site visit…january 2014 kibali gold mine location…

TRANSCRIPT

Site visit…January 2014

Kibali gold mine location…

Mombasa-Kibali supply route…

DRC

DistancesCurrent route

1759 km

Alternative route

2337 km

UgandaKenya

Entebbe

Kampala

Kibali Gold Mine

Mombasa

ì

History of the Kibali project…

September 2009…Randgold and AGA acquired 70% of Kibali project through acquisition of Moto Gold

December 2009…a further 20% purchased from the DRC Government parastatal, Sokimo

Specific objectives at date of acquisition were:

Restate resource model

Optimise feasibility study to include full resource potential of the Kibaligeological model

Build road from Ugandan border to Doko to enable effective logistical supply to the project for construction

Clear illegal miners from the exclusion zone

Establish and maintain security on project area through the full involvement of the Central and Provincial Governments

Resettle over 4000 families to 14 villages in new city of Kokiza

First gold targeted for 2015

In 2011 first gold guidance revised to December 2013

Kibali…project update to December 2013

First gold poured 24 September 2013

Oxide circuit commissioned before end September 2013 ahead of schedule

Remaining sulphide circuit on track for commissioning end Q1 2014

Shaft main sink commenced October 2013

RAP construction completed (4232 houses) and 100% of the families resettled at Kokiza

24 diesel generators commissioned (12 in Q3 and 12 in Q4)

Concentrate tailings facility completed

Nzoro 2 hydropower station construction completed and turbines / generators installed

Nzoro 2 penstock and canal 50% complete

Stakeholders…

Stakeholders Participation…

45%

45%

10%

Kibali shareholding

Randgold Resources AngloGold Ashanti Sokimo

Government participation held by way of Sokimo interest

Kibali Health and Safety…

Safety performance…

0

5

10

15

20

25

30

35

0

1

2

3

4

5

6

7

2011 2012 2013

LTI LTIFR

LTIFR LTI

Health…malaria

0

20

40

60

80

100

120

2011 2012 2013

MIR

Health, safety and environment…

2 mine rescue teams trained

3 fire cars arrived on site

New mine clinic completed and X-ray installed

Medical evacuation simulations on-going

Water monitoring programme - improvement in potable water quality

Dust monitoring programme initiated

New waste site identified

GRI Reporting monthly

New nursery and eco centre established

SHE awareness programmes

Malaria vector control - bush clearance and spraying of camps and surroundings continue

Kibali exploration and upside potential…

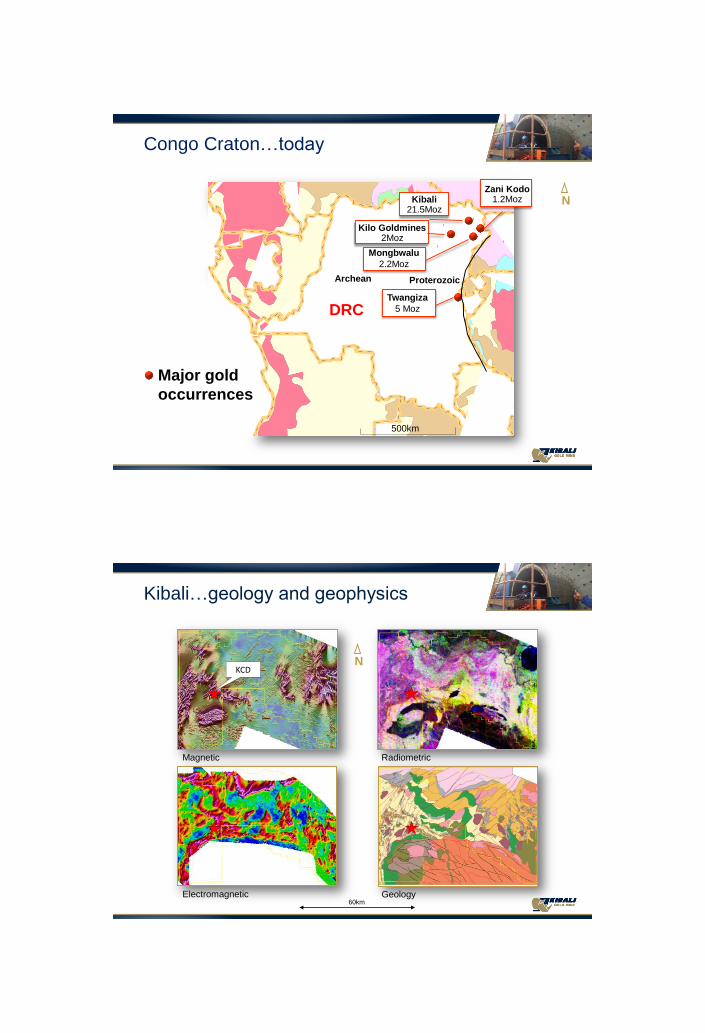

Congo Craton…today

!

!!

!

!

!

!

!

!

Kibali21.5Moz

DRC

500km

ProterozoicArchean

Kilo Goldmines2Moz

Zani Kodo1.2Moz

Mongbwalu

2.2Moz

Twangiza

5 Moz

Major gold

occurrences

N

Kibali…geology and geophysics

Magnetic Radiometric

Electromagnetic Geology

KCDN

60km

Kibali…Geological Model

KCD

3D Looking SW

Durba

9000

5000 3000

NE

NE

East

Transfer

Structure

Examples of S1 foliation being folded (F2) into

‘rods’ and younger crenulation. Develops at all

scales

Intersection lineation is parallel to the long axis

of mineralised lenses of the gold deposits

Kibali…KCD deposit cross sectiongeology and structure

Kibali upside…KCD orebodies

3000 lode –

untested area

for

mineralization

$ 1000 KCD

pit

9000 lode -

Potential

resource

conversion

Phase 2

$ 1000 KCD

pit

$ 1000 Sessenge

pit

9000 lode -

Sessenge open

pit, review

HG

opportunities

5000

$ 1000

Sessenge pit$ 1000 KCD

pit

Phase

2

50 gm /

m100200300

HG

Potential

9000 lode –

ESE trending

HG

opportunities

5000 lode –

down plunge

extension

$ 1000 KCD

pit

5000 lode –

Up plunge Durba

Hill and ESE

extensions

Kibali Upside…brownfields

Mengu Hill

Reserve - 479KozResource outside reserve – 237Koz Resource outside

reserve – 258Koz

Megi

Gorumbwa

Resource outside reserve – 394Koz

KCD Sep 30th 2013

Mengu village

Resource outside reserve – 39Koz

Pakaka

Stockpile - 241Koz Open Pit Reserve – 1,500Koz Open pit resource outside reserve –1,446Koz Underground Reserve – 8,009KozUnderground resource not in reserve –9,351Koz

Kombokolo

Reserve - 91KozResource outside reserve – 54oz

Sessenge

Reserve – 228KozResource outside reserve – 181Koz

Pamao

Reserve - 262KozResource outside reserve – 447Koz

Resource outside reserve – 59Koz

Marakeke

Ndala

Resource outside reserve – 33Koz

Reserve - 741KozResourc e outside reserve – 437Koz

Kibali R.

Nzoro R.

Aru / Arua

Watsa

Dome

Reserve

Resources

Sayi

Mofu

GF Targets

Agbarabo

/ Rhino

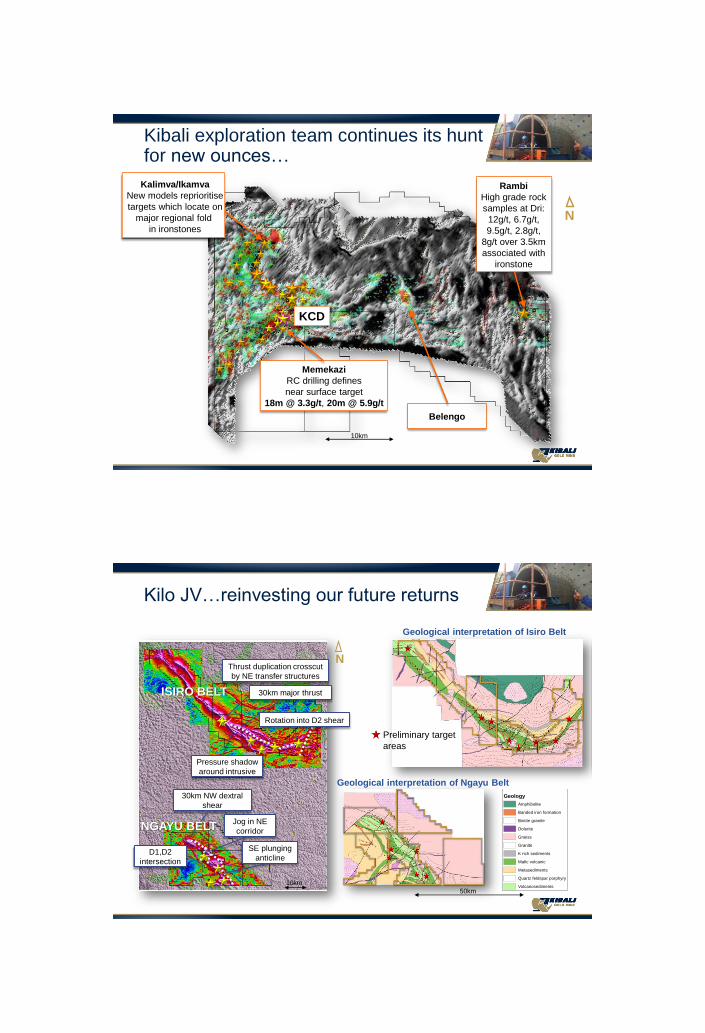

Kibali exploration team continues its hunt for new ounces…

Rambi

High grade rock

samples at Dri:

12g/t, 6.7g/t,

9.5g/t, 2.8g/t,

8g/t over 3.5km

associated with

ironstone

KCD

10km

Memekazi

RC drilling defines

near surface target

18m @ 3.3g/t, 20m @ 5.9g/t

Kalimva/Ikamva

New models reprioritise

targets which locate on

major regional fold

in ironstones

N

Belengo

Kilo JV…reinvesting our future returns

10km

Thrust duplication crosscut

by NE transfer structures

30km major thrust

Rotation into D2 shear

Pressure shadow

around intrusive

SE plunging

anticline

Jog in NE

corridor

30km NW dextral

shear

D1,D2

intersection

Legend

Geology

Amphibolite

Banded iron formation

Biotite granite

Dolerite

Gneiss

Granite

K rich sediments

Mafic volcanic

Metasediments

Quartz feldspar porphyry

Volcanosediments

Geological interpretation of Isiro Belt

Preliminary target

areas

Geological interpretation of Ngayu Belt

ISIRO BELT

NGAYU BELT

50km

N

Kibali mineral resources and reserves …

Kibali mineral resources…Q2 2013

Category Tonnes (Mt) Grade (g/t) Gold (Moz)

Measured

and indicated149 3.6 17

Inferred 52 2.7 4.5

Kibali R.

Nzoro R.

Aru / Arua

Watsa

Dome

Pakaka

16.6Mt @ 2.21g/t, 1.19Moz

Pamao

14.4Mt @ 1.54 g/t, 709koz

Mengu Hill

8.3Mt @ 2.62 g/t, 698koz

Kombokolo

2.1Mt @ 2.1 g/t, 145koz

Sessenge

10Mt @ 1.27 g/t, 409koz KCD

Open pit

38.36Mt @ 2.43 g/t, 2.99Moz

Underground

98.63Mt @ 4.55 g/t, 14.41Moz

Kibali mineral reserves…Q3 2013

Sessenge KCDopen pit

“box cut”

declines

Vertical

shaft 760m

Old Durba

plant

90005000

3000

N

Type Category Tonnes (Mt) Grade (g/t) Gold (Moz)

Stockpile Proven 3.2 2.3 0.2

Open PitsProven and

Probable42 2.5 3.4

Underground Probable 44 5.7 8.0

TotalProven and

Probable89 4.1 12

Kibali Mining…

Kibali KCD Opencast mining…

View of the southern and western limb of the pit

The pit is mining soft sulphide on the southern side

The target is to mine enough sulphide from the pit by end of Q1 for the commissioning of the sulphide circuit.

Kibali opencast mining…

Six pits to be mined over 10 years

KCD pit mining started in July 2012

Production achieved with local trained operators

3 x Liebherr 9350 diggers , 1 x Liebherr 984 digger and 19 x 777G

dedicated to production with a number of auxiliary equipment to support

production

The ore production and plant feed were achieved for the year

Kibali underground mine development…

The underground will consist of:

40Km of Capital lateral development

Expected LOM is 20 years

Vertical ore hosting shaft

Twin decline

Longhole open stope with paste fill

10MW installed refrigeration system with multiple vent raisebore shafts

Capital Footprint of Underground

Boxcut

North Decline

South Decline

West Decline

East Decline

655L Acc

Kibali decline development status…

Positions as of end Q3

Target completion of twin declines for 2013 has been reached

An average of 400m/month of the development was reached with 2 jumbos during the development of the twin decline

Development ore mining and stoping have been brought forward

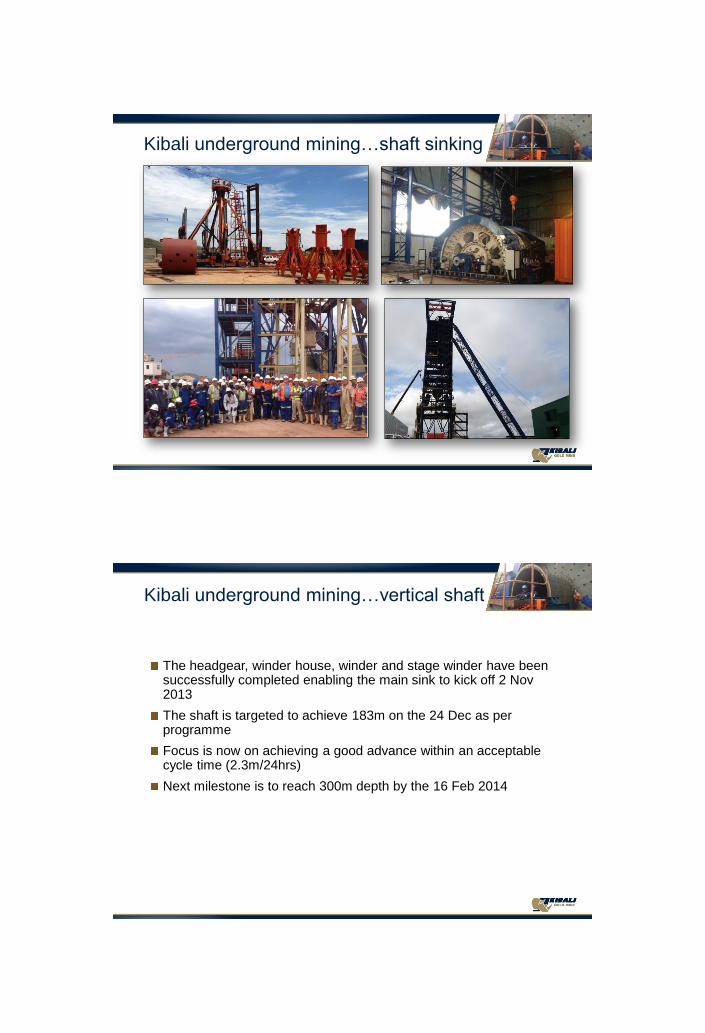

Kibali underground mining…shaft sinking

Kibali underground mining…vertical shaft

The headgear, winder house, winder and stage winder have been successfully completed enabling the main sink to kick off 2 Nov 2013

The shaft is targeted to achieve 183m on the 24 Dec as per programme

Focus is now on achieving a good advance within an acceptable cycle time (2.3m/24hrs)

Next milestone is to reach 300m depth by the 16 Feb 2014

Latest mine design…KCD open pit and underground

Standardised 35m level intervals 5102, 5103 and 9105 lodes

Upgrade of geotechnical model has allowed us to increase the number of large production stope

Mining method of 9105 change from longitudinal to transverse due to increase thickness of the ore

Key changes to mine design since feasibility…

Resource increases due to GC drilling and infill diamond drilling –resulting in larger reserve of 89Mt vs 72Mt in feasibility

Rockmass classification highlights better rock quality allowing for lower ground support costs and larger stopes

UG permeability lower than expected, reducing total pumping requirement from 600l/s to 200l/s

Dedicated refrigeration shaft

SS focus on shaft and BUCS on lateral development

9000 lode adjusted to longitudinal, potentially bringing this lode forward in the mine plan and reducing upfront capital

Brought declinre ore tonnage forward to optimise cashflow before shaft fully commissioned

Further possible optimisation of mine plan…

Up plunge drilling of the 9000 lode – quickly adds more stoping

Satellite pits of Gorumbwa, Aerodrome, Rhino and Mofu give flexibility outside current mine plan

BUCS developing faster than current plan – if they continue we bring the high grade ore forward

Kibali Metallurgical Facility…

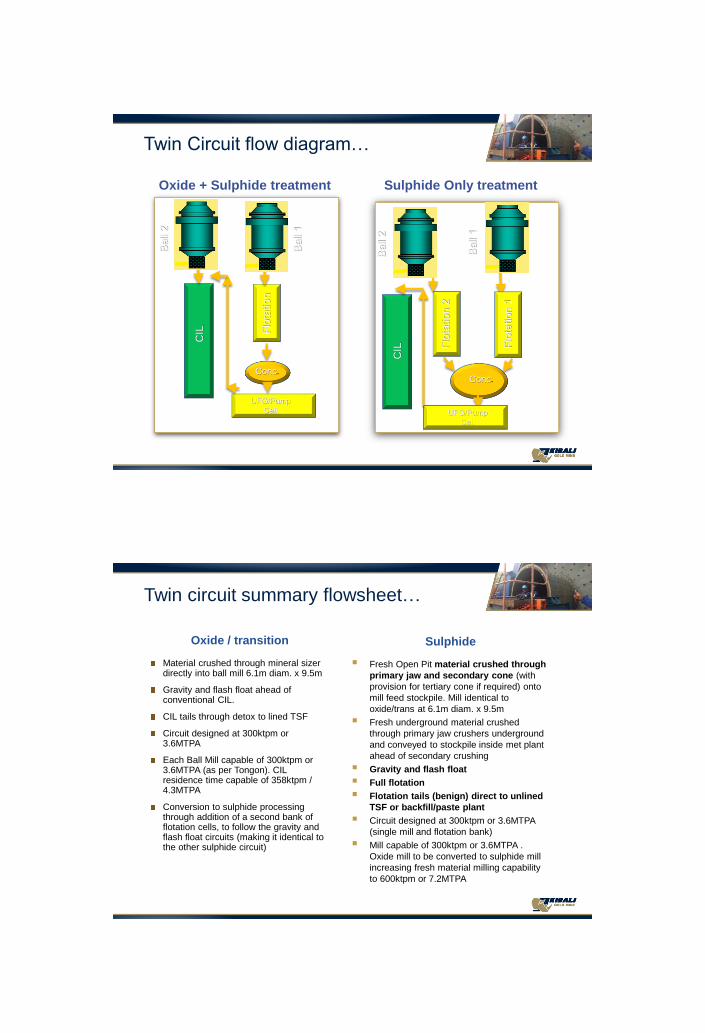

Twin Circuit flow diagram…

CIL F

lota

tio

n

Ball

2

CIL F

lota

tio

n2

Ball

1

Ball

2

Flo

tatio

n1

Conc.

Oxide + Sulphide treatment Sulphide Only treatment

Conc.

Ball

1

UFG/Pump

Cell UFG/Pump

Cell

Twin circuit summary flowsheet…

Material crushed through mineral sizerdirectly into ball mill 6.1m diam. x 9.5m

Gravity and flash float ahead of conventional CIL.

CIL tails through detox to lined TSF

Circuit designed at 300ktpm or 3.6MTPA

Each Ball Mill capable of 300ktpm or 3.6MTPA (as per Tongon). CIL residence time capable of 358ktpm / 4.3MTPA

Conversion to sulphide processing through addition of a second bank of flotation cells, to follow the gravity and flash float circuits (making it identical to the other sulphide circuit)

Fresh Open Pit material crushed through

primary jaw and secondary cone (with

provision for tertiary cone if required) onto

mill feed stockpile. Mill identical to

oxide/trans at 6.1m diam. x 9.5m

Fresh underground material crushed

through primary jaw crushers underground

and conveyed to stockpile inside met plant

ahead of secondary crushing

Gravity and flash float

Full flotation

Flotation tails (benign) direct to unlined

TSF or backfill/paste plant

Circuit designed at 300ktpm or 3.6MTPA

(single mill and flotation bank)

Mill capable of 300ktpm or 3.6MTPA .

Oxide mill to be converted to sulphide mill

increasing fresh material milling capability

to 600ktpm or 7.2MTPA

Oxide / transition Sulphide

Kibali metallurgical facility, generators and sulphide thickeners…

Process commissioning and ramp up…

Oxide Stream…available and commissioned mid Sept 2013

Milling and gravity circuit commissioned and operational

CIL circuit partially completed and available

Concentrate Tailings Facility (CTSF) commissioned enabling the start of deposition

First gold pour from Gravity and Elution Circuit 24.09.2013

Operations and construction managed concurrently

Slow but steady ramp up during the quarter

Throughput rate increased from an average of 219tph in September to 472tph by the end of November 2013;

Mill1 (sulphide) commissioned and put into production 14th December 2013

Plant recovery consistently outperformed the feasibility recovery

Critical dates…metallurgical plant

Construction completion dates:

Phase 1 oxide TSF - Complete

Phase 2 oxide circuit - Complete

Third generator bank - January 2014

Sulphide / float TSF - February 2014

Phase 1 sulphide circuit - February 2014

Phase 2 sulphide circuit - March 2014

Feed sulphide material - Beginning Q2 2014

Phase 2 oxide tailings - Q4 2015

Kibali…5 year forecast production with grade

-

1.0

2.0

3.0

4.0

5.0

-

100

200

300

400

500

600

700

800

2013 2014 2015 2016 2017

Kibali hydropower strategy…

Our power strategy…

Supply concept is a hybrid arrangement

Peak power

Deliver peak power on the available river schemes average flows

Dry season low flow power

Maximize the number of stations supplying to maximize the power available in the low flow periods

Diesel back-up generation

For start-up of shaft winder and Met Plant

Initially provide dry season make-up power from high speed diesel units

Substitute (diesel generation) with smaller hydrostations as overall power demand grows

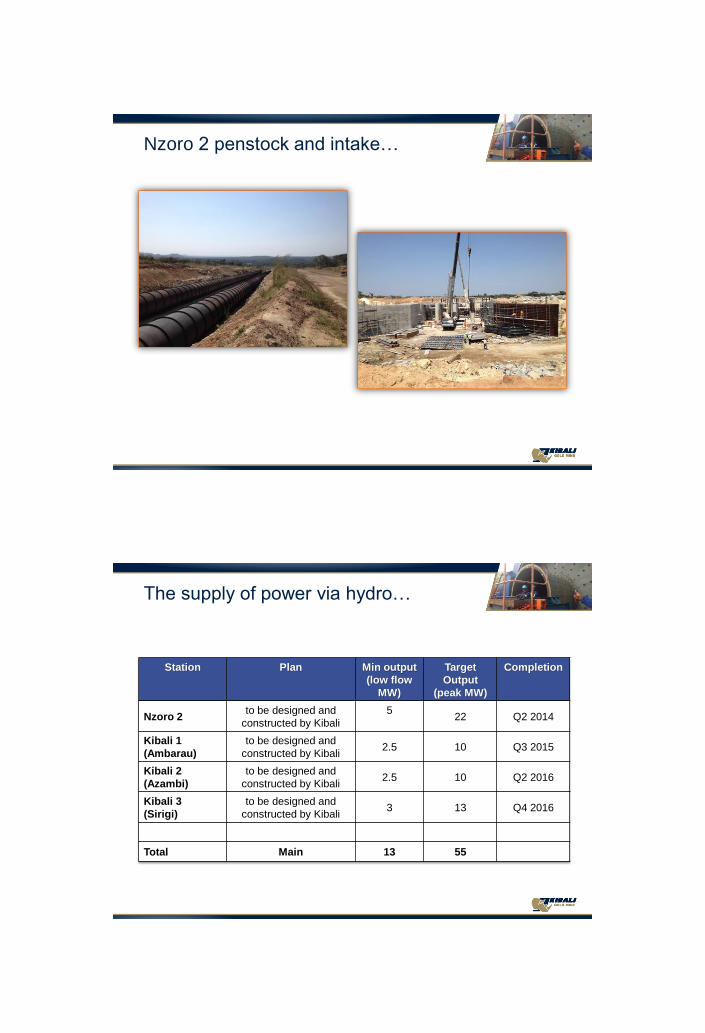

Nzoro 2 penstock and intake…

Station Plan Min output

(low flow

MW)

Target

Output

(peak MW)

Completion

Nzoro 2to be designed and

constructed by Kibali

522 Q2 2014

Kibali 1

(Ambarau)

to be designed and

constructed by Kibali2.5 10 Q3 2015

Kibali 2

(Azambi)

to be designed and

constructed by Kibali2.5 10 Q2 2016

Kibali 3

(Sirigi)

to be designed and

constructed by Kibali3 13 Q4 2016

Total Main 13 55

The supply of power via hydro…

Nzoro 2 turbines during installation…

Kibali hydropower programme…

Projects in progress:

Nzoro 2 hydro station - Complete Q2 2014

Third generator bank - Complete Q1 2014

Ambarau hydro - Complete Q3 2015

Azambi hydro - Complete Q2 2016

Sirigi hydro - Complete Q4 2016

Kibali Capital Programme…

Capital expenditure…

Phase 1 covers the metallurgical facility, one hydropower station and back-upthermal power facility, construction of the tailings storage facility, relocation ofvillages, open pit mining and all shared infrastructure. This is expected to runover a two year period through to Q1 2014

Phase 2 which runs concurrently with Phase 1 but is expected to extend into2016, is focused primarily on the underground development and includes a twindecline and vertical shaft system as well as three hydropower stations. This isexpected to bring the underground into first production by 2014

Phase 1 & 2 2011

Feasibility estimate*

Q3 2013

estimate*

Phase 1 $0.92 bn $1.01 bn

Phase 2 $0.65 bn $0.71 bn

Total $1.57 bn $1.72 bn

*Excluding pre-production expenditure

Kibali operational readiness…

Recruitment, training and operational readiness…

Recruitment and Training

First locally recruited junior plant operators completed in May 2013.

Senior operating staff

Supervisors

Foreman

Process Production Superintendents

Process team (both local and senior) split into two groups and sent for training in Tongon and Morila

Second locally recruited junior operators completed in September 2013

All local operators have been recruited within the locality of Kibali Gold Mine as part of a strategic policy of managing and maintaining KGM social contract. Higher qualified national personnel were recruited in Lubumbashi and Kinshasa (where the skills were not available locally) to fill senior positions.

Process team readiness to operate the plant

Process team back on site for plant startup – 15th August 2013

Complement staff from Randgold mines (Morila, Loulo & Tongon) brought in as

Commissioning support

Enhancement training team for the local operators

Social responsibility…

Kibali social programmes…

RAP

Completion of construction and physical movement of communities

4232 houses build and families moved

2397 graves moved

Smooth transition from end of RAP to construction/production

A communication strategy designed to ensure seamless transition from RAP to start of production

RRL in continuous engagement with community delegates, community leaders and representatives from artisanal miners

13 out of 14 cooperatives now operational and one still in development

Building access to consumer market for farming cooperatives: Nile breweries in Uganda (for Sorghum) and World Food Programme for maize

Social responsibility programmepost RAP…

Community liaison offices deal with grievances from the community

Working on a large scale agriculture initiative - palmoil and others

Plan to transform Kokiza engineering into a development centre

Agriculture

Nursery To generate seeds and saplings

Fish ponds Potential to do cages into Kibali river

Poultry Expanding current quails unit and introduce layers

Maize Sheller 2 machines with capacity of 2 T an hour

Storage Safe for storage of crops

Processing

Honey and peanut processing

unit

Packaging and bottling of honey and peanuts, production of

candles and local alcohol

Maize mills Production of floor

Business

Sewing project Targeting resettled disables to be empowered with sewing skills

Hosting of micro-finance

project

Hold auctions, store items, run classes for higher phase winners

Headquarter of co-ops Meeting/training hall , serve as offices and admin for cooperatives

and community development schemes

Community post RAP …

Stakeholders engagement and community development

Consultation continues through meetings

Big drive on waste management and public health awareness

Training and capacity building through the Community development forum to ensure transition from RAP into community development

Hand over of two 40 feet containers of medical equipment received from CURE

Tied financing project: 2 more auctions held, increased interest from community

Various local economic development initiatives started: e.g.. Tender for camp maintenance in progress

Challenges

Slow ownership of resettlement site by residents and local admin

Very high expectations from people/officials on all levels

Continuous challenge of illegal mining on license area

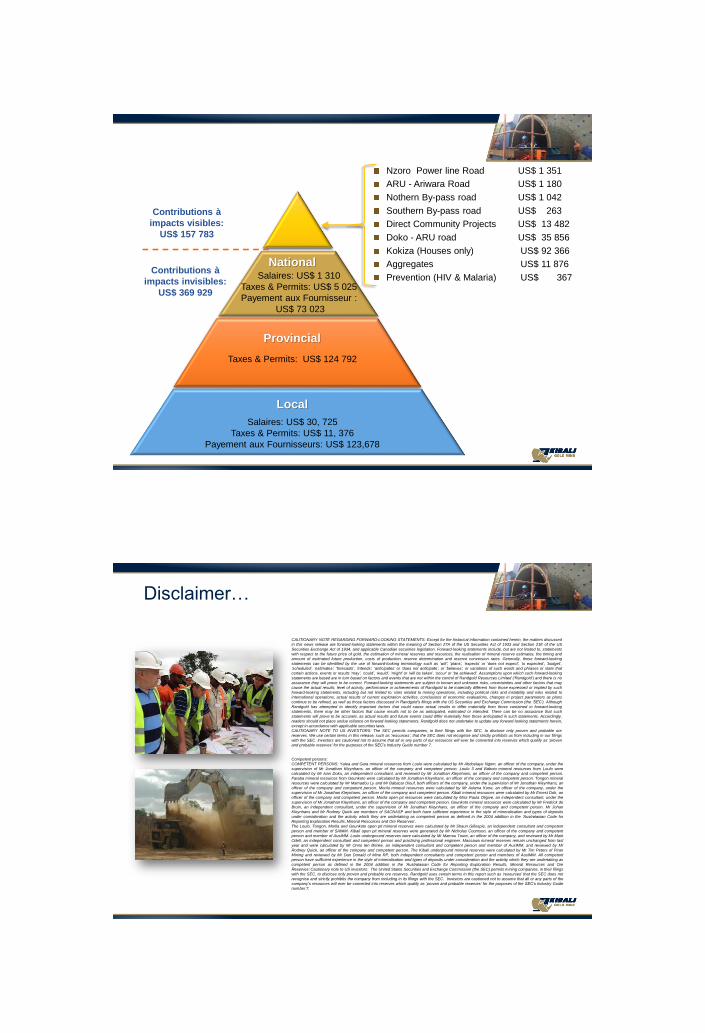

Contributions à

impacts visibles:

US$ 157 783

Contributions à

impacts invisibles:

US$ 369 929

Salaires: US$ 1 310

Taxes & Permits: US$ 5 025

Payement aux Fournisseur :

US$ 73 023

Taxes & Permits: US$ 124 792

Salaires: US$ 30, 725

Taxes & Permits: US$ 11, 376

Payement aux Fournisseurs: US$ 123,678

National

Provincial

Local

Nzoro Power line Road US$ 1 351

ARU - Ariwara Road US$ 1 180

Nothern By-pass road US$ 1 042

Southern By-pass road US$ 263

Direct Community Projects US$ 13 482

Doko - ARU road US$ 35 856

Kokiza (Houses only) US$ 92 366

Aggregates US$ 11 876

Prevention (HIV & Malaria) US$ 367

Disclaimer…

Competent persons:

COMPETENT PERSONS: Yalea and Gara mineral resources from Loulo were calculated by Mr Abdoulaye Ngom, an officer of the company, under the

supervision of Mr Jonathan Kleynhans, an officer of the company and competent person. Loulo 3 and Baboto mineral resources from Loulo were

calculated by Mr Ivan Doku, an independent consultant, and reviewed by Mr Jonathan Kleynhans, an officer of the company and competent person.

Faraba mineral resources from Gounkoto were calculated by Mr Jonathan Kleynhans, an officer of the company and competent person. Tongon mineral

resources were calculated by Mr Mamadou Ly and Mr Babacar Diouf, both officers of the company, under the supervision of Mr Jonathan Kleynhans, an

officer of the company and competent person. Morila mineral resources were calculated by Mr Adama Kone, an officer of the company, under the

supervision of Mr Jonathan Kleynhans, an officer of the company and competent person. Kibali mineral resources were calculated by Mr Ernest Doh, an

officer of the company and competent person. Morila open pit resources were calculated by Miss Paula Oligive, an independent consultant, under the

supervision of Mr Jonathan Kleynhans, an officer of the company and competent person. Gounkoto mineral resources were calculated by Mr Fredrick de

Bruin, an independent consultant, under the supervision of Mr Jonathan Kleynhans, an officer of the company and competent person. Mr Johan

Kleynhans and Mr Rodney Quick are members of SACNASP and both have sufficient experience in the style of mineralisation and types of deposits

under consideration and the activity which they are undertaking as competent person as defined in the 2004 addition in the ‘Australasian Code for

Reporting Exploration Results, Mineral Resources and Ore Reserves’.

The Loulo, Tongon, Morila and Gounkoto open pit mineral reserves were calculated by Mr Shaun Gillespie, an independent consultant and competent

person and member of SAIMM. Kibali open pit mineral reserves were generated by Mr Nicholas Coomson, an officer of the company and competent

person and member of AusIMM. Loulo underground reserves were calculated by Mr Mamou Toure, an officer of the company, and reviewed by Mr Mark

Odell, an independent consultant and competent person and practising professional engineer. Massawa mineral reserves remain unchanged from last

year and were calculated by Mr Onno ten Brinke, an independent consultant and competent person and member of AusIMM, and reviewed by Mr

Rodney Quick, an officer of the company and competent person. The Kibali underground mineral reserves were calculated by Mr Tim Peters of Piran

Mining and reviewed by Mr Dan Donald of Mine RP, both independent consultants and competent person and members of AusIMM. All competent

person have sufficient experience in the style of mineralisation and types of deposits under consideration and the activity which they are undertaking as

competent person as defined in the 2004 addition in the ‘Australasian Code for Reporting Exploration Results, Mineral Resources and Ore

Reserves’.Cautionary note to US investors: The United States Securities and Exchange Commission (the SEC) permits mining companies, in their filings

with the SEC, to disclose only proven and probable ore reserves. Randgold uses certain terms in this report such as ‘resources’ that the SEC does not

recognise and strictly prohibits the company from including in its filings with the SEC. Investors are cautioned not to assume that all or any parts of the

company’s resources will ever be converted into reserves which qualify as ‘proven and probable reserves’ for the purposes of the SEC’s Industry Guide

number 7.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS: Except for the historical information contained herein, the matters discussed

in this news release are forward-looking statements within the meaning of Section 27A of the US Securities Act of 1933 and Section 21E of the US

Securities Exchange Act of 1934, and applicable Canadian securities legislation. Forward-looking statements include, but are not limited to, statements

with respect to the future price of gold, the estimation of mineral reserves and resources, the realisation of mineral reserve estimates, the timing and

amount of estimated future production, costs of production, reserve determination and reserve conversion rates. Generally, these forward-looking

statements can be identified by the use of forward-looking terminology such as ‘will’, ‘plans’, ‘expects’ or ‘does not expect’, ‘is expected’, ‘budget’,

‘scheduled’, ‘estimates’, ‘forecasts’, ‘intends’, ‘anticipates’ or ‘does not anticipate’, or ‘believes’, or variations of such words and phrases or state that

certain actions, events or results ‘may’, ‘could’, ‘would’, ‘might’ or ‘will be taken’, ‘occur’ or ‘be achieved’. Assumptions upon which such forward-looking

statements are based are in turn based on factors and events that are not within the control of Randgold Resources Limited (‘Randgold’) and there is no

assurance they will prove to be correct. Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that may

cause the actual results, level of activity, performance or achievements of Randgold to be materially different from those expressed or implied by such

forward-looking statements, including but not limited to: risks related to mining operations, including political risks and instability and risks related to

international operations, actual results of current exploration activities, conclusions of economic evaluations, changes in project parameters as plans

continue to be refined, as well as those factors discussed in Randgold’s filings with the US Securities and Exchange Commission (the ‘SEC’). Although

Randgold has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking

statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such

statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly,

readers should not place undue reliance on forward-looking statements. Randgold does not undertake to update any forward-looking statements herein,

except in accordance with applicable securities laws.

CAUTIONARY NOTE TO US INVESTORS: The SEC permits companies, in their filings with the SEC, to disclose only proven and probable ore

reserves. We use certain terms in this release, such as ‘resources’, that the SEC does not recognise and strictly prohibits us from including in our filings

with the SEC. Investors are cautioned not to assume that all or any parts of our resources will ever be converted into reserves which qualify as ‘proven

and probable reserves’ for the purposes of the SEC’s Industry Guide number 7.