september 2015 realtors® confidence index

DESCRIPTION

This report is a key indicator of housing market strength based on a monthly survey sent to over 50,000 real estate practitioners.TRANSCRIPT

REALTORS® CONFIDENCE INDEX SURVEY Report on the September 2015 Survey

The REALTORS® Confidence Index (RCI) report provides monthly information about real estate market conditions and expectations, buyer/seller traffic, price trends, buyers’ characteristics, and issues affecting real estate based on a monthly survey of REALTORS®.

The September 2015 report is based on the responses of 3,068 REALTORS® about local market conditions experienced in September and the characteristics of their most recent sale for the month. The data collected from a random sample of REALTORS® is viewed to be representative of the sales for the month.1 The online survey was conducted from October 1-11, 2015. All real estate is local: conditions in specific markets may vary from the overall national trends presented in this report. REALTORS® may be interested in comparing their markets against the national summary.

The RCI report is an output of the Research Division of the NATIONAL ASSOCIATION of REALTORS®.2 For questions or information about this report, please email [email protected].

Lawrence Yun, Senior Vice President and Chief Economist Danielle Hale, Managing Director, Housing Research Gay Cororaton, Research Economist Meredith Dunn, Research Communications Manager

Research Division NATIONAL ASSOCIATION of REALTORS® 500 New Jersey Avenue, NW Washington, DC 20001 202.383.1000

1 The survey is sent to 50,000 REALTORS® who are selected through simple random sampling. To increase the response rate, the survey is also sent to respondents in the previous three surveys who provided their email addresses. The number of responses to a specific question varies because the question may not be applicable to the respondent or because of non-response. To encourage survey participation, eight REALTORS® are randomly selected to receive a gift card. 2 Thanks to Jessica Lautz, Director, Survey Research and Communications, and Amanda Riggs, Research Survey Analyst, for their comments in improving the survey and in editing the report.

1

Table of Contents

Summary .................................................................................................................................................... 3

I. Market Conditions .................................................................................................................................. 4

REALTORS® Broadly Reported an Improving Market Compared to a Year Ago .................................. 4

REALTORS® Still Broadly Optimistic Over the Next Six Months .......................................................... 4

REALTORS® Reported Stronger Buyer and Seller Traffic Compared to a Year Ago ............................. 7

REALTORS® Expect Prices to Increase Modestly in Next 12 Months .................................................. 10

Properties On the Market at 49 Days ...................................................................................................... 11

II. Buyer and Seller Characteristics ......................................................................................................... 14

Sales to First-time Buyers: 29 Percent of Sales ...................................................................................... 14

Sales for Investment Purposes: 13 Percent of Sales ............................................................................... 14

Distressed Sales: Seven Percent of Sales ................................................................................................ 15

Cash Sales: 24 Percent of Sales .............................................................................................................. 17

International Transactions: Less than Two Percent of Residential Market ............................................ 19

Age, Previous Residence, and Type of Property Purchased ................................................................... 20

III. Current Issues .................................................................................................................................... 21

Demand for Rentals Remain Strong ....................................................................................................... 21

Credit Conditions Still Generally Tight .................................................................................................. 23

Contract Settlement Issues: Financing and Appraisals are Major Issues ................................................ 25

2

Summary

The information provided by REALTORS® based on their client interactions indicates that market activity broadly improved in September 2015 compared to a year ago. Compared to August 2015, market activity slowed, in part due to the seasonal downturn after the spring and summer months. On one hand, sustained job growth and low interest rates, with the 30-year fixed mortgage rate back to less than four percent in September, appeared to be boosting demand. On the other hand, the lack of inventory and high home prices were reported to be moderating demand, although some REALTORS® reported declining prices in their areas.

The confidence indices for current conditions and the six-month outlook for single-family, townhome, and condominium properties all increased compared to a year ago but decreased compared to last month, partly due to the seasonal drop in demand.The buyer traffic index also increased compared to a year ago, while the seller traffic index stayed below 50, an indication of tight supply across many local markets. First-time home buyers accounted for 29 percent of sales, the same as last year. Approximately 11 percent of respondents worked with a potential buyer who was previously involved in a foreclosure or short sale. Cash sales made up 24 percent of sales, purchases for investment purposes accounted for 13 percent of sales, and distressed properties dropped to seven percent of sales. Compared to a year ago, properties sold faster, typically at 49 days nationally. It typically took another 35 days to close the sale.

Tight inventories, decreasing affordability, continued tight mortgage availability, and slow/excessively conservative appraisals were the main issues reported by respondents. Approximately 92 percent of respondents reported taking measures to be ready for the implementation of the new disclosure regulations (that took effect on October 3, 2015) such as attending seminars, coordinating with lenders, advising clients, and revising model contracts in line with the new TILA-RESPA guidelines.

September 2015 REALTORS® Confidence Index Survey Highlights Sept 2015 Aug 2015 Sept 2014 RCI Current Conditions: Single-Family Sales 61 66 51 RCI Six-Month Outlook: Single-Family Sales 62 66 53 RCI Buyer Traffic Index 53 60 44 RCI Seller Traffic Index 41 45 39 First-Time Buyers, as Percent of Sales1 29 32 29 Sales to Investors, as Percent of Sales 13 12 14 Cash Sales, as Percent of Sales 24 22 24 Distressed Sales, as Percent of Sales 7 7 10 Second/ vacation homes, as Percent of Sales 9 9 10 Relocation Buyers, as Percent of Sales 14 14 13 Median Days on Market 49 47 56 Median Expected Price Growth in Next 12 Months (%) 3.2 3.5 3.1 1 - NAR’s 2014 Profile of Home Buyer and Sellers (HBS) reports that among primary residence home buyers, 33 percent were first-time home buyers. The HBS surveys primary residence home buyers, while the monthly RCI Survey surveys REALTORS® and also captures purchases for investment purposes and vacation/second homes.

3

I. Market Conditions

REALTORS® Broadly Reported an Improving Market Compared to a Year Ago

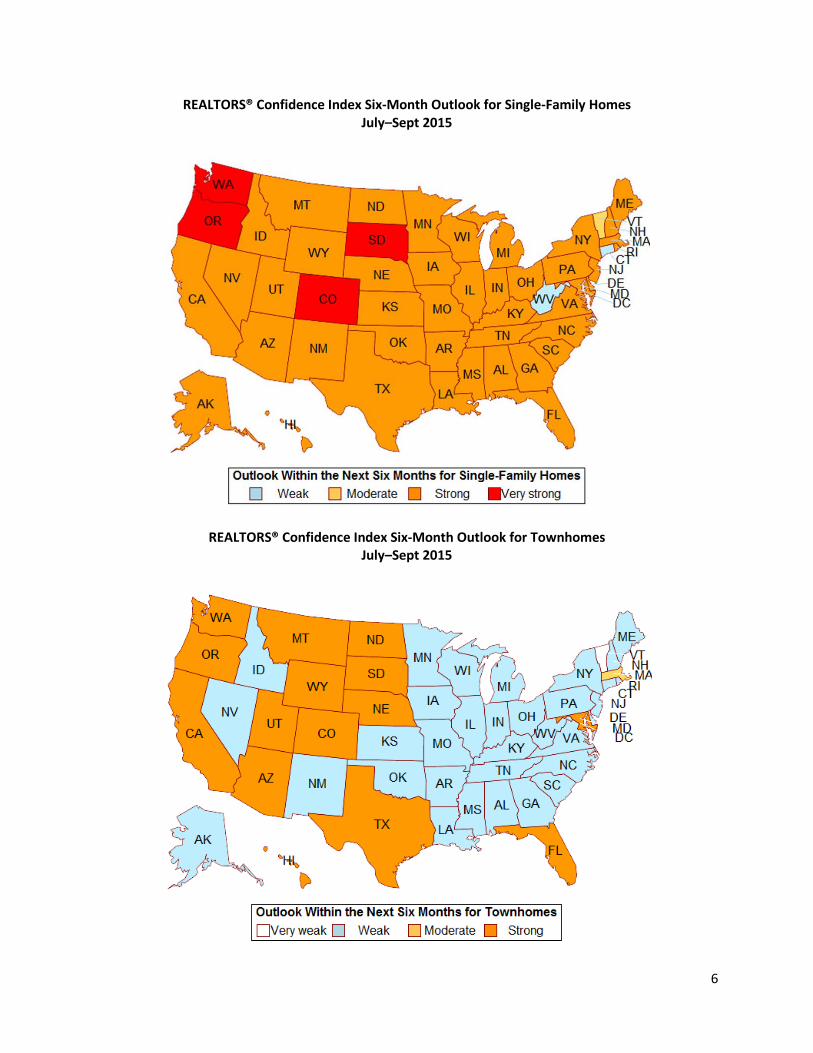

Market conditions vary across local markets and states, but REALTORS® generally reported improving market activity in September 2015 compared to a year ago.3 Compared to August 2015, REALTORS® reported a seasonal slowdown which is normal at this time of the year. The REALTORS® Confidence Index - Current Conditions chart below shows that single-family homes stood at 61 on the index (66 in August 2015; 51 in September 2014). The indices for townhomes and condominiums increased compared to their levels a year ago, but were below 50, indicating more respondents viewed their markets as “weak” than “strong.” REALTORS® continued to report on the difficulty of obtaining financing for condominium unit purchases because many condominiums are not FHA or GSE eligible.4 Sustained job growth and low interest rates, with the 30-year fixed mortgage rate back to less than four percent in September, were reported to be sustaining demand.

REALTORS® Still Broadly Optimistic Over the Next Six Months

In September 2015, REALTORS® were by and large “strongly” confident about the outlook over the next six months for single-family homes compared to a year ago although less so than in August 2015.5 The REALTORS® Confidence Index - Six-Month Outlook registered at 62 (66 in

3 This is a diffusion index which measures the direction of and broadness of the respondents’ market conditios or confidence. An index of 50 indicates a balance of respondents having “weak” (index=0) and “strong” (index=100) expectations or all respondents having moderate (=50) expectations. The index is not adjusted for seasonality effects. 4 FHA and the GSEs have financing eligibility criteria relating to ownership occupancy requirements, delinquent dues, project approval process, and use for commercial space. See the Statement of NAR Submitted for the Record to the Senate Committee Housing and Banking Affairs on December 9, 2014 at http://www.ksefocus.com/billdatabase/clientfiles/172/1/2180.pdf 5 Respondents were asked “What are your expectations for the housing market over the next six months compared to the current state of the market in the neighborhood(s) or area(s) where you make most of your sales?”

61

43

40

0

20

40

60

80

2008

0120

0805

2008

0920

0901

2009

0520

0909

2010

0120

1005

2010

0920

1101

2011

0520

1109

2012

0120

1205

2012

0920

1301

2013

0520

1309

2014

0120

1405

2014

0920

1501

2015

0520

1509

REALTORS® Confidence Index: Current Conditions as of Sept 2015

(50 = "Moderate" Conditions)

Single-family Townhome Condominium

4

August 2015; 53 in September 2014). Confidence indices for townhomes and condominiums also rose, but stayed at below 50, indicating that more respondents viewed their markets as “weak” than “strong.” The respondents expressed concern that the TILA-RESPA Integrated Disclosure (TRID) regulations may lead to delayed closings. The TRID regulations will apply to mortgages for which the application was submitted on or after October 3, 2015.6 To prepare for the change, approximately 92 percent of respondents reported taking steps such as attending education seminars, meeting with lenders, advising clients, and revising model contract forms that include extending the number of days to close to allow for unexpected circumstances.

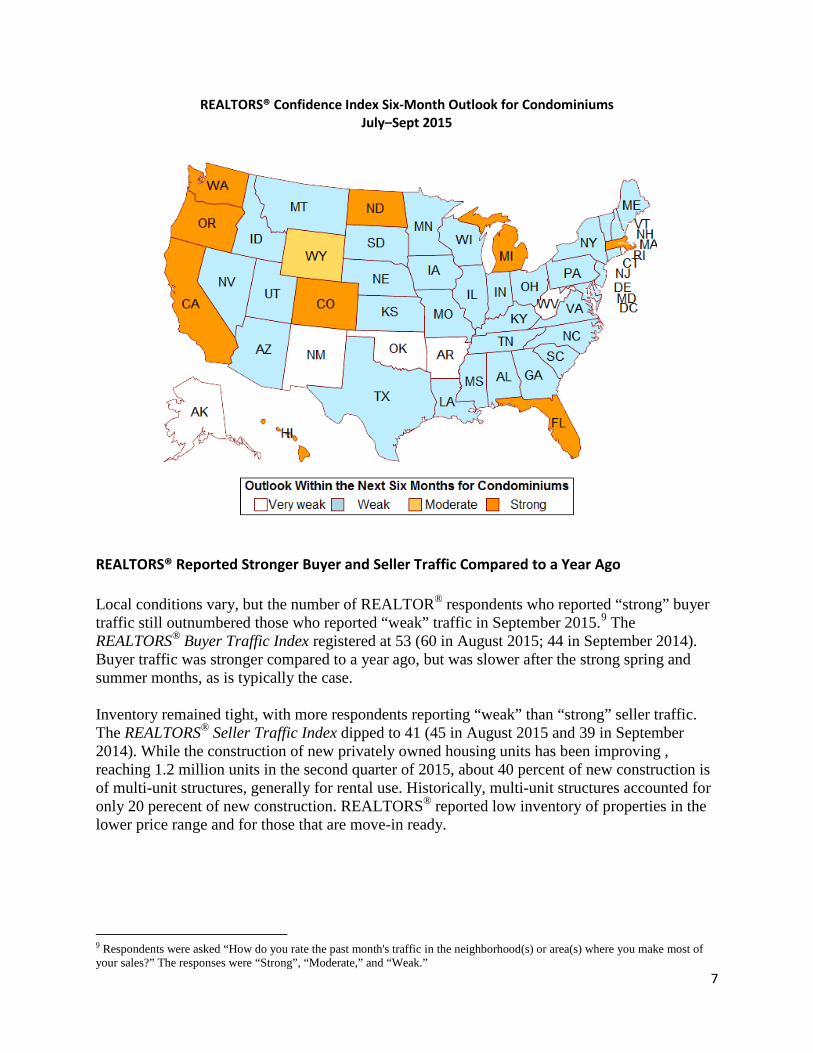

The following maps show the REALTORS® Confidence Index - Six-Month Outlook across property types by state.7 The outlook for single-family homes was broadly “strong” across most states and was most upbeat in Washington, Oregon, Colorado, and South Dakota. In the townhomes market, markets were broadly “strong” in the West region and in Florida, Maryland, and the District of Columbia. The condominium market remains broadly “weak” in many states, but was strong in California, Oregon, Washington, North Dakota, Colorado, Wyoming, Michigan, Massachusetts, and Florida. California, Oregon, Washington, Colorado are experiencing strong job growth and population migration, while Texas and North Dakota appear to be resilient amid the fall in oil prices. REALTORS® have reported difficulty in accessing condominium unit purchase financing for both FHA-insured and the GSE-backed loans. Only 20 percent of condominiums are eligible for FHA condominium unit financing because of strict eligibility criteria such as those pertaining to occupancy requirements and delinquency dues.8

6 TRID prescribes simplified disclosure forms that the lender needs to deliver to the loan applicant after a loan application is received (Loan Estimate) and before a loan is consummated (Disclosure Form) within prescribed business days and waiting periods. The objective is to help consumers understand the key features, costs, and risks of the mortgage loan for which they are applying. See the Consumer Financial Protection Bureau’s guidelines at http://www.consumerfinance.gov/regulatory-implementation/tila-respa/ 7 The market outlook for each state is based on data for the last three months to increase the observations for each state. Small states such as AK, ND, SD, MT, VT, WY, WV, DE, and D.C., may have less than 30 observations. 8 http://www.realtor.org/topics/condominiums/condominium-resource-book

62

45

42

0

20

40

60

80

2008

0120

0805

2008

0920

0901

2009

0520

0909

2010

0120

1005

2010

0920

1101

2011

0520

1109

2012

0120

1205

2012

0920

1301

2013

0520

1309

2014

0120

1405

2014

0920

1501

2015

0520

1509

REALTORS® Confidence Index: Six-Month Outlook as of Sept 2015

(50 = "Moderate" Outlook)

Single-family Townhome Condominium

5

REALTORS® Confidence Index Six-Month Outlook for Single-Family Homes July–Sept 2015

REALTORS® Confidence Index Six-Month Outlook for Townhomes July–Sept 2015

6

REALTORS® Confidence Index Six-Month Outlook for Condominiums July–Sept 2015

REALTORS® Reported Stronger Buyer and Seller Traffic Compared to a Year Ago Local conditions vary, but the number of REALTOR® respondents who reported “strong” buyer traffic still outnumbered those who reported “weak” traffic in September 2015.9 The REALTORS® Buyer Traffic Index registered at 53 (60 in August 2015; 44 in September 2014). Buyer traffic was stronger compared to a year ago, but was slower after the strong spring and summer months, as is typically the case. Inventory remained tight, with more respondents reporting “weak” than “strong” seller traffic. The REALTORS® Seller Traffic Index dipped to 41 (45 in August 2015 and 39 in September 2014). While the construction of new privately owned housing units has been improving , reaching 1.2 million units in the second quarter of 2015, about 40 percent of new construction is of multi-unit structures, generally for rental use. Historically, multi-unit structures accounted for only 20 perecent of new construction. REALTORS® reported low inventory of properties in the lower price range and for those that are move-in ready.

9 Respondents were asked “How do you rate the past month's traffic in the neighborhood(s) or area(s) where you make most of your sales?” The responses were “Strong”, “Moderate,” and “Weak.”

7

In most states, the number of respondents who reported “strong” buyer traffic outnumbered those who reported “weak” buyer, measured by the REALTORS® Buyer Traffic Index. States with the strongest buyer traffic were Washington, Oregon, and Wyoming. Supply conditions, measured by the REALTORS® Seller Traffic Index, remained broadly “weak” in many states, except in Montana, Wyoming, North Dakota, South Dakota , Texas, Alabama, and Maine.

REALTORS® Buyer Traffic Index

July–Sept 2015

53

41

20304050607080

2008

0120

0805

2008

0920

0901

2009

0520

0909

2010

0120

1005

2010

0920

1101

2011

0520

1109

2012

0120

1205

2012

0920

1301

2013

0520

1309

2014

0120

1405

2014

0920

1501

2015

0520

1509

REALTORS® Buyer and Seller Traffic Indices as of Sept 2015

(50 = "Moderate" Conditions)

Buyer Traffic Index Seller Traffic Index

8

REALTORS® Seller Traffic Index July–Sept 2015

NAR also tracks the number of properties shown by REALTORS® based on data available from Sentrilock, LLC data. Foot traffic, as measured by openings of SentriLock LLC’s lock boxes, cooled in September 2015, relative to a year earlier. The index fell from 72.3 to 53.7, but remained above the neutral 50 mark suggesting a modest expansionary trend. The diffusion index measures the share of areas changing relative to a year ago, so the trend suggests plateauing at a high level.This month’s drop in the index in part reflects last year’s strength as the index peaked at 65.3 in September of 2014.10 Foot traffic is an indicator of buyer interest, but a showing may not result in a sale.

10 For more information on the Foot Traffic Index based on Sentrilock, LLC data, please contact Ken Fears or visit: http://www.realtor.org/infographics/foot-traffic

9

REALTORS® Expect Prices to Increase Modestly in Next 12 Months REALTORS® who responded to the September 2015 survey expected prices to increase by 3.2 percent over the next 12 months (3.5 percent in August 2015; 3.1 percent in September 2014).9 REALTORS® expect the recent strong price growth to moderate as rising prices have made homes “unaffordable” for many, with home prices almost at par their levels prior to the housing downturn. The median price of all existing homes sold in the U.S. as of August 2015 was $230,200, almost at par with the peak price of all existing homes at $230,900 in July 2006. The map shows the median expected price change in the next 12 months for each state based on the July-September 2015 RCI surveys.10 REALTOR® respondents from Florida were the most upbeat, with a median expected price growth in the range of five to six percent. In Washington, Oregon, and Colorado, the median expected price growth among respondents was four to five percent.

9 A comparison of the expected price growth for the next 12 months compared to the actual price growth shows the expected price growth to be more conservative than the actual price growth, but both are generally headed in the same direction. 10 In generating the median price expectation at the state level, we use data for the last three surveys to have close to 30 observations. Small states such as AK,ND, SD, MT, VT, WY, WV, DE, and D.C., may have less than 30 observations.

10

Median Expected Price Change of REALTORS® in Next 12 Months, By State July–Sept 2015

Properties On the Market at 49 Days

Properties that closed in September 2015 were typically on the market for a shorter time compared to a year ago, typically at 49 days (47 days in August 2015; 56 days in September 2014).11 Days on market usually increase after the spring and summer months due to the seasonal slowing down in demand. Respondents reported that it typically took another 41 days to close the sale.

Short sales were on the market for the longest time at 135 days, while foreclosed properties generally stayed on the market at 57 days. Non-distressed properties were on the market at 48 days.

11 Respondents were asked “For the last house that you closed in the past month, how long was it on the market from listing time to the time the seller accepted the buyer’s offer?” The median is the number of days at which half of the properties stayed on the market.

11

Approximately 38 percent of properties were on the market for less than a month when sold. About 10 percent were on the market for longer than six months, a decrease from 30 percent in January 2012. Properties that stay on the market for longer are more likely to sell at a discount.

0

50

100

150

200

2011

05

2011

08

2011

11

2012

02

2012

05

2012

08

2012

11

2013

02

2013

05

2013

08

2013

11

2014

02

2014

05

2014

08

2014

11

2015

02

2015

05

2015

08

Median Days on Market of Sales Reported By REALTOR® Respondents as of Sept 2015

All Foreclosed Short sale Not distressed

All: 49 Foreclosed: 57 Short sale: 135 Not distressed: 48

38%

19% 14%

10%

5% 3% 3% 2% 5%

0%5%

10%15%20%25%30%35%40%45%

Less than1 month

1 to lessthan 2months

2 to lessthan 3

months

3 to lessthan 4months

4 to lessthan 5

months

5 to lessthan 6

months

6 to lessthan 9

months

9 to lessthan 12months

12months or

more

Percentage Distribution of Time on Market of Sales Reported by REALTOR® Respondents as of Sept 2015

201409 201508 201509

12

Properties typically sold within a month in California, Utah, Colorado, South Dakota, Nebraska, Texas, and the District of Columbia. In Vermont, properties were typically on the market for longer than 90 days when sold. All real estate is local. State-level data is provided for REALTORS® who may want to compare local markets against the state and national summary.

Median Days on Market for Sales Reported by REALTORS®, By State July–Sept 2015

0%

20%

40%

60%

80%

100%

Less than 3months

3 to less than 6months

6 to less than 9months

9 to less than 12months

12 months ormore

Perc

ent o

f sal

es, b

y da

ys o

n m

arke

t

Days on Market

Properties That Stay Longer on the Market are More Likely to Be Sold at a Discount

Net discount of 12% or higher Net discount of 4% to 11%Net discount of less than 4% No discount or premiumNet premium of up to 4% Net premium of 4% to 11%Net premium of 12% or higher

13

II. Buyer and Seller Characteristics

Sales to First-Time Buyers: 29 Percent of Sales

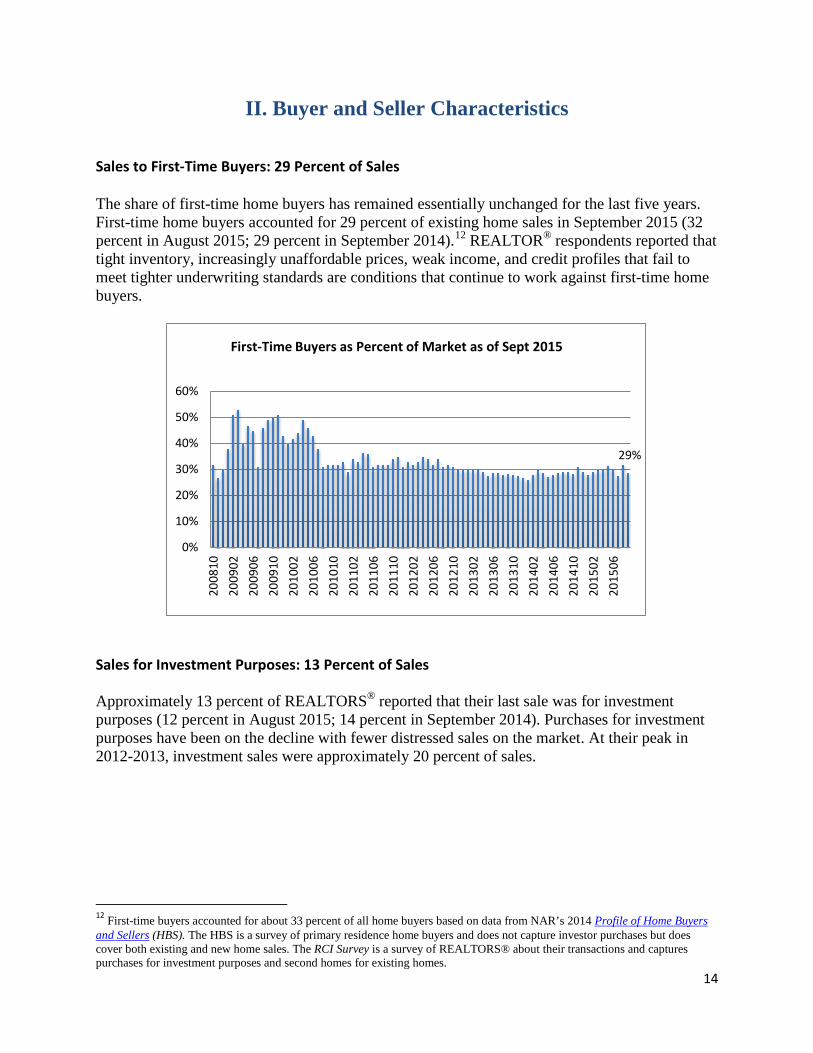

The share of first-time home buyers has remained essentially unchanged for the last five years. First-time home buyers accounted for 29 percent of existing home sales in September 2015 (32 percent in August 2015; 29 percent in September 2014).12 REALTOR® respondents reported that tight inventory, increasingly unaffordable prices, weak income, and credit profiles that fail to meet tighter underwriting standards are conditions that continue to work against first-time home buyers.

Sales for Investment Purposes: 13 Percent of Sales Approximately 13 percent of REALTORS® reported that their last sale was for investment purposes (12 percent in August 2015; 14 percent in September 2014). Purchases for investment purposes have been on the decline with fewer distressed sales on the market. At their peak in 2012-2013, investment sales were approximately 20 percent of sales.

12 First-time buyers accounted for about 33 percent of all home buyers based on data from NAR’s 2014 Profile of Home Buyers and Sellers (HBS). The HBS is a survey of primary residence home buyers and does not capture investor purchases but does cover both existing and new home sales. The RCI Survey is a survey of REALTORS® about their transactions and captures purchases for investment purposes and second homes for existing homes.

29%

0%

10%

20%

30%

40%

50%

60%

2008

1020

0902

2009

0620

0910

2010

0220

1006

2010

1020

1102

2011

0620

1110

2012

0220

1206

2012

1020

1302

2013

0620

1310

2014

0220

1406

2014

1020

1502

2015

06

First-Time Buyers as Percent of Market as of Sept 2015

14

Distressed Sales: Seven Percent of Sales With rising home values and fewer foreclosures, the share of sales of distressed properties continued to decline. In September 2015, distressed sales accounted for seven percent of sales (seven percent in August 2015; ten percent in September 2014). About six percent of reported sales were foreclosed properties, and about one percent were short sales.13 Distressed sales accounted for about a third to a half of sales until 2011. Foreclosed properties sold at an average discount of 17 percent in August 2015. Properties sold as short sales sold at an average discount of 19 percent.

13 The survey asks respondents to report on the characteristics of the most recent sale for the month.

13%

0%

5%

10%

15%

20%

25%

30%

2008

1020

0902

2009

0620

0910

2010

0220

1006

2010

1020

1102

2011

0620

1110

2012

0220

1206

2012

1020

1302

2013

0620

1310

2014

0220

1406

2014

1020

1502

2015

06

Sales to Investors as Percent of Market as of Sept 2015

0%

10%

20%

30%

40%

50%

60%

2008

1020

0902

2009

0620

0910

2010

0220

1006

2010

1020

1102

2011

0620

1110

2012

0220

1206

2012

1020

1302

2013

0620

1310

2014

0220

1406

2014

1020

1502

2015

06Distressed Sales, as Percent of Sales Reported by REALTOR®

Respondents as of Sept 2015

Foreclosed Short sale

Foreclosed: 6% Short sale: 1%

15

Distressed sales have fallen with fewer properties in foreclosure (840,217 properties in the foreclosure inventory as of the second quarter of 2015 from a peak of two million properties in 2009-2010).14 Fewer distressed sales and foreclosures improves home values, creating more home equity for the homeowner. As of the second quarter of 2015, the equity of all households in real estate was valued at $12.2 trillion, or 56 percent of the value of households’ real estate assets. Household equity peaked at $13.3 trillion in the first quarter of 2006.

14 Mortgage Bankers Association, seasonally adjusted data.

17% 19%

0%

5%

10%

15%

20%

25%

2009

0220

0905

2009

0820

0911

2010

0220

1005

2010

0820

1011

2011

0220

1105

2011

0820

1111

2012

0220

1205

2012

0820

1211

2013

0220

1305

2013

0820

1311

2014

0220

1405

2014

0820

1411

2015

0220

1505

2015

08

Mean Percentage Price Discount of Distressed Sales Reported by REALTOR® Respondents as of Sept 2015

Foreclosed Short sale

-

0.50

1.00

1.50

2.00

2.50

0.000.501.001.502.002.503.003.504.004.505.00

Q1/

1980

Q1/

1982

Q1/

1984

Q1/

1986

Q1/

1988

Q1/

1990

Q1/

1992

Q1/

1994

Q1/

1996

Q1/

1998

Q1/

2000

Q1/

2002

Q1/

2004

Q1/

2006

Q1/

2008

Q1/

2010

Q1/

2012

Q1/

2014

inve

ntor

y in

mill

ions

% o

f mor

tgag

es

Mortgage Foreclosure Inventory

Foreclosure Inventory (in millions) As percent of all mortgagesSource: Mortgage Bankers Association downloaded from Haver Analytics.

16

Cash Sales: 24 Percent of Sales The share of cash sales to the market has declined compared to the levels in 2010-2014, but the share remains elevated compared to levels before the housing downturn. Approximately 24 percent of sales were all-cash (22 percent in August 2015; 24 percent in September 2014). Buyers of homes for investment purposes, second homes, and foreign clients are more likely to pay cash than first-time home buyers. As sales to investors and distressed properties have fallen, the share of cash sales has declined as well.

0.0010.0020.0030.0040.0050.0060.0070.0080.00

0.000

2000.000

4000.000

6000.000

8000.000

10000.000

12000.000

14000.000

Q1/

1980

Q1/

1982

Q1/

1984

Q1/

1986

Q1/

1988

Q1/

1990

Q1/

1992

Q1/

1994

Q1/

1996

Q1/

1998

Q1/

2000

Q1/

2002

Q1/

2004

Q1/

2006

Q1/

2008

Q1/

2010

Q1/

2012

Q1/

2014

Owner's Equity, as % of RE assets

Owner's Equity, $bn

Household's Owner's Equity in Real Estate

Households: Owners' Equity in Real Estate (NSA, Bil $)Households: Owners' Equity in Real Estate as a % of Household Real…

Source: FRB, Flow of Funds , Table B.101, from Haver Analytics

24%

0%5%

10%15%20%25%30%35%40%

2008

1020

0902

2009

0620

0910

2010

0220

1006

2010

1020

1102

2011

0620

1110

2012

0220

1206

2012

1020

1302

2013

0620

1310

2014

0220

1406

2014

1020

1502

2015

06

Cash Sales as Percent of Market as of Sept 2015

17

Among mortgage sales reported by the respondents, 36 percent made a downpayment of at least 20 percent, about the same since 2011 when NAR started collecting this data. Among mortgage sales for first-time home buyers, 69 percent had downpayment terms of zero to six percent, a decrease from 77 percent of in 2009. The decreased share of low downpayment loans is one indicator that access to credit has become more difficult for borrowers who cannot afford higher downpayments.

71% 67%

52% 49%

14% 6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

International Investor Distressedsale

Secondhome

Relocation First-timebuyer

Percent of Sales That are All-Cash By Type of Buyer in Sept 2015

36%

0%5%

10%15%20%25%30%35%40%45%50%

2011

0420

1106

2011

0820

1110

2011

1220

1202

2012

0420

1206

2012

0820

1210

2012

1220

1302

2013

0420

1306

2013

0820

1310

2013

1220

1402

2014

0420

1406

2014

0820

1410

2014

1220

1502

2015

0420

1506

2015

08

Percent of Mortgage Sales With Downpayment of At Least 20 Percent as of Sept 2015

18

International Transactions: Less than Two Percent of Residential Market Less than two percent percent of respondents reported their last sale was a purchase by a foreigner not residing in the U.S. International buyers frequently pay cash and have typically purchased properties above the median market price. Based on NAR’s 2015 Profile of Homebuying Activity of International Clients, Florida, California, Texas, and Arizona are the major destinations.

77%

69%

0.50.55

0.60.65

0.70.75

0.80.85

0.9

2009

0620

0909

2010

0220

1005

2010

0820

1011

2011

0220

1105

2011

0820

1111

2012

0220

1205

2012

0820

1211

2013

0220

1305

2013

0820

1311

2014

0220

1405

2014

0820

1411

2015

0220

1505

2015

08

Percent of First-Time Buyers Obtaining a Mortgage Who Had a Down Payment of 0% to 6% as of Sept 2015*

*The data reported for the month is a rolling three-month figure.

1.3%

0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%

2010

0320

1006

2010

0920

1012

2011

0320

1106

2011

0920

1112

2012

0320

1206

2012

0920

1212

2013

0320

1306

2013

0920

1312

2014

0320

1406

2014

0920

1412

2015

0320

1506

2015

09Sales to International Clients as Percent of Market

as of Sept 2015

19

Age, Previous Residence, and Type of Property Purchased Buyers age 34 and under accounted for 28 percent of sales reported by the respondents. Nearly half of buyers were in the age group 35 to 55 years.

Slightly more than half of all reported buyers lived in their own homes, and these include trade-up or trade-down buyers and those who are purchasing a second home or one for investment purpose. Renters accounted for 35 percent of sales, essentially unchanged compared to past months.

0%10%20%30%40%50%60%70%80%90%

100%

2013

07

2013

09

2013

11

2014

04

2014

07

2014

08

2014

09

2014

10

2014

11

2014

12

2015

01

2015

02

2015

03

2015

04

2015

05

2015

06

2015

07

2015

08

2015

09

Age Distribution of Buyers for Sales Reported by REALTOR® Respondents as of Sept 2015

Age 34 and under Age 35 to 55 Age 56 and over

0%

20%

40%

60%

80%

100%

2014

08

2014

09

2014

10

2014

11

2014

12

2015

01

2015

02

2015

03

2015

04

2015

05

2015

06

2015

07

2015

08

2015

09Living Status of Home Buyers at Time of Home Purchase of

Sales Reported by REALTORS® as of Sept 2015

Lives with parents, relatives, or friendsLives in own homeRents an apartment or house

20

Sales data compiled for the January-September 2015 timeframe showed that among buyers 34 years and under, 86 percent purchased single-family homes, compared to the 77 percent rate for buyers 56 years and older. Buyers age 56 and over are about twice as likely to purchase a condominium than other buyers. REALTORS® have also reported a demand for 55 and older community housing as the large baby boomer population continues to move into retirement.

III. Current Issues

Demand for Rentals Remain Strong About 68 percent of REALTORS® reported rising residential rent (71 percent in August 2015; 65 percent in September 2014). Rising rents indicate continued strong demand for rental properties. As of the second quarter of 2015, the CPI-Shelter Index, a measure of rent payments, was up 45 percent compared to the level in the first quarter of 2000. On the other hand, mortgage payments were only six percent higher on account of low mortgage rates. Although rents are rising faster than mortgage payments, the rentership rate has remained elevated, likely due to a mix of factors such as lifestyle choice, financial constraints for younger households, tight underwriting standards, and increasing unaffordability as tight inventory continues to push up prices. As of August 2015, the median home price of all existing homes is 47 percent higher than in Febuary 2012 when prices hit a low of $156,100. Meanwhile, over this same period, the median family income rose by seven percent.

86% 86% 77% 84%

7% 6% 7%

6% 7% 8% 17% 10%

0%

20%

40%

60%

80%

100%

Age 34 and under Age 35 to 55 Age 56 and over All

Type of Residential Property Purchased by Age Group as of Sept 2015

Single-family Townhome Condominium

21

68%

0%10%20%30%40%50%60%70%80%90%

100%

2010

1220

1103

2011

0620

1109

2011

1220

1203

2012

0620

1209

2012

1220

1303

2013

0620

1309

2013

1220

1403

2014

0620

1409

2014

1220

1503

2015

0620

1509

Percent of REALTOR® Respondents Reporting Rising Residential Rents Compared to 12 Months Ago

as of Sept 2015

106

145

507090

110130150170

2000

Q1

2000

Q4

2001

Q3

2002

Q2

2003

Q1

2003

Q4

2004

Q3

2005

Q2

2006

Q1

2006

Q4

2007

Q3

2008

Q2

2009

Q1

2009

Q4

2010

Q3

2011

Q2

2012

Q1

2012

Q4

2013

Q3

2014

Q2

2015

Q1

Index of Mortgage Payments and Rent Payments as of 2015 Q2 (2000 Q1=100)

Mortgage Payment (2000Q1=100) CPI-Shelter Index (2000Q1=100)Source: NAR, BLS downloaded on Haver Analytics

22

Credit Conditions Still Generally Tight

REALTORS® continued to report that credit conditions remain generally tight, with significant loan processing delays. One indicator of credit tightness is the distribution of FICO scores on approved loans. About 48 percent of REALTORS® providing transaction credit score information reported FICO credit scores in the range of 740+. For comparison, in the period 1999-2004, only 37 percent of Fannie Mae’s and 33 percent of Freddie Mac’s 30-year, fixed rate, fully amortizing acquistions had FICO scores greater than 750. As of 2015 Q2, Fannie Mae reported that 63.6 percent of its single-family acquisitions had a FICO credit score of 740 or higher.16

16 Source: Fannie Mae 2015 Second Quarter Credit Supplement downloaded at http://www.fanniemae.com/resources/file/ir/pdf/quarterly-annual-results/2015/q22015_credit_summary.pdf

147

107

80

100

120

140

160

Feb/

2012

Apr/

2012

Jun/

2012

Aug/

2012

Oct

/201

2De

c/20

12Fe

b/20

13Ap

r/20

13Ju

n/20

13Au

g/20

13O

ct/2

013

Dec/

2013

Feb/

2014

Apr/

2014

Jun/

2014

Aug/

2014

Oct

/201

4De

c/20

14Fe

b/20

15Ap

r/20

15Ju

n/20

15Au

g/20

15

Index of Median Existing Home Prices and Median Family Income as of 2015 Q2 (Feb 2012=100)

NAR Median Home Price (Feb 2012=100)

Median Family Income (Feb 2012=100)

3%

50%

48%

0%10%20%30%40%50%60%70%

2012

0220

1204

2012

0620

1208

2012

1020

1212

2013

0220

1304

2013

0620

1308

2013

1020

1312

2014

0220

1404

2014

0620

1408

2014

1020

1412

2015

0220

1504

2015

0620

1508

Percentage Distribution of FICO Scores Reported by REALTOR® Respondents as of Sept 2015

Less than 620 620 to 739 740 or more

23

Among first-time home buyers, 32 percent of buyers were reported to have FICO scores of 740 or higher. Among buyers age 34 years and under, 37 percent had FICO scores of 700 or over. A majority of borrowers with FICO scores of less than 740 availed of “low” downpayment loans (zero to six percent). For example, 76 percent of borrowers with FICO scores of below 620 made a down payment of zero to six percent.

3%

17% 23% 25%

32%

1% 7%

13% 22%

56%

0%10%20%30%40%50%60%

Less than 620 620 to 659 660 to 699 700 to 739 740 or more

Percentage Distribution of FICO Credit Scores for First-time and Non-first- time Buyers Reported by REALTORS®

in Jan-Sept 2015

Yes No

2% 2% 1%

14% 11% 5%

20% 17% 9%

27% 23%

18%

37%

47%

67%

0%

10%

20%

30%

40%

50%

60%

70%

Age 34 and under Age 35 to 55 Age 56 and over

Percentage Distribution of FICO Scores , By Age Group, Based on Mortgage Sales Reported by REALTORS® in Jan-Sept 2015

Less than 620 620 to 659 660 to 699 700 to 739 740 or more

24

Contract Settlement Issues: Financing and Appraisals are Major Issues

In reporting on their last contract that went into settlement or was terminated over the period July-September 2015, REALTORS® reported that 64 percent of contracts were settled on time, 30 percent had delayed settlement, and six percent were terminated.

Of all contracts settled/terminated, financing, appraisal, and home inspection issues were the major problems: 18 percent had financing issues, 11 percent had appraisal issues, and 11 percent had home inspection issues.

Among contracts that had a delayed settlement (30 percent), 42 percent of contracts that were delayed had financing issues.

0%

20%

40%

60%

80%

100%

Less than 620 620 to 659 660 to 699 700 to 739 740 or morePerc

ent o

f rep

orte

d sa

les

Credit score range

Downpayment Terms, by Credit Score Range as Reported by REALTORS®

0 to 6% Downpayment 7 to 10% Downpayment

11 to 19% Downpayment 20 % or more Downpayment

65% 67% 65% 64% 63% 63% 65% 65% 64%

26% 27% 26% 26% 28% 29% 29% 29% 30% 8% 7% 9% 10% 9% 7% 6% 7% 6%

0%20%40%60%80%

100%How Sales Contracts Were Settled in July - Sept 2015*

Contract was terminatedContract was delayed but eventually went into settlementContract was settled on time

* Based on the most recent contract that went into settlement or was terminated during this period.

25

Among contracts that were terminated (six percent), home inspection and financing issues were the major causes, with 28 percent of contracts experiencing both these issues.

49%

18%

11%

11%

5%

4%

2%

1%

1%

10%

No problems encounteredIssues related to obtaining financing

Home inspection/environmental issuesAppraisal issues

Titling/deed issuesContingencies stated in the contract

Issues in buy/sell distressed propertyHome/hazard/flood insurance issues

Buyer lost jobOther

Problems Encountered for Contracts That Went Into Settlement or Were Terminated in July-Sept 2015 *

* Will not sum to 100 percent because multiple responses are allowed. "Other" includes buyer or seller backing out, builder delays, HOA issues, pricing issues, etc.

42% 21%

14%

12%

8%

5%

2%

1%

20%

Issues related to obtaining financingAppraisal issues

Home inspection/environmental issuesTitling/deed issues

Contingencies stated in the contractIssues in buy/sell distressed propertyHome/hazard/flood insurance issues

Buyer lost jobOther

Problems Encountered for Contracts That Were Delayed But Eventually Went Into Settlement in July-Sept 2015

(Delayed Contracts Represent 30 Percent of Closed or Terminated Contracts)

* Will not sum to 100 percent because multiple responses are allowed. "Other" includes buyer or seller backing out, builder delays, HOA issues, pricing issues, documentation issues, etc.

26

28%

28%

13%

11%

4%

2%

1%

1%

Home inspection/environmental issues

Issues related to obtaining financing

Contingencies stated in the contract

Appraisal issues

Issues in buy/sell distressed property

Buyer lost job

Titling/deed issues

Home/hazard/flood insurance issues

Problems Encountered for Contracts That Were Terminated in July-Sept 2015

(Terminated Contracts Represent Six Percent of Closed or Terminated Contracts)

*Will not sum to 100 percent because multiple responses are allowed. "Other" includes buyer or seller backing out, builder delays, HOA issues, pricing issues, documentation issues, etc.

27

The NATIONAL ASSOCIATION of REALTORS®, “The Voice for Real Estate,” is America’s largest trade association, representing over 1 million members, including NAR’s institutes, societies, and councils, involved in all aspects of the real estate industry. NAR membership includes brokers, salespeople, property managers, appraisers, counselors and others engaged in both residential and commercial real estate. The term REALTOR® is a registered collective membership mark that identifies a real estate professional who is a member of the National Association of REALTORS® and subscribes to its strict Code of Ethics. Working for America's property owners, the National Association provides a facility for professional development, research, and exchange of information among its members, and to the public and government for the purpose of preserving the free enterprise system and the right to own real property. The Mission of the NATIONAL ASSOCIATION of REALTORS® Research Division is to collect and disseminate timely, accurate, and comprehensive real estate data and to conduct economic analysis in order to inform and engage members, consumers, policy makers, and the media in a professional and accessible manner. To find out about other products from NAR’s Research Division, visit www.REALTOR.org/research-and-statistics Also follow NAR Research on

https://twitter.com/nar_research

https://www.facebook.com/narresearchgroup

https://www.pinterest.com/narresearch/

https://instagram.com/narresearch/

NATIONAL ASSOCIATION of REALTORS® Research Division 500 New Jersey Avenue, NW Washington, DC 20001 202.383.1000

28