report to cabinet - room 151 to cabinet subject: prudential ... (mrp) policy (how residual capital...

TRANSCRIPT

Report to Cabinet

Subject: Prudential and Treasury Indicators and Treasury Management Strategy Statement (TMSS) 2017/18

Date: 16 February 2017

Author: Deputy Chief Executive and Chief Financial Officer

Wards Affected

All

Purpose

To present for Members’ approval the Council’s Prudential Code Indicators and Treasury Strategy for 2017/18, for referral to Full Council.

Key Decision

This is not a key decision.

Background

1.1 Definition of treasury management

Treasury management is defined as “the management of the local authority’s investments and cash flows, its banking, money-market and capital-market transactions; the effective control of the risks associated with those activities, and the pursuit of optimum performance consistent with those risks.”

The Council is required to operate a “balanced budget”, which broadly means that cash raised during the year will meet cash expenditure. The Localism Act 2011 places a duty on a local authority to calculate its “council tax requirement” for each financial year, and this includes the revenue costs which result from the capital investment decisions of the authority.

Part of the treasury management service is to ensure that cashflow is adequately planned, with cash available when it is needed. Surplus cash is invested with counterparties commensurate with the Council’s low risk appetite, providing adequate liquidity before considering investment return.A further treasury management function is the funding of the Council’s

capital plans. These plans provide a guide to the Council’s borrowing needs, and require longer term cashflow planning to ensure the Council can meet its spending obligations. The management of longer term cash may involve arranging long or short-term loans or the use of longer term cashflow surpluses. On occasion, debt previously drawn may be restructured to meet the Council’s risk or cost objectives.

1.2 Statutory reporting requirements

The Council is required to receive and approve, as a minimum, three main reports each year, which incorporate a variety of polices, estimates and actuals.

1.2.1 Prudential and Treasury Indicators and Treasury Management Strategy Statement (TMSS) -this report

This first, and most important report covers:

The capital plans (including prudential indicators), A minimum revenue provision (MRP) policy (how residual capital

expenditure is charged to revenue over time), The treasury management strategy (how the investments and

borrowings are to be organised) including treasury indicators, An investment strategy (the parameters on how investments are to be

managed).

1.2.2 Mid-year Treasury Management Report

This updates Members on the progress of the capital position, amending prudential indicators as necessary, and whether the treasury strategy is appropriate or whether any policies require revision.The Council has adopted a policy of presenting quarterly treasury management reports to Cabinet, and this exceeds the minimum requirement.

1.2.3 Annual Treasury Report

This provides details of a selection of actual prudential and treasury indicators and actual treasury operations compared to the estimates within the strategy.

1.2.4 Scrutiny

All treasury management reports are required to be adequately scrutinised before being recommended to Council. This role is undertaken by Cabinet. The TMSS is part of the Council’s Budget and Policy Framework and accordingly the Chair of the Overview and Scrutiny Committee has also been consulted. Any comments received will be taken into account before referral to Council.

1.3 Treasury management strategy for 2017/18

The strategy for 2017/18 covers two main areas:

Capital issues: the capital plans and the prudential indicators the minimum revenue provision (MRP) policy

Treasury management Issues: the current treasury position treasury indicators which limit the treasury risk and activities of the

Council prospects for interest rates the borrowing strategy policy on borrowing in advance of need debt rescheduling the investment strategy creditworthiness policy policy on use of external service providers

These elements cover the requirements of the Local Government Act 2003, the CIPFA Prudential Code, Communities and Local Government (CLG) MRP Guidance, the CIPFA Treasury Management Code and CLG Investment Guidance.

1.4 Training

The CIPFA Code requires the responsible officer to ensure that Members with responsibility for treasury management receive adequate training in treasury management. This especially applies to Members responsible for Treasury Management, ie. Cabinet, and the Chief Financial Officer will arrange training for Members as required. The Council’s treasury management advisers, Capita Asset Services (CAS), provided a more detailed training session for Members in February 2016.

The training needs of officers involved with treasury management are reviewed periodically.

1.5 Treasury management consultants

The Council uses CAS as its treasury management advisors, recognising that there is value in employing external providers in order to acquire access to specialist skills and resources. The Council will ensure that the terms of appointment and the methods by which value will be assessed are properly agreed and documented, and subjected to regular review. The Council recognises that responsibility for treasury management decisions remains with the organisation at all times, and will ensure that undue reliance is not placed upon the external service providers.

Proposal

2.1 Capital Affordability and Prudential Indicators 2017/18 to 2019/20

The Council’s capital expenditure plans are the key driver of treasury management activity. The output of the capital expenditure plans is reflected in prudential indicators, which are designed to assist Members to overview and confirm such capital expenditure plans. The indicators for 2017/18 to 2019/20 are attached at Appendix 1.

2.1.1 Capital expenditure

The indicator includes a summary of the proposed capital expenditure plans for 2017/18 to 2019/20.

Portfolio Capital Expenditure:

2017/18 Estimate

£

2018/19 Estimate

£

2019/20 Estimate

£

Housing, Health & Wellbeing 1,156,000 120,000 0Public Protection 1,070,000 820,000 820,000Environment 2,016,900 998,000 528,000Growth & Regeneration 575,000 875,000 0Resources & Reputation 150,000 150,000 150,000Equipment Replacement 0 100,000 100,000Development Bids 0 100,000 100,000

Total Expenditure 4,967,900 3,163,000 1,698,000

The table below summarises the above capital expenditure plans and how these are being financed by capital or revenue resources. Any shortfall of resources results in a borrowing need.

Resources: 2017/18 Estimate

£

2018/19 Estimate

£

2019/20 Estimate

£

Capital Exp £m (above) 4,967,900 3,163,000 1,698,000Financed by:Capital receipts 1,209,000 810,000 710,000Capital grants & contributions 1,170,000 940,000 820,000Direct Revenue Financing 441,400 0 0

Net borrowing need 2,147,500 1,413,000 168,000

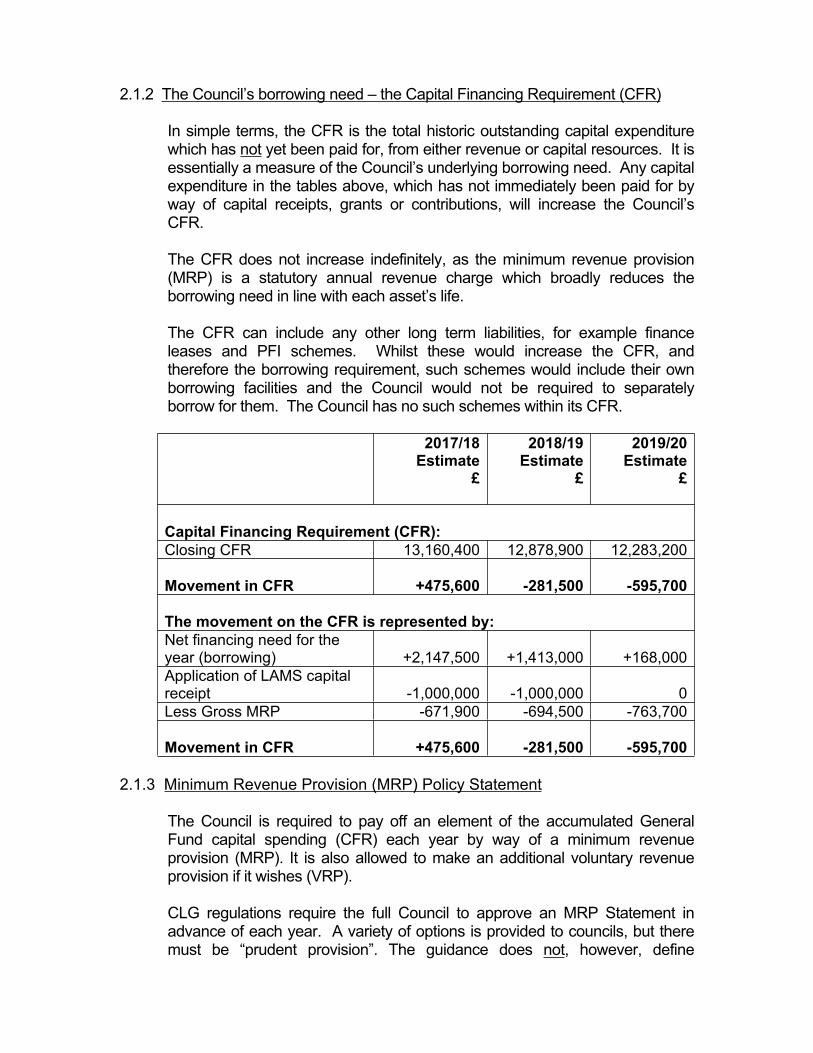

2.1.2 The Council’s borrowing need – the Capital Financing Requirement (CFR)

In simple terms, the CFR is the total historic outstanding capital expenditure which has not yet been paid for, from either revenue or capital resources. It is essentially a measure of the Council’s underlying borrowing need. Any capital expenditure in the tables above, which has not immediately been paid for by way of capital receipts, grants or contributions, will increase the Council’s CFR.

The CFR does not increase indefinitely, as the minimum revenue provision (MRP) is a statutory annual revenue charge which broadly reduces the borrowing need in line with each asset’s life.

The CFR can include any other long term liabilities, for example finance leases and PFI schemes. Whilst these would increase the CFR, and therefore the borrowing requirement, such schemes would include their own borrowing facilities and the Council would not be required to separately borrow for them. The Council has no such schemes within its CFR.

2017/18 Estimate

£

2018/19 Estimate

£

2019/20 Estimate

£

Capital Financing Requirement (CFR):Closing CFR 13,160,400 12,878,900 12,283,200

Movement in CFR +475,600 -281,500 -595,700

The movement on the CFR is represented by:Net financing need for the year (borrowing) +2,147,500 +1,413,000 +168,000Application of LAMS capital receipt -1,000,000 -1,000,000 0Less Gross MRP -671,900 -694,500 -763,700

Movement in CFR +475,600 -281,500 -595,700

2.1.3 Minimum Revenue Provision (MRP) Policy Statement

The Council is required to pay off an element of the accumulated General Fund capital spending (CFR) each year by way of a minimum revenue provision (MRP). It is also allowed to make an additional voluntary revenue provision if it wishes (VRP).

CLG regulations require the full Council to approve an MRP Statement in advance of each year. A variety of options is provided to councils, but there must be “prudent provision”. The guidance does not, however, define

“prudent”, instead making recommendations on the interpretation of the term. It is the responsibility of each authority to decide upon the most appropriate method of making a prudent MRP, having had regard to the guidance and its own circumstances, the broad aim being to ensure that borrowing is repaid over a period that reflects the useful lives of the assets acquired. The Council is obliged to have regard to the CLG guidance, but it is not prescriptive. The Council is recommended to approve the following MRP Statement for 2017/18.

a. The Council will assess MRP in accordance with the recommendations within the guidance issued under section 21(1A) of the Local Government Act 2003.

b. The CFR method, will be used for calculating MRP in respect of all capital expenditure incurred up to and including 31 March 2008. This is the simplest approach available, being calculated as a straightforward 4% of the relevant element of the CFR at the end of the previous year. In the current economic climate the Chief Financial Officer considers that use of the CFR Method is prudent.

c. The Asset Life Method, will be used for calculating MRP in respect of all capital expenditure incurred on and after 1 April 2008. An equal instalment approach will be adopted.

d. The Chief Financial Officer will determine estimated asset lives. Where expenditure of different types is involved, it will be grouped together in a manner which best reflects the nature of the main component of expenditure. It will only be divided up in cases where there are two or more major components, with significantly different asset lives.

e. The Council currently operates two cash-backed Local Authority Mortgage Schemes (LAMS), each based on a five-year advance to Lloyds TSB to match the five-year life of the indemnity. Lloyds TSB terminated all active LAMS schemes on 31 July 2016 and no further applications under Gedling’s remaining scheme have been accepted since that date, however the Council’s two advances with Lloyds remain in place pending their respective maturity dates. Each advance provides an integral part of the mortgage lending under the LAMS scheme, and is treated as capital expenditure and a loan to a third party, therefore the Capital Financing Requirement (CFR) increases by the amount of the advance. When each advance is returned at maturity, on 12 April 2017 and 11 June 2018 respectively, the funds will be classed as capital receipts, and the CFR will reduce accordingly. As the advances are temporary (5-year) arrangements, there is no need to set aside prudent provision to repay the debt liability in the interim period, and there is accordingly no MRP application.

f. In view of the economic climate and significant budgetary pressures, the Council will not provide for an additional voluntary contribution to MRP in 2017/18.

g. Based on the above policy, the net MRP charge for 2017/18 has been calculated as £671,900 as detailed below, and this sum has been included in the Council’s 2017/18 budget proposals. The exact amount of MRP will be subject to change should capital financing decisions alter during the year.

£CFR Method £239,900Asset Life Method £432,000

Gross MRP £671,900

2.1.4 Capital Affordability Prudential Indicators

The previous sections cover the overall “capital” and “control of borrowing” prudential indicators, but within this framework additional prudential indicators are required to further assess the affordability of the capital investment plans. These provide an indication of the impact of the capital investment plans on the Council’s overall finances. The 2017/18 Capital Programme report, an item elsewhere on this agenda, provides full details of the proposed programme. The indicators, which can be found at Appendix 1, represent capital investment plans that have been fully factored into the Council’s Medium Term Financial Plan, and are assessed as affordable, prudent and sustainable, subject to securing the commitment to delivering an efficiency programme in the medium term, as proposed in the Gedling Plan report elsewhere on this agenda. The indicators include:

a. Capital expenditure (see 2.1.1)

b. Capital Financing Requirement (CFR) (see 2.1.2)

c. Ratio of financing costs to net revenue stream

This indicator identifies the trend in the cost of capital (borrowing and other long term obligation costs net of investment income) against the net revenue stream. Estimates of financing costs include current commitments and the proposals included in the Gedling Plan report.

d. Incremental Impact of capital investment decisions on Council Tax

This indicator identifies the revenue costs associated with proposed changes to the three year capital programme recommended in the Gedling Plan report, compared to the Council’s existing approved

commitments and current plans.

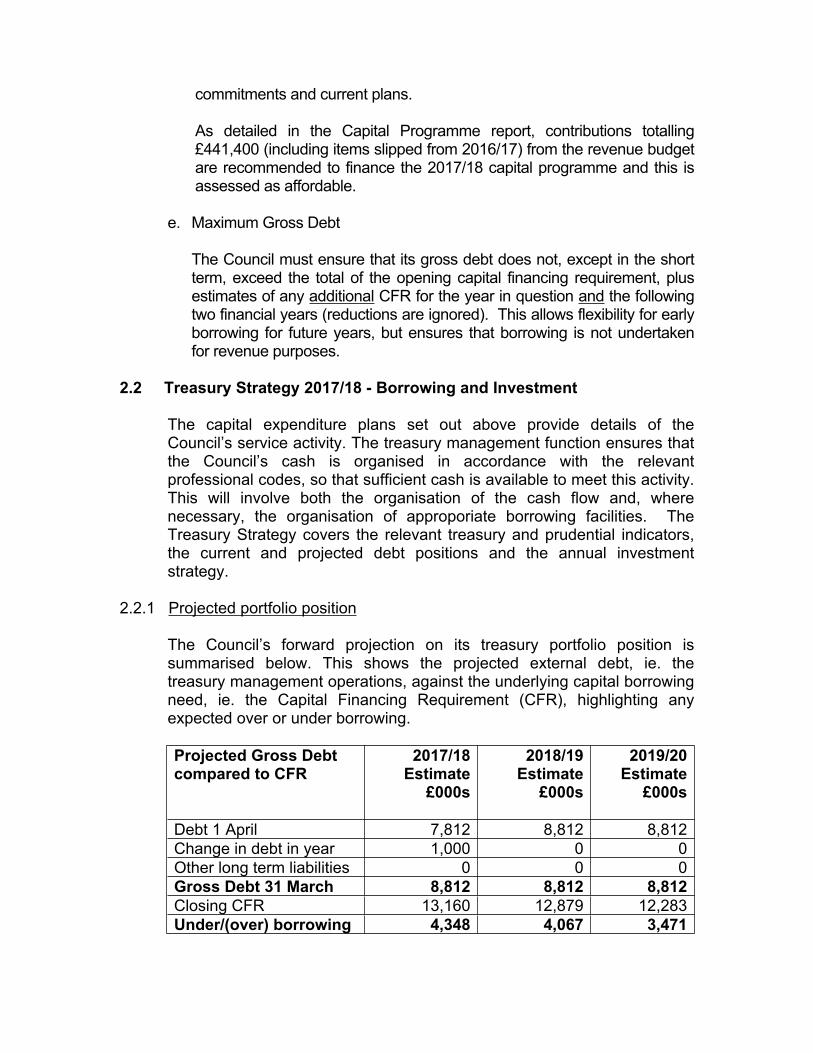

As detailed in the Capital Programme report, contributions totalling £441,400 (including items slipped from 2016/17) from the revenue budget are recommended to finance the 2017/18 capital programme and this is assessed as affordable.

e. Maximum Gross Debt

The Council must ensure that its gross debt does not, except in the short term, exceed the total of the opening capital financing requirement, plus estimates of any additional CFR for the year in question and the following two financial years (reductions are ignored). This allows flexibility for early borrowing for future years, but ensures that borrowing is not undertaken for revenue purposes.

2.2 Treasury Strategy 2017/18 - Borrowing and Investment

The capital expenditure plans set out above provide details of the Council’s service activity. The treasury management function ensures that the Council’s cash is organised in accordance with the relevant professional codes, so that sufficient cash is available to meet this activity. This will involve both the organisation of the cash flow and, where necessary, the organisation of approporiate borrowing facilities. The Treasury Strategy covers the relevant treasury and prudential indicators, the current and projected debt positions and the annual investment strategy.

2.2.1 Projected portfolio position

The Council’s forward projection on its treasury portfolio position is summarised below. This shows the projected external debt, ie. the treasury management operations, against the underlying capital borrowing need, ie. the Capital Financing Requirement (CFR), highlighting any expected over or under borrowing.

Projected Gross Debt compared to CFR

2017/18Estimate

£000s

2018/19Estimate

£000s

2019/20Estimate

£000s

Debt 1 April 7,812 8,812 8,812Change in debt in year 1,000 0 0Other long term liabilities 0 0 0Gross Debt 31 March 8,812 8,812 8,812Closing CFR 13,160 12,879 12,283Under/(over) borrowing 4,348 4,067 3,471

Within the prudential indicators there are a number of key indicators to ensure that the Council operates its activities within well-defined limits. As detailed at 2.1.4 (e) above, to comply with the “gross debt” indicator, the Council must ensure that its gross debt does not, except in the short term, exceed the total of the CFR in the preceding year plus the estimates of any additional CFR for 2017/18 and the following two financial years. This allows some flexibility for limited early borrowing for future years, but ensures that borrowing is not undertaken for revenue purposes.

The Chief Financial Officer can report that the Council has complied with this prudential indicator during the current year, 2016/17, and does not envisage difficulties for the future. This view takes into account current commitments, existing plans, and the proposals in this budget report. Maximum Gross Debt 2017/18

Estimate£000s

2018/19 Estimate

£000s

2019/20 Estimate

£000s

Opening CFR (closing CFR preceding year) 12,685 13,160 12,879Additions (only) in-year + following 2 years 475 0 74

Maximum Gross Debt 13,160 13,160 12,953Estimated GBC debt at 31 March 8,812 8,812 8,812Under/(over) borrowing 4,348 4,348 4,141

2.2.2 Treasury indicators – affordability limits to borrowing (Appendix 1)

a. The Operational Boundary for external debt

This is the limit which external debt is not “normally” expected to exceed. In most cases, this would be a similar figure to the CFR, but it may be lower or higher depending on the levels of actual debt.

b. The Authorised Limit for external debt

This limit represents a control on the “maximum” level of borrowing. It is the statutory limit determined under s3 (1) of the Local Government Act 2003 and represents the limit beyond which external debt is prohibited. The Authorised Limit must be set, and revised if necessary, by Full Council. It reflects a level of external debt which, while not desirable, could be afforded in the short term, but is not sustainable in the longer term. The Government retains an option to control either the total of all Councils’ plans, or those of a specific Council, although this power has not yet been exercised.

2.2.3 Prospects for Interest Rates

The Council has appointed Capita Asset Services (CAS) as its treasury advisor and part of their service is to assist the Council to formulate a view on interest rates. The following table gives the CAS central view as at 20 December 2016 and further information on interest rates can be found at Appendix 2.

The Monetary Policy Committee (MPC) cut Bank Rate from 0.5% to 0.25% in August 2016 to counteract what it forecast was going to be a sharp slowdown in growth in the second half of 2016. It also indicated that a further cut was likely, however economic data since August has been more positive and inflation forecasts have risen substantially as a result of the continuation of the sharp fall in the value of sterling since early August. Consequently, on current trends it is unlikely that there will be another cut – although this cannot be ruled out if there was another significant dip in economic growth.

During the two-year period in which the UK is negotiating the terms for its withdrawal from the EU, it is unlikely that the MPC will do anything to dampen growth prospects, ie. by raising Bank Rate, which will already be adversely impacted by the uncertainties around what form Brexit will eventually take. Accordingly, a first increase to 0.5% is not now expected until Q2 of 2019, after the Brexit negotiations have been concluded (although the period could be extended). However, if strong domestically generated inflation (eg. from wage increases) was to emerge, the pace and timing of increases in Bank Rate could be brought forward.

Economic and interest rate forecasting remains difficult due to the many external influences. The forecasts above, and MPC decisions, will be liable to further amendment depending on economic data and developments in the financial markets over the next year. Geopolitical development, especially in the EU, could also have a major impact.

The overall long-run trend is for gilt yields and PWLB rates to rise, albeit gently. Rates have experienced exceptional levels of volatility and these

have been highly correlated to geopolitical factors, the sovereign debt crisis, and to emerging market developments. It is likely that this volatility will continue for the foreseeable future.

The overall balance of risk to economic recovery in the UK is to the downside, particularly in view of the current uncertainty over the final terms of Brexit, and the timetable for its implementation.

Downside risks to current forecasts for UK gilt yields and PWLB Rates include:

Monetary policy action by the central banks of major economies reaching the limit of its effectiveness, and failing to stimulate significant sustainable growth, combat the threat of inflation, and reduce high levels of debt.

A lack of adequate action by national governments to promote growth through structural reforms, fiscal policy and investment.

Major national polls, for forthcoming elections in the Netherlands, France and Germany. Furthermore, Spain has a minority government, a situation that is potentially unstable.

A potential resurgence of the Eurozone sovereign debt crisis. Weak capitalisation of some European banks. Geopolitical risks in Europe, the Middle East and Asia. UK economic growth and increases in inflation being weaker than

anticipated. Weak growth or recession in the UK’s major trading partners, ie. the

EU and US.

Upside risks include:

UK inflation rising to significantly higher levels than in the wider EU and in the US.

A rise in the US Federal Reserve (Fed) rate, and rising US inflation expectation, which may drag UK yields upwards.

The pace and timing of US Fed rates. A downward revision to the UK’s sovereign credit rating

Borrowing rates were on a generally downward trend during 2016 and fell to historically low levels after the referendum in June and the August MPC meeting when a new package of quantitative easing (QE) was announced. Gilt yields have since risen sharply due to concerns around Brexit, the fall in the value of sterling, and an increase in inflation expectations. In general terms, a policy of avoiding new borrowing by running down cash balances has served well over the last few years, however this should now be reviewed to reduce the risk of incurring higher borrowing costs in future years, when borrowing becomes unavoidable either for financing capital expenditure, or for the refinancing of maturing debt. Investment returns are likely to remain low during 2017/18 and

beyond. Accordingly there will remain a cost of carry to any new long-term borrowing that causes a temporary increase in cash balances.

2.2.4 Borrowing Strategy

a. The Strategy

The Council is currently maintaining an under-borrowed position (see 2.2.1 above). This means that the capital borrowing need (the Capital Financing Requirement), has not been fully funded with loan debt, as cash supporting the Council’s reserves, balances and cash flow has been used as a temporary measure. This represents “internal borrowing”. This strategy is prudent since investment returns remain low, and counterparty risk is still an issue that needs to be considered.

However, against this background and the risks within the economic forecast outlined above, and the potential cost of carry (see 2.2.5 below), caution will be adopted with the 2017/18 treasury operations. The Chief Financial Officer will monitor interest rates in financial markets and adopt a pragmatic approach to changing circumstances:

If it was felt that there was a significant risk of a sharp FALL in long and short term rates (e.g. due to a marked increase of risks around a relapse into recession, or of risks of deflation), then long term borrowings will be postponed, and potential rescheduling from fixed rate funding into short term borrowing will be considered.

If it was felt that there was a significant risk of a much sharper RISE in long and short term rates than that currently forecast, perhaps arising from an acceleration in the start-date and in the rate of increase in central rates in the US and UK, an increase in world economic activity or a sudden increase in inflation risks, then the portfolio position will be re-appraised with the likely action that fixed rate funding will be drawn whilst interest rates are still lower than they will be in the next few years.

Any new borrowing will be discussed with CAS, and any decisions will be reported to Cabinet at the next available opportunity.

b. Treasury Indicators - prudent limits on borrowing activity (Appendix 1)

There are three debt related treasury activity limits (see Treasury Indicators (c) to (e) at Appendix 1), the purpose of which is to restrain the activity of the treasury function within agreed limits, thereby managing risk and reducing the impact of adverse movement in interest rates. However, if limits are set to be too restrictive they will impair opportunities to reduce costs or improve performance:

An upper limit on fixed interest rate exposure. This identifies a maximum

limit for fixed interest rates based upon the debt position net of investments.

An upper limit on variable interest rate exposure. This identifies a maximum limit for variable interest rates based upon the debt position net of investments.

Members are asked to note that additional local indicators are also given for debt and investment individually, expressed as a percentage of the relevant totals.

The maturity structure of borrowing. These gross limits are set to reduce the Council’s exposure to large fixed rate sums falling due for refinancing, and are required for upper and lower limits.

2.2.5 Policy on borrowing in advance of need

The Council will not borrow more than, or in advance of, its needs purely to profit from the investment of the extra sums borrowed, since this is illegal. Any decision to borrow in advance of need will be within the forward-approved CFR estimates, and will be considered carefully to ensure value for money can be demonstrated, and that the Council can ensure the security of such funds.

In determining whether borrowing will be undertaken in advance of need, the Council will ensure that there is a clear link between the capital programme and the maturity profile of the existing debt portfolio which supports the need to take funding in advance of need. It will ensure that the on-going revenue liabilities created, and the implications for future plans and budgets have been considered, and evaluate the economic and market factors that might influence the manner and timing of any decision to borrow. The advantages and disadvantages of alternative forms of funding will be considered, together with the most appropriate periods over which to fund.

Risks associated with any borrowing in advance activity will be subject to prior appraisal and subsequent reporting through the mid-year or annual reporting mechanism.

2.2.6 Debt rescheduling

As short term borrowing rates are expected to be considerably cheaper than longer term fixed interest rates, there may be potential opportunities to generate savings by switching from long term debt to short term debt. However, these savings will need to be considered in the light of the current treasury position and the size of the cost of debt repayment (premiums incurred).

The reasons for any rescheduling to take place will include:

the generation of cash savings and / or discounted cash flow savings helping to fulfil the Treasury Strategy enhance the balance of the portfolio (amend the maturity profile and/or

the balance of volatility)

Consideration will also be given to identifying any residual potential for making savings by running down investment balances to repay debt prematurely as short term rates on investments are likely to be lower than rates paid on current debt.

All rescheduling will be reported to Cabinet at the earliest meeting following action.

2.2.7 Municipal Bond Agency

The Municipal Bond Agency offers loans to local authorities for infrastructure and housing, at borrowing rates potentially lower than those offered by the Public Works Loan Board (PWLB). The Council may make use of this source of borrowing if appropriate, but only with advice from CAS.

2.2.8 Annual Investment Strategy 2017/18

The intention of the Annual Investment Strategy is to provide security of investment and the minimisation of risk. The aim is to generate a list of highly creditworthy counterparties which will also enable diversification and thus the avoidance of concentration risk.

a. Investment Policy

The Council’s investment policy has regard to the CLG’s guidance on Local Government Investments (“the guidance”), and the revised CIPFA Treasury Management in Public Services Code of Practice and Cross Sectoral Guidance Notes (“the CIPFA TM Code”). In accordance with this guidance, and in order to minimise the risk to investment, the Council applies minimum acceptable criteria in order to generate a list of highly creditworthy counterparties. This also enables diversification and thus the avoidance of concentration risk. The Council has clearly stipulated below at 2.2.8 (c) the minimum acceptable credit quality of counterparties for inclusion on its lending list. The Council utilises the CAS creditworthiness methodology, whereby banks’ ratings are monitored on a real time basis with knowledge of any changes notified electronically as the agencies notify modifications.

All investments will be made in sterling, and since the risk appetite of the Council with regard to its investments is very low, its general policy objective is the prudent investment of treasury balances. The Council’s investment priorities are (in order of priority):

The security of capital The liquidity of its investments The rate of return

The borrowing of monies purely to invest or on-lend and make a return remains unlawful, and the Council will not engage in such activity.

Investment instruments identified for use in the financial year are listed at Appendix 3 under “Specified” and “Non-Specified” categories.

Specified Investments:

An investment is a specified investment if all of the following apply:

The investment is denominated in sterling and the payment or repayment is only payable in sterling.

The investment is not “long-term”, ie. it is made for less than one year, a maximum term of 364 days.

The making of the investment is not defined as capital expenditure. The investment is made with a body of high credit quality, or with the

UK government, a local authority or a parish council.

Only minimal reference need be given to specified investments in the Annual Investment Strategy, and they will generally be used for cash-flow management.

Non Specified Investments:

Non-specified investments are all those not meeting the criteria for specified investments above. Accordingly, they may be simple investments made with the same counterparties as specified investments, being “non-specified” only by way of the maturity period being over 364 days (ie. one year or more). Alternatively they may be more complex instruments, or those offering slightly higher risk or lower liquidity. If used at all, non-specified investments will tend only to be used for the longer-term investment of core-balances.

Appendix 3 also sets out:

The advantages and associated risk of investments under the non-specified category.

The upper limit to be invested in each non-specified category. Those instruments best used after consultation with the Council’s

treasury advisers.

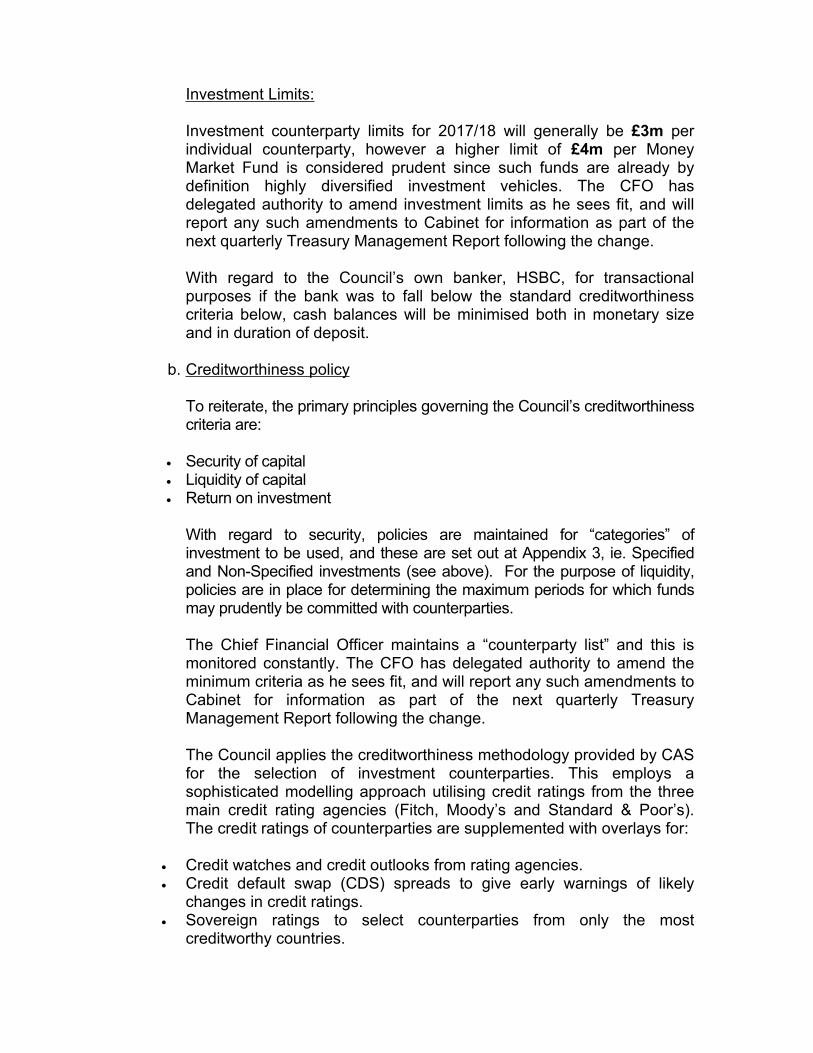

Investment Limits:

Investment counterparty limits for 2017/18 will generally be £3m per individual counterparty, however a higher limit of £4m per Money Market Fund is considered prudent since such funds are already by definition highly diversified investment vehicles. The CFO has delegated authority to amend investment limits as he sees fit, and will report any such amendments to Cabinet for information as part of the next quarterly Treasury Management Report following the change.

With regard to the Council’s own banker, HSBC, for transactional purposes if the bank was to fall below the standard creditworthiness criteria below, cash balances will be minimised both in monetary size and in duration of deposit.

b. Creditworthiness policy

To reiterate, the primary principles governing the Council’s creditworthiness criteria are:

Security of capital Liquidity of capital Return on investment

With regard to security, policies are maintained for “categories” of investment to be used, and these are set out at Appendix 3, ie. Specified and Non-Specified investments (see above). For the purpose of liquidity, policies are in place for determining the maximum periods for which funds may prudently be committed with counterparties.

The Chief Financial Officer maintains a “counterparty list” and this is monitored constantly. The CFO has delegated authority to amend the minimum criteria as he sees fit, and will report any such amendments to Cabinet for information as part of the next quarterly Treasury Management Report following the change.

The Council applies the creditworthiness methodology provided by CAS for the selection of investment counterparties. This employs a sophisticated modelling approach utilising credit ratings from the three main credit rating agencies (Fitch, Moody’s and Standard & Poor’s). The credit ratings of counterparties are supplemented with overlays for:

Credit watches and credit outlooks from rating agencies. Credit default swap (CDS) spreads to give early warnings of likely

changes in credit ratings. Sovereign ratings to select counterparties from only the most

creditworthy countries.

The CAS modelling approach combines credit ratings, credit watches and credit outlooks in a weighted scoring system which is then combined with an overlay of CDS spreads for which the output is a series of colour coded bands which indicate the relative creditworthiness of counterparties. These colour codes are used by the Council to determine the suggested maximum duration of investments with a given counterparty. The colour bandings used by the Council are as follows:

Yellow 5 years (UK government debt or its equivalent) Purple 2 years Blue 1 year (nationalised or semi nationalised UK banks only) Orange 1 year Red 6 months Green 100 days No colour not to be used

The CAS creditworthiness service uses a wider array of information than just “primary” ratings. Furthermore, by using a risk weighted scoring system it does not give undue preponderance to one agency’s rating. All credit ratings are monitored weekly and the Council is also alerted to interim changes via its use of the CAS creditworthiness service.

Ratings under the CAS methodology will not necessarily be the sole determinant for the use of a counterparty. Other information sources used will include market data, the financial press, share price and other such information pertaining to the banking sector in order to establish the most robust scrutiny process on the suitability of potential investment counterparties.

The Council will use approved UK counterparties subject to their individual credit ratings under the CAS methodology. The Council may also use approved counterparties from countries with a minimum sovereign credit rating of AA. No more than £3m will be placed with any non-UK country at any time. The list of countries that currently qualify is shown at Appendix 4, however this list will be adjusted by officers in accordance with this policy should ratings change. The CFO has delegated authority to amend the minimum sovereign credit rating as he sees fit, and will report any such amendments to Cabinet for information as part of the next quarterly Treasury Management Report following the change.

The ultimate decision on what is prudent and manageable for the Council will be taken by the Chief Financial Officer under the approved scheme of delegation.

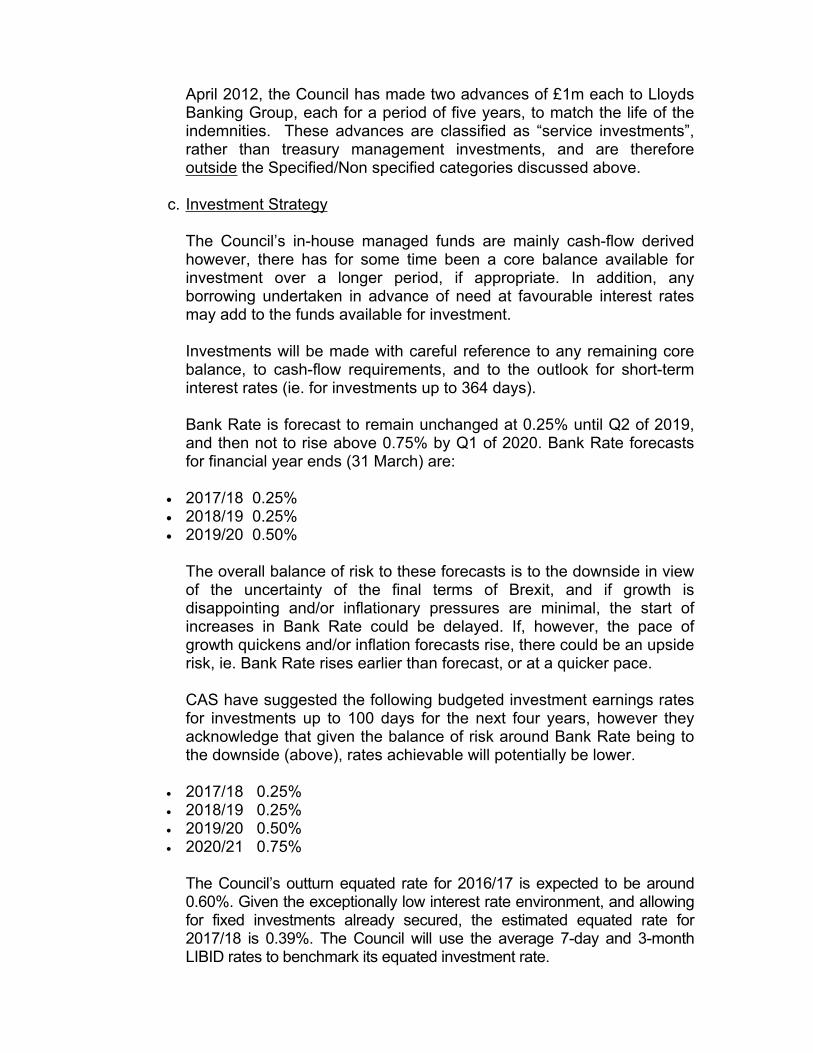

Under the cash-backed Local Authority Mortgage Scheme, launched in

April 2012, the Council has made two advances of £1m each to Lloyds Banking Group, each for a period of five years, to match the life of the indemnities. These advances are classified as “service investments”, rather than treasury management investments, and are therefore outside the Specified/Non specified categories discussed above.

c. Investment Strategy

The Council’s in-house managed funds are mainly cash-flow derived however, there has for some time been a core balance available for investment over a longer period, if appropriate. In addition, any borrowing undertaken in advance of need at favourable interest rates may add to the funds available for investment.

Investments will be made with careful reference to any remaining core balance, to cash-flow requirements, and to the outlook for short-term interest rates (ie. for investments up to 364 days).

Bank Rate is forecast to remain unchanged at 0.25% until Q2 of 2019, and then not to rise above 0.75% by Q1 of 2020. Bank Rate forecasts for financial year ends (31 March) are:

2017/18 0.25% 2018/19 0.25% 2019/20 0.50%

The overall balance of risk to these forecasts is to the downside in view of the uncertainty of the final terms of Brexit, and if growth is disappointing and/or inflationary pressures are minimal, the start of increases in Bank Rate could be delayed. If, however, the pace of growth quickens and/or inflation forecasts rise, there could be an upside risk, ie. Bank Rate rises earlier than forecast, or at a quicker pace.

CAS have suggested the following budgeted investment earnings rates for investments up to 100 days for the next four years, however they acknowledge that given the balance of risk around Bank Rate being to the downside (above), rates achievable will potentially be lower.

2017/18 0.25% 2018/19 0.25% 2019/20 0.50% 2020/21 0.75%

The Council’s outturn equated rate for 2016/17 is expected to be around 0.60%. Given the exceptionally low interest rate environment, and allowing for fixed investments already secured, the estimated equated rate for 2017/18 is 0.39%. The Council will use the average 7-day and 3-month LIBID rates to benchmark its equated investment rate.

An investment treasury indicator and limit must be set for the maximum principal funds invested for periods in excess of 364 days in the forthcoming and two subsequent years (ie. new non-specified investments). The limit for each year is set with regard to the Council’s liquidity requirements.

The treasury indicator and limit for new non-specified investments in each of 2017/18, 2018/19 and 2019/20 is £3m, as detailed at Appendix 1 (treasury indicators) (f), subject always to the overall limit of £5m for total non-specified investments held at any one time, as detailed at Appendix 3.

d. Investments defined as capital expenditure

The acquisition of share capital or loan capital in a body corporate is defined as capital expenditure under regulation 25(1)(d) of the Local Authorities (Capital Finance and Accounting) (England) Regulations 2003. Such investments will have to be funded out of capital or revenue resources, and will be classified as non-specified investments.

Investments in “money market funds”, which are collective investment schemes, and bonds issued by “multilateral development banks”, both defined in SI 2004 No 534, will not be treated as capital expenditure.

A loan or grant or financial assistance by this Council to another body for capital expenditure by that body will be treated as capital expenditure.

e. Provision for credit-related loss

If any of the Council’s investments appear to be at risk of loss due to default, this is a “credit-related loss” and not a loss resulting from a fall in price due to movements in interest rates. In such an instance, the Council will make revenue provision of an appropriate amount.

f. End of Year Investment Report

At the end of the year, the Council will report on its investment activity as part of its Annual Treasury Report.

g. Policy on the use of external service providers

The Council uses CAS as its external Treasury Management advisers, however it recognises that responsibility for Treasury Management decisions remains with the organisation at all times, and will ensure that undue reliance is not placed upon external service providers.

The Council also recognises that there is value in employing external providers of Treasury Management services in order to acquire access

to specialist skills and resources. The Council will ensure that the terms of their appointment and the methods by which their value will be assessed are properly agreed and documented, and subjected to regular review.

2.2.9 Gedling Borough Council scheme of delegation

Full Council is responsible for:

Receiving and reviewing reports on Treasury Management policies, practices and activities

Approval of the annual Strategy (TMSS) Annual budget approval

Cabinet is responsible for:

Approval of, and amendments to, the Council’s adopted clauses, treasury management policy statement and Treasury Management practices

Budget consideration and virement approval Approval of the division of responsibilities Receiving and reviewing regular Treasury Management monitoring

reports, and acting on recommendations Approving the selection of external service providers and agreeing

terms of appointment.

Audit Committee is responsible for:

Reviewing the Treasury Management policy and procedures and making recommendations to the responsible body.

2.2.10 The role of the section 151 officer

The Chief Financial Officer is the Council’s nominated S151 Officer. The role of the S151 (responsible) officer includes the following:

Recommending clauses, Treasury Management Policy and Practices for approval, reviewing these regularly, and monitoring compliance

Submitting regular Treasury Management policy reports Submitting budgets and budget variations Receiving and reviewing management information reports Reviewing the performance of the Treasury Management function Ensuring the adequacy of Treasury Management resources and skills,

and the effective division of responsibilities within the Treasury Management function

Ensuring the adequacy of internal audit, and liaising with external audit The appointment of external service providers

Alternative Options

There are no alternative options, this report being a statutory requirement.

Financial Implications

No specific financial implications are attributable to this report.

Appendices

1. Prudential and Treasury indicators for 2017/18 to 2019/202. Interest rate forecasts3. Specified and non-specified investments4. Approved countries for investment

Background Papers

None identified.

Recommendation

That:

Members approve the Prudential and Treasury Indicators and Treasury Management Strategy Statement 2017/18, which includes the key elements below, and refer it to Full Council for approval as required by the regulations.

1. The Minimum Revenue Provision (MRP) Policy Statement (2.1.3)2. The Borrowing Strategy (2.2.43. The Annual Investment Strategy (2.2.8)4. Capital Affordability Prudential Indicators (Appendix 1)5. Treasury Indicators including affordability limits to borrowing (Appendix 1)

Reasons for Recommendations

To comply with the requirements of the Local Government Act 2003, the CIPFA Prudential Code, CLG MRP guidance, the CIPFA Treasury Management Code and CLG investment guidance.

For more information, please contact:

Alison Ball, Financial Services Manager, on 0115 901 3980