risk management in retirement – what is the optimal home ... meetings/6d-what is the optimal...

TRANSCRIPT

1

Risk Management in Retirement

ndash What is the Optimal Home Equity Release Product

Katja Hanewald1 Thomas Post

2 and Michael Sherris

3

15 July 2012

Draft prepared for the ARIA 2012 Annual Meeting

Please do not cite or circulate without prior consent by the authors

Abstract This paper studies the optimal choice of home equity release products The decision

problem of a retiring couple is modeled that holds the major fraction of their wealth as home

equity and faces longevity long-term care house price and interest rate risk The couple can

choose to buy annuities long-term care insurance and to borrow against the home using

different equity release products These decisions involve the timing problem of when to

optimally release home equity The framework is used to compare the welfare effects of different

home equity release products and to study the role of government-provided long-term care

insurance

JEL Classification D14 D91 G11 R20

Keywords Retirement inter-temporal optimization and decision making home equity release

reverse mortgage annuities long-term care insurance

1 [Contact author] School of Risk and Actuarial and ARC Centre of Excellence in Population Ageing Research

(CEPAR) Australian School of Business University of New South Wales Sydney Australia Email

khanewaldunsweduau

2 Department of Finance School of Business and Economics Maastricht University and Netspar Email

TPostmaastrichtuniversitynl

3 School of Risk and Actuarial Studies and ARC Centre of Excellence in Population Ageing Research (CEPAR)

Australian School of Business University of New South Wales Email msherrisunsweduau

2

1 Introduction

This paper studies the optimal product choice of home equity release products from the

homeownerrsquos perspective in the presence of longevity long-term care house price and interest

rate risk A retiring couple chooses among different home equity release contracts and long-term

care and longevity insurance products Home equity release contracts differ substantially in the

way house price risks are shared and transferred between the homeowner and the lender Due to

this the optimal choice is strongly dependent on the homeownersrsquo individual characteristics

(including risk aversion and a bequest motive) and on the interaction with longevity and long-

term care risks which vary strongly between different institutional settings

Home equity is a very special asset class The home is an investment and a residence providing

non-pecuniary services For example people value the ability to ldquoage in placerdquo (Davidoff

2010c) and even with substantial mortgage balances outstanding people are happy about being

a homeowner (Whitehead and Yates 2010) Homeownership rates are high and are between 50

and 80 for most OECD countries (Andrews and Caldera Saacutenchez 2011) Home equity

represents the major share of the elderlyrsquos total assets For example for households aged 65+ in

the US the value of the primary residence comprises on average (median) 49 (52) of

householdsrsquo total assets with 82 of households aged 65+ actually owning a house (2009 wave

of the Survey of Consumer Finances) A home is not an ideal asset to meet the financial needs of

elderly households especially when having no other substantial sources of income It

concentrates a large amount of household savings in a single asset exposing the household to

substantial idiosyncratic risk (Case Cotter and Gabriel 2011) It is illiquid and in case of urgent

3

cash needs for example due to health shocks it cannot be sold in parts to pay for out-of-pocket

costs

Home equity release products convert home equity into liquid wealth but allow homeowners to

continue residing in their home Markets for equity release products are growing in the US

(Shan 2011) in the UK (KRS 2011) and elsewhere (Reifner et al 2009 Deloitte and

SEQUAL 2012) A range of different contract designs exist that share and transfer house price

risks in various ways between the homeowner and the lender The most common product in most

markets is a reverse mortgage with rolled-up interest (Oliver Wyman 2008 Davidoff 2010c)

This product allows homeowners to participate in house price appreciations while giving

protection to adverse house price developments through a no-negative equity guarantee (NNEG)

typically embedded in the product Home reversion schemes available for example in the UK

and in Australia allow homeowners to transfer a proportion of house price risks to the lender in

exchange for a lump-sum payment and a lease-for-life agreement (Oliver Wyman 2008)

Contract designs also differ in other dimensions such as having a fixed or variable interest rate

(Oliver Wyman 2008) Markets are very dynamic and new products are being constantly

developed (Australian Securities and Investment Commission 2005) Comparing and choosing

among various products with different risk and return features has become an increasingly

important but also increasingly difficult task for todayrsquos homeowners

Several papers examine home equity release products in optimal household portfolios Artle and

Varaiya (1978) show that the possibility of borrowing against home equity in retirement and

thereby relaxing liquidity constraints and smoothing consumption over the life cycle enhances

4

utility Fratantoni (1999) models the product choice between two reverse mortgage designsmdash

annuity payout plan and line-of-credit planmdashfor an elderly homeowners facing non-insurable

expenditure shocks He finds that line-of-credit plans are generally preferable since they are

more flexible and can provide large sums of money in case of the expenditure shock Davidoff

(2009 2010a 2010b) extends this research by allowing for health and longevity risks He

confirms that the availability of the reverse mortgages itself is utility-enhancing and finds

interaction effects with annuities and long-term care insurance For example home equity may

substitute long term care insurance Davidoff (2010c) introduces house price risk into a reverse

mortgage choice model He shows that amortization of interest (rolled-up interest) a feature

inherent in many currently sold contracts types is not always Pareto optimal Likewise Yogo

(2009) considers stochastic housing prices (and stochastic health depreciation) confirming that

reverse mortgages are utility enhancing The decision between fixed-rate and adjustable-rate

products so far has been studied for ldquonormalrdquo mortgages with adjustable-rate products being

found more attractive to homeowners (Campbell and Cocco 2003)

In summary a number of studies using different models find that reverse mortgages are utility-

enhancing The utility gains are shown to depend on the interaction with health and longevity

risks and on the availability of products to insure against these risks

This study provides the following contributions to the literature First we extend previous

models by considering longevity long-term care house price and interest rate risk and by

modeling the household as a couple as reverse mortgage decisions are often triggered by the

5

death of one spouse1 Second a general model is developed covering a range of different equity

release products and the timing problem of when to release home equity Third we analyze the

optimal choice in different institutional settings for long term care insurance (LTCI) and examine

the resulting interactions We distinguish between a setting in which most costs have to be paid

out-of-pocket with private insurance available and a setting in which most long-term care costs

are born by a government-sponsored system

The results of this study show that the couple enjoys large utility gains from having access to

either one of the two equity release products Higher utility gains are found for the reverse

mortgage The household chooses to unlock home equity early on in retirement These key

results emerge consistently across a range of cases with different parameter values The

availability of a government-provided LTCI does not change the use of equity release products

significantly but does change the demand for annuities

The paper is structured as follows Section 2 introduces the life cycle model Section 3 presents

the results Section 4 concludes and discusses policy recommendations

1 Shan (2011) reports that 45 in the US equity release program are single females 34 are couples and 11 are

single males (based on 2007 data) In Australia the majority of equity release customers are couples between 70-75

years old (Deloitte and SEQUAL 2012)

6

2 The Model

21 General Structure of the Model and Timing

The decision problem of a retiring couple is modeled that holds the major fraction of wealth in

their home The index isin is used to denote probabilities payouts or utility values of the

husband (m) and the wife (f) respectively The couple faces longevity risk long-term care risk

house price risk and interest rate risk Different insurance and home equity release products are

available to the couple

The decisions of the couple are modeled in an augmented life cycle model The model extends

previous work by Davidoff (2009 2010b 2010c) by considering a couple by allowing for

interest rate risk by including different types of equity release products and modeling the timing

decision of when to release home equity A two-period model (three points in time) is developed

that captures the couplersquos decisions at retirement and at an advanced age The modelrsquos input

parameters are calibrated such that each of the two periods reflects a multi-year horizon Figure 1

illustrates the decision and timing structure of the model

-- Figure 1 here --

At time t = 0 both spouses are in good health The initial endowment consists of the home and

liquid wealth The couple decides on consumption on saving over the first period of their

retirement on purchasing annuities long-term care insurance (LTCI) and on taking out an equity

release product Equity release products increase liquid wealth available for consumption

saving and for purchasing insurance products

7

At time t = 1 as in Davidoff (2009) each husband and wife independently will be in one of four

health states implying different health care expenses The random house value as well as the

interest rates and mortgage rates for the second period are realized Annuities and LTCI are not

available for purchase at t = 1 There are the following main cases at t = 1

1) Both spouses are dead Their remaining liquid wealth and housing wealth (net of mortgage

repayments) are left as a bequest

2) At least one partner is still alive The household receives payments from insurance contracts

and from equity release products bought at t = 0 Health state-dependent care expenses not

covered by insurance are paid out-of-pocket The couple decides on consumption and saving

over the second period

2a) Both spouses are in a nursing home or one partner is in a nursing home and the other one

is dead The house is sold and all outstanding loans are paid back Additional sale

proceeds are added to liquid wealth

2b) At least one partner is still living at home The couple decides whether to take out another

equity release product

At t = 2 both partners are dead with certainty Remaining liquid wealth and housing wealth (net

of mortgage repayments) are bequeathed

22 Interest Rates Mortgage Rates House Price Growth and Savings Growth

The risk-free interest rate r0 over the first period is known at t = 0 The interest rate r1 over the

second period is a random variable realized at t = 1 Mortgage rates are derived from interest

8

rates by adding a margin ∆RM to r0 and r1 (see Sections 26 and 28 for more details) Savings at

t = 0 S0 and at t = 1 S1 accrue the respective one-year interest rates r0 and r1 At t = 0 the

couple owns a mortgage-free house worth H0 At t = 1 the house value is H1 = H0 middot (1 + g1) and at

t = 2 it is H2 = H1 middot (1 + g2) where the growth rates g1 and g2 are iid random variables

uncorrelated with the interest rate

23 Health States and Care Costs

At t = 0 both husband and wife are in good health and no care expenses have to be paid At time

t = 1 husband and wife are each independently in one of four health states requiring different

levels of health care costs The four states are staying in good health and having no long-term

care costs (state h) with probability ph needing some care at home at cost LTCc (state c) with

probability pc needing to move to a nursing home at care costs LTCn (state n) with probability

pn and being death (state d) with probability pd (ph + pc + pn + pd = 1)

24 Long-Term Care Insurance and Annuity Products

Long-term care insurance (LTCI) covering the care costs in state c and the care costs

13 in state n is available at t = 0 Husband and wife buy separate LTCI contracts The couple

chooses the proportion of insurance coverage by choosing the amount of wealth

spent on LTCI for each partner i = m f LTCI is priced according to the actuarial principle of

equivalence plus a proportional loading LTCI The premium for partial coverage of an

individualrsquos care costs is given by

9

= (1 + ) ∙ ∙ ∙

∙ ()

= (2-1)

Furthermore single life annuities are available at t = 0 Annuities are priced based on the

actuarial principle of equivalence plus a proportional loading A The premium for an annuity

paying $ at t = 1 conditional on survival is given by

= (1 + ) ∙amp( )∙

() =

(2-2)

The annuity payment $ is determined by the amount of wealth the couple decides to invest

in individual irsquos annuity according to formula (2-2)

25 Government-Provided Long-Term Care Insurance

Scenarios are considered in which both public and private long-term care insurance (LTCI) are

available Social insurance arrangements for long-term care services exist in a number of OECD

countriesmdashGerman Japan Korea the Netherlands and Luxembourg (for an overview see

Productivity Commission 2012)

In this study government-provided LTCI is modeled as a compulsory coinsurance arrangement

with a stop loss limit The insurance scheme covers a percentage +- of all care costs up

to an out-of-pocket spending limit This arrangement abstracts from the details of the different

systems and focuses on the impact of possible structures of sharing care costs The arrangement

is in line with suggestions by the UK Commission on Funding of Care and Support which

suggests introducing a social insurance scheme with coinsurance and a cap and agrees with

10

suggestions by the Productivity Commission in Australia (Commission on Funding of Care and

Support 2011 Productivity Commission 2012) The retired household faces no costs for this

insurance but the cost is levied on the working generation The couple can decide to buy private

LTCI coverage for the proportion of care costs not covered by the public LTCI Because the

expected care costs are lower a lower premium for private LTCI results

26 Equity Release Products

261 Overview

The model developed above can accommodate a range of different home equity release products

In this study we focus on lump-sum reverse mortgages and home revision plans (also called sale-

and-lease-back plan or shared equity mortgage) Both products are offered to the household at

t = 0 and t = 1 With these types the analysis covers the main types of equity release schemes

currently available in Australia Canada UK and the US (Oliver Wyman 2008 Davidoff

2010c)2 We focus on reverse mortgages with variable interest rates and a NNEG because this is

the dominant product design in most markets

Often reverse mortgages are offered only to households that own a debt-free home We model

this situation by considering scenarios in which equity release products are only offered once (at

t = 0) The comparison allows us to determine optimal equity release choices from the

householdsrsquo perspective

2 Because the reverse mortgage is available at t = 0 and 1 and private annuities are available for purchase the line-

of-credit and annuity payout plan types of reverse mortgage additionally studied in Fratatoni (1999) are covered

(implicitly) in our analysis

11

262 Lump-sum reverse mortgage with variable interest rates and NNEG

A lump-sum reverse mortgage (RM) with variable interest rates and a no-negative-equity

guarantee is available at t = 0 and t = 1 LSRMτ denotes the loan value of a contract taken out at

time τ paid out as a lump sum at time τ

RMτ_balancet is the time t value of the outstanding loan balance of a reverse mortgage taken out

at time τ This balance is given by compounding LSRMτ at the respective mortgage rate (rolled-up

interest) Mortgage rates are calculated by adding a margin ∆RM to the random interest rate The

margin reflects the price of the no-negative-equity guarantee The value of this guarantee is

different for reverse mortgages taken out at t = 0 and at t = 1 resulting in different margins For a

reverse mortgage taken out at t = 0 the following mortgage rates apply r0 + ∆RM0 over the first

period and r1 + ∆RM0 over the second period (or r0 + ∆RM0 over both periods in case of fixed

interest rates) The margin r1 + ∆RM1 applies over the second period for a reverse mortgage taken

out at t = 1

The loan amounts LSRM 0 and LSRM 1 are decision variables Loan amounts are restricted by a

maximum loan-to-value ratio which is defined in terms of the house value Hτ Different (age-

specific) maximum loan-to-value ratios LTV0max and LTV1

max apply to reverse mortgages taken

out at t = 0 and t = 1 The maximum loan-to-value ratio at t = 1 LTV1max is defined as a

combined loan-to-value ratio

12

A reverse mortgage taken out at t = 0 is repaid at t = 1 if both husband and wife are in a nursing

home one partner is in a nursing home and the other one is dead or both partners are dead

These cases correspond to the cases 1) and 2a) described in Section 21 In the remaining cases

the couple can decide to take out another reverse mortgage at t = 1 and the outstanding loan

balances of both contracts are paid back at t = 2

In case of repayment the house is sold and the proceeds of the sale are used to pay back the total

outstanding reverse mortgage balance RM_balancet = RM0_balancet + RM1_balancet The total

repayment of both reverse mortgage loans is capped by the house value Ht at time t due to the

no-negative-equity guarantee To simplify the pricing repayment of LSRM1 has priority over

repayment of LSRM1 if at time t = 2 LSRM_balance2 lt H2

263 Home reversion plan

Home reversion plans (HR) are offered at t = 0 and t = 1 Under this arrangement the household

sells a share HRτ middot Hτ τ = 0 1 of the home equity to the product provider and receives a lump

sum LSHRτ in return The lump sum LSHRτ is less than the market value of the equity share

reflecting the value of a lease-for-life agreement and house price risk The household does not

have to pay a regular rent on the equity share sold to the bank but the equivalent present value of

rental payments is deducted from the lump-sum payout The equity share of the product provider

appreciates with the house price growth rates That is for example for a HR contracted at t = 0

the product provider owns HR0 middot H1 of the house value at t = 1 and HR0 middot H2 at t = 2

13

A home-reversion plan taken out at t = 0 ends at t = 1 if both husband and wife are in a nursing

home one partner is in a nursing home and the other one is dead or both partners are dead In

the remaining cases the couple can decide to take out another home reversion plan at t = 1 and

both contracts end at t = 2 When the contract ends the house is sold and the sale proceeds are

divided according to equity shares The couplersquos share is added to the liquid wealth that is

bequeathed

27 The Couplersquos Maximization Problem

The couplersquos lifetime utility function V is based on Brown and Poterba (2000) but with a

bequest motive as for example in Inkmann Lopes and Michaelides (2011)3

0(1) = sum 345 ∙ 678 9 + (1 minus 5) ∙ lt ∙ =(1)gtA (2-3)

δ denotes the subjective discount factor of the couple β the utility weight of the bequest motive

5 is an indicator variable taking the value one if at least one member of the couple is alive and

zero otherwise Ct is the consumption in real terms of the husband (m) and wife (f) The wealth

bequeathed by the couple Wt is comprised of liquid wealth and the house value net of payments

to repay equity release products

3 Davidoff (2009) considers an individual whose utility depends on both consumption and the housing stock He

introduces a utility penalty for moving out of the house when in good health and sets this parameter such that

moving is never optimal except when the individual has to go to a nursing home Our model does not incorporate

the decision to move based on stylized facts (Whitehead and Yates 2010) the decision to live in the own home is

assumed to be always optimal when in good health and housing is not needed as an argument in the utility function

(as in Campbell and Cocco 2003)

14

The one-period utility functions of the couple U is given by the equally weighted sum of the

husband and the wifersquos subutility functions Um and Uf (Brown and Poterba 2000)

678 9 = 58 ∙ 6878 9 + 59 ∙ 6979 8 (2-4)

6878 9 = ampBCDB

E)FGH

(I) (2-5)

6979 8 =ampB

EDBC)FGH

(I)

where 58 (59) is the indicator variable taking the value one if the husband (wife) is alive and 0

otherwise The parameter θ controls the degree of jointness (sharing of resources) in

consumption between the husband and the wife Both spouses have their subutility function

defined over consumption with an identical relative risk aversion parameter γ The bequest utility

function B exhibits the same relative risk aversion as U and is given by

=(1) = JBFGH

(I) (2-6)

The couplersquos objective is to maximize the expectation over (2-3) subject to a set of constraints

The couplersquos optimization problem is given by

maxBNOBPQCPQE PRSTUC PRSTUE EW0(1)X Y = 0 1 (2-7)

where the index j refers to cash flows from equity release schemes alternatively available

(j = RM HR) The optimization problem is subject to

(i) consumption and bequest constraints

15

A8 + A9 = 1A minus [A minus8 minus9 minus8 minus9 + [A

8 + 9 = [A ∙ (1 + ]A) minus [+$8 + $9 minus 71 minus+- minus8 ∙ 8 minus

71 minus+- minus9 ∙ 9 + [

Bequest constraint in case of the reverse mortgage

1 = [A ∙ (1 + ]A) + maxW minus _`_bcdcefg 0X

1 = [ ∙ (1 + ]) + maxW^ minus _`_bcdcefg 0X

Bequest constraint in case of the home reversion plan

1 = [A ∙ (1 + ]A) +71 minushiA ∙

1 = [ ∙ (1 + ]) + 71 minushiAminushi ∙ ^

(2-8)

(ii) borrowing constraints

0 le [A le 1A minus8 minus9 minus 8 minus 9 + [A (2-9)

0 le [ le [A ∙ (1 + ]A)+$8 + $9 minus 71 minus+- minus8 ∙ (8 + 138)

minus 71 minus+- minus9 ∙ (9+139) + [

(2-10)

(iii) no-short sale constraints for equity release and insurance products

0 le [A [ 8 9 8 9 (2-11)

and (iv) further product constraints

bull Maximum loan-to-value ratios for the reverse mortgage

[ikA le 0ikA8lm^A (2-12)

16

_`_bcdcefg + [ik le 0ik8lm

bull Maximum home reversion rate

hiAminushi le 1 (2-13)

bull LTCI benefits capped by actual care expenses

le 1 = (2-14)

28 Numerical Calibration of Baseline Parameters

This section describes the numerical calibration of the modelrsquos baseline parameters The

parameters are chosen to reflect the US market and to allow comparison with previous studies

Alternative parameter values are introduced in Section 3 Table 1 summarizes the numerical

calibration To distinguish product design effect from pricing effect especially in the different

equity release products all products are priced such that the product provider makes a zero

expected profit The pricing of the insurance and equity release products reflects the risks

inherent in these products

-- Table 1 here --

281 The Couplersquos Preferences and Endowment

The standard parameters for the couplersquos preferences (relative risk aversion subjective discount

factor strength of the bequest motive) are set within the range typically used in life cycle models

17

in the literature Relative risk aversion γ is set to 2 the subjective discount factor δ is set to 098

and the strength of the bequest motive β is set to 02 (see eg Laibson Repetto and Tobacman

1998 Cocco Gomes and Maenhout 2005 Inkmann Lopes and Michaelides 2011) The

jointness in consumption parameter θ is set to 02 This value is lower than the value of 05 used

by Brown and Poterba (2000) to reflect that jointness of consumption is less effective when one

or both partners are in a nursing home

The US HECM equity release program to which most reverse montages originated belong

requires both spouses to be at least 62 years old to access mortgages Thus the initial age of both

spouses is set to 62 at t = 0The maximum age in the model (at t = 2) is set to 100 and for having

identical period lengths the age at t = 1 is set to 81 making one period 19 years long The initial

endowment consists of liquid wealth of W0 = $135000 and a house worth H0 = $250000 which

reflect the median values for financial assets and primary residences for couples aged 60 to 65 in

the 2009 wave of the Survey of Consumer Finances

282 Interest Rates and House Price Growth

Interest rates are modeled as in Campbell and Cocco (2003) in their analysis of standard

mortgages That is future one-year interest rates are given by the mean rate plus a transitory iid

shock Based on one-year US Treasuries Campbell and Cocco estimate the mean of real

interest rates to be 2 with a standard deviation of 22 The interest rate over the first period

r0 is set equal to the mean real rate

18

Annual house price growth rates are modeled as normally distributed iid random variables The

parameters of the distribution are derived from estimates provided by Campbell and Cocco

(2003) based on the Panel Study of Income Dynamics (PSID) the mean real growth rate is 16

with a standard deviation of 1174

283 Health States Care Costs Long-Term Care Insurance and Annuity Products

For the calibration of the probabilities of the four health states (staying in good health needing

some care at home needing to move to a nursing home being death) and the state-dependent

care costs (0 moderate high 0) the same values are used as in Davidoff (2009) That is the

probabilities for entering the different states are based on Robinson (2002) and the annual care

expenses are based on Ameriks et al (2011) Annual care costs in real terms are $10000 in the

second state $50000 in the third state and zero otherwise LTCI for a 62 year old person is then

priced according to formula (2-1) with the interest rate of 2 Likewise annuities are priced

according to formula (2-2) using the respective survival probabilities A zero loading is assumed

for both the LTCI and annuities (LTCI = LTCI = 0)

284 Fair Pricing of the Reverse Mortgage

The reverse mortgage is priced such that provider of the product makes on average across all

future states a zero profit The profit is calculated as the expected present value of the loan

repayment (discounted using interest rates) minus the initial loan amount A margin ∆RM is

4 The total value of a house consists of the capital value and the rental yields The growth rate calibrated here is the

capital growth rate It excludes rental yields

19

determined that compensates the product provider for the equity guarantee (NNEG) embedded in

the reverse mortgage

Figure 2 gives the margin ∆RM0 for the variable interest rate reverse mortgage taken out at t = 0

for different actual loan-to-value ratios (LTVs) Given the calibration of interest rate house price

and health states the value of the house will always be enough to repay the loan for small LTVs

up to 030 For LTVs between 035 and 085 there are states where the NNEG becomes effective

and this reflects in a positive margin on the interest rate The margins vary between 005 and

186 These values fall into the range reported by Shan (2011) who reports that for US

HECM loans the lenderrsquos margin is typically between 1-2 For LTVs higher than 085 the

profit of the insurer is always negative on average independent of the margin and this

establishes a maximum LTV

-- Figure 2 here --

The pricing of the variable interest rate reverse mortgage offered at t = 1 is similar a margin

∆LS1 is determined to compensate the product provider for the NNEG The value of the NNEG

depends on how much the household has already borrowed at t = 0 on the house price growth

rate over the first period and on interest rates at t = 1 Figure 3 gives the margin ∆RM1 for

different loan amounts represented as ldquoadditional loan-to-value ratiordquo Results are presented for

20

different values of initial borrowing (ie for different LTVRM0 ratios) assuming low house price

growth over the first period and low interest rates over the second period

-- Figure 3 here --

285 Fair Pricing of the Sale and Lease Back Plan

The sale and lease back plan is priced such that product provider makes on average across all

future states a zero profit The providerrsquos profit is calculated as the expected present value of the

proceeds from sale of the equity share minus the initial lump sum paid out to the household This

initial lump sum is reduced to account for the expected present value of rental yields

To determine present values of sale proceeds and rental yields discount factors are used that

reflect house price risk The discount factors for the first period are determined by dividing the

total value of the ldquoreleasedrdquo equity share at t = 1 by the value of that share at t = 0 The total

value includes capital growth as described in Section 282 and rental yields over the first period

A discount factors for the second period is determined in the same way Rental yields over the

first and the second period are computed from an annual rental yield rent which is a percentage

of the equity share HRτ middot Hτ sold at the beginning of the period τ = 0 1

Previous studies on optimal consumption and portfolio choices have considered a rental yield of

6 per year (Yao and Zhang 2005) At this value and given the calibration of interest rate

house price and health states only 24 of the value of the equity share is paid out to the couple

21

under a home reversion plan taken out at t = 0 (and this value is independent of the percentage

HR that the couple decides to sell) In this study a lower (after-tax) rental yield of 2 is used

resulting in 54 of the value of the equity share paid out to the couple Alternatively a rental

yield of 4 is considered

286 Government-Provided Long-Term Care Insurance

With the government-provided LTCI the individual has to cover (1 minus+-) =50 of the

care costs up to a maximum of care costs of $6276 pa (equal to $100000 for the 19-year

horizon) For care costs higher than $6276 pa the individualrsquos out-of-pocket costs are limited

to 50$6276 pa

3 Results

The MATLAB function fmincon was used to implement the couplersquos optimization problem as a

constrained nonlinear optimization problem For the numerical solution of the model the house

price process is discretized using a binomial process (as in Yao and Zhang 2005 or Davidoff

2010c) The interest rate process is discretized in the same way

31 Optimal Equity Release at Different Points in Time

The base case is when the couple decides on consumption saving on purchasing annuities

private long-term care insurance (LTCI) and on taking out an equity release product The model

parameters are the baseline parameters given in Table 1 Different scenarios are compared One

22

scenario without equity release products two scenarios in which either the reverse mortgage or

the home revision plan described in Section 26 are offered only at t = 0 and two scenarios in

which the reverse mortgage or the home revision plan are offered at t = 0 and t = 1

Government-provided LTCI is not available in any of the five scenarios Table 2 gives the

corresponding results

-- Table 2 here --

The results for first three scenarios show that the couple clearly has a demand for equity release

products at time t = 0 When offered the reverse mortgage only at t = 0 the couple chooses to

borrow up to the maximum loan-to-value-ratio (LTV) When offered the home reversion plan at

t = 0 the household chooses to convert a very large proportion HR0 of the home In both cases

the changes in expected discounted utility indicate substantial welfare gains for the couple The

utility gain is higher for the reverse mortgage than for the home reversion plan

Having access to equity release products at time t = 1 in the last two scenarios further improves

the couplersquos utility but the utility gain is smaller than the utility gain from having access to

equity release products at t = 0 Borrowing and home reversion mainly takes place at t = 0

Table 2 reports the couplersquos consumption annuity premiums LTCI premiums and savings at

t = 0 as percentages of initial liquid wealth W0 before equity release The sum of these figures

23

indicates that the couple significantly increases their liquid wealth with equity release products

The reverse mortgage results in higher lump-sum payments which explains why this product is

preferred over the home reversion plan The additional liquidity from the two equity release

products is used to increase consumption C0 and to increase savings Annuity demand is

relatively stable across scenarios It is low because the annuity pays only at t = 1 and because of

the bequest motive Private LTCI demand is also unchanged The couple faces uncertain but

potentially high care costs and always buys full LTCI coverage as a result

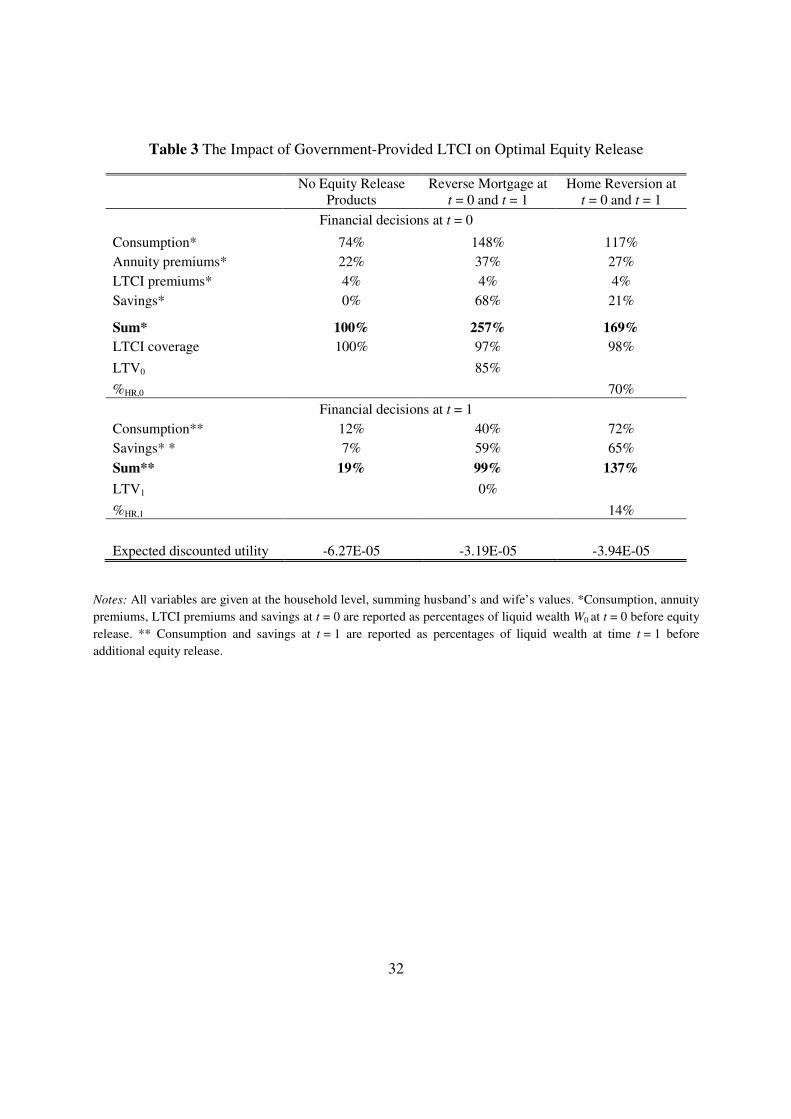

32 Government-Provided Long-Term Care Insurance

Next a variant of the model with compulsory government-provided LTCI as described in

Sections 25 and 286 is considered Again the couple decides on consumption saving on

purchasing annuities private long-term care insurance (LTCI) for the remaining out-of-pocket

care costs and on equity release The model parameters are the baseline parameters given in

Table 1 Three different scenarios are compared One scenario without equity release products

and two scenarios in which the reverse mortgage or the home revision plan described in Section

26 are offered at t = 0 and t = 1 The numerical results for these scenarios are given in Table 3

Scenarios with equity release products offered only at t = 0 are not compared separately

-- Table 3 here --

The couple benefits from the fairly generous government-provided LTCI scheme but the utility

gains are much smaller than the utility gains from having access to equity release products This

24

can be seen by comparing the scenario without equity release products in Table 3 with the base

case results presented in Table 2 in the previous section

Similar levels of equity release are found to be optimal with the government-provided LTCI As

in the base case without public LTCI the couple chooses to borrow up to the maximum loan-to-

value-ratio (LTV) of the reverse mortgage at t = 0 and similar levels of home reversion at t = 0

and t = 1 are found to be optimal

With the government-provided LTCI the couple spends less of their wealth on private LTCI

They still choose to buy full coverage for each partner but because the private insurance only

covers the remaining out-of-pocket care costs the premiums are much lower They use the

additional wealth to buy more annuities

33 Sensitivity Analyses Higher Risk Aversion No Bequest Motive and a Higher House

Value

Table 4 gives the results for three different cases used to test the sensitivity of the base case

results presented in Table 2 in Section 31 In each case one model parameter is varied The first

case is when the couple has no bequest motive (β = 0) in the second case a higher risk aversion

is assumed (χ = 5) and in the third case a higher initial house value of H0 = $500000 is

considered For each case three different scenarios are compared One scenario without equity

25

release products and two scenarios in which the reverse mortgage or the home revision plan

described in Section 26 are offered at t = 0 and t = 1

-- Table 4 here --

In the case without a bequest motive the couple decidesmdashas in the base casemdashto borrow the

maximum loan-to-value-ratio (LTV) allowed with the reverse mortgage at t = 0 When offered

the home reversion plan at t = 0 and at t = 1 they choose to sell their home completely at t = 0

(HR0=100) in exchange for a lump-sum payment and a lease-for-life agreement Without a

bequest motive the couple buys significantly more annuities in all three scenarios than in the

base case with a bequest motive which is in line with the findings of previous studies (Brown

and Poterba 2000) Private LTCI demand is largely unaffected the couple chooses full coverage

for each partner

The middle columns of Table 4 refer to the case when the couple has a higher risk aversion than

in the base case (γ = 5 instead of γ = 2) Again as in the base case the couple decides to borrow

the maximum loan-to-value-ratio (LTV) allowed with the reverse mortgage at t = 0 The home

reversion pattern is different from the base case in Section 31 being more risk averse the

couple decides to release more of their home equity at t = 0 and less at t = 1 (HR0=80 and

HR1=18 compared to 75 and 14 in the base case) The couple buys significantly more

26

annuities in all three scenarios than in the base case but their decision to fully insurance long-

term care costs with private LTCI is unchanged

In the third case presented in the last three columns of Table 4 a higher initial house value of

H0 = $500000 is considered In the base case the house value H0 = $250000 made up 65 of

the couplersquos total wealth at t = 0 This ratio is 79 for a house value H0 = $500000 The results

show that the couple chooses to borrow a similar amount with the reverse mortgage although the

loan-to-value ratios both at t = 0 and at t = 1 are reduced More equity than in the base case is

released with the home reversion scheme

Three key findings emerge across the cases with alternative parameter values (no bequest

motive higher risk aversion and in higher initial house value) and these findings are consistent

with the base case (i) The couple has large utility gains from having access to either one of the

two equity release products (ii) higher utility gains are found for the reverse mortgage and (iii)

equity release predominantly takes place at t = 0

4 Summary and Conclusions

This study models the decision problem of a retiring couple that holds the major fraction of their

wealth as home equity and faces longevity risk long-term care risk house price risk and interest

rate risk The couple can choose to buy annuities long-term care insurance and to borrow

against the home using different equity release products at different point in time The numerical

27

results of this study suggest that the couple enjoys large utility gains from having access to either

one of the two equity release products Higher utility gains are found for the reverse mortgage

The household chooses to unlock home equity early on in retirement The key results are

consistent across a range of cases with different parameter values The availability of a

government-provided LTCI does not change the use of equity release products significantly but

does change the demand for annuities

References

Ameriks J A Caplin S Laufer and S Van Nieuwerburgh (2011) The Joy of Giving or

Assisted Living Using Strategic Surveys to Separate Bequest and Precautionary Motives

Journal of Finance 66 519ndash561

Andrews D and A Caldera Saacutenchez (2011) Drivers of Homeownership Rates in Selected

OECD Countries OECD Economics Department Working Papers No 849 OECD

Publishing

Artle R and P Varaiya (1978) Life cycle consumption and homeownership Journal of

Economic Theory 18 38ndash58

Australian Securities and Investments Commission (2005) Report 59 - Equity release products

November 2005

Brown J R and A Finkelstein (2007) Why is the market for long-term care insurance so

small Journal of Public Economics 91 1967ndash1991

Brown J R and J M Poterba (2000) Joint Life Annuities and Annuity Demand by Married

Couples Journal of Risk and Insurance 67 527ndash553

Campbell J Y and J F Cocco (2003) Household Risk Management and Optimal Mortgage Choice

Quarterly Journal of Economics 118 1449ndash1494

Case K J Cotter and S Gabriel (2011) Housing Risk and Return Evidence from a Housing

Asset-Pricing Model Journal of Portfolio Management 35 89ndash109

28

Cocco J F F J Gomes and P J Maenhout (2005) Consumption and Portfolio Choice Over

the Life-Cycle Review of Financial Studies 18 491ndash533

Davidoff T (2009) Housing Health and Annuities Journal of Risk and Insurance 76 31ndash52

Davidoff T (2010a) Financing Retirement with Stochastic Mortality and Endogenous Sale of a

Home Working Paper

Davidoff T (2010b) Home equity commitment and long-term care insurance demand Journal

of Public Economics 94 44ndash49

Davidoff T (2010c) Interest Accumulation in Retirement Home Equity Products Working

paper University of British Columbia

Davidoff T and G Welke (2006) Selection and Moral Hazard in the Reverse Mortgage

Market Working paper University of CaliforniandashBerkeley

Deloitte and SEQUAL (2012) Australiarsquos reverse mortgage market reached $33bn at 31

December 2011 Media Release 5 June 2012

Commission on Funding of Care and Support (2011) Fairer Care Funding ndash The Report of the

Commission on Funding of Care and Support July 2011 available at

httpwwwdilnotcommissiondhgovuk

Fratantoni M C (1999) Reverse Mortgage Choices A Theoretical and Empirical Analysis of

the Borrowing Decisions of Elderly Homeowners Journal of Housing Research 10 189ndash

208

Inkmann J P Lopes and A Michaelides (2011) How Deep is the Annuity Market

Participation Puzzle Review of Financial Studies 24 279ndash319

Koijen R S J S Van Nieuwerburgh and M Yogo (2011) Health and Mortality Delta

Assessing the Welfare Cost of Household Insurance Choice Netspar Discussion Paper No

052011-050

KRS Key Retirement Solutions (2011) UK Equity Release Market Monitor 2010 Review

Laibson D I A Repetto and J Tobacman (1998) Self-Control and Saving for Retirement

Brookings Papers on Economic Activity 1998 91ndash196

Mitchell O S J M Poterba M J Warshawsky and J R Brown (1999) New Evidence on the

Moneyrsquos Worth of Individual Annuities American Economic Review 89 1299ndash1318

29

Oliver Wyman (2008) Moving beyond HECM in equity release markets available at

httpwwwoliverwymancomdeu-insightsOliver_Wyman_-

_Moving_beyond_HECM_in_equity_release_marketspdf

Productivity Commission (2011) Caring for Older Australians ndash Productivity Commission

Inquiry Report No 53 28 June 2011 available at

httpwwwpcgovauprojectsinquiryaged-care

Reifner U S Clerc-Renaud E F Perez-Carillo A Tiffe and M Knoblauch (2009) Study on

Equity Release Schemes in the EU Part 1 General Report Hamburg

httpwwweurofinasorguploadsdocumentspoliciesequity_release_part1_enpdf

Robinson J (2002) A Long-Term Care Status Transition Model Working paper University of

Wisconsin

Shan H (2011) Reversing the Trend The Recent Expansion of the Reverse Mortgage Market

Real Estate Economics 39 743ndash768

Whitehead C and J Yates (2010) Is there a Role for Shared Equity Products in Twenty-First

Century Housing - Experience in Australia and the UK In S J Smith B A Searle (eds)

The Blackwell Companion to the Economics of Housing The Housing Wealth of Nations

Chichester Wiley-Blackwell

Yao R and H H Zhang (2005) Optimal Consumption and Portfolio Choices with Risky

Housing and Borrowing Constraints Review of Financial Studies 18 197ndash239

Yogo M (2009) Portfolio Choice in Retirement Health Risk and the Demand for Annuities

Housing and Risky Assets NBER Working Paper 15307

30

Table 1 Model Parameters

Parameter Baseline Value Alternative Value

House value t = 0 H0 $250000 $500000 Liquid wealth t = 0 W0 $135000 Age of both spouses t = 0 in years 62

Relative risk aversion γ 2 5 Subjective discount factor δ 098 Jointness of consumption θ 05

Strength of bequest motive β 02 0 Long term care expenses per year LTC

i $10000 (needing some

care at home) $50000 (needing care in a

nursing home)

Mean interest rate per year (= interest rate at t = 0)

r0 20

Standard deviation of interest rate per year

Std(r0) 22

Mean house price growth per year g 16 Standard deviation of house price growth per year

Std(g) 117

Rental yield 2 4 Mortgage rate margin per year mo 0 175 Annuity loading factor λA 0 10

Long term care insurance loading factor

λLTCI 0 16

Coinsurance percentage of the govt-provided LTCI

+- 50

Stop loss of the govt-provided LTCI per year

$6276

Notes This table shows baseline and alternative model parameters All parameters referring to multiple years (subjective discount factor interest rate house price growth mortgage rate) are scaled by the period length (19 years) in the model All monetary values are in real terms

31

Table 2 Optimal Equity Release at Different Points in Time

No Equity Release Products

Reverse Mortgage at

t = 0

Home Reversion at

t = 0

Reverse Mortgage at

t = 0 and t = 1

Home Reversion at

t = 0 and t = 1

Financial decisions at t = 0

Consumption 51 127 141 148 104

Annuity premiums 19 18 28 18 16

LTCI premiums 21 21 21 21 21

Savings 10 92 1 70 34

Sum 100 257 190 257 174

LTCI coverage 100 100 100 100 100

LTV0

85

85 HR0

91

75

Financial decisions at t = 1

Consumption 13 25 77 29 57

Savings 3 75 18 71 73

Sum 16 100 95 100 130

LTV1

0 HR1

14

Expected discounted utility -781E-05 -438E-05 -479E-05 -416E-05 -464E-05

Notes RM denotes the lump-sum reverse mortgage with variable interest rates and a no-negative-equity guarantee HR denotes the home reversion plan All variables are given at the household level summing husbandrsquos and wifersquos values Consumption annuity premiums LTCI premiums and savings at t = 0 are reported as percentages of liquid wealth W0 at t = 0 before equity release Consumption and savings at t = 1 are reported as percentages of liquid wealth at time t = 1 before additional equity release

32

Table 3 The Impact of Government-Provided LTCI on Optimal Equity Release

No Equity Release Products

Reverse Mortgage at t = 0 and t = 1

Home Reversion at t = 0 and t = 1

Financial decisions at t = 0

Consumption 74 148 117

Annuity premiums 22 37 27

LTCI premiums 4 4 4

Savings 0 68 21

Sum 100 257 169

LTCI coverage 100 97 98

LTV0

85 HR0

70

Financial decisions at t = 1

Consumption 12 40 72

Savings 7 59 65

Sum 19 99 137

LTV1

0 HR1 14

Expected discounted utility -627E-05 -319E-05 -394E-05

Notes All variables are given at the household level summing husbandrsquos and wifersquos values Consumption annuity

premiums LTCI premiums and savings at t = 0 are reported as percentages of liquid wealth W0 at t = 0 before equity

release Consumption and savings at t = 1 are reported as percentages of liquid wealth at time t = 1 before

additional equity release

33

Table 4 Sensitivity Analyses Higher Risk Aversion No Bequest Motive and a Higher House Value

No bequest motive (β = 0) Higher risk aversion (χ = 5) Higher house value (H0 = $500000)

No Equity Release Products

Reverse Mortgage

at t = 0 and t = 1

Home Reversion at t = 0 and

t = 1

No Equity Release Products

Reverse Mortgage

at t = 0 and t = 1

Home Reversion at t = 0 and

t = 1

No Equity Release Products

Reverse Mortgage

at t = 0 and t = 1

Home Reversion at

t = 0 and t = 1

Financial decisions at t = 0

Consumption 46 170 133 50 119 95 55 147 165

Annuity premiums 33 47 45 29 34 29 17 74 11

LTCI premiums 21 20 21 21 21 21 21 21 21

Savings 0 20 0 0 84 35 8 0 62

Sum 100 257 199 100 257 179 100 241 258

LTCI coverage 100 96 100 100 100 100 100 100 100

LTV0 85 85 38

HR0 100 80 83

Financial decisions at t = 1

Consumption 95 55 92 91 48 66 69 93 40

Savings 5 44 1 9 52 66 32 13 86

Sum 100 99 94 100 100 132 101 105 127

LTV1 0 0 3

HR1 0 18 10

Expected discounted utility -734E-05 -311E-05 -331E-05 -255E-19 -971E-21 -265E-20 -742E-05 -266E-05 -349E-05

Notes All variables are given at the household level summing husbandrsquos and wifersquos values Consumption annuity premiums LTCI premiums and savings at

t = 0 are reported as percentages of liquid wealth W0 at t = 0 before equity release Consumption and savings at t = 1 are reported as percentages of liquid

wealth at time t = 1 before additional equity release

34

Figure 1 Model Timing

Figure 2 Zero-profit margin for a reverse mortgage taken out at t = 0

Notes This graph shows the margin ∆LS1 for a variable interest rate reverse mortgage taken out at t = 0 for different

actual loan-to-value ratios

t = 0 Period 1 t = 1 Period 2 t = 2

Realization of random

- Health status of husband and wife

- House value

- Interest rate

rarr Borrow against home

rarr Buy annuity

rarr Buy LTCI

rarr Consume and save

rarr If both are dead bequeath net assets

rarr Else

rarr Receive annuity and LTCI payments

rarr Receive accumulated savings

rarr Borrow against home

rarr Cover out-of-pocket care costs

rarr Consume and save

rarr Bequeath net assets

Husband and wife are in

good health

Husband and wife die

Realization of random house value

35

Figure 3 Zero-profit margin for a reverse mortgage taken out at t = 1

Notes This graph shows the margin ∆LS1 for a variable interest rate reverse mortgage taken out at t = 1 The margin differs according to how much the household borrowed at t = 0 Results are given for different values of initial borrowing (ie for different LTVLS0 ratios) and refer to cases with low house price growth over the first period and low interest rates over the second period

2

1 Introduction

This paper studies the optimal product choice of home equity release products from the

homeownerrsquos perspective in the presence of longevity long-term care house price and interest

rate risk A retiring couple chooses among different home equity release contracts and long-term

care and longevity insurance products Home equity release contracts differ substantially in the

way house price risks are shared and transferred between the homeowner and the lender Due to

this the optimal choice is strongly dependent on the homeownersrsquo individual characteristics

(including risk aversion and a bequest motive) and on the interaction with longevity and long-

term care risks which vary strongly between different institutional settings

Home equity is a very special asset class The home is an investment and a residence providing

non-pecuniary services For example people value the ability to ldquoage in placerdquo (Davidoff

2010c) and even with substantial mortgage balances outstanding people are happy about being

a homeowner (Whitehead and Yates 2010) Homeownership rates are high and are between 50

and 80 for most OECD countries (Andrews and Caldera Saacutenchez 2011) Home equity

represents the major share of the elderlyrsquos total assets For example for households aged 65+ in

the US the value of the primary residence comprises on average (median) 49 (52) of

householdsrsquo total assets with 82 of households aged 65+ actually owning a house (2009 wave

of the Survey of Consumer Finances) A home is not an ideal asset to meet the financial needs of

elderly households especially when having no other substantial sources of income It

concentrates a large amount of household savings in a single asset exposing the household to

substantial idiosyncratic risk (Case Cotter and Gabriel 2011) It is illiquid and in case of urgent

3

cash needs for example due to health shocks it cannot be sold in parts to pay for out-of-pocket

costs

Home equity release products convert home equity into liquid wealth but allow homeowners to

continue residing in their home Markets for equity release products are growing in the US

(Shan 2011) in the UK (KRS 2011) and elsewhere (Reifner et al 2009 Deloitte and

SEQUAL 2012) A range of different contract designs exist that share and transfer house price

risks in various ways between the homeowner and the lender The most common product in most

markets is a reverse mortgage with rolled-up interest (Oliver Wyman 2008 Davidoff 2010c)

This product allows homeowners to participate in house price appreciations while giving

protection to adverse house price developments through a no-negative equity guarantee (NNEG)

typically embedded in the product Home reversion schemes available for example in the UK

and in Australia allow homeowners to transfer a proportion of house price risks to the lender in

exchange for a lump-sum payment and a lease-for-life agreement (Oliver Wyman 2008)

Contract designs also differ in other dimensions such as having a fixed or variable interest rate

(Oliver Wyman 2008) Markets are very dynamic and new products are being constantly

developed (Australian Securities and Investment Commission 2005) Comparing and choosing

among various products with different risk and return features has become an increasingly

important but also increasingly difficult task for todayrsquos homeowners

Several papers examine home equity release products in optimal household portfolios Artle and

Varaiya (1978) show that the possibility of borrowing against home equity in retirement and

thereby relaxing liquidity constraints and smoothing consumption over the life cycle enhances

4

utility Fratantoni (1999) models the product choice between two reverse mortgage designsmdash

annuity payout plan and line-of-credit planmdashfor an elderly homeowners facing non-insurable

expenditure shocks He finds that line-of-credit plans are generally preferable since they are

more flexible and can provide large sums of money in case of the expenditure shock Davidoff

(2009 2010a 2010b) extends this research by allowing for health and longevity risks He

confirms that the availability of the reverse mortgages itself is utility-enhancing and finds

interaction effects with annuities and long-term care insurance For example home equity may

substitute long term care insurance Davidoff (2010c) introduces house price risk into a reverse

mortgage choice model He shows that amortization of interest (rolled-up interest) a feature

inherent in many currently sold contracts types is not always Pareto optimal Likewise Yogo

(2009) considers stochastic housing prices (and stochastic health depreciation) confirming that

reverse mortgages are utility enhancing The decision between fixed-rate and adjustable-rate

products so far has been studied for ldquonormalrdquo mortgages with adjustable-rate products being

found more attractive to homeowners (Campbell and Cocco 2003)

In summary a number of studies using different models find that reverse mortgages are utility-

enhancing The utility gains are shown to depend on the interaction with health and longevity

risks and on the availability of products to insure against these risks

This study provides the following contributions to the literature First we extend previous

models by considering longevity long-term care house price and interest rate risk and by

modeling the household as a couple as reverse mortgage decisions are often triggered by the

5

death of one spouse1 Second a general model is developed covering a range of different equity

release products and the timing problem of when to release home equity Third we analyze the

optimal choice in different institutional settings for long term care insurance (LTCI) and examine

the resulting interactions We distinguish between a setting in which most costs have to be paid

out-of-pocket with private insurance available and a setting in which most long-term care costs

are born by a government-sponsored system

The results of this study show that the couple enjoys large utility gains from having access to

either one of the two equity release products Higher utility gains are found for the reverse

mortgage The household chooses to unlock home equity early on in retirement These key

results emerge consistently across a range of cases with different parameter values The

availability of a government-provided LTCI does not change the use of equity release products

significantly but does change the demand for annuities

The paper is structured as follows Section 2 introduces the life cycle model Section 3 presents

the results Section 4 concludes and discusses policy recommendations

1 Shan (2011) reports that 45 in the US equity release program are single females 34 are couples and 11 are

single males (based on 2007 data) In Australia the majority of equity release customers are couples between 70-75

years old (Deloitte and SEQUAL 2012)

6

2 The Model

21 General Structure of the Model and Timing

The decision problem of a retiring couple is modeled that holds the major fraction of wealth in

their home The index isin is used to denote probabilities payouts or utility values of the

husband (m) and the wife (f) respectively The couple faces longevity risk long-term care risk

house price risk and interest rate risk Different insurance and home equity release products are

available to the couple

The decisions of the couple are modeled in an augmented life cycle model The model extends

previous work by Davidoff (2009 2010b 2010c) by considering a couple by allowing for

interest rate risk by including different types of equity release products and modeling the timing

decision of when to release home equity A two-period model (three points in time) is developed

that captures the couplersquos decisions at retirement and at an advanced age The modelrsquos input

parameters are calibrated such that each of the two periods reflects a multi-year horizon Figure 1

illustrates the decision and timing structure of the model

-- Figure 1 here --

At time t = 0 both spouses are in good health The initial endowment consists of the home and

liquid wealth The couple decides on consumption on saving over the first period of their

retirement on purchasing annuities long-term care insurance (LTCI) and on taking out an equity

release product Equity release products increase liquid wealth available for consumption

saving and for purchasing insurance products

7

At time t = 1 as in Davidoff (2009) each husband and wife independently will be in one of four

health states implying different health care expenses The random house value as well as the

interest rates and mortgage rates for the second period are realized Annuities and LTCI are not

available for purchase at t = 1 There are the following main cases at t = 1

1) Both spouses are dead Their remaining liquid wealth and housing wealth (net of mortgage

repayments) are left as a bequest

2) At least one partner is still alive The household receives payments from insurance contracts

and from equity release products bought at t = 0 Health state-dependent care expenses not

covered by insurance are paid out-of-pocket The couple decides on consumption and saving

over the second period

2a) Both spouses are in a nursing home or one partner is in a nursing home and the other one

is dead The house is sold and all outstanding loans are paid back Additional sale

proceeds are added to liquid wealth

2b) At least one partner is still living at home The couple decides whether to take out another

equity release product

At t = 2 both partners are dead with certainty Remaining liquid wealth and housing wealth (net

of mortgage repayments) are bequeathed

22 Interest Rates Mortgage Rates House Price Growth and Savings Growth

The risk-free interest rate r0 over the first period is known at t = 0 The interest rate r1 over the

second period is a random variable realized at t = 1 Mortgage rates are derived from interest

8

rates by adding a margin ∆RM to r0 and r1 (see Sections 26 and 28 for more details) Savings at

t = 0 S0 and at t = 1 S1 accrue the respective one-year interest rates r0 and r1 At t = 0 the

couple owns a mortgage-free house worth H0 At t = 1 the house value is H1 = H0 middot (1 + g1) and at

t = 2 it is H2 = H1 middot (1 + g2) where the growth rates g1 and g2 are iid random variables

uncorrelated with the interest rate

23 Health States and Care Costs

At t = 0 both husband and wife are in good health and no care expenses have to be paid At time

t = 1 husband and wife are each independently in one of four health states requiring different

levels of health care costs The four states are staying in good health and having no long-term

care costs (state h) with probability ph needing some care at home at cost LTCc (state c) with

probability pc needing to move to a nursing home at care costs LTCn (state n) with probability

pn and being death (state d) with probability pd (ph + pc + pn + pd = 1)

24 Long-Term Care Insurance and Annuity Products

Long-term care insurance (LTCI) covering the care costs in state c and the care costs

13 in state n is available at t = 0 Husband and wife buy separate LTCI contracts The couple

chooses the proportion of insurance coverage by choosing the amount of wealth

spent on LTCI for each partner i = m f LTCI is priced according to the actuarial principle of

equivalence plus a proportional loading LTCI The premium for partial coverage of an

individualrsquos care costs is given by

9

= (1 + ) ∙ ∙ ∙

∙ ()

= (2-1)

Furthermore single life annuities are available at t = 0 Annuities are priced based on the

actuarial principle of equivalence plus a proportional loading A The premium for an annuity

paying $ at t = 1 conditional on survival is given by

= (1 + ) ∙amp( )∙

() =

(2-2)

The annuity payment $ is determined by the amount of wealth the couple decides to invest

in individual irsquos annuity according to formula (2-2)

25 Government-Provided Long-Term Care Insurance

Scenarios are considered in which both public and private long-term care insurance (LTCI) are

available Social insurance arrangements for long-term care services exist in a number of OECD

countriesmdashGerman Japan Korea the Netherlands and Luxembourg (for an overview see

Productivity Commission 2012)

In this study government-provided LTCI is modeled as a compulsory coinsurance arrangement

with a stop loss limit The insurance scheme covers a percentage +- of all care costs up

to an out-of-pocket spending limit This arrangement abstracts from the details of the different

systems and focuses on the impact of possible structures of sharing care costs The arrangement

is in line with suggestions by the UK Commission on Funding of Care and Support which

suggests introducing a social insurance scheme with coinsurance and a cap and agrees with

10

suggestions by the Productivity Commission in Australia (Commission on Funding of Care and

Support 2011 Productivity Commission 2012) The retired household faces no costs for this

insurance but the cost is levied on the working generation The couple can decide to buy private

LTCI coverage for the proportion of care costs not covered by the public LTCI Because the

expected care costs are lower a lower premium for private LTCI results

26 Equity Release Products

261 Overview

The model developed above can accommodate a range of different home equity release products

In this study we focus on lump-sum reverse mortgages and home revision plans (also called sale-

and-lease-back plan or shared equity mortgage) Both products are offered to the household at

t = 0 and t = 1 With these types the analysis covers the main types of equity release schemes

currently available in Australia Canada UK and the US (Oliver Wyman 2008 Davidoff

2010c)2 We focus on reverse mortgages with variable interest rates and a NNEG because this is

the dominant product design in most markets

Often reverse mortgages are offered only to households that own a debt-free home We model

this situation by considering scenarios in which equity release products are only offered once (at

t = 0) The comparison allows us to determine optimal equity release choices from the

householdsrsquo perspective

2 Because the reverse mortgage is available at t = 0 and 1 and private annuities are available for purchase the line-

of-credit and annuity payout plan types of reverse mortgage additionally studied in Fratatoni (1999) are covered

(implicitly) in our analysis

11

262 Lump-sum reverse mortgage with variable interest rates and NNEG

A lump-sum reverse mortgage (RM) with variable interest rates and a no-negative-equity

guarantee is available at t = 0 and t = 1 LSRMτ denotes the loan value of a contract taken out at

time τ paid out as a lump sum at time τ

RMτ_balancet is the time t value of the outstanding loan balance of a reverse mortgage taken out

at time τ This balance is given by compounding LSRMτ at the respective mortgage rate (rolled-up

interest) Mortgage rates are calculated by adding a margin ∆RM to the random interest rate The

margin reflects the price of the no-negative-equity guarantee The value of this guarantee is

different for reverse mortgages taken out at t = 0 and at t = 1 resulting in different margins For a

reverse mortgage taken out at t = 0 the following mortgage rates apply r0 + ∆RM0 over the first

period and r1 + ∆RM0 over the second period (or r0 + ∆RM0 over both periods in case of fixed

interest rates) The margin r1 + ∆RM1 applies over the second period for a reverse mortgage taken

out at t = 1

The loan amounts LSRM 0 and LSRM 1 are decision variables Loan amounts are restricted by a

maximum loan-to-value ratio which is defined in terms of the house value Hτ Different (age-

specific) maximum loan-to-value ratios LTV0max and LTV1

max apply to reverse mortgages taken

out at t = 0 and t = 1 The maximum loan-to-value ratio at t = 1 LTV1max is defined as a

combined loan-to-value ratio

12

A reverse mortgage taken out at t = 0 is repaid at t = 1 if both husband and wife are in a nursing

home one partner is in a nursing home and the other one is dead or both partners are dead

These cases correspond to the cases 1) and 2a) described in Section 21 In the remaining cases

the couple can decide to take out another reverse mortgage at t = 1 and the outstanding loan

balances of both contracts are paid back at t = 2

In case of repayment the house is sold and the proceeds of the sale are used to pay back the total

outstanding reverse mortgage balance RM_balancet = RM0_balancet + RM1_balancet The total

repayment of both reverse mortgage loans is capped by the house value Ht at time t due to the

no-negative-equity guarantee To simplify the pricing repayment of LSRM1 has priority over

repayment of LSRM1 if at time t = 2 LSRM_balance2 lt H2

263 Home reversion plan

Home reversion plans (HR) are offered at t = 0 and t = 1 Under this arrangement the household

sells a share HRτ middot Hτ τ = 0 1 of the home equity to the product provider and receives a lump

sum LSHRτ in return The lump sum LSHRτ is less than the market value of the equity share

reflecting the value of a lease-for-life agreement and house price risk The household does not

have to pay a regular rent on the equity share sold to the bank but the equivalent present value of

rental payments is deducted from the lump-sum payout The equity share of the product provider

appreciates with the house price growth rates That is for example for a HR contracted at t = 0

the product provider owns HR0 middot H1 of the house value at t = 1 and HR0 middot H2 at t = 2

13

A home-reversion plan taken out at t = 0 ends at t = 1 if both husband and wife are in a nursing

home one partner is in a nursing home and the other one is dead or both partners are dead In

the remaining cases the couple can decide to take out another home reversion plan at t = 1 and

both contracts end at t = 2 When the contract ends the house is sold and the sale proceeds are

divided according to equity shares The couplersquos share is added to the liquid wealth that is

bequeathed

27 The Couplersquos Maximization Problem

The couplersquos lifetime utility function V is based on Brown and Poterba (2000) but with a

bequest motive as for example in Inkmann Lopes and Michaelides (2011)3

0(1) = sum 345 ∙ 678 9 + (1 minus 5) ∙ lt ∙ =(1)gtA (2-3)

δ denotes the subjective discount factor of the couple β the utility weight of the bequest motive

5 is an indicator variable taking the value one if at least one member of the couple is alive and

zero otherwise Ct is the consumption in real terms of the husband (m) and wife (f) The wealth

bequeathed by the couple Wt is comprised of liquid wealth and the house value net of payments

to repay equity release products

3 Davidoff (2009) considers an individual whose utility depends on both consumption and the housing stock He

introduces a utility penalty for moving out of the house when in good health and sets this parameter such that

moving is never optimal except when the individual has to go to a nursing home Our model does not incorporate

the decision to move based on stylized facts (Whitehead and Yates 2010) the decision to live in the own home is

assumed to be always optimal when in good health and housing is not needed as an argument in the utility function

(as in Campbell and Cocco 2003)

14

The one-period utility functions of the couple U is given by the equally weighted sum of the

husband and the wifersquos subutility functions Um and Uf (Brown and Poterba 2000)

678 9 = 58 ∙ 6878 9 + 59 ∙ 6979 8 (2-4)

6878 9 = ampBCDB

E)FGH

(I) (2-5)

6979 8 =ampB

EDBC)FGH

(I)

where 58 (59) is the indicator variable taking the value one if the husband (wife) is alive and 0

otherwise The parameter θ controls the degree of jointness (sharing of resources) in

consumption between the husband and the wife Both spouses have their subutility function

defined over consumption with an identical relative risk aversion parameter γ The bequest utility

function B exhibits the same relative risk aversion as U and is given by

=(1) = JBFGH

(I) (2-6)

The couplersquos objective is to maximize the expectation over (2-3) subject to a set of constraints

The couplersquos optimization problem is given by

maxBNOBPQCPQE PRSTUC PRSTUE EW0(1)X Y = 0 1 (2-7)

where the index j refers to cash flows from equity release schemes alternatively available

(j = RM HR) The optimization problem is subject to

(i) consumption and bequest constraints

15

A8 + A9 = 1A minus [A minus8 minus9 minus8 minus9 + [A

8 + 9 = [A ∙ (1 + ]A) minus [+$8 + $9 minus 71 minus+- minus8 ∙ 8 minus

71 minus+- minus9 ∙ 9 + [

Bequest constraint in case of the reverse mortgage

1 = [A ∙ (1 + ]A) + maxW minus _`_bcdcefg 0X

1 = [ ∙ (1 + ]) + maxW^ minus _`_bcdcefg 0X

Bequest constraint in case of the home reversion plan

1 = [A ∙ (1 + ]A) +71 minushiA ∙

1 = [ ∙ (1 + ]) + 71 minushiAminushi ∙ ^

(2-8)

(ii) borrowing constraints

0 le [A le 1A minus8 minus9 minus 8 minus 9 + [A (2-9)

0 le [ le [A ∙ (1 + ]A)+$8 + $9 minus 71 minus+- minus8 ∙ (8 + 138)

minus 71 minus+- minus9 ∙ (9+139) + [

(2-10)

(iii) no-short sale constraints for equity release and insurance products

0 le [A [ 8 9 8 9 (2-11)

and (iv) further product constraints

bull Maximum loan-to-value ratios for the reverse mortgage

[ikA le 0ikA8lm^A (2-12)

16

_`_bcdcefg + [ik le 0ik8lm

bull Maximum home reversion rate

hiAminushi le 1 (2-13)

bull LTCI benefits capped by actual care expenses

le 1 = (2-14)

28 Numerical Calibration of Baseline Parameters

This section describes the numerical calibration of the modelrsquos baseline parameters The

parameters are chosen to reflect the US market and to allow comparison with previous studies

Alternative parameter values are introduced in Section 3 Table 1 summarizes the numerical

calibration To distinguish product design effect from pricing effect especially in the different

equity release products all products are priced such that the product provider makes a zero

expected profit The pricing of the insurance and equity release products reflects the risks

inherent in these products

-- Table 1 here --

281 The Couplersquos Preferences and Endowment

The standard parameters for the couplersquos preferences (relative risk aversion subjective discount

factor strength of the bequest motive) are set within the range typically used in life cycle models

17

in the literature Relative risk aversion γ is set to 2 the subjective discount factor δ is set to 098

and the strength of the bequest motive β is set to 02 (see eg Laibson Repetto and Tobacman

1998 Cocco Gomes and Maenhout 2005 Inkmann Lopes and Michaelides 2011) The

jointness in consumption parameter θ is set to 02 This value is lower than the value of 05 used

by Brown and Poterba (2000) to reflect that jointness of consumption is less effective when one

or both partners are in a nursing home

The US HECM equity release program to which most reverse montages originated belong

requires both spouses to be at least 62 years old to access mortgages Thus the initial age of both

spouses is set to 62 at t = 0The maximum age in the model (at t = 2) is set to 100 and for having

identical period lengths the age at t = 1 is set to 81 making one period 19 years long The initial

endowment consists of liquid wealth of W0 = $135000 and a house worth H0 = $250000 which

reflect the median values for financial assets and primary residences for couples aged 60 to 65 in

the 2009 wave of the Survey of Consumer Finances

282 Interest Rates and House Price Growth

Interest rates are modeled as in Campbell and Cocco (2003) in their analysis of standard

mortgages That is future one-year interest rates are given by the mean rate plus a transitory iid

shock Based on one-year US Treasuries Campbell and Cocco estimate the mean of real

interest rates to be 2 with a standard deviation of 22 The interest rate over the first period