should there be lower taxes on patent income? · should there be lower taxes on patent ... sullivan...

TRANSCRIPT

Should there be lower taxes on patent income?

IFS Working Paper W18/19 Fabian GaesslerBronwyn H. HallDietmar Harhoff

1

Shouldtherebelowertaxesonpatentincome?

FabianGaessler,*BronwynH.Hall,†andDietmarHarhoff‡

July2018

Abstract

A“patentbox”isatermfortheapplicationofalowercorporatetaxratetotheincomederivedfromtheownershipofpatents.Thistaxsubsidyinstrumenthasbeenintroducedinanumberofcountriessince2000.UsingcomprehensivedataonpatentfilingsattheEuropeanPatentOffice,includinginformationonownershiptransferspre‐andpost‐grant,weinvestigatetheimpactoftheintroductionofapatentboxoninternationalpatenttransfers,onthechoiceofownershiplocation,andoninventionintherelevantcountry.Wefindthattheimpactontransfersissmallbutpresent,especiallywhenthetaxinstrumentcontainsadevelopmentconditionandforhighvaluepatents(thosemostlikelytohavegeneratedincome),butthatinventionitselfisnotaffected.Thiscallsintoquestionwhetherthepatentboxisaneffectiveinstrumentforencouraginginnovationinacountry,ratherthansimplyfacilitatingtheshiftingofcorporateincometolowtaxjurisdictions.

JELcodes:H32,H34,K34,O34

Keywords:patentbox,IPbox,innovationtax,BEPS,EPO,inventionincentive,patentownership

Acknowledgements:WewouldliketothankseminaraudiencesattheOECD,theMannheimTaxSummerSchool2017,theINNOPAT2017Conference,HarvardBusinessSchool,andthe72ndAnnualCongressoftheInternationalInstituteofPublicFinance(LakeTahoe)forhelpfulcomments.ParticularthanksgotoJostHeckemeyer,DeborahSchanz,JoelSlemrod,MehmetTosun,andAlfonsWeichenrieder.

*MaxPlanckInstituteforInnovationandCompetition,Munich.†MaxPlanckInstituteforInnovationandCompetition,Munich,UniversityofCaliforniaatBerkeley,NBER,andIFS‐London.‡MaxPlanckInstituteforInnovationandCompetition,Munich.

2

1. Introduction

Duringthepast15yearsseveralcountrieshaveintroducedspecialtreatmentforthetaxationofcorporateincomethatderivesfromtheownershipofpatentsor,insomecases,otherIP.Thispolicyinstrument(oftencalleda“patentbox”)isgenerallyintendedtoencouragethelocationofinnovativeactivitybymultinationalsinthecountrythatintroducesit.However,manyeconomistsandotheranalystshaveexpressedskepticismaboutitseffectiveness,giventhemultipleavenuesavailabletosuchcompaniesfortheshiftingofincomeassociatedwithintangibleassets(Griffithetal.2014;Sullivan2015).Thepatentboxcreatesanothersuchavenueforshiftingincome,becausetransferringownershipofapatentfromonecountrytoanotherthathasmorefavorabletaxtreatmentisastraightforwardandrelativelylowcostprocedure.

GiventhewidespreaduseofR&Dtaxcreditstoincentivizeinnovativeactivity,onemaywellaskwhethertheadditionofapatentboxisnecessaryorworthwhile.ClearlytherearedifferencesbetweensubsidizingR&Dandsubsidizingtheincomefrompatents:thefirstisanexanteincentivethattargetsadecisionvariableofthefirm,whereasthesecondisexpostandwillonlybeusedwhenR&Dhasbeeninsomesensesuccessful.Klemens(2016)pointsoutanumberofwaysinwhichanexanteincentivemaybemoredesirable.Theseincludefewerincentivesforshiftingexpensestothehighertaxratearea,difficultiesinallocatingincometothepatent,andlessdistortiontowardsincrementaldevelopmentthatgeneratesincomeonthewholeproductversusinventionofacompletelynewproduct.TothisonecouldaddthatapatentboxprovidesanextraincentiveforthekindofR&Dthatleastneedsencouragement:R&Dwhosereturnsareappropriableviathepatentsystem.IftheargumentforsubsidizingR&Dandinnovativeactivitiesisthattheycreatespilloversandpublicgoodsintheformofknowledge,itseemsoddtoencouragefirmstodirecttheireffortstowardpatentableinventions.

AmoresubstantivedifferencebetweenR&DtaxincentivesandpatentboxesisthatR&Dcoversalimitedrangeofinnovativeactivitiesthataremoreorlesstechnological,andsomesuccessfulpatentedinnovationsarelikelytocomefromotheractivities,especiallyintheservicesector.Ontheotherhand,alimitationofthepatentboxisthatitrequiresapatentorpatentsandsomedesirableinnovativeactivitiesmaynotbepatentable.Afinalobjectionisthatencouragingfirmstopatentsolelyinordertoreceiveataxsubsidyisperverseinanenvironmentwheretheremayalreadybetoomanypatents,inthesensethatsomeofwhichwouldbefoundinvalidifchallenged(USFTC2016andreferencestherein).AsKlemens(2016)says,“Thepatentboxthusgivesnewlifetozombiepatents,”bywhichhemeanspatentsthatwouldnotsurviveifchallenged.1

Oneofthewaysinwhichthepatentboxmayinducenonproductivecorporatebehavioristhatitmayencouragefirmstotransfersomeoralloftheirpatentstojurisdictionsthatofferfavorabletaxtreatmenttoincomederivedfrompatents.InthispaperweinvestigatetheextenttowhichthishashappenedfollowingtheintroductionofapatentboxinseveralEuropeancountries.Welookcloselyatthreequestions:

1Presumablythetaxauthoritieswouldnotwanttogetintothebusinessofchallengingpatentboxpatentsforvalidity.

3

1. Whenatransferofpatentownershipoccursbetweencountries,isthechoiceoftargetcountryaffectedbythedifferenceintaxtreatmentinthetwocountriesandthepresenceofapatentbox?Thatis,werelatetheprobabilityofanownershiptransfertothedifferenceinthemarginaltaxratesfacedbycorporateincomegeneratedbypatentsinthetwocountries.

2. Isthechoiceofprioritycountryinfluencedbythatcountry’streatmentofpatentincome?Wearemotivatedtosomeextentbytheobservationthattheshareofpatentswithaprioritycountrythatdiffersfromthelocationoftheinventionhasrisenintherecentpast.

3. Doespatentableinventioninacountryincreaseaftertheintroductionofapatentbox?Thatis,doesthispolicyinstrumenthavethedesiredeffect?

Inaddition,wehypothesizethatmorevaluablepatents(thatis,patentsthataremorelikelytogenerateincome,viaownprofitsorlicensing)aremorelikelytobesubjecttotransfer.

Toexaminethesequestions,weuseanewdatasetcreatedbyGaesslerandHarhoff(2018)thatcontainsallregisteredpatentownershipinformationchangesofpatentsgrantedorvalidatedinGermanybetween1981and2014.GiventhehighGermanvalidationandrenewalrates,thisdataseteffectivelycapturesallpatenttransfersinEuropeduringtheperiodandwefocusouranalysisonthetransfersofgrantedEuropeanpatents(whichwillalsobeGermanpatentswithveryhighprobability).WecombinethesedatawithpatentdatafromPatstat(April2017edition)anddetaileddataonthevariouspatentboxmeasuresthathavebeenintroducedinEuropeancountriesduringthepasttwodecades.Usingthesedata,welookattheimpactofcorporatetaxesandthepatentboxontwochoices:whethertotransferpatentsacrosscountriesandwhethertochooseaprioritycountryforpatentingthatdiffersfromthecountryofinventorresidence.Wearguethatthelatterchoicemaybedrivenbyapreferencetopatentinacountrywithfavorabletaxtreatmentofpatentincome.Weperformbothanalysesattheaggregate(country)levelandalsoatthelevelofindividualpatents,wherewearealsoabletousepatentcharacteristicstoexaminewhichpatentsaretransferred.Inaddition,welookatwhetherthepresenceofapatentbox(andthereforeanimplicitsubsidytoinnovation)increasesinventiveactivityinacountry.

2. Taxtreatmentofinnovation

Duringthepastdecades,anumberofcountrieshaveintroducedarangeofpoliciesdesignedtoencourageinnovativeactivitybyfirmsresidentinthecountry.Thispolicyfocushasbeendrivenbyincreasedawarenessoftheimportanceofinnovationforeconomicgrowthandargumentsthatfirmslefttotheirowndeviceswouldnotinvestenoughininnovationfromsociety’spointofview(Westmore2013).Amongthesepoliciesareseveralthatmakeuseofthetaxsystem.TheoldestimplicitsubsidyiswidespreadduetobeingincorporatedinstandardaccountingpracticessuchastheUSGenerallyAcceptedAccountingPrinciples(GAAP)2andvariousInternationalAccountingStandardsBoard(IASB)standards:3R&Disgenerallyexpensed,whichcorrespondstoaccelerateddepreciationgivenitseconomiclife(Hall2005,interalia).Inadditiontothis,anumberofcountrieshaveintroducedanR&DtaxcreditthatprovidesareductioninthecostofperformingR&D.For2http://www.fasb.org/home

3https://www.iasplus.com/en/resources/ifrsf/iasb‐ifrs‐ic/iasb

4

detailsonthistaxinstrument,seevariouspublicationsbytheOECD4andforevidenceonitseffectiveness,seeHallandVanReenen(2000)andAppeltetal.(2016).AppendixTableA1indicateswhichofthecountriesinoursamplecurrentlyhavesomekindofR&Dtaxcredit.

Inoursampleof51countries(thelistisshowninAppendixTableA1),thereare13thathaveintroducedsomekindofIPorpatentboxbetween1971and2014,andone(Ireland)thathasdiscontinuedit.5ThepotentialeffectivenessofanIPorpatentboxdependsonitsdesign,andonitsinteractionwiththerestofthecorporatesystem.Thismakestheanalysisofitseffectssomewhatchallenging,asthesamplesizeisrathersmallonceallthedesignfeaturesarecontrolledfor.Evers,MillerandSpengel(2014)andAlstadsæteretal.(2018)reviewtheprovisionsoftheregimeforthe13countries.Thefactthatthesereviewsdonotalwaysagreepreciselyastothedetailsofthepatentboxindicateshowcomplextheinstrumentcanbe.Theimportantdistinctionsarethefollowing:

1. Coverage–insomecases,allformsofintellectualpropertyincomearecovered,ratherthansimplypatents.Thiscouldincludesoftware,copyrights,trademarks,utilitymodels,andeventradesecretsaswellasknow‐howinafewcases.Thereisalsovariationincoverageoverroyaltiesfromothers’useofthefirm’sIPandcapitalgainsfromtheirsale.

2. Grossornetincome–Belgium,Hungary,andPortugalallowIP‐relatedexpensestobedeductedfromordinaryincome,whichisasubstantialtaxadvantage.MostschemesrequiretheseexpensestobedeductedandthereducedtaxrateappliedtothenetincomefromIP.

3. ExistingIP–schemesvaryinwhethertheycoverexistingpatentsoronlythosenewlyobtained,insomecasesrequiringfurtherdevelopmentoftheIPwithintherelevantcountry.

4. AcquiredIP–similarly,thereisvariationinthecoverageofIPacquiredfromothers,andinwhetherthereisafurtherdevelopmentrequirement.

Becauseofthefearthattheintroductionofpatentboxeswouldleadtowastefultaxcompetitionamongcountrieswithoutaconcomitantincreaseininnovativeactivity,theOECDBaseErosionandProfitShifting(BEPS)projectrecommendedin2015thattherebealocaldevelopmentrequirementforthepatenttobeeligible.BEPSreferstosucharequirementasa“nexus”requirement,thatis,arequirementforsignificanteconomicpresenceinthecountry.InthecaseoftheIPorpatentbox,thisisinterpretedasrequiringsomefurtherdevelopmentinthecountryinquestionfortheincomeassociatedwiththepatenttobeeligibleforareducetaxrate.Although2015islaterthantheperiodwestudyhere,severalcountriesinoursamplealreadyhadsuchafurtherdevelopmentrequirementifincomefromthepatentwastobeeligible:Belgium,Spain,theUK,theNetherlands,andPortugal.

Anotherfeatureofmanytaxsystemsthatwillaffecttheabilityofmultinationalstousepatentboxestoreducetheirtaxburdenaretherulesrelatedtocontrolledforeigncompany(CFC)income

4http://www.oecd.org/sti/rd‐tax‐stats.htm

5TheIrishpatentboxwasdiscontinuedaspartofthenationalrecoverybillfollowingthe2008crisis.Anew“knowledgebox”thatiscompliantwithOECD’sBEPS(BaseErosionandProfitShifting)wasintroducedin2015,afteroursampleends.Seehttp://www.oecd.org/tax/beps/formoreinformationonBEPSpolicies.

5

(Deloitte2014).Theserules,whicharecommoninlargedevelopedeconomies,requirethatifaforeigncompanyis50%ormoreownedbyadomesticcompany,itsincomeshouldbetaxedatthedomesticcompanyrateiftheforeigntaxrateislessthanthedomestictaxratebysomeamount.Thecutoffvariesbycountry,butitisusuallybetweenhalfandthreequartersofthedomesticrate.TherulessurroundingtheCFCregimescanbeverycomplex,specifyingtypesofincomeaffected,ownershiprules,etc.TwothingsregardingtheCFCrulesareworthnoting:First,whenacountryhasaCFCregime,therulesusuallyproduceablacklistthatcontainsallofthe“taxhavens”inoursample,attheveryleast.Second,followingaCourtofJusticeoftheEuropeanUniondecisionin2006,theserulescannotbeappliedwithintheEuropeanEconomicArea(EU28plusNorway,Iceland,andLiechtenstein).Bräutigametal.(2017)containsausefuldiscussionofhowthisimpactedtheIPboxes.MuttiandGrubert(2009)explainhowanMNCcanmitigatetheimpactoftheUSCFCrules.

3. Literaturereview

Overthepastyears,aconsiderablenumberofcontributionshavestudiedtherelationshipbetweentaxationandpatentsempirically.Asmallernumberhavefocusedspecificallyontheimpactofapatentboxonthelocationofpatents.Almostnonehaveexaminedotherconsequencesofthepatentbox.Inthissectionwerevieweachofthesegroupsofstudies.Tables1aand1bprovideanoverviewoftheempiricalstudiesthatwefounddirectlyrelevanttothestudyofpatentboxes.Theseanalysesdifferalonganumberofdimensions.Themajorityhavebeendoneatthefirmlevel,andafewatthecountryorpatentlevel.Twolookwithinfirmorcountryatthedifferencesacrosstechnologies.Theyearscoveredaregenerallywithinthe1995‐2015period,whichistheperiodwhenmostoftheIPboxeshavebeenintroduced.Therearerelativelyfewpapersthatincorporateapatentboxintotheanalysisandtheresultsaresomewhatmixed,althoughgenerallypositivebothforthelocationofpatents,andforR&D.Wereviewaselectionofthemostrelevantpapersinthissectionofthepaper.

6

Table1a:Literatureoncorporatetaxationandpatentlocation

CorporatetaxationandpatentliteratureThefirstgroupofpapersfocusesontheimpactofcorporatetaxationsystemsonthefirm’schoiceofpatentsystemandfilinglocation.KarkinskyandRiedel(2012)areamongthefirsttostudypatentfilingbehaviorofmultinationalenterprises(MNEs)withrespecttotaxdifferences.GiventhatpatentsaccountforasizableshareoftheassetvalueofatypicalMNEandthattransfersoftheseassetsaredifficultfortaxauthoritiestoobserveandmonitor,theyrepresentamajoropportunityforprofitshiftingacrosstaxjurisdictions.Hence,MNEsshouldhavestrongincentivestolocatetheownershipofpatentsinalow‐taxcountryandmayevenhaveincentivestolocatethecreationoftheassociatedinventioninthesamecountry,assumingthatthelocusofcreationcanbeshiftedeasily.6Ifshiftingthecreationandownershipofpatentsisnotconstrained,thencorporatepatentingshouldbemorelikelytheloweristhecorporatetaxrate.Moreover,astheseauthorspointout,inhigh‐taxcountriesthesefirmsmaybemorelikelytousetradesecrecy,becausethereisnotaxadvantagetohavingclearlyidentifiableroyaltyincomefrompatents.7Thiswouldagainimpactthenumberofpatentsfiledwhentaxratesarehigh.Astheypointout,theabsolutelevelof6ForasurveyofevidenceonR&Dlocationchoice,seeHall(2011).

7Theargumentwithrespecttotradesecretsisfairlyweak,becausetherearecountervailingeffectssuchasthedangeroflosingsecrecyifthetradesecretisspreadtoother(evenmultiple)taxlocations.Inparticular,ifthetechnologyistobeusedinmultiplesites,therewouldbeatendencytowardspatentinginordertohavebetterlegalrecourse.Therearealsosubstantialdifferencesintradesecrecylegislationacrosscountries.

Paper Data Level #Obs Years Obs/yearDependent

variable(s)Independent variables Method

Dischinger &

Riedel (2011)

European MNEs

with intang.

group

member6,223

1995‐

2005566

intangible

assets (D and

log ratio to

sales)

corp tax rate, tax diff btwn sub

and parent, log sales, pop, R&D,

GDP, growth in GDP per cap,

corruption index, unemployment

logit FE; OLS FE;

IV and GMM on

first differences

Ernst & Spengel

(2011)

EP apps;

AMADEUS

match

firm 80,4841998‐

20078,048 EP patent fi l ings

corp tax, EATR, B‐index, GDP per

cap, pubRD, Tertiary ed, GP

index, Openness, Hi tech exports,

Emply, assets

logit FE ; neg bin

FE

Karkinsky &

Riedel (2012)

EP apps;

AMADEUS

match; 18 EU

countries

firm affi liate 64,0611995‐

20037,118 EP patent fi l ings

corp tax rate, tax diff btwn sub

and parent, royalty rate, CFC

rules, R&D, GDP,corruption

index, IP strength

OLS FE

Griffith, Miller

& O'Connell

(2014)

EP apps;

AMADEUS

match; 18 EU

countries

patent 379,8491985‐

200518,088

fil ing country

choice

GDP, RD/GDP, inventor presence,

tax rate, patent box rate, IP

strength, industry‐location‐firm

size dummies

random

coefficient

mixed logit

Boehm,

Karkinsky,

Knoll, & Riedel

(2015)

EP apps ‐

corporate;

match to

AMADEUS

patent 530,8051978‐

200618,304

applicant/invent

or divergence at

pat level

corp tax rate, pat quality, rule of

law, corruption, GDP and GDP

per cap; CFC; year country

industry FE

probit FE

Dinkel & Schanz

(2015)

worldwide

patstat ‐ MNEs

matched to

AMADEUS

group‐

country62,717

2005‐

20127,840

D(pat abroad)

D (country)

N pats in

country

Tax attractiveness (corp tax rate,

royalty rate, witholding roy rate,

all scaled); D(RD tax), D(transfer

price), CFC, sales, GDP, RD per

cap, distance, app‐reg, emp‐

inventors

probit FE (ind &

year)

neg bin FE

Dudar, Spengel

& Voget (2015)

royalty

payments

country

pairs~20,000

1990‐

2012

~900

~60

countries

royalty streams

royalty tax, tax difference,

corporate tax, IP box dummies,

CFC rules, TP rules, R&D, GDP,

POP in recipient country, trade

between

Poisson PML

7

taxtariffsmaynotbedecisiveasfirmswilloptimizepatentingwithintherangeoftaxsystemstheyareoperatingin.Hence,thedifferencesbetweentaxtariffsacrossthecountriesinwhichafirmisoperatingshouldbeanimportantdeterminantofthelocationofpatenting.Moreover,thelocationrationalemayalsobeaffectedbywithholdingtaxesonroyaltypaymentsforpatentuseandalsobyControlledForeignCompany(CFC)rules,whichtypicallyallowforrecaptureoftaxonpassiveincomegeneratedindesignatedtaxhavencountries(Griffithetal.2014,Boehmetal.2015).Theycontrolfortheserulesintheempiricalexercise.

KarkinskyandRiedelmatchPATSTATpatentdata(October2007version)toinformationonownershipstructureswithinMNEscompiledbyBureauvanDijkintheAMADEUSdata‐base.Thematcheddatacomprisespatentapplicationsfiledbyfirmsfrom18Europeancountries:Belgium,CzechRepublic,Denmark,Finland,France,Germany,Greece,Ireland,Italy,Luxembourg,Netherlands,Norway,Poland,Portugal,Spain,Sweden,Switzerland,andtheUnitedKingdom.Theireconometricspecificationfocusesonthetaxdeterminantsofthepatentapplicationcountbyamultinationalaffiliateiinyeart.AscontrolstheyuselogGDP,lognumberofresearchersintherespectivecountry,indicatorsforthestrengthofpropertyrights(GinarteandPark2007),forthelackofcorruptionandlognumberofemployeesoftheaffiliate.Byusingpanelestimators,theycancontrolforaffiliateandyearfixedeffects.Theresultssuggestthatthecorporatetaxrate(relativetothetaxratesofothergroupmembers)impactspatentapplicationsfiledbyamultinationalaffiliatenegatively.Theeffectisrelativelylargeandappearstoberobusttoanumberofchecks.Invariousspecifications,theresultsindicatethatanincreaseinthecorporatetaxrateofonepercentisassociatedwithareductioninthenumberofpatentapplicationsof3.5%to3.8%.

Boehmetal.(2015)addtotheunderstandingofthepatentlocationdecisionbystudyingthedivergencebetweeninventorandapplicantcountryusingfilingdatafromtheEPOfor1990‐2007.TheystudythedecisiontofileapatentforaninventionthatwasmadeinanEUorOECDcountryinadifferentcountryasafunctionofpatentqualityandtheapplicantcountrytaxrate,aswellastheprobabilitythathigherqualitypatentsarethoseappliedforfromtaxhavencountries.Theyshowthatlow‐taxcountriestendtoattractforeign‐ownedpatentsandthathigh‐taxcountriesaremorelikelytofiletheirpatentsintaxhavencountries,especiallyifthepatentsareof“highquality”bytheusualmeasures.Lowtaxcountriesincludevariousislandtaxhavens,Ireland,Liechtenstein,Luxembourg,andSwitzerland.Theeffectsarerelativelysmallbutsignificant,andarereducedslightlyinthecasewheretheinventorcountryhasimplementedCFCrules.Notethatalthoughtheydistinguishbetweentaxhavensandothercountriesasapplicantlocations,theydonotanalyzethefulldestinationchoicedecision.

Incontrasttotheaboveanalysis,Griffithetal.(2014)areabletodistinguishamongdifferentlocationchoicesforthepatentapplicationbyusingarandomcoefficientslogitmodeltostudyafirm’sdecisionaboutthelocationofpatentownership.Theowneraffiliatecancontract(exante)withtheinventorlocationforR&Dservices,beartheriskoftheR&Dprocessandretainownershipofitsoutput.RightstotheuseofthepatentedinventionarethenlicensedtotheR&D‐performingandotheraffiliatesinexchangeforlicensingfees.Griffithetal.modelthequasi‐rentthattheparentfirmgetsfromselectingaparticularlocationforownershipasafunctionofthetaxrate,thequalityoftheidea,thestrengthofIPrightsintherespectivecountry,thesizeofthelocalmarket,andthe

8

levelofinnovativenessofthecountryinwhichownershipofthepatentresides.Theeconometricmodelisamixedlogit,wherelocationchoicecanalsobeallowedtodependontheunobservedcharacteristicsoftheideaandthelocation.Thefirm’staxrateisnotonlyaffectedbytimeandtargetcountry,butalsobyitshomelocation,sinceControlledForeignCompany(CFC)rulesintroduceaninteractionbetweenthetargetandthehomecountry.Theauthorsusedataonthestatutorycorporatetaxrate(whichisarguedtobeclosetotheeffectivetaxrate)andtheirsampleconsistsofabout1,000ofthelargestpatentingfirmsattheEPOduringtheperiod1985to2005,coveringabout70%ofcorporatepatentapplications.

Aparticularadvantageofthiseconometricsetupisthecomputationofcountry‐specifictaxelasticities.Forexample,theauthorsestimatethattheshareofpatentslocatedinLuxembourghasasemi‐elasticityof3.9%withrespecttothetaxrate,whileGermanyhasamuchloweroneof0.5%.Ingeneral,ownsemi‐elasticitiesaremorepronouncedforsmallerthanforlargercountries.Theauthorsprovideresultsforasimulationexerciseinwhichtheintroductionofpatentboxesisconsidered.Theyfindthatwhilepatentboxesattractpatentincome,theyalsoleadtoasubstantialreductionintaxrevenues.Countriesthatintroducepatentboxesinthetimeperiodconsideredattractmorenewpatents,buttheincreasedshareofpatentfilingsisnotsufficienttooutweightheeffectofthelowertaxrate.

PatentboxliteratureWenowturntothosepapersthatexplicitlyanalyzetheimpactofthepatentboxinstrumentonpatentlocationandtransfer,showninTable1b.Alstadsæteretal.(2018)analyzetheuseofpatentboxregimesbythe2,000largestcorporateR&Dperformersworldwidefortheperiod2000‐2011.Theirsamplecomprises33countries(theEU28,theUSA,Canada,Switzerland,theRepublicofKorea,andChina)andthefirmsaccountforalmost90%ofglobalR&Dspending.Firmsactiveinthreebroadlydefinedsectors(pharmaceuticals,motorvehicles,andinformationandcommunicationtechnologies)areincluded.Usingvariousnegativebinomialmodelsforthenumberofpatentsofaparticulartechnologytypelocatedinacountrybyeachofthesemultinationals,theyfindthatthetaxadvantageofapatentboxdoesinducefirmstolocatetheirpatentsinacountry.However,interpretationoftheregressionsisproblematic,sincetheyincludebothadummyforthepresenceofapatentboxandthetaxadvantageofsuchabox.Thesevariablesareveryhighlycorrelatedandareessentiallytwodifferenterror‐riddenindicatorsofthesameunderlyingconcept.Aspredicted,thebettermeasureenterspositivelyandtheothernegatively(Hall,2004).

9

Table1b:Literatureonpatentboxes

Alstadsæteretal.(2018)alsoexaminetheimpactofthedetailedprovisionsofthepatentbox,findingsomewhatinconsistentresultsacrosstechnologies.Broaderscopeofpatentboxbenefitsmakesaffiliatelocationsmoreattractive,andhigh‐valuepatentsaremoreimpactedthanlow‐valueones.Whiletheauthorsfindataxadvantageforthefirmusingpatentboxes,therearesmallnegativeeffectsonlocalinvention.However,ifthereisalocaldevelopmentrequirement,thispreventspurelyopportunisticshiftingofpatentfilingsandinthiscasepatentboxeshaveasubstantialpositiveimpactondomesticinventions.

BösenbergandEgger(2017)lookatpatentfilingsandpatenttrade(ownershiptransfer)asafunctionofallthepossibletaxincentivesthataffectpatenting.Tothisend,theyconstructacountryleveldatasetwithcomprehensiveinformationonR&Dtaxincentivesfor106countriesbetween1996and2012.ThetwomainmeasurestheycreatearetheeffectivemarginalR&Dcostduetoitsspecialtaxtreatment(EMTR,widelyknownasthe“Bindex”,Warda2002)8andtheeffective

8Technically,theB‐indexistheratiooftheafter‐taxcostofR&Dtotheafter‐taxprofitsofthefirm,soitisequaltounitywhenthereisnospecialtaxtreatmentforR&D,andislessthanoneinthecaseofspecialR&Dtreatment.ThusitisnotreallytheeffectivemarginaltaxrateonR&D(inspiteoftheterminologyusedbyBösenbergandEgger2017),butisnegativelyrelatedtoit.Thisimpliesthattheexpectedimpactoftheb‐

Paper data level #obs years obs/yeardependent

variable(s)independent variables method pat box result

Alstadsaeter,

Barrios,

Nicodeme,

Skonieczna and

Vezzani (2018)

EP apps; ORBIS

data for EU

scoreboard

firms in 33

countries

firm‐

technology‐

industry

~160,0002000‐

20114444? EP patent fi l ings

GDP, inventor presence, tax rate,

patent box rate, triadic pats, IP

strength, country dummies

random effects

neg binomial; R

coeff mixed logit

fi l ings wrt box:

‐5.0 (semi‐

elasticity)

Bösenberg &

Egger (2017)

EP apps; 106

countries

country‐

technology639; 9425

1996‐

201249; 2600

fil ings and

transfers

B‐index, EATR, pat box dummy;

researchers per cap, GDP, avg pat

characteristics

Poisson FE

(year)

seller: 0.43***

buyer: 0.23***

Bradley, Duchy,

and Robinson

(2015)

worldwide

patstat countries 1,487

1990‐

2012

~70

countries

inventor patent

apps; owner

patent apps;

pats with inv

country not

owner country,

etc

Patent box, pat box rate, other

tax vars, GDP, population, patent

system quality

Panel OLS

domestic

inventing

increases if

rate falls; no

impact on

mismatch

owner‐inventor

Dudar, Spengel

& Voget (2015)

royalty

payments

country

pairs~20,000

1990‐

2012

~900

~60

countries

royalty streams

royalty tax, tax difference,

corporate tax, IP box dummies,

CFC rules, TP rules, R&D, GDP,

POP in recipient country, trade

between

Poisson PML

Royalties

increase i f IP

box covering

acquired and

self‐generated

patents

Koethenbuerger,

Liberini &

Stimmelmayr

(2016)

MNCs from

Orbissubsidiaries

85,944

(30,798

matched)

2007‐

2013

12,715

(4,498

matched,

2,942

patenters)

stated profit

before tax

D(patent box),(new pat entrant),

and interactions; assets, leverage

diff‐in‐diff; ind‐

year, ctry‐year

Fes

pat box used

for profit

shifting

Schwab &

Todtenhaupt

(2016)

MNCs from

Orbis/AMADEUS

with sub in

patent box

country match

to PAtSTAT

firm 271,2512000‐

201220,865

worldwide pat

grants

patent box, R&D/GDP, GDP per

cap, corp tax, GDP growth R&D

user cost. Real interest rate, firm

age, assets, work cap, capital

intensity

Poisson FE (firm

& year)

pat box in

other countries

has positive

spillovers on

domestic R&D

Ciaramella

(2017)EP apps firm 329,398

1997‐

2015~16,000

patent transfers

during the exam

phase at the EPO

pat box, corp tax rate, CFC; log

GDP, distance, language, RD/GDPNeg Bin FE (year)

buyer: 1.2***

seller: insig

Mohnen, Vankan

& Verspagen

(2017)

Dutch firm data firm2007‐

2013~15,000

R&D person‐

hoursuse of patent box diff‐in‐diff

pat box

positive for

domestic R&D

10

averagetaxrate(EATR)ontheprofitfromR&D,whichincludesinformationonthecorporatetaxrate.Theyalsoincludedummiesforthepresenceofataxholiday,grant,and/orpatentbox.Notably,theydonotincorporatethepatentboxrateintotheEATRonR&Dprofits.

Theempiricsinthepaperrelatepatentfilingsandpatenttradeacrosscountriestothetaxvariables,patentcharacteristics,countrycharacteristicsanddistancesbetweencountries.TheyfindthatfilingsinacountryrespondtoEATRbutnottotheB‐indexorthepresenceofapatentbox,althoughthesignsofthesecoefficientsareasexpected.PatenttraderespondstotheEATRinthesendingcountryandtotheB‐indexinbothcountries,withanambiguoussignontheB‐indexforthedestinationcountry.9Italsoappearsthatmorevaluablepatentsaremorelikelytobetransferred.Notethatthepatenttrademeasureinthispaperisbasedmainlyontransferspriortograntbyapplicantcountry.However,focusingonlyonpre‐granttransfersmaylimitapplicability.AsGaessler(2016)shows,manytransfersoccurpost‐grant,henceitisuncleartowhatextenttheresultspresentedbyBösenbergandEgger(2017)areaffectedbyselectionissues.Giventhepatentrenewalevidencethatitmaytakeyearstodeterminewhetherapatentableinventionisvaluable,post‐granttransferssuggestthatfirmswaitinordertodeterminewhichpatentstotransfer.

Dudaretal.(2015)usedataon61countriesworldwide1990‐2012toexamineroyaltyflowsbetweencountriesinresponsetotaxdifferences.Theyfindalargeeffect,inthataonepercentdeclineintaxratesbetweenjurisdictionsleadstoa6percentincreaseinroyaltyflows,whichislargerthanmostoftheresultsforpatentsintheliterature.Theyarguethatthisisconsistentwiththeideathathigherqualityintangiblesintheformofpatentsaremorelikelytobetransferred.Astopatentboxes,theyfindthatwhentheyapplytoacquiredandself‐generatedIPintherecipientcountry,royaltypaymentstothatcountrydoincrease.

Bradleyetal.(2015)examineworldwidepatentapplicationsbyinventorsandapplicantsinacountryasafunctionofthepatentboxanditsassociatedtaxratebetween1990and2012.Thistimeperiodmeansthattheyhaverelativelyfewpatentboxobservations(about12percent)andtheydonothavetransferdata,sotheyinfertheimpactontransfersfromchangesinthemismatchbetweeninventorandpatentownercountry.Theyfindthatalowerpatentboxtaxrateisassociatedwithanincreaseindomesticinventorpatenting,butnotwiththepropensityforinventorandownercountriestodiffer.TheyalsofindthatregimesallowingtheuseofacquiredIPlowerdomesticinventoractivity,suggestingsomekindofsubstitutionbetweendomesticinventionactivityandtheuseofacquiredIPfromothercountries,althoughthisconclusionisfairlyspeculative.

Koethenbuergeretal.(2016)looksatwhethermultinationalswhowereabletobenefitfromtheintroductionofapatentboxbecausetheyownedpatentssucceededinincreasingtheiraffiliateprofitsinthepatentboxcountry,whencomparedtomultinationalaffiliatesinthesamecountry

indexandtheEATRonR&Darethesame.Alowerb‐indexisexpectedtoencourageR&D,asdoesalowereffectiveaveragetaxrateontheprofitsfromR&D.

9Theregressionsshowsignsofmisspecification,asthePoissonandnegativebinomialresultsdiffergreatlyintheircoefficients.Forconsistency,itwouldhavebeenbettertoreportPoissonresultswithrobuststandarderrorestimates,sincethenegativebinomialmodelismoresubjecttoinconsistencyofthemeanestimate.

11

whoseparentsdidnothavepatents.Theyuseadifference‐in‐differenceanalysiswithacarefullychosencontrolsampleofmultinationals.Theyalsofindthatthisprofit‐shiftingbenefitwasconfinedtoaffiliatesincountrieswhereexistingand/oracquiredpatentswerecoveredbytherespectivepatentbox.Theirresultdoessuggestthatintheabsenceofthenexusrequirement,profitshiftingviapatenttransferdoestakeplaceinresponsetotheintroductionofthepatentbox.

Inaninterestingstudy,SchwabandTodtenhaupt(2018)lookatadifferentconsequenceoftheintroductionofapatentbox.TheyarguethatbecauseapatentboxinoneofthecountriesinwhichtheyhaveaffiliatesiseffectivelyareductioninthecostofR&Dcapitalthattheyface,itshouldincreasetheirR&Dactivityoverall.TheyconfirmthisideausingapanelofmultinationalfirmsactiveinEuropeduringthe2000‐2012period.Firmsthatareexposedtoapatentboxforoneoftheiraffiliatesincreasetheirpatentoutputbyabout15percent,butonlyifthepatentboxisnotsubjecttoanexusrequirement,consistentwiththeresultsofAlstadsæteretal.andKoethenbuergeretal.UsingconfidentialGermandata,theyarealsoabletolookattheR&DspendingchoicebyGermanmultinationalsandfindthatthistoorespondstotheintroductionofapatentboxwithoutanexusrequirement.Unfortunately,thecountrieswithoutanexusrequirementarearathersmallset:France,Hungary,Malta,andCyprus.Likemanyofthestudies,includingours,identificationnecessarilyrestsonthevariationinpatentboxdesignacrossonlyafewcountries.

LikeBösenbergandEgger(2017),Ciaramella(2017)studiesthetransferofEPpatentsduringtheexaminationphaseattheEPOinresponsetotheintroductionofthepatentbox,butatthefirmlevelandforthe1997‐2015period.Restrictingtheanalysistotransfersmadebeforethepatentsaregrantedcoversabout60percentofalltransfersbyhercomputations.Theresultssuggestthataonepercentincreaseinthetaxrebateassociatedwiththepatentboxwouldinduceabouta10percentincreaseinpatenttransferstothatcountry,andthattheresponseofhigherqualitypatentswouldbeslightlyhigher.Shealsoconfirmsthatpatentboxdesignmatters:restrictingtheuseofacquiredandexistingpatentsandrequiringfurtherdevelopmentofthepatentedinventionbothdiscouragepatenttransfersinresponsetotheavailabilityofalowertaxrate.Theeffectivepatentboxcoefficientisinsignificantlydifferentfromzerowhenfurtherdevelopmentisrequired.

InoneoftheonlypaperstolookattheimpactofthepatentboxonR&Dspending,Mohnenetal.(2017)studytheimpactoftheDutchpatentboxonR&Dperson‐hoursinthefirmsthattakeitup.Theyuseadifferences‐in‐differencesapproachandfindanincreaseinR&Dinresponsetothepatentbox,althoughbytheirestimatestheincreaseisabouthalfofthelosttaxrevenue.ThismakesitasomewhatlessattractivepolicyforinducingR&DwhencomparedtotheapproximatelyunitelasticityestimatesfortheR&Dtaxcredit(HallandVanReenen,2000).

4. Models

Afirminvestingininnovationfacesanumberofdecisions:1)thelocationchoiceforitsR&Dinvestments,2)whethertofileforpatentsontheresult,3)ifso,thelocationofthefirstfiling,4)thelocationofownershipofthepatents,and5)anyotherlocationsinwhichtofile.ThetaxtreatmentofR&Dandpatentswillaffectallthesedecisionstovaryingdegrees.TheR&Dlocationdecisionislikelytobemostsensitivetotheavailabilityofskilledpersonnel,themarketsizeinthecountry,and

12

possiblythe(tax)costofdoingR&D.UnlessthepatentboxhasastrongrequirementthattheassociatedR&Dbedoneinthecountry,thisdecisionisunlikelytobedrivenbyitsavailability.10Similarly,patentcoveragebyitselfisdrivenbytheneedtoexcludeothersinthecountryinquestion,thecostofsuchexclusion,theadequacyofpatentenforcementinthecountry,theavailabilityofadequatetradesecretprotection,andthelike.Conditionalontheexistenceofpatentableinventions,theavailabilityofapatentboxshouldmattermainlyforthelocationofownershipofthepatentandtheabilitytoattachrevenuetothatownership.Thatis,patentingisdrivenbyasetofconsiderationsthatarefairlyorthogonaltothechoiceoflocusforpatentownership,withoneexception.Theexceptionisthatmoreprofitablepatentswillbepreferredfortransfertoalowertaxjurisdiction.

Ouranalysisisperformedattwolevelsofaggregation:countrylevelandpatentlevel.Thefirst,whichaggregatesalltransferstothesendingcountry‐receivingcountry‐yearlevel,allowsustoexaminetheimpactofthetaxvariablesandothercountry‐levelvariablesonthreelocationdecisions:wheretoapplyforthefirst(priority)patentonaninvention,thelocationoftheapplicantcountrywhenapatentisappliedfor,andwhereandwhentotransferownershipofpatents.11Thesecondallowsustoexaminethechoicesattheindividualpatentlevel,whichmeansthatwecanincludepatentcharacteristicsinouranalysis.

Intheaggregateanalysis,weestimateacountdatamodelforthenumberofpatentstransferredfromcountryStocountryBinyeart(orinventedincountrySbutcountryBischosenasthepriorityapplicationorasthelocationoftheapplicant):

(# | , ) ( , )St Bt S B t St BtE transfersS B X X f X X

Thefunctionf(.,.),whichisintendedtocapturetherelativeattractivenessofcountrySandcountryBasalocationfortheprofitsfrompatents,isproxiedbyarangeofvariablesthatdescribethechangingtaxenvironmentinbothcountriesovertime,aswellasothercountrycharacteristics.Weuseagravitymodelofthechoice,wherethedependentvariableisthenumberofpatentsappliedforthatyearbytheinventor‐priority/applicantcountrypair,controllingforcountryandyearfixedeffectsaswellasthetwocountry’sGDP,population,R&D,andpatentingactivity.

Thegeneralformofagravitymodelisthefollowing:

k kijt i j t kit kjt ijt

k k

Y X X

10However,itisinterestingtonotethattheDutchinnovationboxallowsitsuseinthecasewherethefirmhasobtainedanR&Dcertificate,whichisneededtousetheR&Dtaxcredit(BongaertsandIjzerman,2016)reportthatthevastmajorityofDutchfirmsusingtheinnovationbox(82%)makeuseofthisfeatureratherthanusingincomefromapatent.ThisfactalonesuggeststhatpatentboxschemesareunlikelytobeasusefulasR&DtaxcreditsinstimulatingR&D.

11Althoughthetransferchoiceandprioritychoiceareopentoanyapplicant,presumablyonlyapplicantswithlocationsinmultiplecountriesarefreetochoosethecountryfromwhichtheyapply.

13

Inourcasei,jdenotesellerandbuyercountryrespectivelyandtistheyearofpatenttransfer.Yisthenumberofpatentstransferred,XiandXjarethecharacteristicsofcountriesiandj,andηisadisturbance,whichmaybeheteroskedastic.Forestimation,andassumingthatthedisturbanceηisindependentoftherighthandsidevariables,theequationistransformed:

exp ln ln ln ln ln

and E[ | , , ] exp ln ln ln ln ln

ijt i j t k kit k kjt ijtk k

ijt it jt i j t k kit k kjtk k

Y X X

Y i j X X X X

AssuggestedbySantos‐SilvaandTeneyro(2006),thismodelcanbeestimatedbypseudo‐maximumlikelihood,thatis,Poissonwithrobuststandarderrors.Theyshowthatthisestimatorispreferredforgravitymodelsintermsofbiasandhastheadditionalbenefitthatzeroesinthedependentvariableareallowed,whichisnottrueoftheusualloglineartreatmentofthegravityequation.Seethatreferencefordetails.WeusearandomeffectsPoissonmodelwithrobuststandarderrorsclusteredonthebuyer‐sellercountrycombinationsforestimation.Thatis,therearefixedcountryeffects,butrandomeffectsforthecountry(buyer‐seller)combinations.Thismodelismorerobusttomisspecificationthanthealternativenegativebinomialmodel,andthestandarderrorestimatesallowfortheoverdispersion,whichisclearlypresent.Experimentswiththenegativebinomialmodelanditsrandomeffectsversionproducedunstableresults,supportingtheviewthatthisdistributionalassumptionwasnotjustified.

Theaboveanalysisistosomeextentsimplydescriptive,ratherthanbeingderivedfromtheapplicant’schoiceproblem.Amorecompletemodelwouldneedtobeanalyzedatthefirmorpatentlevel.Atanyperiodintime,thefirmfacesthechoiceofkeepingthepatentwhereitisortransferringittoanothertaxjurisdiction.Thereasonsfortransferincludemergers/acquisitions,assetsales,ortaxconsiderations.Ourfocusisthelatter,andweareforcedtoassumethatthetaxeffectisroughlyorthogonaltotheothercausesoftransfer,duetotheabsenceofaccuratedataontheseothercauses.AnalternativeinterpretationisthatourestimatesencompassanytaxadvantagemotivationsderivingfromM&Aactivity.Weaddressthisquestionlaterwhenwefocusinourempiricalworkonintra‐grouptransfersacrosscountries,whicharearguablypurelytaxmotivated.

Oursecondempiricalmodelexaminesthechoiceofwhichpatenttotransfer.Inprinciple,afirmconsideringtransferringownershipofapatentacrosscountriesfacesamultitudeofchoices,andwouldchoosebasedonthetaxrateonpatentincome,thetransfercost,andwhetherithadasubsidiaryinthecountry.Thissuggeststhatachoicemodelsuchaslogitwouldbetheappropriatewaytoanalyzethechoiceofthecountrytowhichtotransferthepatent.However,estimationofsuchamodelwouldbedifficult,giventherelativefewactualobservationsavailableforidentification(IPtaxchangesin12countriesduringtheperiod,withvaryingrules).Thereforewefocusonthechoicetotransferasafunctionofpatentandownercharacteristics,usingalogitmodelwithstandarderrorsclusteredatthepatentlevel.Wethenexplorehowthetypeoftransfer(toatax‐favoredjurisdiction,orwithinagroup)varieswiththesecharacteristics.

14

5. Data

Thereareapproximately1.2millionregisteredownershiptransfersofEuropeanpatents(EP)intheMPI2018patenttransferdatabase.12Abouttwo‐thirdsofthesetransfersarewithinagroupoffirms,whileonlyabout12percentareacrosscountries.ThemostcommontransfersaretoandfromGermanyandtheUnitedStatesandSwitzerland.Grantedpatentsarefarmorelikelytobetransferredandtransferredpatentsareuniformlydistributedacrosstechnologyarea.Formoredetailontherawdata,seeGaesslerandHarhoff(2018).

Forthestudyhere,werestrictthesampletotransfersamong51countriesforwhichwehavetaxinformation.OursampleincludesalmostallEuropeancountries,theUS,Canada,Mexico,Chile,Australia,NewZealand,Japan,Korea,and14“taxhaven”countriesorjurisdictions,mostlyintheCaribbean.Itincludes95percentoftheinternationaltransfersinthedatabase.13ThecompletecountrylistisshowninAppendixTableA1,andthelistofthepatentboxcountriesonlyinAppendixTableA2.

WecombinethesedatawithtaxdatafromAlstadsæteretal.(2018),Eversetal.(2015),andtheOECDoncorporatetaxationandthetaxtreatmentforintangibleassetsincludingpatentboxes.14Figure1ashowsthedistributionofcorporatetaxratesduringthe2000‐2014periodforthe37countrieswhichhavecorporatetaxation(thatis,excludingthe14taxhavens)andFigure1bshowsthedistributionofthewedgebetweentherateonordinaryincomeandthatonpatent‐generatedincomeforthosecountriesthathaveapatentbox.Themediancorporatetaxrateis28percentandthemedianreductionforpatentsisaround18percent.Themediantaxrateonpatent‐relatedincomeforthosecountriesandyearsthathaveapatentboxis7percent.

12TheMaxPlanckInstituteforInnovationandCompetitionPatentTransfersData2018.

13101,091transfersoutof106,642overthe2000‐2014period.

14Wecheckedthecodingoftheexisting/acquiredIPexclusionsandthedevelopmentconditionsattachedinvarioussources.DeterminingtheprecisedefinitionofeligibleIPturnsouttobedifficult,andthereissomeconflictamongthevariousresearchpapers.Inaddition,giventheabilityoffirmstocreatelocalsubsidiaries,itisnotclearthattheserestrictionsbiteinsomecases.Unfortunatelyusingmorenuanceddefinitionsofthesevariablesleavesuswithnodegreesoffreedomtoidentifytheireffects.

15

Figure1

6. Aggregateanalysis

InternationalpatenttransfersOurinitialexploratoryanalysisisattheaggregatelevel.Weobservethenumberofpatenttransfersfromeachof51countriestotheother50countries(excludingwithincountrytransfers).Forestimation,werestrictthetransfersampleto2000‐2014,whichiswhenmostofthepatentboxeswereintroduced.15Thetotalnumberofobservationsinourdataistherefore38,250=15*50*51.16Figure2showstheaggregateEPpatenttransfersintothecountriesthatintroducedthepatentboxduringthe2000‐2014period,asafunctionofthenumberofyearsbeforeandafteritsintroduction.ThefigurealsoshowsthetransfersofEPpatentsrestrictedtobewithinafirmgroup.Bothcurvesshowtheexpectedincreaseintransfersduringthetwoyearsfollowingthepatentboxintroduction,withthewithingroupcurveincreasingsomewhatmore.Theeffectdiminishesafter2years,probablybecausethedesiredtransfershavebeencompleted.Thereisalsoahintofpatentboxanticipationthreeyearspriortoitsintroduction.Itisdifficulttogetprecisedatesforallthe

15Therearetwoexceptions:France(1971‐)andIreland(1973‐2010,2015‐).Asourtransferdatabeginsonlyin1981,Francedoesnotcontributetoidentification,andforIrelandidentificationcomesfromtheboxremovalratherthanintroduction.Therecentlyre‐introducedpatentboxinIrelandisoutsideoursampleyears.

16Twoofthetaxhavenjurisdictions(JerseyandAruba)havenopatentstotransfer,sothetotalnumberofobservationsisactually49*50*15=36,750.Inaddition,Francehasapatentboxduringtheentireestimationperiod,whichmeansitwillnotcontributetoidentificationofthepatentboximpactinthepresenceofthecountrydummy.

16

countriesastowhenthepatentboxfirstbecamearealprobability,butwedoknowthatfortheUK,thelegislationwasactuallyinplacelongbeforethedatewhencoveragebegan(2013).17

Figure2

Asdescribedinsection4,weestimateacountdatamodelforthenumberofpatentstransferredfromcountryStocountryBinyeart.Weincludearangeofvariablesthatdescribethechangingtaxenvironmentinbothcountriesovertime,aswellassomeothercountrycharacteristics.ThestatutorycorporatetaxrateofS(sellercountry)andB(buyercountry)isincludedinmostregressions.Thisrateexcludesanyadvantageduetothepatentbox.Tomodelthepatentbox,weusedeitheradummyforitspresence,orthemagnitudeofthereductionfromthecorporatetaxrate(corporatetaxratelessthetaxrateonincomeattributedtopatents).Theothercountrycharacteristicsincludedarepopulation,realGDPpercapita,EPpatentapplicationspercapita,andtheR&D‐GDPratioplusadummyforthosefewobservationswhereR&Dspendingwasunobtainable.ThepopulationandGDPnumberscomefromthePennWorldTables8.1(Feenstraetal.2015),whiletheR&DfigurescomefromtheUNESCOInstituteforStatisticsdatabaseandarealsoavailablefromtheInternationalMonetaryFundstatisticaldatabase.

Inpracticewefoundthatexcludingthe14taxhavencountriesfromthesamplemadelittledifferencetotheestimates,sowefocushereontheresultsthatarebasedonthe37countrysample,

17Seehttps://www.gov.uk/guidance/corporation‐tax‐the‐patent‐box.Thisdocument,datedJanuary2007,describesthepatentboxtobeintroducedin2013.

17

whichincludesall13countriesthathaveintroducedapatentboxby2014.18TheseresultsareshowninTables2aand2b.Resultsforthe51countrysampleareshowninAppendixTablesB1andB2.

ThefirstthreecolumnsofTable2ashowthebasicresultsforPoissonrandomeffectsestimationofthenumberofinternationalpatenttransfersfromonecountrytoanotheronthetaxvariablesandcompletesetsofdummiesforbuyerandsellercountriesaswellasyeardummies,whilethenextthreecolumnsaddthevariouscountrycharacteristics.19Thecountrydummiesalreadycontroltosomeextentforthefactthattheaveragenumberofpatents,thesizeoftheeconomyanditstechnologicalintensityvaryenormouslyacrosscountries,soaddingthesecharacteristicstotheregressiononlycontrolsfortheirchangeovertime.Wefoundthatonlythebuyercountrypopulationandpercapitalpatentingenteredtheregressionsignificantly.

Columns1and4inTable2includethecorporatetaxratesandthemagnitudeofthedifferencebetweenthecorporatetaxrateandthepatentboxrateforbothcountries.Theoverallcorporatetaxratesdonotentertheregressionsignificantly,althoughwedofindsomeevidenceforpatentboximpactonpatenttransfers.Thepresenceofapatentboxissignificantlynegativefortheseller(sending)countrybutnotforthebuyer(receiving)country.Thusoncewecontrolforseller,buyer,andyear,onlychangesinthepotentialseller’staxrateshaveanynoticeableeffectonthenumberofpatentstransferred,withthelowertaxratesonpatentboxincomeinthesellercountrydiscouragingthetransferofpatents.

AsFigure2suggests,wewouldexpectthatthepatentboximpactonpatenttransfermightbetransitory,becausepatentapplicationsaftertheintroductionofapatentboxwillsimplybemadefromtherelevantjurisdiction.Incolumns2and5ofTable2,thisideaisexploredbyincludingpatentboxdummiesorthepatentboxtaxwedgeonlyinyears0,1,and2followingthepatentboxintroduction.Theresultsshowthatthereisatransitoryimpactofthepatentboxontransferstoacountrywhichisstrongestinyear2.Thatis,ittakessometimeafterthepatentboxintroductionfortransferstothatcountrytorespond.

Columns3and6ofTable2ashowestimateswherewerestrictthetransferstothosethatarewithinthegroup,thatis,transferswithinamultinationalfirm.Inthiscasetheresultsareevenstronger,aswemightexpectgiventhatthetaxbenefitsareentirelywithinthefirm.Thesumofthecoefficientsonthepatentboxwedgeis4or5,whichimpliesthatachangeof10percenttothewedge(e.g.,movingfrom10percentto20percentdifferencefromthecorporatetaxrate)isassociatedwithafourtofive‐foldincreaseinthenumberofpatentstransferred.

18Thesampleis27Europeancountries,Australia,Canada,Chile,Israel,Japan,SouthKorea,Mexico,NewZealand,Turkey,andtheUS.

19Weclusterthestandarderrorsbyorigin‐destinationcountrypairs.Ourestimationstrategymeansthattheaveragetransfereffects(toandfrom)foreachcountryaretreatedasfixedeffects,whiletheaveragetransfereffectbetweenspecificpairsofcountriesistreatedasarandomeffect,conditionaloneachcountry’sownaveragetransferprobability.

18

Table2a

InprinciplethedecisiontotransferIPfromonejurisdictiontoanothershoulddependprimarilyonthedifferenceintaxratesinthetworegimes,ratherthanontheirabsolutelevel.Suchanapproachisalreadysuggestedbythenonsignificanceofbuyercorporatetaxrateandsomeofthesellerpatentboxvariablesinthepreviousmodels.Denotingthestatutorycorporatetaxrateasτandthetaxrateonpatentincomeasρ,wedefinethefollowingvariables:

( ) ( ) ( ) ( )S B

B B S S S B S B

difftax

diffbox

Thesevariablesaredefinedinsuchawaythattheirexpectedcoefficientsarepositive(thegreaterthesellertaxrateisrelativetothebuyertaxrate,thehigherthelikelihoodofatransfer).

Table2bshowstheresultsofestimationwiththesevariables,andadditionalresultsareshowninAppendixTableB3.Neitherdifftaxnordiffboxissignificantbyitselfinpredictingpatenttransfers.Thevariablediffboxisalsointeractedwithseveralotherfeaturesofthetaxsystemintheregressionsfollowing:1)whetherexistingpatentsareeligible(showninTableB3);2)whetheracquiredpatentsareeligible(showninTableB3);3)whetherthereisrequirementoffurther

All All

Within

group All All

Within

group

Variable (1) (2) (3) (4) (5) (6)

Buyer corporate tax rate 0.81 1.07 0.24 ‐1.02 ‐0.71 ‐1.34

(1.28) (1.33) (1.83) (1.25) (1.28) (1.59)

Buyer patent tax rate wedge ‐0.04 ‐0.29

in all years after introduction (0.76) (0.67)

Buyer patent tax rate wedge 0.18 0.17 ‐0.12 ‐0.14

in year of introduction (0.67) (0.87) (0.63) (0.79)

Buyer patent tax rate wedge 1.07 1.59 0.83 1.41

in year after introduction (1.40) (1.53) (1.35) (1.41)

Buyer patent tax rate wedge 2.41* 3.41** 2.05* 3.07**

two years after introduction (1.27) (1.45) (1.21) (1.32)

Seller corporate tax rate 1.11 1.17 0.88 0.59 0.63 0.00

(1.03) (1.00) (1.27) (1.44) (1.43) (1.88)

Seller patent tax rate wedge ‐1.52** ‐1.43** ‐2.01*** ‐1.38** ‐1.33** ‐2.09***

(0.63) (0.62) (0.76) (0.66) (0.67) (0.70)

Chi‐squared 4191.5 4110.5 3139.6 4486.2 4473.0 12817.9

Degrees of freedom 92 94 94 102 104 104

Inter‐country patent transfer flowsDependent variable: Number of patents transferred from seller country to buyer country during the

year

Regressions in columns 4‐6 also include the buyer and seller aggregate patent applications, population, GDP per

capita, and R&D intensity, all in logs.

19,980 observations on 1,332 country pairs, 2000‐2014

Poisson random effects panel regression with standard errors clustered on buyer‐seller country pairs.

Coefficient significance is denoted by * p<0.1, ** p<0.05, *** p<0.01.

All regressions include complete sets of dummies for the 37 buyer and seller countries and years.

19

developmentoftheinventioninthecountry;4)whetherCFCrulesapplybetweenthesellerandbuyercountry.Measuringtheimpactofalltheseresultsischallengingduetoanabsenceofsufficientvariationacrosscountries(seeTableA1).Thereforeweexaminethemoneatatime.Allowingexistingand/oracquiredpatentstobenefitfromthepatentboxdoesnothaveasignificantimpactonthenumberoftransferstothatcountry,althoughthelargestandarderrorsdonotwarrantstrongconclusions.

Incontrast,therequirementforfurtherdevelopmentofthepatentedinventioninthebuyercountrysubstantiallyreducestransfers,whilecountrieswithoutthatrequirementseeanincreaseintransfersfromthepatentbox.Wecancomputethepotentialimpactofachangeinthepatentboxtaxadvantageforsystemswithandwithoutthisfeature,findingthattheresponsetoa10percentincreaseinthetaxadvantagefromapatentboxisassociatedwithanincreaseofabout14percent(standarderror6percent)ifexistingand/oracquiredpatentsareincludedandminus6percent(standarderror10percent)iftheyareexcluded.Thisresultisconsistentwiththeprofit‐shiftingresultsofKoethenbuergeretal.(2016).

CFCrequirementsimposedonthebuyercountrybythesellercountryalsoreducethelikelihoodoftransferringpatents,althoughifthegapincorporatetaxratesislargeenough,itisabletooverridethisimpact.ThepointatwhichtheCFCimpactturnspositiveisacorporatetaxratedifferenceofabout11percent,soitiswellwithinourdata.Again,wecautionthattheconfidenceintervalforthispointisquitebroad,giventhestandarderrors.

Columns4and8inTable2bshowtheresultsforwithin‐grouptransfers,asinTable2a.Theyarequitesimilartothoseforalltheinternationaltransfers,withtheexceptionoftheCFCrules,whichhaveasomewhatstrongerimpactwheninteractedwiththepatentboxdifferentialandaweakerimpactinteractedwiththeoverallcorporatetaxdifferential.

20

Table2b

Theseresultsleadustotwoconclusions.Overall,thepresenceofapatentboxdoesseemtoinducesometransferstothejurisdiction,albeitwithabitoflag.Theresultsalsoshowthatifacountry’spatentboxdoesnotrequirefurtherdevelopmentoftheinventioninthecountry,morepatenttransfertothecountrywillbeinduced.AlongwithCFCrules,thedevelopmentrequirementismoreimportantinourdatathanwhetherornotpre‐existingoracquiredpatentsareincludedamongthepatentseligibleforspecialtaxtreatment.

ChoiceofprioritycountryWenowturntothechoiceofwheretofileforapatentfirst(prioritychoice)andthequestionofwhichcountrywillbechosenasthecountryofownership.Obviouslythislatterquestionaffectsmainlymultinationalfirmsthathavesubsidiariesinseveralcountries.Figure3illustratestheglobalizationtrendsinpatentfilingattheEPO.In1980,thevastmajorityoffilingsweremadefromthecountryoftheinventorresidence,whichispresumablythecountryinwhichtheresearchleadingtotheinventionwasperformed.Thereisasustainedriseincaseswherethechosenprioritycountrywasdifferentfromthatoftheinventor,from5percenttoalmost14percent,andinitialrisefollowedbyalevelingoffincaseswherethecountryoftheapplicant(patentowner)wasdifferentfromthatoftheinventor.Weknowthatoneofthereasonsforthesechangesistheincreasingglobalizationofpatents,withanincreaseinthenumberofjurisdictionsforwhichprotectionforan

All All All

Within

group All All All

Within

group

Variable (1) (2) (3) (4) (5) (6) (7) (8)

Difference: 0.18 0.35 ‐0.31 0.29 0.80 0.79 0.70 0.94

seller corp tax‐buyer corp tax (0.88) (0.90) (0.95) (1.24) (0.98) (0.97) (0.98) (1.30)

Difference: 0.60 1.35** 0.33 0.40 0.39 0.67 0.08 0.30

buyer‐seller patent tax wedge (0.49) (0.63) (0.55) (0.74) (0.49) (0.59) (0.56) (0.69)

D (dev condition on use)*buyer‐ ‐1.95* ‐0.67

seller patent tax wedge (1.03) (0.94)

D (CFC rules apply to buyer) ‐0.37** ‐0.22 ‐0.40*** ‐0.27

(0.17) (0.27) (0.15) (0.21)

D (CFC) * seller‐buyer corp 3.31*** 1.20 2.40* 0.75

tax difference (1.13) (1.77) (1.34) (1.65)

D (CFC) * buyer‐seller patent 1.27 2.22* 1.71* 2.47**

box difference (1.04) (1.26) (0.99) (1.18)

Chi‐squared 4,054.3 4,072.5 4,175.9 3,095.2 4,342.6 4,359.7 4,470.2 11,753.1

Degrees of freedom 90 91 93 93 100 101 103 103

Inter‐country patent transfer flows ‐ exploring tax variables

Dependent variable: Number of patents transferred from seller country to buyer country during the year

Poisson random effects panel regression with standard errors clustered on buyer‐seller country pairs.

19,980 observations on 1,332 country pairs, 2000‐2014

Coefficient significance is denoted by * p<0.1, ** p<0.05, *** p<0.01.

All regressions include complete sets of dummies for the 37 buyer and seller countries and years.

Regressions in columns 5‐8 also include the buyer and seller aggregate patent applications, population, GDP per capita, and R&D

intensity, all in logs.

21

inventionisdesired(Finketal.,2016).Itmayalsobethecasethatfirmsincreasinglyincludethelocationofitspatentfilingsinitstaxplanning.

Figure3

Ifthisisthecase,wewouldexpectthatthedecisiontofilethepriority(first)filinginacountryotherthanthatofinventorresidencemightdependonthepresenceofapatentbox.Similarly,wheretheapplicantlocationdiffersfromtheinventorlocation,itmaybebecausethefirmhaslocatedpatentownershipinamorefavorablejurisdictionfortaxpurposes.WeexplorethesehypothesesinTable3,usingasimilarmodelasintheprevioussection,butwherethe“seller”countryistheinventorcountryandthe“buyer”countryisthepriorityorapplicantcountry.Forconsistencywiththeremainderofthisstudy,weconfinethedatatoEPpatentapplications,whichmayhaveprioritypatentsorapplicantsoutsidethecountriesthatarememberoftheEPC.

ThefirstthreecolumnsinTable3arefortheinventor‐prioritycombinationandthenexttwoarefortheinventor‐applicantcombination.IneachcaseweshowPoissonestimatesofthemodelwherewedonotincludecaseswheretheinventorcountryisthesameastheprioritypatentorapplicantcountry.Columns1and4controlonlyforthetaxdifferencesbetweenthetwocountries,whilecolumns2,3,and5addtheusualgravitymodelvariablesGDPandpopulation,aswellastwovariablesthataretailoredtothesettinghere,R&Dspendingandpatentingintherelevantcountries.

0%

5%

10%

15%

20%

25%

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

EP patent filing globalization

Priority country different from inventor country

Applicant country different from inventor country

Either different from inventor country

22

Table3

Welooksfirstatthequestionofwhetherthechoiceofprioritycountrydependsonitstaxratesrelativetothetaxratesinthecountrywheretheinventorislocated.Incolumns1and2,wefindthathighertaxratesintheinventorcountryrelativetoprioritycountrydepressthechoiceofprioritycountry,whichiscontrarytoone’sintuition.However,column3,whereweestimateaseparateeffectfortheUnitedStates,showsthatthisresultisanartifactofthepreferenceofEPapplicantsfortheUnitedStatesasaprioritycountry,inspiteofitshighcorporatetaxrateduringtheperiod.Weconcludethatthepresenceorabsenceofapatentboxhaslittleimpactontheprioritycountrychoice.However,othervariablesintheregressiondomatterfortheinventor‐prioritychoice:patentingpercapitainbothcountries,thesizeoftheprioritycountry,theGDPpercapitaoftheinventorcountry,andtheGDPoftheprioritycountry(negatively).Itisimportanttokeepinmindthatthesevariablesareidentifiedbychangesovertime,sincethereareacompletesetofinventorandprioritycountrydummiesintheregressions.

Dependent variable:

Difference in corp tax rate ‐2.05*** ‐1.83*** 0.36 0.13 0.17 ‐0.29

inventor less prior/app country (0.56) (0.46) (0.40) (0.43) (0.31) (0.33)

D (US priority) * diff in corp tax rate ‐3.60*** 1.66***

inventor less prior/app country (0.78) (0.58)

Difference in pat box wedge 0.09 0.34 0.44 ‐0.03 ‐0.09 ‐0.09

prior/app less inventor (0.38) (0.32) (0.29) (0.26) ‐0.24 ‐0.22

Log patent apps per capita 0.52*** 0.51*** 0.47*** 0.49***

in inventor country (0.09) (0.08) ‐0.07 ‐0.07

Log patent apps per capita 0.54*** 0.54*** 0.56*** 0.55***

in prior/app country (0.09) (0.08) ‐0.07 ‐0.07

Log real GDP per capita 0.77** 0.54 0.03 0.07

in inventor country (0.35) (0.35) ‐0.14 ‐0.13

Log real GDP per capita ‐0.80** ‐0.61* ‐0.01 ‐0.04

in prior/app country (0.35) (0.35) ‐0.14 ‐0.13

Log population (millions) ‐0.44 ‐1.02* 0.43 0.55

in inventor country (0.64) (0.52) ‐0.44 ‐0.44

Log population (millions) 1.26* 1.71*** 0.63 0.54

in prior/app country (0.69) (0.57) ‐0.45 ‐0.45

Log R&D researchers per M pop 0.34 0.38 ‐0.08 ‐0.09

inventor country (0.31) (0.31) ‐0.14 ‐0.14

Log R&D researchers per M pop ‐0.30 ‐0.34 0.07 0.08

prior/app country (0.30) (0.29) ‐0.14 ‐0.14

Observations 19,980 19,980 19,980 20,535 20,535 20,535

Country pairs 1,332 1,332 1,332 1,369 1,369 1,369

Chi‐squared 7,059.6 78,915.3 81,916.1 10,892.7 100,239.4 111,650.0

Number of coefficients 88 98 99 89 99 100

# The dependent variable is number of patents with the inventor country‐priority/applicant country combination.

Number of patents from an inventor

country with chosen priority country#

Number of patents from an inventor

country with chosen applicant country#

Inventor country to priority/applicant country flows 2000‐2014

Poisson random effects panel regression with standard errors clustered on buyer‐seller country pairs. * p<0.1, ** p<0.05, ***

p<0.01.

All regressions include complete sets of dummies for the 37 inventor and priority/applicant countries, and years 2000‐2014. One

country has no priority apps and is dropped in those regressions.

23

Turningtotheinventor‐applicantcombinations,recallthatonlyapplicantswithapresenceinmultiplecountrieswillbeabletochooseamongthemasalocationfromwhichtofile,whichmayleadtosomewhatweakeffectsinanaggregateregressionthatincludespatentapplicationsownedbyallapplicants.Indeed,wedofindthattheonlysignificantpredictorsoftheinventor‐applicationchoicearethepatentingpercapitainthetwocountries.WhenweaddtheUS‐corporatetaxdifferentialtotheequation,wefindthatapplicantshaveasignificantpreferenceforfilingfromtheUnitedStateswhentheinventorcountrycorporatetaxrateishigh.

Theconclusionfromtheseaggregateresultsisthatthereislittleevidencethatthelocationofpatentfilingsisaffectedbythepresenceofapatentbox,althoughthereisfairlystrongevidencethatthereexistsapreferencefortheUSasthelocusofownershipandprioritypatentinginspiteofthehighstatutorytaxrateinthatcountry(39percentinourtimeperiod).

InventionThepolicyargumentfortheintroductionofapatentboxisthatitshouldencourageinventionandinnovativeactivityintherelevantcountry.Althoughwedonot(yet)havethedatathatwouldallowustoinvestigateinnovativeandR&Dactivitybroadly,withthecurrentdatawecanlookatchangesinthelevelofpatentedinventionsinacountryafterapatentboxisintroduced.Wefirstshowthesimpletrendsaroundaccessiontimeforthe12countriesinourdatasetthathaveintroducedapatentbox.Giventhewiderangeofpatentingactivityacrosscountries,weshowtwofigures,oneforthe6largercountries,andanotherforthe6smallercountries(notethatthescalesdifferbyafactorof50).

Figure4a

24

Figure4b

BecauseofpatentdatatruncationduetolagsinPATSTAT(April2017edition),thefilingsin2015and2016areincomplete.Thismeansthatthewindowwecanexamineendsin2014andthefiguresshowclearlythatforsomecountries(notablytheUK,Switzerland,Cyprus,andPortugal),thereisalmostnotimeafterthepatentboxisintroducedsothepowerofanytestswillbeweak.InthecaseofFrance,thereisnopre‐patentboxdata.ButthemainfindinginthesegraphsisastrongupwardtrendinEPpatentfilingsoverallwhichshowslittlesignsofchangearoundthedatewhenthepatentboxisintroduced.

Toconfirmthevisualevidence,weestimatesomesimpleaggregatepatentregressionsforthelogoffilingsbyinventorsinacountryasafunctionoftheexistenceofapatentbox,thestatutorycorporatetaxrate,thepopulation,realGDP,andR&D‐GDPratioofthecountry,andasetofcountryandyeardummies.Inthiscase,themethodofestimationisordinaryleastsquares,becausemostcountry‐yearcellshavealargenumberofcountsandtherearenozeroes.TheestimationresultsareshowninTable4.Theyarefairlyclear:inventorfilingsdependpositivelyGDPpercapitaandR&Dintensityandinsignificantlynegativelyonthecountry’scorporatetaxrate.Thetwopatentboxvariablesareslightlysignificant,butwiththewrongsign:ifanything,thepresenceofapatentboxreducespatentableinventioninthecountry.

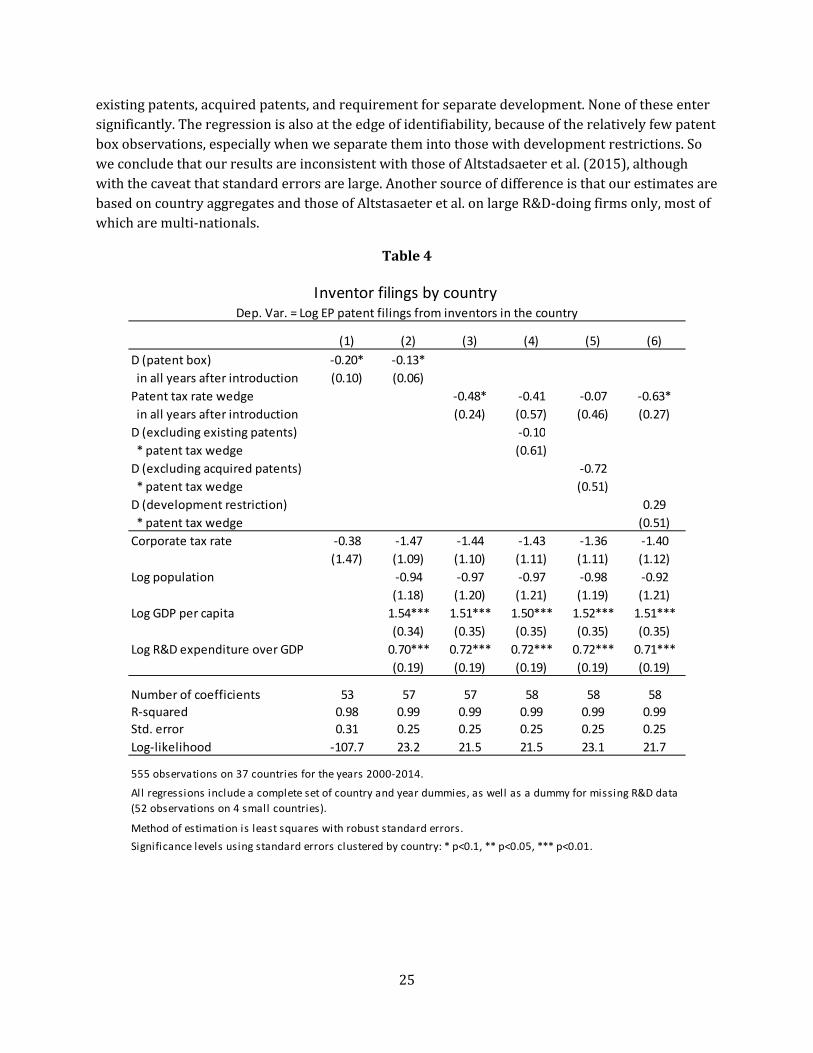

Asmentionedearlier,Altstadsaeteretal.(2015)lookatthechangeinthenumberofinventorsinhostanddestinationcountryinresponsetopatenttransfersatthecompanylevel,andfindthatinventorsinthedestinationcountryaremorelikelytoincreasewhenthereisafurtherdevelopmentrequirementfortheuseofapatentboxwithexistingpatentsthataretransferred.Weprobethisfurtherinincolumns4to6ofTable4,whichaddthedummiesfortheinclusionof

25

existingpatents,acquiredpatents,andrequirementforseparatedevelopment.Noneoftheseentersignificantly.Theregressionisalsoattheedgeofidentifiability,becauseoftherelativelyfewpatentboxobservations,especiallywhenweseparatethemintothosewithdevelopmentrestrictions.SoweconcludethatourresultsareinconsistentwiththoseofAltstadsaeteretal.(2015),althoughwiththecaveatthatstandarderrorsarelarge.AnothersourceofdifferenceisthatourestimatesarebasedoncountryaggregatesandthoseofAltstasaeteretal.onlargeR&D‐doingfirmsonly,mostofwhicharemulti‐nationals.

Table4

(1) (2) (3) (4) (5) (6)

D (patent box) ‐0.20* ‐0.13*

in all years after introduction (0.10) (0.06)

Patent tax rate wedge ‐0.48* ‐0.41 ‐0.07 ‐0.63*

in all years after introduction (0.24) (0.57) (0.46) (0.27)

D (excluding existing patents) ‐0.10

* patent tax wedge (0.61)

D (excluding acquired patents) ‐0.72

* patent tax wedge (0.51)

D (development restriction) 0.29

* patent tax wedge (0.51)

Corporate tax rate ‐0.38 ‐1.47 ‐1.44 ‐1.43 ‐1.36 ‐1.40

(1.47) (1.09) (1.10) (1.11) (1.11) (1.12)

Log population ‐0.94 ‐0.97 ‐0.97 ‐0.98 ‐0.92

(1.18) (1.20) (1.21) (1.19) (1.21)

Log GDP per capita 1.54*** 1.51*** 1.50*** 1.52*** 1.51***

(0.34) (0.35) (0.35) (0.35) (0.35)

Log R&D expenditure over GDP 0.70*** 0.72*** 0.72*** 0.72*** 0.71***

(0.19) (0.19) (0.19) (0.19) (0.19)

Number of coefficients 53 57 57 58 58 58

R‐squared 0.98 0.99 0.99 0.99 0.99 0.99

Std. error 0.31 0.25 0.25 0.25 0.25 0.25

Log‐likelihood ‐107.7 23.2 21.5 21.5 23.1 21.7

555 observations on 37 countries for the years 2000‐2014.

All regressions include a complete set of country and year dummies, as well as a dummy for missing R&D data

(52 observations on 4 small countries).

Significance levels using standard errors clustered by country: * p<0.1, ** p<0.05, *** p<0.01.

Method of estimation is least squares with robust standard errors.

Inventor filings by country Dep. Var. = Log EP patent filings from inventors in the country

26

7. Patentlevelanalysis

Wenowturntoananalysisofthechoiceofpatentstotransfer.Oursampleistheapproximately1,200,000EPpatentsfiledbetween2000and2012thathavebeengrantedasof2014,ofthesepatents5.6percentweresubjecttoanownershiptransferacrosscountries.20Wefocusonthefirsttimethatthepatentistransferred,droppingthefewcaseswherethereismorethanonetransfer.Figure5showstheshareoftransfersasafunctionofthefilingdateofthepatent,togetherwiththenumberofEPpatentstransferredbytransferyear,forbothapplicationsandgrantedpatents.Weusethe2000‐2014periodbecausetherewereveryfewpatentboxcountriespriortothosedates.

Figure5

Wemodelthedecisiontotransferapatentusinglogitprobabilitymodels.Thisapproachhastheadvantagethatitallowsustoeasilyincorporatethechoiceofestimationofdifferenttypes(withingroupornot,toataxhavenornot).Ascontrolvariables,weincludeboththecharacteristicsofthepatenttobetransferredandalsothoseofthepatentowner,whichweexpecttoinfluencebothitstaxstatusandthecostsoftransfer.Thepatentcharacteristicsweincludearethosethathavebeenshowninpreviousworktobeassociatedwithpatentvalue:

20Notallpatentapplicationsintherecentyearsthatwilleventuallybegrantedhavebeengrantedby2014,ofcourse.Yearofapplicationdummiesareincludedinallmodelstocontrolforanydifferencesintransferduetothisfact.

0

2000

4000

6000

8000

10000

12000

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

International transfers of EP patents

Share of EP patents transferred, by filing date

Transfers in current year (RHS)

Transfers of granted patents (RHS)

27

Patentfamilysize(docdbmeasure)–largersizesareassociatedbothwithapplicationinmultiplejurisdictionsandwithmorecomplexcontinuation/divisionalstructures,usedbyfirmsthatanticipatevaluefromtheapplication.

Numberofclaims–frequentlypositivelyassociatedwithvalue,althoughresultscanbeambiguous,asdependentclaimsmayalsorepresentbreadthrestrictions.

Numberofforwardcitations(5‐year)–thenumberoftimesthepatenthasbeencitedinsubsequentpatentfilingsattheEPOduringthefirst5yearsaftertheapplication.

Numberofinventorsnamedonthepatent–alargernumberofinventorsmayimplygreaterexpensedevotedtotheinvention.

Numberofpatentowners(applicants)–however,oftenmultinationalsapplyunderboththeirownnameandthenameoftheirlocalaffiliate,whichmeansthatthisvariablemayinsomecasesproxyformultinationalownership.

Totheseweaddtheageofthepatent.Wehavealimitednumberofapplicantcharacteristics,astheyareentirelybasedonthepatentdata.Theyarethefollowing:

Thesizeoftheapplicant’spatentportfolioatthetimeofthecurrentpatentapplication. AnMNCdummyforwhethertheapplicantisresearchactiveinmorethanonecountry(as

indicatedbypatentingfromthatcountryatleastonceduringtheentireperiod). Adummyforwhethertheapplicantisacorporation(asopposedtoanindividual,

university,non‐profit,orgovernmentalentity).ThisdummyexcludestheMNCdummyabove,whichalsoindicatesacorporation.

Allofthesecharacteristics(withtheexceptionofpatentage)arenon‐time‐varying,whichmakesestimationstraightforwardandallowsustouseamultinomiallogitmodeltoinvestigatethetypeoftransfer.Insomeoftheestimation,wealsoincludedummiesfortheapplicantcountry,thetechnologyareaofthepatentatthe34arealevel,andyeareffectsforthepatentapplicationyear.Testingrevealedthatthecountrydummieswerethemostimportantofthesepredictors,whilethetechnologyareadummieswerelessimportant,withtheexceptionthattheyweakenedthesignificanceoftheclaimsandforwardcitationcoefficients,reflectingthefactthatthesevariablesvarybytechnologyarea.

SimplestatisticsforthesevariablesareshowninAppendixTableA3.Usinganon‐parametricranksumtest,wefindthatinallcasesthedistributionofthevariablesforthepatentsthataretransferredissignificantlytotherightofthatforpatentsthatarenottransferred.Thetransferredpatentsareclearlydifferent,inwaysthatwemightexpectiftheyaremorehighlyvalued.Alsonotethatbecausethedistributionoftheindependentvariablesisquiteskew,weuselogarithmsofthevariablesinalltheestimations(withtheexceptionofthedummies).CorrelationmatricesforthevariablesareshowninAppendixTableA4,withandwithouttheyear,country,andtechnologymeansremoved.Thesecorrelationsarenotespeciallylarge,withtheexceptionofthatbetweenthedummyformultinationalpatentingcorporationsandcumulativepatentholdings,andthedummiesreducethemslightly.

TheresultsofestimatingasimplelogitmodelfortheinternationaltransfersofallEPOpatentsappliedfor2000‐2012thataregrantedby2014areshowninTable5.Duetothelargesizeofthe

28

sample,andthelowprobabilityofatransferinanyyear(about0.3%),wedrawarandom10percentsampleofthenon‐transferredpatents.KingandZeng(2001),amongothers,showsthatwithknownsamplingprobability,logitcoefficientestimatesareunaffectedbythisprocedure,withtheexceptionoftheintercept.Aconsistentestimateoftheinterceptisgivenbythefollowing:

0 0

1ˆ log1

y

y

where 0̂ istheestimatedintercept,ψisthepopulationshareoftransferredpatents,and y isthe

shareofthetransferredpatentsinthesample.Forour10percentsample,thiscorrectionfactorisequalto2.3.21Notethatforrareevents,thecorrectionfactorisapproximatelyequaltothelogoftheoversamplingprobability.

Table5showsthemarginalimpact(inpercentageterms)ontheprobabilityofatransferforeachvariable,whichismoreinterpretablethanthecoefficients.Thisquantitydoesrequirecorrectionforthebiasintheinterceptestimate,ascanbeseentheequationbelow,whereF(.)isthelogitprobability:

( )

(1 exp( ))(1 exp( ))k

F x

x x x

Table5showstheaverageofthisquantityforeachvariablexk.Eachcolumnaddsanothersetofdummies:none,countrydummiesonly,countryandyeardummies,andcountry,year,andtechnologyareadummies.Resultsdonotchangemuchasdummiesareadded,althoughtheeffectsweakensomewhat.Theresultsonpatentvaluelargelysupporttheideathathighervaluepatentsaretransferred,withpositivecoefficientsforfamilysize,numberofclaims,forwardcitations,andnumberofinventors.Whatdoespredictmorestronglythatapatentwillbetransferredisitsownership:whethertheownerhaspatentingactivityinmultiplecountries,andwhetherthefirmisacorporation,evenifitisnotacorporationdoingmultinationalresearch.Patentsthatarepartoflargerportfoliosareslightlylesslikelytobetransferred,whichisplausible,asmanyofthesepatentswillbepartofapatentportfoliostrategythatdependsonquantityratherthanquality.

Itisworthnotingthattheseregressionshaveverylittleexplanatorypower,asthepseudoR‐squaresarealllessthan0.06,evenwhenweincludecountry,year,andtechnologydummies.Sothereremainanumberoffactorsthataffectthechoiceofwhichpatentstotransferthatareunknown.Nevertheless,thecombinedimpactofincreasingthevariouspatentcharacteristicsbyonestandarddeviationistoraisetheprobabilitythatapatentistransferredby0.11%onabaseof0.31%,anincreaseofone‐third.Apatentownedbyamultinationalthatisresearchactiveinmultiplejurisdictionsismuchmorelikelytobetransferredwithanincreaseinprobabilityof0.26%,nearlydoubletheaverage.

21Log[((1‐.00317)/.00317)(0.0309/(1‐0.0309))]=Log(315.5*.0317)=2.302.

29

Table5

Table6exploresthevariationacrossthedifferenttypesoftransfers.Wedefineintra‐grouptransfersthosethataredependentorhierarchicalinGaesslerandHarhoff(2018),andtax‐motivatedtransfersasthosethatareeithertothe14taxhavencountries,ortocountriesthathaveimplementedapatentbox.Thesetwovariablesaretheninteractedtoproduce4possibletransfertypes,andamultinomiallogitmodelisestimatedforthechoiceoftype(theleft‐outcategoryisnotransfer).Themodelisestimatedwithcountryandyeardummies,butwithouttechnologyareadummies,andwefindthatitsexplanatorypowerisslightlyhigherthanthemodelsinTable5.

Variable (1) (2) (3) (4)

Patent family size (docdb) 0.086 0.063 0.063 0.067

(0.001) (0.001) (0.001) (0.002)

Number of claims 0.036 0.021 0.022 0.016

(0.001) (0.001) (0.001) (0.001)

Number of forward citations (5yrs) 0.009 0.010 0.011 0.005

(0.001) (0.001) (0.001) (0.001)

Number of inventors 0.026 0.040 0.040 0.039

(0.002) (0.002) (0.002) (0.002)

Number of patent holders ‐0.069 ‐0.039 ‐0.040 ‐0.030

(0.008) (0.008) (0.008) (0.008)

Age of the patent ‐0.141 ‐0.139 ‐0.139 ‐0.137

(0.001) (0.001) (0.001) (0.001)

Applicant's patent portfolio size ‐0.056 ‐0.040 ‐0.040 ‐0.044

(0.000) (0.001) (0.001) (0.001)

Multinational research activity 0.330 0.270 0.271 0.260

(countries per applicant >1) (0.002) (0.003) (0.003) (0.003)

Patent holder a corporation, ‐0.038 ‐0.021 ‐0.022 ‐0.024

but not an MNC (0.003) (0.003) (0.003) (0.003)

Applicant country dummies no yes yes yes

Year dummies no no yes yes

Technology area dummies no no no yes

Log likelihood ‐454,600.7 ‐447,887.5 ‐447,489.5 ‐445,836.4

Chi‐squared 62,462.0 77,041.4 78,537.5 84,702.0

Degrees of freedom 9 44 57 90

Pseudo R‐squared 0.034 0.048 0.049 0.052

Probability of international patent transfer 2000‐2014Dependent variable: Dummy for first International transfer of patent (mean = 3.07%)

Sample is all granted EP patents with fi l ing date between 1990 and 2014 that are transferred between

2000 and 2014 and a 10 per cent sample of patents not transferred.

Estimates shown are the average marginal impact on the probability in percentage terms. Standard errors

are clustered by patent. * p<0.1, ** p<0.05, *** p<0.01.

All right hand side variables are in log form, with the exception of the multinational and corporation

dummies.

3,428,110 observations on 343,154 patents; 104,664 transfers

30

Therearesomedifferencesinthepatentvaluationcoefficientsacrossthedifferenttypesoftransfers,butnothingterriblysystematic,althoughpatentvalueindicatorsseemtomatterlessforthenon‐grouptax‐motivatedtransfers.Withingrouptransfersalsotendtobeofmuchyoungerpatentsthantheothers.Thenumberofpatentholdersisquitenegativeforallthetransfers,possiblybecauselargenumbersimpedethepursuitoftaxstrategiesinvolvingpatents,duetocoordinationfailurebetweenmultipleindependententitieswhentryingtosellthepatent.Restrictingtointra‐grouptax‐motivatedtransferschangesthesignofthecoefficient:thesetransfersarepositivelyassociatedwiththenumberofpatentholders.Thismaybebecausesuchpatentstendtobeheldbyseveralmembersofthegroup,eventhoughtheyareundercontrolofasingleultimateentity.Relatedtothisisthenon‐MNCcorporationeffect,whichpredictsintra‐grouptax‐motivatedtransfers,butnototherinternationaltransfers.Thesetransfersarethosewithinagroup,wherethegroupisnotnecessarilyresearch‐activeinmorethanonelocation(hencetheMNCdummyiszero).

31

Table6

Ournotverysurprisingconclusionfromexaminingthepatentleveldecisiontotransferownershipinternationallyisthatmorevaluablepatents(byconventionalmeasures)aremorelikelytobetransferred,regardlessofwhetherthetransferistax‐motivatedornot.

Variable

Not a group,

no tax

Group,

no tax

Not a group,

tax Group, tax

Patent family size (docdb) 0.200 0.183 0.176 0.220

(0.009) (0.008) (0.016) (0.012)

Number of claims 0.141 0.086 ‐0.078 0.030

(0.009) (0.008) (0.015) (0.009)

Number of forward citations (5yrs) 0.047 0.033 0.004 0.032

(0.007) (0.006) (0.012) (0.009)

Number of inventors 0.064 0.292 0.033 ‐0.055

(0.012) (0.010) (0.022) (0.016)

Number of patent holders ‐1.047 ‐0.695 ‐1.158 1.547

(0.060) (0.051) (0.117) (0.032)

Age of the patent ‐0.090 ‐0.622 ‐0.117 ‐0.766

(0.005) (0.004) (0.009) (0.005)

Applicant's patent portfolio size ‐0.154 ‐0.085 ‐0.128 ‐0.177

(0.003) (0.003) (0.006) (0.004)

Multinational research activity 0.454 0.947 0.681 1.515

(countries per applicant >1) (0.016) (0.015) (0.027) (0.022)

Patent holder a corporation, ‐0.117 ‐0.272 ‐0.097 0.708

but not an MNC (0.016) (0.017) (0.033) (0.039)

Log likelihood

Chi‐squared

Degrees of freedom

Pseudo R‐squared

A complete set of country and year dummies are included in the estimation.

Coefficient estimates are shown. Standard errors are clustered by patent. * p<0.1, ** p<0.05, *** p<0.01.

The types of transfer are defined by the interaction of the group membership dummy and whether or not the

transfer is to a patent box or tax haven country. The left‐out category is no transfer

3,428,110 observations on 343,154 patents; 104,664 transfers

Multinomial Logit Estimation

Type of international patent transfer 2000‐2014Dependent variable: type of first International transfer of patent (1‐4)

All right hand side variables are in log form, with the exception of the multinational and corporation

dummies.

Sample is all granted EP patents with fi l ing date between 1990 and 2014 that are transferred between 2000

and 2014 and a 10 per cent sample of patents not transferred.

144,019.7

0.064

‐566,537.2

224

32

8. Conclusions

Thispaperreportsonacomprehensiveanalysisoftheeffectsoftheintroductionofalowercorporatetaxrateonpatent‐relatedincomein13Europeancountriesduringthe2000‐2014period,whenthemajorityofthesetaxincentiveswereintroduced.Althoughthischangetothecorporatetaxsystemsdidseemtoincreasetheinternationaltransferofpatentsintoajurisdiction,atleastwhentherewasnorequirementforfurtherdevelopmentdomestically,wefoundrelativelylittleresponsivenessoverall.Thechoiceofpriorityorapplicantcountrywasunaffected,andpatentedinventionsdidnotincreaseinthecountriesofferingapatentbox.Thislastresultisimportant,asitsuggeststhattheprimarystatedgoalofintroducingapatentboxhasnotbeenachieved.

Ourliteraturereviewrevealedawiderangeofapproachestoestimatingthepatentboxeffectaswellassomewhatinconclusiveresults.Wefoundinourexplorationsthatresultshadsizablestandarderrorsandweresensitivetospecification,especiallytotheprecisedefinitionofwhetheracquiredorexistingIPwascoveredbythebox.Withonly13countriesintroducingapatentbox,andallowingforbothyearandcountryeffects,thenumberofactualdegreesoffreedomforidentificationisrathersmall.Identificationisachievedbycomparingthechangeinacountrybeforeandafterpatentboxintroductiontothechangeinanothercountrythatdidnotintroduceapatentbox,controllingforthecommontrendinthetwocountries.Itischallengingthentodistinguishtwocountries,oneofwhichhasanexistingpatentsexclusion,andtheotherwhichdoesnot.Thatisprobablywhythereissomuchvariationintheresultsofthepriorliterature.