red meat sector operating environment july 2015

DESCRIPTION

ÂTRANSCRIPT

The Red Meat Sector Operating Environment

Half-yearly review: July 2015

Iain Macdonald Economics Analyst Quality Meat Scotland 0131 472 4040 [email protected]

2

Executive Summary

Although the UK economy grew more slowly at the beginning of 2015, this seems likely to be a short-lived blip given that most of the economic data has pointed to a self-sustaining economic expansion. Firm consumer and business confidence have underpinned spending on consumption and investment. The labour market has moved closer to normal conditions.

Inflation has fallen well below the Bank of England’s (BoE) 2% target due to lower global commodity prices and heightened retail competition. Since pay growth rose strongly during the first quarter of 2015 (Q1), real wages grew at their fastest rate in a number of years.

Though overall bank lending has remained weak, the flow of credit to UK businesses has reportedly

improved. Increased access to credit has supported the rise in consumer spending.

Food retail sales have continued to lag growth in overall consumer spending.

The monetary stance has continued to support UK economic activity. The slower pace of economic growth and lower inflation expectations have pushed expectations for the first interest rate increase back to early 2016. On the fiscal side, the tax threshold was raised for the 2015/16 financial year but there is the potential for significant cuts to in-work benefits payments to low paid workers.

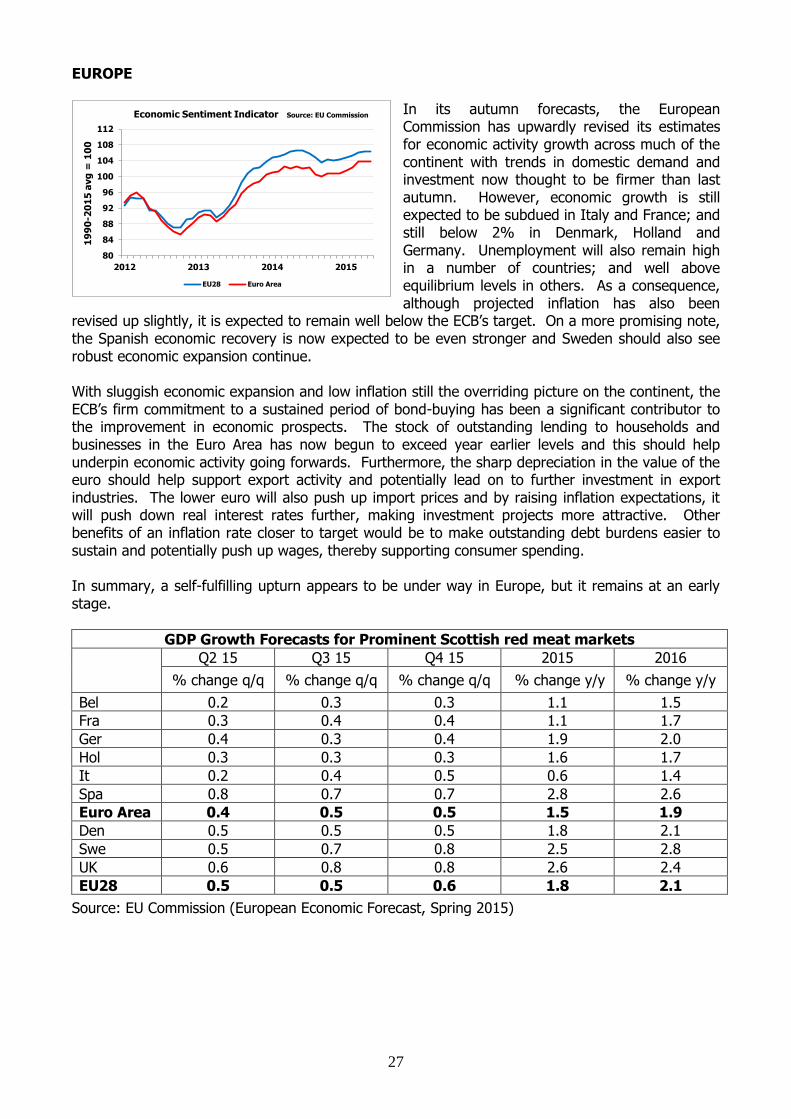

In the Euro Area, economic growth picked up at the beginning of 2015. There were particularly promising signs from Italy and France which had previously been lagging behind. Unemployment continued edging lower, but remained elevated. European Central Bank (ECB) action to cut interest rates, offer cheap financing to banks and to purchase government bonds improved the flow of credit and lowered the value of the euro. In addition to supporting export competitiveness, a lower exchange rate helped return the inflation rate to positive territory following a period of falling prices (deflation) which had posed significant risks to the recovery through its potential impacts on wage setting and debt burdens. Public investment is likely to remain weak but there have been moves towards coordinating fiscal policy to achieve a better balance at the aggregate level.

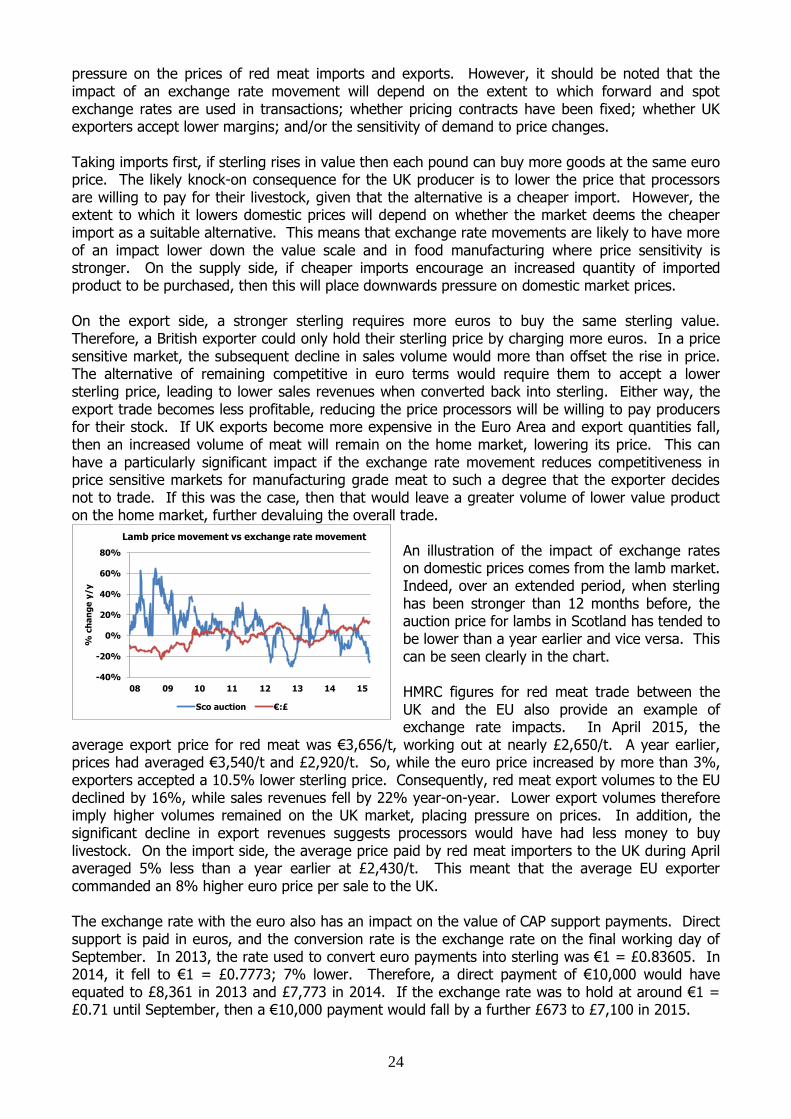

Sterling rose sharply in value against the euro during Q1 2015 after the ECB announced and then implemented a programme of government bond purchases. With the euro trading at around 71-73p in recent months, sterling has been around 12-14% stronger than a year earlier. As a consequence, it has become very difficult for UK red meat exporters to compete in price sensitive markets, limiting export volumes and consequently adding to domestic supplies.

The UK economic outlook continues to look positive. Inflation is expected to pick up in the second half of the year as last year’s fall in food and fuel prices begin to fall out of the annual comparison. However, it is likely to remain below both the BoE target and the level of wage inflation, resulting in a period of significant disposable income growth. The labour market is expected to show further improvements. Exchange rates and an economic slowdown in the emerging markets imply subdued UK export demand, leaving the UK economic expansion reliant on domestic demand.

On the red meat side, increased supplies have placed pressure on retail and producer prices this year. With pig and sheep producer prices sliding significantly, there may be some scope for retail prices to fall back to stimulate consumption. However, with prices for most alternative proteins also flat or falling, it may be difficult for red meat to gain market share.

Going forwards, while domestic production of sheepmeat and pigmeat is likely to remain ahead of year earlier levels, beef production is expected to trail 2014 levels. Imports of beef and lamb may ease back due to lower production in Ireland and New Zealand, respectively, while strong domestic production may result in lower pigmeat import requirements. Due to the exchange rate, exports for all three species are likely to remain difficult; though higher value cuts may see less of an impact given that demand will be less sensitive to prices.

3

Contents Executive Summary ....................................................................................................................................................... 1 What is happening in the UK economy? ................................................................................................................ 4

Macroeconomic Indicators ............................................................................................................................................ 4 Economic Activity: ..................................................................................................................................................... 4 Inflation: ..................................................................................................................................................................... 6 Labour Market: .......................................................................................................................................................... 8 Money & Credit: ...................................................................................................................................................... 11 Money Holdings ....................................................................................................................................................... 11 Credit Availability .................................................................................................................................................... 11

Consumer Indicators ................................................................................................................................................... 12 What has been happening to economic policy in the UK? ............................................................................ 15

Monetary policy: ...................................................................................................................................................... 15 Fiscal Policy: ............................................................................................................................................................ 15

What has been happening in the European economy? .................................................................................. 16 Economic Activity .................................................................................................................................................... 16 Inflation: ................................................................................................................................................................... 17 Labour market: ........................................................................................................................................................ 18 Consumer Trends: .................................................................................................................................................. 20

What has been happening to economic policy in the EU? ............................................................................. 21 Monetary Policy: ...................................................................................................................................................... 21 Fiscal Policy: ............................................................................................................................................................ 22

A focus on exchange rate movements ................................................................................................................. 23 What factors have been influencing the €:£ exchange rate? ........................................................................... 23 What influence does movement in the €:£ have on the red meat industry? ................................................. 23 What has been happening to the $:£ exchange rate and why does it matter? ............................................ 25 What has been happening to the NZ$:£ exchange rate and why does it matter? ....................................... 25

Economic Outlook ........................................................................................................................................................ 26 UK .................................................................................................................................................................................. 26

General Economic Climate:.................................................................................................................................... 26 Economic Activity: ................................................................................................................................................... 26 Inflation: ................................................................................................................................................................... 26 Labour Market: ........................................................................................................................................................ 26 Monetary Policy: ...................................................................................................................................................... 26

EUROPE ......................................................................................................................................................................... 27 Exchange Rate Movements ........................................................................................................................................ 29

€:£ ............................................................................................................................................................................. 29 $:£ ............................................................................................................................................................................. 29 NZ$:£ ........................................................................................................................................................................ 29

What has been happening in the red meat sector? ......................................................................................... 30 Food Price Inflation: ............................................................................................................................................... 30 Beef: ......................................................................................................................................................................... 30 Lamb: ........................................................................................................................................................................ 31 Pork: ......................................................................................................................................................................... 31 Bacon:....................................................................................................................................................................... 31

Review and Outlook for Meat Supplies ................................................................................................................ 32 Beef: ......................................................................................................................................................................... 32 Sheepmeat:.............................................................................................................................................................. 34 Pigmeat: ................................................................................................................................................................... 36

Red Meat Sector Outlook .......................................................................................................................................... 38 Sources ............................................................................................................................................................................ 39 Statistical Appendix .................................................................................................................................................... 40

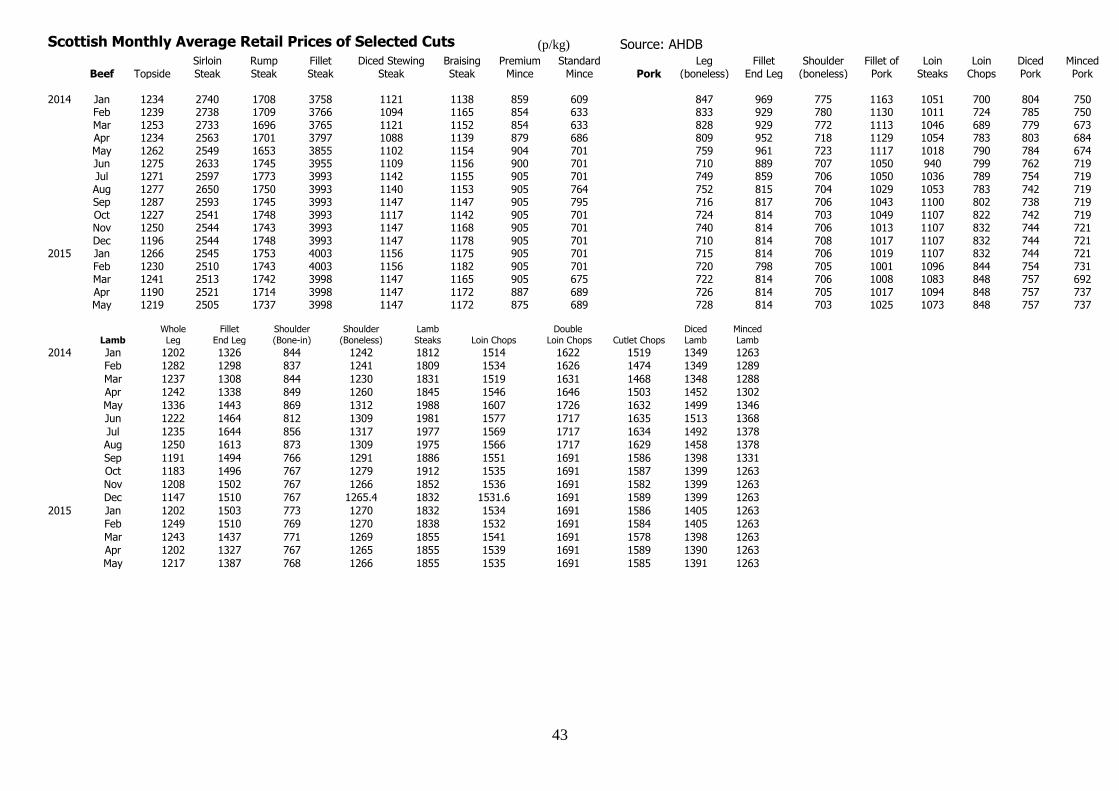

UK Economic Indicators ......................................................................................................................................... 41 Retail Price Index: meat & other food items ...................................................................................................... 42 Scottish Monthly Average Retail Prices of Selected Cuts .................................................................................. 43 UK Farm-to-Retail Price Spreads .......................................................................................................................... 44 EU Economic Indicators ......................................................................................................................................... 45

4

What is happening in the UK economy? Macroeconomic Indicators

Economic Activity:

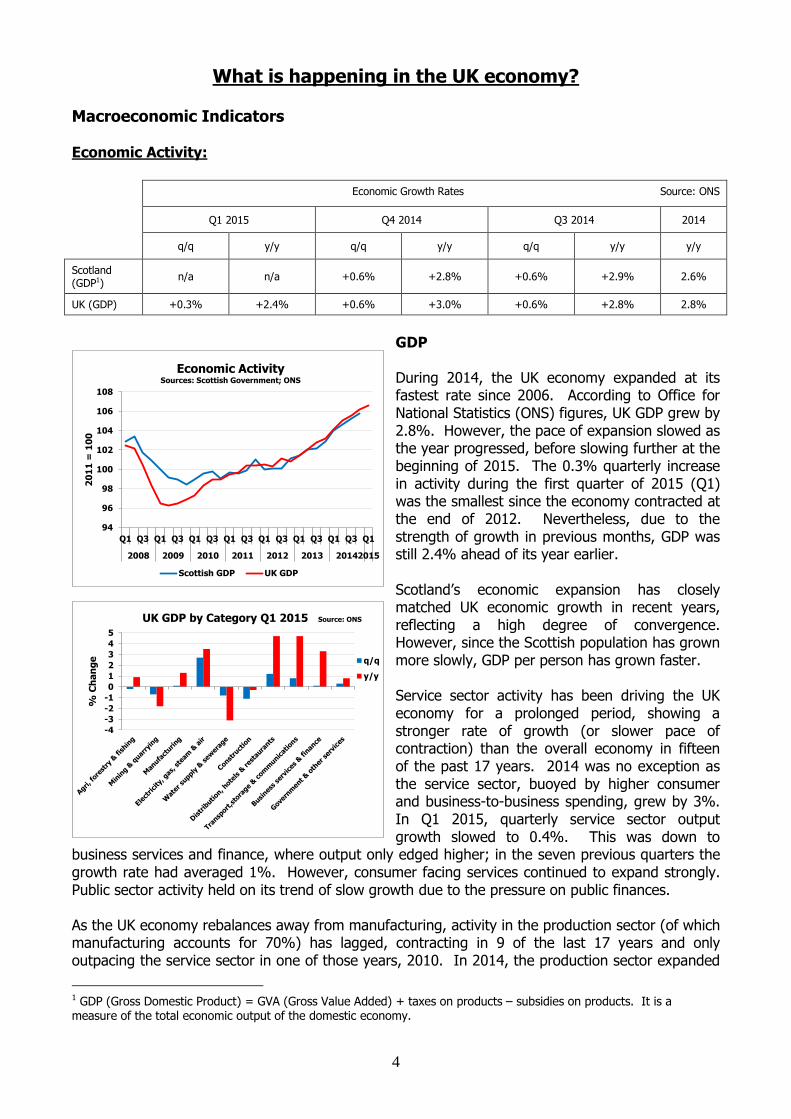

Economic Growth Rates Source: ONS

Q1 2015 Q4 2014 Q3 2014 2014

q/q y/y q/q y/y q/q y/y y/y

Scotland (GDP1)

n/a n/a +0.6% +2.8% +0.6% +2.9% 2.6%

UK (GDP) +0.3% +2.4% +0.6% +3.0% +0.6% +2.8% 2.8%

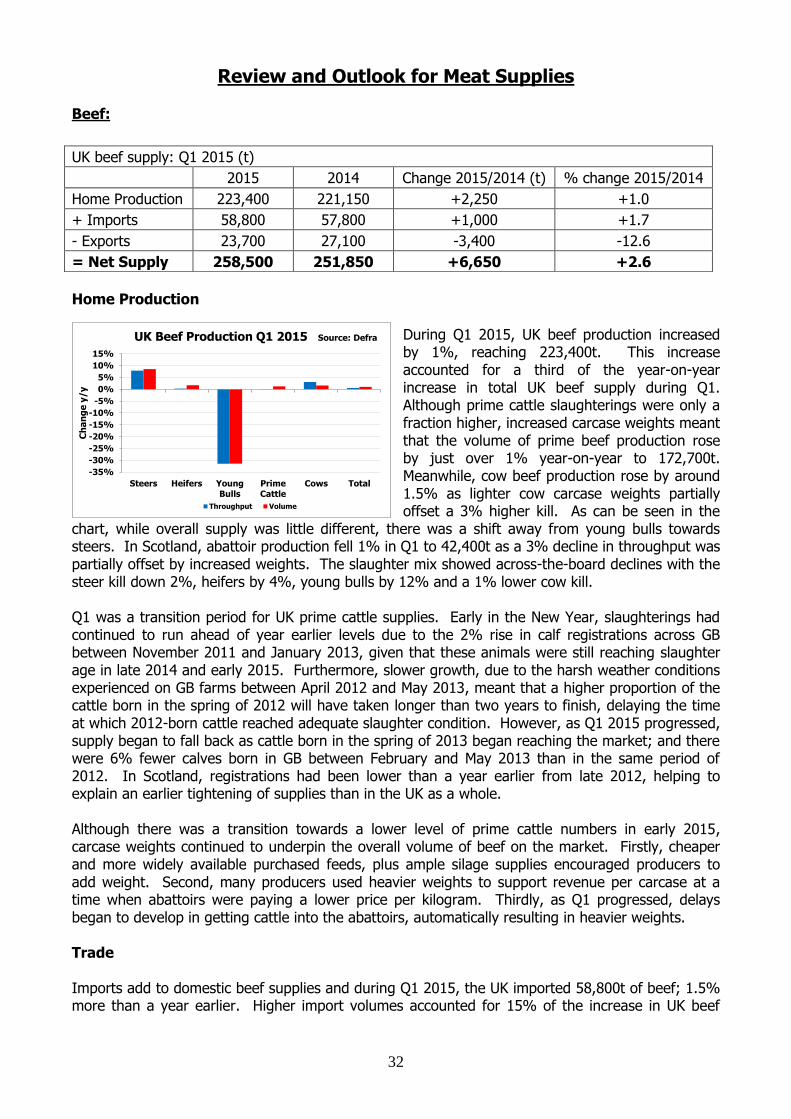

GDP During 2014, the UK economy expanded at its fastest rate since 2006. According to Office for National Statistics (ONS) figures, UK GDP grew by 2.8%. However, the pace of expansion slowed as the year progressed, before slowing further at the beginning of 2015. The 0.3% quarterly increase in activity during the first quarter of 2015 (Q1) was the smallest since the economy contracted at the end of 2012. Nevertheless, due to the strength of growth in previous months, GDP was still 2.4% ahead of its year earlier. Scotland’s economic expansion has closely matched UK economic growth in recent years, reflecting a high degree of convergence. However, since the Scottish population has grown more slowly, GDP per person has grown faster. Service sector activity has been driving the UK economy for a prolonged period, showing a stronger rate of growth (or slower pace of contraction) than the overall economy in fifteen of the past 17 years. 2014 was no exception as the service sector, buoyed by higher consumer and business-to-business spending, grew by 3%. In Q1 2015, quarterly service sector output growth slowed to 0.4%. This was down to

business services and finance, where output only edged higher; in the seven previous quarters the growth rate had averaged 1%. However, consumer facing services continued to expand strongly. Public sector activity held on its trend of slow growth due to the pressure on public finances. As the UK economy rebalances away from manufacturing, activity in the production sector (of which manufacturing accounts for 70%) has lagged, contracting in 9 of the last 17 years and only outpacing the service sector in one of those years, 2010. In 2014, the production sector expanded

1 GDP (Gross Domestic Product) = GVA (Gross Value Added) + taxes on products – subsidies on products. It is a measure of the total economic output of the domestic economy.

-4

-3

-2

-1

0

1

2

3

4

5

% C

ha

ng

e

UK GDP by Category Q1 2015 Source: ONS

q/q

y/y

94

96

98

100

102

104

106

108

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2008 2009 2010 2011 2012 2013 20142015

20

11

= 1

00

Economic Activity Sources: Scottish Government; ONS

Scottish GDP UK GDP

5

by 1.6% as a strong year for manufacturing (+2.9%) was partially offset by weaker utilities output. However, as sterling strengthened against the euro, exporting became less profitable in the second half of 2014 and acted as a drag on manufacturing. Moving into Q1 2015, a further strengthening of sterling dampened manufacturing and output grew by just 0.1% quarter-on-quarter, and by 1.3% year-on-year. The production sector grew at the same quarterly rate of just 0.1%. This left its output only 0.6% higher than a year earlier. The smaller sectors of construction and agriculture, forestry & fishing also slowed during Q1 2014. Construction output decreased by 1.1% on the quarter and by 0.3% year-on-year. Though agricultural output edged lower on the quarter, it remained nearly 1% higher than in early 2014. Purchasing Managers Index (PMI)

A more up-to-date measure of private sector activity comes courtesy of the PMI – a monthly survey of private sector firms. As can be seen in the chart, business activity has continued to exceed the 50 level of no change, signalling growth. However, growth slowed in the second half of 2014 in both manufacturing and services, and has remained on this lower trend. Construction has continued trending downwards. The May survey suggested that service sector

growth slipped to a five month low, having shown strength in March and April. However, at 56.5, the index remained in positive territory; and the three-month rolling average was above the annual average for 2014. Businesses reported growing orders as new services were being offered and marketing campaigns were launched. In addition, production was unable to keep up with demand, leading to increased backlogs of work. It was also noted that the election result had reduced uncertainty and confidence remained strong. Indeed, more than half of the surveyed firms expected increased orders in the year ahead compared with just 7% expecting a decline. Though still growing, manufacturing activity has been subdued since last summer. In May, the index edged up to 52. It was reported that while domestic orders held firm, the export trade was proving difficult as a stronger sterling made it harder to export profitably into the Euro Area; though conversely, a weaker sterling against the US dollar had assisted trade with the rest of the world. The construction sector has cooled sharply in 2015. In part, activity was held back by uncertainty over the outcome of the General Election. After the Election, activity was reported to have picked up, though at 55.9, the PMI was still at its second lowest level since June 2013. Although activity has been more sluggish in 2015, the PMI surveys have continued to report high levels of business confidence and ever-expanding order books. As a result, firms have continued to invest in upgrading their processes, technology and premises. Further evidence has come from the ONS which estimated that business investment picked up by 1.7% during Q1, having slipped back at the end of 2014. This kept it 3.7% above year earlier levels. Summary The previously strong pace of economic recovery in the UK dipped at the turn of the year, mainly down to slower growth in the key business services and finance sector. However, consumer facing industries continued to perform well, helping to offset the difficulties of trading with the Euro Area. With businesses continuing to invest due to a strong outlook, economic growth looks self-sustaining and the poor first quarter may have been a short-lived blip.

40

45

50

55

60

65

70

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M

2013 2014 2015

Dif

fusio

n I

nd

ex

(5

0 =

no

ch

an

ge

)

UK PMI Source: Markit

Manufacturing Services Construction

6

Inflation:

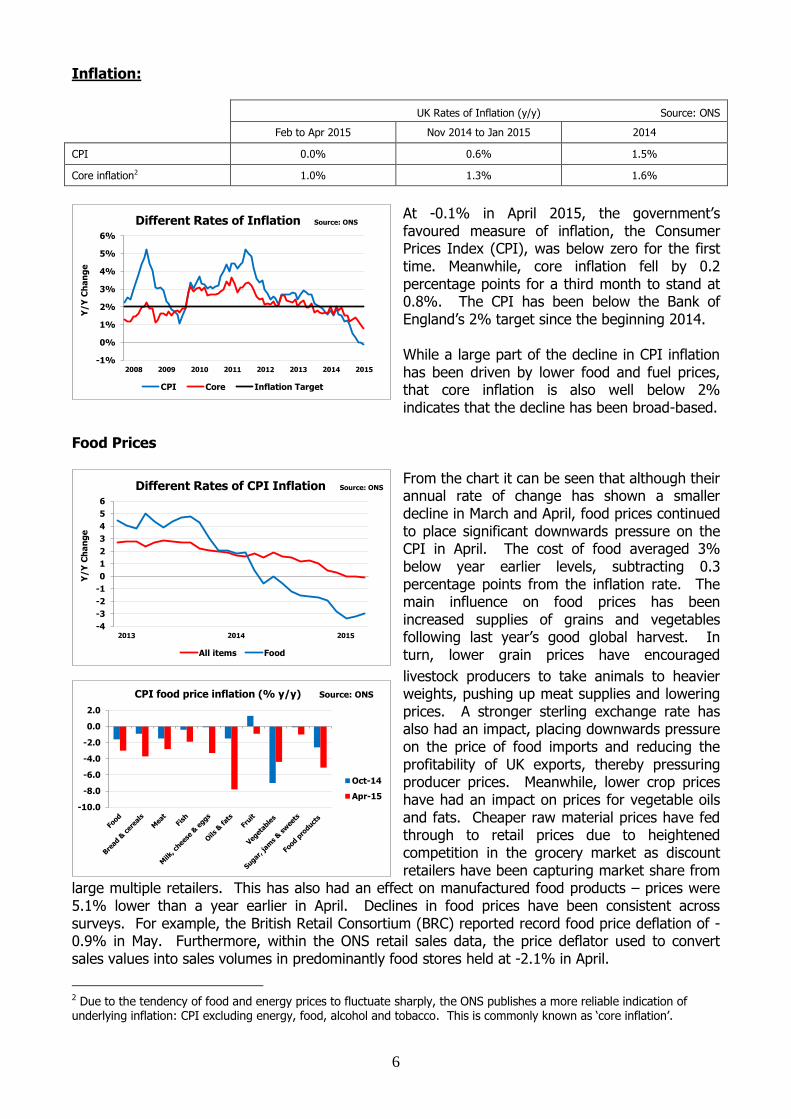

UK Rates of Inflation (y/y) Source: ONS

Feb to Apr 2015 Nov 2014 to Jan 2015 2014

CPI 0.0% 0.6% 1.5%

Core inflation2 1.0% 1.3% 1.6%

At -0.1% in April 2015, the government’s favoured measure of inflation, the Consumer Prices Index (CPI), was below zero for the first time. Meanwhile, core inflation fell by 0.2 percentage points for a third month to stand at 0.8%. The CPI has been below the Bank of England’s 2% target since the beginning 2014. While a large part of the decline in CPI inflation has been driven by lower food and fuel prices, that core inflation is also well below 2% indicates that the decline has been broad-based.

Food Prices

From the chart it can be seen that although their annual rate of change has shown a smaller decline in March and April, food prices continued to place significant downwards pressure on the CPI in April. The cost of food averaged 3% below year earlier levels, subtracting 0.3 percentage points from the inflation rate. The main influence on food prices has been increased supplies of grains and vegetables following last year’s good global harvest. In turn, lower grain prices have encouraged

livestock producers to take animals to heavier weights, pushing up meat supplies and lowering prices. A stronger sterling exchange rate has also had an impact, placing downwards pressure on the price of food imports and reducing the profitability of UK exports, thereby pressuring producer prices. Meanwhile, lower crop prices have had an impact on prices for vegetable oils and fats. Cheaper raw material prices have fed through to retail prices due to heightened competition in the grocery market as discount retailers have been capturing market share from

large multiple retailers. This has also had an effect on manufactured food products – prices were 5.1% lower than a year earlier in April. Declines in food prices have been consistent across surveys. For example, the British Retail Consortium (BRC) reported record food price deflation of -0.9% in May. Furthermore, within the ONS retail sales data, the price deflator used to convert sales values into sales volumes in predominantly food stores held at -2.1% in April.

2 Due to the tendency of food and energy prices to fluctuate sharply, the ONS publishes a more reliable indication of underlying inflation: CPI excluding energy, food, alcohol and tobacco. This is commonly known as ‘core inflation’.

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

CPI food price inflation (% y/y) Source: ONS

Oct-14

Apr-15

-4

-3

-2

-1

0

1

2

3

4

5

6

Y/Y

Ch

an

ge

Different Rates of CPI Inflation Source: ONS

All items Food

-1%

0%

1%

2%

3%

4%

5%

6%

Y/Y

Ch

an

ge

Different Rates of Inflation Source: ONS

CPI Core Inflation Target

7

Fuel & Energy Prices The CPI has also fallen back due to a decline in fuel and household energy prices. Although the oil price has picked up since reaching a low point in January, it has remained around 35% below year earlier levels in sterling terms. As a consequence, transport fuels have fallen in price and were around 12% below year earlier levels in April. The shift in the oil market has been attributed to a significant change in the balance between supply and demand. Indeed, increased shale oil production in the US has raised global oil production, while a strong US dollar and a slower rate of economic growth in China have led to downward adjustments in expected demand. Meanwhile, the combination of falling futures prices and political pressure on energy companies led energy companies to cut their prices at the end of 2014. In April, electricity was slightly cheaper to buy than a year earlier, while gas prices were down by 4%. Consumer Goods Prices

As noted earlier, it is not just the more volatile food and energy prices that have contributed to the slowdown in UK inflation. A significant influence has come from consumer goods. Indeed, during April, prices for durables, semi-durables and non-durables decreased by 2.3%, 0.5% and 0.3%, respectively. Looking more closely at the CPI data showed numerous categories of consumer prices in deflation. These included clothing (-0.3%); footwear (-1.1%); furniture (-1.3%); textiles (-1.4%); sports equipment (-1.2%) and financial services

(-3%). Further evidence came from the BRC survey for April which found non-food prices to be 2.5% lower than a year earlier. In the ONS retail sales dataset, deflators (inflation rates) for textile, clothing & footwear stores and household goods stores stood at -0.9% and -2.2% respectively. A number of factors have been placing pressure on the prices of consumer goods. According to the PMI surveys, lower input costs at manufacturing firms, due to lower commodity prices and a stronger sterling, have been passed on to output prices as a consequence of strong competition in the retail sector. Consumer Services Prices In the service sector, it has been a different story, however. Indeed, the April CPI showed an average 2% increase in prices across the service sector. It should be noted, however, that services price inflation had previously been running at around 2.5%. In April, tight housing supplies saw rents average 2.7% higher than a year earlier. Other services to show above average increases included car maintenance (2.5%) and hotels (3.8%), but cafe and restaurant price increases dipped back to 1.9%. According to PMI surveys, services prices have been pushed up by relatively firm demand which has allowed increased wage costs to be passed on to consumers. Summary To sum up, it appears that inflation has fallen below target due mainly to the pass through of businesses lower raw material costs. These have mostly been driven by global factors, such as lower commodity prices and exchange rates; though strong competition across the domestic retail sector will have contributed to the pass-through effect. Service providers have maintained more pricing power, reflecting the higher level of labour costs within their overall cost of production.

-2.8

3.0

-0.4 0.5

-0.5

2.0

-2.81.0

-0.4

10.0

2.0-0.1

-4

-2

0

2

4

6

8

10

12

% c

ha

ng

e y

/y

CPI by Category April 2015 Source: ONS

8

Labour Market: Employment

According to the ONS Labour Force Survey, UK employment grew by 0.7% on the quarter and by 1.8% year-on-year to reach a new record high of almost 31.1m during Q1 2015. This was the eighth successive quarter of employment growth and the quarterly increase was the fastest in a year and second quickest of the previous two years. Due to the fast pace of job creation, the UK employment to population ratio has now

returned close to its pre-2008 recession peak of just over 60%. Having stagnated at around 59.5% in the final three quarters of 2014, the ratio lifted to 60% in early 2015. This was the highest since Q2 2008. Rising employment has been a function of increased vacancies. During Q1 2015, there were 745,000 outstanding positions in the UK economy. Compared with Q4 2014, this was a rise of more than 4.5%, while they were up by a fifth year-on-year. The number of job openings recovered to its pre-2008 recession level at the end of 2014 and has since grown significantly further. This has given employees increased bargaining power in negotiations over pay and conditions.

Regular private sector surveys of labour market conditions have been broadly supportive of the official figures. In recent months, the PMI surveys have indicated strong job growth across manufacturing, services and construction. This has reportedly been the consequence of order growth outpacing output and leading to backlogs of work, requiring additional staff. Although the Bank of England’s (BoE) monthly Agents’ summary has reported slower rates of

employment growth in 2015, hiring intentions did lift in April across business services, consumer services and manufacturing. In the services sector, the strongest employment growth was reported to have been in IT, as the world moves increasingly towards online enterprise, plus professional services, which includes law and accountancy. By contrast, multiple retailers had reduced staffing levels. Manufacturing was reported to have seen slower employment growth than services. The summary also reported that firms had found it harder to secure the right staff as the labour market had tightened. This was most notable in lower skilled positions where job growth has been particularly strong through 2014 and into 2015. Underemployment A good barometer of the underlying health of the labour market is to look at indicators relating to underemployment, such as the level of part-time, temporary and self-employed work. In terms of full-time versus part-time roles, both had shown increases at a similar pace to overall employment. This meant that 73% of those in employment were in full-time positions. This has not shown any significant increase during the past couple of years of strong job growth, having fallen back from 74-75% following the 2008 recession. This may reflect a shift in the structure of the labour market, with one example being older people re-joining the labour force. Government efforts to increase

28.0

28.5

29.0

29.5

30.0

30.5

31.0

31.5

08 09 10 11 12 13 14 15

57.0

58.0

59.0

60.0

61.0

62.0

63.0

64.0

Nu

mb

er

of

UK

re

sid

en

ts in

wo

rk (

m)

% o

f th

ose

ag

ed

16

-64

in

wo

rk

UK Employment Source: ONS

Employment/Population Ratio (RHS) Total Employment (LHS)

46

50

54

58

62

66

70

J M M J S N J M M J S N J M M J S N J M M J S N J M

2011 2012 2013 2014 2015

Dif

fusio

n I

nd

ex

(5

0 =

no

ch

an

ge

)

Labour Market Barometer Source: Markit

Scotland (Bank of Scotland Labour Market Barometer)

UK (KPMG/REC Report on Jobs)

9

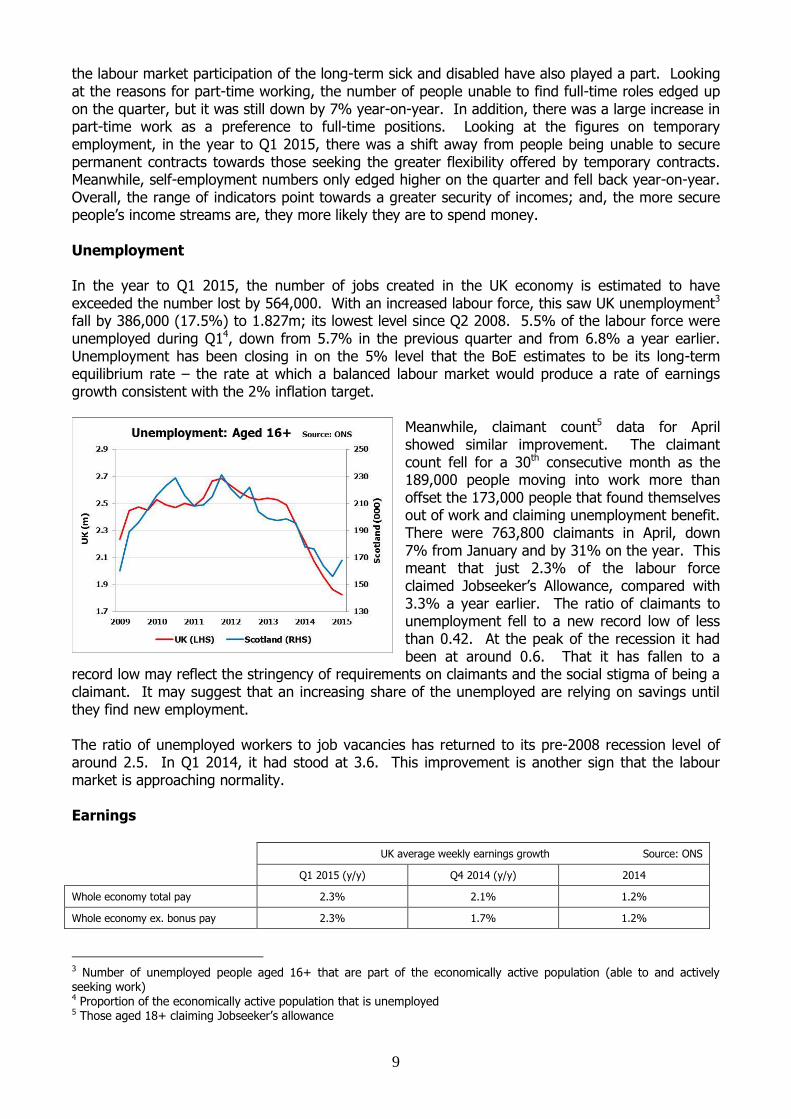

the labour market participation of the long-term sick and disabled have also played a part. Looking at the reasons for part-time working, the number of people unable to find full-time roles edged up on the quarter, but it was still down by 7% year-on-year. In addition, there was a large increase in part-time work as a preference to full-time positions. Looking at the figures on temporary employment, in the year to Q1 2015, there was a shift away from people being unable to secure permanent contracts towards those seeking the greater flexibility offered by temporary contracts. Meanwhile, self-employment numbers only edged higher on the quarter and fell back year-on-year. Overall, the range of indicators point towards a greater security of incomes; and, the more secure people’s income streams are, they more likely they are to spend money. Unemployment In the year to Q1 2015, the number of jobs created in the UK economy is estimated to have exceeded the number lost by 564,000. With an increased labour force, this saw UK unemployment3 fall by 386,000 (17.5%) to 1.827m; its lowest level since Q2 2008. 5.5% of the labour force were unemployed during Q14, down from 5.7% in the previous quarter and from 6.8% a year earlier. Unemployment has been closing in on the 5% level that the BoE estimates to be its long-term equilibrium rate – the rate at which a balanced labour market would produce a rate of earnings growth consistent with the 2% inflation target.

Meanwhile, claimant count5 data for April showed similar improvement. The claimant count fell for a 30th consecutive month as the 189,000 people moving into work more than offset the 173,000 people that found themselves out of work and claiming unemployment benefit. There were 763,800 claimants in April, down 7% from January and by 31% on the year. This meant that just 2.3% of the labour force claimed Jobseeker’s Allowance, compared with 3.3% a year earlier. The ratio of claimants to unemployment fell to a new record low of less than 0.42. At the peak of the recession it had been at around 0.6. That it has fallen to a

record low may reflect the stringency of requirements on claimants and the social stigma of being a claimant. It may suggest that an increasing share of the unemployed are relying on savings until they find new employment. The ratio of unemployed workers to job vacancies has returned to its pre-2008 recession level of around 2.5. In Q1 2014, it had stood at 3.6. This improvement is another sign that the labour market is approaching normality. Earnings

3 Number of unemployed people aged 16+ that are part of the economically active population (able to and actively seeking work) 4 Proportion of the economically active population that is unemployed 5 Those aged 18+ claiming Jobseeker’s allowance

UK average weekly earnings growth Source: ONS

Q1 2015 (y/y) Q4 2014 (y/y) 2014

Whole economy total pay 2.3% 2.1% 1.2%

Whole economy ex. bonus pay 2.3% 1.7% 1.2%

10

Average weekly earnings grew at an annual rate of 2.3% in Q1 2015. Regular pay - which excludes bonus payments - also increased by 2.3%. Both rates have seen notable increases since Q3 2014 and regular pay growth exceeded 2% for the first time since the summer of 2011. During March, regular weekly earnings averaged £461. Meanwhile, bonus payments were at £30, taking total pay to £491 (£25,500 per annum). With pay growth lifting while inflation has fallen sharply, the average worker is now seeing their pay increase in real terms. March was the sixth consecutive month that this was the case and the real terms increase in total pay was at its highest level since December 2007. Prior to October 2014, earnings growth had trailed CPI since September 2009. However, it should be noted that before adjusting for inflation, pay growth has remained well below its average of 4% during the 5 years to Q2 2008. If, as the BoE expects, CPI begins to pick up towards the end of this year, earnings growth will have to rise significantly further if real terms pay is to continue growing strongly. Stronger earnings growth is a further indication of a healthy labour market, suggesting that the previously large pool of available skilled workers from which firms had to draw from has been eroded, thereby bidding up wages through greater competition for staff. Since higher wages are likely to underpin consumer spending, the likelihood of a self-fulfilling positive cycle has increased. One downside for employers, however, is that a tighter labour market makes it harder for firms to find workers with the right skills. In addition to a healthy labour market, higher growth in average earnings may also reflect a shift in employment growth away from the lower end of the wage scale, where the majority of gains had been in 2013/14. Certainly, 72% of the employment growth during the year to Q1 2015 came in the second and third highest skilled categories. However, on the other hand, there was still strong employment growth in the lowest skilled category, while the highest skilled category saw numbers decline.

As can be seen in the average weekly earnings chart, there has clearly been a reversal in growth rates within manufacturing and services. Meanwhile, with public finances under pressure, public sector wages have seen little change in growth rates. In the most recent BoE Agents’ summary, it was noted that lower oil prices had passed through the oil & gas supply chain into wages and that similar developments had occurred in other parts of the manufacturing sector where input costs have fallen. It seems likely that the downturn in export demand

caused by unfavourable exchange rates will also have affected the willingness of firms to pay higher wages. By contrast, the strong performance of consumer-facing service-sector firms is likely to have boosted pay growth; indeed, this has been commented on regularly in the PMI surveys in recent months. At the lower end of the pay scale, a 3% increase in the minimum wage in October 2014 will have had more of an impact in services than in manufacturing. Summary The upturn in the UK economy over the past couple of years has encouraged businesses to take on additional staff to deal with higher levels of orders. Employment growth has outpaced the rise in the UK’s working age population and a wide range of labour market indicators have returned close to their pre-2008 recession levels. With labour market conditions returning to normal, firms have found it harder to find staff to meet their increasing order books and earnings have subsequently picked up; though they have dipped back in manufacturing. As inflation has fallen sharply, real wages have been increasing at their fastest rate since late 2007.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

11 12 13 14 15

3-m

on

th a

vg

(%

y/y)

Average Weekly Earnings Growth Source: ONS

Regular Pay Public Sector Manufacturing Services

11

Money & Credit:

Money Holdings According to the latest BoE data, the aggregate level of money and credit in the UK economy (M4) stood at £1.81 trillion in April. This was up by more than 4% on a year earlier. This means that there was a significant increase in money sitting in bank accounts. Breaking this down, the money holdings of households (includes sole traders and the non-profit sector) grew at a slightly below average rate of 3.5%. Meanwhile, there was a stronger 9.5% rate of money holdings growth at private non-financial corporations (PNFCs) - non-financial companies and partnerships - and a small increase of just over 1% at financial institutions. BoE statistics show that the overall increase in money holdings was supported by an increase in net lending by UK banks and building societies to both households and the private sector - M4 lending was up by 2.5% on the year. This increase was mainly driven by a jump in lending to the financial sector, which rose by 10%. By contrast, there was no change in the level of outstanding lending to PNFCs. Lending to the household sector, meanwhile, rose by approximately 2.5%. While overall M4 lending to PNFC’s was flat year-on-year, it continued to be held back by real estate firms – a legacy of the 2007/8 financial crisis. Indeed, the latest BoE Inflation Report showed that whereas the total stock of loans outstanding to real estate firms was around 5% below its year earlier level in Q1 2015, lending to other non-financial businesses was nearly 5% higher. Credit Availability

The May BoE Agents’ summary of business conditions reported a further improvement in credit availability during April. The survey suggested that banks were now willing to lend to both large and medium-sized companies and greater competition had resulted in more favourable terms for borrowers. For small firms, credit availability had eased, unless they were in the construction or property sectors. Funding from non-bank sources was widely available; the BoE Inflation Report showed a net increase in non-bank funding of £8.3bn during Q1 2015, of which £2.2bn came from equities and bonds. Consumer Credit The main reason for overall lending to households growing more slowly than money holdings was that mortgage financing rose by less than 2% year-on-year in April and it accounted for 88% of all lending to households. Although mortgage approvals picked up strongly in April 2015, they had fallen through much of 2014 and early 2015 after regulations were tightened in the spring of 2014. By contrast, consumer credit has been growing strongly for a prolonged period and was up by 7% year-on-year in April. 36% of consumer credit was extended through credit cards, and it rose by more than 5%. Other loans to consumers increased by more than 8%. In part, this is likely to reflect rising car sales, which, according to the Society of Motor Manufacturers and Traders (SMMT), grew at an annual rate of 5% in April, driven by the availability of cheap financing. Summary As the foundations of the UK economic recovery have strengthened, banks and other lenders have become increasingly confident to lend and have offered better terms to attract borrowers. In addition, small and medium-sized firms have begun to find it easier to access credit for investment. However, the banking sector has remained more risk averse than in the run-up to the 2008 financial crisis and so alternative sources of finance are being secured to enable investment. Despite real wages returning to growth, there has been no let-up in consumer borrowing.

12

Consumer Indicators

Household Incomes

In the second half of 2014 (H2), real household disposable income grew by 0.9% year-on-year to £551bn. This marks an improvement from the first half of the year when real incomes had only edged higher. Though pre-tax money incomes grew by more than 4% during H2, a higher cost of living lowered this to less than 3% when converted into real terms. There was also a net reduction in incomes due to fiscal policy. Indeed, there was 1.5% reduction in social benefits, while, as a function of a growing economy, the amount of tax and national insurance paid rose by 4.5%. Asda, in conjunction with the Centre for Economic & Business Research, produces a more timely indicator of movements in disposable incomes. As can be seen in the chart, UK households have, on average, seen a sharp increase in the level of income they have available to spend on non-essential items. The strong recovery of 2014 has shown no signs of

letting up in 2015 and has been underpinned by lower prices for essential items such as food and fuel at the same time as average earnings growth has increased. The tracker suggests that disposable income was up by an average of 9.5% year-on-year in the February to April period. Clearly, this has the potential to provide a significant boost to consumer spending; though this will depend on how much of the additional income is saved. However, the monthly household finance survey carried out by Markit shows that, on average, UK

households still feel that their finances have remained under pressure. Although a new record high was recorded in May, more respondents were pessimistic than optimistic about their current financial situation6. Finances were supported by increased labour market participation and incomes. Looking forward, households were, on balance, pessimistic for the first time since September 2014. This was driven by an expectation that the cost of fuel and energy would begin to

increase again. In addition, there was a slight increase in the proportion of respondents expecting the first interest rate increase to come within the next 6 months.

6 The HFI has been running since 2009

30

35

40

45

50

55

2010 2011 2012 2013 2014 2015

Dif

fusio

n I

nd

ex

(5

0=

no

ch

an

ge

)

UK Household Financial Situation Source: Markit

Household Finance Index (HFI) Future Finances Index

155

160

165

170

175

180

185

190

2010 2011 2012 2013 2014 2015

£ p

er

we

ek

Monthly Asda Income Tracker

256

260

264

268

272

276

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3

2007 2008 2009 2010 2011 2012 2013 2014

£b

n p

er

qu

art

er

Real household disposable income(Source: ONS)

13

Consumer Confidence

Having dipped back in late 2014, there was a lift in UK consumer confidence during the spring of 20157. Although, the May survey showed a fall in confidence from March and April when it had stood at 4, it remained above zero, indicating a net degree of optimism amongst UK consumers. The three point monthly decrease between April and May was mainly driven by a sharp fall in year-ahead expectations for both personal and general economic conditions. This fall may have been influenced by the result of the UK General

Election. However, there were also slight declines for perceptions of personal and general economic conditions over the past year. Meanwhile, respondents felt less confident about purchasing a big-ticket item than in the previous month. Nevertheless, over the past year, consumer confidence has been at historically high levels. Consumer Spending ONS data shows that in real terms, UK household spending increased by 1% during Q3 2014 and then by 0.6% during Q4. The strong quarterly expansions of H2 2014 were reflected in an annual increase in spending of 2.9%. Spending growth exceeded the rise in disposable incomes as more confident consumers saved less of their income. Indeed, the household savings rate decreased to 5.8% from 6.6% in H2 2013. Looking more closely at the spending data shows that the fastest growing category of expenditure during H2 2014 was recreation & culture; it rose by more than 6% year-on-year. Meanwhile, three

other categories posted growth rates of more than 5%: clothing & footwear; miscellaneous8; and

household goods & services. However, expenditure on food declined by 1.5%.

Within the food category, meat was the best performer in H2 2014, as spending rose by 2% year-on-year. All other categories showed declines, including fish - down 3.3% - and milk, cheese & eggs – down 4.1%. Since spending on food decreased while overall spending rose strongly, the share of food in total consumer spending fell significantly, reaching a record low of 7.4% in Q4. In recent years it had held relatively steady at around 7.7-7.9%. Real terms spending on meat continued to hold at 1.7% of total domestic spending and, at 23.3%,

took its highest share of real terms food spend since the beginning of 2008.

7 The overall index is the average score for each of the five survey questions. Respondents are asked to give a score of 1 if there has been a large improvement; 0.5 for a small improvement; 0 for no change; -0.5 for a slight worsening; or -1 for a considerable deterioration. 8 Personal items such as hairdressing, beauty products, watches, insurance, social care and legal fees

-35

-30

-25

-20

-15

-10

-5

0

5

10

2011 2012 2013 2014 2015

Ind

ex

sco

re

UK Consumer Confidence Source: GfK NOP

1.60%

1.63%

1.66%

1.69%

1.72%

1.75%

1.78%

1.81%

7.4%

7.5%

7.6%

7.7%

7.8%

7.9%

8.0%

8.1%

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3

2009 2010 2011 2012 2013 2014

% o

f to

tal d

om

esti

c e

xp

en

dit

ure

% o

f to

tal d

om

esti

c e

xp

en

dit

ure

Household Expenditure on Food Source: ONS

Food (LHS) Meat (RHS)

14

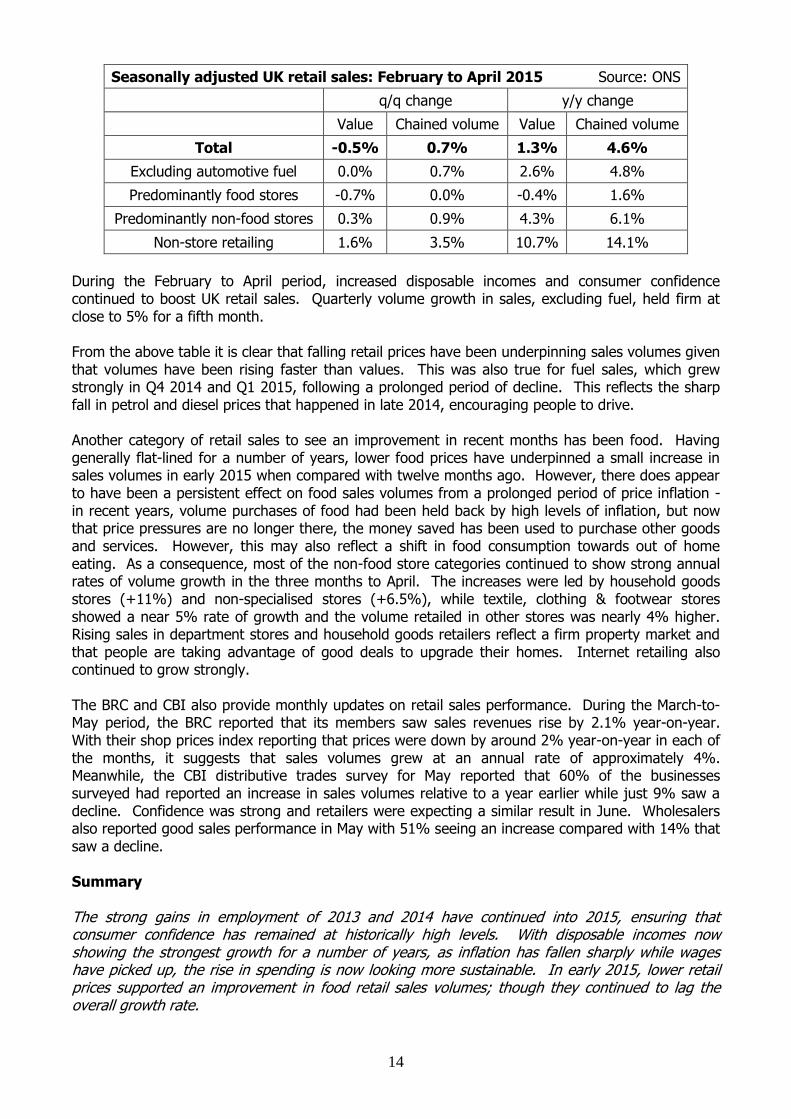

Seasonally adjusted UK retail sales: February to April 2015 Source: ONS

q/q change y/y change

Value Chained volume Value Chained volume

Total -0.5% 0.7% 1.3% 4.6%

Excluding automotive fuel 0.0% 0.7% 2.6% 4.8%

Predominantly food stores -0.7% 0.0% -0.4% 1.6%

Predominantly non-food stores 0.3% 0.9% 4.3% 6.1%

Non-store retailing 1.6% 3.5% 10.7% 14.1%

During the February to April period, increased disposable incomes and consumer confidence continued to boost UK retail sales. Quarterly volume growth in sales, excluding fuel, held firm at close to 5% for a fifth month. From the above table it is clear that falling retail prices have been underpinning sales volumes given that volumes have been rising faster than values. This was also true for fuel sales, which grew strongly in Q4 2014 and Q1 2015, following a prolonged period of decline. This reflects the sharp fall in petrol and diesel prices that happened in late 2014, encouraging people to drive. Another category of retail sales to see an improvement in recent months has been food. Having generally flat-lined for a number of years, lower food prices have underpinned a small increase in sales volumes in early 2015 when compared with twelve months ago. However, there does appear to have been a persistent effect on food sales volumes from a prolonged period of price inflation - in recent years, volume purchases of food had been held back by high levels of inflation, but now that price pressures are no longer there, the money saved has been used to purchase other goods and services. However, this may also reflect a shift in food consumption towards out of home eating. As a consequence, most of the non-food store categories continued to show strong annual rates of volume growth in the three months to April. The increases were led by household goods stores (+11%) and non-specialised stores (+6.5%), while textile, clothing & footwear stores showed a near 5% rate of growth and the volume retailed in other stores was nearly 4% higher. Rising sales in department stores and household goods retailers reflect a firm property market and that people are taking advantage of good deals to upgrade their homes. Internet retailing also continued to grow strongly. The BRC and CBI also provide monthly updates on retail sales performance. During the March-to-May period, the BRC reported that its members saw sales revenues rise by 2.1% year-on-year. With their shop prices index reporting that prices were down by around 2% year-on-year in each of the months, it suggests that sales volumes grew at an annual rate of approximately 4%. Meanwhile, the CBI distributive trades survey for May reported that 60% of the businesses surveyed had reported an increase in sales volumes relative to a year earlier while just 9% saw a decline. Confidence was strong and retailers were expecting a similar result in June. Wholesalers also reported good sales performance in May with 51% seeing an increase compared with 14% that saw a decline. Summary The strong gains in employment of 2013 and 2014 have continued into 2015, ensuring that consumer confidence has remained at historically high levels. With disposable incomes now showing the strongest growth for a number of years, as inflation has fallen sharply while wages have picked up, the rise in spending is now looking more sustainable. In early 2015, lower retail prices supported an improvement in food retail sales volumes; though they continued to lag the overall growth rate.

15

What has been happening to economic policy in the UK?

Monetary policy: At its June meeting, the BoE’s Monetary Policy Committee (MPC) left Bank Rate on hold at 0.5%. The stock of asset purchases (Quantitative Easing/ QE) was also left unchanged at £375bn. By implication, the MPC judged that this monetary stance was appropriate to meet the 2% inflation target in 2-3 years’ time while supporting economic growth and employment. The Minutes of the May MPC meeting showed that both decisions were unanimous; though two Members had come close to voting for an increase in Bank Rate to 0.75%.

With inflation falling back to around zero, the MPC would under normal conditions most likely loosen monetary policy by cutting interest rates or engaging in another round of QE, in order to stimulate the economy to prevent the low level of inflation from becoming ingrained and potentially economically damaging. However, the MPC has felt able to hold its monetary stance on this occasion, as its best collective judgment is that the low level of inflation is temporary. Indeed, in the May minutes, the expectation was that since approximately 75% of the difference between CPI (0% in March) and the BoE’s 2% target could be attributed to energy, food and other goods prices, inflation would lift towards the year-end as the past fall in commodity prices would drop out of the year-on-year comparison. By implication, the MPC felt that the current monetary stance would be required to eliminate the remaining 25% of the downwards pressure on the CPI. Fiscal Policy: Despite the rhetoric of fiscal austerity, the UK government continues to run a large budget deficit and it amounted to 4.8% of GDP in the 2014/15 financial year. This was down from 5.7% in the previous year as tax receipts grew by 3.5% while the increase in spending was limited to less than 1%. Public investment rose by of 7% and this will help raise the future growth potential of the UK economy through improved infrastructure. The budget deficit remains high due to the permanently lower tax revenues from the financial sector, plus the large increase in the income tax earnings threshold which has narrowed the tax base over the past 5 years. On the spending side, despite significant efforts to trim spending in most government departments, an ageing population continues to raise the cost of pensions, health and social care. In their election manifesto, the Conservative Party committed to further sharp cuts to spending in non-essential government departments. Since this is coming on the back of sharp cuts in the past 5 years, it seems likely that some departments will offer a significantly reduced service. One area this may have implications for in the red meat industry is export market access.

However, also in the Conservative manifesto were future tax cuts, and, in the current financial year a rise in the income tax threshold to £10,600 had previously been set. For the basic rate taxpayer, this will have boosted post-tax pay by a little over £2 a week. On the other hand, further reductions to in-work benefits payments may more than offset this. As with all policy changes, some households will be net winners and others net losers. Summary The monetary stance has continued to support UK economic activity. The MPC has not altered its stance despite a sharp fall in inflation since it believes that the fall in inflation has been mostly down to temporary factors which will dissipate later this year. On the fiscal side, the UK government continues to run a large budget deficit. To help support disposable incomes, the tax threshold was raised slightly for the 2015/16 financial year; though a number of benefits were cut.

16

What has been happening in the European economy?

Economic Activity:

Economic Activity in Prominent Scottish red meat markets

GDP Growth

(%Q/Q)

GDP Growth

(%Y/Y)

Q1 2015 Q4 2014 Q1 2015 2014

Bel +0.3 +0.2 +0.9 +1.1

Fra +0.6 0.0 +0.7 +0.4

Ger +0.3 +0.7 +1.0 +1.6

Hol +0.4 +0.8 +2.4 +0.9

It +0.3 0.0 0.0 -0.4

Spa +0.9 +0.7 +2.6 +1.4

Euro Area +0.4 +0.3 +1.0 +0.9

Den +0.4 +0.5 +1.7 +1.1

Swe +0.4 +0.8 +2.5 +2.1

UK +0.3 +0.6 +2.4 +2.8

EU28 +0.4 +0.4 +1.4 +1.3

Nor* +0.5 +0.4 +2.9 +2.2

Swi -0.2 +0.5 +1.1 +2.0

Sources: Eurostat; Statistics Norway; Statistics Denmark; SECO

*Mainland GDP (excluding oil & gas)

After a prolonged period of economic stagnation, the signs from the Euro Area are now looking much more promising. Economic activity began to pick up in a number of countries towards the end of 2014 and became more widespread in Q1 2015. Despite notable improvements in the large economies of France and Italy, which had been struggling in recent years, the overall pace of economic growth was still relatively subdued at 0.4%. This is reinforced by the fact that compared to a year earlier output was only 1% higher in the Euro Area as a whole. However, economic performance has picked up more significantly in Holland and Spain. Outside of the Euro Area, the Nordic countries have shown similarly positive signs. However, the previous economic momentum in Switzerland appears to have reversed in early 2015.

According to the monthly Markit PMI surveys, private sector activity growth fell back in the second half of 2014, but has since rebounded. This has been true for both manufacturing and service sector firms; though the pace of expansion has been stronger in services. The recovery in service sector output indicates that domestic demand within the Euro Area has finally improved. Although new orders and confidence slipped to their lowest level of the year-to-date in May, Spain’s service sector continued to show strength

and French activity had picked up. Meanwhile, the fall in the euro, engineered by ECB action to loosen Euro Area monetary policy, has improved the competitiveness of manufacturing exporters and demand has subsequently taken an upturn. In the May survey, the Spanish manufacturing sector led the way, but there were also reports of strong order growth in Holland and Italy. Meanwhile, although French manufacturers continued to struggle, export orders had improved. Looking out-with the Euro Area, the latest PMIs for Sweden pointed to a strong lift in demand for

44

46

48

50

52

54

56

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M

2013 2014 2015Dif

fusio

n I

nd

ex

(5

0 =

no

ch

an

ge

)

Eurozone PMI Source: Markit

Manufacturing Services

17

both manufacturing and services. However, Switzerland and Norway disappointed, posting manufacturing PMI’s below 50, indicating contraction. Latest Eurostat industrial production figures have shown an upturn; output was 1.8% higher than a year earlier in March in the Euro Area and up 2% in the EU28. Furthermore, it has reached its highest level for around four years. Underpinning the overall expansion in the Euro Area were energy - up nearly 4% - and non-durable consumer goods – up nearly 6%. However, production of intermediate and capital goods were flat while consumer durable production fell back. At the wider EU28 level, there was slow growth in intermediate, capital and consumer durables and stronger increases in energy and non-durables. On a country level, Eurostat figures have shown that industrial output trended higher over the year to March in Germany, Denmark, France, Norway, Holland, Italy and Spain. However, most of these countries were showing a modest level of expansion of around 1-2% per annum. By contrast, industrial output fell back in Sweden; contradicting the PMI indicators. Inflation:

Inflation in the Euro Area has rebounded after falling sharply in late 2014 and early 2015. After four months in deflation, the HICP matched year earlier levels in April and is estimated to have

been 0.3% higher year-on-year during May9.

Although the inflation rate reached a 6-month high, it remained well below the ECB’s 1.5%-2% target. Like in the UK, inflation has been held down by more than falling fuel, food and energy prices; core inflation has been running at or below 1% for nearly two years and although it picked up in May, it was still at just 0.9%.

A breakdown of the provisional data indicates that most of the recovery in the inflation rate has been driven by higher prices for unprocessed food. In 2014, the strong global harvest and the Russian trade ban had placed downwards pressure on food prices and they had shown an annual 1% rate of decline around the turn of the year. However, as the euro fell sharply in value during Q1, the cost of imported foodstuffs picked up significantly and unprocessed food prices were 2.1% higher year-on-year in May. The inflation rate has also edged up in non-energy industrial goods due to exchange rate movements; but at just 0.3%, it remained very low in May as producer prices for industrial goods were broadly flat, while relatively weak domestic demand continued to restrict the ability of firms to raise prices and increase their profit margins. Though still declining sharply – by 5% in May as lower oil prices continue to feed through supply chains - energy prices had been falling at an annual rate of 9% at the beginning of 2015 and so the slower rate of decline will also have had an impact on inflation. Services inflation edged up to 1.3% in May, but since it was not significantly different from its level throughout the past year and remained below the ECB target, it was indicative of weak demand. Indeed, the largest upward contribution to the April inflation rate came from cafes & restaurants; and prices were only 1.4% higher than 12 months before. Of the main markets for Scottish red meat exports, inflation rates during April were generally very low. In France, prices edged higher by 0.1% and there were increases of 0.3-0.5% in Belgium, Denmark, Germany and Sweden. However, Dutch prices were unchanged from a year earlier, while Italy, Spain and Switzerland remained in deflation, posting declines of 0.1%, 0.7% and 0.8%, respectively. Norway was the only exception – its inflation rate was at a more positive 1.8%.

9 HICP: Harmonised Index of Consumer Prices – allows international comparison of inflation rates within the EU

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M

2013 2014 2015

Y/Y

Ch

an

ge

Euro Area Inflation Source: Eurostat

HICP Core

18

The weak inflationary trends across the EU reflect the legacy of subdued consumer demand in addition to lower energy and food prices. The low level of inflation is a real danger as inflation greases the wheels of an economy. Once inflation is low, it can be difficult to turn as it leads people to adjust their expectations, and this can reduce the pressure on wages while purchases may be delayed in anticipation of price cuts, risking a downward spiral. In addition, since inflation erodes the real value of debts, low inflation makes it harder for households and businesses to repay loans, placing further pressure on spending power. It also reduces the propensity to take on new borrowing to finance investment projects by reducing the potential return on investment. A similarly low rate of inflation across Europe also makes it harder for a rebalancing of economies to take place. Firstly, the subdued demand implied by low inflation makes it harder for the less-well performing economies such as Italy to recover through exporting to stronger economies like Germany. Secondly, low inflation makes it more difficult for weaker economies to generate an export-led recovery and improve their competitive position in the global market given that wages, and hence production costs, will be growing at a similar pace. Labour market:

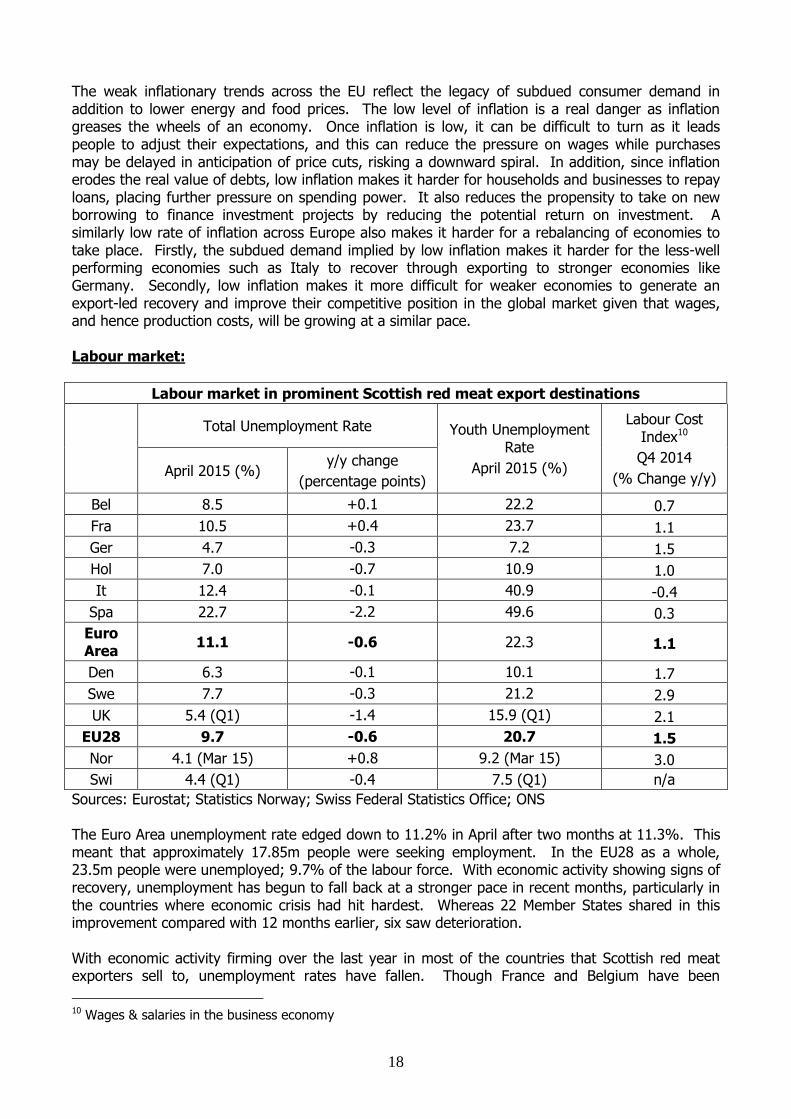

Labour market in prominent Scottish red meat export destinations

Total Unemployment Rate Youth Unemployment Rate

April 2015 (%)

Labour Cost Index10

Q4 2014

(% Change y/y) April 2015 (%)

y/y change

(percentage points)

Bel 8.5 +0.1 22.2 0.7

Fra 10.5 +0.4 23.7 1.1

Ger 4.7 -0.3 7.2 1.5

Hol 7.0 -0.7 10.9 1.0

It 12.4 -0.1 40.9 -0.4

Spa 22.7 -2.2 49.6 0.3

Euro Area

11.1 -0.6 22.3 1.1

Den 6.3 -0.1 10.1 1.7

Swe 7.7 -0.3 21.2 2.9

UK 5.4 (Q1) -1.4 15.9 (Q1) 2.1

EU28 9.7 -0.6 20.7 1.5

Nor 4.1 (Mar 15) +0.8 9.2 (Mar 15) 3.0

Swi 4.4 (Q1) -0.4 7.5 (Q1) n/a

Sources: Eurostat; Statistics Norway; Swiss Federal Statistics Office; ONS The Euro Area unemployment rate edged down to 11.2% in April after two months at 11.3%. This meant that approximately 17.85m people were seeking employment. In the EU28 as a whole, 23.5m people were unemployed; 9.7% of the labour force. With economic activity showing signs of recovery, unemployment has begun to fall back at a stronger pace in recent months, particularly in the countries where economic crisis had hit hardest. Whereas 22 Member States shared in this improvement compared with 12 months earlier, six saw deterioration. With economic activity firming over the last year in most of the countries that Scottish red meat exporters sell to, unemployment rates have fallen. Though France and Belgium have been

10 Wages & salaries in the business economy

19

exceptions, unemployment rates have stabilised in in 2015. In Italy the situation has improved slightly, but the return to economic growth has yet to feed into any significant reduction in unemployment. On a more positive note, there has been a sharp improvement in Spain where unemployment fell by more than half a million in the year to April. Small improvements have been made in Sweden and Denmark, and Holland has continued to make progress after poor performance in 2012 and 2013. Though relatively small improvements have been made in Germany and Switzerland, given that they have come from already low unemployment rates, the progress has been impressive. By contrast, the situation in Norway has deteriorated. On a regional level, there is significant difference in unemployment rates within some of Scotland’s principal trade partners. During 2014, in France, unemployment was at its lowest (7-8%) in the north-west and centre-east, while in Germany, unemployment was extremely low (2-3%) in the south and low in an EU context in the industrial heartlands of the north-west. In Belgium, there was a notable split between Flanders in the north, where rates were around 5%, and the southern Wallonne region, where unemployment averaged nearly 12% in 2014. There was a similar pattern in Italy, where unemployment remained below the EU average in the northern industrial regions (8-9%), but was above 20% throughout much of the south. By contrast, Dutch and Swedish rates were more evenly spread, averaging 5-7% across most of the former, and 7-8.5% in the latter. In addition to the official Eurostat data, labour market trends can also be deducted from the monthly Euro Zone PMI surveys. The surveys carried out in recent months have made good reading. Following a long period of stagnation, the rate of employment growth has picked up strongly in both manufacturing and services as an improvement in order levels has resulted in backlogs building up, leading to increased staffing requirements. Hopefully, this points towards a self-fulfilling upwards cycle where the fall in unemployment generates increased consumer demand and this in turn keeps order books filled and employment levels higher. It is particularly positive that the French private sector has begun to hire workers, after a prolonged period of declines. Moving on to cover wages, the picture looks weaker on the continent than at home as annual increases were lower than in the UK in most of Scotland’s key trading partners. Sweden and Norway were notable exceptions. During Q4, the annual increase across the Euro Area dipped back for a second quarter to its lowest level since Q3 2013. This may reflect that lower inflationary outcomes and expectations across the EU had been factored into pay negotiations. Although this low level of nominal pay growth indicates higher real incomes and better living standards for citizens in employment, if the rate of pay growth has fallen due to the fall in inflation, it would pose problems for consumer demand if food and energy prices begin to show increases towards the end of this year. It would also make it harder for core inflation to return to target. This would be a worrying development, suggesting that the recent improvement in economic activity could run out of steam. In a currency union, relatively low and similar rates of pay growth also limit the ability of the weaker economies to improve competitiveness against the stronger ones. Summary The European economy has shown some promising signs at the beginning of 2015. Some of the economies worst affected by the 2008 crisis have continued to rebound well, and the large economies of France and Italy are now showing more optimistic signs. Indeed, Italy has exited from recession and the French economy grew strongly in Q1 having stalled for 18 months. However, the German economy continued to grow more slowly, and, following a prolonged period of weak economic activity, significant challenges remain. Inflation remains well below the ECBs target and though lower fuel and energy prices may have given a short-term boost to household finances and hence spending, low inflation continues to have a negative impact on expectations and debt burdens; and worryingly, potentially wages. Amidst this difficult economic environment, unemployment has been edging lower, but it remains elevated across much of the continent.

20

Consumer Trends:

Selected statistics - prominent Scottish red meat markets

Retail Sales

Volumes Apr 2014

(% change y/y)

Retail Sales Volumes – food,

beverages & tobacco Apr 2014

(% change y/y)

Consumer Sentiment (% balance)

May 2015 Nov 2014

Bel +0.1 +1.1 -3.1 -14.1

Fra +1.7 +0.6 -17.8 -22.6

Ger +3.7 +2.0 +3.0 -1.6

Hol +2.3 (Mar) +0.9 (Mar) +6.2 +2.8

It +1.8 (Mar) +0.9 (Mar) -8.9 -17.0

Spa +4.2 +1.9 +1.5 -11.8

Euro Area

+2.2 +1.1 -5.5 -11.6

Den +0.4 -0.2 +19.3 +16.7

Swe +2.1 -0.4 +10.2 +13.5

UK +3.3 -2.4 +1.1 +2.6

EU28 +2.6 +0.6 -4.0 -8.1

Nor +3.8 +2.6 +16.9 (Q1) +18.5 (Q3)

Swi -2.8 (Mar) -2.6 (Mar) +1 (April) -11 (October)

Sources: Eurostat; European Commission; Bloomberg; SECO The latest consumer data for the EU points to a small lift in demand. Indeed, after adjusting for inflation, household disposable income per person edged up by 0.1% during Q4 2014, but after stronger growth earlier in the year it was around 1.2% higher than a year earlier. This subdued rate of growth was underpinned by small increases in wages and social benefits. As governments tried to keep their budget deficits within the 3% maximum under the rules of the Stability and Growth Pact, a small increase in taxes placed some pressure on incomes. As a consequence of limited income growth in the Euro Area, real terms household spending also rose by 0.1% on the quarter and by around 1.2% on the year during Q4. With the increase in spending matching income gains, Eurostat figures showed little change in the Euro Area household savings rate. It edged up on the quarter and on the year to 12.9%, but remained close to historically low levels. Move forward six months and the picture looks more promising. The EU Commission’s monthly consumer confidence survey has shown an improvement across most Member States. Indeed, whereas in late 2014 six of Scotland’s main red meat export markets had a net negative balance, by May this had fallen to three; and there had been significant improvements in Belgium and Italy. In France, confidence was slightly better, but it remained firmly in negative territory. In April, retail sales volumes rose by 2.2% year-on-year across the Euro Area and by 2.6% in the EU. However, sales were more subdued in Denmark and Belgium and declined sharply in Switzerland. The overall increase was underpinned by both the rise in consumer sentiment plus falling prices. The strongest growth has been in non-food stores, where the annual increase has consistently been running at around 3%; though textiles, clothing & footwear have underperformed. Retail sales volumes in the food, beverages & tobacco category continued to grow slowly in April; though this may have been artificially low due to the earlier Easter. Markit’s monthly Eurozone Retail PMI surveys pointed to marked improvement in retail sales through the spring, and exceeded the 50 mark of no change for the first time in over a year in May.

21

What has been happening to economic policy in the EU? Monetary Policy: Due to the expected persistence of low inflation in the Euro Area, the ECB has loosened its monetary stance significantly over the past year. At both the June and September 2014 meetings of its Governing Council, the ECB lowered its 3 key interest rates. As a consequence, the deposit rate which the ECB pays banks on their holdings of reserves at the ECB has been in negative territory for a year; and at -0.2% since September. Meanwhile, the refinancing rate, at which banks can borrow from the ECB, has been lowered to just 0.05%11, and the marginal lending rate on overnight borrowing from the ECB is at 0.3%. In theory, interest rate cuts should help stimulate spending and investment, and in turn boost economic activity and move inflation back towards the targeted level of ‘below but close to 2%’. The lowering of the deposit rate below zero was significant as zero tends to be a lower bound on interest rates. However, the ECB felt able to take its deposit rate slightly below zero as the alternative for a financial institution of paying the ECB to hold its excess reserves would be to store the cash; a process that would be costly. As a consequence, banks will have to increase their lending if they want to avoid paying interest on their excess reserves. In addition to lowering interest rates, the ECB also announced that it would launch a new round of targeted long-term refinancing operations (TLTRO)12. These are 4-year loans to financial institutions at low interest rates with the aim of stimulating lending to non-financial private sector firms. The ECB announced that they would be offered to banks in September and December. In a further attempt at lowering borrowing costs, the ECB began purchasing asset-backed securities in October. However, the early signs of these ECB actions were mixed: the level of TLTRO funds accessed disappointed, but bank lending to households and non-financial companies did begin to show some improvement, having contracted consistently for two years. With the inflation rate falling below zero around the turn of the year, the ECB finally made the decision to begin a programme of asset purchases (QE). Ever since the economic crisis, the ECB had stopped short of buying government bonds from banks and investors due to concerns, particularly from Germany, that this would amount to the monetary financing of government borrowing. On January 22, the ECB announced that from March onwards, it would purchase €60bn (£44bn) worth of government bonds each month until at least September 2016. If inflation fails to return to the ECBs target range by September 2016, then it has committed to extending bond buying until this is the case. In addition, it announced that the interest rate charged on TLTRO funding would be cut by 0.1 percentage points. Promisingly, TLTRO take-up exceeded expectations in March and Euro Area money growth (M3) grew at an annual rate of nearly 5% in the three months to April. Over the past six months, a number of non-Euro Area European states have also loosened monetary policy. This has pushed interest rates deeper into negative territory in Denmark and Switzerland, and below zero for the first time in Sweden. In Norway, the main interest rate was cut to 1.5% back in December.

11 These rates were cut by the same degree to maintain the functioning of the money markets. The deposit rate acts as an interest rate floor as if other lenders paid a lower rate, excess reserves would be directed to

the higher rate offered by the ECB. Meanwhile, the refinancing rate acts as a ceiling as if a lender charged more, the borrower would be able to access cheaper funds from the ECB. Since market rates will be

somewhere in between the two, a smaller gap could impair the functioning of interbank lending. 12 The initial LTROs were introduced in the winter of 2011/12 and successfully helped to ease a build-up of financial pressures which were threatening the flow of credit in the Euro Area.

22