second quarter 2009 report investment trends vol. … · second quarter 2009 report investment...

TRANSCRIPT

Sponsored by:

Second Quarter 2009 ReportVol. 5, No. 2Investment Trends

Quarterly

Spotlighton

Nashville

1Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

InThisVolume

Regional and Metro-Level AnalysesComing Soon!

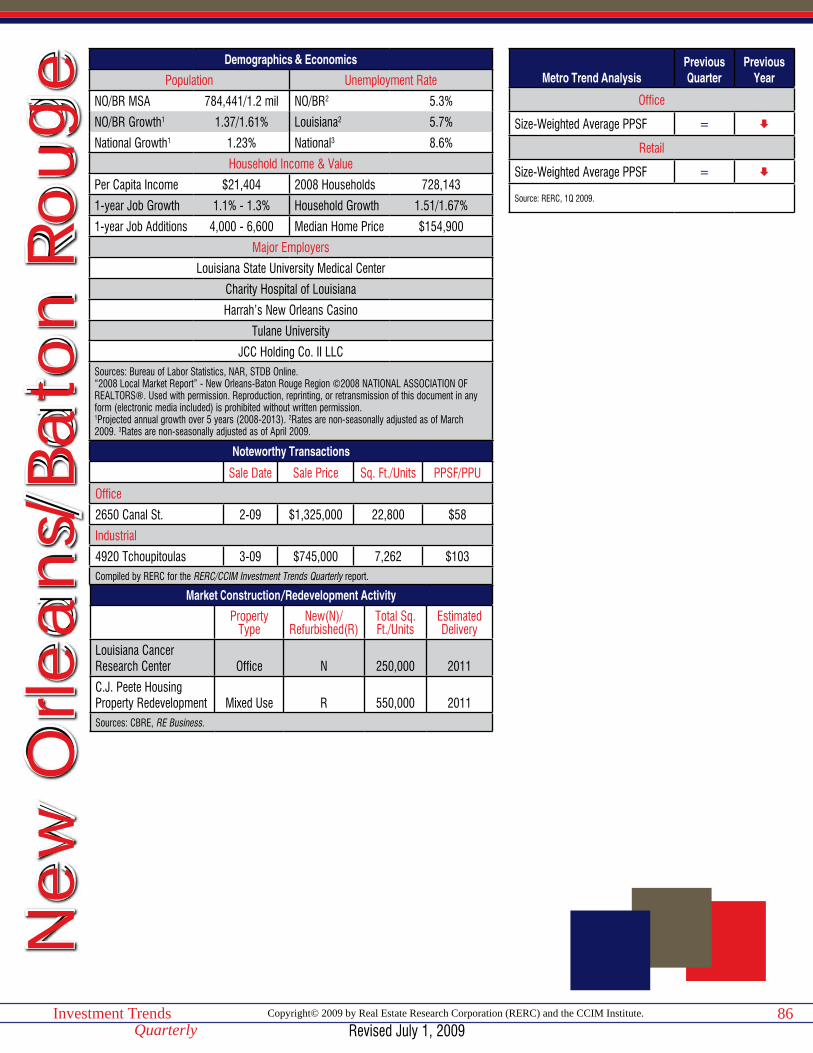

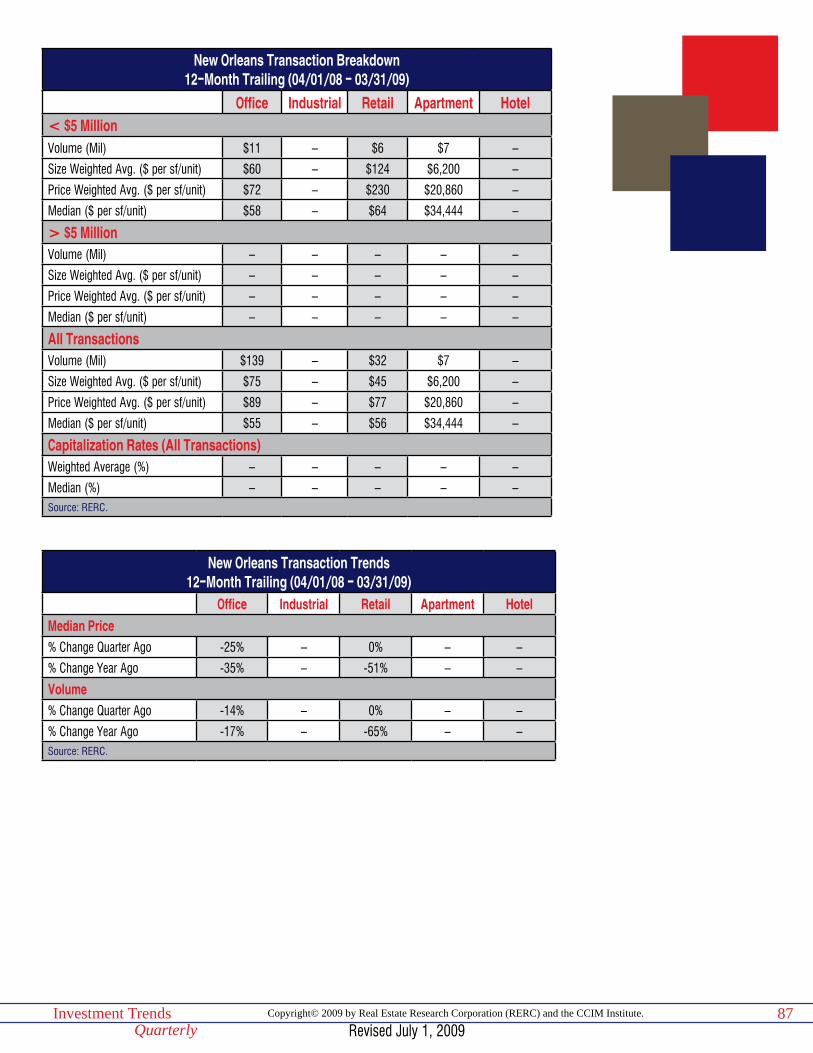

East RegionBaltimore, Boston, Charlotte, Hartford, Norfolk, Northern New Jersey, New York City, Pittsburgh, Philadelphia, Raleigh, Richmond, Washington, D.C.

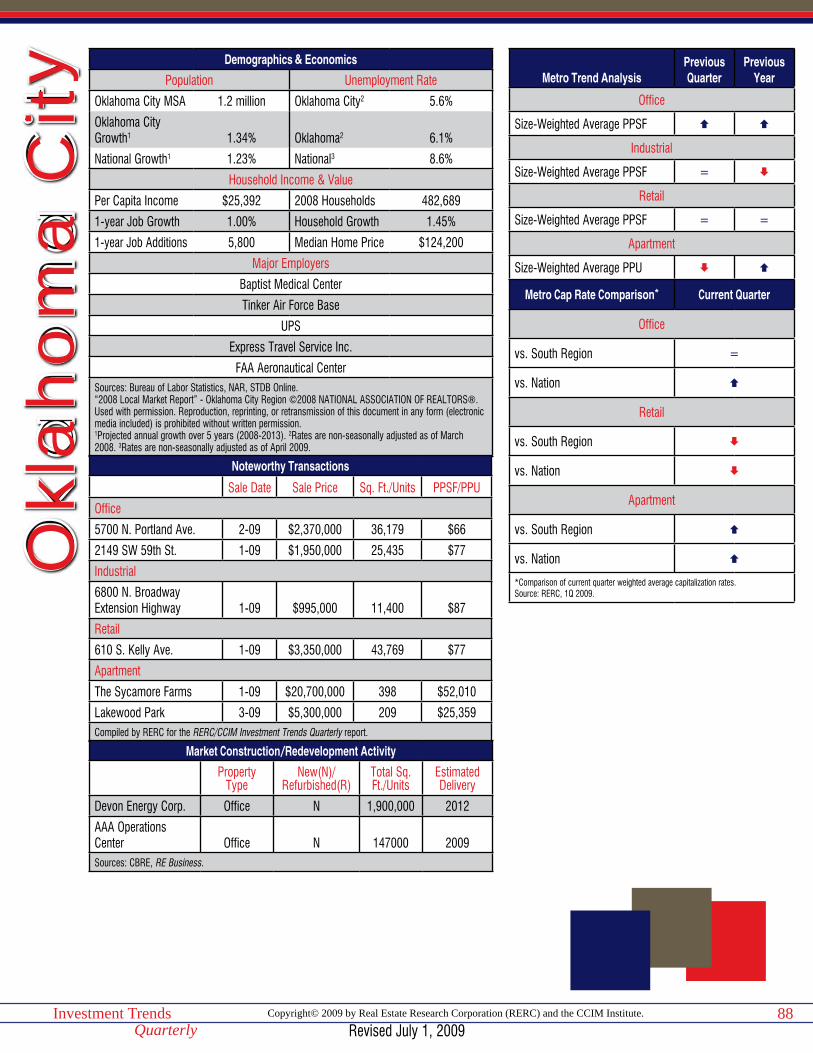

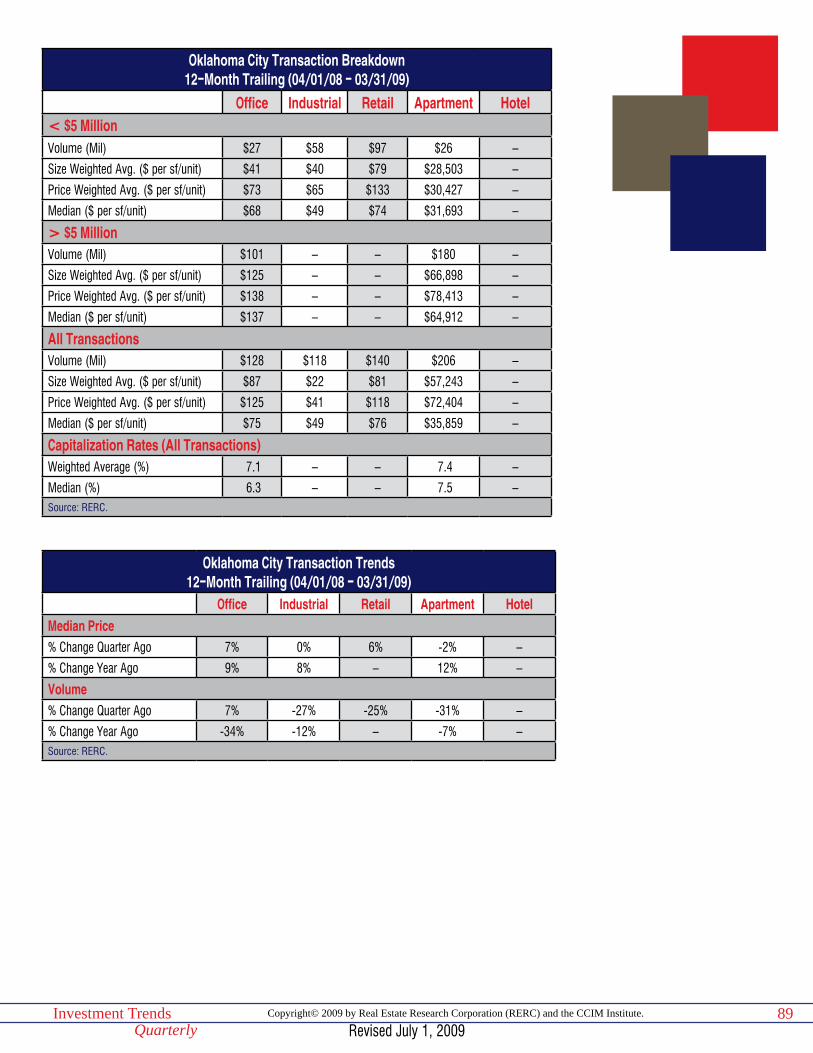

South RegionAtlanta, Austin, Dallas/Ft. Worth, Houston, Memphis, Miami, Nashville, New Orleans/Baton Rouge, Oklahoma City, Orlando, San Antonio, Tampa

Midwest RegionChicago, Cincinnati, Cleveland, Columbus, Detroit, Indianapolis, Kansas City, Milwaukee, Minneapolis, Omaha, St. Louis, Toledo

West RegionDenver, Honolulu, Las Vegas, Los Angeles, Phoenix, Portland, Sacramento, Salt Lake City, San Diego, San Francisco, Seattle, Tucson

Now Available!National OverviewIn Search of Bottom

Economic Background and Investment Environment

How Is Commercial Real Estate Affected?

A Focus on Real Estate Cap Rate & Yield Rate ExpectationsNational Market Analysis & Property Sector Highlights“Nashville Tunes in New Economic Growth...Beyond the Music”ContributorsScope & Methodology

2Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

Foreword

May 2009

Dear Readers,

Although the sense of optimism that we usually have during the spring season is being overshadowed by the reces-sion, there are news flashes here and there that indicate the economic freefall may be slowing. However, first quarter 2009 GDP contraction was nearly as low as that for fourth quarter 2008, and while not as many people in April lost jobs as did people in March, the unemployment rate increased from 8.5 percent in March to 8.9 percent in April. We were reminded that while it appears economic stabilization is underway, there will be many more ups and downs ahead of us before we see anything resembling economic recovery.

As for commercial real estate, a lagging indicator to the economy, we have yet to reach the bottom of this down cycle. For those of you who thought we would never again see anything like the real estate crisis in the early 1990s, it appears that the losses in this recession may be even more severe. In the 1990s, prices declined 30 to 35 percent over 5 years, which was bad enough. However, the crisis we find ourselves in today is happening at an accelerated pace, and real estate prices have fallen 20 to 25 percent on a free and clear basis in just the last 3 quarters!

Beyond price adjustments, reduced returns, and continued lack of credit availability, property fundamentals are de-clining throughout the industry. On a national basis, vacancy rates are up at least a half percentage point for each property type. Prices and rents are declining, absorption is negative, and capitalization rates are increasing. RERC’s analysis of this information, along with the views contributed by many CCIM Institute designees and candidates, is provided in the second quarter 2008 RERC/CCIM Investment Trends Quarterly.

We thank all who responded to and completed RERC’s surveys when encouraged by the CCIM Institute. Your con-tributions to the information available to the commercial real estate industry are needed and appreciated now more than ever.

Sincerely,

Kenneth P. Riggs, Jr., CCIM, CRE, MAIPresident & CEOReal Estate Research Corporation (RERC)

Charles “Mac” McClure, CCIM2009 CCIM Institute PresidentChairman, The McClure Group, Inc.

3Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

InSearchofBottom

The recent Chapter 11 bankruptcy of General Growth Properties, Inc. was a particularly sad day for anyone associated with this real estate investment trust (REIT) or with the Bucksbaum family. Like many other real estate owners who have overleveraged, General Growth was caught in the worst credit and capital markets crisis since the 1930s and was not able to work its way through it without reorganizing. While we understand and appreciate the difficulty General Growth is going through, it is important to also take note of how quickly the financial situation of the nation’s second largest mall owner deteriorated, and how the challenges they have and are going through are also occurring in countless other businesses. The speed at which this recession has deepened and the severity of its damage have shocked us all, from the federal government on down.

Still, in the long run, there may be more hope for General Growth to come back from bankruptcy and to preserve the majority of its assets than it will for many other industries. Although we are seeing some progress in the housing industry, there is much unraveling yet to be done at Fannie Mae and Freddie Mac, with more home foreclosures and further price declines, at least in some regions, still ahead. In addition, the stress tests administered to the large investment houses have not reflected well on the banks’ overall health, and despite some first quarter profits, there are still worrisome piles of legacy/toxic assets on the banks’ books that must somehow be disposed of. The auto industry is at a breaking point, and with the bankruptcy of Chrysler, there are fears that the bankruptcy of General Motors cannot be far behind. An average of 45 percent fewer cars and light trucks were sold by the Big Three last year than in the previous year, and it is no wonder that lower sales volume, added to their other high costs of doing business, may mean the end of this industry as we know it. When we consider the ripple effect on auto parts suppliers of steel, rubber, tech items like CD players or GPS systems, besides the leathers and fabrics that are included in the production of a car or truck, one can get an idea of the additional jobs that are likely to be lost before this is over. Other industries, including insurance, retailing, manufacturing, airlines, hotels and lodging, education, state and local governments, and even healthcare continue to see increased unemployment as well.

As always, it is the loss of jobs that will have the longest-lasting impact on commercial real estate. With unemployment expected to increase at least throughout 2009, the damage to real estate fundamentals will increase accordingly, with higher vacancy, negative absorption, declining rents, and decreased values. It will be some time before we see the bottom of the commercial real estate market and know exactly what it is we have to deal with, but the majority of real estate investors remain determined to work through and overcome the new depths associated with this crisis.

4Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

It seems that most watchers of the economy have spent the majority of first quarter 2009 downgrading their expectations for the rest of this year. We have seen some indications of improvement during the last month or two, but hopes for an early end to the recession were dashed when the Commerce Department reported first quarter gross domestic product (GDP) growth grew at a seasonally-adjusted annual rate of –6.1 percent for first quarter, not much better than the –6.3 percent rate for fourth quarter 2008. In addition to witnessing the worst 6-month economic performance since the 1950s, this is the first time since the mid-1970s that we have seen the economy contract for 3 consecutive quarters.

With the loss of another 674,000 jobs in March 2009 and 539,000 jobs in April, unemployment increased to 8.9 per-cent. Recent losses were higher than most economists had expected, and came from a broad array of companies like United Technologies, Nortel Networks, Pioneer, Goodyear, Smithfield Foods, Nissan Motor, Panasonic, Estee Lauder, PNC Financial Services, and others. Many economists are now predicting that the unemployment rate will reach double digits by the end of this year.

On a local level, 18 of the 372 metros tracked by the Bureau of Labor Statistics (BLS) have jobless rates of at least 15 per-cent, and 109 metros have jobless rates of at least 10 per-cent, with El Centro, Calif., reporting an unemployment rate of 25.1 percent, the highest unemployment rate among these metros.

The pressure remains on consumers, but consumers have less to spend and they are saving more of what they do have during this recession. It is no wonder they are keeping their pocketbooks closed—they have lost retirement savings, lost value in their homes, and are worried about losing their jobs. This loss is real, and it is immense. According to the Federal Reserve, the drop in household net worth, including home values, mutual funds, life insurance, and college and pension funds, dropped by $11 trillion, a decline of nearly 18 percent, during 2008.

Although consumer spending increased 2.2 percent in first quarter 2009, personal consumption fell at a seasonally-adjusted rate of 0.2 percent during the month of March, the fourth such decline during the last 6 months. In addition, retail

sales inched upward during the first part of the quarter, with a 1.9 percent jump in January and a 0.3 percent increase in February, but March retail sales declined 1.1 percent. Per-sonal income fell 0.3 percent in March, the fifth decrease in the last 6 months, while personal savings increased 4.2 per-cent in March, reports the Commerce Department.

As second quarter 2009 gets underway, however, there have been a few signs that the economy could be starting to stabi-lize. Consumer confidence increased to 39.2 in April, up from 26.9 in March. Although this jump was considerable, the in-dex reading overall was approximately two-thirds lower than it was 2 years ago. Still, it is a sign that consumers may be starting to think about loosening up on the purse strings. Ac-cording to the Conference Board, the Present Situation Index and the Expectations Index also rose in April.

The Commerce Department reported that housing starts in-creased 17.2 percent in February 2009 to 572,000 homes, although starts fell 10.8 percent in March to a seasonally-ad-justed 510,000 homes. With the inventory for homes remain-ing high, this decrease is considered a positive factor for the housing market overall in that it helps to keep overall supply from increasing further. Home prices fell 2.2 percent in Febru-ary, according to the Standard & Poor’s/Case-Shiller Index, but it is important to note that the pace of deterioration has slowed and that a period of leveling off may be underway.

Perhaps the most encouraging flicker of improvement in the economy is the stock market’s brief market rally that we en-joyed this April. Although we have a long way to go before we can even imagine recovering what was lost in last fall’s crash, since the stock market generally serves as a leading indica-tor regarding improvement in the economy, there is legitimate hope that things may slowly start to turn around, barring any new calamities.

With respect to the economic landscape, CCIM members who responded to RERC’s survey rated the U.S. economy’s first quarter 2009 performance at 3.5 on a scale of 1 to 10, with 10 being excellent. While low, this rating is up from last quarter’s rating of 2.6. The East and Midwest regional econo-mies received slightly higher ratings than the West and South regions.

Economic Background andInvestment Environment

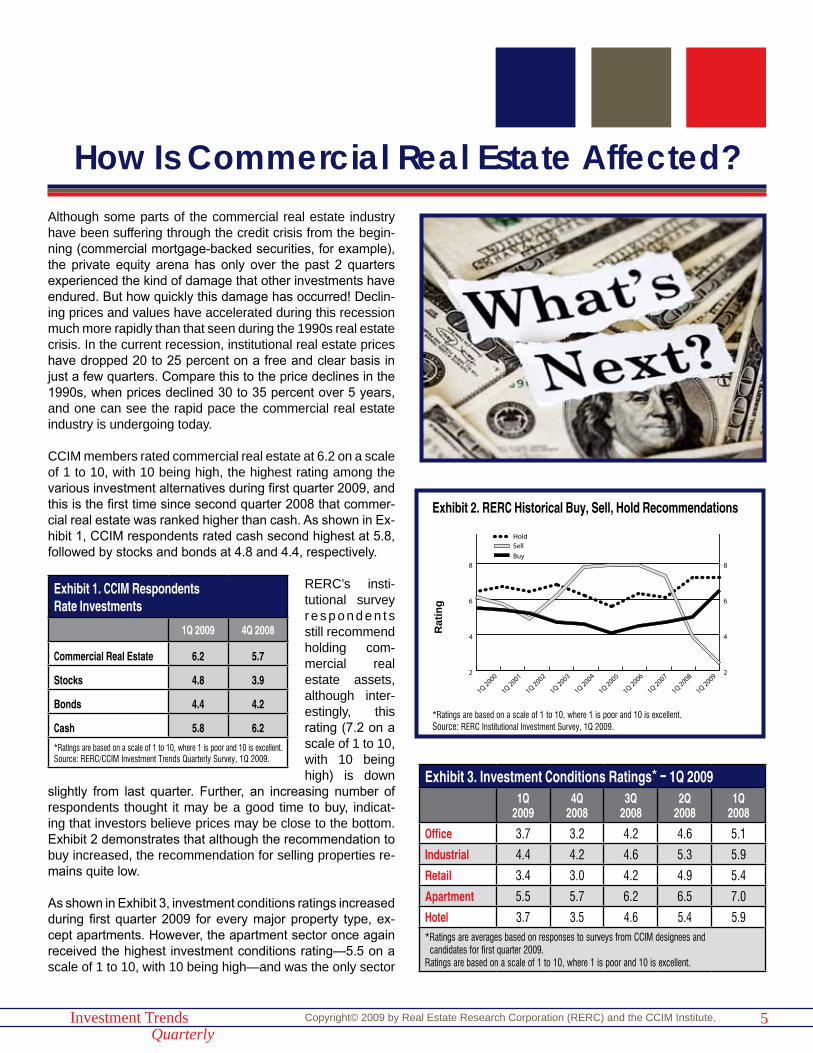

Although some parts of the commercial real estate industry have been suffering through the credit crisis from the begin-ning (commercial mortgage-backed securities, for example), the private equity arena has only over the past 2 quarters experienced the kind of damage that other investments have endured. But how quickly this damage has occurred! Declin-ing prices and values have accelerated during this recession much more rapidly than that seen during the 1990s real estate crisis. In the current recession, institutional real estate prices have dropped 20 to 25 percent on a free and clear basis in just a few quarters. Compare this to the price declines in the 1990s, when prices declined 30 to 35 percent over 5 years, and one can see the rapid pace the commercial real estate industry is undergoing today.

CCIM members rated commercial real estate at 6.2 on a scale of 1 to 10, with 10 being high, the highest rating among the various investment alternatives during first quarter 2009, and this is the first time since second quarter 2008 that commer-cial real estate was ranked higher than cash. As shown in Ex-hibit 1, CCIM respondents rated cash second highest at 5.8, followed by stocks and bonds at 4.8 and 4.4, respectively.

RERC’s insti-tutional survey r e s p o n d e n t s still recommend holding com-mercial real estate assets, although inter-estingly, this rating (7.2 on a scale of 1 to 10, with 10 being high) is down

slightly from last quarter. Further, an increasing number of respondents thought it may be a good time to buy, indicat-ing that investors believe prices may be close to the bottom. Exhibit 2 demonstrates that although the recommendation to buy increased, the recommendation for selling properties re-mains quite low.

As shown in Exhibit 3, investment conditions ratings increased during first quarter 2009 for every major property type, ex-cept apartments. However, the apartment sector once again received the highest investment conditions rating—5.5 on a scale of 1 to 10, with 10 being high—and was the only sector

5Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

How Is Commercial Real Estate Affected?

Exhibit 1. CCIM RespondentsRate Investments

1Q 2009 4Q 2008

Commercial Real Estate 6.2 5.7

Stocks 4.8 3.9

Bonds 4.4 4.2

Cash 5.8 6.2

*Ratings are based on a scale of 1 to 10, where 1 is poor and 10 is excellent.Source: RERC/CCIM Investment Trends Quarterly Survey, 1Q 2009.

Exhibit 3. Investment Conditions Ratings* - 1Q 20091Q

20094Q

20083Q

20082Q

20081Q

2008

Office 3.7 3.2 4.2 4.6 5.1

Industrial 4.4 4.2 4.6 5.3 5.9

Retail 3.4 3.0 4.2 4.9 5.4

Apartment 5.5 5.7 6.2 6.5 7.0

Hotel 3.7 3.5 4.6 5.4 5.9*Ratings are averages based on responses to surveys from CCIM designees and candidates for first quarter 2009.Ratings are based on a scale of 1 to 10, where 1 is poor and 10 is excellent.

2

4

6

8

10

2

4

6

8

10HoldSell

Buy

1Q 2009

1Q 2008

1Q 2007

1Q 2006

1Q 2005

1Q 2004

1Q 2003

1Q 2002

1Q 2001

1Q 2000

Exhibit 2. RERC Historical Buy, Sell, Hold Recommendations

*Ratings are based on a scale of 1 to 10, where 1 is poor and 10 is excellent.Source: RERC Institutional Investment Survey, 1Q 2009.

Rat

ing

6Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

Exhibit 5. What Do the Financial Markets Tell Us?

Compounded Annual Rates of Return as of 3/31/2009

Market Indices YTD 1-Year (2008) 3-Year 5-Year 10-Year 15-Year

Consumer Price Index1 0.58% -0.28% 2.14% 2.60% 2.59% 2.49%

10-Year Treasury Bond2 2.74% 3.44% 4.36% 4.27% 4.65% 5.21%

Dow Jones Industrial Average -12.48% -35.94% -9.52% -3.64% -0.36% 7.34%

NASDAQ Composite3 -3.07% -32.93% -13.23% -5.18% -4.65% 4.92%

NYSE Composite3 -13.52% -43.40% -15.44% -5.48% -2.45% 4.39%

S&P 500 -11.01% -38.09% -13.06% -4.77% -3.00% 5.91%

NCREIF Index -7.33% -14.67% 4.16% 9.43% 9.37% 9.94%

NAREIT Index (Equity REITS) -17.61% -58.16% -25.05% -8.64% 3.89% 5.24%1Based on the published data from the Bureau of Labor Statistics (Seasonally Adjusted).2Based on Average End of Day T-Bond Rates.3Based on Price Index, and does not include the dividend yield.Sources: BLS, Federal Reserve Board, S&P, Dow Jones, NCREIF, NAREIT, compiled by RERC.

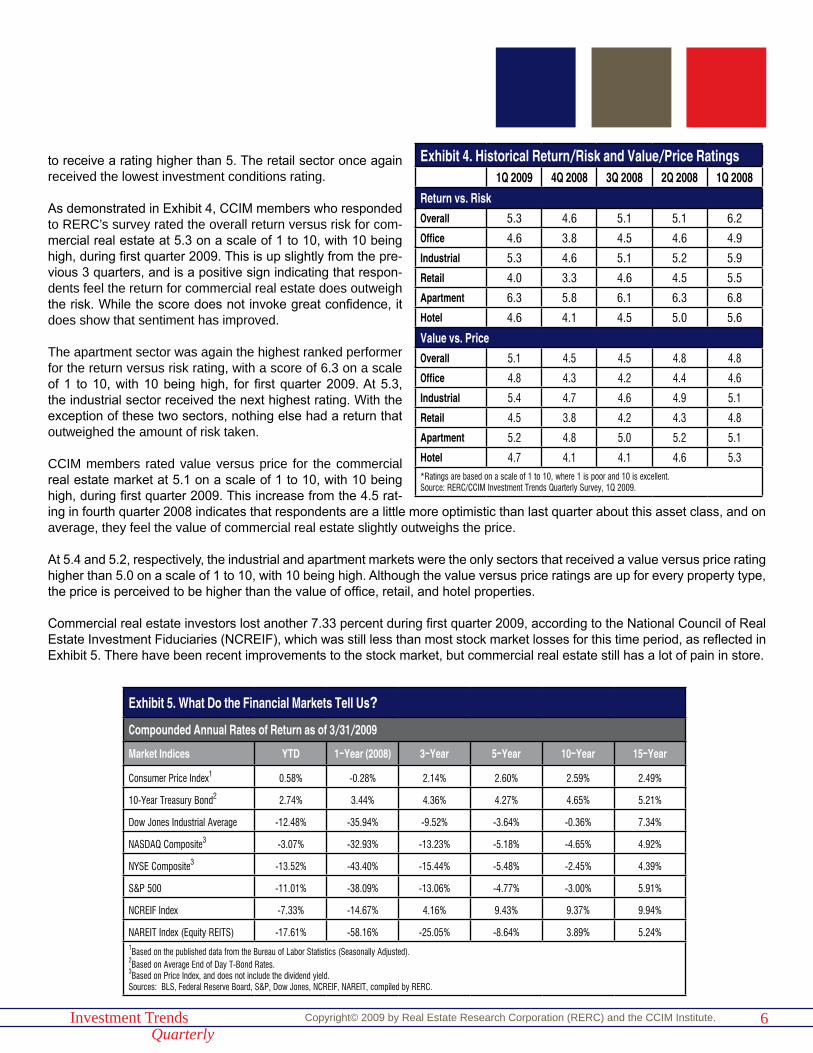

to receive a rating higher than 5. The retail sector once again received the lowest investment conditions rating.

As demonstrated in Exhibit 4, CCIM members who responded to RERC’s survey rated the overall return versus risk for com-mercial real estate at 5.3 on a scale of 1 to 10, with 10 being high, during first quarter 2009. This is up slightly from the pre-vious 3 quarters, and is a positive sign indicating that respon-dents feel the return for commercial real estate does outweigh the risk. While the score does not invoke great confidence, it does show that sentiment has improved.

The apartment sector was again the highest ranked performer for the return versus risk rating, with a score of 6.3 on a scale of 1 to 10, with 10 being high, for first quarter 2009. At 5.3, the industrial sector received the next highest rating. With the exception of these two sectors, nothing else had a return that outweighed the amount of risk taken.

CCIM members rated value versus price for the commercial real estate market at 5.1 on a scale of 1 to 10, with 10 being high, during first quarter 2009. This increase from the 4.5 rat-ing in fourth quarter 2008 indicates that respondents are a little more optimistic than last quarter about this asset class, and on average, they feel the value of commercial real estate slightly outweighs the price.

At 5.4 and 5.2, respectively, the industrial and apartment markets were the only sectors that received a value versus price rating higher than 5.0 on a scale of 1 to 10, with 10 being high. Although the value versus price ratings are up for every property type, the price is perceived to be higher than the value of office, retail, and hotel properties.

Commercial real estate investors lost another 7.33 percent during first quarter 2009, according to the National Council of Real Estate Investment Fiduciaries (NCREIF), which was still less than most stock market losses for this time period, as reflected in Exhibit 5. There have been recent improvements to the stock market, but commercial real estate still has a lot of pain in store.

Exhibit 4. Historical Return/Risk and Value/Price Ratings1Q 2009 4Q 2008 3Q 2008 2Q 2008 1Q 2008

Return vs. RiskOverall 5.3 4.6 5.1 5.1 6.2

Office 4.6 3.8 4.5 4.6 4.9

Industrial 5.3 4.6 5.1 5.2 5.9

Retail 4.0 3.3 4.6 4.5 5.5

Apartment 6.3 5.8 6.1 6.3 6.8

Hotel 4.6 4.1 4.5 5.0 5.6

Value vs. PriceOverall 5.1 4.5 4.5 4.8 4.8

Office 4.8 4.3 4.2 4.4 4.6

Industrial 5.4 4.7 4.6 4.9 5.1

Retail 4.5 3.8 4.2 4.3 4.8

Apartment 5.2 4.8 5.0 5.2 5.1

Hotel 4.7 4.1 4.1 4.6 5.3*Ratings are based on a scale of 1 to 10, where 1 is poor and 10 is excellent.Source: RERC/CCIM Investment Trends Quarterly Survey, 1Q 2009.

7Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

While the U.S. economy continues to suffer the ill effects of the post-credit market extremes, there is evidence that the decline is slowing and we are starting to see a few signs of entering into a period (potentially protracted) of stabilization. Warning: This is not to suggest a recovery is on the horizon. We have much yet to work through, and there will be many more ups and downs before we can expect anything resembling a re-covery in jobs and the housing market. But first, we need to stabilize from the worst shocks to our economy and financial markets since the Great Depression.

Despite the Federal Reserve’s extremely accommodative monetary policy and the influx of capital targeted at the in-vestment banks, many of the same issues that threatened the capital markets remain unresolved. Lack of credit continues as a drain on the economy, as we saw recently with the second consecutive 6-percent contraction in GDP, which was attrib-uted mostly to the continued reduction in business investment (which fell 38 percent in first quarter 2009). Although we are seeing some stabilization in the housing market overall, there are many areas that will see additional price declines. In ad-dition, the stress tests the banks have undergone have indi-cated that the health of the banks remains somewhat precari-ous, with many of them needing additional funds to continue to operate. With respect to commercial real estate, the difficul-ties associated with overleveraging continue to drag down the market, and there is much more pain in store for investors.

The economic stresses causing commercial real estate funda-mentals to deteriorate, particularly additional job losses, are expected to continue throughout the year. With consumers remaining cautious, concentrating on expanding their sav-

ings and replenishing their retirement accounts, investors also should expect slow consumer spending to continue. These factors will further negatively impact the office, industrial, re-tail, apartment, and hotel property sectors.

Since commercial real estate is a lagging indicator to the economy, RERC estimates stabilization in the economy to oc-cur before year-end 2009 with strong signs of this in the sec-ond quarter, and commercial real estate following suit approxi-mately 12 months after stabilization occurs in the economy. That means stabilization in the commercial real estate industry will not begin until mid-2010. Until then and as the commer-cial real estate market continues to struggle with new depths, watch for:

• Lack of credit availability in the near term.

• Fundamentals to continue to deteriorate throughout 2009.

• Vacancy/availability rates to increase in all property sec-tors.

• Capitalization rate increases to begin leveling off.

• Property sale prices and rents to continue to decrease.

• Concessions and terms favoring buyers to continue.

• Buy opportunities in CMBS or with distressed debt proper-ties.

Summary

8Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

NAR Commercial Forecast: February 20092008 2009

2007 2008 2009I II III IV I II III

OFFICE

Vacancy Rate (%) 12.9 13.2 13.4 13.9 14.7 15.7 16.7 12.5 13.4 16.2

Net Absorption (’000 sq. ft.) 3,192 5,206 4,800 -6,893 -15,091 -17,537 -20,336 57,265 12,271 -77,406

Completions (’000 sq. ft.) 15,701 17,637 21,961 12,888 15,733 16,900 19,306 61,102 68,187 71,356

Inventory (millions sq. ft.) 3,427 3,445 3,467 3,480 3,495 3,512 3,532 3,409 3,480 3,551

Rent Growth (%) 1.0 -0.2 -0.6 -0.6 -0.8 -0.9 -1.2 8.0 -0.4 -4.2

INDUSTRIAL

Vacancy Rate (%) 9.8 9.9 10.7 11.1 11.4 11.7 12.2 9.4 10.4 12.0

Net Absorption (’000 sq. ft.) -12,678 -30,441 -8,327 -5,795 -18,540 -32,552 -44,575 120,231 -57,241 -148,062

Completions (’000 sq. ft.) 34,847 42,847 44,639 57,280 12,214 17,249 35,779 126,765 179,613 69,553

Inventory (millions sq. ft.) 12,778 12,821 12,866 12,923 12,935 12,953 12,988 12,399 12,923 12,993

Rent Growth (%) 0.2 0.5 -0.7 -0.8 -0.8 -0.9 -1.2 3.6 -0.8 -4.1

RETAIL

Vacancy Rate (%) 9.0 9.3 9.8 10.8 11.8 12.6 13.4 9.2 9.7 13.0

Net Absorption (’000 sq. ft.) -639 622 -2,157 -8,784 -12,397 -12,503 -12,250 11,081 -7,315 -49,754

Completions (’000 sq. ft.) 5,070 6,296 6,246 8,674 3,483 809 625 29,733 26,286 5,858

Inventory (millions sq. ft.) 1,598 1,606 1,612 1,621 1,624 1,625 1,626 1,580 1,621 1,627

Rent Growth (%) 0.7 0.7 0.8 -4.2 -2.2 -2.6 -2.2 3.2 -2.0 -9.0

MULTIFAMILY

Vacancy Rate (%) 5.5 5.4 5.8 6.1 6.0 6.0 6.0 5.4 5.7 6.2

Net Absorption (Units) -52,603 37,680 27,303 12,001 60,112 57,808 56,998 234,399 24,390 127,523

Completions (Units) 56,275 54,573 53,999 55,926 53,894 58,157 55,731 230,932 220,773 214,027

Inventory (Units in Millions) 14.1 14.1 14.2 14.2 14.3 14.3 14.4 14.0 14.2 14.4

Rent Growth (%) 0.9 0.9 0.5 0.6 0.4 0.4 0.5 3.1 2.9 1.7

Sources: NAR, CBRE/Torto Wheaton Research.

NAR U.S. Economic Outlook: May 20092008 Quarterly 2009 Quarterly 2010 Quarterly Annual

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2007 2008 2009 2010

Annual Growth Rate

Real GDP -0.5 -6.3 -6.1 -1.7 0.3 0.8 1.4 2.6 2.5 2.8 2.0 1.1 -2.9 1.4

Nonfarm Payroll Employment -1.5 -3.7 -5.9 -3.7 -2.1 -0.8 0.0 1.0 1.1 1.2 1.1 -0.4 -3.4 -0.2

Consumer Prices 6.2 -8.3 -2.4 0.7 1.8 2.0 2.1 2.2 2.3 2.5 2.9 3.8 -0.8 1.7

Real Disposable Income -8.5 2.7 6.2 -2.0 0.9 0.7 1.3 1.4 2.2 2.6 2.8 1.3 1.3 1.1

Consumer Confidence 57 41 32 43 44 43 42 40 43 45 103 58 41 43

Unemployment 6.0 6.9 8.1 9.4 10.0 10.5 10.4 10.3 10.2 10.1 4.6 5.8 9.5 10.2

Interest Rates, Percent

Fed Funds Rate 1.9 0.5 0.2 0.1 0.1 0.1 0.1 0.8 1.5 2.0 5.0 1.9 0.1 1.1

3-Month T-Bill Rate 1.5 0.3 0.2 0.3 0.3 0.3 0.3 0.9 1.6 2.1 4.4 1.4 0.3 1.2

Prime Rate 5.0 4.1 3.3 2.9 3.0 3.0 3.0 3.3 4.0 4.8 8.1 5.1 3.1 4.1

Corporate Aaa Bond Yield 5.7 5.8 5.3 5.5 5.5 5.5 5.3 5.0 5.0 4.9 5.6 5.6 5.4 5.1

10-Year Government Bond 3.9 3.3 2.7 3.0 3.0 3.1 3.1 3.1 3.3 3.4 4.6 3.7 2.9 3.2

30-Year Government Bond 4.4 3.7 3.5 3.5 3.5 3.7 3.7 3.7 3.9 4.0 4.8 4.3 3.5 3.8

Source: Forecast produced using Macroeconomic Advisers quarterly model of the U.S. economy. Quarterly figures are seasonally-adjusted annual rates. Assumptions and simulations by NAR's Dr. Lawrence Yun.

9Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

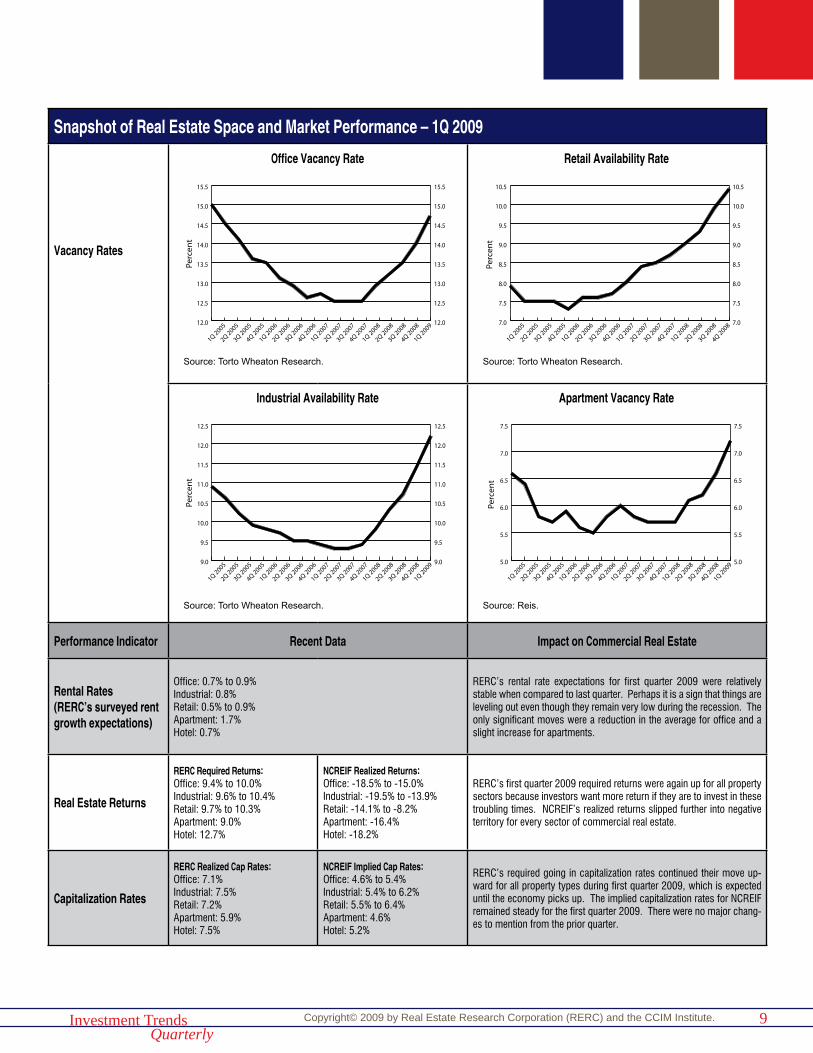

Snapshot of Real Estate Space and Market Performance – 1Q 2009

Vacancy Rates

Performance Indicator Recent Data Impact on Commercial Real Estate

Rental Rates(RERC’s surveyed rent growth expectations)

Office: 0.7% to 0.9%Industrial: 0.8%Retail: 0.5% to 0.9%Apartment: 1.7%Hotel: 0.7%

RERC’s rental rate expectations for first quarter 2009 were relatively stable when compared to last quarter. Perhaps it is a sign that things are leveling out even though they remain very low during the recession. The only significant moves were a reduction in the average for office and a slight increase for apartments.

Real Estate Returns

RERC Required Returns:Office: 9.4% to 10.0%Industrial: 9.6% to 10.4%Retail: 9.7% to 10.3%Apartment: 9.0%Hotel: 12.7%

NCREIF Realized Returns:Office: -18.5% to -15.0%Industrial: -19.5% to -13.9%Retail: -14.1% to -8.2%Apartment: -16.4%Hotel: -18.2%

RERC’s first quarter 2009 required returns were again up for all property sectors because investors want more return if they are to invest in these troubling times. NCREIF’s realized returns slipped further into negative territory for every sector of commercial real estate.

Capitalization Rates

RERC Realized Cap Rates:Office: 7.1%Industrial: 7.5%Retail: 7.2%Apartment: 5.9%Hotel: 7.5%

NCREIF Implied Cap Rates:Office: 4.6% to 5.4%Industrial: 5.4% to 6.2%Retail: 5.5% to 6.4%Apartment: 4.6%Hotel: 5.2%

RERC’s required going in capitalization rates continued their move up-ward for all property types during first quarter 2009, which is expected until the economy picks up. The implied capitalization rates for NCREIF remained steady for the first quarter 2009. There were no major chang-es to mention from the prior quarter.

12.0

12.5

13.0

13.5

14.0

14.5

15.0

15.5

12.0

12.5

13.0

13.5

14.0

14.5

15.0

15.5

1Q 2009

4Q 2008

3Q 2008

2Q 2008

1Q 2008

4Q 2007

3Q 2007

2Q 2007

1Q 2007

4Q 2006

3Q 2006

2Q 2006

1Q 2006

4Q 2005

3Q 2005

2Q 2005

1Q 2005

Perc

ent

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

4Q 2008

3Q 2008

2Q 2008

1Q 2008

4Q 2007

3Q 2007

2Q 2007

1Q 2007

4Q 2006

3Q 2006

2Q 2006

1Q 2006

4Q 2005

3Q 2005

2Q 2005

1Q 2005

Perc

ent

9.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

1Q 2009

4Q 2008

3Q 2008

2Q 2008

1Q 2008

4Q 2007

3Q 2007

2Q 2007

1Q 2007

4Q 2006

3Q 2006

2Q 2006

1Q 2006

4Q 2005

3Q 2005

2Q 2005

1Q 2005

Perc

ent

5.0

5.5

6.0

6.5

7.0

7.5

5.0

5.5

6.0

6.5

7.0

7.5

1Q 2009

4Q 2008

3Q 2008

2Q 2008

1Q 2008

4Q 2007

3Q 2007

2Q 2007

1Q 2007

4Q 2006

3Q 2006

2Q 2006

1Q 2006

4Q 2005

3Q 2005

2Q 2005

1Q 2005

Perc

ent

Source: Torto Wheaton Research.

Source: Torto Wheaton Research.

Source: Torto Wheaton Research.

Source: Reis.

Office Vacancy Rate Retail Availability Rate

Industrial Availability Rate Apartment Vacancy Rate

10Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

-7

-5

-3

-1

1

3

5

7

9

-7

-5

-3

-1

1

3

5

7

9

1Q 2009

3Q 2008

1Q 2008

3Q 2007

1Q 2007

3Q 2006

1Q 2006

3Q 2005

1Q 2005

3Q 2004

1Q 2004

3Q 2003

1Q 2003

3Q 2002

1Q 2002

3Q 2001

1Q 2001

3Q 2000

1Q 2000

Perc

ent C

hang

e Q

uart

er A

go

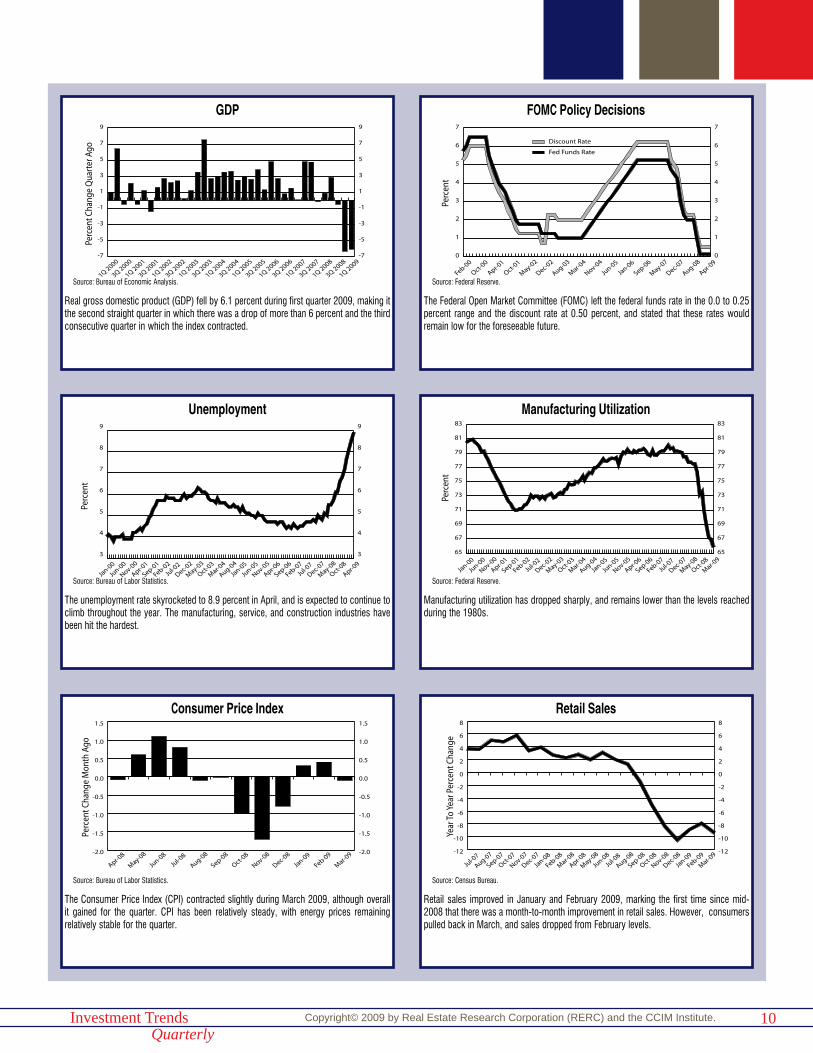

Real gross domestic product (GDP) fell by 6.1 percent during first quarter 2009, making it the second straight quarter in which there was a drop of more than 6 percent and the third consecutive quarter in which the index contracted.

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

Mar-09

Feb-09

Jan-0

9

Dec-08

Nov-08

Oct-08

Sep-08

Aug-08

Jul-0

8

Jun-0

8

May-08

Apr-08

Perc

ent C

hang

e M

onth

Ago

The Consumer Price Index (CPI) contracted slightly during March 2009, although overall it gained for the quarter. CPI has been relatively steady, with energy prices remaining relatively stable for the quarter.

Source: Bureau of Labor Statistics.

Perc

ent

3

4

5

6

7

8

9

3

4

5

6

7

8

9

Apr-09

Oct-08

May-08

Dec-07

Jul-0

7

Feb-07

Sep-06

Apr-06

Nov-05

Jun-0

5

Jan-0

5

Aug-04

Mar-04

Oct-03

May-03

Dec-02

Jul-0

2

Feb-02

Sep-01

Apr-01

Nov-00

Jun-0

0

Jan-0

0

The unemployment rate skyrocketed to 8.9 percent in April, and is expected to continue to climb throughout the year. The manufacturing, service, and construction industries have been hit the hardest.

Source: Bureau of Labor Statistics.

Source: Bureau of Economic Analysis.

Perc

ent

0

1

2

3

4

5

6

7

0

1

2

3

4

5

6

7

Discount Rate

Fed Funds Rate

Apr-09

Aug-08

Dec-07

May-07

Sep-06

Jan-0

6

Jun-0

5

Nov-04

Mar-04

Aug-03

Dec-02

May-02

Oct-01

Apr-01

Oct-00

Feb-00

The Federal Open Market Committee (FOMC) left the federal funds rate in the 0.0 to 0.25 percent range and the discount rate at 0.50 percent, and stated that these rates would remain low for the foreseeable future.

-12

-10

-8

-6

-4

-2

0

2

4

6

8

-12

-10

-8

-6

-4

-2

0

2

4

6

8

Mar-09

Feb-09

Jan-0

9

Dec-08

Nov-08

Oct-08

Sep-08

Aug-08

Jul-0

8

Jun-0

8

May-08

Apr-08

Mar-08

Feb-08

Jan-0

8

Dec-07

Nov-07

Oct-07

Sep-07

Aug-07

Jul-0

7

Year

To Y

ear P

erce

nt C

hang

e

Retail sales improved in January and February 2009, marking the first time since mid-2008 that there was a month-to-month improvement in retail sales. However, consumers pulled back in March, and sales dropped from February levels.

Source: Census Bureau.

65

67

69

71

73

75

77

79

81

83

65

67

69

71

73

75

77

79

81

83

Mar-09

Oct-08

May-08

Dec-07

Jul-0

7

Feb-07

Sep-06

Apr-06

Nov-05

Jun-0

5

Jan-0

5

Aug-04

Mar-04

Oct-03

May-03

Dec-02

Jul-0

2

Feb-02

Sep-01

Apr-01

Nov-00

Jun-0

0

Jan-0

0

Perc

ent

Manufacturing utilization has dropped sharply, and remains lower than the levels reached during the 1980s.

Source: Federal Reserve.

Source: Federal Reserve.

Unemployment

GDP

Consumer Price Index

Manufacturing Utilization

FOMC Policy Decisions

Retail Sales

11Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

Mar-09

Sep-08

Mar-08

Sep-07

Mar-07

Sep-06

Mar-06

Sep-05

Mar-05

Sep-04

Mar-04

Sep-03

Mar-03

Sep-02

Mar-02

Sep-01

Mar-01

Mill

ions

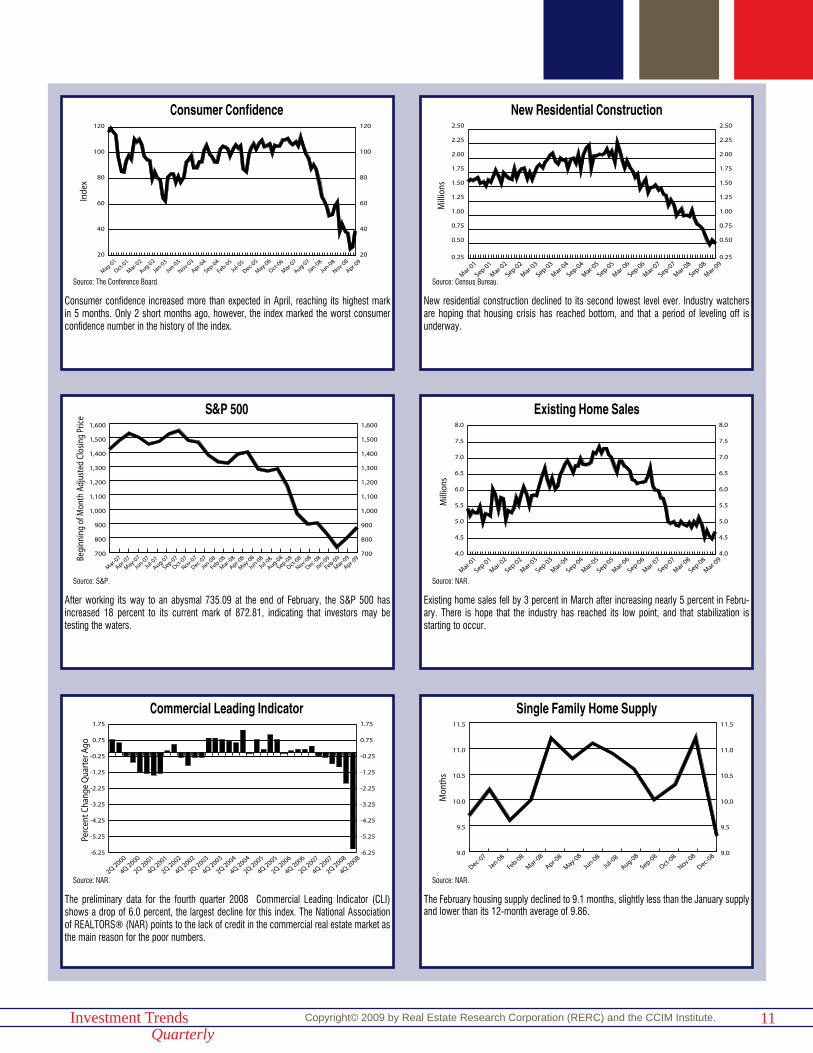

Existing home sales fell by 3 percent in March after increasing nearly 5 percent in Febru-ary. There is hope that the industry has reached its low point, and that stabilization is starting to occur.

Source: NAR.

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

Mar-09

Sep-08

Mar-08

Sep-07

Mar-07

Sep-06

Mar-06

Sep-05

Mar-05

Sep-04

Mar-04

Sep-03

Mar-03

Sep-02

Mar-02

Sep-01

Mar-01

Mill

ions

New residential construction declined to its second lowest level ever. Industry watchers are hoping that housing crisis has reached bottom, and that a period of leveling off is underway.

Source: Census Bureau.

9.0

9.5

10.0

10.5

11.0

11.5

9.0

9.5

10.0

10.5

11.0

11.5

Dec-08

Nov-08

Oct-08

Sep-08

Aug-08

Jul-0

8

Jun-0

8

May-08

Apr-08

Mar-08

Feb-08

Jan-0

8

Dec-07

Mon

ths

The February housing supply declined to 9.1 months, slightly less than the January supply and lower than its 12-month average of 9.86.

Source: NAR.

20

40

60

80

100

120

20

40

60

80

100

120

Apr-09

Nov-08

Jun-0

8

Jan-0

8

Aug-07

Mar-07

Oct-06

May-06

Dec-05

Jul-0

5

Feb-05

Sep-04

Apr-04

Nov-03

Jun-0

3

Jan-0

3

Aug-02

Mar-02

Oct-01

May-01

Inde

x

Consumer confidence increased more than expected in April, reaching its highest mark in 5 months. Only 2 short months ago, however, the index marked the worst consumer confidence number in the history of the index.

-6.25

-5.25

-4.25

-3.25

-2.25

-1.25

-0.25

0.75

1.75

-6.25

-5.25

-4.25

-3.25

-2.25

-1.25

-0.25

0.75

1.75

4Q 2008

2Q 2008

4Q 2007

2Q 2007

4Q 2006

2Q 2006

4Q 2005

2Q 2005

4Q 2004

2Q 2004

4Q 2003

2Q 2003

4Q 2002

2Q 2002

4Q 2001

2Q 2001

4Q 2000

2Q 2000

Perc

ent C

hang

e Q

uart

er A

go

The preliminary data for the fourth quarter 2008 Commercial Leading Indicator (CLI) shows a drop of 6.0 percent, the largest decline for this index. The National Association of REALTORS® (NAR) points to the lack of credit in the commercial real estate market as the main reason for the poor numbers.

Source: NAR.

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

Apr-09

Mar-09

Feb-09

Jan-0

9

Dec-08

Nov-08

Oct-08

Sep-08

Aug-08

Jul-0

8

Jun-0

8

May-08

Apr-08

Mar-08

Feb-08

Jan-0

8

Dec-07

Nov-07

Oct-07

Sep-07

Aug-07

Jul-0

7

Jun-0

7

May-07

Apr-07

Mar-07Be

ginn

ing

of M

onth

Adj

uste

d Cl

osin

g Pr

ice

After working its way to an abysmal 735.09 at the end of February, the S&P 500 has increased 18 percent to its current mark of 872.81, indicating that investors may be testing the waters.

Source: S&P.

Source: The Conference Board.

Consumer Confidence New Residential Construction

S&P 500 Existing Home Sales

Commercial Leading Indicator Single Family Home Supply

12Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

A sustained lack of credit and the economic slump will depress the commercial real estate market this year, according to a forward-looking index and forecast for the commercial real estate sectors published by the National Association of REALTORS® (NAR).

Lawrence Yun, NAR chief economist, said all components of the index declined. “The credit crunch has especially hammered down some components of NAR’s commercial leading indicator,” he said. “A lack of commercial credit is a serious threat to the overall economy. The Federal Reserve needs to use the Term Asset-Backed Securities Loan Facility (TALF) to provide liquidity and support for commercial mortgage-backed securities.”

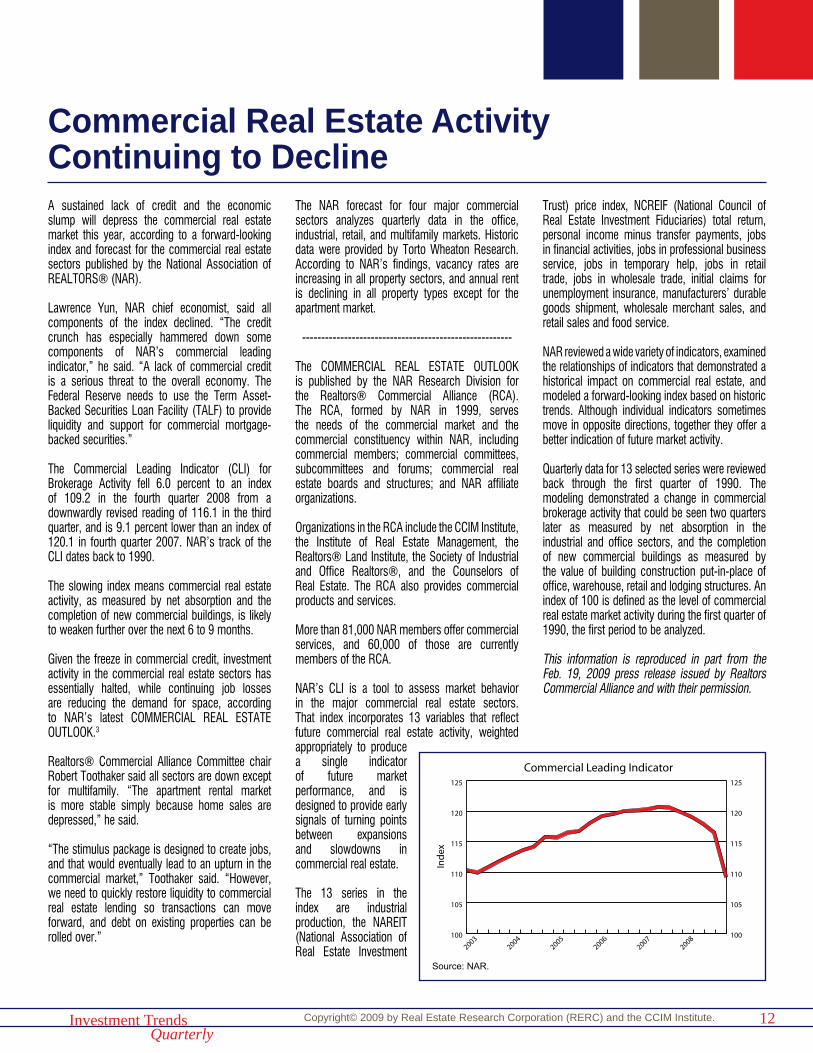

The Commercial Leading Indicator (CLI) for Brokerage Activity fell 6.0 percent to an index of 109.2 in the fourth quarter 2008 from a downwardly revised reading of 116.1 in the third quarter, and is 9.1 percent lower than an index of 120.1 in fourth quarter 2007. NAR’s track of the CLI dates back to 1990.

The slowing index means commercial real estate activity, as measured by net absorption and the completion of new commercial buildings, is likely to weaken further over the next 6 to 9 months.

Given the freeze in commercial credit, investment activity in the commercial real estate sectors has essentially halted, while continuing job losses are reducing the demand for space, according to NAR’s latest COMMERCIAL REAL ESTATE OUTLOOK.3

Realtors® Commercial Alliance Committee chair Robert Toothaker said all sectors are down except for multifamily. “The apartment rental market is more stable simply because home sales are depressed,” he said.

“The stimulus package is designed to create jobs, and that would eventually lead to an upturn in the commercial market,” Toothaker said. “However, we need to quickly restore liquidity to commercial real estate lending so transactions can move forward, and debt on existing properties can be rolled over.”

The NAR forecast for four major commercial sectors analyzes quarterly data in the office, industrial, retail, and multifamily markets. Historic data were provided by Torto Wheaton Research. According to NAR’s findings, vacancy rates are increasing in all property sectors, and annual rent is declining in all property types except for the apartment market.

-------------------------------------------------------

The COMMERCIAL REAL ESTATE OUTLOOK is published by the NAR Research Division for the Realtors® Commercial Alliance (RCA). The RCA, formed by NAR in 1999, serves the needs of the commercial market and the commercial constituency within NAR, including commercial members; commercial committees, subcommittees and forums; commercial real estate boards and structures; and NAR affiliate organizations.

Organizations in the RCA include the CCIM Institute, the Institute of Real Estate Management, the Realtors® Land Institute, the Society of Industrial and Office Realtors®, and the Counselors of Real Estate. The RCA also provides commercial products and services.

More than 81,000 NAR members offer commercial services, and 60,000 of those are currently members of the RCA.

NAR’s CLI is a tool to assess market behavior in the major commercial real estate sectors. That index incorporates 13 variables that reflect future commercial real estate activity, weighted appropriately to produce a single indicator of future market performance, and is designed to provide early signals of turning points between expansions and slowdowns in commercial real estate.

The 13 series in the index are industrial production, the NAREIT (National Association of Real Estate Investment

Trust) price index, NCREIF (National Council of Real Estate Investment Fiduciaries) total return, personal income minus transfer payments, jobs in financial activities, jobs in professional business service, jobs in temporary help, jobs in retail trade, jobs in wholesale trade, initial claims for unemployment insurance, manufacturers’ durable goods shipment, wholesale merchant sales, and retail sales and food service.

NAR reviewed a wide variety of indicators, examined the relationships of indicators that demonstrated a historical impact on commercial real estate, and modeled a forward-looking index based on historic trends. Although individual indicators sometimes move in opposite directions, together they offer a better indication of future market activity.

Quarterly data for 13 selected series were reviewed back through the first quarter of 1990. The modeling demonstrated a change in commercial brokerage activity that could be seen two quarters later as measured by net absorption in the industrial and office sectors, and the completion of new commercial buildings as measured by the value of building construction put-in-place of office, warehouse, retail and lodging structures. An index of 100 is defined as the level of commercial real estate market activity during the first quarter of 1990, the first period to be analyzed.

This information is reproduced in part from the Feb. 19, 2009 press release issued by Realtors Commercial Alliance and with their permission.

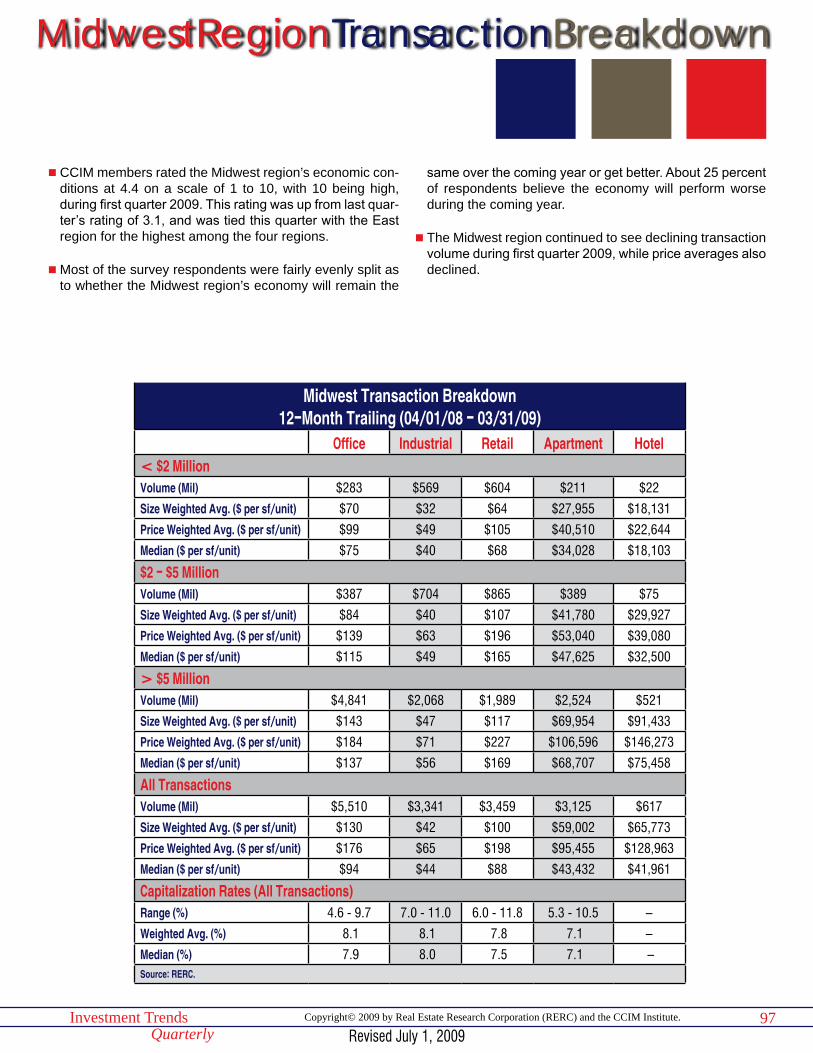

Commercial Real Estate ActivityContinuing to Decline

100

105

110

115

120

125

100

105

110

115

120

125

20082007

20062005

20042003

Ind

ex

Commercial Leading Indicator

Source: NAR.

13Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

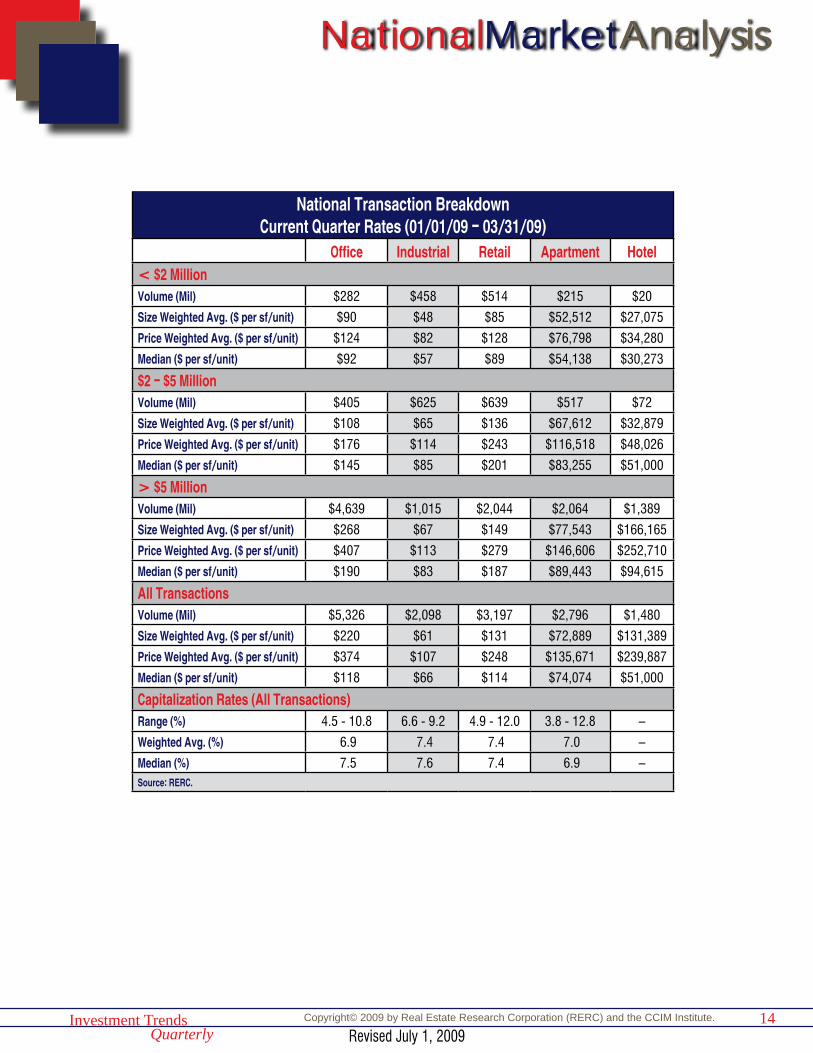

NationalMarketAnalysis

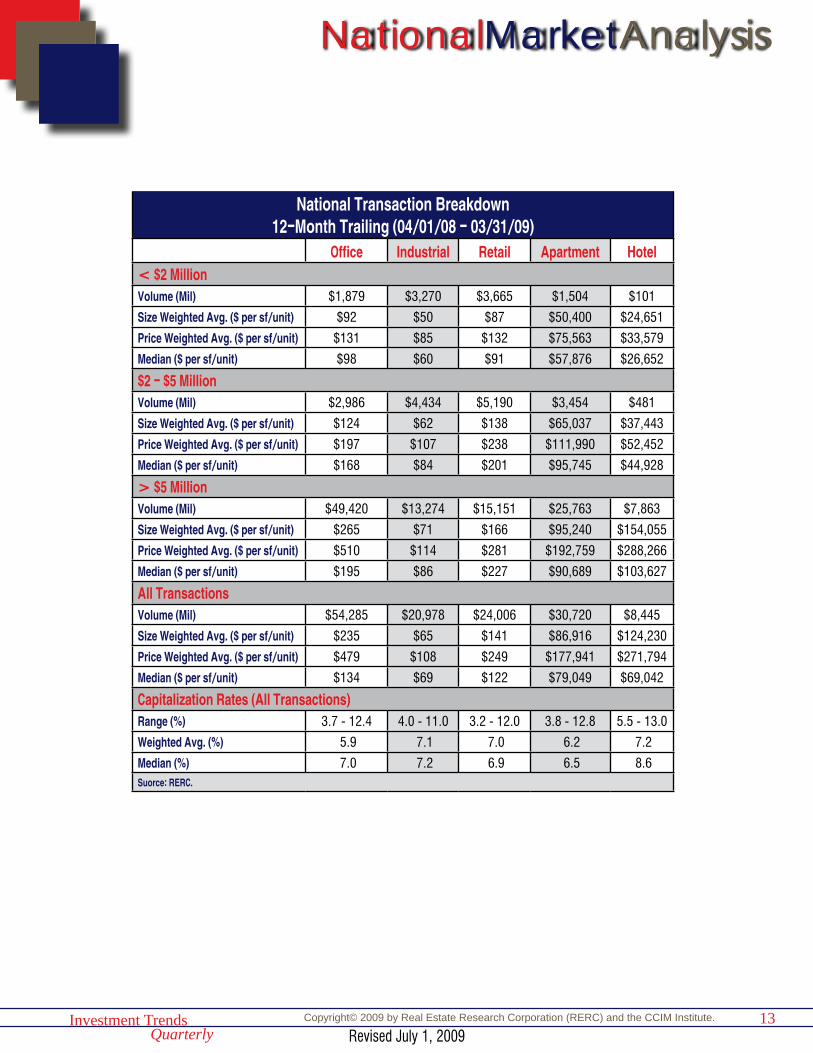

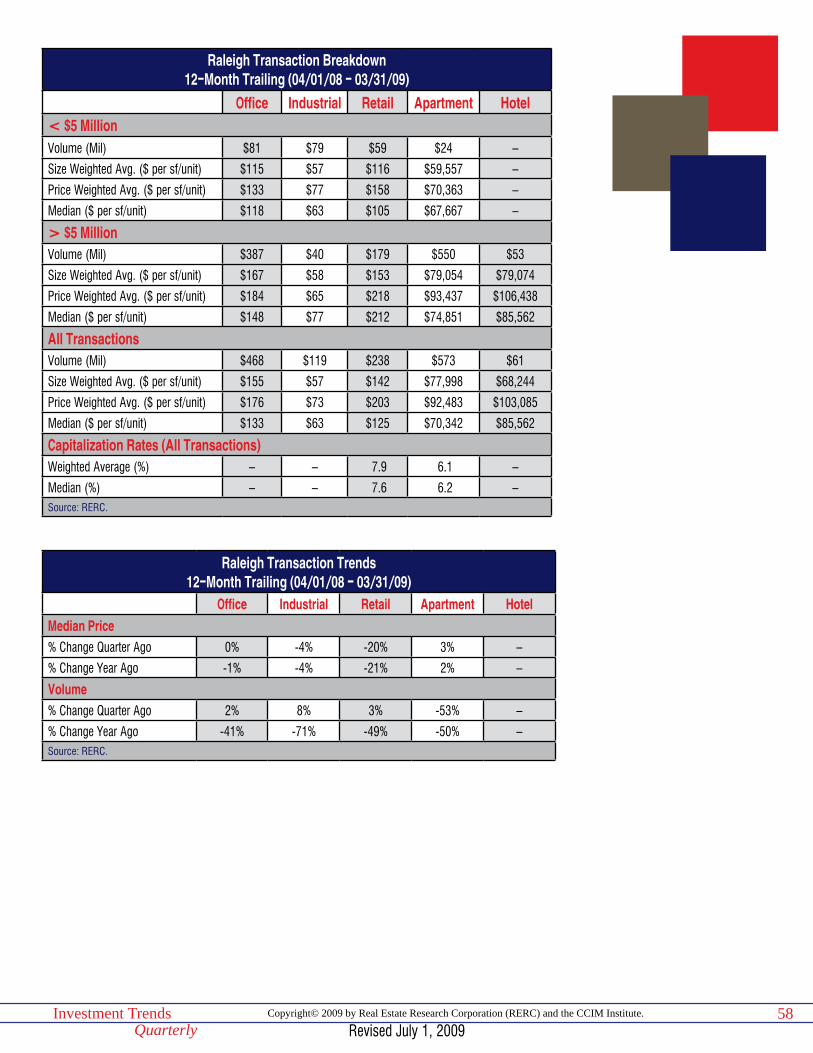

National Transaction Breakdown12-Month Trailing (04/01/08 - 03/31/09)

Office Industrial Retail Apartment Hotel< $2 MillionVolume (Mil) $1,879 $3,270 $3,665 $1,504 $101

Size Weighted Avg. ($ per sf/unit) $92 $50 $87 $50,400 $24,651

Price Weighted Avg. ($ per sf/unit) $131 $85 $132 $75,563 $33,579

Median ($ per sf/unit) $98 $60 $91 $57,876 $26,652

$2 - $5 MillionVolume (Mil) $2,986 $4,434 $5,190 $3,454 $481

Size Weighted Avg. ($ per sf/unit) $124 $62 $138 $65,037 $37,443

Price Weighted Avg. ($ per sf/unit) $197 $107 $238 $111,990 $52,452

Median ($ per sf/unit) $168 $84 $201 $95,745 $44,928

> $5 MillionVolume (Mil) $49,420 $13,274 $15,151 $25,763 $7,863

Size Weighted Avg. ($ per sf/unit) $265 $71 $166 $95,240 $154,055

Price Weighted Avg. ($ per sf/unit) $510 $114 $281 $192,759 $288,266

Median ($ per sf/unit) $195 $86 $227 $90,689 $103,627

All TransactionsVolume (Mil) $54,285 $20,978 $24,006 $30,720 $8,445

Size Weighted Avg. ($ per sf/unit) $235 $65 $141 $86,916 $124,230

Price Weighted Avg. ($ per sf/unit) $479 $108 $249 $177,941 $271,794

Median ($ per sf/unit) $134 $69 $122 $79,049 $69,042

Capitalization Rates (All Transactions)Range (%) 3.7 - 12.4 4.0 - 11.0 3.2 - 12.0 3.8 - 12.8 5.5 - 13.0

Weighted Avg. (%) 5.9 7.1 7.0 6.2 7.2

Median (%) 7.0 7.2 6.9 6.5 8.6 Suorce: RERC.

Revised July 1, 2009

14Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

NationalMarketAnalysis

National Transaction BreakdownCurrent Quarter Rates (01/01/09 - 03/31/09)

Office Industrial Retail Apartment Hotel< $2 MillionVolume (Mil) $282 $458 $514 $215 $20

Size Weighted Avg. ($ per sf/unit) $90 $48 $85 $52,512 $27,075

Price Weighted Avg. ($ per sf/unit) $124 $82 $128 $76,798 $34,280

Median ($ per sf/unit) $92 $57 $89 $54,138 $30,273

$2 - $5 MillionVolume (Mil) $405 $625 $639 $517 $72

Size Weighted Avg. ($ per sf/unit) $108 $65 $136 $67,612 $32,879

Price Weighted Avg. ($ per sf/unit) $176 $114 $243 $116,518 $48,026

Median ($ per sf/unit) $145 $85 $201 $83,255 $51,000

> $5 MillionVolume (Mil) $4,639 $1,015 $2,044 $2,064 $1,389

Size Weighted Avg. ($ per sf/unit) $268 $67 $149 $77,543 $166,165

Price Weighted Avg. ($ per sf/unit) $407 $113 $279 $146,606 $252,710

Median ($ per sf/unit) $190 $83 $187 $89,443 $94,615

All TransactionsVolume (Mil) $5,326 $2,098 $3,197 $2,796 $1,480

Size Weighted Avg. ($ per sf/unit) $220 $61 $131 $72,889 $131,389

Price Weighted Avg. ($ per sf/unit) $374 $107 $248 $135,671 $239,887

Median ($ per sf/unit) $118 $66 $114 $74,074 $51,000

Capitalization Rates (All Transactions)Range (%) 4.5 - 10.8 6.6 - 9.2 4.9 - 12.0 3.8 - 12.8 –

Weighted Avg. (%) 6.9 7.4 7.4 7.0 –

Median (%) 7.5 7.6 7.4 6.9 –Source: RERC.

Revised July 1, 2009

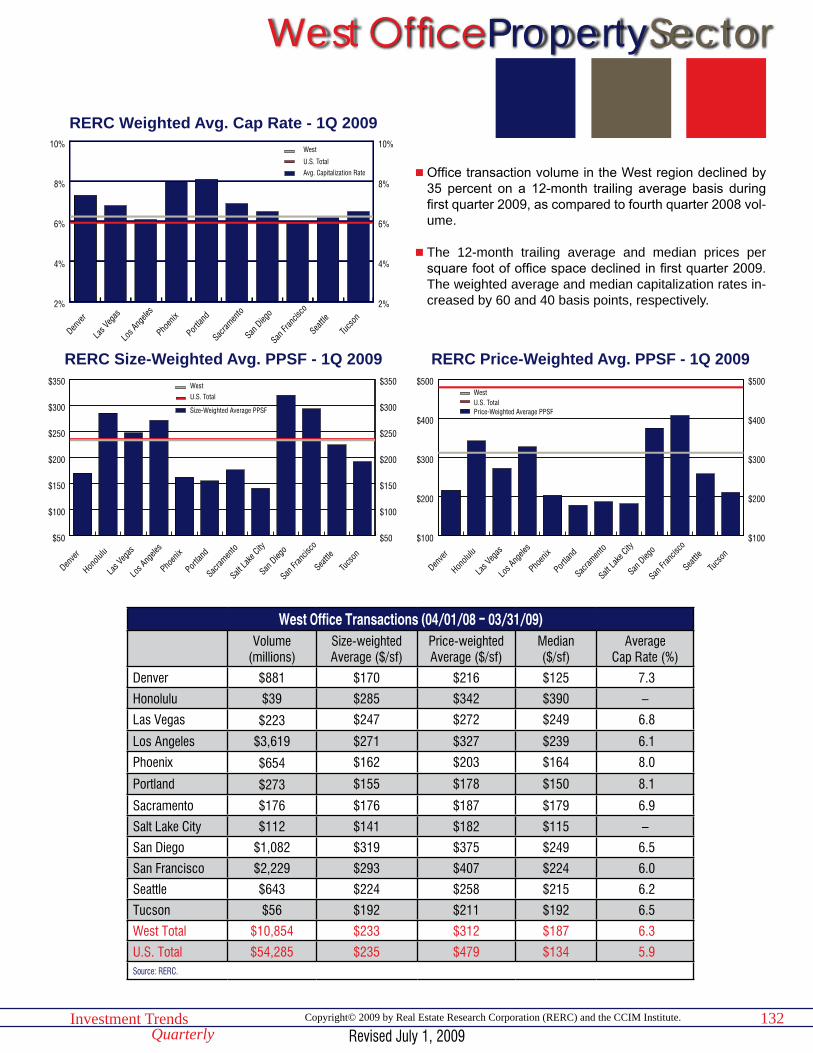

OfficePropertySector

15Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

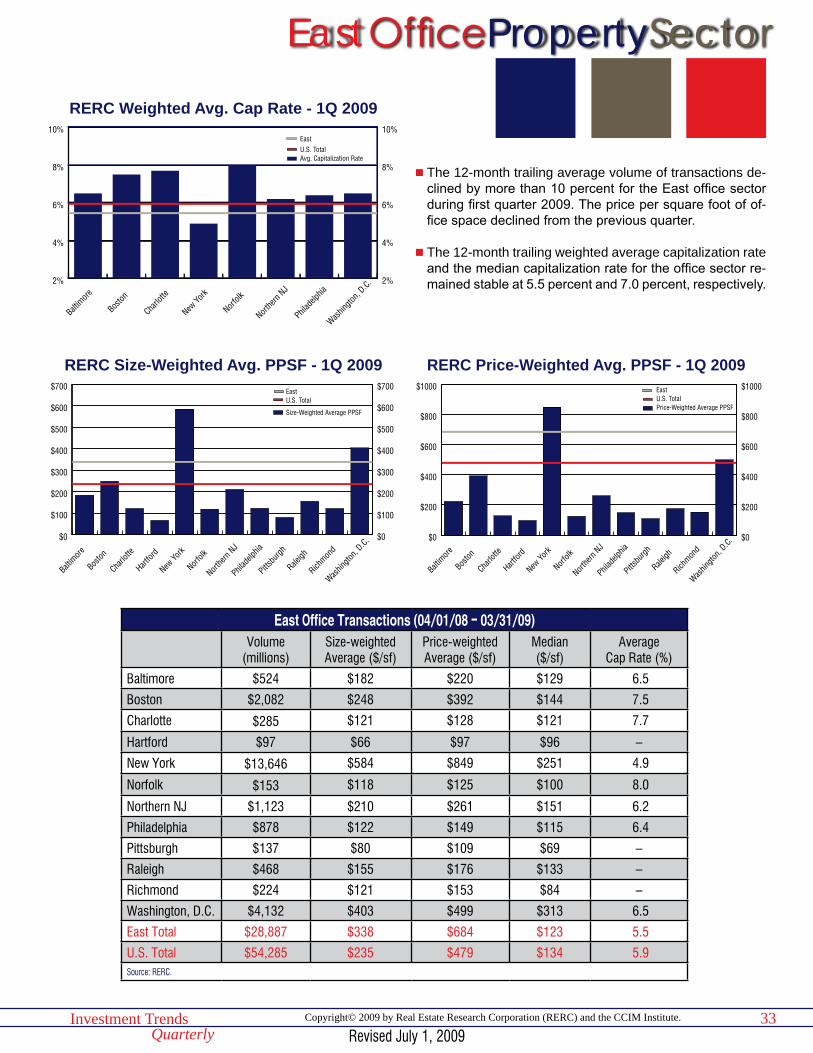

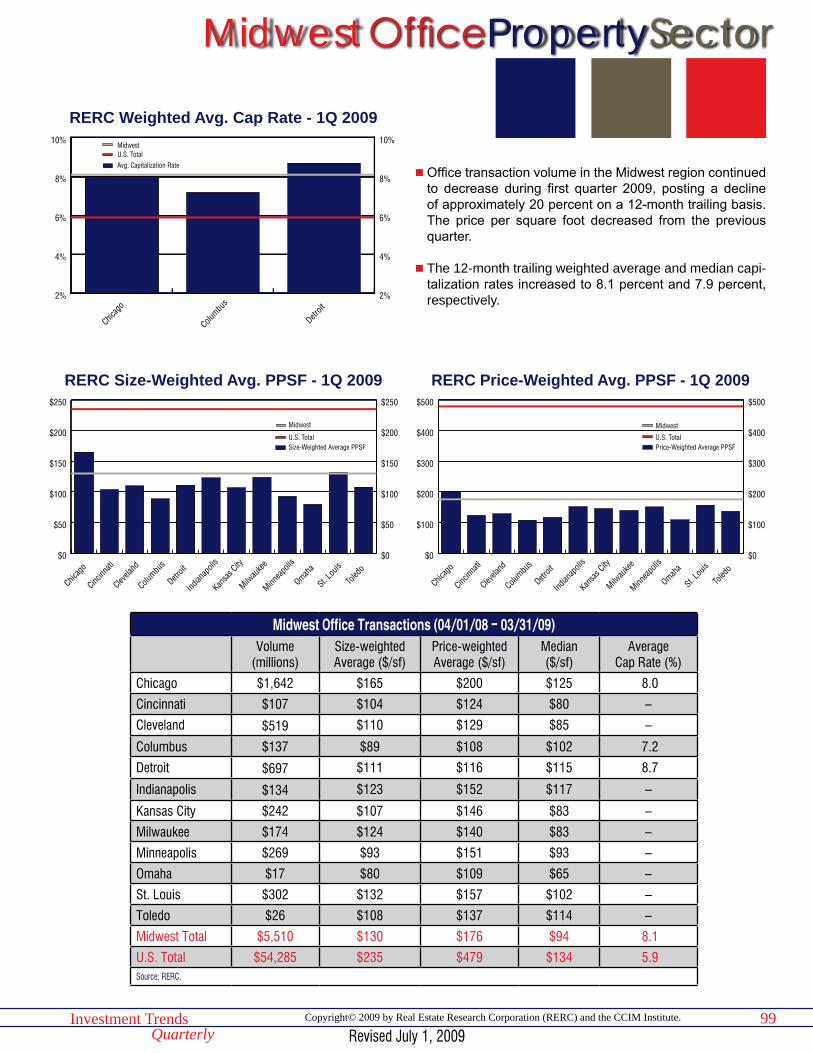

w During first quarter 2009, CCIM designees and candidates who responded to RERC’s survey rated the office sector’s investment conditions rating at 3.7 on a scale of 1 to 10, with 10 being high. The office sector’s rating had been declining since fourth quarter 2007, until this quarter’s in-crease reversed trend.

w RERC’s transaction analysis of the 12-month trailing aver-ages showed continuing declines in the office sector dur-ing first quarter 2009. The volume of transactions contin-ued to slow, while the size-weighted average and median price per square foot fell from last quarter. The weighted average capitalization rate remained stable, while the me-dian capitalization rate increased slightly.

w The return versus risk rating in the office sector increased to 4.6 on a scale of 1 to 10, with 10 being high, during first quarter 2009. This rating tied for the second lowest rating with the hotel sector. The value versus price rating increased to 4.8, up from 4.3 during the previous quarter.

w According to Torto Wheaton Research, the overall vacan-cy rate for the office sector increased by 70 basis points to 14.7 percent during first quarter 2009. The office market posted negative net absorption at a level not seen since fourth quarter 2001.

4%

5%

6%

7%

8%

9%

4%

5%

6%

7%

8%

9%NationalWest

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Weighted Average Capitalization Rate(12-Month Trailing Average)

$100

$200

$300

$400

$500

$600

$700

$800

$100

$200

$300

$400

$500

$600

$700

$800

National

WestMidwestSouthEast

1Q094Q083Q082Q081Q08

RERC Price-Weighted Average PPSF(12-Month Trailing Average)

$100

$150

$200

$250

$300

$350

$400

$100

$150

$200

$250

$300

$350

$400NationalWest

MidwestSouth

East

1Q094Q083Q082Q081Q08

RERC Size-Weighted Average PPSF(12-Month Trailing Average)

OfficeOfficeNational

Most respondents suggested avoiding office property investments for the next year due to “overbuilding, downward pressure on rents, increasing vacancy, and general oversupply.” However, several respondents noted that there are some “small and mid-sized office properties available at great prices in some areas, and if financing becomes available, these kinds of office properties will be a good value.”

Revised July 1, 2009

16Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

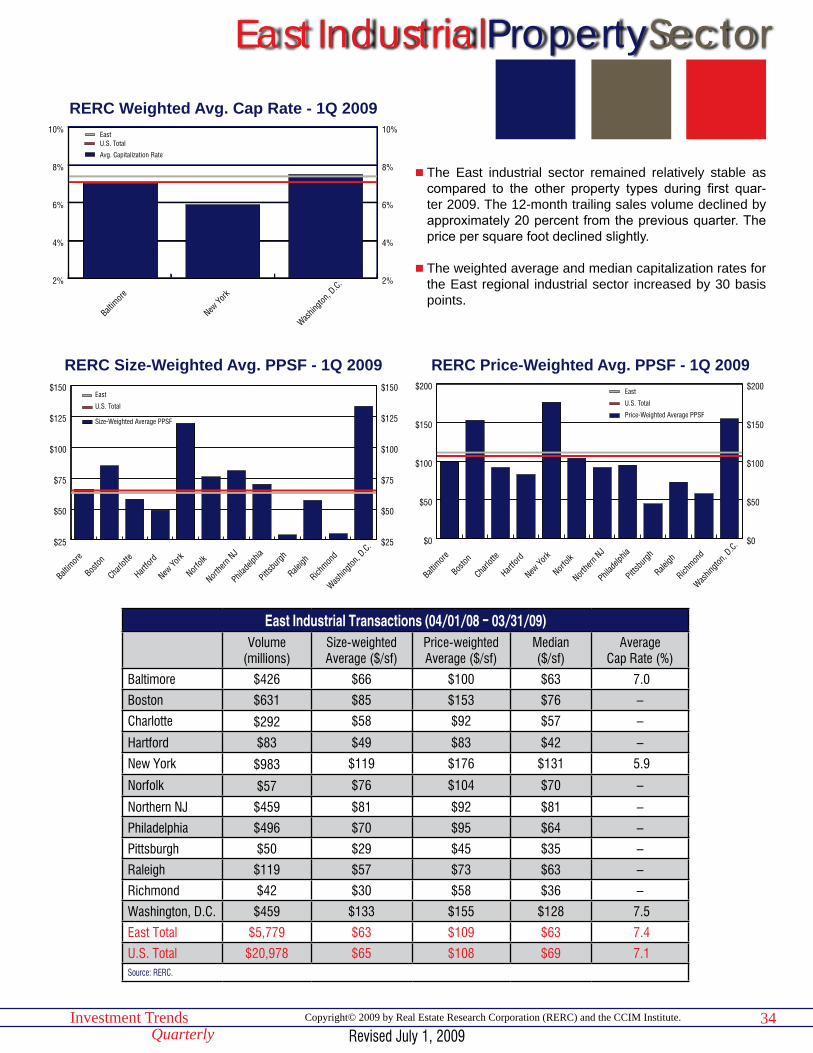

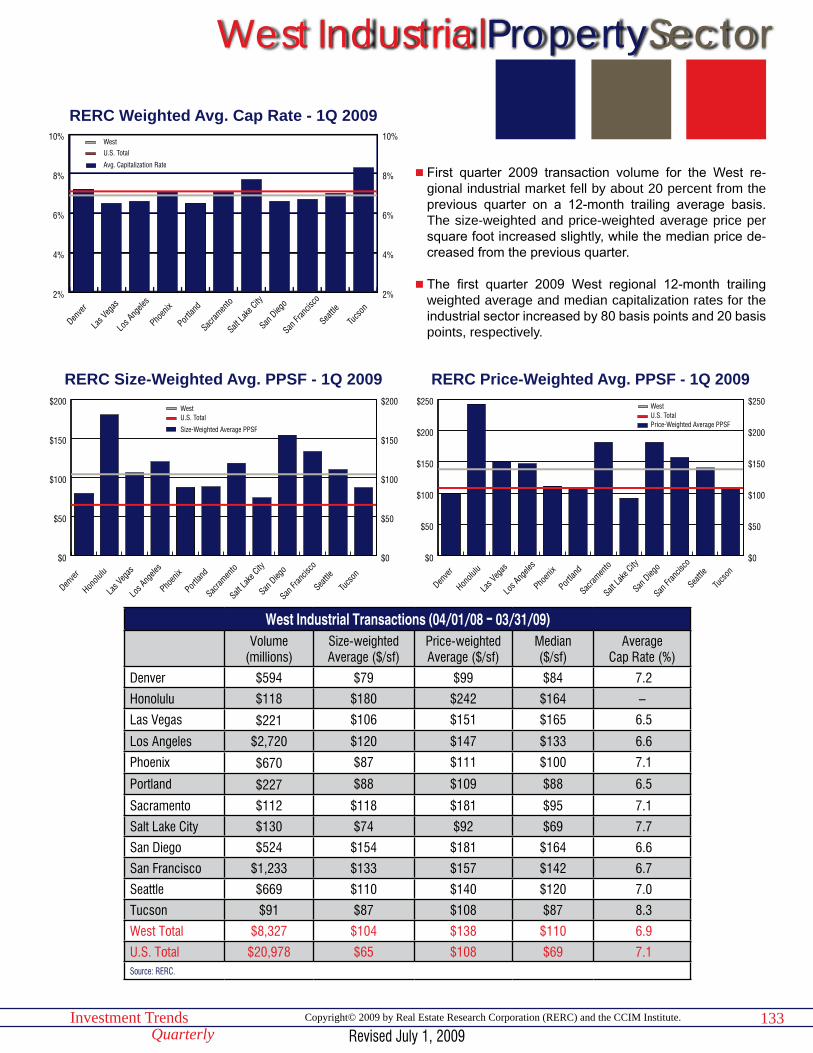

IndustrialPropertySector

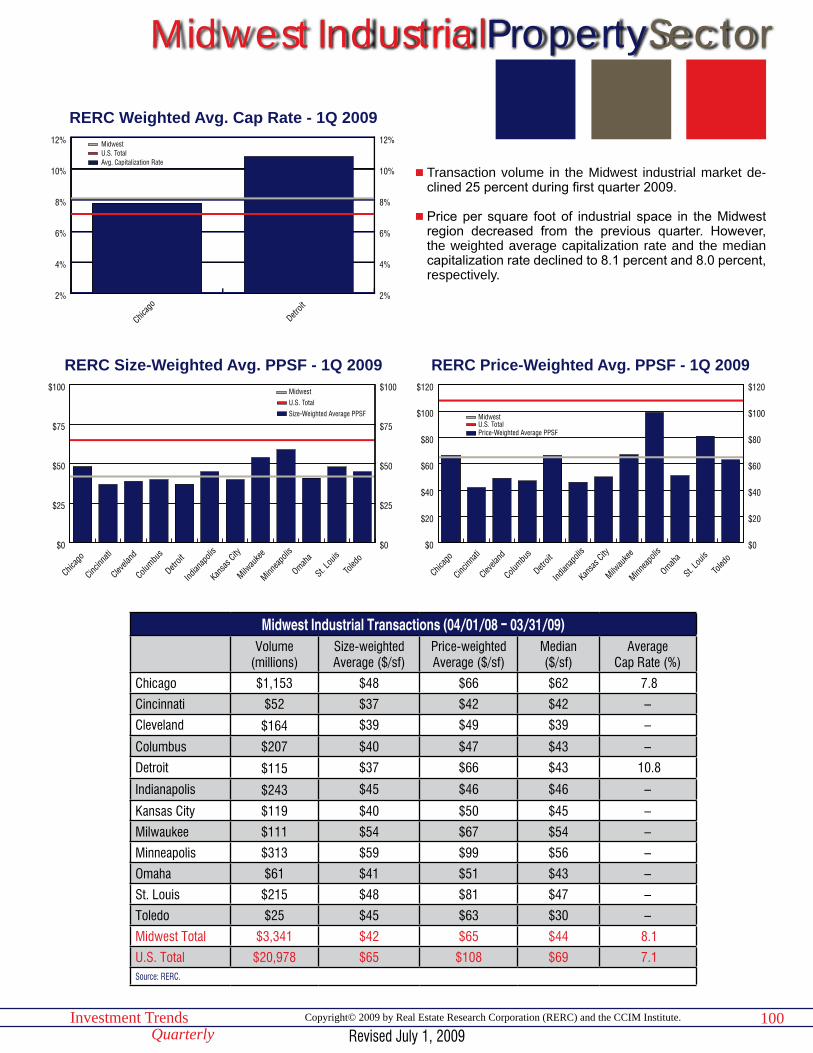

w CCIM survey respondents rated the investment conditions of the industrial sector at 4.4 on a scale of 1 to 10, with 10 being high, during first quarter 2009. The industrial sec-tor received the second highest rating among the property types.

w RERC’s transaction analysis for the industrial sector showed slightly lower average prices for first quarter 2009. The weighted average capitalization rate increased by 40 basis points to 7.1 percent, while the median capitalization rate increased by 20 basis points.

w The industrial sector received a return versus risk rating of 5.3 on a scale of 1 to 10, with 10 being high, during first quarter 2009, tying for the second highest rating among the property types. The value versus price for the industrial sector was rated at 5.4, indicating the value of the proper-ties outweighs the price.

w The overall availability rate for industrial space increased by 80 basis points to 12.2 percent during first quarter 2009. According to Torto Wheaton Research, this is a higher availability rate than that noted during the last two recessions, and is the highest since Torto Wheaton began tracking data for the industrial sector in 1989.

5%

6%

7%

8%

9%

10%

5%

6%

7%

8%

9%

10%NationalWest

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Weighted Average Capitalization Rate(12-Month Trailing Average)

$0

$50

$100

$150

$200

$0

$50

$100

$150

$200NationalWest

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Price-Weighted Average PPSF(12-Month Trailing Average)

$40

$60

$80

$100

$120

$140

$40

$60

$80

$100

$120

$140NationalWest

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Size-Weighted Average PPSF(12-Month Trailing Average)

National

Industrial may be a good sector in which to invest due to pent-up demand in some areas, and “more focus from Congress on U.S. manufacturing and less on off-shore manufacturing.” Long-term industrial may offer good opportunities because the sector has the “shortest ramp-up time” and “requires little capital, high going-in cap rates=instant returns, and a more stable tenant base.” However, in some areas, industrial “still seems to be flat-lining.”

Revised July 1, 2009

17Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

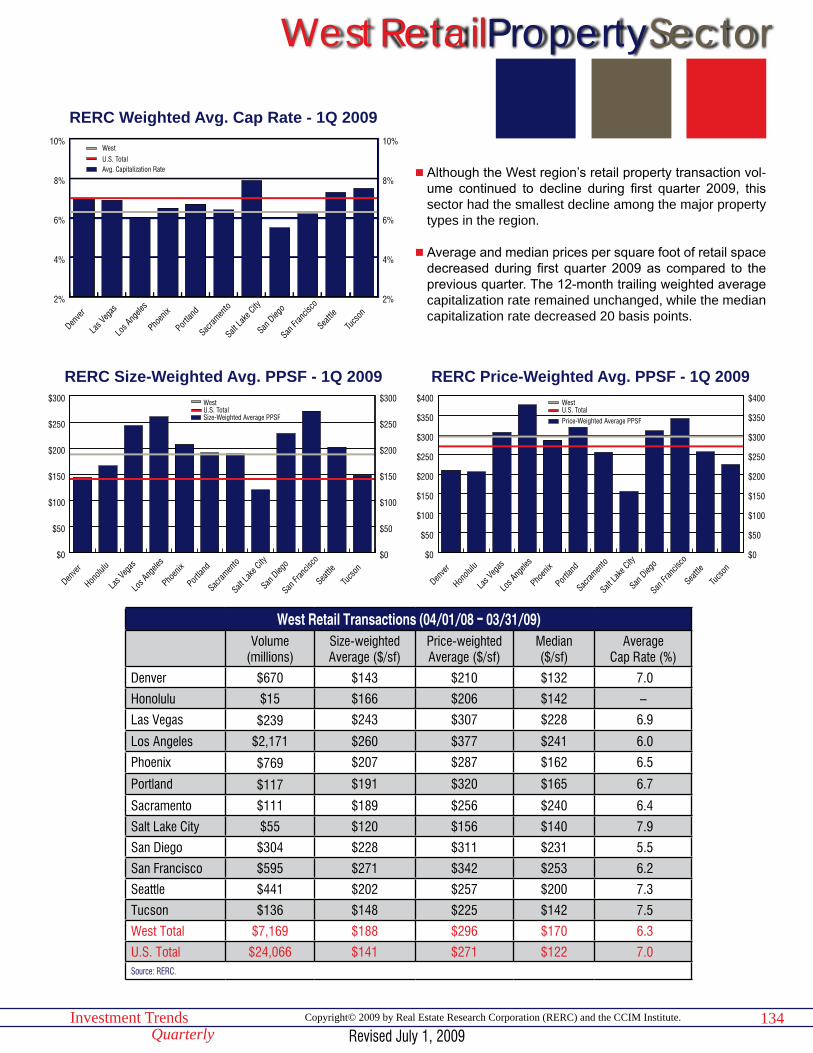

RetailPropertySector

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%NationalWest

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Weighted Average Capitalization Rate(12-Month Trailing Average)

$100

$150

$200

$250

$300

$350

$400

$100

$150

$200

$250

$300

$350

$400NationalWest

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Price-Weighted Average PPSF(12-Month Trailing Average)

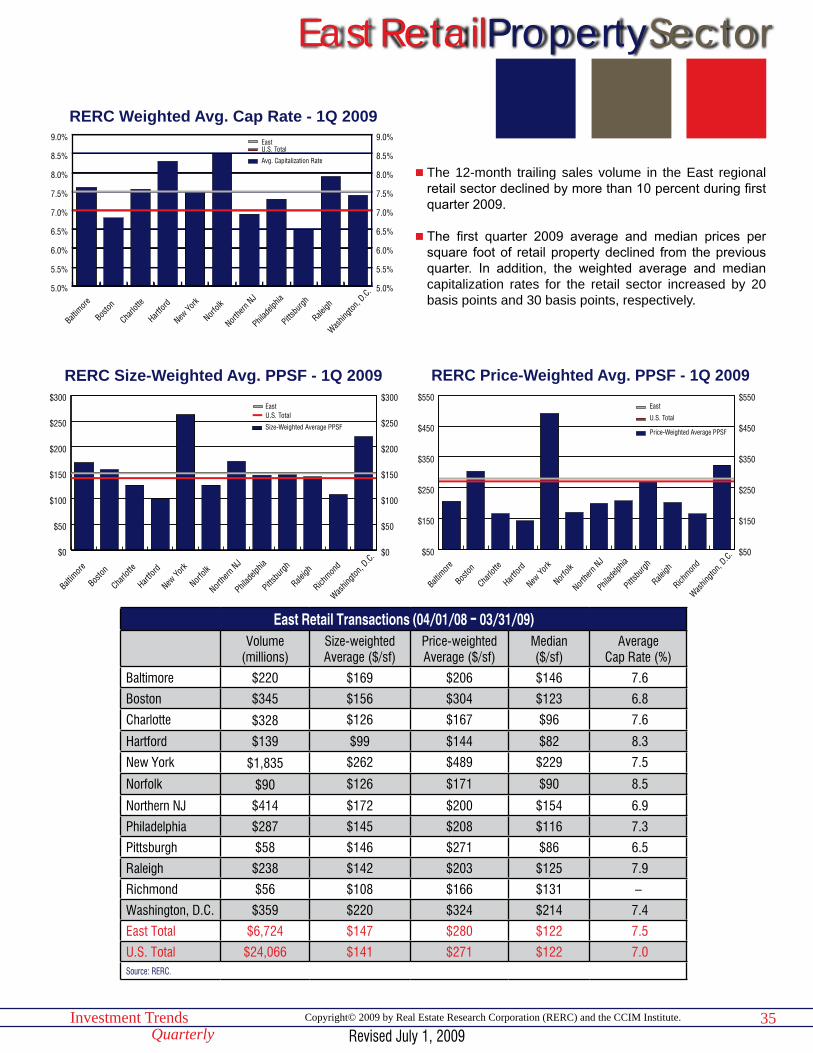

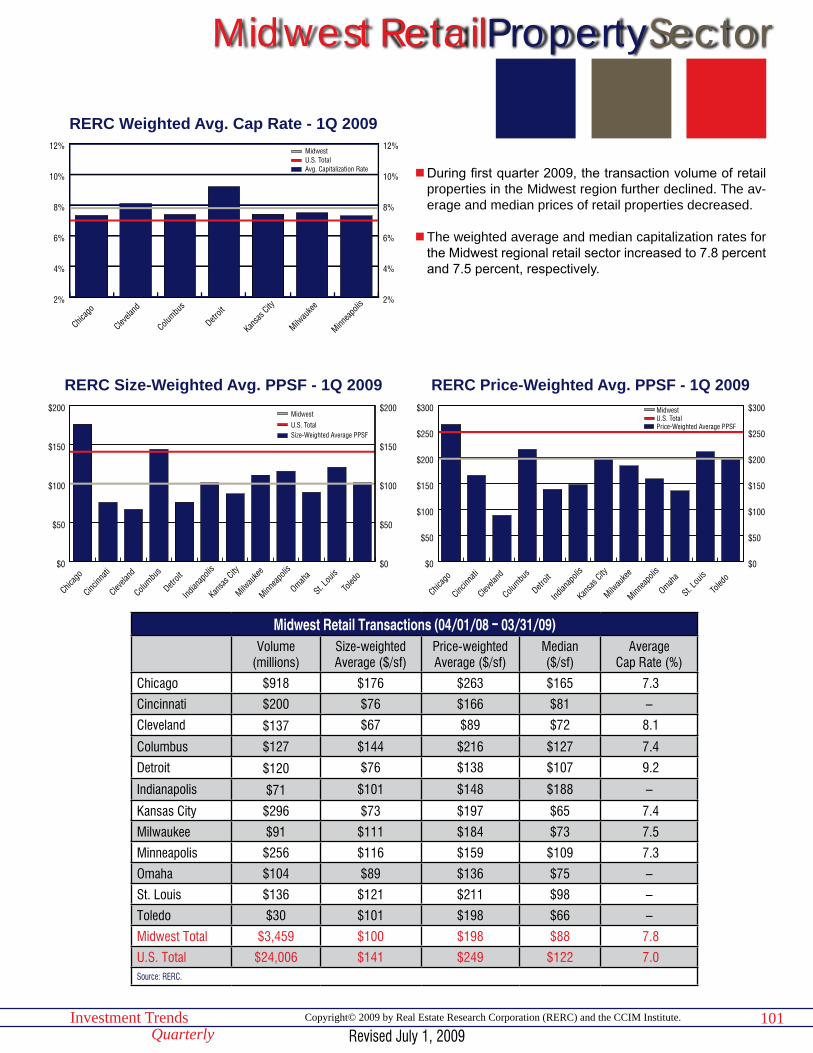

w CCIM designees and candidates who responded to RERC’s investment survey gave the retail sector an in-vestment conditions rating of 3.4 on a scale of 1 to 10, with 10 being high, during first quarter 2009, which was the lowest rating among the property types.

w According to RERC’s transaction analysis, the decline in volume for retail transactions is beginning to slow. The 12-month size- and price-weighted averages and median price per square foot declined from the previous quarter, while the weighted average capitalization rate increased by 60 basis points to 7.2 percent.

w The retail availability rate increased by 50 basis points to 10.4 percent during fourth quarter 2008, according to Torto Wheaton Research. This was the ninth consecutive quar-ter of increased availability in the retail sector. Net absorp-tion was negative for the second quarter in a row.

w The retail sector received a return versus risk rating of 4.0 on a scale of 1 to 10, with 10 being high, during first quar-ter 2009. Even though this rating was the lowest of all the property types, it was an increase from the previous quar-ter’s rating of 3.3. The value versus price rating increased to 4.5, and indicates that investors still believe the value of the properties is lower than the price being asked.

$50

$100

$150

$200

$250

$50

$100

$150

$200

$250NationalWest

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Size-Weighted Average PPSF(12-Month Trailing Average)

National

Most survey respondents remarked that the retail sector should be avoided during the next year because “tenants have not seen the bottom yet for their retail businesses” and “even the big tenants are weak.” However, there are opportunities, particularly in areas with “properties available at 50 to 70 cents on the dollar” or with “owners with cash flow problems who will be forced to sell.”

Revised July 1, 2009

18Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

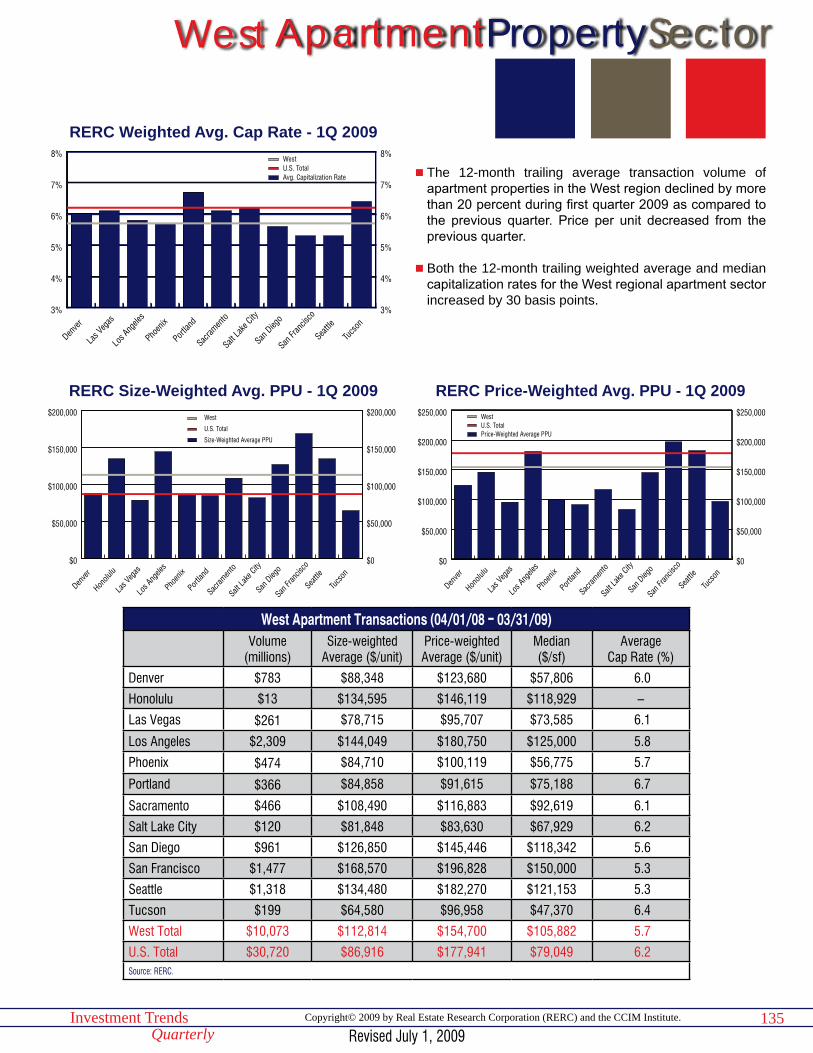

ApartmentPropertySector

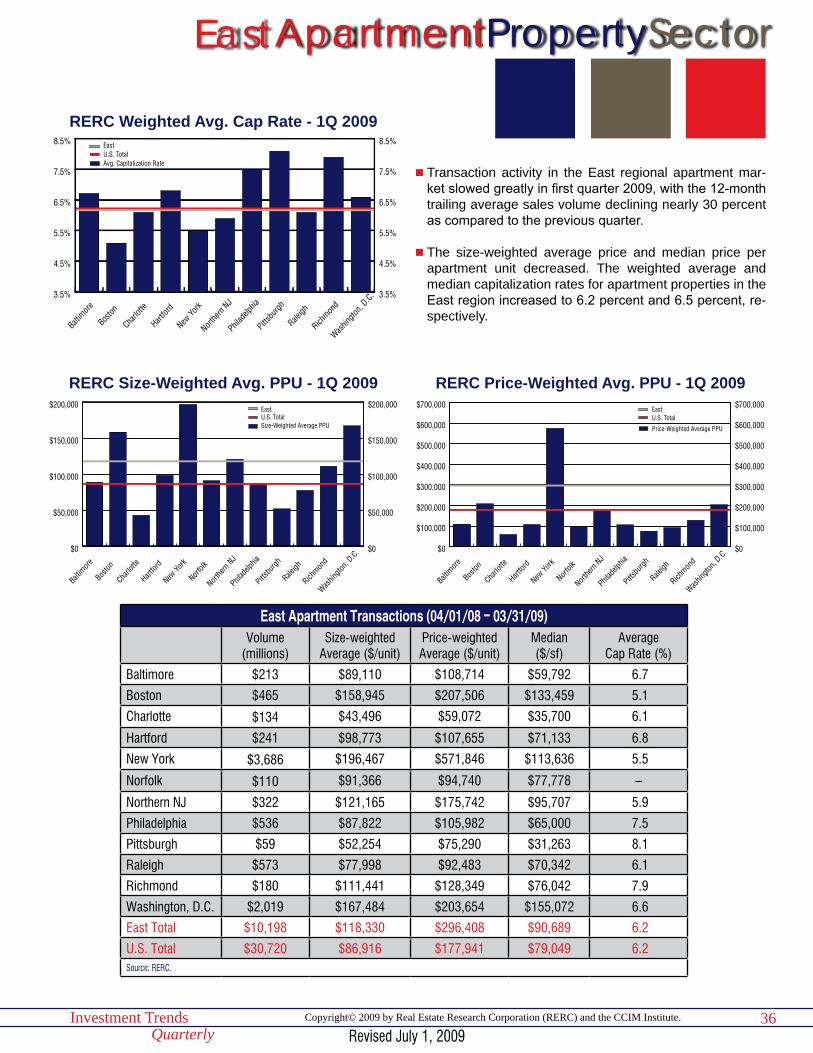

w CCIM survey respondents gave the apartment sector an investment conditions rating of 5.5 on a scale of 1 to 10, with 10 being high, during first quarter 2009. While the apartment sector was the only property type to be rated lower than the previous quarter, it still received the highest rating among the property types during first quarter.

w RERC’s 12-month trailing transaction analysis for first quarter 2009 showed that the volume of transactions de-clined by approximately 25 percent from the previous quar-ter. The size-weighted average and median prices per unit decreased slightly. The weighted average capitalization rate increased by 60 basis points to 6.2 percent, while the median capitalization rate increased 50 basis points to 6.5 percent.

w According to Reis, Inc., the average vacancy rate for the apartment sector increased by 60 basis points to 7.2 per-cent during first quarter 2009. This is the fifth consecutive quarterly increase in apartment vacancy rates. Net absorp-tion was negative for the second consecutive quarter.

w CCIM survey respondents gave the apartment sector a return versus risk rating of 6.3 on a scale of 1 to 10, with 10 being high, which was up from the previous quarter’s rating of 5.8. This rating indicates the respondents believe the return on apartment properties is greater than the risk involved. The value versus price was rated at 5.2, indicat-ing respondents feel the value of apartment properties only slightly outweighs the price paid.

4.5%

5.5%

6.5%

7.5%

8.5%

4.5%

5.5%

6.5%

7.5%

8.5%NationalWest

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Weighted Average Capitalization Rate(12-Month Trailing Average)

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000NationalWest

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Price-Weighted Average PPU(12-Month Trailing Average)

$50,000

$75,000

$100,000

$125,000

$150,000

$50,000

$75,000

$100,000

$125,000

$150,000NationalWest

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Size-Weighted Average PPU(12-Month Trailing Average)

ApartmentApartmentNational

“Apartments will do well because the home foreclosure market will drive rents up” and because of their “overall stability, occupancy, and NOI.” Apartments are expected to “lead the pack if prices come into line with lenders’ requirements.” However, in some areas, like Phoenix, “too much shadow space from single-family homes is affecting occupancy.”

Revised July 1, 2009

19Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

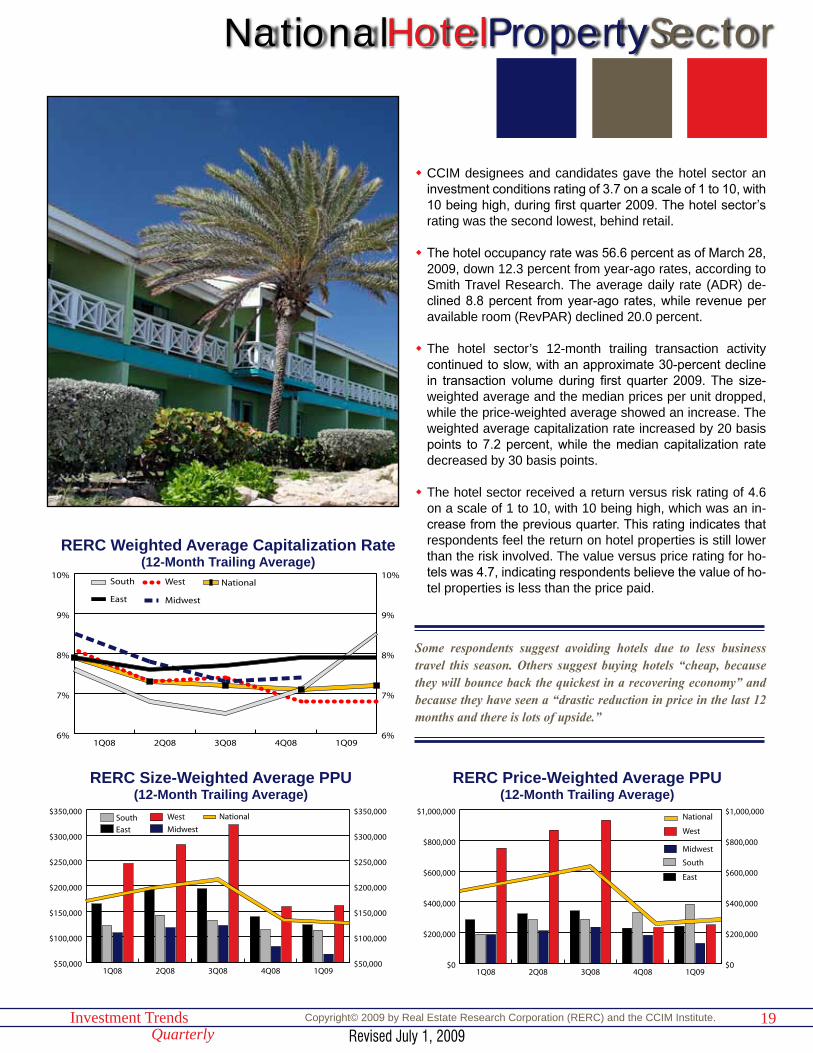

HotelPropertySector

w CCIM designees and candidates gave the hotel sector an investment conditions rating of 3.7 on a scale of 1 to 10, with 10 being high, during first quarter 2009. The hotel sector’s rating was the second lowest, behind retail.

w The hotel occupancy rate was 56.6 percent as of March 28, 2009, down 12.3 percent from year-ago rates, according to Smith Travel Research. The average daily rate (ADR) de-clined 8.8 percent from year-ago rates, while revenue per available room (RevPAR) declined 20.0 percent.

w The hotel sector’s 12-month trailing transaction activity continued to slow, with an approximate 30-percent decline in transaction volume during first quarter 2009. The size-weighted average and the median prices per unit dropped, while the price-weighted average showed an increase. The weighted average capitalization rate increased by 20 basis points to 7.2 percent, while the median capitalization rate decreased by 30 basis points.

w The hotel sector received a return versus risk rating of 4.6 on a scale of 1 to 10, with 10 being high, which was an in-crease from the previous quarter. This rating indicates that respondents feel the return on hotel properties is still lower than the risk involved. The value versus price rating for ho-tels was 4.7, indicating respondents believe the value of ho-tel properties is less than the price paid.

6%

7%

8%

9%

10%

6%

7%

8%

9%

10%NationalWest

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Weighted Average Capitalization Rate(12-Month Trailing Average)

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000National

West

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Price-Weighted Average PPU(12-Month Trailing Average)

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000NationalWest

Midwest

South

East

1Q094Q083Q082Q081Q08

RERC Size-Weighted Average PPU(12-Month Trailing Average)

National

Some respondents suggest avoiding hotels due to less business travel this season. Others suggest buying hotels “cheap, because they will bounce back the quickest in a recovering economy” and because they have seen a “drastic reduction in price in the last 12 months and there is lots of upside.”

Revised July 1, 2009

20Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

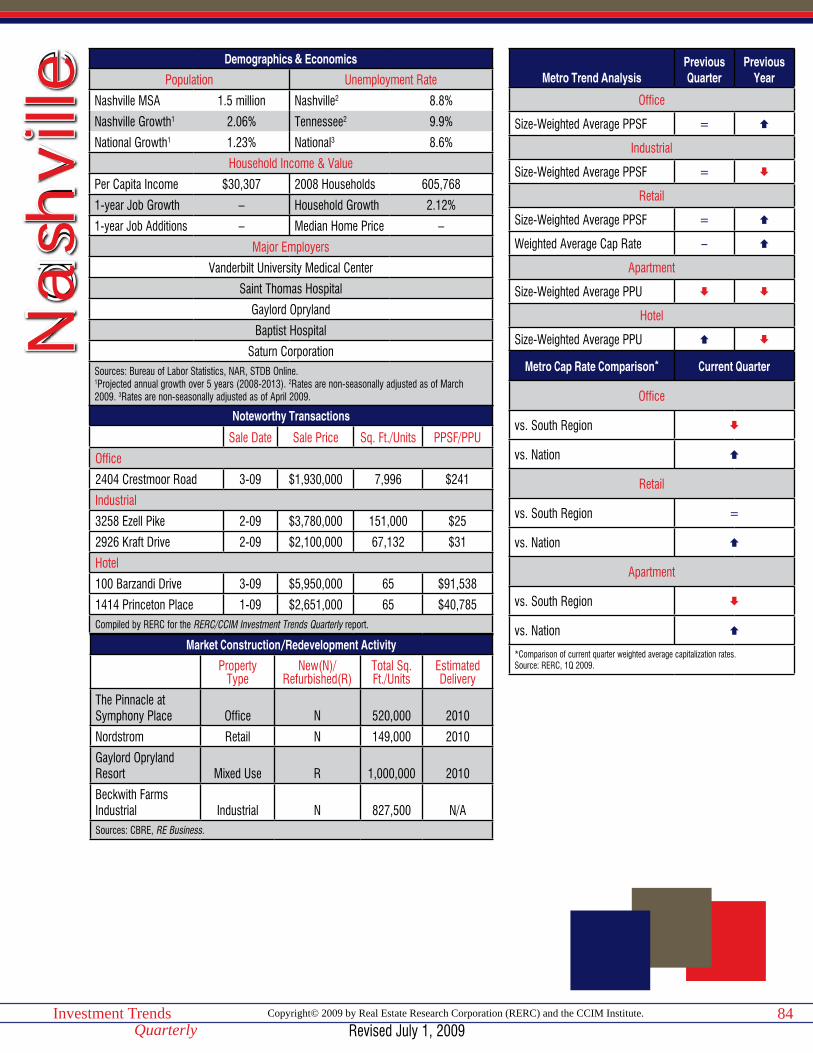

The first verse from an old hit song called “Nashville Cats” starts this way: “Well, there’s thirteen hundred and fifty two guitar pickers in Nashville.” Recorded by the Lovin’ Spoonful in 1966, the country-themed tune was a somewhat tongue-in-cheek tribute to the Tennessee capitol city and its tre-mendous output of live and recorded country music.

Home to the legendary Grand Ole Opry, Nashville has been the undis-

puted seat of country and its various musical offshoots for decades. In the years following World War II, music pioneers opened small studios along Sixteenth Avenue South on what would be later dubbed “Music Row.” Major record companies like RCA, Decca, and Columbia followed, as did publishing houses, music licensing firms, and other business that served the music industry. Radio networks and radio stations began broadcasts. Giants like Elvis Presley, Chet Atkins, and the Everly Brothers recorded seminal tracks there. Music City was born, and it still lives.

Today, Nashville remains one of the nation’s three music industry meccas, and the vibrant scene draws thou-sands of music fans and professionals from coast to coast, thus contributing to the local economy and preserving a big part of the city’s character. Beyond

the studios and honky tonks, there’s a lot more going on in this progressive, mid-South metropolis.

The seat of Tennessee government, Nashville benefits economically from steady state jobs as well as travel/tourism dollars. Thanks to a strong central city-county government, effec-tive economic development practices, dynamic economic drivers through healthcare, technology, and educa-

By Edward M. Bury, APR

Nashville Tunes inNew Economic Growth...

Beyond the Music

Right:Tennessee

State Capitol

Above: Nashville Music District

21Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

tional institutions (there are seven major colleges and universities), over-all affordability, and a central location, Music City dances to a lot of tunes these days and has evolved into a di-verse business center.

According to national publications, Nashville and the state of Tennessee are great places for business. Forbes ranked Nashville as the 25th best U.S. market for career and business growth, and Site Selection magazine, a leading economic develop-ment journal, ranked Tennes-see as having the second-best business climate in the nation. And, Expansion Management ranked Nashville number one in its “50 Hottest Cities” poll for business expansion—for the second consecutive year.

Solid local government is a key reason for the region’s econom-ic success. The metro area of 1.5 million is under the admin-istration of the Metropolitan Government of Nashville and Davidson County, which is com-prised of an elected mayor and Metropolitan Council. Formed in 1963, the government is a consolidation of the two bod-ies—city and county—into a new form of elected administra-tion. According to an excerpt from an online history pub-lished by the Nashville Public Library, “Nashville became the national pioneer in metropolitan organization. Although other

cities had partial consolidation, Nash-ville was the first city in the country to achieve true consolidation.” This con-solidation helped the burgeoning area manage growth and provide needed services as the population shifted to the suburbs in the 1950s.

The local economic development en-gine, the Nashville Area Chamber of Commerce, also is credited with be-ing a catalyst for sound and smart growth.

“We have a truly outstanding cham-ber of commerce,” said Jim Dunn, CCIM, president of Keystone Realty Services of Madison, Tenn., and a 40-year Nashville commercial real es-tate veteran. “Back in the 1970s, the chamber concentrated on luring the smokestack-type of industries, and we got some of those. But one of the leaders had the foresight to say that those really aren’t the kind of jobs we

need in the future—not that we would turn them down.”

Dunn, president of the Middle Tennes-see CCIM Chapter, said new minds on the Chamber later crafted a 10-year plan to bring a wider range of businesses to energize the economy. Their efforts paid off handsomely over the past decade. Dell Computers built its first manufacturing and distribution facility outside of Texas in Nashville, bringing 3,200 jobs. Caremark Phar-macy Services, the parent of the CVS pharmacy retailer, opened its world headquarters in Nashville. The pub-licly-traded Louisiana Pacific Building Materials Company, one of the na-tion’s largest, relocated its corporate headquarters to the city in 2004 from Portland. And, in 2005, automaker Nissan moved its North American headquarters to Franklin, part of the metro area, along with 1,300 jobs. Ac-cording to Expansion Management,

Nashville Transaction Breakdown12-Month Trailing (04/01/08 - 03/31/09)

Office Industrial Retail Apartment Hotel< $5 MillionVolume (Mil) $63 $82 $110 $20 $12

Size Weighted Avg. ($ per sf/unit) $106 $41 $130 $44,255 $30,893

Price Weighted Avg. ($ per sf/unit) $138 $55 $183 $50,026 $33,646

Median ($ per sf/unit) $104 $49 $116 $40,000 $33,176

> $5 MillionVolume (Mil) $211 $27 $155 $272 –

Size Weighted Avg. ($ per sf/unit) $168 $31 $176 $63,153 –

Price Weighted Avg. ($ per sf/unit) $175 $33 $238 $81,432 –

Median ($ per sf/unit) $168 $35 $211 $44,030 –

All TransactionsVolume (Mil) $274 $110 $266 $292 $49

Size Weighted Avg. ($ per sf/unit) $148 $38 $153 $61,371 $48,418

Price Weighted Avg. ($ per sf/unit) $167 $50 $215 $79,296 $55,281

Median ($ per sf/unit) $117 $43 $119 $43,403 $47,414

Capitalization Rates (All Transactions)Weighted Average (%) 6.8 – 7.2 6.4 –

Median (%) 6.9 – 7.3 6.3 –Source: RERC.

Above: Grand Old Opry

Revised July 1, 2009

22Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

Nissan’s decision marks the 17th cor-porate headquarters announcement in Tennessee since January 2003.

In May, the Chamber reported that 74 companies relocated to or expanded operations in the metro area since late 2008, creating 5,722 new jobs. And, the group is negotiating with 26 other companies on job relocation or reten-tion.

Healthcare is widely considered a sought-after economic driver, and the city has emerged as a leader in that field. Healthcare companies based in the Nashville area employ an esti-mated 430,000 workers globally and more than 94,000 in middle Tennes-see alone. The Hospital Corporation of America (HCA), the largest private operator of health care facilities in the world, was founded in and remains headquartered there.

A key factor also paramount to Nash-ville’s boom is its geographic location. Just about in the center of Tennessee, the market can boast six Interstate highway routes that link Nashville with major distribution points nation-wide. Dunn pointed out that from a demographic perspective, the market is within a 24-hour drive of 75 percent of the U.S. population; and, from a climatic perspective, Nashville en-joys four seasons but avoids the ex-tremes—the average low in January is 28 degrees, and the average high in August is 88 degrees.

Much of Nashville’s economic success in terms of corporate relocations has taken place outside the city’s down-town core. But there is also lots go-ing on downtown on the banks of the Cumberland River. In April 2009, the Metropolitan Council approved a land acquisition bill to borrow up to $75 million for land to build a new conven-tion center, a project pushed by Mayor Karl Dean. Dunn noted that federal stimulus funds should help with major infrastructure projects, like improve-ments to an existing commuter rail system and “some significant bridge enhancements.”

A 24-hour city is emerging as multifam-ily residential properties are open or being developed along Church Street and in pocket neighborhoods like North Capitol, SoBro, and the Gulch. The Nashville Downtown Partnership reports: “More condos were sold in downtown Nashville during the first 2 quarters of 2008 than in all of 2007.

Over 900 condos—more than in the 5 previous years combined—are ex-pected to close by the end of 2008. Over 400 more condos will close in 2009.”

Nashvillians seeking a downtown ad-dress have a lot of options at prices far below comparable properties in other major metro markets. Home seekers can opt for a home at The Viridian, a new, luxury 31-story condo property with unit prices ranging from $214,000 to $1.4 million, or a renovated unit at the Lofts of Werthann Mills, where a condominium home developed in a century-old factory building starts at $134,500 and jumps to $429,900.

These and other multifamily homes are within walking distance of the growing arts and entertainment options down-town—options beyond country music, of course. But rest assured, in Music City the music rarely stops.

Above: Nashville Skyline

23Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

B.K. Allen, CCIMB.K. Allen Real EstatePotomac Falls, Virginia

Todd Clarke, CCIMNew Mexico ApartmentsAlbuquerque, New Mexico

Wayne D’Amico, CCIMProperty PoliticsEssex, Connecticut

Paul Fetscher, CCIMGreat American BrokerageLong Beach, New York

Stephen FurnaryING Clarion PartnersNew York, New York

Breck HansonLaSalle Bank, N.A.Chicago, Illinois

Dennis MartinRREEF/DB Real EstateNew York, New York

Jeff Lyon, CCIMGVA Kidder MathewsSeattle, Washington

Buzz McCoyBuzz McCoy Associates, Inc.Los Angeles, California

Tom Nordstrom, CCIMAEGON USA Realty Advisors, Inc.Cedar Rapids, Iowa

Art PasquerellaBerwind Property Group, Inc.Philadelphia, Pennsylvania

Duncan Patterson, CCIMPatterson-Woods AssociatesGreenville, Delaware

Gary M. Ralston, CCIM, SIOR, SRS, CPM, CREFlorida Retail Development, LLCWinter Park, Florida

Cynthia Shelton, CCIMColliers ArnoldOrlando, Florida

Frank Simpson, CCIMThe Simpson CompanyGainesville, Georgia

Allen SmithPrudential Investment Managment ServicesParsippany, New Jersey

Richard SokolovSimon Property GroupIndianapolis, Indiana

John Stone, CCIMJohn M. Stone CompanyDallas, Texas

Dewey Struble, CCIMSperry Van NessReno, Nevada

Julien StudleyJulien Studley, Inc.New York, New York

Allan SweetAMLI Residential Properties TrustChicago, Illinois

Garry Weiss, CCIMFirst Industrial Realty TrustChicago, Illinois

Sam ZellEquity Group InvestmentsChicago, Illinois

RERC~CCIM Investment Trends Quarterly

RERC Editorial Staff

PublisherKenneth P. Riggs, Jr.CFA®, CRE, FRICS, MAI, CCIM

Editor-in-ChiefBarb Bush

Lead AnalystBrian Velky

Research AnalystsGreg PhilippCliff CarlsonCharles GohrMorgan Westpfahl

Design EditorMichelle Houlgrave

Data ManagementBen NeilDaniel Warner

Production CommitteeTerri Cotter

Research AssistantsJeffrey HarmsDavid KellyHerinomena RakotoariveloAnthony Tholkes

CCIM Institute

PresidentCharles “Mac” McClure, CCIM

President-ElectRichard Juge, CCIM

First Vice PresidentFrank Simpson, CCIM

Chief Executive OfficerJonathan Salk

Director of Public RelationsEdward M. Bury, APR

CCIM Member Services CommitteeBrent Case, CCIM, ChairmanMiriam Campos-Root, CCIM, Vice Chairman

Immediate Past ChairmanCCIM Member Services CommitteeSteve Moriera, CCIM

LiasonCCIM Member Services CommitteeKarl Landreneau, CCIM

Advisory Board Members

Copyright Notice for RERC~CCIM Investment Trends Quarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute. All rights reserved. No part of this publication may be reproduced, duplicated, or copied in any form, includ-ing electronic forwarding or copying, xerography, microfilm, or other methods, or incorporated into any information retrieval system, without the written permission of RERC and the CCIM Institute.

24Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

Acknowledgements

REALTORS® Commercial Alliance of the National Association of REALTORS®

NAR PresidentCharles McMillan, CIPS

NAR Executive Vice President/CEODale A. Stinton

RCA Committee RepresentativeRobert Toothaker, CPM

NAR Vice President of Commercial Real EstateJan M. Hope

Real Estate Research CorporationFounded more than 75 years ago, Real Estate Research Corporation (RERC) was the nation’s first independent real estate firm that specialized in both real estate research and analysis. Recognized as a pioneer in the art of real es-tate management and for monitoring key sectors of the economy that influence the real estate industry, RERC has retained its place as one of the industry’s leading real estate investment trends analysts through the publication of such reports as Expectations & Market Realities in Real Estate and the RERC Real Estate Report. Today, RERC is known for its research publications and market studies, commercial property valuations, com-plex consulting assignments, portfolio manage-ment and technology services, and independent fiduciary services.

The CCIM InstituteThe CCIM Institute, headquartered in Chicago, confers the Certified Commer-cial Investment Member designation through an extensive curriculum of 200 classroom hours in addition to professional experience requirements. CCIMs are recognized experts in commercial real estate brokerage, leasing, asset management, valuation, and investment analysis, and form a business net-work encompassing more than 1,000 markets throughout North America, Eu-rope, Asia and the Caribbean. There currently are more than 8,600 CCIM designees, with an additional 8,200 professionals pursuing the designation. CCIM Institute is an affiliate of the National Association of REALTORS®. Visit www.ccim.com.

REALTORS® Commercial Alliance of the National Association of REALTORS®

The REALTORS® Commercial Alliance (RCA) is the commercial division of the National Association of REALTORS® (NAR) that connects commercial real es-tate professionals and exchanges valuable information that contributes to their success. RCA in partnership with NAR’s commercial affiliates—CCIM Institute, the Counselors of Real Estate (CRE), the Institute of Real Estate Management (IREM), the REALTORS® Land Institute (RLI), and the Society of Industrial and Office REALTORS® (SIOR)—is dedicated to collaboration with and building on the strengths of each affiliate entity to benefit the real estate industry. RCA works to serve the needs of members, and to shape and unify the commercial real estate industry through valuable products and services, technology initia-tives, public policy advocacy, education, and research.

The RERC/CCIM Investment Trends Quarterly is produced by Real Estate Research Corporation (RERC) in association with and for members of the CCIM Institute. The RERC/CCIM Invest-ment Trends Quarterly is sponsored by the REALTORS® Com-mercial Alliance of the National Association of REALTORS®.

25Investment TrendsQuarterly

Copyright© 2009 by Real Estate Research Corporation (RERC) and the CCIM Institute.

RealEstateResearchCorporation

Founded in 1931, Real Estate Research Corporation is one of the longest-serv-ing and most recognized national firms devoted to real property research, valu-ation, real estate consulting, indepen-dent fiduciary services, and portfolio services.

“

”

Offices located throughout the U.S., with headquarters in Chicago

LeadershipKenneth P. Riggs, Jr.CFA®, CRE, FRICS, MAI, CCIMPresident & CEO

Jules H. Marling, III, CRE, FRICS, MAIManaging Director

Del H. Kendall, CRE, MAIManaging Director

Donald A. Burns, CRE, FRICS, MAIManaging Director

Gregory P. Kendall, CRE, MAIManaging Director

Kent D. Steele, CRE, FRICS, MAIManaging Director

William L. Corbin, MAIManaging Director

Standard PublicationsRERC Real Estate Report

RERC/CCIM Investment Trends Quarterly

Expectations & Market Realities in Real Estate

Real Estate Research Corporation980 North Michigan Avenue, Suite 1110Chicago, IL 60611-4522Phone: 319.352.1500Fax: 319.352.4050www.RERC.com

Explore our services... ■ Specialized Research■ Independent Fiduciary Services■ Fairness Opinions■ Litigation Support■ Consulting■ Portfolio Services■ Commercial Valuation■ Financial Risk Management■ Market Research & Analysis■ Appraisal Management Services

IndependentTo ensure objectivity and independence, RERC does not engage in any activity that may conflict with the best interests of our cli-ents. As an impartial observer of the markets, RERC is able to collect and synthesize data and commentary unavailable to less independent organizations.

UniqueRERC brings unique and diverse skills to solving complex real estate issues. RERC’s innovative approach to problem solving is fostered by the diverse education and professional backgrounds of our team members.

ExpertiseRERC’s expertise originates from a national presence and per-spective, coupled with local market knowledge gained through the completion of hundreds of engagements annually in every major market. Our clients have found that RERC is relationship-oriented, focusing first and foremost on our clients’ and custom-ers’ needs, and delivering the highest quality products and ser-vices. RERC is an SEC-registered advisor.

27Investment TrendsQuarterly