relatorio e contas 2006 (ingles) - lusitania · encouraging human qualities and individual...

TRANSCRIPT

1

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

2

Man

agem

ent

Repo

rt

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

3

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

CONTENTS

INTRODUCTION 5

MANAGEMENT REPORT

MAIN BUSINESS INDICATORS 6

LUSITANIA'S STRATEGY 7

CORPORATE GOVERNANCE 7

RISK MANAGEMENT AND INTERNAL CONTROL SYSTEMS 9

COMMUNICATION 9

INTELLECTUAL CAPITAL 10

INVESTMENT STRUCTURE 10

SHAREHOLDER STRUCTURE 11

PARTNERSHIPS 11

CLIENTS 13

INNOVATION AND PROJECT MANAGEMENT 13

MAIN EVENTS OF THE YEAR 14

COMMUNITY SUPPORT 15

SUPPORT FOR SPORT AND CULTURE 15

ECONOMIC AND FINANCIAL BACKGROUND 16

LUSITANIA'S PERFORMANCE 18

SOLVENCY 20

RESULTS AND PROFITS 21

PROPOSED DISTRIBUTION OF PROFITS 21

NET WORTH 21

ATTACHMENTS TO THE BOARD OF DIRECTORS' REPORT 25

FINANCIAL STATEMENTS

BALANCE SHEET AS AT 31 DECEMBER 2006 29

PROFIT AND LOSS STATEMENT 2006 FINANCIAL YEAR 31

ATTACHMENTS TO THE FINANCIAL STATEMENTS AS AT 31 DECEMBER 2006 33

PROPERTY OWNED BY THE COMPANY AS AT 31 DECEMBER 2006 53

INVENTORY OF THE LUSITANIA COLLECTION 54

RATIFICATIONS

REPORT AND OPINION OF THE BOARD OF AUDITORS 65

ANNUAL REPORT ON AUDITING DONE BY THE REGISTERED AUDITOR 66

LEGAL RATIFICATION OF ACCOUNTS 67

AUDIT REPORT 69

4

Man

agem

ent

Repo

rt

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

5

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

INTRODUCTION

Pursuant to legislation and the articles of association

we hereby submit for your approval the report and

accounts for the twenty first financial year of

LUSITANIA, Companhia de Seguros, S.A., ending at

31 December 2006.

Continuing the main thrust of the strategy applied over

recent years and approved by our Shareholders,

emphasis is laid on guidelines used in 2006 that will

lead the company to being increasingly available and

accessible to all those it deals with, always observing

principles of greater transparency.

6

Man

agem

ent

Repo

rt

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

PRINCIPAL BUSINESS INDICATORS

Principal Business Indicators

2002 2003 2004 2005 2006Gross premiums earned 107.300 123.068 122.023 129.725 147.350Market share (non-life) 2,8% 3,0% 2,9% 3,0% 3,4%Growth rate of premiums 33,8% 14,7% -0,8% 6,3% 13,6%Claims index 64,3% 62,3% 58,5% 57,8% 77,2%Commissions Rate 13,4% 13,1% 13,2% 14,0% 14,0%Expense ratio 29,7% 28,8% 29,6% 30,6% 29,3%Combined ratio 93,9% 91,1% 88,2% 88,4% 106,2%Combined net ratio 79,0% 80,0% 82,1% 80,1% 83,4%Net result 2.021 1.796 2.563 2.911 2.342Investment 121.446 132.869 142.499 164.736 192.307

N° of employees 302 317 330 331 348Premiums per employee 355 388 370 392 423Policies per employee 1.105 1.134 1.135 1.254 1.432GVA per employee 83 75 82 94 95

Profits from sales 1,9% 1,5% 2,1% 2,2% 1,6%Cash & Reserves 27.032 29.243 31.677 33.351 34.795Profits from cash & reserves 7,5% 6,1% 8,1% 8,7% 6,7%

Costs Type/ Policy 52,29 53,59 53,42 51,99 44,99Personnel costs/Policy 28,33 28,69 29,45 29,42 23,91FSE / Policy 15,94 16,42 16,02 14,98 12,89

Solvency margin cover 1,5 1,4 1,5 1,4 1,4

7

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

LUSITANIA'S STRATEGY

MissionProviding security with a difference

VisionLusitania is a Portuguese insurance company, and topursue its purpose is part of the Montepio Group.The Company aims to achieve high levels of profitand solvency through flexible, motivatedorganisation, high efficiency and quality built onhumanistic values and solid partnerships.

Code of ethicsProviding security with a difference:

Providing solid, stable protection for personsand goods.

Part of the biggest financial group, mutual inorigin.

Sustaining higher profit and solvency levels;Safe-guarding the interests of shareholders, staff,policy holders and third parties as a whole.

Defending moral and human values above all,With solid partnerships, namely with thecompanies of the group, brokers, reinsurersand suppliers.

With flexible organisation able to adaptconstantly to challenges proposed.Asking of its staff a team spirit and dedication,as well as continuous professional development,and constantly high levels of motivation andefficiency.

Providing high quality services.Trading on the market in a spirit of loyalty,cooperation and healthy competition, to meetcompetition, but always promoting ourdistinctions.

The standing working principles in Lusitania are to:

Maintain a high standard of efficiency in allservices, to provide higher profits, adequatereturns on capital invested in the company,while maintaining economic and financial solidity.

Promote an adequate policy for applyingresources that the company manages, balancingimmediate income with added value over themedium and long term.

Set up adequate reserve funds to meetresponsibilities assumed.

Increase the company's market share bearingin mind the objectives fixed by the Group.Prepare strategic and operational plans thatdefine clearly and unequivocally the objectivesto be achieved at any given moment.

Constant improvement for all staff byencouraging human qualities and individuallearning, bearing in mind that this is thecompany's greatest asset.

Maintain an attitude of on-going innovation andcorporate drive with a view to creating newmethods and products and to perfecting existingones, aiming at better consumer awarenessrooted in healthy selective High quality ofservice provided to policy holders and thirdparties.Strict observance of legislation, regulations andinstructions in force.

Objectives and strategiesThe approach defined for the three-year period2006-2008 aligns with the objectives defined forthe Montepio Group. This entails continuing withobjectives already adopted that aim to increaseprofits, productivity levels and improve efficiencyindicators.To this end, the Bank-insurance Channel wasreinforced with the promotion of an integrated offerof financial products and services, withoutoverlooking the good management of the otherdistribution channels.At the same time, priority was given to improvingmanagement processes and systems, promotingquality of service and adopting systems to new legaland regulatory requirements with regard to betterpractices for corporate governance.The strategic guidelines listed below aim to meetand quantify the following objectives:

Achieve a pre-tax profit rate of 14% forshareholders in 4 years.

Technical profitability of 3,5%.

Claims rate lower than 60%.

Expense Ratio of approximately 30%.

Increase market share by 0,2%.

To achieve these results, several projects have beendefined to develop the company, always geared toinvolving the client in solutions. Special attentionhas also been given to studying the implementingmeasures to help observe the new law on insurancebrokerage.

CORPORATE GOVERNANCE

Several projects were continued in 2006 that arehelping to make the company more efficient and

8

Man

agem

ent

Repo

rt

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

stable. Significant progress was made with theanalysis model for balancing assets and liabilitiesand a study was completed on integrated riskmanagement that will make it possible to create anadequate econometric model.At the same time, an analysis was done on risks ofbusiness continuity in the case of unforeseen,catastrophic events, the recommendations of whichwill be put into practice in 2007.Responsibility for internal control lies exclusivelywith the Board of Directors that establishesguidelines periodically. There is now an internalcommittee to monitor this control, composed ofsome of those principally responsible for conductingthe business, and in 2006 the committee metmonthly.

Organisational chart

Corporate Governance

General MeetingDr. Vítor Melícias LopesChairmanEng.º José Joaquim FragosoVice-ChairmanAntónio Ferreira CarvalhoSecretary

Board of Directors

Prof. Dr. José da Silva LopesChairmanDr. José António de Arez RomãoCEO / Board MemberDr. Jorge José Conceição SilvaBoard Member

Board of Auditors

Dr. Vasco Ferreira César das NevesChairmanDr. Luís Bartolomeu Baptista de NagyMemberDr. Fernando Vassalo Namorado RosaMember - Official Registered AuditorDr. Victor Reis Pereira da LuzDeputy Member - Official Registered Auditor

Salaries Board

Dr. Vítor Melícias LopesChairmanDr. Vasco Ferreira César das NevesMemberDr. António de Seixas da Costa LealMember

The death occurred at the start of 2007 of Dr.António de Seixas Costa Leal, former Chairman ofthe Board of Directors of Lusitania. His work andqualities as a person and a manager mark thehistory of the company.

Management and Advisory Bodies

Top ManagementTop level company management is conducted by theExecutive Council that meets weekly and sees tothe implementation of strategies, policies,objectives and guidelines defined by the Board ofDirectors, and it also conducts the managementduties delegated to it by the Board.

Executive Council

Dr. José António de Arez RomãoCEO / Board MemberDr. Jorge José Conceição SilvaBoard MemberMárcio Manuel Ventura FigueiredoSenior Manager

Advisory Councils

With a view to making the management of the

ExecutiveBoard

Board ofDirectors

InformationTechnologies

Corporate RiskManagement

Development& Control

Reinsurance

BankingInsurance

ClientManagement

Marketing

Secretariate

Auditing &ActuarialServices

C. ManagementBusiness

Units

ClaimsManagement

Centre

DistributionCentre

OperationsManagement

ExecutiveBoard

Board ofDirectors

InformationTechnologies

Corporate RiskManagement

Development& Control

Reinsurance

BankingInsurance

ClientManagement

Marketing

Secretariate

Auditing &ActuarialServices

C. ManagementBusiness

Units

ClaimsManagement

Centre

DistributionCentre

OperationsManagement

9

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

company more agile, more receptive to others andever closer to the market, there are several Councilsthat advise Administration.There is an Internal Control Council that meetsmonthly, its aim being to monitor companyperformance and propose to Administrationcorrective measures to help Lusitania achieve itsobjectives.

Internal Control Council

Dr. José António de Arez RomãoCEO / Board MemberDr. Jorge José Conceição SilvaBoard MemberMárcio Manuel Ventura FigueiredoSenior ManagerAntónio Paulo da Silva Gonçalves RaimundoDirector of Business Unit ManagementDra. Ana Isabel Gonzaga de CarvalhoDirector of Claims Management CentreDr. Gonçalo Lopes da Costa Ramos e CostaDirector of OperationsDr. Jorge Rafael Torres Gutierrez de LimaDirector of Distribution ChannelsDr. Nuno Ribeiro Quesada van ZellerDirector of Development and Control

Brokers' CouncilAlong lines similar to those described above, lookingfor closer proximity to the surrounding environmentand making the whole of corporate managementaware of market problems, there is a Brokers'Council, appointed annually, whose members arethe biggest and best agents who have been workingwith Lusitania for many years.This Council meets with Administration once everysix months.

RISK MANAGEMENT AND INTERNALCONTROL SYSTEMS

Risk management is performed using traditionalprocesses, backed up by procedures manualsavailable on the intranet site, and is monitored bythe Actuary responsible, by the internal and externalauditor, as well as by the Internal Control Council.From the start of 2004, new emphasis was laid onthe analysis and development of models forintegrated risk management and adding a consistentdesign to global strategy of the organization and thedecision-making process.Market pressures and strong competition in theinsurance industry, better alignment of the decision-making process, together with an acceptable levelof risk tolerance, the need to maximize the utilityof shareholder capital and a firm intention to focusthe attention of our managers on the future, weredetermining factors in leading the Company torethink its strategy.Facing risk as a challenge rather than a hazard, thecompany has had since January 2005 a specificstructure that corresponds to the expectationsdemanded by Regulation 14/2005-R.Planning for this type of supervisory system that is

both preventative and dynamic, Lusitania prepareda detailed plan of activities in 2005 that served as asupport to the report demanded by the supervisorybody. In it are several projects already underway,such as renewal of the company's governance model,implementation of management models for assetsand liabilities, and integrated risk management.With these projects, Lusitania is preparing to meetthe demands of Solvency II, namely pillars I and II,and has already taken part in preparing the testspromoted by CEIOPS, in collaboration with the ISPand the APS.Apart from this, the opportunity was seized to revi-se the technological recovery plan and a new modelfor the continuity of the business is being developed,the first phase of which has already been completed,as already mentioned.Risk assessment in Lusitania is based on the definitionof the International Association of InsuranceSupervisors. Adopting an integrated view of riskmanagement, the objective is to analyse and controlinterdependence among the different risks, whetherthey are at liabilities level or assets level.Lusitania aims to conclude the subsequent phasesof the corporate risk management model by theend of 2007 in order to guarantee better solutionsfor simulating different development scenarios,carrying on what was established in the activitiesplan.

COMMUNICATION

In 2006 Lusitania developed a coherent, sustainedcommunication process at both internal and externallevels.As part of internal communication the Companymaintained and up-dated regularly the content of itsinternet and intranet sites and publicised generalinformation through its document “Breves Instan-tes”, produced and circulated daily by email to allstaff and Exclusive Agents.Externally, it has been a constant concern of Lusitaniato inform, build up a capital of trust and project acorporative image. To this end the monthlynewsletter highlighting the Company's main eventsis still published by email.The Company also participates regularly in thereview “Em Directo”, the communicationmouthpiece of Montepio, which certainlycontributes to strengthening internal culture andcohesion among staff and the companies in the group.Aware that in trading on a competitive market adistinct corporate and commercial image isnecessary, Lusitania has kept its presence in themedia by sending out press releases on theCompany's relevant results, ensuring publication ofthe same in the leading newspapers and tradejournals.Commercial campaigns were held in the press,aligned with projects for product development, withparticular emphasis on the campaign for the FamilyPlan product, conducted in the first quarter of 2006.This campaign, apart from the commercial aspect,attracted extraordinary funding that went to support

10

Man

agem

ent

Repo

rt

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

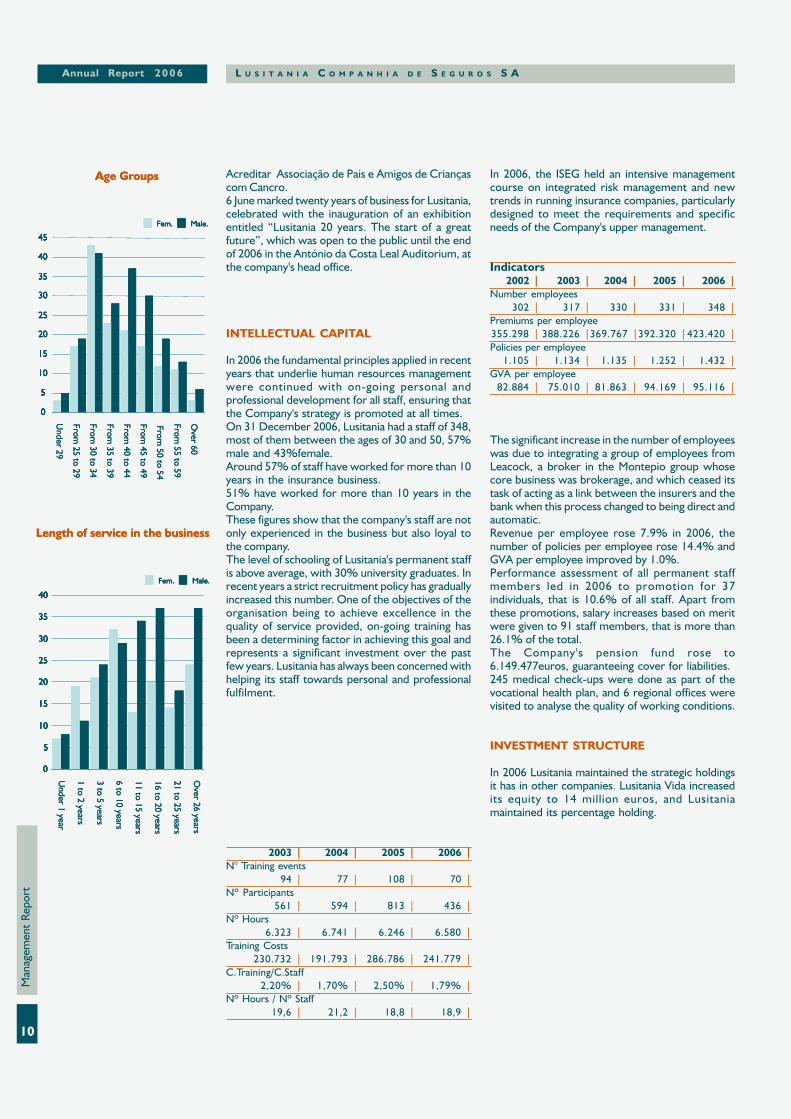

Acreditar Associação de Pais e Amigos de Criançascom Cancro.6 June marked twenty years of business for Lusitania,celebrated with the inauguration of an exhibitionentitled “Lusitania 20 years. The start of a greatfuture”, which was open to the public until the endof 2006 in the António da Costa Leal Auditorium, atthe company's head office.

INTELLECTUAL CAPITAL

In 2006 the fundamental principles applied in recentyears that underlie human resources managementwere continued with on-going personal andprofessional development for all staff, ensuring thatthe Company's strategy is promoted at all times.On 31 December 2006, Lusitania had a staff of 348,most of them between the ages of 30 and 50, 57%male and 43%female.Around 57% of staff have worked for more than 10years in the insurance business.51% have worked for more than 10 years in theCompany.These figures show that the company's staff are notonly experienced in the business but also loyal tothe company.The level of schooling of Lusitania's permanent staffis above average, with 30% university graduates. Inrecent years a strict recruitment policy has graduallyincreased this number. One of the objectives of theorganisation being to achieve excellence in thequality of service provided, on-going training hasbeen a determining factor in achieving this goal andrepresents a significant investment over the pastfew years. Lusitania has always been concerned withhelping its staff towards personal and professionalfulfilment.

2003 | 2004 | 2005 | 2006 |N° Training events

94 | 77 | 108 | 70 |Nº Participants

561 | 594 | 813 | 436 |Nº Hours

6.323 | 6.741 | 6.246 | 6.580 |Training Costs

230.732 | 191.793 | 286.786 | 241.779 |C.Training/C.Staff

2,20% | 1,70% | 2,50% | 1,79% |Nº Hours / Nº Staff

19,6 | 21,2 | 18,8 | 18,9 |

In 2006, the ISEG held an intensive managementcourse on integrated risk management and newtrends in running insurance companies, particularlydesigned to meet the requirements and specificneeds of the Company's upper management.

Indicators2002 | 2003 | 2004 | 2005 | 2006 |

Number employees302 | 317 | 330 | 331 | 348 |

Premiums per employee355.298 | 388.226 |369.767 |392.320 |423.420 |Policies per employee

1.105 | 1.134 | 1.135 | 1.252 | 1.432 |GVA per employee

82.884 | 75.010 | 81.863 | 94.169 | 95.116 |

The significant increase in the number of employeeswas due to integrating a group of employees fromLeacock, a broker in the Montepio group whosecore business was brokerage, and which ceased itstask of acting as a link between the insurers and thebank when this process changed to being direct andautomatic.Revenue per employee rose 7.9% in 2006, thenumber of policies per employee rose 14.4% andGVA per employee improved by 1.0%.Performance assessment of all permanent staffmembers led in 2006 to promotion for 37individuals, that is 10.6% of all staff. Apart fromthese promotions, salary increases based on meritwere given to 91 staff members, that is more than26.1% of the total.The Company's pension fund rose to6.149.477euros, guaranteeing cover for liabilities.245 medical check-ups were done as part of thevocational health plan, and 6 regional offices werevisited to analyse the quality of working conditions.

INVESTMENT STRUCTURE

In 2006 Lusitania maintained the strategic holdingsit has in other companies. Lusitania Vida increasedits equity to 14 million euros, and Lusitaniamaintained its percentage holding.

Age Groups

0

5

10

15

20

25

30

35

40

45

Under

29

From25 to 29

From30 to 34

From35 to 39

From40 to 44

From45 to 49

From50 to 54

From55 to 59

Over

60

Fem. Male.

Age Groups

0

5

10

15

20

25

30

35

40

45

0

5

10

15

20

25

30

35

40

45

0

5

10

15

20

25

30

35

40

45

Under

29

From25 to 29

From30 to 34

From35 to 39

From40 to 44

From45 to 49

From50 to 54

From55 to 59

Over

60

Fem. Male.Fem. Male.

Length of service in the business

0

5

10

15

20

25

30

35

40

Fem. Male.

Under

1 year

1 to 2 years

3 to 5 years

6 to 10 years

11 to 15 years

16 to 20 years

21 to 25 years

Over

26 years

Length of service in the business

0

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40

Fem. Male.Fem. Male.

Under

1 year

1 to 2 years

3 to 5 years

6 to 10 years

11 to 15 years

16 to 20 years

21 to 25 years

Over

26 years

11

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

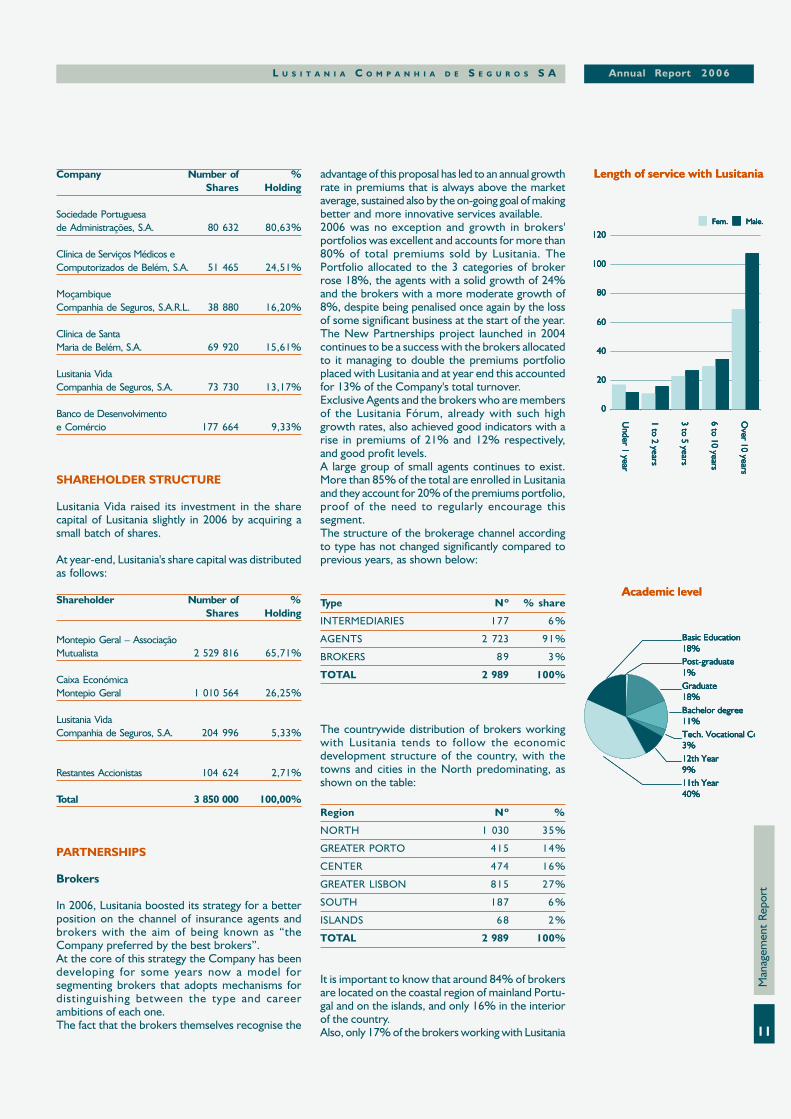

Company Number of %Shares Holding

Sociedade Portuguesade Administrações, S.A. 80 632 80,63%

Clínica de Serviços Médicos eComputorizados de Belém, S.A. 51 465 24,51%

MoçambiqueCompanhia de Seguros, S.A.R.L. 38 880 16,20%

Clínica de SantaMaria de Belém, S.A. 69 920 15,61%

Lusitania VidaCompanhia de Seguros, S.A. 73 730 13,17%

Banco de Desenvolvimentoe Comércio 177 664 9,33%

SHAREHOLDER STRUCTURE

Lusitania Vida raised its investment in the sharecapital of Lusitania slightly in 2006 by acquiring asmall batch of shares.

At year-end, Lusitania's share capital was distributedas follows:

Shareholder Number of %Shares Holding

Montepio Geral – AssociaçãoMutualista 2 529 816 65,71%

Caixa EconómicaMontepio Geral 1 010 564 26,25%

Lusitania VidaCompanhia de Seguros, S.A. 204 996 5,33%

Restantes Accionistas 104 624 2,71%

Total 3 850 000 100,00%

PARTNERSHIPS

Brokers

In 2006, Lusitania boosted its strategy for a betterposition on the channel of insurance agents andbrokers with the aim of being known as “theCompany preferred by the best brokers”.At the core of this strategy the Company has beendeveloping for some years now a model forsegmenting brokers that adopts mechanisms fordistinguishing between the type and careerambitions of each one.The fact that the brokers themselves recognise the

advantage of this proposal has led to an annual growthrate in premiums that is always above the marketaverage, sustained also by the on-going goal of makingbetter and more innovative services available.2006 was no exception and growth in brokers'portfolios was excellent and accounts for more than80% of total premiums sold by Lusitania. ThePortfolio allocated to the 3 categories of brokerrose 18%, the agents with a solid growth of 24%and the brokers with a more moderate growth of8%, despite being penalised once again by the lossof some significant business at the start of the year.The New Partnerships project launched in 2004continues to be a success with the brokers allocatedto it managing to double the premiums portfolioplaced with Lusitania and at year end this accountedfor 13% of the Company's total turnover.Exclusive Agents and the brokers who are membersof the Lusitania Fórum, already with such highgrowth rates, also achieved good indicators with arise in premiums of 21% and 12% respectively,and good profit levels.A large group of small agents continues to exist.More than 85% of the total are enrolled in Lusitaniaand they account for 20% of the premiums portfolio,proof of the need to regularly encourage thissegment.The structure of the brokerage channel accordingto type has not changed significantly compared toprevious years, as shown below:

Type Nº % share

INTERMEDIARIES 177 6 %

AGENTS 2 723 91%

BROKERS 89 3 %

TOTAL 2 989 100%

The countrywide distribution of brokers workingwith Lusitania tends to follow the economicdevelopment structure of the country, with thetowns and cities in the North predominating, asshown on the table:

Region Nº %

NORTH 1 030 35%

GREATER PORTO 415 14%

CENTER 474 16%

GREATER LISBON 815 27%

SOUTH 187 6 %

ISLANDS 68 2 %

TOTAL 2 989 100%

It is important to know that around 84% of brokersare located on the coastal region of mainland Portu-gal and on the islands, and only 16% in the interiorof the country.Also, only 17% of the brokers working with Lusitania

Length of service with Lusitania

0

20

40

60

80

100

120

Under

1 year

1 to 2 years

3 to 5 years

6 to 10 years

Over

10 years

Fem. Male.

Length of service with Lusitania

0

20

40

60

80

100

120

Under

1 year

1 to 2 years

3 to 5 years

6 to 10 years

Over

10 years

Fem. Male.

0

20

40

60

80

100

120

Under

1 year

1 to 2 years

3 to 5 years

6 to 10 years

Over

10 years

Fem. Male.Fem. Male.

Academic level

Basic Education18%Post-graduate1%Graduate18%Bachelor degree11%Tech. Vocational Co3%12th Year9%11th Year40%

Academic level

Basic Education18%Post-graduate1%Graduate18%Bachelor degree11%Tech. Vocational Co3%12th Year9%11th Year40%

Basic Education18%Post-graduate1%Graduate18%Bachelor degree11%Tech. Vocational Co3%12th Year9%11th Year40%

12

Man

agem

ent

Repo

rt

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

are organised as commercial companies, a reflectionof the national situation in the insurance brokeragebusiness and proof of the lack of professionalism inthe sector. However, they do represent 63% of theportfolio placed with Lusitania through the brokersnetwork. With the aim of encouraging an exchangeof experiences, vocational development,strengthening team spirit and alignment with theCompany's strategy, several meetings with brokershave been held, among them:

The II Annual Meeting of Exclusive Agents, inthe Algarve, also attended by the local staff ofthe brokers themselves and Lusitania'scommercial staff who support them.VIII Lusitania Forum, that took place in Lisbonon the topic of “Challenge the present, lead thefuture”, had almost two hundred participants.This meeting included several workshopsenhanced by the presence of universityspecialists, consultants and managers,addressing a range of subjects in marketing,management and technology as well as severaltopics specific to the insurance industry.The II Annual Meeting of New Partnershipsalso held in Lisbon, which helped strengthenthe relationship with a significant number ofnew, high quality agents.The Annual Meeting of Brokers held in thecompany's head office, where several topicsspecific to the brokerage segment werediscussed.

Always aiming to provide its best brokers withmemorable learning experiences, from thepersonal and professional points of view, theCompany organised several loyalty events toselected destinations, among them the UnitedStates, Scotland, Norway, Denmark, Istanbul andTunisia.

Disasters occurring from 2001 to 2005

Date Event Country Losses insured Victims

Million dollars

11-09-2001 Terrorist attack WTC USA 20.716 2.982

06-08-2002 Floods UK, Spain, German, Austria 2.621 38

02-05-2003 Storms USA 3.403 45

11-08-2004 Hurrican Charley USA, Cuba, Jamaica, etc. 8.272 24

26-08-2004 Hurricane Frances USA, Bahamas 5.170 38

13-09-2004 Hurricane Jeanne USA, Caribbean, Haiti, etc. 4.136 3.034

26-12-2004 Earthquake (M.9)+Tsunami Indonesia, Thailand, etc. 2.068 220.000

08-01-2005 Storm Erwin Denmark, Sweden, UK, etc. 1.887 18

24-08-2005 Hurricane Katrina USA, Golf of Mexico, Bahamas 45.000 1.326

20-09-2005 Hurricane Rita USA, Golf of Mexico, Cuba 10.000 34

16-10-2005 Hurricane Wilma USA, Mexico, Jamaica, Haiti, etc. 10.000 35

Source: Sigma, 02/2006

Bank-insuranceBegun in 2005, and concluded in 2006, the projectto connect banking outlets to the insurance systemis now in place. This gives Access to Premiumsimulators, the automatic issue of policies and theimmediate payment of premiums, which all leadsto unequalled gains in productivity and quality ofservice.The new system gives an integral view of clientsand associates of Montepio and provides more directand efficient client attendance.At the same time, new products were launched forthe corporate market, important among them beingMG Mercantil, the Montepio Machines and HeavyEquipment Insurance, the Montepio SafeConstruction Plan, as well as a whole range gearedto supporting leasing products.Also in 2006, studies were begun into a new Motorinsurance product to be sold to Montepio clients,associated both with financing and renting.A new partnership is also being developed with CaixaGalicia that will be further reinforced andconsolidated.

Reinsurers

Internationally 2006 was a calmer year than the onebefore with natural disasters smaller in scale as inmaterial damages and loss of life.This situation brought a more relaxed atmosphereto the September Rendez-Vous, the traditionalinternational reinsurance conference held annuallyin Monte Carlo in the first week of September.With the realism of hind-sight, below is a smallsummary of the major disasters to have occurred inthe past five years, where 2004 is revealed as beingparticularly tragic because of the number of victimsand 2005 suffers from the damages affecting the

13

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

insurance and reinsurance business.Nationally,larger risks continued to spiral upwards, notsupported by optional reinsurance, which causedgrowing difficulties to smaller scale insurancecompanies in gaining access to and even maintainingmajor property and liability risk accounts.Moreover, motor insurance has suffered seriouscorporal damages, with very high estimates,supported to a great extent by reinsurance andaffected by the slowness of the Portuguese courts,remembering that a delay in the decision significantlyraises the final amount of the compensation.Consequently, unable to adopt the management thatwould ensure them a positive result in the longterm, the leading reinsurers for this type of riskhave been increasing the cost of cover,demonstrating their growing concern with thissituation.The entry into force of the valuation table for corpo-ral damages is awaited with great expectationbecause it will help provide timely information andcontrol the result of the business in each year.In 2006, the Portuguese market saw a significantreduction in automatic reinsurance cover for natu-ral disasters, although prices remained the same.This situation, which deteriorates year after year,significantly prejudicing national companies,increases expectation regarding a Disaster Fundbeing set up.All reinsurers working with Lusitania have anexcellent rating and strong leadership and accept atall levels. The technical quality, financial capacity anddiversity of the Company's table of reinsurers,shown below, is an important added value to thecompany.

Company Rating 2005 Rating 2006Swiss Re (leader) AA AAAssurances Mutuelles de France * *Converium BBB+ BBB+Mapfre Re AA- AAMünchener Rück A+ AA-Nacional Re A APartnerRe AA- AA-R+V Versicherungs A+ A+SCOR A- A-Secura A+ A+* Mutual company not listed on the Stock Market

CLIENTS

Lusitania increased its client base in 2006 by around17.1%, against a growth of 8.7% in 2005.In addition to this good performance, an analysis ofthe data reveals other significant indicators that arein line with the Company's strategy and that havehelped increase the share of private clients and ofsmall and very small corporate segments, with aview to grater risk spread and protecting thecompany against the fluctuations of the economiccycle.Proof of good implementation of the strategy mappedout, the company enjoyed growth of approximately26.6% in the number of private clients attracted viathe agents and brokers channel, this segmenttogether with the micro and small companiesaccounting for more than 76% of the premiumsportfolio, compared to 71% in 2005. Among theprivate clients the two most important increasesare in the groups that have generated the mostpositive results.There has also been a significant rise in the numberof policy holders coming through the banking channel,up to 9.4% in 2006.There has also been significantgrowth in the corporate segment, with a rate ofaround 35.7%, reflecting the great capacity thischannel has in associating insurance products withits own financial products, namely loans to firms.To implement the strategic guidelines referred toabove and to achieve the results obtained, Lusitaniacontinued to build on three central pillars:

Developing products adjusted to criticalsegments.Pursuing commercial and incentive policiesadjusted to its distribution channels.Building service capacities to its different targetpublic groups.

In addressing the first pillar, serious majorcompetitive drive is needed in the main insurancesectors Motor and Workmen's Compensation andintegrated product plans are required to promoteaggressive cross selling in advantageous conditions.The second pillar requires a policy for differentiatingcommissions according to the broker segments,products and results achieved, and the use ofproduction competitions and campaigns to help guidethe work of the distribution networks towards themost profitable products and client groups.

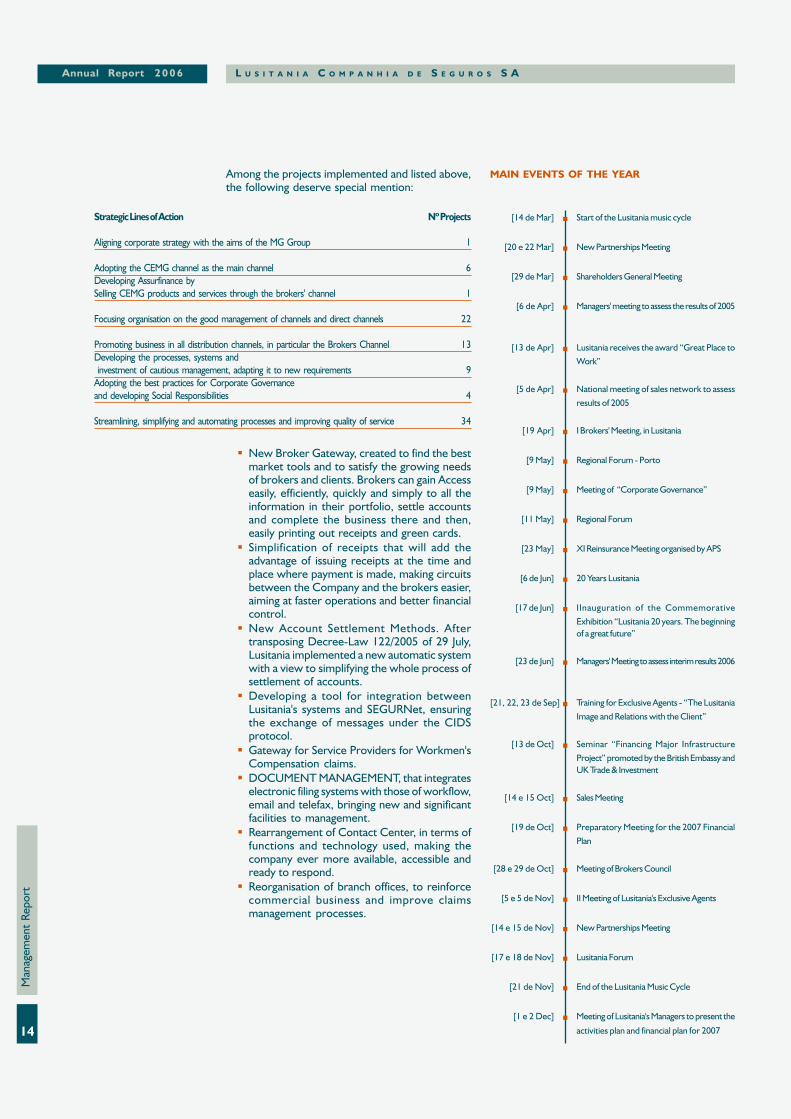

INNOVATION AND PROJECTMANAGEMENT

Continuing the practice of recent years the wholecompany structure is geared to projects that willbring innovation and development and which,clearly, follow a pre-defined strategy.All projects are developed by inter-departmentalteams and around 100 projects were introduced in2006, grouped under eight lines of action:

14

Man

agem

ent

Repo

rt

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

Among the projects implemented and listed above,the following deserve special mention:

New Broker Gateway, created to find the bestmarket tools and to satisfy the growing needsof brokers and clients. Brokers can gain Accesseasily, efficiently, quickly and simply to all theinformation in their portfolio, settle accountsand complete the business there and then,easily printing out receipts and green cards.Simplification of receipts that will add theadvantage of issuing receipts at the time andplace where payment is made, making circuitsbetween the Company and the brokers easier,aiming at faster operations and better financialcontrol.New Account Settlement Methods. Aftertransposing Decree-Law 122/2005 of 29 July,Lusitania implemented a new automatic systemwith a view to simplifying the whole process ofsettlement of accounts.Developing a tool for integration betweenLusitania's systems and SEGURNet, ensuringthe exchange of messages under the CIDSprotocol.Gateway for Service Providers for Workmen'sCompensation claims.DOCUMENT MANAGEMENT, that integrateselectronic filing systems with those of workflow,email and telefax, bringing new and significantfacilities to management.Rearrangement of Contact Center, in terms offunctions and technology used, making thecompany ever more available, accessible andready to respond.Reorganisation of branch offices, to reinforcecommercial business and improve claimsmanagement processes.

Strategic Lines of Action Nº Projects

Aligning corporate strategy with the aims of the MG Group 1

Adopting the CEMG channel as the main channel 6Developing Assurfinance bySelling CEMG products and services through the brokers' channel 1

Focusing organisation on the good management of channels and direct channels 22

Promoting business in all distribution channels, in particular the Brokers Channel 13Developing the processes, systems and investment of cautious management, adapting it to new requirements 9Adopting the best practices for Corporate Governanceand developing Social Responsibilities 4

Streamlining, simplifying and automating processes and improving quality of service 34

MAIN EVENTS OF THE YEAR

[14 de Mar] Start of the Lusitania music cycle

[20 e 22 Mar] New Partnerships Meeting

[29 de Mar] Shareholders General Meeting

[6 de Apr] Managers' meeting to assess the results of 2005

[13 de Apr] Lusitania receives the award “Great Place toWork”

[5 de Apr] National meeting of sales network to assessresults of 2005

[19 Apr] I Brokers' Meeting, in Lusitania

[9 May] Regional Forum - Porto

[9 May] Meeting of “Corporate Governance”

[11 May] Regional Forum

[23 May] XI Reinsurance Meeting organised by APS

[6 de Jun] 20 Years Lusitania

[17 de Jun] IInauguration of the CommemorativeExhibition “Lusitania 20 years. The beginningof a great future”

[23 de Jun] Managers' Meeting to assess interim results 2006

[21, 22, 23 de Sep] Training for Exclusive Agents - “The LusitaniaImage and Relations with the Client”

[13 de Oct] Seminar “Financing Major InfrastructureProject” promoted by the British Embassy andUK Trade & Investment

[14 e 15 Oct] Sales Meeting

[19 de Oct] Preparatory Meeting for the 2007 FinancialPlan

[28 e 29 de Oct] Meeting of Brokers Council

[5 e 5 de Nov] II Meeting of Lusitania's Exclusive Agents

[14 e 15 de Nov] New Partnerships Meeting

[17 e 18 de Nov] Lusitania Forum

[21 de Nov] End of the Lusitania Music Cycle

[1 e 2 Dec] Meeting of Lusitania's Managers to present the

activities plan and financial plan for 2007

15

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

COMMUNITY SUPPORT

Lusitania continued in 2006 to coordinate operationaland strategic objectives with the main socialresponsibilities the company has always defended.To this end, the company's auditorium was madeavailable for holding a number of conferences andsupport given to those working in communityinterest areas, among them:

A seminar on the theme “ The IberianElectricity Market” promoted by the Associa-ção Portuguesa do Centro Europeu das Em-presas com Participação Pública e InteresseEconómico Geral (APOCEEP).MIT Massachusetts Institute of Technologymeeting promoted by Montepio.Meeting of the Bank of Portugal.Public presentation of the National Campaignagainst Domestic Violence, organised by theEstrutura de Missão contra a Violência Domés-tica (EMCVD), and with the support of theAssistant Secretary of State for Rehabilitationand the Secretary of State for the Presidency.Commemoration of the 24th. Anniversary ofthe Associação Portuguesa de Seguradores(APS).Meeting of the Anglo-Portuguese Chamber ofCommerce.Scrabble Júnio Championship, promoted by theAssociação Nacional de Professores de Portu-guês, for children between the ages of 5 and10, part of the incentive for learning Portuguesein Elementary Schools.Launch of the book “Arcádia Notícia de umaFamília Anglo-Portuguesa” by Ana Vicente.

Contributions were also made to somehumanitarian and social institutions.

SPORT AND CULTURAL SUPPORT

Similar to the previous year, Lusitania continued acycle of music in 2006 in its facilities for clients,brokers and staff with a diversified musicalprogramme, including the classics and jazz.In this cycle the following groups performed:

Eloemsemble Baroque quartet with harpsichord.Voices of Broadway.Stéphanie Manzo Harp recital.Quintet in homage of Sarah Vaughan.Clarinet quartet of Lisbon.TGB.Paulo Gaio and António Rosado.Mário Laginha.Jean-François Lézé xylophone recital.Moscow Piano Quartet.Pocket Brass Band.

Repeating the success of the previous year, an open-air concert was held in the garden of the PortoCovo Palace, with the Reunion Big Jazz Band a groupwith 18 players, founded in 2003 under the directionof Claus Nymark, which provided an agreeable

musical evening.The Company held art exhibitions showing thepaintings of Sylvia Purwin Falcão Trigoso and IsabelTorres.

Arts SponsorshipIn 2006, Lusitania continued to be the Official Insurerof the Portuguese Institute of Museums and as suchsponsored several exhibitions, among them:

100 Anos Bonifácio Lázaro Lozano”, in theMuseum of Ethnography and Archaeology.“D. Amélia, uma rainha, um museu”, in theNational Coach Museum.“James Coleman”, in the Chiado Museum.“Roteiros Conímbriga”, in the MonographicMuseum of Conímbriga.“Roteiros Museu Nacional do Azulejo”, in theNational Tile Museum.“O Museu Grão Vasco contado aos mais no-vos”, in the Grão Vasco Museum.“200 Anos de Vestidos de Baptizados”, in theNational Costume Museum.

Lusitania gave its support to other exhibitions,including those organised by the Lisbon MunicipalCouncil:

Exhibition of Gonçalo Duarte, in the GalveiasPalace.Christmas cribs “ O Passado Presente”.Exhibition of João Borges “De lá para Cá”.“Graça Morais” in the Collection of the PaçoD`Arcos Foundation.“IX Exhibition of the Visual Arts”, in the MarineAcademy.

The Company also renewed the agreement withthe Museum of the Presidency of the Republic,where the following exhibitions were promoted:

Presidentes de Portugal”.“O Motor da República, os Carros dos Presi-dentes”.

In the literary field, Lusitania helped publish a bookon the life and works of Carlos Reis, considered tobe one of the most important Portuguese landscapeand portrait artists of the close of the XIX centuryand the first half of the XX century.

Support was also given to the “RE.AL” Theatre andContemporary Dance Company, which hasperformed in Barcelona, Paris, Lisbon, Nyon,Salzburg and Brussels.

SponsorshipContinuing the tradition of giving its support to sportsevents Lusitania promoted and supported thefollowing sports and sports groups:

Skysurf: José Veras, seven times national SkySurfchampionship and holder of two bronze medalsin European Championships.Athletics: athletes of the Clube Oriental de Pechão,Sonata Milusauskaite holder of 4th. position inworld and European ranking and Ana Cabecinha,Portuguese Champion on covered track.

16

Man

agem

ent

Repo

rt

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

Handcycling: 1º International HandcyclingChampionship organised by Parasport.Golf: Golf Tournament “Goal in One” and GolfTournament “Gala Week” both held in Quinta doLago.Sail: Participation in regattas for Açor leisure craft.Futsal: Support for the Futsal team of Estoril Praiada Fundação Fausto Figueiredo.Cross country: Lisbon Dakar Rally, by supportingthe pair Pedro Grancha and Victor Jesus in aMitsubishi Pagero DiD.

Lastly, Lusitania became the Official Patron of thePortuguese Tennis Federation.

ECONOMIC AND FINANCIALBACKGROUND

International EconomyThe world economy continued to expand in 2006,with global wealth likely to rise by 5.1%, accordingto European Commission estimates, due to a greatextent to development in some of the Asiancountries.

Chine continued its upward economic spiral,sustained by exports and investment, and shouldsettle at 10.4%, although there may be a slightslackening off in the next two years to 9.8% in 2007and 9.7% in 2008. India is following this trend andshould increase wealth by 8.1% in 2006, 7.4% in2007 and 7.3% in 2008.

The economy of the USA should record growth of3.4%, a slight rise against the 3.2% of 2005, but aslow-down to 2.3% is expected for 2007 due to afall in domestic consumer spending and majordownturns in the real estate sector. A recovery of2.8% is expected in 2008.

The Japanese economy increased its growth, risingfrom 2.6% in 1005 to 2.7% in 2006, boosted byincreases in private consumption and in the FBCFbut, due to a deterioration in net exports, real GDPis unlikely to rise much above 2% in coming years.The euro zone economy is beginning to showsignificant improvement. According to the EuropeanCommission, growth of GDP should be around 2.6%in 2006, far higher than the 1.4% of 2005. Thisrecovery is due to an increase in private spendingand investment, which reveals some improvementin the confidence index of economic agents.

Unemployment should be the lowest since 2001(7.9%) and the about-turn in the Balance ofPayments, from negative to positive, provides somesolidity for future growth because the Euro Zonewill be less dependent on external demand.

Fluctuations in the price of oil throughout the yearconfirmed its volatility, with Brent reaching amaximum of 78 dollars a barrel on the London

market, despite closing the year at the same 60dollars per barrel with which the year began. Thefutures market and current expectations regardingthe oil price, suggest that prices will remain high asa result of the political instability in some producercountries, made worse by high global demand.

Inflation has remained relatively stable throughoutthe world, due to a drop in the price of food andindustrial products, the result of the phenomenonof corporate cost rationalisation and the increase inthe number of low cost producers on the worldmarket. In addition, constraints on salary increaseshave compensated partially for the rise in the priceof oil. In the euro zone, inflation should settle at2.2%.

The main financial markets were up throughout2006, reflecting the expectation of high profits andgreater certainty indicators. In the euro zone shareswere up in most business sectors, the main indexesbeing up by around 20%.

The trend on Exchange markets was for the euro torise. The European currency has been benefitingfrom market speculation that central banks are likelyto raise interest rates. The market expects the ECBwill raise interest rates in Europe at a rate higherthan the FED in the USA and the BoJ in Japan. Againstthe main international currencies the euro was up11.17% against the dollar and 12% against the yen.

After a year in which steering rates for the eurozone have remained at all time lows, in 2006, theECB raised rates 5 times by 25 base points, thereference rate rising from 2.5% to 3.5%. Forecastssuggest that interest rates will rise on two moreoccasions in 2007. The expectation of furtherincreases is linked above all to the need to holdinflation in the euro zone around a threshold of 2%.

National EconomyAfter a weak growth of 0.4% in 2005, GDP in Por-tugal should rise 1.2% in 2006, according to theBank of Portugal. However, although this is a positivetrend it is still below the European average, as hasbeen the case for the past five years.

Estimated growth for 2006 should be basedfundamentally on rising exports, while thecontribution from domestic demand is likely to bepractically nil. The likely fall in the contribution fromdomestic demand compared to the two previousyears reflects a marked slow-down in private andpublic consumption, as well as a sharper fall in theFBCF. Domestic spending is still restricted by thenegative evolution of monetary conditions and bythe need to correct the structural imbalance ofpublic accounts, in a context of continued slowgrowth in the Portuguese economy.

The economic growth forecast for 2006 should helpkeep the unemployment rate at the 7.6% of 2005.

0%

2%

4%

6%

8%

10%

12%

2005 2006 2007 2008

World USA Japan

Euro Zone China

Source: European Commission

Economic Growth

0,40,50,60,70,80,91,01,11,21,31,4

01 02 03 04 05 06

Euro/Dollar

50

70

90

110

130

150

170Euro/Yen

EUR/USD EUR/JPY

Source: European Central Bank

Euro Exchange Rate

GDP trends

-2%-1%0%1%

2%3%4%5%

98 99 00 01 02 03 04 05 06(e)

GDP pm

Source: Banco de Portugal

0%

2%

4%

6%

8%

10%

12%

2005 2006 2007 2008

World USA Japan

Euro Zone China

Source: European Commission

Economic Growth

0%

2%

4%

6%

8%

10%

12%

2005 2006 2007 20080%

2%

4%

6%

8%

10%

12%

2005 2006 2007 2008

World USA Japan

Euro Zone China

Source: European Commission

Economic Growth

0,40,50,60,70,80,91,01,11,21,31,4

01 02 03 04 05 06

Euro/Dollar

50

70

90

110

130

150

170Euro/Yen

EUR/USD EUR/JPY

Source: European Central Bank

Euro Exchange Rate

0,40,50,60,70,80,91,01,11,21,31,4

01 02 03 04 05 06

Euro/Dollar

50

70

90

110

130

150

170Euro/Yen

EUR/USD EUR/JPY

Source: European Central Bank

Euro Exchange Rate

GDP trends

-2%-1%0%1%

2%3%4%5%

98 99 00 01 02 03 04 05 06(e)

GDP pm

Source: Banco de Portugal

GDP trends

-2%-1%0%1%

2%3%4%5%

98 99 00 01 02 03 04 05 06(e)

GDP pm

Source: Banco de Portugal

17

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

There is likely to be a budget deficit of 4.6% of GDPat year end, a fall of 1.4% compared to 2005, whichmay keep the country true to its objectives of 3% in2008.

The inflation rate settled at 3.1% at the close of2006, due to the effect of increasing VAT from 19%to 21% in June 2005, by rising import prices and bythe significant increase in the price of someunprocessed food products.

As to be expected in a year in which the EuropeanCentral Bank raised the reference rate by 125 b.p.,the six-months Euribor followed this increase risingfrom 2.6% to 3.8% throughout 2006.

The Portuguese stock market performed well, andin line with the major international stock markets.At the close of 2006, the PSI 20 index rose 30%, Itshould be underscored that a part of this excellentperformance in 2006 was due to Public Offers toBuy that stimulated the market.

Analysis of sectorsIn the first three quarters of 2006 GVA rose inFinancial and Real Estate Business by 3.6%, duemainly to high growth in Financial Business. Duringthe same period there was also a rise in GVA forCommerce, Restaurants and Hotels of 2.4% and aslight recovery in Industry of 1.6%. On the negativeside, there was a sharp fall of 8% in the Constructionsector.

The national insurance marketThe national insurance market, which has hadgrowth levels ahead of those of the economy inrecent years, saw this trend change in 2006 with areduction of 2.3% in the value of overall production.This reduction is due to a considerable fall in theLife sector, which although increasing 39.8% in thefirst quarter of the year, will close 2006 with a lossof 4.1%, compared with 2005, a year in which thissector increased 46.2% against 2004.

However, throughout 2006 the Non-Life sectorenjoyed stable monthly growth of between 0.8%and 2.6%, closing the year with an increase of 1.5%compared to the closing figure for 2005. If theinflation forecast by the Bank of Portugal wasdiscounted from yearly growth, then there was adrop in revenue from the non-life sectors of 1.8%,in real terms.

Motor insurance, which accounts for 46% of theNon-Life market, rose by only 0.3% but, accordingto ACAP (Automobile Association) data, the lightvehicles market fell 5.1% in 2006 compared to thesame period in the previous year.The population's growing concern for medical careand the known shortcomings of the National HealthService are, without doubt, some of the reasonsthat explain the increase of 9.7% in premiums in

the Health sub-sector.2006 saw stagnation in all of the sectors in the Fireand Allied Perils sectors, with only a rise of 0.5%.Even Workmen's Compensation took a downturnin revenue of 0.7%, reflecting the country's weakeconomic growth and salary constraints.

As in other sectors, in the insurance industry therehas also been concentration. In 2001 there were 86companies trading and in 2006 only 68 activeinsurers. From this it is not surprising that 5companies with the largest share account for 61%of the market.

Turnover in the insurance industry, which wasmaking an increasing contribution to GDP up to2005, when it rose to 9.15%, fell in 2006, closingthe year at 8.6%, halting the cycle of drawing closerto the more developed European countries, whichcontribute around 10%.

According to information from the Associação Por-tuguesa de Seguradores, referring to the last quarterof 2006, the claims ratio for direct insurance, priorto calculating costs per type, for all of the non-Lifeinsurance sectors, was 61.8%, which is practicallythe same amount for the same time in 2005, whenit was 61.6%.

Among the main insurance sectors, there was anincrease of 5% in claims in the Fire and Allied Perilsgroup, which reached around 41%. The claims ratefor Motor insurance was 68.2%, a slight fallcompared to the 68.9% of 2005. Claims in theAccident and Health insurance sectors fell 0.8%,and are now at 68.3% of premiums. However, thisratio is likely to suffer an increase by the end of theyear, even exceeding 70%.

Prospects for business developmentIn 2006 the insurance business achieved the averagelevel of the European market in its contribution toGross Domestic Product. Associating this with lowexpectations for economic growth it is unlikely thatthe insurance business will show much sign ofexpansion, particularly in the Non-Life sectors inwhich Lusitania deals.

However, we are sure that the way in which thebusiness is shared out among the different insurancecompanies will continue similar to 2005, with smalland average sized, stable, well organised companiesthat are flexible and hard working benefiting fromthe instability that the major units will continue toexperience as a result of recent restructuring, whichin some cases was not concluded.

A new brokerage law will come into force in 2007,which as a whole will introduce several positivemeasures that will promote more professionalismand transparency in the sector although initially itwill increase competition for the best and biggestbrokers with a likely rise in acquisition costs.

Inflation Rate

4,3%3,1%

0%1%2%3%4%5%6%

2002 2003 2004 2005 2006

Source: Instituto Nacional de Estatística

Inflation Rate

4,3%3,1%

0%1%2%3%4%5%6%

2002 2003 2004 2005 2006

4,3%3,1%

0%1%2%3%4%5%6%

2002 2003 2004 2005 2006

Source: Instituto Nacional de Estatística

Interest Rate

5,2%

3,8%

0%

1%

2%

3%

4%

5%

6%

99 00 01 02 03 04 05 06

Euribor (6m)

Source: European Banking Federation

Interest Rate

5,2%

3,8%

0%

1%

2%

3%

4%

5%

6%

99 00 01 02 03 04 05 06

Euribor (6m)

Source: European Banking Federation

PSI 20 Index2006

8

9

10

11

J F M A M J J A S O N D

(in thousands of euros)

Source: EURONEXT Lisbon

PSI 20 Index2006

8

9

10

11

J F M A M J J A S O N D8

9

10

11

J F M A M J J A S O N D

(in thousands of euros)

Source: EURONEXT Lisbon

18

Man

agem

ent

Repo

rt

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

LUSITANIA'S PERFORMANCE

TECHNICAL BUSINESS

PolicesThe number of policies in force on 31 December2006, added to the number of temporary contractsissued in the financial year, rose to 498,282, up 20.2% against 2005, (see graph showing policynumbers).

Although all the main insurance sectors showedsignificant gains, particularly Workmen'sCompensation, which rose 9.8% and Multi-risks,which rose 11.6%, there was also growth in theMotor insurance sector of around 50%, onlyexceeded by the Maritime Hull sector, which rose65.2%.174,507 new policies were issued in 2006, up 72,254against 2005.

The number of cancellations was also high at 34.7%,reaching 75,456 contracts in 2006, against 56,031 in2005, due mainly to cancellations caused by thefailure to make on-going payments.

It is important to remember that the number ofthis type of cancellation has almost trebled sincethe change to the legal regime applied to the paymentof insurance policies, because in 2005 the numberof cancellations was 13,450 against 35,561 in 2006.This change in the law had no effect on payment ofthe first receipt, in which the number of casesincreased only 3.7%, a significantly lowerpercentage than the increase of new contracts, (seegraph on Premium numbers).

PremiumsReturns on insurance premiums in 2006 exceeded147 M€ , a growth of 13.6%.

2002 2003 2004 2005 2006Gross premiumsearned 107.300 123.068 122.023 129.725 147.350Growthrate 33,80% 14,70% -0,80% 6,30% 13,60%Numberof contracts 333.807 359.481 374.700 414.634 498.282Year andfollowing 317.375 346.082 361.710 400.813 483.840Temporary(earned) 16.432 13.399 12.990 13.821 14.442Growthrate -2,80% 7,70% 4,20% 10,70% 20,20%Average premiumper policy 321 342 326 313 296

Motor insurance contributed most towards this,with 32.6%. Personal Accidents also roseconsiderably, by 17.9%, and Workmen'sCompensation, after a slight fall in 2005, rose 6.5%in 2006.

Under Material Risks, the expected fall in the Fireand Allied Perils portfolio was added to the effect ofportfolio selection at mid-year, with resultsmitigated by underwriting many small contracts.

Apart from these risks and the Goods Transportsector, Lusitania had an above-market average risein all other sectors with a subsequent gain in marketshare.

Average premiumsThe average Premium per policy dropped from€ 313, in 2005, to € 296, in 2006. The most significantreductions were observed in Motor insurance, from€ 333 to € 294, and in material risks, from € 152 to€ 139. Workmen's compensation also fell slightly,far less than in 2005.

These developments are linked to portfolioselection, as already mentioned, and to focussingthe sales network on individual business and smalland medium sized companies.

Portfolio compositionSimilar to what happened in 2005, in 2006 the Mo-tor insurance sector increased its share of theportfolio from 33% to 38%. Naturally, all othersectors saw their share of the company's portfoliocomposition fall. Even so, Motor insurance in theLusitania portfolio is lower than that of the market,where it accounts for 46% of revenue from theNon-Life sectors, (see graph of revenue structure).

ClaimsThere was an atypical increase in claims costs in2006, the year closing with a rate of 77.2%, justifiedby three Multi-Risk insurance claims for very largeamounts, to a great extent covered by reinsurancetreaties, to which were added a large number ofclaims resulting from the floods last October.

DI Claims a)

Insurance Sectors 2005 2006ACCIDENTS AND HEALTH 74,4% 70,5%Workmen's Compensation 79,0% 72,8%Personal Accidents 21,6% 29,6%Health 86,4% 88,9%FIRE AND ALLIED PERILS 31,7% 118,4%Fire and natural elements 36,7% 9,3%MultiRisk 36,0% 127,8%Other Material Damages -22,5% 68,0%MOTOR 59,9% 64,8%TRANSPORT 39,7% 10,4%Goods 40,8% 5,0%Carriage and Hull 37,2% 23,0%THIRD PARTY LIABILITY 42,2% 37,1%SUNDRY 25,0% 50,8%TOTAIS 57,8% 77,2%a) Prior to entering “costs per Type”

Number of policies

333.807359.481 374.700

414.634

498.282

2002 2003 2004 2005 2006

Number of policies

333.807359.481 374.700

414.634

498.282

2002 2003 2004 2005 2006

333.807359.481 374.700

414.634

498.282

2002 2003 2004 2005 2006

333.807359.481 374.700

414.634

498.282

2002 2003 2004 2005 2006

Premium trends

107.300123.068

147.350

129.725122.023

50.000

100.000

150.000

2002 2003 2004 2005 2006

(thousands of euros)

Premium trends

107.300123.068

147.350

129.725122.023

50.000

100.000

150.000

2002 2003 2004 2005 2006

(thousands of euros)

Revenue Structure 2006

Motor38%

Sundry1%

Accident & Health37%

Transport1%

Fire & Allied Perils22%

Third Party1%

Revenue Structure 2006

Motor38%

Sundry1%

Accident & Health37%

Transport1%

Fire & Allied Perils22%

Third Party1%

19

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

There was also an increase in the claims rate forthe Motor sector, that took it to 64.8%, still belowthe average for the Portuguese market and which isrelated to the sharp increase in the respectiveportfolio.

Similar to 2005, the Health sector also contributedto claims costs with a 2.5 percentage point increasein the claims ratio, closing the year at 88.9%, in linewith the worsening trend in this sector on theinsurance market, the result of an increase in thecosts of health care services.

To offset this, there was a reduction in the costs ofWorkmen's Compensation, that meant a fall of 6.2percentage points in the claims ratio, compared to2005, reflecting the effort made to control costsand optimise claims management processes.

For the third consecutive year, there was a fall inthe number of fatal labour accidents, accompanyingthe national trend, which is still far from satisfactoryor comparable to levels in other Europeancountries. Every effort must continue to be madetowards an increasing awareness on the part of ourcompanies of the urgent need to improve labouraccident prevention and safety conditions at the worksite.

The other sectors, although scarcely significant,have performed evenly as in previous years.

Running costsRunning costs are the same as in 2005 and accountfor 14% of total gross premiums earned in the year,although the contribution of reinsurers has beenreduced by around one percentage point a result ofthe change in the structure of the portfolio.

Outward reinsuranceIn 2006, most Portuguese companies suffered highmaterial losses, the majority due to the floods thatoccurred in the fourth quarter of the year.

Lusitania followed the market trend and was hit bythree large materials claims, two affecting its directbusiness and one affecting the fronting business ithas with the Royal & SunAlliance network. Suchevents, rare in the history of Lusitania, prevent theaccounts balance from showing its usual benefit toreinsurers.

However, if we subtract from the total reinsurancebusiness the sumo of these unusual claims described,results become positive, both for contractual andoptional business, and results are stable andconsistent.

This fact has meant that renewal of the reinsuranceprogramme has proceeded smoothly and withouttoo much financial burden, Lusitania benefiting notonly from stable statistics and with a significantbenefit accumulated for reinsurance, but also froman international image of good management, strictprinciples and transparency.

Reducing the ceding rate was a priority in the yearand it has been both achieved and exceeded, withits index falling practically 2 percentage points from17.03% to 15.25%. The company's strategy ofpreferring small scale risks and increasing the mo-tor insurance portfolio also contributed here, witha ceding rate lower than average.

Internally, the project was carried forward forCompany information to have access to reinsurancedocuments and the second phase of the projectshould be completed in 2007.

Inward reinsuranceLusitania continued its policy of inward insuranceclosely restricted to partnerships or insurersbelonging to the Montepio Group.

Participation in the Pool CIAR was renewed,because this has helped the Company get a betterunderstanding of other markets, exchange technicalexperience and inward reinsurance with balanced,stable results in the long term.

Support provided to Impar de Cabo Verde achieveda highly gratifying balance in 2006 now that resultsare significantly positive in relative terms, and thatcompany has its programme placed autonomouslywith a range of well-known international companies.An important phase in Lusitania's support to Impar,begun in 2002, has now come to an end.

The business begun by Moçambique, Companhiade Seguros continued in the form of definition andacceptance of the respective reinsurance programmeand support provided in several technical areas.

There is no other active inward reinsurance, andparticipation in Pool Atómico Português and in Ris-cos Espaciais is in run-off.

Costs according to typeLusitania has always submitted Costs per Type thatare below average for the Non-Life market and the2006 financial year closed with a reduction in thisindicator, which has meant a gain in productivity andan improvement in competitive capacity.These conclusions are confirmed in the followingtable that reveals that measures adopted to optimisework procedures continue to bring benefits.

Market2002 2003 2004 2005 2006 2005

Costs per Type/ Premiums 16,3% 15,7% 16,4% 16,6% 15,2% 19,6%Personnel costs/Premiums 9,0% 8,6% 9,2% 9,4% 8,1% 9,2%FSE / Premiums 5,1% 5,0% 5,0% 4,8% 4,4% 6,9%

Market2002 2003 2004 2005 2006 2005

Costs per Type / Policy 52 54 53 52 45 63Personnel costs / Policy 28 29 29 29 24 29FSE / Policy 16 16 16 15 13 23

12%

14%

16%

18%

20%

22%

2002 2003 2004 2005 2006

Ceding rate

12%

14%

16%

18%

20%

22%

12%

14%

16%

18%

20%

22%

2002 2003 2004 2005 2006

Ceding rate

20

Man

agem

ent

Repo

rt

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

Portfolio composition according to type of asset

31-Dec-05 31-Dec-06 Var. Amount % Amount % %National Shares 8 698 5,28% 11 805 6,14% 35,73%Foreign Shares 6 785 4,11% 6 578 3,42% -3,05%National Public Debt 3 028 1,83% 3 818 1,99% 26,10%Foreign Public Debt 18 673 11,34% 18 220 9,47% -2,43%Other National Bonds 4 712 2,86% 2 857 1,49% -39,36%Other Foreign Bonds 45 823 27,82% 53 653 27,90% 17,09%FIM National 3 869 2,35% 1 223 0,64% -68,40%FIM Foreign 2 026 1,23% 2 928 1,52% 44,57%FII National 1 582 0,96% 1 643 0,85% 3,86%FII Foreign 0.00 0,00% 0.00 0,00% 0,00%Property 38 247 23,22% 41 880 21,78% 9,50%Liquidity 24 366 14,79% 38 874 20,21% 59,54%Loans 3 144 1,91% 4 993 2,60% 58,80%Other Assets 3 783 2,30% 3 835 1,99% 1,37%Global Value of Portfolio 164 736 100,00% 192 307 100,00% 15,61%(in thousands of euros)

Net Investment

2004 2005 2006Liquidity 452 2 075 204Term Deposits -8 545 -1 149 14 304Bonds 15 914 17 234 7 280Shares 169 -138 1 129Investment Funds -1 717 209 -1 953Property 604 1 266 2 455Lusitania Collection 208 24 52Loans -30 319 1 848TOTAL 7 055 19 842 25 319(in thousands of euros)

Concentration of Portfolio per Issuing Country

31-Dec-05 31-Dec-06 Amount % Amount %Portugal 91 430 55,50% 113 089 58,81%Spain 15 412 9,36% 16 684 8,68%França 13 465 8,17% 15 076 7,84%France 12 604 7,65% 13 726 7,14%The Netherlands 6 282 3,80% 8 032 4,18%United Kingdom 5 730 3,48% 6 478 3,37%United States 5 022 3,05% 5 274 2,74%Italy 3 600 2,19% 3 785 1,97%Áustria 2 053 1,25% 2 144 1,11%Luxemburg 1 515 0,92% 1 548 0,80%Others 7 623 4,63% 6 471 3,36%TOTAL 164 736 100,00% 192 307 100,00%(in thousands of euros)

Asset managementThe Company's investment policy continues to bebased on criteria of caution in asset selection that isappropriate for the insurance business.The Company's portfolio, which at year-endamounted to around 192 million euros, is comprisedmainly of bonds and property. Risk assets representless than 9.56% of the total, while financialinvestment funds represent 2.16%.The managed bond portfolio rose to more than 78.5million euros, of which around 47.48% are fixedrate securities. Fluctuating rate securities accountfor around 50.60% of these assets, which means areverse in the share between fixed and fluctuatingrate securities, justified by Euribor trends in 2006.Similarly, the relative share of liquidity valuesrepresent not only demand deposits and cash, butalso the amounts of term deposits, and they amountto 20.21% of the portfolio.Investment, net of disinvestment, at purchaseprices, was € 25,319,270.12. The table shows netinvestment for the year according to type.

Already considering investments at list prices, thevariation in the total value was more than 27.5million euros compared to 2005. The portfoliostructure in 2005 and 2006 is shown on the table“Composition of the portfolio according to type ofasset”.

The portfolio risk is essentially in Portugal or theEuropean Union. There has been an increase ininvestments in Portugal and in high rating countries,namely Spain, France and Germany. With theexception of two Mozambican securities, theCompany's entire portfolio is in euros.

The quality of securities making up the bond portfoliois shown on the table “Rating for Bond Portfolio”.

More than 29% of the portfolio is rated AAA andmore than 92% is represented by assets with arating of A- or higher, according to Standard & Poor'srating.Around 94% of the portfolio matures in 2008, orbeyond, which compares with 88% in 2005, asshown on the table “Maturity of bond portfolio”.

In terms of portfolio duration, around 77% of assetsmature in 3 years or beyond then, and approximately66% mature beyond 5 years, as shown on the table“Duration of bond portfolio”. In 2005, these ratioswere 80% and 68% respectively.

SOLVENCY

When the solvency margin is calculated as demandedby the Instituto de Seguros de Portugal, the itemsin the margin are 1.4 times greater than the value ofthe same. This percentage reveals the Company'sdegree of economic and financial autonomy.

21

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

Rating of bond portfolio

31-Dec-05 31-Dec-06 Amount % Amount %AAA 23 425 32,43% 22 867 29,11%AA+ 570 0,79% 200 0,25%AA 3 951 5,47% 4 640 5,91%AA- 9 285 12,85% 10 910 13,89%A+ 15 002 20,77% 16 571 21,10%A 9 027 12,50% 10 282 13,09%A- 4 011 5,55% 7 072 9,00%BBB+ 1 764 2,44% 1 829 2,33%BBB - - - 0,00%BBB- - - - 0,00%BB+ - - - 0,00%BB - - - 0,00%BB- 166 0,23% 156 0,20%B+ - - - 0,00%B- 378 0,52% 634 0,81%CCC - - - 0,00%CC - - - 0,00%C - - - 0,00%D - - - 0,00%Unknown 4 657 6,45% 3 387 4,31%TOTAL 72 236 100,00% 78 548 100,00%(in thousand of euros)

Maturity of Bond Portfolio

31-Dec-05 31-Dec-06 Amount % Amount %2005 200 0,28% 0.00 0,00%2006-2007 8 512 11,78% 4 681 5,96%2008-2010 13 548 18,75% 15 987 20,35%2011-2015 23 041 31,90% 26 976 34,35%2016-2020 14 528 20,11% 18 718 23,83%2021-2030 7 027 9,73% 7 504 9,55%2031 5 380 7,45% 4 682 5,96%TOTAL 72 236 100,00% 78 548 100,00%(in thousand of euros)

Duration of bond portfolio

31-Dec-05 31-Dec-06 Amount % Amount %< 6 months 1 392 1,93% 3 224 4,11%6 months to 1 year 2 309 3,20% 1 606 2,04%1 year 3 years 11 107 15,38% 12 865 16,38%3 years 5 years 8 047 11,14% 8 857 11,28%5 years 10 years 22 900 31,70% 27 809 35,40%> 10 years 26 481 36,65% 24 187 30,79%n.d. 0.00 0,00% 0.00 0,00%TOTAL 72 236 100,00% 78 548 100,00%(in thousand of euros)

Profits

2002 2003 2004 2005 2006Profits from Sales 1,9% 1,5% 2,1% 2,2% 1,6%Capital & Reserves 27 031 736 29 243 429 31 677 499 33 351 351 34 795 084Income on Capital & Reserves 7,5% 6,1% 8,1% 8,7% 6,7%

RESULTS AND PROFITS

Pre-tax results in 2006 amounted to •3,130,284.14,up 5.0% against 2005. The Net Profit was slightlylower than that of 2005, given the increase in theestimated amount for corporate tax.

In these terms, remuneration on capital is slightlylower than in 2005, despite 2006 having seen stronggrowth and an increase in market share.

PROPOSED DISTRIBUTION OF PROFITS

The Board of Directors proposes to the GeneralMeeting the following distribution of profits for 2006:

Legal Reserve 234 179,83Free Reserve 413 618,48Dividends 1 694 000,00Total 2 341 798,31

Employee profit share, to be attributed as laid downin the Statutes, is already provided for, and is alreadydeducted from Net Profit.

NET WORTH

Once the distribution of profits proposed by theBoard of Directors to the General Meeting ofShareholders is approved, the Company's Cash andReserves will amount to 33,101,084.08 euros, anincrease in value of 5.9% between 2005 and 2006,and 26.3% in the past five years, after depreciationof the goodwill value of the acquisition operationsfor the portfolios of Royal & SunAlliance and Génesis.

22

Man

agem

ent

Repo

rt

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

23

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

In concluding we would like to thank the Associação Portuguesa de Seguradores,the Brokers' Associations and the insurance industry unions as well as:

Instituto de Seguros de Portugal. The Board of Directors and Employees of Lusitania Vida. Our Brokers. Our Reinsurersand

our Policyholders.

The Board of Directors also expresses its gratitude to the Shareholders and, inparticular, Montepio Geral, for their constant support.

Lisbon, 27 February 2007

The Board of Directors

José da Silva LopesChairman

José António de Arez RomãoCEO / Board Member

Jorge José Conceição SilvaBoard Member

24

Man

agem

ent

Repo

rt

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

25

Man

agem

ent

Repo

rt

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

ATTACHMENT TO THE BOARD OF DIRECTORS' REPORT

Shares held by Directors and Auditors as laid down in Article 477 of theCommercial Company Code

Shares held on 31.12.2006

Board of Directors

Montepio Geral - Associação Mutualista 2 529 816

Caixa Económica Montepio Geral 1 010 564

Dr. José António de Arez Romão 5 000

Dr. Jorge José da Conceição Silva 5

Board of Auditors

Dr. Vasco Ferreira César das Neves 100

26

Fina

ncia

l St

atem

ents

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

27

Fina

ncia

l St

atem

ents

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

Balance Sheet as at 31 December 2006

Profit and Loss - Financial Year 2006

Attachments to the Balance Sheet and Profit

and Loss Statement as at 31 December 2006

Property

Inventory of the Lusitania Collection

28

Fina

ncia

l St

atem

ents

L U S I T A N I A C O M P A N H I A D E S E G U R O S S AAnnual Report 2 0 0 6

29

Fina

ncia

l St

atem

ents

Annual Report 2 0 0 6L U S I T A N I A C O M P A N H I A D E S E G U R O S S A

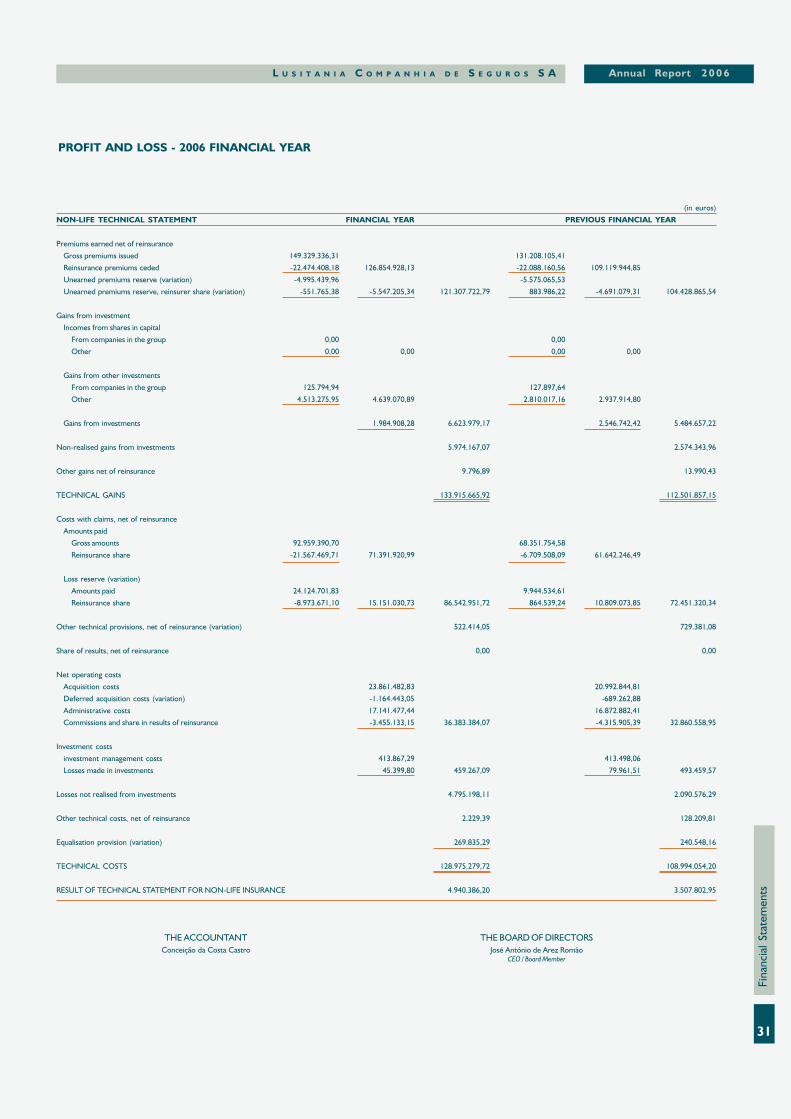

(in euros)

FINANCIAL YEAR LAST

FINANCIAL YEAR

ASSETS Gross Depreciations Net Net

Assets and Provisions Assets Assets

Intangible fixed assets 6.697.750,78 4.063.198,36 2.634.552,42 2.440.248,63Investments Land and buildings 41.880.283,11 0,00 41.880.283,11 38.246.744,59 For own use 37.214.335,09 37.214.335,09 33.759.098,31 Rented 3.751.631,49 3.751.631,49 4.412.413,48 Property under construction and cash advances 914.316,53 914.316,53 75.232,80 Investments in companies in the group and associates 2.930.398,11 0,00 2.930.398,11 3.404.699,79 Capital shares in companies in the group 1.490.079,36 1.490.079,36 1.473.168,30 Bonds and other loans to companies in the group 990.000,00 990.000,00 1.493.049,69 Capital shares in associated companies 450.318,75 450.318,75 438.481,80 Bonds and other loans to associated companies 0,00 0,00 0,00 Other financial investments 142.033.189,31 0,00 142.033.189,31 117.824.690,09 Shares, other fluctuating income securities and participation units 22.236.826,99 22.236.826,99 21.048.071,74 Bonds and other fixed income securities 77.557.917,02 77.557.917,02 70.743.096,16 Mortgage loans 1.980.541,35 1.980.541,35 2.550.000,00 Other loans 3.012.068,51 3.012.068,51 593.965,60 Deposits in credit institutions 33.410.986,67 33.410.986,67 19.106.402,74 Other 3.834.848,77 3.834.848,77 3.783.153,85 Deposits with ceding companies 129.530,70 0,00 129.530,70 41.225,76 Investments in Life Insurance in which the investment risk in born by the Policy Holder 0,00 0,00 0,00 0,00 Technical Provisions for Reinsurance Ceded 22.294.284,23 0,00 22.294.284,23 13.871.391,86 Unearned premiums reserve 4.657.885,63 4.657.885,63 5.209.651,01 Mathematical provision for life insurance 0,00 0,00 0,00 Loss reserve 17.636.398,60 17.636.398,60 8.661.740,85 Provision for profit share 0,00 0,00 0,00 Other technical provisions 0,00 0,00 0,00 Technical provisions for life insurance in which the investment risk is born by the policy holder 0,00 0,00 0,00 Debtors 65.754.322,54 2.423.252,69 63.331.069,85 52.694.316,49 For direct insurance operations Companies in group 990.694,40 990.694,40 630.522,42 Holdings 3.396,53 3.396,53 7.255,78 Other debtors 53.716.313,27 1.636.294,91 52.080.018,36 45.014.573,43 Reinsurance operations Companies in group 0,00 0,00 0,00 Holdings 0,00 0,00 0,00 Other debtors 4.087.866,96 4.087.866,96 3.288.764,72 Other operations Companies in group 0,00 0,00 0,00 Holdingss 0,00 0,00 0,00 Other debtors 6.956.051,38 786.957,78 6.169.093,60 3.753.200,14 Capital underwriters 0,00 0,00 0,00 0,00 Other Assets 11.831.364,65 5.178.229,90 6.653.134,75 6.445.223,85 Tangible fixed assets and stocks 6.367.962,78 5.178.229,90 1.189.732,88 1.185.396,34 Cash and bank deposits 5.463.401,87 5.463.401,87 5.259.827,51 Other 0,00 0,00 0,00 Accruals and Deferrals 4.954.792,26 0,00 4.954.792,26 3.616.960,45 Interest to be received 1.419.411,69 1.419.411,69 1.021.208,89 Other accruals and deferrals 3.535.380,57 3.535.380,57 2.595.751,56

Total Assets 298.505.915,69 11.664.680,95 286.841.234,74 238.585.501,51

ATHE ACCOUNTANT THE BOARD OF DIRECTORSConceição da Costa Castro José António de Arez Romão

CEO / Board Member

BALANCE SHEET AS AT 31 DECEMBER 2006

30

Fina

ncia

l St

atem