separation of debt and monetary management in india · and fiscal operations; debt management...

TRANSCRIPT

IIMB Management Review (2015) 27, 56e71

ava i lab le a t www.sc ienced i rec t . com

ScienceDirect

journa l homepage: www.e lsev ier .com/ locate / i imb Production and hosting by Elsevier

ROUND TABLE

Separation of debt and monetarymanagement in India*

Charan Singh*

Economics and Social Sciences, Indian Institute of Management Bangalore, Bangalore, Karnataka, India

Available online 6 March 2015

KEYWORDSDebt management;Separation of debt andmonetary management;Debt managementoffice (DMO);Independence of acentral bank;Independent debtmanagement office

* This paper is based on the ModuleManagement held at IIM Bangalore on* Tel.: þ91 80 2699 3818.E-mail address: [email protected] under responsibility of In

http://dx.doi.org/10.1016/j.iimb.2010970-3896 ª 2015 Indian Institute of

Abstract Thediscussion highlights the importance of and the need for a separate debtmanage-ment office, separate from themonetary authority. The objective of debtmanagement is raisingresources from the market at minimum cost while containing the risks, while that of the mone-tary authority is to achieve price stability. In the years preceding the financial crisis of 2008, sep-aration of debt and monetary management was a settled norm and a number of countries withliberalized financial markets and high levels of government debt sought to adopt professionaldebtmanagement techniques to save cost and to provide policy signals to themarket. Separationof debtmanagement is essential to preserve the integrity and independence of the central bank,to ensure transparency and accountability, and to improve debt management by entrusting it toportfolio managers with expertise in modern risk management techniques. In India, debt ismanagedby the central and state governments, and theRBI. The separation of debtmanagementwould provide focus to the task of asset-liability management of government liabilities, under-take risk analysis and also help the government to prioritize public expenditure through higherawareness of interest costs. The separation would also be helpful for the borrowing programmewhich would have to be completed without the support of the regulatory or supervisory author-ity. This may lead to widening of investor base and market friendly yield curve.

But after the great financial recession of 2008, the issue has re-emerged as in many countries,especially the advanced economies, the scope of fiscal operationswas expanded, and the debt toGDP ratios have increased substantially. Similarly, in view of the sensitiveness of the issue, espe-cially amidst less developed financial markets, there has been some re-thinking on the issue; inIndia, the Reserve Bank has also been re-thinking the separation issue and seems reluctant giventhe present context of the economy.ª 2015 Indian Institute of Management Bangalore. Production and hosting by Elsevier Ltd.All rights reserved.

on Debt Management under the aegis of the 9th Annual International Conference on Public Policy andAugust 11, 2014. Views are personal.

et.indian Institute of Management Bangalore.

5.01.007Management Bangalore. Production and hosting by Elsevier Ltd. All rights reserved.

Separation of debt and monetary management 57

Introduction

In recent years, after the global crisis (2008), the issue ofseparation of monetary management from fiscal and debtmanagement operations has re-emerged. In many coun-tries, during the period of crisis, the scope of fiscal oper-ations was expanded; the debt to GDP ratios also increasedsignificantly. Consequently debt management encountereddifficulties, and coordination between monetary manage-ment and debt management assumed greater significance.

Historically, the debt crises of 1982 and the East Asianfinancial crisis of 1997 led many countries to assign priorityto public debt management and several countries chose toseparate debt management from monetary management.As government securities markets became mature and moresophisticated, a separate institutional structure wasconsidered to be better suited to achieve an appropriatebalance between monetary policy and debt managementobjectives. In normal economic circumstances the centralbank operates at the short end of the market and debtmanagement at the long end to minimize cost of raisingresources but in times of crisis, the operations can becomeblurred. A separation in responsibilities was considered abetter solution that would reduce the risk of policy con-flicts. Once the financial markets had developed, the roleof the central bank in sustaining the stability of marketswas considered minimal. Therefore, in many of the Orga-nisation for Economic Co-operation and Development OECDcountries, separation of debt management and monetarymanagement was undertaken in the 1990s.

The round table discussion follows a brief contextualintroduction to the issue, covering the objectives of debtmanagement; traditional and post-crisis viewpoints aboutseparation of debt management; central banks’ indepen-dence; coordination between debt management, monetaryand fiscal operations; debt management practice in India;and the role of the Reserve Bank of India (RBI).

Objectives of debt management

The main objective of debt management is to minimize thecost of borrowings over the medium to long run, consistentwith a prudent degree of risk. To achieve this, promotionand development of efficient primary and secondary mar-kets for government securities is an important comple-mentary objective. Hence, public debt management can beexplained as the process of executing a strategy for man-aging the government’s debt e to raise the requiredamount of borrowings, pursue cost/risk objectives, and alsomeet any other goal that the government might have set(IMF, 2003). This assumes added significance with high fiscaldeficits and government debt.

Separate debt management office e atraditional view

There was a growing consensus among practitioners until2008 to treat debt management as a separate policy

1 Operational risk, generally neglected in debt management, pertains2 In case the two are not separated, then debt management policy evenauthorities attempt to use debt instruments to strengthen monetary poinstrument from monetary policy. A number of countrieswith liberalized financial markets and high levels of gov-ernment debt sought to adopt professional debt manage-ment techniques to save cost and to provide policy signalsto the market (Giovannini, 1997). The benefits of separa-tion of the two functions were basically conditional uponthe level of financial development as argued byBlommestein and Turner (2012). The trend started withNew Zealand in the 1980s, with the government recognizingthe need for proper policy assignment and an account-ability framework for debt management to meet the fiscaltargets set in the Fiscal Responsibility Act. In Europe,several countries that were heavily indebted in the late1980s and early 1990s, such as Belgium, France, Ireland andPortugal, decentralized debt management to varying ex-tents, in order to reduce the variability of debt service costthat could jeopardize the targets set by the Growth andStabilization Pact. In the UK, debt management re-sponsibilities were taken away from the Bank of England inorder to remove the perception of conflict of interest inconducting debt management and monetary operations(Togo, 2007).

A number of countries have chosen to open a separatedebt management office to have a more focussed debtmanagement policy in terms of cost of borrowings, marketdetermined yield curve, and optimal mix of maturity profileof outstanding loans (Table 1). The location of the debtmanagement office is important and depends on a numberof considerations. The dispersal of debt managementfunctions within different layers of government can lead tolack of coherent debt management policy and overall riskassessment, and therefore higher operational risk.1 SomeOECD countries have opted for an autonomous debt man-agement office to improve operational efficiency whileothers, seeking a balance between public policy andfinancial management, have a separate office but operatingunder the Ministry of Finance (MOF). In Denmark, debtmanagement is undertaken by a privately owned centralbank (OECD, 2002). In the case of developing countries,Currie, Dethier and Togo (2003) argue that the separateoffice can be initially placed under the MOF while Kalderen(1997) suggests that a separate office may be unsuitable foroverall policy effectiveness of debt management.

On the basis of the experience of OECD countries,Cassard and Folkerts-Landau (1997) concluded that severalreasons emerge that justify the separation of debt man-agement e to preserve the integrity and independence ofthe central bank, to shield debt management from politicalinterference, to ensure transparency and accountability,and to improve debt management by entrusting it to port-folio managers with expertise in modern risk managementtechniques. The separation of debt management andmonetary management positively affects expectations as itexplicitly indicates to the market that monetary policy isindependent of debt management.2

The classic conflict between monetary policy and debtmanagement policy, and operations relates to the fixationof interest rates. The interest rates on government secu-rities are crucial in determining the yield curve and prices

to internal processes, people and systems.tually becomes subservient to the monetary policy as the monetarylicy signals and to enhance the credibility of the central bank.

Table 1 Location of debt management office in select countries.

Country Location of debt management office Scope of debt management Advisory board

Cash Debt Contingent

1. Australia Separate agency under Treasury since 1999 Yes Yes No Yes2. Brazil Debt office under Treasury since 1988 Yes Yes No No3. Colombia Debt office under Treasury since 1991 No Yes Yes Yes4. Denmark Debt office in central bank Yes Yes Yes No5. France Separate agency under Treasury since 2001 Yes Yes No Yes6. Germany Separate agency under Treasury since 2001 Yes Yes No No7. Ireland Separate agency under Treasury since 1991 Yes Yes No Yes8. Italy Debt agency under Treasury e 1997 Yes Yes No No9. Mexico Separate office in Treasury No Yes Yes No

10. New Zealand Separate office under Treasury since 1988 Yes Yes Yes Yes11. Poland Debt office within Treasury since 1994 No Yes Yes No12. Portugal Separate debt office under Treasury since 1996 Yes Yes Yes Yes13. Sweden Separate debt office under Treasury since 1789 No Yes Yes Yes14. UK Separate debt office under Treasury since 1997 Yes Yes No Yes15. USA Debt office within Treasury Yes Yes No No16. South Africa Debt Management Office within Treasury Yes Yes Yes No

Source: Singh (2005).

58 C. Singh

of financial assets in the economy. The conflict of debtmanagement with monetary management arises due to thechoice of keeping debt servicing costs low over the shortterm or over the medium-long term. A separation of thesetwo was expected to avoid such conflicts and improvepolicy credibility.

In case the central bank conducts debt managementpolicy, conflicting situations may emerge. Questions arisesuch as whether liquidity should be tightened based onmonetary conditions prevailing in the economy or relaxedto ensure success of market borrowing programme of thegovernment? Another area of concern could be interestrates which are of prime importance to the central bankand serve as a benchmark in transmission mechanismthrough the yield curve. The government would like toborrow at low costs while the central bank might considermonetary tightening in the context of financial stabilitymore important. Further, the central bank may be temptedto manipulate financial markets to reduce the interest ratesat which government debt is issued (Cassard & Folkerts-Landau, 1997). In the case of developing countries, wherefinancial markets are generally underdeveloped there is yetanother concern and that is the limited financing options ofthe government and uncertain cash requirements thatconstrain independence of the central bank. Taylor (1998)argues that the accord between the Federal Reserve(Fed) and the Treasury in 1951 in the US, which emanci-pated the Fed from assisting the Treasury in borrowings atlow rates of interest, helped the Fed to focus on interestrates. Even if a separate department within the centralbank conducts debt management, the market will stillperceive that the debt management decisions are influ-enced by inside information on interest rates policy. Incontrast, a statutory and separate authority for debtmanagement could facilitate direct reporting to the

3 http://www.carnegie-rochester.rochester.edu/nov04-pdfs/gk.pdf.

parliament which will prompt better fiscal discipline,appropriate audit, and financial and management controls.

Central bank independence

The other factor supporting separation of debt from mon-etary management was the argument in favour of inde-pendence of the central bank. In the years until 2008,because of the great moderation and Volcker’s victory overinflation3 in the 1980s, substantial evidence had beenadvanced in theoretical and empirical literature to supportthe political and economic independence of the centralbank (Grilli, Masciandaro & Tabellini, 1991a). In support ofcentral bank independence, Kydland and Prescott (1977),Barro and Gordon (1983a and 1983b), Burdekin and Laney(1988), Eschweiler and Bordo (1993) and Grilli,Masciandaro, and Tabellini (1991b) argue that more inde-pendent central banks reduce the rate of inflation, whileAlesina and Summers (1993) conclude that such indepen-dence has no impact on real economic performance.Wagner (1998) argues that making a central bank inde-pendent lowers “expectations” pertaining to inflation ofthe private sector that determine wage and price con-tracts, and thereby also the expectations that impact ex-change rates.

Separate debt management office e post-crisisview

Following the financial crisis of 2008, there has been arethink on the issue of separation of debt managementfrom monetary management because of the following fac-tors a) a sharp increase in government deficit and debt,because of the fiscal stimulus; b) the use of unconventional

Separation of debt and monetary management 59

monetary policy in advanced countries involving large scalepurchase of government securities of varying maturities; c)imposition of new liquidity requirements resulting in higherdemand for government securities; and d) increase inforeign ownership of government debt.

Thus, the thrust of the recent debate is that under adifficult macroeconomic situation, the lines between debtand monetary policy become blurred and hence the twofunctions should be brought under the same agency. In theUK, there is a discussion on this but not in the US where thetwo functions were separated in 1951. Goodhart (2012)argues that under quantitative easing there is a possibilitythat the policy of debt management, if separate, cannegate the policy of the central bank, and separation be-tween debt management and monetary policy is not desiredas the existing arrangements are already under stress. Onthe other hand, the Study Group (SG) commissioned by theCommittee on the Global Financial System (2011), observedthat there was little evidence that existing arrangementsfor operational independence of sovereign debt manage-ment and monetary policy have created material problems.

Need for coordination

In each country, the economic situation, including thestate of domestic financial markets and the degree ofcentral bank independence, would play an important rolein determining the range of activities to be handled by thedebt manager and the level of coordination that isnecessary with monetary management. Monetary policyand debt management clearly have to be complementaryto each other but debt management should not beconsidered a tool of monetary management nor shouldmonetary policy be considered the objective of debtmanagement (Bank of England, 1995). In the case of theEconomic and Monetary Union (EMU), monetary policy isoperated by the European Central Bank (ECB) while na-tional authorities conduct debt management. The sharingof adequate information between treasuries, nationalcentral banks and the ECB is a norm, and ensures efficientliquidity management.

In the case of developing countries, coordination be-tween fiscal, monetary, and debt management functions isconsidered even more crucial, where financial markets areunder-developed and forecasts of government revenuesand expenditure are inaccurate. The issuance of govern-ment securities by a separate debt office needs to beclosely coordinated with the open market operations un-dertaken by the central bank to ensure appropriateliquidity conditions in the market.

Therefore, the role of the central bank in public debtmanagement, though separated, would continue to becrucial. As an issuing agency of government securities, thecentral bank organizes rules and procedures for selling anddelivering securities and for collecting payments for thegovernment. As a fiscal agent, the central bank makes andreceives payments, including interest payments andservicing of principal. As adviser to the government and to

4 Stockholm Principles (2011) were promulgated by debt managers and c5 Exceptions are Jammu and Kashmir, and Sikkim.6 Thorat, Singh and Das (2003).

the debt manager, it could provide policy inputs on thedesign of the debt programme, mix of debt instruments andmaturity profile of debt stock. These inputs would be usefulin providing stability to the overall debt programme,facilitating smooth functioning of the market, andproviding a stable environment for the conduct of monetarypolicy.

Recent experience shows that there is a need for closecommunication and coordination among the relevantagencies managing monetary policy and debt management,as stressed by the Study Group commissioned by theCommittee on the Global Financial System (2011), and as isconsistent with the Stockholm Principles (2011).4

Another important change is concurrently occurring inthe monetary policy objectives internationally. Whiletheoretical arguments can be made to justify recent de-partures from policy, the reality is that in the post-crisisworld, objectives of the central bank are no longer limitedto price stability. A dilution of central bank independencehas occurred because of the multiple objectives such aspursuit of GDP growth, job creation, and financial stability.The need to establish priorities when there are trade-offsclearly requires political decisions which cannot be madeby unelected officials alone. Moreover, by pushing interestrates toward zero, the current policy of quantitative easinghas strong, often regressive income effects which cannot beimplemented without political patronage. Hence theemerging consensus in the post-crisis period is that centralbanks’ decision-making should be subject to political con-trol (Blejer, 2013).

Debt management in India

In India, presently, public debt management is dividedbetween the central and state governments, and the RBI.The RBI manages the market borrowing programme of thecentral and state governments.5 External debt is manageddirectly by the central government. The RBI acts as thedebt manager for marketable internal debt for the centralgovernment as an obligation and for the state governmentsby an agreement under the RBI Act, 1934. The RBI decidesthe maturity pattern, calendar of borrowings, instrumentdesign and other related issues in consultation with thecentral government (IMF, 2003).6

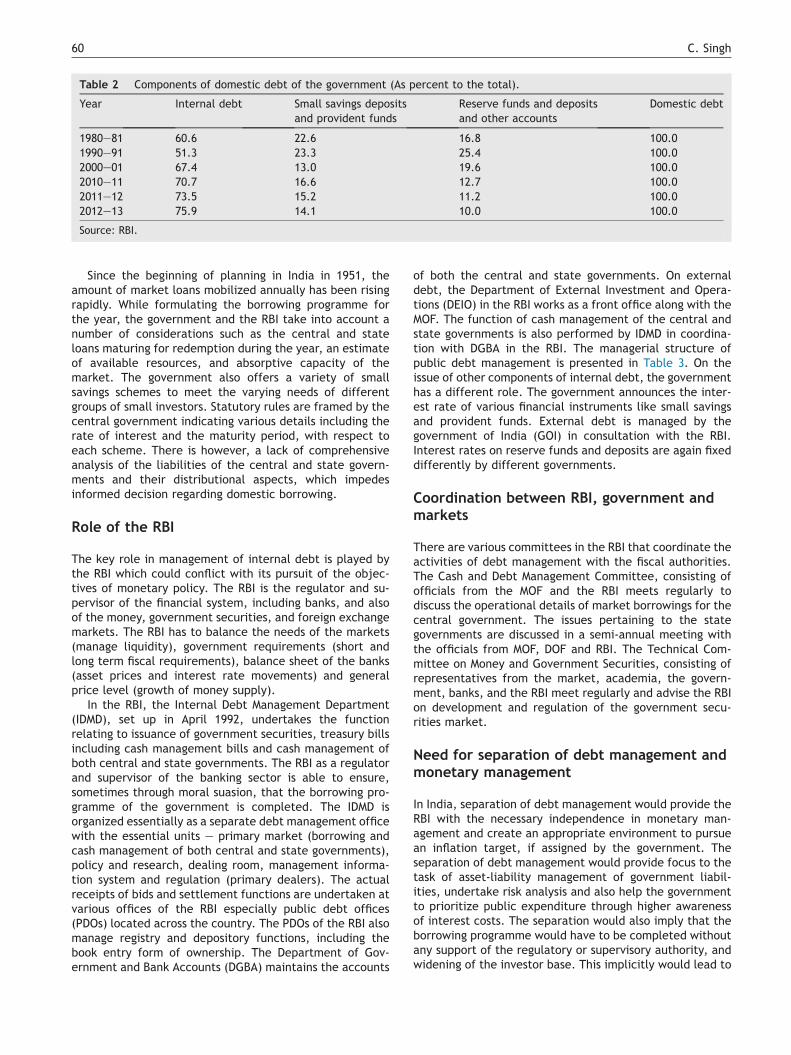

The most important component of domestic debt is in-ternal debt (Table 2). The Constitution of India provides forthe option of placing a limit on the internal debt, both atthe centre and the states, but no such limit has beenimposed so far. Internal debt, the most prominent compo-nent of domestic debt, consists of markets loans, treasurybills and other bonds issued by the central and state gov-ernments or all types of borrowings by the government. Inaddition to internal debt, the government also raises re-sources through small savings and contributions to provi-dent funds. Loans from banking and financial institutionsare mainly raised by the state government. Governmentsalso raise resources termed as reserve funds and deposits,which need to be managed.

entral bankers from 33 advanced and emerging market economies.

Table 2 Components of domestic debt of the government (As percent to the total).

Year Internal debt Small savings depositsand provident funds

Reserve funds and depositsand other accounts

Domestic debt

1980e81 60.6 22.6 16.8 100.01990e91 51.3 23.3 25.4 100.02000e01 67.4 13.0 19.6 100.02010e11 70.7 16.6 12.7 100.02011e12 73.5 15.2 11.2 100.02012e13 75.9 14.1 10.0 100.0

Source: RBI.

60 C. Singh

Since the beginning of planning in India in 1951, theamount of market loans mobilized annually has been risingrapidly. While formulating the borrowing programme forthe year, the government and the RBI take into account anumber of considerations such as the central and stateloans maturing for redemption during the year, an estimateof available resources, and absorptive capacity of themarket. The government also offers a variety of smallsavings schemes to meet the varying needs of differentgroups of small investors. Statutory rules are framed by thecentral government indicating various details including therate of interest and the maturity period, with respect toeach scheme. There is however, a lack of comprehensiveanalysis of the liabilities of the central and state govern-ments and their distributional aspects, which impedesinformed decision regarding domestic borrowing.

Role of the RBI

The key role in management of internal debt is played bythe RBI which could conflict with its pursuit of the objec-tives of monetary policy. The RBI is the regulator and su-pervisor of the financial system, including banks, and alsoof the money, government securities, and foreign exchangemarkets. The RBI has to balance the needs of the markets(manage liquidity), government requirements (short andlong term fiscal requirements), balance sheet of the banks(asset prices and interest rate movements) and generalprice level (growth of money supply).

In the RBI, the Internal Debt Management Department(IDMD), set up in April 1992, undertakes the functionrelating to issuance of government securities, treasury billsincluding cash management bills and cash management ofboth central and state governments. The RBI as a regulatorand supervisor of the banking sector is able to ensure,sometimes through moral suasion, that the borrowing pro-gramme of the government is completed. The IDMD isorganized essentially as a separate debt management officewith the essential units e primary market (borrowing andcash management of both central and state governments),policy and research, dealing room, management informa-tion system and regulation (primary dealers). The actualreceipts of bids and settlement functions are undertaken atvarious offices of the RBI especially public debt offices(PDOs) located across the country. The PDOs of the RBI alsomanage registry and depository functions, including thebook entry form of ownership. The Department of Gov-ernment and Bank Accounts (DGBA) maintains the accounts

of both the central and state governments. On externaldebt, the Department of External Investment and Opera-tions (DEIO) in the RBI works as a front office along with theMOF. The function of cash management of the central andstate governments is also performed by IDMD in coordina-tion with DGBA in the RBI. The managerial structure ofpublic debt management is presented in Table 3. On theissue of other components of internal debt, the governmenthas a different role. The government announces the inter-est rate of various financial instruments like small savingsand provident funds. External debt is managed by thegovernment of India (GOI) in consultation with the RBI.Interest rates on reserve funds and deposits are again fixeddifferently by different governments.

Coordination between RBI, government andmarkets

There are various committees in the RBI that coordinate theactivities of debt management with the fiscal authorities.The Cash and Debt Management Committee, consisting ofofficials from the MOF and the RBI meets regularly todiscuss the operational details of market borrowings for thecentral government. The issues pertaining to the stategovernments are discussed in a semi-annual meeting withthe officials from MOF, DOF and RBI. The Technical Com-mittee on Money and Government Securities, consisting ofrepresentatives from the market, academia, the govern-ment, banks, and the RBI meet regularly and advise the RBIon development and regulation of the government secu-rities market.

Need for separation of debt management andmonetary management

In India, separation of debt management would provide theRBI with the necessary independence in monetary man-agement and create an appropriate environment to pursuean inflation target, if assigned by the government. Theseparation of debt management would provide focus to thetask of asset-liability management of government liabil-ities, undertake risk analysis and also help the governmentto prioritize public expenditure through higher awarenessof interest costs. The separation would also imply that theborrowing programme would have to be completed withoutany support of the regulatory or supervisory authority, andwidening of the investor base. This implicitly would lead to

Table 3 Management of public debt in India.

Major items Appropriated by Managed by Fixation authority for/determination of

Amount Maturity Interest rate

1 2 3 4 5 6

Market loans Centre MOF, RBI MOF MOF, RBI MarketState DOF, RBI MOF DOF, RBI RBI, Market

Market bonds Centre RM, MOF, RBI RM, MOF RM RM, MOF, RBIState RD, DOF, RBI RD, DOF RD RD

Treasury bills Centre MOF, RBI MOF, RBI MOF, RBI MarketWMA Centre MOF, RBI MOF, RBI MOF, RBI RBI

State DOF, RBI RBI RBI RBILoans from Bk & FI State DOF RD RD RD, DOFSmall savings State MOF, DOF MOF, DOF MOF MOFProvident funds Centre MOL, MOF MOL, MOF MOL MOL

State MOL, DOF DOF MOL MOLReserve funds/Deposits Centre RM, MOF RM RM RM

State RD, DOF RD RD RDExternal debt Centre MOF, RBI MOF MOF MOFContingent liabilities Centre RM, MOF RM RM RM

State RD, DOF RD RD RD

MOF e Ministry of Finance; DOF e Department of Finance; MOL e Ministry of Labour; RM e Respective ministry; RD e Respectivedepartment; Bk e Banks; FI e Financial institutions; WMA e Ways and Means advances.Source: Author’s compilation.

Separation of debt and monetary management 61

a more representative market-determined yield curvereflecting term structure and liquidity of the outstandingportfolio. The need for setting up a specialized frameworkon public debt management which will take a comprehen-sive view of the liabilities of the government and establishthe strategy for low-cost financing in the long run has beenadvocated by various expert committees since the late1990s (Table 4).

In India, a watershed moment in the institutional ar-rangements of debt management was the setting up of themiddle office in the Ministry of Finance in 2008 to formulatedebt management strategy for the central government.Again, the Union Budget 2011e12 stated that the govern-ment was in the process of setting up an independent DebtManagement Office (DMO) in the Ministry of Finance. Simi-larly, the Union Budget for 2012e13 proposed to move thePublic Debt Management Agency Bill in parliament.

However, an important re-think in the whole process wasrequired because the RBI was not convinced that the sep-aration would be useful for the financial markets (Khan,2014). Despite consistency in recommendations of sepa-rating debt management from monetary management,there has been hesitancy on part of the RBI and GOI, asdocumented in speeches by the top management and ar-guments offered in the annual reports of the RBI. The mainarguments advanced are that there already is a separatedepartment within the RBI and that during these criticaleconomic years, need for coordination would be immenseand that the government may not have the necessaryexperience or expertise.

7 The Round Table Discussion on Debt Management was held at IIM Bangaand academic in nature. The views expressed by the panellists shourespective panellists as these were in pursuance of academic argumen

Separation of debt and monetary managementin India: A panel discussion7

AnchorCharan SinghPanelistsHarun R KhanDeputy Governor, Reserve Bank of IndiaK KanagasabapathyFormer Director, EPW Research FoundationR K PatnaikProfessor, SP Jain Institute of Management and

Research, MumbaiVijay Singh ChauhanDirector, Ministry of Finance, Government of IndiaPeeyush KumarDirector, Ministry of Finance, BudgetRitvik PandeyIndian Administrative ServiceBenno FerrariniSenior Economist, Asian Development BankCharan Singh (CS): The central bank’s effective auton-

omy remains somewhat ambiguous till date; hence, it ispossible that the Reserve Bank of India may becomevulnerable to the populist policy measures of the centralgovernment? In that case, meeting policy objectivesincluding debt management will be practically difficult.Under such circumstances don’t you think a separate DebtManagement Office (DMO) with autonomous powers wouldserve the purpose more effectively?

lore in August 2014. The views of the panellists are strictly personalld not be construed as those of the affiliated institutions of thets in an academic institution.

Table 4 Timeline: separation of debt management.

Year Source Recommendations

1997 Report of the Committee on Capital AccountConvertibility (Chairman: Dr. S.S. Tarapore)

Setting up of an Office of the Public Debt (OPD)

1997 A Working Group on Separation of Debt Managementfrom Monetary Management (Chairman: M. Narasimham)

Separate Debt Management Office (DMO) as a companyunder the Indian Companies Act

2000 The Advisory Group on Transparency in Monetary andFinancial Policies

Independent DMO, in a phased manner

2001 The RBI Annual Report 2000e01 Separate DMO2001 The Internal Expert Group on the Need for a Middle

Office for Public Debt Management, (Chairman: A.Virmani)

Establishing an autonomous Public Debt Office

2003 The Fiscal Responsibility and Budget Management(FRBM) Act

Prohibits the Reserve Bank from participating in theprimary market for central government securities witheffect from April 2006

2004 The Report on the Ministry of Finance for 21st Century(Chairman: Vijay Kelkar)

National Treasury Management Agency

2006 Fuller Capital Account Convertibility (Chairman: S.S.Tarapore)

Set up of Office of Public Debt outside RBI

2007 The Union Budget 2007e08 Establishment of a DMO in the government.2008 The High Level Committee on Financial Sector Reforms

(Chairman: Raghuram Rajan)Structural change of public debt management, such thatit minimises financial repression and generates a vibrantbond market. Set up independent DMO

2008 Internal Working Group on Debt Management (Chairman:Jahangir Aziz)

Establishing a DMO

2009 Committee on Financial Sector Assessment (Chairman:Rakesh Mohan)

Setting up DMO

2012 Report of the Working Group on Debt Management Office(Chairman: Govinda Rao)

Independent DMO

2012 The Financial Sector Legislative Reforms CommissionApproach Paper

Separation of debt management with specializedinvestment banking capability for public debtmanagement

2013 The Financial Sector Legislative Reforms Commission(Chairman: B.N. Srikrishna)

Specialized framework to analyse comprehensivestructure of liabilities of the government, andstrategizing minimal cost techniques for raising andservicing public debt over the long term within anacceptable level of risk

Source: Various Reports, GOI and RBI.

62 C. Singh

Harun Khan: The public discourse has focussed on threekinds of conflict in sovereign debt management being doneby the central bank: a) The objective of the RBI as a publicdebt manager may conflict with the prevailing monetarypolicy stance and the market participants; the central bankmay not be increasing interest rates to keep borrowingcosts low and thereby compromising on inflation manage-ment; b) The central bank, being also a debt manager,could take government debt on its balance sheet to ensuresuccessful government borrowing implying that the gov-ernment borrowing plan is completed without any shortageof resources to the government; and c) The imperatives ofthe government borrowing programme may influence thedecision of the RBI as regulator of banks, to reduce theStatutory Liquidity ratio (SLR) requirements. In my view,the institutional arrangements for debt management musttake into account the country specific context and re-quirements. To set the context for this debate, we canexamine the conflict of interest argument in the Indian

context. Even as the government’s borrowings went up bothin absolute and proportional terms, the RBI raised policyrates several times during the past five years; clearly indi-cating its commitment to price stability. The FRBM Act,2003 which precluded the RBI from participating in theprimary auction of government bonds has resolved theconflict of interest with monetary policy. Monetary signal-ling in India is now done by the repo rate (policy rate) underthe liquidity adjustment facility (LAF) and not the bondyields. While theoretical formulations can conjecture con-flicts of interest, the validity of assumptions need to betested by evaluation of experience/performance and onthat count, conflict of interest cannot be established withregard to the RBI.

K Kanagasabapathy: The RBI is legally not an autonomousinstitution. It claims often to enjoy a certain degree ofoperational independence in the area of monetary man-agement. But, in the present arrangement where the RBIis burdened with the responsibility of internal debt

Separation of debt and monetary management 63

management, the RBI’s use of monetary instruments espe-cially for liquidity management such as cash reserve ratio,liquidity adjustment facility, and open market operationscan be clouded easily by the compulsion to achieve theobjectives of debt management such as smooth conduct ofthe government’s market borrowing programme and keep-ing the government securities’ yields under check. Other-wise, how one can explain consistently negative yield of 10year maturity prevalent in the market in recent times? Inthat process, the government securities (G-Sec) yield curvewhich is expected to serve as the benchmark for debt andcredit markets in general gets distorted. The interest ratechannel of monetary policy is rendered ineffective. In thisenvironment, creation of a separate DMO with independentobjectives can definitely help in freeing the RBI from the useof monetary instruments for debt management and to avoidmispricing of government securities yields.

Peeyush Kumar: The argument is self-defeating. It mustbe appreciated that the debt obligations of the governmentflow out of its fiscal operations. There is parliamentarycontrol on the fiscal policy, which in turn determines theborrowing obligations of the government. Moreover, underthe FRBM regime, levels of deficit are subject to directlegislative control. Subject to these parliamentary controls,debt management is purely an executive function of thegovernment. There is a little sense in talking of an inde-pendent debt authority. Presently, debt is managed by theRBI as an agent of the government. If the government sochooses, it can take up debt management directly orthrough an attached office. In any arrangement, debtfunctions will by definition continue to be intimately linkedto fiscal policy of the government. Therefore, it cannot beargued that independent debt management will betterserve the cause of seclusion from the populist measures ofthe government. On the contrary the RBI may be at arm’slength from the government in this respect as compared toany other alternative.

R. K. Pattnaik: There has been some debate in the paston the separation of debt management from the RBI. Aperusal of the debate revealed that in the RBI itself therewere differences of opinion. Nevertheless, the statementof the then RBI Governor (Dr. Subbarao) against the sepa-ration was praiseworthy, particularly in the context of theproposal in the Union Budget 2011e12 to introduce thePublic Debt Management Agency Bill. The MOF of the gov-ernment of India should consider revisiting the whole issuein the light of the governor’s public statement and alsoDeputy Governor Mr. Khan’s views expressed in this con-ference as, globally, there is wide recognition that debtmanagement is no longer a routine exercise. For prudentfiscal, monetary, and debt management, it is advisable thatdebt management should continue with the RBI. The sep-aration of debt management from the RBI will have anadverse impact on the market. It is pertinent to note that inthe dynamic environment created by the introduction ofthe Liquidity Adjustment Facility (LAF) in 2000 and theprohibition on RBI’s participation in the primary marketunder the FRBM Act, 2003, the primary market interestrates, which are auction-driven, are no longer viewed asinterest rate signalling by the RBI. Therefore, the conven-tional argument that there is conflict of interest does nothave much validity. Furthermore, the cost of government

borrowings is inextricably linked to the level of fiscal deficitrather than the arrangement for debt management by thecentral bank. Evidence suggests that the smooth conduct ofthe government’s large borrowing programme has beenfacilitated because the RBI, apart from being the bankerand debt manager to the government, also has a broadrange of responsibilities, including regulation and surveil-lance of financial institutions, financial markets, and mar-ket infrastructure.

Ritvik Pandey: If it is perceived that the RBI’s autonomyis at risk due to populist policy measures of the centralgovernment, it is hard to believe that a newly constitutedDMO can maintain its autonomy. Over the years, the RBI hasearned its autonomy and independence in the system andwould be far more capable of handling populist policymeasures than any other body.

CS: What is the right model for a separate DMO? Shouldit be with the government, the RBI or an independent debtmanagement body?

Harun Khan: To put the debate in its historical context,with regard to the location of sovereign debt managementfunctions, a multiplicity of arrangements exist around theworld: in the MOF, central bank or autonomous debt man-agement agency. Cross country experience shows that thereis no international best practice and the adoption of anyparticular model could depend on country specific circum-stances. In the 1990s, several OECD countries entrusteddebt management to separate agencies with the objectiveof providing monetary policy independence to central banksso that they could concentrate on inflation managementand not be impacted by the conflicting objective of raisingdebt for the sovereign at low cost. It was also perceived thatindependent DMOs would improve operations of debt man-agement through improved accountability and specializa-tion. Many developed nations have followed suit.

Vijay Singh Chauhan: Debt management function per-formed by the RBI is an agent-function performed on behalfof the GOI as the principal. In fact the GOI pays debtmanagement fees to the RBI for the same. In such a sce-nario, the issue also merits consideration from the point ofview of the principal’s freedom to choose the agent.

Peeyush Kumar: I would like to refrain from voicing apersonal opinion in the matter, as I am directly dealing withthe subject in my official capacity. Suffice it to say that thegovernment has announced its decision to separate debtfunctions from the RBI. It is desirable that the governmentand the RBI work out the mechanism jointly so as to ensurethat the emerging structure is ably designed.

R. K. Pattnaik: Debt management should be with theRBI. Independent management and issuance of governmentdebt could distort the sovereign yield curve in a thin mar-ket, jeopardizing the monetary signalling and its trans-mission across the yield curve. In my considered view, alikely outcome of the separation could be the emergence ofmultiple debt management agencies, viz one for the stategovernments’ market borrowings and another for the cen-tral government borrowings. What will happen to the publicdebt offices of the RBI? In such a scenario, coordinationamong debt managers will be difficult and will eventuallylead to conflict and confusion.

K Kanagasabapathy: In creating a new institution forpublic debtmanagement, the complex nature of government

64 C. Singh

liabilities has to be prominently kept in mind. First, govern-ment liabilities include other liabilities besides market debt.Second, it includes both internal and external borrowings.Third is the three layers of governmentdcentre, states, andlocal bodies. An independentDMOshouldbeable to integrateall these. Apart from central and state governments, the RBIis also a stake holder because of the close nexus betweenfiscal and monetary management. Therefore, an idealstructure would be an independent statutory body ownedjointly by central and state governments and the RBI witharm’s length relationship with all these stakeholders. Thisstructure can enable a holistic view of public debt, its sus-tainability and related risks, and also ensure that govern-ments do not fail to meet the fiscal rules and discipline asdemanded by the fiscal responsibility and budget manage-ment legislations and related commitments.

CS: Would a separate DMO help in making monetarypolicy more independent?

Harun Khan: The process of managing public debt is anonerous responsibility, with implications for financial sta-bility in the short to medium term and inter-generationalequity in the long run. Our debt portfolio is reasonablystable and sustainable and due to our conscious strategy ofelongation of maturity, low level of foreign currency debt,and large domestic investor base, risks are at a low level.There is, however, an unfinished agenda of consolidation ofpublic debt and we are moving towards this goal by activedebt management through re-issuances, buybacks andswitches. More efforts are needed to develop a deep andliquid G-Sec market that allows the government to borrowmore efficiently, different classes of investors to enter andexit the market freely, and private sector issuers to pricetheir offerings transparently. We are, therefore, committedto improving liquidity. The RBI has discharged its mandateof managing the public debt in an efficient and effectivemanner. There is merit in continuance of the presentinstitutional arrangement. If at all separation of debtmanagement from central bank has to be effected, itshould be preceded by a well thought strategy focussing onperfect co-ordination among the DMO, the MOF and the RBI.

Peeyush Kumar: The idea of separation of debt func-tions from the central bank emanated because of inherentconflict of interest between the debt functions and otherobligations especially with the central bank’s role in tar-getting inflation through interest rates. Internationally alsoit is unanimously accepted that there is an inherent conflictof interest. However, there are differences on how toresolve this conflict. While some countries have argued forseparation of the two functions, it is also generally agreedthat there has to be close co-ordination between the debtmanagement, fiscal policy, and the monetary policy;liquidity management is contingent upon the debt functionand has to be calibrated in tandem. Therefore, by defini-tion, the debt manager, the government and the RBI needto work in close co-ordination. It is the institutionalarrangement required for this harmonization that is underdiscussion. Under the existing scheme, RBI manages thedebt functions and liquidity internally, with effective syn-chronization by the government of the former. Once thedebt function is segregated from RBI, the policies will haveto be synchronized between the Government, central bankand the debt manager effectively.

R. K. Pattnaik: Not necessarily. The RBI has been suc-cessfully managing the government borrowing programmewith its knowledge and experience in studying marketliquidity, investors’ appetite and risk constraints, apartfrom timing of debt issuance in line with its avowedobjective of maintaining financial stability. There has notbeen any empirical research to prove that the monetarypolicy function has been adversely affected because theRBI is the debt manager. Furthermore, evidence suggeststhat the cash management of the government has remainedpoor and inefficient. The RBI, as banker and debt manager,has been helpful in accommodating the deficit and surplusmode, taking into account the absorptive capacity of themarket. One doubts if an independent body will have theexperience to handle cash management of such magnitudeand varying degree. In the post-crisis environment globally,there has been a renewed focus on debt management asbeing a critical element in the overall conduct for financialstability, as events in Greece have shown. Studies under-taken by multilateral agencies such as the World Bank, In-ternational Monetary Fund (IMF) and Bank for InternationalSettlements (BIS) observe that there is merit in leaving debtmanagement with central banks. The BIS study (November2010) particularly noted that debt management can nolonger be viewed as a routine function that can be dele-gated to a separate, independent body. Instead, suchmanagement lies at the crossroads between monetary andfiscal policy. The study further opined that during difficulttimes, government securities market conditions are bettermanaged by the central banks. In view of this, the studyrecommended that the central banks should be encouragedto revert to their role of managing national debt. Therecent handling of the market borrowing programme by theRBI in a non-disruptive manner in its capacity as debtmanager and monetary authority clearly indicates thatthere exists a strong confluence of interest in debt andmonetary management, contrary to the conventional viewthat there is a conflict of interest. In view of the abovefactors, it is imperative that debt management continueswith the RBI. The Middle Office that has been set up withinthe MOF may be further strengthened to coordinate andprovide technical and analytical input to the cash and debtmanagement committee. The GOI may reconsider theintroduction of the bill on Public Debt Management Agencywith an emphasis on separation of debt management fromthe RBI.

K Kanagasabapathy: Operational independence inmonetary policy would require some legislative changes.Even in the absence of that, separation of debt manage-ment can help making monetary policy more independentthan what it is today.

CS: In the current economic situation, when debt to GDPratio has been declining, would separating debt frommonetary management be useful for India?

Harun Khan: A point that merits attention is that theproponents of separation, while citing examples fromcountries which differ significantly with regard to institu-tional milieu from India, pay little attention to nuances ofdebt management operations. For instance, domestic debtin the UK is managed by the DMO, whereas external debt isthe responsibility of the Bank of England. The whole conceptof an “all-in-one debt office” is a theoretical construct

Separation of debt and monetary management 65

rather than a real organisation. It is also important to notethat sovereign debt management (SDM) is much more than amere resource raising exercise especially in a developingcountry context like ours. The size and dynamics of gov-ernment market borrowing has a much wider influence oninterest rate movements and systemic liquidity. An auton-omous DMO, driven by specific objectives exclusivelyfocussing on debt management, may not be able to managethis complex task involving various trade-offs. With regardto autonomous DMOs focussing on specific responsibilities,the experience of European debt managers is instructive.The experience of the DMO in the Euro area (especiallyGreece, Portugal and Ireland) has been less than satisfac-tory. The independent DMOs seemed to have been guided byperverse incentives and issued short-term/foreign debt in adisproportionate fashion, intensifying roll-over risk, sover-eign risk and financial instability. The debt managementstrategy and operations have resulted in a skewed maturityprofile with balloon payments. For instance, Greece hasbunched maturities during 2010e19 with interest paymentson public debt constituting nearly 40% of Greece’s budgetdeficit during 2009. Large proportion (above 70%) of debt ofPortugal, Greece and Ireland was held by non-residents. Asforeign investors turned risk averse and started withdrawinginvestments, rating agencies downgraded the debt of thesecountries. The debt management strategy has jeopardizedthe fiscal situation and financial stability. Therefore, anautonomous DMO focussing on specific objectives, such ascost minimisation in isolation and not in conjunction withother macro-economic policies may result in sub-optimaldebt management outcomes. Persistent fiscal deficit war-ranting huge borrowings, often at the cost of flow of reservesto the private sector, has been the predominant feature ofthe Indian economy. Increasing borrowings by the govern-ment, the central and the state governments, have to bestrategically planned and tactically executed keeping inview the market conditions, liquidity situation, and macro-economic implications. Thus, given the persistently largesize of the market borrowings, there is a strong case forconfluence of interest between monetary policy and debtmanagement in India. In a situation of excess capital flowsrequiring forex intervention from the RBI and the conse-quent sterilization through issuance of government secu-rities under the Market Stabilisation Scheme (MSS), thecoordination of debt management with these operationsneeds to continue. Separation of debtmanagement from theRBI will make it very difficult to harmonize these operationsas is done at present.

In India, the genesis of the proposal could be traced backto various committees/working groups, such as Committeeon Capital Account Convertibility (1997); Review Group ofStanding Committee on International Financial Standards &Codes (2004), Percy Mistry Committee (2007), InternalWorking Group on Debt Management, MOF (2008), andfinally Financial Sector Legislative Reforms Committee(2013), which suggested separation of debt managementfrom monetary management. During this phase the RBI,while suggesting separation, has made it conditional onattainment of three milestones: development of the G-Secmarket, durable fiscal correction, and an enabling legisla-tive framework. It is argued that a separate DMO will helpestablish transparency, and assign specific responsibility

and accountability on the debt manager and could lead toan integrated and more professional management of allgovernment liabilities, with a focussed mandate. The sig-nificant impact of government borrowing on the broaderinterest rate structure in the economy and, therefore, onthe monetary transmission process in financial markets,makes it a critical component of the macroeconomicmanagement framework. In such a scenario, central bankinvolvement in managing the market volatility and marketexpectations arising out of government debt borrowingbecomes necessary. Past experience, reinforced by therecent developments regarding huge market borrowing ofthe government, has shown the necessity of this approach.Such will be the case even if the central bank is dis-associated from the operational aspects of debt issuance.This being so, it is better for the central bank to havehands-on involvement. It is, therefore, imperative thatfuture course of action needs to be decided based onground realities of our country rather than from an ideo-logical perspective emerging from post-crisis internationalexperience and the fact that the separation of debt man-agement from the central bank could compromise theeffectiveness of monetary policy, efficiency of debt man-agement, and stability of financial markets. Therefore,there is a strong case for continuance of present system ofcentral bank managing debt management in India. In case,however, a decision is taken to move the debt managementfunction to a separate unit, it needs to be preceded by wellthought out strategy on timing of commencement of itsoperations, selection of personnel, their incentive struc-ture, performance evaluation benchmarks from the longterm debt sustainability points of view and arrangementsfor perfect institutional and operational co-ordinationamong the debt management unit, the MOF and the RBI.

Peeyush Kumar: There is no good time for separation ofdebt functions. Of course, the RBI has raised the issue ofhigh levels of debt and prevailing macro-economic condi-tions to argue for deferring the segregation of the debtfunction to a more opportune time, but the merit of thisargument is debatable. It is a fact that high levels of gov-ernment borrowings require active liquidity managementby the bank. Since the central bank does not issue its ownsecurities, it may require using government borrowing formarket interventions under special circumstances. Thisbrings back the argument that there has to be close andeffective coordination between the debt operations andmarket operations. An independent debt manager leads toanother layer in this coordination matrix and may lead todifficulty if this is not managed with dexterity. But that isan argument for better institutional arrangement; thetiming of this arrangement is not the issue, It would becritical to design appropriate institutional mechanisms atwhatever juncture it is attempted.

R. K. Pattnaik: The Indian economy in the post-crisisperiod has been characterized by deceleration in growthand persistent inflation. Themain contributing factor to sucheconomicmalaise is poor fiscal management. Even under thegiven FRBM Act, the Indian authorities were unsuccessful inadhering to the golden rule of government finance, that is,the elimination of revenue deficit. Thus, the borrowings bythe government are pre-empted for meeting current con-sumption expenditure. The continuation of revenue deficit

66 C. Singh

has adversely affected growth through dissaving of thegovernment. Furthermore, this has led to a lower provisionfor capital outlay. Inflation management is difficult as theexpenditure pattern of the government fuelled the demandside, thereby making monetary policy ineffective. It has alsoconstrained the scope of fiscal space.

As long as revenue deficit remains in the fiscal sector thethreat to fiscal deficit and debt continues. One wonderswhether the GOI, which has failed to put in place aneffective and efficient cash management system, canhandle debt management with a separate debt manage-ment office. The RBI is right in its recent assertion that theseparation of debt management from RBI is a sub optimalchoice. In the same spirit one could also argue that fixationof ways and means advances (WMA) limits with mutualagreement, which has largely remained arbitrary, is also asub-optimal choice. It is important to note that poor cashmanagement practice not only wastes money, but also in-hibits the development of local financial markets and un-dermines the effectiveness of monetary policy. First, thelimits could be formula-based as it is for the state govern-ments. Second, in order to even out bunching of receiptsfrom advance income tax payments, a monthly basis systemcould be considered against the present system of quarterlybasis. Third, the receipts given to state governments interms of grants and tax could be reworked taking into ac-count the cash flows. Fourth, since consolidated sinkingfund has not been put in place so far for the GOI, it may beconsidered, to take care of the repayment system. Fifth,the calendar for market borrowings and treasury bills to alarge extent takes care of repayments but it could be re-examined taking into account the cash flow statement. Forthis to be effective, all the agents have to be pro-active,not leaving the management to the RBI. Sixth, the approachso far has been to treat cash management of GOI and stategovernments separately. It is appropriate to put in place acomprehensive approach. Seventh, it would be advisable tohave an expert committee to review the current arrange-ments for WMA/overdraft/surplus and prescribe the limitsand other related arrangements.

CS: How do you explain the difference in the fiscaldeficit and borrowing requirement of the central govern-ment observed in many of the years?

Vijay Singh Chauhan: In theory, the fiscal deficit of thegovernment will equal the net borrowing (i.e. net ofrepayment), adjusted for the changes in the cash balances.In the case of GOI, the position is rather complicated. Firstly,central government has a single cash balance accountcovering the consolidated fund, the public account, and thecontingency fund. As you know, fiscal deficit relates only totransactions covered by consolidated fund. Therefore, sur-pluses in public account reduce the market borrowingrequirement. Secondly, the cash balance account of all thestate governments and the central government is linkedthrough the mechanism of ad hoc treasury bills. Put simply,cash balance surpluses of state governments get transferredas borrowing to central government. Since, state govern-ments have been running cash surplus for many years now,the market borrowing requirement of central governmentcan be reduced to that extent. Thirdly, there exists themechanism of Market Stabilization Scheme (MSS) whichprovides for GOI borrowing in excess of its requirement, at

the request of RBI for sterilization purposes. Since borrowedfunds are not available for spending and are sequestered, itdoes not impact fiscal deficit.

CS: In the pre-crisis period a dominant view wasemerging that cash, debt, and liquidity managementshould be segregated. What are the reasons after theglobal financial meltdown that led to a predominant shiftin that view? What according to you would be the correctapproach for India to follow?

Harun Khan: In the pre-crisis phase, the functions ofmonetary policy, financial stability and sovereign debtmanagement (SDM) used to be looked upon as an “impos-sible trinity”. Post-crisis, their interdependence isincreasingly being recognized. Unlike in the past, centralbanks’ operations are not currently confined to the shorterend but are carried out across the yield curve. Similarly,government debt managers, opportunistically or undercompulsion, are increasingly operating at the shorter end.This has intensified the interaction between monetarypolicy and SDM, warranting greater coordination in the in-terest of policy credibility and financial stability. Interna-tionally, there has been a rethinking on the issue of debtmanagement by central banks, with scholars like CharlesGoodhart articulating that debt management being a crit-ical element in the overall conduct of macroeconomicpolicy, central banks should be encouraged to revert totheir role of managing the national debt. In this context,the cause of coordination is always better served under thesame roof than by a separation from the central bank,accompanied by a closer inter-institutional coordination.There could be an argument that coordination mechanismcould be designed between the central bank and the DMOeither by statute or executive order. The experience ofcoordination mechanisms between the DMO and the centralbank, which are vital for economic management, is how-ever, far from satisfactory and has impacted debt man-agement. There have been instances of failed auctions, inthe UK (March 2009) for instance, causing reputation riskfor both the authorities. Against this backdrop, it is stronglyfelt that given the large size of the market borrowings,there is a confluence of interest between monetary policyand debt management in India.

K Kanagasabapathy: Cash and debt management func-tions are inseparable by definition since it is the need forcash that necessitates borrowings. Also the situation ofcash surplus needs to be handled in an integrated manner.Liquidity management is essentially a monetary operation.The liquidity management by the central bank shouldensure that the quantum channel of monetary policyoperating through its liquidity management is consistentwith its tight or easy policy stance. For instance when atight monetary policy stance is taken it is necessary thatthe liquidity is also kept tight in the system. If enormousliquidity is provided when the policy stance is tight, it willnot ensure effective operation of the interest rate channel.When cash and debt management is combined withliquidity management, then the liquidity management canbe clouded by the objectives of debt management. This isone reason why the G-Sec yields get mispriced contrary tomonetary policy stance. While liquidity management is tobe independent of cash and debt management, it is stillnecessary that the monetary authority is kept informed of

Separation of debt and monetary management 67

cash and debt flows impacted by the debt managementagency’s actions since the total liquidity in the system isinfluenced by movements in cash balances of governmentsand also primary issuances of government debt. This in-formation sharing will ensure smooth operation of liquiditymanagement consistent with monetary policy stance.

Peeyush Kumar: The US Fed policy of quantitativeeasing was to a great extent responsible for the bubble thatwas created in years preceding global financial crisis (GFC).The 2008 crisis was also the result of reckless debt practicesadopted by some countries, especially in the EuropeanUnion. Thus analysis of the financial crisis faced at theglobal level led to the growing sense that the cash, debtand liquidity management functions must be discharged intandem by the central banks. It was in some way a reversalof the earlier stance of segregation of these functions, andthere was general consensus that there had to effectivedovetailing of these policies even when they were beingperformed separately. India has had a record of prudentfinancial systems which was demonstrated by the fact thatGFC did not have any direct impact on Indian financialmarkets. There can be no denying the fact that debt policyand liquidity management functions are intertwined andeven if they are to be segregated there will be need forsynergy in policy. Much depends on the institutionalarrangement and its functioning.

R. K. Pattnaik: A very careful decision needs to betaken. One has to note that cash, debt, and liquiditymanagement are public goods. The persistence of largesurplus in recent times by the government with the RBI hasadverse implications for fiscal policy, monetary andliquidity management, and domestic public debt manage-ment. Unlike the cash deficit management, the cash surplusmanagement has not received adequate public attention.This could be because in public policy it is apparentlyassumed that the emergence of surplus is “good” anddeficit is “bad”. The persistence of cash surplus also makesdebt management difficult. In recent times, there wereinstances of cancellation of auction of dated securities andtreasury bills implying that the calendar of issues becomesredundant and there is a stress on price discovery process insubsequent auctions. We have a Cash and Debt Manage-ment Committee which is an excellent institutionalarrangement with representatives from the RBI and thegovernment. Further strengthening of this institutionalmechanism could be a better option than separation offunctions. A few policy options for the consideration of thecommittee are in order.

First, introduction of an ex ante cash flow statement ona daily basis to analyze the cyclical and structural factors.Second, elimination of structural factors contributing tocash surplus and fixing a limit of surplus for the governmentin the same manner as WMA.

Third, transferring the investment in 14-day intermedi-ate treasury bills with immediate effect to ‘consolidatedsinking fund’ investment to address the humps in debtrepayment in the immediate future. Fourth, advance taxcollection on a monthly basis in place of a quarterly basis.Fifth, in order to ensure transparency, the central govern-ment and the RBI may consider disseminating data to thepublic on the modalities of surplus investment, which in-cludes the volume, rate of interest, and maturity. Sixth,

one option which needs serious consideration of the au-thorities is the investment of government surplus in themarket through an auction system.

CS: What are your views on debt sustainability? Is therean internationally accepted benchmark for assessing thesustainability of domestic debt? If not, what is the under-lying mechanism adopted by the GOI to identify thethreshold range of sustainable debt?

Benno Ferrarini: International bodies, such as the IMF,have adopted a debt ratio of 40% to GDP as a rule-of-thumbbenchmark for emerging markets. Unfortunately, it is farfrom straightforward to establish a relevant benchmark, ordebt limit, that distinguishes a safe debt ratio from a per-ilous one. Such a benchmark should reflect a country’s debttolerance, that is its capacity to successfully manage fiscalpolicy as debt rises. But debt tolerance depends on a widerange of country specific factors, including debt structure,hidden liabilities, economic volatility, institutional quality,adjustment record, and default history that are difficult totranslate into a benchmark. In the case of India, thebenchmark is likely much higher than 40% to GDP. Thecountry’s share of external debt is small, which limitsexposure to foreign sentiment and discipline about debtsustainability. Moreover, debt financing and management inIndia is greatly facilitated by the fact that the public sectoritself, through shares in banks and insurance companies,holds a significant share of GOI securities. Finally, nearly allof the government debt is in fixed interest loans and theaverage residual maturity of the central government debt isrelatively long by international standards, so the refinanc-ing risk is low. Notwithstanding these considerations, thereis no room for complacency and the public debt ratio mustbe held closely in check. The global financial crisis in 2008and a marked slowdown of GDP growth more recently un-derscore the need for continuing policy focus to ensurefiscal sustainability and financial stability, and for furtheraction towards strengthening the practices India employs inmanaging its public debt.

Peeyush Kumar: There are no internationally acceptedbenchmarks for sustainable levels of debt. Some advancedeconomies have very high levels of debt without any majormacro-economic instability; while a few countries withrelatively lower levels of debt have faced serious crisis.Interestingly, emerging economies generally have morestable debt levels. Debt sustainability has to be viewed inthe specific macro-economic framework of the country;pertinently in the context of debt profile, external risk,financial systems etc. In the Indian context, where debt ispredominantly exchange-rate shock free and domesticallyheld in fixed tenor instruments, level of debt is not anoverwhelming concern. Of more immediate concern is theincreasing size of gross borrowing especially with roll-overraising the gross borrowing. With increase in governmentborrowing, crowding out of private investment has a dele-terious impact on the growth cycle. The government has,under the new FRBM regime, limited its borrowing levels toprovide impetus to private investment and revival ofgrowth cycle.

R. K. Pattnaik: Our empirical exercise reveals that thetax buoyancy for the centre is around 1.35 and the totalrevenue buoyancy is 1.17, whereas the expenditure elas-ticity is 1.22. This indicates that an elimination of revenue

68 C. Singh

deficit in the medium term looks difficult unless tax buoy-ancy is further increased with emphasis on minimizing thestructural component. In non-interest revenue expendi-ture, the structural component predominates. However,the share of development expenditure in this category islower than the non-development components. The persis-tence of revenue deficit accentuates the vicious cycle ofdeficit and debt. The current debt to GDP ratio at around50% for India seems to be lower than the European econo-mies, the US and Japan. However, a sheer low number ismeaningless until the sustainability factor is suitablyaddressed by elimination of revenue deficit. In a federalset-up like India, the analysis of fiscal sustainability isincomplete without addressing underlying issues in statefinances. Evidence suggests that fiscal consolidation interms of reduction in revenue deficit has been moreencouraging in case of state governments. However, ourtechnical analysis suggests that this improvement has beenachieved to a large extent by the Finance Commission (FC)awards. Thus, the indicative ceiling on overall transfer tostates on the revenue account is set at 39.5% of gross rev-enue receipts of the centre on the basis of the recom-mendation of the Thirteenth FC. Thus, the elimination ofrevenue deficit will have implication for state finances interms of the tax devolution to states as well as grants-in-aidto states. For example, the share of grants in the totaltransfer has come down from 18.9% to 15.1% from theTwelfth to Thirteenth FC.

Ritvik Pandey: While the state debt was relativelysteady at around 20e22% of GDP till the year 1997e98, itstarted increasing sharply after that. The fiscal deficit alsoremained below 3% of GDP till 1997e98, but increased to4.5% by 1999e2000. One main reason for this sharp increasewas implementation of Fifth Pay Commission report by thestates and poor revenue performance by the states. By theend of 2003e04, the debt levels touched almost 32% of GDP.To give a historical perspective, the debt to GDP ratio in1971e72 was 20% compared to 4% in 1951e52. It came downto 18% by 1983e84 and increased to 20% percent by1988e89. Therefore, the debt stress witnessed by thestates during the first few years of this century was un-precedented and took its toll on delivery of public services.The states found it difficult to even pay salaries andrepeatedly faced cash crunch. The debt of the state has tobe approved by the central government. This had been theprimary source of control over the state debt till the 12thFC recommended that states legislate their FRBM Acts. The12th FC also mandated states to chalk out a debt consoli-dation roadmap in accordance with broad targets recom-mended by it. Later, the 13th FC refined the debtconsolidation roadmap and gave a formula for determiningthe borrowing ceiling of a state by the centre. Normally,the overall borrowing ceiling is decided by the formulagiven by the 13th FC and then using a projected amount ofinflows from other sources, the amount to be raised throughMarket Borrowings is determined based on which the RBIdraws a borrowing calendar. Experience has shown that thedebt and deficit levels prescribed by the successive FCs,which now form part of the FRBM Acts of the states haveworked well. It is not an easy job to fix an exactly optimallysustainable debt level. However, from a practical view-point, a good benchmark is one that is acceptable,

implementable, and maintains the balance betweenaffordability and the development needs of the govern-ment. To this effect, the current ceilings have passed thetest of time.

CS: What has been the impact of low buoyancy of cen-tral transfers and spillover of central pay revisions on statefinances?

Peeyush Kumar: The transfer of funds from the centreto the states has been increasing on two counts. One,successive FCs have been increasing the state’s share ofdevolution, and the centre has been increasing the planscheme allocations both under the centrally sponsoredschemes and central assistance to States. As a result ofincreasing devolution from the centre, state finances haveshown marked improvement. With development functionsbeing largely taken care by the funds from the centre,states have not only adhered to their respective fiscal tar-gets but to a large extent achieved surplus on revenueaccount, despite pay revisions.

Ritvik Pandey: State finances have seen many cycles ofups and downs since independence and states have adopteddifferent strategies to cope with the financial challengesthat they faced from time to time. The states’ capacity todeal with the challenges differs widely. While some statesare largely self-reliant, others heavily rely on centralfinancial assistance. While some face resource disabilitydue to structural issues, others have been facing problemsdue to poor fiscal management over long term. Similarly,the cost disabilities faced by each state also differs. Thesedisparities have led to each state being in a different statuswhen it comes to debt and deficit management. While thestate finances have been primarily guided by factors such ascomposition of economy, demography, social development,and geography, there even have been certain one-offevents that have had lasting or even permanent impacton a few states. For example, terrorism in Punjab has hadalmost a permanent impact on the debt levels that thestate has been into. There are certain events that haveimpacted the debt levels of all states but have haddifferent impact on different states depending on theirfiscal capacity, such as in the case of pay commissions.Overall, states have evolved their own strategies for debtand deficit management depending on their strengths andchallenges. However, there has been some uniformity intheir approaches, especially recently, mainly due to theoverall legal framework, role of the centre and other cen-tral bodies like the RBI and the approach followed by thecentral finance commissions.

CS: The FRBM guidelines necessitate significant reduc-tion in fiscal deficit, which may eventually affect govern-ment expenditure on the social sector. In this regard, towhat extent will the FRBM Act be feasible for an emergingcountry like India?

Peeyush Kumar: Fiscal responsibility and budget man-agement is the mechanism of legislative control over debt.It is not only desirable but also essential in a parliamentarysystem to have such a control on one of the most importantparameters of fiscal policy. The constitutional provisions ofbudgetary control provide for expenditure control but sincethere is no direct control on revenues, deficit is incidentalrather than a principal policy instrument. Fiscal re-sponsibility and budget management brings back the focus

Separation of debt and monetary management 69

on deficit and requires government to determine the size ofborrowing upfront. In this sense, FRBM changes the orien-tation of fiscal policy. Since the turn of this century, it hasbecome the mainstay of fiscal policy both at the centre andstate level. In emerging countries like India there is a def-inite need to provide for welfare and social sectors to caterto the vulnerable sections. However, it is also incumbent onthe government to provide the right policy direction togrowth to meet the growing aspirations of the nation.Governments have to be responsible enough to provideimpetus to growth, which in turn allows access to moreresources for welfare measures. There is a fine balancebetween the competing demands, and FRBM enjoins thegovernment to follow a prudent debt and fiscal policy.

R. K. Pattnaik: The preamble to the FRBM Act 2003states that it is: “An Act to provide for the responsibility ofthe central government to ensure inter-generational equityin fiscal management and long term macro-economic sta-bility by achieving sufficient revenue surplus and removingfiscal impediments in the effective conduct of monetarypolicy and prudential debt management consistent withfiscal sustainability through limits on the central govern-ment borrowings, debt and deficits, greater transparency infiscal operations of the central government and conductingfiscal policy in a medium-term framework and for mattersconnected therewith or incidental thereto”. Fiscal re-sponsibility and budget management is based on the aboveobjectives. Therefore, in the long run it is growth and socialsector supportive. The fiscal consolidation through FRBMshould emphasize the four Fs of fiscal empowerment(maximize revenue to the budget), fiscal transparency(avoidance of any creative accounting), fiscal marksman-ship (maintaining budget integrity avoiding large deviationin the budget estimates, revised estimates and accountsfigures) and fiscal space (counter cyclical policies tomanage the fluctuations in business environment due toexogenous shocks). If these four wheels are strong the fiscalsector cart will have a smooth run.

Ritvik Pandey: Reduction of deficit does not necessarilymean reduction in expenditure. In fact, in India fiscal re-forms have been mainly revenue led. Governments at bothlevels realized that the revenue realization has been at asub-optimal level and embarked upon ambitious revenuereforms, many of which were targetted towards fixing taxadministration. Expenditure reforms in India are yet to takeoff full steam. Impact of some of the reforms like the shiftto a contributory pension scheme will be visible only after adecade or so. Social sector spending should only be the lastcasualty of fiscal reforms since many other opportunitiesexist.

CS: What are your views on the introduction of theconcept of effective revenue deficit in fiscal calculus?

R. K. Pattnaik: In my considered view, introduction ofeffective revenue deficit (ERD) is a classic case of creativeaccounting and is against any norm of fiscal prudence. Whatare the advantages of ERD? The union budget makes adistinction in functional expenditure categories. Capitalgrants should not be part of revenue expenditure as it ismeant for creating capital assets. What are the disadvan-tages of ERD? It is against the constitutional provisions ofbudget making. Annual financial statement (AFS) presentedto the parliament according to Article 112 of the Constitution