retail confidence for christmas 2017 - barclays … · retail confidence for christmas 2017 the...

TRANSCRIPT

Retail Confidence for Christmas 2017The outlook for this year’s festive season

2 of 19

ContentsSurvey highlights 03

Executive summary 04

Christmas outlook: still room for cheer 05

Mixed fortunes for categories 07

Case study: Fortnum & Mason 09

The rise of multi-channel 11

Case study: Oliver Bonas 13

Influences on Christmas trading 15

Planning with care for Black Friday 17

Insight: British Retail Consortium 18

About the author 19

Wrapping up 19

The research for this report has been conducted by GlobalData as of 4th October 2017 from a sample size of 250

3 of 19

Survey highlights

Top 3 growth categories: Top 3 biggest challenges:

71%of retailers expect Christmas trading this year to be the same or better than last year

49%

expect Christmas revenues to grow this year

30%

of revenues expected to be from online sales

49%

of sales expected to be multi-channel

50%

say they will limit Black Friday deals to certain channels

Gift cards and vouchers Beauty and health Homewares Online competition Logistics stress IT failure

!

££££££

4 of 19

Executive summaryRetail sector shows resilience in the face of numerous challenges.

Retailers are demonstrating considerable resilience as they look ahead to festive trading this year, according to our annual Retail Confidence for Christmas survey. There is, however, also a mood of realism in the face of a number of challenges facing the sector.

Nearly a third of UK retailers say they are more confident about Christmas trading this year, while just under 40% say they feel about the same as last year.

The majority of retailers in our survey believe festive trading revenues will see moderate growth compared to last year, while just under a third think they will be flat.

There is, however, a greater emphasis on managing costs and protecting margins suggested by this year’s survey. This is perhaps not surprising given the uncertainties surrounding the economic impact of Brexit and rising costs brought about by business rates increases, the momentum of National Living Wage increases and the Apprenticeship Levy, as well as the impact on imports of the devaluation of the pound against both the dollar and the euro since the EU referendum.

Online and multi-channel forge ahead Our survey once again highlights the opportunities presented by online Christmas shopping. The retailers in our survey expect 30% of their revenues to come through online sales this

Christmas. Our research also shows that sales are becoming increasingly multi-channel, with nearly half of retailers expecting Christmas revenues to be generated in this way.

Black Friday appears to be diminishing in importance slightly, according to our survey, however it clearly still has a significant influence on Christmas sales, with close to three-quarters of respondents believing that Black Friday pulls sales forward. Retailers clearly don’t want to miss out but, equally, say they don’t want to discount too heavily – a difficult balancing act. Many say they intend to manage Black Friday more carefully this year to protect margins.

Meanwhile, the mixed overall outlook for the sector can be at least partly explained by diverging expectations about different retail categories. While gift cards, health and beauty, electricals and homeware, for example, are predicted to produce above average revenue growth, mixed or flat sales are anticipated in food and clothing, books and films.

Realism reigns There is considerable concern among the retailers in our survey about consumer confidence – over 40% believe it will have a negative impact on their Christmas trading. This is combined with other concerns relating in part to the UK’s imminent departure from the EU, in particular the impact on staff availability.

Data from GfK showed UK consumer confidence down one point in October, although its Major Purchases Index was up for the third month running.1 Office for National Statistics figures show that retail sales fell by 0.8% in September from their August level, although this was still a year-on-year increase compared with September 2016, continuing a long-term trend as the 53rd consecutive month of year-on-year increase in retail sales.2

Clearly times are getting tougher – but retailers should take care that their focus on costs and margins does not come at the expense of all-important investment in marketing and online capability to help them weather a tougher market.

1 GfK press release, 31 October 20172 https://www.ons.gov.uk/businessindustryandtrade/retailindustry/bulletins/retailsales/september2017#main-points

Our survey once again highlights the opportunities presented by online Christmas shopping

5 of 19

Christmas outlook: still room for cheerThe majority of retailers predict Christmas trading in 2017 will be as good or better than last year.

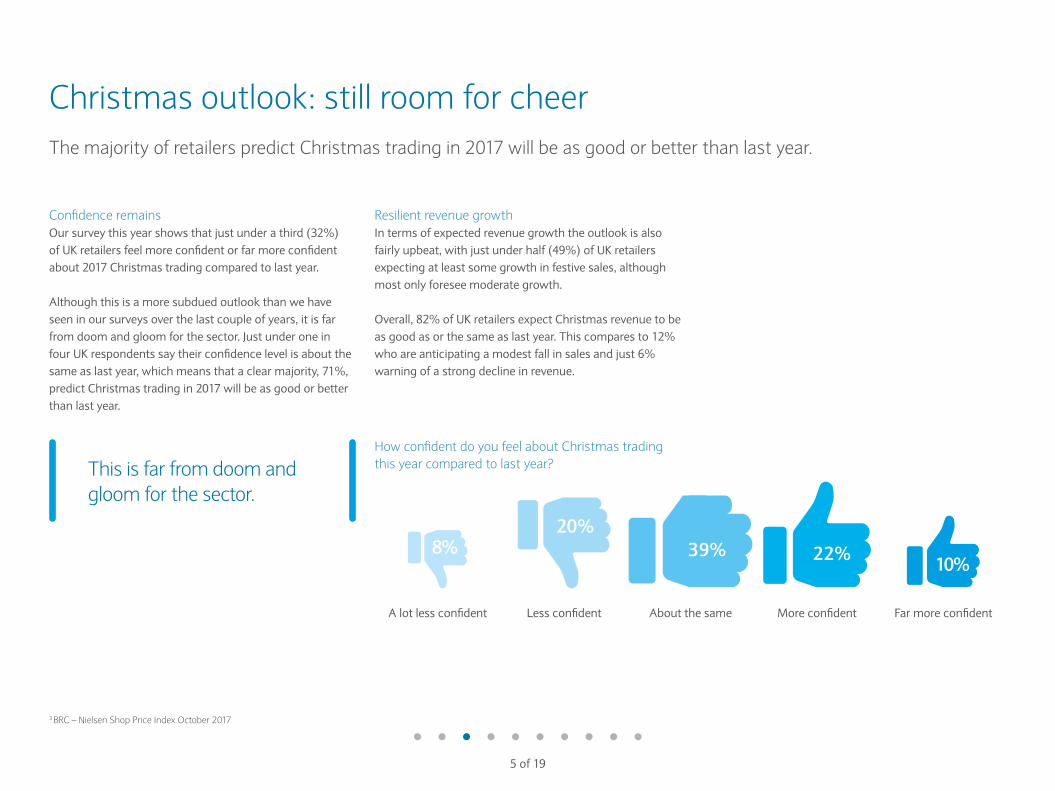

Confidence remainsOur survey this year shows that just under a third (32%) of UK retailers feel more confident or far more confident about 2017 Christmas trading compared to last year.

Although this is a more subdued outlook than we have seen in our surveys over the last couple of years, it is far from doom and gloom for the sector. Just under one in four UK respondents say their confidence level is about the same as last year, which means that a clear majority, 71%, predict Christmas trading in 2017 will be as good or better than last year.

Resilient revenue growthIn terms of expected revenue growth the outlook is also fairly upbeat, with just under half (49%) of UK retailers expecting at least some growth in festive sales, although most only foresee moderate growth.

Overall, 82% of UK retailers expect Christmas revenue to be as good as or the same as last year. This compares to 12% who are anticipating a modest fall in sales and just 6% warning of a strong decline in revenue.

This is far from doom and gloom for the sector.

3 BRC – Nielsen Shop Price Index October 2017

How confident do you feel about Christmas trading this year compared to last year?

A lot less confident Less confident About the same More confident Far more confident

8%20%

39% 22% 10%

6 of 19

Compared to last Christmas, how do you expect your company’s retail revenues to change this Christmas?

The latest data from the British Retail Consortium, however, offers a note of caution. It shows that while retail sales grew 2.1% in Q3 2017, price inflation is playing a significant role in the rate of growth, particularly for food revenues, which grew 3.5% in Q3, compared to 0.9% for non-food. Electronics saw year-on-year inflation in October for the first time since the BRC index started in 2006.3

It is also worth noting that our survey was undertaken before the threatened increase in interest rates became a reality with the Bank of England’s 0.25% adjustment in the base rate announced at the start of November.

Small/Moderate decline

12%

Flat

32%

Strong decline

6%

Strong growth

8%

Small/Moderate growth

40%

7 of 19

Mixed fortunes for categoriesWhile gift cards and vouchers are expected to perform strongly, the outlook is less promising for food and clothing.

Varied expectations Significant variations in expectations for retail sub-categories may explain the mixed outlook within the sector as a whole.

Our survey shows that retailers expect the gift card,health and beauty, electricals and homeware categories to see above-average growth rates, while food, clothing and DIY products are predicted to deliver mixed or flat returns this Christmas.

Gift cards and vouchers are expected to be the strongest performers with 64% of UK respondents predicting growth. This category has proved particularly resilient for a number of years now – reflecting consumer preference for practical solutions to the perennial gift-buying challenge which absolve shoppers of having to think too hard about what to give.

These findings may also reflect the growing importance of retail experiences over products. Research by Retail Economics and Squire Patton Boggs4 highlights this fundamental shift, with the traditional role of the store morphing into a more multifunctional experience-based

setting designed to invite, inspire, win and retain customers’ loyalty. The growing importance of this ‘experience economy’ will touch every part of the retail sector.

Health and beauty is expected to be the next best performing category, with just under 64% of retailers predicting revenue growth. Although this category has consistently delivered robust sales over the last few years, there is a slight decline in expectations for this Christmas compared to last year, perhaps in anticipation of softer sales of lower value products through supermarkets while higher-end department store sales remain strong.

Homeware and electricals are also expected to be strong with 60% of retailers expecting sales growth in the former and 51% in the latter.

Gift cards and vouchers are expected to be the strongest performers

Mixed views Views about Christmas trading prospects for food and groceryare mixed. Sales expectations are steady but not spectacular, with concerns around volumes. Almost two-thirds (64%) of UK retailers expect no growth or some decline.

While it looks like a similar story for clothing, there is some consolation for under-pressure fashion retailers that only 11% expect a decline in revenue. These figures reflect soft sales in a very competitive sector characterised by discount-savvy shoppers. The clothing sector is probably still a little over-serviced and there has arguably been insufficient investment in stores and product to attract footfall. Other retail categories that aren’t expected to do so well include DIY and home improvement – just 22% of retailers predict revenue growth in this category, although 62% think it will at least match Christmas 2016. A quarter of retailers expect spending on books to shrink and a third of our survey respondents think the same about music and film – no great surprise given the well-documented challenges these categories face.

4 The Retail Experience Economy: The Behavioural Revolution, 2017

8 of 19

Thinking about the following categories, how do you expect overall retail spending within each to change this Christmas compared to last?

0 10 20 30 40 50 60 70 80

Strong growth Small/Moderate growth Flat Small/Moderate decline Strong decline

Clothing, footwear, accessories

Food and grocery

Electricals

Homewares

Furniture and floor coverings

DIY and home improvement

Beauty and health

Books

Music and film

Stationery

Toys and games

Gift cards and vouchers

Luxury products

Experience gifts

Other

90 0 10 20 30 40 50 60 70 80 90

9 of 19

Case study: Fortnum & MasonThe famous London luxury retailer is reinventing Christmas for new audiences while staying true to its values and heritage.

For a business dedicated to providing customers with a little indulgence at Christmas and other important gifting seasons throughout the year, the festive period is more critical to Fortnum & Mason than for many other retailers. Chief Financial Officer Justin Carmichael says the key challenge each Christmas is judging the timing and scale of demand and providing a product mix that captures the imagination and offers customers “something beyond the monotony of the high street”. Dealing with the production and logistics required for its world famous Christmas hampers alone requires extensive detailed planning as well as a healthy dose of belief and confidence based on past experience, says Justin. But the modern Fortnum & Mason is about much more than Christmas hampers.

Riding the undercurrentsWith interest rates up and falling real earnings impacting wider consumer confidence, as well as higher operating cost and labour market pressures, Justin believes that the current market is a tough place to trade for retailers without a strong brand identity and expects the “squeezed middle” of the sector to face some choppy waters this Christmas.

With Christmas Day falling on a Monday this year he also expects a later buying pattern and a very strong last Friday as many people delay their shopping until the final week. Despite these challenges, Justin anticipates a strong Christmas trading for Fortnum & Mason, with growth across all channels, as customers trade into a brand they trust in more cautious times.

Refining the brandThe 300+ year old company has worked hard on repositioning its brand over the last few years, giving customers a more accessible entry point to high quality luxury gifts and treats, while remaining true to its values and heritage. Justin says these brand values are really important for what is still essentially a family business delivering change in the modern world of retail. “I believe customers are really looking for something different in a price-led, digital retail world. Provenance, quality and service are something we offer in abundance”. Innovation of product and services are key, continuing to push boundaries to make the brand relevant to today’s consumer – the roaring success of a gin & tonic flavoured tea as part of its ‘Oddi-Teas’ collection is a prime example, with over 7 million social views.

10 of 19

Experiential approach In many ways Fortnum & Mason epitomises the experiential approach to retail. “There’s been a gradual trend towards enhancing the in-store experience to give it a sense of occasion that digital can’t necessarily provide”, Justin says. This extends beyond the flagship store in London’s Piccadilly, to locations at key international travel hubs such as St Pancras and Heathrow’s T5 as part of a strategy to allow international travellers to take the brand home with them to key overseas markets. It also includes new innovations such as Fortnum’s lead sponsorship of the annual Skate festival at Somerset House, which includes pop-up retail and hospitality experience, as well as a click and collect service. As well as more innovative attractions like its in-store Steampunk experience, which brings theatre to the famous tea emporium. “Getting our products out of their packaging and allowing customers to interact with them, understanding their provenance and how to enjoy the sense of occasion is a big part of the in-store experience.”

Logistics challengeJustin anticipates that a later Christmas shopping pattern this year will be even more pronounced online due to greater consumer trust in digital platforms to deliver at the last minute. Ironically, the investments that so many retailers have made in more robust logistics and IT infrastructures to cope with fast delivery will be placing even greater pressure on them by encouraging people to shop later. “The big change is what logistics providers now offer, both to us as a customer and in the services our customers receive, such as named day or Sunday delivery or collection from a site of your choice. The customer experience extends beyond the stores and online, to their experience with our logistics partners, so they have to share our values.” Fortnums has recently extended the capacity of its distribution centre by 40% to put itself in a stronger position to meet its customer needs and continue to drive double digit growth.

Digital reach“Digital obviously increases our accessibility and reach and reduces the barriers to growth as an international brand. It’s getting easier to track customer behaviour online and we combine this with monitoring in-store footfall and transactional data across locations and channels.”

Digital also provides Fortnum & Mason with great opportunities for personalisation, which is another important way to differentiate, whether it’s a personalised bottle of champagne or digital experiences like its Tea Post, a tea subscription service. Digital sits firmly under the remit of the Customer Experience Director on Fortnums’ Executive team and the business has seen consistent +20% growth over the last four years. The vast majority of the annual sales of its iconic hamper are made online.

Mixing up marketingSocial media plays an increasingly important role in Fortnums’ marketing mix, allowing the business to tap into the power of online communities and key influencers whose followers are increasingly able to make instant purchases based on their recommendations. A significant change in marketing approach this year has been an above-the-line press advertising campaign aimed at creating awareness outside Christmas, but which will also run weekly through the Christmas trading period. Justin expects the campaign to reinforce the already strong trends the business has seen this year as it looks forward to another record Christmas.

11 of 19

The rise of multi-channelOnline shopping is expected to grow to 30% of Christmas revenues and our research underlines the growing importance of multi-channel retail.

Online sales growthRespondents to our survey are clear that the proportion of revenue from online sales over Christmas 2017 is expected to be higher than in 2016. UK retailers expect 30% of their festive revenues through online channels, including desktop, laptop and mobile devices. That compares with expected revenues in physical stores of 66%.

This proportion of online revenues is roughly where we would expect it to be for the festive season, compared to a lower share at other times of the year. Office for National Statistics figures for September this year showed that 17% of all UK retail sales were through online channels. Some estimates suggest that the continuing changes in consumer habits will see online shopping grow to 46 million online purchasers by 2021.5

BRC figures show a year-on-year 2% drop in footfall across the UK’s shopping locations in October, with only retail parks managing to grow shopper numbers.6

Over 40% of the retailers in our survey say they will be investing in additional online capability or infrastructure this Christmas as a result of these trends.

Predicted sales through mobile devices, at 13%, are perhaps slightly lower than might be expected, given the attractions of buying Christmas gifts at work or during a commute with a smartphone or tablet. This could be because the significant growth in mobile shopping predicted last Christmas – 77% of UK retailers expected to see the most growth in that channel – didn’t quite materialise.

According to Facebook however, Christmas 2016 was the first time it saw its global mobile conversations overtake desktop. It also says UK mobile shoppers start their Christmas shopping earlier than desktop and store shoppers.7

UK retailers predict that almost half (49%) of their Christmas revenues will be multi-channel in 2017

5 https://www.barclayscorporate.com/insight-and-research/industry-expertise/from-browse-to-buy-the-conversion-challenge.html6 BRC - Springboard Footfall and Vacancies October 20177 Retail Gazette, 7 November 2017 https://www.retailgazette.co.uk/blog/2017/11/comment-marketers-put-mobile-first-christmas

12 of 19

Importance of multi-channel Our survey provides clear evidence of the growing importance of multiple customer touchpoints, for example, researching gifts in a physical store and then buying online, and vice versa. UK retailers predict that almost half (49%) of their Christmas revenues will be multi-channel in 2017.

According to Retail Economics’ research8, 40% of shoppers say they are likely to spend more with a retailer who offers a meaningful shopping experience in store. Its report suggests that, with customers more empowered than ever before, the key retail battleground is around creating meaningful experiences throughout the entire multi-channel customer journey. This highlights the critical importance of customer data and personalised content.

Converting multi-channel browsing into sales by making purchasing a seamless experience for consumers at every touchpoint is clearly a key challenge for retailers. It requires continued investment in technologies and processes that deliver what multi-channel customers want, including free delivery and free returns, access to customer reviews and simple checkout processes that do not require them to create an online account.

Maximising the potential of online and multi-channel sales clearly also requires strong digital expertise in the boardroom to complement traditional buying, merchandising and marketing skills.

What proportion of Christmas revenue do you expect will be multichannel – that is a sale that involves one or more channels (e.g. research in store, buy online; or, buy online, collect in store)?

66%

17%

13%

Onlinevia mobile devices

Onlinevia a desktop/laptop

Physical stores

3%

Mail order

1%

Other (specify)

8 The Retail Experience Economy: The Behavioural Revolution, 2017

13 of 19

Case study: Oliver BonasIndependent high street fashion and lifestyle chain Oliver Bonas is readier than ever for the peak in the retail calendar.

Christmas is clearly a key time for Oliver Bonas, given the nature of its offering, with profitability peaking and revenues doubling in December compared with the rest of the year, according to managing director and founder Oliver Tress.

In tracking year-on-year, like-for-like performance, Oliver says in-store spending tends to accelerate from the last week of November, peaking a week or two before Christmas. Meanwhile, e-commerce usually peaks a little earlier – about two or three weeks before Christmas. As customers’ confidence in online delivery has increased, online sales are now sustained for longer – right up to the week before Christmas.

While external factors such as Brexit and higher interest rates are an ever-present cause for concern for Christmas trading, Oliver says the company keeps its focus on the internal issues that are under its control.

Product mix“We want to be the best we can be,” says Oliver. “We have to get the product right and make sure we keep the ship pointing in the right direction.”

Adjusting the product mix and changing the way stores are merchandised is clearly critical over the Christmas trading period. Homeware and gifts really come into play and the Oliver Bonas stores give more space to items such as candles, frames and mugs, as well as accessories, while fashion options are reduced to those with a Christmas focus.

Coherent messageThe company has focused on building a more co-ordinated marketing strategy in the lead up to this festive season, working with its retail, e-commerce and digital marketing teams to ensure they put out the same messages about products at the same time. Oliver says they are also using Facebook more than ever to reach out to target customers.

“Our customers are very active Facebook users. This gives us opportunities to reach customers in a really targeted way and we spend a lot of time looking at what’s working, but it also presents a challenge because Facebook is always changing.”

Christmas is such a strong trading period for Oliver Bonas that it has so far felt little need to discount products in the run-up.

14 of 19

“We really believe our products are right, we price them appropriately in the beginning and want people to feel that we’re special. We think it takes away some of our brand value if we discount too much.”

This is reflected in a very cautious approach to Black Friday, with discounts limited to just a few items online on a category-by-category basis. “We don’t think it’s the right time for us and feel the short term benefits just get you into a cycle of discounting,” says Oliver. “We find just a few categories where we think it will work really well and use it as an opportunity to attract customers and we do get a massive uplift in traffic.”

Competitive edgeTo stay ahead of its mainstream competitors, who Oliver says are getting better and faster at producing more current, trend-led products, the company has to operate under shorter timeframes and be more daring with its products.

“Social media has given everyone access to more current design input than they used to have. There’s more and more demand for attractive, well-priced homeware, for example, because of the impact of social media sharing. The transmission of ideas happens more quickly and standards have improved.”

Around five years ago the company committed to selling its own label products, with almost everything designed in-house, except for items like greeting cards and books.

“We’ve stopped looking at Pinterest for design inspiration. Although there’s always a challenge in staying relevant, we need to trust our own judgement if we want to be more innovative, original and challenging than the competition. If you use the same social media as everyone else, then you’ll have the same products as everyone else. We look for more bedrock sources of inspiration.”

Customer journey With so many different touchpoints available to customers, Oliver says understanding what has driven a customer into the store or website is the holy grail of retail. Oliver Bonas has a number of measures in place including footfall counters in some stores that are then compared with conversion rates. They also look at how people have arrived at the website and where they have clicked through from.

“It can be an imperfect science – it doesn’t always give us a complete perspective, but we put a lot of effort into understanding the customer journey. In some ways this whole move to online has just heightened and exaggerated the basic retail tenets and you just have to be better at it than a few years ago.”

The futureWith another six stores set to open before Christmas to add to its 60-strong portfolio, the whole in-store experience remains critical for the company, especially in its bigger stores. Sales on the website grew by 93% last year, and while some retailers have struggled with bricks-and-mortar sales, Oliver Bonas’ in-store sales have grown consistently, with mid-single-digit like-for-likes last year.

“My instinct is that we’re getting a bit more mature as a business and facing a typical headwind in trying to grow online and in stores. We can’t predict the future with certainty, but it’s probably unreasonable to expect our stores to keep growing. Behaviour is changing.

“In the future there may come a point where a store isn’t massively profitable but it still contributes to the overall business strategy of bringing customers in and raising awareness. But we’re not yet at the point of having to make those difficult decisions.”

15 of 19

Influences on Christmas tradingWith consumer confidence beyond their control, retailers’ focus is on investing in marketing and online capacity.

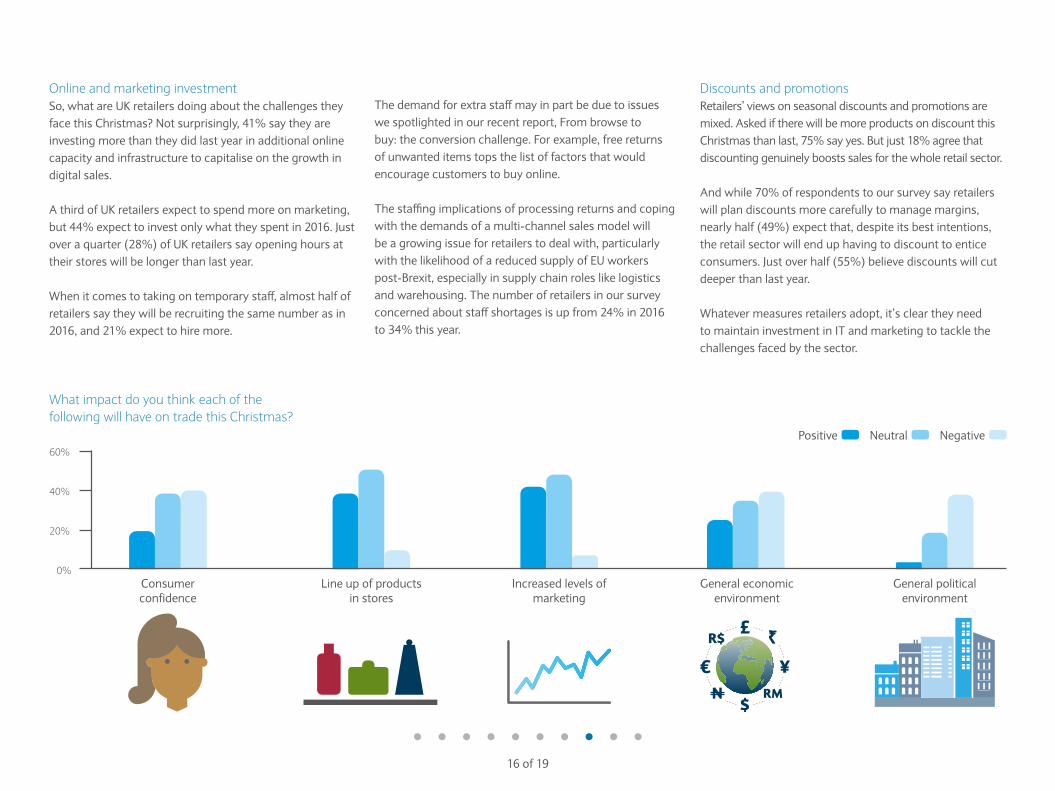

Biggest ImpactRetailers believe consumer confidence and the general economic environment will potentially have the biggest negative impact on trade this Christmas. Just over 40% are worried about shoppers’ confidence and the same number fear economic conditions could hit sales, with the threat of higher interest rates no doubt weighing heavily on some at the time of the survey.

Commenting on a one-point fall in its consumer confidence index in October, analysts at GfK said that consumers were showing “no real get-up-and-go” as concerns about the UK’s economic prospects dampened the outlook. However it said that spending on major items was up for the third month running, largely due to surging credit card use at the expense of saving.

The BRC says consumer spending power is being “squeezed, but not strangled”, with real wage growth still in negative territory. However, it believes the impact of this is being tempered by record low unemployment and continued consumer borrowing.

The retailers in our survey are more positive about the potential impact of factors within their control, such as the line-up of products in store and marketing spend. 43% of UK retailers say they expect more investment in marketing to have a positive impact, although half predict it will bring no change.

As ever retailers will need to be smart about their marketing and driving potential customers to multi-channel touchpoints will be vital.

Online giants the biggest challengeWhen asked about their expected biggest challenges over the coming Christmas season, growing competition from online retailers like Amazon and eBay are out in front. This year 69% of UK retailers say this is one of their main challenges, compared with 61% in our 2016 survey.

Concern about IT failures and logistics are also up significantly on last year – not surprisingly given the ever-growing volumes of online shopping. Concerns about logistics stress have risen from 40% last year to 49% this year, while the proportion of retailers worried about IT failure is up from 32% to 40%.

This sentiment reflects the well-documented difficulties faced by a number of retailers in dealing with festive trade volumes over the past couple of years. While Christmas 2016 might not have been as challenging as 2015, it is clear the sector is still focused on avoiding any repeat of past problems.

The steady march of online shopping of course presents opportunities as well as challenges and many retailers are grappling with how best to engage with the online giants while retaining control of their customer relationships and pricing.

Retailers believe consumer confidence and the general economic environment could have the biggest negative impact on trade this Christmas.

16 of 19

Online and marketing investmentSo, what are UK retailers doing about the challenges they face this Christmas? Not surprisingly, 41% say they are investing more than they did last year in additional online capacity and infrastructure to capitalise on the growth in digital sales.

A third of UK retailers expect to spend more on marketing, but 44% expect to invest only what they spent in 2016. Just over a quarter (28%) of UK retailers say opening hours at their stores will be longer than last year.

When it comes to taking on temporary staff, almost half of retailers say they will be recruiting the same number as in 2016, and 21% expect to hire more.

The demand for extra staff may in part be due to issues we spotlighted in our recent report, From browse to buy: the conversion challenge. For example, free returns of unwanted items tops the list of factors that would encourage customers to buy online.

The staffing implications of processing returns and coping with the demands of a multi-channel sales model will be a growing issue for retailers to deal with, particularly with the likelihood of a reduced supply of EU workers post-Brexit, especially in supply chain roles like logistics and warehousing. The number of retailers in our survey concerned about staff shortages is up from 24% in 2016 to 34% this year.

0%

20%

40%

60%

Consumer confidence

Line up of products in stores

Increased levels of marketing

General economic environment

General political environment

Positive Neutral Negative

What impact do you think each of the following will have on trade this Christmas?

Discounts and promotionsRetailers’ views on seasonal discounts and promotions are mixed. Asked if there will be more products on discount this Christmas than last, 75% say yes. But just 18% agree that discounting genuinely boosts sales for the whole retail sector.

And while 70% of respondents to our survey say retailers will plan discounts more carefully to manage margins, nearly half (49%) expect that, despite its best intentions, the retail sector will end up having to discount to entice consumers. Just over half (55%) believe discounts will cut deeper than last year.

Whatever measures retailers adopt, it’s clear they need to maintain investment in IT and marketing to tackle the challenges faced by the sector.

¥€

$RM

R$

N

R£

17 of 19

Planning with care for Black FridayRetailers are focused on managing discounts and sales offers to avoid the pitfalls and maximise the benefits.

Striking the right balanceLast year’s Black Friday did not prove to be as disruptive an event as it was in 2015 and the retail sector expects about the same level of activity in 2017. Nevertheless, the sector seems determined to plan more carefully for Black Friday this time around.

Our survey shows that close to three-quarters (72%) of retailers in the UK think the discounts offered on Black Friday will pull sales forward. Of these, the highest proportion (38%) says Black Friday brings between 1% and 9% of sales forward.

Damage limitation appears to be the approach that many retailers will be taking to the November sales. Strategies highlighted by our survey include limiting deals to particular stores, channels or product categories, curtailing the number of sale items and the lifespan of discounts.

Exactly half of our respondents say they will only offer deals through certain channels, for example just online or just at stores. The next most popular strategy is to offer discounts for shorter periods. Just over a third (36%) of retailers plan to limit the amount of product on offer, while 22% intend to be less generous with discounting.

However, most UK retailers say there will be more products on discount this Christmas than last year and 41% say discounting will start earlier in 2017.

Longer buying periodBRC figures9 show clear evidence of a double sales hump that didn’t exist before Black Friday. Despite the reservations about Black Friday among the retailers we surveyed, it seems unlikely that the longer Christmas buying period starting in October will disappear any time soon.

Clearly, retailers still see Black Friday as important but our survey indicates that most intend to manage it more carefully in order to protect margins. Of course this is a fine line to tread: retailers clearly don’t want to miss out on the volume of sales the event offers but, equally, don’t want to discount too heavily at the busiest time of the shopping year.

This raises some important questions about when and how deep to discount? Retailers will be monitoring trading conditions very closely and will need the agility to respond to fluctuations in the market, such as rapid changes in consumer confidence perhaps caused by external events such as the recent increase in the Bank of England base rate.

Most UK retailers say there will be more products on discount this Christmas than last year and 41% say discounting will start earlier

What things are you doing for Black Friday this year?

9 BRC release, 6 December 2016 www.brc.org.uk/news/2016/black-friday-drives-record-online-penetration

Being less generous with discounts

Limiting deals to certain channels – e.g. just

stores, just online, etc.

Limiting offers to certain customers

Not participating in the Black Friday

eventOther/Nothing

Offer discounts for a very short period

of time

41

Limiting the amount of product on offer

36

22Buying in special

purchase products

40

5014

27 19

18 of 19

Insight: British Retail ConsortiumRachel Lund, Head of Retail Insight and Analytics at the British Retail Consortium looks at some of the key factors expected to impact on Christmas trading this year.

Christmas can see some retailers clearing 30% more sales than in an average month. However, this year, the UK economic backdrop could have a big impact on how well this period of traditionally increased consumer activity will go.

UK retail sales for October were pretty weak: they fell by 1% on a like-for-like basis from October 2016, while footfall was down 2% year-on-year. This doesn’t necessarily mean Christmas 2017 is going to be disappointing for all retailers, given that month by month short-term factors can lead to volatility in sales, but it does indicate that there is some underlying weakness in consumer spending.

Buying powerDespite the media attention on Brexit, our experience is that consumers’ focus is on their own personal finances. Wages are being squeezed in real terms and although credit cards and other forms of borrowing are helping to fill the gap, our expectation is that with pressures on household budgets this Christmas is unlikely to be much bigger for retail sales compared to last year.

Food is an integral part of the festivities, but with higher prices on average this year we may see consumers less inclined than usual to shift up to premium-range items at Christmas. Nonetheless, food sales are likely to absorb more of households’ spending, leaving a tougher market for non-food retail.

Even with consumers’ budgets under strain, however, there may still be some strong performing high-end products that are particularly valued. So, within categories like clothing, electronics and homeware there might be one relatively expensive product that does very well, while other less distinctive items struggle. As always, the challenge for retailers is having the right product at the right price.

A question of timingThe fact Christmas Day fell on a Sunday last year encouraged people to do more last-minute shopping and drove a lot of late sales in-store. Even so, online non-food Christmas sales in 2016 grew 7.2% compared to 2015, compared to total year-on-year sales growth of just 1.7%, continuing the consistent shift to online we’ve witnessed over the last few years.

Many retailers have made considerable investments in logistics as they compete to enhance their delivery services. So while we expect the store to be dominant in the final week before Christmas again this year, online may make further inroads as consumers put their faith in next-day or same-day delivery in the final few days.

Of course Black Friday has been a disruptive factor over the past few years with slightly more Christmas sales at a discount as a result. While this causes a headache for retailers, many will participate in some manner. Black Friday in 2016 did see an uplift in sales on the day, but over the whole week sales weren’t significantly above 2015 and we expect something similar this year.

19 of 19

To find out more about our Retail and Wholesale team, or to access more of our thought leadership materials, visit barclays.com/corporatebanking Barclays Bank PLC is registered in England (Company No. 1026167) with its registered office at 1 Churchill Place, London E14 5HP. Barclays Bank PLC is authorised by the Prudential Regulation Authority, and regulated by the Financial Conduct Authority (Financial Services Register No. 122702) and the Prudential Regulation Authority. Barclays is a trading name and trade mark of Barclays PLC and its subsidiaries.

IBIM7596. November 2017.

• 71% of UK retailers believe the 2017 festive season will be as good or better than last year

• Just under half of retailers expect to increase revenue this Christmas, but there is a greater emphasis on managing costs

• Gift cards, health and beauty, electricals and homeware are expected to be the strongest categories, with mixed or flat sales anticipated in food and clothing, books and films

• Retailers expect 30% of their revenues through online sales this Christmas – and there is clear evidence of the growing importance of multi-channel shopping

• In addition to online competition, retailers see logistics and IT failures as their biggest challenges this Christmas

• Over 40% believe consumer confidence will have a negative impact on their Christmas trading

• Black Friday may be becoming less important, but requires careful management to protect margins, for example by restricting deals to certain channels

Wrapping upAbout the authorIan Gilmartin is Head of Industry for Retail and Wholesale at Barclays Corporate Banking across the UK and Ireland, where Barclays has operated a sector specialism for almost 30 years. He and his team of Relationship Directors are

responsible for thousands of clients, ranging from boutique fashion houses and high-street booksellers to department stores and listed companies.

Ian has over 20 years of corporate banking experience and has spent the last five years providing specialist banking services to retailers and wholesalers as part of the leadership within Barclays Retail and Wholesale team. Prior to that he was a Senior Relationship Director in the Technology, Media and Telecoms team, and has experience of other sector verticals from his early career.

Since taking on his current role, Ian has become a regular commentator in the national, regional and trade media on retail trends and industry issues, as well as retail sales figures.

Ian Gilmartin Head of Retail and Wholesale Corporate Banking

T: 020 7116 [email protected]