reforming power markets: lessons from five developing countries presented at: workshop on power...

Post on 20-Dec-2015

213 views

TRANSCRIPT

Reforming Power Markets:Lessons from Five Developing Countries

presented at:Workshop on Power Sector Reform:

Rio de Janeiro, 5-6 April 2004

David G. Victor

Program on Energy and Sustainable Development

Stanford University

http://pesd.stanford.edu/

Program on Energy & Sustainable Development

1. Electricity Market reforms Five-country comparison

(Brazil, China, India, Mexico, South Africa) IPPs

2. Geopolitics of Natural Gas Looking to 2030

3. Rural energy supply Shift from traditional to modern fuels and

technologies4. Climate change policy

Beyond Kyoto

Power Sector Reform in Developing Countries

1. Causes of Reform From state-centered to market-oriented

power systems

2. Speed and Character of Reform

3. Outcomes Impact on organization of the power sector Impact on the “social contract”

1. Causes of Reform

• In the advanced industrialized nations– Goal: economic efficiency– Expected outcome: tariff reductions

• In these five developing countries– Goal: financial solvency and investment– Realistic outcome: tariff increases

End of the Declining Cost Paradigm:United States example

Average U.S. Retail Electricity Prices

05

10152025303540

1926

1931

1936

1941

1946

1951

1956

1961

1966

1971

1976

1981

1986

1991

1996

19

95

U.S

. c

en

ts/k

wh

Number of Steam Electric Generators, U.S.

0

500

1000

1500

2000

2500

3000

1920 1930 1940 1950 1960 1970

Nu

mb

er o

f S

team

Pla

nts

3

4

5

6

7

8

9

10

11

12

13

14

15

16

172

00

2

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Wh

ole

sa

le P

ric

e (

20

01 c

/kW

h)

Regulated Current Cost Accounting

Regulated Historical Cost Accounting

Competitive Scenario

Expected Future Costs of Power Delivery in South Africa

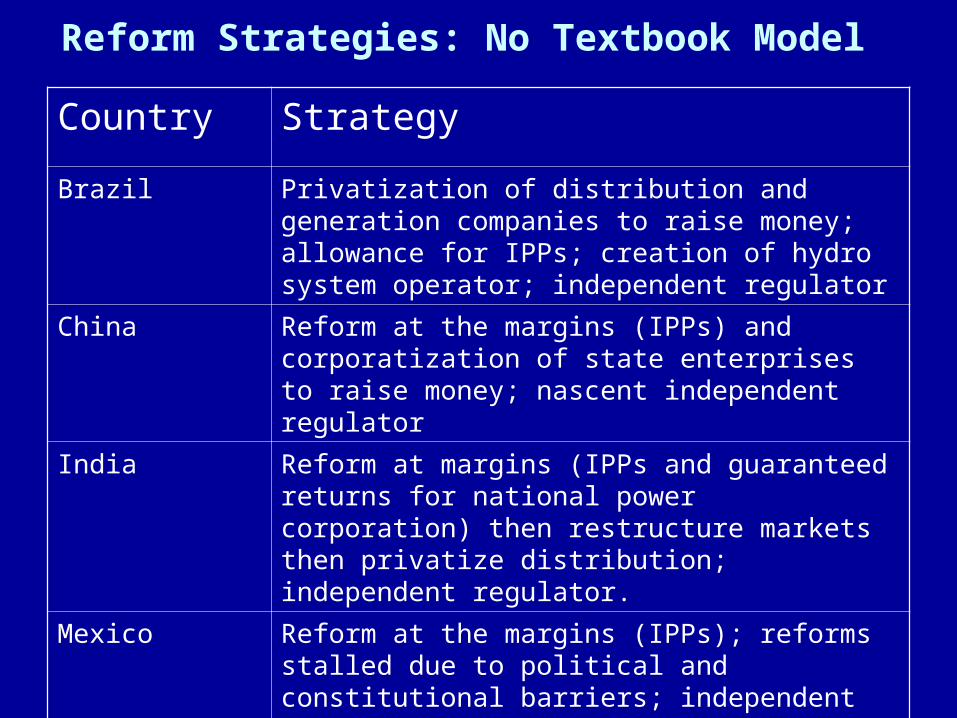

Reform Strategies: No Textbook Model

Country StrategyBrazil Privatization of distribution and generation

companies to raise money; allowance for IPPs; creation of hydro system operator; independent regulator

China Reform at the margins (IPPs) and corporatization of state enterprises to raise money; nascent independent regulator

India Reform at margins (IPPs and guaranteed returns for national power corporation) then restructure markets then privatize distribution; independent regulator.

Mexico Reform at the margins (IPPs); reforms stalled due to political and constitutional barriers; independent regulator

South Africa Aggressive electrification; reform of distributors; corporatization of utility; independent regulator

2. Speed and Character of Reforms

• Electricity Reforms depend on other reforms– Factor Markets

• Labor; fuels– Judicial

• Independent regulators– Corporate Governance and accounting

• Essential for regulatory oversight and private investment– Finance

• The single most important factor• State sector finance; soft budget constraints

– Contrast w/ OECD• reform with “rule of law,” market institutions, and independent

financial sectors already in place

3. Outcomes:Organization of the Power Sector• Emergence of “hybrid markets”

– Partially state-controlled• Financing; tariffs

– Partially market• Project and concession bidding• Brief market experiments

– Six provinces in China (1999-2001)

– A sustainable model for investment?• Predictability and solvency

Value and Number of Financial Closings of Greenfield Electricity Projects in East Asia and the Pacific

0

2000

4000

6000

8000

10000

12000

14000

1994 1995 1996 1997 1998 1999 2000 2001

Year

Va

lue

in U

S$

mill

ion

s

0

5

10

15

20

25

30

35

40

45

50

Value ofinvestment

Number offinancialclosings

Hybrid Markets

• Fragmented Ownership and Control– Isolated pockets of profitability: listed corporations– Pervasive under-performing: retained by the state

• Hybrid financing– Hard debt; equity squeeze; soft loans; pervasive state “safety

nets”• Hybrid governance

– “JV model” survives– Constant pressure to “socialize the downside and privatize the

upside”• Policy implications: tunneling strategies?

– APDRP in India• Policy implications: large effect of transparency reforms

– Corporate governance and accounting

3. Outcomes (continued)

• Impact of Restructuring on Reliability?– Still unclear– Financial reforms probably very positive

• Impact on “social contract”– Electric services for the poor

• Neutral to positive

– Protection of the environment• Neutral to positive

– Investment in innovation• Very negative?

Final Observations

• Central role for “non-electric” reforms– Especially financial and judicial reforms

• Importance of building coalitions for reforms– Coalitions that favor reform– “tunneling through” opposition

• APDRP in India

• Independent regulators as substitutes for government– To create confidence and stability

• Regulators overseeing hybrid markets, not textbook markets– Key issues: governance, transparency, IPP tenders– Lesser issues: market power, congestion

[backup slides follow]

From State-Centered to Market-Centered…

• Organization– Unbundling; fragmentation

• Ownership– Privatization, IPPs

• Financing– Market finance replaces “soft budgets”

• Governance and Accounting– External shareholder accountability

• Oversight– From the state to independent regulators

Five Critical Developing Countries

Country Populat’n Income

(GDP/cap $, PPP)

GDP

(billionUS$)

PowerSupply

(Twh)

Gen. Capacity

(Gw)

DominantFuel

NewFuel

Brazil 170m 7625 595 332 69 Hydro(88%)

Gas(0.2%)

China 1262m 3976 1079 1240 294 Coal (78%)

Gas(0.4%)

India 1016m 2358 456 527 108 Coal(75%)

Gas(6%)

Mexico 98m 9023 575 192 39 Oil (47%)

Gas(18%)

SouthAfrica

43m 9401 126 200 40 Coal(93%)

Gas(0%)

Why No “Textbook” Restructuring? (1)

• Key Reform Driver: Need for New Capacity– Tight systems; bad context for true markets– How to attract investors

• Markets, or stability?• Brazil’s experience

– Fast reformers focus on IPPs• China, India, Mexico, Brazil

– Slower reformers have excess capacity• South Africa

– Contrast w/ OECD: efficiency driven reforms

Electric Power Restructuring: Financing Options

Need new capacity

Self-financing through retained earnings

Financing through the state

Financing at margin (e.g., IPPs)

Financing through restructuring

PPAs (local & FDI

Unbundling SOEs, new governance,

independent regulators, market rules, etc.

Time for a Change?CFE’s slow expansion in Mexico

0%10%20%30%40%50%60%70%80%90%

100%

1930 1940 1950 1960

CFEChapalaImpulsoraMexicana

Source: Energy Ministry with CFE and LyFC data.

38,195

51,468 48,94654,244 53,064

61,72366,401 66,352

71,19174,334

IPPs in Mexico: Visions for the Future Close to 60 billion dollars will be required during the next 10 years in

the power sector.

Only 47% of the investment is expected to come from the Federal Budget.

2002-20112002-2011

(Billion pesos of 2002)(Billion pesos of 2002)IPP and FPIPP and FP

Federal BudgetFederal Budget

39%

61% 59% 51% 52% 47% 41% 42% 41% 42%

61%

39%41%

49% 48%

53%59% 58.0%

59%58%

0

15.000

30.000

45.000

60.000

75.000

90.000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Conclusion: Implications for Regulation

• Regulators overseeing hybrid markets, not markets– Key issues: governance, transparency, IPP

tenders– Lesser issues: market power, congestion– Interplay with other reforms

• Regulators as “replacement” for the State– Example of tariff control– Especially in democratic countries?

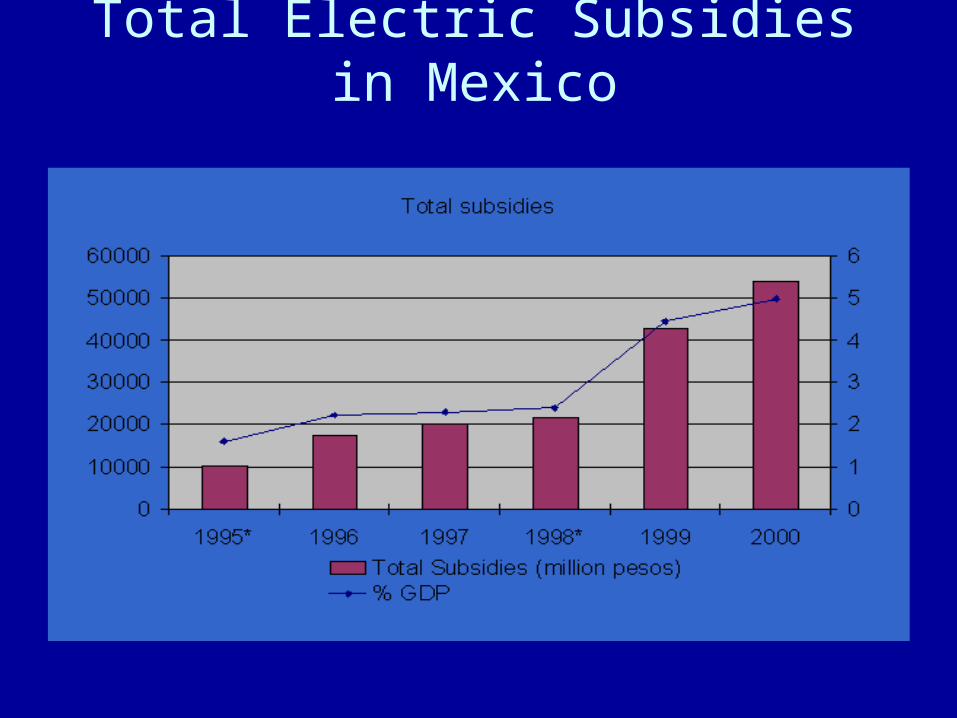

Total Electric Subsidies in Mexico

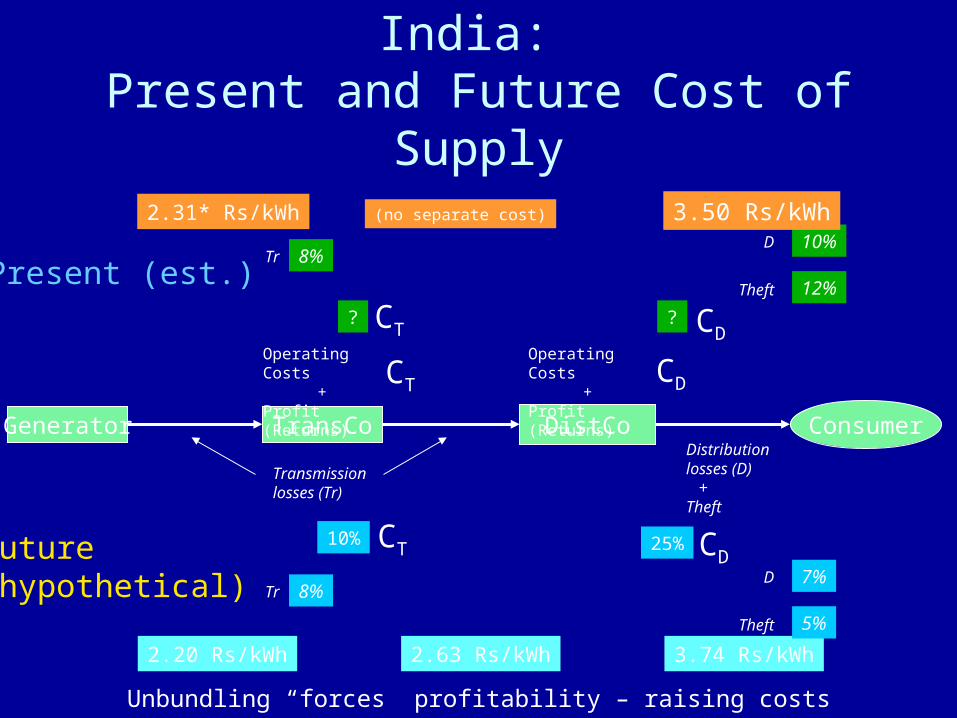

India: Present and Future Cost of Supply

Unbundling “forces” profitability – raising costs

Generator TransCo DistCo Consumer

Transmission losses (Tr)

Distribution losses (D) +Theft

Operating Costs

+Profit (Returns)

Operating Costs

+Profit (Returns)

CT CD

2.20 Rs/kWh 2.63 Rs/kWh 3.74 Rs/kWh

25%10%

7%

5%

8%D

Theft

Tr

CT CD

Future(hypothetical)

??

2.31* Rs/kWh10%

12%

8%

(no separate cost) 3.50 Rs/kWhD

Theft

Tr

CT CD

Present (est.)

Power Consumption in ChinaPower Consumption Structure

0

200

400

600

800

1000

1200

1400

1980 1984 1988 1992 1996 2000

TW

h

Residential

Tertiary

Industry

Agriculture

41.6

426.3

195.6

378.7

449.2

194.4

239.9 ps/kWh(Average)

5.00 ¢/kWh

Prices

Power Consumption and Tariffs in India

Domestic21%

Commercial5%

Agricultural30%

Industry31%

Outside 1%

Railway2%

Others10%

Source: Planning Commission

Consumption 315 Billion kWh