retirement and investment webinar series - risk - … · 2015-10-13 · aon hewitt retirement and...

TRANSCRIPT

Aon HewittRetirement and Investment

Retirement and Investment Webinar SeriesOctober 14, 2015

Aon HewittRetirement and Investment

Year-End Retirement Planning—Financial Issues and Opportunities• Joan Boughton• Eric Keener• Dan McFall• Alan Parikh• Brian Walker

Aon HewittRetirement and Investment 3

Agenda Slide

Section 1 Spot Rate Approach to Measuring Benefit CostSection 2 Case Study: AT&TSection 3 Retirement Age TrendsSection 4 Longevity Trends and Other Assumptions

Aon HewittRetirement and Investment 4

Spot Rate Approach to Measuring Benefit Cost

Aon HewittRetirement and Investment 5

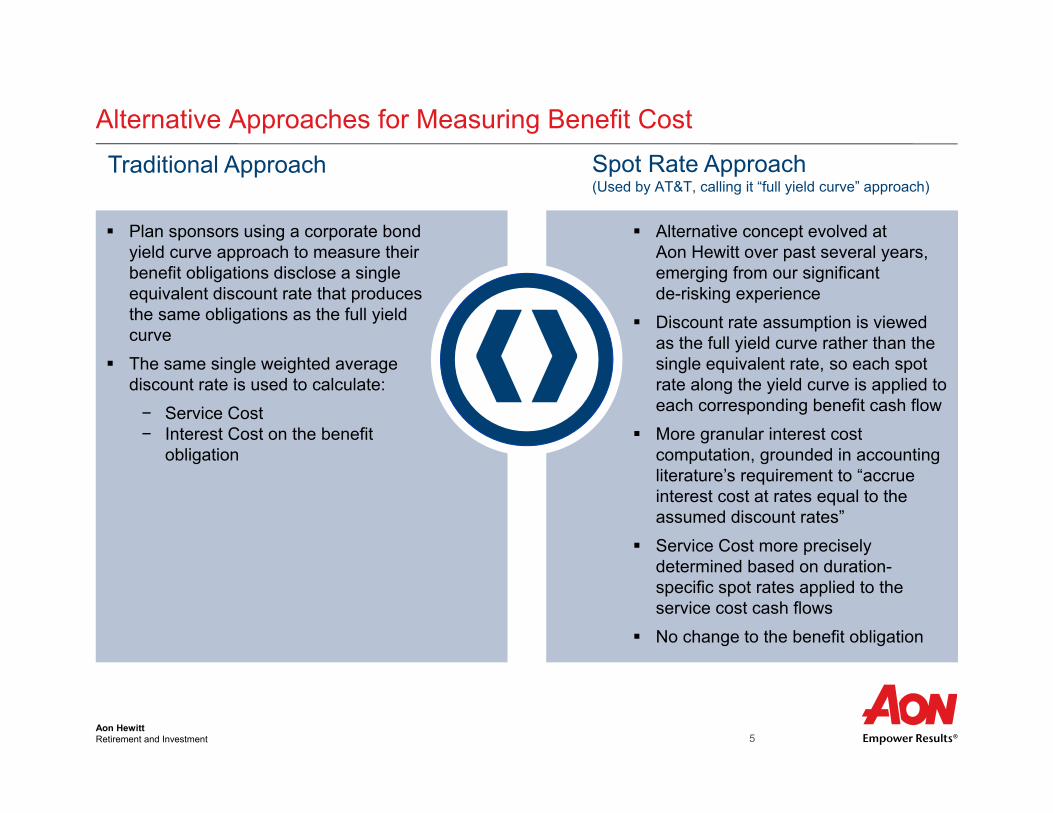

Alternative Approaches for Measuring Benefit Cost

❰❱ Plan sponsors using a corporate bond

yield curve approach to measure their benefit obligations disclose a single equivalent discount rate that produces the same obligations as the full yield curve

The same single weighted average discount rate is used to calculate:− Service Cost− Interest Cost on the benefit

obligation

Alternative concept evolved at Aon Hewitt over past several years, emerging from our significant de-risking experience

Discount rate assumption is viewed as the full yield curve rather than the single equivalent rate, so each spot rate along the yield curve is applied to each corresponding benefit cash flow

More granular interest cost computation, grounded in accounting literature’s requirement to “accrue interest cost at rates equal to the assumed discount rates”

Service Cost more precisely determined based on duration-specific spot rates applied to the service cost cash flows

No change to the benefit obligation

Traditional Approach Spot Rate Approach(Used by AT&T, calling it “full yield curve” approach)

Aon HewittRetirement and Investment 6

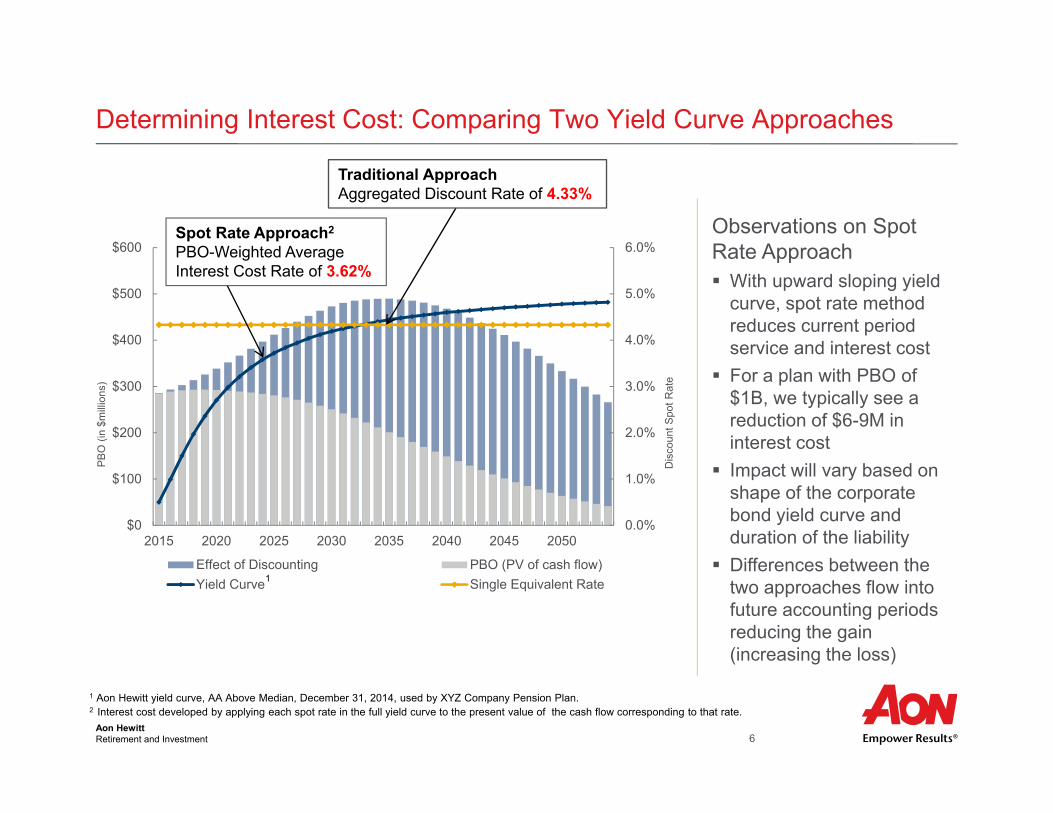

Determining Interest Cost: Comparing Two Yield Curve Approaches

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

$0

$100

$200

$300

$400

$500

$600

2015 2020 2025 2030 2035 2040 2045 2050

Effect of Discounting PBO (PV of cash flow)Yield Curve Single Equivalent Rate

1 Aon Hewitt yield curve, AA Above Median, December 31, 2014, used by XYZ Company Pension Plan.2 Interest cost developed by applying each spot rate in the full yield curve to the present value of the cash flow corresponding to that rate.

Spot Rate Approach2

PBO-Weighted AverageInterest Cost Rate of 3.62%

Dis

coun

t Spo

t Rat

e

PB

O (i

n $m

illio

ns)

Traditional ApproachAggregated Discount Rate of 4.33%

Observations on Spot Rate Approach With upward sloping yield

curve, spot rate method reduces current period service and interest cost

For a plan with PBO of $1B, we typically see a reduction of $6-9M in interest cost

Impact will vary based on shape of the corporate bond yield curve and duration of the liability

Differences between the two approaches flow into future accounting periods reducing the gain (increasing the loss)

1

Aon HewittRetirement and Investment 7

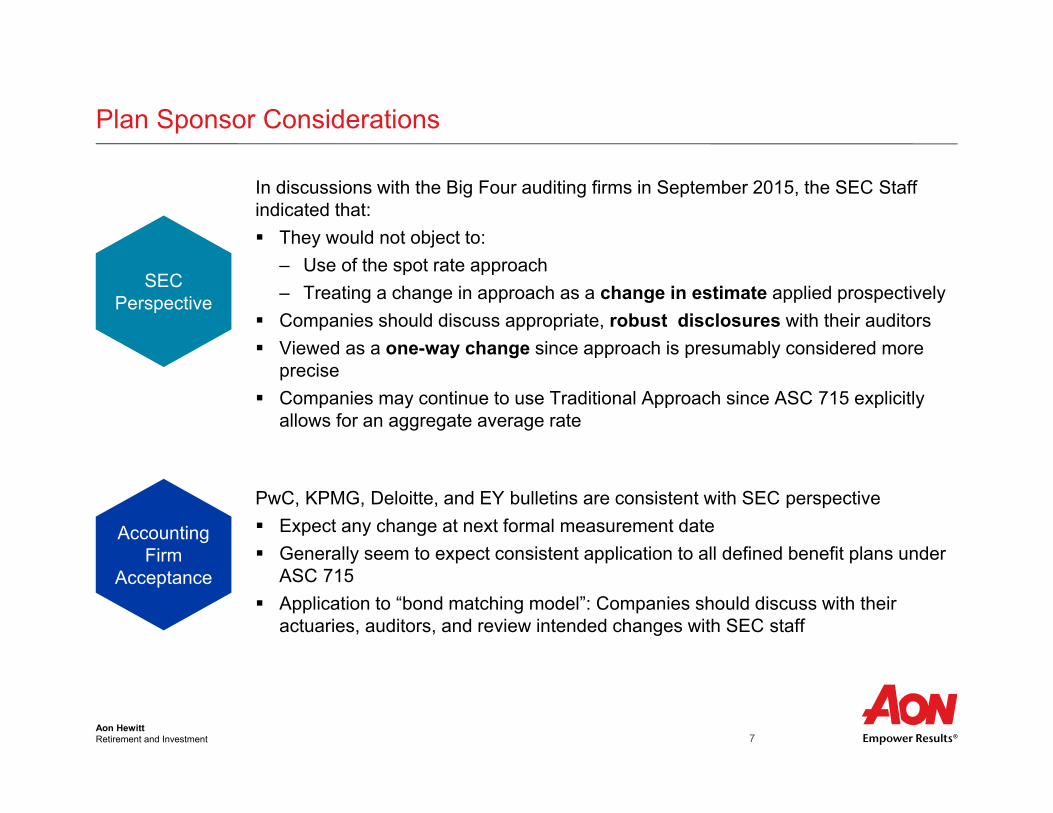

Plan Sponsor Considerations

In discussions with the Big Four auditing firms in September 2015, the SEC Staff indicated that: They would not object to:

– Use of the spot rate approach– Treating a change in approach as a change in estimate applied prospectively

Companies should discuss appropriate, robust disclosures with their auditors Viewed as a one-way change since approach is presumably considered more

precise Companies may continue to use Traditional Approach since ASC 715 explicitly

allows for an aggregate average rate

PwC, KPMG, Deloitte, and EY bulletins are consistent with SEC perspective Expect any change at next formal measurement date Generally seem to expect consistent application to all defined benefit plans under

ASC 715 Application to “bond matching model”: Companies should discuss with their

actuaries, auditors, and review intended changes with SEC staff

SEC Perspective

Accounting Firm

Acceptance

Aon HewittRetirement and Investment 8

Back Testing Analysis of Interest Cost Shows Volatility

0123456789

10

Estimated Reduction in Interest CostRelative to Traditional Approach

Reduction in Interest Cost

’04 ’05 ’06 ’07 ’08 ’09 ’10 ’11 ’12 ’13 ’14 ’15

6.48 5.94 5.84 5.95 6.63 6.87 6.04 5.69 4.88 4.43 5.21 4.33

5.32 5.24 5.52 5.75 6.14 6.72 5.11 4.62 4.06 3.49 4.18 3.62

1.16 0.70 0.32 0.20 0.49 0.15 0.93 1.07 0.82 0.94 1.03 0.71

Fiscal Year

EquivalentDiscount Rate %

Spot Rate Interest %

Reduction %

Inverted Treasury Curve 12/31/2006

CurveFlattened2004–2006

ABC Retirement Plan ($1B PBO)

$ M

illio

ns

Flat Corporate Bond Curve 12/31/08

Aon HewittRetirement and Investment 9

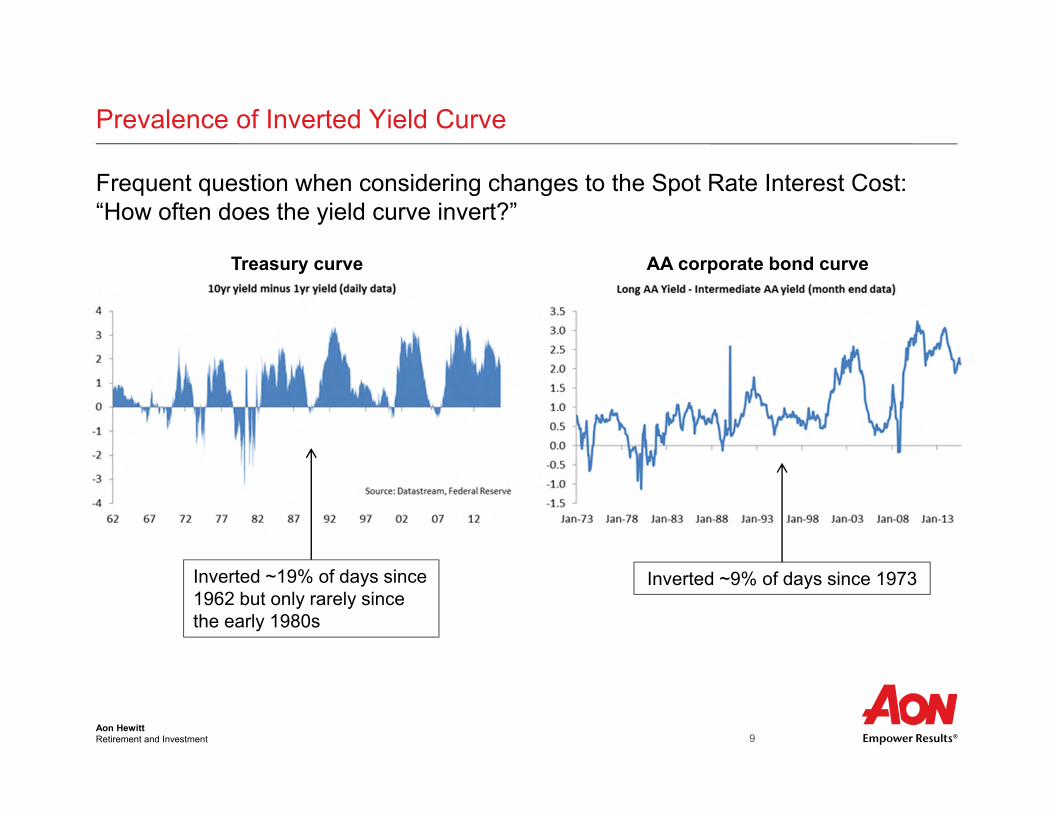

Prevalence of Inverted Yield Curve

Frequent question when considering changes to the Spot Rate Interest Cost: “How often does the yield curve invert?”

Treasury curve AA corporate bond curve

Inverted ~19% of days since 1962 but only rarely since the early 1980s

Inverted ~9% of days since 1973

Aon HewittRetirement and Investment 10

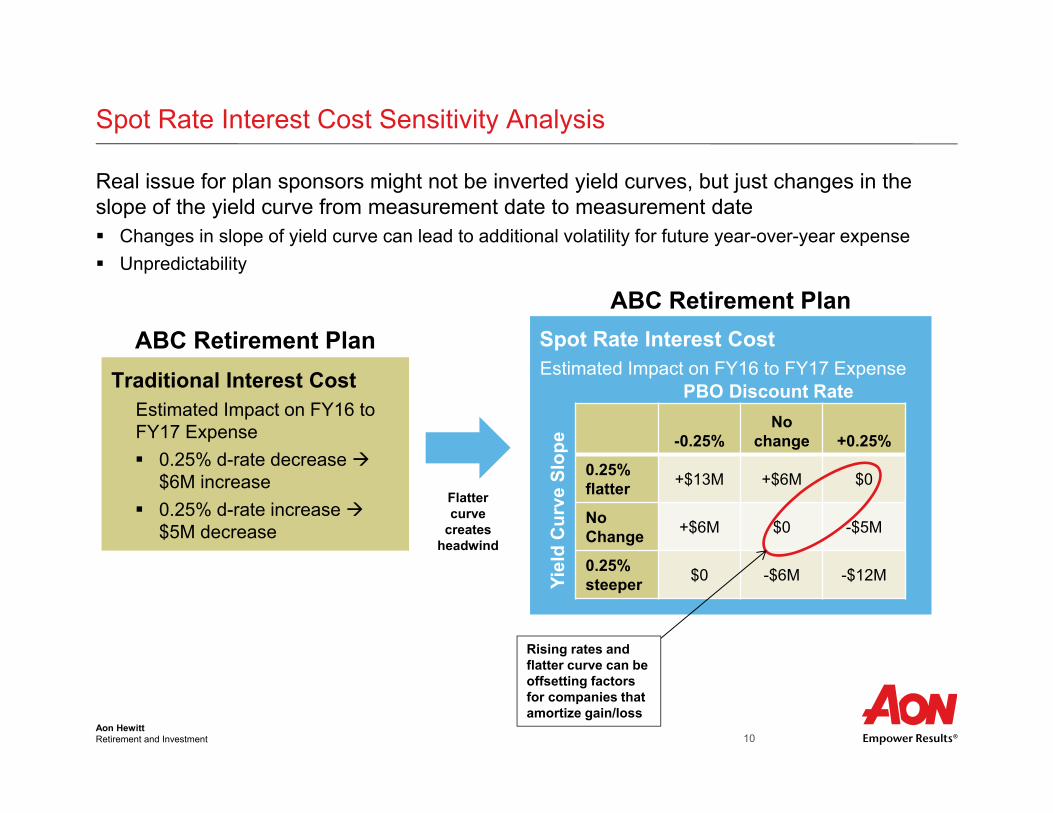

Spot Rate Interest Cost Sensitivity Analysis

Real issue for plan sponsors might not be inverted yield curves, but just changes in the slope of the yield curve from measurement date to measurement date Changes in slope of yield curve can lead to additional volatility for future year-over-year expense Unpredictability

Traditional Interest CostEstimated Impact on FY16 to FY17 Expense 0.25% d-rate decrease

$6M increase 0.25% d-rate increase

$5M decrease

Spot Rate Interest CostEstimated Impact on FY16 to FY17 Expense

-0.25%No

change +0.25%

0.25% flatter +$13M +$6M $0

NoChange +$6M $0 -$5M

0.25% steeper $0 -$6M -$12M

PBO Discount Rate

Yiel

d C

urve

Slo

pe

Rising rates and flatter curve can be offsetting factors for companies that amortize gain/loss

Flatter curve

creates headwind

ABC Retirement PlanABC Retirement Plan

Aon HewittRetirement and Investment 11

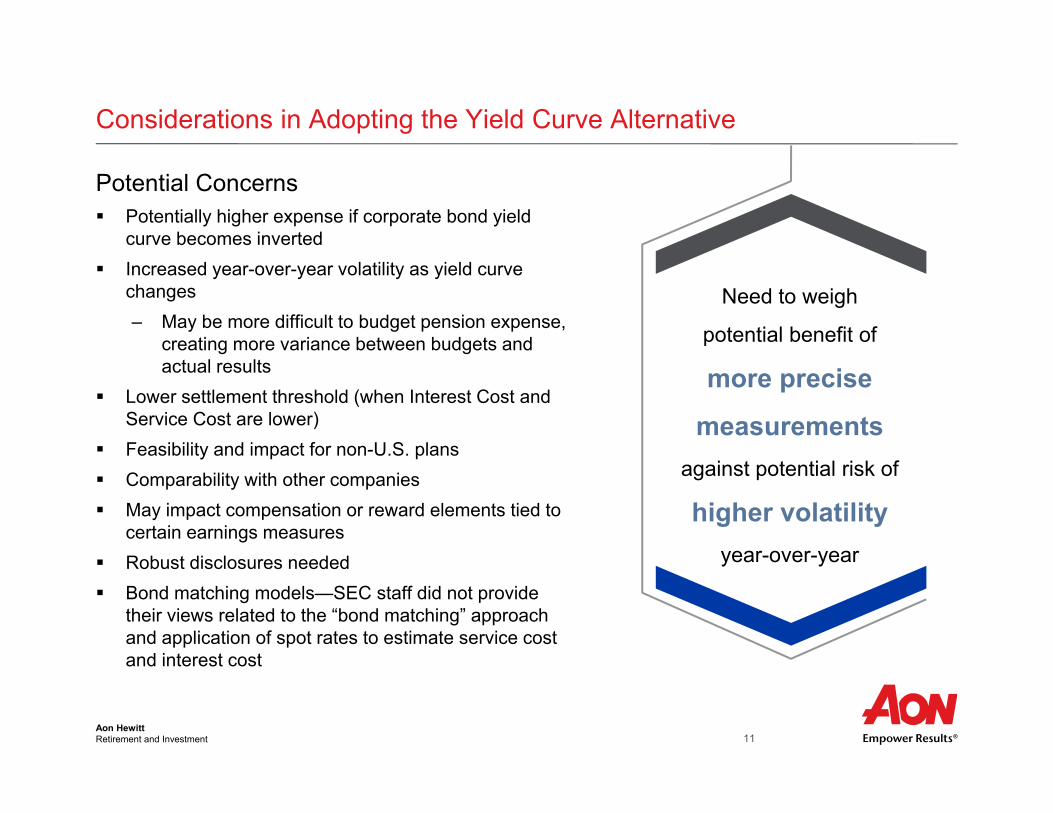

Considerations in Adopting the Yield Curve Alternative

Need to weigh

potential benefit of

more precise

measurements against potential risk of

higher volatility year-over-year

Potential Concerns Potentially higher expense if corporate bond yield

curve becomes inverted Increased year-over-year volatility as yield curve

changes– May be more difficult to budget pension expense,

creating more variance between budgets and actual results

Lower settlement threshold (when Interest Cost and Service Cost are lower)

Feasibility and impact for non-U.S. plans Comparability with other companies May impact compensation or reward elements tied to

certain earnings measures Robust disclosures needed Bond matching models—SEC staff did not provide

their views related to the “bond matching” approach and application of spot rates to estimate service cost and interest cost

Aon HewittRetirement and Investment 12

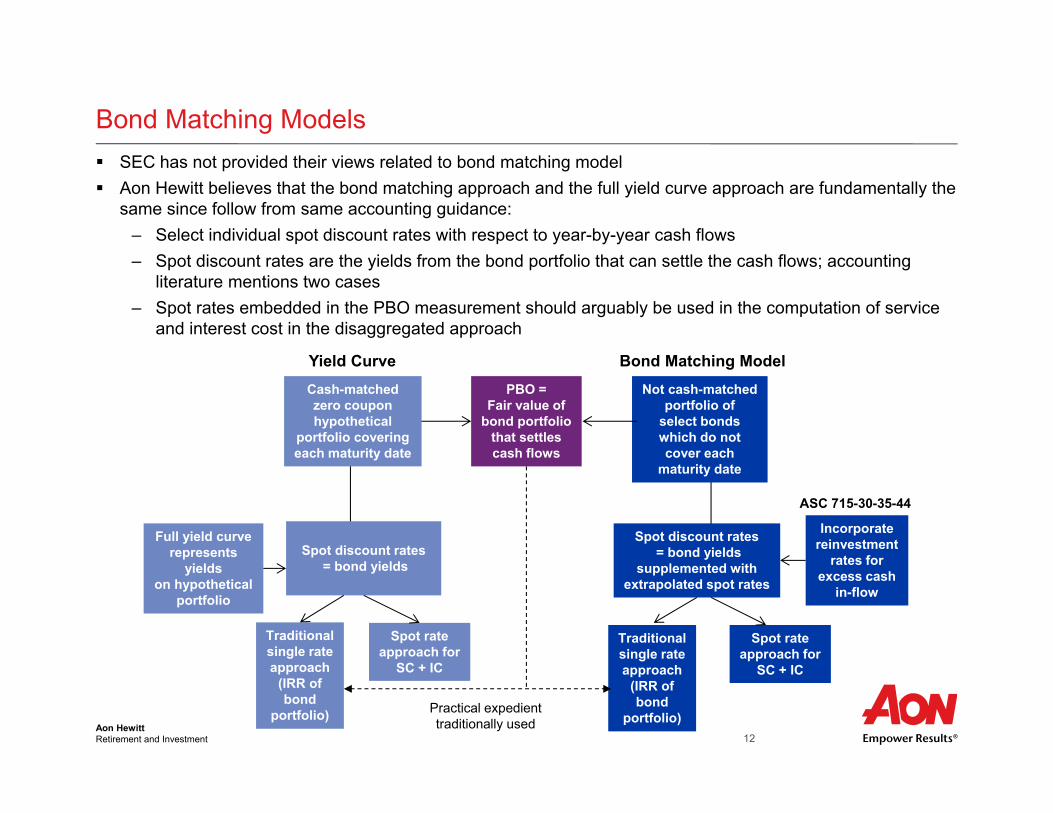

Bond Matching Models SEC has not provided their views related to bond matching model Aon Hewitt believes that the bond matching approach and the full yield curve approach are fundamentally the

same since follow from same accounting guidance:– Select individual spot discount rates with respect to year-by-year cash flows– Spot discount rates are the yields from the bond portfolio that can settle the cash flows; accounting

literature mentions two cases– Spot rates embedded in the PBO measurement should arguably be used in the computation of service

and interest cost in the disaggregated approach

Yield CurveCash-matchedzero couponhypothetical

portfolio coveringeach maturity date

Spot discount rates= bond yields

Full yield curverepresents

yieldson hypothetical

portfolio

Traditionalsingle rateapproach

(IRR of bond

portfolio)

Spot rateapproach for

SC + IC

Bond Matching ModelNot cash-matched

portfolio ofselect bondswhich do notcover each

maturity date

Spot discount rates= bond yields

supplemented withextrapolated spot rates

Incorporatereinvestment

rates forexcess cash

in-flow

Traditionalsingle rateapproach

(IRR ofbond

portfolio)

Spot rateapproach for

SC + IC

ASC 715-30-35-44

PBO =Fair value of

bond portfoliothat settlescash flows

Practical expedienttraditionally used

Aon HewittRetirement and Investment 13

Case Study: AT&T

Aon HewittRetirement and Investment 14

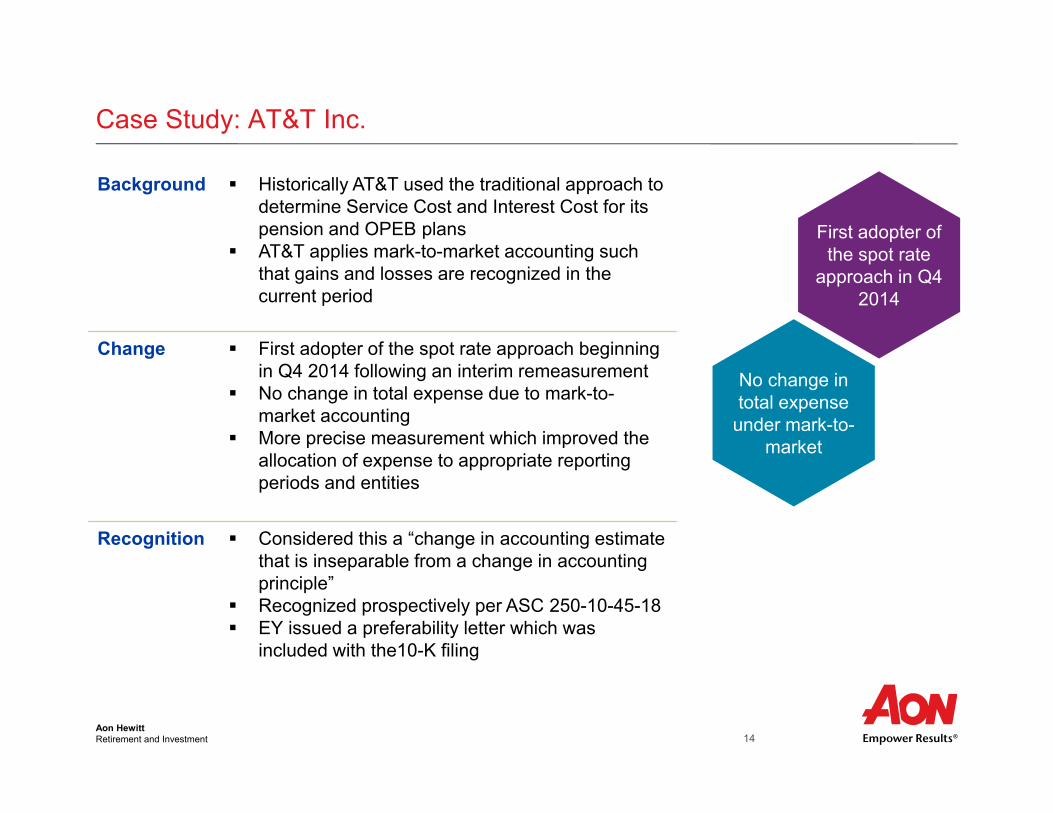

Case Study: AT&T Inc.

Background Historically AT&T used the traditional approach to determine Service Cost and Interest Cost for its pension and OPEB plans

AT&T applies mark-to-market accounting such that gains and losses are recognized in the current period

Change First adopter of the spot rate approach beginningin Q4 2014 following an interim remeasurement

No change in total expense due to mark-to-market accounting

More precise measurement which improved the allocation of expense to appropriate reporting periods and entities

Recognition Considered this a “change in accounting estimate that is inseparable from a change in accounting principle”

Recognized prospectively per ASC 250-10-45-18 EY issued a preferability letter which was

included with the10-K filing

First adopter of the spot rate

approach in Q4 2014

No change in total expense

under mark-to-market

Aon HewittRetirement and Investment 15

Retirement Age Trends

Aon HewittRetirement and Investment 16

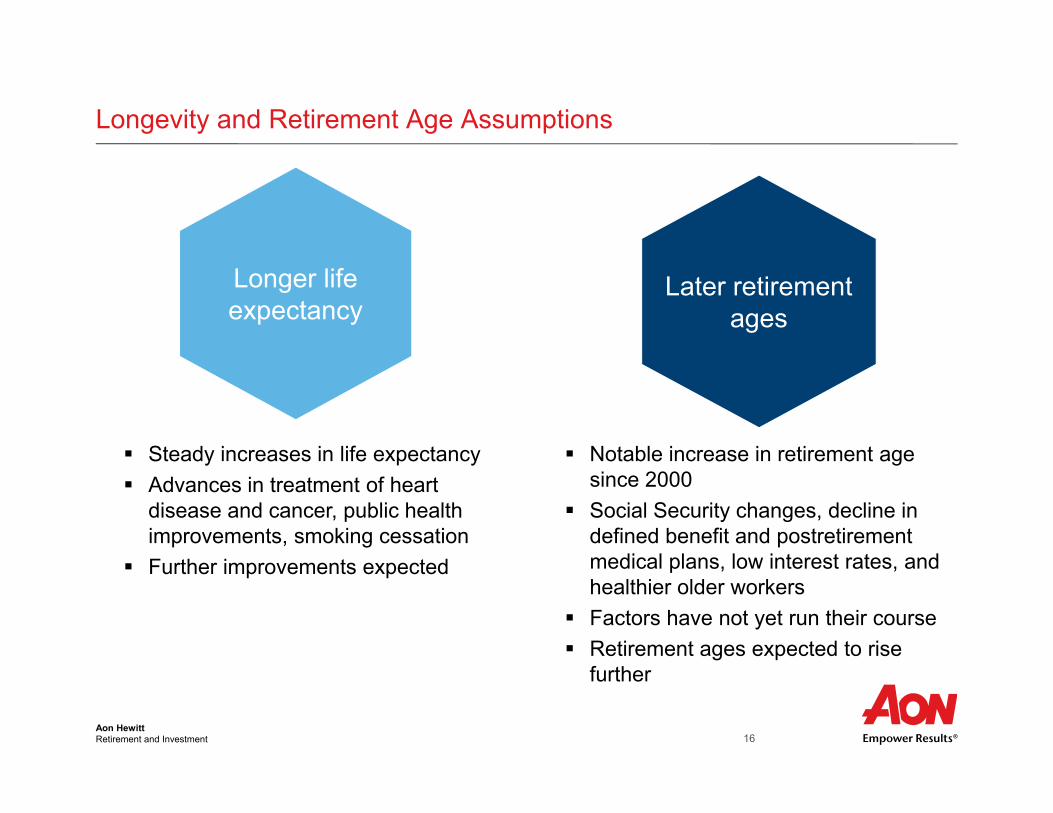

Longevity and Retirement Age Assumptions

Longer life expectancy

Steady increases in life expectancy Advances in treatment of heart

disease and cancer, public health improvements, smoking cessation

Further improvements expected

Later retirement ages

Notable increase in retirement age since 2000

Social Security changes, decline in defined benefit and postretirement medical plans, low interest rates, and healthier older workers

Factors have not yet run their course Retirement ages expected to rise

further

Aon HewittRetirement and Investment 17

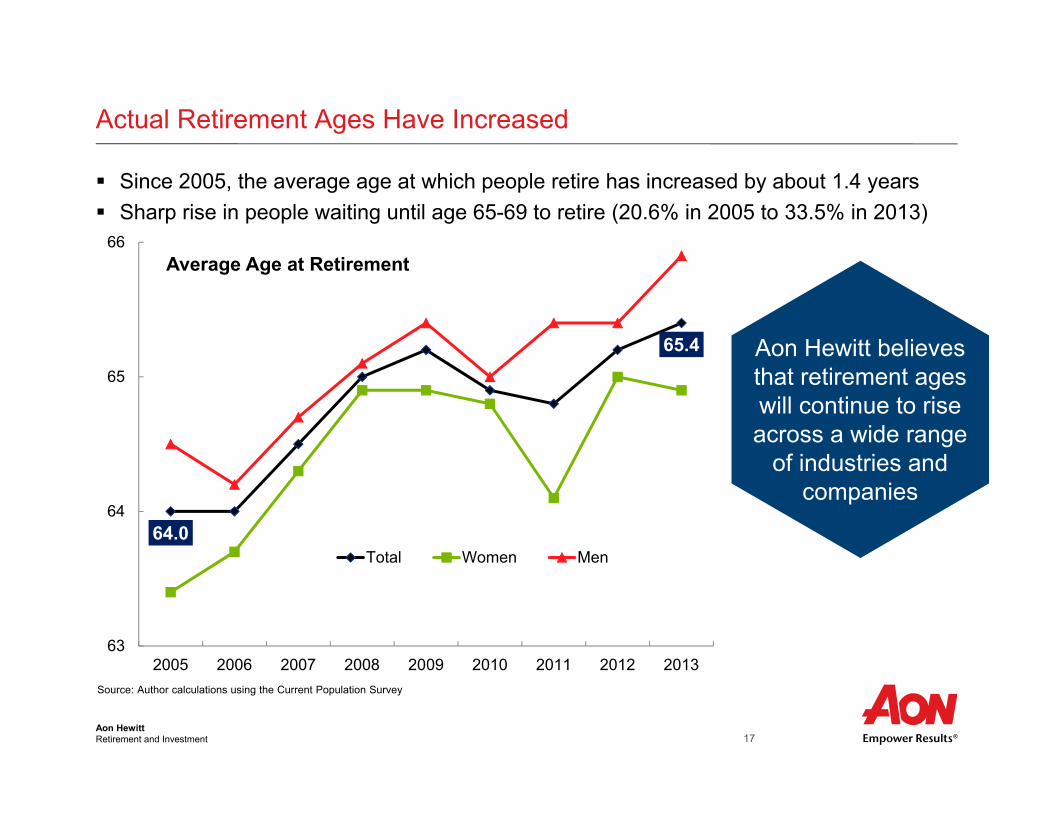

Actual Retirement Ages Have Increased

Since 2005, the average age at which people retire has increased by about 1.4 years Sharp rise in people waiting until age 65-69 to retire (20.6% in 2005 to 33.5% in 2013)

64.0

65.4

63

64

65

66

2005 2006 2007 2008 2009 2010 2011 2012 2013

Average Age at Retirement

Total Women Men

Source: Author calculations using the Current Population Survey

Aon Hewitt believes that retirement ages will continue to rise across a wide range

of industries and companies

Aon HewittRetirement and Investment 18

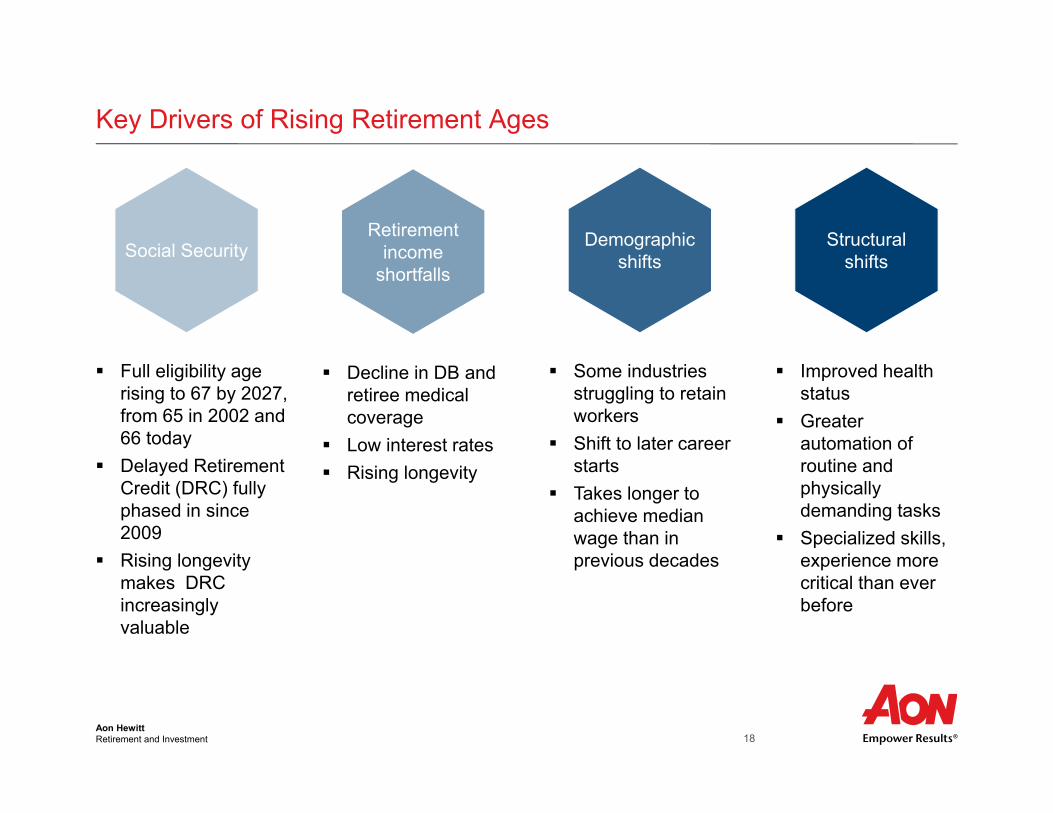

Key Drivers of Rising Retirement Ages

Retirement income

shortfalls

Decline in DB and retiree medical coverage

Low interest rates Rising longevity

Demographic shifts

Some industries struggling to retain workers

Shift to later career starts

Takes longer to achieve median wage than in previous decades

Structural shifts

Improved health status

Greater automation of routine and physically demanding tasks

Specialized skills, experience more critical than ever before

Social Security

Full eligibility age rising to 67 by 2027, from 65 in 2002 and 66 today

Delayed Retirement Credit (DRC) fully phased in since 2009

Rising longevity makes DRC increasingly valuable

Aon HewittRetirement and Investment 19

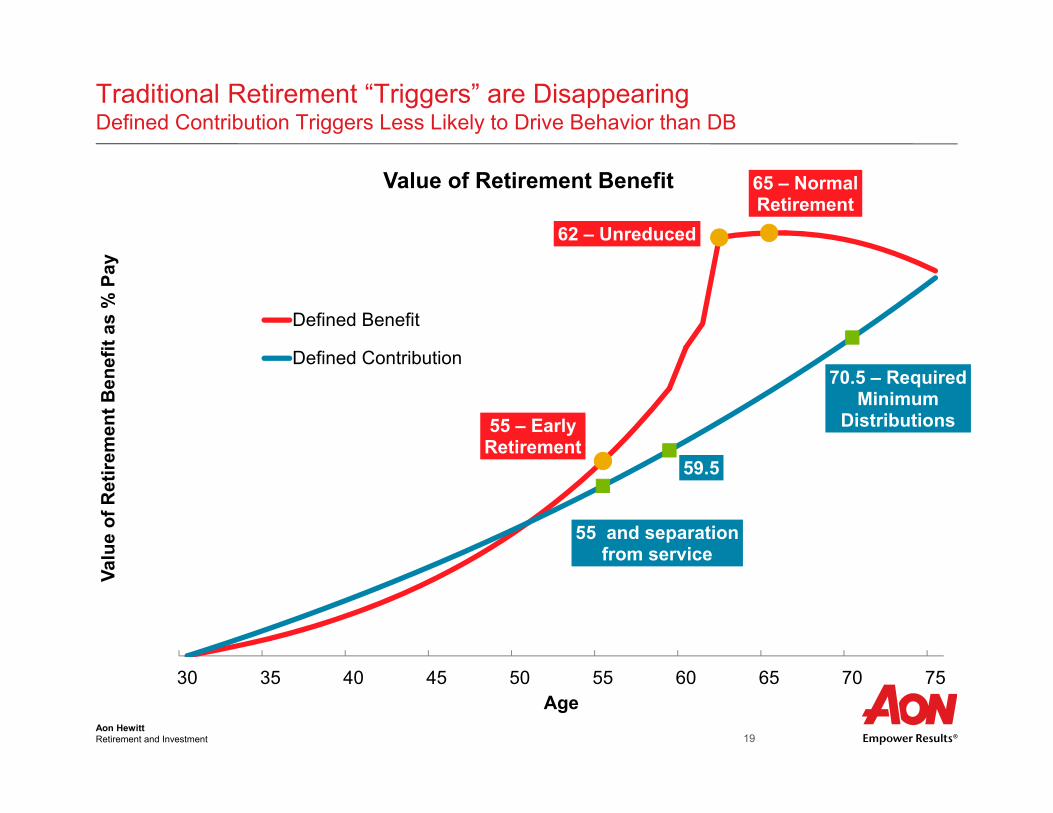

Traditional Retirement “Triggers” are DisappearingDefined Contribution Triggers Less Likely to Drive Behavior than DB

55 – Early Retirement

62 – Unreduced

65 – Normal Retirement

55 and separation from service

59.5

70.5 – Required Minimum

Distributions

30 35 40 45 50 55 60 65 70 75

Valu

e of

Ret

irem

ent B

enef

it as

% P

ay

Age

Value of Retirement Benefit

Defined Benefit

Defined Contribution

Aon HewittRetirement and Investment 20

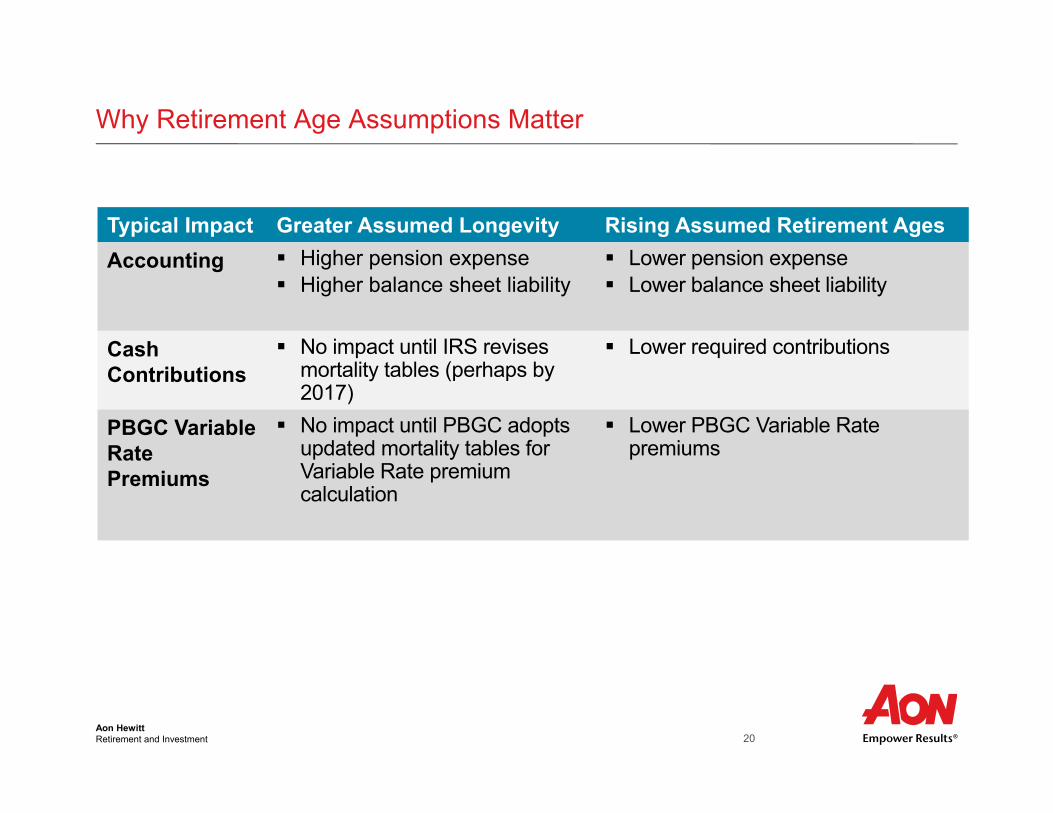

Why Retirement Age Assumptions Matter

Typical Impact Greater Assumed Longevity Rising Assumed Retirement AgesAccounting Higher pension expense

Higher balance sheet liability Lower pension expense Lower balance sheet liability

CashContributions

No impact until IRS revisesmortality tables (perhaps by 2017)

Lower required contributions

PBGC Variable Rate Premiums

No impact until PBGC adopts updated mortality tables for Variable Rate premium calculation

Lower PBGC Variable Rate premiums

Aon HewittRetirement and Investment 21

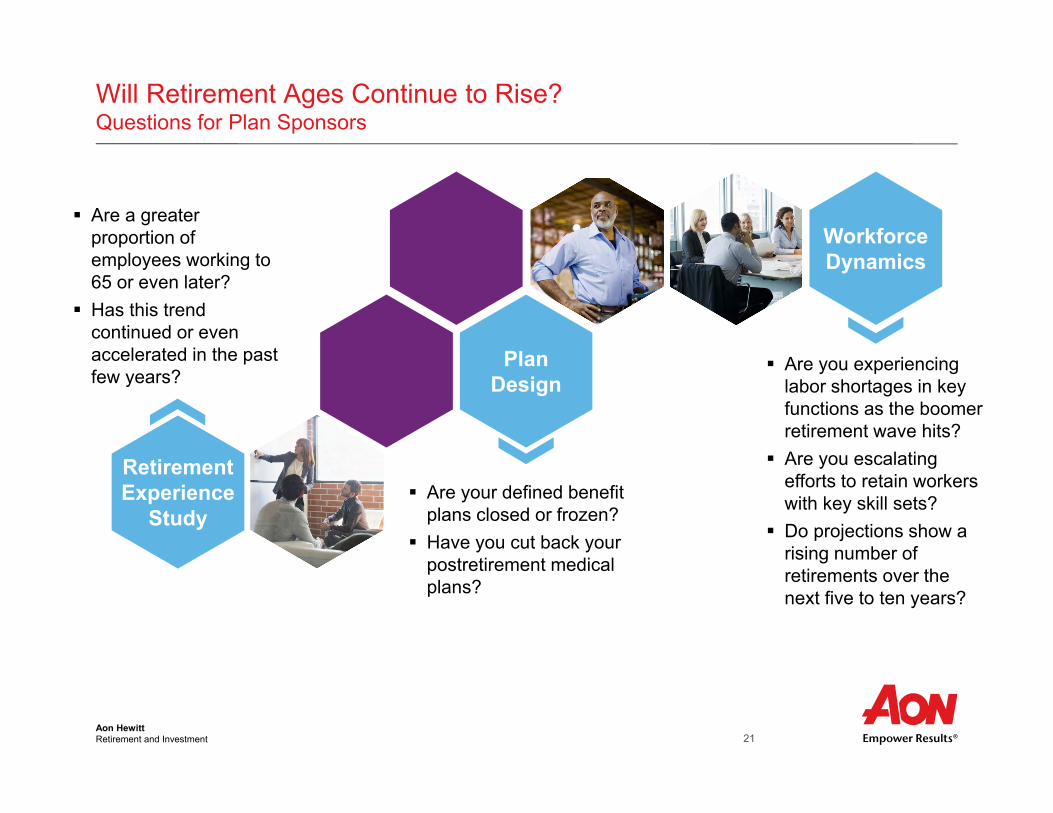

Will Retirement Ages Continue to Rise?Questions for Plan Sponsors

Are a greater proportion of employees working to 65 or even later?

Has this trend continued or even accelerated in the past few years?

Are your defined benefit plans closed or frozen?

Have you cut back your postretirement medical plans?

Are you experiencing labor shortages in key functions as the boomer retirement wave hits?

Are you escalating efforts to retain workers with key skill sets?

Do projections show a rising number of retirements over the next five to ten years?

Plan Design

Retirement Experience

Study

Workforce Dynamics

Aon HewittRetirement and Investment 22

Longevity Trends and Other Assumptions

Aon HewittRetirement and Investment 23

SOA Issues Updated Mortality Improvement Assumptions

On October 8, 2015 the Society of Actuaries (SOA) released updated mortality improvement assumptions for retirement plans (MP-2015)

Reflects additional data that Social Security Administration has released since prior assumptions (MP-2014) were developed

– Data shows lower mortality improvement in 2010 – 2011 than in previous years– Results in lower projected future improvements in SOA model

Key question: Does data indicate a new long-term trend? Or just random noise? SOA expects to:

– Release annual updates going forward– Explore availability of more current information to decrease lag time– Issue next update in mid-2016?

MP-2015 produces

1-2%Typical reduction in plan

liability vs. MP-2014

Aon HewittRetirement and Investment 24

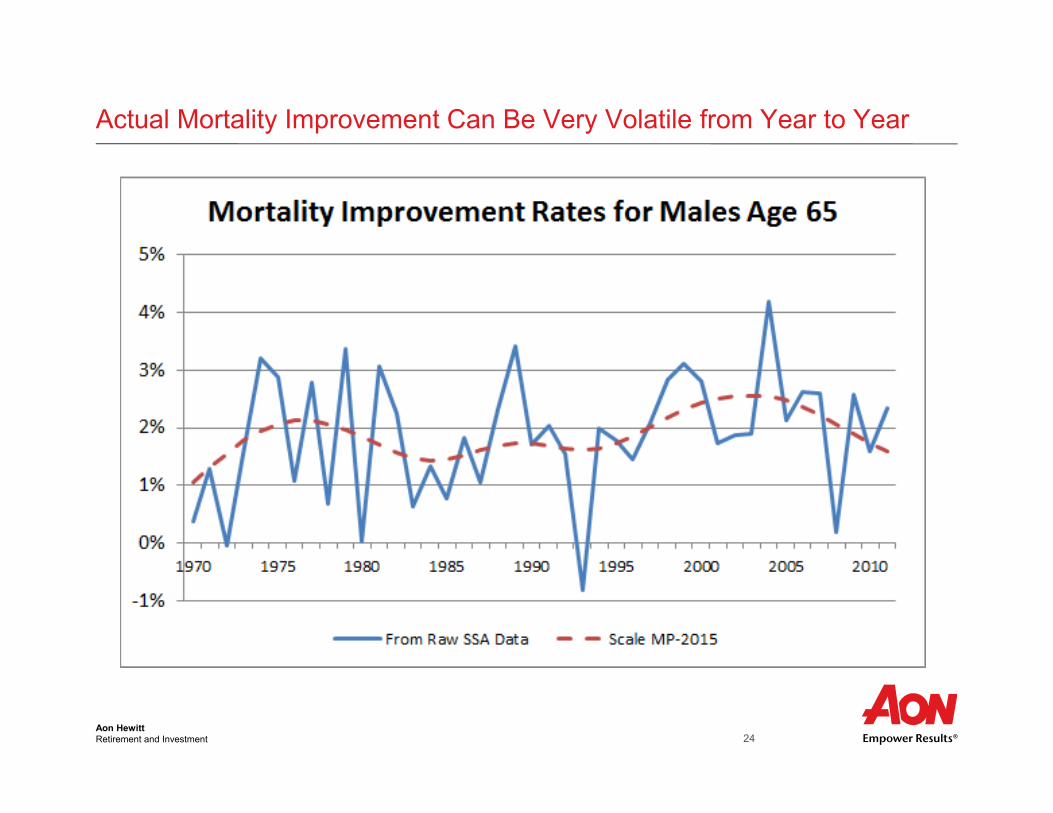

Actual Mortality Improvement Can Be Very Volatile from Year to Year

Aon HewittRetirement and Investment 25

Updated Mortality Improvement Assumptions –Next Steps for Plan Sponsors

Plan sponsors should consider reflecting new data in 2015 year-end disclosures and 2016 expense– Could use MP-2015 or an alternative

assumption If reflect new data this year, auditors may expect

annual updates going forward as new data is released– Could result in additional volatility

Future updates could increase plan liabilities if mortality improvement is greater than expected

Key Takeaways MP-2015 produces

lower liabilities than MP-2014 Consider reflecting

in 2015 disclosures and 2016 expense Note potential for

added volatility going forward

Aon HewittRetirement and Investment 26

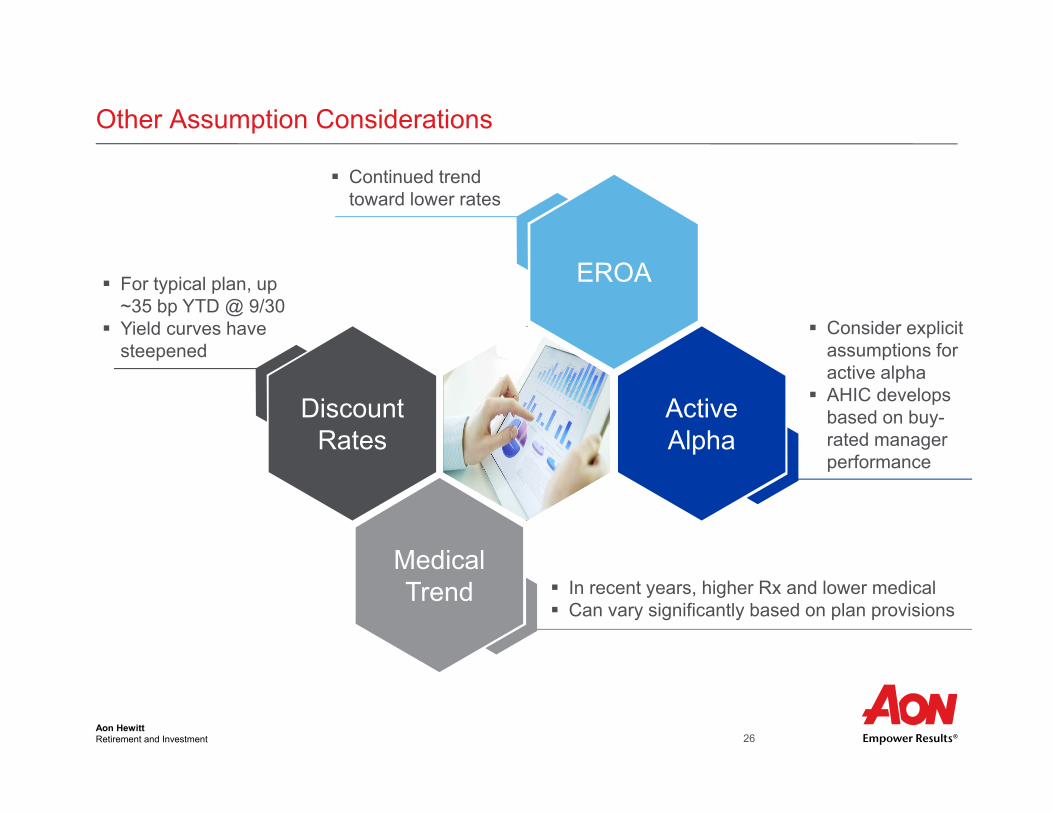

Other Assumption Considerations

Discount Rates

ActiveAlpha

EROA

Medical Trend

For typical plan, up ~35 bp YTD @ 9/30

Yield curves have steepened

Consider explicit assumptions for active alpha

AHIC develops based on buy-rated manager performance

Continued trend toward lower rates

In recent years, higher Rx and lower medical Can vary significantly based on plan provisions

Aon HewittRetirement and Investment 27

Questions and AnswersEmail [email protected] with questions for our speakers.

Aon HewittRetirement and Investment 28

Speaker Biographies

Joan BoughtonJoan is an actuary and Partner at the firm, co-leading Aon Hewitt’s national Retirement Strategy and Design / IDEA team. She consults on HR and retirement strategy, design, implementation, administration, communication, financing, and ongoing plan management.

Eric KeenerEric is a Partner and Chief Actuary of Aon Hewitt's U.S. Retirement Practice. He leads our National Actuarial Resource Team and is responsible for delivering training, thought leadership, technical guidance, and day-to-day assistance to our consultants as they serve our clients. He also consults with several large clients on a broad range of retirement plan issues.

Dan McFallDan is an actuary and Partner with Aon Hewitt. He is one of Aon Hewitt’s thought leaders and consults with some of our largest retirement clients on retirement strategy, design, financing, and ongoing plan management.

Alan ParikhAlan is a member of Aon Hewitt’s National Actuarial Resource Team, helping Aon Hewitt consultants deliver quality work and value-added consulting across the United States. He is also a member of Pension Committee of the Actuarial Standards Board, a CFA charterholder, and CAIA charterholder.

Brian WalkerBrian is an actuary and Associate Partner in Aon Hewitt’s Retirement and Investment practice. He advises clients on funding and accounting requirements for their retirement programs, and provides strategic advice on retirement plan design, executive retirement benefits, postretirement benefits, and plan administration.

Aon HewittRetirement and Investment 29

About Aon Hewitt

Aon Hewitt empowers organizations and individuals to secure a better future through innovative talent, retirement and health solutions. We advise, design and execute a wide range of solutions that enable clients to cultivate talent to drive organizational and personal performance and growth, navigate retirement risk while providing new levels of financial security, and redefine health solutions for greater choice, affordability and wellness. Aon Hewitt is the global leader in human resource solutions, with over 30,000 professionals in 90 countries serving more than 20,000 clients worldwide. For more information, please visit aonhewitt.com.

© Aon plc 2015. All rights reserved.