section 3. asic industry trends - smithsonian...

TRANSCRIPT

ASSPs AND ASICs

The term ASIC (Application Specific IC) has been a misnomer from the very beginning. ASICs, asnow known in the IC industry, are really customer specific ICs. In other words, the gate array orstandard cell device is specifically made for one customer. ASIC, if taken literally, would meanthe device was created for one particular type of system (e.g., a disk-drive), even if this device issold to numerous customers and/or is put in the IC manufacturer’s catalog.

Currently, a device type that is sold to more than one user, even if it is produced using ASIC tech-nology, is considered a standard IC or ASSP (Application Specific Standard Product). Thus, weare left with the following nomenclature guidelines (Figure 3-1).

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-1

3 ASIC INDUSTRY TRENDS

Figure 3-1. ASIC Industry Terminology

ASIC: A device produced for only one customer. PLDs are included as ASICs because the customer “programs” that device for its needs only. CSIC: What ASICs should have been called from the beginning. Some companies differentiate an ASIC from a CSIC by who completes or is responsible for the majority of the IC design effort. If it is the IC producer, the part is labeled a CSIC, if it is the end-user, the device is called an ASIC. This term is not currently used very often in the IC industry. ASSP: A relatively new term for ICs targeting specific types of systems. In many cases the IC will be manufactured using ASIC technology (e.g., gate or linear array or standard cell techniques) but will ultimately be sold as a standard device type to numerous users (i.e., put into a product catolog). If the end-user helped the IC producer design the ASSP, that user is typically given a market leadtime (i.e., window of opportunity) to use the device before it is made available to its competitors. CSP: Customizable Standard Products are 70 to 90 percent standard with 10 to 30 percent of the chip available for user-specified logic, memory, or peripheral functions.

19181ASource: ICE, "Status 1996"

One problem many IC producers have run into while producing ASSPs is that in order to providethe optimum part, the IC producer must understand the system application at least as well as theend-user. Because this system-level expertise is not easy to acquire, most ASSP vendors haveformed close relationships or partnerships with end-users. In this way, the IC vendor and end-user work closely together early in the system design cycle in order to properly define the ASSPdevice.

In general, as standard ICs take aim at ever finer segments of the marketplace, they ultimatelyevolve into ASSPs. In other words, at some point in time there could be very few standard ICs;most devices produced would be aimed at specific system needs. An example would be certainDRAMs architecturally optimized for a hand-held telecom system, laptop PC, or HDTV set. Thisis precisely the direction the IC industry is now heading.

Figure 3-2 shows some of the devices that National Semiconductor considers ASSPs. As IC pro-ducers customize their devices for specific system needs, the list of ICs labeled as ASSPs contin-ues to expand. In 1995, Sharp Corporation plans to release an ASSP product based upon the33MHz ARM RISC 32-bit MPU core. The ARM ASSP will include a 480x320 monochrome LCDcontroller, 115-kbaud serial data infrared transceiver, write-back cache controller, on-board SRAMoptimized for real-time interrupt, and pulse-width modulators. As was mentioned earlier, 20years from now there may be few “standard” ICs produced.

Although the 1995 ASIC market is estimated to have been $15.7 billion, the ASSP-type products(which are part of the special purpose MOS Logic category) are taking away some of its momen-tum (Figure 3-3). Overall, the ASIC market (not including full custom) is forecast to follow totalIC industry growth rates fairly closely.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-2

Figure 3-2. Sampling of ASSPs from National Semiconductor

• Mainframe connectivity solutions • FDDI devices • Local area network (LAN) ICs • Telecommunications products (e.g., CODECs) • Graphics ICs • Mass storage devices • Real-time clocks • DRAM management ICs • Floppy-disk devices • UARTs

17776Source: ICE, "Status 1996"

Does the proliferation of ASSPs and more customer-specific standard products mean an end to theASIC market? No. This is because most of the pros and cons of ASICs versus ASSPs or standardproducts still exist.

The primary advantage of ASSPs or standard products is the ability to immediately (most of thetime) purchase the ICs and get the system to market quickly. However, ASIC devices allow thesystem producer to differentiate its product from the competition. The result is that many timesthe system producer is able to gain marketshare and/or better profit margins.

In some cases standard products and ASICs are merging in an attempt to offer the benefits of bothapproaches. In 1993, TI announced that it was merging an enhanced version of its standard fixed-point TMS320C25 DSP chip and 15,000 usable and customizable 0.8-micron CMOS gate-arraygates on one device. Thus, the user is able to take advantage of well characterized high-perfor-mance DSP circuitry while at the same time adding unique features to give its system a differen-tial advantage over its competitors. TI estimated that 30 percent of its total DSP IC sales in 1995would be in customizable version form.* This percentage was expected to rise to 50 percent in2000.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-3

0

1

2

3

4

5

6

7

8

1995 (EST)

199419931992

Year

Bill

ion

s o

f D

olla

rs

26%

26%

28%

20204ASource: ICE, "Status 1996"

3.75

4.74

5.98

7.63

Figure 3-3. Special Purpose MOS Logic Market (1992-1995)

* Through 1995 TI’s belief in the success of its customizable DSP was well founded. TI’s big jump in gate array sales in1994 and 1995 was greatly due to the success of its gate array DSP program.

Another grey area is where Cirrus Logic takes one of its ASSP ICs and customizes a portion of itfor one of its customers. Typically only about 5-10 percent of the new design is customized for theend-user. This “tweaked” device is still normally classified as an ASSP since the majority of thecircuitry is still ASSP-based.

There is no question that the IC industry will continue to evolve toward devices that are specifi-cally suited for the customers’ needs. ICE believes that various versions of ASICs and ASSPs willco-exist to help serve those needs in the most economical and efficient manner possible.

ASIC Definitions

Some basic definitions and classifications are shown below in order to define what ICE meanswhen using the various terms used to describe today’s ASIC devices. ASIC stands for ApplicationSpecific Integrated Circuit and according to ICE’s definition includes gate arrays, standard cells(sometimes called cell-based), full custom, and programmable logic devices (PLDs). Thesedevices are classified as either semicustom, custom, or PLDs. Formal definitions are given inFigure 3-4.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-4

I. Semicustom IC - A monolithic circuit that has one or more customized mask layers, but does not have all mask layers customized, and is sold to only one customer.

Gate Array - A monolithic IC usually composed of columns and rows of transistors (organized in blocks of gates). One or more layers of metal interconnect are used to customize the chip. Sometimes called an uncommitted logic array (ULA). Linear Array - An array of transistors and resistors that performs the functions of several linear ICs and discrete devices.

II. Custom IC - A monolithic circuit that is customized on all mask

layers and is sold to only one customer.

Standard Cell IC - A monolithic IC that is customized on all mask levels using a cell library that embodies pre-characterized circuit structures. ICs that are designed with a silicon compiler are included in this category. Most "embedded" arrays are included in this category. Full Custom IC - A monolithic IC that is at least partially "handcrafted". Handcrafting refers to custom layout and connection work that is accomplished without the aid of a silicon compiler or standard cells.

13660ESource: ICE, "Status 1996"

Figure 3-4. ASIC Definitions

ICE does not include ASSPs in its ASIC market figures. An example of an ASSP part that is notclassified as an ASIC by ICE is Hitachi’s H8/300H Series of microcontrollers. Although theH8/300H user is able to customize this MCU using an extensive Hitachi cell library, the finisheddevices are almost always allowed to be sold to other Hitachi customers after a certain period oftime (Motorola has a similar program using its 68HC05 MCUs).

In mid-1994, Motorola announced its FlexCore program that allows the end-user to use Motorola’s32-bit MPUs as cores in cell-based designs. This program is significantly different from its, andHitachi’s, MCU ASSP offerings in that the finished devices will most likely stay proprietary to theoriginal customer. Thus, these devices are considered to be standard cell ASICs.

The FlexCore-type ASIC program* is a prime example why ASSPs will not eliminate the marketfor ASICs. As was mentioned earlier, ASSPs will still hold an advantage in time-to-market, butthey will never be able to compete with the product differentiation capability of robust ASIC offer-ings such as FlexCore.

Another ASIC segment that needs additional clarification and discussion is the PLD category. ICEincludes under the generic term PLD the simple bipolar fuse-programmable PAL devices (e.g., the22V10) produced by AMD, TI, and National, the complex programmable (CPLD) devices (thattypically have configurable macrocells, multiple feedback paths, etc.) that are usually MOS mem-ory cell-based, and what are called field programmable gate arrays (FPGAs). Figure 3-5 comparesthe architectures of a typical CPLD and a typical FPGA.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-5

Figure 3-4. ASIC Definitions (continued)

III. Programmable Logic Device (PLD) - A monolithic circuit with fuse, antifuse, or memory cell-based circuitry that may be programmed (customized), and in some cases, reprogrammed by the user (in-system or prototype form).

Simple PLD (SPLD) - Usually a PAL or PLA, typically contains less than 750 logic gates. Complex PLD (CPLD) - A hierarchical arrangement of multiple PAL-like blocks. Field Programmable Gate Array (FPGA) - A PLD that offers fully flexible interconnects, fully flexible logic arrays, and requires functional placement and routing. Electrically Programmable Analog Circuit (EPAC) - A PLD that allows the user to program and reprogram basic analog functions.

13660ESource: ICE, "Status 1996"

* Zilog has a similar program for its Z80 MCU devices.

The FPGAs are produced using MOS memory cell (and thus are usually reprogrammable) or anti-fuse technology. The physical (e.g., line lengths) and electrical characteristics of the interconnectsare unknown before programming, just like a gate array.

As was shown, the PLD classification now encompasses a broad range of products and most peo-ple in the IC industry are aware that the term PLD is no longer synonymous with the nearly obso-lete bipolar fuse-programmable PAL.

Another definitional clarification that should be mentioned is in the standard cell category. Manyof the standard cell designs produced in the ASIC industry use a combination of pre-characterizedand “handcrafted” circuit structures. ICE categorizes an ASIC that has 50 percent or more of itscircuitry composed of cells as a standard cell IC. If less than 50 percent of the circuitry is from pre-characterized cells (with the majority of the design being handcrafted), the IC is considered a fullcustom ASIC.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-6

20205Source: CICC 1995/ICE, "Status 1996"

SPLD Block

SPLD Block

CPLD

SPLD Block

SPLD Block

Global Bus

Logic Block

Interconnect

I/O Cell

FPGA

Figure 3-5. CPLD Versus FPGA Structures

Another device that deserves some further discussion is the embedded array ASIC. When design-ing with this device, the customer first identifies any megacell functions that will be needed. TheASIC producer optimizes the layout of the cell-based design and then begins producing basewafers. While the base wafers are being fabricated, the customer is finishing design work for theuncommitted random logic area (gate array portion) that was set aside in the initial design. Afterthe base wafer is finished being processed, the gate array area of the base wafer is metallized.

The ultimate goal of the parallel random logic design and cell-based wafer fabrication efforts ofthe embedded array program is to shorten the turnaround time encountered with standard celldevices. Many embedded array producers are achieving turnaround times very close to those ofgate arrays.

Although both standard cell and gate array design and fabrication techniques are used on theembedded array, because all of the mask layers of the device are customized for the user, ICE willclassify the embedded array ASICs (e.g., VLSI Technology’s Flex-Arrays) as standard cells.

Throughout “Status 1996” ICE usesterms such as available, total, raw,and usable when referring to gatedensities. Figure 3-6 shows the def-initions followed by ICE in regard togate count. Typical usable gatecounts for various ASICs are shownin Figure 3-7.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-7

AVAILABLE, TOTAL OR RAW GATES The number of unconnected gates on a device.

USABLE GATES The number of gates that can typically be interconnected implementing an "average" design. Usable gate count will always be less than the number of available, total, or raw gates.

16779Source: ICE, "Status 1996"

Figure 3-6. Gate Count Definitions

ASIC Type Usable Gate Percentage

Double-Level Metal MOS PLD

Triple-Level Metal MOS PLD

Double-Level Metal Channelled Gate Array

Double-Level Metal Channelless Gate Array

Triple-Level Metal Channelless Gate Array

Five-Layer Metal Channelless Gate Array

Standard Cell

Full Custom

30 - 50

60 - 70

85 - 95

40 - 50

60 - 70

75 - 85

85 - 95

100

16780BSource: ICE, "Status 1996"

Figure 3-7. Sampling of Usable Gate Counts

As total gate densities have increased, the IC manufacturer has had to go to a greater number ofinterconnect levels (i.e., metal layers) to keep die size and usable gate counts manageable. Thishas been especially evident with the new triple-level metal PLDs. As will be discussed, the newPLD technologies are helping reduce PLD die size dramatically, and in turn, significantly reducemanufacturing costs.

Of course the move to a greater number of metal layers comes with cost and complexity problems.With an increasing number of ASIC designs being pad limited (i.e., the die size is dictated by thenumber of I/O pads rather than the logic gate area) the move to more layers of metal has pro-ceeded very slowly in the ASIC user base.

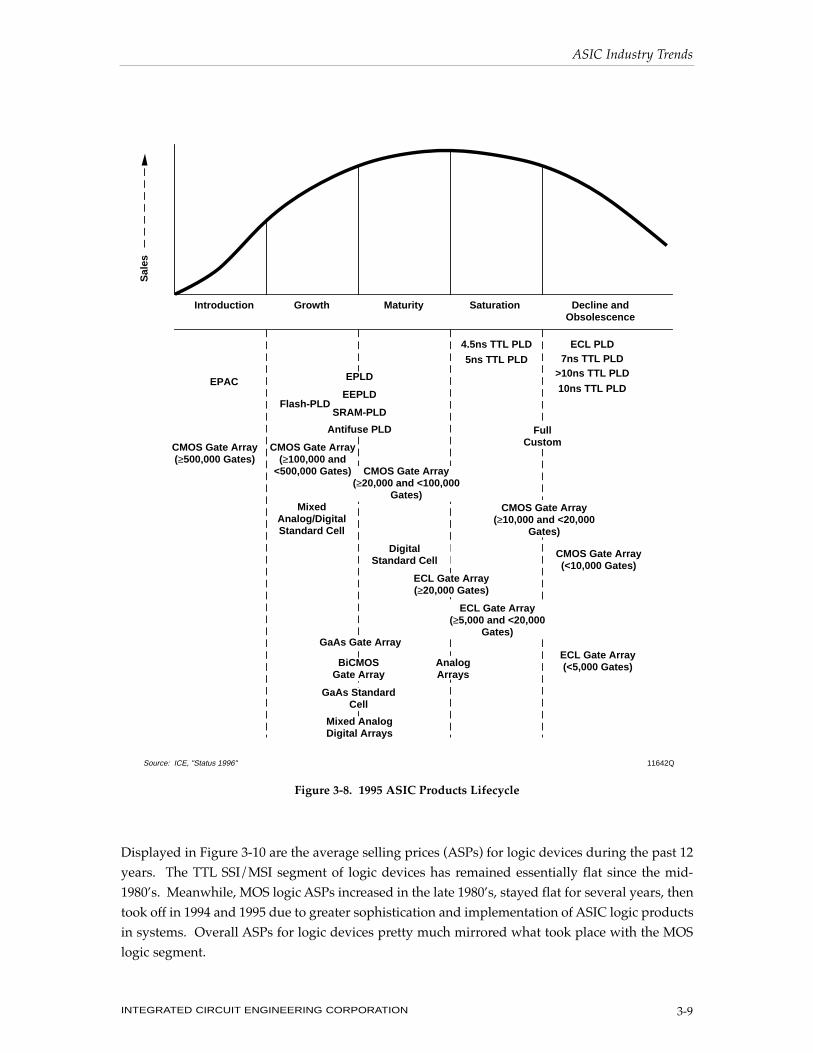

ASIC Product Lifecycle

Figure 3-8 shows the 1995 location of each of the major ASIC families on the product lifecyclecurve. It is interesting to note that most of the classifications still reside on the growth side of thecurve. As the ASIC market matures, the majority of the ASIC product types will be in orapproaching the maturity stage of their lifecycles in the late 1990’s.

Low density (i.e., less than 10,000 gates) gate arrays are considered to be in the saturation/declinestage. In 1995, many gate array vendors were shying away from accepting designs for low gatecount arrays. As veteran IC buyers know, once products enter the latter stages of the lifecycle,price becomes a secondary concern to availability. Likewise, slow bipolar TTL PALs are quicklylosing marketshare and are now in the decline stage. As shown, replacement products for theslow bipolar TTL PAL and low density gate array, such as MOS PLDs, are currently in the intro-duction or growth/maturity stage.

THE LOGIC MARKET

An analysis of the logic market provides a good background to the study of the ASIC market sincea vast majority of ASIC products perform some basic logic function within a system.Approximately 20 percent of 1994 and 1995 worldwide IC output was for some form of logic device.

Figure 3-9 shows the logic trends by technology. The most obvious trend shown on the graph isthe tremendous growth of CMOS logic. In eight years (1987-1995), CMOS technology grew from55 percent of the logic market to 85 percent. On the other hand, older technologies such as NMOSand bipolar are quickly being phased out. ECL technology, after maintaining about eight percentof the logic marketshare for several years, declined to around three percent in 1995 and is forecastto drop to a smaller marketshare percentage through the year 2000. Many of the better perfor-mance characteristics of ECL and other older technologies have been replicated in CMOS andBiCMOS technologies in recent years. These two technologies will dominate not only the logicmarket (98 percent in the year 2000), but all digital IC production in the foreseeable future.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-8

Displayed in Figure 3-10 are the average selling prices (ASPs) for logic devices during the past 12years. The TTL SSI/MSI segment of logic devices has remained essentially flat since the mid-1980’s. Meanwhile, MOS logic ASPs increased in the late 1980’s, stayed flat for several years, thentook off in 1994 and 1995 due to greater sophistication and implementation of ASIC logic productsin systems. Overall ASPs for logic devices pretty much mirrored what took place with the MOSlogic segment.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-9

CMOS Gate Array (≥10,000 and <20,000

Gates)

Introduction Growth Maturity Saturation Decline and Obsolescence

Sal

es

ECL PLD

>10ns TTL PLD

11642Q

EPLD

EEPLD

SRAM-PLD

Full CustomCMOS Gate Array

(≥100,000 and <500,000 Gates) CMOS Gate Array

(≥20,000 and <100,000 Gates)

Digital Standard Cell

Mixed Analog/Digital Standard Cell

ECL Gate Array (≥20,000 Gates)

ECL Gate Array (≥5,000 and <20,000

Gates)

ECL Gate Array (<5,000 Gates)

GaAs Gate Array

BiCMOS Gate Array

Analog Arrays

Source: ICE, "Status 1996"

Antifuse PLD

GaAs Standard Cell

5ns TTL PLD 7ns TTL PLD

10ns TTL PLD

4.5ns TTL PLD

Mixed Analog Digital Arrays

CMOS Gate Array (<10,000 Gates)

Flash-PLD

CMOS Gate Array (≥500,000 Gates)

EPAC

Figure 3-8. 1995 ASIC Products Lifecycle

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-10

0

10

20

30

40

50

60

70

80

90

100

2000 $50.0B

1995 $24.5B

1994 $19.7B

1987 $11.6B

1982 $3.3B

Per

cen

t o

f T

ota

l Lo

gic

Mar

ket

*Includes 1% for GaAs

51%

8%

18%

23%

27%

8%

10%

55%

10% 8%4%

<1%4%

4%

3% 2%

<1%

5%

93%*85%

82%

12875N

TTL and Other Bipolar

ECL

NMOSCMOS

BiCMOS

Source: ICE, "Status 1996"

Figure 3-9. Logic Market Trends

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

1995199419931992199119901989198819871986198519841983

TTL SSI/MSI

MOS Logic

Total Logic

AS

P (

$)

(EST)

20197A

Year

Source: WSTS/ICE, "Status 1996"

Figure 3-10. Average Selling Price for Logic Devices

ASIC MARKET FORECAST

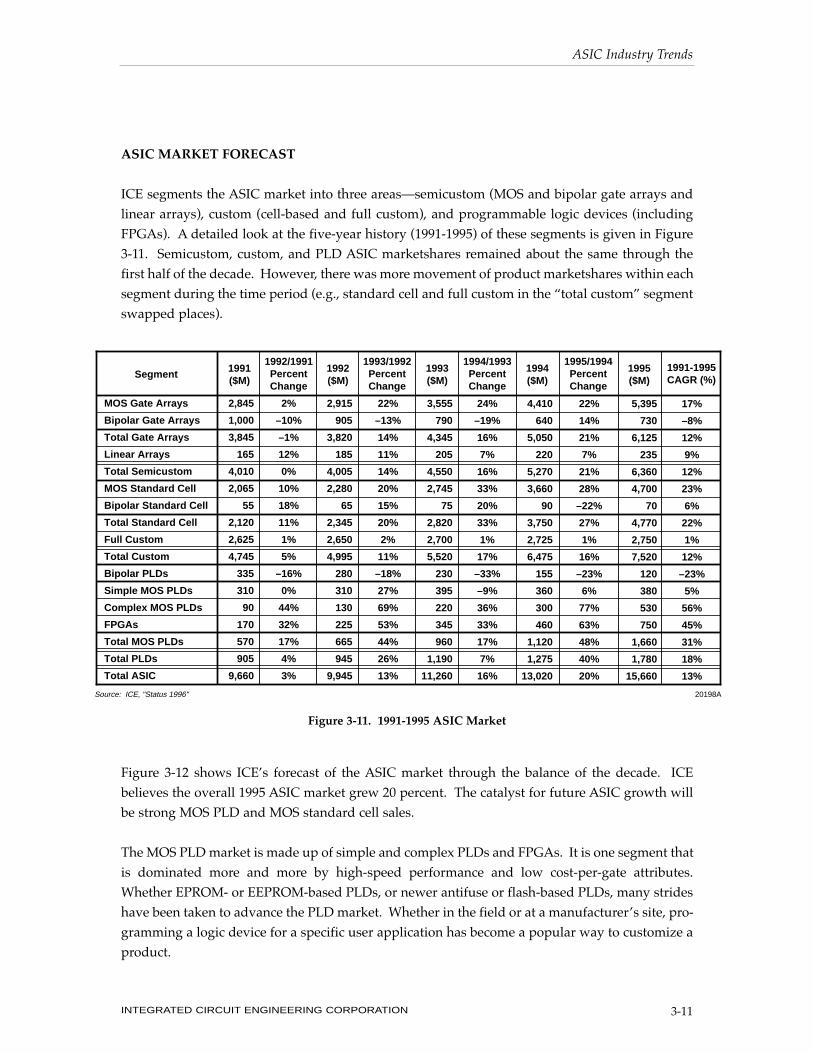

ICE segments the ASIC market into three areas—semicustom (MOS and bipolar gate arrays andlinear arrays), custom (cell-based and full custom), and programmable logic devices (includingFPGAs). A detailed look at the five-year history (1991-1995) of these segments is given in Figure3-11. Semicustom, custom, and PLD ASIC marketshares remained about the same through thefirst half of the decade. However, there was more movement of product marketshares within eachsegment during the time period (e.g., standard cell and full custom in the “total custom” segmentswapped places).

Figure 3-12 shows ICE’s forecast of the ASIC market through the balance of the decade. ICEbelieves the overall 1995 ASIC market grew 20 percent. The catalyst for future ASIC growth willbe strong MOS PLD and MOS standard cell sales.

The MOS PLD market is made up of simple and complex PLDs and FPGAs. It is one segment thatis dominated more and more by high-speed performance and low cost-per-gate attributes.Whether EPROM- or EEPROM-based PLDs, or newer antifuse or flash-based PLDs, many strideshave been taken to advance the PLD market. Whether in the field or at a manufacturer’s site, pro-gramming a logic device for a specific user application has become a popular way to customize aproduct.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-11

MOS Gate Arrays

Bipolar Gate Arrays

Total Gate Arrays

Linear Arrays

Total Semicustom

MOS Standard Cell

Bipolar Standard Cell

Total Standard Cell

Full Custom

Total Custom

Bipolar PLDs

Simple MOS PLDs

Complex MOS PLDs

FPGAs

Total MOS PLDs

Total PLDs

Total ASIC

2,845

1,000

3,845

165

4,010

2,065

55

2,120

2,625

4,745

335

310

90

170

570

905

9,660

2%

–10%

–1%

12%

0%

10%

18%

11%

1%

5%

–16%

0%

44%

32%

17%

4%

3%

2,915

905

3,820

185

4,005

2,280

65

2,345

2,650

4,995

280

310

130

225

665

945

9,945

22%

–13%

14%

11%

14%

20%

15%

20%

2%

11%

–18%

27%

69%

53%

44%

26%

13%

3,555

790

4,345

205

4,550

2,745

75

2,820

2,700

5,520

230

395

220

345

960

1,190

11,260

24%

–19%

16%

7%

16%

33%

20%

33%

1%

17%

–33%

–9%

36%

33%

17%

7%

16%

4,410

640

5,050

220

5,270

3,660

90

3,750

2,725

6,475

155

360

300

460

1,120

1,275

13,020

22%�

14%�

21%�

7%�

21%�

28%�

–22%�

27%�

1%�

16%�

–23%�

6%�

77%�

63%�

48%�

40%�

20%

5,395�

730�

6,125�

235�

6,360�

4,700�

70�

4,770�

2,750�

7,520�

120�

380�

530�

750�

1,660�

1,780�

15,660

17%�

–8%�

12%�

9%�

12%�

23%�

6%�

22%�

1%�

12%�

–23%�

5%�

56%�

45%�

31%�

18%�

13%

Segment

1991 ($M)

1992/1991 Percent Change

1992 ($M)

1993/1992 Percent Change

1993 ($M)

1994/1993 Percent Change

1994 ($M)

1995/1994 Percent Change

1995 ($M)

1991-1995 CAGR (%)

20198ASource: ICE, "Status 1996"

Figure 3-11. 1991-1995 ASIC Market

The future of the total custom segment (specifically, the standard cell market) also appears brightin ICE’s ASIC forecast. ICE anticipates the standard cell market more than doubling from an esti-mated $4.8 billion in 1995 to approximately $12.7 billion in the year 2000. In fact, ICE forecaststhat the MOS standard cell market will be the largest ASIC product category (surpassing MOSgate arrays) beginning in 1998.

With few exceptions, growth in most product areas appears promising through the year 2000.However, if the word “bipolar” is associated with a category, it spells doom. The mainstream ICmarket has moved away from bipolar-based products toward MOS-based technology. As a result,bipolar gate arrays and bipolar PLDs are forecast to be the poorest performing of all ASIC seg-ments.

Despite the ASIC market forecast calling for sustained growth, the ASIC market will representonly nine percent of the total worldwide IC market in the year 2000. This will be down from 12percent of the IC market in 1995 and 21 percent of the IC market in 1991.

Perhaps a better way of determining the performance of the ASIC market is to view cumulativeannual growth rates (CAGRs, Figure 3-13). Here, the “hot” markets such as complex PLDs,FPGAs, MOS standard cells, and MOS gate arrays are exposed. At the same time, the demise ofbipolar ASICs is evident as well. The total ASIC market is forecast to grow at a healthy 15 percentCAGR through the end of the decade, with four categories equaling or bettering that performanceand six categories not growing at the same rate as the overall market.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-12

MOS Gate Arrays

Bipolar Gate Arrays

Total Gate Arrays

Linear Arrays

Total Semicustom

MOS Standard Cell

Bipolar Standard Cell

Total Standard Cell

Full Custom

Total Custom

Bipolar PLDs

Simple MOS PLDs

Complex MOS PLDs

FPGAs

Total MOS PLDs

Total PLDs

Total ASIC

Segment

6,200�

600�

6,800�

240�

7,040�

5,700�

75�

5,775�

2,800�

8,575�

90�

360�

675�

905�

1,940�

2,030�

17,645

13%�

–25%�

10%�

2%�

9%�

17%�

7%�

17%�

2%�

12%�

–22%�

–3%�

23%�

19%�

16%�

15%�

11%

1996 ($M)

15%�

–18%�

11%�

2%�

11%�

21%�

7%�

21%�

2%�

14%�

–25%�

–5%�

27%�

21%�

17%�

14%�

13%

1996/1995 Percent Change

1997/1996 Percent Change

1997 ($M)

7,000�

450�

7,450�

245�

7,695�

6,650�

80�

6,730�

2,850�

9,580�

70�

350�

830�

1,075�

2,255�

2,325�

19,600

1998/1997 Percent Change

15%�

–24%�

13%�

4%�

12%�

23%�

6%�

23%�

2%�

17%�

–14%�

–4%�

28%�

27%�

22%�

21%�

15%

1998 ($M)

8,050�

340�

8,390�

255�

8,645�

8,180�

85�

8,265�

2,900�

11,165�

60�

335�

1,060�

1,365�

2,760�

2,820�

22,630

1999/1998 Percent Change

17%�

–26%�

15%�

4%�

15%�

23%

6%�

23%�

2%�

17%�

–17%�

–4%�

29%�

28%�

24%�

24%�

17%

1999 ($M)

9,400�

250�

9,650�

265�

9,915�

10,050�

90�

10,140�

2,950�

13,090�

50�

320�

1,365�

1,750�

3,435�

3,485�

26,490

2000/1999 Percent Change

18%�

–26%�

17%�

4%�

17%�

25%�

11%�

25%�

2%�

20%�

–20%�

–6%�

30%�

30%�

27%�

26%�

19%

2000 ($M)

11,100�

185�

11,285�

275�

11,560�

12,550�

100�

12,650�

3,000�

15,650�

40�

300�

1,775�

2,275�

4,350�

4,390�

31,600

1991-2000 CAGR (%)

16%�

–17%�

13%�

6%�

12%�

22%�

7%�

22%�

1%�

14%�

–21%�

0%�

39%�

33%�

25%�

19%�

14%

1995-2000 CAGR (%)

16%�

–24%�

13%�

3%�

13%�

22%�

7%�

22%�

2%�

16%�

–20%�

–5%�

27%�

25%�

21%�

20%�

15%

20199ASource: ICE, "Status 1996"

Figure 3-12. 1996-2000 ASIC Market Forecast

At one time (1986) full custom products accounted for more than half of ASIC marketshare. Now,though this segment is growing ever so slightly in terms of dollars, it is being replaced by devicessuch as standard cells. Full custom ASICs are forecast to represent only nine percent of total ASICproduct marketshare in the year 2000 (Figure 3-14). Supercomputer manufacturers and the mili-tary are the best examples of full custom users. Since overall military spending is down and withsupercomputer power in desktop systems, it stands to reason that there will be less demand forfull custom devices. Meanwhile, standard cell devices, which held 31 percent ASIC marketsharein 1995, are forecast to account for 40 percent in the year 2000.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-13

Product1991-2000 CAGR (%)

1991-1995 CAGR (%)

1995-2000 CAGR (%)

Complex PLDs

FPGAs

MOS Standard Cell

MOS Gate Arrays

Total ASIC

Bipolar Standard Cell

Linear Arrays

Full Custom

Simple PLDs

Bipolar PLDs

Bipolar Gate Arrays

39�

33�

22�

16�

14�

7�

6�

1�

—�

–21�

–17

56�

45�

23�

17�

13�

6�

9�

1�

5�

–23�

–8

27�

25�

22�

16�

15�

7�

3�

2�

–5�

–20�

–24

20195ASource: ICE, "Status 1996"

Figure 3-13. ASIC Product CAGRs

Gate and Linear Arrays

30%

Standard Cell 11%

Full Custom 52%

PLDs 7%

Gate and Linear Arrays

41%

Standard Cell 31%

Full Custom 17%

PLDs* 11%

Gate and Linear Arrays 37%

Standard Cell 40%

Full Custom 9%

PLDs* 14%

1986 $4.7B

1995 $15.7B

2000 $31.6B

16278J

*FPGAs 5% in 1995, 7% in 2000.Source: ICE, "Status 1996"

Figure 3-14. ASIC Product Marketshare

As touched upon earlier, the market forecast for MOS standard cell and gate array devices appearspromising, but other older technologies are forecast to continue their trek toward obsolescence. InFigure 3-15, forecasts for several logic technologies are shown—and most are in a steady decline.The graphs point out that most designers (and users) have made the switch to MOS technologiesto achieve the desired effects of their ASIC devices. Of the non-MOS segments, only TTL/OtherLogic still shows some signs of life. This mainstream technology of a few years ago was used innumerous applications and remained a rather large market even in 1995. Due to its sheer size andrelatively widespread use, this market segment will be the slowest to decline.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-14

0

500

1000

1500

2000

19951994199319921991

YearTTL/Other Standard Logic Market

Mill

ion

s o

f D

olla

rs

0

200

400

600

800

1000

19951994199319921991

1,000

905

YearBipolar Gate Array Market

Mill

ion

s o

f D

olla

rs

0

100

200

300

400

19951994199319921991

335

280

230

155120

–16%

–18%

–23%

–33%

YearBipolar PLD Market

Mill

ion

s o

f D

olla

rs

0

1,000

2,000

3,000

4,000

5,000

19951994199319921991

2,0652,280

2,745

3,660

4,700

10%20%

33%

28%

YearMOS* Standard Cell Market

Mill

ion

s o

f D

olla

rs

0

1000

2000

3000

4000

5000

6000

19951994199319921991

2,845 2,915

3,555

4,410

5,395

2% 22%

24%

22%

YearMOS* Gate Array Market

Mill

ion

s o

f D

olla

rs

0

100

200

300

400

500

19951994199319921991

500

390

315

150

200

–22%

–19%

–36%

–25%

YearNMOS Logic Market

Mill

ion

s o

f D

olla

rs

18928DSource: ICE, "Status 1996"

*Includes BiCMOS and GaAs

1,505 1,455

1,7301,630 1,620

–3% 19%

–6%–1%

(EST) (EST)

(EST)(EST)

(EST) (EST)

790

640730

–10%

–13%

–19% 14%

Figure 3-15. Selected 1991-1995 Logic Markets

Quarterly market size for each of the four main ASIC products is shown in the next several charts.In Figure 3-16, the MOS gate array market is shown as a gradually upward sloping curve. Recenthistory shows this market performing best during the second and third quarters of each year.

The MOS standard cell market is shown on a quarterly basis in Figure 3-17. Much more dramat-ic growth characterized this segment during the past few years. Besides being used in more wide-spread applications, the sizable market increase for standard cells might be explained in the factthat many companies re-classified their full custom devices as standard cell products in 1994 and1995.

Figure 3-18 portrays the rise in quarterly MOS PLD sales dating back to 1989. For the time peri-od shown, this market steadily increased. At least it did so until severe pricing pressures kept themarket size flat from 3Q93 through 2Q94. New product offerings from several suppliers helpedrevive the MOS PLD market in late 1994 and throughout 1995.

Meanwhile, the theme for bipolar ASIC devices—in this case, for bipolar PLDs—is repeated inFigure 3-19. Since 1989, the bipolar PLD market has dropped steeply. This market shows a ten-dency to rebound slightly every once in a while, but overall, the trend is still down.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-15

1989 1990 1991 1992

Do

llars

(M

illio

ns)

Year17778JSource: WSTS/ICE, "Status 1996"

1993

1994

1995

400

500

600

700

800

900

1,000

1,100

1,200

1,300

4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q(EST)

Figure 3-16. Quarterly MOS Gate Array Market (1989-1995)

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-16

250

350

450

550

650

750

850

950

4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q

1992 1993 1994 1995

YearSource: WSTS/ICE, "Status 1996" 18930E

Do

llars

(M

illio

ns)

(EST)

Figure 3-17. Quarterly MOS Standard Cell Market (1992-1995)

0

50

100

150

200

250

300

350

400

450

500

4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q

1993 1994 19951992199119901989

Source: WSTS/ICE, "Status 1996" 18929E

Do

llars

(M

illio

ns)

Year

(EST)

Figure 3-18. Quarterly MOS PLD Market (1989-1995)

TOP TEN ASIC VENDOR SALES

Before listing any ASIC vendor sales, it should be noted that the ICE ASIC sales estimates do notinclude standard products designed from standard cell libraries or with silicon compilers. Onlygate and linear arrays, full custom, and standard cell devices not listed in a catalog, as well asPLDs, are considered ASICs.

Figure 3-20 provides a list of the top 10 ASIC (not including full custom) suppliers for 1995. Withtotal ASIC sales of $1.27 billion, NEC held on to the top spot on the leading ASIC supplier list in1995. NEC posted strong gate and linear array sales, but also made an effort to strengthen its stan-dard cell sales as well. In doing so, it captured just under 10 percent of the total ASIC market.

ICE estimates that LSI Logic moved ahead of Fujitsu into the number two spot in the 1995 ASICranking. LSI Logic’s standard cell ASIC sales have increased from $105 million in 1993 to an esti-mated $555 million in 1995. It would not be surprising to see LSI Logic overtake NEC as theworldwide leading ASIC vendor in 1996!

A newcomer to the top ten ASIC ranking in 1995 is Xilinx*, the longtime leader in the FPGA mar-ketplace. ICE believes that Xilinx has a chance of passing Hitachi in ASIC sales in 1996.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-17

1989 1990 1991 1992Year

17777K

Do

llars

(M

illio

ns)

Source: WSTS/ICE, "Status 1996"

1993 1994 1995

20

30

40

50

60

70

80

90

100

110

120

130

4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q(EST)

Figure 3-19. Quarterly Bipolar PLD Market (1989-1995)

* Longtime ASIC top ten vendor VLSI Technology slipped out of the top ten ranking in 1995 with $440 million in ASICsales.

Also in the top 10 list is Symbios Logic, Inc. Symbios is the former NCR facility in Colorado thatwas purchased (and renamed) by Hyundai. In purchasing the NCR ASIC business, Symbios(Hyundai) became an immediate contender in the worldwide ASIC market.

GATE AND LINEAR ARRAY SUPPLIERS

Displayed in Figure 3-21 are the top gate array manufacturers and their sales for 1994 and 1995.Four companies, Fujitsu, NEC, Toshiba, and LSI Logic, accounted for about 50 percent of all gatearray sales in 1995. The top ten gate array suppliers accounted for 80 percent of sales. In the caseof the top four players, each has been a steady player in the gate array business for many years.A new entry into the top ten gate array ranking in 1995 was IBM. The figures listed for IBM areonly its merchant sales and do not include internal transfers.

At the number six position in 1995 was TI. It reported an increase in gate array sales of 46 percentduring the year. This large increase was partly due to it providing customizable DSP devices. TIwill build a device that features its DSP core surrounded by gate array technology. While this canbe labeled as either a DSP or an ASIC, ICE classifies the product as an ASIC device.

Of the 35 companies listed in the gate array supplier chart, eight posted flat or declining revenuein 1995. Some, such as Raytheon were phasing out of the bipolar gate array business. Meanwhile,Siemens was phasing out of the MOS gate array market.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-18

*Not including full custom **Includes FPGA Sales

NEC

LSI Logic

Fujitsu

Toshiba

TI

AT&T

Hitachi

Xilinx

Motorola

Symbios

Top Ten Total

Other Suppliers

Total Market

Top Ten Marketshare

CompanyPercent Of Total ASIC

Market

Gate And Linear Array Sales ($M)

Standard Cell Sales

($M)

PLD** Sales ($M)

925�

615�

940�

635�

490�

94�

500�

—�

355�

35�

4,589�

1,771�

6,360�

73%

340�

555�

225�

235�

315�

655�

75�

—�

125�

410�

2,935�

1,835�

4,770�

61%

—

—

—

—�

38�

82�

—�

530�

10�

—�

660�

1,120�

1,780�

37%

10%�

9%�

9%�

7%�

7%�

6%�

4%�

4%�

4%�

3%�

63%�

37%�

100%�

63%

20194ASource: ICE, "Status 1996"

Total ASIC Sales

($M)

1,265�

1,170�

1,165�

870�

843�

831�

575�

530�

490�

445�

8,184�

4,726�

12,910�

63%

1

2

3

4

5

6

7

8

9

10

1995 Rank

Figure 3-20. 1995 Top Ten ASIC Leaders

Gate arrays have found their way into more small, electronic sets with advanced functions. Speedand low power, two of the most preferred performance characteristics in ICs, are especiallydesired in gate arrays. Manufacturers have been quick to respond to these needs while addingdensity as well. Typically, 0.8-micron technology is used to manufacture the majority of gatearrays. However, companies have pushed the process technology envelope to 0.5 micron andsmaller for the more-than-one-million-gate gate arrays that have been built in limited quantities.Some research prototype gate arrays have been built using 0.2-micron technology.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-19

1995 Rank

Company1994 Sales ($M) 1995 Sales ($M, EST)

MOS Bipolar Total MOS Bipolar Total

1995/1994 Percent Change

1995 Percent

Marketshare

1 2 3 4 5 6 7 8 9

10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35

Fujitsu NEC Toshiba LSI Logic Hitachi TI Motorola IBM Mitsubishi Samsung VLSI Technology GEC Plessey S-MOS/Seiko Oki SGS-Thomson AMI AT&T Matsushita National ROHM AMCC Symbios Sanyo Sharp Atmel Siemens* Vitesse** Orbit MHS Ricoh Sony*** Chip Express Kawasaki Steel LG Semicon Raytheon*** Others Total

550�685�525�575�305�335�182�

80 139�

90�108�

93�75�78�80�38�50�44�39�36�12�32�28�30

6�5�

25�12�22�19�15�10�10�10� —�67�

4,410

250�50�— —

115�—

125�— — — —�8

— — — — 10�— — — 28 — — — —�25 — — —�— 5�

— — — 15�

9�640

800�735�525�575�420�335�307�

80 139�

90�108�101�

75�78�80�38�60�44�39�36�40�32�28�30

6�30�25�12�22�19�20�10�10�10�15�76�

5,050

645�830�635�615�360�490�200�160 155�155�130�121�105�

87�83�61�50�53�42�40�14�35�31�30 30�

3�27�27�26�21�20�20�15�10�—�69�

5,395

295�65�—�—�

140�—�

155�— — — — — — — — — 10 — — — 25 — — — — 25�— — — — — — — — 5�

10�730

940�895�635�615�500�490�355�160�155 155�130�121�105�

87�83�61�

60�53�42�40�39�35�31�30 30�28�27�27�26�21�20�20�15�10�

5�79�

6,125

18�22�21�

7�19�46�16�

100�12�72�20�20�40�12�

4�61�—�20�

8�11�–3�

9�11�—

400�–7�

8�125�

18�11�—�

100�50�—�

–67�4�

21

15.3�14.6�10.4�10.0�

8.2�8.0�5.8�2.6�2.5�2.5�2.1�2.0�1.7�1.4�1.4�1.0�1.0�0.9�0.7�0.7�0.6�0.6�0.5�0.5 0.5�0.5�0.4�0.4�0.4�0.3�0.3�0.3�0.2�0.2�0.1�1.2�

100.0

13636P

*Phasing out CMOS gate arrays **GaAs ***Phasing out bipolar gate arraysSource: ICE, "Status 1996"

Figure 3-21. Merchant Gate Array Leaders

It seems gate array implementation has grown as the average number of gates per device hasincreased. As recently as five years ago, average gate array density was in the 10,000-gate range.In 1995, ICE estimates that 90 percent of all gate arrays were shipped with greater than 10,000gates. More specifically, ICE believes that 40 percent of gate arrays were shipped with between20,000 and 50,000 gates in 1995 (Figure 3-22). By the year 2000, ICE anticipates the majority of gatearrays will have an average usable gate count closer to 100,000 gates.

Placing large numbers of gates on a gate array has not been an insurmountable hurdle. Manycompanies have developed gate arrays with over one million available gates. At these densities,it becomes increasingly possible to incorporate large-scale circuitry in a single chip. Circuit den-sity and manufacturing have brought gate arrays to a higher level of acceptance and integration.The biggest challenges facing designers of these “mega” gate arrays are test and packaging issues.

The gate array market by region is shown in Figure 3-23. In 1995, the increased value of the yenhelped Japan become the largest market for gate arrays. Japan had a 35 percent share of the MOSgate array market in 1994 (estimated at 40 percent in 1995), while the North American market was39 percent in 1994 (estimated at 36 percent in 1995).

In the year 2000, ICE expects the North American and Japanese markets to remain the largest forgate array products. Pacific Rim countries, excluding Japan but including Korea, Taiwan, and oth-ers, will garner an increasing percentage of marketshare.

The trend toward MOS technology (CMOS and BiCMOS) will continue in the gate array market(Figure 3-24). In some cases, designers and manufacturers will take advantage of the low powerconsumption and high speed characteristics of BiCMOS technology in the coming five years.However, CMOS technology continues to be refined to the point where it can perform at a levelapproaching BiCMOS. Therefore, it will continue to expand as the preferred technology whenbuilding gate arrays.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-20

≤10K Gates 10% 10K - 20K

Gates 30%

20K - 50K Gates 40%

>50K Gates 20% 1995

$5.4B

18931DSource: ICE, "Status 1996"

Figure 3-22. 1995 MOS Gate Array Market by Gate Count (Usable)

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-21

Europe 14%

Japan 43%

North America

34%

ROW 9%

1995

Total Market = $6.1B

Europe 15%

Japan 39%

North America

34%

ROW 12%

2000

Total Market = $11.3B

8881XSource: ICE, "Status 1996"

Europe 14%

Japan 40%

North America

36%

ROW 10%

1995

Europe 15%

Japan 38%

North America

35%

ROW 12%

2000

Europe 10%

Japan 65%

North America

23%

ROW 2%

1995

Europe 9%

Japan 72%

North America

18%

ROW 1%

2000

Total MOS Market = $5.4B Total MOS Market = $11.1B

Total Bipolar Market = $730M Total Bipolar Market = $185M

Figure 3-23. Worldwide Digital Gate Array Market by Region

Figure 3-24. Digital Gate Array Market by Process Technology

BiCMOS 8%

CMOS* 80%

Bipolar 12%

1995

BiCMOS 9%

CMOS 87%

Bipolar 2%

2000

GaAs 2%

Total Market = $6.1B Total Market = $11.3B

8870ZSource: ICE, "Status 1996"

*Includes GaAs

In contrast, bipolar’s share of the gate array market is forecast to slide from 12 percent in 1995 totwo percent in the year 2000. This steep drop is due to the slumping military IC market as wellas the replacement of ECL arrays in large-scale computing systems with GaAs, BiCMOS, andCMOS ICs.

The worldwide gate array market by end use is segmented in five categories and shown in Figure3-25. Data processing applications are where most gate arrays were destined in 1995. By the year2000, the picture will not change much. Data processing and telecom applications will expandslightly, while other applications decline. The military segment will be a smaller player despitethe fact the Defense Department is very encouraged about further incorporating gate arrays intoits systems.

Linear arrays put the functions of several analog ICs and discrete products onto a single chip.Most linear arrays consist of bipolar transistors and resistors, but can also include capacitors, junc-tion field-effect transistors, and Schottky diodes.

Linear arrays have had a difficult time gaining significant market acceptance. One reason for thisis design difficulties. Other concerns include noise isolation, isolating the substrate, interfacingthe chip with external circuitry, and keeping NRE costs and schedules short. Also, the lack of stan-dardized test methods has traditionally been a stumbling block for linear ASICs.

The leading linear array manufacturers and their sales are provided in Figure 3-26. For the sec-ond straight year sales of linear arrays increased only seven percent. The “other” categoryshowed a steep decline due to Micro Linear and Raytheon phasing out their analog array busi-nesses.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-22

Data Processing

55%

1995

Telecom 19%

Industrial 13%

Consumer 10%

Military 3%

2000 Industrial 11%

Telecom 21%

Consumer 9%

Military 1%

Data Processing

58%

Total Market = $11.3B9933TSource: ICE, "Status 1996"

Total Market = $6.1B

Figure 3-25. Gate Array Market by Application

STANDARD CELL SUPPLIERS

Leading standard cell ASIC manufacturers and their 1994 and 1995 sales numbers are shown inFigure 3-27. AT&T and LSI Logic were the only companies that posted more than 10 percent mar-ketshare in 1995. It should be noted that, being a former “captive” supplier, AT&T did a lot ofinternal business. The internal business represented approximately 30 percent of its total standardcell sales in 1995.

LSI Logic moved from sixth place in 1994 to second place in 1995! Given LSI’s recent standard cellsales surge, it is likely to capture the number one ranking in 1996.

Similar to the gate array ranking, IBM’s standard cell figures only include its merchant sales. ICEexpects that IBM will break into the top ten standard cell sales ranking in 1997.

Five companies among the 38 listed increased sales by triple-digit amounts in 1995. Among themwas LSI Logic, which saw its standard cell business increase 124 percent. LSI Logic took severalsteps to improve its product line, including its first move into the mixed-signal arena. Its firstmixed-signal standard cells focus on data-conversion cells, but will be expanded over time toinclude a wide range of functions. LSI claims an advantage in the mixed-signal market because itmanufactures its devices using a digital CMOS process designed to keep costs down.

Motorola increased its cell-based ASIC sales 116 percent in 1995, mostly by using its FlexCore pro-gram to grow its standard cell business. FlexCore combines a standard product with functionsdesired by a user to create a quasi-application-specific chip. FlexCore takes Motorola’s 68000-fam-

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-23

Company1993 Sales ($M)

Maxim

SGS-Thomson

AT&T

NEC

GEC Plessey

Ricoh

Universal

Gennum

Exar

Cherry

Others

Total

32�

30�

22�

20�

22�

12�

11�

7�

8�

7�

34�

205

13649QSource: ICE, "Status 1996"

1994 Sales ($M)

38�

35�

26�

25�

18�

15�

12�

10�

9�

8�

24�

220

1995 Sales

($M, EST)

42�

38�

34�

30�

20�

17�

13�

12�

10�

9�

10�

235

1995/1994 Percent Change

11�

9�

31�

20�

11�

13�

8�

20�

11�

13�

–58�

7

1995�Percent

Marketshare

18�

16�

14�

13�

9

7�

6�

5�

4�

4�

4�

100

1995 Rank

1

2

3

4

5

6

7

8

9

10

—

—

Figure 3-26. Linear Array Leaders

ily core processor and allows a designer to integrate desired features such as up to 100,000 gatesof custom logic, memory, and peripheral modules. It is a feature that is very attractive and verywell understood by the design community. Customers get what looks like an ASIC device, butuses industry-standard third-party design tools. The bottom line for Motorola was a very nicegain in standard cell sales.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-24

1995 Rank

Company1994 Sales ($M) 1995 Sales ($M, EST)

MOS Bipolar Total MOS Bipolar Total

1995/1994 Percent Change

1995 Percent

Marketshare

1 2 3 4 5 6 7 8 9

10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38

AT&T LSI Logic Symbios NEC TI VLSI Technology Toshiba Fujitsu Alcatel Mietec Motorola SGS-Thomson IBM Matsushita AMS Exar GEC Plessey Harris Hitachi Sharp National ES2 Ricoh Atmel LG Semicon Mitsubishi S-MOS/Seiko Dialog MHS Triquint* Samsung Hughes Sanyo AMI Oki Siemens** Kawasaki Steel Elex ABB Hafo Others Total

600�248�322�260�345�262�173�180�159�

58 64�40�68�75�74�75�60�30�50�58�36�40 —�18�31�31�27�22�20�15�20�20�17�15�20�10 11

9�97�

3,660

— — — — — — — 5

— — — — — — — 65�15 — — — — — — — — — — — — — — — — — — — — — 5

90

600�248�322�260�345�262�173�185�159�

58 64�40�68�75�74�

140�75�30�50�58�36�40 —�18�31�31�27�22�20�15�20�20�17�15�20�10 11

9�102�

3,750

655�555�410�340�315�310�235�220�166�125 100�100�

98�97�95�45�54�75�55�50�48�45 45�40�35�35�33�26�25�25�24�24�23�20�15�15 14 11�97�

4,700

— — — — — — —�5

— — — — —�— — 35�26 — — — — — — — — —�— — — — — — — — — — — — 4�

70

655�555�410�

340�315�310�235�225�166�125 100�100�

98�97�95�80�80�75�55�50�48�45 45�40�35�35�33�26�25�25�24�24�23�20�15�15 14 11�

101�4,770

9�124�

27�31�–9�18�36�22�

4�116

56�150�

44�29�28�

–43�7�

150�10�

–14�33�13

N/A�122�

13�13�22�18�25�67�20�20�35�33�

–25�50 27 22�–1�27

13.7�11.6�

8.6�7.1�6.6�6.5�4.9�4.7�3.5�2.6 2.1�2.1�2.1�2.0�2.0�1.7�1.7�1.6�1.2�1.0�1.0�0.9 0.9�0.8�0.7�0.7�0.7�0.5�0.5�0.5�0.5�0.5�0.5�0.5�0.4�0.3 0.3 0.2�2.1�

100.0�

13638N

*GaAs **Phasing out of standard cell businessSource: ICE, "Status 1996"

Figure 3-27. Standard Cell IC Leaders

In the number three position was Symbios Logic, Inc. (formerly NCR). It increased its standardcell business 27 percent in 1995. It continued to emphasize its cell-based library—one that is 0.5micron and based on a 3V optimized, triple-level metal, CMOS process providing functionalitythat is 20 percent faster and consumes 50 percent less power than the company’s previous best-performing standard cell family.

Overall, the standard cell market grew 27 percent in 1995 and is forecast to continue to grow at astrong pace through the balance of the decade.

As shown in Figure 3-28, CMOS standard cells dominated the market in 1995 and are forecast todo so again in the year 2000. As in the gate array market, there will likely be marginal increasesin the use of BiCMOS technology. Even GaAs technology may see a small increase in use through-out the industry. However, CMOS devices will dominate.

The worldwide standard cell market by geographic sector is displayed in Figure 3-29. In 1994,Japan’s share of the standard cell market was 35 percent; 34 percent in North America. In 1995,Japan’s share grew, while it slipped for North America. There is no denying that Japanese firmsperformed well in the 1995 standard cell market, but some of the 1995 growth in the Japanese mar-ket is attributable to the rise in the value of the yen. Continuing through the year 2000, the ROWregion will gain additional marketshare, at the expense of the Japanese region.

The 1995 and 2000 standard cell markets by application are provided in Figure 3-30. Much likethe gate array market, data processing and telecom will continue to be the leading consuming seg-ments for standard cell devices through the year 2000. Marginal expansion is forecast for the con-sumer/auto sector. Automobiles are incorporating ever-increasing electronic sophistication intotheir systems and standard cells will be a big part of that business. Meanwhile, the industrial andmilitary segments will decline to account for slightly more than three percent by the year 2000.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-25

CMOS 93%

BiCMOS 4%Bipolar

2%

1995

CMOS 91%

BiCMOS 6%

Bipolar <1%GaAs

2%

GaAs 1%

Total Market $12.7BTotal Market $4.8B12907PSource: ICE, "Status 1996"

2000

Figure 3-28. Standard Cell Market by Process Technology

Within the standard cell segment is the mixed-mode (or mixed-signal) cell-based market. Figure3-31 lists the top mixed-mode standard cell suppliers and their sales for 1994 and 1995.

Rising performance and increasing integration has opened up new avenues for mixed-signalASICs. Accordingly, the number of companies involved in the mixed-signal market keeps grow-ing. The mixed-signal market used to be the playground of the small or mid-size company. In1993, Alcatel Mietec was the leading mixed-signal supplier. More recently, some large firms haveseen the value of being a part of this market and have moved in. AT&T (the largest supplier in1995), Symbios, TI, and SGS-Thomson are four large corporations that saw their mixed-mode salesincrease nicely in 1995. Overall, the mixed-signal market grew 22 percent in 1995.

The mixed-mode standard cell market forecast is shown in Figure 3-32. ICE estimates that mixed-mode devices accounted for 26 percent of the $4.8 billion standard cell market in 1995. By the year2000, mixed-mode devices are forecast to increase to 30 percent of the $12.7 billion standard cellmarket. That amounts to a 26 percent cumulative annual growth rate over the five-year period.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-26

Japan 38%

Europe 24%

North America

30%

ROW 8%

1995

Japan 35%

Europe 24%

North America

30%

ROW 11%

2000

Total Market = $4.8B Total Market = $12.7B10403VSource: ICE, "Status 1996"

Figure 3-29. Worldwide Standard Cell Market by Region

Telecom 30%Data

Processing 51%

1995

Military 1%

Consumer/Auto 14%

Industrial 4%

Telecom 33%Data

Processing 48%

2000

Military <1%

Consumer/Auto 16%

Industrial 3%

12906NSource: ICE, "Status 1996"Total Market = $12.7BTotal Market = $4.8B

Figure 3-30. Standard Cell Market by Application

PLD SUPPLIERS

The top players in the PLD market and their sales for 1994 and 1995 are shown in Figure 3-33. Thenumbers displayed do not include software and development system sales. This list is dominat-ed by North American companies (nine of the top ten). In fact, the nine U.S. suppliers shown inthe list accounted for 95 percent of the 1995 PLD market. There are several small-to-medium sizecompanies that vigorously compete for PLD marketshare. Firms such as Xilinx (which, with anaggressive strategy, took over the leading position in 1994), Altera, Lattice, and Actel have allfound a particular niche in the marketplace.

Lively competition in the PLD market led to at least three “marginal” players announcing theirintentions to exit the PLD market in 1994 and 1995. National started by proclaiming that itstopped taking new orders for programmable logic. Next, Intel announced that it sold its pro-grammable logic business to Altera for $50 million in cash and stock. Lastly, Actel declared thatit purchased the FPGA business of its second-source partner, Texas Instruments.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-27

Company1993 Sales ($M)

AT&T

Alcatel Mietec

Symbios

TI

GEC Plessey

AMS

Exar

SGS-Thomson

Harris

NEC

Others

Total

96�

116�

70�

70�

88�

46�

19�

18�

26�

10�

211�

770

20400Source: ICE, "Status 1996"

1994 Sales ($M)

138�

130�

90�

86�

120�

58�

48�

30�

36�

25�

249�

1,010

1995 Total Standard

Cell

655�

166�

410�

315�

80�

97�

95�

100�

80�

340�

2,432�

4,770

Mixed-Signal Percent of Total

26�

78�

30�

37�

94�

76�

76�

50�

60�

13�

13�

26

1995 Sales

($M, EST)

170�

130�

125�

115�

75�

74�

72�

50�

48�

45�

326�

1,230

1995/1994 Percent Change

23�

—�

39�

34�

–38�

28�

50�

67�

33�

80�

31�

22

1995�Percent

Marketshare

14�

11�

10�

9�

6�

6�

6�

4�

4�

4�

27�

100

1995 Rank

1

2

3

4

5

6

7

8

9

10

—

—

Figure 3-31. Mixed-Signal Standard Cell Leaders

15431LSource: ICE, "Status 1996"

Digital 74%

Mixed-Mode 26%

1995 $4.8B

2000 $12.7B

Digital 70%

Mixed-Mode 30%

Figure 3-32. Mixed-Mode Standard Cell Market Forecast

The competition never sleeps in the PLD market. During 1994 and 1995, suppliers continued tobattle for increased marketshare by adding special features or making devices faster or more com-plex. The result was a steep decline in prices. For example, in 2Q95, Cypress Semiconductorannounced price reductions of as much as 40 percent on many of its CPLDs and FPGAs. Cypresshas an advantage over many other PLD suppliers in that it owns several wafer fabs. Therefore, ithas the flexibility to adjust manufacturing schedules to meet PLD demand and with high-volumeruns is often able to charge less than other vendors.

Falling prices (20-25 percent in 1994) resulted in slow PLD market growth in 1994. The PLD mar-ket increased just seven percent to $1.275 billion in 1994 but recovered with a 40 percent increasein 1995. The forecast through the end of the decade calls for greater market expansion. As shownearlier in this section, the overall PLD market is forecast to have a cumulative annual growth rateof 20 percent from 1995 through the year 2000. Complex PLDs and FPGAs will contribute themost to the expected growth.

One the major benefits driving PLD usage continues to be the time-to-market factor. Of three prof-itability factors (including excessive production costs and development cost overrun), time-to-market is oftentimes the most critical in an electronics industry where market windows seem tobe continually shrinking.

PLD marketshare for 1995 is displayed in Figure 3-34. AMD, which held a 46 percent PLD mar-ketshare in 1988, secured only 18 percent in 1995. Its PLD market grip loosened quickly becauseof aggressive competition from some of the “younger” suppliers mentioned previously. In addi-

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-28

1995 ($M, EST)1994 ($M)

305�

181�

270�

120�

68�

43�

64�

83�

16

21�

104�

1,275

530�

355�

242�

165�

100�

82�

81�

5�

30

10�

60�

1,660

Xilinx

Altera*

AMD

Lattice

Actel

AT&T

Cypress

TI

Atmel

Philips

Others**

Total

305�

181�

178�

120�

68�

43�

64�

40�

16

3�

102�

1,120

—

—

73

—

—�

—

—

33�

—

13

1�

120

530�

355�

315�

165�

100�

82�

81�

38�

30

23�

61�

1,780

COMPANYMOS TOTAL BIPOLARBIPOLAR MOS TOTAL

13601P

—�

—

92

—

—�

—

—

43�

—

18

2

155

Source: ICE, "Status 1996"

1995/1994 PERCENT CHANGE

74�

96�

17�

38�

47�

91�

27�

–54�

88

10�

–41�

40

1995 PERCENT

MARKETSHARE

30�

20�

18�

9�

6�

5�

4�

2�

2

1�

3

100

1995 RANK

1

2

3

4

5

6

7

8

9

10

1Does not include software and development system sales. *Purchased Intel's PLD business in 1994. **National is phasing out both MOS and bipolar PLDs by the end of 1995.

Figure 3-33. PLD Sales Leaders1

tion, up until around 1990, AMD emphasized bipolar PLDs. In fact, 1993 was the first year AMDproduced a greater percentage of CMOS PLDs than bipolar PLDs (AMD is still the leading bipo-lar PLD supplier). AMD now vigorously pursues CMOS technology.

Figure 3-35 shows the 1994 and 1995FPGA sales leaders. Xilinx stillholds a commanding 70 percentshare of the FPGA market.However, companies like Actel,AT&T, IBM, and Motorola all havebig plans to take larger percentagesof the future FPGA market.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-29

AMD 18%

AT&T 4%

Altera 20%

Lattice 9%

Xilinx 30%

Cypress 5%

Other 8%

$1,720M

Altera 21%

Lattice 10%

Xilinx 32%

Cypress 5%

AMD 15%

Other 6%

$1,660M

BIPOLARCMOS

TOTAL PLD MARKET

13602PSource: ICE, "Status 1996"

Actel 6%

Actel 6%

AT&T 5%

AMD 61%

TI 28%

Philips 11%

National <1%

$120M

Figure 3-34. 1995 PLD Marketshare

Company

Xilinx

Actel*

AT&T

Cypress

Others

Total

20401Source: ICE, "Status 1996"

1994 Sales ($M)

300�

68�

43�

2�

47�

460

1995 Sales

($M, EST)

525�

100�

75�

13�

37�

750

1995/1994 Percent Change

75�

47�

74�

550�

–22�

63

1995�Percent

Marketshare

70�

13�

10�

2�

5�

100

1995 Rank

1

2

3

4

—

—

*Purchased TI's antifuse FPGA business in 1995.

Figure 3-35. Leading FPGA Suppliers

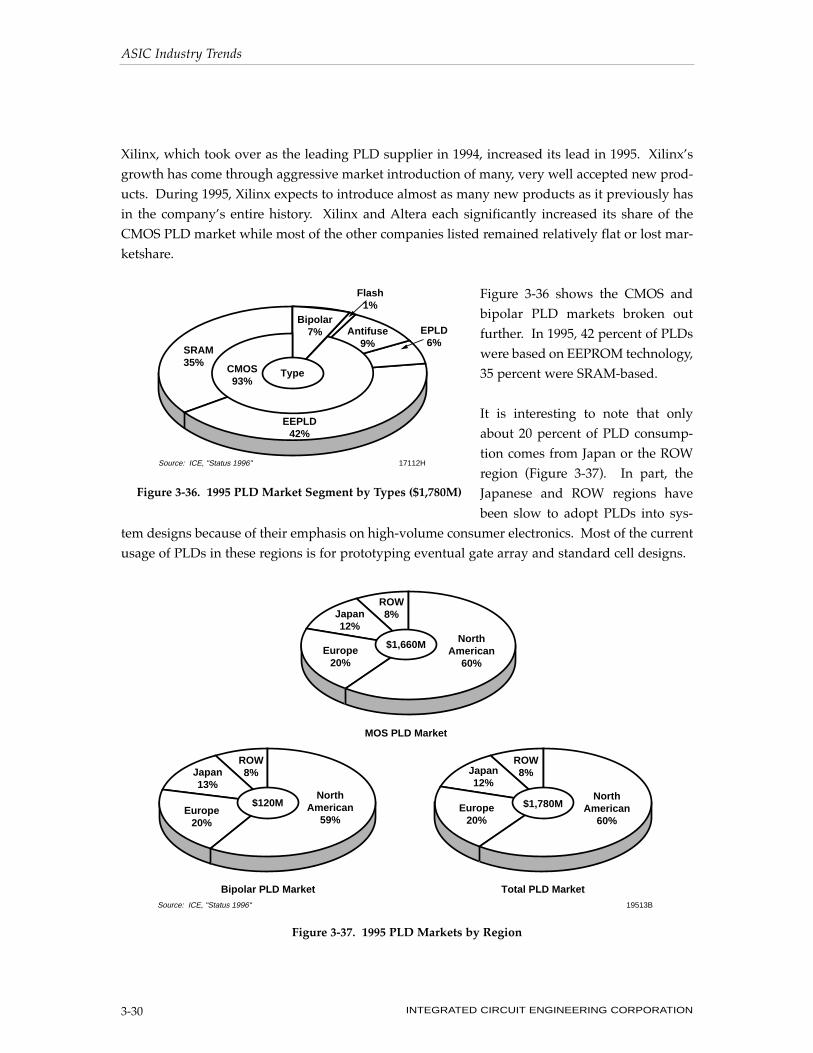

Xilinx, which took over as the leading PLD supplier in 1994, increased its lead in 1995. Xilinx’sgrowth has come through aggressive market introduction of many, very well accepted new prod-ucts. During 1995, Xilinx expects to introduce almost as many new products as it previously hasin the company’s entire history. Xilinx and Altera each significantly increased its share of theCMOS PLD market while most of the other companies listed remained relatively flat or lost mar-ketshare.

Figure 3-36 shows the CMOS andbipolar PLD markets broken outfurther. In 1995, 42 percent of PLDswere based on EEPROM technology,35 percent were SRAM-based.

It is interesting to note that onlyabout 20 percent of PLD consump-tion comes from Japan or the ROWregion (Figure 3-37). In part, theJapanese and ROW regions havebeen slow to adopt PLDs into sys-

tem designs because of their emphasis on high-volume consumer electronics. Most of the currentusage of PLDs in these regions is for prototyping eventual gate array and standard cell designs.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-30

Antifuse 9%

EPLD 6%

EEPLD 42%

SRAM 35%

Bipolar 7%

17112HSource: ICE, "Status 1996"

Flash 1%

CMOS 93%

Type

Figure 3-36. 1995 PLD Market Segment by Types ($1,780M)

North American

60%

North American

59%

North American

60%

ROW 8%

ROW 8%

ROW 8%

Japan 12%

Japan 13%

Japan 12%

Europe 20%

Europe 20%

Europe 20%

$1,660M

$120M $1,780M

MOS PLD Market

Bipolar PLD Market Total PLD Market19513BSource: ICE, "Status 1996"

Figure 3-37. 1995 PLD Markets by Region

Throughout 1995 many PLD suppliers reported that the market for PLDs in Japan was picking upsteam. It seems that the tight supply of less-than-10K-gate gate arrays is partially responsible forthis increased PLD usage.

REGIONAL ASIC MARKETSHARE

The 1995 company marketshare for various ASIC segments is shown in Figure 3-38. The areasinclude North America, Japan, Europe, and the Rest of the World (ROW). A company’s sales areclassified into one of the categories based on the location of its headquarters. So, even though acompany such as Texas Instruments has fabs located around the world, its headquarters are inNorth America and therefore all sales are credited to that region.

When it comes to ASIC devices, North American manufacturers have control in three of the fourmajor ASIC segments. With the exception of gate arrays, North American manufacturers domi-nated production in each major ASIC category in 1995.

Though North American firms can boast of significant ASIC production, the sum dollar total of allthree markets in which it dominates is only slightly more than the gate array market—the marketin which the Japanese have the highest share. Hyundai’s purchase of NCR (now Symbios) in 1994accounted for the large increase (to 11 percent in 1995 from less than one percent in 1995) in ROWshare of the standard cell market.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-31

0

10

20

30

40

50

60

70

80

90

100

���������������������������������

������������������������������������������������������������������

����������������������

���������������������������������������������������������������������������������������������������

����������������������������������������

Gate Arrays

($6,125M)

Standard Cells

($4,770M)

PLDs ($1,780M)

Analog Arrays ($235M)

Total ASIC* ($12,910M)

Per

cen

tag

e

34%

58%

49%

26%

14%

98%

57%

23%

49%

38%

8%

3%1% 5%

North American Companies

Japanese Companies

��������������������European

CompaniesRest of World Companies

*Not including full custom12910VSource: ICE, "Status 1996"

20%

11%

1%

5%

Figure 3-38. 1995 ASIC Segment Marketshare

Japanese companies have been most successful in the gate array market. Figure 3-39 shows thatalmost three-fourths of Japanese companies’ ASIC sales are gate arrays. North American sales in1995 were roughly split between the standard cell, gate array, and PLD business segments.European and ROW companies both emphasized standard cell products.

The total worldwide ASIC market (not including full custom) forecast by region is shown inFigure 3-40. By the year 2000, the North American market is expected to be the largest consumerof ASICs. It should be noted that, although the Japanese ASIC market is very large, much of theASIC IC value “consumed” in Japan is from internal transfers at the large electronics conglomer-ates (e.g., Fujitsu, Hitachi, NEC, etc.).

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-32

Gate Arrays 73%

Standard Cells 26%

PLDs <1% Analog Arrays 1%

$4.9B

Japanese Companies

European Companies

Gate Arrays 33%

Standard Cells 38%

PLDs 27%

Analog Arrays 2%

$6.3B

Standard Cells 64%

Gate Arrays 29%

Analog Arrays 5%

PLDs 2%

$1.0B

North American Companies

17794FSource: ICE, "Status 1996"

*Not including full custom

$0.7BStandard

Cells 74%

Gate Arrays

26%

ROW Companies

Figure 3-39. 1995 ASIC* Sales by Product Type

Japan 37%

North America 36%

Europe 19%

ROW 8%

Japan 33%

North America 36%

Europe 20%

ROW 11%

1995�$12.9B

2000�$28.6B

20402Source: ICE, "Status 1996"

Figure 3-40. Worldwide ASIC Markets by Region (Not Including Full Custom)

ASIC TECHNOLOGY TRENDS

Standard Cells (i.e., Cell-Based)

The two main technology thrusts in the standard cell ASIC segment in 1995 were the announce-ments and early implementation of 0.35µm, or finer, three- to five-layer metal CMOS technologyand the addition of sophisticated specialty cells and cores to the cell-based libraries. As wasshown earlier, the standard cell portion of the ASIC market is one of the fastest growing segments.The fast-paced technology improvements in the cell-based segment mentioned above are respon-sible for this growth surge.

While 0.35µm cell-based ASICs will represent only a small portion of the total ASIC marketthrough 1996, VLSI technology and Hitachi envision fast rising demand for the technology, frommany different system segments. As shown in Figure 3-41, the average gate density of the fivesegments listed is forecast to go from about 35K gates in 1993 to 1.4M gates in 1997. Moreover,average performance of these five segments is forecast to surge from 35MHz in 1993 to 150MHzin 1997! There is little doubt that million plus gate devices operating at 150MHz or higher willdemand 0.35µm technology.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-33

0.01 0.1 1.0 100

50

100

150

200

250

Network Computing Systems

Mobile PC

Consumer

Wireless

CY '97CY '95

CY '93

Per

form

ance

(M

Hz)

Integration (millions of gates)

20056Source: Hitachi/VLSI Technology/ICE, "Status 1996"

Figure 3-41. New Digital Markets for Advanced Cell-Based ASICs

Shown below are some selected standard cell offerings that are serving the diverse ASIC needs ofthe system manufacturer. Many of the process-related announcements (e.g., LSI Logic’s G10 tech-nology) are not standard cell specific but will be used for gate arrays as well.

• In 2Q94 Motorola announced its 0.65µm FlexCore program for customizing MPU-basedASICs using its cell-based technology. Typical NREs are $125K. The first processor coresavailable were the 68EC000 and 68020. A 68030 core (12 MIPS) surfaced in late 1994 and a 36MIPS 68040 was due in 1995. Power PC601 and 68060 cores are expected in 1996 (Figure 3-42). The FlexCore devices are targeting applications that typically use more than 100K unitsper year. Motorola states that turnaround time from concept to silicon for FlexCore deviceswill be about 6-9 engineering months.

• LSI Logic licensed the Rambus ASIC cell for use in its CoreWare cell-based library.

• Mitsubishi plans to incorporate its M36066A 64-bit Alpha MPU (licensed from DEC) as a corecell for internal use in 1996 and external cell-based sales in 1997.

• In 4Q94 LSI Logic introduced three MIPS R4000-architecture core MPUs into its cell-basedlibrary (CoreWare). Figure 3-43 describes these three cores.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION3-34

EC000 1992

'020 1Q94

'030 4Q94

'040 1995

'060 1996

Source: Motorola/ICE, "Status 1996" 19185

Per

form

ance

(M

IPS

)

0

10

100

Figure 3-42. FlexCore Core Processor Performance/Availability

• In 2Q95 VLSI Technology announced it had included a DSP core cell (Pine—from DSPGroup) into its standard cell library. DSP Group’s second-generation DSP cell “Oak” is alsoexpected to be licensed by VLSI at a later date.

• NEC introduced its cell-based 0.35µm CMOS ASIC technology (CB-C9) in 4Q95. Volumeproduction of the CB-C9 devices is expected in 2Q96. Some key aspects of the process areshown below.

Technology: 0.35µm drawn (0.27µm Leff) CMOSMetal Layers: 2 or 3Raw Gates: 80K to 3.5MUsable Gates: 50K to 1.6MPad Count: 104 to 1,200Performance: 113ps at F/O=2, L=0.44mm, Vdd= 3.3V

151ps at F/O=2, L=0.44mm, Vdd= 2.5VSpecial Macros: ARM7TDMI, RISC CPU, V30MX (Intel 80286 compatible),

Multiplier, PLL, A/D +D/A, Rambus interface cell

• In 3Q95 SGS-Thomson introduced the first member (ST20C4) of its 0.5µm 32-bit RISC coreprocessor (40MIPS at 50MHz) family.

• In 4Q95 Hitachi began offering its SH-1 32-bit RISC CPUs as part of its 0.5µm cell-based ASIClibrary. Hitachi also licensed an MPEG-3 decompression core from CompCore MultimediaInc. for use in its cell-based library.

• In 4Q95 IBM unveiled an extensive plan to target the cell-based ASIC marketplace using awide range of what it calls “system building blocks” (Figure 3-44). Figure 3-45 shows theadvanced technologies IBM will use to target the leading-edge ASIC market.

• LSI Logic introduced its G10™ ASIC process in 3Q95. Figure 3-46 shows some of the newG10 characteristics as well as a history of previous LSI Logic ASIC technologies. Figure 3-47shows the various sub-families of the G10 technology and their targeted applications.Volume production of ASICs using the new process is due in 1Q96.

ASIC Industry Trends

INTEGRATED CIRCUIT ENGINEERING CORPORATION 3-35

Uses 0.5µ technology, 5K gates, 4mm2 in size, operates up to 60MHz, targeting cost sensitive applications (e.g., portable telecom, consumer multimedia, etc.). Uses 0.5µ technology, 9K gates, superscalar RISC MIPS-II processor, operates up to 80MHz, targeting data processing applications. Will use 0.35µ technology, was due out in 2H95, 64-bit internal data path.

CW4001 CW4010 CW4100

20057ASource: ICE, "Status 1996"