scottish labour - best future for pensions

DESCRIPTION

As September the 18th approaches, this paper outlines why the best future for Scotland's pensioners - present and future - is the strength and security of the UK.TRANSCRIPT

! 1

Executive Summary

!• Scottish Labour believes in a welfare system which ensures that – even with

increased taxable capability at the devolved level – enough capacity exists to

redistribute public resources to where it is most needed.

!• Today, as part of the UK, Scottish pensioners receive £9.6 billion in pensions and

pensioner benefits annually – £500 million more than the amount they would get if

the payment was based on our population share of the UK. This means that

Scottish pensioners are almost £500 better off on average each year as part of

the United Kingdom.

!• For us, it is a matter of principle that an old-age pensioner in Glasgow should be

paid the same pension as someone in Gloucester, or that an individual who falls

on difficult times in Edinburgh should be entitled to unemployment benefits no

higher or lower than a person facing similar circumstances in Essex. This is the

view of the vast majority of Scots – as evidenced by the Scottish Social Attitudes

Survey data – who believe that pensions and benefits should remain a reserved

responsibility.

!• In Scotland a higher proportion of over-60s are Pension Credit claimants than in

the rest of Great Britain (19 per cent vs 17 per cent), with the result that average annual spend per over-60 resident is higher in Scotland than GB as a whole

(£515 per annum in Scotland in 2013-14 compared with £504 in GB).

!• The pooling of risks and resources is made explicit in national insurance

contributions. UK national insurance is the largest insurance scheme of all,

securing benefits to all through the widest possible risk pool.

! 2

!o According to HMRC, Scotland accounts for 8.2 per cent (£8,415 million) of

the UK’s National Insurance Contribution receipts in 2012-13 (£102,037

million).

o However, total social protection spend (the totality of benefit and social

care spend) in Scotland in 2012-13 was £22,458 million (8.9 per cent of

the UK total).

!• As the UK Government argues, if the government of an independent Scottish

state decided to set aside the age 67 timetable it would need to consider:

!o the extra State Pension spending that would result from people retiring

earlier. This would cost a future Scottish state around £6 billion

between 2026-27 and 2035-36 in benefit expenditure (in current

prices); and

o the loss in Gross Domestic Product from those people who have left

the labour market earlier than if the pension age were raised to 67 as in

the forecasts – around £9 billion between 2026-27 and 2035-36 (in

current prices).

!• The government of an independent Scotland would need to give serious

consideration to the administration and payment of pensions, how to provide

adequate pension protection for savers and how to disentangle cross-border

contribution records and liabilities.

!

! 3

!BEST FUTURE FOR SCOTLAND’S PENSIONS

!In this paper, we show how by pooling and sharing our resources across the whole

of the UK, pensions are more affordable in Scotland today and in the future. Only

separation puts the pensions of Scots at risk.

Scottish Labour believes in a welfare system which ensures that – even with

increased taxable capability at the devolved level – enough capacity exists to

redistribute public resources to where it is most needed.

Today, as part of the UK, Scottish pensioners receive £9.6 billion in pensions and

pensioner benefits annually – £500 million more than the amount they would get if

the payment was based on our population share of the UK.

This means that Scottish pensioners are almost £500 better off on average each

year as part of the United Kingdom.

The number of state pensioners in Scotland was 1,020,190 in 2012-13 – and this is

projected to increase over the coming years.

The per-pensioner averages are thus as follows:

!The pooling of risks and resources is made explicit in national insurance

contributions. UK national insurance is the largest insurance scheme of all, securing

benefits to all through the widest possible risk pool.

For us, it is a matter of principle that an old-age pensioner in Glasgow should be paid

the same pension as someone in Gloucester, or that an individual who falls on

difficult times in Edinburgh should be entitled to unemployment benefits no higher or

lower than a person facing similar circumstances in Essex. This is the view of the

£500 million

Divided by:

1,020,190 state pensioners £490

! 4

vast majority of Scots – as evidenced by the Scottish Social Attitudes Survey data –

who believe that pensions and benefits should remain a reserved responsibility.

Labour strongly believes in a Welfare State that redistributes resources from the

areas of greatest wealth to the areas of greatest need. Scotland benefits from this

arrangement: as part of the UK, for example, we have 8.3 per cent of the population,

yet receive 11 per cent of incapacity benefits, mainly because of the disproportionate

number of Scots afflicted by mining and associated diseases, a sad legacy resulting

from Scotland’s strong and proud industrial heritage.

People in need should benefit wherever they live in the UK because they share

common citizenship – this is central to Labour’s idea of the “sharing union”.

Accordingly, we have a single system of income support and old-age pension across

the UK. The SNP make the opposite argument: for them, social solidarity ends at

Gretna Green, and they do not believe we should support friends, family and those in

need south of Berwick.

Remaining part of the large UK national insurance scheme matters to Scotland.

There is, moreover, a particular issue surrounding the age structure of the population

in Scotland. As our population is getting older more quickly than the rest of the UK,

the pressure on old-age pensions will loom ever large. In UK national insurance,

with resources mutually shared, potential risks like this are pooled to provide greater

security for all.

Labour believes that large-scale divergence in the provision of cash benefits would

be a retrograde step, resulting in the tearing apart of one of the most enduring bonds

that have united us.

Social security is the UK Government’s single largest item of public expenditure. In

2012-2013, total government expenditure in Great Britain on benefits, tax credits and

state pensions was £207 billion. Payments aimed at pensioners (such as the state

pension, pension credit, etc.) accounted for 54 per cent of total social security spend,

and this is projected to rise to 55 per cent by 2018-19. In Scotland, social protection

spending including benefits – such as old age pensions, child benefit, income

support and disability benefits – accounted for nearly 40 per cent of identifiable

public spending. The table below shows the scale of benefits expenditure in

Scotland (excluding tax credits). Old-age pensions, as can be seen, are by far the

biggest component of the benefits bill. ! 5

In comparison to England, Scotland has relatively high levels of benefit spending,

which is, in large part, driven by long-term social trends. Scotland is now

economically typical of the UK in terms of income and unemployment, but some

continuing high levels of benefit expenditure may still be linked to the de-

industrialisation that took place during the 1980s. The levels of benefit spending in

future however will be substantially driven by the changing age structure of the

population.

Expenditure by UK Department for Work and Pensions on Benefits in Scotland, 2012-13

£ million Percentage

Attendance Allowance 489 3.0

Bereavement Benefit-Widow's Benefit 59 0.4

Carer's Allowance 169 1.2

Council Tax Benefit 380 2.6

Disability Living Allowance of which children of which working age of which pensioners

1,450 114 821 515

9.9

Discretionary Housing Payments 4 0.02

Employment & Support Allowance 752 5.2

Housing Benefit 1,789 12.3

Incapacity Benefit 539 3.7

Income Support of which on Incapacity Benefit of which lone parents of which carers of which others

496 267 162 44 24

3.4

Industrial Injuries Benefits 92 0.6

Jobseeker's Allowance 478 3.3

Maternity Allowance 27 0.2

Over 75 TV Licences 49 0.3

Pension Credit 688 4.7

Severe Disablement Allowance of which working age of which pensioners

97 80 17

0.7

State Pension 6,783 46.5 ! 6

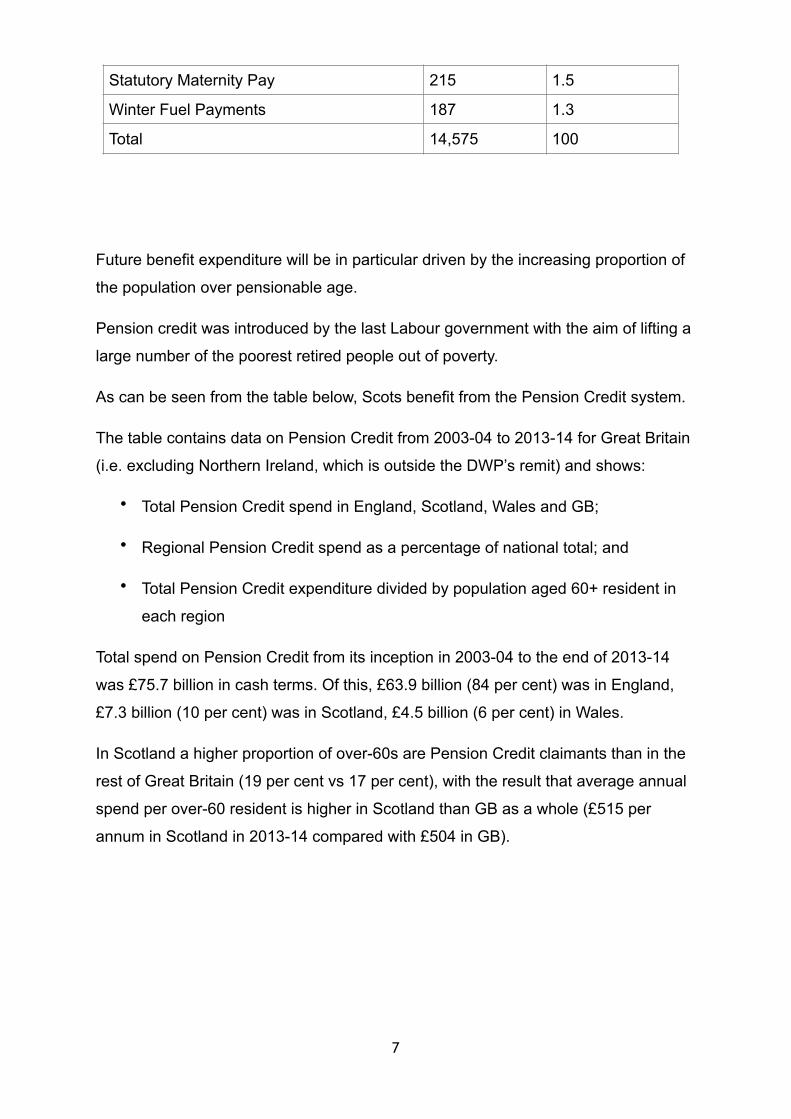

!!Future benefit expenditure will be in particular driven by the increasing proportion of

the population over pensionable age.

Pension credit was introduced by the last Labour government with the aim of lifting a

large number of the poorest retired people out of poverty.

As can be seen from the table below, Scots benefit from the Pension Credit system.

The table contains data on Pension Credit from 2003-04 to 2013-14 for Great Britain

(i.e. excluding Northern Ireland, which is outside the DWP’s remit) and shows:

• Total Pension Credit spend in England, Scotland, Wales and GB;

• Regional Pension Credit spend as a percentage of national total; and

• Total Pension Credit expenditure divided by population aged 60+ resident in

each region

Total spend on Pension Credit from its inception in 2003-04 to the end of 2013-14

was £75.7 billion in cash terms. Of this, £63.9 billion (84 per cent) was in England,

£7.3 billion (10 per cent) was in Scotland, £4.5 billion (6 per cent) in Wales.

In Scotland a higher proportion of over-60s are Pension Credit claimants than in the

rest of Great Britain (19 per cent vs 17 per cent), with the result that average annual

spend per over-60 resident is higher in Scotland than GB as a whole (£515 per

annum in Scotland in 2013-14 compared with £504 in GB).

!!

Statutory Maternity Pay 215 1.5

Winter Fuel Payments 187 1.3

Total 14,575 100

! 7

Pension Credit expenditure

2003/04

2004/05

2005/06

2006/07

2007/08

2008/09

2009/10

2010/11

2011/12

2012/13

2013/14

Total Pension Credit spend

Outturn

Outturn

Outturn

Outturn

Outturn

Outturn

Outturn

Outturn

Outturn

Outturn

Estimate

£ million

£ million

£ million

£ million

£ million

£ million

£ million

£ million

£ million

£ million

£ million

England

1,961 5,015 5,400 5,771 6,189 6,480 6,851 6,963 6,821 6,376 6,039

Scotland

240 602 644 686 735 759 787 785 751 688 643

Wales 135 353 381 410 442 464 490 493 479 446 421

Overseas

0 1 1 1 2 1 1 1 1 1 1

Great Britain (and overseas)

2,336 5,971 6,426 6,869 7,367 7,703 8,129 8,242 8,052 7,511 7,104

Pension Credit - regional spend as a % of Great Britain (and abroad) total

% of GB total

% of GB total

% of GB total

% of GB total

% of GB total

% of GB total

% of GB total

% of GB total

% of GB total

% of GB total

% of GB total

England

84.0%

84.0%

84.0%

84.0%

84.0%

84.1%

84.3%

84.5%

84.7%

84.9%

85.0%

Scotland

10.3%

10.1%

10.0%

10.0%

10.0%

9.9% 9.7% 9.5% 9.3% 9.2% 9.1%

Wales 5.8% 5.9% 5.9% 6.0% 6.0% 6.0% 6.0% 6.0% 5.9% 5.9% 5.9%

Overseas

0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Great Britain (and overseas)

100.0%

100.0%

100.0%

100.0%

100.0%

100.0%

100.0%

100.0%

100.0%

100.0%

100.0%

Pension Credit claimants as % of population aged 60 and over

2003/04

2004/05

2005/06

2006/07

2007/08

2008/09

2009/10

2010/11

2011/12

2012/13

2013/14

England

17.6%

20.7%

21.3%

21.2%

20.7%

20.2%

19.9%

19.5%

18.7%

17.4%

16.7%

! 8

!

Scotland

22.2%

24.7%

25.4%

25.3%

24.7%

24.0%

23.1%

22.7%

21.5%

19.9%

18.8%

Wales 18.9%

22.3%

23.1%

23.2%

22.6%

22.1%

21.9%

21.4%

20.6%

19.3%

18.5%

Great Britain (excl. abroad)

18.1%

21.1%

21.7%

21.7%

21.1%

20.6%

20.3%

19.9%

19.1%

17.8%

17.0%

! 9

!!

! 10

Old-age pensions are now the main contributory benefit (insurance stamps matter for

them), and most other benefits are now means-tested and supported from general

taxation. Nevertheless, welfare is still a system of mutual insurance. Every

individual faces risks like old age, illness, and unemployment: rather than carrying

these risks individually they are pooled – not in a pension fund or a friendly society,

but across an entire country, to become not private but “social” insurance.

Individuals pay in, increasingly via general taxation (based on ability to pay rather

than an insurance premium), and take the benefits when they need them. Obviously

the larger the pool, the more the risks are likely to average out, and the easier an

insurance scheme is to manage. Social insurance provides the largest pool of all.

It is not surprising that nationalists want to devolve welfare: they want to create a

more exclusively Scottish sense of national identity to replace the loyalties which

already bind British people together. The SNP have played politics with welfare.

However, when their own Expert Working Group on Welfare reported, it concluded

that an independent Scotland should continue to share resources with the rest of the

UK. This would mean that the system would still be constrained by choices made in

the rest of the UK, while leaving Scotland with no political representation. By pooling

our resources across the UK we can share the burden of funding and administering

our social security system.

Our social security system is a deeply complex, integrated cross-border arrangement

that cannot easily be separated. The SNP’s own Expert Working Group, indeed,

conceded this point: “A downside of continuing to share services might be that an

independent Scottish Government finds itself unable to implement some of its early

priorities for change to the benefit system”. 1

Similarly, Dr Nicola McEwen, Director of Public Policy at the University of

Edinburgh’s Academy of Government and Senior ESRC Scotland Fellow, has

argued: “The agencies delivering welfare services are scattered across the UK, and

many are in Scotland. But the welfare system is nonetheless deeply integrated. It is

dependent upon a core IT system run by the UK Department for Works and

Pensions that determines entitlements based upon policies set by the UK

! 11

Expert Working Group on Welfare, The Expert Working Group on Welfare, (Edinburgh: Scottish 1

Government, June 2013), p. 66.

government. Relatively minor modifications can be accommodated - as is the case

currently in Northern Ireland where social security is devolved. But it would be

extremely difficult to share the administration and delivery of services if entitlements

were markedly different north and south of the border”. 2

Pension experts have warned about the risks of separation to Scottish pensions.

The Institute for Chartered Accountants Scotland (ICAS), for instance, highlighted

that companies with defined benefits schemes would have to fully fund their

schemes if they operated between an independent Scotland and the UK, in order to

comply with EU law. That would mean finding resources to fund the £177 billion

pension shortfall, if companies wanted to operate schemes in Scotland and the UK.

The SNP have failed to provide any certainty about pensions in an independent

Scotland. When questioned with real and legitimate concerns from people across

Scotland, the SNP accuse pro-UK campaigners of “scaremongering”. This is despite

the fact that the SNP Finance Secretary, John Swinney, admitted in a private memo

that cuts to pensions would have to be made: “Spending on state pensions and

public sector pensions is also driven by demographics, and is set to rise … At

present HM Treasury and DWP absorb the risk of growth in demand in the widest

sense and therefore all associated costs. In future [if Scotland was to leave the UK]

we will assume responsibility for managing such pressure. This will imply more

volatility in overall spending than at present … The [Scottish Government’s Fiscal

Commission] Working Group will consider the affordability of state pensions as its

work on fiscal sustainability proceeds”.

Scotland’s population in the future is going to have more old people in relation to

younger people than the UK as a whole. This demographic reality means that if

Scotland left the UK we would be faced with a stark choice: reduce the state pension

or meet the shortfall via higher taxes or cuts in other social spending. This is a point

that has been made by the Institute for Fiscal Studies (IFS): “The more rapid growth

in the elderly population in Scotland, combined with the greater amounts spent on

benefits for older people (largely in the form of state pensions, but also disability

benefits) can clearly be expected to lead to more rapid growth in benefit spending in

Scotland than in Great Britain as a whole”. 3

! 12

Nicola McEwen, “SNP must set out their welfare vision”, (University of Edinburgh, June 2013)2

Institute of Fiscal Studies, Government spending on public services in Scotland: current patterns 3

and future issues, (London: Institute for Fiscal Studies, September 2013), p. 53.

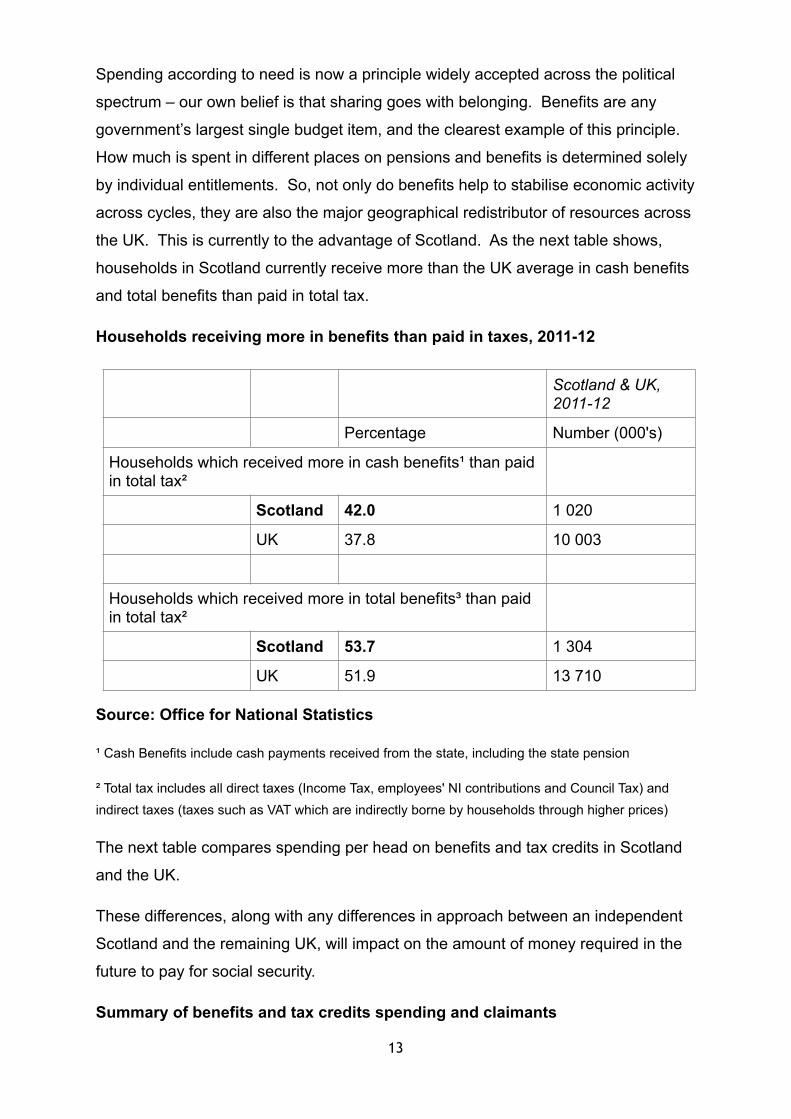

Spending according to need is now a principle widely accepted across the political

spectrum – our own belief is that sharing goes with belonging. Benefits are any

government’s largest single budget item, and the clearest example of this principle.

How much is spent in different places on pensions and benefits is determined solely

by individual entitlements. So, not only do benefits help to stabilise economic activity

across cycles, they are also the major geographical redistributor of resources across

the UK. This is currently to the advantage of Scotland. As the next table shows,

households in Scotland currently receive more than the UK average in cash benefits

and total benefits than paid in total tax.

Households receiving more in benefits than paid in taxes, 2011-12

Source: Office for National Statistics

¹ Cash Benefits include cash payments received from the state, including the state pension

² Total tax includes all direct taxes (Income Tax, employees' NI contributions and Council Tax) and indirect taxes (taxes such as VAT which are indirectly borne by households through higher prices)

The next table compares spending per head on benefits and tax credits in Scotland

and the UK.

These differences, along with any differences in approach between an independent

Scotland and the remaining UK, will impact on the amount of money required in the

future to pay for social security.

Summary of benefits and tax credits spending and claimants

Scotland & UK, 2011-12

Percentage Number (000's)

Households which received more in cash benefits¹ than paid in total tax²

Scotland 42.0 1 020

UK 37.8 10 003

Households which received more in total benefits³ than paid in total tax²

Scotland 53.7 1 304

UK 51.9 13 710

! 13

Expenditure £billion Claimants (thousands)

Claimants as % of population

2012-13 figures Scotland United Kingdom

Scotland United Kingdom

Scotland United Kingdom

State Pension 6.8 78.3 1,020 11,915 19.2% 18.7%

Pension Credit 0.7 7.8 248 2,599 4.7% 4.1%

Housing Benefit – pensioners

0.5 6.6 162 1,595 3.0% 2.5%

Disability benefits – pensioners

1.0 10.6 259 2,749 4.9% 4.3%

Other pensioner benefits

0.3 3.1

Share of pensioner benefits paid overseas

0.3 3.4

Total pensioner benefits

9.6 109.9

Incapacity Benefits 1.5 14.0 273 2,613 5.1% 4.1%

Income Support 0.2 2.9 118 1,322 2.2% 2.1%

Jobseeker’s Allowance

0.5 5.4 141 1,569 2.7% 2.5%

Housing Benefit – working age

1.2 17.9 322 3,618 6.1% 5.7%

Disability benefits – working age and children

0.9 9.3 227 2,330 4.3% 3.7%

Personal tax credits 2.2 29.8 361 4,618 6.8% 7.2%

Child Benefit 0.9 12.2 1,023 13,713 19.3% 21.5%

Other working-age and children’s benefits

0.5 6.1

Share of working-age benefits and tax credits paid overseas

0.0 0.2

Total working-age and children’s benefits

8.1 97.7

Other benefits 0.1 0.9

Total benefits and tax credits

17.7 208.6

Population (mid-2012, millions)

5.3 63.7

of which children aged 0-15

0.9 12.0

of which working age (16-State Pension Age)

3.3 39.5

of which above State Pension Age

1.1 12.2

! 14

!All welfare systems involve pooling both risks and the resources. The logic of

pooling risks among individuals, regions and across generations within the largest

possible geographical area is widely recognised. Economic shocks tend to be

asymmetric, affecting individuals and regions in different ways and at different times.

Resource-pooling at the UK-level provides UK citizens with the safety-valve of a

broader and more versatile tax base to cope with such unpredictability.

A less theoretical argument for the pooling of resources is whether Scotland could

continue to afford, on its own, its present levels of welfare spending. A short

summary of Scotland’s fiscal position is as follows. Public expenditure per head in

Scotland is significantly higher than in the UK as a whole. (Devolved public

spending is approximately 18 per cent per head higher, and overall identifiable

expenditure about 14 per cent. The remainder, non-identifiable expenditure on

services such as defence, is mostly allocated on a per capita basis.) Tax revenue

(excluding North Sea oil) is estimated to be slightly below the UK average per head.

On this basis, Scotland would fall far short of the money it needed to sustain present

public services and welfare benefit payments. Some of the gap could be filled if

Scotland is credited with all off-shore oil revenue arising off Scottish coasts to spend

on Scottish services. However, this would leave Scotland very vulnerable when the

oil revenue runs out, or when its price fluctuates in global commodity markets. This

makes the theoretical argument about risk pooling much more real.

In July 2013, it is also worth noting, the IFS produced a briefing note, Government

spending on benefits and state pensions in Scotland: current patterns and future

issues, which analysed current patterns of benefit spending, reviewed some

possibilities for policy change and commented upon the long-term demographic and

fiscal outlook. The IFS concluded that any major redesign of the benefits system,

under enhanced devolution or independence, would require Scotland either to spend

more on cash benefits than is spent now, requiring increased levels of taxation, or

else create large numbers of losers, who will typically have fairly low incomes.

Finally, if Scotland were to leave the UK, there would also be significant cost

implications resulting from the need to protect, and regulate pensions, support

Expenditure per head of population

3,335 3,275

! 15

automatic-enrolment schemes and unscramble UK state pensions from those of an

independent Scotland. There would be a need to create and deliver similar systems

to a much smaller population without the economies that are made possible by being

part of UK-wide systems. Furthermore, some proportion of the liabilities for public

service pension schemes would become the obligation of an independent Scotland,

with estimates suggesting the total liability figure could be around £100 billion.

!!!!!!!!!!!!!!!!!!!

! 16

!Pensions – stronger together

As the UK Government has argued, pensioners living in Scotland have benefited

from the current UK pension system, including a UK-wide National Insurance system

and a Pension Service network supporting 13 million State Pension recipients across

Great Britain and overseas. Scotland now has the lowest proportion of pensioners

with very low incomes in the UK.

The Scottish financial sector serves customers all over the UK and is deeply

embedded in the UK’s regulatory framework. It is also a key element of the Scottish

economy. It has a high concentration of the UK’s life insurance and pension

services, accounting for 24 per cent of the total UK sector.

Over decades we have together developed a complex UK regulatory architecture

which protects the pensions of Scots. The Financial Services Compensation Scheme

(FSCS), the Pension Protection Fund (PPF) and The Pensions Regulator (TPR)

together provide a UK wide firewall for Scots against the loss of pension savings.

How much would it cost to withdraw Scots from this UK wide pensions architecture

and how much would it cost a separate Scotland to then mimic the rUK pensions

architecture? The cost of withdrawing Scots workers from the new UK auto-

enrolment pension system and the new UK Government backed National

Employment Savings Trust (NEST) pension scheme that accompanies auto-

enrolment has not been discussed. How much would this cost and would Scotland

then set up its own version of auto-enrolment and NEST?

What about the future of the PPF which pays pensions to UK workers who otherwise

would lose their pension savings when their employer goes bust. The pensions of

24,000 Scots are paid and managed by the PPF - supporting the Ayrshire steel

workers who found their pension pots emptied when Allied Steel went bust until the

PPF stepped in. Contrast this with the Irish workers left high and dry when Waterford

Crystal went bust. While the PPF guarantees pensions for Waterford's former UK

employees Irish workers continue their legal fight to get a pension from the Irish

state.

As the UK Government has identified, the scale and reach of pensions in the UK is

significant and delivers a wide range of services, including:

! 17

• collection of National Insurance – £104.5 billion in 2012-13;

• the Pension Service network which administers payments and other services

to nearly 13 million contributory State Pension recipients in Great Britain with

spending for 2012-13 of around £80 billion;

• a National Insurance crediting system to protect the pension position of

parents and carers, for people seeking work and people who are

incapacitated;

• an information service for individuals about their State Pension to help them

plan for their retirement. During 2012-13 the UK Government issued around

600,000 State Pension statements, and works in partnership with private

pension schemes to provide combined pension statements;

• payment of state pensions to 1.2 million pensioners living overseas through a

series of complex bilateral and international arrangements;

• the Pension Tracing Service, which in 2012-13 helped over 90,000 customers

to successfully trace a lost pension;

• the Pensions Advisory Service – which provides free information, guidance

and help to members of the public on all pension matters;

• the distribution of tax relief for private pension saving – £34.8 billion in

2012-13;

• the Pensions Regulator, which regulates more than 50,000 private sector

schemes with over 15 million members;

• the Pension Protection Fund, which protects the rights of some 11.4 million

people in eligible occupational schemes. The Fund estimates that by the end

of March 2013, it had paid out over £793 million in compensation;

• the structures – including a £16 million on-going communications campaign –

to support the introduction of automatic enrolment into workplace pensions, so

that six to nine million people will start to save or save more for their

retirement. DWP estimates this will generate £11 billion a year in pension

saving in steady state (by 2020); and

! 18

• the successful launch of National Employment Savings Trust – currently with

2,500 employers and over 1 million members.

!!!!!!!!!!!!!!!!!!!National insurance contributions – Scotland and the rest of the UK

According to HMRC, Scotland accounts for 8.2 per cent (£8,415 million) of the UK’s

National Insurance Contribution receipts in 2012-13 (£102,037 million).

! 19

The National Insurance Fund does not break down spend by UK “region”; however,

there is data available by region on various elements of benefit spend. The Institute

for Fiscal Studies has argued that the existence of a separate National Insurance

Fund reflects an approach to accounting for expenditure on contributory benefits –

but it does not, in any material way, restrict the amounts of money that could be

spent on these benefits.

The NI Fund is notionally used to finance contributory benefits, but in years when the

Fund was not sufficient to finance benefits, it has been topped up from general

taxation revenues, and in years when contributions substantially exceed outlays (as

they have every year since the mid-1990s), the Fund builds up a surplus, largely

invested in gilts. These exercises in moving money from one arm of government to

another maintain a notionally separate Fund, but merely serve to illustrate that NI

contributions and NI expenditure proceed on essentially independent paths.

In 2012-13 spending on state pensions in Scotland was £6,783 million. Total social 4

protection spend (the totality of benefit and social care spend) in Scotland in 2012-13

was £22,458 million (8.9 per cent of the UK total) . 5

In February 2014, ICAS published a report, which argued that some outstanding

questions remained on this issue:

• In our view, [several] … key questions about transitional arrangements remain

outstanding and some may not be answerable prior to the referendum … [This

includes] what amount or reimbursement would the Scottish Government seek

to negotiate from the UK Government by way of providing for those with

“accrued” entitlement to a UK State pension i.e. both individuals in receipt of a

State pension and those of working age? How might this be calculated? 6

Other questions raised by ICAS on the State Pension were as follows:

• What transitional arrangements would be needed to successfully migrate

responsibility for the payment of the State pension to pensioners living in

! 20

https:--www.gov.uk-government-uploads-system-uploads-attachment_data-file-266830-4

expenditure_by_region_201213.xls

Scottish Government, Government Expenditure and Revenue Scotland 2012-13. Available at: http:--5

www.scotland.gov.uk-Resource-0044-00446179.pdf

ICAS, Scotland’s Pensions Future: Have Our Questions Been Answered? February 20146

Scotland at the date of independence, including communication with

individuals?

• What transitional arrangements would need to be made to ensure that the

“accrued” entitlement to the State pension of those of working age living in

Scotland at the date of independence are successfully transferred, including

communication with individuals?

• How does the Scottish Government propose to define “living in Scotland at the

date of independence” or “country of residence at the date of independence”

for the purpose of determining entitlement to a Scottish State pension? How

would this definition dovetail with arrangements for determining citizenship

and any flexibility for individuals to choose, including any potential to choose

dual citizenship?

• Would there be any scope for mitigating the possible effects of a minimum

qualifying period for the single tier pension (currently proposed as 7-10 years)

for both the Scottish and UK State pensions, given that EU law may not permit

special arrangements between Member States?

• What amount or reimbursement would the Scottish Government seek to

negotiate from the UK Government by way of providing for those with

“accrued” entitlement to a UK State pension i.e. both individuals in receipt of a

State pension and those of working age? How might this be calculated?

• Are there any legal barriers which would prevent the rUK, as a member of the

EU, transferring responsibility for the “accrued” State pension entitlements of

those living in Scotland at the date of independence?

The current Scottish Government’s White Paper suggests that in the event of a vote

for independence it would review the UK Government’s decision to bring forward the

increase in State Pension age to 67 and draws attention to the fact that average life

expectancy in Scotland is lower than the UK average. While it is the case that

average life expectancy in Scotland is lower than that for the rest of the UK,

projected life expectancy across all UK nations is increasing.

Projected life expectancy increases for men reaching age 65 across the UK

1990 2000 2010 2020 2030

! 21

!As the UK Government argues, if the government of an independent Scottish state

decided to set aside the age 67 timetable it would need to consider:

• the extra State Pension spending that would result from people retiring earlier.

This would cost a future Scottish state around £6 billion between 2026-27 and

2035-36 in benefit expenditure (in current prices); and

• the loss in Gross Domestic Product from those people who have left the

labour market earlier than if the pension age were raised to 67 as in the

forecasts – around £9 billion between 2026-27 and 2035-36 (in current

prices).

The government of an independent Scotland would need to give serious

consideration to the administration and payment of pensions, how to provide

adequate pension protection for savers and how to disentangle cross-border

contribution records and liabilities.

Scotland 14.6 17.3 19.5 20.9 22.1

England 15.8 18.9 21.1 22.4 23.6

Wales 15.3 18.5 20.5 21.9 23.1

N. Ireland 15.4 18.4 20.5 21.8 23.0

! 22