s an ra l ro ad n e t wo rk m a n a g em en t syst em …

TRANSCRIPT

SANRAL ROAD NETWORK

MANAGEMENT SYSTEM

1

By Dumi Nkabinde

30 August 2019

PRESENTATION OUTLINE

• RSA Roads, Why care for the asset

• SANRAL Network Condition

• Road Asset Management System by SANRAL

• SANRAL Budget / Projects

• Future Transport

2

3

Authority Paved Gravel Total

SANRAL 22 214 0 22 214

Provinces - 9 46 548 226 273 272 821

Metros - 8 51 682 14 461 66 143

Municipalities 37 680 219 223 256 903

Total 158 124 459 957 618 081

Un-Proclaimed (Estimate) 131 919 131 919

Estimated Total 158 124 591 876 750 000

SA ROAD NETWORK - 2018

Un-Proclaimed Roads = Public roads not formally gazetted by any Authority

4

Freight flow on road and rail (10th State of Logistics Survey 2014)

Also important to note that of the person trips recorded in National Household Travel

Survey, 2013, by transport modes are as follow:

Minibus taxi’s (41.6%)

Private Vehicles (23.4%)

Walking (18.5%) – Along road corridors

busses (10.2%)

Trains (4.4%)

Other (1.9%)

2017 figures indicated similar trend.

Roads account for 87.9% of Freight and 93.7% of Person Trips

Mode Choice Factor Percentage

Travel time 32.6

Travel Cost 26.1

Flexibility 9.2

Other 32.1

SOUTH AFRICAN ROAD USE 5

6

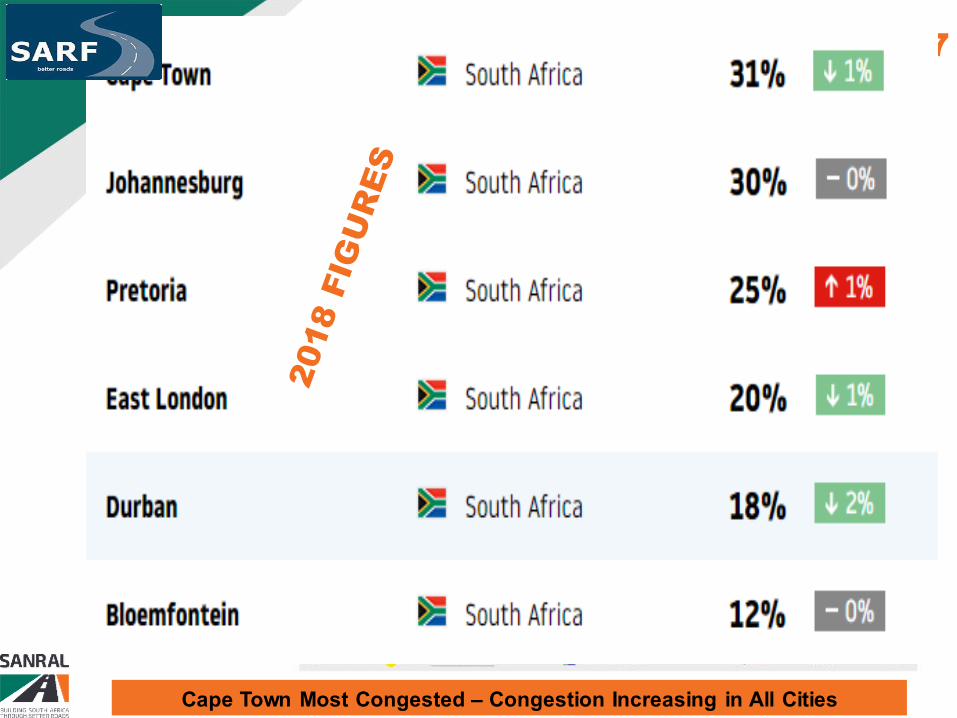

SA ROAD CONGESTION - 2017

Cape Town Most Congested – Congestion Increasing in All Cities

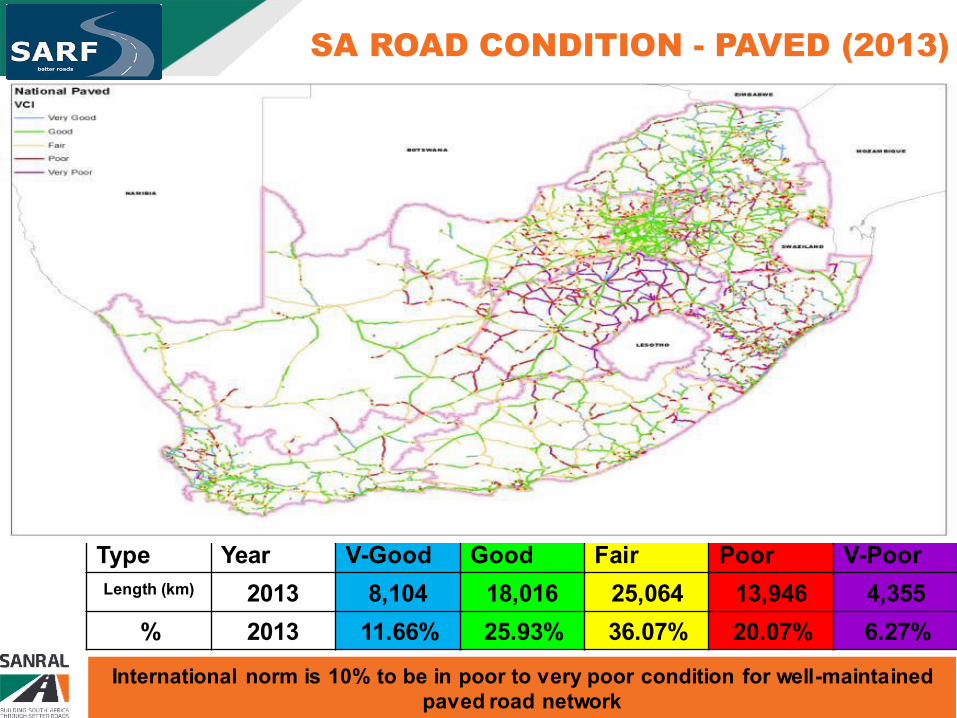

SA ROAD CONDITION - PAVED (2013)

Type Year V-Good Good Fair Poor V-Poor

Length (km) 2013 8,104 18,016 25,064 13,946 4,355

% 2013 11.66% 25.93% 36.07% 20.07% 6.27%

International norm is 10% to be in poor to very poor condition for well-maintained paved road network

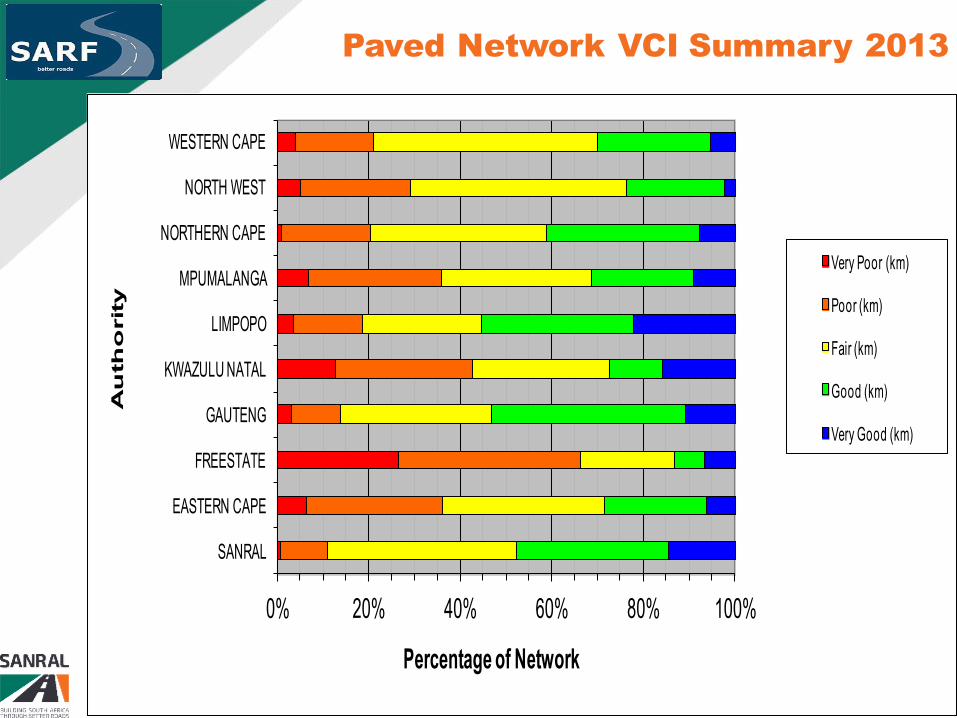

Paved Network VCI Summary 2013

0% 20% 40% 60% 80% 100%

SANRAL

EASTERN CAPE

FREESTATE

GAUTENG

KWAZULU NATAL

LIMPOPO

MPUMALANGA

NORTHERN CAPE

NORTH WEST

WESTERN CAPE

Percentage of Network

Au

th

orit

y

Very Poor (km)

Poor (km)

Fair (km)

Good (km)

Very Good (km)

8

0

20

40

60

80

100

2008 2013 2018 2023 2028

Year

Ro

ad

Co

nd

itio

n Good

Fair

Poor

Very Poor

Preventative Maintenance Actions

No Maintenance

Moisture Ingress

(Typically Designed for Traffic Expected over 20-30 Years)

Road Deterioration due to Traffic Loading & Environment

Very Good

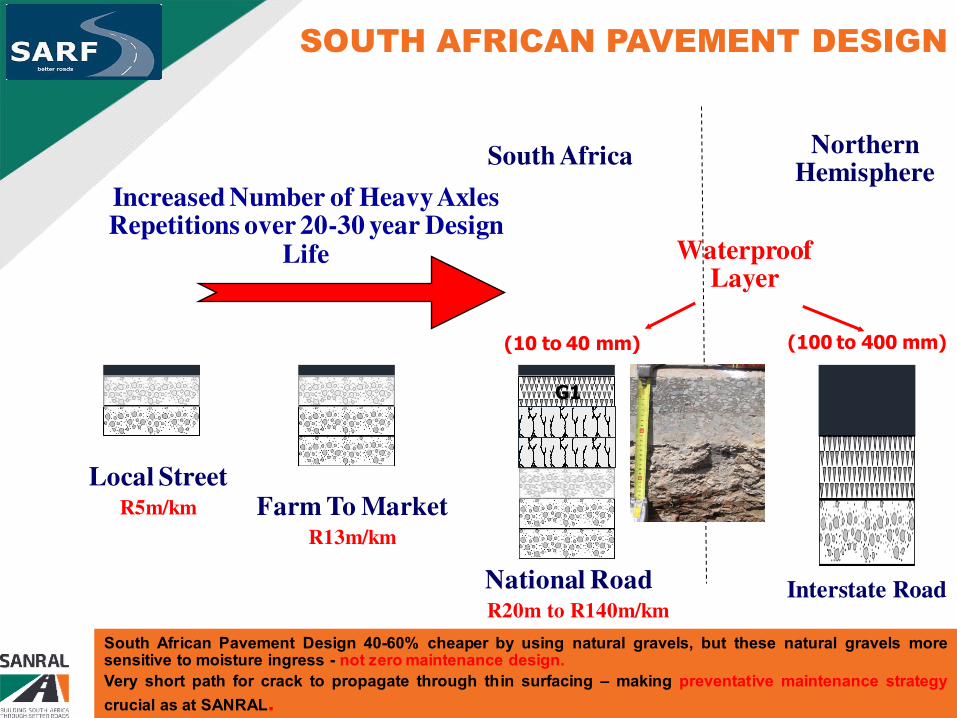

SOUTH AFRICAN PAVEMENT DESIGN

SA Pavement Design Requires Performance of Preventative Maintenance to achieve design life – Not Zero Maintenance Design

Northern Hemisphere

Waterproof Layer

Local Street R5m/km Farm To Market

R13m/km

National Road R20m to R140m/km

Increased Number of Heavy Axles Repetitions over 20-30 year Design

Life

South Africa

SOUTH AFRICAN PAVEMENT DESIGN

(10 to 40 mm) (100 to 400 mm)

G1

Interstate Road

10

South African Pavement Design 40-60% cheaper by using natural gravels, but these natural gravels more sensitive to moisture ingress - not zero maintenance design.

Very short path for crack to propagate through thin surfacing – making preventative maintenance strategy

crucial as at SANRAL.

New Road CONSTRUCTON Cost per km

Difference due to terrain (Flat, Rolling, Mountainous), Number of Interchanges, Number of Trucks, Climate, etc.

Our Pavements are seriously getting old 12

As seen 76% of paved network older than original 20 year design life, resulting in a high risk for accelerated deterioration under poor preventative maintenance regime as with most road authorities in South Africa.

Why is it Happening – Axle Loads

Decreasing

Layer

Strength

RSA designed for 8.2 ton axle load, Now its 9 ton SADC accord signed 2015 allows 10 ton. Overstressing of the weaker layers subgrades Economic Growth Just-in-time (small frequent loads) => no warehouse costs

Wearing course

Base layer

Subbase layer

Upper selected subgrade

Lower selected subgrade

In situ subgrade

Structural layers •High shear stress •“Large” strains

Subgrade •Low shear stress •Small strains

Surfacing

Half-axle tyre loads

13

Why is it Happening – Tyre Pressure

Modern truck tyres are 30% more fuel efficient, but

results in 30% + increase in damage to pavement

surface layers (especially when overloaded and

under or over inflated)

New Tyre Technology

Increased Tyre Pressure to

Reduce Contact Area

Which results in reduce Rolling

Resistance and 30% decrease in

Fuel Consumption

Decreasing

Layer

Strength

Wearing course

Base layer

Subbase layer

Upper selected subgrade

Lower selected subgrade

In situ subgrade

Structural layers •High shear stress •“Large” strains

Subgrade •Low shear stress •Small strains

Surfacing

Half-axle tyre loads

14

PORT SHEPSTONE

CHIPINGE

DURBAN

BEIRA

FRANCISTOWN

GABORONE

WINDHOEK

WALVISBAY

KEETMANSHOOP

BLOEMFONTEIN

ROUXVILLE

WEPENER

KLERKSDORP

ZEERUST JOHANNESBURG

MAPUTO

LADYSMITH

VOLKSRUST

EAST LONDON

PORT ELIZABETH MOSSEL BAY

OUDTSHOORN

CERES

CAPE TOWN

MESSINA

TZANEEN

SOMERSET WEST

PRETORIA

Wet (>1000 mm/yr)

Moderate (500 – 1000)

Dry (< 500 mm/yr)

Where is it Happening – Rainfall Zones

Wetter areas have higher moisture ingress risk if no preventative maintenance.

Wetter areas have more intense agriculture activity, more traffic. KZN traffic 16X that of NCP

15

0

20

40

60

80

100

2008 2013 2018 2023 2028

Year

Ro

ad

Co

nd

itio

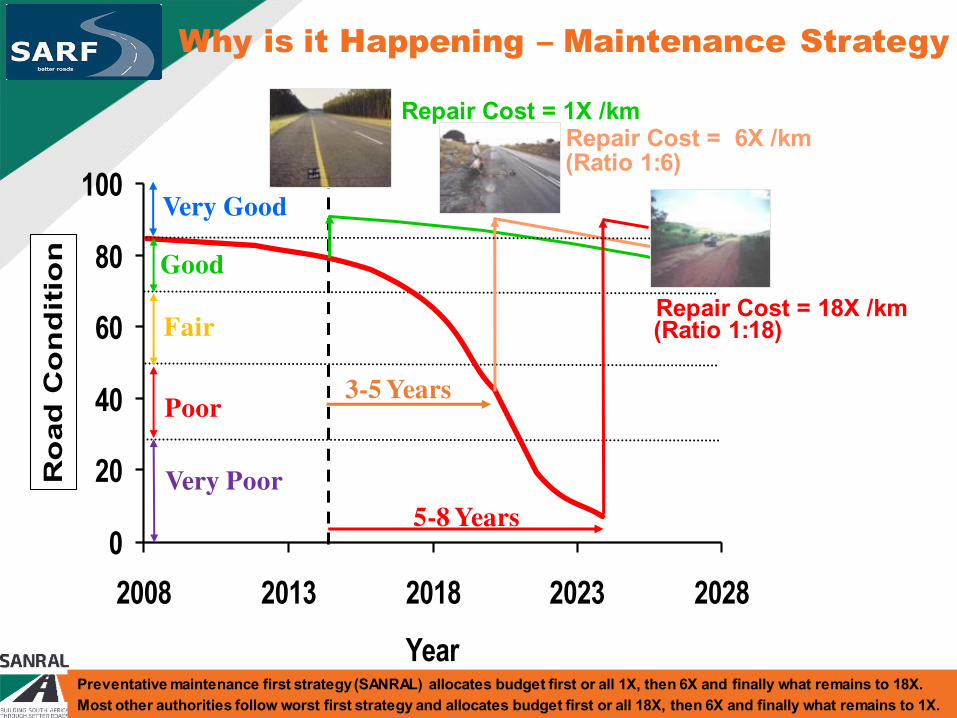

nWhy is it Happening – Maintenance Strategy

Repair Cost = 1X /km

Good

Fair

Poor

Very Poor

3-5 Years

Repair Cost = 6X /km

5-8 Years

Repair Cost = 18X /km

(Ratio 1:6)

(Ratio 1:18)

Very Good

16

Preventative maintenance first strategy (SANRAL) allocates budget first or all 1X, then 6X and finally what remains to 18X.

Most other authorities follow worst first strategy and allocates budget first or all 18X, then 6X and finally what remains to 1X.

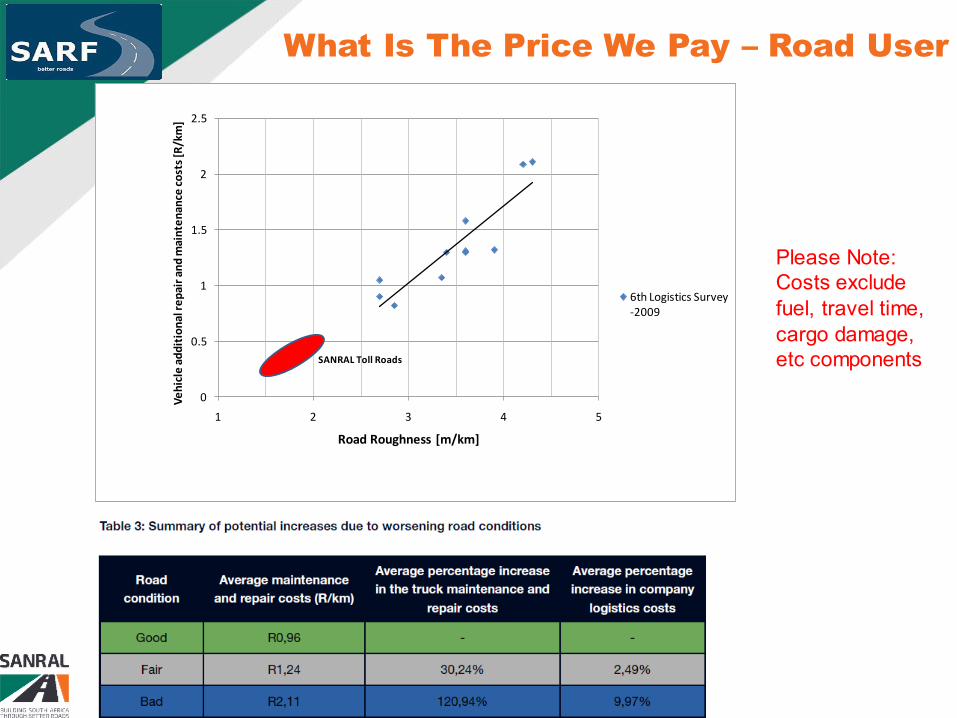

Road User Cost is up to 90% of Total Life Cycle Transportation Cost Road User Cost – Fuel, Oil, Tyres, Maintenance, Depreciation, Accidents, Time, Cargo Damage

Distance Travel in 1 hour: Very Good = 100km vs Very Poor = 20 to 25 km

17

What Is The Price We Pay – Road User

What Is The Price We Pay – Road User

Please Note: Costs exclude fuel, travel time, cargo damage, etc components

18

0

0.5

1

1.5

2

2.5

1 2 3 4 5

Ve

hic

le a

dd

itio

na

l re

pa

ir a

nd

ma

inte

na

nce

co

sts

[R/k

m]

Road Roughness [m/km]

6th Logistics Survey

-2009

SANRAL Toll Roads

19

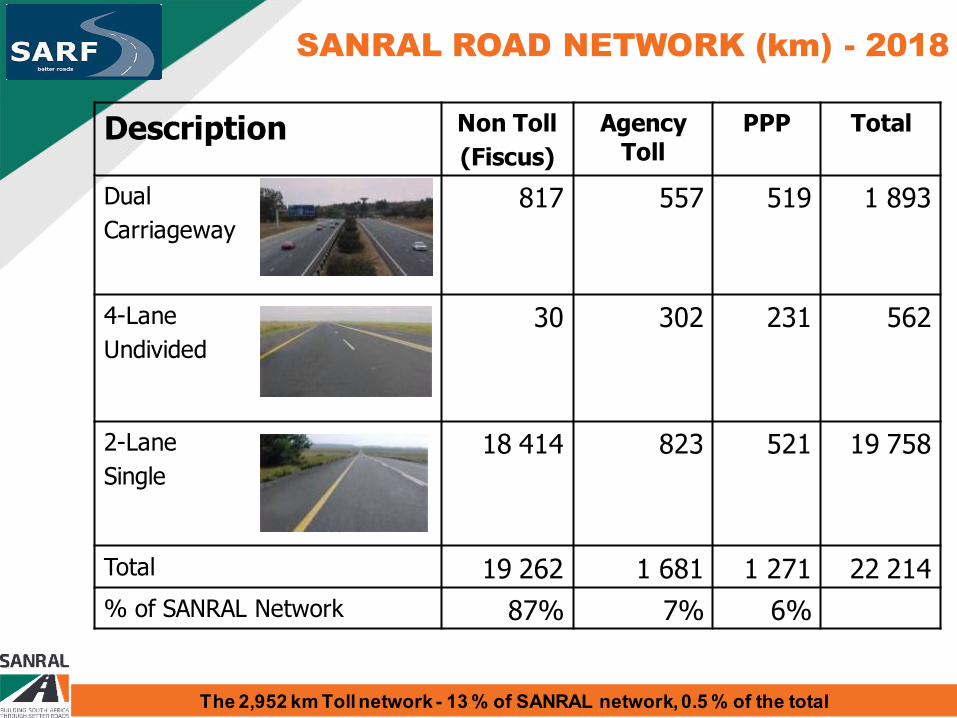

SANRAL NETWORK CONDITION

Description Non Toll

(Fiscus)

Agency Toll

PPP Total

Dual

Carriageway

817

557 519 1 893

4-Lane

Undivided

30 302 231 562

2-Lane

Single

18 414 823

521

19 758

Total 19 262 1 681 1 271 22 214

% of SANRAL Network 87% 7% 6%

SANRAL ROAD NETWORK (km) - 2018

The 2,952 km Toll network - 13 % of SANRAL network, 0.5 % of the total

20

SANRAL PAVEMENT CONDITION - 2018

Type Year V-Good Good Fair Poor V-Poor

Length (km) 2018 3,609 10,730 7,001 887 13

% 2018 16.3% 48.3% 31.5% 4.0% 0.1%

21

SANRAL PAVEMENT CONDITION TREND

Currently 900 km or 4.1% of SANRAL roads are in poor to very poor surface condition, which are well within the international norm of 10% for well-maintained network. The Average OCI of 74, is also above international norm of 70.

This is largely due to the preventative maintenance first strategy followed by SANRAL, the impact of all preventative maintenance on roads incorporated since 2012 is evident in 2016 & 2017 condition results.

The condition of remainder of strategic and primary roads under provincial administration is substantially worse (36.2% in poor to very poor), and needs to be addressed as matter of priority due to negative impact on South African economy.

22

SANRAL AVERAGE DAILY TRAFFIC

More than 70 % of SANRAL network has less than 5000 vpd – “Below Toll Threshold” – Thus reliant on National Treasury allocations. 30 % Toll viable of which 13 % is already tolled.

23

SANRAL NETWORK VEHICLE KILOMETRE TRAVEL

SANRAL network only 3.6% of length, but carries 34.1% of vehicle kilometres. Also carries 70% of the long distance road freight traffic (43% of total freight).

24

25

Road Asset

Management System

by SANRAL

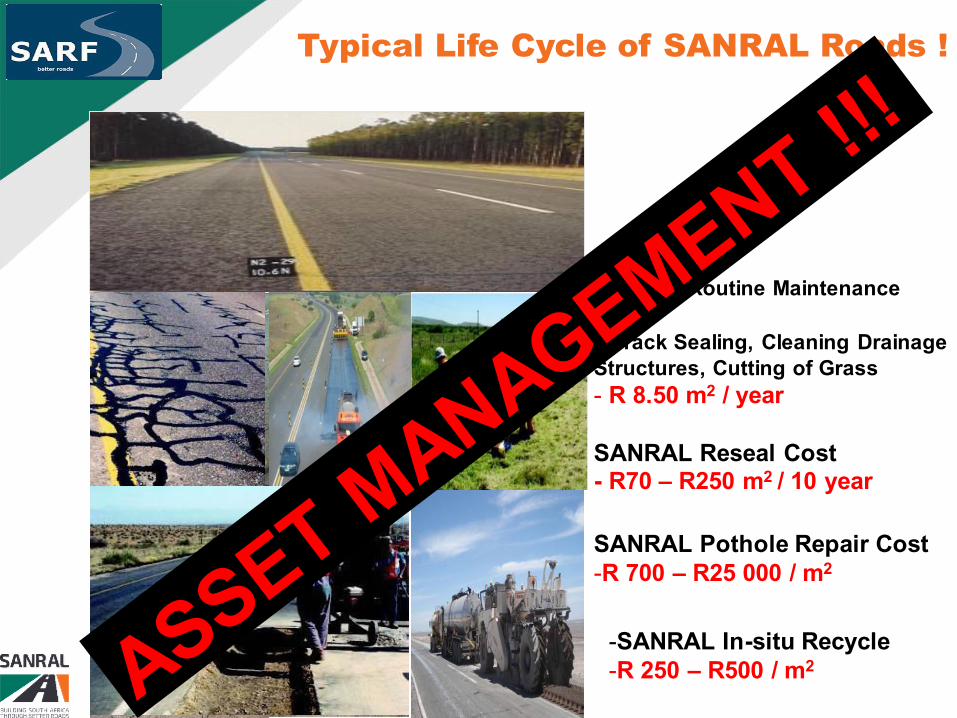

Typical Life Cycle of Most Roads !

New Road - Deterioration over time due to Traffic Loading &

Environment

NO Preventative Maintenance - Crack Sealing /Resealing - Cleaning Drainage Structures - Cutting of Grass

26

What Is The Solution – Automatic Pothole Patching?

Nooooooo…. Potholes are the symptom

not the cause…

27

Typical Life Cycle of SANRAL Roads !

SANRAL Routine Maintenance Cost

- Crack Sealing, Cleaning Drainage

Structures, Cutting of Grass

- R 8.50 m2 / year SANRAL Reseal Cost - R70 – R250 m2 / 10 year

SANRAL Pothole Repair Cost -R 700 – R25 000 / m2

-SANRAL In-situ Recycle -R 250 – R500 / m2

28

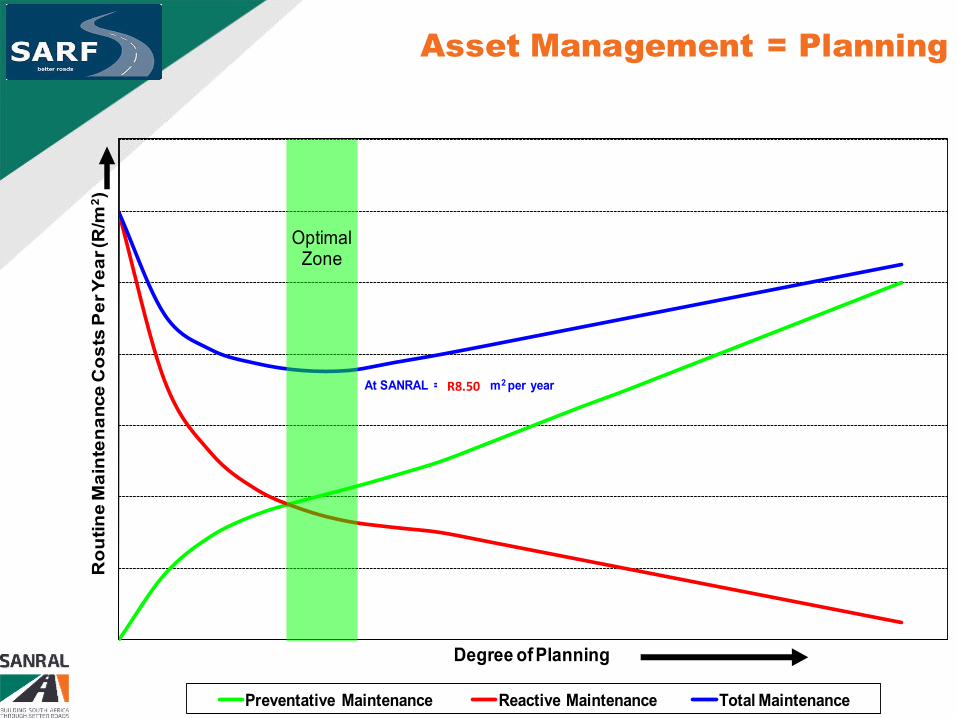

Asset Management = Planning

Ro

uti

ne

Ma

inte

na

nce

Co

sts

Pe

r Y

ea

r (R

/m2)

Degree of Planning

Preventative Maintenance Reactive Maintenance Total Maintenance

Optimal Zone

At SANRAL = R 6.50 / m2 per yearR8.50

29

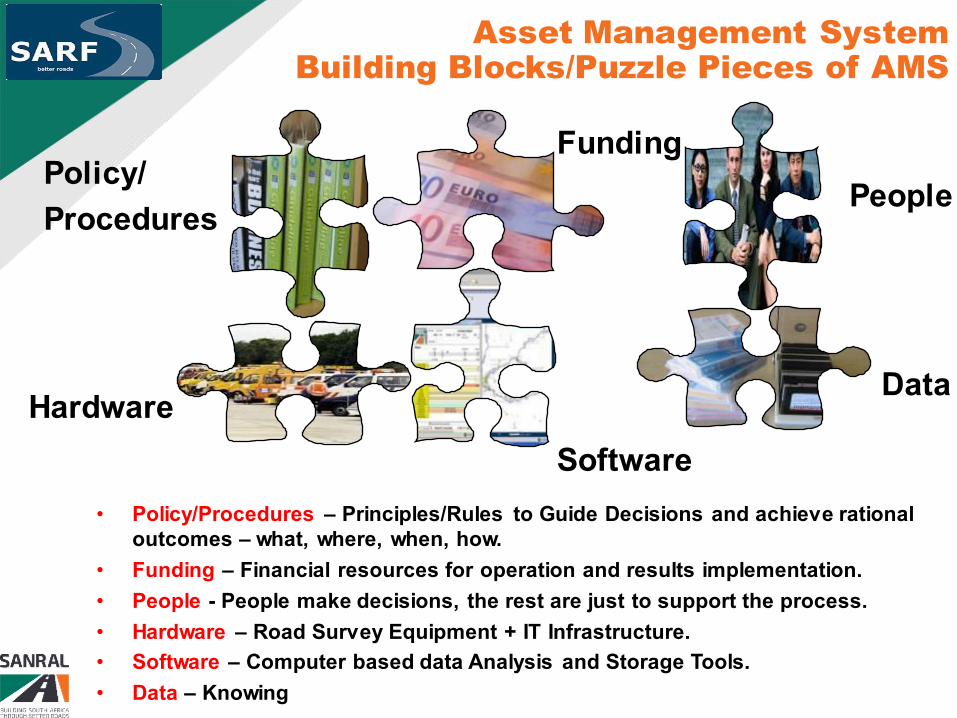

Asset Management System Building Blocks/Puzzle Pieces of AMS

• Policy/Procedures – Principles/Rules to Guide Decisions and achieve rational outcomes – what, where, when, how.

• Funding – Financial resources for operation and results implementation.

• People - People make decisions, the rest are just to support the process.

• Hardware – Road Survey Equipment + IT Infrastructure.

• Software – Computer based data Analysis and Storage Tools.

• Data – Knowing what you have, its condition and performance Trend.

Hardware

Software

Data

People

Funding Policy/

Procedures

30

• For asset management to be successful all the “pieces of the puzzle” need to be in place in a “balanced equilibrium”

• It does not help you have the most advance survey vehicle but no means

to effectively store and analyse the data, or

• Have the most sophisticate software, but the quality of your data is

suspect !

• Without Funding and People – Nothing will happen !!!

Hardware

Software

Data

People

Funding

Policy/

Procedures

Road Asset Management System - Success 31

AMS Hardware/Condition Data: SANRAL

Various condition parameters collected using SANRAL Road Survey

Vehicles: • Standardized procedures (COTO TMH 13)

• Roughness – how bumpy is the road – speed, wear, etc

• Rut Depth – water pond on surface - safety

• Macro Texture – assist vehicle tire to drain water – safety, noise

• Cracking – how much water will get in - deterioration

• Deflection – remaining structural life of pavement

• Alignment (DGPS) – Speed, Fuel Consumption, etc

• ROW Video – Road Signs, Section Measurements, etc

• Surveys at between 75 to 100 km/h

2D/3D Surface Images

32

AMS Condition Data - Bridges

• Manual Visual Assessments (DER) • Bridge condition is visually assessed through a standardized procedure (COTO

TMH 19) by certified inspectors to determine the Degree, Extent and Relevancy of each defect.

• Bridge repairs are prioritised according to severity and Relevancy of defects

• 3 to 5 year cycle

• 9874 Bridges & Major Culverts

0

33

AMS Condition Data : Traffic Data

• Traffic Event Logger (TEL) Standardized procedures (COTO TMH 3, 8, 14) Inductive Loop Based Technology (1000)

+ Piezo (200) + WIM (45)

Cluster Monitoring 1 to 3 year for Secondary Stations

34

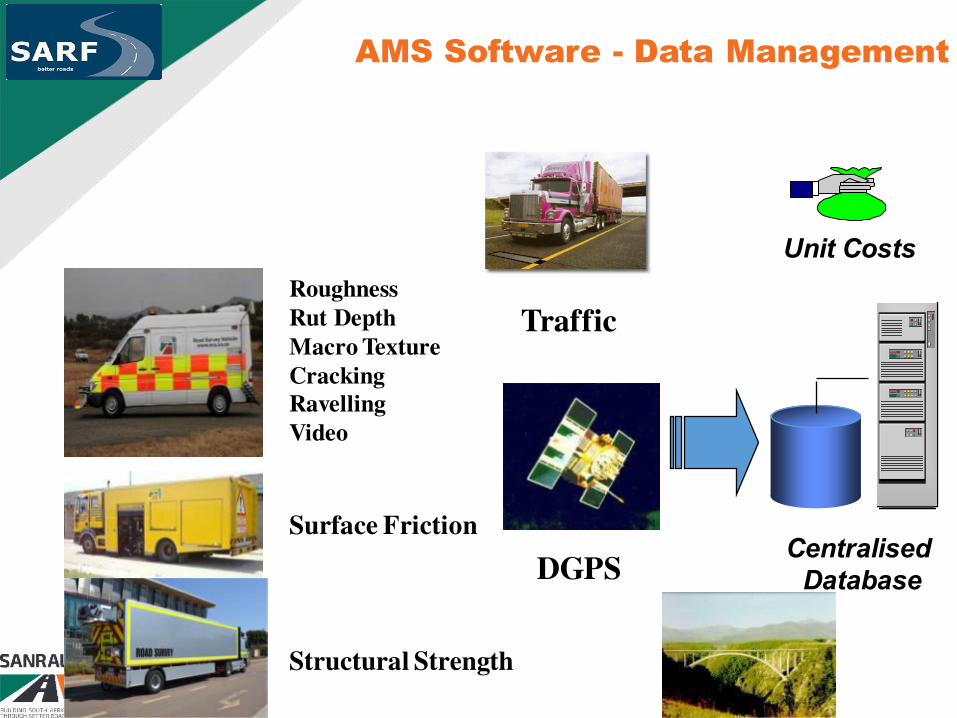

AMS Software - Data Management

Roughness

Rut Depth

Macro Texture

Cracking

Ravelling

Video

Surface Friction

Structural Strength

Centralised

Database

Traffic

Bridge

DGPS

Unit Costs

36

Economic Analysis

& Optimisation

Road Deterioration &

Maintenance Effects

Road User Effects

Centralised

Database

Dynamic

Segmentation

Uniform Sections

AMS Software - Life Cycle Modelling

Condition Surveys

37

HDM-4 Road Network Inputs

129 Variables

38

SANRAL AMS Budgeting Procedure

Instrumental Data

CBA

Priority

List

PMS RDME

RUE

Bridge Inspections

BMS BDME

RUE

CBA

Priority

List

Traffic

Projected Total Volume (Sites)

No. America Europe Asia-Pacific Government Total

Sm. Systems 12,000 6,600 2,100 3,000 23,700

Med. Systems 6,200 3100 560 950 10,810

Lg. Systems 2,650 1850 180 400 5,080

Total 20,850 11,550 2,840 4,350 39,590

Projected Total Revenue (billions of $)

No. America Europe Asia-Pacific Government Total

Sm. Systems $1.12 $0.62 $0.20 $0.28 $2.21

Med. Systems $1.59 $0.80 $0.14 $0.24 $2.78

Lg. Systems $1.80 $1.26 $0.12 $0.27 $3.46

Total $4.52 $2.67 $0.46 $0.80 $8.45

Super Project List

Budget Optimisation (forward)

Projected Total Volume (Sites)

No. America Europe Asia-Pacific Government Total

Sm. Systems 12,000 6,600 2,100 3,000 23,700

Med. Systems 6,200 3100 560 950 10,810

Lg. Systems 2,650 1850 180 400 5,080

Total 20,850 11,550 2,840 4,350 39,590

Projected Total Revenue (billions of $)

No. America Europe Asia-Pacific Government Total

Sm. Systems $1.12 $0.62 $0.20 $0.28 $2.21

Med. Systems $1.59 $0.80 $0.14 $0.24 $2.78

Lg. Systems $1.80 $1.26 $0.12 $0.27 $3.46

Total $4.52 $2.67 $0.46 $0.80 $8.45

Eastern Projected Total Volume (Sites)

No. America Europe Asia-Pacific Government Total

Sm. Systems 12,000 6,600 2,100 3,000 23,700

Med. Systems 6,200 3100 560 950 10,810

Lg. Systems 2,650 1850 180 400 5,080

Total 20,850 11,550 2,840 4,350 39,590

Projected Total Revenue (billions of $)

No. America Europe Asia-Pacific Government Total

Sm. Systems $1.12 $0.62 $0.20 $0.28 $2.21

Med. Systems $1.59 $0.80 $0.14 $0.24 $2.78

Lg. Systems $1.80 $1.26 $0.12 $0.27 $3.46

Total $4.52 $2.67 $0.46 $0.80 $8.45

Southern Projected Total Volume (Sites)

No. America Europe Asia-Pacific Government Total

Sm. Systems 12,000 6,600 2,100 3,000 23,700

Med. Systems 6,200 3100 560 950 10,810

Lg. Systems 2,650 1850 180 400 5,080

Total 20,850 11,550 2,840 4,350 39,590

Projected Total Revenue (billions of $)

No. America Europe Asia-Pacific Government Total

Sm. Systems $1.12 $0.62 $0.20 $0.28 $2.21

Med. Systems $1.59 $0.80 $0.14 $0.24 $2.78

Lg. Systems $1.80 $1.26 $0.12 $0.27 $3.46

Total $4.52 $2.67 $0.46 $0.80 $8.45

Northern Projected Total Volume (Sites)

No. America Europe Asia-Pacific Government Total

Sm. Systems 12,000 6,600 2,100 3,000 23,700

Med. Systems 6,200 3100 560 950 10,810

Lg. Systems 2,650 1850 180 400 5,080

Total 20,850 11,550 2,840 4,350 39,590

Projected Total Revenue (billions of $)

No. America Europe Asia-Pacific Government Total

Sm. Systems $1.12 $0.62 $0.20 $0.28 $2.21

Med. Systems $1.59 $0.80 $0.14 $0.24 $2.78

Lg. Systems $1.80 $1.26 $0.12 $0.27 $3.46

Total $4.52 $2.67 $0.46 $0.80 $8.45

Western

Programming Programming Programming Programming

Pavement Management System Bridge Management System

39

42

SANRAL BUDGET / PROJECTS

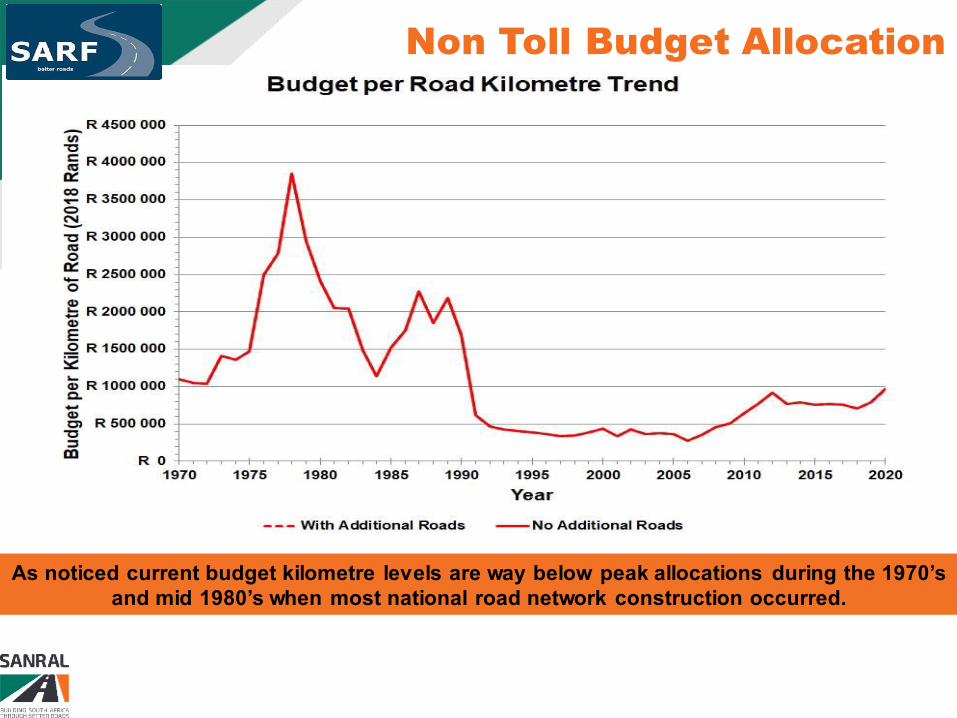

Non Toll Budget Allocation

As noticed current budget kilometre levels are way below peak allocations during the 1970’s and mid 1980’s when most national road network construction occurred.

43

Major Cost Drivers

Bitumen represents anything from 5 % to 60 % of the cost of a maintenance activity, as a result the length of road that can be maintained per year for every Rand is impacted by

these bitumen price fluctuations that is beyond control of SANRAL.

44

Major Cost Drivers

Considering the expenditure on the SANRAL network, it is obvious that the length of road that can be maintained per year for every Rand has been decreasing over time at rates much

higher than what the CPI indicates.

45

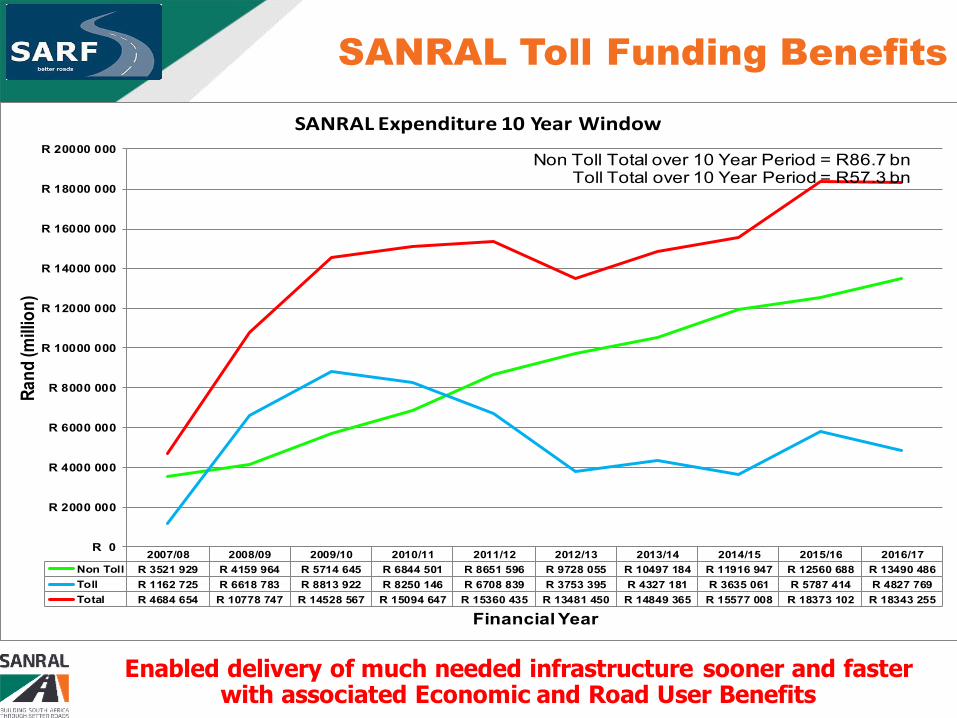

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17

Non Toll R 3521 929 R 4159 964 R 5714 645 R 6844 501 R 8651 596 R 9728 055 R 10497 184 R 11916 947 R 12560 688 R 13490 486

Toll R 1162 725 R 6618 783 R 8813 922 R 8250 146 R 6708 839 R 3753 395 R 4327 181 R 3635 061 R 5787 414 R 4827 769

Total R 4684 654 R 10778 747 R 14528 567 R 15094 647 R 15360 435 R 13481 450 R 14849 365 R 15577 008 R 18373 102 R 18343 255

R 0

R 2000 000

R 4000 000

R 6000 000

R 8000 000

R 10000 000

R 12000 000

R 14000 000

R 16000 000

R 18000 000

R 20000 000

Ra

nd

(mill

ion

)

Financial Year

SANRAL Expenditure 10 Year Window

Non Toll Total over 10 Year Period = R86.7 bnToll Total over 10 Year Period = R57.3 bn

SANRAL Toll Funding Benefits

Enabled delivery of much needed infrastructure sooner and faster with associated Economic and Road User Benefits

46

Umhlanga 1980

Economic Development Follows Road Investment

Umhlanga 1987

Economic Development Follows Road Investment

Umhlanga 2018

SANRAL Projects over MTEF 50

MTEF 363 Projects R64.7 billion

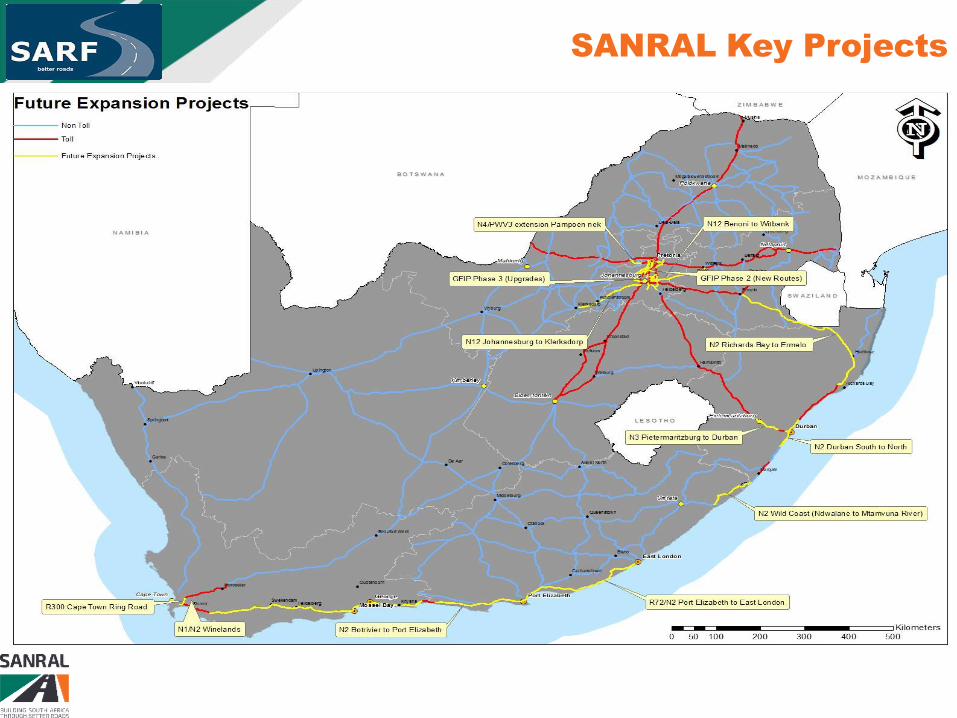

SANRAL Key Projects: Status

Project Initial Capital Costs

(R’000 2014R) Current Status

GFIP Phase 2 (New Routes) R 25 768 840 Nothing - Not declared national roads (Gauteng)

GFIP Phase 3 (Upgrades) R 17 655 160 Nothing - Not declared national roads (Gauteng)

R300 Cape Town Ring Road R 4 861 600 Nothing - Extensions not declared national roads

N1/N2 Winelands R 9 316 100 Toll Declaration set aside, cannot proceed until funding is

resolved

N2 Botrivier to Port Elizabeth R 11 272 540 Basic Planning, cannot proceed until funding is resolved / EIA

N2 Wild Coast (Ndwalane to Mtamvuna River)

(SIP 3) R 7 578 656

Construction funded by Fiscus, 1 Bridge Awarded, 1 in Tender

Adjudication, Haul Road Construction 98% Completed, Road

Detail design in Progress, Toll Declaration for Operations

Required by National Treasury

N2 Durban South (Prospecton) to North

(Umdloti) R 7 847 000 Detail design, cannot proceed until funding is resolved / EIA

N2 Richards Bay to Ermelo R 7 284 140 Detail Design, cannot proceed until funding is resolved / EIA

N3 Pietermaritzburg (Twickenham) to Durban

(EB Cloete) (SIP 2) R 15 777 205 Detail design, cannot proceed until funding is resolved / EIA

N3 De Beers (SIP 2) R 5 500 000 N3 De Beers replaced with New Van Reenen Development.

Complex Concession Amendments Required to implement

N4/PWV3 extension Pampoen nek R 1 716 900 Pampoen Nek Construction Started (Non Toll) due to ROD

Expiring

N12 Johannesburg to Klerksdorp R 2 731 700 Basic Planning, cannot proceed until funding is resolved / EIA

N12 Benoni to Witbank R 811 840 Basic Planning, cannot proceed until funding is resolved / EIA

R72/N2 Port Elizabeth to East London R 6 301 200 Detail Design, Phased Construction Started (Non Toll)

R573 Moloto Road (SIP 1) R 3 902 176 Detail Design, Phased Construction Started in Limpopo and

Mpumalanga (Non Toll), Gauteng Part not declared national road

Note: Most of these key capacity expansion projects (R128 bn) were previously planned to occur through toll financing, if no longer possible, then SANRAL will require additional funding from National Treasury to enable implementation.

51

SANRAL Key Projects 52

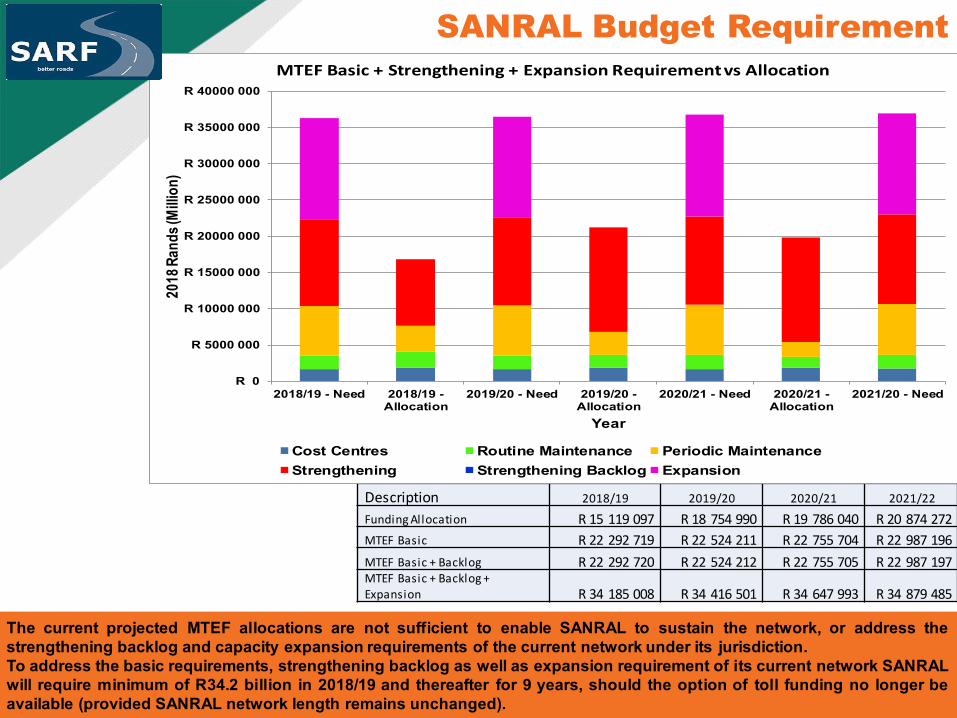

SANRAL Budget Requirement

Description 2018/19 2019/20 2020/21 2021/22

Funding Allocation R 15 119 097 R 18 754 990 R 19 786 040 R 20 874 272

MTEF Basic R 22 292 719 R 22 524 211 R 22 755 704 R 22 987 196

MTEF Basic + Backlog R 22 292 720 R 22 524 212 R 22 755 705 R 22 987 197

MTEF Basic + Backlog +

Expansion R 34 185 008 R 34 416 501 R 34 647 993 R 34 879 485

53

R 0

R 5000 000

R 10000 000

R 15000 000

R 20000 000

R 25000 000

R 30000 000

R 35000 000

R 40000 000

2018/19 - Need 2018/19 -Allocation

2019/20 - Need 2019/20 -Allocation

2020/21 - Need 2020/21 -Allocation

2021/20 - Need

2018

Ran

ds

(Mill

ion

)

Year

MTEF Basic + Strengthening + Expansion Requirement vs Allocation

Cost Centres Routine Maintenance Periodic Maintenance

Strengthening Strengthening Backlog Expansion

The current projected MTEF allocations are not sufficient to enable SANRAL to sustain the network, or address the strengthening backlog and capacity expansion requirements of the current network under its jurisdiction. To address the basic requirements, strengthening backlog as well as expansion requirement of its current network SANRAL will require minimum of R34.2 billion in 2018/19 and thereafter for 9 years, should the option of toll funding no longer be available (provided SANRAL network length remains unchanged).

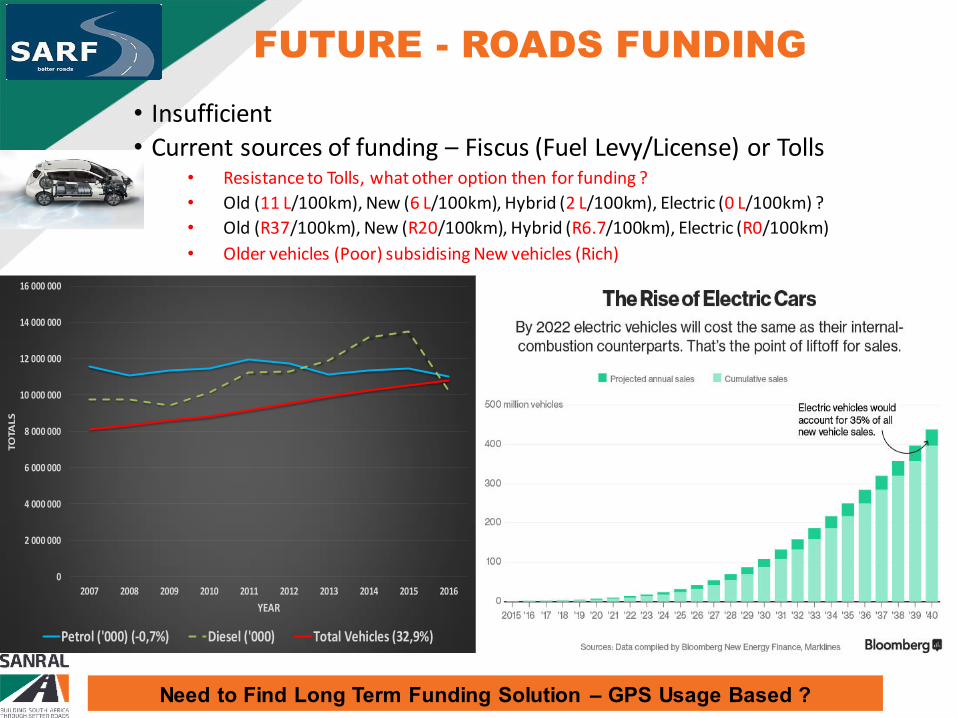

FUTURE - ROADS FUNDING

• Insufficient

• Current sources of funding – Fiscus (Fuel Levy/License) or Tolls • Resistance to Tolls, what other option then for funding ?

• Old (11 L/100km), New (6 L/100km), Hybrid (2 L/100km), Electric (0 L/100km) ?

• Old (R37/100km), New (R20/100km), Hybrid (R6.7/100km), Electric (R0/100km)

• Older vehicles (Poor) subsidising New vehicles (Rich)

54

0

2 000 000

4 000 000

6 000 000

8 000 000

10 000 000

12 000 000

14 000 000

16 000 000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

TO

TA

LS

YEAR

Petrol ('000) (-0,7%) Diesel ('000) Total Vehicles (32,9%)

Need to Find Long Term Funding Solution – GPS Usage Based ?

55

Future Transport that

SANRAL must consider

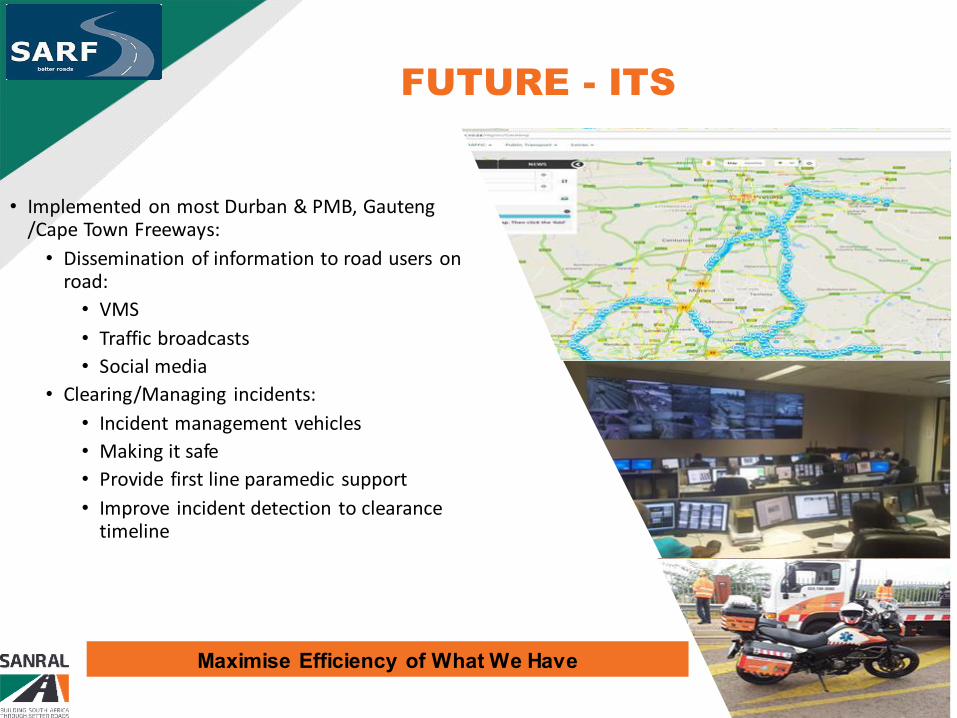

FUTURE - ITS

• Implemented on most Durban & PMB, Gauteng /Cape Town Freeways:

• Dissemination of information to road users on road:

• VMS

• Traffic broadcasts

• Social media

• Clearing/Managing incidents:

• Incident management vehicles

• Making it safe

• Provide first line paramedic support

• Improve incident detection to clearance timeline

56

Maximise Efficiency of What We Have

FUTURE WIM USE

• Overload Control • Old – Screeners at Static Weigh Bridges

• 50 to 100 km impact radius

• Construction/Operational Costs

• Human Factor

• Future – WIM-Enforcement • Direct Weight Enforcement integrate with Average

Speed over Distance (ASOD) – 250+ Installations • Been trialled over past 5 years

• Awaiting National Regulator Compulsory Standards Type Approval for ASOD and WIM-E

• End 2018

• Realtime Integration to SANRAL Central Operations Centre

• Realtime Tracking of Load Movements Country Wide (OD)

• Direct Enforcement (Speed/Load)

• Insurance Fraud

• Security Applications

• Abnormal Permits Enforcement

• Industry Self Regulation Verification

57

57 (Not to scale)

FUTURE – PERSONAL ROAD TRANSPORT

• Autonomous Vehicles / Mobility as a Service (Maas)

58

Autonomous Vehicles

2025 – Level 4 (option for override)

Benefits:

Accident Reduction

Closer following distances - increasing capacity

of existing roadways

Intersection Efficiency

No road signs / lane markings /safety barriers -

Dynamic lanes that can shift direction

Significant parking reduction (23 hours)

Mobility for All (No Driver Licence)

Distance to work - Increase

Mobility as a Service (Maas)

The provision of transport as a flexible, personalised on-

demand service that integrates all types of mobility

opportunities and presents them to the user in a

completely integrated manner to enable them to get

from A to B as easily as possible.

Already now (Uber, Google Waze) but real change

with autonomous vehicles !

Benefits:

Private Vehicle Ownership Reduction

Significant parking reduction

Tracking user demand in real time and optimising demand

dynamically with available capacity

Dynamic pricing to encourage users to avoid peak time

services and spread demand

FUTURE – PERSONAL ROAD TRANSPORT 59

60

FUTURE – SMART ROADS

Electric Charging Lanes ? Modular Pre Cast Units ?

Electric Trucks ?

FUTURE – NEW TRANSPORT MODES

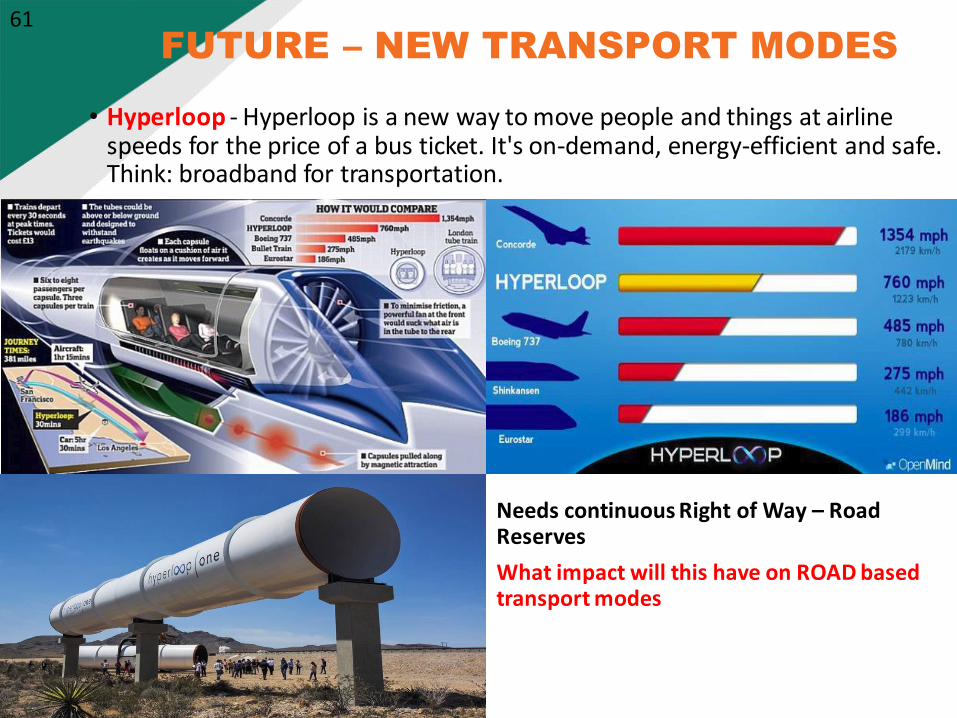

Needs continuous Right of Way – Road Reserves

What impact will this have on ROAD based transport modes

• Hyperloop - Hyperloop is a new way to move people and things at airline speeds for the price of a bus ticket. It's on-demand, energy-efficient and safe. Think: broadband for transportation.

61

THANK YOU www.sanral.co.za

62

62