s3.amazonaws.coms3.amazonaws.com/zanran_storage/€¦ · 2001 was a strong year for australian...

TRANSCRIPT

AAUUSSTTRRAALLIIAA’’SS TTRRAADDEE

22000022

OUTCOMES AND

OBJECTIVES

STATEMENT

AUSTRALIA’S TRADE

© Commonwealth of Australia 2002

This work is copyright. The material contained in this statement may be freely quoted withappropriate acknowledgment.

Includes Index.

ISBN 0-642-99639-3.

1. International trade. 2. Australia – Commerce. 3. Australia – Foreign economic relations. I.Australia. Dept. of Foreign Affairs and Trade.

337.94

Produced by the Trade Development Division of the Department of Foreign Affairs and Trade withinput from Austrade. A number of Commonwealth Government agencies provided assistance,particularly, Agriculture, Fisheries and Forestry – Australia; the Department of Industry, Tourism and Resources and the Department of Transport and Regional Services.

The Department of Foreign Affairs and Trade would like to thank the following for providingphotographs: Austrade (pages 51, 53, 54, 59, 91, 93 and 113); Supermarket to Asia Ltd (pages 8 and 104); Meat and Livestock Australia (page 23); Newspix Photo Service (pages 11, 21 and 31); AAP Photo Service (pages 92 and 117); Reuters Photo Service (page 36); The Gulf Times (page 6); Austal Ships (page 129) and AusAID (page 133).

Edited by Paul Myler, with assistance from Nathan Backhouse, Cynthia Dearin, Alba Salsone, Axel Wabenhorst, DFAT’s Market Information and Analysis Unit, Kelly Ralston and Julie Monson(Austrade), and Jeff Fitzgibbon (external editor).

Design and typeset by Di Walker Design, Canberra.

Printed by National Capital Printing, Canberra.

Unless otherwise specified, all amounts are in Australian dollars.

ii

2001 was a strong yearfor Australian exports,despite the economicdownturn experiencedby most of our majortrading partners. A verycompetitive Australiandollar helped underpinrobust growth in exportvolumes, and strong

prices in key commodity markets also helpedboost Australian dollar prices received for exports.

The value of Australia’s exports of goods andservices increased by 8 per cent to $154 billion in2001. This performance builds on the record 25 percent growth recorded in 2000. Export volumes roseby 1 per cent, while the prices received formerchandise exports rose 7 per cent. Merchandiseexports to all major trading partners grew strongly,with exports to China, the European Union andthe United States experiencing particularly strongrises of 26, 18 and 8 per cent respectively.

Australia’s strong export performance saw it recorda $2.7 billion trade surplus in 2001. This representsa turnaround of $10.1 billion on the $7.4 billiondeficit recorded in 2000.

I commend Australian business for this result. It confirms that Australian firms are respondinginnovatively and successfully to changes in theinternational economy. Several of these successfulfirms are highlighted in this statement, althoughthere are many thousands more that areenergetically and creatively pursuing exports.

Australia will need all this creativity anddedication to maintain our momentum in 2002. It is clear that, with Europe, Japan and the UnitedStates all suffering an economic downturn,

with flow-on effects to ASEAN and other majorcustomers of our goods and services, 2002 will bea challenging year. The pace of our export growthhas already slowed significantly, and will slowfurther if global demand remains suppressed.

The Australian Government stands ready to facethese challenging times, in partnership withbusiness and the community. Australia needsexports and we need more Australian businesses tobecome exporters. Exports are critical to generatingwealth, creating jobs and raising living standardsfor all Australians. The dynamism of our exportsector was a key reason why Australia withstoodthe worst impacts of the Asian financial crisis of1997-98. An entrepreneurial export sector can helpus in the face of the current world slowdown.

The Government expects world growth to return tonear the long-run average of 3-4 per cent by 2003.We want to have a new crop of exporters readyand able to exploit this return to global growth.

The Government has set itself the ambitious goalof doubling the number of Australian businessesexporting by 2006 and is already taking steps,primarily through Austrade, to pursue this by:

• committing $21.55 million over four years to the TradeStart and Export Access initiatives,including funding for ten new offices;

• raising the minimum Export MarketDevelopment Grant (EMDG) from $2 500 to $5 000, at a cost of $1.6 million over four years;

• increasing its trade outreach effort to ensuremore Australians are aware of the role ofexporting and the benefits of trade.

Despite the recent Farm Bill and steel setbacks inthe United States, there is renewed internationalmovement on trade liberalisation. A new World

M i n i s t e r ’s Fo re w o rd iii

MINISTER’S FOREWORD

iv

Trade Organization (WTO) Round was launchedin Doha and our officials in Geneva are beginningnegotiations that must result in a non-discriminatory approach to agriculture trade. We also hope to make significant gains for ourvibrant and growing services export sector as wellas building on past progress in opening marketsfor industrial products.

For a relatively small trading nation, a universallyrecognised, rules-based system is the best meansof defending our interests and pressing for greateraccess to key markets. But we are not relyingsolely on the WTO. Australia’s trade policy aimsto secure the best possible access to overseasmarkets for Australian exporters – whereveropportunities to do so appear. In these times ofeconomic uncertainty, the Government is – morethan ever – vigorously protecting Australia’sinterests through a multi-faceted trade policy.Multilateral, regional and bilateral strategies allhave an important role in promoting Australia’strading interests.

We have backed this commitment with increasedresources for trade negotiations. The Governmenthas established an Office of Trade Negotiationswithin the Department of Foreign Affairs and Tradeto bring together trade specialists to help Australianexporters open up markets and win trade disputes.The new Office of Trade Negotiations will have 60 per cent more staff than the correspondingdivision at the end of the Uruguay Round ofmultilateral negotiations in 1993. The Office’sleadership team will be supplemented by a SpecialNegotiator with responsibility for free tradenegotiations, a Special Negotiator for Agricultureand an additional senior appointment to Australia’sWTO mission in Geneva to strengthen thenegotiating team in Geneva.

We are establishing new alliances – either throughthe Cairns Group or new issue-specific groups – to secure favourable trade outcomes from themultilateral trading system. As a medium-sizedplayer, Australia needs to be clever in buildingcoalitions. In particular, Australia must continue tobuild stronger relations with developing countries.

Our interests in agricultural reform are closelyaligned and developing countries are playing anincreasingly significant role across the WTO agenda.

Our commitment to APEC is unfaltering. APECsolidarity helped prevent a return to tradeprotectionism, despite the East Asian financialcrisis and the current economic downturn, andcontinues to promote positive approaches to thechallenges of globalisation and trade facilitation.APEC’s cross-section of developed anddeveloping economy membership was useful inbuilding consensus for launch of a new round ofWTO negotiations in Doha.

The commitment made by ASEAN EconomicMinisters and Australian and New Zealand Trade Ministers in September 2001 to endorse a framework for the ASEAN Free TradeArea–Australia–New Zealand Closer EconomicRelations (AFTA-CER) Closer EconomicPartnership (CEP) builds on six years of work on trade facilitation and economic cooperationbetween the two regions. The CEP frameworkprovides, for the first time, a formal and structuredapproach to promoting trade, investment andregional economic integration. And, importantly,this commitment was made against a backdrop of slowing regional and global growth. Theframework will be embodied in an instrument to be signed by Ministers in September 2002 in Brunei.

This Government also recognises that bilateralinitiatives can offer significant benefits. Worktowards open and comprehensive Free TradeAgreements (FTAs) with important neighbourslike Singapore and Thailand contributes to ourbroader strategic objective of achieving an openglobal and regional trading environment that willdeliver benefits to all.

Australia also sees potential for substantial gainsfrom an FTA with the largest and most dynamiceconomy in the world – the United States.Improved access to US markets would have directbenefits for Australian exporters. Economicmodelling has shown that these benefits could addup to $2 billion a year for the Australian economy.

However, a US FTA would deliver more than justdirect trade benefits. It would also be an effectivemeans of attracting US investment at a time ofintense international competition for US businessand investors. And, by closely aligning the twoeconomies, an FTA would facilitate adoption byAustralian companies of US best practice in areassuch as business administration and e-business.

The Government is also constantly looking atfresh ways to inject momentum and growth intoour strongest and most mature tradingrelationships. Under the rubric of ‘strengtheningeconomic relations’, traditional trading partners inJapan, South Korea and China are being exposedto the modern, diverse, innovative Australianeconomy in ways which can promote a broaderrange of commercial interaction.

The world trading environment is undergoingconstant change. In this dynamic environment,governments cannot afford to become lazy orhave all their trade policy eggs in one basket. This Government has the energy, commitmentand vision to pursue an active and diverse tradepolicy, as I am sure you will see from this TradeOutcomes and Objectives Statement.

And, of course, this Government has acontinuing commitment to providing exporterswith a strong economic foundation and flexibleindustrial relations framework on which to buildtheir business.

Our multi-faceted trade policy will deliver forAustralians in the city and the bush. I hopeAustralian business, large and small, urban andregional, will join the Government in our quest todouble the number of exporters.

Mark VaileMinister for Trade

vM i n i s t e r ’s Fo re w o rd

Introduction

Australia’s ambitious trade policy agenda reflectsthe link between trade and the success of thenational economy. Trade has always been good forAustralia, helping maintain its enviable standard ofliving. Exporters generally provide better wages,salaries and conditions for their employees.Australian exporters are also among the fastest-growing companies, providing increasing jobopportunities for Australian workers. Over the pastten years, around 1.7 million Australian jobs a yearon average have been directly or indirectlyconnected to exports. One in five Australian jobsnow relies on the export sector. In rural and regionalAustralia, that figure increases to one in four jobs.

In 2001, the value of Australian exports of goodsand services increased by 8 per cent to $154 billion.This strong performance saw Australia record a$2.7 billion trade surplus, a turnaround of $10.1 billion on the $7.4 billion trade deficit in2000. Merchandise exports to all major tradingpartners grew strongly, with exports to Chinagrowing by 26 per cent, the European Union by 18 per cent, the United States by 8 per cent andJapan by 9 per cent. ASEAN grew by 2 per centand East Asia as a whole by 7.6 per cent. The lowvalue of the Australian dollar and strongfundamentals of the economy have contributed tothe ongoing competitiveness of Australia’s exports,despite the slowing global economy.

Exports of primary products (rural, mineral andenergy) increased by 12 per cent in 2001, butAustralia’s reliance on them has diminished inrecent years such that they constituted only 45 percent of Australian exports in 2001. As tariffs havefallen, the manufacturing sector has increased its

output and diversity, and exports of elaboratelytransformed manufactures have risen dramatically.Exports of manufactures rose by 11 per cent in2001, and now constitute 30 per cent of totalexports. Exports of services fell 1.5 per cent in 2001following the Olympics-related peak in 2000, but now make up 20 per cent of total exports.

The Government’s domestic economic reformagenda has provided a strong and resilienteconomic base for exporters. Sound fiscal policyhas maintained the confidence of financial markets,and has helped keep long-term interest rates low.Australia’s microeconomic reform agenda,including the introduction of a new taxationsystem, labour market reform and privatisation ofpublic utilities, has also generated productivitydividends for exporters. The InternationalMonetary Fund (IMF) forecasts that the Australianeconomy will grow by 3.3 per cent in 2002 – among the highest growth rates in the OECD.

The international tradingenvironment

The international trading environment is enteringa challenging period. Many of Australia’s tradingpartners, including Japan, the United States, theEuropean Union and the countries of South-EastAsia, have been experiencing an economicdownturn, leading to slowing growth in demandfor Australian exports. The global economicdownturn was accentuated by the 11 Septemberterrorist attacks, with world growth for 2001revised down to 2.4 per cent in the second half of2001. World governments responded quickly withfiscal and monetary policy measures designed to

EXECUTIVE SUMMARY

vi

restore spending and confidence. World interestrates are at 30-year lows, and major economiessuch as the United States and Japan haveannounced fiscal stimulus packages. Worldgrowth for 2002 is forecast to continue at 2.4 percent but is predicted to return to near the long-term average of between 3 and 4 per cent in 2003.World financial markets are now at levelscomparable to those before September 11.

The launch of a new round of global tradenegotiations at the Fourth WTO MinisterialConference in Doha, Qatar, in November 2001 wasa positive outcome for Australia. This had been akey trade policy goal for the Government for anumber of years, and the Government isdetermined that real and substantial market accessgains – particularly in agriculture – will result fromthe Doha Round. Australia remains one of the fewdeveloped countries with significant export markets– primarily in Asia – that still have high tariffs.

The WTO’s rules-based trading system is the bestway for a relatively small trading nation likeAustralia to defend its interests and press forgreater access to key markets. The disputeresolution mechanism ensures that commitmentsand obligations in WTO agreements are respected,guarantees access to overseas markets and protectsagainst unfair trading practices. In 2001, the WTOmade several rulings in Australia’s favour,including in disputes with the United States (lamb)and South Korea (beef). In coming years, globalcommitment to trade liberalisation will depend onleadership from the largest economies, includingtheir compliance with adverse WTO rulings andrestraint on export subsidies, tax breaks forexporters and punitive tariffs.

Implementation of China’s WTO obligations islikely to be the most important trade liberalisinginfluence in the global economy until theconclusion of the Doha Round. The accessions ofChina and Chinese Taipei will create bothopportunities and challenges for Australianbusiness. China is likely to attract furtherinvestment, possibly at the expense of other East

Asian economies, helping China’s exports andexposing domestic firms to greater competition.This opening of China’s economy will boost itsefficiency, including in its manufacturing sector,which will make Australia an important source ofhigh-quality raw materials. Australia’s goodstrade with China should also diversify, asincreasingly affluent Chinese consumers demandhigh-quality foods, manufactures and services.

Globalisation is presenting Australian businesswith exciting new opportunities. It enablesAustralian business to find new markets for itsproducts, attract international capital to develop itseconomic potential, and access better and cheaperbusiness inputs to make domestic enterprisesglobally competitive. Many Australian companieshave successfully integrated into the worldeconomy and are competing with the world’s best.By competing in the global market, Australianfirms become more efficient and innovative,adopting and developing global best practice.

Some Australian industries and communities havefaced difficulties as international competition hasincreased and protection for local industries hasbeen reduced. However, Australia’s future restson its ability to embrace change. The Governmentis committed to helping communities in theprocess of structural adjustment brought on byincreased international competition.

The trade liberalisation track that Australia haschosen is the right one. For some years, the pricesAustralians pay for imports have been fallingrelative to the prices received for exports. Australiahas embarked on a long-term improvement in itsterms of trade. Australia is getting richer.

The new WTO Round

Australia was strongly committed to the launch ofthe new WTO Round in Doha in November 2001.Gains from trade liberalisation since 1986 haveprovided the average Australian family with morethan $1 000 extra a year. It is estimated that a 50

viiE x e c u t i v e S u m m a r y

viii

per cent reduction in protection globally woulddeliver a further economic boost to Australia ofmore than $7 billion a year.

Australia is determined that real and substantialmarket access gains will result from the DohaRound, and hopes to move the negotiationsforward as quickly as possible to secure earlybenefits. The Doha Ministerial Declaration placesthe elimination of agricultural export subsidies onthe agenda for the first time ever. Total subsidiesfor agriculture in OECD countries rose to astaggering US$327 billion in 2000, approximatelysix times the total flow of aid to developingcountries. These subsidies encourage excessproduction, leading to unstable and depressedworld prices. The ambitious agricultural mandatehas significant potential to expand global marketsfor Australian farmers and food producers.

The Doha Declaration also gives a commitment tonegotiate on a wide range of issues, includingservices, industrial products, intellectual property,anti-dumping and other WTO rules issues,dispute settlement, and some trade andenvironment issues. The strong influence ofdeveloping countries is reflected in thedevelopment focus of the Doha Round and willhave an important influence on the futureoperations of the WTO.

The negotiating mandate provides a good basisfor further liberalisation, but the ambitiousrhetoric that accompanied the launch has yet toface the test of negotiations.

Beyond the WTO – Australia’smulti-faceted trade policy

Australia is not relying solely on the WTO forgreater access to overseas markets. Australia isalso pursuing regional and bilateral initiativeswhere the parties are willing to proceed faster andliberalise more profoundly than can be achievedby the entire WTO membership. These strategiesalso build momentum for WTO negotiations and

can create useful templates for dealing with newand complex issues.

Australia places a priority on helping develop aprosperous region – and in the process, creatingcustomers for Australian goods and services.Encouraging trade and investment liberalisation isat the core of Australian efforts, but parallelreforms in areas such as economic and corporategovernance, infrastructure and information andcommunications technology (ICT) development,trade facilitation and capacity-building are alsorequired throughout the Asia Pacific. Australiahas been pursuing these goals through a varietyof regional forums, principally APEC.

Australia led the successful campaign to introduce‘pathfinder’ initiatives at the Shanghai APECLeaders Meeting in October 2001. These initiativeswill enable those APEC economies that can movemore quickly to pursue the Bogor Goal moreaggressively. Many of the pathfinder initiativeswill focus on trade facilitation and reducing thecosts of doing business in the region.

In September 2001, ASEAN Economic Ministersand Australian and New Zealand Trade Ministersendorsed a framework for a Closer EconomicPartnership (CEP), building on the trade facilitationand economic cooperation of recent years. Thisprovides, for the first time, a formal, structuredapproach to promoting trade, investment andeconomic integration between these countries.Ministers agreed to an initial work program inareas including customs, e-commerce and smalland medium enterprises. The framework will beembodied in an instrument to be signed byMinisters in September 2002 in Brunei.

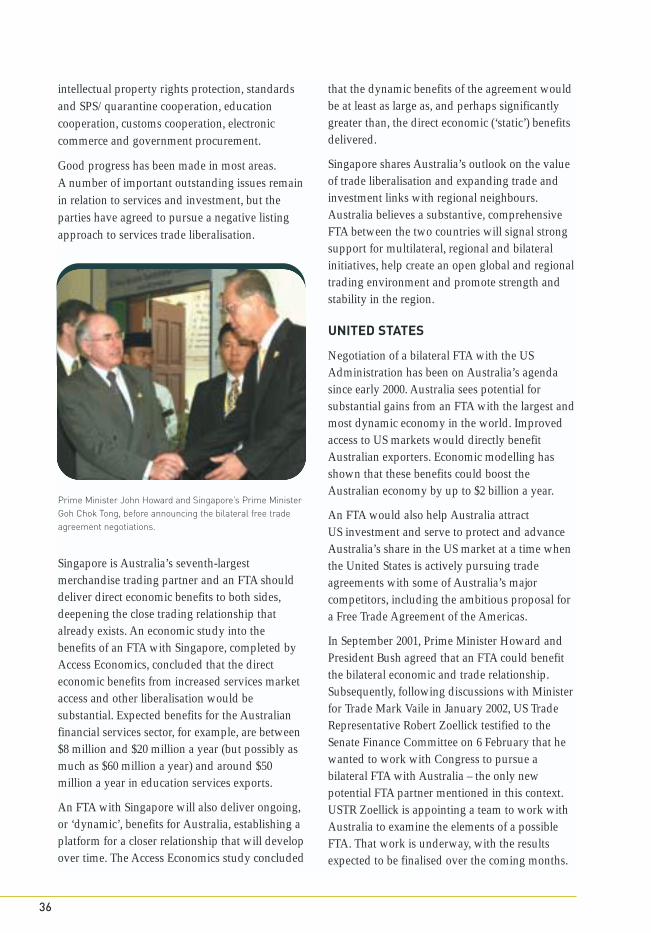

Australia pursues bilateral trade arrangementswhere these can deliver substantial economic gainsmore rapidly than multilateral or regionalapproaches. The Government is committed to freetrade agreements (FTAs) that are comprehensiveand transparent. Australia already has onecomprehensive FTA with New Zealand, commonlyknown as CER (Closer Economic Relations), and isnegotiating an FTA with Singapore. Good progress

has been made on the latter, but provisions onservices and investment liberalisation remaincontentious. Bilateral FTAs are also beingconsidered with Thailand and the United States.

Australia is also pursuing a range of initiatives tostrengthen economic relations with some of itslargest trading partners. In the case of Japan andSouth Korea, the aim is to broaden the relationshipsbeyond their pre-globalisation, commodities-basedstatus. Australia’s China initiative aims to takeadvantage of China’s accession to the WTO,strengthening trade relations in key sectors such asfinancial and legal services, education, socialwelfare, agriculture, the environment and inconnection with the Beijing Olympics.

The Government is also pursuing sectoralinitiatives to facilitate exports. An Action Agendahas been developed to help the freight logisticsindustry meet the challenges of globalisation,environmental sustainability and infrastructurerequirements. Similar efforts are being madethrough APEC and other regional initiatives toimprove transport and logistics throughout theregion. The Government is also pursuing initiativesin paperless trading and e-commerce, biosecurity,and standards and conformance to reduceexporters’ costs of doing business internationally.

Growing the exportercommunity

Although exports grew from $101 billion in 1996to a $154 billion in 2001, less than 4 per cent of theAustralian firms contributed to this result. This isa low proportion of exporters by internationalstandards. There is enormous untapped exportpotential, particularly in the small to mediumenterprise (SME) sector. The Government isworking to encourage more exporters and higherlevels of trade because of the macroeconomicbenefits of exports and the quality of jobsprovided by exporters. The Government has setitself the ambitious target of doubling the numberof Australian businesses exporting by 2006.

To help achieve its goal, the Government willcommit a further $21.6 million over four years toAustrade’s existing TradeStart and Export Accessinitiatives. The TradeStart network of offices inrural and regional Australia helps rural andregional businesses access Austrade’s exportdevelopment opportunities. From 2002–03, tennew TradeStart offices will open. The ExportAccess program helps prepare Australian SMEsfor exporting through a 12-month counselling andtraining program. During 2001, some 568 SMEswere supported under the program. Austrade alsoprovides seminars on e-commerce for exportersand on how to get into export.

The Export Market Development Grant (EMDG)scheme helps small business to develop exportmarkets by reimbursing up to 50 per cent ofcompanies’ overseas promotional expenses. In 2000–01, the scheme distributed grants to thevalue of $134.6 million to 2 886 businesses. The Government is raising the minimum grantfrom $2 500 to $5 000 from 1 July 2002. Austrade’sNew Exporter Development program, beginningin July 2002, will deliver coaching and trainingprograms to SMEs in rural, regional and outermetropolitan areas during the various stages ofpreparation for export.

Key trade objectives for 2002

Trade performance is built by committed,sustainable exporters, not governments.Increasing the pool of successful exporters willstrengthen the Australian economy. That is whythe Government is implementing strategies,primarily through Austrade, designed to doublethe number of sustainable exporters in theAustralian business community by 2006.

The Government is simultaneously pursuing amulti-faceted trade policy, working at multilateral,regional and bilateral levels to capture the benefitsof trade liberalisation and internationalinvestment for Australia – and ensure openmarkets and low-cost trading arrangements forour current and future exporters.

ixE x e c u t i v e S u m m a r y

x

In the new Doha Round of global tradenegotiations, the Government will work hard forsubstantial reductions in agricultural exportsubsidies and the reform of other trade-distortingmeasures that impede Australian competitivenessand block access to markets. The Government alsoaims to move the negotiations on services andindustrial products forward as quickly as possibleto secure early benefits.

Australia will continue its commitment to APECincluding through the ‘pathfinder’ initiativemechanism. It will also cooperate with ASEANand New Zealand to formalise the AFTA-CERCEP Framework through signature of aministerial declaration expressing the politicalcommitment of members to work towards moreclosely integrated economies.

The Government will push for the completion ofnegotiations for a free trade agreement withSingapore and for the launch of negotiations withThailand and the United States. It will also pursuestrengthened economic relations with Japan andSouth Korea and a framework economicagreement with China.

Through Austrade, the Government has identifiedeight sectors with particularly strongopportunities for export growth in the future:agribusiness, automotive, defence, education,environment, sporting and other infrastructure,knowledge-based industries (business services,ICT and biotechnology) and tourism.

The Market Development Group has identifiedadditional immediate market access objectives for2002. These include the development of a long-term supply and investment partnership forliquefied natural gas (LNG) with China; increasedexports of live animals to Taiwan, Vietnam,Indonesia and Europe; increased exports ofeducation services to Indonesia and Brazil;increased automotive component exports to China;and new markets for Australian information andcommunications technology and biotechnology inJapan and China. A full range of other product ormarket specific access issues are also pursued bythe global network of posts as well as Canberra-based officers as a matter of course.

INCREASED RESOURCES DEDICATED TO TRADE NEGOTIATIONS

The Australian Government has increased resources for trade negotiation in response to its activeand diverse trade agenda. First and foremost, it has established an Office of Trade Negotiationswithin the Department of Foreign Affairs and Trade to bring together trade specialists to helpAustralian exporters open up markets and win trade disputes. The new Office of TradeNegotiations will have 60 per cent more staff than the corresponding division at the end of theUruguay Round of multilateral negotiations in 1993. The Office’s leadership team will besupplemented by a Special Negotiator with responsibility for free trade negotiations and a SpecialNegotiator for Agriculture. The Government has also made an additional senior appointment toAustralia’s WTO mission in Geneva to strengthen the negotiating team in Geneva. Together withthe Ambassador to the WTO, this new senior appointment will be responsible for agriculturenegotiations and coordination of the Cairns Group.

MINISTER’S FOREWORD iii

EXECUTIVE SUMMARY vi

TABLE OF CONTENTS xi

1: THE TRADE POLICY ENVIRONMENT 1

A new WTO round launched 5The development agenda 5

Global enthusiasm for free trade agreements 7

Regional developments 8

Maintaining momentum for liberalisation – the need for leadership 9

2: THE NEW WTO ROUND – AUSTRALIA’S INTERESTS AND STRATEGY 13

Agriculture 16

Industrials 18

Services 19

New issues on the WTO agenda 20Competition policy 20Investment 20Environment 20TRIPS and pharmaceuticals 21Expansion of geographic indications 22

Fighting for a fair go 23

Recent and forthcoming accessions 25

3: BEYOND THE WTO – AUSTRALIA’S MULTI-FACETED TRADE POLICY 27

Enhancing exporters’ competitiveness 30

APEC and other regional initiatives – creating prosperous markets 31APEC 31Australia, New Zealand and ASEAN 33Australia and the Indian Ocean 33

C o n t e n t s xi

TABLE OF CONTENTS

xii

Bilateral strategies – linking Australia to major markets 35Free Trade Agreements 35

New Zealand 35Singapore 35United States 36Thailand 37

Strengthening economic relations 37Japan 37Republic of Korea 38China 39

Faster, cheaper, safer – trading into the new millennium 40Transport and logistics 40Paperless trading 41E-commerce 41Biosecurity 42International trade rules for biotechnology 43Standards and conformance 44

4: GROWING AUSTRALIA’S EXPORT COMMUNITY 49

Doubling the size of the export community 51

Capturing export opportunities 54Australia’s global network 55

Attracting overseas investment 56

Building commitment to trade and investment 58Exporting for the future 59

Supporting Australian companies and exporters 60TradeStart 60Export Access 61E-commerce for exporters 61Getting into Export seminars 62TradeSat 62Industry specialists 62Export Advisory Service 62

Financing export activity 64Export Market Development Grants 64EFIC credit insurance and trade finance 65

Government and business working as one 68Government–business consultation 68State and territory government trade promotion activities 70Growing international demand for Australian products 71

5: AUSTRALIA’S TRADE PERFORMANCE IN 2001 73

6: THE INTERNATIONAL ECONOMIC OUTLOOK 81

World economic performance 83

Australia’s key markets: outlook and opportunities 85Japan 85United States 88China 92Republic of Korea 95New Zealand 98European Union 100ASEAN 103

Emerging markets 107Middle East 107Latin America 111Central, East and South Europe 114India 117

7: EXPORT OPPORTUNITIES 121

Tourism 123

Agribusiness and Food 124

Automotive 126

Defence 128

Education 130

Environment 131

Infrastructure 132

Knowledge-based products and services 134

Information and communications technology 134Business and professional service 135Biotechnology 135

8: INTERNATIONAL TRADE – GOOD FOR AUSTRALIA 139

Exporting to prosperity 142

Clearing the air – myths and facts about trade, investment and globalisation 144

Good trade policy: delivering for Australians 146

xiiiC o n t e n t s

xiv

APPENDIX 1: STATISTICAL TABLES 150

Table 1: Australia’s principal merchandise export destinations 150

Table 2: Australia’s principal merchandise import sources 151

Table 3: Australia’s services exports 152

Table 4: Australia’s services imports 153

Table 5: Foreign investment in Australia 154

Table 6: Australian investment abroad 155

Table 7: Australia’s balance of payments 156

APPENDIX 2: MARKET DEVELOPMENT GROUP PRIORITIES FOR 2002 157

Objectives for Europe, Americas, Middle East, Africa and South Pacific (March 2001 – March 2002) 157Objectives for North Asia, South and South-East Asia (June 2001 – June 2002) 158

APPENDIX 3: PROGRESS AGAINST OBJECTIVES IDENTIFIED IN TRADE OUTCOMES AND OBJECTIVES STATEMENT 2001 159

China 159

India 166

Latin America 171

APPENDIX 4: PROGRESS AGAINST OBJECTIVES IDENTIFIED IN TRADE OUTCOMES AND OBJECTIVES STATEMENT 2000 174

Central and South Eastern Europe 174

European Union 177

Hong Kong 179

Mexico 181

Middle East 182

Papua New Guinea 184

Peru 187

Philippines 189

Singapore 190

South Asia 194

APPENDIX 5: GLOSSARY OF TERMS 196

APPENDIX 6: PUBLICATIONS 198

APPENDIX 7: FOREIGN AFFAIRS AND TRADE PORTFOLIO 201

INDEX 203

THE TRADE POLICYENVIRONMENT 1

THE TRADE POLICY ENVIRONMENT IS

UNDERGOING DYNAMIC CHANGE

CH

AP

TE

R

1

• A new WTO Round was launched in Doha. This was the Government’s primary tradepolicy goal over recent years. A 50 per cent further reduction in protection globallywould deliver an economic boost of more than $7 billion a year to Australia.

• The increase in numbers and growing assertiveness of developing countries in theWTO led to the ‘Doha Development’ Agenda. Developing alliances with thesecountries, through the Cairns Group or new issue-specific alliances, will beimportant for successful promotion of Australia’s interests in the Doha Round.

• The WTO has become more legalistic and both the US and EU have felt unable tocomply with adverse rulings on key policies, with uncertain implications formembers’ acceptance of future rulings.

• China has completed its accession to the WTO. Implementation of China’s WTOaccession obligations is likely to be the major liberalising dynamic within the globaleconomy in forthcoming years – at least until completion of the Doha Round.Australia will be working with China to ensure Australian companies benefit fromthe opportunities deriving from China’s implementation.

• Enthusiasm for FTAs continues unabated, despite the launch of the Doha Round.Comprehensive FTAs can complement multilateral negotiations where parties canliberalise faster and deeper than can be achieved by the whole WTO membership.They are also useful in addressing new issues such as e-commerce.

• It is clear there will be continued efforts over coming years to forge an East Asianregional identity. ASEAN+3 is the primary manifestation of this, but furtherdevelopment will involve a delicate balancing of the strategic interests andambitions of Japan and China.

• Australia and New Zealand are the first ASEAN dialogue partners to agree a formaland structured approach for promoting trade, investment and regional economicintegration. Importantly, this decision to enhance and formalise relations was madeagainst a backdrop of slowing regional and global growth.

• Given the global preponderance of the US economy, US leadership in the WTO andtruly pro-liberalisation policies at home are more important than ever to tradeliberalisation efforts. Australia is closely watching developments in the US on tradepromotion authority, the Farm Bill and the Foreign Sales Corporations ruling. The imposition of a safeguard measure on steel will have global repercussions.

AT A GLANCE

2

The international trade policy environment isentering a challenging period – a new WorldTrade Organization (WTO) Round has beenlaunched, with the active involvement ofdeveloping countries; China has completed itsaccession to the WTO and must now begin todischarge its obligations (under close scrutinyfrom trading partners); and economic downturnhas stimulated continuing challenges toAustralia’s goal of an integrated, liberalisedglobal economy.

The 11 September terrorist attacks have shakenconsumer and business sentiment and accentuatedthe slowdown of the global economy. The attackshave jolted the established order of political andsecurity affairs, but the impact on trade policy isless apparent.

Australia will meet the challenges of the changingtrading environment through a mixture ofmultilateral, regional and bilateral strategies, andwork with major players in the internationalenvironment to take advantage of the changestaking place. Our trade and economic interests arenot constrained by geography. We trade heavilywith Asia; invest predominantly in the US, Europeand New Zealand; and are closely allied withdistant and disparate countries like Chile,Paraguay and South Africa in the Cairns Group.

The launch of the Doha Round has been a keytrade policy goal for the Government for anumber of years. For a medium-sized economylike Australia, the importance of a transparent,predictable, rules-based multilateral tradingsystem should never be underestimated. The Government is determined that real andsubstantial market access gains – particularly inagriculture – will result from the Doha Round.

Australia remains one of the few developedcountries with significant export markets –primarily in Asia – that still have high tariffs.Reducing these barriers will be a challenge, one that will require a wide range of strategies.Fortunately for Australia, some of these countrieshave been reassessing their economic and tradepolicies in the wake of the economic downturn,especially in global demand for information andcommunications technology (ICT) products, andthe sharp reversal of foreign direct investmentflows away from South-East Asia towards China.This has opened up opportunities for Australiaacross our multilateral, regional and bilateral freetrade agreement (FTA) strategies.

Enthusiasm for FTAs continues unabated, despitethe launch of the Doha Round. And there areclearly going to be continued efforts over comingyears to forge an East Asian regional identity, withJapanese Prime Minister Koizumi the latest toespouse such a vision – encompassing North Asia,South-East Asia, Australia and New Zealand.

Membership of the WTO has increased by morethan 50 per cent since the end of the UruguayRound – a sign that the WTO is a club thatcountries want to belong to – but there is agrowing developed/developing country divide.The increase in numbers and the growingassertiveness of developing countries were a newdynamic in Doha, leading to the creation of the‘Doha Development’ Agenda. The implications ofChina’s accession on the functioning of the WTOare uncertain.

At the same time, the WTO has become morelegalistic and, while the legally enforceabledispute settlement system works most of thetime, it can discourage resolution of problems by

3T h e T r a d e P o l i c y E n v i r o n m e n t

CH

AP

TE

R

1

4

negotiation. Australia has had some notablevictories that have opened significantopportunities for Australian exporters. Exports ofbeef to South Korea and of lamb to the UnitedStates were the most prominent successes in 2001.However, both the United States and theEuropean Union have been unable to complywith adverse rulings on key policies because ofthe perceived political and/or commercial costs

of doing so, with uncertain implications formembers’ acceptance of future rulings. The recentEU victory in the US Foreign Sales Corporationscase is perhaps one of the most challengingrulings, and Australia awaits the US response.Given the global preponderance of the USeconomy, US leadership in the WTO and trulypro-liberalisation policies at home are moreimportant than ever to trade liberalisation efforts.

BENEFITING FROM LIBERALISATION

Australian jobs and living standards are more dependent than ever on how well Australia performsin the global market place. To get the most from international trade, Australia needs a strongrules-based multilateral trading system that guarantees access to overseas markets and providesa predictable international environment for exports to grow. As a medium-sized and broadly-basedeconomy, Australia cannot go it alone.

Full implementation of the Uruguay Round was conservatively estimated to add about $4.4 billiona year to Australia’s real GDP (in 1992 dollars) and boost exports by over $5 billion a year. Gainsfrom trade liberalisation since 1986 have provided the average Australian family with more than$1 000 extra per year. It is estimated that a 50 per cent reduction in protection globally woulddeliver a further economic boost to Australia of more than $7 billion a year. Developing countriesalso stand to benefit, with global gains from a further 50 per cent cut in agricultural support alonelikely to amount to an additional $53 billion in global GDP.

These figures represent real jobs and real incomes for exporting businesses and communitiesthroughout Australia. For these reasons, Australia was a strong supporter of the launch of a newround at the Doha Ministerial Conference.

The new trade round faced numerous obstacles andits launch was uncertain until the closing hours ofthe Doha conference. International trade issues havebecome increasingly complex, particularly now theWTO comprises 144 members, over three-quartersof which are developing countries. With the failureto launch a round in Seattle in 1999, the importanceof a successful meeting in the current climate wasnot lost on members. That a meeting of 142 WTOmembers, together with China and Chinese Taipei,was being held in the Middle East, close to a warzone, against the background of 11 September andsigns of a slowing global economy, sent key signalsto the international economic community on theimportance of continuing multilateral tradenegotiations.

Ending the discrimination against agriculturaltrade is a key priority for Australia in the newround. Australian agriculture has a fundamentaldependence on global markets. Ninety eight percent of wool, 76 per cent of wheat and 63 per centof beef is ultimately exported. Agriculturalsupport in OECD countries rose to a staggeringUS$327 billion in 2000, approaching US$1 billion aday, equivalent to about six times the total flow ofaid to developing countries. The MinisterialDeclaration from Doha places elimination ofexport subsidies on the agenda for the first time ever.

The Doha Declaration also gives a specificcommitment to negotiations on a wide range ofissues, including services, industrial products,intellectual property, WTO rules (including anti-dumping), dispute settlement and some trade andenvironment issues. Further work will also takeplace on a number of the trade-linked or so-called

‘Singapore issues’ (investment, competition policy,transparency in government procurement andtrade facilitation) with a view to a decision onnegotiations at the next Ministerial Conference inMexico in 2003.

The ambitious rhetoric and support for tradeliberalisation that accompanied the launch of theDoha Round has yet to face the test of actualnegotiations. Ministers have set an ambitioustimeframe for the negotiations to be concluded byno later than 1 January 2005. The difficulties inreaching agreement on the negotiating mandate,and the modalities for negotiations since Doha,highlight the task that lies ahead in securingconsensus on issues of substance. In contrast tothe Uruguay Round, there is no simple, over-arching balance between issues this time. This willrequire Australia to participate in or develop avariety of issue-specific alliances.

The development agenda

Developing countries emerged as key players inthe lead-up to the Doha Ministerial Conference,using the preparatory process as an opportunityto establish coalitions and formulate a coordinatedapproach to common concerns, particularlyfundamental agricultural reform.

The strong influence of developing countriesduring the negotiations is reflected in thedevelopment focus of the new round (the DohaDevelopment Agenda) and the increased emphasison integrating developing countries into the WTO system through greater capacity-building,technical assistance and special and differential

T h e T r a d e P o l i c y E n v i r o n m e n t 5

A NEW WTO ROUND LAUNCHED

CH

AP

TE

R

1

6

treatment. Ministerial agreement to a separateTrade-Related Aspects of Intellectual PropertyRights (TRIPS)/public health declaration at Dohawas another key victory for developing countries.The TRIPS Declaration is a good outcome that willhelp to address public health concerns such asaccess to medicines in the developing world.

This renewed focus on developing countrymembers will affect the future work program ofthe WTO and the resources allocated to theirinvolvement. This changing dynamic, coupledwith the accession of People’s Republic of Chinaand Chinese Taipei and an increasingly diversemembership base, will have an importantinfluence on the future operations of the WTO.

Australia will continue to engage with developingcountry members. Australia is committed toaddressing developing country concerns aboutdifficulties in the implementation of WTOagreements that emerged from the Uruguay Roundand its interests in agricultural reform are similar.Australia provides a program of technicalassistance and policy dialogue with developingcountries in our immediate region and beyond,aimed at strengthening their capacity to participatefully in the new trade negotiations and to takeadvantage of new market access opportunities. Forexample, in 2002, Australia is conducting a tradepolicy training course for African trade negotiators.

HH the Sheikh Hamad bin Khalifa al-Thani of Qatar opening the WTO conference in Doha, Qatar with WTO Director General MikeMoore (left) and HE the Minister of Finance, Economy and Trade Yousuf Hussain Kamal.

The number of countries exploring or enteringinto free trade agreement (FTA) negotiations hasaccelerated in recent years. Among the mostactivist bilateral FTA proponents have been Chile,Singapore, Mexico and New Zealand. However,even stalwart multilateralist countries – such asJapan and South Korea – are increasinglycanvassing potential FTAs. Japanese PrimeMinister Koizumi’s emerging vision for regionalengagement is of particular interest to Australiaand follows China’s agreement to develop an FTAwith ASEAN. The WTO Secretariat has identifiedsome 170 regional trade agreements (RTAs,comprising FTAs and customs unions) andestimates that their number could grow to 250 by2005. About 43 per cent of world trade is intra-RTA trade, and this could rise to over 50 per centby 2005.

Global interest in FTAs has been motivated by a range of factors, including a desire to gainmaximum short-term benefits in advance of theWTO Round, an attempt to capture strategicadvantages by establishing closer links betweenparticular countries, and an interest in triallingliberalisation in a smaller, more comfortableenvironment than the multilateral one.Development of the North American Free TradeAgreement (NAFTA), the potential of the FreeTrade Agreement of the Americas (FTAA) andexpansion of the European Union has influencedcountries outside these regions to explore linksboth with their own neighbours and into theseagreements.

Australia is pursuing a WTO-consistent FTAagenda with major trading partners. Negotiationsare underway with Singapore and Australia isexploring possible FTAs with Thailand and theUnited States. Such bilateral deals can offerAustralia great benefits where the other partiesare willing to proceed faster and undertake moreprofound liberalisation than can be achieved bythe entire WTO membership.

The decision to launch a new WTO Round atDoha is unlikely to have an immediate impact onthe trend towards FTAs. There has been increasingrecognition that FTAs can complement and buildmomentum for multilateral trade liberalisation, aslong as they cover substantially all trade in goodsand substantial sectoral coverage in services. FTAs can also play a particularly useful role indeveloping templates for new and complex issuessuch as competition policy, investment andelectronic commerce, or accelerating liberalisationin areas such as services.

T h e T r a d e P o l i c y E n v i r o n m e n t 7

GLOBAL ENTHUSIASM FOR FREE TRADE AGREEMENTS

CH

AP

TE

R

1

Efforts to forge an East Asian regional identitycontinue. The primary manifestation of this trend –the ASEAN+3 process – has already affectedinternational interaction in the region. Cooperationto date has focused on financial architecture. The pace of diversification into a wider economicand political agenda is difficult to predict.

Australia and New Zealand are the first ASEANdialogue partners to agree to a formal andstructured approach for promoting trade,investment and regional economic integration.Importantly, the September 2001 decision toenhance and formalise relations through theframework for AFTA-CER Closer EconomicPartnership was made against a backdrop ofslowing regional and global growth.

The later agreement in Brunei in November 2001that China and ASEAN should pursue a free tradearea within ten years reflects the growing role thatChina wants to play in Asia. ASEAN is alreadythe most important destination for Chineseexternal investment and accounts for 8 per cent ofChina’s total trade.

The East Asian financial crisis gave China theopportunity to become more involved and opento others within the region. It has prospered whilemany fell on hard times. Chinese confidence hasalso been boosted by the upsurge in foreign directinvestment, the growing competitiveness ofChinese goods on international markets, accessionto the WTO, chairing of APEC, hosting the 2008 Olympic Games and its ability to weatherthe worst effects of the current slowing of theworld economy. In turn, China’s persistently goodeconomic performance generates interest in Chinawithin the region.

REGIONAL DEVELOPMENTS

8

Australian food products on sale at the Australian Pavilion ofthe NTUC Fairprice supermarket in Bukit Timah Plaza,Singapore.

International support for trade liberalisation is,in reality, more limited than the ambitiousrhetoric at the launch of the Doha Round andnumerous efforts to negotiate free tradeagreements would indicate.

Implementation of China’s WTO accessionobligations is likely to represent the majorliberalising dynamic within the global economy inforthcoming years – at least until completion ofthe Doha Round.

The close, pragmatic relationship between theEuropean Union and the United Statescontributed to the launch of the new WTO Round,but it is expected to be tested over coming years.In the immediate future, the question of steelsafeguards and the Foreign Sales Corporationsdispute will strain recent goodwill.

Encouraging reform of theEuropean Union’s CommonAgricultural Policy

Enlargement of the European Union in 2004 willplace great pressure on the EU’s CommonAgricultural Policy (CAP) if it is retained in itscurrent form. The European Union’s ‘Agenda 2000’was intended to tackle this issue. However, to date,the European Union has embraced only verymodest reforms and many EU members seeAgenda 2000 as unfinished business.

Rural development and environmental concerns,coupled with a succession of recent high-profilefood safety concerns, including BSE (‘mad cowdisease’), have placed additional pressure on theEuropean Union to shift CAP expenditure awayfrom a focus on quantity towards production ofhigh-quality food and the preservation of the rural

environment. The 2002 mid-term review of theCAP will give Australia an opportunity to press theEuropean Union to make some changes in thisdirection but, with elections due in France andGermany, reforms are only likely to be modest inthe short term.

The Doha Round, with its ambitious agriculturalmandate, presents a real challenge for the EU andCAP reform. It focused on improved marketaccess, phasing out all forms of export subsidies,and substantial reductions in domestic support –three areas of most concern to Australia and theCairns Group of agricultural fair traders. Australiaand other Cairns Group members will work atboth the EU member state and the EuropeanCommission levels to encourage development ofoptions to reform the CAP consistent with theDoha Declaration’s intent.

US leadership is important

For over half a century the United States has playeda leading role in the multilateral trading system inseeking open markets and expanded internationaltrade. The Bush Administration has indicated that itremains committed to these principles. This wasreflected in the Administration’s commitment to thelaunch of a new round of WTO trade negotiationsat Doha in November 2001. But while theAdministration has been talking up free trade, theinternational trade debate has become more difficultand politicised within the United States. Debatesabout Trade Promotion Authority (TPA), the newfarm bill and the announcement of safeguardmeasures on steel imports have been influencedheavily by domestic politics. The WTO’s recentruling in the United States – Foreign Sales Corporationsdispute is also likely to be increasingly contentious.

T h e T r a d e P o l i c y E n v i r o n m e n t 9

MAINTAINING MOMENTUM FOR LIBERALISATION– THE NEED FOR LEADERSHIP

CH

AP

TE

R

1

10

From Australia’s perspective, the potentialprotectionist and trade distorting impact of thenew farm bill is a matter of serious concern, as isthe imposition of restrictions of Australian steelexports to the US. The Government is alsoconcerned that TPA legislation provides theAdministration with sufficient scope to exercisestrong leadership in the WTO negotiations,especially on agriculture reform.

TRADE PROMOTION AUTHORITY

The Government has welcomed the passage ofTrade Promotion Authority (TPA) by the USHouse of Representatives, and looks forward to itsearly passage by the US Senate. Should the Houseand Senate TPA legislation differ, which is likely, aconference between both chambers will then benecessary to determine the final version of the bill.The granting of TPA will enhance the BushAdministration’s capacity to engage in global andregional trade liberalisation initiatives. Houseconsideration of TPA saw the accommodation ofcongressional views on various trade issues,including steel and agriculture, and caveats suchas requirements for notification to, andconsultations with, the Congress. The AustralianGovernment will closely monitor how the TPAlegislation develops and how its caveats areimplemented by the US Administration.

FARM BILL

The Government has closely followed thedevelopment of the 2002 US Farm Bill, draftedagainst a backdrop of markedly increased USagricultural support. The Bill has the potential tolock in high US farm support until well into thisdecade, adversely affect Australian agricultureand limit the flexibility of the United States toshow strong leadership on agriculture reform inthe WTO.

The Australian Government and industryrepresentatives have made submissions andrepresentations to the United States protesting thecostly protectionist and trade distorting measuresbeing considered in the Bill. The measures have

the potential to destabilise and depress worldagricultural prices, reduce aggregate US andworld incomes and harm overseas producers.Despite the United States’ leading role in the pushfor free agricultural trade, US farm assistancerivals that of the European Union in six keycommodity groups: wheat, coarse grains, rice,oilseeds, sugar and milk. These commodities andcotton, which is also highly assisted, represent justunder 30 per cent of US agricultural production.And the biggest subsidies go to the richest, largestproducers, because payments are based on pastacreages and yields. The losers are the smaller,poorer farmers who could benefit if Congressspent less on subsidising production and more onother forms of farm assistance.

STEEL

This year is likely to be a challenging one for theAustralian steel industry as it faces an uncertainoutlook. In a global industry already experiencingconsiderable problems, the decision by the UnitedStates to impose wide-ranging import restrictionsfor three years with effect from 20 March 2002 islikely to lead to some major disruptions in worldsteel trade. The effects will be exacerbated if othermajor trading nations respond with their ownimport restrictions. The US decision is likely to facea challenge in the WTO, although this processcould take some time. Australia was successful insecuring arrangements that will preserve the bulkof our steel exports to the US, specifically through atariff free quota for slab steel and a product-specificexclusion for certain hot-rolled coil. While this wasa positive outcome, the high US tariffs will stillhave an impact on a number of our steel exportswhich will face a 30% tariff in the US market. TheGovernment is maintaining close consultation withthe steel industry to develop strategies for dealingwith the uncertainties in the global steel market.

FOREIGN SALES CORPORATIONS

Australia was an active third party in the UnitedStates – Foreign Sales Corporations (FSC) dispute inwhich the WTO again ruled against tax subsidiesprovided to United States companies for export.The scheme – which provides United Statescompanies some US$4 billion a year in tax breaks– impacts on the conditions of competition facingAustralian exporters in all markets. The EuropeanUnion has moved to secure WTO retaliation rightswhich, if applied, could result in a damagingtrade war and impede progress in the new roundof WTO negotiations. The Government isencouraging both parties to exercise restraint andfor the United States to comply with the WTOfindings as soon as possible.

M a i n t a i n i n g M o m e n t u m f o r L i b e r a l i s a t i o n – T h e N e e d f o r L e a d e r s h i p

11T h e T r a d e P o l i c y E n v i r o n m e n t

News of China’s accession to the WTO hits the streets in China

CHINA’S ACCESSION TO THE WTO

After 14 years of negotiations, China was accepted as a member of the WTO at the MinisterialMeeting in Doha on 11 November 2001. China formally joined the organisation on 11 December.Accession to the WTO will accelerate the opening of China’s economy and increase businessopportunities for Australia. It should boost the efficiency of the Chinese economy and increase thevolume of goods and services currently traded with China.

The development of competitive manufacturing as a result of economic reform and tradeliberalisation in China will make Australia even more important as a source of high-quality rawmaterials. Industries that are expected to benefit include wool, sugar, wheat, barley, meat,seafood, horticulture, dairy, cotton, rice, oilseeds, wine, processed foods, hides and skins,chemicals, pharmaceuticals, metals, information technology and automotive sectors. Australia’sgoods trade will also diversify as increasingly affluent segments of the Chinese market demandmore sophisticated manufactures and higher-quality foods.

Similarly, increasing demand for sophisticated services and progressive market opening willcontinue to boost opportunities for trade in services. In particular, Australia has been assured thatChina sees no substantive difficulties in granting additional licenses to Australian firms in theinsurance and banking sectors, and for legal and accountancy practices.

The Government is committed to ensuring Australian exporters are made aware of the newopportunities offered by China’s accession. In March 2002 Austrade, in conjunction with stategovernments, delivered a series of briefings around Australia on the regional economic andmarket implications of China and Taiwan joining the World Trade Organisation. The seminars wereaimed at Australian businesses currently engaged in or with an interest in trading with China,Hong Kong and Taiwan.

CH

AP

TE

R

1

12

NEED TO KNOW MORE?

More information on the WTO Round (including the Doha Declaration), trade and development andAustralia’s position on Free Trade Agreements is available at www.dfat.gov.au/trade/. Alternately,you can subscribe to regular bulletins on progress in the Doha Round negotiations by [email protected].

The WTO website (www.wto.org) contains information about the progress of negotiations, includingthrough its regular newsletter, Focus.

Extensive Austrade briefing sheets on the industry-specific opportunities resulting from China’sWTO Accession can be accessed by searching under China at www.austrade.gov.au .

Department of Foreign Affairs and Trade (1999) Global Trade Reform 2000: Maintaining the Momentum,DFAT, Canberra.

OECD (2001), Agricultural Policies in OECD Countries – Monitoring and Evaluation, Paris.

REFERENCES

THE NEW WTO ROUND –AUSTRALIA’S INTERESTS AND

STRATEGY

THE DOHA ROUND MUST

END DISCRIMINATION

AGAINST AGRICULTURE

2C

HA

PT

ER

2

• Australia is seeking real and substantial market access gains from the Doha Round. The ambitious rhetoric accompanying the launch has yet to face the test of negotiations.Much hard work remains, but rapid progress will be needed to meet the January 2005timeframe set for conclusion of the negotiations.

• The mandate for phase-out of agricultural export subsidies was an important victory forAustralia. Australia will also seek a comprehensive formula for agricultural tariff cutswhich addresses tariff peaks and tariff escalation.

• Australia will seek to address tariff peaks and escalation, and widespread use of specific,compound and nuisance tariffs in the industrials negotiations. The Government isconsidering whether to pursue across-the-board, sectoral or request-offer formulas, or a combination of these, for industrials’ tariff reductions.

• Australia has tabled negotiating proposals identifying barriers to services trade andrecommendations to overcome them in twelve priority sectors: business services (otherthan professional services), construction, distribution, education, environment, financial,maritime transport, telecommunications, and the professional services of legal,architecture, engineering and accountancy.

• The Government will work for a balanced framework of multilateral rules on competition.Australia has a world-class competition policy regime and would not expect any difficultiesin complying with multilateral rules.

• The Government seeks rules on investment which provide foreign investors with greatercertainty and predictability, while maintaining the integrity of Australia’s foreigninvestment screening regime. Pre-establishment investment commitments should bebased on a positive list approach.

• Australia welcomed negotiations to reduce the harmful impact of fisheries subsidies andthe strong commitment to environmentally sustainable development in Doha. However,negotiations on the relationship between WTO rules and multilateral environmentalagreements should not increase trade protection.

• Access to medicines was addressed in a positive way that takes into account both the needfor incentives to support multi-million dollar research programs and the need foraffordable access to medicines for the world’s poor.

• Australia will oppose extension of the geographic indication protection given to wine andspirits to all foods. This would prevent Australian producers from using terms such as‘basmati rice’ or ‘kalamata olives’ in domestic and export markets.

• The Government will continue to defend vigorously the interests of Australian producersthrough the WTO dispute settlement system. In 2001, Australia won major disputes withthe US (lamb) and South Korea (beef).

• The Government has increased resources dedicated to the Doha Round negotiations

AT A GLANCE

14

Launching a new round of trade negotiations atDoha, Qatar, in 2001 was a significant steptowards global trade liberalisation. Much hardwork remains to be done, but rapid progress isneeded to meet the ambitious January 2005timeframe set for the conclusion of thenegotiations. Australia hopes to move thenegotiations forward as quickly as possible tosecure early benefits from liberalisation.

The World Trade Organization (WTO) TradeNegotiations Committee met in Geneva in lateJanuary 2002 to agree the structure, rules andprocedures for the Doha Round negotiations. The WTO Director-General, in an ex-officio capacity,has been appointed chair. Dr Supachai Panichpakdiwill replace Mr Mike Moore from September 2002until 1 January 2005, when the negotiations arescheduled to conclude. Eight negotiating bodieshave been established – agriculture, services,industrial products, a wines and spirits register,WTO rules, dispute settlement, trade andenvironment, and a review of all special anddifferential treatment provisions for developingcountries. The Trade Negotiations Committee alsoagreed on a list of principles and practices coveringtransparency, process and the role of chairpersons.

Pursuing an active multi-faceted trade agendaparallel to the Doha Round of multilateral tradenegotiations is ambitious. To ensure its success,

the Government has increased resources for tradenegotiation. The Government has established anOffice of Trade Negotiations (OTN) within theDepartment of Foreign Affairs and Trade to bringtogether trade specialists to help Australianexporters open up markets and win tradedisputes. The new Office of Trade Negotiationswill have 60 per cent more staff than thecorresponding division at the end of the UruguayRound of multilateral negotiations in 1993. The Office’s leadership team will be supplementedby a Special Negotiator with responsibility for freetrade negotiations, a Special Negotiator forAgriculture and an additional senior appointmentto Australia’s WTO mission in Geneva tostrengthen the negotiating team in Geneva.

T h e N e w W T O R o u n d – A u s t r a l i a ’s I n t e re s t s a n d S t r a t e g y 15

Minister for Trade Mark Vaile with US Trade RepresentativeRobert Zoellick (centre) and David Spencer, AustralianAmbassador and Permanent Respresentative to the WTO(left), in Doha at the WTO Ministerial Meeting

WTO ADVISORY GROUP

In April 2001, the Government established the WTO Advisory Group to provide it with another avenueof expert advice on WTO-related issues. The establishment of the Advisory Group reflects theGovernment’s commitment to consult widely to ensure the views of the Australian community aretaken into account in the development of negotiating positions and proposals in the WTO. The groupcomprises experts drawn from industry, community non-government organisations, trade unionsand academia. It played an important role in helping define Australia’s position for the DohaMinisterial Conference and a number of members joined the official Australian delegation.

CH

AP

TE

R

2

AGRICULTURE

16

Australia is determined to establish a fairer andmore market-oriented agricultural trading system.Agriculture accounts for 26 per cent of Australia’stotal merchandise exports so a strong outcomefrom these negotiations is one of theGovernment’s highest priorities.

Agriculture negotiations in the WTO began inMarch 2000, as part of Uruguay Round follow-upknown as the Built-in Agenda. However, the DohaDeclaration’s mandate for agricultural reformrepresent a significant gear change. Importantly,despite EU opposition, members agreed toreduction of all forms of export subsidies inagricultural trade, with a view to phasing them out.

The difficult issues of entrenched agriculturalprotection and broad-based subsidies can only betackled through the WTO. In 2000, total supportto agriculture in OECD countries, including alltransfers from consumers and taxpayers toagricultural producers, was estimated at US$327 billion. Australia’s agricultural producershave done exceptionally well to be competitive insuch a highly distorted world market. It followsthat they are well placed to benefit from anyimprovements in the trading environment.

Australia, with Cairns Group members, hassubmitted four ambitious negotiating proposalsfor the WTO agriculture negotiations, coveringmarket access, export competition, domesticsupport and export restrictions and taxes.

The market access proposal calls for deep cuts intariffs and substantial increases in market accessopportunities. In the Uruguay Round ofnegotiations, developed countries agreed to reducetheir tariffs on agricultural products by 36 per centoverall, with a minimum reduction of 15 per centfor each tariff line. Australia is seeking even more

ambitious tariff reductions and increased marketaccess opportunities from the Doha Round. In particular, Australia will seek a comprehensiveformula for tariff cuts to address tariff peaks andtariff escalation across all agricultural sectors.

The Cairns Group’s proposal on export competitionfocuses on elimination of all forms of exportsubsidies. Export subsidies depress and destabiliseinternational market prices and are the most trade-distorting of agricultural policies. The phase-outand eventual elimination of export subsidiesthrough the Doha Round will relieve Australianexporters of the burden of export subsidy-drivencompetition for the first time in decades.

Although countries agreed to cap and reduce theirexpenditure on trade and production-distortingdomestic support in the Uruguay Round,expenditure levels have remained high and globalexpenditure has actually increased since 1998 inresponse to low commodity prices. The CairnsGroup’s domestic support proposal calls forsubstantial reductions in all forms of trade andproduction-distorting domestic support. It targets,for example, market price support schemes, but not infrastructure development or pest control programs.

Modalities for the agricultural negotiations,including the form of market accessimprovements, steps by which export subsidieswill be phased out, further disciplines fordomestic support, and special measures fordeveloping countries, are to be agreed by 31 March 2003. Following this, WTO Members must determine by the 2003 WTO MinisterialConference how best to apply these modalities to their domestic schedules and must then gainacceptance of their proposal by other WTOMembers by January 2005.

AUSTRALIA, THE CAIRNS GROUP AND DEVELOPINGCOUNTRIES – A NATURAL ALLIANCE ON AGRICULTURE

The Cairns Group is committed to the principle ofspecial and differential treatment for developingcountries, as an integral part of the WTO agriculturenegotiations. The framework for liberalisation mustsupport the economic development and technicalassistance requirements of developing and smallstate members.

The Cairns Group’s program of outreach to otherdeveloping countries – all but three of the CairnsGroup are developing countries – remains a priority.Australia has contributed to this outreach effortthrough visits by senior officials to key developingcountries, publications of major studies on policyissues of interest to developing countries andsponsoring and promoting seminars on these sameissues. Major developing countries, including Egypt,India, Pakistan, Nigeria and Kenya, are now showinginterest in the Cairns Group’s reform agenda and howit would advance their own interests.

A g r i c u l t u r e

17T h e N e w W T O R o u n d – A u s t r a l i a ’s I n t e re s t s a n d S t r a t e g y

Trade Minister Mark Vaile addressing the CairnsGroup Ministerial Meeting held in Punta del Este,Uruguay. The Cairns Group is an important elementof Australia’s trade strategy.

CH

AP

TE

R

2

COALITION-BUILDING IN THE WTO

As a medium-sized player, Australia needs to be clever in building coalitions to secure the bestoutcomes for Australia from the Doha Round. Australia’s priorities include:

• continuing to work closely with Cairns Group members to ensure that the Doha Round succeedsin delivering fundamental agricultural reform;

• building stronger coalitions with other countries on issues such as services, industrials,environment and geographical indications;

• cooperating closely with the United States and engaging strongly with the European Union;

• building stronger relationships with developing countries, whose interests in agricultural reform,for example are closely aligned to those of Australia.

18

The reduction of tariff and non-tariff barriersunder the multilateral trading system has createdsignificant market access opportunities forindustrial (or non-agricultural) products. However,significant barriers remain. Tariff reductions arenot evenly spread across products or sectors, andtariff peaks, tariff escalation and widespread use ofspecific and compound tariffs and nuisance tariffsall limit the trade liberalisation process.

Australia is pleased with the broad mandate onindustrials market access negotiations in the DohaDeclaration. It does not exclude any sensitiveproducts, nor does it restrict methods forachieving further reductions in tariff and non-tariff barriers. Industrials negotiators areconsidering whether tariff reductions are to takeplace according to an across-the-board formula,on a sectoral basis, on a request–offer basis, or acombination of these or other arrangements.

The Uruguay Round negotiations on industrialtariffs resulted in:

• an overall cut of 38 per cent in the tariffs ofdeveloped countries;

• a jump from 20 to 43 per cent in the value ofimported industrial products that receive dutyfree treatment in developed countries; and

• a decline from 7 to 5 per cent in the proportion ofimports subject to tariffs of 15 per cent or higher.

In addition, the percentage of bound tariff linesrose from 78 to 99 per cent for developedeconomies, from 22 to 72 per cent for developingeconomies and from 73 to 98 per cent for theformer communist economies in transition.

In the Doha Round, Australian negotiators will bepushing for improvements in market accessopportunities for Australia’s exports of industrialproducts greater than those negotiated in theUruguay Round.

Australia’s first task is identifying market accessbarriers for its industrial goods and determiningthe most effective means of reducing oreliminating these barriers. The Department ofForeign Affairs and Trade is gathering informationfrom a range of sources, including throughconsultation with industry stakeholders, relevantCommonwealth and State Government agenciesand overseas posts as part of this process.Industrials negotiations will need to move quickly,keeping pace with the agriculture and servicesnegotiations that began in 2000, to ensure that allnegotiations are completed by the 1 January 2005deadline for the Doha Round negotiations.

INDUSTRIALS

The services sector in Australia covers a large,diverse and rapidly growing area of economicactivity. Services now constitute around two-thirdsof Australia’s GDP; four in five Australians areemployed in service industries; and servicescurrently constitute around 20 per cent ofAustralia’s rapidly diversifying exports – or $31.2 billion 2001. Australia therefore has astrong national interest in the removal of barriersto greater market access overseas.

Mandated negotiations on services began on1 January 2000, before the launch of the DohaRound, as part of the Uruguay Round’s Built-inAgenda. They received renewed impetus in Dohawhen Ministers agreed on a timeframe for themarket access phase of the negotiations. Membersare expected to submit initial requests for marketaccess improvements by 30 June 2002 and initialoffers by 31 March 2003.

Australia has tabled negotiating proposalsreflecting its priority interests in twelve sectors:business services (other than professional services),construction, distribution, education,environmental services, financial services,maritime transport, telecommunications, and theprofessional service sub-sectors of legal,architecture, engineering and accountancy.Australia has also indicated our strong interests intourism and air transport services.

These negotiating proposals identify barriers totrade in services and make recommendations inbroad, non-country specific terms, on how toovercome them. The negotiating proposals are aprecursor to the request-offer stage of negotiations.Over 100 negotiating proposals are on the table.The majority of them are from developedcountries, although developing country membershave expressed interest in sectors such as tourism,distribution and energy services.

Australia is now preparing initial negotiatingrequests. This involves accumulation of detailedinformation on market barriers facing Australianservice exporters in different countries. The Department of Foreign Affairs and Trade isconsulting industry stakeholders, relevantCommonwealth and State Government agenciesand overseas posts as part of this process. TheDepartment maintains a commercial-in-confidencedatabase of market access barriers, which will alsobe drawn upon to prepare the requests.

The Department is also consulting communitygroups interested in services. The DohaMinisterial Declaration reaffirmed the right ofWTO members to regulate the supply of services,including introducing new regulations on thatsupply. This reinforced the clear expectation thatgovernments will continue to provide and fundservices across a wide range of social policy areasin pursuit of their national objectives.

19T h e N e w W T O R o u n d – A u s t r a l i a ’s I n t e re s t s a n d S t r a t e g y

CH

AP

TE

R

2

SERVICES

Competition policy

At the Doha Conference, Ministers agreed to a two-stage process aimed at identifying core principlesfor competition policy, with a future decision onnegotiations to be taken by explicit consensus at theFifth Ministerial Conference in 2003.

Australia’s priority is to work towards a balancedframework of multilateral rules on competition.Australia has already been involved in negotiationof APEC’s non-binding Principles to EnhanceCompetition and Regulatory Reform, and these willcontribute to the discussion in the WTO. Australiahas a world-class competition policy regime andwould not expect to face any difficulties incomplying with any multilateral rules.