republic of tunisia - oecd · 25 3.5 infant mortality republic of tunisia: country assistance...

TRANSCRIPT

Republic of TunisiaCountry Assistance Evaluation

2004The World Bank

Washington, D.C.

W O R L D B A N K O P E R A T I O N S E V A L U A T I O N D E P A R T M E N T

http://www.worldbank.org/oed

Advance Copy

© 2004 The International Bank for Reconstruction and Development / The World Bank

1818 H Street, NW

Washington, D.C. 20433

Telephone: 202-473-1000

Internet: www.worldbank.org

E-mail: [email protected]

All rights reserved

Manufactured in the United States of America

First edition September 2004

The findings, interpretations, and conclusions expressed here are those of the author(s) and do not necessarily reflect the

views of the Board of Executive Directors of the World Bank or the governments they represent.

The World Bank cannot guarantee the accuracy of the data included in this work. The boundaries, colors,

denominations, and other information shown on any map in the work do not imply on the part of the World Bank any

judgment of the legal status of any territory or the endorsement or acceptance of such boundaries.

Rights and Permissions

The material in this publication is copyrighted. Copying and/or transmitting portions or all of this work without permission

may be a violation of applicable law. The World Bank encourages dissemination of its work and will normally grant

permission promptly.

For permission to photocopy or reprint any part of this work, please send a request with complete information to the

Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, USA, telephone 978-750-8400, fax 978-750-4470,

www.copyright.com.

All other queries on rights and licenses, including subsidiary rights, should be addressed to the Office of the Publisher,

World Bank, 1818 H Street NW, Washington, DC 20433, USA, fax 202-522-2422, e-mail [email protected].

Cover photos courtesy of the World Bank Photo Library.

ISBN 0-8213-5974-6

e-ISBN 0-8213-5975-4

Library of Congress Cataloging-in-Publication data have been applied for.

Printed on Recycled Paper

World Bank InfoShop

E-mail: [email protected]

Telephone: 202-458-5454

Facsimile: 202-522-1500

Operations Evaluation Department

Knowledge Programs and Evaluation Capacity

Development (OEDKE)

E-mail: [email protected]

Telephone: 202-458-4497

Facsimile: 202-522-3125

This advance copy of the Tunisia Country Assistance Evaluation is provided for the convenience of the attendees atthe Conference on Effectiveness of Policies and Reforms: What We Have Learned. Although every effort has beenmade to ensure the accuracy of this advance copy, some elements contained herein may be corrected or otherwisealtered in the course of publication. The published evaluation, which will be available next month, remains the docu-ment of record.

i i i

v Acknowledgments

vii Preface, Prefacio, Préface

ix Executive Summary, Résumen, Résumé Analytique

xvii Acronyms and Abbreviations

1 1 Tunisia’s Socioeconomic Development: Progress Achieved and Challenges Ahead 1 Background 3 Poverty and Social Conditions 5 Debt Burden and External Assistance 5 Meeting the Challenges of Globalization

9 2 World Bank Assistance Program9 World Bank Assistance Strategies 10 Economic and Sector Work 13 Lending

17 3 The Development Impact of World Bank Assistance17 Macroeconomic Stabilization, Growth, and Structural Reforms 22 Human Development and Progress toward MDGs 26 Poverty Alleviation and Rural Development 28 Outcome, Sustainability, and Institutional Development

31 4 Contributors’ Performance31 Tunisia’s Own Central Role 32 The World Bank’s Performance 33 Other Development Partners 34 Exogenous Factors

37 5 Recommendations

39 Annexes41 A: Statistical Annexes 79 B: List of People Met on Mission in Tunisia (and World Bank and IMF

Staff Interviewed) 83 C: Guide to OED’s Country Assistance Evaluation Methodology 87 D: Management Action Record

Contents

89 Attachments89 1: Islamic Development Bank—Tunisia Country Assistance Evaluation 93 2: Report from the Committee on Development Effectiveness (CODE)

97 Endnotes

99 References

Boxes7 1.1 Mise à niveau Program (Enterprise Restructuring and Upgrading)11 2.1 World Bank Strategies23 3.1 Tunisia’s Progress in Meeting the Millennium Development Goals

Tables3 1.1 Tunisia’s Export Diversification, 1980–013 1.2 Main Macroeconomic Indicators4 1.3 Poverty and Inequality Trends in Tunisia, 1990–004 1.4 Selected Human Development Indicators in Tunisia and Comparator

Countries6 1.5 Tunisia: Net Receipts of External Financial Resources, 1990–01 13 2.1 Distribution of World Bank Commitments by Sector (FY90–03)14 2.2 IBRD Proposed and Actual Lending, FY97–0214 2.3 OED Evaluation Findings of Recently Evaluated Projects by Value18 3.1 Tunisia and Comparators: Per Capita Income Indicators21 3.2 Privatization by Sector, in million Tunisian Dinar 28 3.3 Northwest Mountainous Areas Development Project: Selected Results

from the 2000 Survey

Figures10 2.1 Bank Commitments, Disbursements, and Transfers21 3.1 Business Climate Indices for Tunisia, MNA, and OECD 25 3.2 Education System Expansion at the Post-Basic Level25 3.3 Net Primary Enrollment25 3.4 Illiteracy25 3.5 Infant Mortality

R E P U B L I C O F T U N I S I A : C O U N T R Y A S S I S TA N C E E VA L U AT I O N

i v

v

Acknowledgments

Fareed M. A. Hassan was the Task Manager for thisreport and acknowledges with thanks the con-tributions by Adil Kanaan and Isabelle Tsakok(Consultants). Ibrahim A. Elbadawi and JorgeGarcia-Garcia reviewed the report. Gonzalo Sali-nas provided statistical information and JaniceJoshi, administrative support.

The evaluation is the second cooperative ef-fort with the Islamic Development Bank, fol-lowing the joint evaluation of the Jordanprogram. The support of Bader Eddine Nouioua,Adviser, Operations Evaluation and Audit, IDB,and Djelloul Al-Saci, Head, Operations Evalua-

tion Office, IDB, is greatly acknowledged. Gre-gory K. Ingram, Director-General, OperationsEvaluation, and Kyle Peters, Senior Manager,OEDCR, provided overall guidance, with substantial input into the formulation of the report.

Special thanks are due to the officials of thegovernment of Tunisia for their valuable assis-tance and to the civil society and donor repre-sentatives interviewed in the country. The reporthas also benefited significantly from helpful andconstructive suggestions from numerous WorldBank, IDB, and IMF staff.

Director-General, Operations Evaluation: Gregory K. IngramDirector, Operations Evaluation Department: Ajay Chhibber

Senior Manager, Country Evaluation & Regional Relations: R. Kyle PetersTask Manager: Fareed M.A. Hassan

PREFACE

This Country Assistance Eval-uation (CAE) on Tunisia is the secondcooperative effort with the OperationsEvaluation Office (OEO) of the IslamicDevelopment Bank, following the jointOED-OEO assessment of the JordanProgram. The two institutions carriedout a joint assessment of Tunisia’s eco-nomic and social development since1990 and the challenges facing thecountry. There will be two separatereports; the assessments of each in-stitution’s assistance program wereprepared in parallel. This report ben-efited from consultations and com-ments from OEO staff, and the twoevaluations generally agree on theiranalysis. The Executive Summary ofthe Islamic Development Bank’s re-port is attached (Attachment 1).

A joint OED-OEO mission visitedTunisia in September 2003. The visitwas facilitated by arrangementsmade by the staff of the TunisianMinistry of Economic Developmentand International Cooperation. Theircooperation and assistance is grate-fully acknowledged.

The report is organized as fol-lows: Chapter 1 assesses Tunisia’ssocioeconomic development and thechallenges ahead. This chapter iscommon to the evaluation reports ofboth the World Bank and the IslamicDevelopment Bank. The subsequentchapters examine the effectiveness ofWorld Bank assistance in addressingthese challenges. The last chaptermakes recommendations.

This Country Assistance Evalua-tion was written by Fareed M.A. Has-

PREFACIO

La presente Evaluación de laAsistencia al País (EAP) para Túnezes la segunda iniciativa en coopera-ción con la Oficina de Evaluación deOperaciones (OEO) del Banco Islámicode Desarrollo (BIsD), tras la evalua-ción conjunta del DEO y la OEO delPrograma para Jordania. Ambas insti-tuciones llevaron a cabo una evalua-ción conjunta del desarrolloeconómico y social de Túnez desde1990, así como de los desafíos que elpaís enfrenta. Se entregarán dos in-formes independientes; las evalua-ciones del programa de asistencia decada institución han sido elaboradasen paralelo. Este informe contó con elaporte de consultas y comentarios delpersonal de la Oficina de Evaluaciónde Operaciones; en términos genera-les, las dos evaluaciones concuerdanen su análisis. Se adjunta la Reseña delinforme del Banco Islámico de Desa-rrollo (Anexo 1).

En septiembre de 2003, una mi-sión conjunta del DEO y la OEO efec-tuó una visita a Túnez. La visita fuepropiciada por las gestiones del per-sonal del Ministerio de DesarrolloEconómico y Cooperación Interna-cional de Túnez, al que debemosnuestro reconocimiento y gratitudpor su cooperación y asistencia.

El informe se organiza como sedetalla a continuación. El Capítulo 1evalúa el desarrollo socioeconómicode Túnez y los desafíos futuros. Esecapítulo es común a los informes deevaluación del Banco Mundial y elBanco Islámico de Desarrollo. Loscapítulos subsiguientes examinan la

PRÉFACE

La présente Évaluation del’aide par pays (CAE) sur la Tunisie estle second effort de collaboration avecle Bureau de l’évaluation des opéra-tions (OEO) de la Banque islamique dedéveloppement, suite à l’évaluationconjointe OED-OEO du Programme jor-danien. Les deux institutions ont menéà bien une évaluation conjointe du dé-veloppement économique et social dela Tunisie depuis 1990 et des défis aux-quels est confronté le pays. Il y auradeux rapports séparés ; l’évaluationdu programme d’aide de chaque insti-tution a été préparée en parallèle. Cerapport a bénéficié des consultationset des commentaires du personnel del’OEO et les deux évaluations concor-dent de manière générale dans leuranalyse. La note de synthèse du rapportde la Banque islamique de dévelop-pement est ci-jointe (Pièce jointe 1).

Une mission conjointe OED-OEOs’est rendue en Tunisie en sep-tembre 2003. Cette visite a été faci-litée par les arrangements effectuéspar le personnel du Ministère tuni-sien du développement économiqueet de la coopération internationale.Nous tenons ici à les remercier deleur coopération et de leur aide.

Le rapport est organisé commesuit : Le chapitre 1 est une évaluationdu développement socioécono-mique de la Tunisie et des défis aux-quels elle va être confrontée. Cechapitre est commun aux deux rap-ports d’évaluation, celui de laBanque mondiale et celui de laBanque islamique de développe-ment. Dans les chapitres suivants

P R E FA C E

v i i

EN

GL

ISH

FR

AN

ÇA

IS

ES

PA

NO

L

san (Task Manager) with con-tributions by Djelloul Al-Saci(IDB); Adil Kanaan, IsabelleTsakok, and Elaine W. Ooi(Consultants). Gonzalo Sali-nas and Janice Joshi providedstatistical analysis and ad-ministrative support.

Ibrahim Elbadawi and Jorge Gar-cia-Garcia peer-reviewed the report.The assistance of peer reviewers inproviding detailed comments on anearlier draft is gratefully acknowl-edged. Those comments, as well asothers, received during OED’s man-agement review meeting, have beentaken into account in the evaluation.

Comments from the RegionalManagement of the Bank have alsobeen reflected in the report. TheRegional response to the Manage-ment Action Record is included asAnnex D. Copies of the draft reportwere sent to the government forreview, and no written commentswere received.

eficacia de la asistencia delBanco Mundial para abordarestos desafíos. El último ca-pítulo presenta recomenda-ciones.

Esta Evaluación de Asis-tencia al País ha sido redac-tada por Fareed M.A. Hassan

(Gerente de tareas), con los aportesde Djelloul Al-Saci (BIsD); Adil Ka-naan, Isabelle Tsakok y Elaine W. Ooi(Consultores). Gonzalo Salinas y Ja-nice Joshi brindaron análisis estadís-ticos y apoyo administrativo.

Ibrahim Elbadawi y Jorge Garcia-Garcia estuvieron a cargo de la revi-sión entre pares del informe.Deseamos destacar nuestro agrade-cimiento a los colegas revisores porla ayuda prestada. Sus comentariosdetallados, así como otros recibidosdurante la reunión de análisis de ges-tión, se han tenido en cuenta en laevaluación.

El informe también refleja las ob-servaciones de los directivos de laOficina Regional del Banco. Se in-cluye, como Anexo D, la respuesta re-gional al Registro de Acción deGestión. Se han enviado al gobiernocopias del informe preliminar para suanálisis, y no se han recibido co-mentarios por escrito.

est examinée l’efficacité del’aide de la Banque mondialedans la façon d’aborder cesdéfis. Dans le dernier cha-pitre sont faites des recom-mandations.

L’Évaluation de l’aide parpays a été rédigée par Fareed

M.A. Hassan (Chef de projet) avec lacontribution de Djelloul Al-Saci(BID), Adil Kanaan, Isabelle Tsakoket Elaine W. Ooi (Consultants). Gon-zalo Salinas et Janice Joshi ont ap-porté les analyses statistiques et lesoutien administratif.

Ibrahim Elbadawi et Jorge Gar-cia-Garcia ont été réviseurs-pairspour ce rapport. Nous tenons à re-mercier les réviseurs-pairs pour avoirapporté leurs commentaires dé-taillés sur une version antérieure dudocument. Il a été tenu compte dansl’évaluation de ces commentaires,ainsi que d’autres commentairesreçus au cours de la réunion de ré-examen de la direction de l’OED.

Il a également été tenu comptedans ce rapport des commentairesde la Direction régionale de laBanque. La réponse régionale aux ré-sultats des mesures de gestion fi-gure à l’Annexe D. Copie du projetde rapport a été adressé au Gou-vernement pour examen et aucuncommentaire écrit n’a été reçu.

R E P U B L I C O F T U N I S I A : C O U N T R Y A S S I S TA N C E E VA L U AT I O N

v i i i

FR

AN

ÇA

IS

ES

PA

NO

L

EN

GL

ISH

RÉSUMÉ ANALYTIQUE

La présente Évaluation del’aide par pays a été préparée en col-laboration avec la Banque islamiquede développement. Le développementsocioéconomique de la Tunisie depuis1990 et les défis auxquels est confrontéle pays ont été évalués conjointement ;le programme d’aide de chaque insti-tution a été évalué en parallèle.

La Tunisie a réussi la transition quil’a fait passer d’exportations fondéessur les ressources, principalement depétrole et de gaz, à celles de produitsmanufacturés et de services. L’éco-nomie est à présent principalementdominée par les exportations textiles,électriques et mécaniques et de trans-formation des aliments, le tourisme etles activités connexes, et la productiond’olives et de céréales. Le taux decroissance réelle du PIB augmentede façon constante, passant de 3 % paran au cours de la période 1985-1990à plus de 5 % par an au cours de la pé-riode 1996-2002. Aujourd’hui, avecun revenu par habitant de 2000 dol-lars US, les Tunisiens disposent d’unrevenu réel deux fois et demie supé-rieur à celui de leurs parents il y atrente ans. La Tunisie a signé un ac-cord d’association avec l’Union eu-ropéenne (AAUE) qui prévoit unlibre-échange pour les produits ma-nufacturés d’ici 2008. L’UE est le prin-cipal partenaire commercial de laTunisie, la région est la source de 67 %des mouvements de capitaux en di-rection de la Tunisie, elle représenteune large part du marché touristiquede la Tunisie, et c’est la région ayantla plus grande communauté de Tuni-

EXECUTIVESUMMARY

This Country Assistance Eval-uation was prepared in collaborationwith the Islamic Development Bank.Tunisia’s socioeconomic developmentsince 1990 and the challenges facingthe country were assessed jointly;each institution’s assistance programwas evaluated in parallel.

Tunisia has successfully shiftedfrom resource-based exports domi-nated by oil and gas to manufac-tures and services. The economy isnow driven mainly by textiles, elec-trical, mechanical, and food pro-cessing exports; tourism and relatedactivities; and production of olivesand cereals. Real GDP growth hasbeen consistently rising, increasingfrom 3 percent annually over 1985-90 to more than 5 percent annuallyover 1996–02. Today, with a percapita income of US$2,000, Tunisiansenjoy more than two-and-a-halftimes the real incomes that theirparents had thirty years ago. Tunisiasigned an association agreementwith the European Union (EUAA)that provides for free trade in man-ufacturing by 2008. The EuropeanUnion (EU) has been Tunisia’s dom-inant trading partner; the region isthe source of 67 percent of capitalflows into Tunisia, accounts for alarge share of Tunisia’s tourism mar-ket, and is the region with the largestcommunity of expatriate Tunisians.As such the economy is vulnerableto adverse developments in the EU.

Rapid growth made possible a re-markable improvement in social in-dicators and a decline in the poverty

RÉSUMEN

Esta Evaluación de Asistenciaal País ha sido preparada en colabo-ración con el Banco Islámico de De-sarrollo. Se llevó a cabo unaevaluación conjunta del desarrollo so-cioeconómico de Túnez desde 1990 yde los desafíos que enfrenta el país; seevaluaron en paralelo los programasde asistencia de cada institución.

Túnez ha realizado con éxito elpaso de exportaciones basadas en re-cursos (principalmente petróleo ygas) a las de manufacturas y servi-cios. En la actualidad, la economíaestá impulsada principalmente porlas exportaciones textiles, electro-mecánicas y las relacionadas con elprocesamiento de alimentos, asícomo por las actividades turísticas yafines y la producción de aceitunas ycereales. El PIB real ha crecido enforma constante, de un 3 por cientoanual entre 1985 y 1990 a más de un5 por ciento anual entre 1996 y 2002.Hoy, con ingresos per cápita de USD2.000, los ingresos reales de los tu-necinos corresponden a dos veces ymedia los que obtenían sus padreshace treinta años. Túnez ha celebradoun acuerdo de asociación con laUnión Europea (EUAA, por sus siglasen inglés) que prevé la implementa-ción del libre comercio de manufac-turas para 2008. La Unión Europea(UE) ha sido el principal socio co-mercial de Túnez; la región es lafuente del 67 por ciento del flujo decapital hacia Túnez, representa unagran proporción del mercado del tu-rismo en ese país y constituye la re-gión con la mayor comunidad de

E X E C U T I V E S U M M A R Y

i x

EN

GL

ISH

FR

AN

ÇA

IS

ES

PA

NO

L

rate from 40 percent in 1970to 4 percent in 2000; the re-maining poverty is predom-inately rural. But if thevulnerable population justabove the poverty line is in-cluded, the percentage of thepoor would increase by an-

other 6 percentage points to over 10percent. Addressing vulnerabilityand rural poverty remains a priority,as does reconciling Bank and gov-ernment estimates of the breakdownof poverty between rural and urbanareas. Tunisia’s social indicators arebetter on average than the MiddleEast and North Africa (MNA) Regionand better than other lower middle-income countries. Tunisia leads theMNA Region in gender equity. Chal-lenges relate to sustaining highergrowth, achieving closer integrationwith the EU, and improving effi-ciency of social services in the faceof Tunisia’s vulnerability to externalshocks, its level of indebtedness andthe more competitive environmentit will likely confront in the future.

The Bank’s strategy since 1990,rooted in wide-ranging and influen-tial analytic and advisory activities,was to support macroeconomic sta-bilization, pro-market structural re-forms to foster growth, and socialprograms as well as human devel-opment. The strategy was relevant tothe government’s priorities outlinedin a series of national developmentplans. An increased focus on the so-cial sectors was aligned with the Mil-lennium Development Goals(MDGs) and the country’s emphasison human resource development.The Bank lending program is largeboth in per capita terms and as ashare of the MNA portfolio. Annualaverage lending commitments forfiscal years 1990–03 were US$200

tunecinos expatriados. Por talmotivo, la economía es vul-nerable a cualquier circuns-tancia adversa que puedaafectar a la UE.

El rápido crecimiento hizoposible una mejora notableen los indicadores sociales, así

como una reducción en la tasa de po-breza, del 40 por ciento en 1970 al 4por ciento en el año 2000; la pobrezaque aún persiste es predominante-mente rural. No obstante, si se inclu-yera a la población que se encuentrajusto por encima de la línea de po-breza, el porcentaje de pobres se in-crementaría en otros 6 puntosporcentuales, a más del 10 por ciento.La vulnerabilidad y la pobreza ruralcontinúan siendo temas prioritarios,al igual que la conciliación de las es-timaciones del Banco y el gobiernocon respecto a la distribución de la po-breza en las áreas rurales y urbanas.En promedio, los indicadores socia-les de Túnez superan al resto de la re-gión del Medio Oriente y Norte deÁfrica (MENA) u otros países de in-greso mediano bajo; el país tambiénes líder en esta región en cuanto a laigualdad de los géneros. Los desafíosque enfrenta consisten en poder sos-tener un crecimiento elevado, lograruna mayor integración con la UE ymejorar la eficiencia de los serviciossociales, en vista de la vulnerabilidadde Túnez ante golpes externos, sunivel de endeudamiento y el entornomás competitivo que probablementedeba enfrentar en el futuro.

Desde 1990, la estrategia delBanco, con base en actividades deanálisis y asesoramiento influyentes yde gran alcance, consistió en apoyarla estabilización macroeconómica, asícomo las reformas estructurales parapromover programas sociales y decrecimiento, y el desarrollo humano.

siens expatriés. De par ce fait,l’économie est vulnérable auxévénements défavorables sur-venant dans l’UE.

La croissance rapide arendu possible une remar-quable amélioration des indi-cateurs sociaux et une

diminution du taux de pauvreté qui estpassé de 40 % en 1970 à 4 % en 2000 ;la pauvreté restante est principale-ment rurale. Mais si l’on inclut la po-pulation vulnérable juste au-dessusdu seuil de pauvreté, le pourcentagedes pauvres augmente de 6 points etdépasse les 10 %. Le règlement de lavulnérabilité et de la pauvreté ruralereste une priorité, tout comme le faitde rapprocher les estimations de laBanque et du Gouvernement quant àla répartition entre les zones ruraleset urbaines. Les indicateurs sociauxde la Tunisie sont meilleurs enmoyenne que ceux de la régionMoyen-Orient et Afrique du Nord(MOAN) ou d’autres pays à faible re-venu intermédiaire ; elle est égale-ment en tête de la région MOAN en cequi concerne l’égalité des sexes. Lesdéfis ont trait à la durabilité d’unecroissance élevée, à la possibilité deparvenir à une intégration plus étroiteavec l’UE et à l’amélioration de l’effi-cacité des services sociaux, face à lavulnérabilité de la Tunisie aux chocs ex-térieurs, à son niveau d’endettementet à l’environnement plus compétitifauquel elle sera vraisemblablementconfrontée à l’avenir.

La stratégie de la Banque depuis1990, sur la base d’activités analy-tiques et à caractère consultatif à vasteinfluence, a été de soutenir la stabili-sation macroéconomique, les ré-formes structurales axées sur lemarché afin de promouvoir la crois-sance et les programmes sociaux ainsique le développement humain. La

R E P U B L I C O F T U N I S I A : C O U N T R Y A S S I S TA N C E E VA L U AT I O N

x

EN

GL

ISH

FR

AN

ÇA

IS

ES

PA

NO

L

million (or US$20 per capitaper year), representing overone quarter of the MNA Re-gional portfolio. Annual av-erage net disbursementswere only US$27 million, andnet transfers were negativefor most of the period. Policy-

based lending, in conjunction withvarious donor programs, accountedfor 40 percent of total lending and ad-dressed trade, financial, and privatesector development. Investmentloans supported mainly rural andhuman development projects. TheBank served as a significant catalystfor mobilizing resources, leveragingnearly US$1 for every IBRD dollar.

With timely and effective supportfrom the Bank and other donors,Tunisia averted a balance of paymentcrisis in the late 1980s, and sincethen has maintained a solid recordof macroeconomic stability and re-markable socioeconomic progress.The main attributes of Tunisia’s suc-cess were ownership and broad po-litical consensus, a well-developedhuman resource base, and a stablemacroeconomic environment. TheBank’s programs successfully pro-moted policy reforms. Substantialfinancial sector reforms wereachieved as well as the removal ofdisincentives for investment and theprivatization of public enterprises.Tariffs have been reduced and theeconomy is now more open to theoutside world. Manufactured exportshave grown steadily, increasing theirshare to 80 percent. The overallsoundness of the banking systemhas improved, as indicated byprogress in prudential ratios. Priva-tization in the banking sector hasalso advanced.

Bank assistance also contributedto significant progress in the rural

Esta estrategia era relevantepara las prioridades del go-bierno, planteadas en unaserie de planes nacionales dedesarrollo. La mayor atencióna los sectores sociales era com-patible con los Objetivos deDesarrollo del Milenio (ODM)

y el énfasis del país en el desarrollo delos recursos humanos. El programa definanciamiento del Banco es impor-tante, tanto en valores per cápitacomo en términos de la proporciónque representa en la cartera para la re-gión de Medio Oriente y Norte deÁfrica. Los compromisos de financia-miento anual promedio para los ejer-cicios fiscales de 1990 a 2003 fueronde USD 200 millones (o USD 20 percápita por año); esto representa másde un cuarto de la cartera regional.Los desembolsos netos anuales pro-medio fueron de sólo USD 27 millo-nes, y las transferencias netas fueronnegativas para la mayor parte del pe-ríodo. El financiamiento basado enpolíticas, conjuntamente con diversosprogramas de donantes, representóun 40 por ciento del financiamientototal y se destinó al desarrollo co-mercial, financiero y del sector pri-vado. Los préstamos para inversión sedestinaron a apoyar principalmenteproyectos de desarrollo rural y hu-mano. El Banco tuvo una importantefunción catalizadora al movilizar re-cursos a razón de USD 1 por cadadólar del BIRF.

A fines de la década de 1980, con unapoyo oportuno y eficaz del Banco yotros donantes, Túnez evitó una crisisde la balanza de pagos, y desde en-tonces ha mantenido un historial só-lido de estabilidad macroeconómica yun notable progreso socioeconómico.Los factores principales del éxito deTúnez han sido la identificación con losprogramas y el amplio consenso polí-

stratégie correspondait auxpriorités du Gouvernementexposées dans une série deplans nationaux de dévelop-pement. La focalisation accruesur les secteurs sociaux étaitdans la lignée des Objectifs dedéveloppement pour le mil-

lénaire (ODM) et de l’accent mis parle pays sur le développement des res-sources humaines. Le programme deprêts de la Banque est important, tantpar habitant qu’en tant que part duportefeuille MOAN. Les engagementsannuels moyens de prêts pour lesexercices 1990 à 2003 étaient de 200millions de dollars US (soit 20 dol-lars US par habitant par an), ce qui re-présente plus d’un quart duportefeuille de la région MOAN. Lesdécaissements annuels moyens netsn’ont été que de 27 millions de dol-lars US et les transferts nets ont été né-gatifs pour la plus grande partie de lapériode. Les prêts fondés sur la poli-tique stratégique, conjointement auxprogrammes de divers bailleurs defonds, ont représenté 40 % du totaldes prêts et ont été destinés au dé-veloppement commercial, financier etdu secteur privé. Les prêts pour pro-jets d’investissement ont soutenuprincipalement des projets ruraux etde développement des ressourceshumaines. La Banque a servi de cata-lyseur notable pour la mobilisationde ressources, obtenant près de 1dollar US pour chaque dollar BIRD.

Grâce au soutien effectif et entemps utile de la Banque et d’autresbailleurs de fonds, la Tunisie a évitéune crise de la balance des paiementsà la fin des années 80 et a depuis réussià maintenir une stabilité macroéco-nomique et un progrès socioécono-mique remarquable. Les principalescaractéristiques du succès de la Tuni-sie ont été sa prise en charge et un

E X E C U T I V E S U M M A R Y

x i

EN

GL

ISH

FR

AN

ÇA

IS

ES

PA

NO

L

and social sectors. TheBank’s major contribution inthe rural sector was in put-ting Tunisian agriculture onthe path of liberalization, sup-porting reform measures thatcontributed to increasingfarm incomes in remote

areas, and improving resource man-agement sustainability. With Banksupport, Tunisia made impressiveprogress in almost all areas coveredby the MDGs, already meeting sometargets—and the country is likely tomeet others by 2015. For example,by the mid-1990s, almost all chil-dren attended school, meeting theMDGs of universal primary educa-tion. Overall, the outcome of theBank’s assistance program is ratedsatisfactory based on its substantialrelevance and efficacy. Institutionalcapacity was strengthened furtherwith the Bank’s support, and insti-tutional development impact is ratedsubstantial.

Despite significant developmentprogress and the satisfactory out-come of the Bank’s assistance pro-gram, shortfalls in some areas,combined with the more competi-tive environment that Tunisia willlikely face in the future, pose risks tosustaining its remarkable develop-ment performance. Both the lowrate of private investment and the in-efficiency of overall investment areindicators that past growth may bedifficult to sustain without deeper re-form. One area where progress re-mained below Bank expectationswas promoting private sector de-velopment; the government stillplays a significant role in economicactivity. In the financial sector, pub-lic banks remain large in terms of as-sets, and non-performing loansimpose a heavy burden on the sec-

tico, así como una base de re-cursos humanos calificada yun entorno macroeconómicoestable. Los programas delBanco promovieron con éxitolas reformas a las políticas. Selograron reformas sustancia-les en el sector financiero, así

como la eliminación de desincentivospara la inversión y la privatización deempresas públicas. Se redujeron lastarifas, y la economía está ahora másabierta al mundo. Las exportaciones demanufacturas han experimentado uncrecimiento sostenido, hasta repre-sentar un 80 por ciento del total. La so-lidez general del sistema bancario hamejorado, como lo indica el avancede los coeficientes prudenciales. Laprivatización del sector bancario tam-bién ha experimentado avances. Laasistencia del Banco contribuyó asi-mismo a un progreso significativo enlos sectores social y rural. El principalaporte del Banco al sector rural fueponer a la agricultura de Túnez en elcamino de la liberalización, apoyandoreformas que contribuyeron a incre-mentar los ingresos agrícolas en áreasremotas y a mejorar la sostenibilidadde la gestión de recursos. Con el apoyodel Banco, Túnez hizo avances nota-bles en casi todas las áreas de los ODM,pues ya ha alcanzado algunos objeti-vos, y probablemente cumpla otrospara el año 2015. Por ejemplo, para me-diados de la década de 1990 casi todoslos niños habían asistido a la escuela,con lo que se cumplió la ODM de laeducación primaria universal. En tér-minos generales, el resultado del pro-grama de asistencia del Banco seconsidera satisfactorio, debido a su re-levancia y su eficacia sustanciales. La ca-pacidad institucional se fortaleció aúnmás con el apoyo del Banco, y se con-sidera que ha habido un impacto sus-tancial sobre el desarrollo institucional.

large consensus politique, unebase de ressources humainesbien développée et uncontexte macroéconomiquestable. Les programmes de laBanque ont réussi à promou-voir des réformes stratégiques.D’importantes réformes du

secteur financier ont été effectuées,tout comme le retrait des mesures dedissuasion à l’investissement et à la pri-vatisation des entreprises publiques.Les tarifs douaniers ont été réduits etl’économie est à présent plus ouvertesur le monde extérieur. Les exporta-tions de produits manufacturés ontaugmenté de façon constante, leurpart arrivant à 80 %. La solidité d’en-semble du système bancaire s’est amé-liorée comme le montre laprogression des ratios prudentiels. Laprivatisation du secteur bancaire aégalement progressé. L’aide de laBanque a elle aussi contribué à l’avan-cement non négligeable du secteurrural et du secteur social. La plus im-portante contribution de la Banque enfaveur du secteur rural a été de placerl’agriculture tunisienne sur la voie dela libéralisation, en soutenant des me-sures de réforme qui ont contribué àl’augmentation du revenu fermierdans les zones retirées et à l’amélio-ration de la durabilité de la gestiondes ressources. Avec le soutien de laBanque, la Tunisie a fait d’énormesprogrès dans presque tous les do-maines couverts par les ODM ; elle adéjà atteint certains objectifs et va vrai-semblablement atteindre les autresd’ici 2015. Par exemple, vers le milieudes années 90 presque tous les enfantsallaient à l’école, atteignant ainsi lesODM d’éducation primaire univer-selle. Dans leur ensemble, les résultatsdu programme d’aide de la Banque estnoté comme satisfaisant sur la base desa pertinence et de son efficacité im-

R E P U B L I C O F T U N I S I A : C O U N T R Y A S S I S TA N C E E VA L U AT I O N

x i i

EN

GL

ISH

FR

AN

ÇA

IS

ES

PA

NO

L

tor and pose risks to stability.In trade policy, tariff rates re-main above competitors’ lev-els, and more needs to bedone to ensure that discrim-ination against non-EU tradeis eliminated within the over-all framework of the EUAA.

Another area where the govern-ment’s program needs to be en-hanced and the Bank needs to directits attention more than in the past isthe overall efficiency and fiscal sus-tainability of social expenditures, asexpenditures on social services re-main high. Education expansion atthe post-basic level and a decline inbasic education enrollment due todemographic changes will necessi-tate efficiency improvements. In therural sector, addressing issues suchas land tenure, rural finance, non-farm rural development, and re-search and extension will beimportant, as these are areas wherepast Bank assistance programs wereless successful. Finally, past positivedevelopment outcomes have fos-tered a large middle class that willpress for more participation in thedevelopment process. In the past,Tunisia has managed well its eco-nomic and regional political uncer-tainties by maintaining social andmacroeconomic stability, graduallydiversifying its export base, and forg-ing closer relations with the EU.Given its past record, sustainabilityof the achievements is rated likely.

This evaluation recommends thatthe Bank should continue to sup-port improving the environment forprivate sector development and en-hancing competitiveness, as thecountry seeks to integrate more intothe global economy and will con-front an increasingly competitive cli-mate in the next few years. Adopting

Pese a los avances signifi-cativos en el desarrollo y alresultado satisfactorio del pro-grama de asistencia delBanco, las deficiencias en al-gunas áreas, combinadas conel entorno más competitivoque Túnez posiblemente en-

frente en el futuro, plantean riesgospara la sostenibilidad de su desta-cado desarrollo. Tanto la baja tasa deinversión privada como la ineficien-cia de las inversiones en general in-dican que el crecimiento pasadoposiblemente sea difícil de mante-ner si no se profundiza la reforma. Unárea en la que el progreso no satisfizolas expectativas del Banco fue la pro-moción del desarrollo del sector pri-vado; el gobierno continúadesempeñando un papel significa-tivo en la actividad económica. En elsector financiero, los bancos públicossiguen estando sobredimensionadosen términos de activos, y los présta-mos no redituables representan unacarga pesada para el sector, ademásde constituir un riesgo para la esta-bilidad. En materia de política co-mercial, los aranceles siguen estandopor encima de los niveles de los com-petidores, y es necesario tomar másmedidas tendientes a eliminar la dis-criminación contra el comercio pro-veniente de países fuera de la UE,dentro del marco general del EUAA.Otra área en la que es necesario me-jorar el programa del gobierno, y a laque el Banco necesita prestar másatención que en el pasado, es la efi-ciencia general y la sostenibilidad fis-cal del gasto social, pues el gasto enservicios sociales sigue siendo ele-vado. La expansión de la educaciónen el nivel posterior al básico, con-jugada con la declinación en la ins-cripción en la educación básicadebido a cambios demográficos,

portantes. La capacité institu-tionnelle s’est vue renforcéeplus encore grâce au soutiende la Banque et l’impact entermes de développement ins-titutionnel est noté commeimportant.

En dépit de notables pro-grès au niveau du développement etles résultats satisfaisants du pro-gramme d’aide de la Banque, les in-suffisances dans certains domaines,combinées au contexte plus compé-titif auquel la Tunisie sera vraisem-blablement confrontée à l’avenir,posent des risques pour le maintiende ses remarquables performancesau niveau du développement. Tantle faible taux des investissements pri-vés que l’inefficacité globale des in-vestissements sont des indicateursqu’il peut être difficile de soutenir lacroissance passée sans des réformesplus profondes. Un domaine dans le-quel le progrès est resté en deçà desattentes de la Banque est la promo-tion du développement du secteurprivé ; le gouvernement joue encoreun rôle non négligeable dans l’activitééconomique. Dans le secteur finan-cier, les banques publiques demeu-rent importantes en termes de totalde bilan et les créances non produc-tives imposent un lourd fardeau surle secteur et posent des risques entermes de stabilité. Dans le domainede la politique commerciale, les tarifsdouaniers demeurent au dessus du ni-veau des concurrents et il convient defaire plus pour assurer que la discri-mination à l’encontre du commercenon UE soit éliminée dans le cadreglobal de l’AAUE. Un autre domaineoù le programme du gouvernementa besoin d’être amélioré et auquel laBanque doit prêter une plus grandeattention que par le passé, est l’effi-cacité globale et la durabilité fiscale

E X E C U T I V E S U M M A R Y

x i i i

EN

GL

ISH

FR

AN

ÇA

IS

ES

PA

NO

L

a results-based approach,with agreed and monitorableoutput and outcome indica-tors embedded in an im-proved monitoring andevaluation framework, wouldhelp to anchor the Bank’s as-sistance program in the fu-

ture. Specifically, the Bank should(i) help the country pursue tradeopenness with the EU and the restof the world, (ii) help improve thebusiness environment through reg-ulatory and judiciary reforms, in-cluding measures to reduce the flowand stock of non-performing loans,and (iii) promote enterprise and fi-nancial sector privatization. FutureBank programs should also (iv) helpstrengthen rural institutions to sup-port efficient output and input mar-kets (for example, land and ruralfinance) while maintaining socialand political stability through bettertargeted safety nets. After 21 yearswithout a rural sector-wide review,the Bank should undertake one toinform its future programs. Finally,the Bank should also fill the gaps incore diagnostic economic and sec-tor work (ESW) by completing apublic expenditure review (PER), aCountry Financial Accountability As-sessment (CFAA), and a Country Pro-curement Assessment Review(CPAR). In particular, a PER couldhelp build capacity to prioritize pub-lic spending and provide the basisfor measures to efficiently addresseducation expansion.

harán necesaria la imple-mentación de mejoras orien-tadas a la eficiencia. En elsector rural será importanteabordar temas como la te-nencia de tierras, el financia-miento del sector rural, eldesarrollo rural no agrícola y

la investigación y extensión, pues sonáreas en las que los programas deasistencia anteriores del Banco hantenido menos éxito. Por último, losresultados positivos del pasado enel área del desarrollo han promovidola formación de una gran clase mediaque ejercerá presión para lograr unamayor participación en el procesode desarrollo. En el pasado, Túnez hatenido se ha manejado bien ante la in-certidumbre económica y política re-gional, manteniendo la estabilidadsocial y macroeconómica, diversifi-cando gradualmente su base de ex-portaciones y forjando relacionesmás estrechas con la UE. A la luz desus antecedentes, se considera pro-bable que pueda sostener sus logros.

Esta evaluación recomienda que elBanco continúe apoyando las mejo-ras coyunturales para el desarrollodel sector privado y el aumento de lacompetitividad, dado que el país pro-cura profundizar su integración a laeconomía global, y probablementedeba enfrentar un clima cada vez máscompetitivo en los años venideros. Laadopción de un enfoque orientado alos resultados, con indicadores deproductos y resultados acordados enun entorno mejorado de seguimientoy evaluación, ayudaría a forjar unabase firme para el programa de asis-tencia del Banco en el futuro. Espe-cíficamente, el Banco debería (i)ayudar al país a procurar lograr laapertura comercial con la UE y elresto del mundo, (ii) contribuir a me-jorar el entorno comercial mediante

des dépenses sociales, car lesdépenses en matière de ser-vices sociaux demeurent éle-vées. L’expansion del’enseignement au delà del’enseignement de base et ladiminution des inscriptionsau niveau de l’enseignement

de base en raison de changementsdémographiques nécessiteront desaméliorations en termes d’efficacité.Dans le secteur rural, il sera importantd’aborder des questions commecelles de la propriété foncière, du fi-nancement rural, du développement,de la recherche et de la vulgarisationruraux hors exploitations agricoles,car ce sont là des domaines dans les-quels les programmes d’aide de laBanque n’ont pas par le passé aussibien réussi. Enfin, les résultats posi-tifs passés en matière de développe-ment ont favorisé une vaste classemoyenne qui va exiger une plusgrande participation au processus dedéveloppement. Par le passé la Tuni-sie a bien géré ses incertitudes éco-nomiques et de politique régionale enmaintenant une stabilité sociale etmacroéconomique, en diversifiantgraduellement ses exportations et enétablissant des rapports plus étroitsavec l’UE. Compte tenu de ses résul-tats passés, la durabilité de ces résul-tats est jugée comme vraisemblable.

Les recommandations de la pré-sente évaluation sont que la Banquedevrait continuer à soutenir l’amélio-ration de la conjoncture pour le dé-veloppement du secteur privé et unemeilleure compétitivité à mesure quele pays cherche à s’intégrer plus en-core dans l’économie mondiale etsera confrontée dans les prochainesannées à un contexte de plus en plusconcurrentiel. Le fait d’adopter une ap-proche fondée sur les résultats avecdes extrants convenus et contrôlables

R E P U B L I C O F T U N I S I A : C O U N T R Y A S S I S TA N C E E VA L U AT I O N

x i v

EN

GL

ISH

FR

AN

ÇA

IS

ES

PA

NO

L

reformas regulatorias y jurí-dicas, por ejemplo con medi-das para reducir el flujo y lacantidad de préstamos no re-dituables, y (iii) promover laprivatización del sector fi-nanciero y de las empresaspúblicas. Los programas fu-

turos del Banco deberían, además, (iv) ayudar a fortalecer las institu-ciones rurales a fin de dar apoyo a losmercados eficientes de productos einsumos (por ejemplo, el financia-miento rural y de adquisición de tie-rras) manteniendo a la vez laestabilidad social y política a través deredes de seguridad mejor orienta-das. Después de 21 años sin realizarun examen con alcance a todo el sec-tor rural, el Banco debería llevarlo acabo para informar sus futuros pro-gramas. Por último, el Banco tam-bién debería llenar el vacío existenteen materia de trabajos básicos dediagnóstico con estudios económicos y sectoriales, mediante una Revisióndel Gasto Público, una Evaluación dela Capacidad de Gestión Financiera yuna Evaluación de las Contratacio-nes del País. En particular, el estudiodel gasto público podría ayudar a for-talecer las capacidades para priori-zar el gasto público y proporcionar unparámetro de medición para abor-dar con eficiencia la expansión de laeducación.

et des indicateurs de résultatsintégrés dans une démarchede supervision et d’évaluationaiderait à asseoir le pro-gramme d’aide de la Banque àl’avenir. En particulier, laBanque devrait (i) aider le paysà poursuivre l’ouverture de

son commerce avec l’UE et le reste dumonde, (ii) aider à améliorer lecontexte commercial par le biais de ré-formes réglementaires et judiciaires,y compris des mesures visant à ré-duire le flux et les réserves de créancesnon productives, et (iii) promouvoirla privatisation des entreprises et dusecteur financier. Les programmes fu-turs de la Banque devraient égale-ment (iv) aider à renforcer lesinstitutions rurales en soutenant desmarchés d’intrants et d’extrants effi-caces (par exemple le financementfoncier et rural) tout en maintenant lastabilité sociale et politique par le biaisd’une meilleure protection sociale ci-blée. Après 21 ans sans un examende l’ensemble du secteur rural, laBanque devrait en entreprendre unpour transmettre l’information auxprogrammes futurs. Enfin, la Banquedevrait également combler les lacunesdes activités économiques et secto-rielles de base (ESW) en effectuantun examen des dépenses publiques(PER), une évaluation de la respon-sabilisation financière du pays (CFAA)et une revue de la passation des mar-chés du pays (CPAR). Un PER pourraitnotamment aider au renforcementdes capacités visant à établir les prio-rités des dépenses publiques et àfournir la base pour des mesures per-mettant d’aborder de façon efficacel’expansion de l’éducation.

E X E C U T I V E S U M M A R Y

x v

FR

AN

ÇA

IS

ES

PA

NO

L

Gregory K. Ingram Director-General, Operations Evaluation

x v i i

AAA Analytical and advisory activitiesAAL Agricultural Adjustment LoanAFD Agence Française de Développement

French Development AgencyAfDB African Development BankASIL Agricultural Sector Investment LoanBNA Banque Nationale AgricoleBNP Banque Nationale de ParisCAE Country Assistance EvaluationCAS Country Assistance StrategyCEM Country Economic MemorandumCFAA Country Financial Accountability AssessmentCPAR Country Procurement Assessment ReviewECAL Economic Competitiveness Adjustment LoanEFRSL Enterprise and Financial Reform Support LoanEIB European Investment BankESW Economic and sector workEQIP Education Quality Improvement ProgramEU European UnionEUAA European Union Association AgreementFDI Foreign Direct InvestmentFSD Financial sector developmentGDP Gross domestic productGNI Gross national incomeGNP Gross national productGOT Government of TunisiaGSM Global System MobileIBRD International Bank for Reconstruction and DevelopmentIDB Islamic Development BankIMF International Monetary FundINS National Institute of StatisticsITPAL Industry and Trade Policy Adjustment LoanKfW Kreditanstalt für Wiederaufbau (German Agency for Reconstruction) M&E Monitoring and evaluationMDG Millennium Development GoalMEDA Mesures d’accompagnement financiers et techniques à la reforme des

structures économiques et sociales dans le cadre du partenariat euro-méditerranéen

MFA Multifibre Arrangement MM Macroeconomic managementMNA Middle East and North Africa RegionMOA Ministry of AgricultureMOE Ministry of EducationNGO Nongovernmental organizationNPL Nonperforming loansODESYPANO Office du Développement Sylvo-Pastoral du Nord-OuestOECD Organisation for Economic Co-operation and DevelopmentOED Operations Evaluation Department

ACRONYMS AND ABBREVIATIONS

PE Public enterprisePER Public Expenditure Review PERL Public Enterprise Restructuring LoanPPAR Project Performance Assessment ReportQAG Quality Assurance GroupQR Quantitative restrictionsSAL Structural Adjustment LoanSDR Special Drawing RightsSMEs Small and medium-size enterprisesUNDP United Nations Development ProgramVAT Value added taxWSIP Water Sector Investment ProjectWTO World Trade Organization

R E P U B L I C O F T U N I S I A : C O U N T R Y A S S I S TA N C E E VA L U AT I O N

x v i i i

1

Tunisia’s SocioeconomicDevelopment Progress Achieved and Challenges Ahead

This Country Assistance Evaluation (CAE) looks at the effectiveness ofWorld Bank assistance since 1990 from three perspectives: an analysisof the Bank’s assistance program, the Bank’s development impact, and

the contribution of the Bank and its development partners to developmentoutcomes. Annex C describes the methodology. The evaluation is based onbackground studies, internal World Bank reports, and interviews with gov-ernment officials, Bank staff, donors, and civil society. Annex B contains a listof the people interviewed. The CAE was prepared in collaboration with theIslamic Development Bank.

BackgroundTunisia gained its independence from France in1956. As a republic with a strong central author-ity vested in the president, it has since experi-enced political stability at a time when itsneighborhood has been experiencing signifi-cant turmoil. As a moderate Arab country inNorth Africa, it has managed not to beabsorbed within the vortex of the morecomplex Middle Eastern politics, whilemaintaining a good link with its Arabneighbors, often serving as an interlocutor, or apolitical haven. The United States hasannounced the opening in 2004 of a regionaloffice in Tunis of the US–Middle East Partner-ship Initiative. As with its neighbors in North

Africa, much of Tunisia’s land is arid, or semi-arid, with as little as 3 percent of arable landirrigated, while rain-fed agriculture is subject tosevere annual fluctuations in rainfall. In 2002,the population of 9.8 million had a per capitaincome of US$2,000 (annex table A.1).

After independence, the political leadershipopted initially for a dirigiste economic system,with mainly public ownership of manufacturingindustries, banks, and other financial institu-tions. At independence, the country’s mostimportant raw materials were petroleum,natural gas, and phosphates. However, oil andgas production has been decreasing as reserveshave been depleted, and the quality ofphosphate deposits is poor. As an alternative

11

source of income, attention has been given tothe development of manufacturing, tourism,and other services. At the same time, thecountry invested heavily in human resourcedevelopment and paid particular attention towelfare and education. This proved animportant contributor to Tunisia’s economicperformance in subsequent decades.

The oil boom of the 1970s. The multi-fold increasein the price of crude generated high exportrevenues that financed significantly higherlevels of investment (30 percent of GDP),particularly in manufacturing. As a result, realGDP growth averaged 7.4 percent annuallythroughout the 1970s. High oil revenuesallowed the economy to perform well under thedirigiste system. Directive policies controllinginvestment and prices were broadly applied, inthe context of protected trade and generoussubsidies to enterprises. The priority given tohuman resource development continued.

The first half of the 1980s: decline and apprehension.Problems with economic performance startedto emerge in the early 1980s as oil prices andproduction levels declined, while high invest-ment levels and public expenditures weremaintained. Although Tunisia’s Sixth Five-YearPlan (1982–86) proposed stringent policies,unaffordable investment levels and lax policiescontinued, leading to a deterioration in themacroeconomic situation. By 1984, inflationhad risen to 10 percent; the current accountdeficit had grown to almost 11 percent of GDP,external debt to 46 percent of GDP, and thedebt service ratio to 21 percent. By 1985, abalance of payment crisis appeared imminent.

The turning point in the mid-1980s. Faced withgrowing macroeconomic imbalances, thegovernment pursued a program of stabilizationand adjustment supported by the World Bankand the International Monetary Fund (IMF).The reform program proceeded at a gradualbut steady pace, consolidating past progress,although the state continued to keep aprominent position in the economy. The fiscaldeficit and inflation fell, and GDP grew at 4

percent per annum between 1987 and 1994.The fiscal and current account deficits havehovered around 4 percent of GDP since themid-1990s.

A new phase of development by the mid-1990s. GivenTunisia’s limited domestic markets, the govern-ment decided to increase its integration in theworld economy to accelerate higher growth. In1995, Tunisia became the first country in theregion to sign an association agreement with theEU (EUAA). The agreement includes provisionsfor the phased establishment of a free tradezone for manufacturers over a 12-year period(1996–08). Also, Tunisia signed bilateral tradeagreements with Morocco, Jordan, Libya, Iraq,and Syria. The economy is now more open tothe outside world, and imports and exportsconstitute about 90 percent of GDP, up from 70percent in the mid-1980s. This ratio comparesfavorably to other Middle East and North Africa(MNA) countries at similar income level (annextable A.2k).

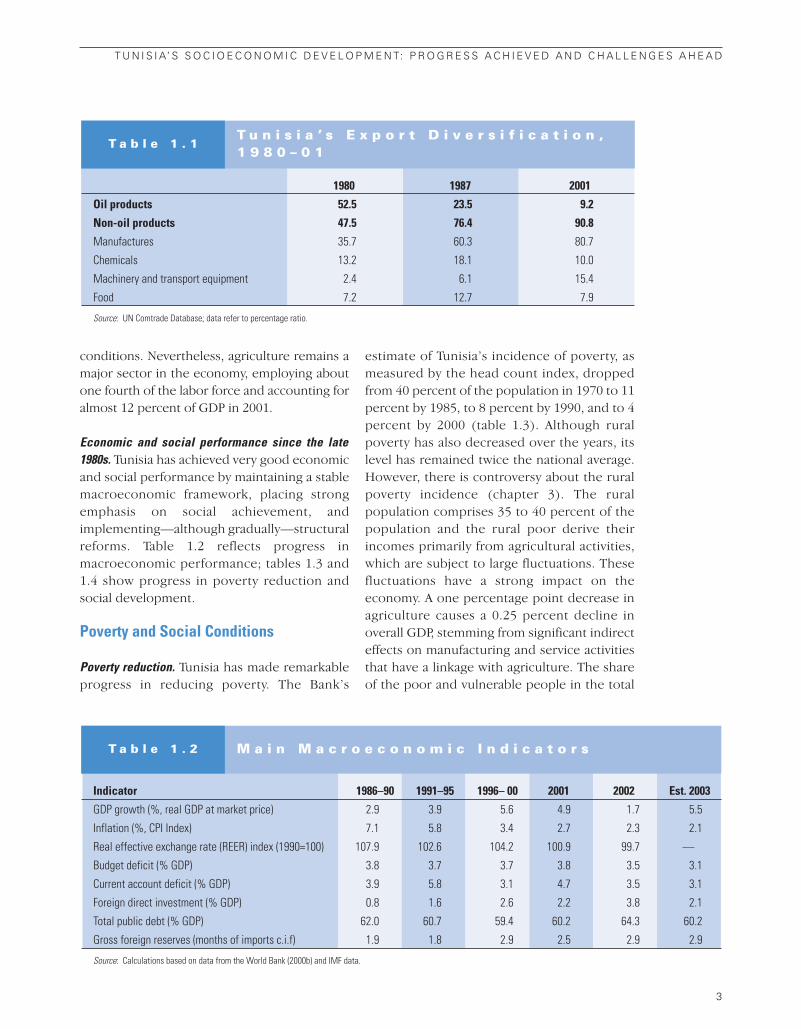

From oil dominated and volatile to more stable anddiversified economy. Since the mid-1980s,Tunisia’s exports have been successfully diversi-fied, moving away from resource-based exportsdominated by oil and gas to manufactures (table1.1). Export of manufactures has grown ataround 10 percent a year in real terms since1987, increasing the share of manufactures inexports to over 80 percent. Tunisia’s economy isnow driven mainly by textiles, electrical andmechanical equipment, and food processing (inthe manufacturing sector), tourism and relatedactivities (in the services sector), and produc-tion of olives and cereals (in the agriculturalsector). Tunisia’s major exports are now textilesand leather (making up 50 percent of exports).Today, Tunisians enjoy more than two-and-a-halftimes the real incomes that their parents hadthirty years ago. The service sector, whichaccounts for nearly 60 percent of GDP, has beenproviding the largest contribution. Theindustrial sector is the second largest, withabout 28 percent of GDP, and has been fairlydynamic. Agriculture’s contribution to growthfluctuates widely, largely based on weather

2

R E P U B L I C O F T U N I S I A : C O U N T R Y A S S I S TA N C E E VA L U AT I O N

conditions. Nevertheless, agriculture remains amajor sector in the economy, employing aboutone fourth of the labor force and accounting foralmost 12 percent of GDP in 2001.

Economic and social performance since the late1980s. Tunisia has achieved very good economicand social performance by maintaining a stablemacroeconomic framework, placing strongemphasis on social achievement, andimplementing—although gradually—structuralreforms. Table 1.2 reflects progress inmacroeconomic performance; tables 1.3 and1.4 show progress in poverty reduction andsocial development.

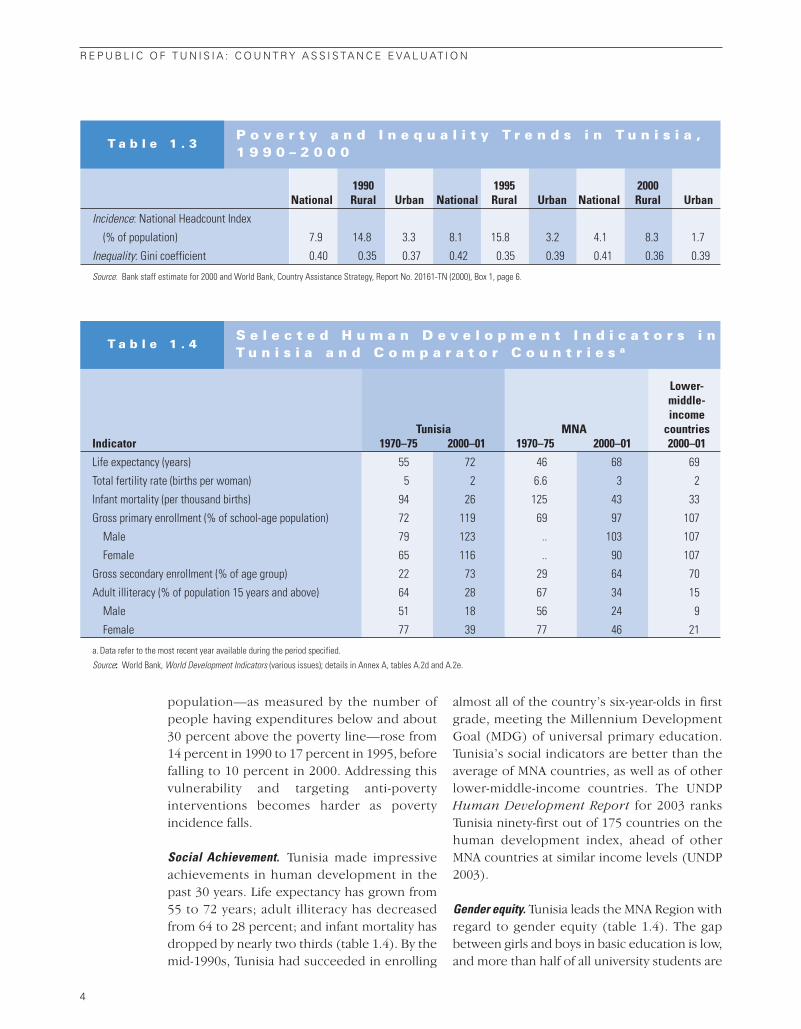

Poverty and Social Conditions

Poverty reduction. Tunisia has made remarkableprogress in reducing poverty. The Bank’s

estimate of Tunisia’s incidence of poverty, asmeasured by the head count index, droppedfrom 40 percent of the population in 1970 to 11percent by 1985, to 8 percent by 1990, and to 4percent by 2000 (table 1.3). Although ruralpoverty has also decreased over the years, itslevel has remained twice the national average.However, there is controversy about the ruralpoverty incidence (chapter 3). The ruralpopulation comprises 35 to 40 percent of thepopulation and the rural poor derive theirincomes primarily from agricultural activities,which are subject to large fluctuations. Thesefluctuations have a strong impact on theeconomy. A one percentage point decrease inagriculture causes a 0.25 percent decline inoverall GDP, stemming from significant indirecteffects on manufacturing and service activitiesthat have a linkage with agriculture. The shareof the poor and vulnerable people in the total

T U N I S I A’ S S O C I O E C O N O M I C D E V E L O P M E N T: P R O G R E S S A C H I E V E D A N D C H A L L E N G E S A H E A D

3

1980 1987 2001

Oil products 52.5 23.5 9.2

Non-oil products 47.5 76.4 90.8

Manufactures 35.7 60.3 80.7

Chemicals 13.2 18.1 10.0

Machinery and transport equipment 2.4 6.1 15.4

Food 7.2 12.7 7.9

Source: UN Comtrade Database; data refer to percentage ratio.

T u n i s i a ’ s E x p o r t D i v e r s i f i c a t i o n ,1 9 8 0 – 0 1

T a b l e 1 . 1

Indicator 1986–90 1991–95 1996– 00 2001 2002 Est. 2003

GDP growth (%, real GDP at market price) 2.9 3.9 5.6 4.9 1.7 5.5

Inflation (%, CPI Index) 7.1 5.8 3.4 2.7 2.3 2.1

Real effective exchange rate (REER) index (1990=100) 107.9 102.6 104.2 100.9 99.7 —

Budget deficit (% GDP) 3.8 3.7 3.7 3.8 3.5 3.1

Current account deficit (% GDP) 3.9 5.8 3.1 4.7 3.5 3.1

Foreign direct investment (% GDP) 0.8 1.6 2.6 2.2 3.8 2.1

Total public debt (% GDP) 62.0 60.7 59.4 60.2 64.3 60.2

Gross foreign reserves (months of imports c.i.f) 1.9 1.8 2.9 2.5 2.9 2.9

Source: Calculations based on data from the World Bank (2000b) and IMF data.

M a i n M a c r o e c o n o m i c I n d i c a t o r sT a b l e 1 . 2

population—as measured by the number ofpeople having expenditures below and about30 percent above the poverty line—rose from14 percent in 1990 to 17 percent in 1995, beforefalling to 10 percent in 2000. Addressing thisvulnerability and targeting anti-povertyinterventions becomes harder as povertyincidence falls.

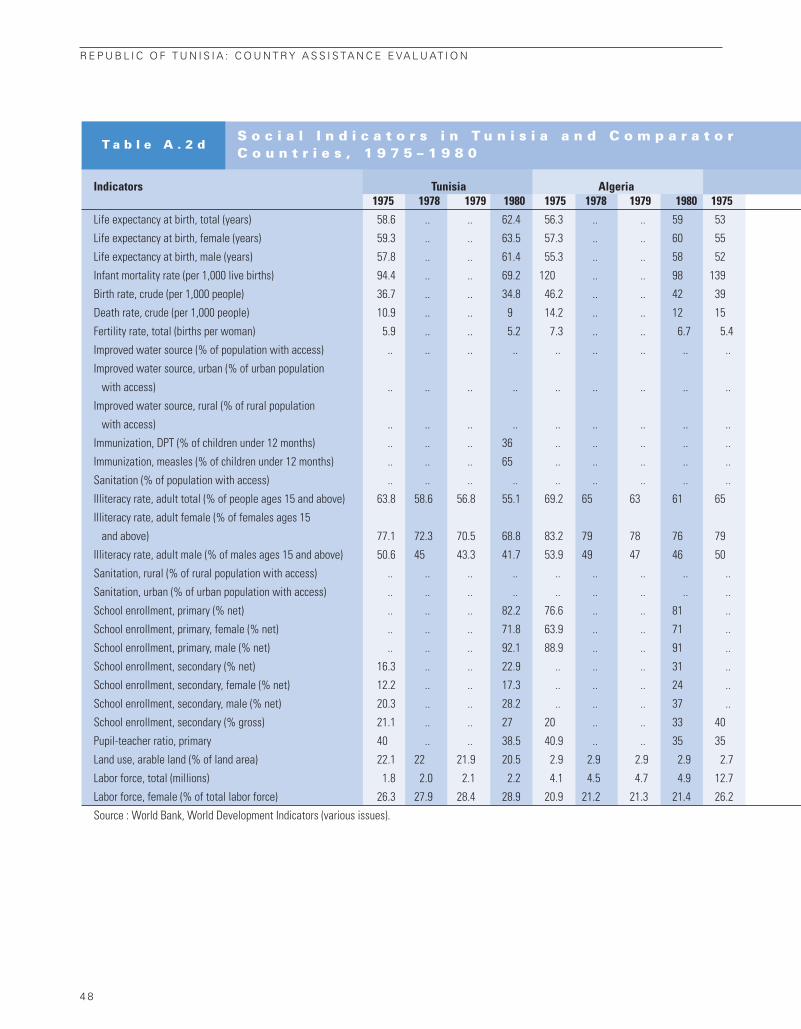

Social Achievement. Tunisia made impressiveachievements in human development in thepast 30 years. Life expectancy has grown from55 to 72 years; adult illiteracy has decreasedfrom 64 to 28 percent; and infant mortality hasdropped by nearly two thirds (table 1.4). By themid-1990s, Tunisia had succeeded in enrolling

almost all of the country’s six-year-olds in firstgrade, meeting the Millennium DevelopmentGoal (MDG) of universal primary education.Tunisia’s social indicators are better than theaverage of MNA countries, as well as of otherlower-middle-income countries. The UNDPHuman Development Report for 2003 ranksTunisia ninety-first out of 175 countries on thehuman development index, ahead of otherMNA countries at similar income levels (UNDP2003).

Gender equity. Tunisia leads the MNA Region withregard to gender equity (table 1.4). The gapbetween girls and boys in basic education is low,and more than half of all university students are

4

R E P U B L I C O F T U N I S I A : C O U N T R Y A S S I S TA N C E E VA L U AT I O N

1990 1995 2000National Rural Urban National Rural Urban National Rural Urban

Incidence: National Headcount Index

(% of population) 7.9 14.8 3.3 8.1 15.8 3.2 4.1 8.3 1.7

Inequality: Gini coefficient 0.40 0.35 0.37 0.42 0.35 0.39 0.41 0.36 0.39

Source: Bank staff estimate for 2000 and World Bank, Country Assistance Strategy, Report No. 20161-TN (2000), Box 1, page 6.

P o v e r t y a n d I n e q u a l i t y T r e n d s i n T u n i s i a ,1 9 9 0 – 2 0 0 0

T a b l e 1 . 3

Lower-middle-income

Tunisia MNA countries Indicator 1970–75 2000–01 1970–75 2000–01 2000–01

Life expectancy (years) 55 72 46 68 69

Total fertility rate (births per woman) 5 2 6.6 3 2

Infant mortality (per thousand births) 94 26 125 43 33

Gross primary enrollment (% of school-age population) 72 119 69 97 107

Male 79 123 .. 103 107

Female 65 116 .. 90 107

Gross secondary enrollment (% of age group) 22 73 29 64 70

Adult illiteracy (% of population 15 years and above) 64 28 67 34 15

Male 51 18 56 24 9

Female 77 39 77 46 21

a. Data refer to the most recent year available during the period specified.

Source: World Bank, World Development Indicators (various issues); details in Annex A, tables A.2d and A.2e.

S e l e c t e d H u m a n D e v e l o p m e n t I n d i c a t o r s i nT u n i s i a a n d C o m p a r a t o r C o u n t r i e s aT a b l e 1 . 4

women. Compulsory education for girls andboys through ninth grade has helped bridge thegap between female and male school enroll-ment rates. The status of women has improvedsteadily, with rates of female labor force partici-pation that are higher than for other countriesin the Region, but at 32 percent (in 2001), lowcompared with other lower-middle-incomecountries (World Bank data, 2003). Tunisia’sfemale participation rate in the workforceincreased by 4 percentage points during the1990s. Tunisian women received the right tovote immediately after independence in 1957,before many other MNA countries; the propor-tion of seats held by women in the nationalparliament was 12 percent in 2001. Tunisia ranksabove the MNA average on the United NationsGender Development Index (GDI).1 Asindicated earlier, this was due to the directattention given to human resource develop-ment, with particular emphasis on genderequity.

Further progress in the social sectors isrequired to consolidate past gains and prepareTunisia for a more competitive environment inthe twenty-first century. There is still room forenhancing the quality and efficiency of socialachievements. For example, the school systemis still burdened with high dropout and repeti-tion rates in the upper grades. Adult illiteracyrates remain high. Public health resources arenot used efficiently (as evidenced by low ratesof use of public health services), and the qualityof services does not meet the population’sexpectations. Social progress has beenachieved at a high cost relative to comparatorcountries: public expenditures on educationare 7.7 percent of GNP compared to a MNAaverage of 5.2 percent and a lower-middle-income-country average of 4.9 percent (WorldBank 2000b). Similarly, Tunisia’s healthexpenditures of 5.5 percent of GDP are higherthan the MNA average of 4.6 percent (WorldBank data, 2003).

Debt Burden and External Assistance Despite its remarkable economic progress andability to weather past shocks, Tunisia’seconomy remains vulnerable to external

shocks. The ratio of external debt to GDP isrelatively high, hovering around 60 percent(table 1.2), and the U.S. dollar, with a share ofover 40 percent, dominates the currencycomposition of this debt. These factorstogether with the current account and budgetdeficits make the country vulnerable toexternal shocks. Furthermore, foreignexchange reserves have remained low (belowthree months of imports). The economyweathered past shocks well (for example, thecontinued aftermath of September 11, 2001,events and a terrorist attack in Djerba, whichled to a sharp drop in tourism) in terms ofmaintaining macro balances. However, thetransition to greater integration into globalmarkets raises challenges for debt sustainabil-ity due to competitive pressures and increasedexposure to volatility.2 Tunisia has recentlybeen trying to diversify the currency composi-tion of its debt by issuing euro-dominatedsovereign bonds, as it did in July 1999. Also thegovernment is gradually shifting from externalto domestic sources of financing.

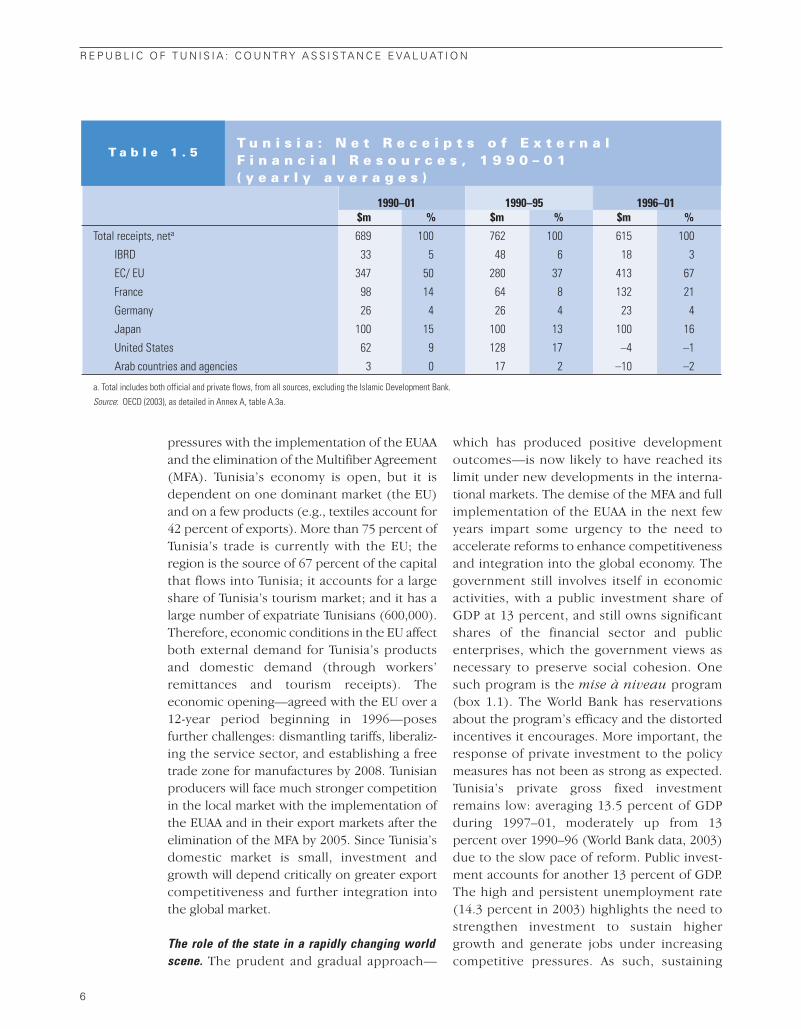

Tunisia has received large net financial flows(including grants and private flows), averagingnearly US$700 million annually (3.5 percent ofGDP) over the 1990–01 period (table 1.5). Inper capita terms, Tunisia received an annualaverage of US$70 per capita in net flows, belowthose for other MNA countries at similarincome levels. The Bank has provided signifi-cant assistance to Tunisia, committing US$2.7billion for 40 loans since 1990. With old loansbeing serviced and repaid, the Bank’s share ofnet flows to Tunisia is about 5 percent. Since1996, EU member states have providedincreased assistance to support the implemen-tation of Tunisia’s association agreement in1995. The share of the EU and France nearlydoubled in the 1996–01 period. Also, Tunisia isone of the largest recipients of IslamicDevelopment Bank (IDB) assistance, with $1.2billion in financing since 1976 (or about US$2per capita per year).

Meeting the Challenges of GlobalizationIncreasing competitive pressures. The Tunisianeconomy will face increasing competitive

T U N I S I A’ S S O C I O E C O N O M I C D E V E L O P M E N T: P R O G R E S S A C H I E V E D A N D C H A L L E N G E S A H E A D

5

pressures with the implementation of the EUAAand the elimination of the Multifiber Agreement(MFA). Tunisia’s economy is open, but it isdependent on one dominant market (the EU)and on a few products (e.g., textiles account for42 percent of exports). More than 75 percent ofTunisia’s trade is currently with the EU; theregion is the source of 67 percent of the capitalthat flows into Tunisia; it accounts for a largeshare of Tunisia’s tourism market; and it has alarge number of expatriate Tunisians (600,000).Therefore, economic conditions in the EU affectboth external demand for Tunisia’s productsand domestic demand (through workers’remittances and tourism receipts). Theeconomic opening—agreed with the EU over a12-year period beginning in 1996—posesfurther challenges: dismantling tariffs, liberaliz-ing the service sector, and establishing a freetrade zone for manufactures by 2008. Tunisianproducers will face much stronger competitionin the local market with the implementation ofthe EUAA and in their export markets after theelimination of the MFA by 2005. Since Tunisia’sdomestic market is small, investment andgrowth will depend critically on greater exportcompetitiveness and further integration intothe global market.

The role of the state in a rapidly changing worldscene. The prudent and gradual approach—

which has produced positive developmentoutcomes—is now likely to have reached itslimit under new developments in the interna-tional markets. The demise of the MFA and fullimplementation of the EUAA in the next fewyears impart some urgency to the need toaccelerate reforms to enhance competitivenessand integration into the global economy. Thegovernment still involves itself in economicactivities, with a public investment share ofGDP at 13 percent, and still owns significantshares of the financial sector and publicenterprises, which the government views asnecessary to preserve social cohesion. Onesuch program is the mise à niveau program(box 1.1). The World Bank has reservationsabout the program’s efficacy and the distortedincentives it encourages. More important, theresponse of private investment to the policymeasures has not been as strong as expected.Tunisia’s private gross fixed investmentremains low: averaging 13.5 percent of GDPduring 1997–01, moderately up from 13percent over 1990–96 (World Bank data, 2003)due to the slow pace of reform. Public invest-ment accounts for another 13 percent of GDP.The high and persistent unemployment rate(14.3 percent in 2003) highlights the need tostrengthen investment to sustain highergrowth and generate jobs under increasingcompetitive pressures. As such, sustaining

6

R E P U B L I C O F T U N I S I A : C O U N T R Y A S S I S TA N C E E VA L U AT I O N

1990–01 1990–95 1996–01$m % $m % $m %

Total receipts, neta 689 100 762 100 615 100

IBRD 33 5 48 6 18 3

EC/ EU 347 50 280 37 413 67

France 98 14 64 8 132 21

Germany 26 4 26 4 23 4

Japan 100 15 100 13 100 16

United States 62 9 128 17 –4 –1

Arab countries and agencies 3 0 17 2 –10 –2

a. Total includes both official and private flows, from all sources, excluding the Islamic Development Bank.

Source: OECD (2003), as detailed in Annex A, table A.3a.

T u n i s i a : N e t R e c e i p t s o f E x t e r n a l F i n a n c i a l R e s o u r c e s , 1 9 9 0 – 0 1 ( y e a r l y a v e r a g e s )

T a b l e 1 . 5

Tunisia’s positive economic performance in themore competitive environment it is likely toface in the next decade will likely requirereducing the government’s role in economicactivity, as well as continuing to improve thedesign and operational efficiency of the regula-tory and incentives regime, with the objective

of leveling the playing field within the privatesector. Past positive development outcomeshave fostered a large middle class (80 percentof the population) that will press for greaterparticipation in the development processthrough an increased role for civil society andthe private sector in the process.

T U N I S I A’ S S O C I O E C O N O M I C D E V E L O P M E N T: P R O G R E S S A C H I E V E D A N D C H A L L E N G E S A H E A D

7

Mise à niveau program and the Government Ninth DevelopmentPlan (1997–01). The Ninth Development Plan aimed at improv-ing business conditions and competitiveness. Within this frame-work, the mise à niveau program targeted the modernization ofindustrial infrastructure by adopting new technology, promot-ing quality, and training workers. The program finances: (i) up-grading and modernization of equipment, for which the subsidycovers 10 to 20 percent of the cost; (ii) the cost of “intangibles”(e.g., consultants and software), for which the subsidy coversup to 70 percent of the cost; and (c) financial restructuring, forwhich no subsidy is provided.

Mise à niveau program coverage. This program started in 1996and has been targeted at small and medium enterprises (SMEs),i.e., enterprises with more than 10 employees. So far, 2,700 outof approximately 3,600 eligible enterprises have participated. Ofthese, 1,550 have had their restructuring programs approved.However, the program is having difficulty reaching the small endof the SME sector since these firms have problems in obtainingthe required commercial bank sponsorship. They are too smallfor the commercial banks and too large for the specializedmicro credit bank.

Program effectiveness. About 1,550 enterprises benefitedfrom the program, requiring total investment expenditures ofTunisian dinar (TD) 2.5 billion (US$1.8 billion) and matching in-centives grants from the government of TD 356 million (US$260

million or 1.3% of GDP). These grants are funded by a 1 percentsurcharge on the value added tax (VAT), which has raised, so far,about TD 30–40 million annually. In addition, the EU and theAfrican Development Bank (AfDB) supported the program. Themanagement of the mise à niveau concluded that, between 1997and 2003, the firms benefiting from the program seem to have out-performed the manufacturing sector’s benchmark with regardto turnover (11 percent growth compared to 8.5 percent for thebenchmark); export growth (16 percent growth compared to 11percent); and employment growth of 4 percent (not bench-marked). However, the real net effect of the mise à niveau pro-gram is not clear, either in terms of actual improved performancein relations to enterprises that have not benefited from such as-sistance, or in terms of penetration of export markets.

The mise à niveau program is controversial. While the EU andthe AfDB are supporting the program financially, the Bank hasreservations about its efficacy and the distorted incentives it en-courages. The government feels that it would be politically verydifficult to subject enterprises to more competition without sup-porting the enterprises with technical assistance and equipmentfinancing to upgrade their operations. The government alsoseeks to support social stability through this program. TheBank’s reluctance to support this program, given its reservationsabout the program’s efficacy and targeted nature of the support,is justified.

M i s e à n i v e a u P r o g r a m ( E n t e r p r i s e R e s t r u c t u r i n g a n d U p g r a d i n g )

B o x 1 . 1

Source: OED Mission findings.

9

World Bank AssistanceProgram

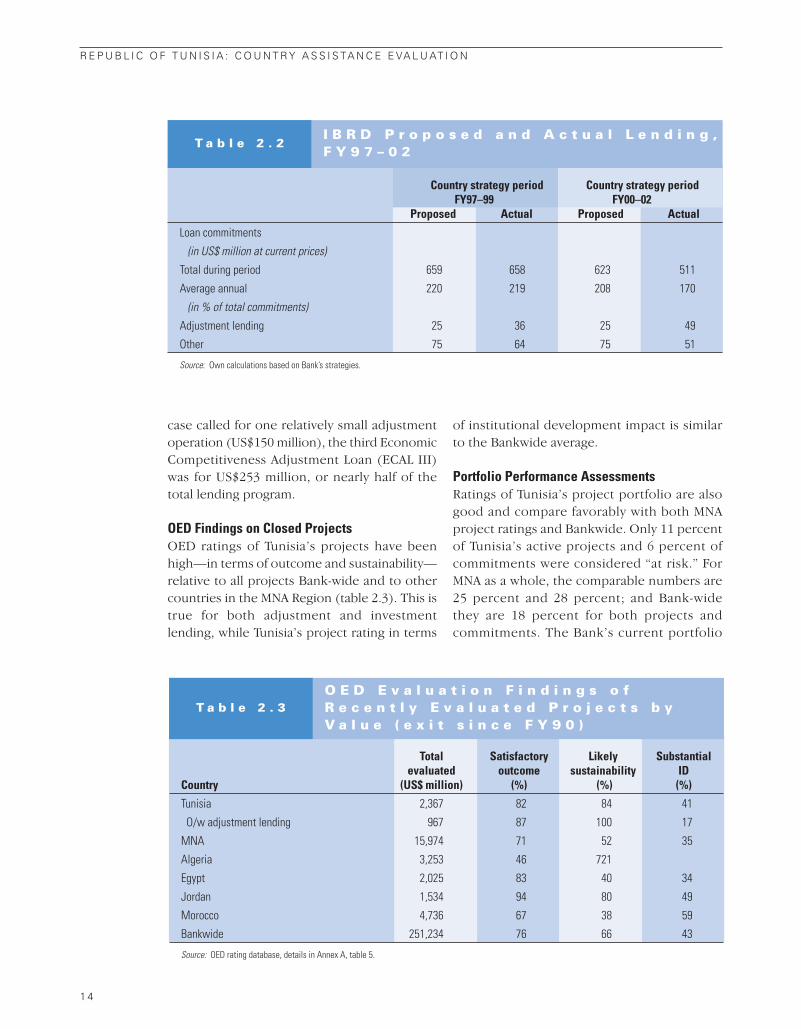

The World Bank has been a large player in Tunisia in terms of both lend-ing and policy influence. Annual average lending commitments for fiscalyears 1990–03 were US$200 million (or US$20 per capita per year), rep-

resenting over one-quarter of the MNA portfolio (figure 2.1). Annual average netdisbursements were US$27 million; however, net transfers were negative for mostof the period, as old loans were being serviced and repaid (the Bank has com-mitted US$5.1 billion for 121 projects since 1958).

The Bank also served as a significant catalystfor mobilizing resources, leveraging US$1 onevery IBRD dollar. The Bank also maintained anactive policy dialogue, and its analytical workpointed out the agenda for reforms and guidedBank strategies and lending.

World Bank Assistance StrategiesIn the 1990s and in 2000, World Bank programswere guided by country strategy documents (box2.1). The overarching strategy objective is growthwith equity. The Bank emphasized support for (i)stability and growth, boosting competitiveness,enhancing outward orientation, and rejuvenatingprivate investment; (ii) human development; and(iii) rural development.

The mid-1990s country strategy was basedon the 1995 Country Economic Memorandum(CEM), which argued for a Bank program inTunisia that would support the country’sefforts to promote economic integration within

the world economy, and particularly that of theEU, while maintaining social stability andenvironmental sustainability (World Bank1995b). The proposed Bank program underthis country strategy emphasized nonlendingservices and, within lending operations, sectorinvestment loans to support targeted sectoralpolicies to modernize key sectors (box 2.1).

The 2000 Country Assistance Strategy (CAS)reaffirmed the main themes and objectives ofits predecessor, reflecting the judgment thatBank assistance to Tunisia should stay thecourse of a strategy that had yielded goodresults so far and was still appropriate. Accord-ingly, the Bank would support Tunisia’s effortsto: increase its outward orientation; develop alarger and more dynamic private sector; furtherstrengthen human resources; and consolidateenvironmental management (box 2.1).

World Bank strategies were relevant andconsonant with Tunisia’s development priorities

22

as outlined in a series of five-year plans. Forexample, the Ninth Development Plan(1997–00) aimed at opening up the economy tocompetition while maintaining macroeconomicstability and strengthening the social agenda andenvironment management. The Tenth Develop-ment Plan (2002–06) also aims to strengthencompetitiveness, embrace the knowledgeeconomy, and meet the jobs challenge. TheBank strategies reflected Tunisia’s developmentpriorities as outlined in its development plans.The increased focus on the social sectors in theBank strategies has been appropriate and isreasonably aligned with the MDGs and thecountry’s emphasis on human resourcedevelopment.

While largely relevant to Tunisia’s develop-ment constraints and priorities, the countrystrategies did not pay sufficient attention to thefiscal sustainability of social policies, withhealth care and social affairs absorbing a fifth ofgovernment spending and general educationanother fifth of the budget. There are seriouseducation sector fiscal issues looming, withdeclining primary student populations andbooming demand for secondary and highereducation.

World Bank strategies developed indicatorsfor monitoring results, but several of these aredifficult to measure effectively since they are

neither quantified nor time-bound. Manyindicators exhibit such weaknesses as vaguewording, input orientation, or no baseline data.For example, in the education sector, the 2000CAS progress indicators include “greater costrecovery in higher education, improvements inteacher training”; in the health sector,“enhance efficiency of public expenditure onhealth.” Despite the declaration about theimportance of monitoring and evaluation(M&E), the commitment to M&E is weak.1 The2000 CAS (p. 33) noted that the indicators weresubject to refinements: “These indicators, to berefined with additional data availability, havebeen designed from available baseline valuesand reasonable medium-term targets.”

Economic and Sector Work Economic and sector work (ESW) was relevant,of high quality, conformed to the Bank’sassistance strategy, and provided a solid basisfor policy dialogue with the government(annex table A.4). Some core diagnostic ESW—including the 1995 Country EconomicMemorandum (CEM), the 2000 Social andStructural Review, and the 1995 Poverty Allevia-tion report—covered macro, social, andsectoral issues, and informed Bank strategiesas discussed below. Other ESW sought toaddress known policy shortcomings in such

1 0

R E P U B L I C O F T U N I S I A : C O U N T R Y A S S I S TA N C E E VA L U AT I O N

–300

–200

–100

0100

200

300

400

500

90 91 92 93 94 95 96 97 98 99 00 01 02 03

US$m

Commitments Net disbursements Net transfers

B a n k C o m m i t m e n t s , D i s b u r s e m e n t s , a n dT r a n s f e r s

F i g u r e 2 . 1

sectors as finance and water, as well as laborand employment issues (annex table A.4). Onthe other hand, the last agricultural sectorreview was undertaken in 1982.

The World Bank’s analytic and advisory activi-ties (AAA) were generally sound but had somenotable omissions, as discussed below. Tunisiais a relatively small country and increasing itsintegration into the global markets wasappropriately emphasized; the high tariff andnon-tariff barriers of the 1980s were distor-tionary, and replacing them with low anduniform tariffs was the right approach. Themain thrust of the 1990 analytical work was toargue the case for a greater openness in theTunisian economy in order to increase competi-tion and thereby the efficiency of investment.The work also emphasized the need to explic-

itly adopt a more aggressive export-orientationpolicy. The recommendations of a subsequenteconomic report in 1991 reinforced those of theearlier work and stressed the need to increasethe efficiency of investment by increasingdomestic and foreign competition.