risk changes and external financing activities: tests of ... · risk changes and external financing...

TRANSCRIPT

Risk Changes and External Financing Activities: Tests of the Dynamic Trade-off Theory of Capital Structure*

Martin J. Dierker Korea Advanced Institute of Science and Technology (KAIST)

Jun-Koo Kang Nanyang Technological University of Singapore

Inmoo Lee Korea Advanced Institute of Science and Technology (KAIST)

Sung Won Seo Ajou University

June 2017

* Phone numbers are +82-2-958-3415 (Dierker), +65-6790-5662 (Kang), +82-2-958-3441 (Lee), and +82-31-219-3688 (Seo). We are grateful for valuable comments from Tim Loughran, Sheridan Titman, and seminar participants at KAIST, the 2012 Allied Korean Finance Association Meetings, and the 2013 Annual Conference on Asia-Pacific Financial Markets. We also thank Byoung Hyun Jeon for his excellent research assistance. All errors are our own.

3

Risk Changes and External Financing Activities: Tests of the Dynamic Trade-off Theory of Capital Structure

Abstract We provide new insight into the relevance of the dynamic trade-off theory of capital structure by examining firms’ external financing activities following risk changes. Consistent with the prediction of the dynamic trade-off theory but inconsistent with the pecking order theory and the market timing explanation, we find that firms issue equity (debt) following risk increases (decreases). The results hold for subsamples of financially unconstrained firms and are robust to a variety of risk measures including stock return volatility, default probability, implied asset volatility, and adjusted Ohlson (1980) scores. Keywords: Capital structure theory, Dynamic trade-off, Pecking-order, Market timing, Risk change, External financing activities JEL Classification: G32, G33, G35

1

I. Introduction

There has been much debate about the relative importance and relevance of various capital

structure theories such as theories based on the trade-off between the tax benefits of debt and the

expected costs of bankruptcy (Kraus and Litzenberger (1973), Miller (1977)), adverse selection

costs (Myers and Majluf (1984)), and market timing (Baker and Wurgler (2002)). In particular, in

response to the debate on the relevance of the static trade-off theory,1 academics have turned to

dynamic versions of the trade-off theory. Fischer, Heinkel, and Zechner (1989), for instance, show

that when capital structure adjustments are costly, firms take recapitalization actions only when

the benefits of recapitalization outweigh its costs. 2 As emphasized by several studies, such

adjustment costs are nontrivial and can impose a serious challenge in testing the dynamic trade-

off theory of capital structure due to numerous assumptions required in the measurement of

adjustment costs.3

In this study, we evaluate the importance of the dynamic trade-off theory relative to two other

capital structure theories (pecking order and market timing theories) by examining firms’ external

financing decisions following changes in one of the key determinants of the trade-off theory, risk.

In spite of strong evidence on significant changes in firm risk over time (e.g., Campbell et al.

1 For example, Myers (1993) and Graham (2000) point out that a negative correlation between profitability and leverage ratios is the most critical evidence against the static trade-off theory, while Andrade and Kaplan (1998) argue that, from an ex-ante perspective, expected financial distress costs are likely to be small in comparison to the tax benefits of debt. 2 In the absence of adjustment costs, the trade-off theory suggests a positive relation between profitability and leverage ratios, as profitable firms are more likely to utilize bigger debt tax shields. However, firms facing high adjustment costs may find it optimal to remain inactive in the external financial market. Hennessy and Whited (2005) and Strebulaev (2007) demonstrate that adjustment costs in a dynamic trade-off theory can explain the observed negative relation between market leverage ratios and profitability and other empirical challenges. Welch (2004), however, argues that stock returns, not target leverage, drive capital structures. Leary and Roberts (2005) find evidence on the importance of adjustment costs but conclude that further work is needed to distinguish between the predictions of the dynamic trade-off theory and those of a pecking order theory modified for bankruptcy risk. 3 For example, while Strebulaev (2007) calibrates a multitude of parameters to generate meaningful cross-sectional variation, he still assumes that certain parameters are equal for all firms. As an example, he assumes that the present values of net payouts and book assets are scaled to an identical value for all firms at the initial date.

2

(2001), Ang et al. (2006), Adrian and Rosenberg (2008)) and the theoretical link between risk

changes and capital structure, empirical evidence on the effects of risk changes on a firm’s capital

structure decision is scarce.4 We fill this gap in the literature by using a firm’s external financing

activities as a setting for our study.

Focusing on external financing activities has several advantages. First, as we discuss later, it

allows us to test the importance and relevance of the three capital structure theories we consider

in our study because they yield quite different predictions about the optimal financing method

when firms enter external capital markets following risk changes. Second, it allows us to examine

the dynamic trade-off theory of capital structure without measuring adjustment costs since firms

that engage in external financing activities have already incurred adjustment costs. This avoidance

of adjustment cost measurement greatly reduces the challenge in testing the dynamic trade-off

theory of capital structure that previous studies have faced. Third, unlike many prior studies that

examine leverage decisions over time, our approach does not require the estimation of a target

leverage ratio, which is hard to define and difficult to measure. Instead of estimating target leverage

ratios, our approach utilizes the fact that, according to the dynamic trade-off theory, an increase

(decrease) in firm risk lowers (raises) its target leverage ratio, holding everything else constant.

Thus, if the firm decides to enter external capital markets to raise capital after experiencing risk

changes, it is likely to choose a financing method that moves it towards a lower (higher) target

4 Leland (1994) theoretically shows that increases in risk reduce debt capacity, while Chen (2010) points out that countercyclical variation in risk premiums, default probabilities, and default losses increases the present value of expected default losses, leading to lower optimal leverage ratios. Gormley, Matsa, and Milbourn (2012) empirically show that leverage is related to the change in firm litigation risk for a small set of firms. Numerous studies also show that leverage decreases with asset or return volatility (e.g., Harris and Raviv (1991), Ju, Parrino, Poteshman, and Weisbach (2005)). However, these studies do not explicitly examine how firms respond to changes in risk and change their capital structures accordingly.

3

leverage ratio.5 In performing our tests, we address potential problems arising from persistent

unobservable factors such as indirect bankruptcy costs by including firm fixed effects.

Although previous studies also examine a firm’s capital structure decision around its external

capital raising period,6 our approach differs from these studies in that we focus on the choice of a

firm’s external financing method following a change in risk. Under the dynamic trade-off theory,

a firm’s capital structure decision in response to a change in risk depends not only on its risk level,

but also on the (hard to observe) costs of raising external capital. When risk changes, the firm is

likely to raise external capital to move toward its optimal leverage as far as the benefits from such

a capital-raising activity is sufficiently greater than its costs.7 If an increase (decrease) in risk

lowers (raises) the target leverage ratio and a firm decides to enter external capital markets to raise

additional external capital, the dynamic trade-off theory predicts that the firm is more likely to

issue equity (debt) or buy back debt (equity) following an increase (decrease) in risk. Therefore,

risk increases (decreases) are expected to be associated with leverage-decreasing (increasing)

activities.8

5 Interestingly, many previous studies that estimate target ratios do not explicitly model risk as an explanatory variable. It is also important to note that, as shown by Chen and Zhao (2007) and Chang and Dasgupta (2009), the results in prior studies that firms pursue a target leverage ratio do not necessarily imply evidence in favor of the dynamic trade-off theory. Although the estimation of target leverage ratios is not required in our analysis, we nevertheless include estimated target leverage ratios as a control in the regressions to make our results comparable to those in prior studies. 6 For example, Hovakimian, Hovakimian, and Tehranian (2004) focus on the period during which firms issue both debt and equity. Danis, Rattl, and Whited (2014) pay close attention to the case when firms simultaneously issue a large amount of debt and pay out a large amount of internal capital through cash dividends or share repurchases, whereas Korteweg and Strebulaev (2013) examine cases of refinancing in which firms’ net debt (equity) issuance is greater than 5% of the book value of assets. 7 Costly adjustment of its capital structure represents a real option to a firm, and the value and optimal exercise timing of this option also depend on the firm’s risk level. Only if the benefits from raising (reducing) external capital are sufficiently large, the firm is expected to raise (retire) a type of external capital that allows it to move closer to its optimal leverage. 8 Previous studies focus mainly on adjustment costs associated with raising external capital. However, since forgoing the opportunity to invest in good projects that unexpectedly arrive after the reduction of capital can be considered a part of the adjustment costs, such adjustment costs can also be significant.

4

In contrast, the capital structure explanations by Myers and Majluf (1984) and Baker and

Wurgler (2002) do not assign an equally important and explicit role to firm risk. For example,

under the pecking order theory, a firm’s preference for debt over equity does not depend on its risk

level as far as the risk level does not affect the degree of the firm’s information asymmetry. An

increase in risk, however, may restrict the firm’s ability to raise debt. However, at least for a

subsample of firms that are financially unconstrained (and thus are unlikely to exhaust their debt

capacity when risk increases), the pecking order theory predicts that these firms will choose debt

as the source of their external capital whenever they raise external capital regardless of the

direction of risk changes.

The market timing argument of Baker and Wurgler (2002), which suggests that firms are more

likely to issue equity at times when their valuation (measured by the market-to-book ratio) is high,

also does not explicitly model firm risk and the complex interplay between dynamically changing

risk levels and market misvaluation. However, their argument implicitly suggests that as a firm’s

risk increases, its equity value tends to decrease,9 for example, due to an increase in the cost of

equity capital, and therefore, it is less likely to issue equity following an increase in its risk.10

The above three capital structure theories also have different predictions for firms’ external

capital reducing activities (i.e., buyback decisions) following risk changes. While the dynamic

trade-off theory predicts that, following risk increases (decreases), firms will buy back debt

(equity), the market timing theory predicts the opposite. Although Baker and Wurgler (2002) are

9 We empirically support this prediction later in our analysis. 10 One may argue that the change in risk affects only a firm’s fundamental equity value but not its misvaluation (i.e., difference between observed and fundamental values) and thus does not influence the firm’s incentives to take advantage of misvaluation. However, given managers’ general view that misvaluation is correlated with past stock return performance (Graham and Harvey (2001)), significant changes in prices following risk changes are likely to affect misvaluation (or at least managers’ perception of misvaluation of firms’ shares) and therefore, our prediction above is likely to hold.

5

not explicit about how firms buy back external capital in responses to risk changes, according to

their key argument that equity misvaluation drives firms’ financing decisions, firms are expected

to buy back securities that are undervalued (or relatively less overvalued). As we show later, the

market-to-book ratio tends to decrease (increase) following risk increases (decreases), all else

being equal. If managers believe that a firm’s equity is more likely to be undervalued (overvalued)

following an increase (decrease) in the market-to-book ratio, the market timing theory predicts that

firms repurchase equity following risk increases but retire debt following risk decreases.

On the other hand, the pecking order theory predicts that firms reduce debt in response to both

increases and decreases in risk. Under the pecking order theory, as Shyam-Sunder and Myers (1999)

argue, firms with financing surpluses prefer debt retirements over stock repurchases when they use

their surpluses to buy back securities, possibly to preserve their debt capacity or to avoid the

payment of high equity prices when they repurchase shares under asymmetric information. Thus,

the pecking order theory suggests that, irrespective of the direction of risk changes and whether

firms are financially constrained or not, firms prefer to retire debt when they have to reduce

external capital.11

In sum, the different predictions for the relation between risk changes and future external

financing activities discussed above allow us to evaluate the importance of the dynamic trade-off

theory of capital structure relative to other competing capital structure theories. Table 1

summarizes the preferred type of security that a firm issues (or buys back) as its risk changes under

each of the three competing capital structure theories.12 To provide supporting evidence on the

11 One caveat is that, due to asymmetric information, it is possible that firms issue overvalued equity or buy back undervalued equity if the benefits obtained from exploiting misvaluation are greater than the adverse selection costs. This possibility predicts that firms repurchase equity following risk increases but retire debt following risk decreases, the predictions similar to those of the market timing theory. 12 Risk changes are likely to affect the width of the target range of leverage under the dynamic trade-off theory but we do not explicitly address this issue since our approach focuses on external financing activities that occur after

6

effect of risk changes on capital structure under the dynamic trade-off theory, we perform a

simulation based on Strebulaev (2007). The result in Figure 1 shows a negative relation between

risk changes and the optimal leverage.13

Changes in other determinants of capital structure could also be very useful to understand a

firm’s optimal capital structure decisions. We focus on risk changes since, as discussed above, risk

changes play a different role in a firm’s choice of external financing methods under the three

different capital structure theories. 14 In contrast, these predictions are unclear for other

determinants of capital structure such as asset tangibility.15

To perform our analysis, we use both market- and accounting-based risk measures. We use

stock return volatility, default probability, and implied asset volatility estimates as market-based

measures of firm risk. In addition, despite the limitations of accounting-based measures

documented by Hillegeist et al. (2004), we use an adjusted Ohlson’s (1980) O-score (Franzen,

Rodgers, and Simin (2007)) as an alternative measure of risk. For each of these risk measures, we

investigate how changes in a firm’s risk are associated with its future external financing activities

and leverage changes.16 We find that all these risk measures are highly persistent during our

sample period. Since a firm would not necessarily need to react to risk changes if they were

considering adjustment costs and changes in the target ranges of leverage. 13 Appendix A describes the details on the procedures used to obtain simulation results in Figure 1. 14 Another reason for focusing on risk changes is that, unlike risk levels, they have been largely neglected in the literature. Moreover, unlike some other determinants that are important in the trade-off theory, such as bankruptcy costs, market-based measures of firm risk have the advantage of being observable at high frequency and displaying pronounced variation over time. 15 For example, increases in asset tangibility predict increases in leverage under the trade-off and pecking order theories due to increased debt capacity, while the market timing theory does not provide a clear prediction except that the market timing behavior is less likely to be observed since valuation becomes easier. 16 To the extent that these risk measures are affected by changes in leverage, contemporary changes in risk may be related to leverage changes. However, this is not a major concern in our paper since we examine external financing activities following risk changes instead of examining the contemporaneous relation between external financing activities and risk changes.

7

transitory, this result provides another rationale for why risk changes should be an important

consideration in the test of capital structure theories.17

Using a sample of firms listed on NYSE, Amex, or Nasdaq from 1972 to 2011, we find a

significantly positive relation between risk changes and leverage increasing external financing

activities. Specifically, we find that firms are more likely to issue equity (debt) when they raise

external capital following risk increases (decreases). Similarly, firms are more likely to reduce

external capital by buying back debt (equity) following risk increases (decreases). These results

are consistent with the predictions of the dynamic trade-off theory but inconsistent with those of

the pecking order theory and the market timing theory. In terms of economic significance, a one-

standard-deviation increase in annual changes in equity volatility (19%) leads to an increase in

firms’ net equity issue (or a decrease in firms’ net debt issue) of 0.55% of their total assets in the

following year, which in turn leads to a decrease in market leverage of 1.18%. Given that the mean

market leverage for the full sample is 38.8%, this effect is economically large and significant.

These results are more pronounced when we extend the observation window from one to three

years after the increase in risk and are also robust to using a variety of alternative risk measures

and controlling for endogeneity bias.

We also find that our results do not change when we limit our attention to subsamples of firms

facing fewer financial constraints, as measured by the Whited and Wu (2006) index of constraints

and the size-age (SA) index proposed by Hadlock and Pierce (2010). The pecking order theory

suggests that these firms particularly prefer to issue debt over equity because they are likely to

have easier access to debt markets due to their large debt capacity even after risk increases.

17 Results are unreported for brevity but available upon request.

8

Therefore, these results further support the dynamic trade-off theory but dispute the pecking order

theory.18

Moreover, we find that an increase in firm risk is associated with a fall in a firm’s valuation

as measured by the market-to-book ratio. Thus, according to the market timing theory, firms are

less likely to issue equity following risk increases since they may perceive their equity not being

overvalued. This result, together with evidence that firms are more likely to choose equity

financing following risk increases, further suggests that the dynamic trade-off theory explains a

firm’s capital structure decision following risk changes better than the market timing theory. In

sum, our results are most consistent with the implications of the dynamic trade-off theory but

inconsistent with the results of recent studies that document evidence against the trade-off theory

of capital structure.19

Our study contributes to the ongoing debate about firms’ capital structure decisions in several

ways. First, we propose a simple, clear way to test the relevance of the dynamic trade-off theory

relative to the pecking order theory and the market timing explanation. Unlike previous studies

that examine a firm’s capital structure decisions during its external capital raising period, we focus

on the relation between risk changes and external financing decisions, which allows us to minimize

the concern about mismeasuring adjustment costs and target leverage ratios.

Second, our study emphasizes the importance of changes in, not levels of, risk in capital

structure decisions. In spite of a strong theoretical link between risk changes and capital structure

18 Using Canadian data, Dong et al. (2012) show that firms time their equity issuance when they are not financially constrained. They further show that firms follow the pecking order only when their shares are not overvalued. 19 For example, Hovakimian, Kayhan, and Titman (2012) find that firms with a higher likelihood of substantial losses in bankruptcy tend to choose capital structures that have greater exposure to bankruptcy risk, which cannot be easily reconciled with the (static) trade-off theory.

9

and empirical evidence on time variation in risk, previous studies on capital structure focus mainly

on the relation between leverage and the level of risk.

Third, our findings add to the literature on a firm’s dynamic capital structure choice in which

the tax benefits of debt and expected bankruptcy costs play an important role. While some recent

studies show that the (static) trade-off theory does not have significant power in explaining the

cross-sectional variation of firms’ capital structure choices (e.g., Hovakimian, Kayhan, and Titman

(2012)), our study shows that the time-series variation of observed firms’ financing choices is

consistent with the dynamic trade-off theory. This result complements the findings of previous

studies on the dynamic trade-off theory, which use other approaches (e.g., structural estimation in

Hennessy and Whited (2005), simulation in Strebulaev (2007)) to explain persistent cross-

sectional patterns in firms’ capital structures.

The paper proceeds as follows. In Section II, we describe our key risk measures and control

variables and outline the methodology. Section III presents our main empirical results. In Section

IV we further examine the relevance of each capital structure theory by performing additional tests.

Section V summarizes and concludes.

II. Data and Methodology

A. Data

Our sample consists of all NYSE, Amex, or Nasdaq firms available on both CRSP and

Compustat between 1971 and 2011. As in Vassalou and Xing (2004), we start our sample period

in 1971 because there are insufficient debt-related financial data prior to 1971 in Compustat. All

the variables used in the paper are measured at fiscal year-ends. To focus on firms with meaningful

data, we exclude firms with a negative book equity value, a market-to-book asset ratio above 10,

10

or total assets below US$ 10 million. We also exclude utility (SIC 6000-6999) and financial (SIC

4900-4949) firms since their capital structure decisions are subject to regulatory constraints. In

addition, as in Kayhan and Titman (2007), we exclude firms with book leverage ratios above 100%.

Finally, to mitigate potential problems caused by extreme outliers, we winsorize all variables at

the 1st and 99th percentiles in each year, as in Leary and Roberts (2005) and Kale and Shahrur

(2007). Since our analyses require the measurement of changes in risk, we further delete the first

year of our sample period. Our final sample consists of 82,723 firm-year observations over the

period 1972-2011.

B. Risk Measures

To test the importance of firms’ risk changes in their capital structure decisions, we use various

risk measures. Roll (1984) argues that financial markets tend to incorporate information about

firms in a timely and forward-looking manner, suggesting that market-based risk measures are

good measures of firm risk and thus accurately capture time-series fluctuations in risk. Confirming

this argument, Hillegeist et al. (2004) show that as predictors of financial distress, market-based

risk measures, such as those obtained by fitting the Merton (1974) model, significantly outperform

accounting-based risk measures. Therefore, we focus on the following three market-based risk

measures as our key measures of firm risk: stock return volatility, default risk, and implied asset

volatility. The latter two are estimated on the basis of the Merton (1974) model.20 We also use a

20 In a dynamic capital structure trade-off theory, the underlying source of risk comes typically from the volatility of a firm’s assets, such as the volatility of its unlevered asset value (Fischer, Heinkel, and Zechner (1989)), or the volatility of cash flow generated from its assets (Goldstein, Ju, Leland (2001), Stebulaev (2007)). Although equity volatility and the probability of bankruptcy typically play a less prominent role in developing dynamic capital structure models, we still use them in our analyses since they are easy to measure and, in reality, can play an important role in a firm’s capital structure decision. For example, managers may pay a significant attention to the probability of bankruptcy when making borrowing decisions since a high level of the probability of bankruptcy jeopardizes their job security and related other benefits.

11

risk measure based on financial statements, namely, a version of Ohlson’s (1980) adjusted O-score

(Franzen, Rodgers, and Simin (2007)), as an alternative measure of firm risk.

First, the volatility of stock returns reflects uncertainty in the market value of a firm’s equity.

Although the volatility of a firm’s total assets may provide a better measure of its risk on theoretical

grounds, we focus on equity volatility in measuring firm risk due to the illiquidity of debt markets.

To measure stock return volatility, EquityVol, we calculate the standard deviation of 52 weekly

stock returns in each fiscal year and multiply it by the square root of 52 to annualize it. Due to the

residual nature of equity claims, the use of equity volatility may entail a potential endogeneity

problem when studying firms’ capital structure using market leverage since an increase in equity

risk reflected in the cost of equity is likely to decrease the market value of equity more than the

value of debt, thereby resulting in a contemporaneous increase in the leverage ratio. However, this

is not a major concern in our paper since we examine external financing activities following risk

changes instead of the contemporaneous relation between external financing activities and risk

changes. Furthermore, it should be noted that this effect goes in the opposite direction compared

with the effect predicted by the dynamic trade-off theory (i.e., firms reduce leverage when risk

increases). Thus, all else being equal, this endogeneity problem should make it harder for us to

support the dynamic trade-off theory. Finally, we also present results based on the book value of

leverage, which is not affected by this potential endogeneity problem.

Second, default risk, which is effectively a measure of the probability that a firm will enter

into costly financial distress, is measured based on the Merton (1974) model. We measure it,

Merton, in a similar way as in Vassalou and Xing (2004).

Third, implied asset volatility captures the uncertainty in asset values, not equity values, which

ultimately matter in avoiding financial distress. Another important reason to use asset volatility as

12

one of our risk measures is the fundamental role it plays in dynamic trade-off models. We compute

implied asset volatility, AssetVol, as the annualized standard deviations of daily changes in asset

values calculated in the process of estimating Merton’s default probabilities in each year (i.e.,

estimated 𝜎𝜎𝐴𝐴). To annualize the standard deviation of daily changes in asset values, we multiply it

by the square root of 252, the approximate number of trading days per year.

Finally, we use the adjusted O-score (1980), O-Score, as our measure of accounting-based risk.

This measure is estimated following Franzen, Rodgers, and Simin (2007), who propose the

adjustment method for net income, total assets, and total liabilities to avoid misclassifying

financially healthy R&D-intensive firms as financially distressed firms and to treat R&D in a more

conservative way. A detailed description on how Merton, AssetVol, and O-score are measured is

provided in Appendix C.

C. Dependent Variables

To examine the effects of risk changes on firms’ capital structure decisions, we use three

measures as dependent variables: leverage-increasing external financing activities (LIEFA [t+1]),

book leverage ratio, and market leverage ratio. As discussed above, the dynamic trade-off theory

predicts that firms adjusting external capital following a risk increase (decrease) are likely to

choose a financing method that helps decrease (increase) their leverage ratio. To capture this

external financial activity, we create a variable, leverage-increasing external financing activities,

LIEFA [t+1], as one of our key dependent variables of interest. LIEFA [t+1] is computed as the

scaled sum of external financing activities that increase a leverage ratio (i.e., issue of new debt and

repurchase of equity) minus those that reduce a leverage ratio (i.e., reduction of debt and issue of

13

new equity).21 The reason for using LIEFA [t+1] is as follows. If two otherwise similar firms differ

in their adjustment costs and investment opportunities, it is possible that one firm prefers to

respond to a risk increase by issuing equity, while the other firm finds it more cost-effective to buy

back debt in order to reduce its leverage. LIEFA allows us to verify whether firms respond to

changes in risk in a manner consistent with the dynamic trade-off theory, as both of the

aforementioned firms will have negative LIEFA.

Specifically, LIEFA is measured as the ratio of the difference between net long-term debt issue

and net equity issue in year t+1 to lagged total assets. The difference between net debt issue and

net equity issue is calculated as long-term debt issuance (DLTIS) minus long-term debt reduction

(DLTR) minus sale of common and preferred stocks (SSTK) plus purchase of common and

preferred stocks (PRSTKC). LIEFA [t+2] and LIEFA [t+3] are calculated by summing LIEFAs over

two and three years starting from year t+1, respectively.22

As alternative dependent variables, we use the book (market) leverage ratio, measured as the

ratio of the book value of debt to the book (market) value of total assets. The market value of total

assets is computed as total assets (AT) minus the book value of equity plus the market value of

equity, and the book value of debt is computed as total assets minus the book value of equity. As

in Kayhan and Titman (2007), the book value of equity is estimated as total assets minus the sum

21 Whether a positive value of LIEFA indeed leads to an increase in leverage depends on both the original level of leverage and other factors such as retained earnings, deprecation (book leverage), or stock returns (market leverage). For example, suppose that a firm with a debt-to-equity ratio of 10% raises 2% of existing equity value (E) through equity issuance and 1% of existing equity value through debt issuance. After issuance, this firm’s debt-to-equity ratio will increase from 10% to 10.78% (= (0.1× E + 0.01×E) / (E +0.02×E) = 0.11/1.02), but it will have a negative LIEFA. This is one of several reasons why the relation between external financing decisions and leverage changes is known to be complex (Welch (2011)). Therefore, we also use changes in market and book leverage ratios as alternative dependent variables in our analyses to check whether the choice of external financing method is in line with the direction of changes in leverage ratios. 22 As an alternative way to measure leverage-increasing external financing activity over multiple years, we define LIEFA [t+2] (LIEFA [t+3]) as the ratio of the difference between net long-term debt issue and net equity issue during the year t+1-year t+2 (t+3) period to total assets in year t. In unreported results, we find that the qualitative results based on this alternative measure are similar to those reported in the paper.

14

of total liabilities (LT) and the liquidation value of preferred stock (PSTKL) plus deferred taxes,

investment credit (TXDITC), and convertible debt (DCVT). When PSTKL is not available, the

redemption value (PSTKRV), or the carrying value (PSTK) if PSTKRV is not available, is used.23

The market value of equity is measured at the fiscal year-end.

D. Regression Specification and Control Variables

To test whether firms engage in leverage-increasing external financing activities following

changes in risk, we run the following ordinary least squares (OLS) panel regression model that

controls for various factors that affect a firm’s capital structure decision:

titititi

titititi

tititititististi

FirmD YearDLdefB CRdummyCRdef FDEBITDLTA

r MBMBRiskRisk =LevorLIEFA

,,13,12,11

10,9,8,7,6

,51,4,31,2,10,, )(

εβββ

βββββ

ββββββ

++++

+++++

++∆++∆+∆ −−++

, (1)

Our main independent variables of interest in Eq. (1) are the change in risk, ∆𝑅𝑅𝑅𝑅𝑅𝑅𝑅𝑅𝑖𝑖,𝑡𝑡, and

lagged risk level, 𝑅𝑅𝑅𝑅𝑅𝑅𝑅𝑅𝑖𝑖,𝑡𝑡−1. The other variables are well known to explain firms’ capital structure

and external financing choices and are included as controls. As shown in previous studies (e.g.,

Loughran and Ritter (1995)), a firm’s financing decision may depend on its market valuation,

which also affects its capital structure. To measure the market valuation of the firm, we estimate

the market-to-book total assets ratio, MB. Given that changes in firm valuation (or changes in

investment opportunities) can also affect firms’ external financing decisions and changes in

leverage, we also control for changes in MB, MB Change (Baker and Wurgler (2002)).24

23 Annual Industrial Compustat data variable names are in parentheses. 24 In Eq. (1), for risk and MB, we use both their changes and lagged values. However, for LTA, FD, r and EBITD, we

15

Welch (2004) demonstrates that past stock returns are a driver of market leverage, which in

turn may also affect financing decisions in subsequent periods. Thus, we include one-year stock

return (r) during the fiscal year in our regression.

Size can affect firms’ financing decisions in several ways. For example, large firms are more

likely to be mature and diversified, and have better access to capital markets. They are also less

subject to information asymmetry, which, according to the pecking order theory, may help reduce

the extent of price drops if the firm issues equity. Finally, large firms’ information is easily

available to outside investors and they are subject to fewer trading frictions, which is likely to

reduce the likelihood of stock price misvaluation in the stock market, affecting the potential for

market timing. Thus, to control for these effects, we include the natural logarithm of total assets

(AT), LTA, in the regressions.

According to the dynamic trade-off theory, a firm’s profitability can be an important

determinant of its capital structure since profitable firms can take advantage of larger debt tax

shields. Profitability is also important under the pecking order theory, which suggests that

profitable firms are less likely to depend on external financing. Therefore, we control for

profitability, EBITD, defined as earnings before interest, tax, and depreciation (OIBDP) over total

assets at the beginning of the fiscal year in the regressions.

How leverage changes over time and what types of capital firms choose also depend on the

total amount of external financing raised. To measure the latter, similar to Frank and Goyal (2003),

we define a firm’s financial deficit, FD, as the ratio of the sum of net equity and long-term debt

use only their values in year t and do not include their changes in the regression. We include changes in MB since they are related to changes in both firm valuation (market timing theory) and investment opportunities (pecking order and dynamic trade-off theories) and thus are relevant to all three capital structure theories considered in the paper. However, in unreported tests, we repeat our analyses using both levels of and changes in LTA, FD, r, EBITD, risk and MB in the regressions and find qualitatively similar results as those reported in the paper.

16

issues to total assets at the beginning of the year (i.e., [sale of common and preferred stock (SSTK)

– purchase of common and preferred stock (PRSTKC) + long-term debt issuance (DLTIS) – long-

term debt reduction (DLTR)] divided by AT in year t-1).

Graham and Harvey (2001) and Hovakimian, Kayhan, and Titman (2009) show that firms pay

close attention to their target credit ratings. This finding suggests that any gap between target and

actual credit ratings is likely to induce firms to adjust their capital structure in an effort to maintain

their credit ratings at target levels. As a credit rating is also closely related to firm risk, we need to

control for it in our regression. We estimate a firm’s target credit rating, TRating, by calculating

the fitted value from an ordered probit regression estimated in each year as in Hovakimian, Kayhan,

and Titman (2009). The details of this regression model and the results from the ordered probit

regression used to estimate the target credit rating in 2011 are presented in Appendix D.25 We

define credit rating deficit (CRdef) as the difference between TRating and the actual credit rating

and include it in the analyses. Since there are many firms that do not have available credit rating

information, we include a dummy variable, CRdummy, to indicate those firms with available credit

rating information.

Although our approach does not require us to measure target leverage ratios in testing the

dynamic trade-off theory of capital structure and, as discussed above, there is a debate on the

existence and measurement of target leverage ratios, we control for these ratios in our analysis to

facilitate comparison with previous studies (e.g., Hovakimian, Opler, and Titman (2001)). We

estimate target leverage ratios (Tlev) using a similar method to that in Kayhan and Titman (2007),

which is described in Appendix E. We measure book leverage deficit, LdefBt, as the difference

between the target book leverage ratio and the actual book leverage ratio, TlevBt – LevBt. If a firm

25 Results for other years are available upon request.

17

pursues a target leverage ratio, we expect that the firm’s financing and capital structure decisions

depend on how far it is away from its target (i.e., the leverage deficit).26 A non-zero leverage

deficit at time t can arise because the firm may have deviated from its target capital structure in

the past or because the target leverage ratio has shifted over the last year. Thus, lagged leverage

deficit and changes in target leverage that are used in the previous studies are subsumed in a single

variable here for the sake of simplicity.

Despite the importance of risk as a determinant of the optimal target leverage ratio in the

dynamic trade-off theory, previous studies have often not explicitly included firm risk in their

estimation of target leverage ratios. The focus of our study is not to propose a marginal

improvement in estimating target leverage ratios, but to test if firms rationally respond to changes

in risk levels in a way which is consistent with the dynamic trade-off theory. Thus, we follow the

method used in previous studies and do not include risk in estimating target leverage ratios to make

the comparison with these studies easier.

It should be also noted that some of our independent variables such as EBITD and MB are also

used as inputs to calculate other control variables. For instance, EBITD is included in the

calculation of FD and LdefB, and MB is included in LdefB. This inclusion is consistent with the

literature (e.g., Kayhan and Titman (2007)) and ensures that our results are not driven by a simple

correlation between risk changes and other variables that are known to be important determinants

of capital structure decisions.

Finally, we control for year and firm fixed effects by using year and firm dummy variables,

YearD and FirmD, respectively. Controlling for firm fixed effects mitigates the endogeneity

26 We calculate both market and book leverage deficits and use them in the regression analyses. However, since the results using these two leverage deficit measures are qualitatively similar, we report only the results based on book leverage deficits in the paper.

18

concern that our results are driven by omitted unobservable firm characteristics. However, as

shown in Petersen (2009), including firm dummy variables is effective only if firm fixed effects

are permanent. Therefore, as an additional cautionary treatment, we use firm-clustered standard

errors in calculating t-statistics, as suggested by Petersen (2009). All other variables are defined in

previous sections and are also summarized in Appendix B.

III. Empirical Results

A. Summary Statistics

Table 2 shows the summary statistics for our sample firms. The average total assets and market

capitalization are $2.07 billion and $2.04 billion (adjusted to 2011 purchasing power using the

Consumer Price Index), respectively. The average annual stock returns and the profitability

(EBITD) are 18.2% and 14.5%, respectively. The mean market (book) leverage is 38.8% (44.2%)

while the mean annual change in market (book) leverage is 0.8% (0.7%), indicating that during

our sample period, on average, firms have slightly increased their leverage ratios. The mean book

leverage deficit (LdefB) is 1.4%, suggesting that our sample firms’ book leverage ratios are on

average about 1% lower than their target leverage ratios.

The average LIEFA[t+1] is 0.54% while the median LIEFA[t+1] is -0.22%. These results

suggest that on average, firms issued more debt than equity during our sample period, albeit the

median suggests the opposite. The average (median) financial deficit, FD, is 4.4% (0.0%),

indicating that the average (median) annual total amount of external financing is around 4% (0%)

of total assets at the beginning of each year. Since the sum of FD and LIEFA[t+1] represents twice

19

the amount of net long-term debt issuance, on average, firms raised about 2.5% (≈ (4.4% +

0.54%)/2) of total assets through net long-term debt issuance per year.27

The average (median) annual equity volatility, implied annual asset volatility, default risk, and

adjusted-Ohlson’s score are, respectively, 53% (46%), 50% (41%), 2.7% (0.0%), and -1.6 (-1.6).

The average (median) annual changes in market-based risk measures vary from -0.56% (-0.74%)

to 0.19% (0.00%) and the annual average (median) change in Ohlson’s score is 0.02 (-0.01).

B. Correlation and Univariate Analyses

In Table 3, we report the correlations among changes in leverage, external financing activity,

the level of risk, and the change in risk used in our analyses. We find that risk change variables are

significantly negatively correlated with changes in market leverage and LIEFA in the following

year, even though the magnitudes of their correlation coefficients are not high. The correlations

between risk changes and book leverage changes in the following year, and their significance vary

across risk measures.

We also find that our risk change variables are significantly positively correlated with each

other, although the magnitudes of the correlation coefficients vary across the pairs of risk change

measures. There are also significant positive correlations among the levels of our risk measures. It

is noteworthy that the correlations between our risk measures are typically lower than one,

suggesting that consistent with our previous discussion, they capture different aspects of firm risk.

All three market-based risk measures are only weakly, albeit significantly, correlated with the O-

score, an accounting-based risk measure, perhaps due to the latter’s lack of timely updates.

27 This number is a rough estimation because FD is measured as the sum of net equity and net debt issuances in year t whereas LIEFA[t+1] is measured as the difference between net debt and net equity issuances in year t+1.

20

Financial deficit, FD, is significantly positively correlated with changes in market and book

leverage ratios in the following year, suggesting that after raising external capital, leverage ratios

tend to increase in the following year. However, it is negatively correlated with LIEFA in the

following year. We do not find any consistently strong correlation between FD and risk change (or

risk level) variables. MB and stock returns are significantly positively correlated with changes in

market leverage in the following year, but they are significantly negatively correlated with changes

in book leverage and LIEFA in the following year. Finally, MB and stock returns are significantly

negatively correlated with risk change variables, consistent with the conjecture that holding

everything else constant, stock prices decrease as risk increases. In untabulated tests, we check the

correlations between risk change (level) measures and other firm characteristics reported in Table

3 and find that none of the correlations is high enough to cause multicollinearity problems in our

subsequent empirical analyses.

In Table 4, we report univariate results for changes in MB, LIEFA, and leverage ratios for each

group formed on the basis of firms’ annual risk changes. In each year, firms in the top 20%, the

middle 60%, and the bottom 20% of each risk change measure are classified as “High risk change,”

“Middle risk change,” and “Low risk change” firms, respectively.

The number of observations in each category is shown in the first row, and the average change

in risk is shown in the second row. As expected, changes in the risk of “High risk change” firms

are significantly greater than those of “Low risk change” firms, as shown in the last column.

Consistent with the results in Table 3, MB decreases significantly more for “High risk change”

firms than for “Low risk change” firms, indicating that, on average, increases in risk lower firm

valuation.

21

The next three (last three) rows show the average LIEFA and changes in leverage ratios for

each group during the one-year (three-year) period following risk changes. As shown in the last

four columns, where the differences of the averages between “High risk change” and “Low risk

change” groups are presented, we find that relative to firms experiencing a low change in equity

volatility (our main risk measure), firms experiencing a high change in equity volatility are

significantly less likely to engage in external financing activities that increase their leverage. These

results hold both for the subsequent year (t+1) as well as over the following three years (t+3). As

a result, the average change in market leverage for “High risk change” firms over the subsequent

one-year (three-year) period is 1.19 (2.46) percentage points lower than the average change made

by “Low risk change” firms. This difference is significant at the 1% level. The same pattern is

observed when we replace equity volatility with the estimated likelihood of default. With respect

to the other risk measures, although we find that the effect has consistently the same sign, it is not

always statistically significant. Overall, the results in Table 4 suggest that “High risk change” firms

engage in less leverage-increasing external financing activities than “Low risk change” firms,

consistent with the prediction of the dynamic trade-off theory.

C. Regression of LIEFA and Changes in Leverage on Risk Change Variables

Table 5 presents the results from panel regressions of LIEFA and changes in market (book)

leverage in the following year on changes in risk. The dependent variables are as follows: LIEFA

in columns (1) through (4), changes in book leverage ratios in columns (5) through (8), and changes

in market leverage ratios in columns (9) through (12). T-statistics based on clustered standard

errors at the firm level are reported in parentheses. In general, consistent with the predictions of

the dynamic trade-off theory, we observe significantly negative associations between risk changes

22

and both LIEFA and changes in leverage ratios in the following year. The results in column (1)

suggest that a one standard deviation increase in annual changes in equity volatility (19%) leads

to a decrease in LIEFA of 0.55% (= 0.19 × -0.029) in the following year, which is close to the

average absolute value of LIEFA for the full sample (0.54%). Such an increase in risk reduces book

leverage by 0.21% (= 0.19 × -0.011, see column (5)) and market leverage by 1.18% (= 0.19 × -

0.062, see column (9)) on average, both of which are significant at the 1% level.

Managers may be concerned not only about large increases in risk but also about high risk

levels. Supporting this view, we find that the risk level at the beginning of the year is significantly

negatively related to LIEFA and changes in leverage in the following year. The results in columns

(1), (5), and (9) indicate that a one standard deviation increase in the level of equity volatility (29%)

leads a firm to decrease LIEFA by 0.81% (= 0.29 × -0.028) and market [book] leverage by 1.77%

(= 0.29 × -0.061) [0.41% (= 0. 29 × -0.014)] in the subsequent year.28

Columns (2) to (4), (6) to (8), and (10) to (12) provide the results for the alternative risk

measures we consider. Overall, the results confirm our intuition that pronounced increases in risk

as well as high risk levels lead firms to adopt external financing choices that serve to decrease

leverage and that these choices indeed result in lower leverage ratios.

Turning to the control variables, consistent with previous studies, we find that issue activity

(FD) and leverage changes are only weakly correlated and often go in opposite directions (Welch

(2011)). In addition, we find that, as pointed out by Chen and Zhao (2007) and Chang and Dasgupta

(2009), changes in the leverage ratios of firms with high or low leverage ratios do not necessarily

28 Interestingly, the coefficients on lagged risk levels in columns (1), (2) and (9) are very similar to those on risk changes. There is no theoretical reason for this to be the case, and indeed, unreported results show that this is no longer true when we analyze LIEFA or leverage changes over two- and three-year windows following a risk change.

23

match with their financing choices: for example, a firm with 10% leverage needs to issue at least

nine times more equity than debt in order to reduce its leverage ratio.

It should be also noted that the dependent variables used in our study (i.e., changes in future

leverage) are different from those in most previous studies (i.e., levels of current or future leverage

ratios), and this could lead to differences in results between the studies. For example, consistent

with Hovakiminan, Opler and Titman (2001), we find that although profitability is negatively

associated with changes in book leverage, it is positively associated with LIEFA. We also find that

the change in the market-to-book ratio is positively associated with changes in market leverage

but negatively associated with LIEFA. In addition, the coefficients on size are significantly negative

for changes in book leverage but significantly positive for both LIEFA and changes in market

leverage. Although the coefficients on the control variables do not always have consistent signs in

explaining changes in book leverage, changes in market leverage, and LIEFA, we find consistent

results across different dependent variables: The coefficients on risk changes are significantly

negative for LIEFA and leverage changes, indicating that firms experiencing risk increases tend to

engage in fewer leverage-increasing financing activities in the following year.

In Table 6, we examine whether the relation between risk changes and leverage changes are

consistent across positive and negative risk changes. We replace the risk change variables used in

Table 5 with the maximum (minimum) of risk change and zero for positive (negative) risk changes

(i.e., positive risk changes = max (risk change, 0) and negative risk changes = min (risk change,

0)). We use this approach since firms with positive and negative risk changes may face different

levels of difficulty in raising capital; for example, while firms that experience a decrease in risk

may find it relatively easy to increase leverage by buying back shares or issuing debt, firms that

experience an increase in risk may face greater challenges in reducing leverage by issuing equity

24

or buying back debt. However, the results in Table 6 show that our key findings are generally

consistent across positive vs. negative risk changes. With respect to our main risk measure,

EquityVol, columns (1), (5) and (9) document nearly identical regression coefficients for positive

and negative risk changes. The same pattern generally holds with respect to other risk measures

except that the result for negative risk changes based on O-score is the opposite of the previous

results for book leverage changes. Overall, these results rule out our concern that the results in

Table 5 are driven by an inherent asymmetry in firms’ ability to respond to positive vs. negative

changes in risk.29

Due to adjustment costs, firms may not adjust their capital structure immediately after risk

changes. As documented in Leary and Roberts (2005), it can take more than a year before firms

adjust their capital structures. To address this issue, in Table 6, we also examine the relation

between risk changes in year t and external financing activities over year t+1 to year t+2 (t+3).

Our results are indeed consistent with the argument that the speed of firms’ capital structure

adjustment is slow. We find that the association between risk changes and future external financing

(leverage decisions) becomes more pronounced and consistent across alternative risk measures

over longer horizons. To facilitate comparison with our results in Table 5, consider a firm

experiencing a one standard deviation increase in the change of equity volatility: Over the next

three years, this firm decreases LIEFA by 0.86% (= 0.19 × - 0.045). At the same time, its book and

market leverage ratios decrease by 0.63% (= 0.19 × - 0.033) and 2.01% (= 0.19 × - 0.106),

respectively. Adjusted R-squared also increases and the results become more consistent across four

29 In untabulated tests, we repeat the regression analyses of LIEFA[t+1] reported in Table 5 after decomposing LIEFA into two parts, Net Debt Issues[t+1] and Net Equity Issues[t+1] to examine which component drives the results. We find that the results are mostly driven by Net Debt Issues[t+1]. For Net Debt Issues[t+1], the coefficients on the change in risk are significantly negative except for AssetVol, while for Net Equity Issues[t+1] × -1, the corresponding coefficients are significantly negative only when O-Score is used as a risk measure.

25

risk measures as we extend the time horizon to measure the external financing and leverage

changing activities.

In particular, with respect to AssetVol, the main underlying risk measure of Fischer, Heinkel,

and Zechner (1989), we find that consistent with the dynamic trade-off theory of capital structure,

its increase leads firms to significantly reduce their book (column (6)) and market leverage

(column (10)) in subsequent years. Interestingly, however, these reductions do not appear to be

driven by external financing choices (column (2)).

D. Robustness Tests

In this subsection we examine whether our results are robust to controlling for potential

endogeneity problems not captured by firm fixed effects. One concern with our results in the

previous section is that the results may be driven by spurious correlations between risk variables

and other well-known determinants of optimal capital structure discussed above. To address this

concern, we first regress the risk variables on several determinants of capital structure as follows:

titititititi

titititititi

FirmD YearDLdefB EBITDr CRdummyCRdef FDMBMBLTA =Risk

,,11,10,9,8,7

6,5,41,3,2,10,

εββββββββββββ

++++++

++++∆++ − , (2)

where Risk is one of four risk variables used in Table 4 (equity volatility (EquityVol), implied asset

volatility (AssetVol), Merton default risk (Merton), and adjusted O-score (O-Score)); MB is the

market-to-book asset ratio; FD is financial deficit; CRdef is credit rating deficit; CRdummy is an

indicator for those firms with available credit rating information; r is the one-year buy-and-hold

stock return; EBITD is profitability; LdefB is the book leverage deficit; YearD is a year indicator;

26

and FirmD is a firm indicator. See Appendix B and our discussion above for precise definitions of

each variable.

We then use the residuals from the above panel regressions as the measures of firms’ residual

risk levels. Residual risk changes are subsequently measured as the changes in the residuals over

two consecutive years. This approach allows us to mitigate the concern that our previous risk

variables simply capture other determinants of firms’ capital structure.30

The results are presented in Table 7. In the first three rows, we report the results for the one-

year period following risk changes and in the next three rows, we report the results for the three-

year period following risk changes. We find that the results are similar to those presented in Tables

5 and 6. Thus, our results in the previous sections are unlikely to be driven by close correlations

between our risk measures and other control variables.31

IV. Pecking Order or Market Timing?

While the results thus far are generally consistent with the dynamic trade-off theory, in this

section, we further examine the relevance of the pecking order theory and the market timing theory

in explaining our results. According to the pecking order theory, firms prefer to issue debt over

equity and therefore would issue debt even after risk increases unless such increases in risk

significantly constrain their ability to borrow. However, when firms are financially constrained,

30 The common approach to address the endogeneity problems is to have either an exogenous event that exogenously changes firm risk but that does not affect firm leverage in any other way, or an instrumental variable (IV) that is related to the change in firm risk but unrelated to firm leverage. However, such an event or an IV that is related to risk changes but truly exogenous to firm leverage is hard to come by in our analysis. Nevertheless, we reestimate the regressions using a two-stage least squares regression in which we use the industry median risk change and the industry lagged risk level as the IVs for risk change and lagged risk level, respectively. Industry is defined based on the two-digit SIC codes. We find that the results for three-year horizons are qualitatively similar to those reported in Table 5 except for changes in book leverages. We admit the possibility that these IVs may not satisfy the exclusion condition of the IVs. 31 In untabulated tests, as an alternative way to control for time-invariant omitted firm characteristics, we use the first-difference method by replacing all dependent and explanatory variables with those measured using the change, and reestimate all regressions reported in Table 5. We find that the qualitative results do not change.

27

they may have difficulty in accessing debt markets after risk increases. Therefore, focusing only

on the subsample of financially unconstrained firms instead of the full sample allows us to

unambiguously test the importance of the pecking order theory relative to the dynamic trade-off

theory (which predicts the issuance of equity following risk increases). We use the Whited and Wu

index of constraints (Whited and Wu (2006)) and the size-age (SA) index proposed by Hadlock

and Pierce (2010) to identify firms that are less likely to be financially constrained.32

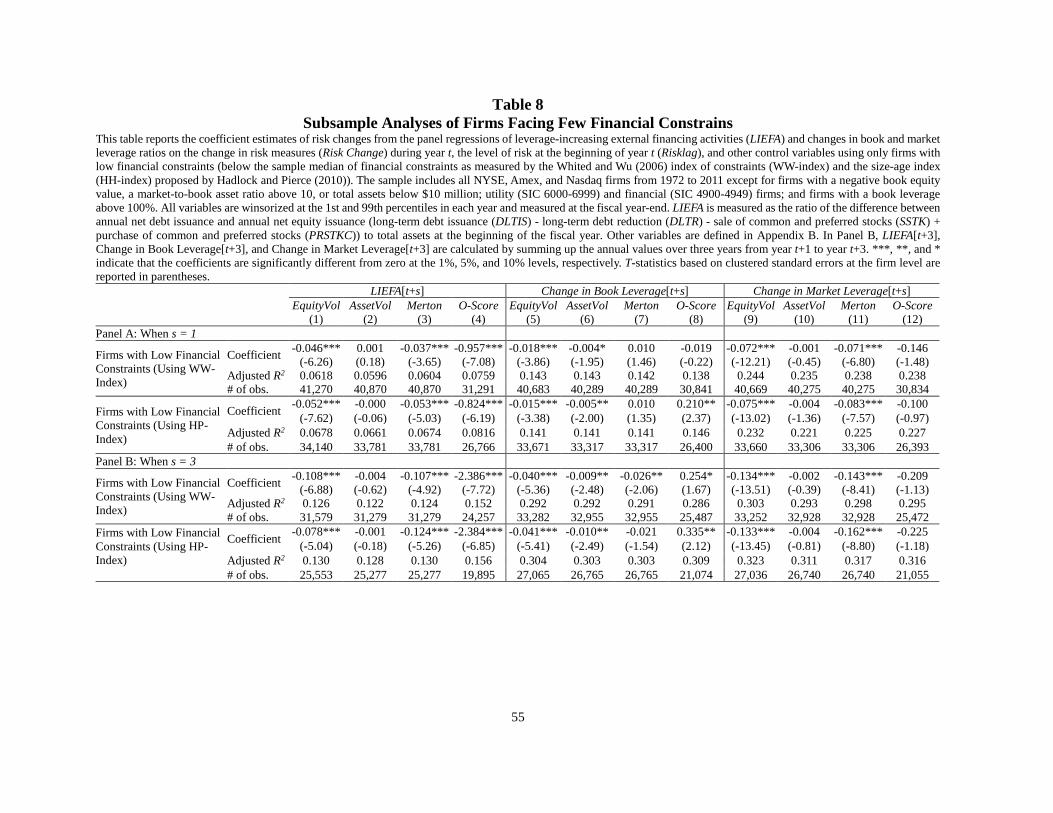

Table 8 reports the results using firms with below-median values of financial constraints as

measured by these methods. Panel A shows the effect of changes in risk on LIEFA and changes in

market (book) leverage in the following year. The results are similar to those reported in Table 5.

When we extend the observation window for the dependent variables from one to three years

(Panel B), we again observe similar results.33

In summary, the results in Table 8 are qualitatively similar to those using the full sample,

which is more consistent with the predictions of the dynamic trade-off theory than the pecking

order theory. In particular, our results for LIEFA presented in columns (1) – (4) show that less

financially constrained firms tend to be less likely to make leverage-increasing security choices

following risk increases, which is hard to reconcile with the pecking order theory.

32 Following Whited and Wu (2006) and Hennessy and Whited (2007), the Whited and Wu index is constructed as – 0.091 × cash flow over total assets – 0.062 × indicator set to one if the firm pays cash dividends, and zero otherwise + 0.021 × long term debt over total assets – 0.044 × logarithm of total assets + 0.102 × average industry sales growth, estimated separately for each three-digit SIC industry and each year – 0.035 × firm sales growth, with all variables defined as in Whited and Wu (2006). Hadlock and Pierce (2010) use a size and age index to measure financial constraints, which is calculated as 0.737 × size + 0.043 × size2 – 0.040 × age, where size is the log of inflation-adjusted book assets (capped at $4.5 billion) and age is the number of years (capped at thirty-seven years) the firm has been on Compustat. 33 These results are consistent with those of Fama and French (2005). They find that most firms issue or retire equity each year and that typical equity issuers are healthy firms not under financial difficulties, contradicting with the pecking order theory. They conclude that equity issuing decisions of more than half of their sample firms violate the pecking order.

28

Next, to further test the relevance of the market timing theory in explaining firms’ capital

structure decisions, we examine whether a firm’s market valuation (MB ratio) is indeed affected

by its risk changes. The evidence presented thus far is inconsistent with the market timing

explanation as far as MBs decrease as risk increases. Although the correlation results presented in

Table 3 confirm this view, we conduct a formal test to examine whether MB actually increases as

risk increases after controlling for several variables that affect firm valuation.

The results are reported in Table 9. We regress the change in MB on several variables including

i) risk change (Risk Change), ii) risk level at the beginning of the year (Risklag), iii) MB at the

beginning of the year (MBlag), iv) size (LTA), v) profitability (EBITD), and vi) year and firm fixed

effects. The results show that risk changes are indeed significantly negatively related to

contemporaneous changes in MB, supporting the conjecture that risk increases lead to decreases

in MBs. Therefore, our main results showing that firms tend to engage less LIEFA following risk

increases are inconsistent with the market timing explanation.

Finally, we divide the firms into four subgroups according to whether they have positive or

negative FD in year t+1 (i.e., whether they raise or reduce external capital) and whether they

experience an increase or a decrease in risk and examine whether the relations between risk

changes and future LIEFA (changes in leverage ratios) differ across these subgroups by estimating

the regression separately for them. As summarized in Table 1, the three capital structure theories

we consider predict that firms choose different types of securities to achieve their external

financing goals depending on their need to raise or reduce external capital following risk changes.

The results are reported in Table 10. We find that consistent with the dynamic trade-off theory, the

coefficient estimates on risk change variables that are significant have a negative sign in the

29

majority of subgroups.34 Moreover, we find the negative coefficient on risk changes not only for

capital raising (positive FD) subsamples but also for capital reducing (negative FD) subsamples

where we expect the negative coefficient only under the dynamic trade-off theory even among

financially constrained firms. This negative coefficient suggests that firms tend to decrease their

book and market leverage ratios when they experience an increase in risk, which is consistent with

the dynamic trade-off theory.

In sum, the results in Tables 8, 9, and 10 indicate that our main results of significant negative

relations between risk changes and LIEFA and between risk changes and changes in leverage ratios

are most consistent with the dynamic trade-off theory of capital structure rather than the two

alternative theories of capital structure.

V. Summary and Conclusion

Although there has been much debate over the importance of various capital structure theories

in explaining firms’ actual capital structure decisions, the evidence in the literature is not

conclusive. In this paper, we focus on one of the most important factors that affect firms’ capital

structure decisions, namely, risk, and examine how firms determine their capital structure in

response to changes in risk. More specifically, we use various measures of risk, including stock

return volatility, default risk, implied asset volatility, and an adjusted O-score, and study which

theory of capital structure among the dynamic trade-off theory, the pecking order theory, and the

market timing theory explains firms’ external financing decisions best in response to risk changes.

34 However, there are a few cases where the results are more consistent with alternative theories. For example, the only significantly positive coefficient on the risk change variables in the regression of LIEFA [t+3] is found for firms with a negative FD in column (2), where risk is measured by implied asset volatilities. This result is more consistent with the market timing explanation.

30

To the extent that firm risk fluctuates over time and risk affects optimal leverage ratios,

focusing on the relation between risk changes and future external financing activities allows us to

obtain new insights into the importance of these capital structure theories. Our approach also

allows us to test the relevance of capital structure theories without measuring adjustment costs

since we focus on the group of firms that have already undertaken external financing activities. In

addition, our approach does not require estimating a target leverage ratio since it utilizes the fact

that, holding everything else constant, an increase (decrease) in risk tends to lower (raise) the target

leverage ratio.

Consistent with the prediction of the dynamic trade-off theory of capital structure, our

simulation results show that the optimal leverage is negatively related to risk changes. More

importantly, we find that firms prefer to issue equity (debt) over debt (equity) following risk

increases (decreases). These findings are robust to using a variety of risk measures.

Our results also hold when we limit our attention to a subsample of firms facing few financial

constraints for which the pecking order theory is more likely to be applicable. In addition, we find

that an increase in a firm’s risk is associated with a fall in its equity valuation as measured by the

market-to-book ratio, indicating that risk increases reduce the likelihood of the firm’s

overvaluation. This result further suggests that the dynamic trade-off theory explains a firm’s

capital structure decisions in response to changing risk levels better than the market timing theory.

Finally, when we repeat our regression analyses separately for subsamples classified according to

whether firms raise or reduce external capital and whether they experience an increase or a

decrease in risk, we find that the coefficient estimates on risk change variables are significantly

negative in the majority of subsamples. These results further support the dynamic trade-off theory.

31

Overall, our study shows that the dynamic trade-off theory best explains the evolution of

capital structures over time in relation to changes in risk, thus highlighting its importance in

explaining firms’ external financing and capital structure decisions over time.

32

Appendix A. Numerical Example of the Relation between Optimal Leverage and Risk

Changes

In Figure 1, to better understand the relation between the optimal leverage ratio and risk

changes in a dynamic trade-off theory setting, we present simulation results based on Strebulaev

(2007). This appendix describes the details on the procedures used to obtain these simulation

results. Specifically, in Table I of his paper, Strebulaev (2007) states that the optimal market

leverage ratio (ML) decreases as the volatility of firm’s cash flow (σ) increases, but does not

provide any details on the magnitudes of the impacts of risk changes on optimal leverage ratios.

Using the mean parameter values reported in Table II of Strebulaev (2007), we examine how much

a firm’s optimal market leverage ratio changes as the volatility of its cash flow changes around the

sample mean (i.e., 25.5%).

Similar to Goldstein, Leland and Ju (2001), Strebulaev (2007) assumes that firms will retire

their outstanding debt at par and sell a new, larger debt if their values increase, thus reaching an

upper refinancing boundary (U). However, if firms perform poorly and reach a liquidity barrier

(L), they will sell a fraction (1 – k) of assets to resolve financial distress. Following asset sales,

these poorly performing firms may recover and reach an upper refinancing boundary (LU) or they

may need to inject new equity capital. Equity holders will optimally default if the firm’s condition

continues to worsen and reaches a default barrier (B). Figure 1 of Strebulaev (2007) summarizes

possible paths of firm values under these scenarios. At each refinancing point, the amount of debt

outstanding and consequently net payout increase by either γU or γLU, depending on whether the

liquidity barrier has not (γU) or has been hit (γLU) before reaching the refinancing point. Under

these assumptions, Strebulaev (2007) shows that it is sufficient to examine a firm’s capital

33

structure decision by focusing on the dynamic optimal capital structure problem over a single

refinancing cycle (i.e., a period from one debt issue until the upper refinancing barrier, either U or

LU, is hit and the refinancing decision is made). This simplification is possible because a single

refinancing cycle is representative of all subsequent cycles in the sense that in a subsequent

refinancing cycle, the firm can be considered as a larger copy of itself (i.e. at each refinancing

point, the values of equity and debt as well as net payouts all increase by the same, constant rate,

either γU or γLU, depending on whether the liquidity barrier has been hit before reaching the

refinancing point). Thus, once the optimal values of debt and equity during a single refinancing

cycle are identified at the beginning of its cycle, we can directly calculate the firm’s optimal market

leverage ratio at the refinancing point as the ratio of the value of debt divided by the combined

values of debt and equity.

Using the mean parameter values (excluding cash flow volatility, σ) specified in Table II of

Strebulaev (2007) together with a chosen cash flow volatility parameter value, σ, and the

linearization assumption of the net payout ratio (Eq. (12) of Strebulaev (2007)) used to determine

the drift rate of payouts, 𝜇𝜇, we discretize and simulate 10,000 sample paths over 500 quarters for

a firm’s net payouts to claimholders including governments (δ: before-tax net cash flows)

according to Eq. (1) of Strebulaev (2007). Based on these simulated net payout paths together with

initial trial values of three of the four control variables (coupon (c) = 2.0582, the proportion by

which the net payout increases between two refinancing points if the refinancing barrier has not

been hit first (γU) = 1.6508, and the proportion by which the net payout increases between two

refinancing points if the liquidity barrier has been hit first (γLU) = 1.6335), we use the smooth-

pasting condition (Eq. (13) of Strebulaev (2007)) to determine the value of the fourth control

variable, the default threshold (δB), and then calculate the market values of equity (ER(δ0)) and debt

34

(DR(δ0)) at the beginning of a refinancing cycle as specified in Eqs. (4) and (5) of Strebulaev (2007),

respectively. Next, we calculate the value of debt at time zero (D(δ0)) using his Eq. (7) and in turn,

the ex-ante firm value that shareholders try to maximize at each refinancing point before debt

issuance (F(δ0)) using his Eq. (10). Thus, the value of the shareholder’s claim after debt issuance

(E(δ0)) is determined as F(δ0) – (1-qRC) × D(δ0), where qRC is the proportional adjustment costs of

debt at the refinancing point and it is reflected in the calculation of F(δ0).

After we estimate initial values of firm, debt and equity, we revise the value of the default

threshold (δB) that satisfies the smooth-pasting condition of Eq. (13) of Strebulaev (2007). Then,

we use standard numerical optimization techniques to search for the values of control variables

that maximize the firm value, F(δ0). We repeat this procedure of updating δB and three control

variables until we cannot make either an improvement in the value of the shareholders’ claim (F(δ0))

or a change in the values of the control variables, which exceeds preset cutoff points. Finally, based

on firm value maximized, we calculate the optimal market leverage ratio. The results using this

simulation analysis are presented in Figure 1, which shows how the optimal market leverage

changes as the asset (cash flow) volatility changes from 0.055 to 0.455, two standard deviations

below and above the sample mean of 0.255 as reported in Strebulaev (2007). The figure clearly