sap mobile consumer survey report_apac

TRANSCRIPT

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

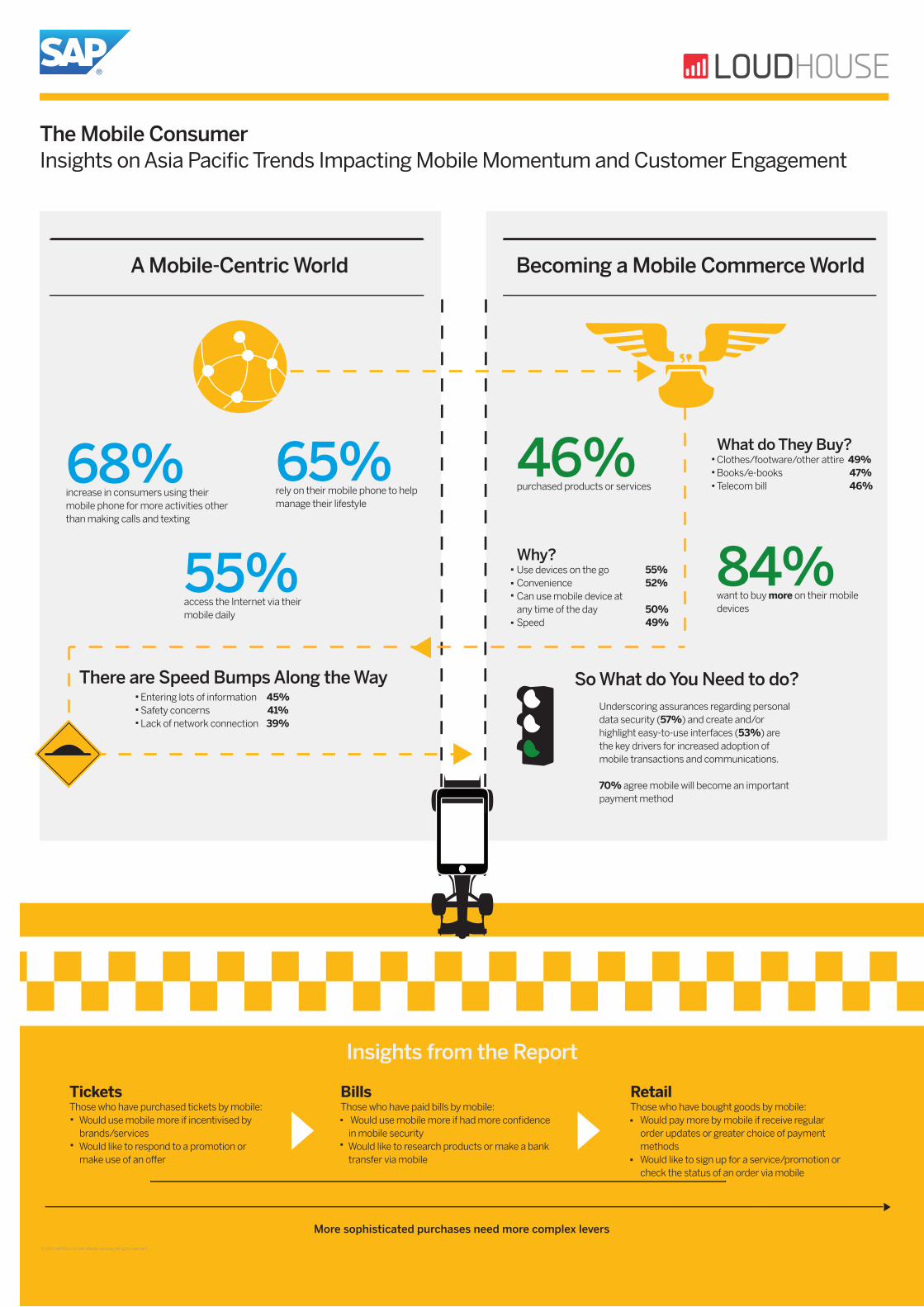

55%access the Internet via their mobile daily

84%want to buy more on their mobile devices

Why?Use devices on the go 55% Convenience 52%Can use mobile device at any time of the day 50% Speed 49%

The Mobile ConsumerInsights on Asia Pacific Trends Impacting Mobile Momentum and Customer Engagement

68%increase in consumers using their mobile phone for more activities other than making calls and texting

65%rely on their mobile phone to help manage their lifestyle

46%purchased products or services

A Mobile-Centric World Becoming a Mobile Commerce World

What do They Buy?Clothes/footware/other attire 49% Books/e-books 47%Telecom bill 46%

There are Speed Bumps Along the WayEntering lots of information 45% Safety concerns 41% Lack of network connection 39%

So What do You Need to do?Underscoring assurances regarding personal data security (57%) and create and/or highlight easy-to-use interfaces (53%) are the key drivers for increased adoption of mobile transactions and communications.

70% agree mobile will become an important payment method

Insights from the ReportTicketsThose who have purchased tickets by mobile: Would use mobile more if incentivised by brands/services Would like to respond to a promotion or make use of an offer

BillsThose who have paid bills by mobile: Would use mobile more if had more confidence in mobile security Would like to research products or make a bank transfer via mobile

RetailThose who have bought goods by mobile: Would pay more by mobile if receive regular order updates or greater choice of payment methods Would like to sign up for a service/promotion or check the status of an order via mobile

More sophisticated purchases need more complex levers

The Mobile ConsumerInsights on Asia Pacific Trends Impacting Mobile Momentum and Customer Engagement

© 2

013

SAP

AG o

r an

SAP

affilia

te c

ompa

ny. A

ll rig

hts

rese

rved

.

2 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

Table of Contents

4 Introduction

5 Devices,AppetiteandUse

10 Maturity,LifestyleandWork

14 PreferencesandLevers

18 MobileWalletOppportunities

22 Conclusion

25 Appendix

The Mobile Consumer: Findings for Asia Pacific

3 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

Creating demand for mobile services relies on an understanding of mobile user behaviour. The following report provides marketers in the mobile industry with insights on the global trends impacting mobile momentum.

The Mobile Consumer: Findings for Asia Pacific

4 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

Regional appetite for different mobile services and applications varies dramatically, and the ways in which users transact and communicate via mobile depends on the activities undertaken. Cultural, economic and technology norms shape regional uses of mobile, whilst an array of user requirements influence preferences towards appropriate marketing channels, relationships and incentives as they shop, spend and surf.

In order to make informed marketing decisions and better understand mobile momentum and customer engagement across the globe, SAP commissioned independent research among mobile users across 4 key regions, encompassing 17 countries:

• North America (NAM)• Europe, Middle East and Africa (EMEA)• Latin America (LATAM)• Asia Pacific (APAC)

This report will focus in more detail on the Asia Pacific (APAC) region. For the purpose of this research, Asia Pacific is comprised of the following countries:

• China• India• Japan • Australia

Within the APAC region, Japan and Australia have already reached a level of mobile maturity, yet for India and China, mobile device use is evolving. This varied momentum contributes to differences in mobile ownership, appetite and behaviour.

Growth in smartphone technology and the blur of social, mobile and traditional marketing channels has seen users becoming motivated by a range of complex factors. The greater the sophistication of mobile use, the greater the sophistication of consumer needs. As the commercial elements of mobile interaction continue to take shape, organisations capitalising on mobile channels need to balance the advancement of mobile functionality with these needs. Not all successful examples of mobility are based on ‘bleeding edge’ innovation. The right service for the right user, marketed in the right way is a simplistic, yet appropriate, mantra for marketing strategy in the mobile sector.

Introduction

RESEARCHMETHODOLOGY3,288interviewswereconductedwithadultsaged18+whoownamobilephone(basicorsmartphone)inAPAC(Chinan=1000,Indian=1050,Japann=651,Australian=587).RespondentscompletedanonlinesurveyinMarch/April2013.ResearchconductedbyLoudhouse,anindependentresearchagencybasedinLondon.

The Mobile Consumer: Findings for Asia Pacific

5 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

APAC has the highest penetration of smartphones globally, with just over three quarters (76%) of smartphone users interviewed in the survey, a little higher than the global average of 72%. However, there is a level of variation across the APAC sample with ownership in the more mature markets of Japan (61%) and Australia (69%) being somewhat lower than in India (74%) and, in particular, China (92%).

In general, more APAC users turn to their mobile device throughout the day than is the global norm. As with all regions, making or receiving calls is the most popular activity at 79% (rising to 91% in China and 95% in India), followed by sending or receiving texts (69%). At a secondary level, over half (55%) use their mobile phone on a daily basis for general Internet access or to send or receive emails (53%), highlighting a natural

move in the direction of increased channels of mobile communication.

While daily banking via mobile and buying goods and services are just above the global level, APAC users are much more likely than the global average to use their mobile moderately (a few times a week or monthly) for banking (37% vs. 29% global) and buying goods and services (37% vs. 26% global). Again, these activities are led by India (38% banking and 39% purchases) and China (54% for both banking and purchases) in particular.

Figure 1 shows that while online (70%) and in-store (73%) are the main ways that respondents have purchased goods and services in the past 12 months, APAC users are also looking to other channels for transaction. Purchase via mobile Internet (36%), via a downloadable app (24%) and via SMS (19%)

Devices, Appetite and Use

In storeOnline (not via mobile phone)

By mobile phone - via mobile InternetBy telephone call (landline or mobile)

By mobile phone - via a downloadable appMail order

By mobile phone - SMSDon’t know

36%

25%

24%

21%

19%

2%

70%

73%

Net: by mobile phone 46%

Figure1Purchasing methods in past 12 months

The Mobile Consumer: Findings for Asia Pacific

6 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

(55%), that it is convenient (52%), can be used day or night (50%) and is quick (49%) are all key drivers for further adoption in the APAC region. Indeed, scores for usage on-the-go and convenience are both significantly higher than for EMEA and NAM.

There are, however, some challenges raised by APAC users when communicating and transacting with organisations via their mobile, albeit at a slightly lower level than the global average. The key issue, cited by 45% of users, is the hassle of having to enter a lot of personal information

are all above the global average. As observed in the sample, this potentially also points to the high smartphone penetration in the region. Nevertheless, there is variation within the region with the emerging economies of China and India leading the way.

As Figure 2 shows, the benefits of communicating and transacting with organisations via mobile device for APAC users centre around the com-patibility of mobile with their lifestyle. The fact that consumers can use their mobile on the go

Figure2Benefits of mobile interactions

I can use it on the goIt’s convenient

I can use it at any time of the day or nightIt’s quick

It’s easy to useReceiving a quick response to queries

It’s free of charge (no postage, travel or call)I can store details on my phone for future use

It fits in with my needs and lifestyleIt’s secure

It provides better information than other methodsOther benefits

Don’t knowI don’t think there are any benefits

55%

52%

50%

49%

45%

40%

38%

33%

29%

25%

20%

4%

4%

8%

The Mobile Consumer: Findings for Asia Pacific

7 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

when transacting and communicating via their mobile device (Figure 3). Additionally, there are concerns over safety when using mobile for purchasing (41%), and also 39% state a potential lack of access to the Internet at the time of the transaction. Within the region, there is a slightly different picture depending on whether the market is mature or emerging. Safety is more important in the mature markets of Australia (43%) and Japan (37%), while the hassle of entering information is a deterrent for users in India (48%) and China (54%).

Within the APAC region there appears to be huge potential for the future of mobile transactions, with 84% of users expressing an appetite for

buying goods and services using their mobile phone in the future (Figure 4). This compares with 82% globally. Half of these users (42%) have never before used mobile transactions but would like to do so in the future, and half (42%) have used their mobile previously to buy goods and wish to make further purchases with their mobile. At a lower level, 14% have used their mobile to buy goods but are not expecting to use this method in the future.

The interest in future purchases by mobile is further underpinned by 77% of users agreeing that organisations should use any available technology to make life easier for customers. This is marginally below the global average

Figure3Challenges of mobile interactions

Hassle of having to enter a lot of personal information

I don’t think it’s safe

I might not have Internet access at that time

Lack of immediate customer service

The interface is hard to see

I’m not interacting with a human being

I am able to communicate with service providers without my mobile phone

I don’t know how to do it

Another challenge

Don’t know

There are no challenges

45%

41%

39%

33%

27%

23%

19%

14%

6%

7%

7%

The Mobile Consumer: Findings for Asia Pacific

8 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

communication and interaction with customers. As with all regions, the majority of APAC users (72%) agree that they are often frustrated by automated voice phone systems when they call a service provider. Indeed, over half (58%) agree that they would be willing to switch to a different provider if they could interact with them better through their mobile phone. This is slightly higher than the global average of 54%.

Used mobileto buy goodsand content 14%

Net: Want to buy goods / more on mobile: 84%

Figure4Appetite for purchasing via mobile

Not used mobile to

buy goods but want to 42%

Not used mobile to buy goods and content 2%

Used mobile to buy goods and want to do it

more 42%

of 80% and highlights the extent to which APAC consumers have become used to, and expecting of, increasing sophistication of mobile connectivity with organisations.

Indeed, users are increasingly willing to hold organisations accountable if they do not meet service levels and any technological advances in the future should look to also improve

The Mobile Consumer: Findings for Asia Pacific

9 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

The majority of APAC respondents agree that they rely on their mobile phone to help them manage their lifestyle.

The Mobile Consumer: Findings for Asia Pacific

10 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

The emerging markets of India and China show an enthusiasm for a fast pace of change and the adoption of more sophisticated transactional activities via their mobile. In contrast, the more mature markets of Australia and Japan appear more reticent. This leads to key variations in response by users, and it is crucial for organisa-tions to bear these regional distinctions in mind when planning marketing activity.

In line with the global view, under half of APAC users agree that they tend to use their mobile phone more for work than leisure activities. As Figure 5 shows, there is no real difference

depending on whether the user is a smartphone owner (49%) or owns a basic mobile (48%). However, there is variation within the region, with the emerging markets of India (68%) and China (54%) showing higher levels of agreement than the mature countries of Australia (17%) and Japan (22%).

The majority of APAC respondents agree that they rely on their mobile phone to help them manage their lifestyle. There is some difference due to device type ownership, as highlighted in Figure 6, with smartphone owners (73%) some-what more inclined to agree compared to basic

Maturity, Lifestyle and Work

Figure6Agreement with statement: “I rely on my mobile phone to help manage my lifestyle”

71%

EMEA LATAM NAMAPAC

73% 64%73%51% 58% 26%62%

Smartphone owners

Basic mobile phone owners

Figure5Agreement with statement: “I tend to use my mobile phone more for work than for leisure activities” by ownership of mobile type

49%

APAC EMEA LATAM NAM

39% 58% 22%48% 29% 53% 11%

Smartphone owners

Basic mobile phone owners

The Mobile Consumer: Findings for Asia Pacific

11 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

mobile owners (62%). Again, these figures are driven by users in the emerging economies of India (80%) and China (75%) which show more inclination towards reliance on their mobile than the mature markets of Australia (48%) and Japan (41%).

Two-thirds (68%) of APAC users agree that compared to 12 months ago, they now use their mobile phone for more activities other than just making calls and texting, which is above the global average of 63% (Figure 7). This figure is again clearly driven by the emerging markets of India (80%) and China (86%) who are enthusiastic in their adoption of new ways to use their mobile

compared to the mature markets of Australia (47%) and Japan (37%).

Nevertheless, while users in the mature APAC markets of Australia and Japan may not feel they are overly reliant on their mobile to manage their lifestyle, they do acknowledge the impact that not having their mobile would have. Over half (54%) of Australian users and 72% of Japanese users agree that having their mobile lost or stolen would really affect their personal productivity. The impact is felt even more keenly in the emerging markets of India (88%) and China (93%) where the reliance on mobile phones is more evident.

.

Figure7Agreement with statement: “Compared to 12 months ago, I use my mobile phone for more activities other than making calls and texting/sending”

87%

Mexico China Chile UKSpainBrazilRussiaColombiaEgyptSouthAfrica

IndiaSaudiArabia

USAGermanyFranceAustralia Japan

86% 84% 83% 80% 74% 69% 67% 66% 63% 63% 50% 47% 47% 44% 38% 37%

Emerging mobile markets Developing mobile markets Mature, saturated mobile markets

APAC68%

The Mobile Consumer: Findings for Asia Pacific

12 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

There are many factors that underpin trends within the APAC region, and they can be summarised into three key areas:

• Economy: More rapid GDP growth and relative consumer momentum in India and China compared to the mature markets of Australia and Japan

• Infrastructure: Mobile network and mobile Internet services outperform legacy telecoms infrastructure in the emerging countries

• Device Culture: Basic handset use and transactional SMS services are more prevalent in India and China as they adopt new services at a faster pace

The Mobile Consumer: Findings for Asia Pacific

13 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

Consumers across the globe have witnessed simultaneously an increase in the sophistication of mobile devices available and an increase in the complexity and variety of transactions that can be made via mobile.

The Mobile Consumer: Findings for Asia Pacific

14 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

.

Preferences and Levers

Consumers globally have seen an increase in the sophistication of mobile devices available with a corresponding rise in the complex nature and scope of transactions that mobile now enables. Figure 8a groups various types of mobile purchases into three distinct categories: Tickets, Bills and Retail. These groups represent a spectrum of purchase complexity and motivations:

• Tickets: simple purchases of paper or virtual tokens that provide access to a service or event

• Bills: mandatory payments for goods or service already received or utilised

• Retail: physical items purchased and commonly dispatched by post

Within the APAC region, users engage with a variety of transaction complexities. Those who choose to purchase using their mobile are most likely to buy clothes (49%), purchase books or e-books (47%) or pay their telecom bills (46%) (Figure 8b).

However, there are some distinct differences in the purchase activities undertaken across the region. Chinese users have adopted their mobile device as a channel for transactions with some enthusiasm and they are just as likely to purchase groceries (61%) as they are to buy clothes (61%) or pay telecoms bills (61%). Indian users are almost equal in their enthusiasm and are most likely to purchase tickets for travel (62%), buy

More sophisticated purchases need more complex levers

Figure8aDrivers for different purchase types using mobile

TicketsThose who have purchased tickets by mobile:

• Would use mobile more if incentivised by brands/services

• Would like to respond to a promotion or make use of an offer

BillsThose who have paid bills by mobile:

• Would use mobile more if had more confidence in mobile security

• Would like to research products or make a bank transfer via mobile

RetailThose who have bought goods by mobile:

• Would pay more by mobile if receive regular order updates or greater choice of payment methods

• Would like to sign up for a service/ promotion or check the status of an order via mobile

The Mobile Consumer: Findings for Asia Pacific

15 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

.

entertainment services (54%) and pay telecoms bills (51%).

The more mature markets of Japan and Australia are more restrained in their adoption of mobile transactions generally, yet there are some activities they feel more comfortable with. Japanese users are likely to buy groceries (40%), purchase books and e-books (39%) or buy clothes and other attire (27%) via mobile, while Australian users choose to buy entertainment services (36%) and purchase books and e-books (29%).

In part, these national variations are down to the maturity of the market and the higher level of engagement witnessed in emerging markets. In part, it will be a feature of the national culture. As such, it is key that organisations look to understand any national characteristics. One market is not the same as another, and there are variations within mature and emerging markets.

Various marketing levers to encourage mobile use were evaluated against each purchase type in order to understand user preferences for factors

Figure8bPurchase types using mobile

Clothes/footware/other attireBooks/e-books

Telecom bill (e.g. phone, Internet)Groceries/food

Entertainment (e.g. cinema, theatre)Tickets for travel/transport

Music downloads (e.g. iTunes)Utility bills (e.g. water, electricity)

Electronic appliancesTravel/holidays

Home furniture/goodsJewellery

OtherDon’t know

49%

47%

46%

33%

44%

2%

11%

19%

26%

31%

42%

44%

Tickets Bills Retail

45%

11%

34%

The Mobile Consumer: Findings for Asia Pacific

16 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

such as prompts or characteristics of the operating environment. Findings from this evaluation describe a relationship between purchase ‘drivers’ and purchase types that aligns the complexity of what is paid for with a sophistication of the journey to the item or service itself.

In line with global thinking, 67% of APAC users agree that a greater choice of payment methods would encourage them to make a purchase from an organisation or retailer (vs. 64% globally). Again, it is the emerging markets of China (70%) and India (81%) that drive this level of agreement, with the mature markets of Australia (49%) and Japan (56%) being more reserved.

67% of APAC users agree that a greater choice of payment methods would encourage them to make a purchase from an organisation or retailer.

The Mobile Consumer: Findings for Asia Pacific

17 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

There is general agreement in the region (70%) with the view that mobile phones will be more important as a payment method in the future.

The Mobile Consumer: Findings for Asia Pacific

18 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

.

Mobile Wallet Opportunities

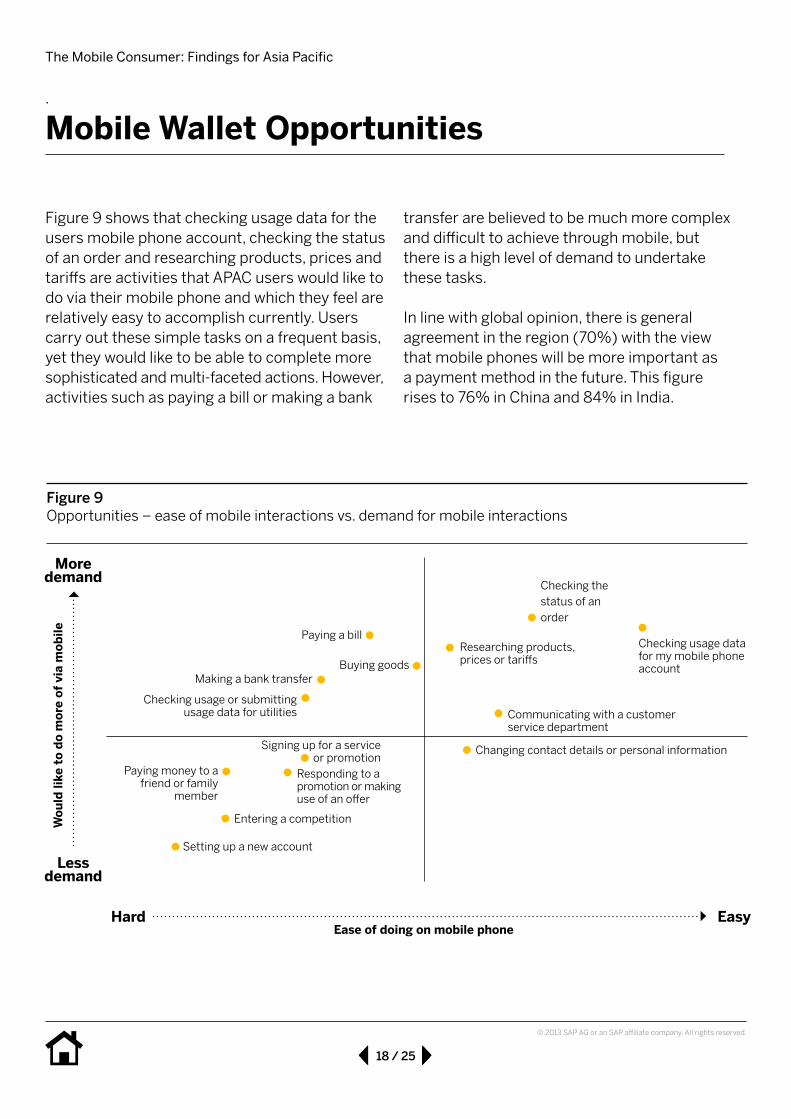

Figure 9 shows that checking usage data for the users mobile phone account, checking the status of an order and researching products, prices and tariffs are activities that APAC users would like to do via their mobile phone and which they feel are relatively easy to accomplish currently. Users carry out these simple tasks on a frequent basis, yet they would like to be able to complete more sophisticated and multi-faceted actions. However, activities such as paying a bill or making a bank

transfer are believed to be much more complex and difficult to achieve through mobile, but there is a high level of demand to undertake these tasks.

In line with global opinion, there is general agreement in the region (70%) with the view that mobile phones will be more important as a payment method in the future. This figure rises to 76% in China and 84% in India.

Figure9Opportunities – ease of mobile interactions vs. demand for mobile interactions

Paying a bill

Changing contact details or personal information

Communicating with a customer service department

Checking usage data for my mobile phone account

Checking the status of an order

Responding to a promotion or making use of an offer

Hard Easy

Lessdemand

Moredemand

Making a bank transfer

Checking usage or submitting usage data for utilities

Entering a competition

Buying goodsResearching products, prices or tariffs

Paying money to a friend or family

member

Setting up a new account

Signing up for a service or promotion

Ease of doing on mobile phone

Wou

ld li

ke to

do

mor

e of

via

mob

ile

The Mobile Consumer: Findings for Asia Pacific

19 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

Furthermore, APAC users believe that once they gain confidence in mobile security (54%) and assurance in how to use their mobile device as a payment method (40%), they will increase their mobile payment activity. Indeed, as Figure 10 also shows, assurances about personal data security (57%) and an easy-to-use interface (53%) are the key drivers for increased adoption of mobile transactions and communications in APAC markets. At a secondary level, free Wi-Fi

Internet access being available in more places (51%) and receiving discounts, offers and coupons (48%) are also important drivers towards increased mobile purchasing and interactions.

The demand for further enhanced yet simpler transaction capabilities by mobile is highlighted in user expectations of a ‘mobile wallet’. APAC users expect to be able to pay a bill (54%), buy goods online (53%) and use it as a means to

.

Figure10Drivers to communicate/transact more via mobile phone

Assurances about personal data securityEasy-to-use interface

Free wifi Internet access in more places Receiving discounts, offers or coupons

Instant/real-time help availableMore shops and retailers offering mobile communications

More information on how it worksMore mobile phones on the market that enable sophisticated communications

Knowing that someone is personally helping youSomething else

Don’t knowNothing would encourage me

57%

53%

51%

48%

34%

4%

7%

25%

29%

33%

42%

11%

The Mobile Consumer: Findings for Asia Pacific

20 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

Figure11Expectations of a mobile wallet

Pay a billBuy goods online

Check my bank balanceMake a bank transfer

Check the status of an orderBuy goods costing a small amount

Buy goods in a shopResearch products, prices or tarrifs

Choice to pay with a variety of payment methods or cardsPay money to a friend or family member

Check usage data for my mobile phone accountCheck usage or submit usage data for utilities

Top up mobile phone creditCommunicate with a customer service department

Enable me to use loyalty cardsSign up for a service or promotion

Respond to a promotion or make use of an offerChange contact details or personal information

Share contact details with friends or familySet up a new account

Enter a competitionBuy goods costing a large amount

None of theseDon’t know

54%

53%

52%

47%

42%

35%

37%

38%

38%

38%

39%

40%

43%

31%

30%

29%

28%

27%

27%

23%

22%

21%

8%

7%

check their bank balance (52%) (Figure 11). Within the region, users in China, India and also Australia were more decisive on what they expected from the mobile wallet, with views from Japanese users at a somewhat lower level.

While there is potential for growing complexity in mobile transactional offerings, the importance of personal and data security and ease of use should not be overlooked by organisations at any point in the innovation process, as these are the ultimate drivers for future take-up of mobile products and services.

The Mobile Consumer: Findings for Asia Pacific

21 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

On its current trajectory, mobile occupies a tempting combination of loyalty card, cash, research tool, location tracker and credit card.

The Mobile Consumer: Findings for Asia Pacific

22 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

.

Conclusion

The commitment to mobile as a recognised ‘transactional device’ changes both the marketing potential and data capabilities offered by mobile services. On its current trajectory, mobile occupies a tempting combination of loyalty card, cash, research tool, location tracker and credit card. This transition raises the stakes for organisations marketing and connecting to customers either exclusively via mobile or as part of a multi- channel mix.

Brand loyalty becomes essential as any business on the mobile browser has the potential to own the customer relationship and all service providers now compete for mindshare in a space that was once the exclusive domain of telecoms businesses. The research points to five key elements that should inform CMO thinking to best tackle the challenges that lay ahead.

ThePaceofChangeThe Mobile Consumer research survey shows an international mobile user community running at different speeds, maturing at different rates and presenting different opportunities, creating marketing complexity.

Within the APAC region, the emerging economies of India and China are more enthusiastic about a mobile future and make an explicit link between increasing mobility and its impact on their lives.

They are less reliant on leading edge technology to drive behaviour, and are eager to try new things. The more mature APAC economies of Japan and Australia are less impulsive and appear somewhat indifferent to the mobile pace and potential. Nevertheless, these markets acknowledge the importance and benefit of more integrated, easier-to-use yet sophisticated mobile products and services.

AdoptionOptions‘Macro-momentum’ may differ across the APAC region, but the research also shows that users express preferences around the functionality and models of engagement based on the type of mobile activity they undertake. Checking a train time is about ease of use, buying the ticket is about speed and security, while reserving a hotel room or buying a travel case for the journey online requires various kinds of prompts and assurances: payment choice, status checking, incentives and customer service.

OpportunityOptimisationUsers enjoy undertaking simple information-based activities as they are easy and, in return, convenient to do. Yet complex functionality brings with it practical challenges. A significant opportunity exists for mobile service providers and brands to capitalise upon. Providers should understand that users now expect to be able to

The Mobile Consumer: Findings for Asia Pacific

23 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

engage at a higher level, and they seek to do so simply and effectively. Providers are tasked with meeting and exceeding these expectations.

SimpleMobilitySimplicity forms the basis of why users embrace mobile technology – adoption of services is accelerated by ease of use. Simplicity brings with it convenience, and this in turns creates benefits for users. However these benefits can be compromised by unwanted complexity and security threats. The mobile industry should seek to minimise, or at least appease, such concerns going forward. In practice, a careful balance needs to be maintained. Whilst simple functionality is fundamental, if security is the source of complexity issues, it is often a necessary price to pay.

Within the APAC market, both security and an easy to use interface are shown as key drivers to increased adoption of further mobile transaction. Assurances around personal information and

transactional data security while retaining a simple and easy to use format will be crucial in underpinning any future rise in consumer purchase take-up.

SmartphonetoSmartServicesAs the level of device sophistication starts to become commonplace, a transition from focusing on ‘device tech’ to service becomes more apparent. As a result, consumers will be increasingly influenced by service excellence over technology sophistication. This places pressure on the marketing and operational infrastructure of business selling and providing services via mobile – technology companies have to become more ‘service-centric’ and service businesses (banks, retailers, etc.) have to adapt to working in a complex mobile environment. As the landscape transforms, brands must understand their customers better in order to fully realise and capitalise on the customer relationship. By doing so, mobile providers and brands will be better placed to engage users and create higher value services in the future.

.

Brands must understand their customers better in order to fully realise and capitalise on the customer relationship.

The Mobile Consumer: Findings for Asia Pacific

24 / 25

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

Consumers will be increasingly influenced by service excellence over technology sophistication.

.

Appendix

© 2013 SAP AG or an SAP affiliate company. All rights reserved.

ResearchMethodology3,288 interviews were conducted with adults aged 18+ who own a mobile phone (basic or smartphone) in APAC (China n=1000, India n=1050, Japan n=651, Australia n=587). Respondents completed an online survey in March/April 2013. Research conducted by Loudhouse, an independent research agency based in London.

AboutLoudhouseAs part of Octopus Group, Loudhouse is one of the UK’s leading performance and influencer marketing agencies, working with blue chip clients in technology, business services, finance and retail sectors.

Formoreinformation,gotoloudhouse.co.uk

AboutSAPAs the market leader in enterprise application software, SAP (NYSE: SAP) helps companies of all sizes and industries run better. From back office to boardroom, warehouse to storefront, desktop to mobile device, SAP empowers people and organisations to work together more efficiently and use business insight more effectively to stay ahead of the competition. SAP applications and services enable more than 195,000 customers to operate profitably, adapt continuously, and grow sustainably around the world.

Formoreinformation,gotosap.com