report no. 8044-tun republic of tunisia public disclosure ......report no. 8044-tun republic of...

TRANSCRIPT

Report No. 8044-TUN

Republic of TunisiaCountry Economic Memorandum: The Road toan Outward-Oriented Economy(In Five Volumes) Volume Ill: Annex 2The Tunisian Financial System in Support of Investment

March 1990Country Operations DivisionCountry Department 11Europe, Middle East and North Africa Region

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in' the performance of their official duties Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

FOR OMCIAL USE ONLY

REPUBLIC OF TUNISIA

ANE 2

THE TUNISIAN FINANCIAL SYSTEM INSUPPORT OF INVESTMENT

This document has a restacrted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

GLOSSARY OF ABBREVATIONS

APB Association Professionnelle des Banques(Professional Associatior of Banks)

BCT Banque Centrale de Tunisie(Central Bank of Tunisia)

Billets de tresorerie Commercial paperBons d'Equipement Treasury Bonds (Government bonds)Bons du Trdsor Treasury billsCENT Caisse d'Epargne Nationale Tunisienne

(National Savings Bank)CNEL Caisse Nationale d'Epargne-Logement

(Housing savings fund)FOPRODI Fonds de promotion et de decentralisation industrielle

(Industrial development fund)FOSDA Fonds sp4cial de developpement agricole

(Agricultural development fund)IPbC ImtwL suL !es revenus des creances

(Tax on income from credit)IRVM Impot sur les revenus des valeurs mobili6res

(Tax on income from marketable financial instruments)

REPUBLIC OF TUNISIA

THE TUNISIAN FINANCIAL SYSTEM IN SUPPORT OF INVESTMENT

TABLE OF CONTENTS

Page

I. INTRODUCTION . . . . . . . . . . . . . . .

II. THE STRUCTURE OF THE FINANCIAL SYSTEM . 2 . . . . . . . . . 2The system in the first half of the 1980s . . . . . . 3Recent Reforms . . . . . . . . . . . . . . . . . . . 6The functioning ot the money market . . . . . . . . . 14

III. FINANCE AND THE MOBILIZATION OF SAVING . . . . . . . . . . 16Saving vs savings: what finance can do . . . . . . . 16Competition for savings . . . . . . . . . . . . . . . 17

±V. FINANCE AND INVESTMENT . . . . . . . . . . . . . . . . . . 20Investment behavior and financial incentives . . . . 20The capital market ................. 22Forced investment: tax or subsidy ? . . . . . . . . 24Summary and Recommendations . . . . . . . . . . . . . 26

REPUBLIC OF TUNISIA

THE TUNISIAN FINANCIAL SYSTEM IN SUPPORT OF INVESTMENT

I. INTRODUCTION

1. When financial systems function smoothly, they often go unnoticedand, indeed, are unappreciated for their contribution to mobilizing savings andensuring its productive allocation. In Tunisia the financial system--mainlythe banking sector--instead attracts attention for its reputedly high profits,its lack of innovation, and in recent years for a lack of support for privateinvestment. Public sector officials and private sector participants alike arequick to accuse the banks of being excessively conservative and of not being a"real partner" of industry. Thus the failure of private sector investment torecover rapidly following the adjustment program of 1985/6 is, in the view ofsome, due to the risk aversion of the banking sector and its uncompetitivemarket.

2. There is much truth in this view, but it is incomplete and quicklybecoming outdated. The financial sector has been going through such rapid changethat a truer view now would be that the contribution of the sector to therecovery of investment and its greater efficiency will depend on the speed andenterprise with which agents in the sector respond to the reforms that have beenoccurring. The same question of how firms respond to the new environment hasbeen discussed in the in the mair. report in the broader of the context of theoverall liberalization program, but it is in the financial sector that thereforms have been especially fast and sweeping, and where the expectations ofchange and innovation have been most firmly established. A number of structuralproblems and obstructions to efficient operation of the market mechanism remain,but the pace of reform does not appear to have slackened, so that it can beexpected that the issues they pose will be addressed. The Central Bank, whichhas been the main initiator of the reforms, has felt its pace to be constrainedby the need for the support of the banks, and the dangers both of alienating theusers of the financial system and of causing shocks that could createinstability.

3. The major outstanding issues of the financial system reflect theseconstraints. They are the method of funding government debt, requirements tolend to priority sectors, caps on banks spreads, excess concentration, a rigidbank salary structure, a marked scarcity of equity and collateral, and a fragilebalance sheet position. Public ownership of some of the largest banks appearsto complicate attempts to increase competition. Limitations on interest spreadsseem inconsistent with the Government's desire to encourage risk taking, whilethe offering of government debt at high rates, as was the case in 1988 and inearly 1989, can prompt a form of financial crowding out. Yet because of concernsthat the degree of competition is insufficient, the Tunisian authorities have

- 2 -

been a.erse to removing remaining interest rate controls--in fact, they usedmoral suasion in early 1989 to reduce spreads even further. The absence ofgenerally accepted accounting standards and undeveloped auditing standardslessens the transparency of financial statements and thereby both hinders thedevelopment of an equity market and renders term lending less attractive.

4. This annex will describe the structure of the Tunisian financialsystem, analyze its role in mobilizing savings and financing investment, andenumerate the constraints and incentives facing the financial institutions there.Since the liberalization of the financial system began only recently, and sincemany of the features of the current system reflect a more heavily regulatedsystem, the next section will begin with a brief description of the system duringthe early 1980s and then describe some of the reforms. Although as will be seenthe Tunisian financial system does an admirable job of mobilizing savings, avariety of constraints--and the lingering effects of regulation--hinder itsability to allocate these savings efficiently. The concluding section offerssome recommendations to improve the financial system's support of investment.A key part of the recommendations is to increase the reliance on market interestrates and to induce more vigorous competition.

II. THE STRUCTURE OF THE FINANCIAL SYSTEM

5. The Tunisian financial system has undergone significant changes inthe last 3 years, moving from a heavily regulated framework, in which credit wasprimarily allocated and interest rates managed by the Government, to one in whichthe banks have more scope to allocate credit and, within limits, set interestrates. Rather than being implemented by a system of rediscounting, monetarypolicy is now effectuated primarily through the money market. A significant CMmarket is now functioning and there is a market for the issue of commercialpaper, though it only became active at the end of 1989. Although fixedpercentages (up to 25 percent) of bank deposits must be held in the form of long-term government debt (Bons d'Eguipement) and loans for housing finance, a marketin 3-month Treasury bills (Bons du Tr6sor) began in 1989 and eventually maypermit decreased reliance on the forced allocation of long-term government bonds.

6. As noted below, significant restraints remain on banks. Deposit andinvestment banks continue to be segmented, and there is only a minute equitymarket. The absence of more vigorous competition is abetted by the Government'sample provision of a risk free asset that recently has been bearing an attractiverate of interest. Banks generally are underprovisioned and undercapitalized,and thus may be expected to avoid actions that could lead to an increase incompetition and lower profits. Even with their new freedoms, banks may beaffected by habits acquired during periods of heavy regulation. Indeed, the mostremarkable feature of deregulation is that it has been at the initiative of theCentral Bank, which had to confer with the banks in their design. The banksappear to be beginning to behave more competitively, even if it may be some timebefore Tunisia has a dynamic, innovative banking sector. But, the reforms havecreated momentum in that direction.

- 3 -

Table 1TUNISIA: BANK OWNERSHIP, 1987

Assets Percentage of ShaXes Held by:Bank (M Dinars) Public Sector Private Sector Foreign Sector

BNT 1,184 58.2 41.8 0STB 1,173 56.7 43.3 0BIAT 545 8.5 56.1 35.4UIB 433 57.7 25.6 16.7BS 430 51.5 33.9 14.7BT 379 0 61.2 38.8UBCI 299 0 48.6 51.4CFCT 262 0 100.0 0ATB 147 0 36.6 63.4BFT 60 27.7 20.3 50.0

Source: BCT

The system in the first half of the 1980s

7. Tunisia's financial system is well developed in comparison with manydeveloping countries. Its main components are the Central Bank (BCT), twelvedeposit (commercial) banks, eight investment banks (also termed developmentbanks), one specialized savings institutions (CENT), and eight offshore banks.Of the deposit banks, one was a specialized savings institution for housing, theCNEL, which has been transformed into a deposit bank specializing in housing,the Banque de l'Habitat, and another is the onshore branch established inNovember 1989 by one of the offshore banks. One investment bank, the BanqueNationale de D6veloppement Agricole (BNDA) was merged with the Banque Nationalede la Tunisie (BNT) in October 1989 to create the Banque Nationale Agricole(BNA). The Government holds a majority share in four of the largest fivecommercial banks and has a 50 percent stake in most of the investment banks (seeTable 1). Additionally, there are several portfolio management and insurancecompanies, a leasing firm, the postal checking center, and the stock exchange.The commercial banks dominate the system in terms of their share of assets,deposits, and credit to the economy (see Table 2). Although this broad structurepersists today, in the early 1980s the system was highly segmented.

- 4 -

Table 2THE STRUCTURE OF THE FINANCIAL SYSTEM(Millions of Dinars, November 1988)

Credit toAssets (X) Deposits (r) the Economy (X)

Commercial Banks 5,409 (73.5) 3,206 (90.6) 4,136 (76.2)Other FinancialInstitutionsi 1,950 (26.5) 333.1 (9.4) 1,294 (23.8)

1/ Comprises the development banks, CENT, CNEL, a leasing firm,the offshore banks and portfolio management firms

Source: BCT Statistigues Financieres

Commercial banks funded themselves through demand, savings, and time deposits,which together accounted for about two-thirds of their total resources, enjoyedrediscounting and advance facilities of up to 17.5 percent of their totaldeposits, and, along with the development banks, were allowed access to specialresources of the Government or resources raised from abroad for the financingof certain credits. The investment banks were not allowed to accept depositsexcept in special circumstances and instead relied on the aforementioned specialresources--in particular, foreign borrowing--as well as on eauity funds andissues of their own, generally longer-term obligations. Investment banks alsowere--and still are--precluded from providing short-term credit.

8. This segmentation limited competition, and was reinforced bycomprehensive controls on interest rates for both deposits and loans and oncommissions as well. Interest rates in real terms on deposits generally werenegative, as were rates on many loans (see Table 3). The scope, if any, forinterest rate variation left to the banks was a range of 25 or 50 basis points.Additionally, there was a system of prior authorization (autorisation prealable)and refinancing approval (accord de refinancement) which limited the types ofloans granted and restricted the ability of banks to offer different terms.Under this system, in effect until December 1986, the commercial banks neededthe prior authorization of the BCT for short-term loans in excess ofTD 1 million, for medium-term loans other than to certain priority sectors (SMEs,exports, and agriculture), and for all long-term lending. Refinancing of short-term loans in excess of TD 100,000 also required central bank approval. Althoughthere has been a money market since the early 1960s, it was more akin to arediscount window of the BCT. Interbank operations were not allowed, and thecentral bank set both the interest rate and the refinancing accorded each bank.

- 5 -

INTEREST RATES AND INFLATIONPercent per Aamum

Sept. 1. 1977 April 1, 1981 April 22. 1985to March 31, 1981 to April 21, 1865 to Dec. 31, 19868v

Demand Denosits 1.00-2.00 1.00-2.00 1.00-2.00

Soecial SavinsaAccounts

0-12 months 4.00 5.50 6.7S12-18 months 5.25 6.75 7.7518-24 months 6.50 7.75 8.7524 + months 7. 0 8.76 9.75

Terms DeRouits

3-6 months 1.50 3.50 4.506-12 months 3.00 5.00 6.0012-18 months 4.50 6.25 7.2518-24 months 6.00 7.50 8.5024 + months 7.00 8.50 9.50-10.00

Lending Rates

Overdrafts 8.50-8.75 10.00-10.50 12.625Short-termPriority 5.00-7.75 5.50-7.75 6.00-10.00Non-priority 7.25-7.75 8.50-9.00 10.00-10.50

Medium-termPriority 5.50-7.00 5.50-9.75 5.50-8.50Non-priority 8.00-8.25 9.75-10.00 11.50-11s50

Long-termPriority 10.50 12.00-12.50Non-priority - -

Consumers Prices3. 8.42 9.57 7.36

/ On January 1, 1987, deposits rates were dneeulated and non-priority loan rates were limited to 300 basispoints over the money market rate.

I/ Average annual rate during the period.

Source: BCT Statistioues Financlires

9. Most significantly, the commercial banks were subject to severeportfolio requirements. Under the Ratio Global du Financemenr de DevelopRement,the commercial banks were required to allocate up to 43 percent of their depositsin the following manner: they could be required to hold the equivalent of up to20 percent of their deposits in the form of 10-year Treasury bonds (Borsd'Eguinement) and a further 5 percent in the form of bonds issued by the housingsavings fund, CNEL; and their medium- and long-term lending had to reach18 percent, of which 2 percent was to go to SMEs. Any shortfalls were penalizedby compulsory reserves at the Central Bank equal to the shortfall and not bearinginterest. The CNEL made little use of this financing and the proportion of CNELbonds never topped 1 percent of deposits. (In practice the proportion ofTreasury bonds to deposits often fluctuates around 22-24 percent.) Reserve

requirements on deposits of residents had been 0 percent since 1982 until theywere raised to 2 percent in June 1989.Y

10. Thus prior to the 1986 reforms the Tunisian financial system wasrepressed. In part because inflation rates remained under control, real interestrates were not as sharply negative as in the Southern Cone countries of LatinAmerica but were sufficiently low to guarantee that some mechanism other thanthe price system was being used to allocate credit. In Tunisia, it was theextensive use of government credit guidelines that allocated credit. Clientsshowing up at the lending window of commercial banks already had the Government'sapproval and, consequently, the incentive for banks to expend much effort inevaluating credit decisions was low. This habit and the requisite skills maytake some time to develop.

Recent Reforms

11. Beginning in December 1986 the Tunisian authorities began toliberalize the financial system. Deposit rates were freed, with the exceptionof rates on special savings accounts and the convertible dinar accounts ofTunisians working abroad (both pay a minimum of the average money market rate(TMM) less 200 basis points). Lending rates of commercial banks, except topriority sectors, were partially liberalized, in that they were subject to aceiling over the money market rate. Initially that ceiling was 300 basis pointsbut, in January 1989, the deposit banks responded to Government suasion andvolunteered tE.rough their Association Professionnelle des Banques (APB) to limittheir spreads to 250 basis points as part of the Government's program toencourage investment. Investment banks are not subject to interest rate capsbut are forced to keep their rates close to those offered by deposit banks.

12. The global ratio has also been modified; the requirement that mediumand long term loans be equal to at least 18 percent of deposits has been replacedby the requirement that the equivalent of at least 10 percent of deposits be lenton preferential terms to the sectors classified as priority--agriculture, smalland medium enterprise, and exports. The penalty for shortfalls is the same asit was for the 18 percent ratio. Since June 1989 the investment banks have beenallowed to make preferential medium term loans i.e. less than seven years. Allthe subsidy comes from the State since these loans are eligible for rediscountingat the Central Bank at the rates indicated in Table 4. The portiotis of theseloans that cannot be so rediscounted pay interest at the normal lending ratesof the banks, thus raising the effective cost to the borrower. Although thebanks' margins are narrow, they appear to cover the costs. The attracti3n tothe deposit banks is that these loans give them a competitive advantage ovfr theinvestment banks, since roughly 80 percent of preferential loans are shor; termand the costs of administering relatively small scale investments are too high

I, There were minor exceptions: non-resident suspense accounts (through whichdividend payments transit) and capital accounts were subject to 40 percentreserve requirements, while convertible dinar accounts of Tunisiannationals were exempt. These exceptions were removed in February 1990.

for the investment banks to be attracted by the allowed margins. The banks arealso used to channel some lending to priority sectors from budgetary funds(ressou ces sg6ciales), such as the FOSDA for agriculture and the FOPRODI forsmall industrial enterprises.

Tabe1 4

PRIORITY INTEREST RATESV(Percent per Annum)

Priority Sector Rediscount Lending RediscountableRates Rate portion in X

1. ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~1. Short Ter

Certain guaranteedagricultural credits 3.00 7.00 100

Export financing 4.00 6.00 85Seasonal agricultural advances 4.75 7.00 100Advances for cereals, olive oil,

wine 4.75 6.00 85

2. Medium Term

Crafts and manual trades 5.50 7.00 100Energy 5.50 7.00 100Agriculture 6.00 7.50 100Exports, small and medium

enterprise 6.50 8.00 100

1/ In effect since September 1988

Source: BCT

13. At least as significant potentially, the minima above which priorauthorization or refinancing approval was required were raised and thenabandoned in 1988. Indeed, the central bank even stopped collecting the detailedinformation on the nonfinancial sector, which in the past it had required to makecredit judgements. The former system was quite cumbersome, in that long delayswere required to obtain central bank approval and then actually obtain the fundsfrom a commercial bank.

- 8 -

14. Along with the reforms, the taxation of financial instruments beganto be changed, starting with taxes on borrowing. Throughout the 1980s there werethree taxes on overdrafts, which added as much as 315 basis points to the maximumlending rate, and one tax on loans. The first, the Commission de Garantie, isused to finance certain priority sector loans. The second, the Commission deP6r6guation de Change, covers losses for the foreign exchange risk guaranteescheme that the Government provided until last year. Although the scheme is nowdefunct, the tax is still collected to cover outstanding losses. Finally, therewas the Taxe sur la Prestation des Services, or TPS, now the Value Added Tax onlending. Its rate rose gradually from 7.5 percent in 1978 to 14.3 percent in1987--for overdrafts it was applied to the sum of the lending rate plus the twoother taxes--but then was reduced in stages to zero by November 1988. TheGovernment also reduced the Commission de Garantie tax by half. Thus, as shownin Table 5, the maximum total cost of borrowing declined from 16.1 percent in1987 to 12.1 percent in February 1988. At present the wedge between the ratereceived by the banks and that paid on overdrafts by the borrowers is0.8125 percent.

Table 5THE IMPACT ON TAXES ON LENDING RATES

(Percent per annum)

Lending Rate Commission Commission Total Cost(max.) de Garantie de P6requation TPS of Overdrafts

1978-80 8.750 0 0 0.658 9.4081981 9.875 0.625 0 0.790 11.2901982-84 9.875 0.625 0 0.913 11.4131985 11.500 0.625 0.5 1.173 13.9781986 11.500 0.625 0.5 1.481 14.1061987 13.000 0.625 0.5 2.017 16.1421988 12.500 0.625 1' 0.5 2.017 a 15.64019892' 11.250 0.313 0.5 0 12.063

1/ Lowered to 0.3125 in November, 1988/ Lowered to 0.846 in July and to 0 in November

.X As of February, 1989

Source: BCT and Bank staff estimates

15. Finally, as explained in the following section, the money market wasliberalized, new instruments were allowed, and the Central Bank began to relyon the money market as its main conduit for the implementation of monetary

policy. Although the BCT continues to rediscount loans to priority sectors,such injections are now required to be offset in the money market, therebyrobbing rediscounts of their influence on monetary policy. Perhaps the mostinteresting feature of Tunisian financial reform is the manner in which it cameabout. In many markets, financial innovation has resulted in part from acompetitive response of financial firms to a changing environment. For instance,in the United States and several other industrial countries, some large corporateborrowers attained as high or higher credit ratings than their banks, were notburdened by reserve or capital requirements, and therefore began to borrowdirectly at lower cost. Reduced loan demand by high quality borrowers and lowerprofitability from lending activities led banks to seek out other areas forprofitable expansion. Thus banks behaved in line with survival theories of thefirm, according to which dwindling profits, through either poor experience oran increasingly competitive environment, give impetus to innovation. Indeed,innovation seemed to occur foremost in the United States and the Euromarkets,where competition appeared to be the most intense. To be sure, other factorsencouraged innovation, most notably the advances in data collection, computing,and communication, and the deregulation of financial markets. But in manyinstances, innovation seemed to spur deregulation, rather than vice versa.

16. In Tunisia, innovation has thus far been overwhelmingly at theinitiative of the Government. In fact, it was only through long consultationsthat the banks were won over to some of the measures, especially the ending ofthe "autorisation pr6alable", having found comfort in their interpretation thatthis system provided an implicit assurance that Central Bank refinancing wouldalways be available. By granting prior authorization for loans and settinginterest rates, the Government in effect was actively helping to limit bankcompetition. Thus it is not surprising that some banks did not want any change.Their volunteering, through the APB, to limit their spreads this year providesfurther evidence that banks are inclined to collusion, at least as regardslending. As regards deposits, the authorities find that competition is greater.

17. That innovation has been initiated by the regulatory authorities,rather than arising from competitive activity, is perhaps the best evidence thatthe competitive habit in Tunisian finance is not well developed. In additionto the aftereffect of regulation, the dearth of competition may reflect a highdegree of concentration. Unfortunately, measures of concentration present anambiguous picture. According to one measure, the Herfindahl-Hirshman index ofindustrial concentration, Tunisia's banking system is not nearly as concentratedas in other developing countries (see Table 6). In particular, it appears tobe much less concentrated than the system in Algeria and about on par with thatin Morocco.V This index has some appeal. First, under certain types of marketstructure, the markup over cost can be proven to be proportional to the H-index.

This index is defined as: H - E(a,/A)]2

where a, represents the volume of assets in bank i and A is the totalassets of the banking system. Thus the index implies that the greaterthe number of banks and the more equal they are in size, the lesser isthe degree of concentration. With possible values between zero and one,countries with an index close to one would have greater degrees of bankconcentration.

- 10 -

Also, it does as wvll or better than other ratios in predicting profi rates byindustry in the United States.Y Although the Herfindahl index usually accordswith another popular measure, the three-bank ratio (the share of deposits heldby the three largest banks), this is not always the case: as seen in Table 6,in the early 1980s--and in all likelihood recently as well--the latter ratiorates the Tunisian banking sector as among the most concentrated in the group.

See Patrick Honohan, "Concentration Measures in Banking," World Bank memo,March 1989.

- 11 -

Table 6CONCENTRATION MEASURES IN BANKING

H-Index 3-Bank 4-BankCountry 1986-87 Ratio, 1981-83 Ratio, 1986

Algeria 0.29 - 100Bangladesh 0.20 74Botswana 0.45 100Brazil 35Cameroon 0.18 82Chile 0.09 42 54Colombia 0.40 45

Costa Rica 92C6te dllvoire 0.14 67Ecuador - 32 -

Ghana - 100Indonesia 0.10 66Kenya - 65Malaysia - 42 64

Morocco 0.18 - 70Nigeria 0.09 - 52

Pakistan 0.26 - -Philippines 0.06 - 40Peru - 51 -

Senegal 0.16 - 78

Thailand 0.13 - 65Tunisia 0.19 69 80Turkey 0.04 50 52Uganda - - 52

Venezuela 31 -Yugoslavia - - 70

Avarage 18.5 44.0 69.9REmge 0.04 - 0.45 31 - 69 40 - 100

Source: Roberto de Rezende Rocha, "Costs of Intermediation in DevelopingCountries: A Preliminary Investigation", The world Bank, Industryand Finance series, Volume 18, 1986, and World Bank estimates.

- 12 -

18. Finally, the absence of competition would be expected to be evincedin interest spreads. As seen in Table 7, both Tunisia's gross interest margins(interest received less interest paid, plus other net income, such as commissionsand fees) and operating costs compared favorably with those of other developingcountries and were about equal to the OECD average in 1982. However, since bothpublic and private sector banks wages are determined by the Governi4ent, thiscomparison perhaps suggests less about the efficiency of Tunisian banks than itdoes about the level of wages. In fact, in 1986 gross margins of Tunisian banksstill were virtually identical to the unweighted average of those in the OECDarea, but net margins were higher (1.6 percent of total assets, compared with1.1 percent in the OECD), reflecting lower salaries and, perhaps, less investmentin computerization. The after-tax (and after provisions) profit rate, relative

j to assets, also was slightly higher in Tunisia than in the OECD (0.5 percent,compared with 0.36 percent in the latter).

19. To be sure, this comparison says nothing about the adequacy ofprovisions. Indeed, the Tunisian authorities consider overall provisions to beinadequate.v Provisioning has grown rapidly in recent years, but it startedfrom a small base. Yet the authorities and banks are reluctant to accelerateprovisioning by reducing dividends because they judge that it will make itdifficult for the financial system to raise capital in the future, while theincrease in the rate of provisioning would be fairly small. This supposes thatthe public's view of the banks' condition is overly sanguine and that thereaction would be extreme. Moreover, there is some scope for reducing dividendsto provision; in 1987 dividends were about TD 12 million, equivalent to about19Z of net profits after tax. By comparison, in Morocco banks have sounderportfolios and paid out dividends equal to about 21% of profits.

20. Over the longer term it is likely that the financial reforms alreadyin place will put more pressure on bank profits. As noted below, the reformof the money market likely will lead to some financial disintermediation, evenif the commercial paper market remains small. Although there is hope that, ina less regulated environment, banks will become more innovative and competitive,it may take some time for practices developed during a long period of heavyGovernment intervention to wear off. Thus reforms should be considered whichwill hasten this process.

Provisioning was deterred by the lack of tax concessions. Provisions upto only 10 percent of profits were tax deductible and had to be spread overfive years. Thus banks with lower profits -- and quite possibly a greaterneed to provision - - had less incentive to do so. Such a system does notinduce a prompt recognition of problem loans. In fact, until recently,banks could not provision until they had demonstrated that they hadexhausted every legal means (despite the backlog in the court system) tocollect on their loanst This has now been eased; the limit was raised to20 percent of profits in December 1988 and the five year period has beendropped. But provisioning is limited to loans for which judicialproceedings for recovery have been started.

- 13 -

Table 7

ASSESSMENT OF THE EFFICIENCY OF THE FINANCIAL SYSTEMSOF DEVELOPING COUNTRIES

Deviations from OECD averageTotal values as a Z of GDP

Assets/ Gross OperatingCountry Series Year GDP Margin Costs

Brazil 1981 10 largestholdings 0.134 2.9 1.3

Colombia 1982 AllCommercial 0.247 0.7 0.7

Ecuador 1982 AllCommercial 0.329 1.0 -

Korea 1981 NationwideCommercial 0.293 0.2 0.0

Liberia 1981 AllCommercial 0.279 1.6 1.2

Malaysia 1982 AllCommercial 0.729 0.0 0.0

Mexico 1983 DomesticBanks 0.233 0.6 0.5

Pakistan 1983 AllCommercial 0.464 0.2 0.2

Peru 1981 AllCommercial 0.202 1.4 0.8

Portugal 1982 FinancialSystem 1.369 0.0 0.0

Sri Lanka 1983 AllCommercial 0.369 0.8 0.6

Thailand 1980 AllCommercial 0.408 0.3 0.0

Tunisia 1982 AilCommercial 0.524 0.1 0.0

Turkey 1980 AllCommercial 0.281 1.8 1.7

Turkey 1983 AllCommercial 0.452 0.9 0.8

Venezuela 1980 AllCommercial 0.377 0.7 0.6

Source: Roberto de Rezende Rocha, "Costs of Intermediation in DevelopingCountries: A Preliminary Investigation," The World Bank, Industryand Finance Series, Volume 18, 1986.

- 14 -

The functioning of the money market

21. In January 1988 the money market underwent a fundamental reform whichrepresented an important step towards alleviating the degree of segmentationbetween commercial and investment banks and also should help to stimulatecompetition. The reform had several aspects. First, banks were permitted toissue certificates of deposit (CDs) in a minimum denomination of TD 500,000,and multiples thereof. CDs have terms of 10 days to 5 years, in multiples of10 days, though only deposit banks can issue them with durations of one year orless. Second, non-bank enterprises or other organizations were permitted toparticipate in the money market as lenders, and now can place funds by buyingCDs or other instruments. Third, using a new instrument, dubbed billets detr6s2rerie (a form of commercial paper), non-banks with a minimum capital ofTD 1 million can borrow from other money market participants.

22. These reforms are potentially far-reaching. Allowing non-banks toparticipate could increase the degree of competition in the deposit market, forwhen banks need funds they will bid up the money market rate, leading non-financial firms to switch their deposits into a money market instrument.However, such a shift, which would raise the average cost of funds to the banksand shorten their average maturity, has not yet occurred in significant amountsbecause the weakness of domestic activity has limited the demand for loanablefunds.

23. CDs were immediately successful and their volume has fluctuatedbetween TD 180 million and TD 220 million for most of 1989. But, the new elementof competition that the introduction of commercial paper was to add came slowly,because, at the start, their conditions of issue were too unattractive for themto become significant. Practically no commercial paper was issued until a seriesof modifications and clarifications were made in May 1989. Denominations werethen reduced from multiples of TD 500,000 to multiples of TD 100,000 andmaturities were increased from multiples of 10 days, with a maximum of 180 days,to multiples of 10 days, or multiples of months or years, up to five years. Itwas also made clear that an irrevocable bank guarantee was not a prerequisite,as had been thought, but that it would be enough to have a bank line of creditto cover the issuer's liquidity needs in case money market conditions preventedearlier commercial papers of the issuer from being rolled over without excessivecost. The banks had, at first, little interest in fostering an instrument thatcompeted with their deposits and, hence, charged high premia for theirguarantees. But the measures of May 1989 appear to have reduced the obstaclesto the use of commercial paper: the amount outstanding in February 1990 wasaround TD 40 million and it had reached as high as TD 54 million in Januar-y 1990.

24. Commercial paper markets often do not appear at an early stage inthe development of finance. The U.S. market was an exception, tracing its originto the early 19th century. Limits on interstate branching inhibited the easingof seasonal credit demands in various parts of the country and led firms incredit scarce areas to float their own paper directly on the N.Y. market. Themarket was subsequently boosted in the 1920s with the birth of consumer financecompanies and was furthered stimulateci in the late 1960s with the rise of moneymarket interest rates above that allowed on bank CDs. Thus non-financialcorporations were prompted to go directly to the market, a trend more recently

- 15 -

encouraged by the decline of the credcitworthiness of most money center banks.2In Europe and Japan, the development of the commercial paper market came muchlater and reflected both the improved creditworthiness of nonfinancialcorporations and the lower regulatory costs of direct issues, such as the savingson capital requirements by these firms. In none of these market are backupsrequired, and in some markets they are not used or are demanded by the marketaccording to the level of risk perceived.

25. The reforms of January 1988 changed the nature of Central Bankintervention. Beforehand there was an inter-bank market, but it went throughthe Central Bank, which lent and borrowed at the same rates. The differencebetween the lending and borrowing constituted the Central Bank's interventionthrough the money market. The system was changed in January 1988 to one ofweekly auctions and further elaborated in May 1989. At present the Central Banksets its monetary targets, i.e., the amount of liquidity it will provide, andthen calls for bids from the banks (Appel d'offres). It then can run throughthe bids, going from the highest interest rate downwards, until it reaches itstarget. Or, it can fix the interest rate and accommodate the demands expressedat rates at least equal to the rate it has chosen, in full or in uniformproportion. The Central Bank can also blend these two methods. These CentralBank credits are backed by securities held at the banks (prises en pension) andhave a term of seven days. The calls for bids take place on Mondays. To reducethe liquidity of the banks, the Central Bank can also call for offers from thebanks for loans for a specified period and then accept the offers in order ofincreasing interest rates until it reaches its target (adjudication). Shouldbanks need direct recourse to financing, the Central Bank can accommodate themat penalty rates for seven days against securities held at the banks.

26. Since draining operations can be cumbersome, the Central Bank addedto its array of instruments by introducing, in September 1989, short-termTreasury bills. Thirteen week bills have already been issued and bills of 26and 52 weeks are expected to be issued in the first half of 1990. By the endof 1989 the outstanding amount of Treasury bills was TD 173 million, of whichTD 124 million were held by non-bank institutions and individuals. Treasurybills have two additional advantages, apart from making it easier to drainliquidity. One is that they help lessen the crowding out of the private sertorin long term instruments. The other is that they replace Treasury bonds (Bonsd'equiDement), whose coupon, is now less competitive because a partial taxexemption it enjoyed has been removed by the new law on direct taxation (seeparagraphs 41 and 47).

IV See Marcia Stigum, The Money Market, 1983, for more on the development ofU.S. money markets.

- 16 -

III. FINANCE AND THE MOBILIZATION OF SAVING

Saving vs. savings: what finance can do

27. The development of the financial sector, its ability to offer savingsvehicles, and the confidence with which it is viewed are some of the factorsthat influence people's desire to save and, especially, their desire to savethrough the financial system. By offering instruments bearing an attractiverate of return, banks and other institutions can foster the financial habit.These effects presumably operate over the long term. Most empirical researchon the effects of financial liberalization concentrates on the impact of realinterest rates on the rate of saving--since the other aspects of liberalizationare difficult to quantify--and finds in general very little, if any, effect.To be sure, raising real interest rates may increase the stock of savingsintermediated by the financial sector but shows little effect on the rate ofsaving as measured by national income accounts.V

Table 8LIQUIDITY RATE IN TUNISIA

(Percent of GDP)

1977 1980 1983 1988

Ml 26.2 27.1 30.3 24.3

M2 39.8 41.2 44.0 47.5

Source: IFS

One problem with these studies is that they assume that both the realinterest rate and savings are known with precision. The former usuallyis approximated by the nominal interest rate minus the actual rate ofinflation, even though it is the expected rate of inflation that mattersin rate of return calculations. Instances in which government deregulatedinterest rates with little or no increase in saving may merely reflect thegeneral expectation that inflation was headed back up, that thederegulation will only be temporary, or the influence of other economicforces, such as monetary stringency. The lack of credibility in interestrate reforms is especially likely in countries such as Turkey or theSouthern Cone countries of Latin America, where negative real interestrates had persisted for years and, in some cases, for decades.

- 17 -

28. Recent Tunisian experience is consistent with that of developingcountries in general. As noted in the main part of the report, the rate ofsaving has declined in recent years, despite the improvement in real yieldsavailable to savers compared with those in the 1970s. This decline reflectedseveral influences, not least of which in recent years was the drop in realwages, between 1983 and 1986. However, as seen in Table 8, the ratio of broadmoney to GDP, the popular measure of savings intermediated by the financialsystem, has risen noticeably in the last decade, especially since the early1980s. Concomitantly, the ratio for narrow money has dropped, providing someevidence for the interest sensitivity of Tunisian savers. On the one hand,financial deepening is not very advanced ir. comparison with some of Tunisia'sneighbors, as indicated in Table 9. However, compared with other developingcountries, the degree of financial deepening in Tunisia is fairly high. Infact, as seen in Table 10, the M2/GNP ratio in 1987 was quite a bit higher thanthe average of rapidly growing developing countries during the 1977-87 period,as was the average saving rate.V Aggregate statistics, then would seem toindicate that the Tunisian financial sector does a reasonable job of mobilizingsavings.

Competition for savings

29. One important factor helping to increase the stock of savingsintermediated by the financial sector has been the lifting and finally thederegulation of interest rates. In the late 19703, short-term saving rates werefixed at 1.5 percent to 3 percent, while inflation was in the range of5.5 percent to 10 percent. In response the Government raised the structure ofinterest rates in 1981, but the acceleration of inflation to 13.6 percent in 1982thwarted their attempts to improve the attractiveness of rates on savingsaccounts. In 1985 rates were increased more significantly again, and thenderegulated as of January 1, 1987. After a few days of unrestricted competition,the banks agreed on the structure of term rates for individual depositors, whichare seen in Table 11. However, banks circumvent this agreement and reasonablyvigorous competition for deposits is reported. Moreover, enterprises receivemore favorable rates, especially with their ability to participate in the CDmarket. Indeed, there have been reports that banks offer CD rates slightlyabove the market to retain their large corporate customers, presumably makingup the loss on other business.

1 Tunisia's less productive capital stock has left its growth rate onlyroughly in line with the developing country average. Also, over the period,most countries experience increasing financial deepening and thus endedthe period with a higher ratio. Most dramatically, in Korea the M3/GNPratio was around 40% as recently as 1980 but soared to over 80% in 1986with the rapid growth of the non-bank financial sector.

- 18 -

Table 9

K2(as a fraction of GDP)

1980 1986

Tunisia 0.41 0.46Morocco 0.43 0.51Greece 0.55 0.64Turkey 0.21 0.30Spain 0.81 0.69Portugal 1.09 1.13Italy 0.73 0.62

Source: IFS

Table 10SAVING, GROWTH, AND FINANCIAL DEEPENINIG IN DEVELOPING COUNTRIES

(weighted averages, 1965-87)

Country Groups by Gross National Gross Investment/ Change inGDP Growth Rate Saving/GDP GDP GDP/Investment M2/GDP

High Growth(over 7X)7 Countries 28.0 28.6 26.3 43.01J

Medium Growth(3 - 7X)51 Countries 18.5 22.6 23.6 31.2

Slow Growth(< 3%)22 Countries 19.0 19.0 10.1 23.8

Tunisia 19.9v 28.5V 13.3W 43.0

1/ 1977-87L/ 1976-87S1 1983-88

Source: V_orld Development Report, 1989, page 27, The World Bank, 1989, and IFS.

- 19 -

Table 11TERM DEPOSIT RATES

Share of Total Interest After TaxMaturity (X, Nov. 1988) Rate Return

3-6 months 5.9 7 5.66-12 months 6.5 8 6.412-24 months 25.6 9 7.2Over 24 months 62.0 10 8.0

Source: BCT

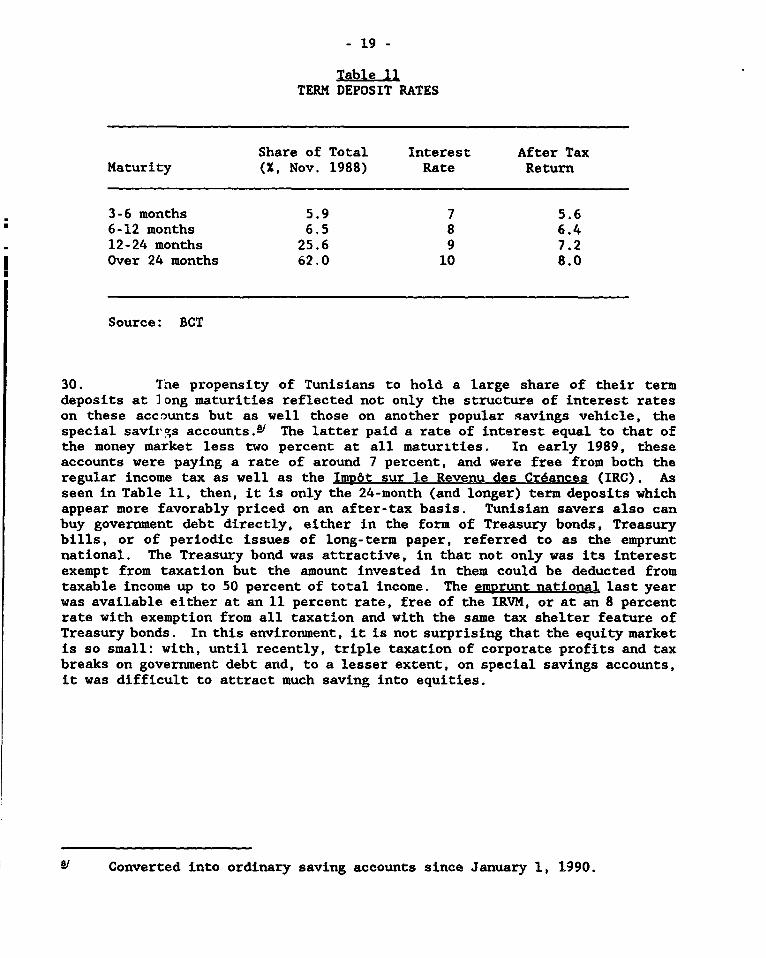

30. The propensity of Tunisians to hold a large share of their termdeposits at long maturities reflected not only the structure of interest rateson these accounts but as well those on another popular Ravings vehicle, thespecial savirgs accounts.f' The latter paid a rate of interest equal to that ofthe money market less two percent at all maturities. In early 1989, theseaccounts were paying a rate of around 7 percent, and were free from both theregular income tax as well as the Impot sur le Revenu des Creances (IRC). Asseen in Table 11, then, it is only the 24-month (and longer) term deposits whichappear more favorably priced on an after-tax basis. Tunisian savers also canbuy govertment debt directly, either in the form of Treasury bonds, Treasurybills, or of periodic issues of long-term paper, referred to as the empruntnational. The Treasury bond was attractive, in that not only was its interestexempt from taxation but the amount invested in them could be deducted fromtaxable income up to 50 percent of total income. The emprunt national last yearwas available either at an 11 percent rate, free of the IRVM, or at an 8 percentrate with exemption from all taxation and with the same tax shelter feature ofTreasury bonds. In this environment, it is not surprising that the equity marketis so small: with, until recently, triple taxation of corporate profits and taxbreaks on government debt and, to a lesser extent, on special savings accounts,it was difficult to attract much saving into equities.

1/ Converted into ordinary saving accounts since January 1, 1990.

- 20 -

IV. FINANCE AND INVESTMENT

Investment behavior and financial incentives

31. Rather than by raising the overall flow rate of saving, financialdeepening, by increasing the proportion of saving mobilized by the financialsystem, tends to raise the efficiency of investment. In order to allocatecapital efficiently, finance depends on relative prices and, especially, on realrates of return as guideposts. Compared with severely distorted financialmarkets, in which ex post real interest rates have been known to be as negativeas -50 percent or as high as 75 percent, in Tunisia real interest rates at leastseem to be broadly appropriate. Real deposit rates are in a range of -1 percentto 2 percent, depending on the term, while real borrowing rates for industrialinvestments were 3 percent to 4.5 percent, in early 1989, depending on the viewof underlying inflation,v though they rose to 6-10 percent by the end of theyear. Since both excessively negative and excessively positive real rates cancreate and/or reflect severe distortion in the credit allocation process, on thesurface Tunisia would seem to have little cause for concern.

32. Yet with inNastment performing below expectations, the financialsystem often is faulted. From the end of 1986 to August 1989 credit to theeconomy from the deposit banks has increased by only 6 percent of the 52 percentgrowth of total assets. Meanwhile, deposit bank holdings of cash plus depositsat the central bank increased 117 percent. Indeed, had the proportions of thebanks' balance sheets remained unchanged from late 1986, domestic credit wouldhave been about 15 percent higher than what was achieved. Of course, a changein asset allocation represents the banks' response to their environment. Hadthe economy been stronger or interest rates free to fluctuate, more credit mightbeen allocated to the domestic economy. Nonetheless, the criticism of thebanking system's support for investment in recent years is particularly strident,reflecting perceptions that the sector is both excessively profitable and riskaverse.

33. Several factors account for the perceived risk aversion of banks inTunisia. First, the end of the prior approval process has in a sense leftdeposit banks in a new, more uncertain world. They no longer have cause tobelieve that the Government will rescue them if their lending decisions proveunwise. Investment banks in general concentrated their lending on public sectorenterprises and thus tended to assume some Government support if their investmentmet with difficulty. Credit evaluation in all likelihood was underdeveloped,exacerbated by the absence of adequate financial incentives for bankingpersonnel.

34. Second, concomitantly with the reorientation of the financial system,Tunisia was exposed to several important changes in relative prices, such asthose associated with the devaluation in 1986, the decrease in the effective

Although the coaisumption deflator rose by 7.1% last year, some bankersassumed an underlying inflation rate of up to 10%.

- 21 -

rate of protection, and the sharp reduction in public sector investment. Giventhat some in the business sector still seem to be uncertain about theGovernment's intentions regarding industrial policy, a wariness on the part offinancial institutions is not surprising. Moreover, although following the 1986devaluation the export sector might have been expected as of late 1987 to beginprospering, as it subsequently has, the world economic outlook--and in particularthe growth outlook for Europe--was especially dismal at the end of 1987 as aresult of the crash of equity markets in industrialized countries. As ofDecember 1987 the OECD was forecasting a slowdown of real GDP growth in Europeto under 2 percent for 1988; the actual result was a sharp acceleration to3.8 percent. Since the European market accounts for 70 percent of Tunisia'sexports, it is likely that both firms and their financiers pulled back somewhatfrom investment for part of last year until the surprising vigor of Europeangrowth became evident.

35. Third, banks in general are characterized as having inadequateprovisions following the failure of a substantial number of Tunisian firms.Many observers assume that as financial institutions get into difficulties, th1eytend to engage in riskier lending decisions, often "betting the bank.' Thisbehavior, supported by many experiences, but most recently in the case of U.S.savings and loans institutions, is often taken for granted. In Tunisia it ispossible that a deteriorating balan^e sheet has produced the reverse effect,leading banks to become more cautious. For the more common response of engagingin riskier behavior applies to private financial institutions, while in Tunisiathe banks said to have the most fragile balance sheets are public banks.Managers of public banks may believe that their institutions will not be allowedto fail and that their positions are secure--providing that their lendingdecisions can be justified to government authorities. Private bank managers donot have to explain their lending decisions if they pay off, and if they do not,and the bank would have failed in any case, there is nothing to be lost bybetting the bank. Banks also have another option, when accounting standards arelax, of merely continuing to accrue interest and thereby appearing profit'Ale.Moreover, providing managers believe that their institution might be salvageable,they might be disposed to take fewer risks, particularly if provided with allattractive riskless asset.

36. Thus it is conceivable that the Tunisian banks have become morecautious. It has been argued by many that from the late 1870s onwards Britishbanks pulled back from long-term lending following a series of financialpanics.A These panics are thought to have made British bankers focus on theinadequacy of accounting standards and the lack of transparency for U.K.businesses. Hence they concentrated on safe, short-term, and largely self-liquidating loans and on investing in low-risk Government, railway, and publicutility securities. Indeed, the banks' ability to concentrate in suchinvestments was supported by their ample supply. In contrast, the large banksin the United States and Germany, despite at least as troublesome an experiencewith financial crises, became actively involved in raising long-term industrialfinance through underwriting and placing new issues of company securities. The

MM William P. Kennedy, Industrial structure, capital markets and the originsof British economic decline, 1987.

- 22 -

involvement of these large banks, with their substantial financial, monitoring,and informational resources, encourages outside investors.

37. Tunisian banks, which previously had the comfort of prior approvalof loans to public enterprises, are facing an uncertain market with fragilebalance sheets. In all likelihood, the main factors behind the decline ofinvestment were macroeconomic, but there may have been an element of the Britishdisease as well. If so, it is far too soon to tell if this will prove to belonglasting. Loan approvals jumped at the end of 1988 and in the first fewmonths of 1989, though the increase might just reflect a delay of loanapplications resulting from the widely expected cuts in taxes on borrowing.Although macroeconomic factors accounted for the slowdown of investment since1986, the encouragement of generally-accepted accounting standards, as discussedbelow, would help to encourage the banks to lend for longer-term projects andthereby avoid a retreat into short-term investments. To be sure, a greaterreliance on funding government debt at market rates and a reduction in itsavailability, especially at the long end, also would aid this process.

The capital market

38. In common with many other developing countries, the Tunisianfinancial market outside the banking sector is quite small. Longer-term capitalmarkets and especially equity markets require great amounts of reliableinformation--yet it is precisely this type of information that is in short supplyin developing economies. Even after adjusting for the small size of the Tunisianeconomy, the capitalization of the Tunisian equity market is low relative to thecountries classified as emerging markets by the IFC. In fact, the capitalizationto GNP ratio is about one-tenth the size of the smallest figure in thai group.Numerous factors account for the underdevelopment of the equity marke. and ofTunisian capital markets in general. First, the institutional investor marketis not helped by the existence of a generous but underfunded social s curitysystem. Moreover, insurance companies have been making serious losses over thepast few years inasmuch as premia are set by the Government at an artificiallylow level, relative to the generous disbursements set by the judicial system.Also, the savings instruments which the insurance industry can offer are limitedto 200 to 550 basis points below that on savings accounts with banks.

39. Second, in common with many developing countries, though surprisinggiven Tunisia's relatively high per capita income in that group, is the absenceof well-defined accounting standards and the lack of "transparency." Even moreso than with lending, the development of equity depends crucially on theavailability and reliability of information sufficient for the continuousmonitoring of the health of the underlying asset. But in Tunisia businessesdevelop their own sets of accounts- -often, many of them, for various purposes- -asthe need arises. Shareholders have little evidence that the published resultshave any bearing on the true state of the firm. Investment banks often takeequity positions along with their loans but with great reluctance. They arevirtually compelled to do so, since without taking an equity position they areat a disadvantage given the commercial banks' lower cost of funds. However, theyusually attempt to extricate themselves as soon as possible since, withoutownership cortrol, their investment is often poorly remunerated. Not

- 23 -

surprisingly, the few cases in which the investment banks have gained controlare regarded as being quite successful for the investment banks.

40. Third, there is a problem with collateral. It is scarce, especiallyin relation to Tunisia's level of development, in part related to the difficultyin getting clear title to real estate. More generally, court delays can stretchthe foreclosure process to 15 years, by which time the value of any underlyingcollateral may be largely depleted. Because the expected return on any pieceof collateral is so low, banks typically overcollateralize, which also has theeffect of binding clients to the'r bank.

41. Finally, until recently equity financing suffered severe taxdisadvantages relative to debt financing. Until 1984, dividends were tripletaxed, in that in addition to the double taxation of distributed dividends seenin the United States, the Imp6t sur le Revenu de la Valeur Mobiliere (IRVM) wascollected without credit. Following reforms in 1986-7, equity earnings weremerely double-taxed. The lower relative cost of debt financing was encouragedas well by the maintenance of negative real interest rates for a varietyinvestments until the mid-1980s. As noted above, special savings accounts andgovernment debt enjoyed tax advantages that made the growth of a viable equitymarket difficult. One of the great virtues of the law on direct taxation thattook effect on January 1, 1990, is that it eliminates these distortions.Corporate tax is paid on profits and, without double taxation through personalincome tax on distributed dividends.

42. By improving auditing and transparency and perhaps with the help offurther tax incentives, the Tunisian equity market could grow rapidly. Alreadya training project with IFC is well advanced, thereby eliminating one possiblebrake on development. Although equity market reforms are typically thought tohave a long gestation period, Korean experience suggests that a rapid return onthese reforms is possible. There the number of stocks listed rose from 24 atthe start of 1968 to 356 a decade later and capitalization soared commensurately.As is the case in Tunisia, firms initially relied on bank loans and foreignfinancing, while equity financing was small-scale and primarily family-based.There was not even a government securities market, as government debt wasallocated by quotas among financial institutions. However, in 1968 a series oflaws and reforms were launched to foster the development of capital markets,including the required auditing of listed corporations and a variety ofinducements to make listing financially attractive to issuers and stockholdingappealing to investors. These inducements included favorable prices for stockpurchase of publicly held corporations, especially by employees, little or notaxation of corporate dividends at the individual level (0 to 5 percent, comparedwith 20 percent for dividends from unlisted corporations), less favorable taxtreatment for real assets, and reduced corporate tax rates and more generousdepreciation rules for listed companies. The latter may have been necessary onlyto compensate for the excessive pressure on corporations to price initial issueswell below market. Financial support also was provided to underwriting groups.Rather than a blueprint for fostering equity market growth, the Korean casedemonstrates the possible pace of development once disincentives are removed.

43. With tax distortions substantially alleviated, the lack oftransparency and a limited supply of equities remain the most serious restraints

- 24 -

on market growth. As an alternative to granting fiscal incentives to foster thespread of standard accounting systems, the Government through the BCT may wantto encourage the banks to require standard and audited financial information fromtheir clients. For example, loans not supported by audited standard accountscould be lead to the downgrading of a bank's portfolio or higher requiredprovisions. Since audited statements would be required for loans, the currentdisincentive to being listed on the equity market would be eliminated.Privatization also would help: of the 50 enterprises listed last year, most wereowned entirely or in part by the public sect. c and hence were not traded. Endingthe extreme tax advantages available to individual holders of government debt--especially the ability to offset other income with interest earnings--as wellas more realistic pricing of such debt would provide a more receptive marketfor equities.

Forced investment: tax or subsidy?

44. The financing of the government deficit has the potential toalternate between being a tax on financial institutions and a subsidy. From 1987until January 1989, the interest rate on Treasury bonds was 6.5 percent, withthe value of this return vary'ng greatly with the holder. For banks this returnwas quite attractive, even though the money market rate averaged over 9 percentduring the period. Since 40 percent of the interest earned on Treasury bondsheld by banks was exempt from corporate taxation, while other assets throughoutthe period were subject to a tax rate of 44 percent, these bonds wereattractively priced. Thus with a reduced tax rate of 26.4 percent(44 percent * .60), the net after tax yield on these bonds was 4.784 percent andtheir implicit gross yield would have been 8.542 percent (4.784/(100 - 44)).SyHowever, other financial instruments were taxed twice--not just by a corporateincome tax but also be a type of withholding tax (the IRVM equal to 20 percentlast year) against which no tax credits were allowed, while the Treasury bondswere exempt from this additional tax. Thus the net return on Treasury bondsrepresented a higher implicit gross yield, namely,

4.784 percent/ (1 - .20 - (.8 * .44)) - 10.68 percent.

Moreover, in 1988, aware of the implicit gross yield on this "forced" investment,the authorities decided to issue a small amount (40 million dinars) of long termdebt (the Em runt national, a 5-year bond) priced at 11 percent. The slightlyhigher yield was justified to induce the public and the banks to buy governmentdebt freely. However, the issue was bought up immediately, and the Governmentissued another 80 million dinar, which also was promptly purchased.

45. During most of 1988, then, banks had the alternative of lending tothe industrial sector at a rate to them of 11.6 percent to 12.3 percent,depending on the money market rate, or holding risk free government bonds at orjust under 11 percent (even though borrowers paid a higher rate because of thetax wedge noted above). In view of the aforementioned uncertainties affecting

il This paragraph draws from Dimitri Vittas, "Reforme des Instruments duTresor," World Bank memo, March 1988.

- 25 -

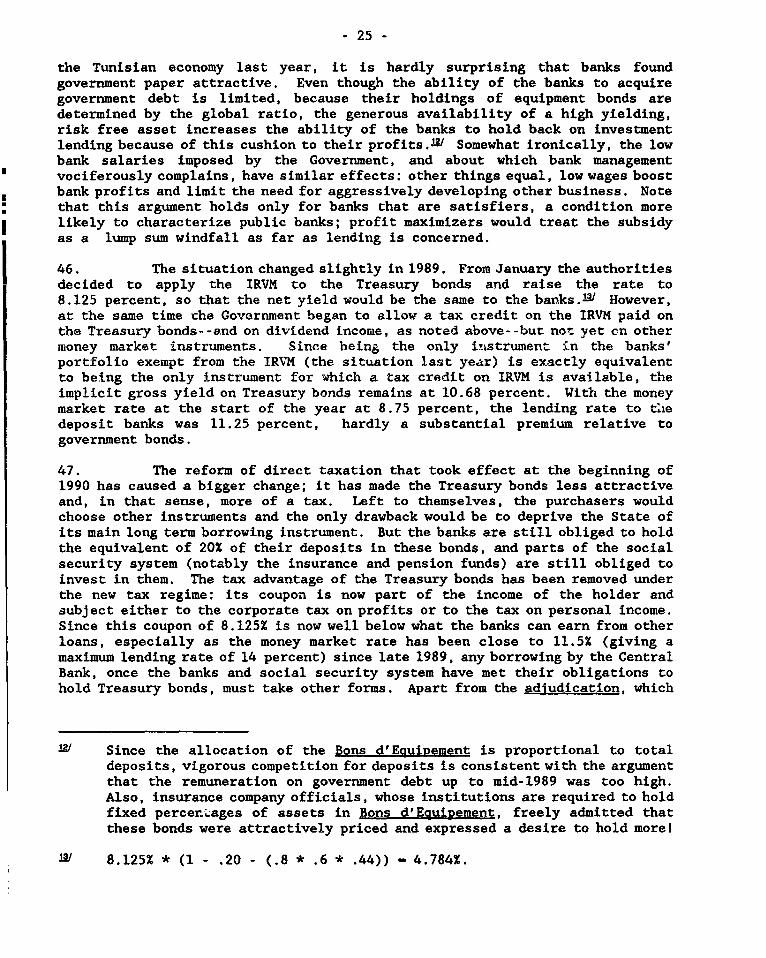

the Tunisian economy last year, it is hardly surprising that banks foundgovernment paper attractive. Even though the ability of the banks to acquiregovernment debt is limited, because their holdings of equipment bonds aredetermined by the global ratio, the generous availability of a high yielding,risk free asset increases the ability of the banks to hold back on investmentlending because of this cushion to their profits.IV Somewhat ironically, the lowbank salaries imposed by the Government, and about which bank managementvociferously complains, have similar effects: other things equal, low wages boostbank profits and limit the need for aggressively developing other business. Notethat this argument holds only for banks that are satisfiers, a condition morelikely to characterize public banks; profit maximizers would treat the subsidyas a lump sum windfall as far as lending is concerned.

46. The situation changed slightly in 1989. From January the authoritiesdecided to apply the IRVM to the Treasury bonds and raise the rate to8.125 percent, so that the net yield would be the same to the banks.AV However,at the same time che Government began to allow a tax credit on the IRVM paid onthe Treasury bonds--and on dividend income, as noted above--but not yet cn othermoney market instruments. Since being the only insstrument in the banks'portfolio exempt from the IRVM (the situation last year) is exactly equivalentto being the only instrument for which a tax credit on IRVM is available, theimplicit gross yield on Treasury bonds remains at 10.68 percent. With the moneymarket rate at the start of the year at 8.75 percent, the lending rate to tiledeposit banks was 11.25 percent, hardly a substantial premium relative togovernment bonds.

47. The reform of direct taxation that took effect at the beginning of1990 has caused a bigger change; it has made the Treasury bonds less attractiveand, in that sense, more of a tax. Left to themselves, the purchasers wouldchoose other instruments and the only drawback would be to deprive the State ofits main long term borrowing instrument. But the banks are still obliged to holdthe equivalent of 20% of their deposits in these bonds, and parts of the socialsecurity system (notably the insurance and pension funds) are still obliged toinvest in them. The tax advantage of the Treasury bonds has been removed underthe new tax regime: its coupon is now part of the income of the holder andsubject either to the corporate tax on profits or to the tax on personal income.Since this coupon of 8.125% is now well below what the banks can earn from otherloans, especially as the money market rate has been close to 11.5% (giving amaximum lending rate of 14 percent) since late 1989, any borrowing by the CentralBank, once the banks and social security system have met their obligations tohold Treasury bonds, must take other forms. Apart from the adjudication, which

12J Since the allocation of the Bons d'EguiRement is proportional to totaldeposits, vigorous competition for deposits is consistent with the argumentthat the remuneration on government debt up to mid-1989 was too high.Also, insurance company officials, whose institutions are required to holdfixed percer.ages of assets in Bons d'EquiRement, freely admitted thatthese bonds were attractively priced and expressed a desire to hold morel

L3/ 8.125% * (1 - .20 - (.8 * .6 * .44)) - 4.784%.

- 26 -

is a money market mechanism and, hence very short term, these forms haveconsisted of the emprunt ntional, which was a highly sought after, but costly,medium term instrumentlY, and the Treasury bills introduced in September 1989.The availability of these alternatives and the general lowering of direct taxesto some extent compensate the banks for the obligation to hold Treasury bonds.But the low coupon on these bonds is, nonetheless, distortionat- and limits thedevelopment of the secondary bond market. It is also a tax on the socialsecurity system, which can ill afford it. The authorities are deterred fromadjusting the coupon to the market by the immediate budgetary cost, though,ultimately, the deficits of the social security system are made up throughbudgetary transfers and the only budgetary gain from not raising the coupon, ifthere is one, is the implicit tax on the banks.

48. Besides its price, another notable feature of government finance isthat with most debt being long term, the Government helps to satisfy banks' andinvestors' demand for long-term assets. With cash surplus units normallydesiring some combination of short-, medium-, and long-term assets, the relianceof the Government on long-term instruments likely reduces t.he amount of tern Ufinancing available to the private sector, though cther factors, sucn as thelack of transparency, act to bias the demand for private sector financial assetsto the short end. Thus it is important that the Government issue debt at avariety of maturities. Government bonds can, in theory, be traded on the stockexchange, but in practice the low coupon rules it out. The development oftrading in medium and long term paper issued by the private sector is likely tobe easier if trading in government paper is already common. Treasury bills canbe bought and sold by the public through the banks.

Summary and Recommendations

49. The Tunisian financial system has made great progress in recent yearsin moving from a centralized system, with heavy reliance on the Government forsetting credit decisions, to a more market-oriented one with room for initiativeon the part of the banks. The central bank is no longer active in allocatingcredit, and there is some scope for the banks to set interest rates. Althoughpriority credits are still granted at subsidized rates, the number of categoriesmeriting such treatment has diminished markedly. Real deposit rates for termsavings are zero or mildly positive, depending on the maturity. The reform ofthe money market lessens the degree of segmentation between cash-rich and cash-poor banks and, by providing for the possibility of a commercial paper market,may increase competition in the financial market. The ending of the priorapproval process, a variety of macroeconomic shocks, and weak balance sheets ofmany borrowers appear to have conspired to make the banks risk averse.

50. Now is the time to build on these changes. Since the Tunisianauthorities are concerned about a lack of competition in the banking sector, andsince both quantitative measures and anecdotal evidence are consistent with only

B4 Banks have been obliged by the authorities to pass all the emnrunt nationalon to the public.

- 27 -

limited competition, reforms to increase the degree of competition are especiallydesirable. Although the banks likely would resist, it would be preferable thatthe BCT require the banks to move to a posted prime system, in which the bankswould be required to advertise interest rates (and fees) charged to their bestcustomers. Borrowers thereby would be more inclined to shop around to searchout the bank that would accord them the best treatment--exactly the type ofresponse needed to enforce competition.

51. With required advertising of rates helping to intensify competition,the gradual lifting of the cap on interest spreads could be undertaken with lessfesar of a jump in interest rates. Moreover, it would be better to have the capbe a limit on the average interest rate on a bank's loans, so that banks couldfund somewhat riskier but likely more profitable investments. Lifting the limitand making it an average, rather than an absolute cap, would give the banks aneffectively wider margin in which to compete. In early 1989, the weakness ofdereand reportedlv had led some banks to offer loans to their best customersreportedly at only 50 basis points above the. money market rate. Thus initiallythis proposal uwty not entail any general increase in rates, but would increasethe banks' flexibility to fund a wide variety of projects, including riskier butpotentially rewarding ventures that are presently rationed from the market.

52. Subsidized interest rates for priority sectors do not belong in amarket-oriented system: in many countries they have tended to distort theallocation of credit and encourage the waste of resources. Experience indicatesthat credit availability is far more important than its price in encouraginginvestment. Moreover, in Tunisia market segmentation between deposit andinvestment banks was enhanced by the fact that the latter were not accorded thesame rediscount privileges and therefore could not compete for business in thismarket. Even though the formal restriction on investment banks providingpreferential credit has been removed, the margins they are allowed are too narrowfor the effect to be significant (see paragraph 12). Any reduction ofrediscounting should be accompanied by a move to market interest rates onpriority credits.

53. With more room to compete, and especially to pursue riskier credits,bank staff need to be better trained and subject to an incentive system thatboth amply rewards success and penalizes failure. The current practice ofregulating bank salaries at low levels, with minimal salary gradation, coupledwith the difficulty, in common with nonfinancial firms, in dismissing employees,hardly contributes to an optimal selection of credits. Although such anincentive system was acceptable when credits were authorized by the BCT, it isat odds with the current market-oriented system and, a fortiori, incompatiblewith Tunisia's aspirations of becoming a regional financial center. Bankersshould be encouraged to recognize promptly doubtful and bad loans by allowingfull and immediate tax deductions of provisions.

54. The development of a more dynamic financial system in recent yearsmight have been hindered by the portfolio requirement on banks' holding ofgovernment paper. In the past this system has alternated between being a taxand, in effect, a subsidy. As noted above, the offering of a high-yielding risk-free asset can help banks more comfortably refrain from lending, especially when

- 28 -

the yield is insignificantly below the maximum at which banks can lend. Moreover,the oversubscription of the emgrunt national suggests thlat the Government hasbeen paying too much for its borrowings. Hence the Government should move toan auction system for marketing its debt. As has been the case in Japan, whichalso previously had only 10-year government bonds, the availability of shorter-term public debt instruments, such as Treasury bills, likely will help to deepenrapidly secondary markets and to stimulate further innovation. Greater relianceon short-term instruments to finance Government also should leave more room atthe long end of the market for private sector borrowing.

55. Competition in developing countries often can be stimulated byallowing foreign entry. One major foreign bank which had operated offshoreopened an onshore branch in November 1989, and the authorities are thought tobe considering further moves in this direction. With abnormally low bankprovisions, Tunisian banks can ill-afford to have profits reduced by an onslaughtof foreign competition. Also, given the likelihood that reforms already in placewill raise the average cost of funds to the banks, and the possibility that thebanks currently are beginning to compete, further foreign e,itry might best beallowed gradually as more evidence on the imieact of current reforms becomesclear. As rLoted above, a system of postitng intierest rates and commissions forprime customers also would foster competition, as would a move to a more flexibleinterest cap (from an overall to an average basis) and finally, the eventualelimination of such restrictions.

56. Tunisian finance has been hobbled by the absence of a viable equitymarket. Most proposals for encouraging the growth of an equity market, such asthe promulgation of accounting standards and the development of an auditingsystem, do not bear fruit within a short period of time. But efforts in thisdirection should begin at once. Since one factor constraining equities is thatmany of the companies presently listed--generally the largest and best-knowninstitutions in the country- -are in part government-owned and thus little traded,a privatization program would help develop the market. The authorities couldconsider beginning the program with the banks.

57. These recommendations would allow Tunisia to face the 1990s with amore developed and dynamic financial system. Competition in all likelihood wouldbe more advanced, and term lending more widespread. Banks balance sheets wouldbe in a healthier position and mor rational criteria would be imposed on creditallocation. The level of investment relative to GDP might not be substantiallyhigher than it is today, but the efficiency of capital would be expected to benoticeably higher, allowing Tunisian society to grow and prosper withoutabstaining from consumption. Finally, it would be reasonable to expect thatlonger-term investment would be more easily financed, with interest rates freeto price risky investments. The Government removed from its dominance of long-term finance, and an equity market well on the road to development.

C: \IJT\TUN\CEM\TUANA. 2