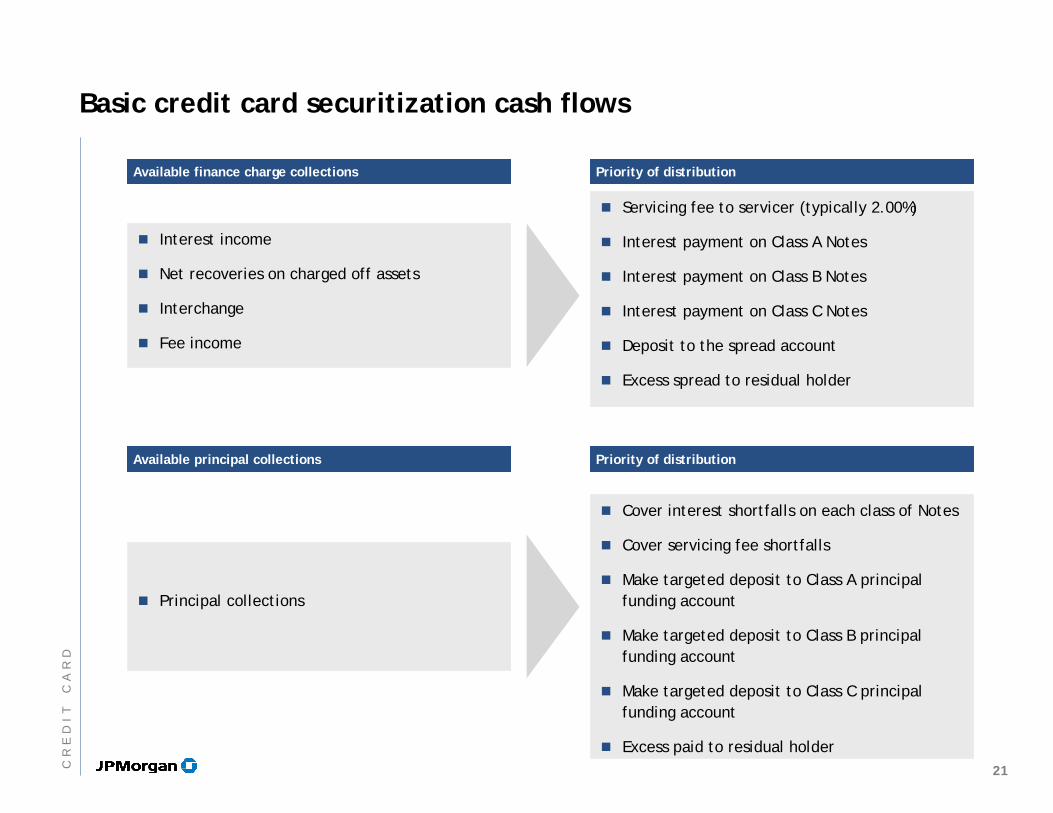

Basic credit card securitization cash flows

Interest income

Net recoveries on charged off assets

Interchange

Fee income

Servicing fee to servicer (typically 2.00%)

Interest payment on Class A Notes

Interest payment on Class B Notes

Interest payment on Class C Notes

Deposit to the spread account

Excess spread to residual holder

Available finance charge collectionsAvailable finance charge collections Priority of distributionPriority of distribution

Available principal collectionsAvailable principal collections Priority of distributionPriority of distribution

Principal collections

Cover interest shortfalls on each class of Notes

Cover servicing fee shortfalls

Make targeted deposit to Class A principal funding account

Make targeted deposit to Class B principal funding account

Make targeted deposit to Class C principal funding account

Excess paid to residual holder21C

RE

DI

TC

AR

D

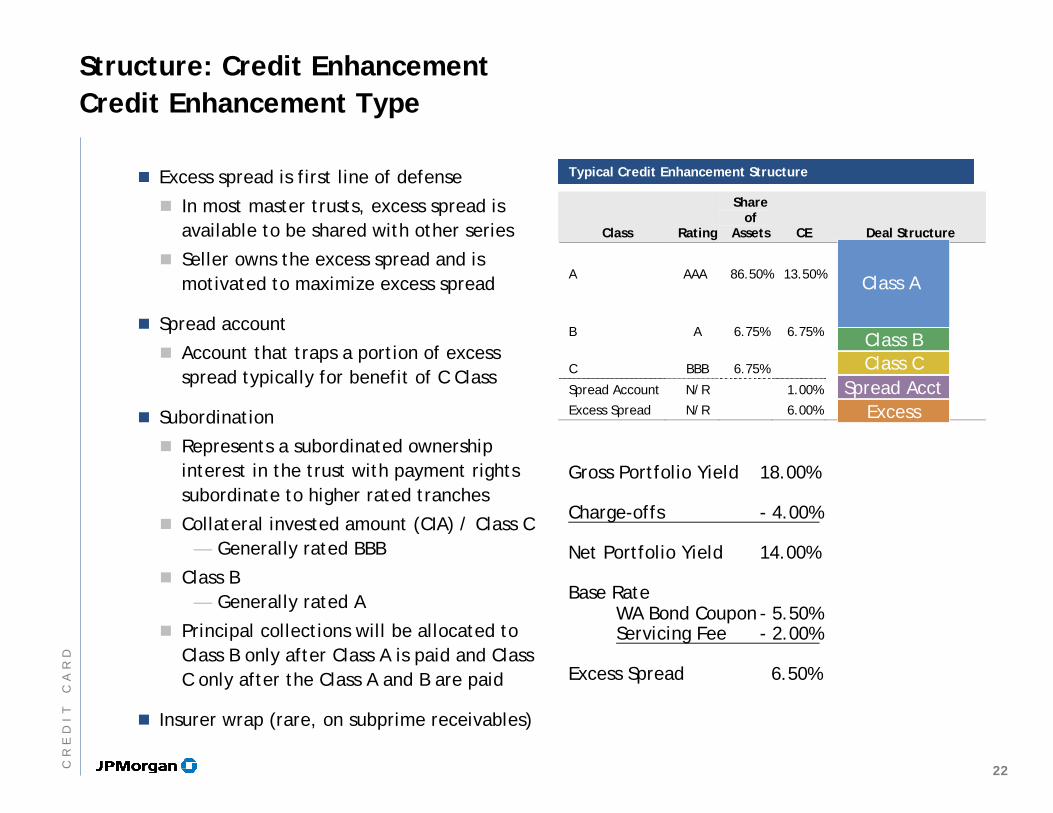

Structure: Credit EnhancementCredit Enhancement Type

Excess spread is first line of defense

In most master trusts, excess spread is available to be shared with other series

Seller owns the excess spread and is motivated to maximize excess spread

Spread account

Account that traps a portion of excess spread typically for benefit of C Class

Subordination

Represents a subordinated ownership interest in the trust with payment rights subordinate to higher rated tranches

Collateral invested amount (CIA) / Class C — Generally rated BBB

Class B— Generally rated A

Principal collections will be allocated to Class B only after Class A is paid and Class C only after the Class A and B are paid

Insurer wrap (rare, on subprime receivables)

Class Rating

Share of

Assets CE Deal Structure

A

AAA

86.50%

13.50%

B

A

6.75%

6.75%

C BBB 6.75%

Spread Account N/R 1.00%

Excess Spread N/R 6.00%

Class A

Class BClass C

ExcessSpread Acct

Typical Credit Enhancement StructureTypical Credit Enhancement Structure

Gross Portfolio Yield 18.00%

Charge-offs - 4.00%

Net Portfolio Yield 14.00%

Base RateWA Bond Coupon - 5.50%Servicing Fee - 2.00%

Excess Spread 6.50%

22CR

ED

IT

CA

RD

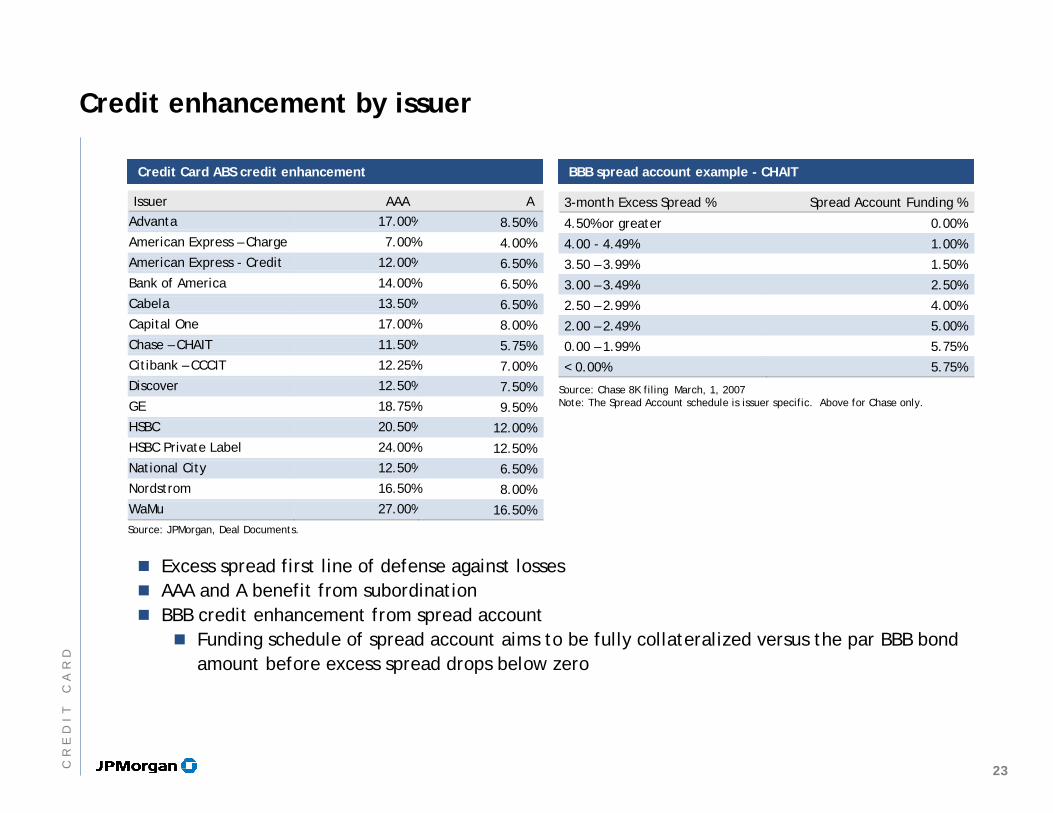

Credit enhancement by issuer

Credit Card ABS credit enhancement Credit Card ABS credit enhancement

Source: JPMorgan, Deal Documents.

BBB spread account example - CHAITBBB spread account example - CHAIT

3-month Excess Spread % Spread Account Funding %

4.50% or greater 0.00%

4.00 - 4.49% 1.00%

3.50 – 3.99% 1.50%

3.00 – 3.49% 2.50%

2.50 – 2.99% 4.00%

2.00 – 2.49% 5.00%

0.00 – 1.99% 5.75%

< 0.00% 5.75%

Source: Chase 8K filing March, 1, 2007Note: The Spread Account schedule is issuer specific. Above for Chase only.

Excess spread first line of defense against lossesAAA and A benefit from subordinationBBB credit enhancement from spread account

Funding schedule of spread account aims to be fully collateralized versus the par BBB bond amount before excess spread drops below zero

Issuer AAA A Advanta 17.00% 8.50% American Express – Charge 7.00% 4.00% American Express - Credit 12.00% 6.50% Bank of America 14.00% 6.50% Cabela 13.50% 6.50% Capital One 17.00% 8.00% Chase – CHAIT 11.50% 5.75% Citibank – CCCIT 12.25% 7.00% Discover 12.50% 7.50% GE 18.75% 9.50% HSBC 20.50% 12.00% HSBC Private Label 24.00% 12.50% National City 12.50% 6.50% Nordstrom 16.50% 8.00% WaMu 27.00% 16.50%

23CR

ED

IT

CA

RD

Structure: Cashflow Mechanics Early Amortization Events Protect Investors

Deals are structured with early amortization triggers to protect investors from extended exposure to deteriorating asset quality. If an early amortization event occurs, deal begins to pay out immediately.

All principal collections become allocable to investors immediately and cash on deposit in accumulation account is paid to investors sequentially

Principal is no longer limited to controlled amortization/accumulation amount

Investors get a portion of principal normally allocable to the seller

Typical Early Amortization Events

Seller/Servicer— Failure or inability to make required deposits or payments— Failure or inability to transfer receivables to the trust when necessary— False representations or warranties— Certain events of default, bankruptcy, or receivership of the seller or servicer

Legal— Trust becomes classified as an “investment company” under the Investment

Company Act of 1940

Performance— Three-month average excess spread falls below a minimum level (i.e., zero)— Seller’s participation falls below the required level— Portfolio principal balance falls below the invested amount

24CR

ED

IT

CA

RD

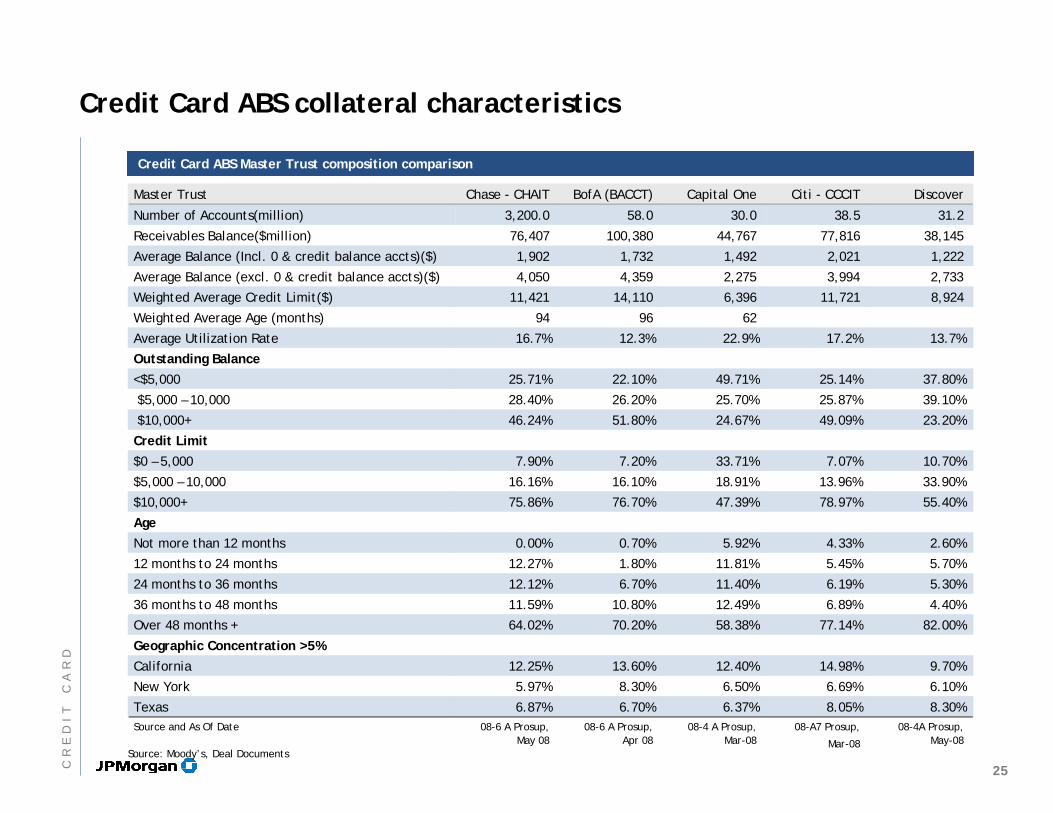

Credit Card ABS collateral characteristics

Credit Card ABS Master Trust composition comparison Credit Card ABS Master Trust composition comparison

Source: Moody’s, Deal Documents

Master Trust Chase - CHAIT BofA (BACCT) Capital One Citi - CCCIT Discover

Number of Accounts(million) 3,200.0 58.0 30.0 38.5 31.2

Receivables Balance($million) 76,407 100,380 44,767 77,816 38,145

Average Balance (Incl. 0 & credit balance accts)($) 1,902 1,732 1,492 2,021 1,222

Average Balance (excl. 0 & credit balance accts)($) 4,050 4,359 2,275 3,994 2,733

Weighted Average Credit Limit($) 11,421 14,110 6,396 11,721 8,924

Weighted Average Age (months) 94 96 62

Average Utilization Rate 16.7% 12.3% 22.9% 17.2% 13.7%

Outstanding Balance

<$5,000 25.71% 22.10% 49.71% 25.14% 37.80%

$5,000 – 10,000 28.40% 26.20% 25.70% 25.87% 39.10%

$10,000+ 46.24% 51.80% 24.67% 49.09% 23.20%

Credit Limit

$0 – 5,000 7.90% 7.20% 33.71% 7.07% 10.70%

$5,000 – 10,000 16.16% 16.10% 18.91% 13.96% 33.90%

$10,000+ 75.86% 76.70% 47.39% 78.97% 55.40%

Age

Not more than 12 months 0.00% 0.70% 5.92% 4.33% 2.60%

12 months to 24 months 12.27% 1.80% 11.81% 5.45% 5.70%

24 months to 36 months 12.12% 6.70% 11.40% 6.19% 5.30%

36 months to 48 months 11.59% 10.80% 12.49% 6.89% 4.40%

Over 48 months + 64.02% 70.20% 58.38% 77.14% 82.00%

Geographic Concentration >5%

California 12.25% 13.60% 12.40% 14.98% 9.70%

New York 5.97% 8.30% 6.50% 6.69% 6.10%

Texas 6.87% 6.70% 6.37% 8.05% 8.30% Source and As Of Date 08-6 A Prosup,

May 08 08-6 A Prosup,

Apr 08 08-4 A Prosup,

Mar-08 08-A7 Prosup,

Mar-08

08-4A Prosup, May-08

25C

RE

DI

TC

AR

D

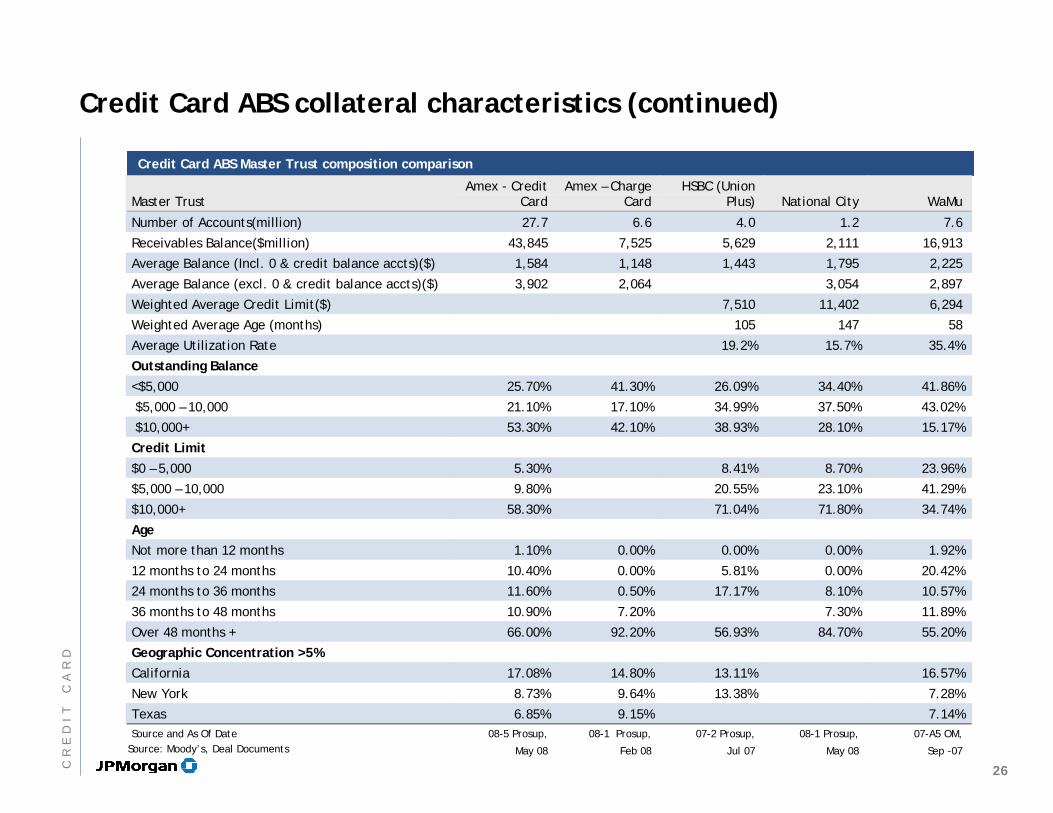

Credit Card ABS collateral characteristics (continued)

Credit Card ABS Master Trust composition comparison Credit Card ABS Master Trust composition comparison

Master Trust Amex - Credit

Card Amex – Charge

Card HSBC (Union

Plus) National City WaMu

Number of Accounts(million) 27.7 6.6 4.0 1.2 7.6

Receivables Balance($million) 43,845 7,525 5,629 2,111 16,913

Average Balance (Incl. 0 & credit balance accts)($) 1,584 1,148 1,443 1,795 2,225

Average Balance (excl. 0 & credit balance accts)($) 3,902 2,064 3,054 2,897

Weighted Average Credit Limit($) 7,510 11,402 6,294

Weighted Average Age (months) 105 147 58

Average Utilization Rate 19.2% 15.7% 35.4%

Outstanding Balance

<$5,000 25.70% 41.30% 26.09% 34.40% 41.86%

$5,000 – 10,000 21.10% 17.10% 34.99% 37.50% 43.02%

$10,000+ 53.30% 42.10% 38.93% 28.10% 15.17%

Credit Limit

$0 – 5,000 5.30% 8.41% 8.70% 23.96%

$5,000 – 10,000 9.80% 20.55% 23.10% 41.29%

$10,000+ 58.30% 71.04% 71.80% 34.74%

Age

Not more than 12 months 1.10% 0.00% 0.00% 0.00% 1.92%

12 months to 24 months 10.40% 0.00% 5.81% 0.00% 20.42%

24 months to 36 months 11.60% 0.50% 17.17% 8.10% 10.57%

36 months to 48 months 10.90% 7.20% 7.30% 11.89%

Over 48 months + 66.00% 92.20% 56.93% 84.70% 55.20%

Geographic Concentration >5%

California 17.08% 14.80% 13.11% 16.57%

New York 8.73% 9.64% 13.38% 7.28%

Texas 6.85% 9.15% 7.14% Source and As Of Date 08-5 Prosup,

May 08

08-1 Prosup,

Feb 08

07-2 Prosup,

Jul 07

08-1 Prosup,

May 08

07-A5 OM,

Sep -07

Source: Moody’s, Deal Documents

26CR

ED

IT

CA

RD

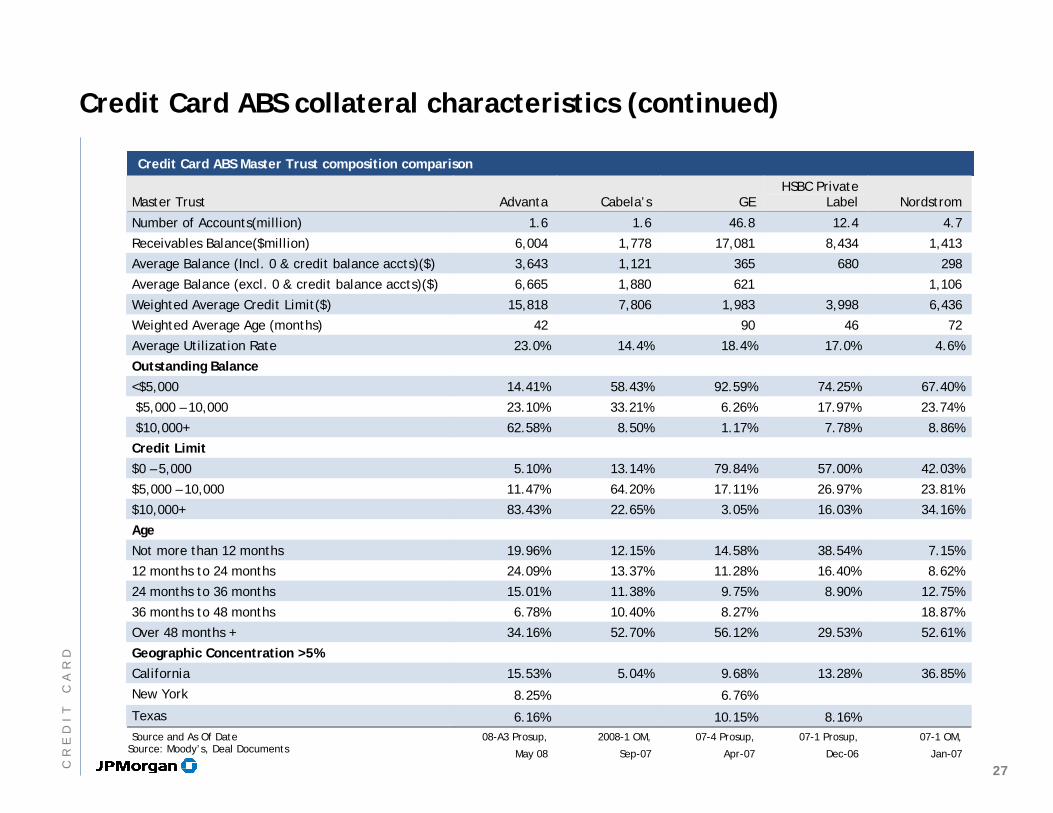

Credit Card ABS collateral characteristics (continued)

Credit Card ABS Master Trust composition comparison Credit Card ABS Master Trust composition comparison

Master Trust Advanta Cabela’s GE HSBC Private

Label Nordstrom

Number of Accounts(million) 1.6 1.6 46.8 12.4 4.7

Receivables Balance($million) 6,004 1,778 17,081 8,434 1,413

Average Balance (Incl. 0 & credit balance accts)($) 3,643 1,121 365 680 298

Average Balance (excl. 0 & credit balance accts)($) 6,665 1,880 621 1,106

Weighted Average Credit Limit($) 15,818 7,806 1,983 3,998 6,436

Weighted Average Age (months) 42 90 46 72

Average Utilization Rate 23.0% 14.4% 18.4% 17.0% 4.6%

Outstanding Balance

<$5,000 14.41% 58.43% 92.59% 74.25% 67.40%

$5,000 – 10,000 23.10% 33.21% 6.26% 17.97% 23.74%

$10,000+ 62.58% 8.50% 1.17% 7.78% 8.86%

Credit Limit

$0 – 5,000 5.10% 13.14% 79.84% 57.00% 42.03%

$5,000 – 10,000 11.47% 64.20% 17.11% 26.97% 23.81%

$10,000+ 83.43% 22.65% 3.05% 16.03% 34.16%

Age

Not more than 12 months 19.96% 12.15% 14.58% 38.54% 7.15%

12 months to 24 months 24.09% 13.37% 11.28% 16.40% 8.62%

24 months to 36 months 15.01% 11.38% 9.75% 8.90% 12.75%

36 months to 48 months 6.78% 10.40% 8.27% 18.87%

Over 48 months + 34.16% 52.70% 56.12% 29.53% 52.61%

Geographic Concentration >5%

California 15.53% 5.04% 9.68% 13.28% 36.85%

New York 8.25% 6.76%

Texas 6.16% 10.15% 8.16%

Source and As Of Date 08-A3 Prosup,

May 08

2008-1 OM,

Sep-07

07-4 Prosup,

Apr-07

07-1 Prosup,

Dec-06

07-1 OM,

Jan-07 Source: Moody’s, Deal Documents

27CR

ED

IT

CA

RD

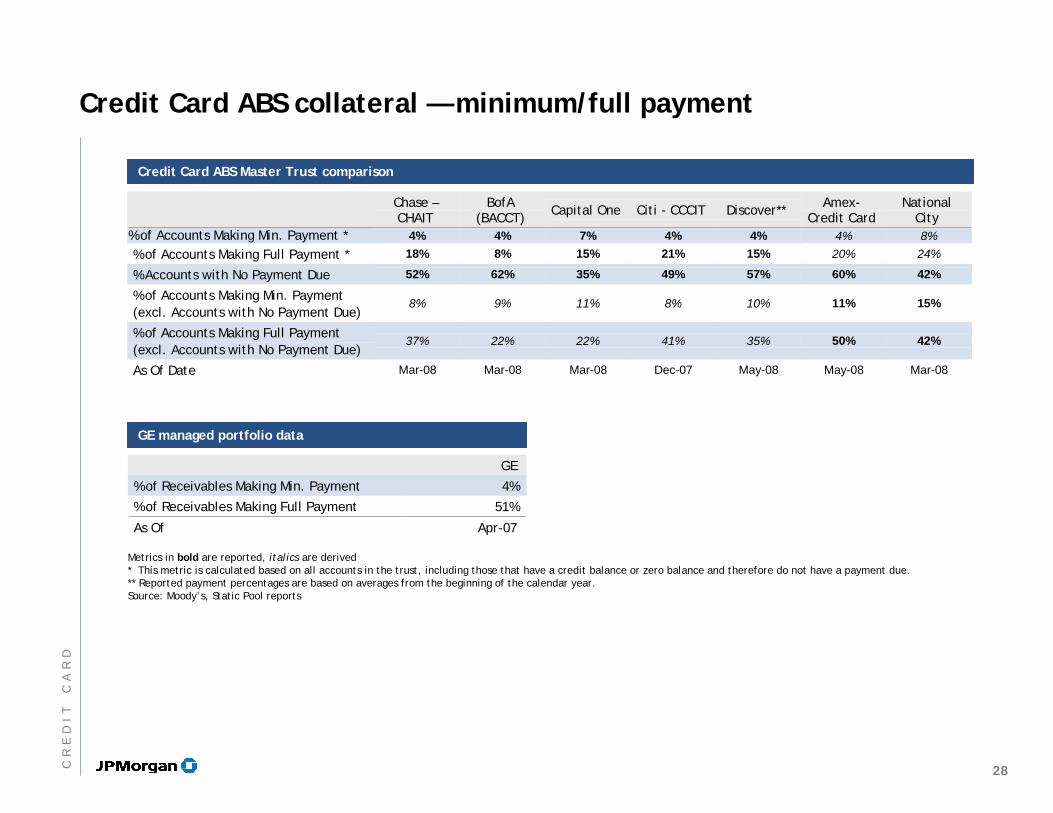

Credit Card ABS collateral — minimum/full payment

Credit Card ABS Master Trust comparison Credit Card ABS Master Trust comparison

Metrics in bold are reported, italics are derived* This metric is calculated based on all accounts in the trust, including those that have a credit balance or zero balance and therefore do not have a payment due.** Reported payment percentages are based on averages from the beginning of the calendar year.Source: Moody’s, Static Pool reports

Chase – CHAIT

BofA (BACCT) Capital One Citi - CCCIT Discover** Amex-

Credit Card National

City % of Accounts Making Min. Payment * 4% 4% 7% 4% 4% 4% 8% % of Accounts Making Full Payment * 18% 8% 15% 21% 15% 20% 24%

% Accounts with No Payment Due 52% 62% 35% 49% 57% 60% 42%

% of Accounts Making Min. Payment (excl. Accounts with No Payment Due)

8% 9% 11% 8% 10% 11% 15%

% of Accounts Making Full Payment (excl. Accounts with No Payment Due)

37% 22% 22% 41% 35% 50% 42%

As Of Date Mar-08 Mar-08 Mar-08 Dec-07 May-08 May-08 Mar-08

GE managed portfolio dataGE managed portfolio data

GE

% of Receivables Making Min. Payment 4%

% of Receivables Making Full Payment 51%

As Of Apr-07

28CR

ED

IT

CA

RD

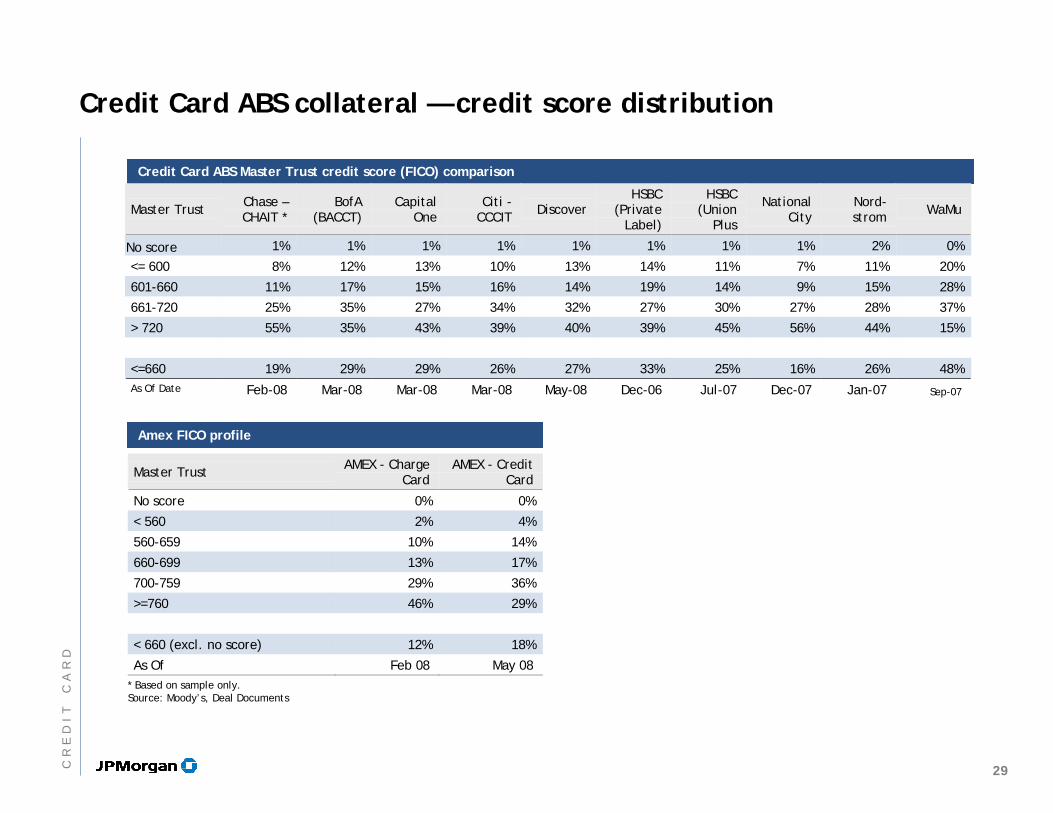

Credit Card ABS collateral — credit score distribution

Credit Card ABS Master Trust credit score (FICO) comparison Credit Card ABS Master Trust credit score (FICO) comparison

* Based on sample only. Source: Moody’s, Deal Documents

Master Trust Chase – CHAIT *

BofA (BACCT)

Capital One

Citi - CCCIT Discover

HSBC (Private

Label)

HSBC (Union

Plus

National City

Nord-strom WaMu

No score 1% 1% 1% 1% 1% 1% 1% 1% 2% 0%

<= 600 8% 12% 13% 10% 13% 14% 11% 7% 11% 20%

601-660 11% 17% 15% 16% 14% 19% 14% 9% 15% 28%

661-720 25% 35% 27% 34% 32% 27% 30% 27% 28% 37%

> 720 55% 35% 43% 39% 40% 39% 45% 56% 44% 15%

<=660 19% 29% 29% 26% 27% 33% 25% 16% 26% 48% As Of Date Feb-08 Mar-08 Mar-08 Mar-08 May-08 Dec-06 Jul-07 Dec-07 Jan-07 Sep-07

Amex FICO profileAmex FICO profile

Master Trust AMEX - Charge Card

AMEX - Credit Card

No score 0% 0%

< 560 2% 4%

560-659 10% 14%

660-699 13% 17%

700-759 29% 36%

>=760 46% 29%

< 660 (excl. no score) 12% 18%

As Of Feb 08 May 08

29CR

ED

IT

CA

RD

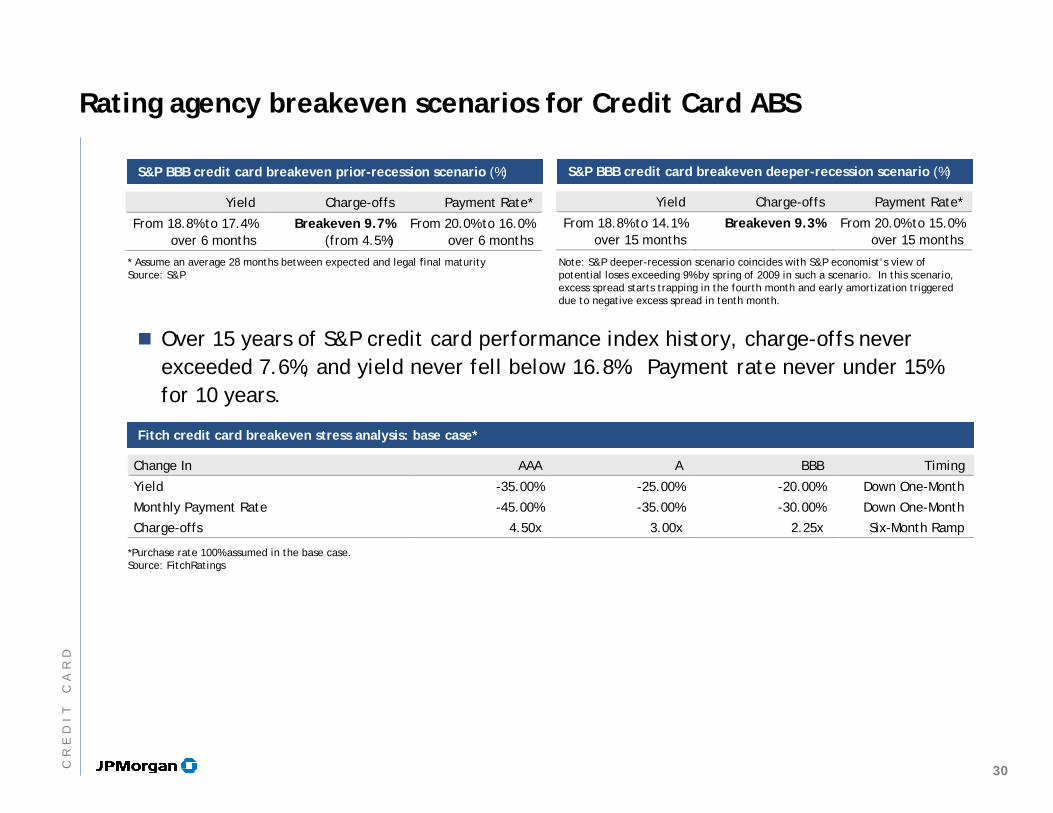

Rating agency breakeven scenarios for Credit Card ABS

Yield Charge-offs Payment Rate*

From 18.8% to 17.4% over 6 months

Breakeven 9.7% (from 4.5%)

From 20.0% to 16.0% over 6 months

S&P BBB credit card breakeven prior-recession scenario (%) S&P BBB credit card breakeven prior-recession scenario (%)

* Assume an average 28 months between expected and legal final maturity Source: S&P

Yield Charge-offs Payment Rate*

From 18.8% to 14.1% over 15 months

Breakeven 9.3% From 20.0% to 15.0% over 15 months

S&P BBB credit card breakeven deeper-recession scenario (%) S&P BBB credit card breakeven deeper-recession scenario (%)

Note: S&P deeper-recession scenario coincides with S&P economist’s view of potential loses exceeding 9% by spring of 2009 in such a scenario. In this scenario, excess spread starts trapping in the fourth month and early amortization triggered due to negative excess spread in tenth month.

Over 15 years of S&P credit card performance index history, charge-offs never exceeded 7.6%, and yield never fell below 16.8%. Payment rate never under 15% for 10 years.

Fitch credit card breakeven stress analysis: base case*Fitch credit card breakeven stress analysis: base case*

Change In AAA A BBB Timing

Yield -35.00% -25.00% -20.00% Down One-Month

Monthly Payment Rate -45.00% -35.00% -30.00% Down One-Month

Charge-offs 4.50x 3.00x 2.25x Six-Month Ramp

*Purchase rate 100% assumed in the base case.Source: FitchRatings

30CR

ED

IT

CA

RD

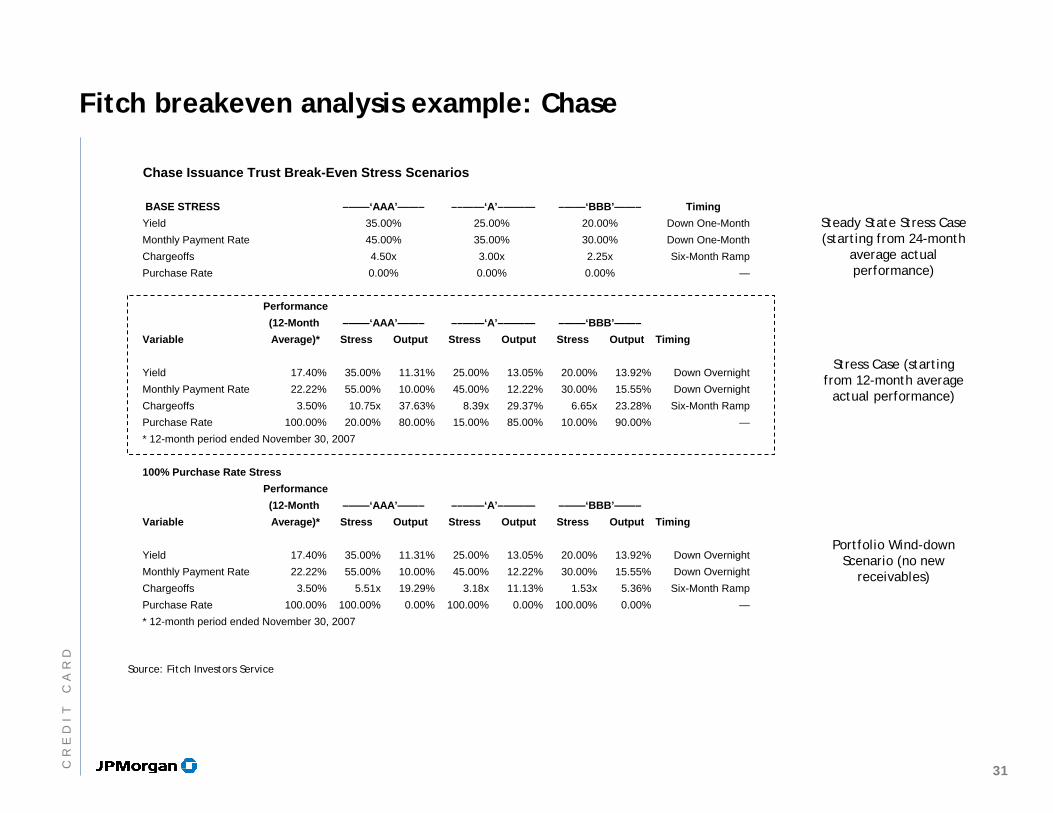

Fitch breakeven analysis example: Chase

Stress Case (starting from 12-month average

actual performance)

Portfolio Wind-down Scenario (no new

receivables)

Steady State Stress Case (starting from 24-month

average actual performance)

Source: Fitch Investors Service

Chase Issuance Trust Break-Even Stress Scenarios

BASE STRESS TimingYield Down One-MonthMonthly Payment Rate Down One-MonthChargeoffs Six-Month RampPurchase Rate —

Performance(12-Month

Variable Average)* Stress Output Stress Output Stress Output Timing

Yield 17.40% 35.00% 11.31% 25.00% 13.05% 20.00% 13.92% Down OvernightMonthly Payment Rate 22.22% 55.00% 10.00% 45.00% 12.22% 30.00% 15.55% Down OvernightChargeoffs 3.50% 10.75x 37.63% 8.39x 29.37% 6.65x 23.28% Six-Month RampPurchase Rate 100.00% 20.00% 80.00% 15.00% 85.00% 10.00% 90.00% —* 12-month period ended November 30, 2007

100% Purchase Rate StressPerformance(12-Month

Variable Average)* Stress Output Stress Output Stress Output Timing

Yield 17.40% 35.00% 11.31% 25.00% 13.05% 20.00% 13.92% Down OvernightMonthly Payment Rate 22.22% 55.00% 10.00% 45.00% 12.22% 30.00% 15.55% Down OvernightChargeoffs 3.50% 5.51x 19.29% 3.18x 11.13% 1.53x 5.36% Six-Month RampPurchase Rate 100.00% 100.00% 0.00% 100.00% 0.00% 100.00% 0.00% —* 12-month period ended November 30, 2007

–——‘AAA’——– ––——‘A’–——— –——‘BBB’——–

0.00% 0.00% 0.00%

–——‘AAA’——– ––——‘A’–——— –——‘BBB’——–

45.00% 35.00% 30.00%4.50x 3.00x 2.25x

–——‘AAA’——– ––——‘A’–——— –——‘BBB’——–35.00% 25.00% 20.00%

31CR

ED

IT

CA

RD

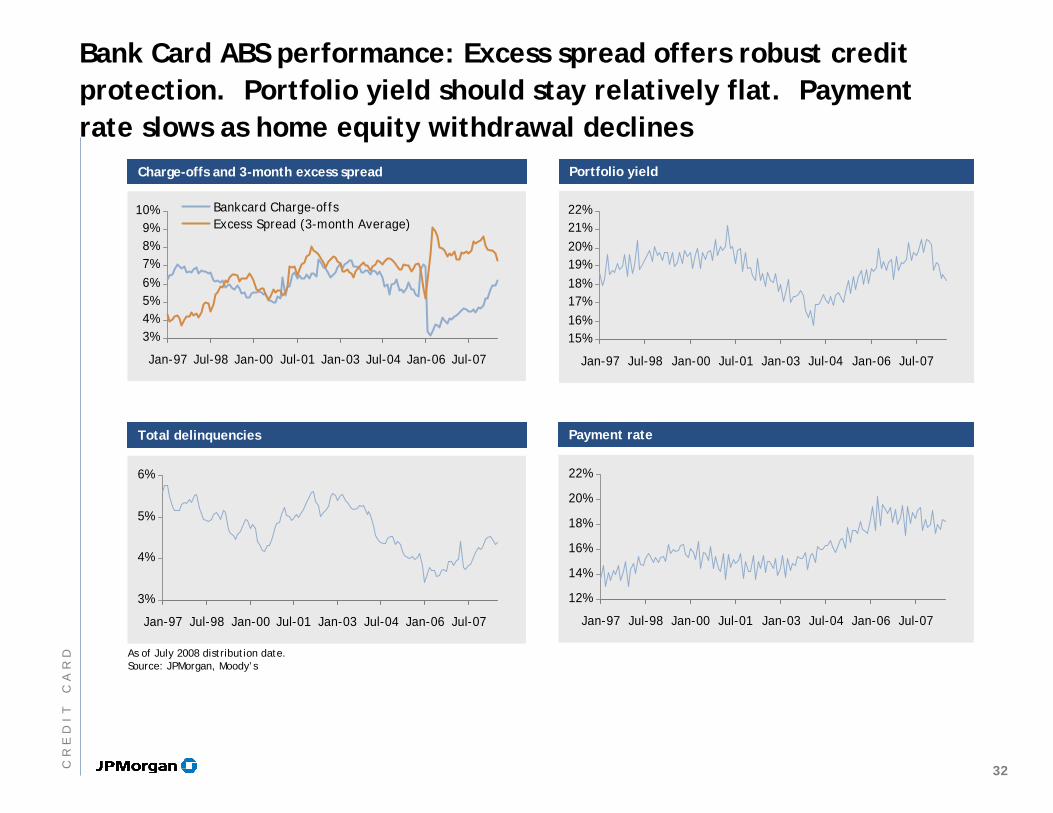

15%16%17%18%19%20%21%22%

Jan-97 Jul-98 Jan-00 Jul-01 Jan-03 Jul-04 Jan-06 Jul-07

As of July 2008 distribution date.Source: JPMorgan, Moody’s

Portfolio yieldPortfolio yieldCharge-offs and 3-month excess spreadCharge-offs and 3-month excess spread

3%4%5%6%7%8%9%

10%

Jan-97 Jul-98 Jan-00 Jul-01 Jan-03 Jul-04 Jan-06 Jul-07

Bankcard Charge-offs Excess Spread (3-month Average)

Bank Card ABS performance: Excess spread offers robust credit protection. Portfolio yield should stay relatively flat. Payment rate slows as home equity withdrawal declines

Payment ratePayment rate

12%

14%

16%

18%

20%

22%

Jan-97 Jul-98 Jan-00 Jul-01 Jan-03 Jul-04 Jan-06 Jul-07

Total delinquenciesTotal delinquencies

3%

4%

5%

6%

Jan-97 Jul-98 Jan-00 Jul-01 Jan-03 Jul-04 Jan-06 Jul-07

32CR

ED

IT

CA

RD

Seller / ServicerSeller / Servicer PortfolioPortfolio

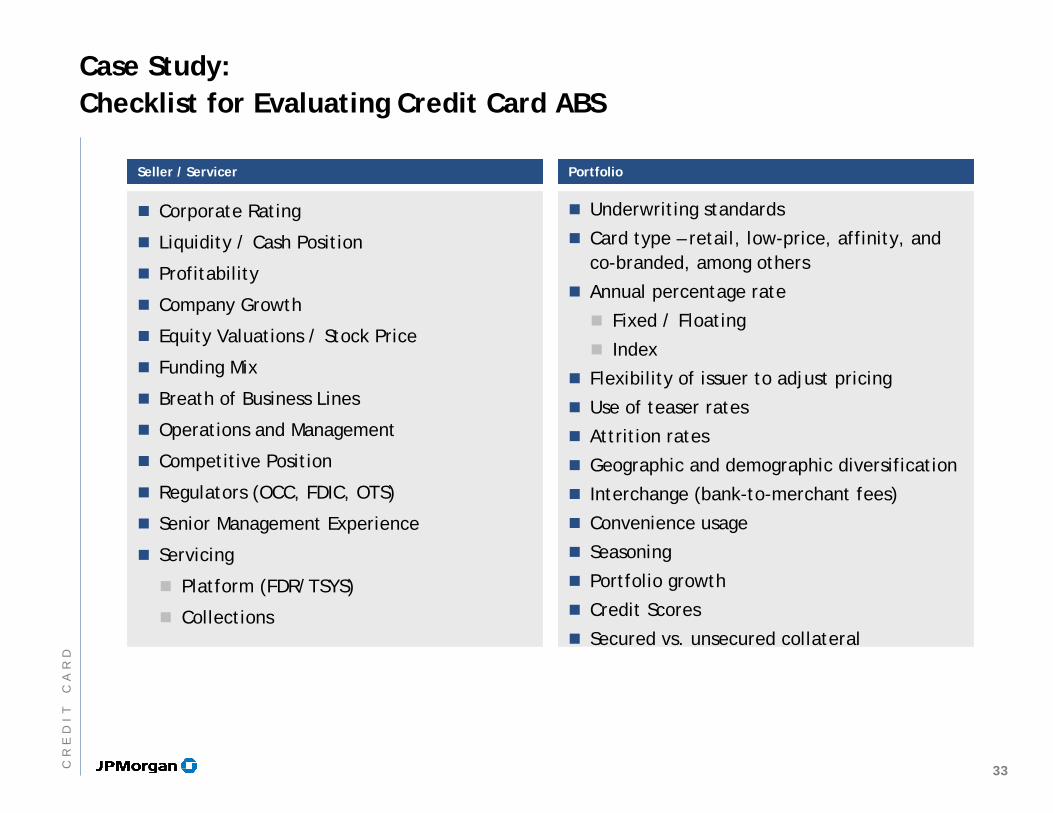

Case Study:Checklist for Evaluating Credit Card ABS

Corporate Rating

Liquidity / Cash Position

Profitability

Company Growth

Equity Valuations / Stock Price

Funding Mix

Breath of Business Lines

Operations and Management

Competitive Position

Regulators (OCC, FDIC, OTS)

Senior Management Experience

Servicing

Platform (FDR/TSYS)

Collections

Underwriting standards

Card type – retail, low-price, affinity, and co-branded, among others

Annual percentage rate

Fixed / Floating

Index

Flexibility of issuer to adjust pricing

Use of teaser rates

Attrition rates

Geographic and demographic diversification

Interchange (bank-to-merchant fees)

Convenience usage

Seasoning

Portfolio growth

Credit Scores

Secured vs. unsecured collateral

33CR

ED

IT

CA

RD

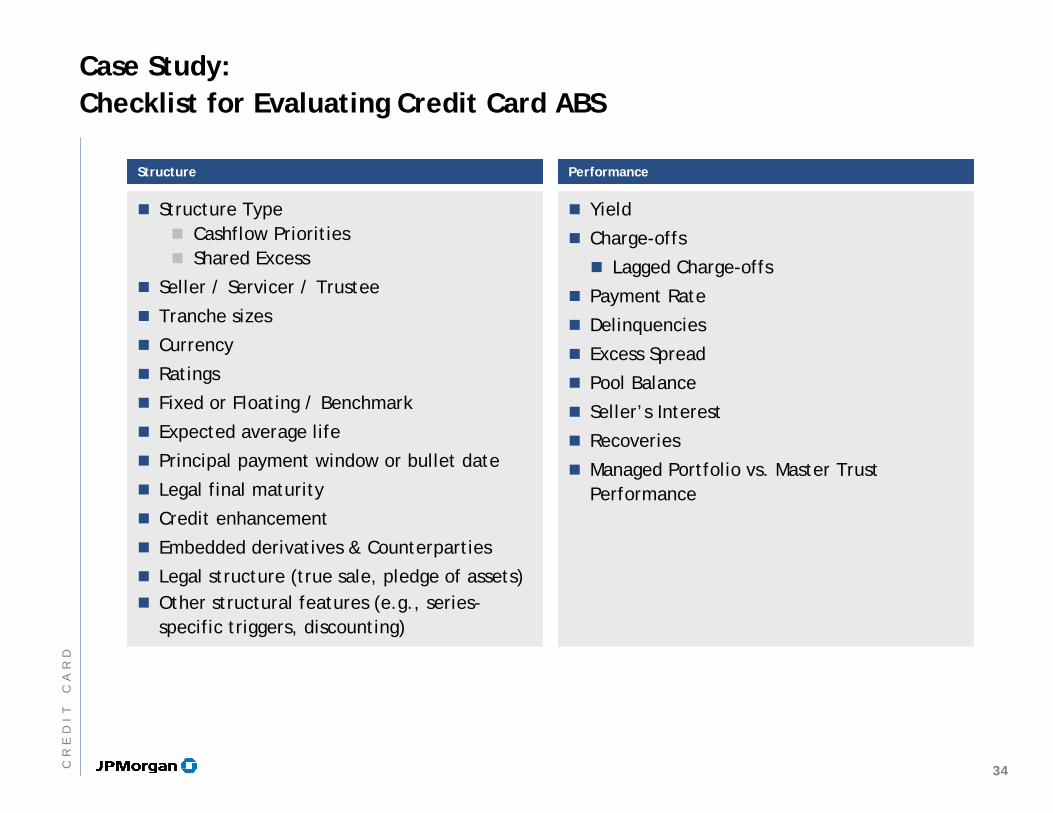

StructureStructure PerformancePerformance

Case Study:Checklist for Evaluating Credit Card ABS

Structure TypeCashflow PrioritiesShared Excess

Seller / Servicer / Trustee

Tranche sizes

Currency

Ratings

Fixed or Floating / Benchmark

Expected average life

Principal payment window or bullet date

Legal final maturity

Credit enhancement

Embedded derivatives & Counterparties

Legal structure (true sale, pledge of assets)Other structural features (e.g., series-specific triggers, discounting)

Yield

Charge-offs

Lagged Charge-offs

Payment Rate

Delinquencies

Excess Spread

Pool Balance

Seller’s Interest

Recoveries

Managed Portfolio vs. Master Trust Performance

34CR

ED

IT

CA

RD

AgendaAgenda

Page

Home Equity ABS

Student Loan ABS (FFELP)

Automobile ABS

Credit Card

Introduction to ABS

35

1

11

35

53

86

IN

VE

ST

IN

GI

NA

SS

ET

BA

CK

ED

SE

CU

RI

TI

ES

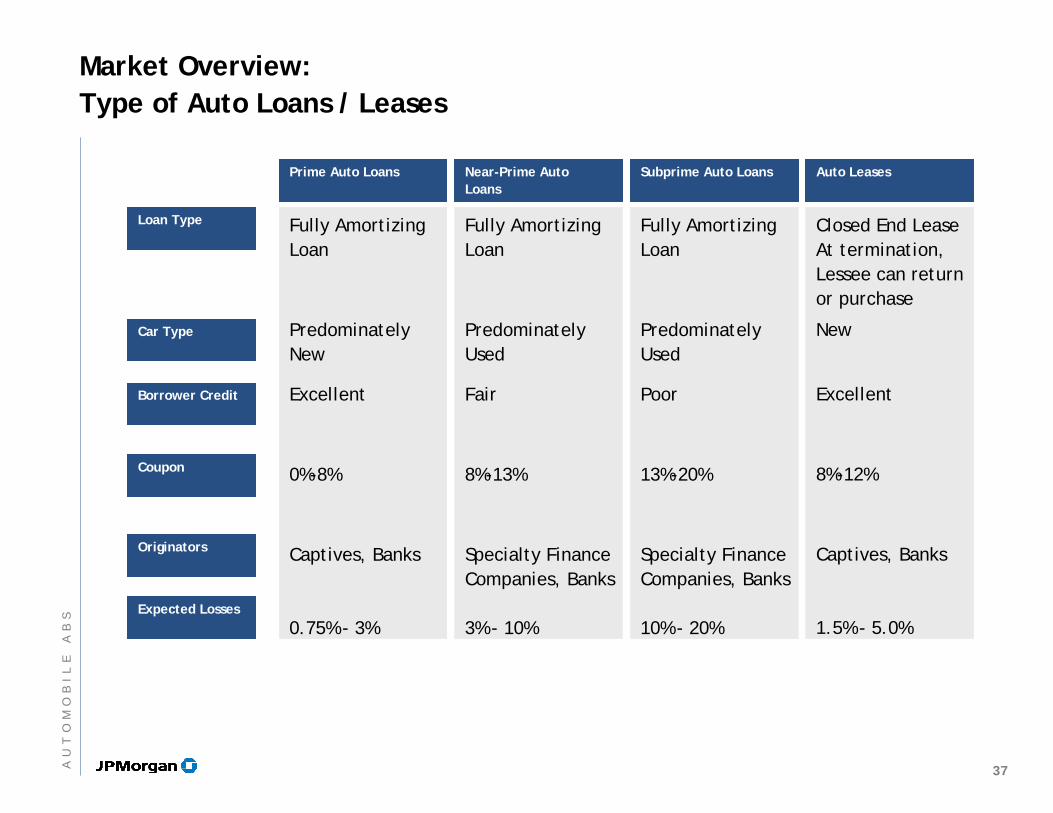

Market Overview:Auto Receivables

Secured consumer installment loans or leases used to finance new and used car purchases

Receivables carry a fixed interest rate and are usually originated for 36, 48, or 60 months (and typically extend no more than 5years)

Receivables originated by

Auto manufacturer finance subsidiaries (Captives)— GMAC, Ford, Daimler, Toyota, Honda, BMW

Banks— Chase, USAA

Specialty Finance Companies— AmeriCredit, Capital One, CarMax

36AU

TO

MO

BI

LE

AB

S

Prime Auto LoansPrime Auto Loans Near-Prime Auto Loans

Near-Prime Auto Loans

Subprime Auto LoansSubprime Auto Loans

Market Overview: Type of Auto Loans / Leases

Fully Amortizing Loan

Predominately New

Excellent

0%-8%

Captives, Banks

0.75% - 3%

Fully Amortizing Loan

Predominately Used

Fair

8%-13%

Specialty Finance Companies, Banks

3% - 10%

Fully Amortizing Loan

Predominately Used

Poor

13%-20%

Specialty Finance Companies, Banks

10% - 20%

Loan TypeLoan Type

Car TypeCar Type

Borrower CreditBorrower Credit

CouponCoupon

OriginatorsOriginators

Expected LossesExpected Losses

Auto LeasesAuto Leases

Closed End Lease At termination, Lessee can return or purchase

New

Excellent

8%-12%

Captives, Banks

1.5% - 5.0%

37AU

TO

MO

BI

LE

AB

S

Total = $__mm

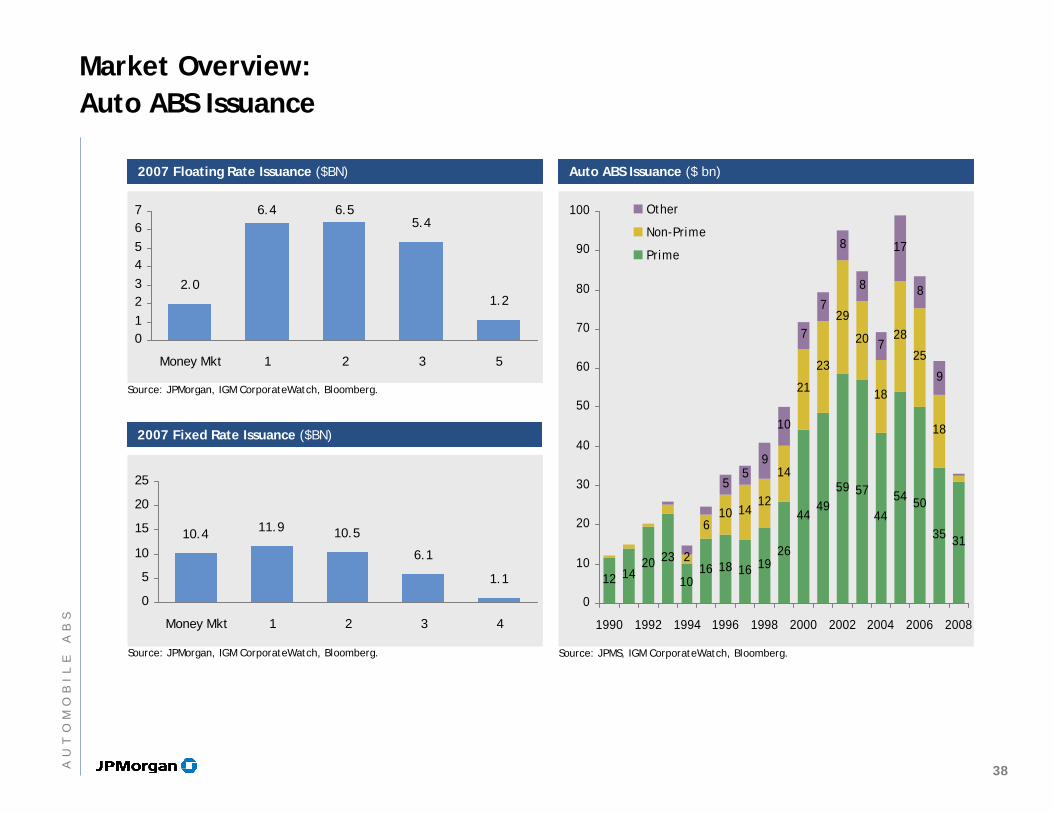

Market Overview:Auto ABS Issuance

Auto ABS Issuance ($ bn)Auto ABS Issuance ($ bn)

12 1420 23

1016 18 16 19

26

4449

59 57

44

54 50

35 312

610 14

12

14

21

23

29

20

18

28

25

18

55

9

10

7

7

8

8

7

17

8

9

0

10

20

30

40

50

60

70

80

90

100

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Other

Non-Prime

Prime

Source: JPMS, IGM CorporateWatch, Bloomberg.

Source: JPMorgan, IGM CorporateWatch, Bloomberg.

Source: JPMorgan, IGM CorporateWatch, Bloomberg.

2007 Floating Rate Issuance ($BN)2007 Floating Rate Issuance ($BN)

2007 Fixed Rate Issuance ($BN)2007 Fixed Rate Issuance ($BN)

2.0

6.4 6.55.4

1.2

01234567

Money Mkt 1 2 3 5

10.4 11.9 10.5

6.1

1.1

0

5

10

15

20

25

Money Mkt 1 2 3 4

38AU

TO

MO

BI

LE

AB

S

Source: JPMS, IGM CorporateWatch, Bloomberg.

Market Overview:Auto ABS Issuance

Top Prime Auto ABS Issuers by 2007 Volume ($ bn)Top Prime Auto ABS Issuers by 2007 Volume ($ bn)

Issuer 2005 2006 2007

GMAC 3.04 6.05 7.56

Ford 9.68 8.94 5.04

Honda 7.70 4.08 2.91

USAA 4.53 5.24 2.56

CarMax 1.59 1.27 2.15

DaimlerChrysler 4.00 6.58 2.10

Nissan 4.23 3.41 2.06

World Omni 1.73 1.84 2.00

AmeriCredit 2.00

Capital One 1.50 2.25 1.75

Hyundai 0.77 1.88 0.86

Merrill Lynch 1.77 0.77

Goldman Sachs 1.29 0.85 0.66

Wachovia 2.90 1.30 0.65

JPMorgan (JPMART) 0.56 0.45

Franklin Auto 0.35 0.36 0.33

Chase 3.62 2.33

Other 5.17 3.15

Total 53.88 50.09 33.86

Top Non-Prime Auto ABS Issuers by 2007 Volume ($ bn)Top Non-Prime Auto ABS Issuers by 2007 Volume ($ bn)

Issuer 2005 2006 2007

AmeriCredit 5.50 4.70 5.00

Capital One 7.20 7.00 4.25

Drive 0.18 0.19 2.30

Wachovia 2.70 1.95

Triad 2.85 2.84 1.37

CPS 2.01 2.83 0.90

HSBC automotive 0.86

UPFC 0.59 0.62 0.50

Long Beach 0.66 0.91 0.49

Prestige 1.40 1.60 0.33

Drive Time 0.70 0.95 0.32

Credit Acceptance 0.42 0.49 0.20

First Investors 0.20

WFS 0.15 0.24

Wells Fargo 5.73

Total 27.39 25.27 18.46

39AU

TO

MO

BI

LE

AB

S

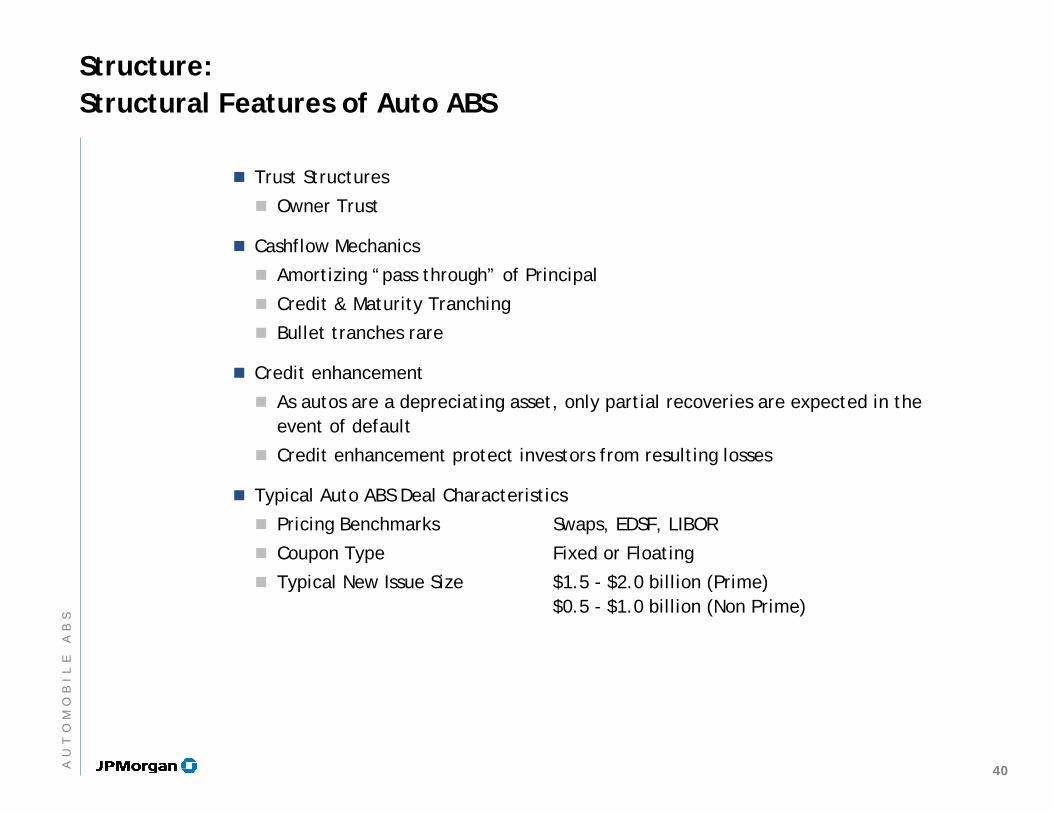

Structure: Structural Features of Auto ABS

Trust Structures

Owner Trust

Cashflow Mechanics

Amortizing “pass through” of Principal

Credit & Maturity Tranching

Bullet tranches rare

Credit enhancement

As autos are a depreciating asset, only partial recoveries are expected in the event of default

Credit enhancement protect investors from resulting losses

Typical Auto ABS Deal Characteristics

Pricing Benchmarks Swaps, EDSF, LIBOR

Coupon Type Fixed or Floating

Typical New Issue Size $1.5 - $2.0 billion (Prime)$0.5 - $1.0 billion (Non Prime)

40AU

TO

MO

BI

LE

AB

S

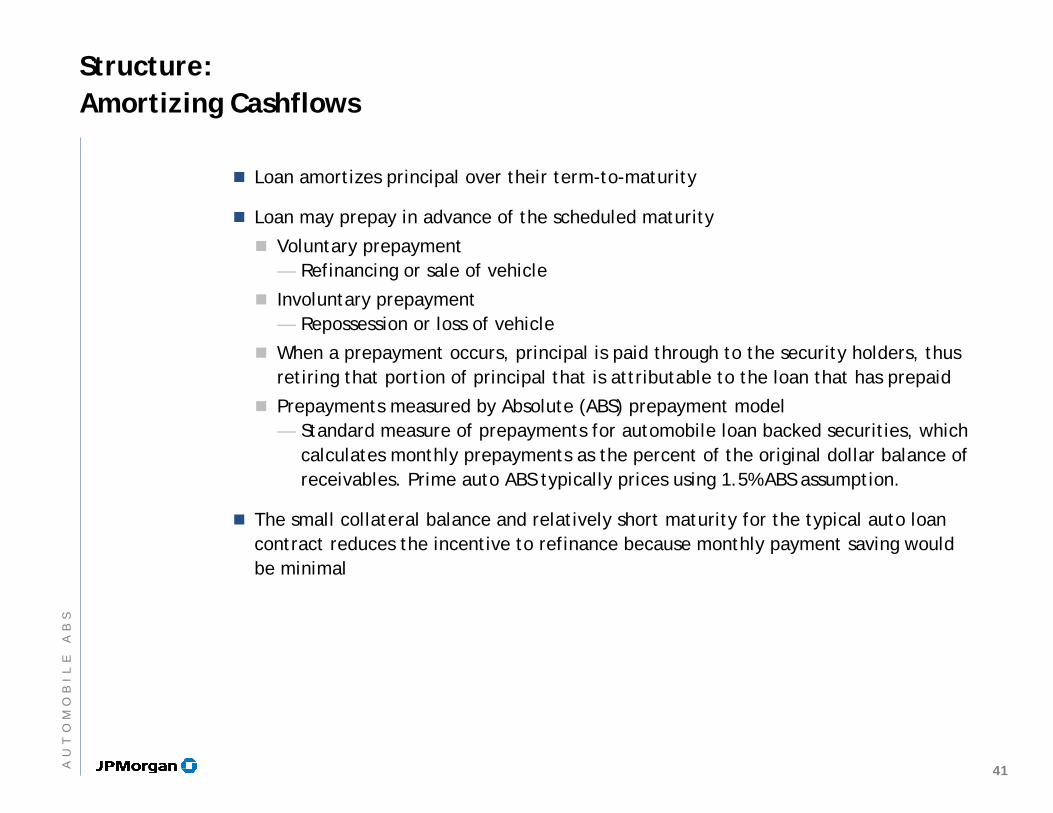

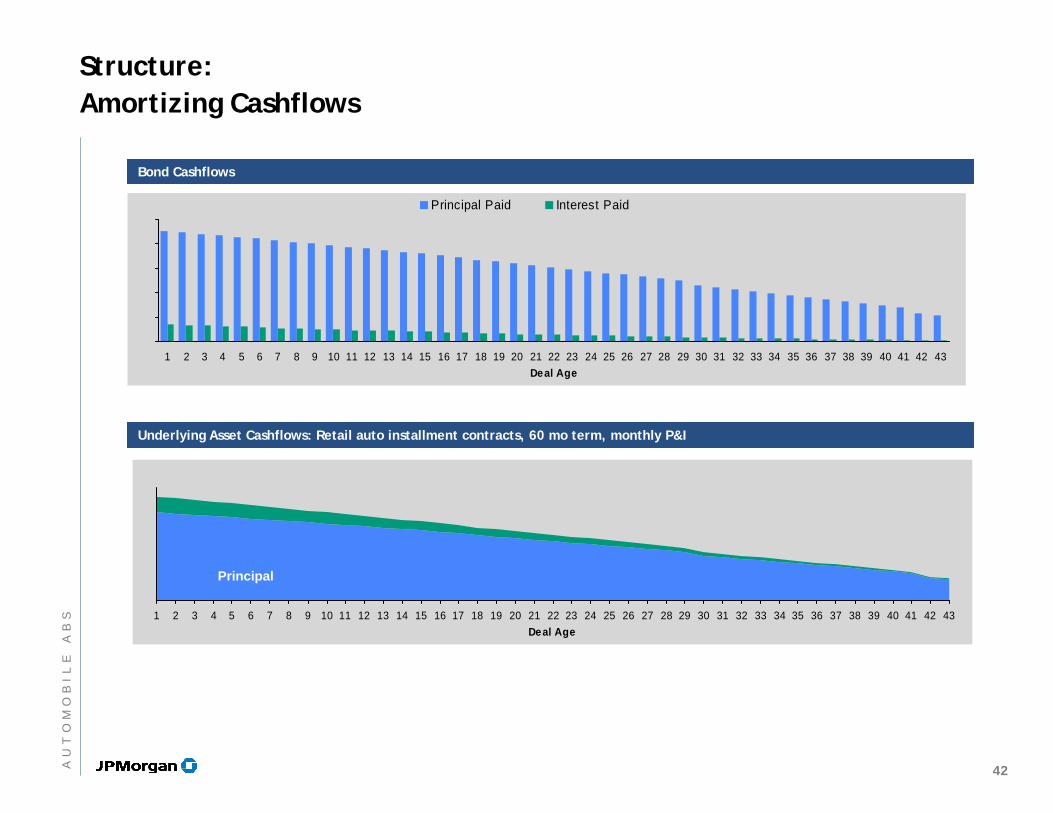

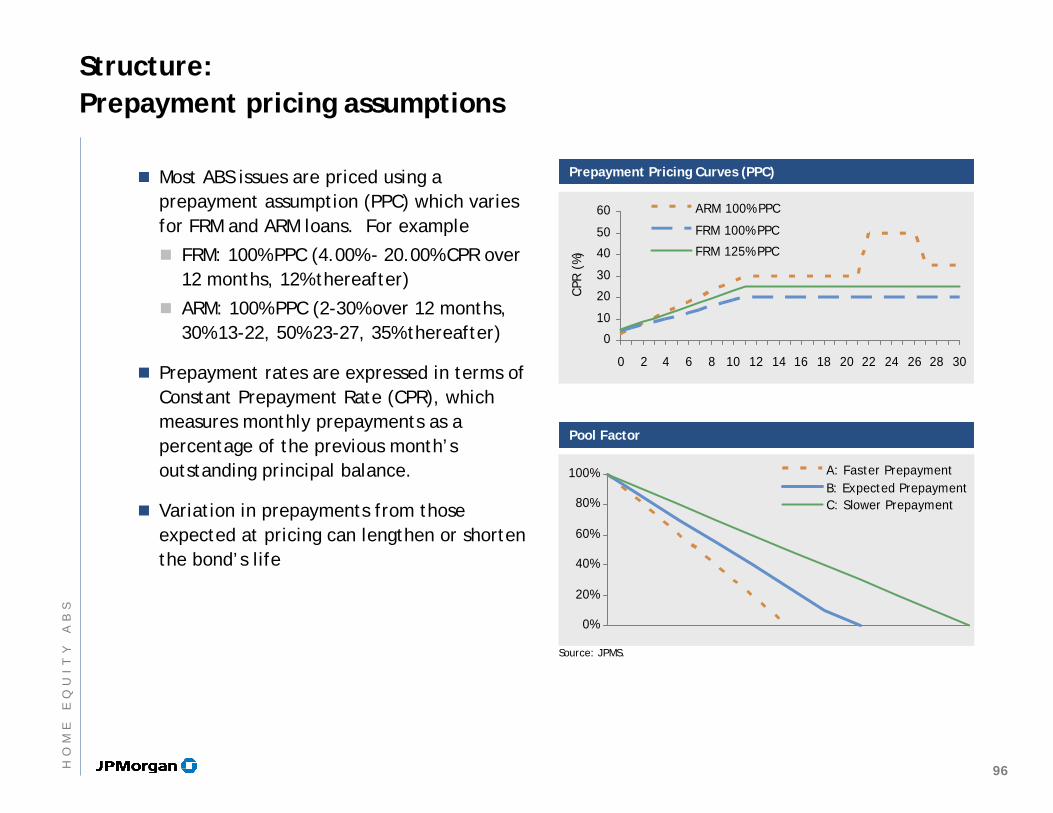

Structure:Amortizing Cashflows

Loan amortizes principal over their term-to-maturity

Loan may prepay in advance of the scheduled maturity

Voluntary prepayment— Refinancing or sale of vehicle

Involuntary prepayment— Repossession or loss of vehicle

When a prepayment occurs, principal is paid through to the security holders, thus retiring that portion of principal that is attributable to the loan that has prepaid

Prepayments measured by Absolute (ABS) prepayment model— Standard measure of prepayments for automobile loan backed securities, which

calculates monthly prepayments as the percent of the original dollar balance of receivables. Prime auto ABS typically prices using 1.5% ABS assumption.

The small collateral balance and relatively short maturity for the typical auto loan contract reduces the incentive to refinance because monthly payment saving would be minimal

41AU

TO

MO

BI

LE

AB

S

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43Deal Age

Principal Paid Interest Paid

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43Deal Age

Principal

Structure:Amortizing Cashflows

Bond CashflowsBond Cashflows

Underlying Asset Cashflows: Retail auto installment contracts, 60 mo term, monthly P&IUnderlying Asset Cashflows: Retail auto installment contracts, 60 mo term, monthly P&I

42AU

TO

MO

BI

LE

AB

S

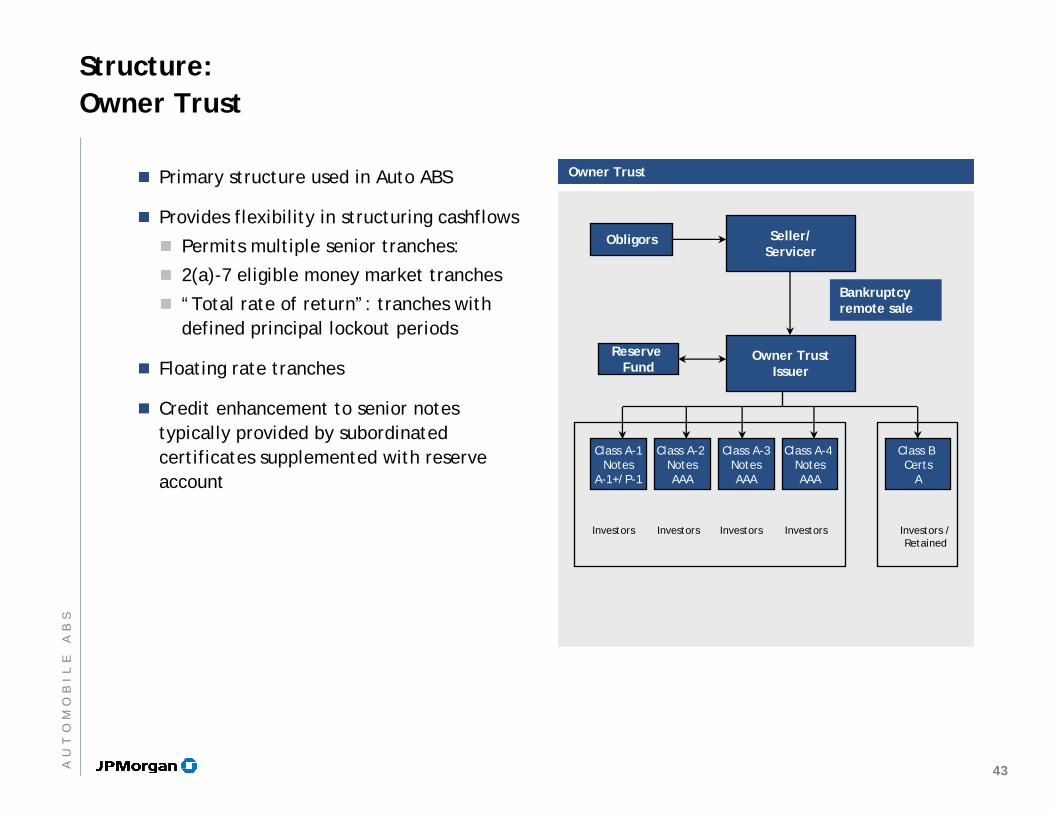

Obligors Seller/Servicer

Investors Investors

Reserve Fund

Class A-1Notes

A-1+/P-1

Class A-2 NotesAAA

Bankruptcy remote sale

Owner TrustIssuer

Investors /Retained

Class B Certs

A

Investors Investors

Class A-3NotesAAA

Class A-4 NotesAAA

Structure:Owner Trust

Primary structure used in Auto ABS

Provides flexibility in structuring cashflows

Permits multiple senior tranches:

2(a)-7 eligible money market tranches

“Total rate of return”: tranches with defined principal lockout periods

Floating rate tranches

Credit enhancement to senior notes typically provided by subordinated certificates supplemented with reserve account

Owner TrustOwner Trust

43AU

TO

MO

BI

LE

AB

S

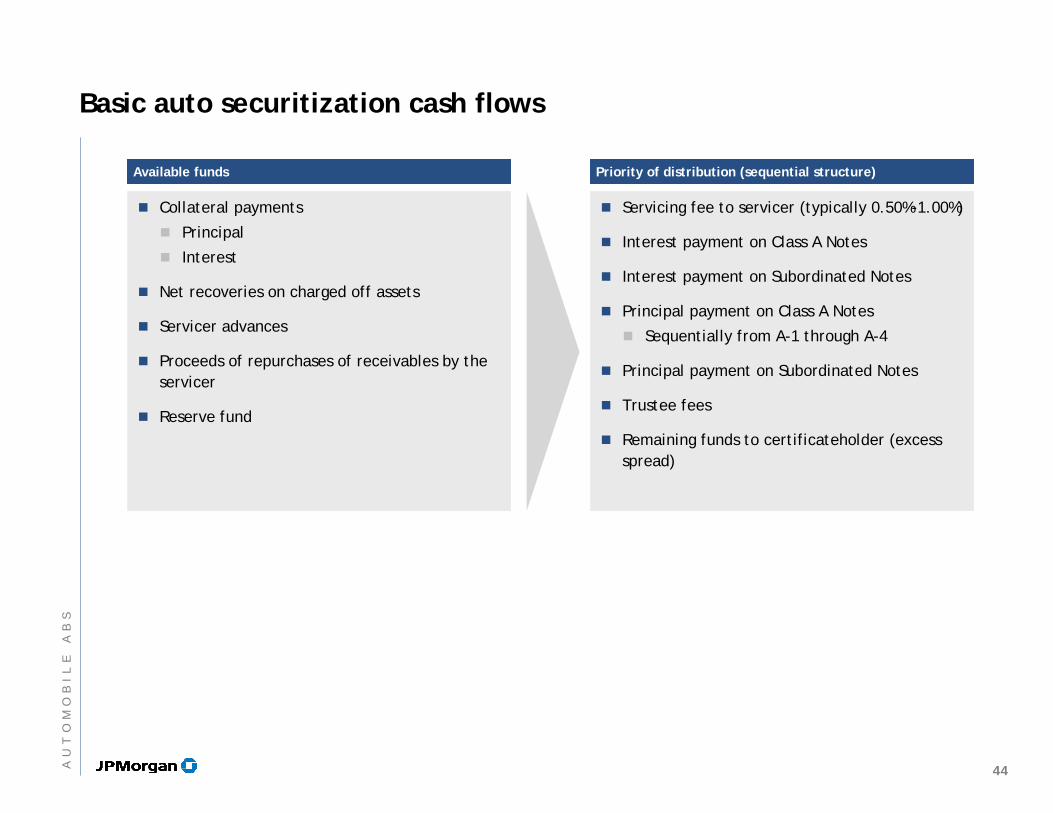

Basic auto securitization cash flows

Collateral payments

Principal

Interest

Net recoveries on charged off assets

Servicer advances

Proceeds of repurchases of receivables by the servicer

Reserve fund

Servicing fee to servicer (typically 0.50%-1.00%)

Interest payment on Class A Notes

Interest payment on Subordinated Notes

Principal payment on Class A Notes

Sequentially from A-1 through A-4

Principal payment on Subordinated Notes

Trustee fees

Remaining funds to certificateholder (excess spread)

Available fundsAvailable funds Priority of distribution (sequential structure)Priority of distribution (sequential structure)

44AU

TO

MO

BI

LE

AB

S

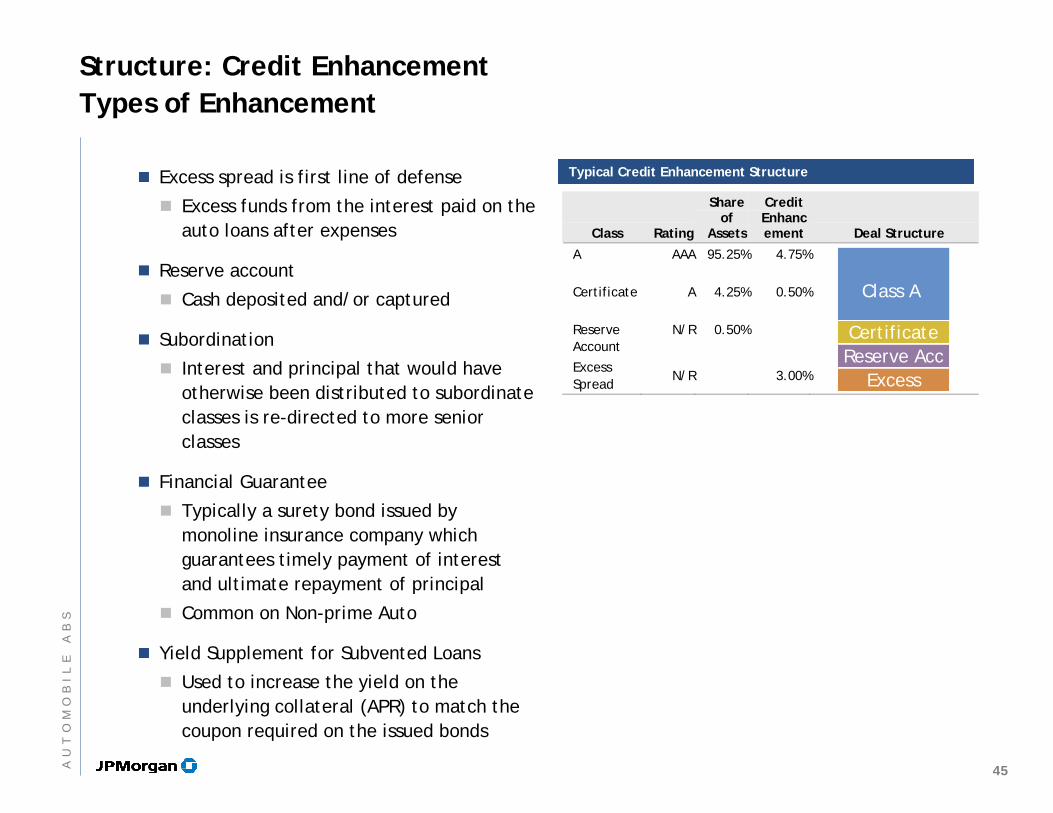

Structure: Credit EnhancementTypes of Enhancement

Excess spread is first line of defense

Excess funds from the interest paid on the auto loans after expenses

Reserve account

Cash deposited and/or captured

Subordination

Interest and principal that would have otherwise been distributed to subordinate classes is re-directed to more senior classes

Financial Guarantee

Typically a surety bond issued by monoline insurance company which guarantees timely payment of interest and ultimate repayment of principal

Common on Non-prime Auto

Yield Supplement for Subvented Loans

Used to increase the yield on the underlying collateral (APR) to match the coupon required on the issued bonds

Class Rating

Share of

Assets

Credit Enhancement Deal Structure

A

AAA 95.25% 4.75%

Certificate

A 4.25% 0.50%

Reserve Account

N/R 0.50%

Excess Spread

N/R 3.00%

Typical Credit Enhancement StructureTypical Credit Enhancement Structure

Class A

Certificate

ExcessReserve Acc

45AU

TO

MO

BI

LE

AB

S

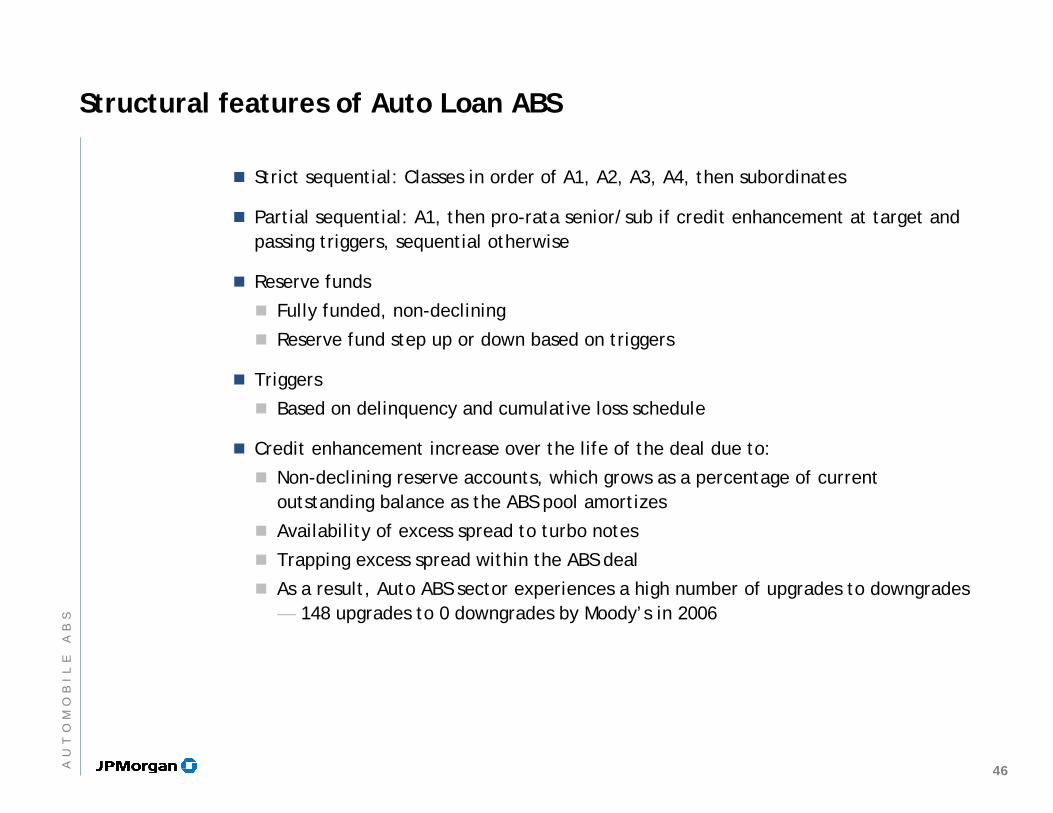

Structural features of Auto Loan ABS

Strict sequential: Classes in order of A1, A2, A3, A4, then subordinates

Partial sequential: A1, then pro-rata senior/sub if credit enhancement at target and passing triggers, sequential otherwise

Reserve funds

Fully funded, non-declining

Reserve fund step up or down based on triggers

Triggers

Based on delinquency and cumulative loss schedule

Credit enhancement increase over the life of the deal due to:

Non-declining reserve accounts, which grows as a percentage of current outstanding balance as the ABS pool amortizes

Availability of excess spread to turbo notes

Trapping excess spread within the ABS deal

As a result, Auto ABS sector experiences a high number of upgrades to downgrades — 148 upgrades to 0 downgrades by Moody’s in 2006

46AU

TO

MO

BI

LE

AB

S

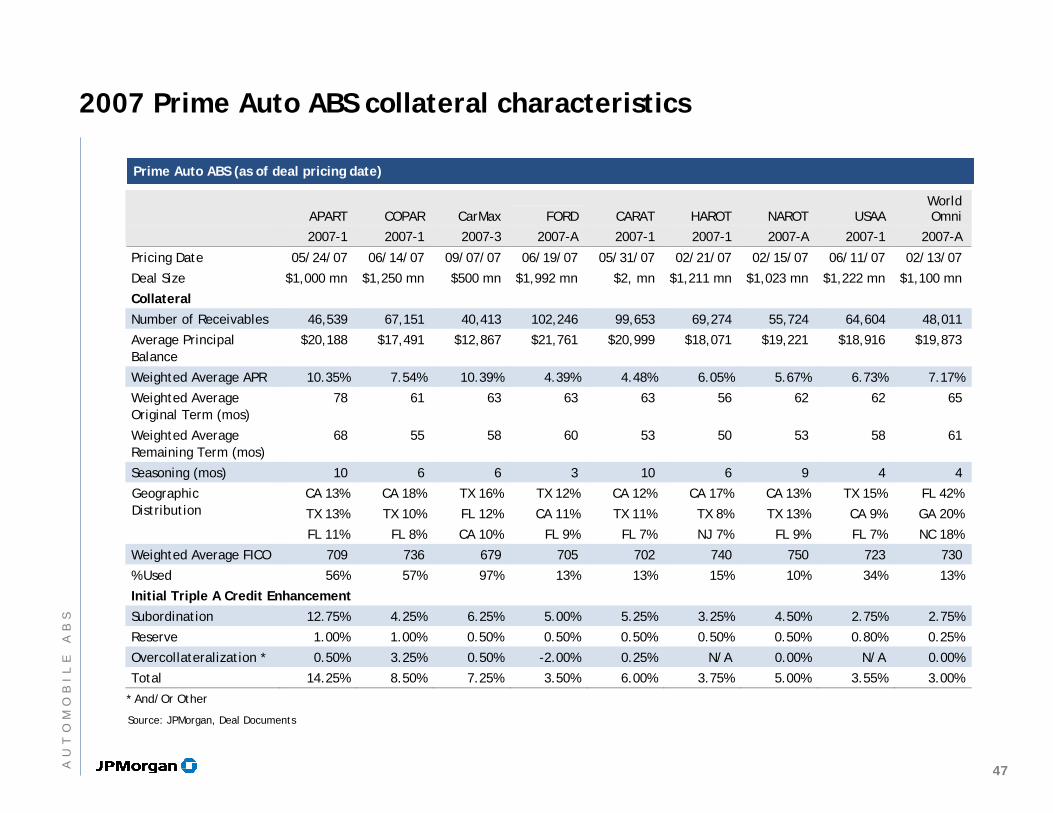

APART COPAR CarMax FORD CARAT HAROT NAROT USAA World Omni

2007-1 2007-1 2007-3 2007-A 2007-1 2007-1 2007-A 2007-1 2007-A

Pricing Date 05/24/07 06/14/07 09/07/07 06/19/07 05/31/07 02/21/07 02/15/07 06/11/07 02/13/07

Deal Size $1,000 mn $1,250 mn $500 mn $1,992 mn $2, mn $1,211 mn $1,023 mn $1,222 mn $1,100 mn

Collateral

Number of Receivables 46,539 67,151 40,413 102,246 99,653 69,274 55,724 64,604 48,011

Average Principal Balance

$20,188 $17,491 $12,867 $21,761 $20,999 $18,071 $19,221 $18,916 $19,873

Weighted Average APR 10.35% 7.54% 10.39% 4.39% 4.48% 6.05% 5.67% 6.73% 7.17%

Weighted Average Original Term (mos)

78 61 63 63 63 56 62 62 65

Weighted Average Remaining Term (mos)

68 55 58 60 53 50 53 58 61

Seasoning (mos) 10 6 6 3 10 6 9 4 4

CA 13% CA 18% TX 16% TX 12% CA 12% CA 17% CA 13% TX 15% FL 42%

TX 13% TX 10% FL 12% CA 11% TX 11% TX 8% TX 13% CA 9% GA 20%

Geographic Distribution

FL 11% FL 8% CA 10% FL 9% FL 7% NJ 7% FL 9% FL 7% NC 18%

Weighted Average FICO 709 736 679 705 702 740 750 723 730

% Used 56% 57% 97% 13% 13% 15% 10% 34% 13%

Initial Triple A Credit Enhancement Subordination 12.75% 4.25% 6.25% 5.00% 5.25% 3.25% 4.50% 2.75% 2.75%

Reserve 1.00% 1.00% 0.50% 0.50% 0.50% 0.50% 0.50% 0.80% 0.25%

Overcollateralization * 0.50% 3.25% 0.50% -2.00% 0.25% N/A 0.00% N/A 0.00%

Total 14.25% 8.50% 7.25% 3.50% 6.00% 3.75% 5.00% 3.55% 3.00%

* And/Or Other

Prime Auto ABS (as of deal pricing date)Prime Auto ABS (as of deal pricing date)

Source: JPMorgan, Deal Documents

2007 Prime Auto ABS collateral characteristics

47AU

TO

MO

BI

LE

AB

S

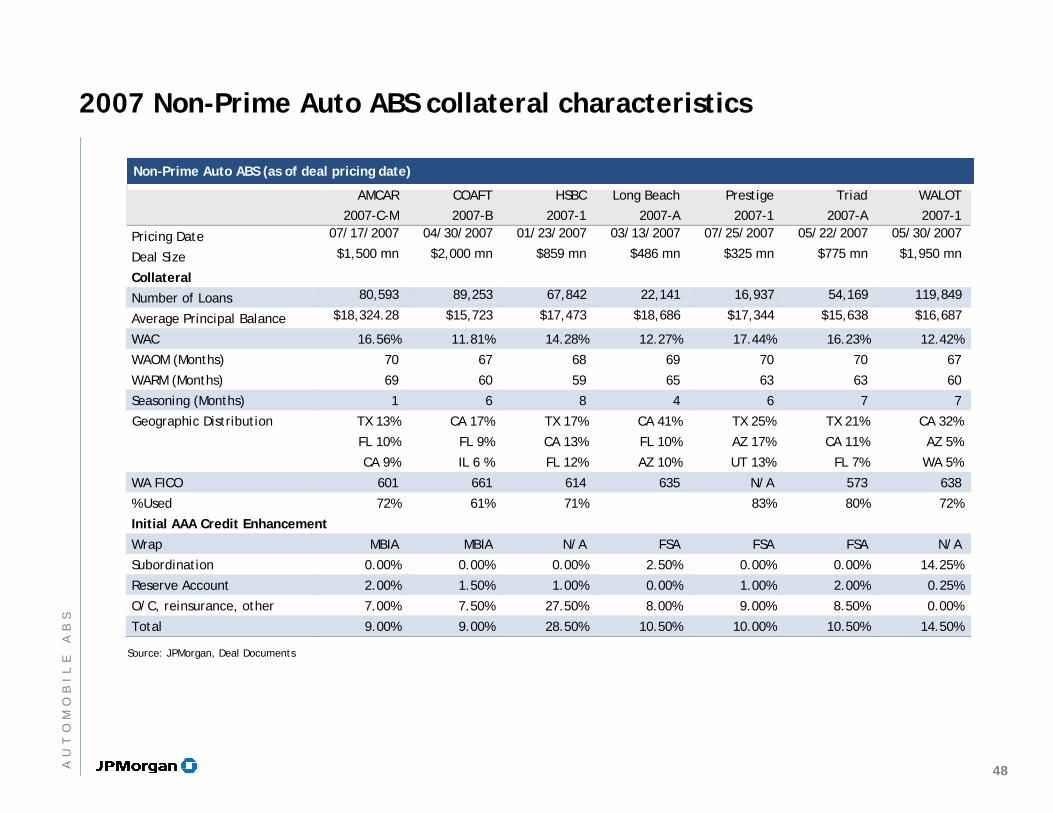

AMCAR COAFT HSBC Long Beach Prestige Triad WALOT

2007-C-M 2007-B 2007-1 2007-A 2007-1 2007-A 2007-1

Pricing Date 07/17/2007 04/30/2007 01/23/2007 03/13/2007 07/25/2007 05/22/2007 05/30/2007

Deal Size $1,500 mn $2,000 mn $859 mn $486 mn $325 mn $775 mn $1,950 mn

Collateral

Number of Loans 80,593 89,253 67,842 22,141 16,937 54,169 119,849

Average Principal Balance $18,324.28 $15,723 $17,473 $18,686 $17,344 $15,638 $16,687

WAC 16.56% 11.81% 14.28% 12.27% 17.44% 16.23% 12.42%

WAOM (Months) 70 67 68 69 70 70 67

WARM (Months) 69 60 59 65 63 63 60

Seasoning (Months) 1 6 8 4 6 7 7

TX 13% CA 17% TX 17% CA 41% TX 25% TX 21% CA 32%

FL 10% FL 9% CA 13% FL 10% AZ 17% CA 11% AZ 5%

Geographic Distribution

CA 9% IL 6 % FL 12% AZ 10% UT 13% FL 7% WA 5%

WA FICO 601 661 614 635 N/A 573 638

% Used 72% 61% 71% 83% 80% 72%

Initial AAA Credit Enhancement

Wrap MBIA MBIA N/A FSA FSA FSA N/A

Subordination 0.00% 0.00% 0.00% 2.50% 0.00% 0.00% 14.25%

Reserve Account 2.00% 1.50% 1.00% 0.00% 1.00% 2.00% 0.25%

O/C, reinsurance, other 7.00% 7.50% 27.50% 8.00% 9.00% 8.50% 0.00%

Total 9.00% 9.00% 28.50% 10.50% 10.00% 10.50% 14.50%

Non-Prime Auto ABS (as of deal pricing date)Non-Prime Auto ABS (as of deal pricing date)

Source: JPMorgan, Deal Documents

2007 Non-Prime Auto ABS collateral characteristics

48AU

TO

MO

BI

LE

AB

S

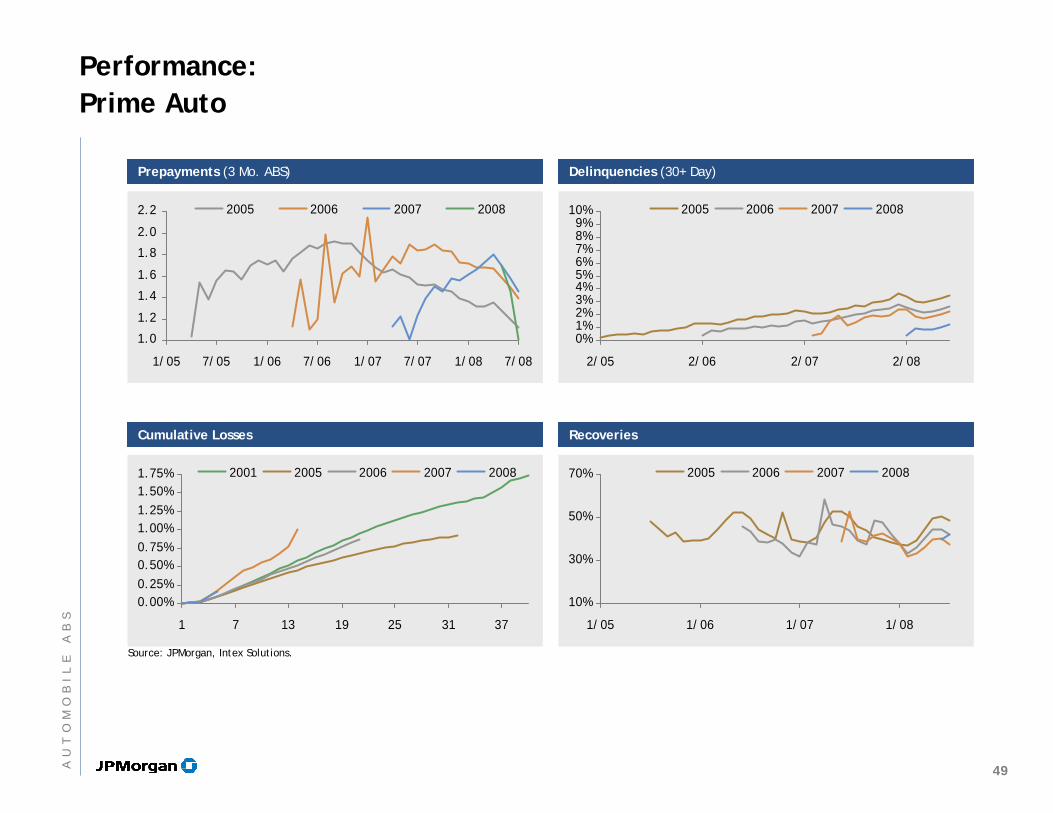

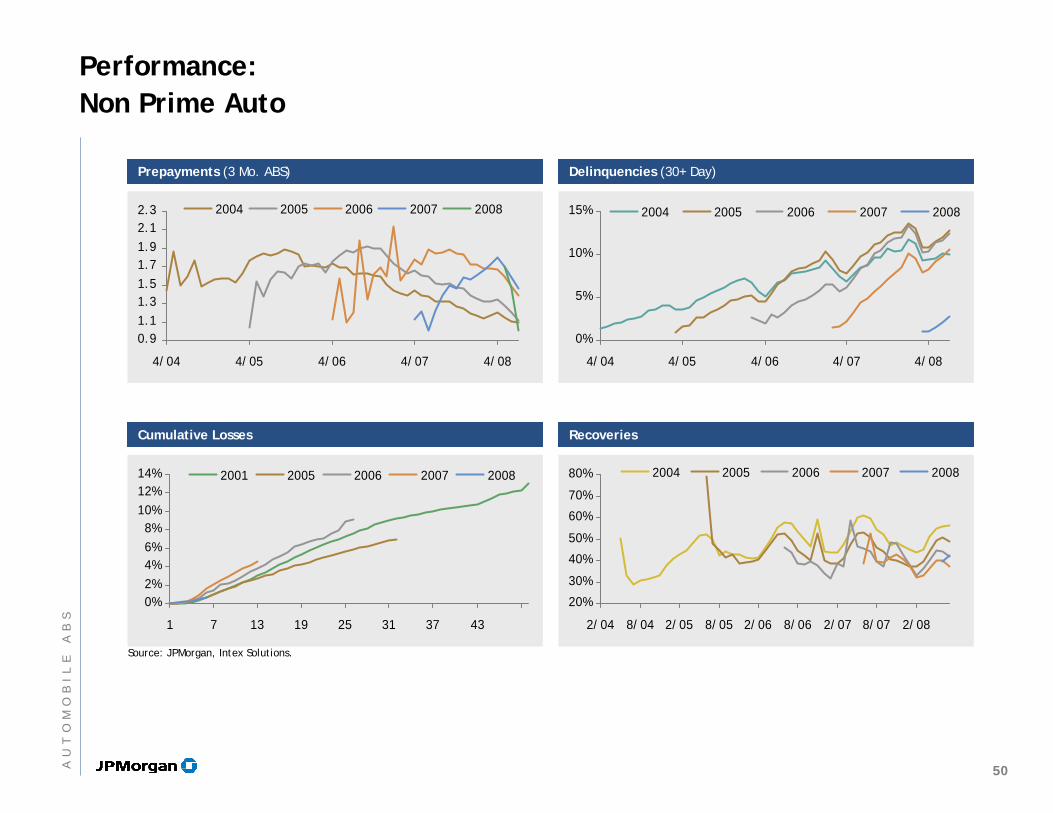

Source: JPMorgan, Intex Solutions.

Prepayments (3 Mo. ABS)Prepayments (3 Mo. ABS) Delinquencies (30+ Day)Delinquencies (30+ Day)

Cumulative LossesCumulative Losses RecoveriesRecoveries

1.0

1.2

1.4

1.6

1.8

2.0

2.2

1/05 7/05 1/06 7/06 1/07 7/07 1/08 7/08

2005 2006 2007 2008

Performance:Prime Auto

0.00%0.25%0.50%0.75%1.00%1.25%1.50%1.75%

1 7 13 19 25 31 37

2001 2005 2006 2007 2008

0%1%2%3%4%5%6%7%8%9%

10%

2/05 2/06 2/07 2/08

2005 2006 2007 2008

10%

30%

50%

70%

1/05 1/06 1/07 1/08

2005 2006 2007 2008

49AU

TO

MO

BI

LE

AB

S

Source: JPMorgan, Intex Solutions.

Prepayments (3 Mo. ABS)Prepayments (3 Mo. ABS) Delinquencies (30+ Day)Delinquencies (30+ Day)

Cumulative LossesCumulative Losses RecoveriesRecoveries

Performance:Non Prime Auto

0%2%4%6%8%

10%12%14%

1 7 13 19 25 31 37 43

2001 2005 2006 2007 2008

0%

5%

10%

15%

4/04 4/05 4/06 4/07 4/08

2004 2005 2006 2007 2008

20%

30%

40%

50%

60%

70%

80%

2/04 8/04 2/05 8/05 2/06 8/06 2/07 8/07 2/08

2004 2005 2006 2007 2008

0.91.11.31.51.71.92.12.3

4/04 4/05 4/06 4/07 4/08

2004 2005 2006 2007 2008

50AU

TO

MO

BI

LE

AB

S

Seller / ServicerSeller / Servicer PortfolioPortfolio

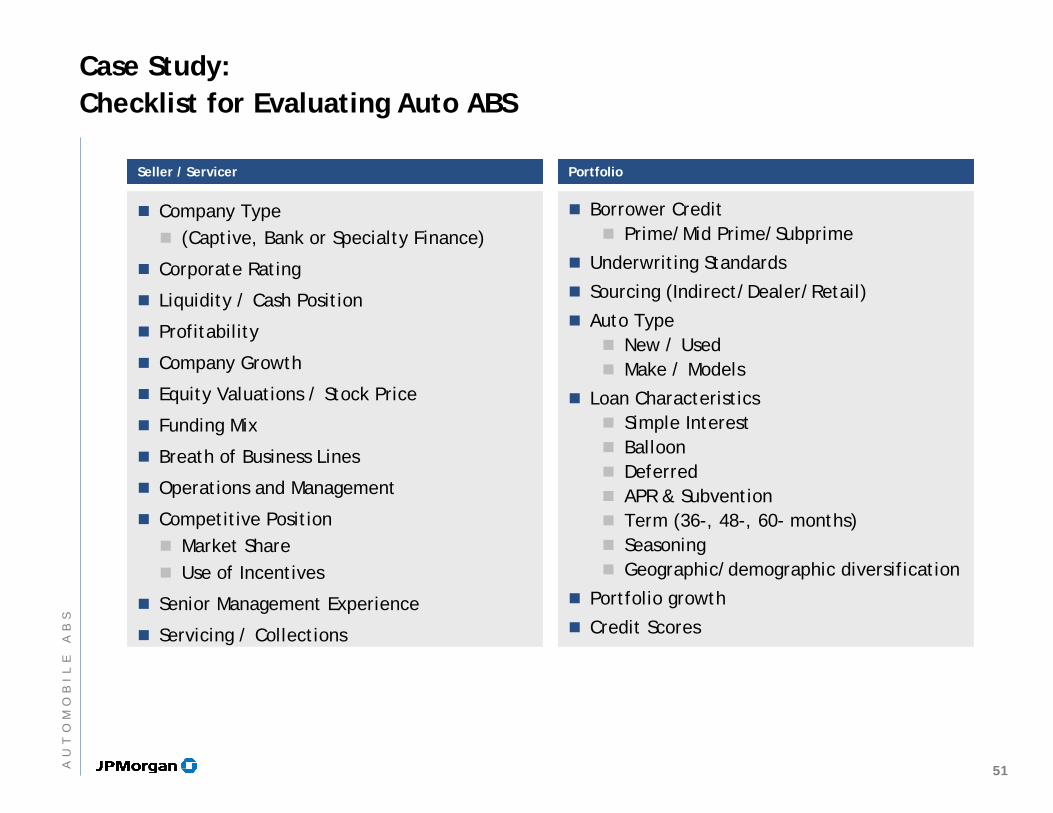

Case Study:Checklist for Evaluating Auto ABS

Company Type(Captive, Bank or Specialty Finance)

Corporate Rating

Liquidity / Cash Position

Profitability

Company Growth

Equity Valuations / Stock Price

Funding Mix

Breath of Business Lines

Operations and Management

Competitive PositionMarket ShareUse of Incentives

Senior Management Experience

Servicing / Collections

Borrower CreditPrime/Mid Prime/Subprime

Underwriting Standards

Sourcing (Indirect/Dealer/Retail)

Auto TypeNew / UsedMake / Models

Loan CharacteristicsSimple InterestBalloonDeferredAPR & SubventionTerm (36-, 48-, 60- months)SeasoningGeographic/demographic diversification

Portfolio growth

Credit Scores

51AU

TO

MO

BI

LE

AB

S

StructureStructure PerformancePerformance

Case Study:Checklist for Evaluating Auto ABS

StructureCashflow PrioritiesOwner vs. Grantor TrustCredit Enhancement— Wrap vs. Senior Sub— Subordinate lockouts— Reserve Fund

— Targets / Step-ups / FloorsYield Supplement Accounts

Seller / Servicer / Trustee

Tranche sizes

Ratings

Fixed or Floating / Benchmark

Expected average life

Principal payment window or bullet date

Embedded derivatives & Counterparties

Legal structure (true sale, pledge of assets)

Charge-offs

Prepayment Rate

Delinquencies

Recoveries

Excess Spread

Managed Portfolio vs. ABS Performance

52AU

TO

MO

BI

LE

AB

S

AgendaAgenda

Page

Home Equity ABS

Student Loan ABS (FFELP)

Automobile ABS

Credit Card

Introduction to ABS

53

1

11

35

53

86

IN

VE

ST

IN

GI

NA

SS

ET

BA

CK

ED

SE

CU

RI

TI

ES

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

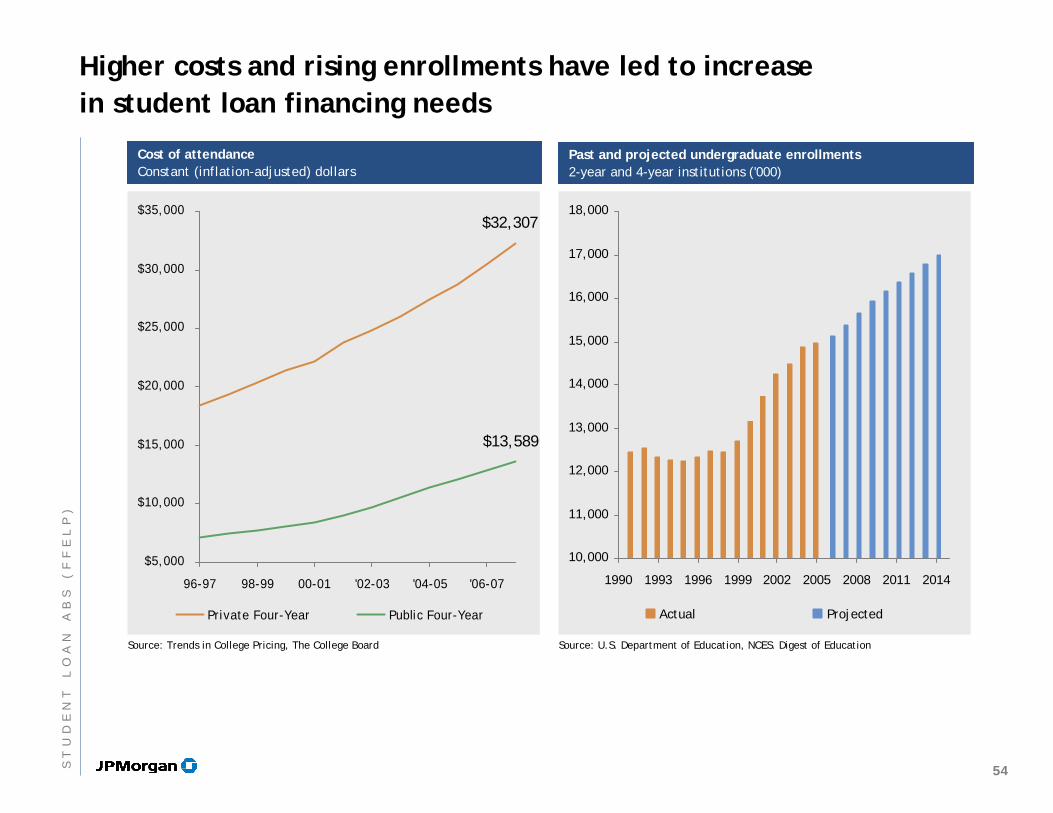

96-97 98-99 00-01 '02-03 '04-05 '06-07

Private Four-Year Public Four-Year

Source: Trends in College Pricing, The College Board Source: U.S. Department of Education, NCES. Digest of Education

Cost of attendanceConstant (inflation-adjusted) dollars

Cost of attendanceConstant (inflation-adjusted) dollars

Higher costs and rising enrollments have led to increase in student loan financing needs

$13,589

$32,307

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

1990 1993 1996 1999 2002 2005 2008 2011 2014

Actual Projected

Past and projected undergraduate enrollments2-year and 4-year institutions ('000)

Past and projected undergraduate enrollments2-year and 4-year institutions ('000)

54ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

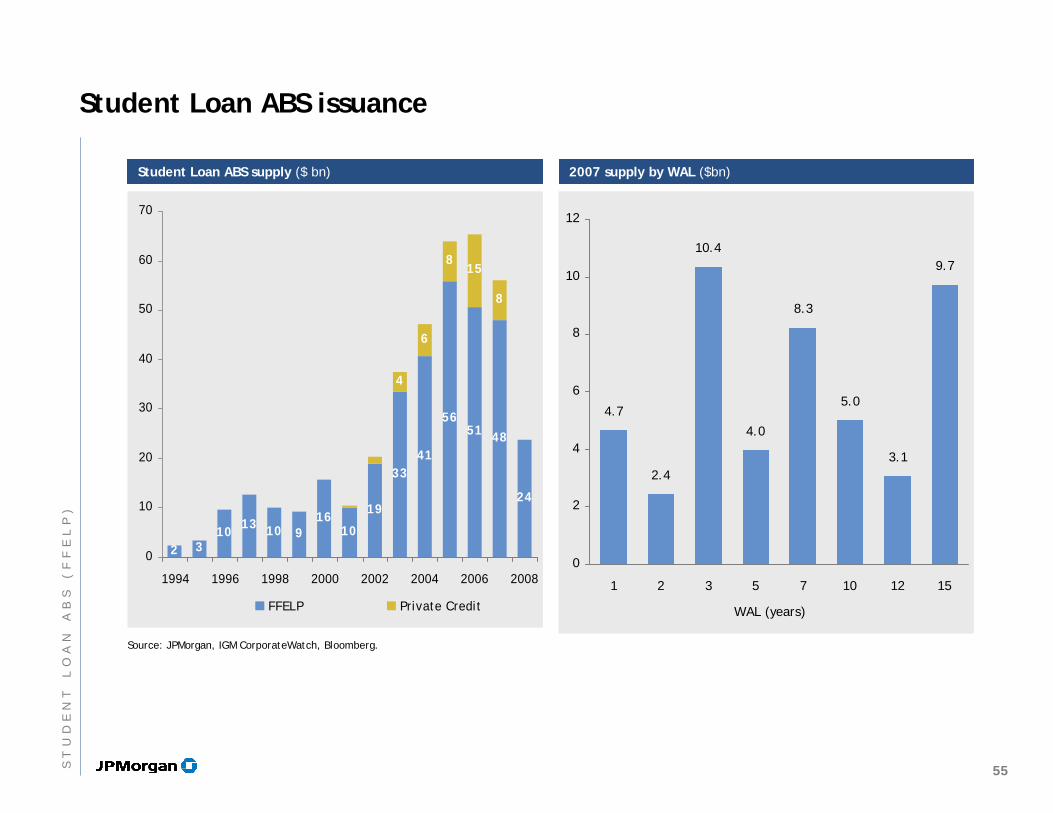

Student Loan ABS issuance

Student Loan ABS supply ($ bn)Student Loan ABS supply ($ bn)

2 310 13 10 9

1610

19

3341

5651 48

24

4

6

815

8

0

10

20

30

40

50

60

70

1994 1996 1998 2000 2002 2004 2006 2008

FFELP Private Credit

2007 supply by WAL ($bn)2007 supply by WAL ($bn)

4.7

2.4

10.4

4.0

8.3

5.0

3.1

9.7

0

2

4

6

8

10

12

1 2 3 5 7 10 12 15

WAL (years)

Source: JPMorgan, IGM CorporateWatch, Bloomberg.

55ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

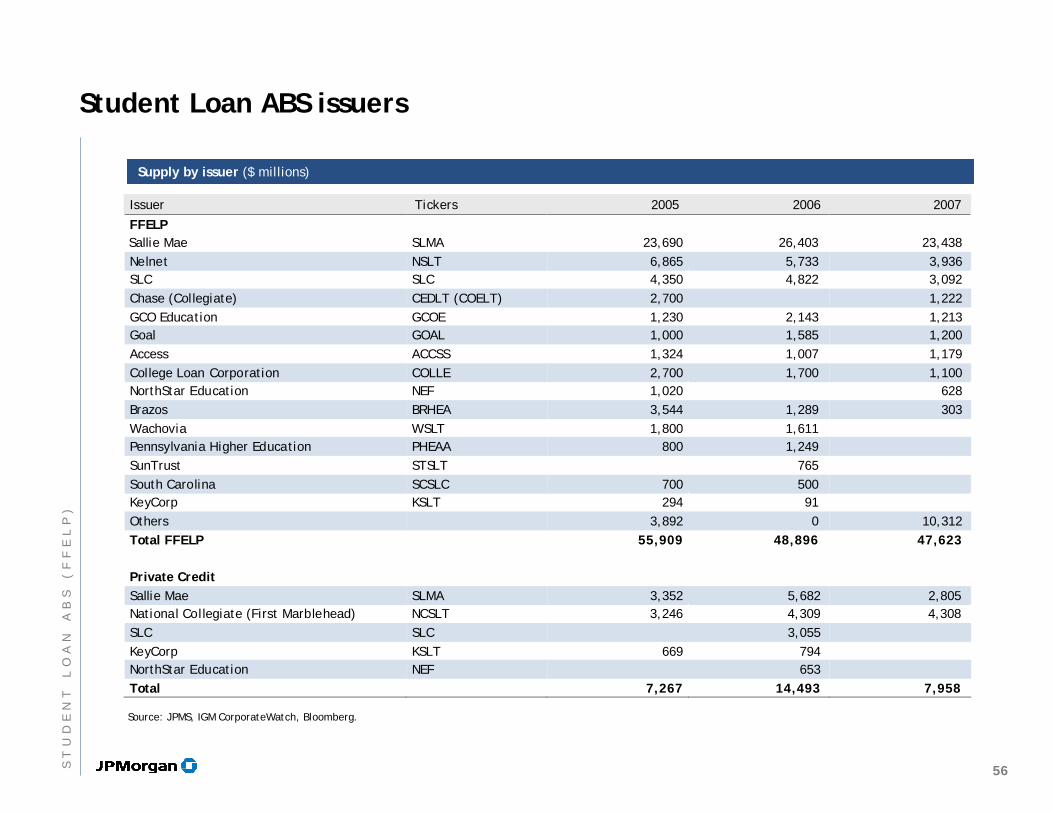

Student Loan ABS issuers

Supply by issuer ($ millions)Supply by issuer ($ millions)

Source: JPMS, IGM CorporateWatch, Bloomberg.

Issuer Tickers 2005 2006 2007

FFELP Sallie Mae SLMA 23,690 26,403 23,438 Nelnet NSLT 6,865 5,733 3,936 SLC SLC 4,350 4,822 3,092 Chase (Collegiate) CEDLT (COELT) 2,700 1,222 GCO Education GCOE 1,230 2,143 1,213 Goal GOAL 1,000 1,585 1,200 Access ACCSS 1,324 1,007 1,179 College Loan Corporation COLLE 2,700 1,700 1,100 NorthStar Education NEF 1,020 628 Brazos BRHEA 3,544 1,289 303 Wachovia WSLT 1,800 1,611 Pennsylvania Higher Education PHEAA 800 1,249 SunTrust STSLT 765 South Carolina SCSLC 700 500 KeyCorp KSLT 294 91 Others 3,892 0 10,312 Total FFELP 55,909 48,896 47,623 Private Credit Sallie Mae SLMA 3,352 5,682 2,805 National Collegiate (First Marblehead) NCSLT 3,246 4,309 4,308 SLC SLC 3,055 KeyCorp KSLT 669 794 NorthStar Education NEF 653 Total 7,267 14,493 7,958

56ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

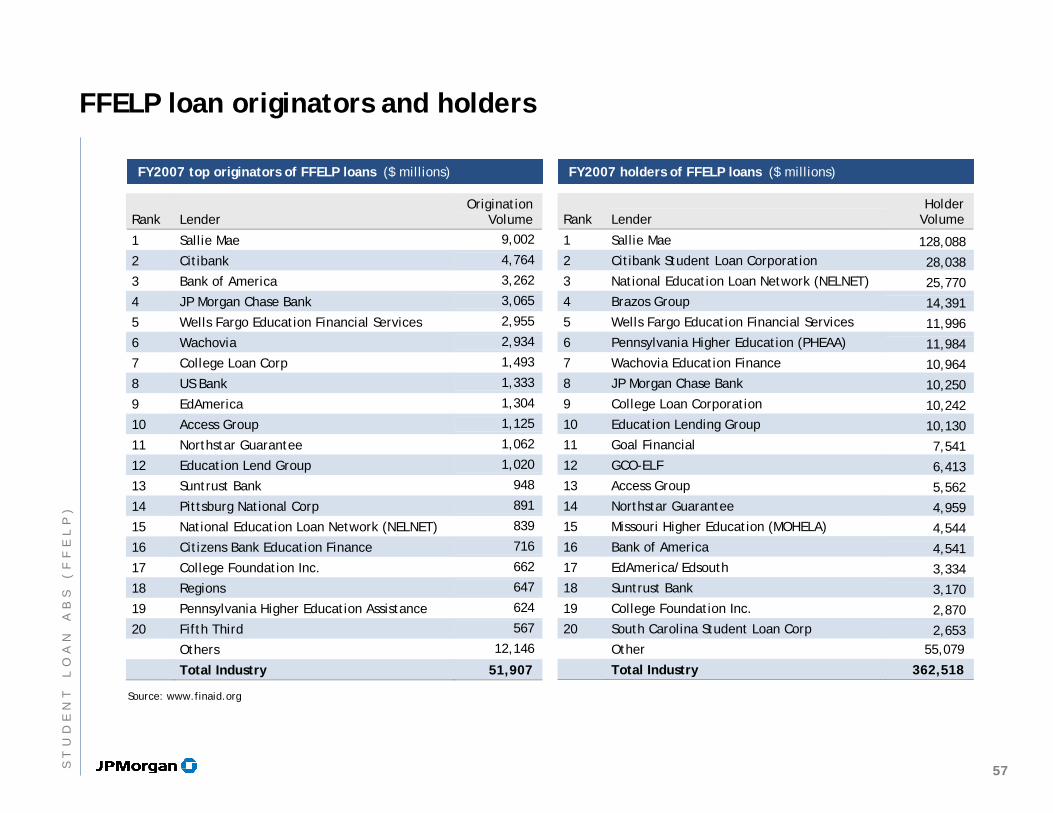

FFELP loan originators and holders

FY2007 top originators of FFELP loans ($ millions)FY2007 top originators of FFELP loans ($ millions) FY2007 holders of FFELP loans ($ millions)FY2007 holders of FFELP loans ($ millions)

Rank Lender Origination

Volume

1 Sallie Mae 9,002

2 Citibank 4,764

3 Bank of America 3,262

4 JP Morgan Chase Bank 3,065

5 Wells Fargo Education Financial Services 2,955

6 Wachovia 2,934

7 College Loan Corp 1,493

8 US Bank 1,333

9 EdAmerica 1,304

10 Access Group 1,125

11 Northstar Guarantee 1,062

12 Education Lend Group 1,020

13 Suntrust Bank 948

14 Pittsburg National Corp 891

15 National Education Loan Network (NELNET) 839

16 Citizens Bank Education Finance 716

17 College Foundation Inc. 662

18 Regions 647

19 Pennsylvania Higher Education Assistance 624

20 Fifth Third 567

Others 12,146

Total Industry 51,907

Source: www.finaid.org

Rank Lender Holder

Volume

1 Sallie Mae 128,088 2 Citibank Student Loan Corporation 28,038 3 National Education Loan Network (NELNET) 25,770 4 Brazos Group 14,391 5 Wells Fargo Education Financial Services 11,996 6 Pennsylvania Higher Education (PHEAA) 11,984 7 Wachovia Education Finance 10,964 8 JP Morgan Chase Bank 10,250 9 College Loan Corporation 10,242 10 Education Lending Group 10,130 11 Goal Financial 7,541 12 GCO-ELF 6,413 13 Access Group 5,562 14 Northstar Guarantee 4,959 15 Missouri Higher Education (MOHELA) 4,544 16 Bank of America 4,541 17 EdAmerica/Edsouth 3,334 18 Suntrust Bank 3,170 19 College Foundation Inc. 2,870 20 South Carolina Student Loan Corp 2,653 Other 55,079

Total Industry 362,518

57ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

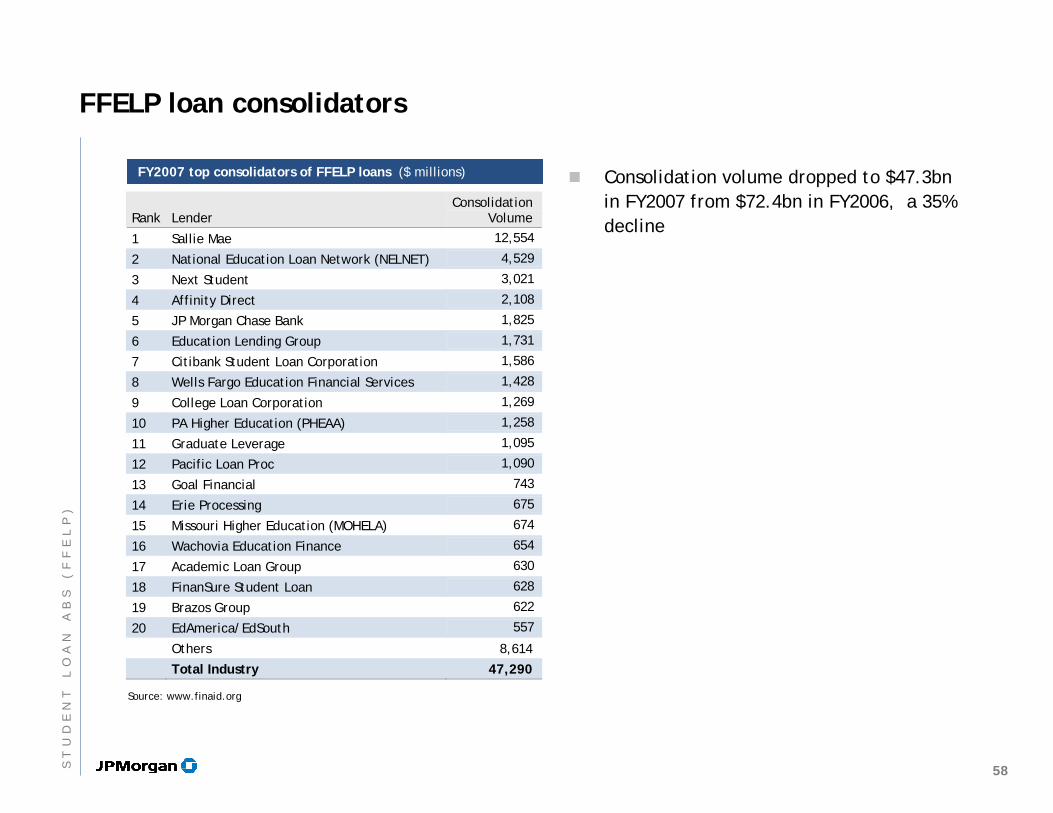

FFELP loan consolidators

FY2007 top consolidators of FFELP loans ($ millions)FY2007 top consolidators of FFELP loans ($ millions)

Rank Lender Consolidation

Volume

1 Sallie Mae 12,554

2 National Education Loan Network (NELNET) 4,529

3 Next Student 3,021

4 Affinity Direct 2,108

5 JP Morgan Chase Bank 1,825

6 Education Lending Group 1,731

7 Citibank Student Loan Corporation 1,586

8 Wells Fargo Education Financial Services 1,428

9 College Loan Corporation 1,269

10 PA Higher Education (PHEAA) 1,258

11 Graduate Leverage 1,095

12 Pacific Loan Proc 1,090

13 Goal Financial 743

14 Erie Processing 675

15 Missouri Higher Education (MOHELA) 674

16 Wachovia Education Finance 654

17 Academic Loan Group 630

18 FinanSure Student Loan 628

19 Brazos Group 622

20 EdAmerica/EdSouth 557

Others 8,614

Total Industry 47,290 Source: www.finaid.org

Consolidation volume dropped to $47.3bn in FY2007 from $72.4bn in FY2006, a 35% decline

58ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

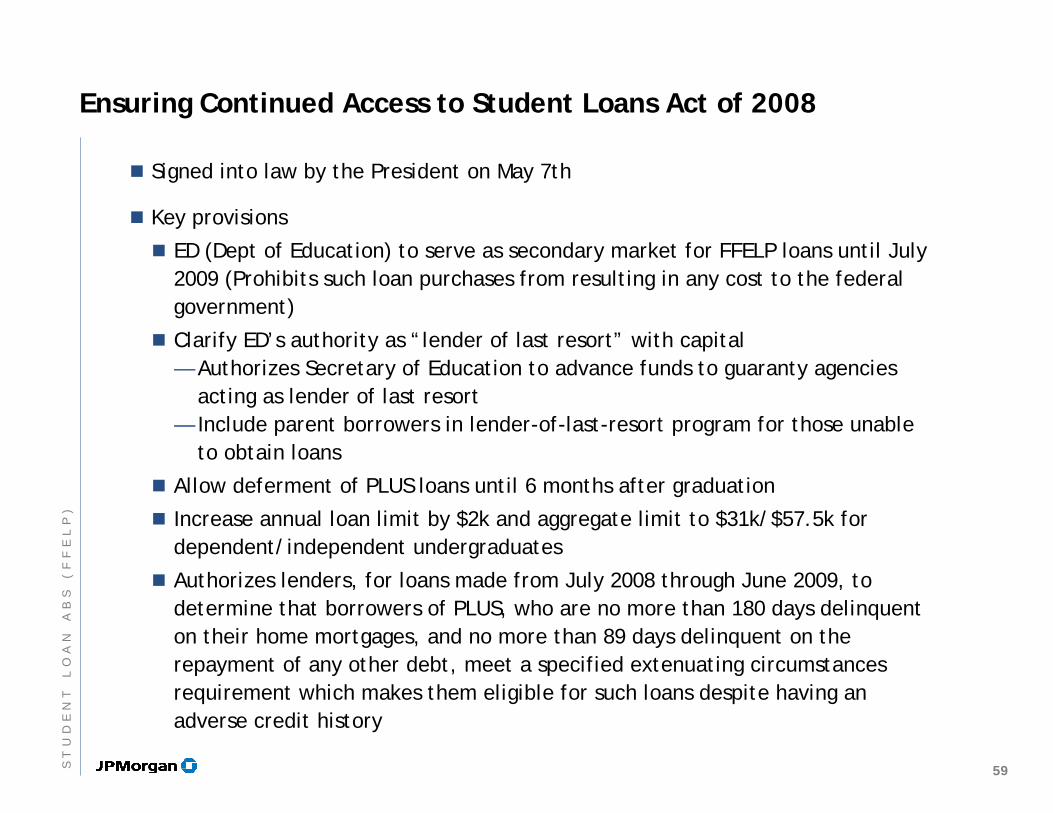

Ensuring Continued Access to Student Loans Act of 2008

Signed into law by the President on May 7th

Key provisions

ED (Dept of Education) to serve as secondary market for FFELP loans until July 2009 (Prohibits such loan purchases from resulting in any cost to the federal government)

Clarify ED’s authority as “lender of last resort” with capital— Authorizes Secretary of Education to advance funds to guaranty agencies

acting as lender of last resort— Include parent borrowers in lender-of-last-resort program for those unable

to obtain loans

Allow deferment of PLUS loans until 6 months after graduation

Increase annual loan limit by $2k and aggregate limit to $31k/$57.5k for dependent/independent undergraduates

Authorizes lenders, for loans made from July 2008 through June 2009, to determine that borrowers of PLUS, who are no more than 180 days delinquent on their home mortgages, and no more than 89 days delinquent on the repayment of any other debt, meet a specified extenuating circumstances requirement which makes them eligible for such loans despite having an adverse credit history

59ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

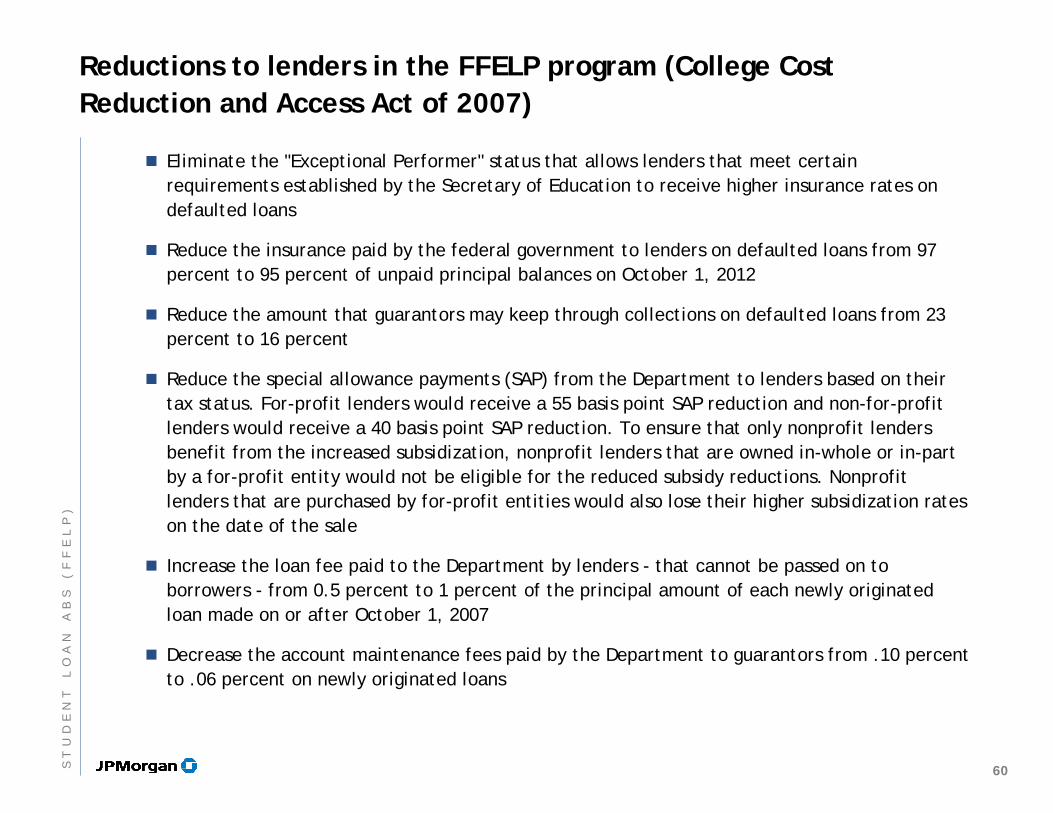

Reductions to lenders in the FFELP program (College Cost Reduction and Access Act of 2007)

Eliminate the "Exceptional Performer" status that allows lenders that meet certain requirements established by the Secretary of Education to receive higher insurance rates on defaulted loans

Reduce the insurance paid by the federal government to lenders on defaulted loans from 97 percent to 95 percent of unpaid principal balances on October 1, 2012

Reduce the amount that guarantors may keep through collections on defaulted loans from 23 percent to 16 percent

Reduce the special allowance payments (SAP) from the Department to lenders based on their tax status. For-profit lenders would receive a 55 basis point SAP reduction and non-for-profit lenders would receive a 40 basis point SAP reduction. To ensure that only nonprofit lenders benefit from the increased subsidization, nonprofit lenders that are owned in-whole or in-part by a for-profit entity would not be eligible for the reduced subsidy reductions. Nonprofit lenders that are purchased by for-profit entities would also lose their higher subsidization rateson the date of the sale

Increase the loan fee paid to the Department by lenders - that cannot be passed on to borrowers - from 0.5 percent to 1 percent of the principal amount of each newly originated loan made on or after October 1, 2007

Decrease the account maintenance fees paid by the Department to guarantors from .10 percent to .06 percent on newly originated loans

60ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

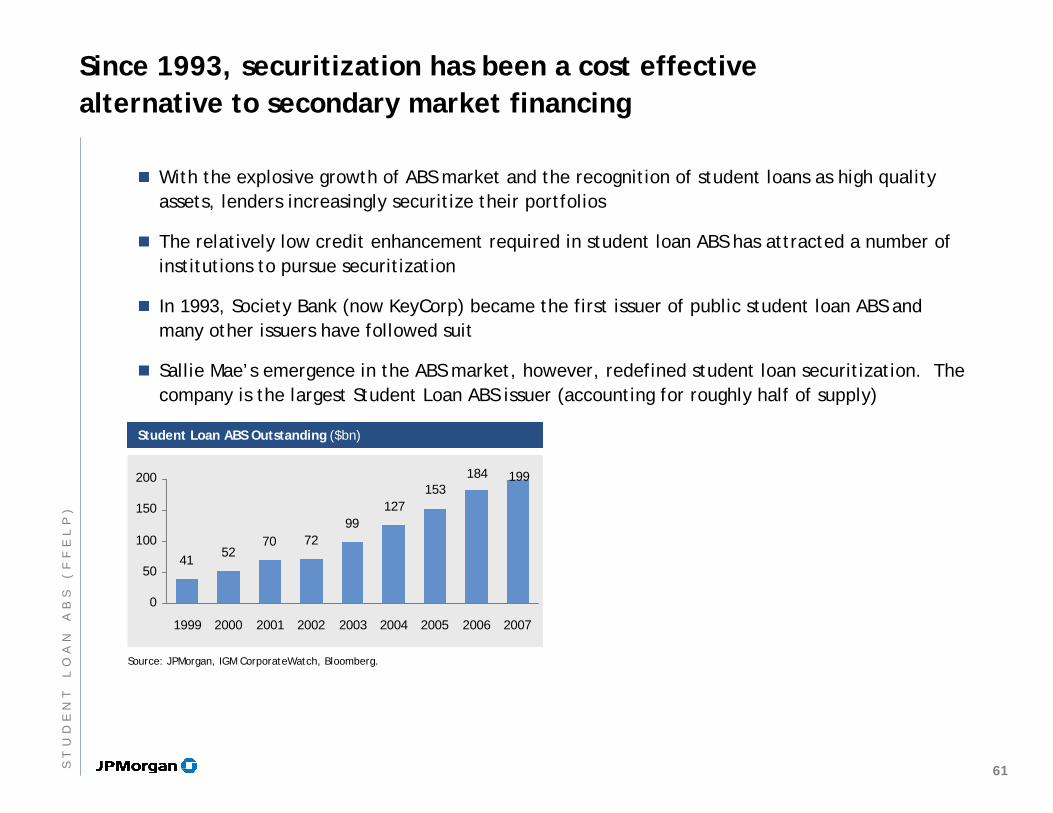

Since 1993, securitization has been a cost effective alternative to secondary market financing

With the explosive growth of ABS market and the recognition of student loans as high quality assets, lenders increasingly securitize their portfolios

The relatively low credit enhancement required in student loan ABS has attracted a number of institutions to pursue securitization

In 1993, Society Bank (now KeyCorp) became the first issuer of public student loan ABS and many other issuers have followed suit

Sallie Mae’s emergence in the ABS market, however, redefined student loan securitization. The company is the largest Student Loan ABS issuer (accounting for roughly half of supply)

Source: JPMorgan, IGM CorporateWatch, Bloomberg.

Student Loan ABS Outstanding ($bn)Student Loan ABS Outstanding ($bn)

4152

70 7299

127153

184 199

0

50

100

150

200

1999 2000 2001 2002 2003 2004 2005 2006 2007

61ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

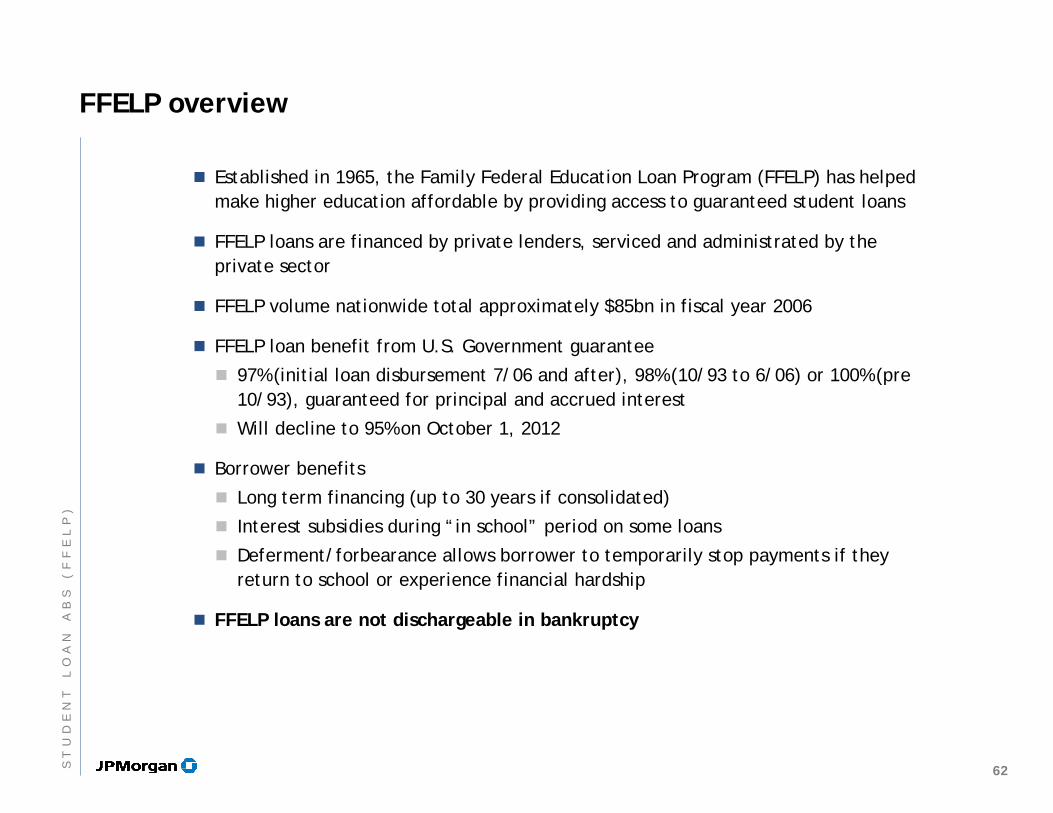

FFELP overview

Established in 1965, the Family Federal Education Loan Program (FFELP) has helped make higher education affordable by providing access to guaranteed student loans

FFELP loans are financed by private lenders, serviced and administrated by the private sector

FFELP volume nationwide total approximately $85bn in fiscal year 2006

FFELP loan benefit from U.S. Government guarantee

97% (initial loan disbursement 7/06 and after), 98% (10/93 to 6/06) or 100% (pre 10/93), guaranteed for principal and accrued interest

Will decline to 95% on October 1, 2012

Borrower benefits

Long term financing (up to 30 years if consolidated)

Interest subsidies during “in school” period on some loans

Deferment/forbearance allows borrower to temporarily stop payments if they return to school or experience financial hardship

FFELP loans are not dischargeable in bankruptcy

62ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

FFELP loan types

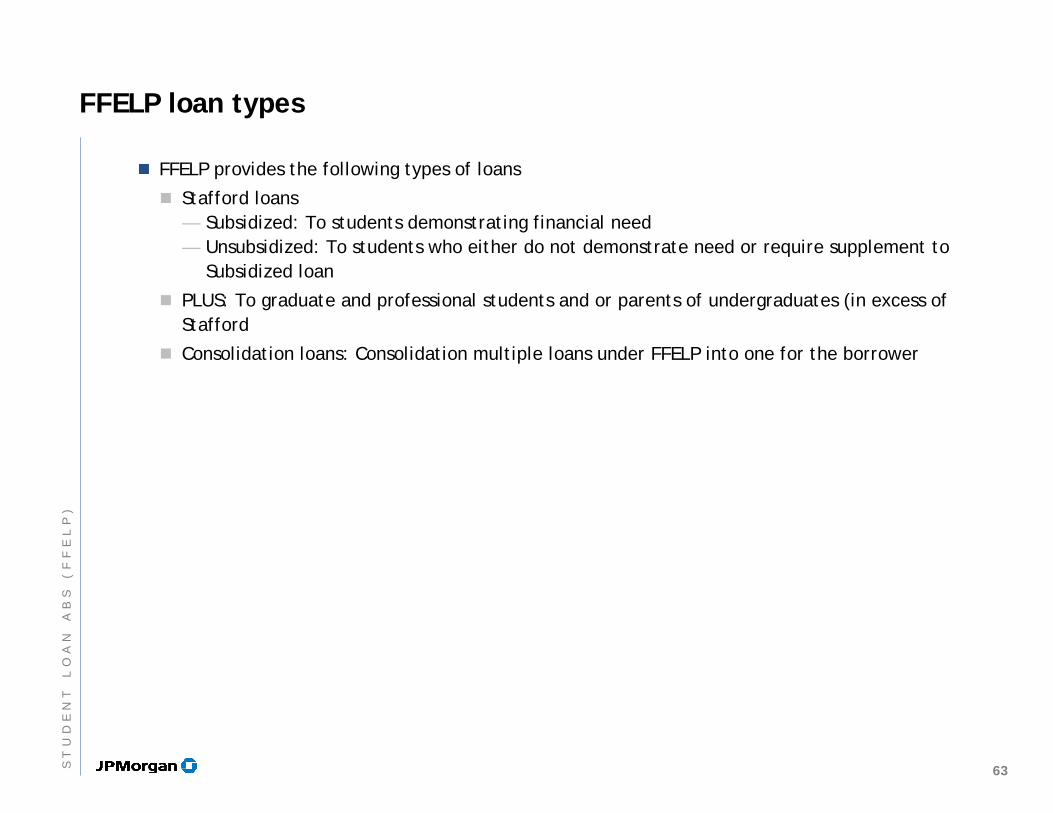

FFELP provides the following types of loans

Stafford loans — Subsidized: To students demonstrating financial need— Unsubsidized: To students who either do not demonstrate need or require supplement to

Subsidized loan

PLUS: To graduate and professional students and or parents of undergraduates (in excess of Stafford

Consolidation loans: Consolidation multiple loans under FFELP into one for the borrower

63ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

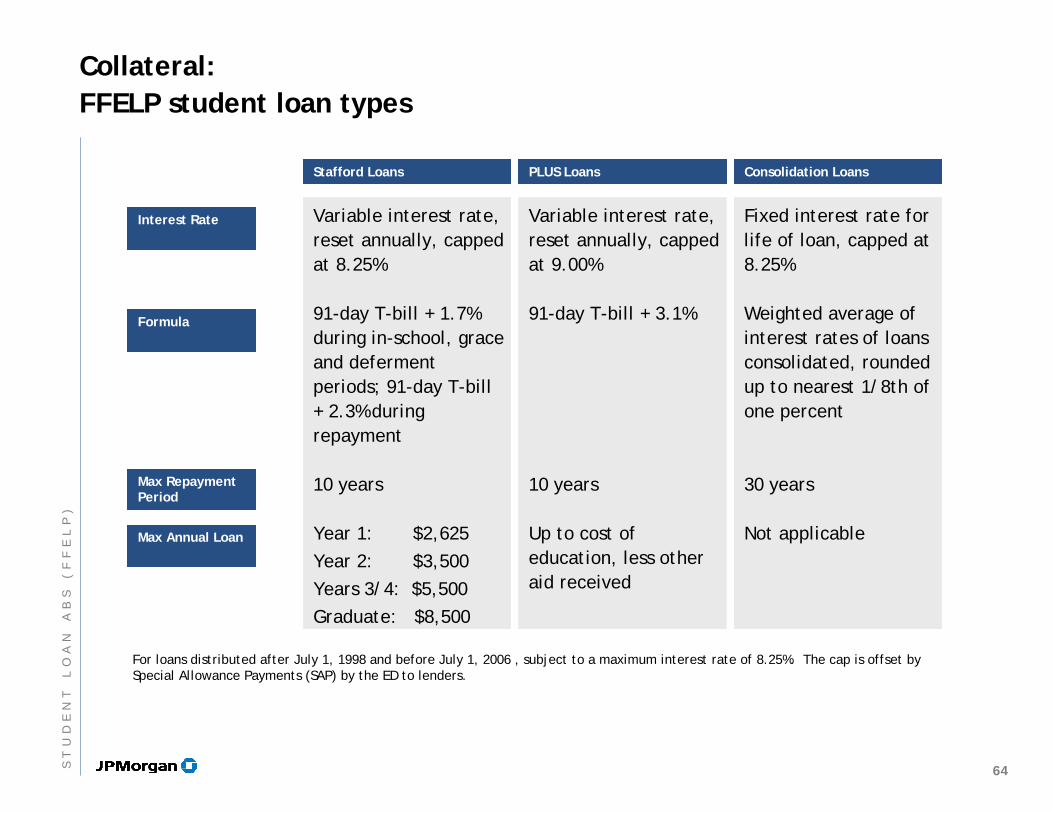

Stafford LoansStafford Loans PLUS LoansPLUS Loans Consolidation LoansConsolidation Loans

Collateral:FFELP student loan types

Variable interest rate, reset annually, capped at 8.25%

91-day T-bill + 1.7% during in-school, grace and deferment periods; 91-day T-bill + 2.3% during repayment

10 years

Year 1: $2,625Year 2: $3,500Years 3/4: $5,500Graduate: $8,500

Variable interest rate, reset annually, capped at 9.00%

91-day T-bill + 3.1%

10 years

Up to cost of education, less other aid received

Fixed interest rate for life of loan, capped at 8.25%

Weighted average of interest rates of loans consolidated, rounded up to nearest 1/8th of one percent

30 years

Not applicable

Interest RateInterest Rate

FormulaFormula

Max Repayment Period

Max Repayment Period

Max Annual LoanMax Annual Loan

For loans distributed after July 1, 1998 and before July 1, 2006 , subject to a maximum interest rate of 8.25%. The cap is offset by Special Allowance Payments (SAP) by the ED to lenders.

64ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

Stafford student loan rates

Stafford loan ratesStafford loan rates

Trigger Date Borrower Rate Maximum Borrower Rate Interest Rate Margin

<10/1/81 7% 7% N/A

1/1/81-9/12/83 9% 9% N/A

9/13/83-6/30/88 8% 8% N/A

7/1/88-9/30/92 8% for 48 months; then, 91-day Treasury + Margin

8% for 48 months, then 10% 3.25%

10/1/92-6/30/94 91-day Treasury + Margin 9% 3.10%

7/1/94-6/30/95 91-day Treasury + Margin 8.25% 3.10%

7/1/95-6/30/98 91-day Treasury + Margin 8.25% 2.50% (in school, grace, or deferment), 3.10% (repayment)

7/1/98 – 6/30/98 91-day Treasury + Margin 8.25% 1.70% (in school, grace, or deferment), 2.30% (repayment)

7/1/06 - 9/30/07 Fixed 6.8% N/A

>10/1/07 Decline to fixed 3.4% by 7/1/2011 N/A

65ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

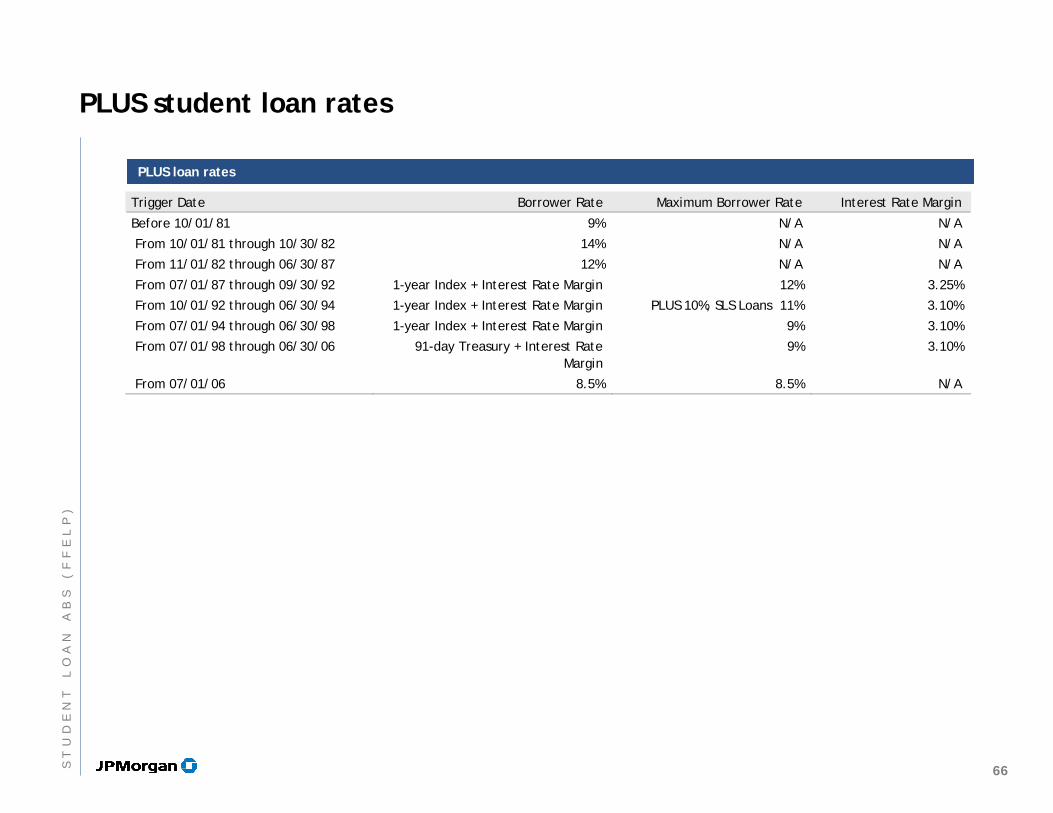

PLUS student loan rates

PLUS loan ratesPLUS loan rates

Trigger Date Borrower Rate Maximum Borrower Rate Interest Rate Margin

Before 10/01/81 9% N/A N/A

From 10/01/81 through 10/30/82 14% N/A N/A

From 11/01/82 through 06/30/87 12% N/A N/A

From 07/01/87 through 09/30/92 1-year Index + Interest Rate Margin 12% 3.25%

From 10/01/92 through 06/30/94 1-year Index + Interest Rate Margin PLUS 10%, SLS Loans 11% 3.10%

From 07/01/94 through 06/30/98 1-year Index + Interest Rate Margin 9% 3.10%

From 07/01/98 through 06/30/06 91-day Treasury + Interest Rate Margin

9% 3.10%

From 07/01/06 8.5% 8.5% N/A

66ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

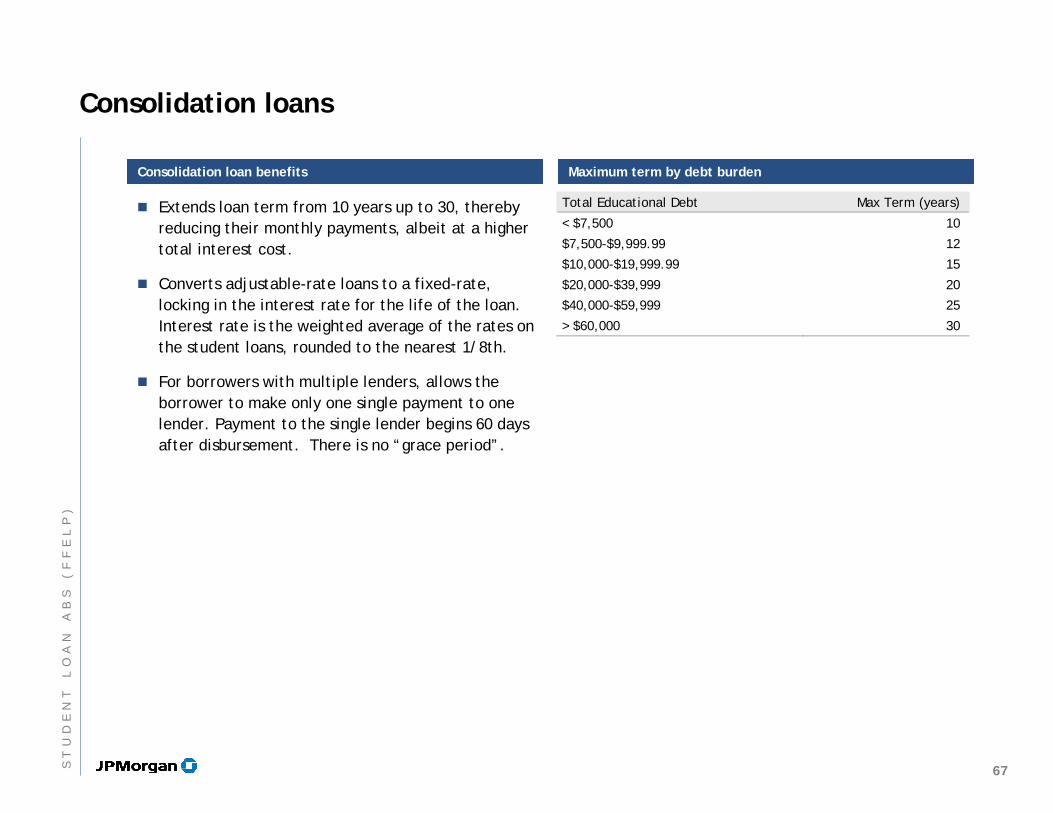

Consolidation loans

Consolidation loan benefitsConsolidation loan benefits Maximum term by debt burdenMaximum term by debt burden

Extends loan term from 10 years up to 30, thereby reducing their monthly payments, albeit at a higher total interest cost.

Converts adjustable-rate loans to a fixed-rate, locking in the interest rate for the life of the loan. Interest rate is the weighted average of the rates on the student loans, rounded to the nearest 1/8th.

For borrowers with multiple lenders, allows the borrower to make only one single payment to one lender. Payment to the single lender begins 60 days after disbursement. There is no “grace period”.

Total Educational Debt Max Term (years)

< $7,500 10

$7,500-$9,999.99 12

$10,000-$19,999.99 15

$20,000-$39,999 20

$40,000-$59,999 25

> $60,000 30

67ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

Interest Subsidy Payments and Special Allowance Payments

Dept of Education (ED)

Borrower

SAP and ISP

Paid quarterly

Principal and Interest

Lender

Interest Subsidy Payment (ISP)

Federal government pays for in-school, grace and deferment interest on subsidized loans

Available for Stafford Subsized and Subsidized Consolidation Loans

Special Allowance Payment (SAP)

Provides lenders with minimum returns to either the 91-day T-Bill or 90-day CP plus a spread

Available for Stafford and Consolidation Loans

Available for PLUS loans when borrower hits a cap

68ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

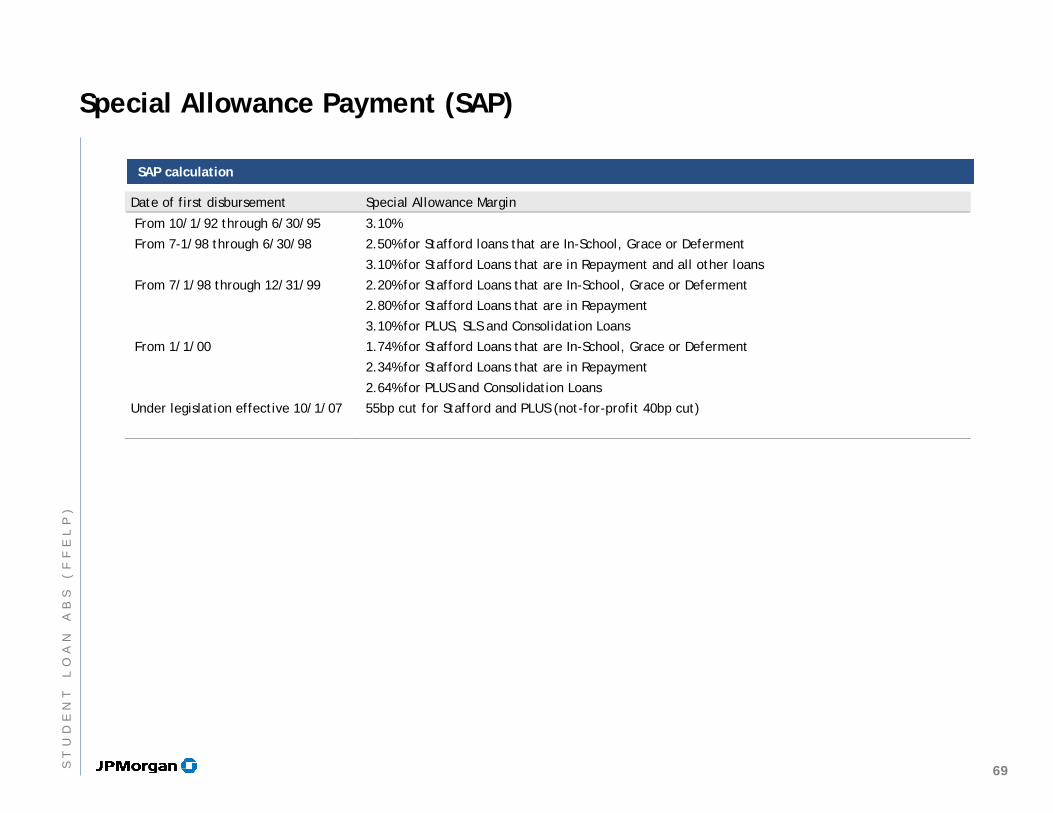

Special Allowance Payment (SAP)

SAP calculationSAP calculation

Date of first disbursement Special Allowance Margin

From 10/1/92 through 6/30/95 3.10%

From 7-1/98 through 6/30/98 2.50% for Stafford loans that are In-School, Grace or Deferment

3.10% for Stafford Loans that are in Repayment and all other loans

From 7/1/98 through 12/31/99 2.20% for Stafford Loans that are In-School, Grace or Deferment

2.80% for Stafford Loans that are in Repayment

3.10% for PLUS, SLS and Consolidation Loans

From 1/1/00 1.74% for Stafford Loans that are In-School, Grace or Deferment

2.34% for Stafford Loans that are in Repayment

2.64% for PLUS and Consolidation Loans

Under legislation effective 10/1/07 55bp cut for Stafford and PLUS (not-for-profit 40bp cut)

69ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

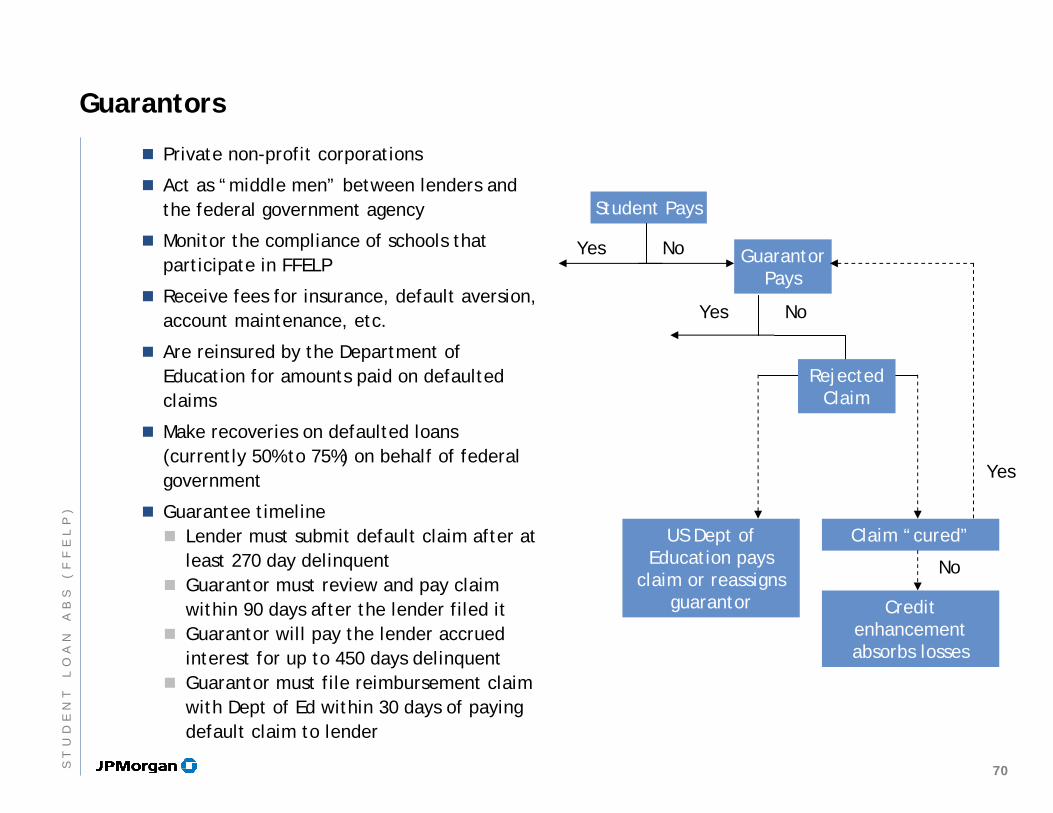

Guarantors

Private non-profit corporations

Act as “middle men” between lenders and the federal government agency

Monitor the compliance of schools that participate in FFELP

Receive fees for insurance, default aversion, account maintenance, etc.

Are reinsured by the Department of Education for amounts paid on defaulted claims

Make recoveries on defaulted loans (currently 50% to 75%) on behalf of federal government

Guarantee timelineLender must submit default claim after at least 270 day delinquentGuarantor must review and pay claim within 90 days after the lender filed itGuarantor will pay the lender accrued interest for up to 450 days delinquentGuarantor must file reimbursement claim with Dept of Ed within 30 days of paying default claim to lender

Student Pays

Guarantor Pays

Yes No

Yes No

Rejected Claim

US Dept of Education pays

claim or reassigns guarantor

Claim “cured”

Credit enhancement absorbs losses

Yes

No

70ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

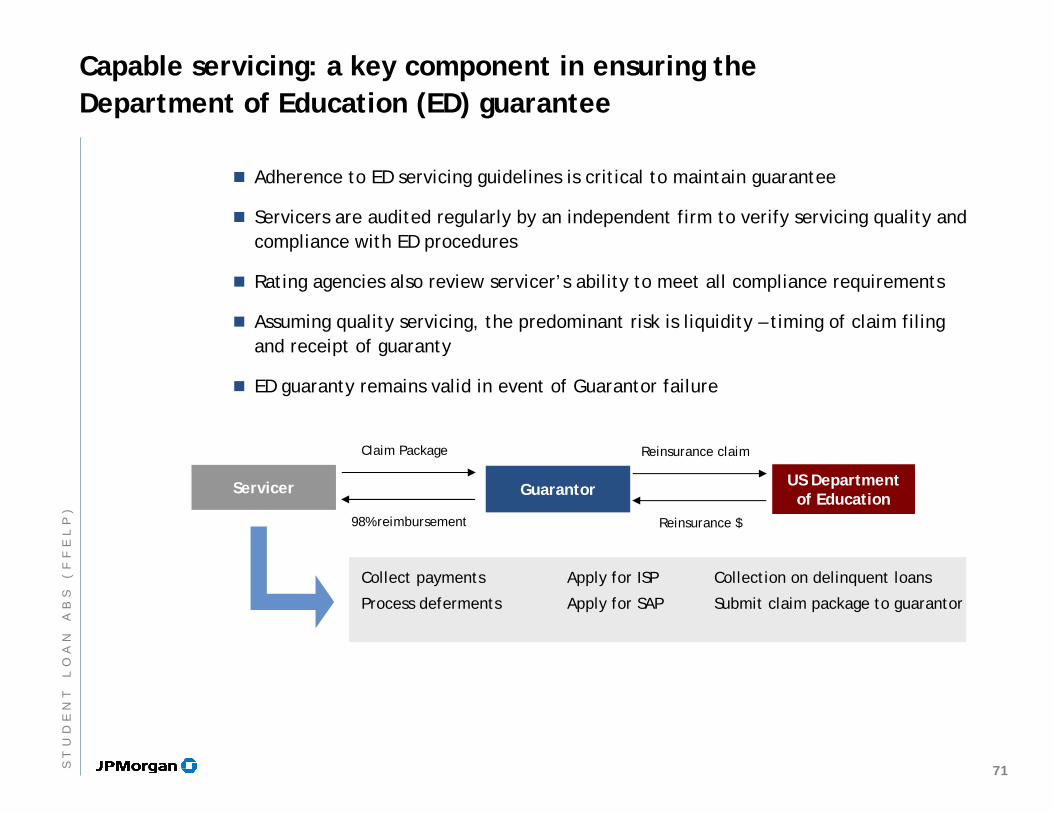

Servicer Guarantor

Claim Package

98% reimbursement

Collect payments

Process deferments

Reinsurance claim

Reinsurance $

US Departmentof Education

Apply for ISP

Apply for SAP

Collection on delinquent loans

Submit claim package to guarantor

Capable servicing: a key component in ensuring the Department of Education (ED) guarantee

Adherence to ED servicing guidelines is critical to maintain guarantee

Servicers are audited regularly by an independent firm to verify servicing quality and compliance with ED procedures

Rating agencies also review servicer’s ability to meet all compliance requirements

Assuming quality servicing, the predominant risk is liquidity – timing of claim filing and receipt of guaranty

ED guaranty remains valid in event of Guarantor failure

71ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

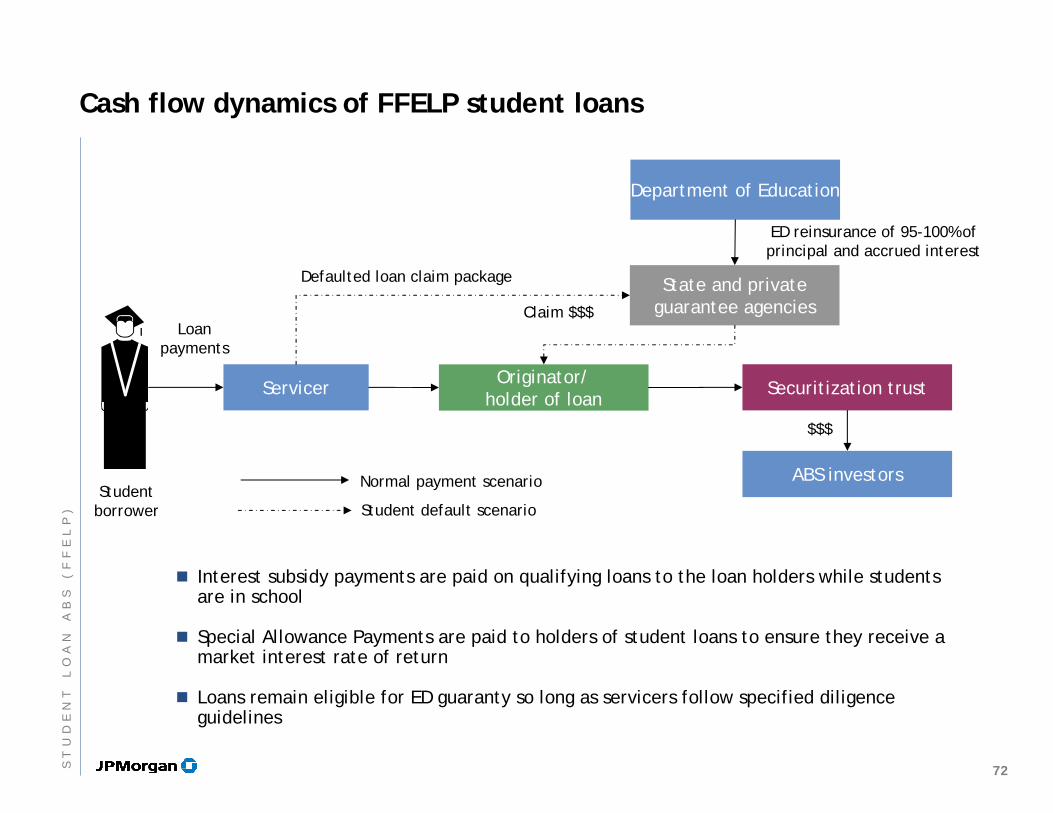

Cash flow dynamics of FFELP student loans

Department of Education

State and private guarantee agencies

ABS investors

Securitization trustOriginator/holder of loan

Servicer

Defaulted loan claim package

Claim $$$

$$$

Normal payment scenario

Student default scenario

ED reinsurance of 95-100% of principal and accrued interest

Loan payments

Student borrower

Interest subsidy payments are paid on qualifying loans to the loan holders while students are in school

Special Allowance Payments are paid to holders of student loans to ensure they receive a market interest rate of return

Loans remain eligible for ED guaranty so long as servicers follow specified diligence guidelines

72ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

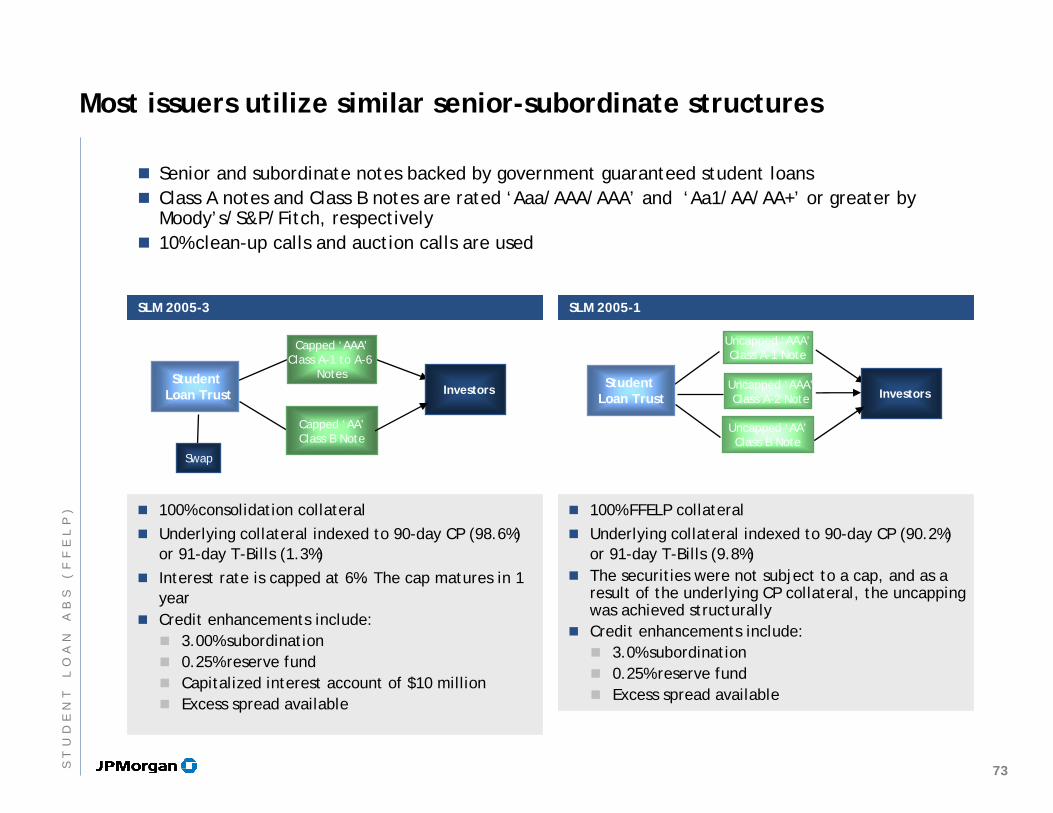

Most issuers utilize similar senior-subordinate structures

100% consolidation collateralUnderlying collateral indexed to 90-day CP (98.6%) or 91-day T-Bills (1.3%)Interest rate is capped at 6%. The cap matures in 1 yearCredit enhancements include:

3.00% subordination0.25% reserve fund Capitalized interest account of $10 millionExcess spread available

100% FFELP collateralUnderlying collateral indexed to 90-day CP (90.2%) or 91-day T-Bills (9.8%)The securities were not subject to a cap, and as a result of the underlying CP collateral, the uncapping was achieved structurallyCredit enhancements include:

3.0% subordination0.25% reserve fund Excess spread available

SLM 2005-3SLM 2005-3 SLM 2005-1SLM 2005-1

Senior and subordinate notes backed by government guaranteed student loans Class A notes and Class B notes are rated ‘Aaa/AAA/AAA’ and ‘Aa1/AA/AA+’ or greater by Moody’s/S&P/Fitch, respectively10% clean-up calls and auction calls are used

Student Loan Trust

Capped ‘AAA’Class A-1 to A-6

Notes

Capped ‘AA’Class B Note

Investors

Swap

Student Loan Trust

Uncapped ‘AAA’Class A-1 Note

Uncapped ‘AAA’Class A-2 Note

Uncapped ‘AA’Class B Note

Investors

73ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

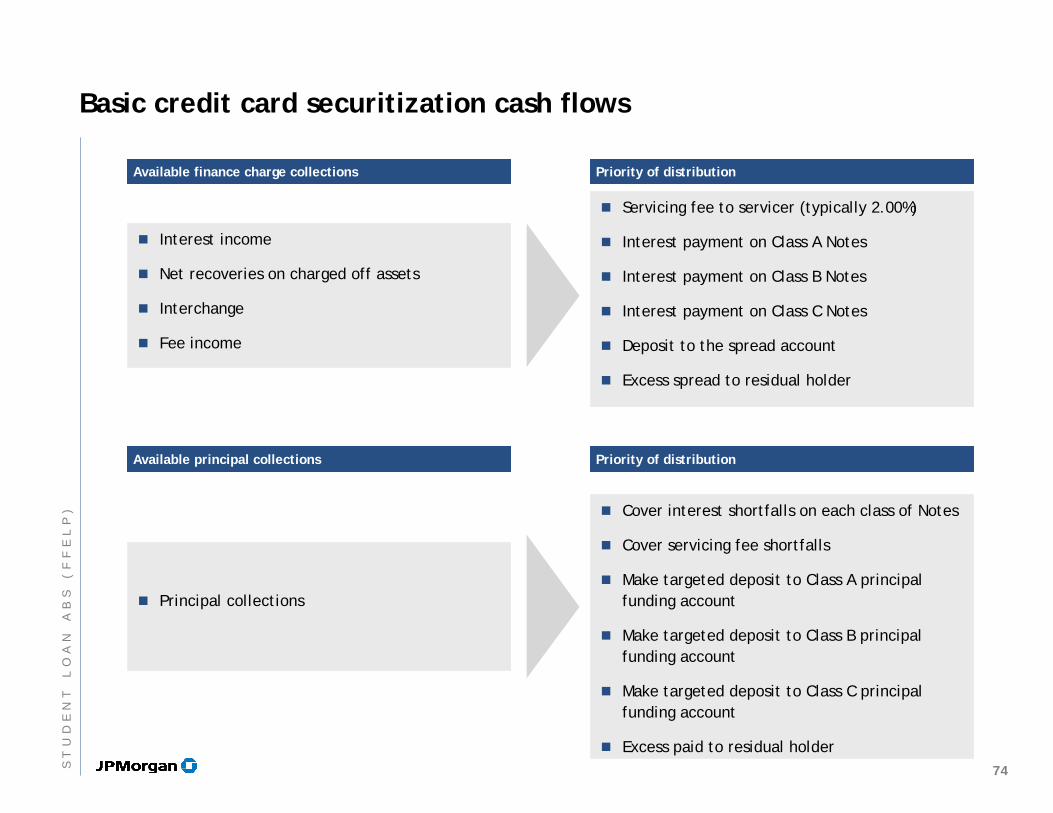

Basic credit card securitization cash flows

Interest income

Net recoveries on charged off assets

Interchange

Fee income

Servicing fee to servicer (typically 2.00%)

Interest payment on Class A Notes

Interest payment on Class B Notes

Interest payment on Class C Notes

Deposit to the spread account

Excess spread to residual holder

Available finance charge collectionsAvailable finance charge collections Priority of distributionPriority of distribution

Available principal collectionsAvailable principal collections Priority of distributionPriority of distribution

Principal collections

Cover interest shortfalls on each class of Notes

Cover servicing fee shortfalls

Make targeted deposit to Class A principal funding account

Make targeted deposit to Class B principal funding account

Make targeted deposit to Class C principal funding account

Excess paid to residual holder74S

TU

DE

NT

LO

AN

AB

S(

FF

EL

P)

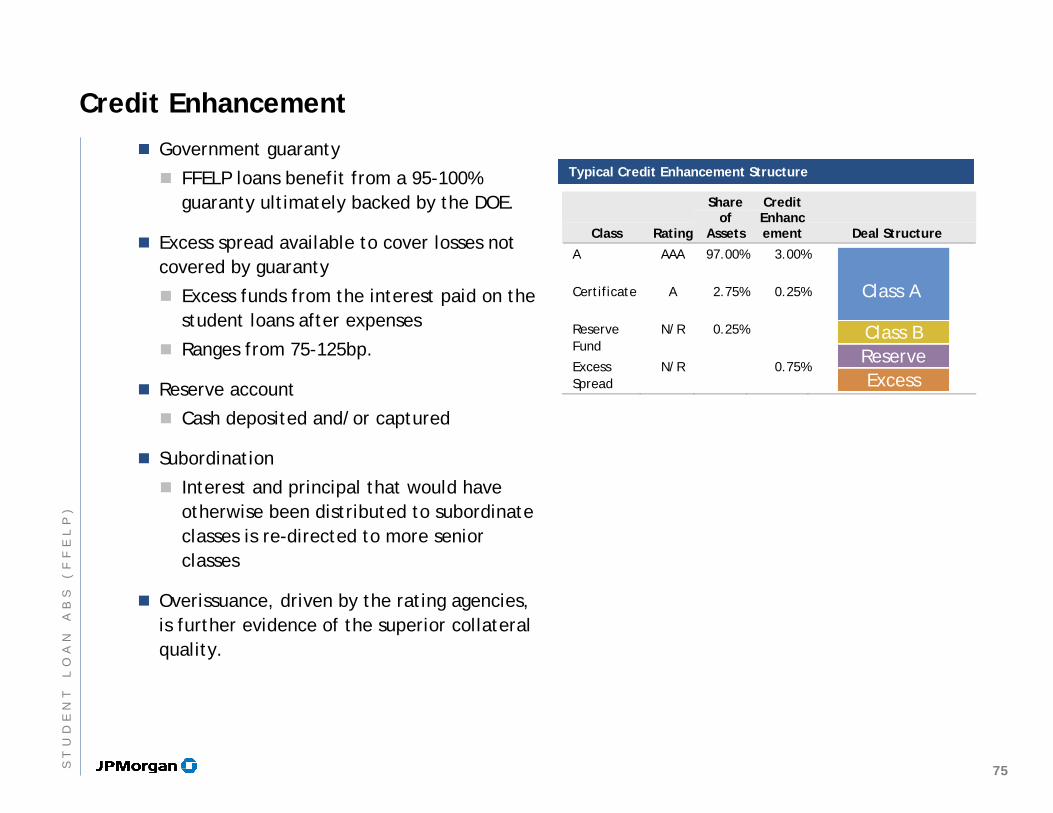

Credit EnhancementGovernment guaranty

FFELP loans benefit from a 95-100% guaranty ultimately backed by the DOE.

Excess spread available to cover losses not covered by guaranty

Excess funds from the interest paid on the student loans after expenses

Ranges from 75-125bp.

Reserve account

Cash deposited and/or captured

Subordination

Interest and principal that would have otherwise been distributed to subordinate classes is re-directed to more senior classes

Overissuance, driven by the rating agencies, is further evidence of the superior collateral quality.

Class Rating

Share of

Assets

Credit Enhancement Deal Structure

A

AAA 97.00% 3.00%

Certificate

A 2.75% 0.25%

Reserve Fund

N/R 0.25%

Excess Spread

N/R 0.75%

Typical Credit Enhancement StructureTypical Credit Enhancement Structure

Class A

Class B

ExcessReserve

75ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

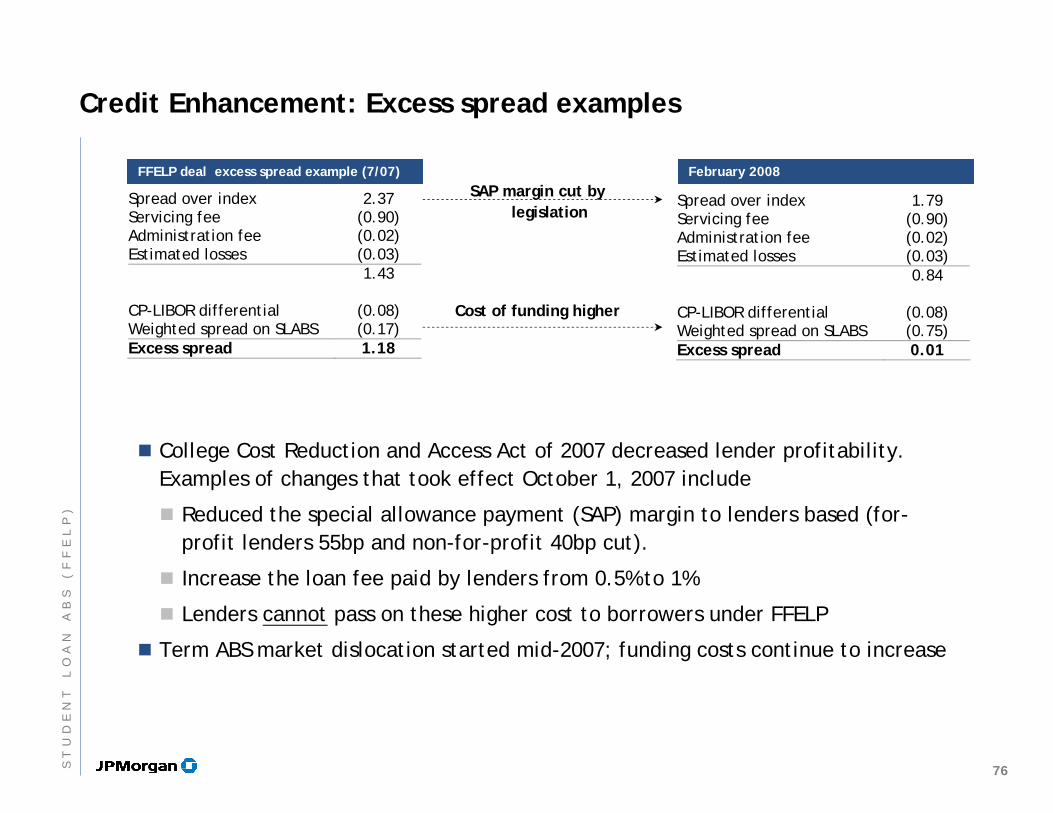

Credit Enhancement: Excess spread examples

February 2008February 2008FFELP deal excess spread example (7/07)FFELP deal excess spread example (7/07)

Spread over index 2.37 Servicing fee (0.90) Administration fee (0.02) Estimated losses (0.03)

1.43

CP-LIBOR differential (0.08) Weighted spread on SLABS (0.17) Excess spread 1.18

Spread over index 1.79 Servicing fee (0.90) Administration fee (0.02) Estimated losses (0.03)

0.84

CP-LIBOR differential (0.08) Weighted spread on SLABS (0.75) Excess spread 0.01

SAP margin cut by legislation

Cost of funding higher

College Cost Reduction and Access Act of 2007 decreased lender profitability. Examples of changes that took effect October 1, 2007 include

Reduced the special allowance payment (SAP) margin to lenders based (for-profit lenders 55bp and non-for-profit 40bp cut).

Increase the loan fee paid by lenders from 0.5% to 1%

Lenders cannot pass on these higher cost to borrowers under FFELP

Term ABS market dislocation started mid-2007; funding costs continue to increase

76ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

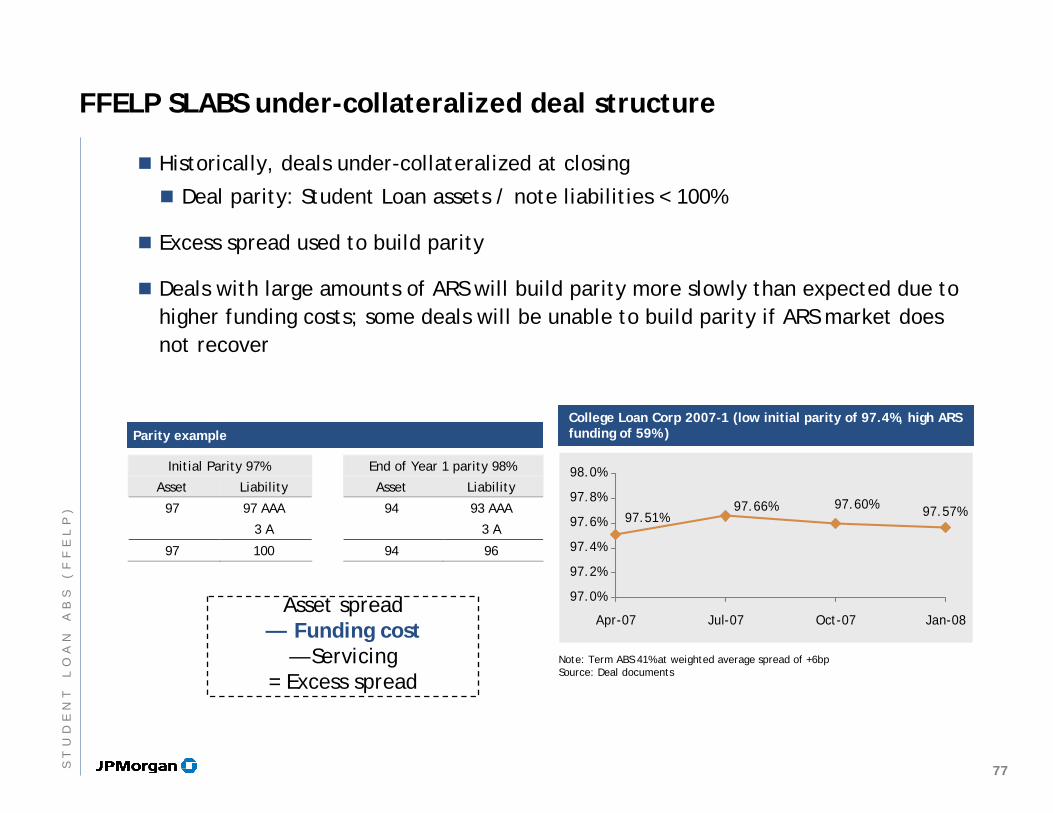

FFELP SLABS under-collateralized deal structure

Historically, deals under-collateralized at closing

Deal parity: Student Loan assets / note liabilities < 100%

Excess spread used to build parity

Deals with large amounts of ARS will build parity more slowly than expected due to higher funding costs; some deals will be unable to build parity if ARS market does not recover

Asset spread— Funding cost

— Servicing = Excess spread

Parity exampleParity example

Initial Parity 97% End of Year 1 parity 98%

Asset Liability Asset Liability

97 97 AAA 94 93 AAA

3 A 3 A

97 100 94 96

97.57%97.60%97.51%

97.66%

97.0%

97.2%

97.4%

97.6%

97.8%

98.0%

Apr-07 Jul-07 Oct-07 Jan-08

College Loan Corp 2007-1 (low initial parity of 97.4%, high ARS funding of 59% )

College Loan Corp 2007-1 (low initial parity of 97.4%, high ARS funding of 59% )

Note: Term ABS 41% at weighted average spread of +6bpSource: Deal documents

77ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

Recent changes in deal structure

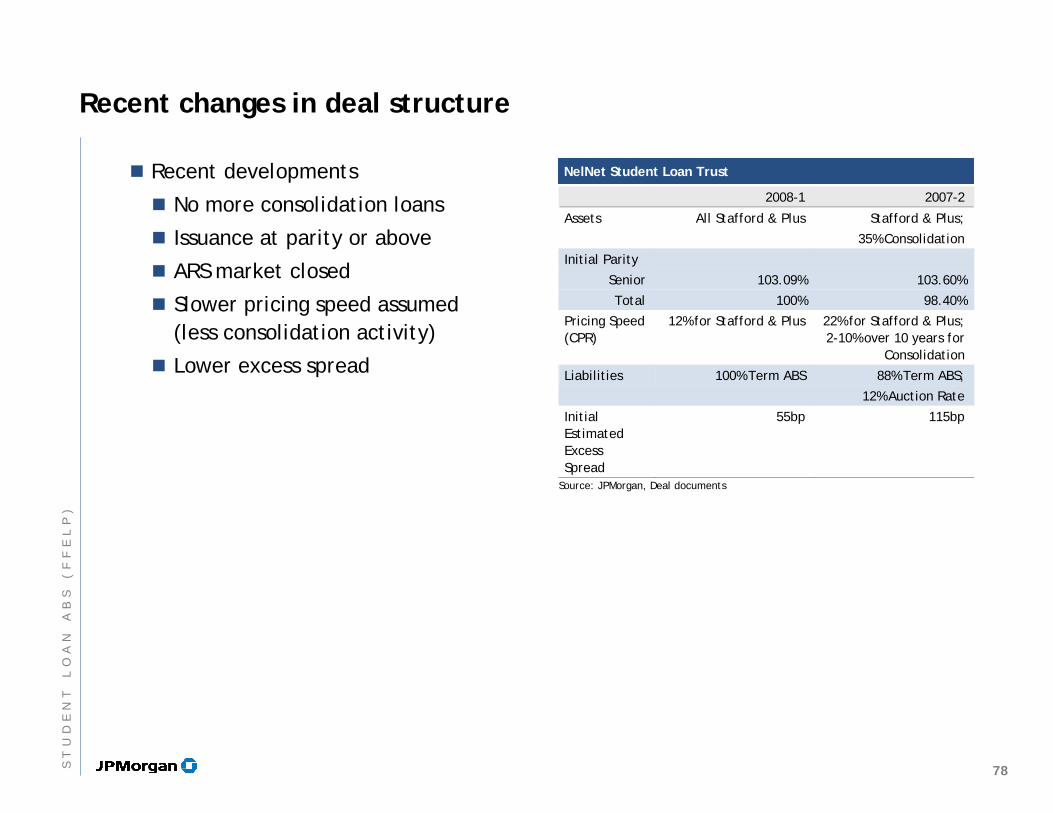

Recent developments

No more consolidation loans

Issuance at parity or above

ARS market closed

Slower pricing speed assumed (less consolidation activity)

Lower excess spread

NelNet Student Loan TrustNelNet Student Loan Trust

2008-1 2007-2

Assets All Stafford & Plus Stafford & Plus;

35% Consolidation

Initial Parity

Senior 103.09% 103.60%

Total 100% 98.40%

Pricing Speed (CPR)

12% for Stafford & Plus 22% for Stafford & Plus; 2-10% over 10 years for

Consolidation

Liabilities 100% Term ABS 88% Term ABS;

12% Auction Rate

Initial Estimated Excess Spread

55bp 115bp

Source: JPMorgan, Deal documents

78ST

UD

EN

TL

OA

NA

BS

(F

FE

LP

)

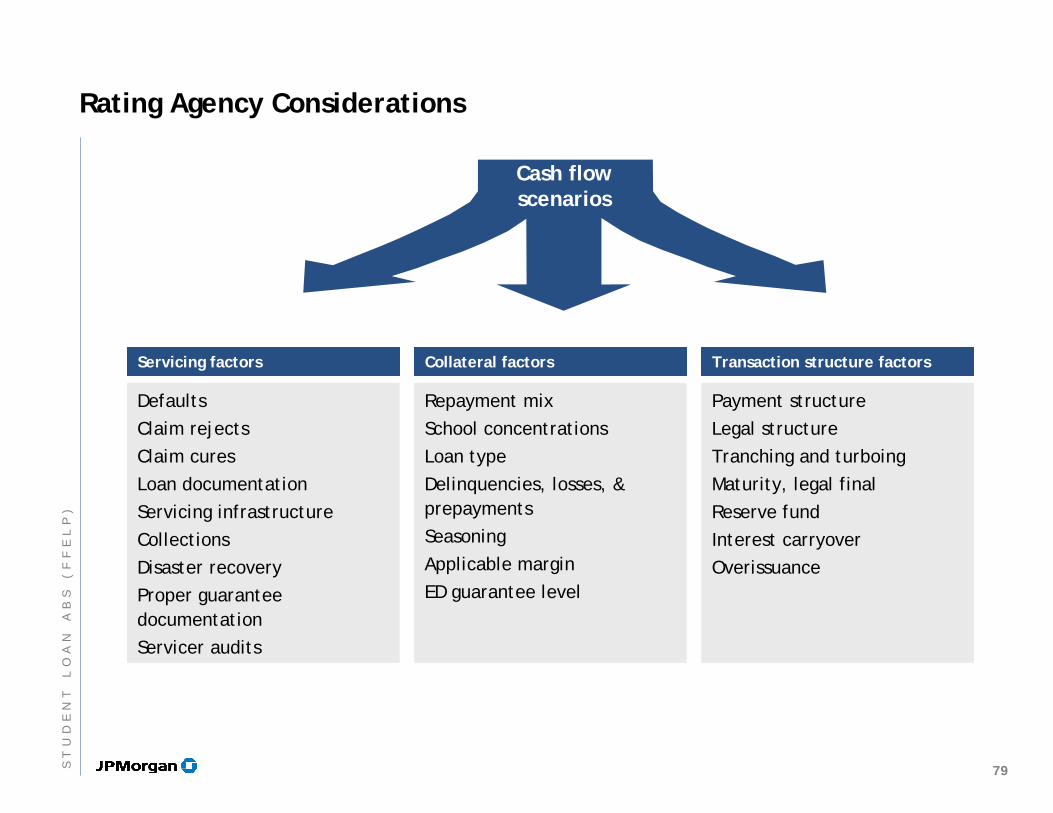

Rating Agency Considerations

Cash flowscenarios

Servicing factorsServicing factors Collateral factorsCollateral factors Transaction structure factorsTransaction structure factors

DefaultsClaim rejectsClaim curesLoan documentationServicing infrastructureCollectionsDisaster recoveryProper guarantee documentationServicer audits