shale gas treatment challenges and requirements gas treatment challenges and requirements . ... uop...

TRANSCRIPT

© 2013 UOP LLC. All rights reserved.

Hanbing Ding

13th U.S.-China Oil & Gas Industry Forum September 25, 2013 Xi’an, China

Shale Gas Treatment Challenges and Requirements

Honeywell’s Businesses $37.6 billion in revenues in 2012, 50% outside of U.S. Nearly 122,000 employees operating in 100 countries 19,000 engineers and scientists A Fortune 100 company with Morristown, NJ global corporate headquarters

Aerospace Automation &

Control Solutions

Performance Materials &

Technologies Transportation

Systems

UOP 6084A-2 2

UOP Offers to the Oil and Gas Industry Upstream Midstream Downstream

Exploring for, drilling for and producing crude oil

and natural gas

Processing, storage and transportation

Refining and converting oil / gas into end products such as

fuels and chemicals

UOP technology, materials and services

enable natural gas resource development

UOP processing technology,

equipment, materials and services

3

Shale Resource Processing Challenges

4

Gas Value Chain Challenges • Supply diversification

– LNG, biogas, shale gas, tight gas, SNG, CBM, and conventional gas vary in quality and composition

– Unconventional gas quality in China will most certainly vary between and within fields

• Demand diversification – Pipeline network delivers to customers with varying needs – Stranded gas brings additional challenges

• Agile and flexible solutions required

5

Lessons from U.S. Shale Gas Variability

Well C1 C2 C3 CO2 N2

1 80.3 8.1 2.3 1.4 7.9 2 81.2 11.8 5.2 0.3 1.5 3 91.8 4.4 0.4 2.3 1.1 4 93.7 2.6 0.0 2.7 1.0

Well C1 C2 C3 CO2 N2

1 79.4 16.1 4.0 0.1 0.4 2 82.1 14.0 3.5 0.1 0.3 3 83.8 12.0 3.0 0.9 0.3 4 95.5 3.0 1.0 0.3 0.2

Barnett Shale Gas Composition Marcellus Shale Gas Composition

Well C1 C2 C3 CO2

1 87.7 1.7 2.5 8.1 2 88.0 0.8 0.8 10.4 3 91.0 1.0 0.6 7.4 4 92.8 1.0 0.6 5.6

Well C1 C2 C3 CO2 N2

1 27.5 3.5 1.0 3.0 65.0 2 57.3 4.9 1.9 0.0 35.9 3 77.5 4.0 0.9 3.3 14.3 4 85.6 4.3 0.4 9.0 0.7

New Albany Shale Gas Composition Antrim Shale Gas Composition

“Microbial production and modification of gases in sedimentary basins: A geochemical case study from a Devonian shale gas play”, AAPG Bulletin, Vol 87, No. 8 (August 2003)

“Oil and gas geochemistry and petroleum systems of the Fort Worth basin”, AAPG Bulletin, Vol. 91, No. 4 (April 2007)

“Compositional variety complicates processing plans for US shale gas”, Oil & Gas Journal, March 9, 2009

“Identification of microbial and thermogenic gas components from Upper Devonian black shale cores, Illinois and Michigan basins”, AAPG Bulletin, Vol 92, No. 3 (March 2003)

6 Variations in C2, C3, CO2, Nitrogen, and Other Components

in Shale Gas Impact Interchangeability with Other Gas Supplies 6

-20%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

$80 WTI $70 WTI $60 WTI

US High Rates of Return in Liquids-Rich Plays Driving Activity

DRY WET

Liquid rich field plays are forecasted to generate over 75% of incremental gas in USA (+4 TCF) over next 6 years

Rat

e of

Ret

urn

GPM 4-9 4-9 4-7 8-13 4-9 3-9 4-9 3-9 1-2 1-2 1-2 <1 <1

All Wet US Gas Plays Drive >20% Return at Current Prices

DRY

HH Dry Gas Price = $3.00/MMBTU NGL Price = 40% WTI

7

Gas Plant Development: Decision Criteria

Contaminants

By-Products Products Opp. Efficiency Consumption Disposal

Acid Gases: CO2, H2S, Mercaptan, COS Other: Mercury, Arsenic, Nitrogen, Water

Availability Flexibility

Energy Chemicals Labor

Air Water Subsurface

Methane Ethane Propane Butanes C5

+ condensate Oil

Sales gas / LNG NGL’s Spec products C5

+ condensate

Upstream Factors

Downstream Factors

Plant Configuration & Design Decisions: Gas Processing Functional Blocks

Compression Acid Gas Removal

Sour Gas Removal

Hydrocarbon Management Dehydration

Other Contaminant

Removal Utilities & Disposal

HC Distribution

Production Profile

Pressure, Flow

Ambient Conditions

Offshore/ Onshore

Environmental Constraints

Fiscal Regime

Midstream Factors

UOP 6084B-8 8 Many Factors Impact Selection of Gas Processing Technologies 8

Integrated Solutions Offer Operating & Investment Flexibility

Decision Tree Logic Summary

1) Select the proper technology within each separate gas processing block

2) Account for interactions across the different processing blocks

3) Adjust sequence of processing blocks for overall system optimization

9

No One Size Fits All Solution for Acid Gas Removal

Acid Gas Removal Technologies

Partial Pressure Acid Gas in Product, psia

Parti

al Pr

essu

re A

cid G

as in

Fee

d, p

sia

Amine Process

Membrane Systems

Physical Solvent Process

Molecular Sieves

10

Maximize value of gas projects with speed of implementation Monetize methane and natural gas liquids

Imperatives

1

2

11

QUICKLY Monetize the Widest Possible Range of Natural Gas Compositions at The Lowest Installed Cost

Rapid NGL Recovery is Paramount

Procurement Begins at Order Date

Flexibility in Feed Composition

Reduced Engineering

Subvendor Delivery Optimization

Reduced Field Construction

In-Parallel Field Skid Construction

Skid Mounted Mobility

12

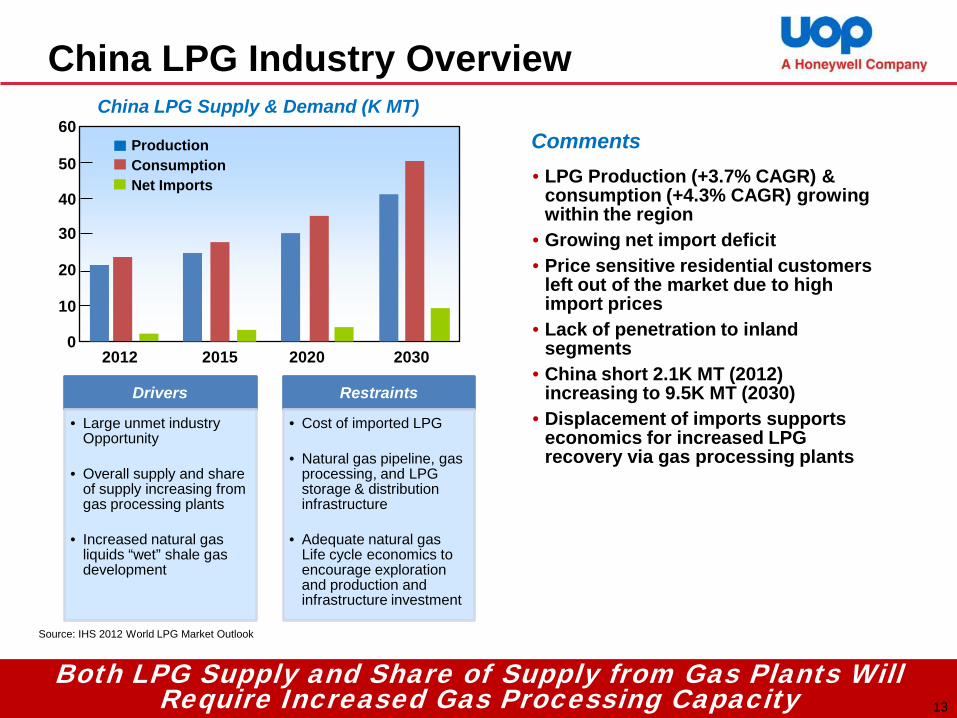

Both LPG Supply and Share of Supply from Gas Plants Will Require Increased Gas Processing Capacity

China LPG Industry Overview

Drivers

• Large unmet industry Opportunity

• Overall supply and share of supply increasing from gas processing plants

• Increased natural gas liquids “wet” shale gas development

Restraints

• Cost of imported LPG

• Natural gas pipeline, gas processing, and LPG storage & distribution infrastructure

• Adequate natural gas Life cycle economics to encourage exploration and production and infrastructure investment

Source: IHS 2012 World LPG Market Outlook

• LPG Production (+3.7% CAGR) & consumption (+4.3% CAGR) growing within the region

• Growing net import deficit • Price sensitive residential customers

left out of the market due to high import prices

• Lack of penetration to inland segments

• China short 2.1K MT (2012) increasing to 9.5K MT (2030)

• Displacement of imports supports economics for increased LPG recovery via gas processing plants

Comments China LPG Supply & Demand (K MT)

2012 2015 2020 2030

60

50

40

30

20

10

0

Production Consumption Net Imports

13

• Typical example of revenue associated with NGL recovery • 200 MMSCFD of 3 GPM gas (~1,100 BTU/SCF) • Monthly revenue: 5.8 MM$

Methane

Ethane

Propane

n-Butane

i-Butane

Natural Gasoline

Shale Gas

200 million cubic feet per day

(MMcf/d)

Barrel Comp

67%

15%

4%

5%

9%

Example Price

Basis1

Fuel Value

Fuel Value

$950 MT

$950 MT

$700 MT

$950 MT

Value over fuel $M/month

$0.0

$0.0

$1.2

$1.5

$2.5

$4.3

1. Average fuel gas value $9/mmbtu

Amount Generated Monthly

$9.5MM

UOP Modular Plants – Delivered Faster, Adding Value, No Schedule impact

Rapid NGL Recovery Improves Return on Investment

@ 3

GP

M N

GL’

s

14

Rapid Gas Value Possible

Modular Design

Modular Pre-Engineered Plants

Speed to Gas Your Plant Installed in 19 Weeks

15

Factory Built and Ready for Installation

UOP Cryogenic Plant Skids

16

Plant Case Study:

Marcellus Basin

Scenario: A natural gas processing company was concerned that it was unable to service existing customers and capture future opportunities in the Marcellus, a rapidly expanding geographical area. The company did not have enough processing capacity, and the lead time for a custom facility was too long. UOP solution: With a modular, pre-engineered design, a Honeywell UOP Russell cryogenic plant could be delivered in half the time of a custom plant. Results: As a result, the natural gas processing company completed the project on time and within budget. This allowed for the rapid capture of future business opportunities by expanding to multiple trains for processing and fractionation. The customer improved their returns by an estimated $2-5 million for every additional day that each train of their plant was up and running

17

Nat Gas Conditioning

Dehydration • Mol Sieve Adsorption • Glycol (TEG, DEG) Absorption

Acid Gas Treatment • Amine Units (100-1000 gpm1) • Membrane Units (1+ BCFD) Sulfur Recovery • Modular Claus (10-100+ LTPD) • Sulfur Scavengers Hg Removal Units

Rich Gas Conditioner

Fractionation Deethanizer / Depropanizer / Debutanizer

1gpm = gallons of amine per minute

SEG

MEN

T NGL Recovery NGL Upgrading

GAS

NG

L C

ON

TEN

T (G

PM2 )

Mechanical Refrigeration

Cryogenic Turboexpander

UOP Equipment Lines O

FFER

ING

DeEnthanizer DePropanizer DeButanizer Butane Splitter

Natural Gasoline

I-Butanes

N-Butanes

Mix-Butanes

Propane Purity Ethane

Y-GR

ADE

OR R

AW M

IX

2GPM = gallons of NGL per thousand scf of natural gas

9

6

4

3

2

UOP 6084C-18 Complete Modular Equipment Solution 18

Methane and NGL Monetization Options

Methane

Deet

hani

zer

Depr

opan

izer

Debu

tani

zer

Ethane

Propane

Butane

Natural Gasoline

Shale Gas

Dem

etha

nize

r

2

Gas Field

Upgrade to Higher Value Products 19

Upgrade Methane to Transportation Fuel

Component Mol% (typical)

Methane (C1) 85-95%

Ethane (C2) 5-10%

Propane (C3) 2-5%

Butane+ (C4+) 2-3%

Carbon Dioxide (CO2) 1-4%

Trace Components H2S, Hg, R-SH, COS

Pipeline Feed (gas inlet) Typical Gas Specification

Component Mol % (max)

Methane (C1) >95%

Ethane (C2) <6-8%

Propane (C3) <3%

Butane 1ppmv

Carbon Dioxide (CO2) 50ppm

Pentane & Heavier <0.1mol%

Heating Value

•1050 btu/scf (Europe & US) •1140 btu/scf

(Asia, max)

LNG Product Specifications

LNG Feedstock Gas Pretreatment

& Liquefaction

Small Scale LNG as Virtual Pipeline and as Substitute for Diesel…After Pretreatment

20

Upgrade Methane to Olefins

• Methanol-to-Olefins (MTO) is now a reality in China • >20 MTO projects in various stages of D&C • UOP’s work in MTO dates back to 1980’s • UOP has 4 UOP licensed plants in China • First UOP Advanced MTO Process Unit to s/u in 2013

MTO Ethylene & Propylene ($1300/MT)

Natural Gas – $3-6/MMBtu ($140-240/MT)

Synthesis Gas

Production

Methanol Synthesis

Coal ($25-100/MT)

Picture of UOP Advanced MTO Process at Wilson Clean Energy 21

0

20

40

60

80

100

120

140

2001 2006 2011 2016 2021

Supply from Refinery FCCsSupply from Steam CrackersDemand (Polymer/Chemical Gr.)

“Propylene Gap” is growing – Propylene demand growing at ~4%

CAGR – Crackers shifting to lighter

feedstocks, with less propylene – “On-Purpose Propylene” to fill the

gap; MTO and PDH

“Propylene Gap”

Data Source: IHS Chemical

Propylene Supply / Demand (MMTPA)

Global Propylene Gap PDH - Propane Dehydro

Monetize Propane to Propylene

C3

Hydrogen

C3=

“Single Feed – Single Product” enables simple project execution Excellent forward or back integration 14 operating PDH plants world-wide

(9 utilize UOP’s Oleflex Process) New unit activity focused in China

and North America UOP has 16 PDH awards since 2011

UOP OleflexTM Process

$500/MT – $800/MT

$1300/MT

Oleflex™ - A Key Technology for Filling Propylene Gap 22

Alternate Products ETBE HPIB MMA Isoprene

Fresh Methanol

Net Gas

MTBE

C4 LPG

C5+

DIB Column

ButamerTM Unit

DeC3 Column

C3-

EthermaxTM Unit

CSP ORU

Oleflex Unit

nC4 → iC4

iC4 → iC4=

Monetize Butanes to Fuels & Petrochemicals

6 Commissioned MTBE Complexes with UOP Oleflex Process 7 New C4 Oleflex Awards since 2011

4 mixed C3/C4 Oleflex Units – “Best of Both Worlds”

$800- 900/MT

$375/MT

$1150/MT

23

Hanbing Ding,Sr. Sales Leader O: +86 10 8432 3928 M: +86 186 1833 6085 F: +86 10 6437 6616 E: [email protected] Victor Wen, Sr. Sales Manager O: +86 10 8432 3982 M: +86 139 1172 6957 F: +86 10 6437 6616 E: [email protected]

UOP Contacts in China

Thank You!

24