short-term and winter fuels outlook guy f. caruso administrator energy information administration...

TRANSCRIPT

Short-Term andWinter Fuels Outlook

Guy F. CarusoAdministrator

Energy Information Administration

New York Energy ForumNew York, NY

October 16, 2007www.eia.doe.gov

Short-Term Energy Outlook, October 2007

Tight global oil market conditions are projected to continue through 2008.

• OPEC production decisions will continue to influence the oil market situation.

• Low surplus production capacity of 2 to 3 million barrels per day, concentrated in Saudi Arabia, weakens the market's ability to respond to supply disruptions.

• Oil prices likely to remain high at least through 2008.

• Many uncertainties could alter the outlook and create volatility in global oil markets.

Short-Term Energy Outlook, October 2007

0

10

20

30

40

50

60

70

80

90

100

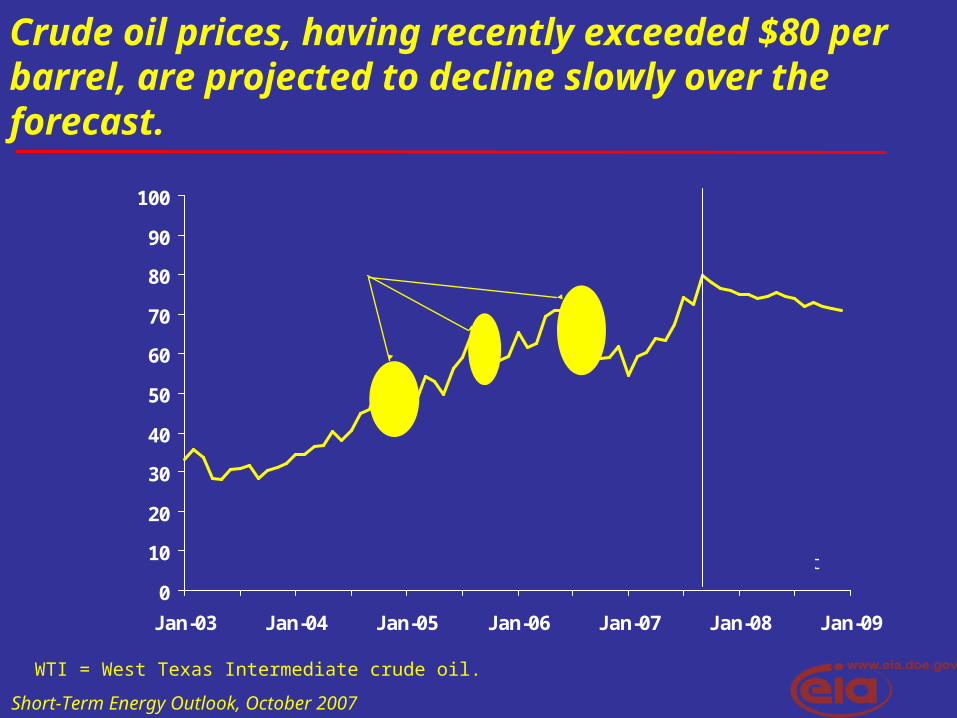

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

WTI Price

(Dollarsper

Barrel)

Forecast

Crude prices often decline just

prior to winter

Crude oil prices, having recently exceeded $80 per barrel, are projected to decline slowly over the forecast.

WTI = West Texas Intermediate crude oil.

Short-Term Energy Outlook, October 2007

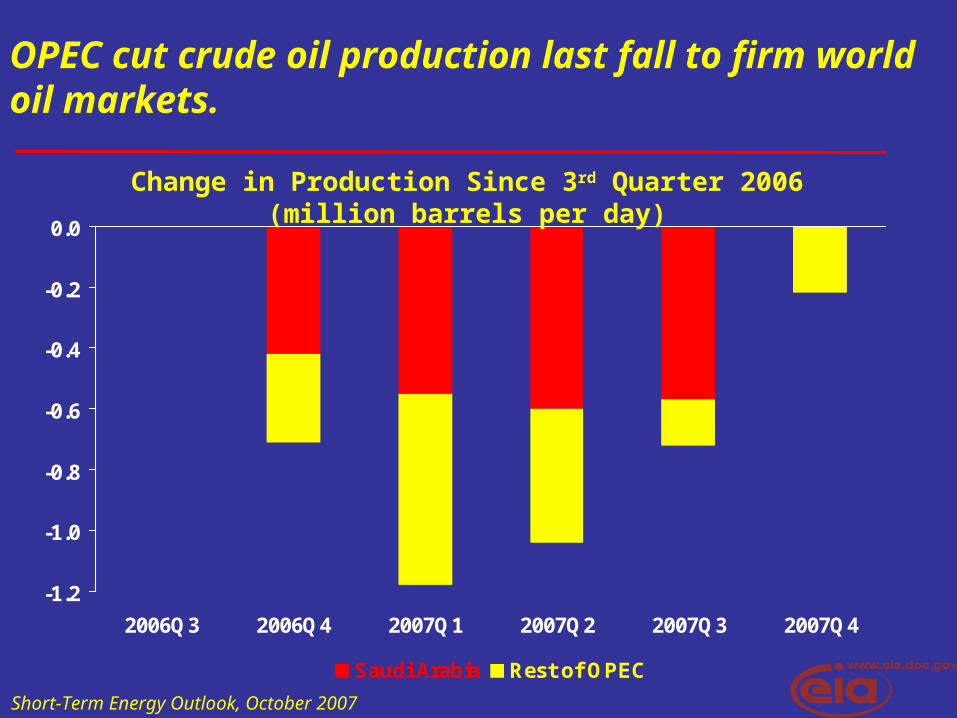

OPEC cut crude oil production last fall to firm world oil markets.

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

2006Q3 2006Q4 2007Q1 2007Q2 2007Q3 2007Q4

Saudi Arabia Rest of OPEC

Total OPEC

Change in Production Since 3rd Quarter 2006(million barrels per day)

Short-Term Energy Outlook, October 2007

OECD commercial stocks have fallen from record highs to near-normal levels.

-20

0

20

40

60

80

100

120

140

160

180

2006

Q1

2006

Q2

2006

Q3

2006

Q4

2007

Q1

2007

Q2

2007

Q3

2007

Q4

Difference From 5-Year Average(Million Barrels)

Short-Term Energy Outlook, October 2007

Market balance may loosen slightly in 2008.

0.2

1.1

1.4

1.8

2.0

1.4

1.11.0

0.80.9

0.1

0.5

0.3

0.6

1.3 1.3

1Q2007 2Q2007 3Q2007 4Q2007 1Q2008 2Q2008 3Q2008 4Q2008

Million Barrels per Day

World Oil Consumption Growth Non-OPEC Production Growth

Short-Term Energy Outlook, October 2007

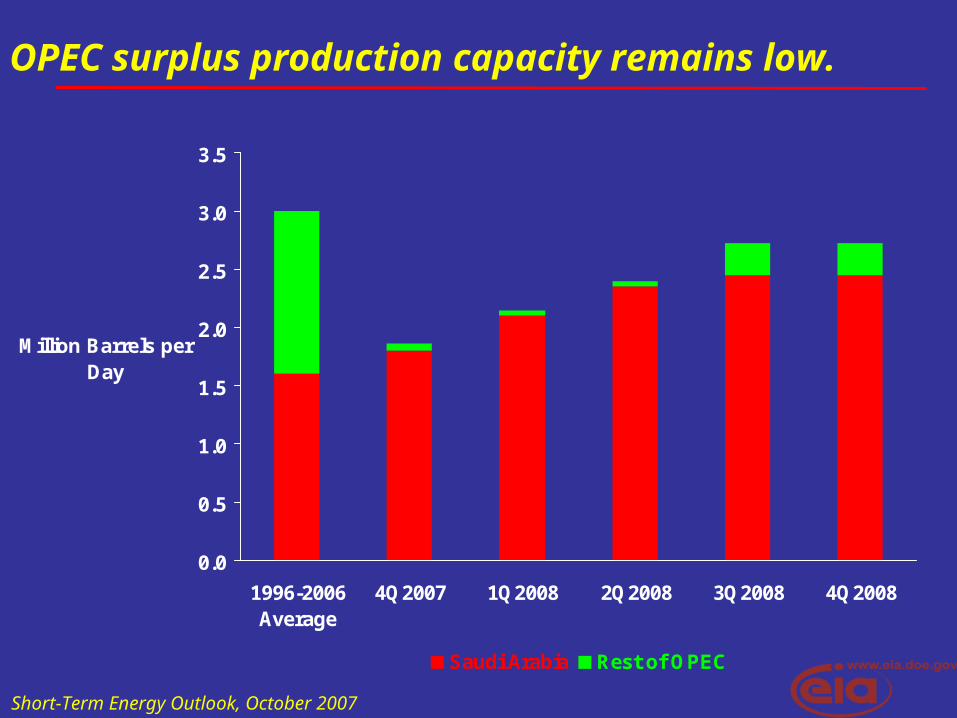

OPEC surplus production capacity remains low.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1996-2006Average

4Q2007 1Q2008 2Q2008 3Q2008 4Q2008

Million Barrels per Day

Saudi Arabia Rest of OPEC

Short-Term Energy Outlook, October 2007

Dollar-based economies have experienced higher oil prices than those with other currencies.

0

10

20

30

40

50

60

70

80

90

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07

West TexasIntermdiate(Dollars per

Barrel)

$ per barrel

€ per barrel

$79.91

€57.50

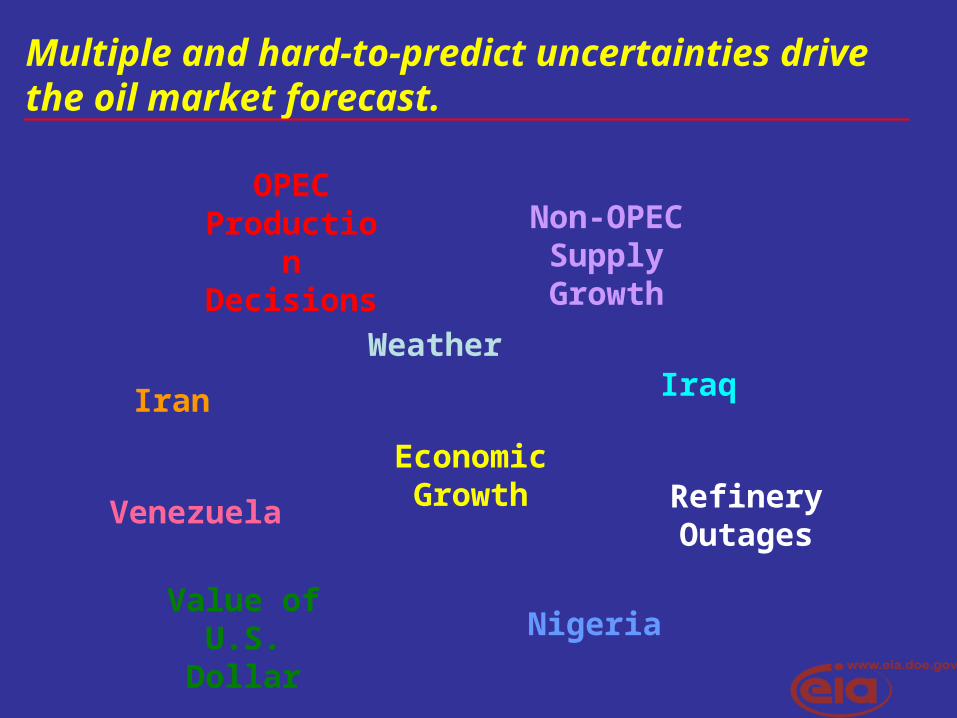

Multiple and hard-to-predict uncertainties drive the oil market forecast.

Weather

Non-OPEC Supply Growth

Iran Iraq

Economic Growth

OPEC Production Decisions

Nigeria

Venezuela

Value of U.S. Dollar

Refinery Outages

Short-Term Energy Outlook, October 2007

U.S. average fuel expenditures are expected to be higher for all fuels this winter, October – March.

Average Household Expenditures (Percent Change from Last Winter)

Fuel Base Case If 10% Warmer Than Forecast

If 10% Colder Than

Forecast

Natural Gas 9.5 -1.7 20.3

Heating Oil 21.8 9.8 31.6 Propane 16.3 4.3 27.7 Electricity 3.9 -1.3 7.2 Average Expenditures

9.8 0.1 18.4

Winter = October 1 through March 31.Expenditures are based on typical per household consumption adjusted for weather. Warmer and colder cases represent 10-percent decrease or 10-percent increase in heating degree-days, respectively.

Short-Term Energy Outlook, October 2007

Retail gasoline prices are projected to be higher in 2008.

0

50

100

150

200

250

300

350

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Centsper

Gallon

Forecast

Average Summer Price2006 $2.84 / gallon2007 $2.93 / gallon2008 $2.97 / gallon

Summer = April 1 through September 30.

Short-Term Energy Outlook, October 2007

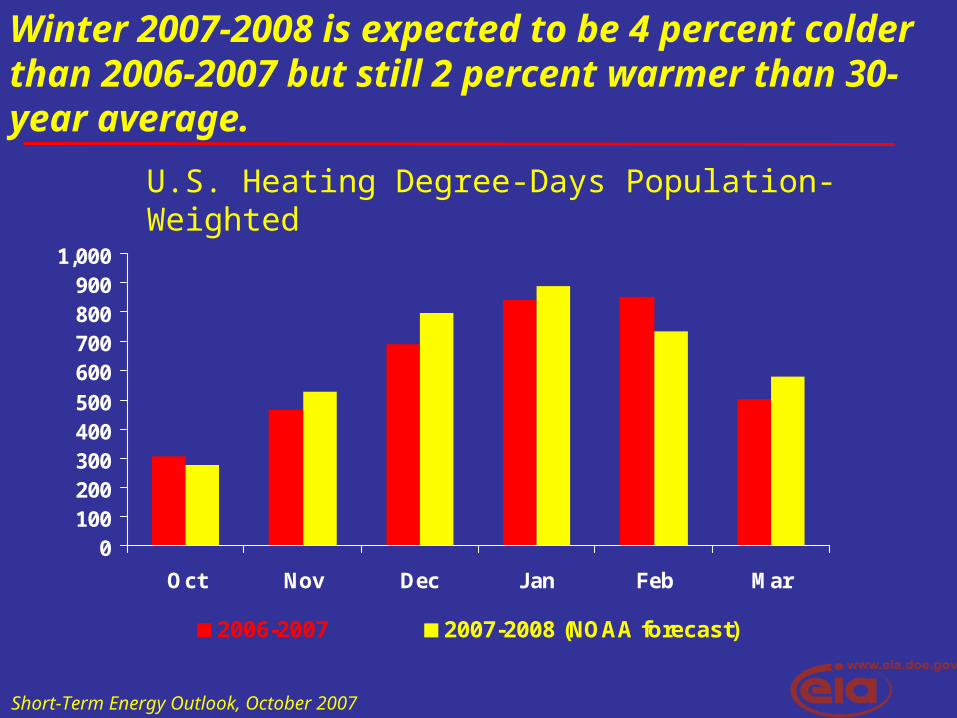

U.S. Heating Degree-Days Population-Weighted

Winter 2007-2008 is expected to be 4 percent colder than 2006-2007 but still 2 percent warmer than 30-year average.

0100200300400500

600700800900

1,000

Oct Nov Dec Jan Feb Mar

2006-2007 2007-2008 (NOAA forecast)

Short-Term Energy Outlook, October 2007

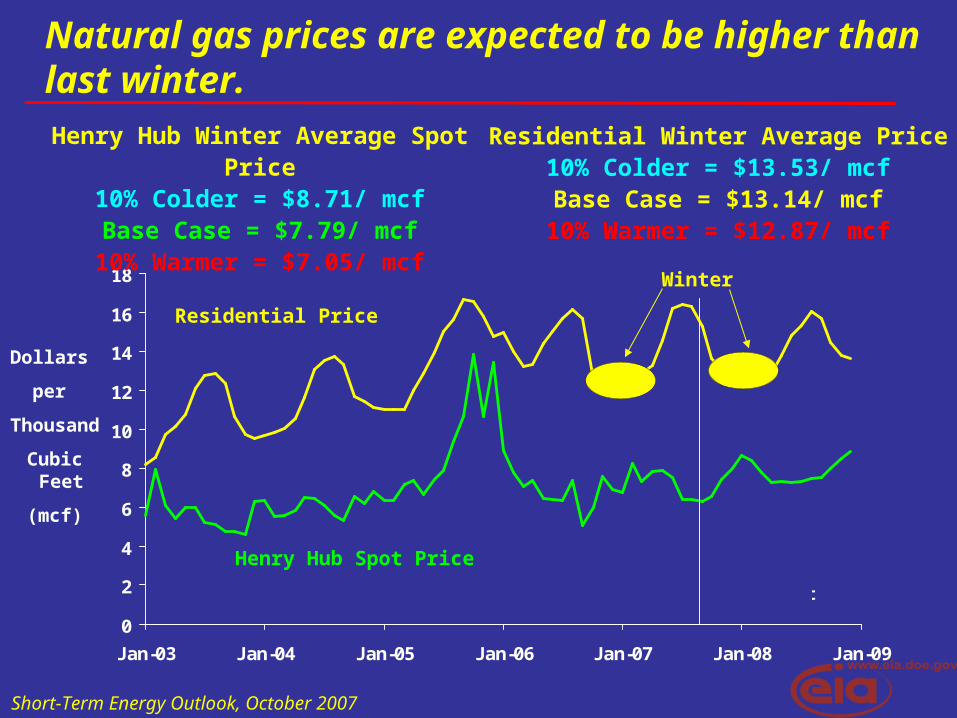

Natural gas prices are expected to be higher than last winter.

0

2

4

6

8

10

12

14

16

18

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Forecast

Henry Hub Winter Average Spot Price10% Colder = $8.71/ mcfBase Case = $7.79/ mcf

10% Warmer = $7.05/ mcf

Dollars

per

Thousand

Cubic Feet

(mcf)

Residential Winter Average Price10% Colder = $13.53/ mcfBase Case = $13.14/ mcf

10% Warmer = $12.87/ mcf

Residential Price

Henry Hub Spot Price

Winter

Short-Term Energy Outlook, October 2007

-800

-600

-400

-200

0

200

400

600

800

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Base Case 10% Colder 10% Warmer

Forecast

Deviation from 5-year Average (Billion Cubic Feet)

U.S. natural gas in storage is projected to remain above historical averages.

Short-Term Energy Outlook, October 2007

Natural gas heating bills are projected to be higher for all regions this winter.

Households using natural gas as primary heating fuel

58%

55%

79%

41%

66%

U.S.

Northeast

Midwest

South

West

Percent Change from Last Winter (Projected)

ConsumptionAverage

PriceTotal

Expenditures

West + 2 + 2 + 5

South + 1 + 9 + 11

Midwest + 3 + 8 + 11

Northeast + 6 + 4 + 10

U.S. Average + 3 + 6 + 10

Short-Term Energy Outlook, October 2007

Retail heating oil prices are projected to average about 40 cents per gallon higher than last winter.

0

50

100

150

200

250

300

350

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Centsper

Gallon

Forecast

October 2007 – March 2008 Average

10% Colder = $2.91/ gallon

Base Case = $2.88/ gallon

10% Warmer = $2.85/ gallon

Short-Term Energy Outlook, October 2007

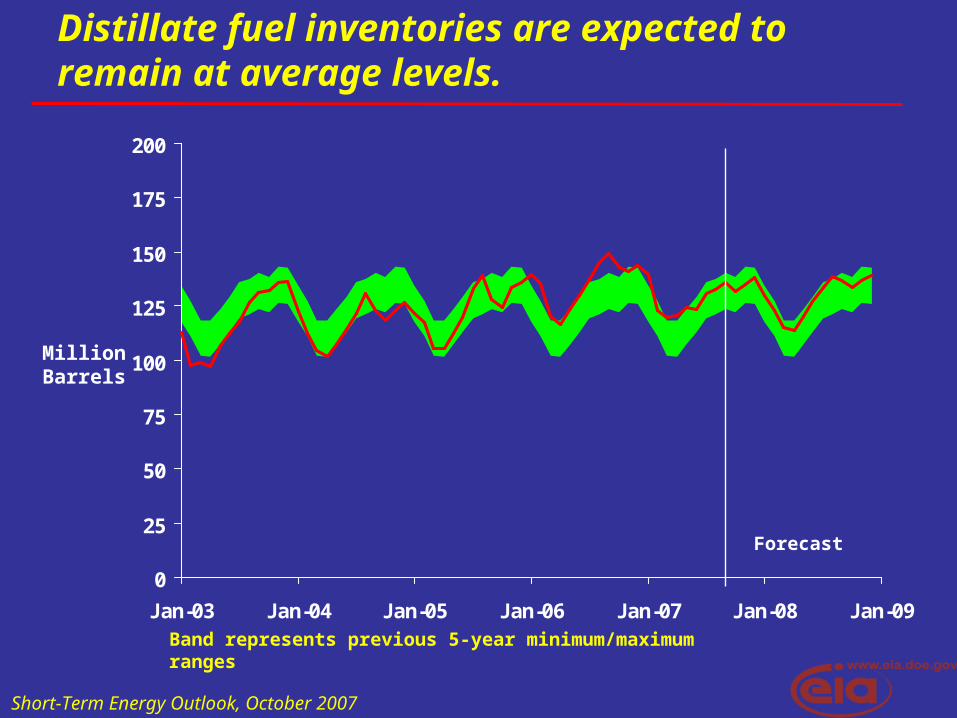

Distillate fuel inventories are expected to remain at average levels.

0

25

50

75

100

125

150

175

200

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Band represents previous 5-year minimum/maximum ranges

Forecast

MillionBarrels

Short-Term Energy Outlook, October 2007

U.S. winter heating oil expenditures projected to increase for all regions.

Percent Change from Last Winter (Projected)

ConsumptionAverage

PriceTotal

Expenditures

West + 4 + 13 + 18

South + 6 + 19 + 26

Midwest + 4 + 18 + 23

Northeast + 5 + 16 + 22

U.S. Average + 5 + 16 + 22

Households using heating oil as primary heating fuel

7%

3%

2%

1%

32%

U.S.

Northeast

Midwest

South

West

Short-Term Energy Outlook, October 2007

Residential propane prices are expected to average about 23 cents per gallon higher than last winter.

0

50

100

150

200

250

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Centsper

Gallon

Forecast

October 2007 – March 2008 Average10% Colder = $2.34/ gallonBase Case = $2.28/ gallon

10% Warmer = $2.20/ gallon

Short-Term Energy Outlook, October 2007

Propane inventories are low.

0

10

20

30

40

50

60

70

80

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

History / Base Case 10% Colder

10% Warmer

Colored green bands represent normal range published in Energy Information Administration, Weekly Petroleum Status Report.

Short-Term Energy Outlook, October 2007

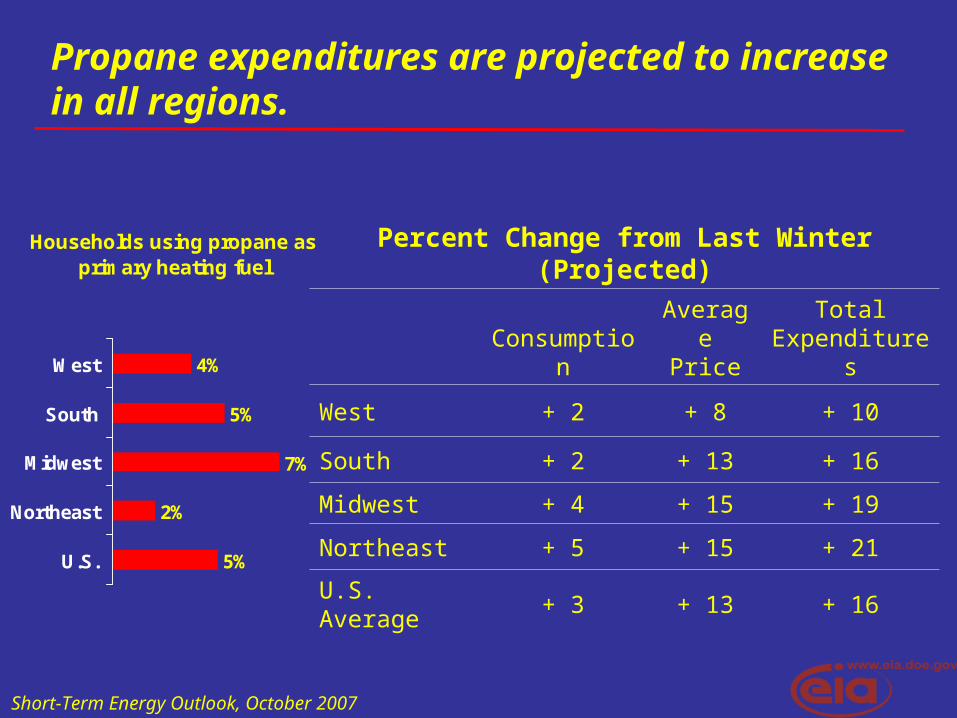

Propane expenditures are projected to increase in all regions.

Percent Change from Last Winter (Projected)

ConsumptionAverage

PriceTotal

Expenditures

West + 2 + 8 + 10

South + 2 + 13 + 16

Midwest + 4 + 15 + 19

Northeast + 5 + 15 + 21

U.S. Average + 3 + 13 + 16

Households using propane as primary heating fuel

5%

2%

7%

5%

4%

U.S.

Northeast

Midwest

South

West

Short-Term Energy Outlook, October 2007

Winter electricity expenditure increases are expected to be smaller than other fuels.

Percent Change from Last Winter (Projected)

ConsumptionAverage

PriceTotal

Expenditures

West + 2 + 4 + 5

South + 1 + 2 + 3

Midwest + 2 + 2 + 4

Northeast + 4 + 3 + 7

U.S. Average + 2 + 2 + 4

Households using electricity as primary heating fuel

30%

11%

11%

52%

30%

U.S.

Northeast

Midwest

South

West

Short-Term Energy Outlook, October 2007

Summary

• On average, U.S. households will pay about $88, or 10 percent, more for heating this winter.

• Higher expenditures are driven by higher fuel prices and weather-

related increases in consumption.

• Under the baseline forecast, natural gas expenditures could be about $78, or 10 percent, higher for the average U.S. household this winter.

• Heating oil expenditures are projected to be about $319, or 22 percent, higher for the average U.S. household this winter.

• Electricity expenditures are forecasted to be $32, or 4 percent, higher for the average U.S. household this winter.

• A colder winter would raise estimated expenditures somewhat from those of the base case.

Short-Term Energy Outlook, October 2007

Guy F. Caruso

Periodic Reports

Petroleum Status and Natural Gas Storage Reports, weekly

Short-Term Energy Outlook, monthly

Annual Energy Outlook 2007, February 2007

International Energy Outlook 2007, May 2007

Examples of Special Analyses

“Economic Effects of High Oil Prices,” Annual Energy Outlook 2006

Analysis of Oil and Gas Production in the Arctic National Wildlife Refuge,

March 2004

The Global Liquefied Natural Gas Market: Status and Outlook, December 2003

“Impacts of Increased Access to Oil and Natural Gas Resources in the Lower 48 Federal Outer Continental Shelf,” Annual Energy Outlook 2007

www.eia.doe.gov