scope for indo-uk collaboration in the · pdf fileassess prospects for venture capital funding...

TRANSCRIPT

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

SCOPE FOR INDO-UK COLLABORATION

IN THE SEMICONDUCTOR DRIVEN INDUSTRY

Final report

April 2008

India Semiconductor Association and UK Trade Investment India

Feedback Business Consulting Services Pvt. Ltd. India

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

Table of contents

Index Page Number

Engagement background 5

1. Summary 7

1. Conclusions and recommendations 10

2.0 India semiconductor industry overview 20

2.1 India semiconductor market overview 21

2.1.1 Semiconductor design services 22 2.1.2 Semiconductor product market 23

Geographical clustering in India 24

2.2 Indian universities – Overview 26

2.2.1 Incubation centres 28

2.2.2 University - industry collaboration in India 30

Case studies / success stories – industry- institution participation: 32

2.3 Semiconductor policy in India 34

2.3.1 Key highlights of the policy 34

2.3.2 Incentives for investors 34

2.3.3 Benefits of the policy 35

2.3.4 Challenges 35

2.3.5 SMDP (Special Manpower Development Program) 35

2.4 Strengths and weaknesses of Indian universities and companies 36 2.4.1 Strengths and weaknesses of Indian universities in the field of semiconductors

36

Exhibit: Definitions 36

2.4.2 Strengths, weaknesses of semiconductor companies 38 UK semiconductor market details 40

3.1 UK semiconductor industry overview 41

3.1.1 Overview of the semiconductor industry in the UK 41

3.1.2 Semiconductor design companies in the UK 43

Geographical clusters in UK 46

3.2 Universities in the UK – Overview 49

3.2.1 Overview 49

3.2.2 Nature of research 50

3.2.4 University - industry collaboration 52

3.4 Venture capitalists in UK – Overview 57

3.5 Allied organisations 58

3.6 Analysis of the UK semiconductor industry 60

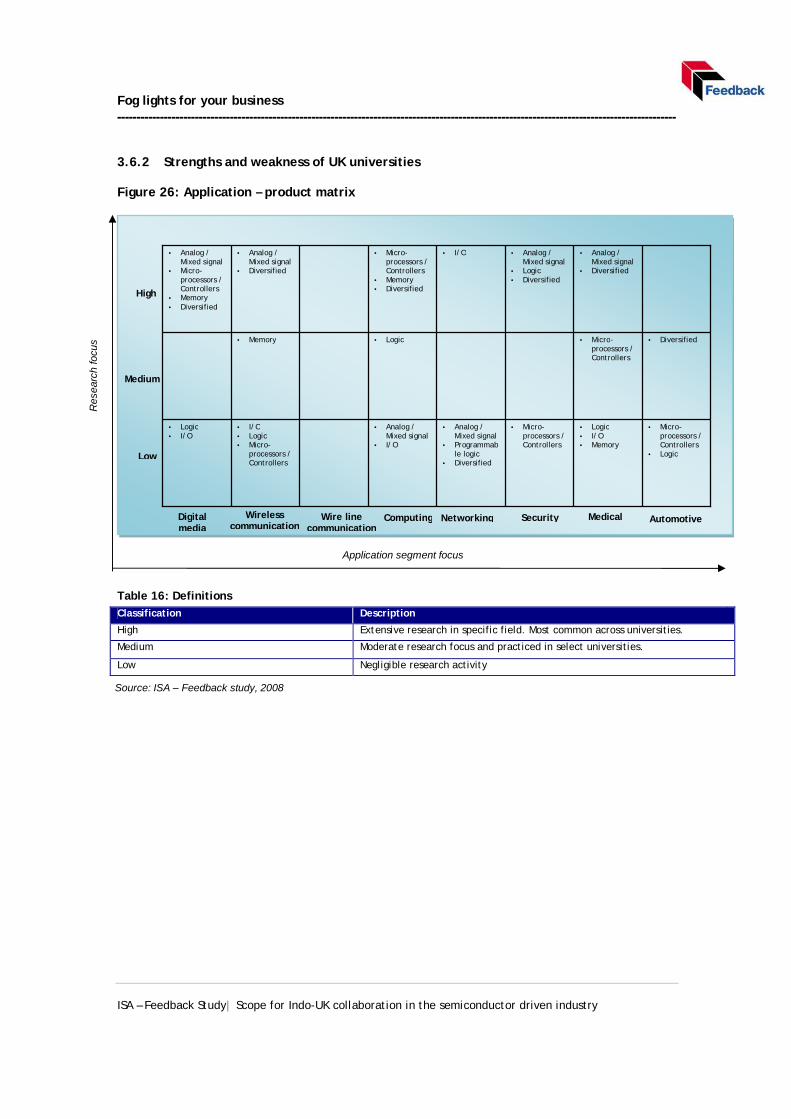

3.6.1 Strengths and weaknesses of UK universities in the field of semiconductors:

60

3.6.2 Strength weakness analysis of UK universities 61

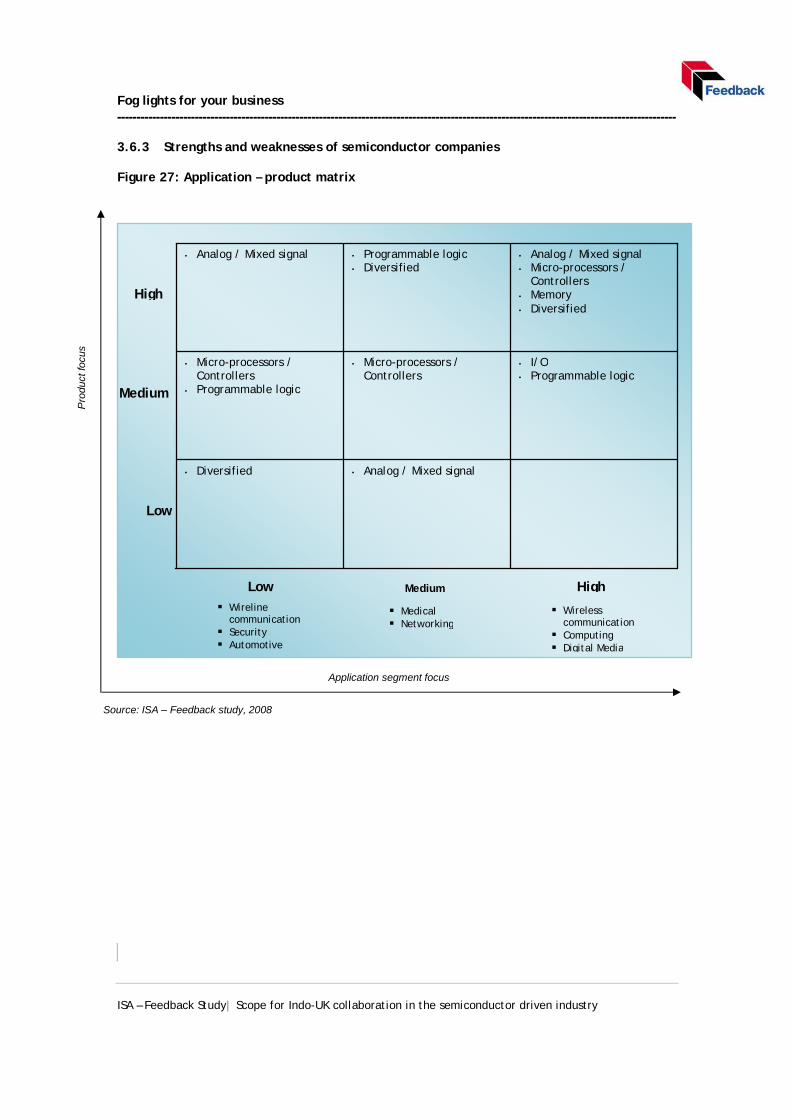

3.6.3 Strengths, weaknesses of semiconductor companies 62

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

Figure Page Number

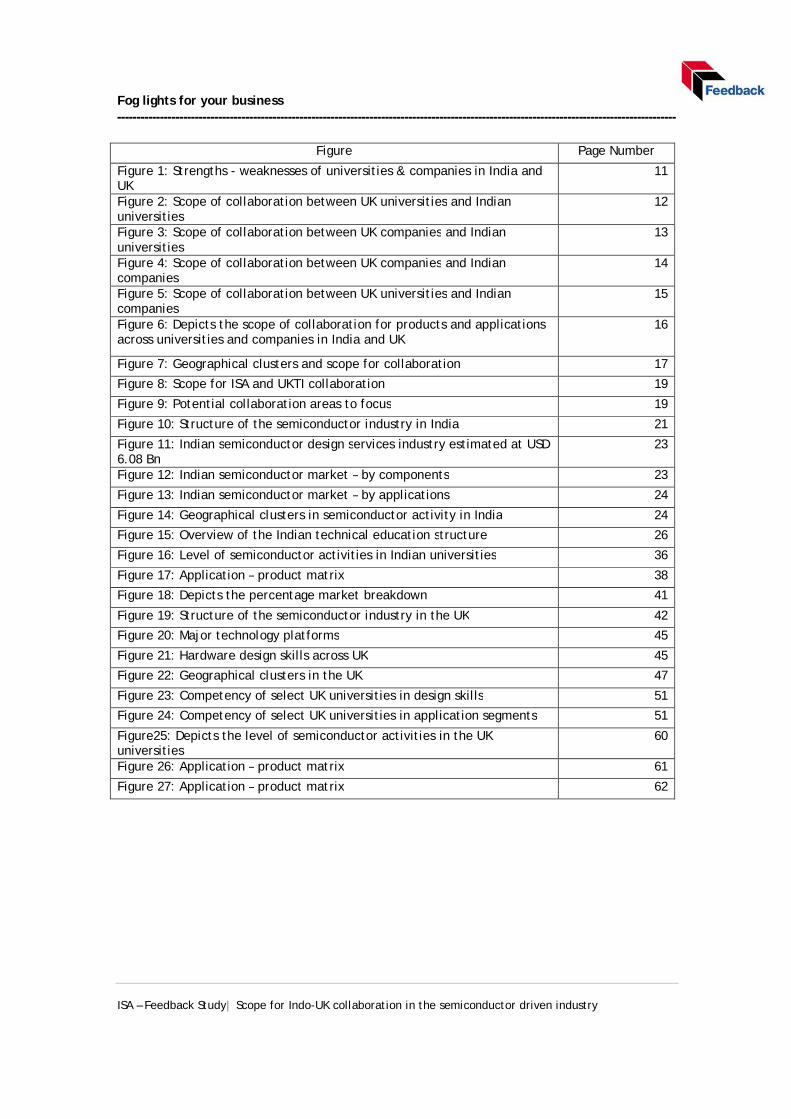

Figure 1: Strengths - weaknesses of universities & companies in India and UK

11

Figure 2: Scope of collaboration between UK universities and Indian universities

12

Figure 3: Scope of collaboration between UK companies and Indian universities

13

Figure 4: Scope of collaboration between UK companies and Indian companies

14

Figure 5: Scope of collaboration between UK universities and Indian companies

15

Figure 6: Depicts the scope of collaboration for products and applications across universities and companies in India and UK

16

Figure 7: Geographical clusters and scope for collaboration 17

Figure 8: Scope for ISA and UKTI collaboration 19

Figure 9: Potential collaboration areas to focus 19

Figure 10: Structure of the semiconductor industry in India 21

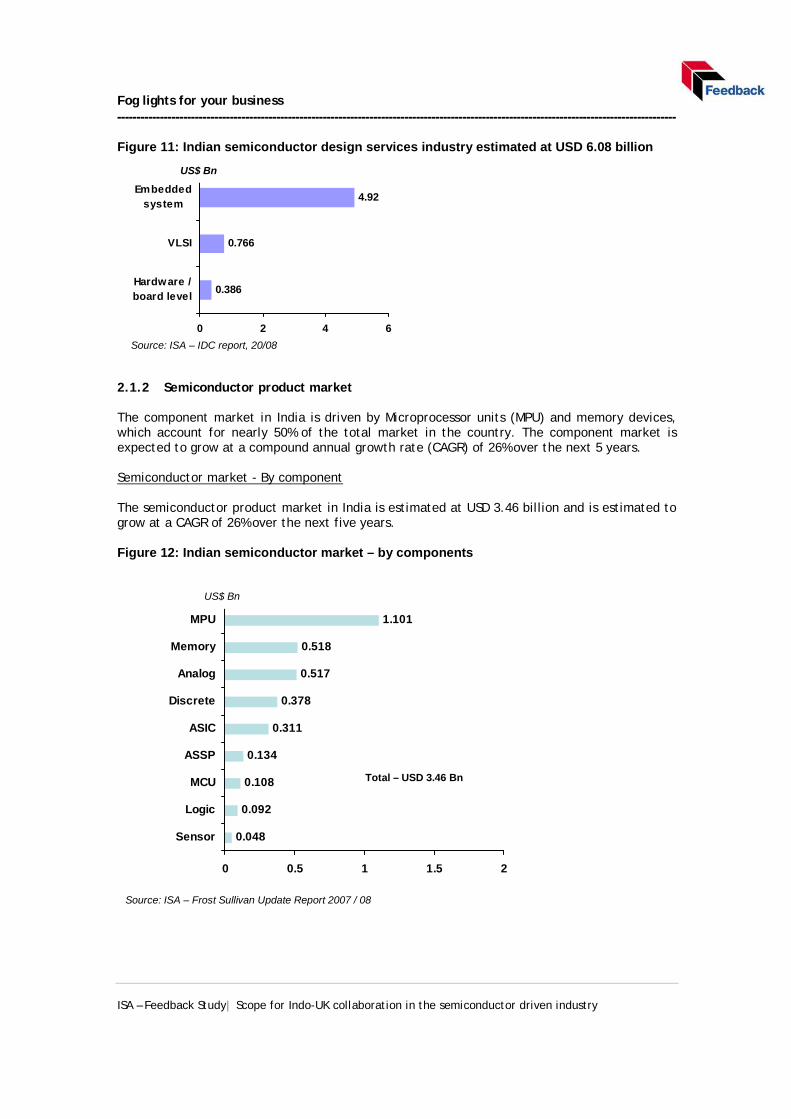

Figure 11: Indian semiconductor design services industry estimated at USD 6.08 Bn

23

Figure 12: Indian semiconductor market – by components 23

Figure 13: Indian semiconductor market – by applications 24

Figure 14: Geographical clusters in semiconductor activity in India 24

Figure 15: Overview of the Indian technical education structure 26

Figure 16: Level of semiconductor activities in Indian universities 36

Figure 17: Application – product matrix 38

Figure 18: Depicts the percentage market breakdown 41

Figure 19: Structure of the semiconductor industry in the UK 42

Figure 20: Major technology platforms 45

Figure 21: Hardware design skills across UK 45

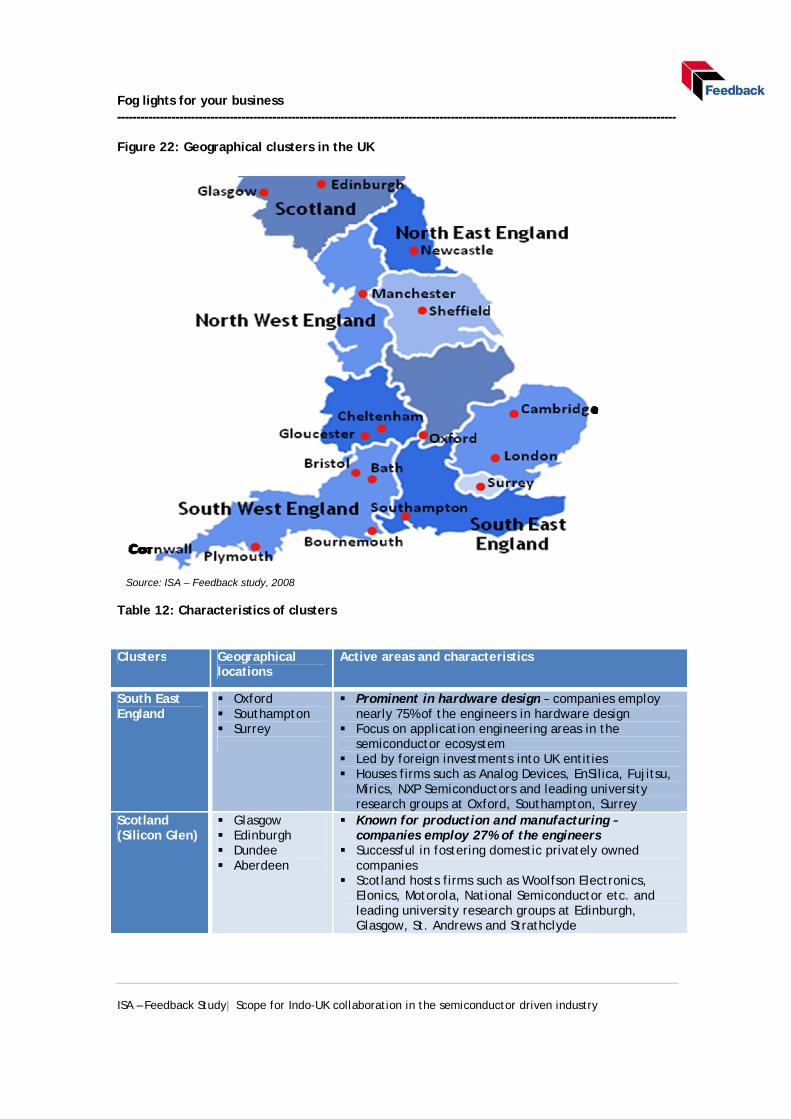

Figure 22: Geographical clusters in the UK 47

Figure 23: Competency of select UK universities in design skills 51

Figure 24: Competency of select UK universities in application segments 51

Figure25: Depicts the level of semiconductor activities in the UK universities

60

Figure 26: Application – product matrix 61

Figure 27: Application – product matrix 62

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

Table Page Number

Table 1: Ratings on a 1 to 10 point scale based on the activities, focus, strengths and weaknesses of counterparts across India and UK

11

Table 2: Geographic clusters and their characteristics 25

Table3: Nature of research on semiconductors in Indian universities 27

Table 4: Indicative list of active incubators in Indian institutes 29

Table 5: Indicative list of successful start-ups 29

Table 6: Some instances of university-industry collaboration in the area of semiconductors

30

Table 7: Challenges faced by institutes for research activities 32

Table 8: Incentives for setting up fab units in SEZ location 34

Table 9: Application versus product matrix 37

Table 10: Classification for application versus product matrix 37

Table 11: UK companies present in India – a few examples 39

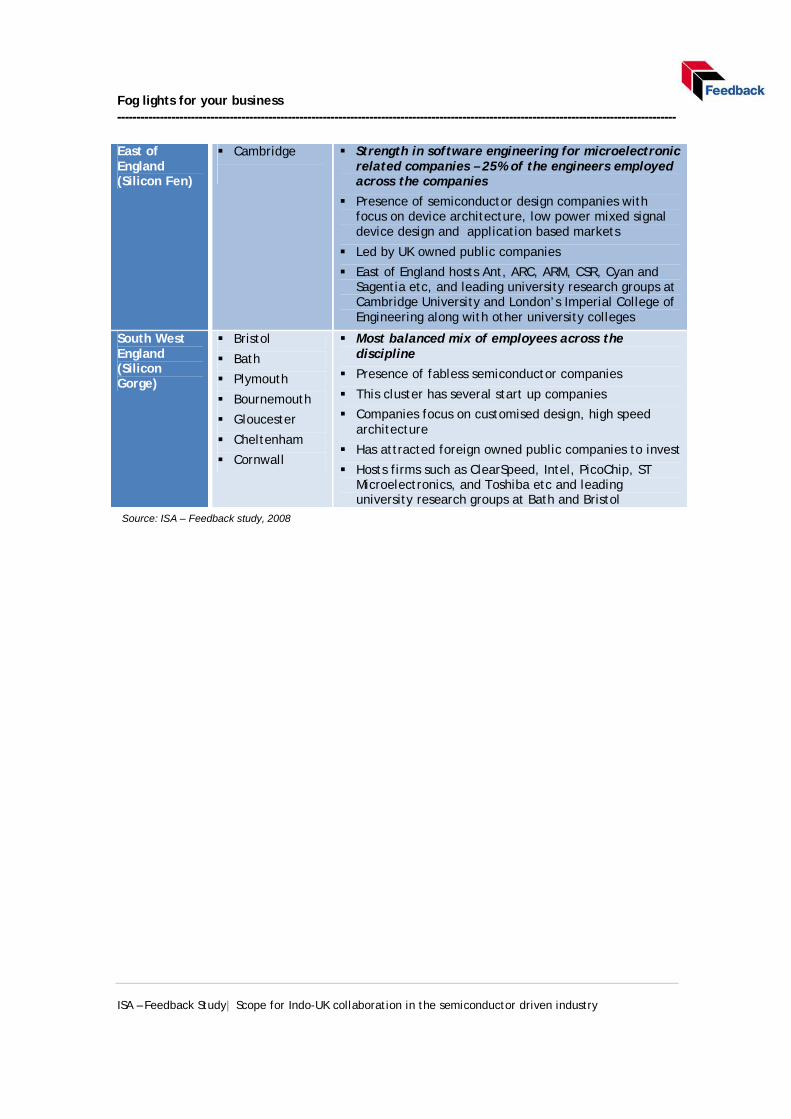

Table 12: Characteristics of clusters 47

Table 13 Depicts select examples of university-industry collaboration 53

Table 14: Allied organisations and their activities in the areas of semiconductors

58

Table 15: Definitions 60

Table 16: Definitions 61

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

Engagement background ISA is the trade body representing the Indian semiconductor driven industry. ISA has around 130 members from the semiconductor driven industry from India and outside. These include design companies, solar fabs, manufacturing companies, VLSI companies, EDA companies and others in the ecosystem like venture funds, legal and academic institutions. ISA aims to establish India as the preferred global semiconductor destination. It is committed towards building global awareness for the Indian semiconductor driven industry and supporting its growth through focused activities. ISA has played a prominent role in supporting the Government of India in the formation of the Semiconductor Policy 2007. UK Trade & Investment (UKTI) is a Government organisation that helps UK-based companies succeed in an increasingly global economy. The range of expert services offered by UKTI is tailored to the needs of individual businesses to maximise their international success. They provide companies with knowledge, advice and practical support. UKTI’s aim is to enhance the competitiveness of companies in the UK through overseas trade and investments and to attract a continuing high level of quality foreign direct investment. Science and Innovation Network (SIN) is an arm of the UKTI. It was established by the UK’s Foreign Commonwealth Office in 2000, in response to the growing importance of science, technology and innovation for the country’s future. SIN helps deliver UK success by:

· facilitating collaboration between UK universities and research laboratories and public and private-sector counterparts abroad; bilateral scientific workshops, conferences and other networking activities

· raising awareness of the UK as a global leader in science and innovation; providing expert advice and leadership in support of R&D investment projects; working with UK Trade and Investment to help technology-intensive UK-based companies penetrate the supply chains of multi-national enterprises and global markets; providing intelligence to UK innovation networks on overseas science and technology advances

· gathering and disseminating best practice in science and innovation policy; developing international frameworks in breakthrough technologies such as stem cell research; promoting UK excellence in science with key international decision-makers

ISA-UKTI wishes to promote Indo-UK collaboration in the semiconductor-driven industry. This study seeks to set out the potential grounds for the collaboration. Key business objectives 1. Identify particular sectors or areas of the Indian semiconductor industry that can be

supported by UK companies 2. Assess the synergies between the UK semiconductor sector and the Indian counterpart 3. Assess the cluster of semiconductor industry in the UK that could forge partnerships with

the Indian counterpart 4. Identify potential areas where the UK research community could help the Indian

semiconductor industry 5. Potential effects of India’s new semiconductor policy on Foreign Direct Investment (FDI) in

research, design and manufacturing 6. Assess prospects for venture capital funding for UK-based embedded companies 7. Identify and suggest mechanisms likely to be most successful in facilitating UK companies

to collaborate with the Indian semiconductor sector 8. Identify potential for the Indian semiconductor industry to work with UK universities

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

9. To assess whether ISA or UKTI could be a facilitator or a single point of contact for the Indo-UK embedded sector

Approach and methodology

Interviews with key stakeholders through the primary route to establish the level of semiconductor activity and the scope for collaboration

• Primary interviews with stakeholders across firms, academia, associations and Government • Lists of respondents built through discussions with ISA-UKTI and using Feedback’s body of

knowledge

• Relevant secondary data sourced – Published information; industry / association reports, etc. • Web based searches

Primary Secondary

Universities and

companies in India and UK

Industry experts,

Government

Annual reports, industry

publications, web sources

Methodology

Sources

Focus

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

1. Executive Summary

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

Summary

This report presents the results and analysis of the study “Scope for Indo – UK collaboration in

the semiconductor-driven industry”. The report has been undertaken by ISA – Feedback during

February - March 2008. Our primary target audience included universities, companies, venture

capitalists and other stakeholders. The research output provides a detailed understanding of

the various activities undertaken in research and incubation services by universities, product

and applications focus of companies, geographical clusters, industry – university collaborations

and the level of Government support/ both in India and the UK in the semiconductor industry.

Major findings of the research

§ Semiconductor driven activities both in India and the UK are primarily in the area of

design. Both countries have limited production and manufacturing infrastructure.

Current demand is met through imports. Communications, IT and consumer electronics

are the major application areas in India accounting for 85% of demand. Industrial,

telecommunications, transport and consumer electronics are the major applications in

the UK, accounting for 50% of the demand.

§ The UK design industry is dominated by foreign owned companies with widespread

leading edge digital and analog design activities. Major design strengths of UK

companies are in the areas of VLSI, FPGA and CAD tool development for wireless,

digital media and communications applications. Indian design houses include both

captive arms of global semiconductor companies and third party service providers

executing design projects. There are only a few companies capable of complete

product development. This is in contrast to companies in the UK whose focus and

strengths are in IP creation and complete product development. Indian companies

specialise in VLSI, hardware / board level design and embedded systems in wireless

communication, computing and networking.

§ The UK has four geographic regions with high concentration of semiconductor

activities; each region appears to have distinct characteristics. South East of England

which has significant foreign investments into UK entities has a strong focus on

hardware design. Scotland (Silicon Glen) known for production and manufacturing in

the UK, has a large number of domestic owned companies. East of England (Silicon Fen)

with strengths in software engineering for microelectronic related companies is

dominated by UK owned public companies. South West of England (Silicon George) with

a balanced mix of companies across disciplines has attracted more foreign owned

public company investments. Each of these locations is characterised by strong

academia support to meet manpower requirements of the companies.

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

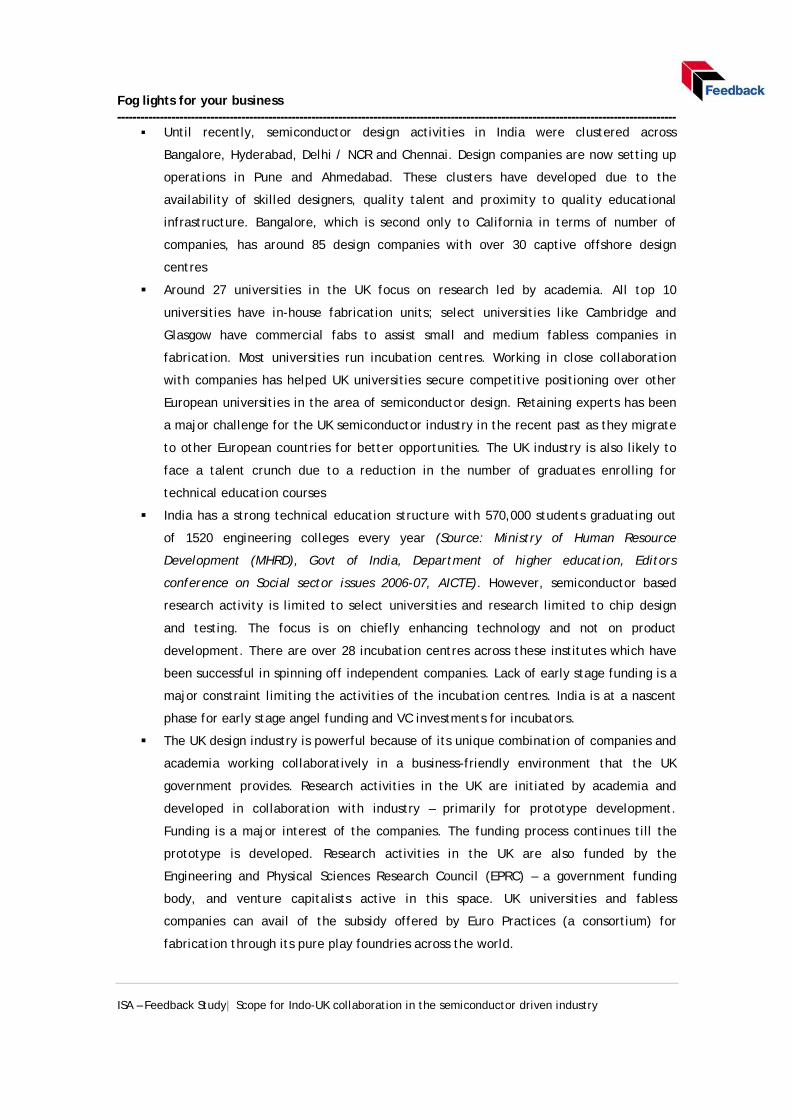

§ Until recently, semiconductor design activities in India were clustered across

Bangalore, Hyderabad, Delhi / NCR and Chennai. Design companies are now setting up

operations in Pune and Ahmedabad. These clusters have developed due to the

availability of skilled designers, quality talent and proximity to quality educational

infrastructure. Bangalore, which is second only to California in terms of number of

companies, has around 85 design companies with over 30 captive offshore design

centres

§ Around 27 universities in the UK focus on research led by academia. All top 10

universities have in-house fabrication units; select universities like Cambridge and

Glasgow have commercial fabs to assist small and medium fabless companies in

fabrication. Most universities run incubation centres. Working in close collaboration

with companies has helped UK universities secure competitive positioning over other

European universities in the area of semiconductor design. Retaining experts has been

a major challenge for the UK semiconductor industry in the recent past as they migrate

to other European countries for better opportunities. The UK industry is also likely to

face a talent crunch due to a reduction in the number of graduates enrolling for

technical education courses

§ India has a strong technical education structure with 570,000 students graduating out

of 1520 engineering colleges every year (Source: Ministry of Human Resource

Development (MHRD), Govt of India, Department of higher education, Editors

conference on Social sector issues 2006-07, AICTE). However, semiconductor based

research activity is limited to select universities and research limited to chip design

and testing. The focus is on chiefly enhancing technology and not on product

development. There are over 28 incubation centres across these institutes which have

been successful in spinning off independent companies. Lack of early stage funding is a

major constraint limiting the activities of the incubation centres. India is at a nascent

phase for early stage angel funding and VC investments for incubators.

§ The UK design industry is powerful because of its unique combination of companies and

academia working collaboratively in a business-friendly environment that the UK

government provides. Research activities in the UK are initiated by academia and

developed in collaboration with industry – primarily for prototype development.

Funding is a major interest of the companies. The funding process continues till the

prototype is developed. Research activities in the UK are also funded by the

Engineering and Physical Sciences Research Council (EPRC) – a government funding

body, and venture capitalists active in this space. UK universities and fabless

companies can avail of the subsidy offered by Euro Practices (a consortium) for

fabrication through its pure play foundries across the world.

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

§ In contrast to the UK, research activities in India focusing on the area of Electronic

Design Automation are initiated by companies. Academia-industry collaboration for

research is not comprehensive. Industry funding for research is limited to providing

tools and lab equipment, and is not focussed on the entire life cycle of the project.

The impetus to become a major hub for the entire semiconductor value chain has

however begun in earnest with support from the Indian Government.

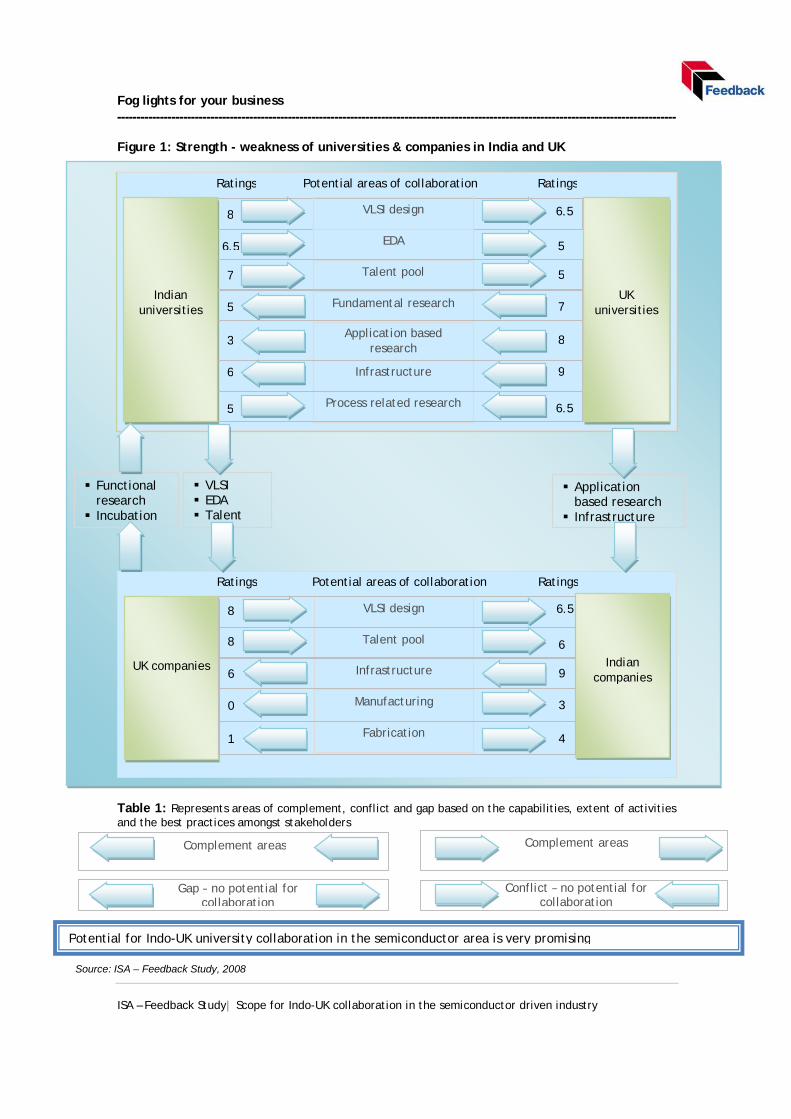

Conclusions and recommendations

The study reveals a synergy between India and the UK primarily in the areas of design, device

and applications. Figure 1 represents the strength and weakness of universities and companies

in India and the UK. Area of collaboration is derived based on the capabilities, extent of

activities, best practices followed across the counterparts in India and UK. For example, UK

universities score high in the areas of application based research, infrastructure and

fundamental research when compared to Indian universities. These are the complement areas

where Indian universities tend to gain out of the collaborations with the UK universities.

Similarly, there is scope for collaboration between the UK companies and the Indian

universities; the UK companies can look at local talent, EDA capabilities and VLSI design

expertise as the potential areas of collaboration. The direction of the arrow as shown in the

Table 1 shows the potential information flow between the counterparts in India and UK.

Arrows following one another indicates the potential areas for collaboration as they

complement each other. The arrows in two opposite directions indicate the gap – no potential

for collaboration and the arrows moving head on indicate the conflict areas – which mean

there is very little scope for collaboration, as each one is self-sufficient.

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

Figure 1: Strength - weakness of universities & companies in India and UK

Table 1: Represents areas of complement, conflict and gap based on the capabilities, extent of activities and the best practices amongst stakeholders

UK companies

Fabrication

Manufacturing

Infrastructure

Talent pool

VLSI design

Indian companies

Potential areas of collaboration Ratings Ratings

6.5

6

9

3

4

8

8

6

0

1

Indian universities

UK universities

Potential areas of collaboration Ratings Ratings

5

5

7

8

9

6.5

8

6.5

7

5

3

6

5 Process related research

Infrastructure

Application based research

Fundamental research

Talent pool

EDA

VLSI design 6.5

Complement areas Complement areas

Gap – no potential for collaboration

Conflict – no potential for collaboration

§ VLSI § EDA § Talent

§ Application based research

§ Infrastructure

§ Functional research

§ Incubation

Potential for Indo-UK university collaboration in the semiconductor area is very promising

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

Figure 2: Scope for collaboration between Indian and UK universities

UK universitie

Indian universiti

• Faster prototyping

• Access to

quality talent

• Access to advanced tools and facilities for research

• Scope to work

on next level technology

Areas of collaboration Benefit Benefit

• VLSI design • EDA • Fundamental research • Application

research • Talent pool • Infrastructure • Embedded systems

· Academia initiated research – primary focus

· Limited number of students engaged in design

· Strength lies is fundamental research

· State of the art infrastructure; strong government support

· Chip design and testing · Embedded systems · Core strengths lie in VLSI

design, modelling and simulation

· Strong analytical skill sets

· Quality of talent pool · Quality of educational

infrastructure

Ø Assistance on

VLSI design and analytical skills from Indian Universities

Ø Student Academia Internship programme

Ø Access to specialised labs based in UK

UK universities Indian universities Benefit analysis

Knowledge transfer through university exchange programmes and funding by industry & Government will be critical to success

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

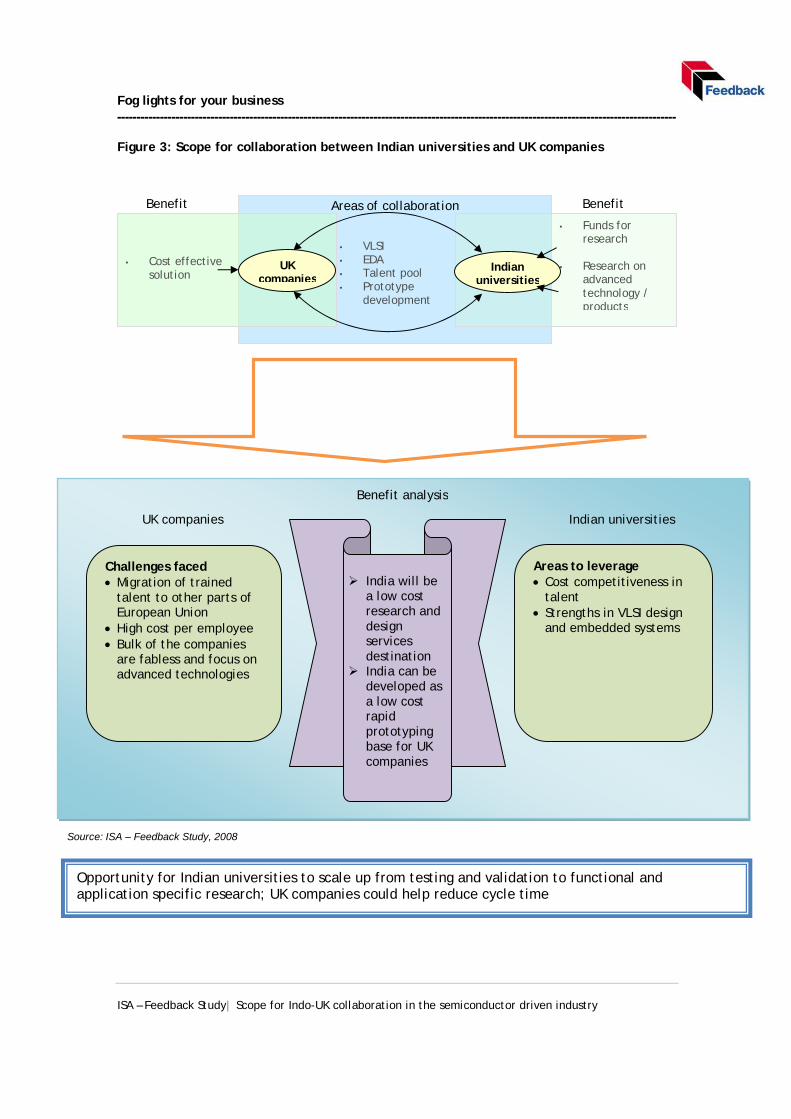

Figure 3: Scope for collaboration between Indian universities and UK companies

UK companies

Indian universities

• Cost effective solution

• Funds for research

• Research on

advanced technology / products

• VLSI • EDA • Talent pool • Prototype

development

Benefit Benefit Areas of collaboration

Challenges faced · Migration of trained

talent to other parts of European Union

· High cost per employee · Bulk of the companies

are fabless and focus on advanced technologies

Areas to leverage · Cost competitiveness in

talent · Strengths in VLSI design

and embedded systems

Ø India will be

a low cost research and design services destination

Ø India can be developed as a low cost rapid prototyping base for UK companies

UK companies Indian universities

Benefit analysis

Opportunity for Indian universities to scale up from testing and validation to functional and application specific research; UK companies could help reduce cycle time

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

Figure 4: Scope for collaboration between Indian and UK companies

UK companies

Indian companies

• Talent cost advantage

• Availability of

trained designers

• Scope to work on advanced tools

• Scope to work

on application specific research

• VLSI • Embedded systems • Hardware/ board

design • Talent pool • Knowledge transfer

on technology tools

Areas of collaboration Benefit Benefit

Challenges faced · Talent crunch; high cost

of manpower · Large number of design

(fabless) companies

Areas to leverage · Availability of talent with

potential to deliver on application research

· Small start ups, currently focussing on circuit design and CAD simulation

Ø India will be

a low cost research and product development destination

UK companies Indian companies

Benefit analysis

Indian & UK companies could complement each others’ strengths for faster product development

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

Figure 5: Scope for collaboration between Indian companies and UK universities

UK universities

Indian companies

• Funding advantage

• Application specific product research

• Faster

prototype development

• Application specific research

• Infrastructure (fabs and labs)

Areas of collaboration Benefit Benefit

· State of the art infrastructure

· Application specific research focus

· Focus on products for current market needs rather than futuristic technologies

Ø Indian

companies will have access to state of art infrastructure for product development

UK universities Indian companies Benefit analysis

Indian companies could leverage strengths of UK universities for state-of-the-art research

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

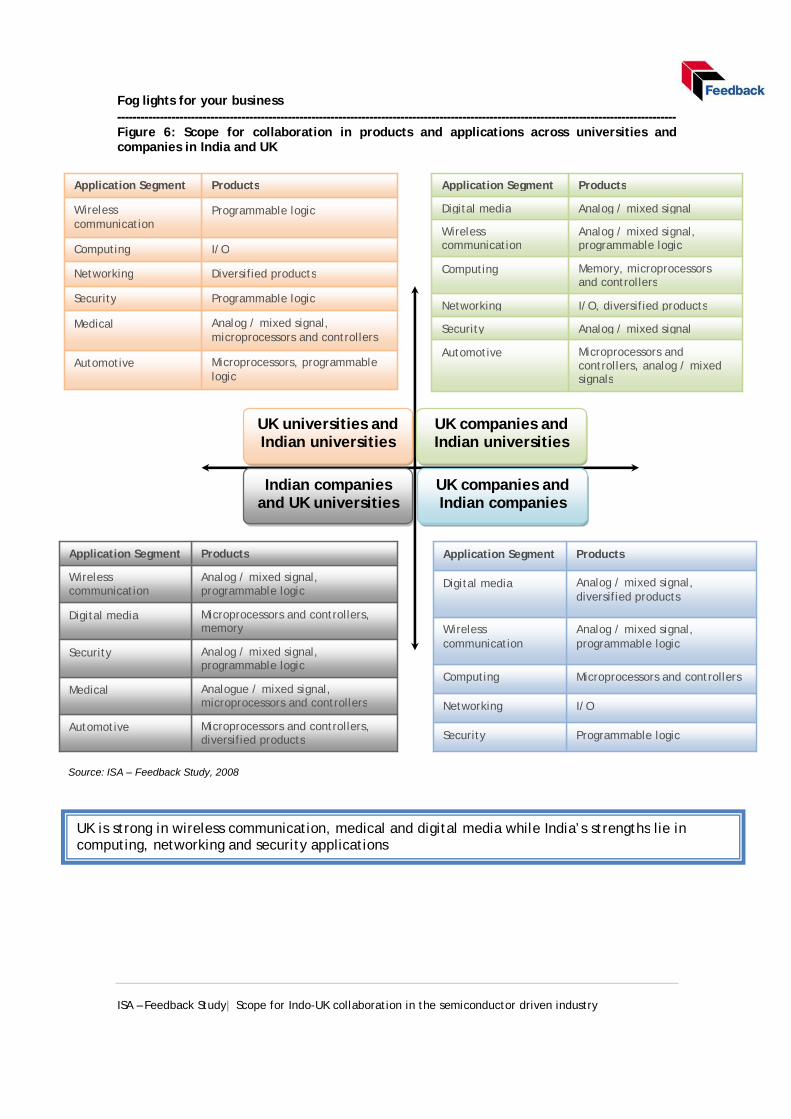

Figure 6: Scope for collaboration in products and applications across universities and companies in India and UK

Microprocessors, programmable logic

Automotive

Analog / mixed signal, microprocessors and controllers

Medical

Programmable logic Security

Diversified products Networking

I/O Computing

Programmable logic Wireless communication

Products Application Segment

Microprocessors and controllers, analog / mixed signals

Automotive

Analog / mixed signal Security

I/O, diversified products Networking

Memory, microprocessors and controllers

Computing

Analog / mixed signal, programmable logic

Wireless communication

Analog / mixed signal Digital media

Products Application Segment

Programmable logic Security

I/O Networking

Microprocessors and controllers Computing

Analog / mixed signal, programmable logic

Wireless communication

Analog / mixed signal, diversified products

Digital media

Products Application Segment

Microprocessors and controllers, memory

Digital media

Microprocessors and controllers, diversified products

Automotive

Analogue / mixed signal, microprocessors and controllers

Medical

Analog / mixed signal, programmable logic

Security

Analog / mixed signal, programmable logic

Wireless communication

Products Application Segment

UK companies and Indian companies

Indian companies and UK universities

UK universities and Indian universities

UK companies and Indian universities

UK is strong in wireless communication, medical and digital media while India’s strengths lie in computing, networking and security applications

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

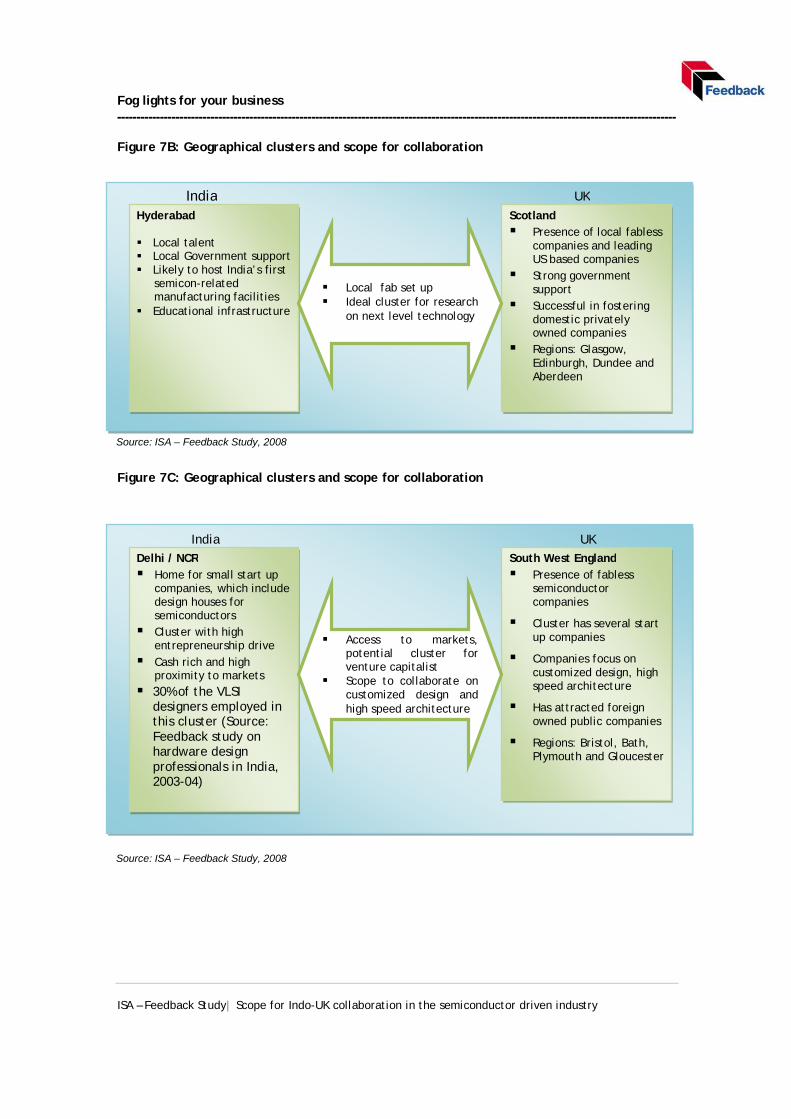

Figure 7: Geographical clusters and scope for collaboration

Figure 7A: Geographical clusters and scope for collaboration

Bangalore § Top global cluster in

semiconductor design § Home for over 85

design companies with over 30 captive offshore design centres

§ Nearly 57% of the VLSI designers employed in the semiconductor design companies in this cluster (Source: Feedback study on hardware design professionals in the country, 2003-04)

India South East England § Focus on application

engineering in the semiconductor ecosystem

§ Prominent in hardware design

§ Led by foreign investments into UK

§ Regions: Oxford, Southampton, Surrey

East of England § Presence of

semiconductor design companies with focus on device and application based markets

§ Lead by UK owned public companies

§ Region: Cambridge

§ Talent availability to

work on semiconductor design

§ Rapid growth and development in semiconductors

§ Collaboration from design to application of semiconductors

UK

Source: ISA – Feedback Study, 2008

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

Figure 7B: Geographical clusters and scope for collaboration Figure 7C: Geographical clusters and scope for collaboration

Hyderabad

§ Local talent § Local Government support § Likely to host India’s first

semicon-related manufacturing facilities

§ Educational infrastructure

India Scotland § Presence of local fabless

companies and leading US based companies

§ Strong government support

§ Successful in fostering domestic privately owned companies

§ Regions: Glasgow, Edinburgh, Dundee and Aberdeen

§ Local fab set up § Ideal cluster for research

on next level technology

UK

Delhi / NCR § Home for small start up

companies, which include design houses for semiconductors

§ Cluster with high entrepreneurship drive

§ Cash rich and high proximity to markets

§ 30% of the VLSI designers employed in this cluster (Source: Feedback study on hardware design professionals in India, 2003-04)

India South West England § Presence of fabless

semiconductor companies

§ Cluster has several start up companies

§ Companies focus on customized design, high speed architecture

§ Has attracted foreign owned public companies

§ Regions: Bristol, Bath, Plymouth and Gloucester

§ Access to markets, potential cluster for venture capitalist

§ Scope to collaborate on customized design and high speed architecture

UK

Source: ISA – Feedback Study, 2008

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

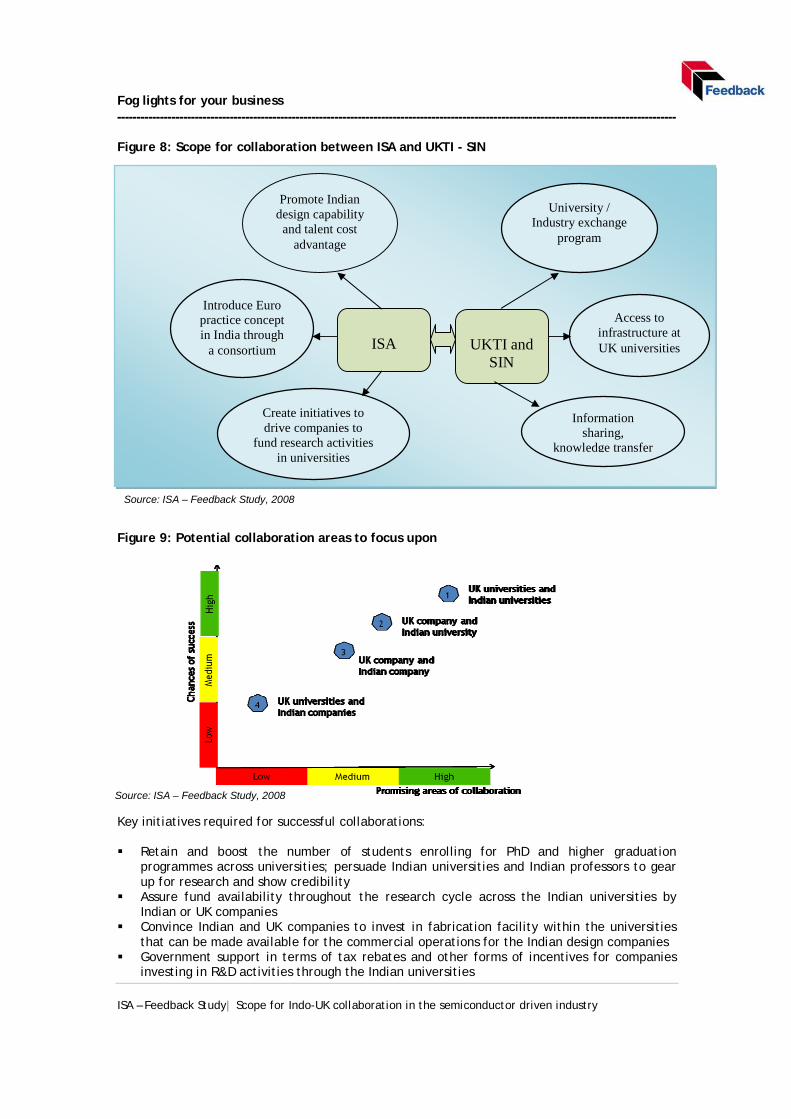

Figure 8: Scope for collaboration between ISA and UKTI - SIN

Figure 9: Potential collaboration areas to focus upon

Key initiatives required for successful collaborations: § Retain and boost the number of students enrolling for PhD and higher graduation

programmes across universities; persuade Indian universities and Indian professors to gear up for research and show credibility

§ Assure fund availability throughout the research cycle across the Indian universities by Indian or UK companies

§ Convince Indian and UK companies to invest in fabrication facility within the universities that can be made available for the commercial operations for the Indian design companies

§ Government support in terms of tax rebates and other forms of incentives for companies investing in R&D activities through the Indian universities

Promote Indian design capability

and talent cost advantage

Introduce Euro practice concept in India through

a consortium

Create initiatives to drive companies to

fund research activities in universities

ISA

UKTI and

SIN

University / Industry exchange

program

Access to infrastructure at UK universities

Information sharing,

knowledge transfer

Source: ISA – Feedback Study, 2008

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

2. India semiconductor market details

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

2.1 India semiconductor market overview

The middle class population is estimated to grow from 360 mn in 2006 to 525 mn in 2010. The annual household income for this class is between USD 10,000 to 55,500 (Source: India Brand Equity Forum, IBEF). This class is driving the electronic products market in India which has been estimated at USD 16.1 billion in 2006-07 (Source: Electronics Component Manufacturers Association). India's total semiconductor consumption is estimated at USD 3.46 billion in 2007–08 (Source: ISA- Frost Update Report 2007/08) primarily serviced by imports. The local manufacturing base is inadequate to cater to the domestic demand, which is increasing at 26% per annum. Prominent global semiconductor companies have been present in India for a while and operate through liaison offices, sales and marketing offices, design houses and/or through a well entrenched network of distributors and resellers. India has emerged as a strong base for R&D centres. Indian Design Centres or IDCs have graduated from executing small projects to driving critical ones. It is becoming increasingly common to find leading edge designs for the global market being driven by these IDCs. In addition, IDCs provide global support on tools and methodology. The design market has grown significantly due to the increasing number of international companies setting up offshore design and development centres in India and through expansion of current centres. Triggers for these activities include the following:

· Market need for regular introduction of new product variants / models has forced original equipment manufacturers (OEMs) / product companies to seek reduction in product development cycle time through outsourcing arrangements

· Declining margins and R&D budgets have driven companies to look for cost effective solutions without compromising on the quality of work

· Availability of a large base of engineering workforce coupled with their proficiency in English have made India an attractive destination for design and development

· Electronic design automation (EDA) companies (both product and services) are the starting block for the VLSI and hardware board design market. EDA companies have taken the lead in developing engineering human resource for the industry in India.

Figure 10: Structure of the semiconductor industry in India

Semiconductor Product Market

Semiconductor Device

Manufacturing

Semiconductor Design Services

• Semiconductor design continues to remain a core strength of India

• As per industry leaders, around 150 companies which specialize in VLSI design, embedded systems and hard ware / board level design are present in India

• VLSI design, hardware / board design, embedded systems market is estimated at USD 6.08 bn

• There is limited semiconductor manufacturing activity in India at present. Currently, India has no commercial wafer fab plants

· Design houses in India get chips fabricated at TSMC, SMIC and other pure play foundries

• Five major application segments contribute to the semiconductor demand in India

- Telecom - IT and Office Automation - Electronics - Industrial - Automotive

• Telecom, IT and Electronics are the high growth areas, accounting for 85%1 of total demand

• Consumption of semiconductors is estimated at USD 3.46 bn in 2007 – 081

1 Based on ISA – Frost Sullivan Update Report 2007 / 08 Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

2.1.1 Semiconductor design services The Indian semiconductor industry is dominated by players engaged in chip design. The semiconductor design space in the country consists of VLSI design, board design and embedded system companies - India has around 150 chip design companies (both Indian and subsidiaries of US and European chip firms), with almost all global semiconductor design companies having a presence here. Industry leaders believe that India is becoming a ‘design store’ with strengths in intellectual property (IP) development, integration and embedded system services. The ISA – IDC Report 2008 estimates the integrated chip design workforce in India to be around 130,000 while those working on embedded software total around 107,000. VLSI design From an electronics design perspective, the market can be divided into three segments: · The first segment comprises global MNCs and market makers who employ around 14,000

designers. They are associated with design chain methodology and the challenges associated with shrinking process nodes (65 nm and below)

· The second segment is shared by two domains: ‘pure play’ design services companies and fabless semiconductor companies. Over the last decade, multinationals have been associated with Indian service companies for complex projects in the design chain. Design services companies have moved up the value chain and bagged prestigious projects that have a worldwide impact

· The third segment is the Government including defence and space, with an increased focus on communication and defence products. The R&D centres of these organisations are producing complex designs.

VLSI design activities are clustered in four major cities of India. Bangalore is the biggest cluster, followed by Hyderabad, Delhi NCR and Chennai. Bangalore has around 85 of the 150 firms (including multinationals) engaged in chip design in India – making it one of the major global clusters in chip design along with the Silicon Valley, Cambridge (UK) and Taiwan. India is also emerging as the hotbed of wireless IC design with around 38% of Indian designers working on designs targeting wireless and mobile applications, compared to around 22% in Europe. (Source: India Brand Equity Forum, IBEF) Currently, product design involves IC design, board design and embedded software development – all done in conjunction with each other. The traditional separation between software digital logic analog and PCB is rapidly breaking down resulting in design convergence. This industry is witnessing rapid changes in technology – moving towards 65 nm geometry.

Embedded system design India’s strength in embedded design is reflected in its expertise in handling hardware and embedded design required to support lower power nodes. An increase in the number of international companies establishing their offshore centres in India has in turn spurred growth in Indian design services. Global majors have also shown confidence in the capabilities of Indian design companies by awarding them critical projects. India’s competitive edge in the global market is its talent base with design capabilities. Global companies are aware of the availability of this talent pool and are leveraging it effectively.

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

Figure 11: Indian semiconductor design services industry estimated at USD 6.08 billion

2.1.2 Semiconductor product market The component market in India is driven by Microprocessor units (MPU) and memory devices, which account for nearly 50% of the total market in the country. The component market is expected to grow at a compound annual growth rate (CAGR) of 26% over the next 5 years. Semiconductor market - By component The semiconductor product market in India is estimated at USD 3.46 billion and is estimated to grow at a CAGR of 26% over the next five years. Figure 12: Indian semiconductor market – by components

0.386

0.766

4.92

0 2 4 6

Hardware /board level

VLSI

Embeddedsystem

US$ Bn

Source: ISA – IDC report, 20/08

0.048

0.092

0.108

0.134

0.311

0.378

0.517

0.518

1.101

0 0.5 1 1.5 2

Sensor

Logic

MCU

ASSP

ASIC

Discrete

Analog

Memory

MPU

Total – USD 3.46 Bn

US$ Bn

Source: ISA – Frost Sullivan Update Report 2007 / 08

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

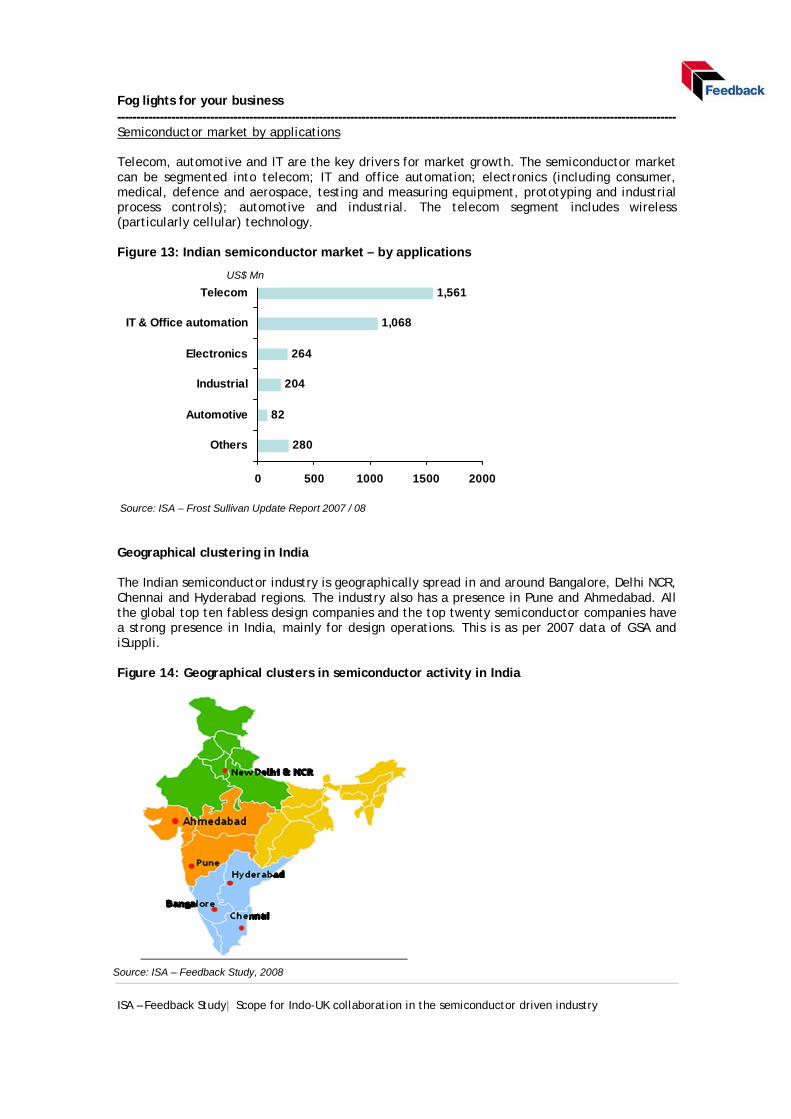

Semiconductor market by applications Telecom, automotive and IT are the key drivers for market growth. The semiconductor market can be segmented into telecom; IT and office automation; electronics (including consumer, medical, defence and aerospace, testing and measuring equipment, prototyping and industrial process controls); automotive and industrial. The telecom segment includes wireless (particularly cellular) technology. Figure 13: Indian semiconductor market – by applications Geographical clustering in India The Indian semiconductor industry is geographically spread in and around Bangalore, Delhi NCR, Chennai and Hyderabad regions. The industry also has a presence in Pune and Ahmedabad. All the global top ten fabless design companies and the top twenty semiconductor companies have a strong presence in India, mainly for design operations. This is as per 2007 data of GSA and iSuppli.

Figure 14: Geographical clusters in semiconductor activity in India

280

82

204

264

1,068

1,561

0 500 1000 1500 2000

Others

Automotive

Industrial

Electronics

IT & Office automation

Telecom

US$ Mn

Source: ISA – Frost Sullivan Update Report 2007 / 08

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

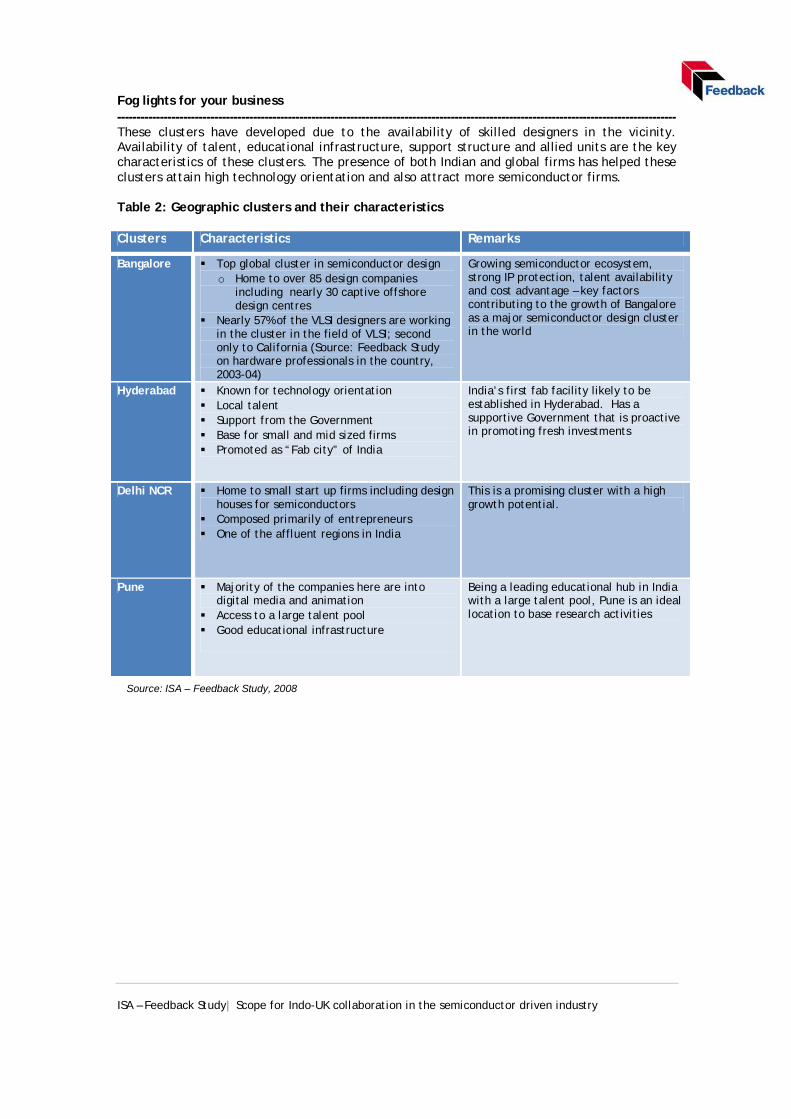

These clusters have developed due to the availability of skilled designers in the vicinity. Availability of talent, educational infrastructure, support structure and allied units are the key characteristics of these clusters. The presence of both Indian and global firms has helped these clusters attain high technology orientation and also attract more semiconductor firms. Table 2: Geographic clusters and their characteristics Clusters Characteristics Remarks

Bangalore § Top global cluster in semiconductor design o Home to over 85 design companies

including nearly 30 captive offshore design centres

§ Nearly 57% of the VLSI designers are working in the cluster in the field of VLSI; second only to California (Source: Feedback Study on hardware professionals in the country, 2003-04)

Growing semiconductor ecosystem, strong IP protection, talent availability and cost advantage – key factors contributing to the growth of Bangalore as a major semiconductor design cluster in the world

Hyderabad § Known for technology orientation § Local talent § Support from the Government § Base for small and mid sized firms § Promoted as “Fab city” of India

India’s first fab facility likely to be established in Hyderabad. Has a supportive Government that is proactive in promoting fresh investments

Delhi NCR § Home to small start up firms including design houses for semiconductors

§ Composed primarily of entrepreneurs § One of the affluent regions in India

This is a promising cluster with a high growth potential.

Pune § Majority of the companies here are into digital media and animation

§ Access to a large talent pool § Good educational infrastructure

Being a leading educational hub in India with a large talent pool, Pune is an ideal location to base research activities

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

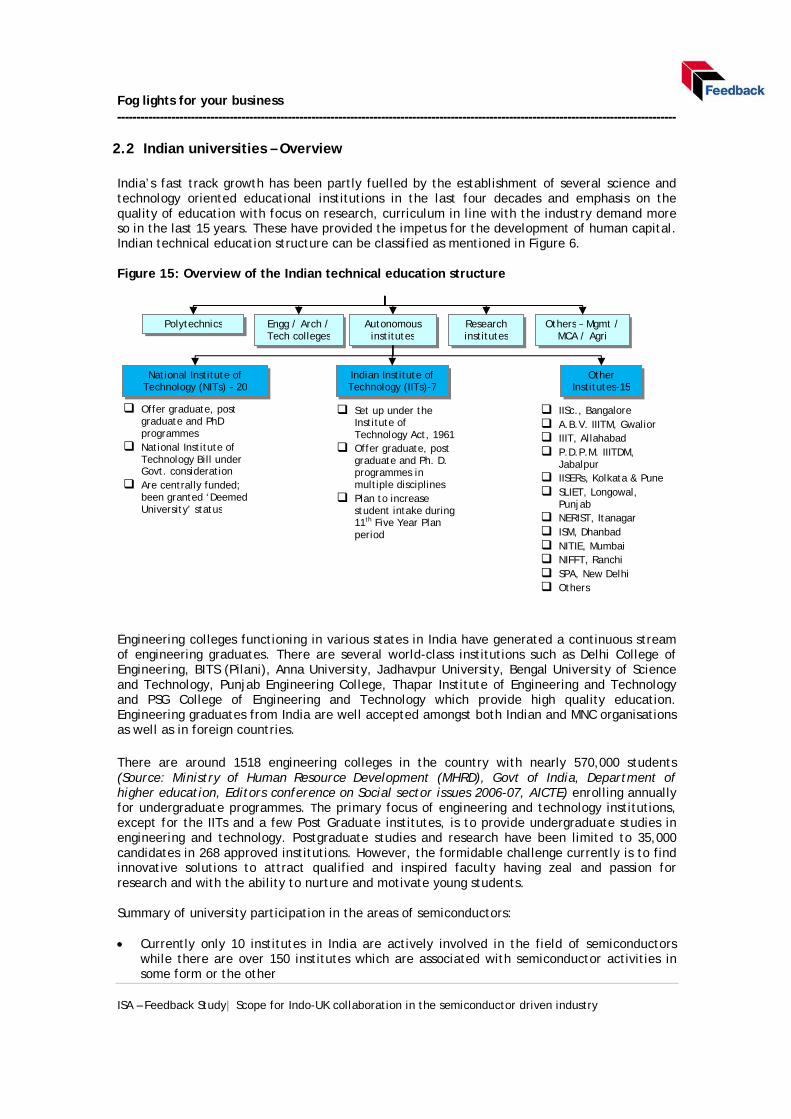

2.2 Indian universities – Overview India’s fast track growth has been partly fuelled by the establishment of several science and technology oriented educational institutions in the last four decades and emphasis on the quality of education with focus on research, curriculum in line with the industry demand more so in the last 15 years. These have provided the impetus for the development of human capital. Indian technical education structure can be classified as mentioned in Figure 6. Figure 15: Overview of the Indian technical education structure

Engineering colleges functioning in various states in India have generated a continuous stream of engineering graduates. There are several world-class institutions such as Delhi College of Engineering, BITS (Pilani), Anna University, Jadhavpur University, Bengal University of Science and Technology, Punjab Engineering College, Thapar Institute of Engineering and Technology and PSG College of Engineering and Technology which provide high quality education. Engineering graduates from India are well accepted amongst both Indian and MNC organisations as well as in foreign countries. There are around 1518 engineering colleges in the country with nearly 570,000 students (Source: Ministry of Human Resource Development (MHRD), Govt of India, Department of higher education, Editors conference on Social sector issues 2006-07, AICTE) enrolling annually for undergraduate programmes. The primary focus of engineering and technology institutions, except for the IITs and a few Post Graduate institutes, is to provide undergraduate studies in engineering and technology. Postgraduate studies and research have been limited to 35,000 candidates in 268 approved institutions. However, the formidable challenge currently is to find innovative solutions to attract qualified and inspired faculty having zeal and passion for research and with the ability to nurture and motivate young students. Summary of university participation in the areas of semiconductors: · Currently only 10 institutes in India are actively involved in the field of semiconductors

while there are over 150 institutes which are associated with semiconductor activities in some form or the other

Engg / Arch / Tech colleges

Research institutes

Others – Mgmt / MCA / Agri

Autonomous institutes

Indian Institute of Technology (IITs)-7

National Institute of Technology (NITs) – 20

Other Institutes-15

Polytechnics

q Set up under the Institute of Technology Act, 1961

q Offer graduate, post graduate and Ph. D. programmes in multiple disciplines

q Plan to increase student intake during 11th Five Year Plan period

q IISc., Bangalore q A.B.V. IIITM, Gwalior q IIIT, Allahabad q P.D.P.M. IIITDM,

Jabalpur q IISERs, Kolkata & Pune q SLIET, Longowal,

Punjab q NERIST, Itanagar q ISM, Dhanbad q NITIE, Mumbai q NIFFT, Ranchi q SPA, New Delhi q Others

q Offer graduate, post graduate and PhD programmes

q National Institute of Technology Bill under Govt. consideration

q Are centrally funded; been granted ‘Deemed University’ status

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

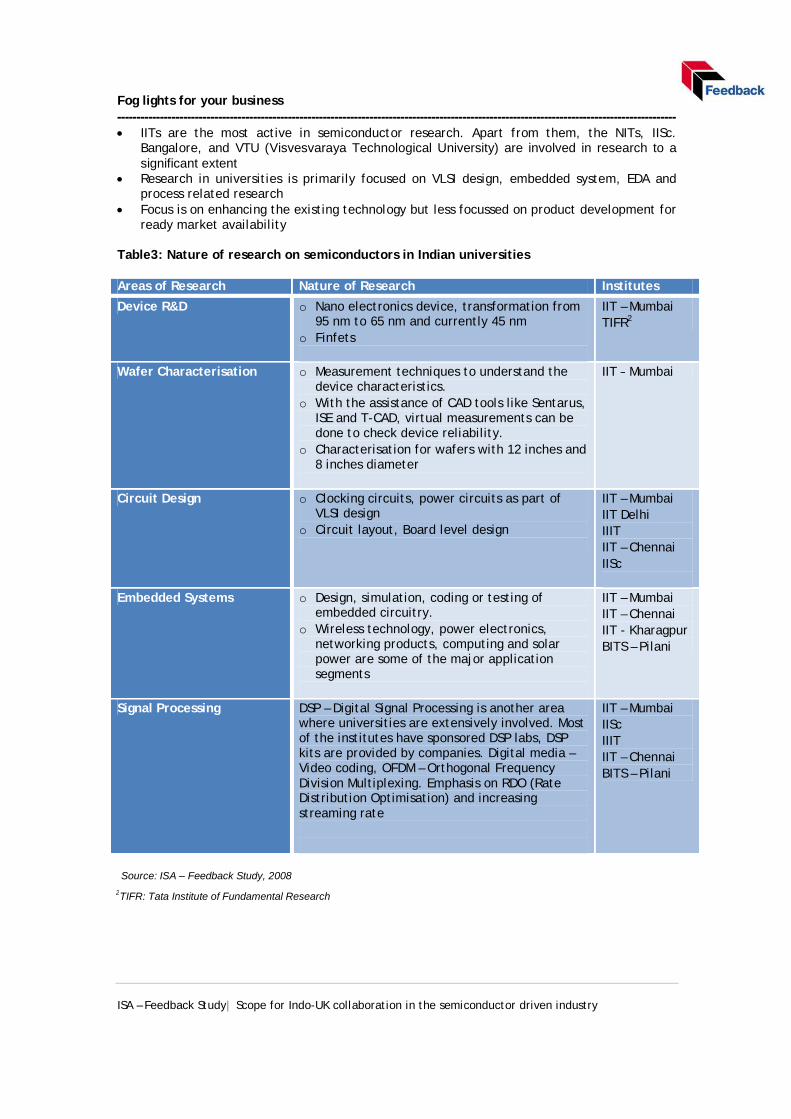

· IITs are the most active in semiconductor research. Apart from them, the NITs, IISc. Bangalore, and VTU (Visvesvaraya Technological University) are involved in research to a significant extent

· Research in universities is primarily focused on VLSI design, embedded system, EDA and process related research

· Focus is on enhancing the existing technology but less focussed on product development for ready market availability

Table3: Nature of research on semiconductors in Indian universities Areas of Research Nature of Research Institutes

Device R&D o Nano electronics device, transformation from 95 nm to 65 nm and currently 45 nm

o Finfets

IIT – Mumbai TIFR2

Wafer Characterisation o Measurement techniques to understand the device characteristics.

o With the assistance of CAD tools like Sentarus, ISE and T-CAD, virtual measurements can be done to check device reliability.

o Characterisation for wafers with 12 inches and 8 inches diameter

IIT – Mumbai

Circuit Design o Clocking circuits, power circuits as part of VLSI design

o Circuit layout, Board level design

IIT – Mumbai IIT Delhi IIIT IIT – Chennai IISc

Embedded Systems o Design, simulation, coding or testing of embedded circuitry.

o Wireless technology, power electronics, networking products, computing and solar power are some of the major application segments

IIT – Mumbai IIT – Chennai IIT - Kharagpur BITS – Pilani

Signal Processing DSP – Digital Signal Processing is another area where universities are extensively involved. Most of the institutes have sponsored DSP labs, DSP kits are provided by companies. Digital media – Video coding, OFDM – Orthogonal Frequency Division Multiplexing. Emphasis on RDO (Rate Distribution Optimisation) and increasing streaming rate

IIT – Mumbai IISc IIIT IIT – Chennai BITS – Pilani

Source: ISA – Feedback Study, 2008 2TIFR: Tata Institute of Fundamental Research

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

2.2.1 Incubation centres Current status Incubation centres are operational at the IISc in Bangalore and in all the IITs in India. These have been set up by the faculty and alumni. Start-up units are spun off after a 2–3 year incubation period. Funding assistance for these start-ups is provided by the institutes and the alumni association. In India, TBIs (Technology Business Incubators) can play an important role in facilitating research. Such incubation centres in the US are known to add value to the institute and the company. They have enabled academic institutes to augment financial resources while pursuing their research activities. Many successful companies were set up and nurtured in this environment. In order to enable speedy commercialisation of R&D and establish closer links between R&D institutes, academia, and industry, the Department of Science and Technology (DST), Government of India, has set up 28 TBIs at various Indian institutes. Activity The start-up units are provided all facilities at the institute including space in the building/ university campus for research work. The focus of these units is to develop a patent which is commercially saleable in the market, after which the units are spun off from the universities. TBIs provide the start-up businesses with mentorship, incubation, patenting and external funding support. They create a research-friendly environment through the following activities:

· Initiating industry – funded projects: TBIs help faculty members undertake R&D projects on individual or joint proposals.

· Setting up work groups: TBIs help set up dedicated work groups that undertake multiple projects in areas that have research potential, particularly from the point of view of industry requirements.

· Establishing joint R&D centres: TBIs help in the establishment of joint R&D centres with help from industry or the government.

· Providing support to start ups: Entrepreneurs with ideas can start research at incubation centres, while simultaneously working on establishing their own set –up. Support provided by such incubation centres include:

o Administrative support and office facilities o Expertise in legal, financial, business and technical fields o Commercial support, i.e. access to market research, liaising with venture

capitalists, etc. Trends In the past, a few units have been spun off through this process. Most of these units were design based, with project orders from Indian or global companies. One of the major factors limiting the incubation activity is the initial funding requirements. India is at a nascent phase for early stage angel funding and venture capital investments for incubators.

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

Table 4: Indicative list of active incubators in Indian institutes: Sr. No

Institute Incubator name Year of establishment

1. IIT Kharagpur Science and Technology Entrepreneurs Parks 1982

2. NIT Trichy Science and Technology Entrepreneurs Parks 1983

3. IISc Bangalore Society for Innovation and Development 1991

4. PSG Coimbatore Science and Technology Entrepreneurs Parks 1998 5. IIT Delhi Technology Business Incubator 2000

6. IIT Mumbai Society for Innovation and Entrepreneurship 2005

7. BITS – Pilani Technology Business Incubator -

8. IIT Chennai Technology Business Incubator - Table 5: Indicative list of successful start-ups: Sr. No.

Institute Company Field

1. IISc Bangalore PicoPeta Simputers Pvt. Ltd. Hardware and Software solutions for various business domains

2. IISc Bangalore Esquibe Communication Solutions Pvt. Ltd

IP creation in sensors, signals and systems

3. IIT Mumbai Powai Labs Technology Technologies Pvt. Ltd

EDA

4. IIT Mumbai Embedded Robot Technologies Pvt. Ltd

Artificial vision software protocol

5. IIT Chennai Neuro Synaptics IP creation and solutions in the area of neuro technology

6. IIT Chennai Midas Communication Technologies

Telecommunication solutions

7. PSG Coimbatore Onspec - Legend VLSI design Outlook Incubation activity in Indian universities has recorded an increase with Venture Capitalists showing interest in small start-ups. These VCs, most of them based in the Silicon Valley in the US, typically visit India once a month to meet entrepreneurs and research professors for discussions on the semiconductor activity in the country. Incubation activity is likely to come up in the NITs in the future. In an effort to encourage entrepreneurship skills among students, IIT Kharagpur has proposed to start a School of Entrepreneurship from the academic year 2008. Up to twenty students interested in starting a business would be admitted through the Joint Entrance Examination mode (IIT – JEE) and will be provided training in management, finance and innovation, in addition to the regular B.Tech course.

Source: ISA – Evalueserve Study, 2008

Source: ISA – Evalueserve Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

2.2.2 University - industry collaboration in India Current status Semiconductor research activity in Indian universities is primarily driven by industry initiatives to work on specific areas in semiconductors. Industry has been striving constantly to help students and research graduates get practical experience in new technology platforms. Most of the companies supply design, testing and simulation tools to universities to encourage the use of current market driven technologies. University – industry research collaboration model This model was initiated in India by some of the bigger names in the Indian Semiconductor Industry. Texas Instruments and Intel are trend setters and have funded universities to set up labs. Companies like Cadence and ARM assist universities with specific tools which help groom students to meet industry expectations and standards. The VLSI Design Tools and Technology (VDTT), Advanced VLSI Design Lab and Nano Electronics Design Centre are some of the industry – university initiatives started to improve the scope of semiconductor research in India. At present, VLSI design is the most popular research area. Most often, companies either fund the institutes or supply development kits and tools necessary for research activity. Design tools are supplied either free of cost or at highly subsidised rates to provide access to the latest technology design and simulation tools. The research leads, who are usually professors, make proposals to indicate the required funding and the number of students for the research project. The period of collaboration depends on the intensity of research and typically ranges from 7 – 8 months to 3 years. The scope of industry – university research is currently very limited with industry just facilitating research and not investing heavily into it. Emphasis is on applied research and not much on business aspects. Training and support also form key features of such collaborative efforts. A few companies have introduced training programmes for the faculty and students.

Table 6: Instances of university - industry collaboration in the area of semiconductors

Note: This is an indicative list compiled from available data

Institutes Research areas, research infrastructure Corporate alliance

IIT-Kharagpur

· Microelectronics and VLSI are the major areas of research

· The Advanced CAD Lab at IIT Kharagpur is one of its kind in India and is currently running several projects sponsored by various national and international agencies such as the Ministry of Information Technology, DRDO and ISRO. The projects encompass the design and implementation of digital and mixed-signal chips for various applications related to digital signal processing, image processing and communication system.

· The Advanced VLSI Design Lab (AVDL) is promoted by the IIT Foundation along with National Semiconductor, Sun Microsystems, Cadence Design, Synopsys, and Agilent Technologies. Projects include DC-DC

· Intel · IHP, Germany · National

Semiconductor · Sun Microsystems

Cadence Design Systems

· Synopsys · Agilent

Technologies

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

converters, oscillators, encryption circuits, 3G communication components, etc. Some ongoing projects include designing efficient power management circuits, design of low power RF modules, and work in the areas of VLSI design and wireless technologies.

IIT-Chennai · The institute carries out research in fabrication and modelling of microelectronic devices; design of analog, mixed signal and digital VLSI chips and computer aided VLSI design

· The VLSI design group is equipped with about 40 workstations having state-of-the-art tools for IC/FPGA designs. Mixed signal ICs in sub micron CMOS processes have been successfully designed, fabricated, and characterized in the last few years.

· Research in the areas of RF and mixed signal design, analysis and simulation of noise in circuits, VLSI, DSP architectures, and reconfigurable computing.

· Currently working on 4G Telecom

· Intel · NXP Semiconductors

IIT-Mumbai · One of the most active universities in semiconductor field with twelve core faculty and 110 postgraduate students working on Microelectronics and VLSI.

· The state-of-the-art facilities include Class 1000 Clean Room (class 100 work areas) with facilities for complete IC manufacturing (optical and EB lithography, RIE, deposition, sputter, RTP, and furnace facilities)

· Since 1985, over sixty sponsored projects, totalling USD 8 million, have been undertaken by the VLSI group.

· Communication projects - development of a hot-carrier simulator, modelling of power semiconductor devices and CMOS device design and optimization for mixed-signal applications.

· Currently developing a state of the art Nano electronics design and fabrication lab with Applied Materials, US

· Research in the field of flash memory devices

· Motorola · GE · Intel · Sandisk · Renesas · Infineon · Applied Materials

IIT-Delhi · Research areas are EDA (Electronics Design Automation) and computer architecture, low power design and synthesis, embedded systems, FPGA based designing, system level design, and modelling.

· Leading projects taken up by students were sponsored by Intel and NXP centred on low-power designs for mobility devices.

· Intel · NXP Semiconductors

IISc – Bangalore

· Digital Signal Processing (DSP) and analog & mixed signal systems

· Texas Instruments

IIIT · Automatic Energy Measurements · NXP Semiconductors

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

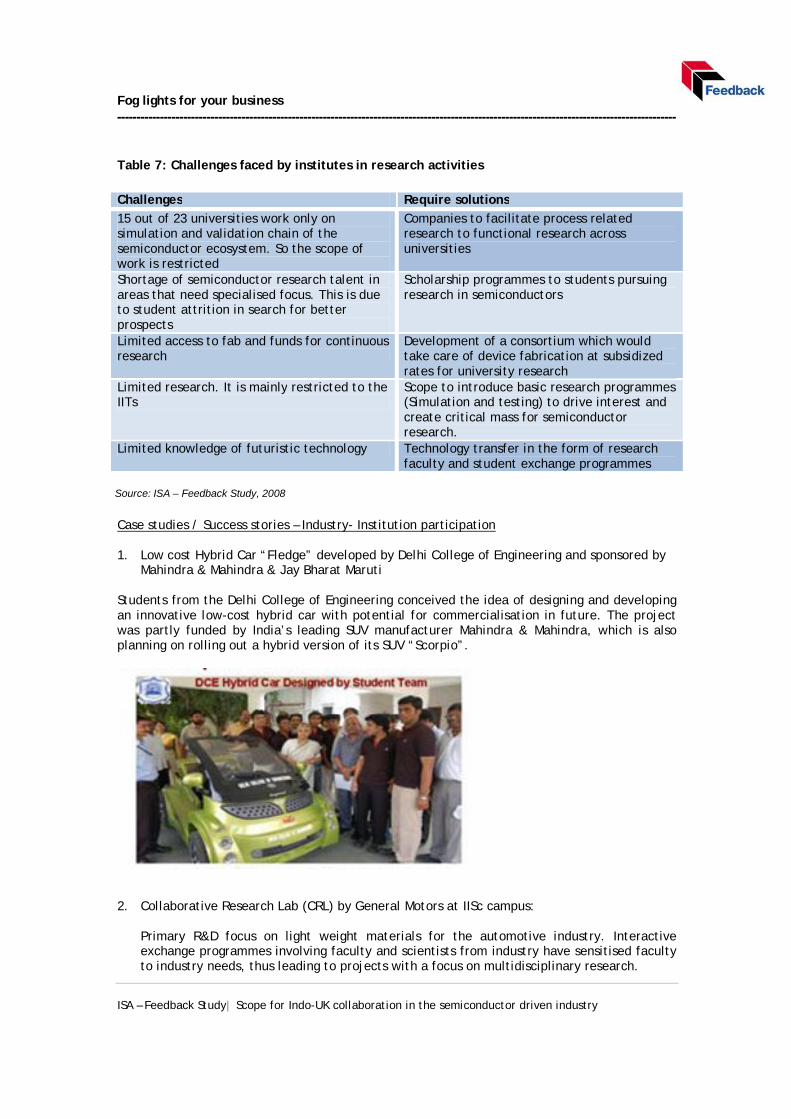

Table 7: Challenges faced by institutes in research activities

Challenges Require solutions

15 out of 23 universities work only on simulation and validation chain of the semiconductor ecosystem. So the scope of work is restricted

Companies to facilitate process related research to functional research across universities

Shortage of semiconductor research talent in areas that need specialised focus. This is due to student attrition in search for better prospects

Scholarship programmes to students pursuing research in semiconductors

Limited access to fab and funds for continuous research

Development of a consortium which would take care of device fabrication at subsidized rates for university research

Limited research. It is mainly restricted to the IITs

Scope to introduce basic research programmes (Simulation and testing) to drive interest and create critical mass for semiconductor research.

Limited knowledge of futuristic technology Technology transfer in the form of research faculty and student exchange programmes

Case studies / Success stories – Industry- Institution participation 1. Low cost Hybrid Car “Fledge” developed by Delhi College of Engineering and sponsored by

Mahindra & Mahindra & Jay Bharat Maruti

Students from the Delhi College of Engineering conceived the idea of designing and developing an innovative low-cost hybrid car with potential for commercialisation in future. The project was partly funded by India’s leading SUV manufacturer Mahindra & Mahindra, which is also planning on rolling out a hybrid version of its SUV “Scorpio”.

2. Collaborative Research Lab (CRL) by General Motors at IISc campus:

Primary R&D focus on light weight materials for the automotive industry. Interactive exchange programmes involving faculty and scientists from industry have sensitised faculty to industry needs, thus leading to projects with a focus on multidisciplinary research.

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

3. CorDECT - a low-cost advanced Wireless Access System developed by Midas Communication

Technologies and IIT Madras, in association with Analog Devices, USA The technology provides complete wireless access solution with seamless integration of high quality voice and 35/70 kbps Internet access to its wireless subscribers. The technology is based on the DECT (Digitally Enhanced Cordless Telecommunication) air interface standard specification of the European Telecommunication Standards Institute (ETSI). In India, corDECT is manufactured under license by Crompton Greaves, Electronics Corporation of India Ltd (ECIL), HFCL and Shyam Telecom Ltd. One of most successful and early installations of corDECT has been in the African island nation of Madagascar. corDECT is operational in the city of Tamatave (formerly Toamasina) for over two years now, and subsequently it has been installed in the cities of Sambava and Anthala. Fiji Telecom installed corDECT to serve its subscribers in the island of Ba, far away from the capital Suva. In the course of the last couple of years, corDECT was tested by telecom standardisation bodies in Argentina, Brazil, Europe (ETSI), Kenya, Angola, Tunisia, Nigeria, and was cleared for induction in their respective networks. Currently, there are field trials underway in Iran, Egypt and Yemen. Commercial corDECT systems are also operational in Argentina, Brazil, Tunisia and Nigeria. Outside of India, corDECT is manufactured under licence by BBS Access in Singapore and by Omniacom in Tunisia. corDECT will soon be manufactured locally in Brazil too. (Source: Indian innovators association)

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

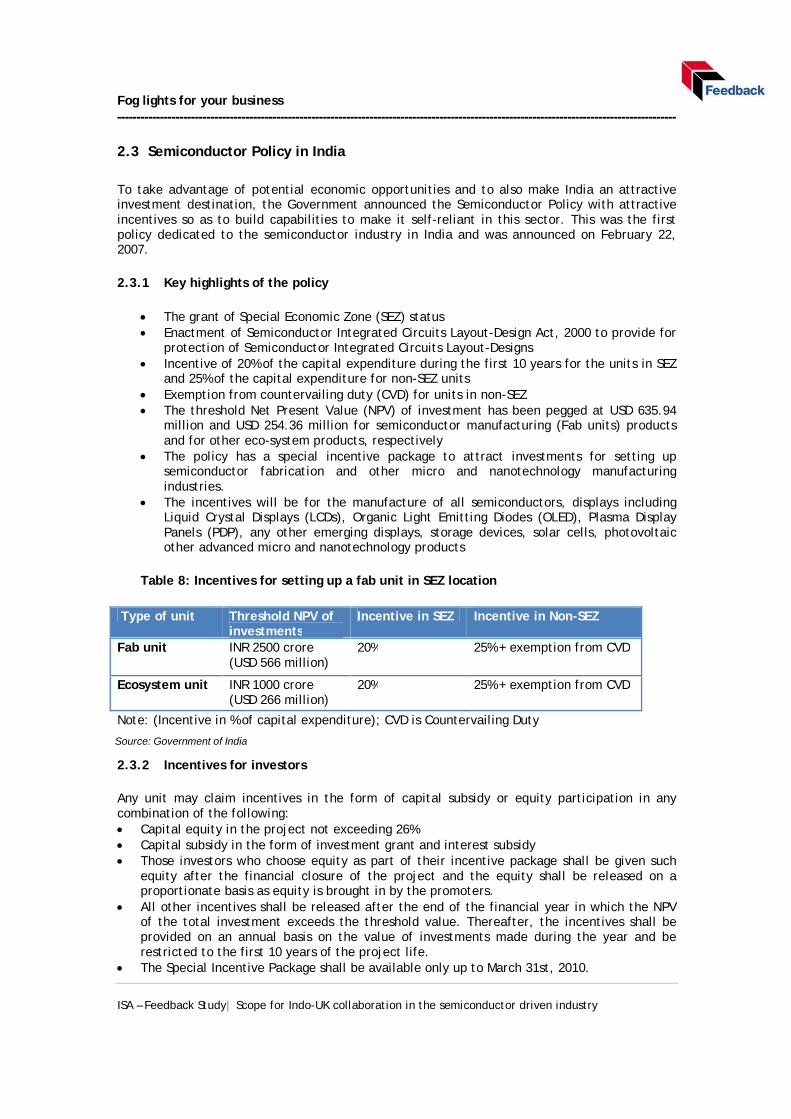

2.3 Semiconductor Policy in India

To take advantage of potential economic opportunities and to also make India an attractive investment destination, the Government announced the Semiconductor Policy with attractive incentives so as to build capabilities to make it self-reliant in this sector. This was the first policy dedicated to the semiconductor industry in India and was announced on February 22, 2007.

2.3.1 Key highlights of the policy

· The grant of Special Economic Zone (SEZ) status · Enactment of Semiconductor Integrated Circuits Layout-Design Act, 2000 to provide for

protection of Semiconductor Integrated Circuits Layout-Designs · Incentive of 20% of the capital expenditure during the first 10 years for the units in SEZ

and 25% of the capital expenditure for non-SEZ units · Exemption from countervailing duty (CVD) for units in non-SEZ · The threshold Net Present Value (NPV) of investment has been pegged at USD 635.94

million and USD 254.36 million for semiconductor manufacturing (Fab units) products and for other eco-system products, respectively

· The policy has a special incentive package to attract investments for setting up semiconductor fabrication and other micro and nanotechnology manufacturing industries.

· The incentives will be for the manufacture of all semiconductors, displays including Liquid Crystal Displays (LCDs), Organic Light Emitting Diodes (OLED), Plasma Display Panels (PDP), any other emerging displays, storage devices, solar cells, photovoltaic other advanced micro and nanotechnology products

Table 8: Incentives for setting up a fab unit in SEZ location

Type of unit Threshold NPV of investments

Incentive in SEZ Incentive in Non-SEZ

Fab unit INR 2500 crore (USD 566 million)

20% 25% + exemption from CVD

Ecosystem unit INR 1000 crore (USD 266 million)

20% 25% + exemption from CVD

Note: (Incentive in % of capital expenditure); CVD is Countervailing Duty 2.3.2 Incentives for investors Any unit may claim incentives in the form of capital subsidy or equity participation in any combination of the following: · Capital equity in the project not exceeding 26% · Capital subsidy in the form of investment grant and interest subsidy · Those investors who choose equity as part of their incentive package shall be given such

equity after the financial closure of the project and the equity shall be released on a proportionate basis as equity is brought in by the promoters.

· All other incentives shall be released after the end of the financial year in which the NPV of the total investment exceeds the threshold value. Thereafter, the incentives shall be provided on an annual basis on the value of investments made during the year and be restricted to the first 10 years of the project life.

· The Special Incentive Package shall be available only up to March 31st, 2010.

Source: Government of India

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

2.3.3 Benefits of the policy The semiconductor policy is primarily formed to facilitate device manufacturing in the semiconductor ecosystem. The growth in market volumes and the outlook to adapt newer technologies have provided impetus to the semiconductor industry in India. Currently, India imports a significant amount of semiconductors for its domestic market. With a view to making the country self sufficient, the policy is aimed at starting up fabrication, assembly and packing units in the country (ATMP – Assembly Test Mark Pack). 2.3.4 Challenges Significant investments are required for setting up fabrication units (around USD 2 billion per unit). This makes it difficult for a private entity to make the total investment and reap benefits; further, rapid technology upgrading requires continuous investments and with growing markets, sustainability of such fabs is tough. For commercial fabs to be operational, the companies need to look at global markets. 2.3.5 SMDP (Special Manpower Development Program) The industry body is actively involved in the Special Manpower Development Program, a government initiative with the private industry. The objective of the programme is to facilitate faculty training. The SMDP focuses on supplying kits to universities and encouraging VLSI as a part of the curriculum. Under the renewed version of the scheme 2007, nineteen new universities will be targeted, bringing the total to thirty two.

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

2.4 Strengths and weaknesses of Indian universities and companies

2.4.1 Strength and weakness analysis of Indian universities in the field of semiconductors: Figure 16: Level of semiconductor activities in Indian Universities

Note: Research initiation by industry is higher than the universities as they provide the latter with the basic EDA tools and equipment Exhibit: Definitions Categories Variables Description Research activity

VLSI design Activities in the field of VLSI, FPGA design Process related research Research on device physics - alternate

materials, characterization Fundamental research Research activity on futuristic technology such

as 4G Telecom, Wimax, etc. EDA Modelling and simulation of devices, system Application based research Research on direct end products

Infrastructure and resources

Infrastructure Design labs and kits for research activities Source of funds Funds generated through university internal

accruals, government , companies Incubation Activities of incubation cell within the

university and number of successful launches. Talent pool Number of students pursuing semiconductor

research in universities Research initiative

University driven research Research initiated by university professors Company driven research Research initiated by companies

0 1 2 3 4 5 6 7 8 9

EDA

Application based research

Process related research

VLSI design

Talent pool

Source of funds

Company driven research

Fundamental research

University driven research

Incubation

Infrastructure

Extent of semiconductor research activities, support from companies and funding

Research initiative

High Low

Infrastructure and Resources Research Activities

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

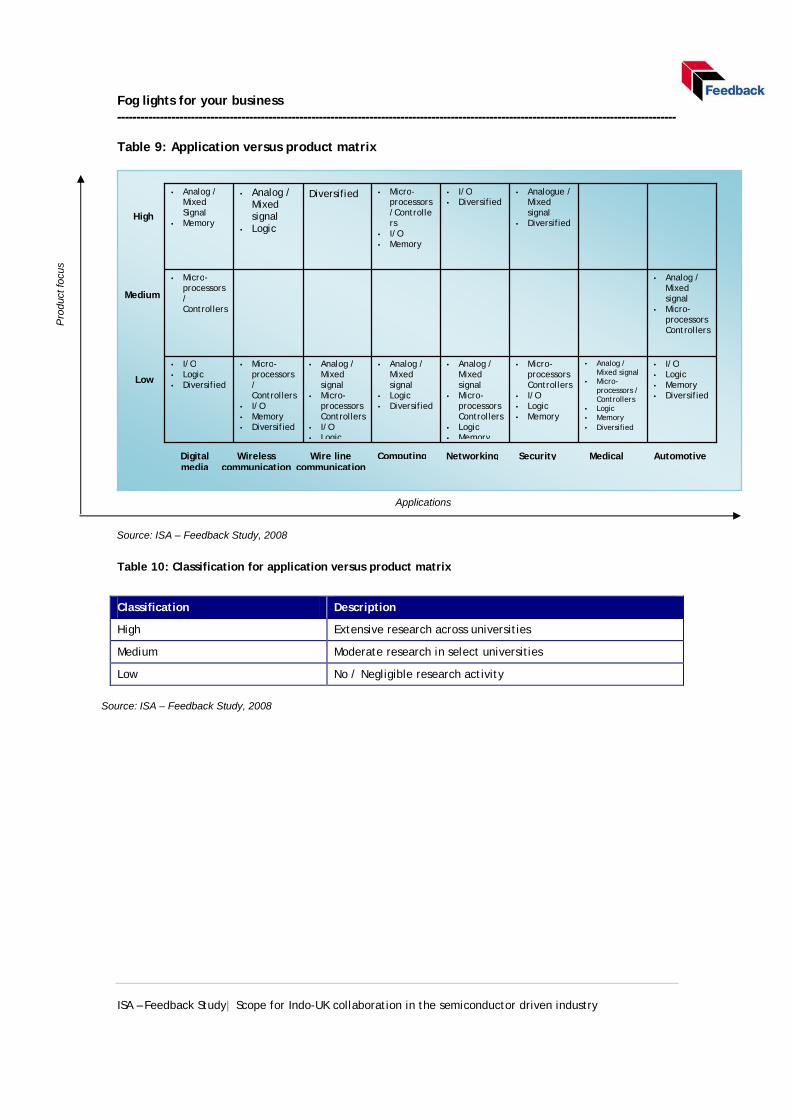

Table 9: Application versus product matrix

Table 10: Classification for application versus product matrix

Classification Description

High Extensive research across universities

Medium Moderate research in select universities

Low No / Negligible research activity

• I/O • Logic • Memory • Diversified

• Analog / Mixed signal

• Micro-processors / Controllers

• Logic • Memory • Diversified

• Micro-processors Controllers

• I/O • Logic • Memory

• Analog / Mixed signal

• Micro-processors Controllers

• Logic • Memory

• Analog / Mixed signal

• Logic • Diversified

• Analog / Mixed signal

• Micro-processors Controllers

• I/O • Logic

• Micro-processors / Controllers

• I/O • Memory • Diversified

• I/O • Logic • Diversified

• Analog / Mixed signal

• Micro-processors Controllers

• Micro-

processors / Controllers

• Analogue /

Mixed signal

• Diversified

• I/O • Diversified

• Micro-processors /Controllers

• I/O • Memory

Diversified • Analog / Mixed signal

• Logic

• Analog / Mixed Signal

• Memory

High

Medium

Low

Digital media

Wireless communication

Wire line communication

Computing Networking Security Medical Automotive

Applications

Pro

duct

focu

s

Source: ISA – Feedback Study, 2008

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

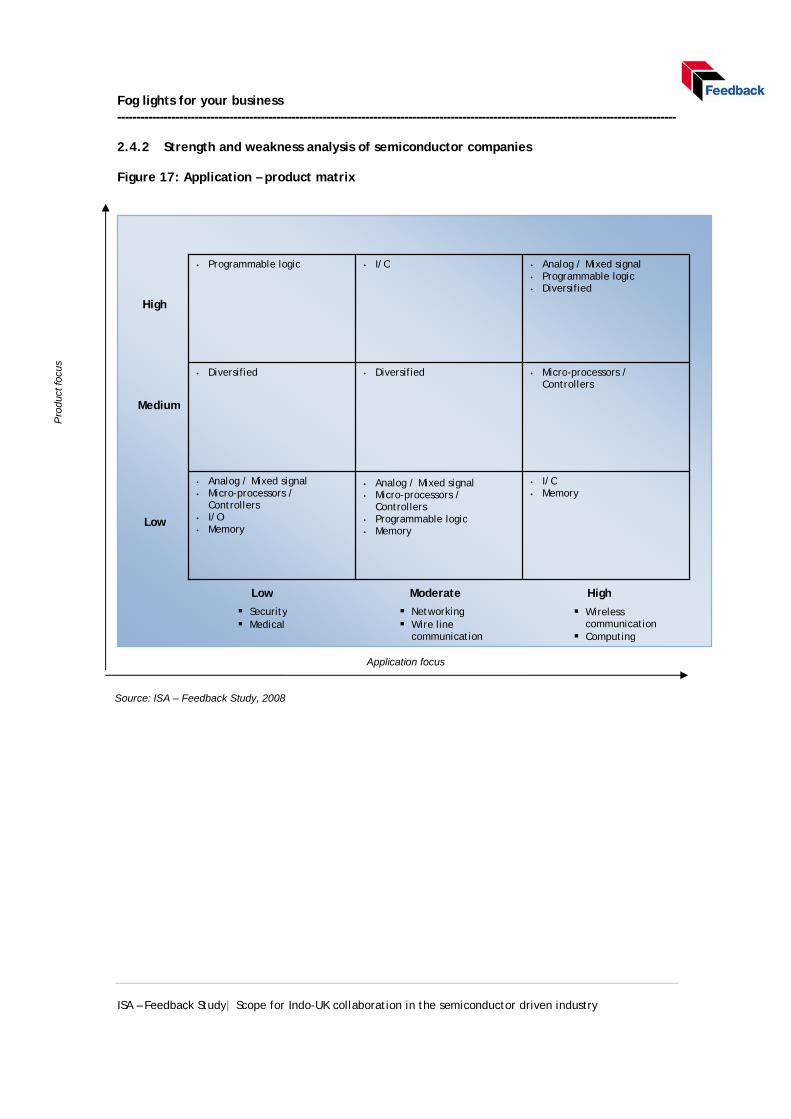

2.4.2 Strength and weakness analysis of semiconductor companies Figure 17: Application – product matrix

• I/O • Memory

• Analog / Mixed signal • Micro-processors /

Controllers • Programmable logic • Memory

• Analog / Mixed signal • Micro-processors /

Controllers • I/O • Memory

• Micro-processors / Controllers

• Diversified

• Diversified

• Analog / Mixed signal • Programmable logic • Diversified

• I/O

• Programmable logic

High

Low

High Moderate Low

§ Security § Medical

§ Networking § Wire line

communication

§ Wireless communication

§ Computing

Medium

Application focus

Pro

duct

focu

s

Source: ISA – Feedback Study, 2008

Fog lights for your business ------------------------------------------------------------------------------------------------------------------------------------------------

ISA – Feedback Study| Scope for Indo-UK collaboration in the semiconductor driven industry

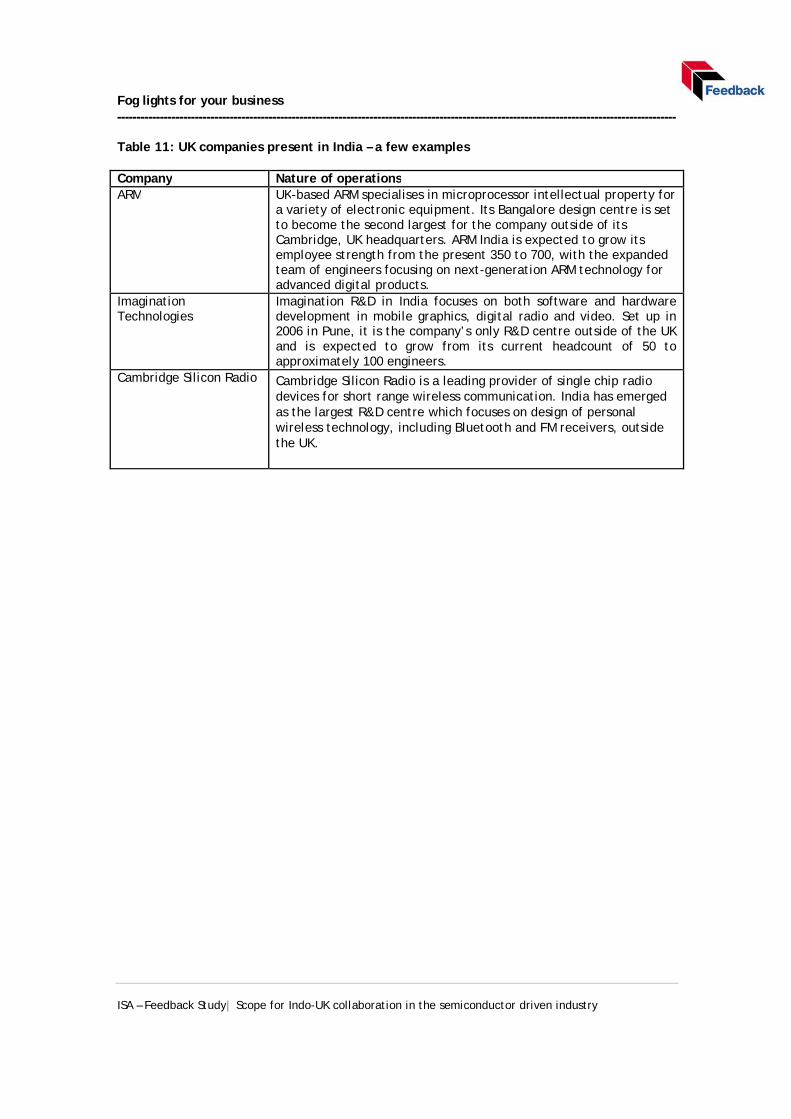

Table 11: UK companies present in India – a few examples Company Nature of operations ARM UK-based ARM specialises in microprocessor intellectual property for

a variety of electronic equipment. Its Bangalore design centre is set to become the second largest for the company outside of its Cambridge, UK headquarters. ARM India is expected to grow its employee strength from the present 350 to 700, with the expanded team of engineers focusing on next-generation ARM technology for advanced digital products.

Imagination Technologies