robert e wiltbank, phd wade t brooks · angel investing, like formal vc, is a homerun game, where...

TRANSCRIPT

RobertEWiltbank,PhD

WadeTBrooks

Manythankstothesupportof:

2016Reportwith2017update

ForewordThisresearchhasbeenapartofanongoingbodyofworkoverthelast15years;manypeoplehavemadethispossible.Thefieldofangelinvestingismadeupofindividualsworkingtogethertocreateapositiveimpactinadditiontocreatingsuccessfulnewbusinesses.Wearegratefultothoseinvestorswhohavetakenthetimetosharetheirdatawithus.Thisdatadoesn’tcomeinacleanandconsistentformat,andforthisstudywearereallygratefulfortheworkthatKatieHamburghasdoneorganizingandstructuringthedataforanalysis.Angelinvestorsareprivateinvestors,andhavenorequirementtosharetheirinformation,whichmakesthisresearchverychallenging.WithoutthesupportoftheKauffmanFoundation,whoalsosupportedthe2007ReturnstoAngelInvestorsinGroupsstudy,andtheNASDAQOMXEducationFoundationthisworkwouldnothavebeenpossible.Lastly,we’regratefulfortheorganizationalsupportofouracademicinstitution,WillametteUniversity,aswellastheAngelResourceInstitute.

ExecutiveSummary Thisstudydetailstheoutcomesof245venturesthatcompletedtheircyclefrombirthtoeitherasuccessfulexitorashutdown.ThesecompanieswereidentifiedaspartoftheongoingmarketactivityresearchthatwereportintheHALOreport,andfromtheinvestmentdetailfrom20angelfunds,allintheUnitedStates.95%oftheangelinvestmentsweremadeinthesecompaniesbetween2001and2012,and91%ofthemcompletedbetween2010and2016.Atthehighestlevelofdescription,theoverallcashoncashmultipleisestimatedat2.5Xcapital.Thatis,thesumofallcashreturnedfromthesecompaniestotheirangelinvestorsdividedbythesumofallcashinvestedbythoseangelinvestorsequaled2.5.Themeanamountoftimethoseinvestorshadtheircashlockedintothosecompanieswas4.5years.Modelingtheexitsandtheirholdingperiods,weestimatethegrossinternalrateofreturntobe22%.(Grossmeansthatthereturndoesnotaccountforinvestmentcosts,likelegalfees.)Overall,thisreturnissomewhatlowerthan,butquiteconsistentwith,priorresearch.Lookingmorecloselyattheresults,theskewofthedataisclear,andisconsistentwithpriorresearchonbothangelinvestingandformalventurecapital.10%oftheexitsgenerated85%ofallcash.Angelinvesting,likeformalVC,isahomerungame,wheremostinvestmentsresultinlosses,buttheoccurrenceoflargehomerunsarethekeydriveroftherateofreturn.Inthisdataset,thefailurerate(investmentsthatwhencompletedreturnedlessthana1Xmultipletotheirinvestors)reached70%ofallinvestments.LookingatthereturndistributioninFigure1,weobservethatthepercentofexitsinthe1X–5Xcategoryislowerinthisstudythaninpriorresearch,withthedeclineresultingintheincreasedfailureratewereport.Wespeculatethisisaresultdrivenbythe2008-2010recession.Companieswhichmightotherwisehavereachedasmallpositiveexitwereunabletodosoduringtherecession,resultinginsteadinahigherfailureratethanthepriorstudies.Homerunexitsstillrepresentabout10%ofalloutcomeswhichkepttheoverallmultipleat2.5X.Thisisthepracticaleffectofthestatementthat“ventureinvestingisahomerungame.”Theotherpracticalimplicationofthatstatementisthatthedistributionofoutcomesishighlyskewed:themedianmultipleisbelow1X,whilethemeanisa2.5Xmultiple.InFigure2,onecanobserveaveryconsistentpatternofoutcomesacrossmultiplestudies(whichcoverdifferenttimeframes,economiccycles,geographies,andunitsofanalysis).ThestabilityoftheseresultsincreasesourconfidencethattheresultswereportherearerepresentativeofoutcomesexperiencebygroupangelinvestorsintheU.S.

In2017,weexecutedafollow-onanalysisofdatafortheongoingventuresfromthedatasetdescribedabove,thatwereeithershutdownorhadliquidityeventsduring2016.Inthisaddendum,therewere20additionaloutcomes.Theseoutcomeswerelessattractiveasasubset,butthesampleistoosmall(at20)togeneralizetoanystatementabout‘returnsin2016.’However,whenaggregatedwiththeresultsabove,weestimatethatthesetproduceda2.3Xmultiple,withanIRRofapproximately19.3%

MethodologyThisstudyisdesignedandexecutedatthecompanylevelofanalysis.Weusedatafromeachcompanyaboutitsfundraisingandultimateoutcometoanalyzethereturnstotheirangelinvestors.Asinpriorstudies,wehaveaworkingdefinitionofangelinvestorsaspeopleinvestingtheirownmoneydirectlyintonewventures.Wherethereisafundinvolved,thatfundoverwhelminglyconsistsofthemembers’owncash,andisdirectedbythemembers,ratherthanbygeneralpartnersinaformalventurecapitalfund.Themethodofthisstudyissignificantlydifferentthanthe2007and2009studies.Thepriorstudiescaptureddatadirectlyfromangelinvestorsabouteachoftheircompletedangelinvestments.Theprimarybenefitofthenewapproachistoenablethetrackingofangelreturnsinatimelyandrepeatablefashion.The‘cost’ofthischangeisthatweareunabletocapturemorestrategicallyinterestingvariables,suchastherelationshipofduediligenceandindustryexpertisetoinvestoroutcomes.Thesamplingframesandtimeframeofthedatawereportinthisstudyaredetailedbelow.TimeFrameTheinvestmentoutcomesof245separatecompaniesformthebasisfortheresultsofthisstudy.91%ofthosecompanieseithershutdown,wereacquired,orwentpublicbetweentheyearsof2010and2016.95%oftheangelinvestmentsmadeintothesecompaniestookplaceafter2001.Thecompaniesinitiallyenteredthesampleif,priorto2012,they:

1. ReceivedanangelinvestmentfromgroupangelinvestorsthatwasreportedtousviathereportingprocessfortheHALOReportÔoftheAngelResourceInstitute.or

2. Receivedanangelinvestmentfromanangelgroupsidecarfund,oranangelgroupthatdoesallofitsgroupinvestmentdirectlyfromafundofitsmembers.

Werefertothefirstcaseasthe“HaloReportset”astheywereidentifiedintheHALOreportingprocess.Werefertothesecondcaseasthe“AngelFundset”astheywereidentifiedbyangelfunds.

TheHALOReportSetThissetofcompaniesrepresentsalongitudinalpanelofcompanydatareportedfromU.S.angelinvestorgroupstotheHALOreportpriorto2012.356suchfirmswereidentifiedinthismanner.Ofthose356companies,109haveruntheircourseandbecomecompletedinvestmentstotheirangelinvestors.Theremaining247firmswillbetrackedmovingforwardintimeandwillgrowtheoveralldatasetweusetotrackreturns.Ofthose109companies,56%oftheiroutcomesoccurredbetween2013-2016,36%between2010-2012,and8%occurredpriorto2010.Individualcompanydatawasderivedfromtwosources:PitchbookandInventurist.Pitchbookrunsalargedatacollectionandanalysisservicesacrossthespectrumofprivate/alternativeclassesofinvestment,particularlyventureinvesting.Theiremployeessearchforinformationaboutcompanies,theirfundraising,theirprogress,andtheirstatusonarecurringbasisfrombothprimaryandsecondarysources.Ultimatesourcesincludedirectcompanyconversations,informationsubmittedbyinvestors,andinformationfoundonlineandinpressreleases.Forcompaniesthathadyettohavealiquidityevent,wetrackedtheirsocialmediaactivityviaInventuristtoevaluatetheirstatus.Thishelpedusdetermineiftheywerestilloperating.MostdatabasesofthePitchbookvarietyunderrepresentcompaniesthathaveceasedtooperatebecausetheyarehardertoidentify.ValidityandtheHALOreportsetTherearethreeprimaryadvantagesfromavalidityperspectiveusingthislongitudinalapproach.First,ithasnosurvivorbias,whichisasignificantimprovementoverpriorstudies.Companiesareidentifiedatthepointofinitialinvestment,ratherthanatthetimeoftheexecutionofthestudy.Asaresult,wesampleintofirmsthatwouldhavebeenshutdownpriortothis2016study,avoidingabiastowardonlythosefirmsthatsurvivedto2016.Inaddition,thereisnoselectionbiasontheoutcomesofthecompaniesbecauseallreportingisdoneatthepointofinitialinvestment,wheninvestorsarethemostoptimistic.Lastly,itisrepeatable,andenablesthedatatobeaggregatedovertimewithmoreconsistencythantheinvestorsurveyapproachusedinthepriorstudies.Conversely,untilthecompletesetof356companiesisfullycompletedthedatawillremainrightjustified.Wecanonlyreportdataoncompaniesthathavecompletedasofthetimeofthisstudy,andthereforeitispossiblethatongoingcompaniesaresystematicallydifferentthanthecompaniesthatarenowcompleted.Becauseittakeslongertorealizewinninginvestmentsthantorealizelosses,theongoingcompaniesmayhaveahigherportionofwinnersremainingin

thatsetthantheinvestmentsalreadycompleted.Lastly,thePitchbookdatacollectionprocess,inpractice,appearstohavebettervisibilityofdataaboutcompaniesthatalsohavereceivedformalventurecapitalinvestment.Inthisstudytwo-thirdsofcompaniesalsotookonformalVCinvestmentpriortotheircompletion,comparedtoone-thirdofcompaniesinWiltbank&Boeker2007.AngelFundSetComplementingtheHaloReportsetisagroupofcompaniesinvestedinbyAngelFundsintheUnitedStates.Thesefundsarestructuredeitherassidecarfunds,whereafundco-investswithmembersastheymakeindividualinvestmentdecisions,andgroupfunds,wherememberspooltheirmoneytogetherandinvestcollectively.Thedecisionrulesandpolicesthattriggerinvestmentsvary,butinallcasestheyaremakingdirectinvestmentoftheirownmoneyintoearlystagecompanies.Werequesteddatafrom31angelfunds,andreceiveddatafrom20.Thisresultedininformationon136completedinvestments.Theydirectlyreportedtheirportfoliotousandweonlyincludedinformationfromthecompaniesthathavecompleted(shutdownorliquidityevent).ThetimingofthedataissimilartotheHALOReportset,with65%oftheinvestmentscompletedfrom2013-2016,25%from2010-2012,and10%priorto2010.Thisdatahashighvaliditybecauseit’sreporteddirectlyfromtheGP’sofafund.Fundshaveaformalstructureandassuchsystematicallytracktheirinvestmentsmorethanindividualangelinvestors.Inmostcasesthedatathatwasreceivedisinthesamespreadsheetsusedfortheiroperationalportfoliotracking,andtheyonlyneededtoforwardthemtous.Becausethosespreadsheetsarecontinuallymaintainedandusedforinternaltrackingpurposes,futurestudiesusingongoingportfoliosdataishighlyreplicableandmoretimelythanthemethodspreviouslyused.TheAngelFundsetisslightlymoreexposedtosurvivorbiasandself-selection.Whileweknowwehaveallofthelongeststandingangelfundsinthisstudy,theremaybeangelfundsthatweareunawareofthatstartedandstoppedoperatingpriortothisstudy.Wewouldofcoursebeunabletoincludetheminourstudy.Inaddition,notallangelfundssharedtheirdataforthisresearch,with11fundsselectingoutofthestudy.Theprimaryreasongivenforselectingoutwasthattheywerenewerfundswithnocompletedinvestments,butotherfactorscouldalsobeinvolvedthatmaybiastheresults.Inbothcaseswebelievethepossibleeffectontheresultsofthestudyaresmall.Thecompaniesidentifiedinthetwoapproachesabove(theHALOReportandtheAngelFundsets)comprisethedatasetforthisTrackingAngelReturnsstudy.Foreachcompany,weanalyzedthetiminganddollaramountsinvestedbyangelinvestors,aswellastheamountand

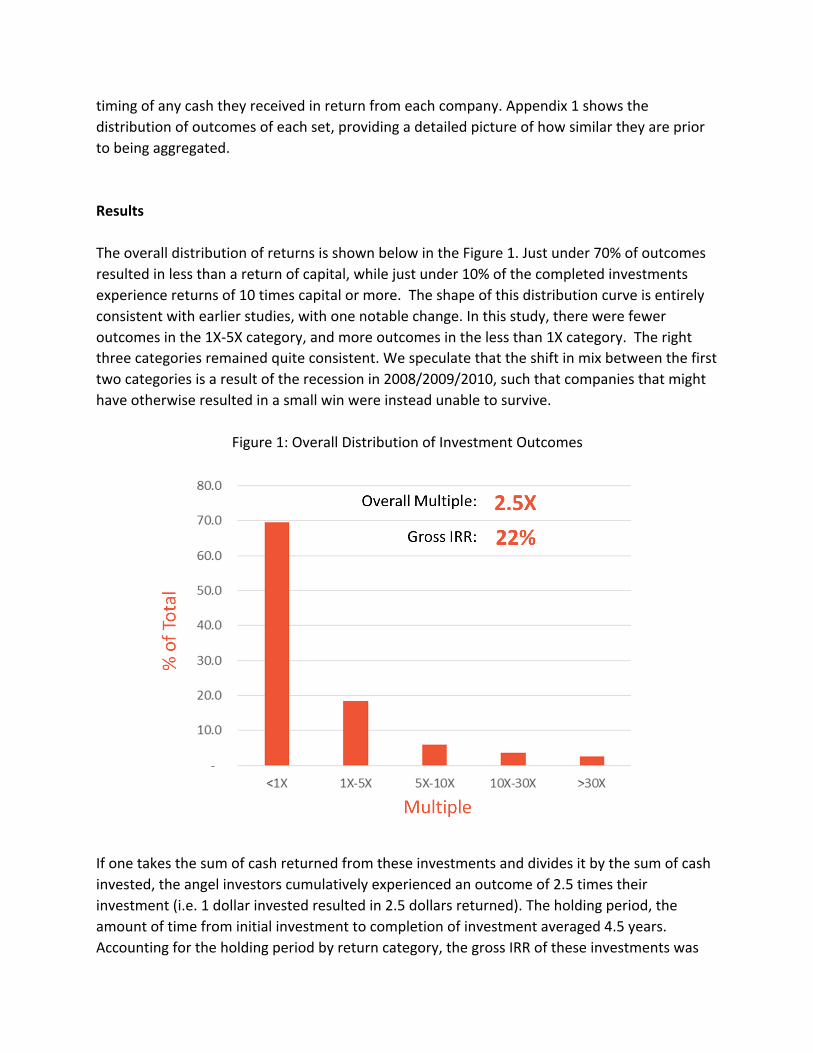

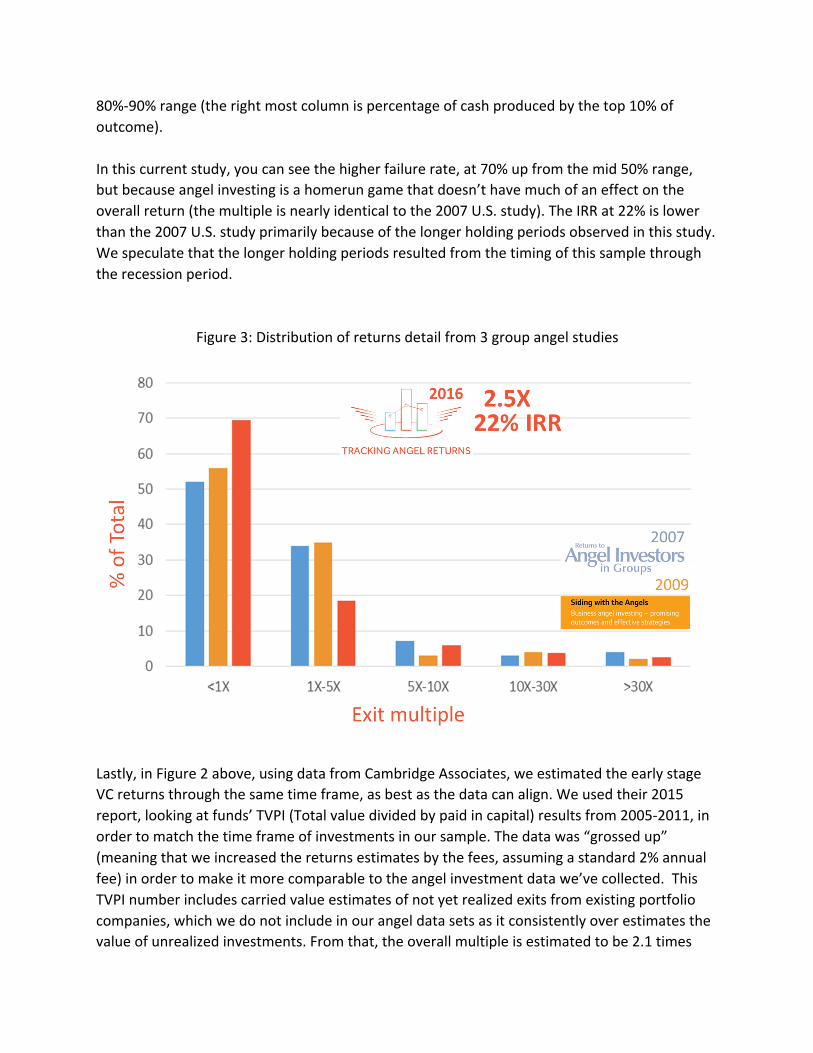

timingofanycashtheyreceivedinreturnfromeachcompany.Appendix1showsthedistributionofoutcomesofeachset,providingadetailedpictureofhowsimilartheyarepriortobeingaggregated.ResultsTheoveralldistributionofreturnsisshownbelowintheFigure1.Justunder70%ofoutcomesresultedinlessthanareturnofcapital,whilejustunder10%ofthecompletedinvestmentsexperiencereturnsof10timescapitalormore.Theshapeofthisdistributioncurveisentirelyconsistentwithearlierstudies,withonenotablechange.Inthisstudy,therewerefeweroutcomesinthe1X-5Xcategory,andmoreoutcomesinthelessthan1Xcategory.Therightthreecategoriesremainedquiteconsistent.Wespeculatethattheshiftinmixbetweenthefirsttwocategoriesisaresultoftherecessionin2008/2009/2010,suchthatcompaniesthatmighthaveotherwiseresultedinasmallwinwereinsteadunabletosurvive.

Figure1:OverallDistributionofInvestmentOutcomes

Ifonetakesthesumofcashreturnedfromtheseinvestmentsanddividesitbythesumofcashinvested,theangelinvestorscumulativelyexperiencedanoutcomeof2.5timestheirinvestment(i.e.1dollarinvestedresultedin2.5dollarsreturned).Theholdingperiod,theamountoftimefrominitialinvestmenttocompletionofinvestmentaveraged4.5years.Accountingfortheholdingperiodbyreturncategory,thegrossIRRoftheseinvestmentswas

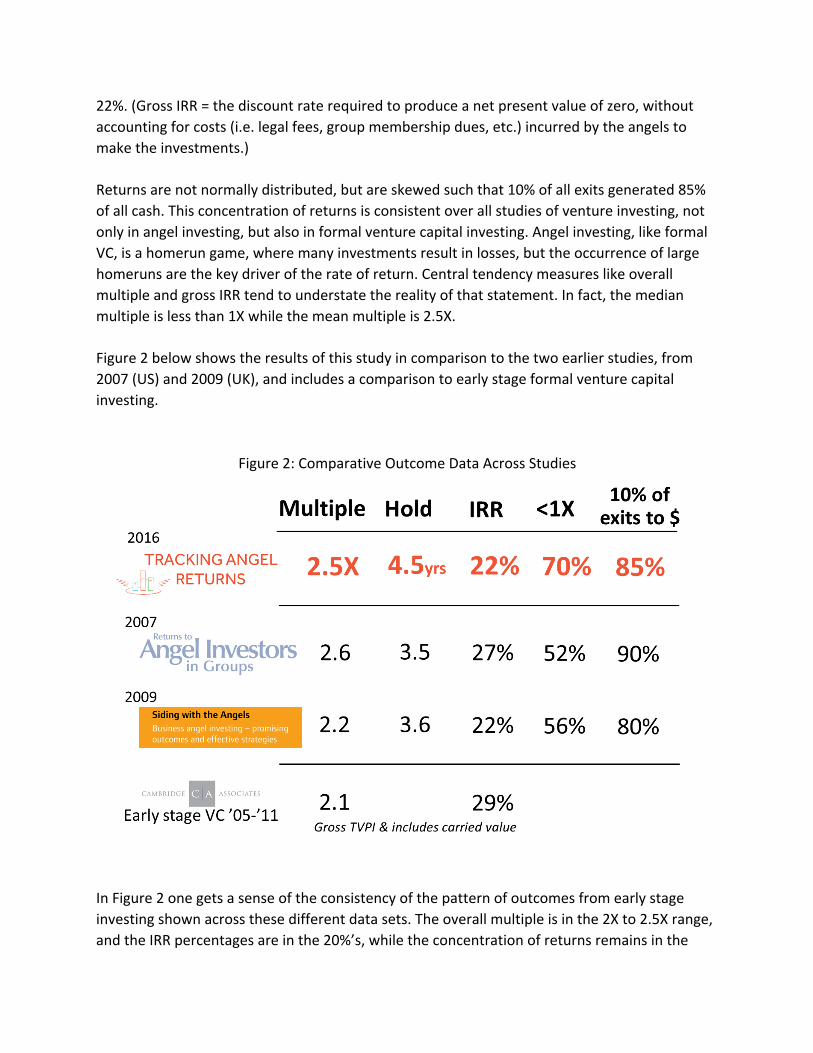

22%.(GrossIRR=thediscountraterequiredtoproduceanetpresentvalueofzero,withoutaccountingforcosts(i.e.legalfees,groupmembershipdues,etc.)incurredbytheangelstomaketheinvestments.)Returnsarenotnormallydistributed,butareskewedsuchthat10%ofallexitsgenerated85%ofallcash.Thisconcentrationofreturnsisconsistentoverallstudiesofventureinvesting,notonlyinangelinvesting,butalsoinformalventurecapitalinvesting.Angelinvesting,likeformalVC,isahomerungame,wheremanyinvestmentsresultinlosses,buttheoccurrenceoflargehomerunsarethekeydriveroftherateofreturn.CentraltendencymeasureslikeoverallmultipleandgrossIRRtendtounderstatetherealityofthatstatement.Infact,themedianmultipleislessthan1Xwhilethemeanmultipleis2.5X.Figure2belowshowstheresultsofthisstudyincomparisontothetwoearlierstudies,from2007(US)and2009(UK),andincludesacomparisontoearlystageformalventurecapitalinvesting.

Figure2:ComparativeOutcomeDataAcrossStudies

InFigure2onegetsasenseoftheconsistencyofthepatternofoutcomesfromearlystageinvestingshownacrossthesedifferentdatasets.Theoverallmultipleisinthe2Xto2.5Xrange,andtheIRRpercentagesareinthe20%’s,whiletheconcentrationofreturnsremainsinthe

80%-90%range(therightmostcolumnispercentageofcashproducedbythetop10%ofoutcome).Inthiscurrentstudy,youcanseethehigherfailurerate,at70%upfromthemid50%range,butbecauseangelinvestingisahomerungamethatdoesn’thavemuchofaneffectontheoverallreturn(themultipleisnearlyidenticaltothe2007U.S.study).TheIRRat22%islowerthanthe2007U.S.studyprimarilybecauseofthelongerholdingperiodsobservedinthisstudy.Wespeculatethatthelongerholdingperiodsresultedfromthetimingofthissamplethroughtherecessionperiod.

Figure3:Distributionofreturnsdetailfrom3groupangelstudies

Lastly,inFigure2above,usingdatafromCambridgeAssociates,weestimatedtheearlystageVCreturnsthroughthesametimeframe,asbestasthedatacanalign.Weusedtheir2015report,lookingatfunds’TVPI(Totalvaluedividedbypaidincapital)resultsfrom2005-2011,inordertomatchthetimeframeofinvestmentsinoursample.Thedatawas“grossedup”(meaningthatweincreasedthereturnsestimatesbythefees,assumingastandard2%annualfee)inordertomakeitmorecomparabletotheangelinvestmentdatawe’vecollected.ThisTVPInumberincludescarriedvalueestimatesofnotyetrealizedexitsfromexistingportfoliocompanies,whichwedonotincludeinourangeldatasetsasitconsistentlyoverestimatesthevalueofunrealizedinvestments.Fromthat,theoverallmultipleisestimatedtobe2.1times

capital,withanIRRof29%.TheIRRat29%inspiteofthelowercashoncashmultipleistheresultofsignificantlyshorterholdingperiodsforformalVC’s.Theangelinvestmentdatacomparesfavorablytotheformalventurecapitalestimates,thoughcertainlythemeasurementerrorishigherintheangelinvestingestimatesgiventhesmallersamplesize.However,theangelinvestmentdataincludesnocarriedvalueestimatesforongoingportfoliocompanieswhichisdefinitelybeneficialfromavalidityperspective.Theevidencesupportsthestatementthatgroupangelinvestorsexperienceanoverallreturnthatisatleastasgoodasthatofearlystageformalventurecapital.Conclusions&FutureResearchWeprimarilyobservetheconsistentpatterninFigure3ofoutcomesacrossmultiplestudies(whichcoverdifferenttimeframes,economiccycles,geographies,andunitsofanalysis).ThisincreasesourconfidencethattheseresultsarerepresentativeofoutcomestoU.S.groupangelinvesting,andpossiblyevenearlystageventureinvestingmorebroadly.Generaloutcomeexpectationstogroupangelinvestingare:

1. Highlyconcentratedreturns:10%produce80%-90%ofcashreturns2. Highlyrisky:inany1investmentthemostlikelyoutcomeisalossofcapital3. Illiquidinvestment:morethan4yearminimumholdtimesbeforeliquidityisachieved4. Overallreturnexpectationifonepersistsisveryattractive:2.2–2.6timescapital

Theprimarydifferencesinthisresearchstudywereanincreaseinthefailurerateandtheholdingperiod,whichresultedindeclineofthegrossIRR;allofwhichareconsistentwiththetimeframeofthestudyoccurringthroughaverydeeprecession.OurprimaryinterestwithfutureresearchwillbetotracktheoutcomesoftheremainingportfolioinboththeHALOReportÔandAngelFundsub-sets.

Addendum

TrackingAngelReturns20172016additionaloutcomes

Aperpetualchallengetoinvestigatingreturnstoangelinvestorsiscapturingtheongoingflowofinvestmentoutcomes.Aspartofthisresearch,wereportourextendedefforttotrackadditionaloutcomesfromthedatacollectiondescribedearlierinthispaper.Specifically,wetrackedallofthe247investmentsfromtheHaloReportSet(detailedinthemainbodyofthisreport)thatwerestillongoingin2016.Thestatusatthestartof2017ofthe247companieswasdeterminedusingdatafromPitchbook.Pitchbookemploysanalyststhatuseanarrayofapproaches,fromentirelyautomatedtodirectcontacting,inordertocaptureascompleteandcurrentdataasexistsontheseearlystagecompanies.Asdescribedearlier,thisdatasethasaninherentbiastowardventurecapitalbackednewventuresbecausethoseventurestendtobemore“visible”totheirdatacollectionefforts.Wechosethismethod,asopposedtodirectcontactingoftheventures,inadirectattempttocreateafeasible,ratherthanHerculean,processforsustainingongoingreturnsresearch.Allresearchchoicesinvolvetrade-offs.Inthiscase,whiletheapproachistheonlycurrentlyfeasiblewaytosustainongoinglongitudinaldata,itdoeslimitthedepthoftheresearchquestionsonemightaskaboutthesecompaniesandtheirinvestors.(Forexample,bestpracticesusedtomakeinvestmentdecisions,andhowtheyrelatetotheoutcomes.)Asinthelargereffortdescribedearlier,wearealsoabletoavoidsurvivorbiasusingtheHaloReportSet,andminimizeself-selectionbiasesusingthemixofdatacollectioneffortsemployedbyPitchbook.Onefinalpointtoemphasizeisthatthe‘samplesize’foranygivenyearbasedonthissetisverysmall,certainlytoosmalltogeneralizeinanysense.Therefore,attemptingtogeneralizetheoutcomesdescribedbelowtorepresentreturnslookedforangelbackedfirmsintheU.S.during2016wouldbemisguided.ItistheopinionoftheauthorsthattheaggregatedsetisthecurrentbestestimateofangelinvestmentoutcomesforangelinvestorsassociatedwithAngelinvestmentgroupsmakingearlystageinvestmentsinstartupcompanies.

AtthispointwecandescribetheoutcomesthathaveoccurredoverthepastyearfromamongtheHaloReportSet.Asof2017,20ofthe247ongoingventureshadreachedtheirconclusionandarenolongerongoing.These20hadraisedatotalof$67.5Mfromangelinvestors,ameanof$3.4Mandmedianof$1.7M.Thisskew(thelargedifferencebetweenthemeanandmedian)isnormalfordatainthisfield,withjustafewhavingraised$10M+whilemostventuresraisedapproximately$1M-$2Mfromangelinvestors.Thecompaniesthateithershutdownorhadaliquidityeventin2016hadraiseddoublethecapitalasthosethatcompletedpriorto2016.Infact,themediancapitalraisedintheaggregatedsampleis$600Kcomparedtothe$1.7Mmedianvalueofthissetof20.Theinvestmentholdingperiodofthis2016groupfromtheHaloReportSetwaslonger,obviously,thantheholdingperiodoftheinvestmentsthatfinishedpriorto2016.Themeanholdingperiodforthese20companieswas6.5years,comparedtothe4.5yearsofthepre-2016group,andthiswasthecaseforboththesuccessfulandunsuccessfulexits.ThisismerelyanartifactofthechoicetotrackonlytheongoinginvestmentsfromtheHaloReportSetdescribedearlierinthispaperforafixedtimewindow(2016).Theoverallsamplehasameanholdingperiodof4.8years;definitelylongerbymorethanayear,comparedtothe2007and2009returnstudies.Theoutcomesofthese20companiestrackedtocompletionthrough2016werenotasattractiveasthelargergroupreportedearlier.7wereacquired(35%),and13wentoutofbusiness(65%),whichisonparwiththeearliergroup.However,thelongerholdingperiod,theincreasedcapitalamountraisedbythegroup,andafewlowvalueacquisitionsleadtoamultipleofjust1.2X,withanIRRofapproximately4%.Withjust20investmentoutcomes,however,it’snotrealistictomakeanysortofgeneralizedstatementaboutreturnstoangelinvestorsoverallduring2016.Ratherthangeneralizefromthissmall2016set,wecanaddtheseoutcomestothegroupofcompletedinvestmentspriorto2016.ThisincreasestheNofthecompanyoutcomestoangelinvestorsfrom245to265companies.Theaggregatedoutcomesgenerateanoverallmultipleof2.3X(vs2.5X)andanoverallIRRof19.3%(vs.22%),pulleddownbecauseofthelessattractivesetofoutcomesthatoccurredin2016.

2016AdditionalOutcomes

20investmentscompleted7acquired,13wentoutofbusiness

Capitalraised:$67.5M

2Xhighercapitalintensity

Holdingperiod:6.5vs.4.5yearsSametimeforwinsasforlosses

Addedtooverallsampleresults:

2.3Xmultiple,19.3%IRR

Oneoftheinterestingdetailsofthis2016groupfromtheHaloReportSetisthattheunsuccessfuloutcomesraisednearlytwicetheamountofcapitalasthosethatexitedsuccessfully.Thispointstowardakeychallengeinventureinvesting,thetensionbetweendiminishingmarginalreturnstoinvestingadditionalcapitalandtimeandseveraldecision-makingbiases.Investorsneedtocarefullyconsidertheirriskofescalationofcommitment,thetendencytoavoidrealizinglossesbyinvestingintosituationstrendingdownward,andsocialpressuretobeloyaltoco-investorsandentrepreneursinwhomthey’veinvested.Inadditiontothe2007and2009studiesthatobservethenegativerelationshipbetweenreturnsandfollow-oninvestments,wepointtotwoacademicstudiesspecificallyrelatingthoseideastonewventureinvesting.

ThrowingGoodMoneyafterBad?,publishedinAdministrativeScienceQuarterly(200752:248-285).ByIGuler.

InvestmentandReturnsinSuccessfulEntrepreneurialSell-outs,publishedintheJournalofBusinessVenturingInsights(20153:16-23).ByN.Dew,S.Read,andR.Wiltbank.

Withallofthatsaidthesinglemostdominantfactor,andthiscan’tbereiteratedoftenenough,istheoccurrenceofunusuallylargehomerunliquidityeventsinwhateversetisbeingtracked.Overallreturnstoearlystageventureinvesting,byAngelsorVCfunds,aredrivenbyunusualandverylargeliquidityevents.Whenthoseoutcomesareinyourportfolio,orinadataset,thereturnstendtowardtheoverallnormsofthose“assetclasses.”Whenthosehomerunsaren’tinanyparticularsubset,thereturnswillbeunattractive,particularlyonariskadjustedbasis.Angelinvestorsthatsystematicallyinvestinventuresthataren’tplausiblyscalabletolargewinsareunlikelytoreachthereturnsdescribedthroughoutthisresearch.Overall,theempiricalevidenceaggregatedanddescribedinourresearchsuggeststhatAngelinvestors,associatedwithangelgroups,whoinvestinarelativelylargersetofnewventures,eachofwhichseemtoholdthepotentialtodramaticallygrowhaveexperiencedoutcomesatleastasattractiveasformalventurecapitalinvestors,andprobablysomewhatmoreattractive.In2018,ifthisresearchweretocontinue,227venturesfromtheHaloReportSetwouldbetrackedviaPitchbookonceagainlookingforshutdownsorliquidityevents.Oneofthechallengestothiseffortisthatofthe7acquisitionsreportedin2016,only2ofthempubliclyreportedthevalueoftheirliquidityevent.Weovercamethischallengebydirectlycontactedinvestorsinthesecompaniesthroughpersonalrelationshipsandconfidentiallycollectedinformationregardingthecashreturnedfromthoseevents.Thisisnotsustainableasamethod,obviously,andpointsagaintothechallengeoftrackinginvestmentreturndatainthisprivatemarket,withnoLP/GPreportingrequirements.

OneofthemotivatingfactorsforthecomparisontotheCambridgeAssociatesdatainfigure2ofthemainbodyofthisresearchreportistoconsiderthepracticalityofusingseedstageventurecapitalinvestmentreturnsasaproxyforthereturnstoangelinvesting.Ifthiswerepursued,onemustexplicitlyaccountforthechallengeofcarriedvalueshidingtruereturns,aswellasthegeographicconcentrationofventureinvesting.Butifthosecouldbeeffectivelyhandled,thepracticalimprovementinestimatingreturnstoangelinvestingwouldbesignificant.

Appendix1

Outcomedistributionpriortoaggregation

Black=HaloReportSetBlue=AngelFundSet

Numberoneachcolumn=Meanyearsinvestmentheld