retail shake-up; store closings are opportunities for … states/markets...retail shake-up; store...

TRANSCRIPT

Retail shake-up; Store closings are opportunities for expanding retailers

Research & Forecast Report

MINNEAPOLIS-ST. PAUL | RETAILFebruary 2017

Vacancy & Absorption Trends The vacancy rate in the Minneapolis-St. Paul retail market increased for the second quarter in a row to 5.7 percent, which is up from year-end 2015’s rate of 4.4 percent. There was 70,545 square feet of negative absorption during the quarter which included Sears closing its store at Eden Prairie Center, K-Mart closing a store in West St. Paul and Office Max closing three stores in Lakeville, Burnsville and Brooklyn Park. Some of that negative absorption was mitigated by strong construction activity in the grocery sector.

Store Closings and Grocery Expansions Additional store closings include Macy’s and Barnes & Noble in the Minneapolis CBD. Macy’s will be closing its store after an investor purchased the site and plans to redevelop it. Golfsmith, Hancock Fabrics, Old Country Buffet and Rainbow Foods are also closing stores due to bankruptcy or poorly performing locations. Golden Corral is stepping in to fill several Old Country Buffet locations and is also looking to open at additional locations made available when Old Country Buffet declared bankruptcy.

We continue to monitor a steady stream of national retailers seeking to open stores in the Minneapolis-St. Paul market, especially in prime trade areas. Grocers continue to compete for market share. Fresh Thyme Farmer’s Market opened three new stores in Plymouth, Vadnais Heights and Savage adding to existing stores in Bloomington and Apple Valley. Cub Foods opened a store in Blaine and a store in Oakdale (replacing another Cub one block away), and Kowalski’s opened a new store in a former Rainbow Foods in Shoreview. There are two Hy-Vee stores, three Fresh Thyme Farmers Markets, a Trader Joe’s and an Aldi under construction. In Oakdale, the new Cub Foods is located directly across the street from Hy-Vee. Other grocers seeking to grow are Lunds & Byerly’s, Cub Foods, Whole Foods Market, Kowalski’s, Jerry’s Foods along with Walmart and Target.

Net Absorption1,000,000

500,000

0

(500,000)

(1,000,000)

(335,329)

(962,017)

508,759

(143,478)SF A

bsor

bed

632,849431,134

872,912 1,111,241

2008 2009 2010 2011 2012 2013 2014 2015

(246,509)

2007

251,879

2016

Vacancy

10%

8%

6%

4%

2%

0

5.1%

6.9% 7.3% 6.8%

Perc

ent V

acan

t

6.2%

5.4%4.9%

2008 2009 2010 2011 2012 2013 2014 2015

4.4%

2007

3.6%

2016

5.7%

SUBSCRIBE TO OUR BLOG

Market IndicatorsRelative to prior period Q4 2016 VACANCY NET ABSORPTION RENTAL RATE

2 Minneapolis-St. Paul Research & Forecast Report | February 2017 | Retail | Colliers International

3Minneapolis-St. Paul Research & Forecast Report | February 2017 | Retail | Colliers International

QSRs and Coffee Café Zupas, Naf Naf Grill and Piada are examples of restaurants opening locations in this market. Fast casual/quick serve restaurants are eager to expand in this market alongside established players such as Noodles and Chipotle.

Tim Hortons debuted in the market with a store at the Mall of America and one in Dinkytown in Minneapolis; the company has plans for additional locations in Brooklyn Park and Savage. Dunkin’ Donuts opened stores in New Hope, MSP International Airport and Roseville in their push to expand in this market. Both Tim Hortons and Dunkin’ Donuts will compete with existing coffee players Caribou Coffee and Starbucks, which are already well-established here. Starbucks is planning several new stores and is partnering with Hy-Vee to open shops in their Minneapolis-St. Paul locations.

Restaurants, Wine & Spiking Rates Rental rates continue to be at high levels and time will tell if there are retailers that are able to sustain sales levels to pay these rates. Prime retail locations are seeing unprecedented activity and increasing rents driven primarily by QSR restaurants that seek spaces near well-anchored projects. In other areas, there are retail centers that have had the same vacancies for several years. We are beginning to see concessions creep into negotiations in an effort to get some of the longer-held vacancies leased up. In addition to high rental rates at prime locations, occupancy costs continue to rise as CAM and taxes push upward.

Retailers, particularly restaurants, must also contend with worker shortages and rising costs of service employees. QSRs are responding by adding kiosks and online ordering to reduce the need for in-store employees.

Market Activity > Hy-Vee recently announced their plans for a 105,000-square-

foot store in Chaska, adding to their existing stores in New Hope, Oakdale, Brooklyn Park, Lakeville, and Eagan. There are stores under construction in Savage and Cottage Grove and additional locations planned for Maple Grove, Shakopee, Robbinsdale, Columbia Heights and Farmington.

> Investment demand for grocery retail properties is strong:

» Hurd Real Estate purchased the Hy-Vee in Brooklyn Park from Ryan Companies for $24.1 million. Ryan developed the property for Hy-Vee, which totals 104,000 square feet and includes a gas station. Hurd owns 19 other Hy-Vee leased properties in the Midwest.

» Palm Beach, Florida-based Sterling Organization bought three Cub Foods-anchored shopping centers in Fridley, Blaine and Burnsville from Tri Land Properties.

> Golden Corral is planning to take over former Old Country Buffet restaurants in Coon Rapids and Woodbury. These locations would add to the stores in Maplewood and Maple Grove that opened in 2016.

> The Sears store at Eden Prairie mall closed and Sears is also planning to close its store in Coon Rapids this spring.

> Lifetime Fitness CEO Bahram Akradi has submitted plans for a lifestyle center in Chanhassen called Avienda. The mixed-use project would include 435,000 square feet or retail, 40,000 square feet of office space, 300 market rate apartments, 100 senior living units and two hotels.

> Centennial Shops in Edina sold for $32.1 million to Ramco-Gershenson Properties Trust. Ramco bought the 85,000-square-foot property from Cypress Equities. Tenants at the center include West Elm, Container Store, Potbelly, Leeann Chin and Five Guys Burger and Fries.

Hy-Vee, Brooklyn Park Ryan Companies sold the HyVee in Brooklyn Park, completed in 2016, to Hurd Real Estate for 24.1 million.

25%

20%

15%

10%

5%

0CBD Community Neighborhood Regional

2.8%7.5%

5.5%

17.2%

Perc

ent V

acan

t

Vacancy - Q4 2016

Outlet

0%

Net Absorption - Q4 2016400,000

200,000

0

(200,000)

(400,000)

(24,614)

SF A

bsor

bed

CBD Community NeighborhoodRegionalOutlet

201,782

(43,208)0

(204,505)

4 Minneapolis-St. Paul Research & Forecast Report | February 2017 | Retail | Colliers International

Tenant Tracker

Expanding

New or Looking

5Minneapolis-St. Paul Research & Forecast Report | February 2017 | Retail | Colliers International

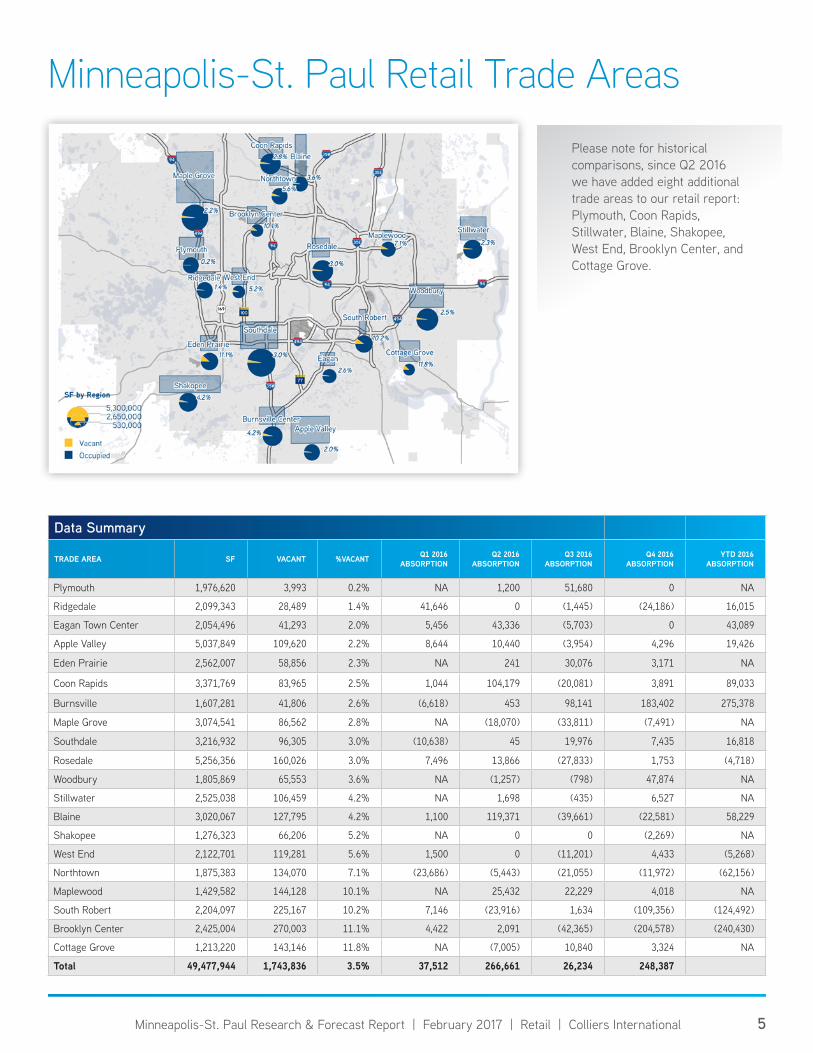

Data Summary

TRADE AREA SF VACANT %VACANT Q1 2016 ABSORPTION

Q2 2016ABSORPTION

Q3 2016ABSORPTION

Q4 2016ABSORPTION

YTD 2016ABSORPTION

Plymouth 1,976,620 3,993 0.2% NA 1,200 51,680 0 NA

Ridgedale 2,099,343 28,489 1.4% 41,646 0 (1,445) (24,186) 16,015

Eagan Town Center 2,054,496 41,293 2.0% 5,456 43,336 (5,703) 0 43,089

Apple Valley 5,037,849 109,620 2.2% 8,644 10,440 (3,954) 4,296 19,426

Eden Prairie 2,562,007 58,856 2.3% NA 241 30,076 3,171 NA

Coon Rapids 3,371,769 83,965 2.5% 1,044 104,179 (20,081) 3,891 89,033

Burnsville 1,607,281 41,806 2.6% (6,618) 453 98,141 183,402 275,378

Maple Grove 3,074,541 86,562 2.8% NA (18,070) (33,811) (7,491) NA

Southdale 3,216,932 96,305 3.0% (10,638) 45 19,976 7,435 16,818

Rosedale 5,256,356 160,026 3.0% 7,496 13,866 (27,833) 1,753 (4,718)

Woodbury 1,805,869 65,553 3.6% NA (1,257) (798) 47,874 NA

Stillwater 2,525,038 106,459 4.2% NA 1,698 (435) 6,527 NA

Blaine 3,020,067 127,795 4.2% 1,100 119,371 (39,661) (22,581) 58,229

Shakopee 1,276,323 66,206 5.2% NA 0 0 (2,269) NA

West End 2,122,701 119,281 5.6% 1,500 0 (11,201) 4,433 (5,268)

Northtown 1,875,383 134,070 7.1% (23,686) (5,443) (21,055) (11,972) (62,156)

Maplewood 1,429,582 144,128 10.1% NA 25,432 22,229 4,018 NA

South Robert 2,204,097 225,167 10.2% 7,146 (23,916) 1,634 (109,356) (124,492)

Brooklyn Center 2,425,004 270,003 11.1% 4,422 2,091 (42,365) (204,578) (240,430)

Cottage Grove 1,213,220 143,146 11.8% NA (7,005) 10,840 3,324 NA

Total 49,477,944 1,743,836 3.5% 37,512 266,661 26,234 248,387

Minneapolis-St. Paul Retail Trade Areas

Please note for historical comparisons, since Q2 2016 we have added eight additional trade areas to our retail report: Plymouth, Coon Rapids, Stillwater, Blaine, Shakopee, West End, Brooklyn Center, and Cottage Grove.

6 Minneapolis-St. Paul Research & Forecast Report | February 2017 | Retail | Colliers International

7Minneapolis-St. Paul Research & Forecast Report | February 2017 | Retail | Colliers International

Kris SchiselSenior Associate | Retail LeasingDIRECT +1 952 897 [email protected]

Recently, major retailers have announced their exit from downtown Minneapolis and some believe this is a signal of weakening retail viability in the downtown CBD. However, it can be argued that the reset button has just been hit and we’re on the verge of a downtown Minneapolis retail refresh. The idea that retail is dying in downtown Minneapolis is a misconception, a more forward-thinking viewpoint is that retail is reinventing itself in downtown Minneapolis. Sure, there are major retailers leaving, but we’re on the verge of a revival and with the growth in office and residential – retail has the potential to gain major momentum in the near future. Consistently, the marriage between retail, office and residential is a more accurate measure of overall CRE health for urban markets.

Foot traffic in the day and night = strong retail opportunities What creates a healthy environment for a thriving retail industry in a downtown area? Foot traffic, and foot traffic at all times throughout the week. With the explosion of residential development and the increase in high-end condos being filled faster than they can be constructed – downtown Minneapolis is breeding a perfect environment for a booming retail scene. The residential market in Minneapolis is growing faster than anyone anticipated with numbers exceeding projections exponentially. In 2016 downtown Minneapolis population was 40,864, a 31.5 percent increase since 2006. According to the Minneapolis Downtown Council, that number will double by 2025.

Increased residential foot traffic will help to strengthen downtown populations in the evening, but the healthy office industry is filling the sidewalks from 9 – 5. Office daytime population is a strong indicator for potential retailers and restaurants and the office economy in downtown Minneapolis is flourishing. Tech, public relations and creative firms are flocking to the exposed brick and timber vibes of historic office buildings. Traditional law firms and accounting firms are refreshing their Class A spaces to attract and retain millennial talent that is now the largest generation in the workforce. These office inhabitants are the people who are thriving in a healthy economy – which means they’ve got money to spend at restaurants, local shops and at grocers, like Whole Foods Market on their way home.

The Twin Cities continues to raise its profile when it comes to tourism, and tourism means more people walking our streets. Most recently, the metro area was named as the 4th best city for an affordable getaway by Food and Wine, the 12th best place to celebrate New Year’s Eve and the 10th best city for football fans, both by WalletHub. These accolades are proof that Minneapolis continues to be a growing tourist destination. New development, top restaurants, state-of-the-art sports venues like U.S. Bank Stadium and Target Field and our active social scene continues to drive people into downtown Minneapolis only adding to the potential to strengthen and define the best-fit retail presence.

What does it all mean? We’ve proven that we have a captive audience in downtown Minneapolis with money to spend. Office, residential and tourism in a strong economy will only continue to drive the potential for successful retail in this market. The Twin Cities metro is a wealthy, educated community, but in true Midwestern-fashion, we expect and shop for value. A high-end big-box retailer may not succeed in this market as opposed to somewhere that Midwest values aren’t so widespread. The addition of Saks Off 5th Avenue and Nordstrom Rack could prove successful for the bargain-minded crowd. We’ve got a captive audience for retail and we love a good bargain, but one thing we’ll pay more for is to support our local retailers. We’re willing to look beyond value when it comes to supporting our local and homegrown products.

Downtown retail is not dead…or dying. The reboot will lead to a reenergized market, but only if it includes retail options that fit market and consumer demands. A new era of boutique, local, catered and custom retail options will emerge along with scaled-down big box retailers to create a uniquely Minnesotan twist on the new version of downtown Minneapolis retail.

Spotlight Trends: Retail Reboot in Downtown Minneapolis

8 Minneapolis-St. Paul Research & Forecast Report | February 2017 | Retail | Colliers International

The above is a list of tenants that have signed leases during the current quarter and not actual absorption, which is recorded when the tenant opens at the location.

Goodwill Continues to expand in this market, opening two new stores during the quarter in White Bear Lake and Oak Park Heights.

Lease Activity

TENANT PROPERTY ADDRESS CITY SF SUBMARKET

Hobby Lobby Burnhill Plaza 1200-1400 County Rd 42 W Burnsville 50,019 Southeast

Furniture Barn Midway Corners Development 1365-1389 University Ave W University Ave & Albert St Saint Paul 26,000 Northeast

Goodwill 4500 Centerville Rd 4500 Centerville Rd White Bear Lake 20,600 Northeast

Goodwill Krueger Ln Krueger Ln Oak Park Heights 20,600 Northeast

Aldi Plaza 3000 3000 White Bear Ave Maplewood 18,375 Northeast

Petco Central Park Commons A-B-C-D 1505 Central Park Commons Dr Eagan 15,125 Southeast

The Tile Shop Central Park Commons T & U 1440-1460 Central Park Commons Dr Eagan 13,984 Southeast

Tutor Time 4673 White Bear Pkwy 4673 White Bear Pkwy White Bear Lake 11,263 Northeast

Family Dollar Town & Country Square 1901 Cliff Rd Burnsville 9,200 Southeast

Dollar Tree Highland Plaza Shopping Center 3001-3047 Nicollet Ave Minneapolis 9,024 Southwest

Clothes Mentor Riverdale Crossing Bldg D & E 13040-13060 NW Riverdale Dr Coon Rapids 7,491 Northeast

Famous Footwear Marketplace at 42 14020-14130 Highway 13 S Savage 6,220 Southwest

Medical Express Urgent Care 7658 Brooklyn Blvd 7658 Brooklyn Blvd Brooklyn Park 5,678 Northwest

Peoples Bank 1909-1911 Highway 36 W 1909-1911 Highway 36 W Roseville 5,055 Northeast

Med Express 1963 Robert St S 1963 Robert St S Saint Paul 4,620 Southeast

3Soteric Life Stonegate Plaza 5213-5293 Shoreline Dr 5229 Shoreline Drive Mound 4,460 West

Rainbow Apparel Robin Center 4048 Lakeland Ave N 4114 Lakeland Ave N Robbinsdale 4,320 Northwest

ATT Crossroads on 7 415 N 17th Ave Hopkins 3,090 Southwest

Significant Lease and Sales Activity

9Minneapolis-St. Paul Research & Forecast Report | February 2017 | Retail | Colliers International

Sales Activity

PROPERTY NAME ADDRESS CITY BUYER SELLLER SF PRICE PRICE PSF

Mills Fleet Farm 8400 Lakeland Ave N Brooklyn Park Davidson Kempner KKR 246,891 $38,487,827 $156

Mills Fleet Farm 1935 Levi Griffin Rd Carver Davidson Kempner KKR 270,006 $28,278,306 $105

Fridley Market 250 57th Ave NE Anoka Sterling Organization Tri-Land Properties, Equity Grp Invts 145,121 $26,750,000 $184

Mills Fleet Farm 10250 Lexington Ave NE Anoka Davidson Kempner KKR 245,575 $25,719,595 $105

Mills Fleet Farm 5635 Hadley Ave N Oakdale Davidson Kempner KKR 236,711 $24,791,249 $105

Hy-Vee 9349 Zane Ave N Minneapolis Hurd Real Estate Services Ryan Companies 103,882 $24,100,000 $232

Mills Fleet Farm 17070 Kenrick Ave Lakeville Davidson Kempner KKR 202,669 $21,225,958 $105

Oak Park Plaza 10855 University Ave NE Anoka Sterling Organization Tri-Land Properties,

Equity Grp Invts 105,360 $16,750,000 $159

Zachary Square Shopping Center 11395 96th Ave N Maple Grove Walter Cox; Parnassus

Preparatory School Buhl Investors 110,000 $13,575,000 $123

Burnsville Market 1750 County Rd 42 W Burnsville Sterling Organization Tri-Land Properties,

Equity Grp Invts 137,396 $10,000,000 $73

Walgreens 2610 Central Ave NE Minneapolis Green Family Partners LLC Capital Real Estate 16,685 $8,910,000 $534

11633-11651 Ulysses Street

11633-11651 Ulysses St NE Anoka Cole Capital Ryan Companies 33,500 $7,030,000 $210

Riverdale Village 3570 River Rapids Dr Anoka River Rapids Prop LLC OneCorp 11,221 $6,600,000 $588

Butcher & The Boar 1121 Hennepin Ave Minneapolis STORE Capital (REIT)Butcher & The Boar; Douglas A Van Winkle

5,140 $6,000,000 $1,167

Walgreens 4880 Central Ave NE Anoka Harbor Group Int'l 13,650 $6,000,000 $440

Trader Joes 9102 Hudson Rd Woodbury Clarion Partners Loja Group LLC 16,310 $5,990,000 $367

590 Prairie Center Drive 590 Prairie Center Dr Eden Prairie Sentinel Management Co OneCorp 7,233 $5,775,000 $798

Hobby Lobby 2600 American Blvd W Minneapolis Doug Hoskin, Com'l

Prtnrs Exchange CoPine Tree Commercial 64,130 $5,750,000 $90

Walgreens - Brooklyn Park 7700 Brooklyn Blvd Minneapolis Rodin Global Prop Trust Walgreens 15,120 $5,408,780 $358

Walgreens - Woodbury 1965 Donegal Dr Woodbury Rodin Global Prop Trust Walgreens 15,120 $5,408,780 $358

Terrace Center 3501 W Broadway Ave Minneapolis Inland Development

Partners LLC Brixmor 135,023 $5,200,000 $39

Great Plains Center 7905 Great Plains Blvd Chanhassen Anil K Jain NHH Properties 10,186 $4,820,000 $473

PetSmart 10451 Baltimore St NE Anoka Adam Young and Julie B

Young Living Trust Buhl Investors 17,014 $4,511,000 $265

fmr Central Valu Center 4300 Central Ave NE Anoka Hy-Vee Brixmor 126,665 $3,850,000 $30

Lino Lakes Marketplace 717 Apollo Dr Anoka Anil K Jain Pine Ridge Capital 18,027 $3,250,000 $180

Lake Shoppes 834 Lake St S Forest Lake Rtf Investments LLC Roseside Resources LLC 65,494 $2,800,000 $43

Blair Arcade East (Retail) 165 Western Ave N Saint Paul Excelsior Group Ted Glasrud Associates 25,000 $2,414,280 $97

8078 Brooklyn Blvd 8078 Brooklyn Blvd Minneapolis STORE Capital (REIT) David Hayes 6,700 $2,100,000 $313

Significant Lease and Sales Activity

10 Minneapolis-St. Paul Research & Forecast Report | February 2017 | Retail | Colliers International

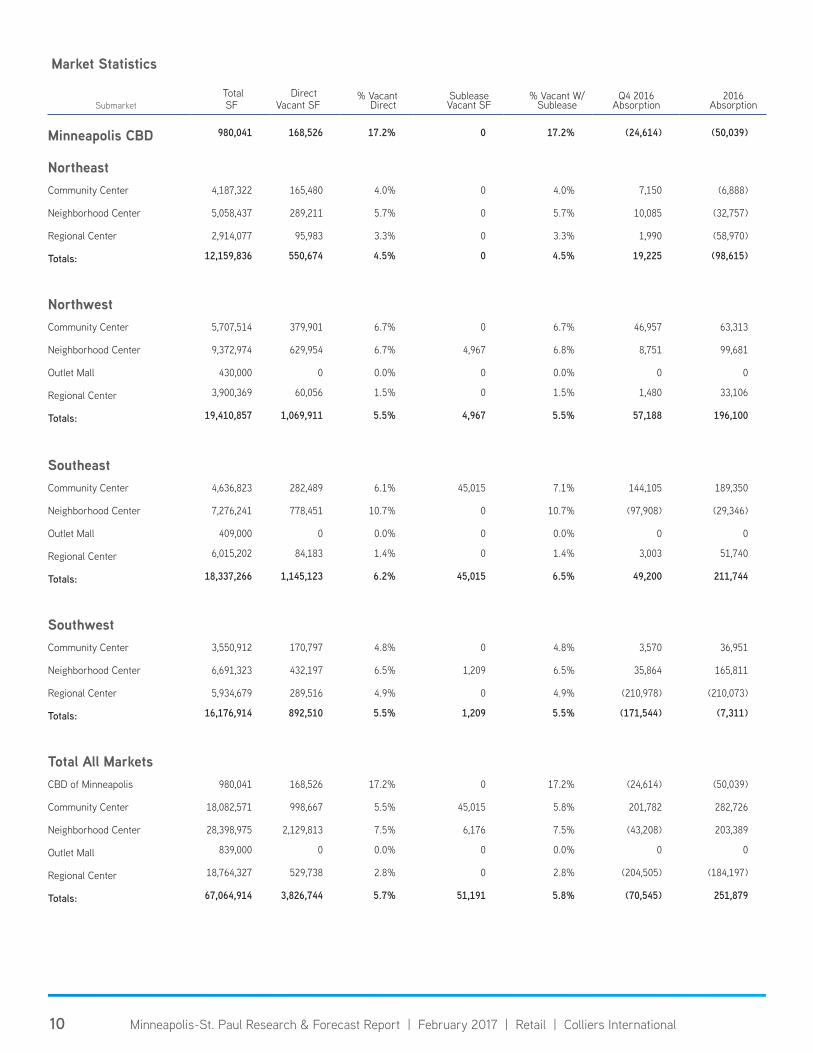

Submarket Total SF

Direct Vacant SF

% Vacant Direct

Sublease Vacant SF

% Vacant W/ Sublease

Q4 2016Absorption

2016 Absorption

Minneapolis CBD 980,041 168,526 17.2% 0 17.2% (24,614) (50,039)

NortheastCommunity Center 4,187,322 165,480 4.0% 0 4.0% 7,150 (6,888)

Neighborhood Center 5,058,437 289,211 5.7% 0 5.7% 10,085 (32,757)

Regional Center 2,914,077 95,983 3.3% 0 3.3% 1,990 (58,970)

Totals: 12,159,836 550,674 4.5% 0 4.5% 19,225 (98,615)

NorthwestCommunity Center 5,707,514 379,901 6.7% 0 6.7% 46,957 63,313

Neighborhood Center 9,372,974 629,954 6.7% 4,967 6.8% 8,751 99,681

Outlet Mall 430,000 0 0.0% 0 0.0% 0 0

Regional Center 3,900,369 60,056 1.5% 0 1.5% 1,480 33,106

Totals: 19,410,857 1,069,911 5.5% 4,967 5.5% 57,188 196,100

SoutheastCommunity Center 4,636,823 282,489 6.1% 45,015 7.1% 144,105 189,350

Neighborhood Center 7,276,241 778,451 10.7% 0 10.7% (97,908) (29,346)

Outlet Mall 409,000 0 0.0% 0 0.0% 0 0

Regional Center 6,015,202 84,183 1.4% 0 1.4% 3,003 51,740

Totals: 18,337,266 1,145,123 6.2% 45,015 6.5% 49,200 211,744

SouthwestCommunity Center 3,550,912 170,797 4.8% 0 4.8% 3,570 36,951

Neighborhood Center 6,691,323 432,197 6.5% 1,209 6.5% 35,864 165,811

Regional Center 5,934,679 289,516 4.9% 0 4.9% (210,978) (210,073)

Totals: 16,176,914 892,510 5.5% 1,209 5.5% (171,544) (7,311)

Total All MarketsCBD of Minneapolis 980,041 168,526 17.2% 0 17.2% (24,614) (50,039)

Community Center 18,082,571 998,667 5.5% 45,015 5.8% 201,782 282,726

Neighborhood Center 28,398,975 2,129,813 7.5% 6,176 7.5% (43,208) 203,389

Outlet Mall 839,000 0 0.0% 0 0.0% 0 0

Regional Center 18,764,327 529,738 2.8% 0 2.8% (204,505) (184,197)

Totals: 67,064,914 3,826,744 5.7% 51,191 5.8% (70,545) 251,879

Market Statistics

BROKERAGE SERVICES CONTACT:William M. Wardwell SIOR

Executive Vice President | Brokerage Minneapolis-St. Paul+1 952 897 [email protected]

FOR MORE INFORMATION:Maura Carland Director of ResearchMinneapolis-St. Paul+1 952 828 [email protected]

Copyright © 2016 Colliers International.

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report.

554 offices in 66 countries on 6 continentsUnited States: 153 Canada: 34 Latin America: 24 Asia Pacific: 231 EMEA: 112

$2.5billion in annual revenue

2billion square feet under management

16,000professionals and staff

Colliers International | Minneapolis-St. Paul4350 Baker Road, Suite 400Minnetonka, MN 55343

www.colliers.com/msp

SUBSCRIBE TO OUR BLOG